supply chain excellence in the german aerospace industry

TRANSCRIPT

An initiative by

Supply Chain Excellence

in the German aerospace industry

Status quo and outlook for the German aerospace industry On behalf of the German Federal Ministry for Economic Affairs and Energy

Seite 2

224

0

60

11

124

194

88

150

188

255

155

181

153

61

86

113

196

247

190

190

220

127

127

127

Supported by regional as well as state

associations, BDLI and SPACE Germany Political patronage

Supply Chain Excellence: Collaboration of aerospace industry

stakeholders throughout Germany

North Rhine-

Westphalia

Lower Saxony

Bremen

Hamburg

Schleswig-

Holstein Mecklenburg-

Pomerania

Brandenburg

Berlin

Saxony

Saxony-

Anhalt

Thuringia Hesse

Rhineland-

Palatinate

Baden-

Wuerttemberg Bavaria

Saarland

Seite 3

224

0

60

11

124

194

88

150

188

255

155

181

153

61

86

113

196

247

190

190

220

127

127

127

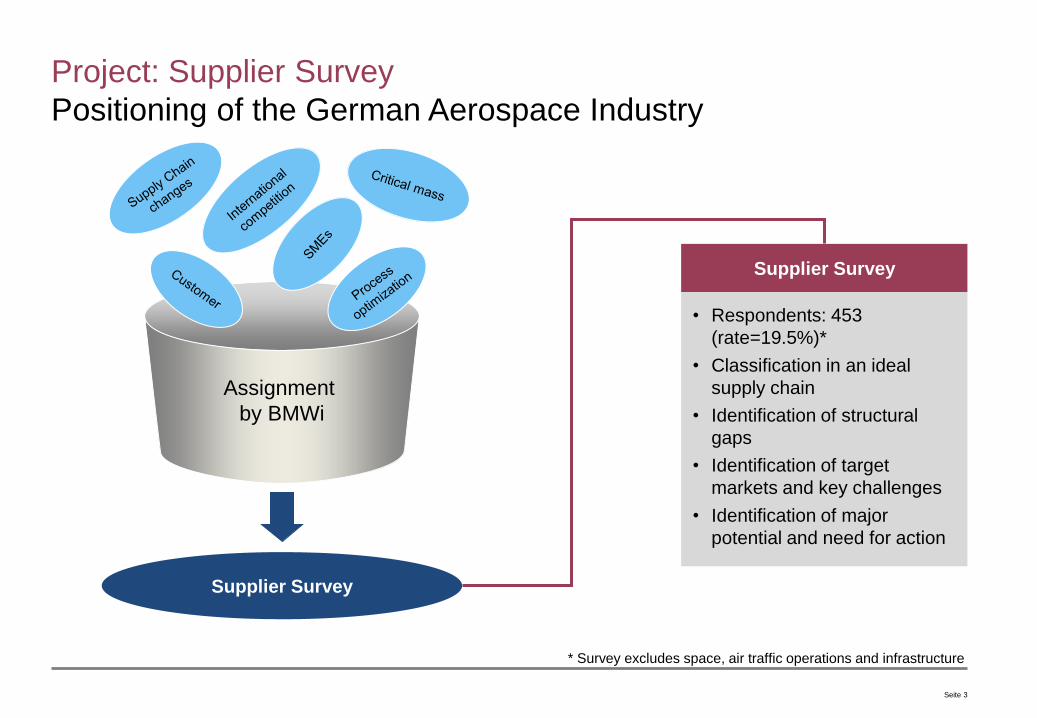

Project: Supplier Survey

Positioning of the German Aerospace Industry

Assignment

by BMWi

Supplier Survey

Supplier Survey

• Respondents: 453

(rate=19.5%)*

• Classification in an ideal

supply chain

• Identification of structural

gaps

• Identification of target

markets and key challenges

• Identification of major

potential and need for action

* Survey excludes space, air traffic operations and infrastructure

Seite 4

224

0

60

11

124

194

88

150

188

255

155

181

153

61

86

113

196

247

190

190

220

127

127

127

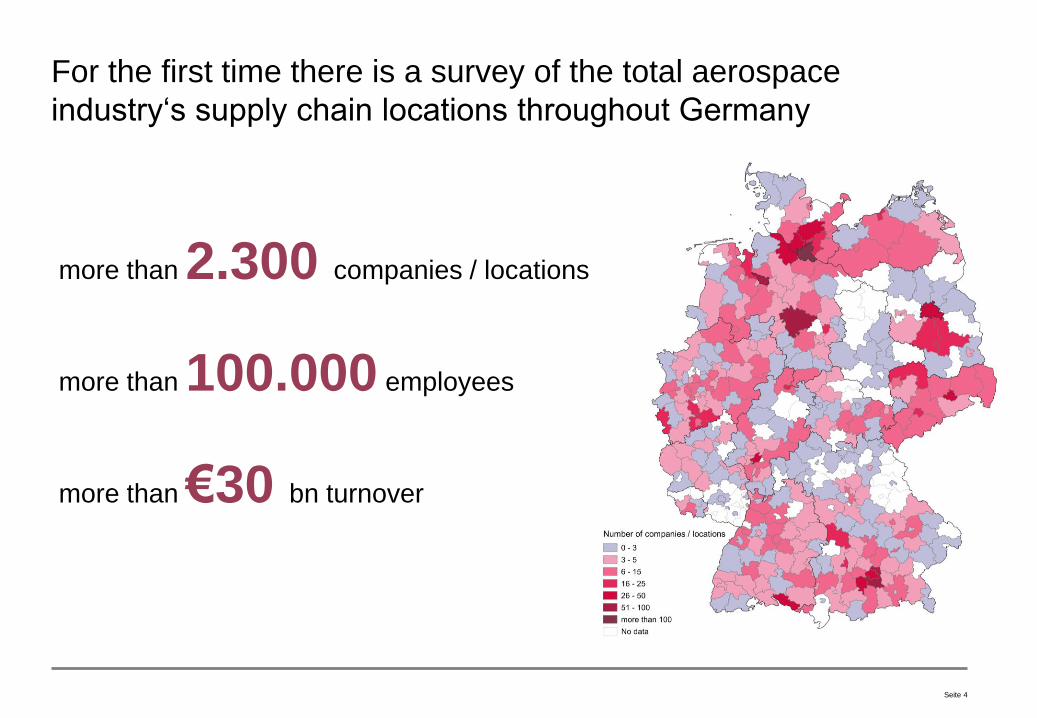

For the first time there is a survey of the total aerospace

industry‘s supply chain locations throughout Germany

more than 2.300 companies / locations

more than 100.000 employees

more than €30 bn turnover

Seite 5

224

0

60

11

124

194

88

150

188

255

155

181

153

61

86

113

196

247

190

190

220

127

127

127

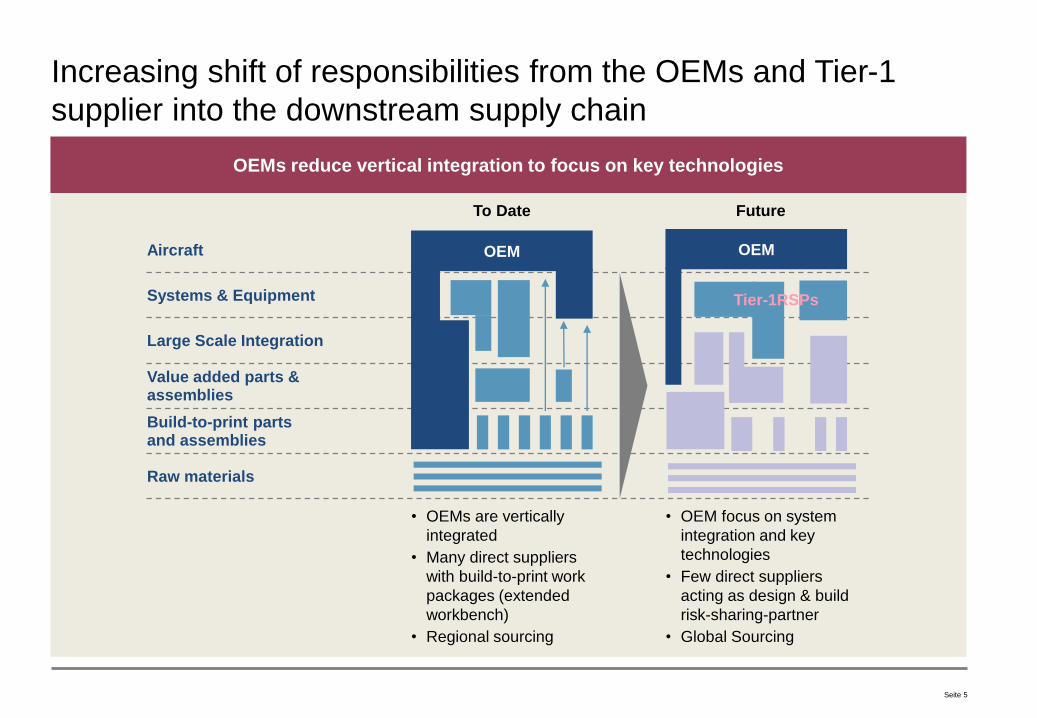

OEMs reduce vertical integration to focus on key technologies

Increasing shift of responsibilities from the OEMs and Tier-1

supplier into the downstream supply chain

• OEM focus on system

integration and key

technologies

• Few direct suppliers

acting as design & build

risk-sharing-partner

• Global Sourcing

• OEMs are vertically

integrated

• Many direct suppliers

with build-to-print work

packages (extended

workbench)

• Regional sourcing

Raw materials

Value added parts & assemblies

Large Scale Integration

Systems & Equipment

Build-to-print parts and assemblies

Aircraft OEM

To Date Future

OEM

Tier-1RSPs

Seite 6

224

0

60

11

124

194

88

150

188

255

155

181

153

61

86

113

196

247

190

190

220

127

127

127

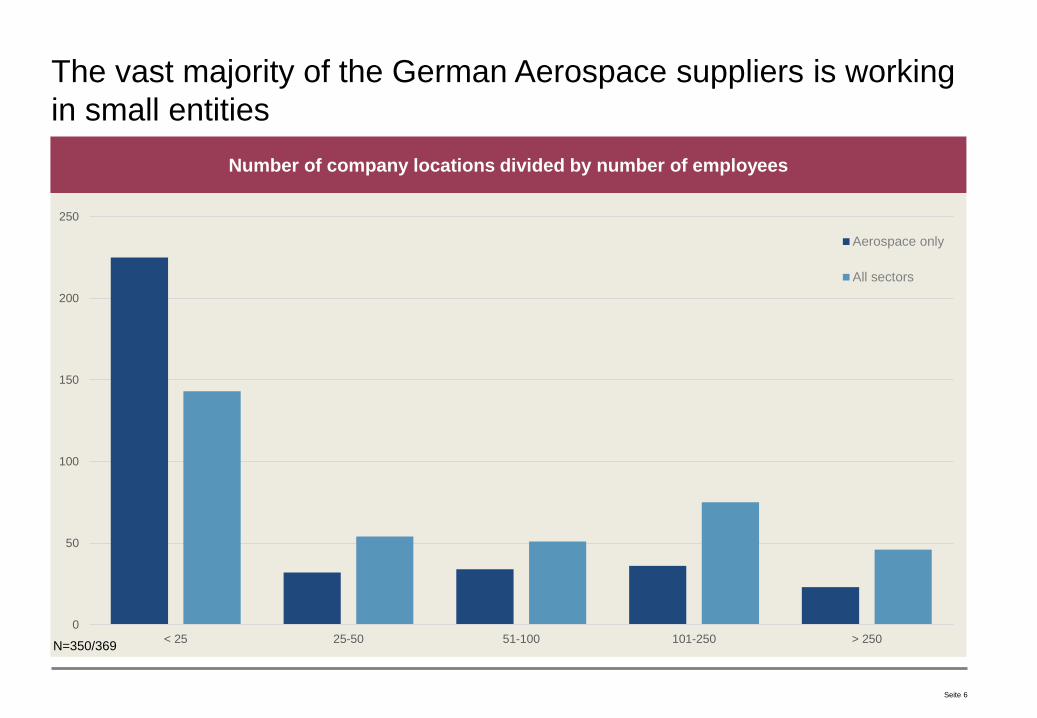

Number of company locations divided by number of employees

The vast majority of the German Aerospace suppliers is working

in small entities

0

50

100

150

200

250

< 25 25-50 51-100 101-250 > 250

Aerospace only

All sectors

N=350/369

Seite 7

224

0

60

11

124

194

88

150

188

255

155

181

153

61

86

113

196

247

190

190

220

127

127

127

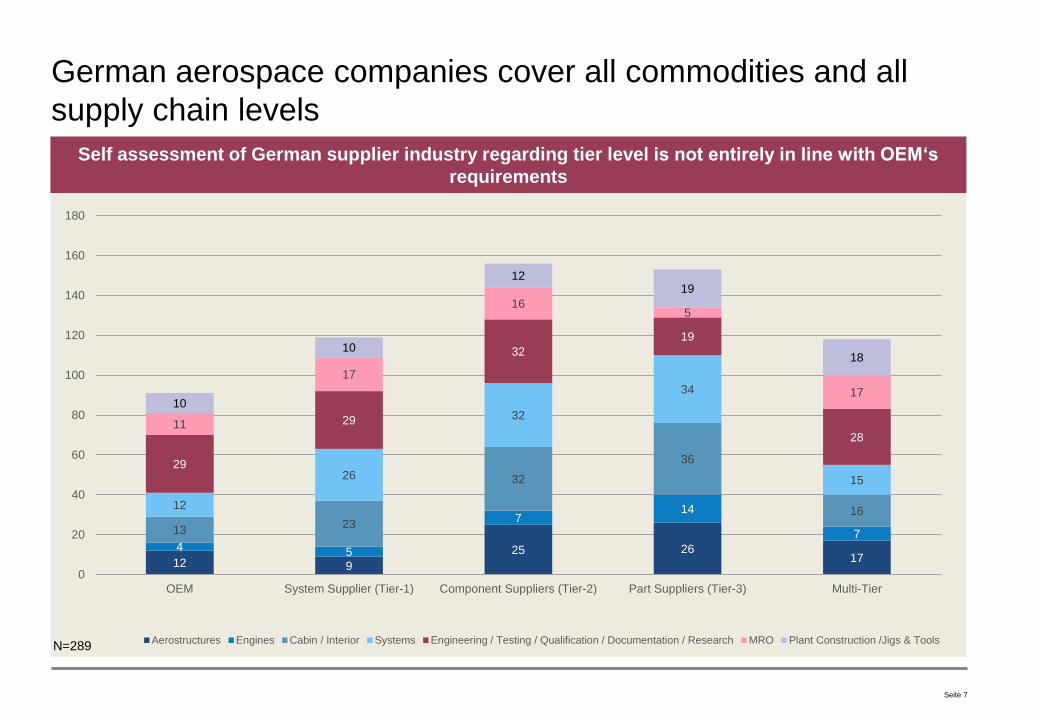

Self assessment of German supplier industry regarding tier level is not entirely in line with OEM‘s

requirements

German aerospace companies cover all commodities and all

supply chain levels

N=289

12 9

25 26 17

4 5

7 14

7 13 23

32

36

16 12

26

32

34

15

29

29

32

19

28 11

17

16 5

17 10

10

12 19

18

0

20

40

60

80

100

120

140

160

180

OEM System Supplier (Tier-1) Component Suppliers (Tier-2) Part Suppliers (Tier-3) Multi-Tier

Aerostructures Engines Cabin / Interior Systems Engineering / Testing / Qualification / Documentation / Research MRO Plant Construction /Jigs & Tools

Seite 8

224

0

60

11

124

194

88

150

188

255

155

181

153

61

86

113

196

247

190

190

220

127

127

127

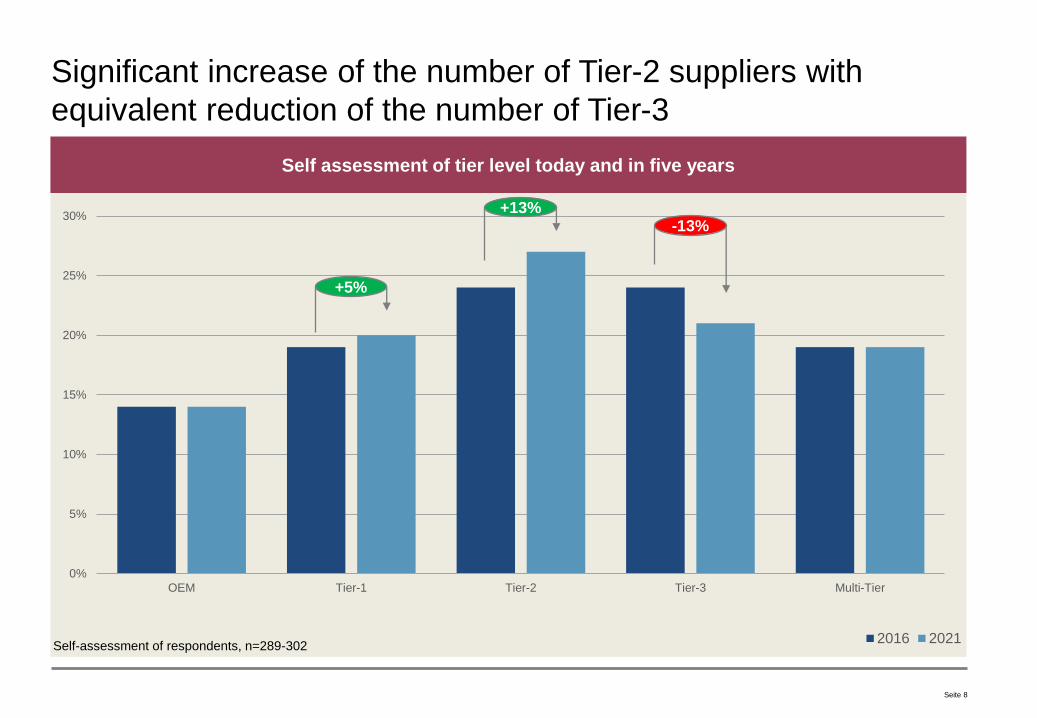

Significant increase of the number of Tier-2 suppliers with

equivalent reduction of the number of Tier-3

Self assessment of tier level today and in five years

Self-assessment of respondents, n=289-302

0%

5%

10%

15%

20%

25%

30%

OEM Tier-1 Tier-2 Tier-3 Multi-Tier

2016 2021

+13%

+5%

-13%

Seite 9

224

0

60

11

124

194

88

150

188

255

155

181

153

61

86

113

196

247

190

190

220

127

127

127

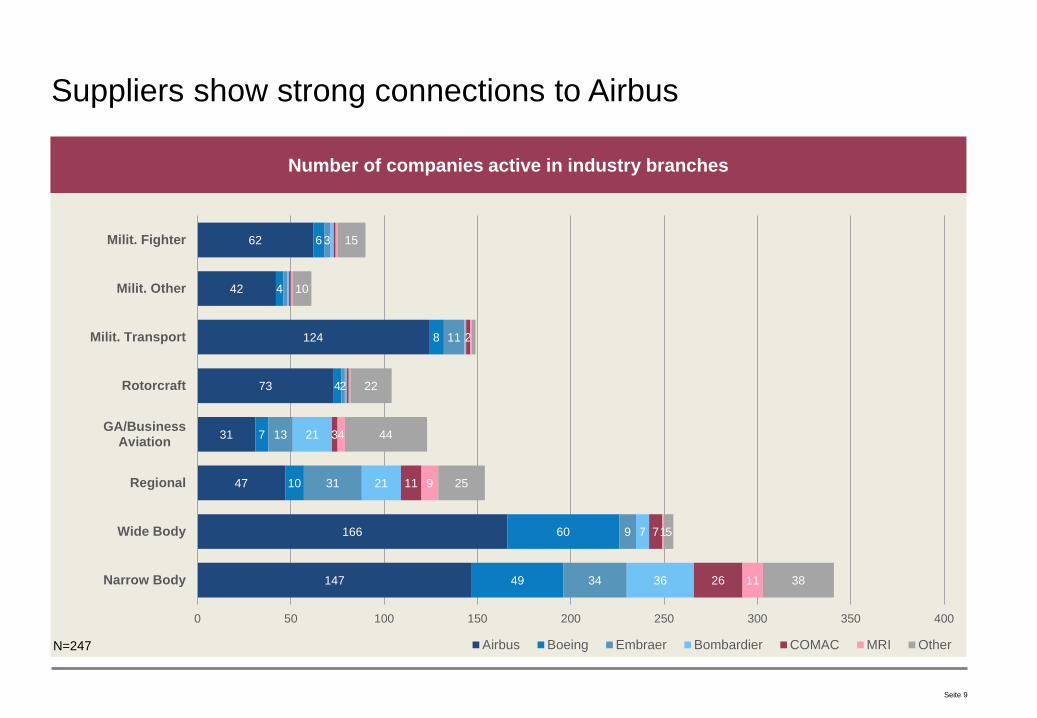

Suppliers show strong connections to Airbus

Number of companies active in industry branches

N=247

147

166

47

31

73

124

42

62

49

60

10

7

4

8

4

6

34

9

31

13

2

11

3

36

7

21

21

26

7

11

3

2

11

1

9

4

38

5

25

44

22

10

15

0 50 100 150 200 250 300 350 400

Narrow Body

Wide Body

Regional

GA/BusinessAviation

Rotorcraft

Milit. Transport

Milit. Other

Milit. Fighter

Airbus Boeing Embraer Bombardier COMAC MRI Other

Seite 10

224

0

60

11

124

194

88

150

188

255

155

181

153

61

86

113

196

247

190

190

220

127

127

127

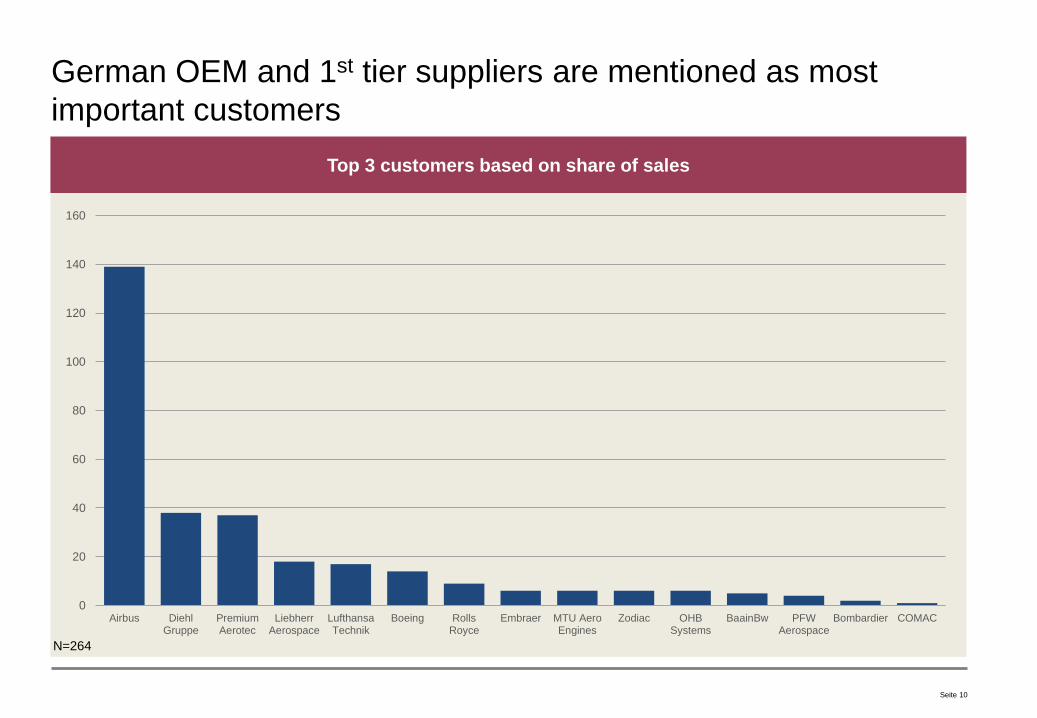

German OEM and 1st tier suppliers are mentioned as most

important customers

Top 3 customers based on share of sales

N=264

0

20

40

60

80

100

120

140

160

Airbus DiehlGruppe

PremiumAerotec

LiebherrAerospace

LufthansaTechnik

Boeing RollsRoyce

Embraer MTU AeroEngines

Zodiac OHBSystems

BaainBw PFWAerospace

Bombardier COMAC

Seite 11

224

0

60

11

124

194

88

150

188

255

155

181

153

61

86

113

196

247

190

190

220

127

127

127

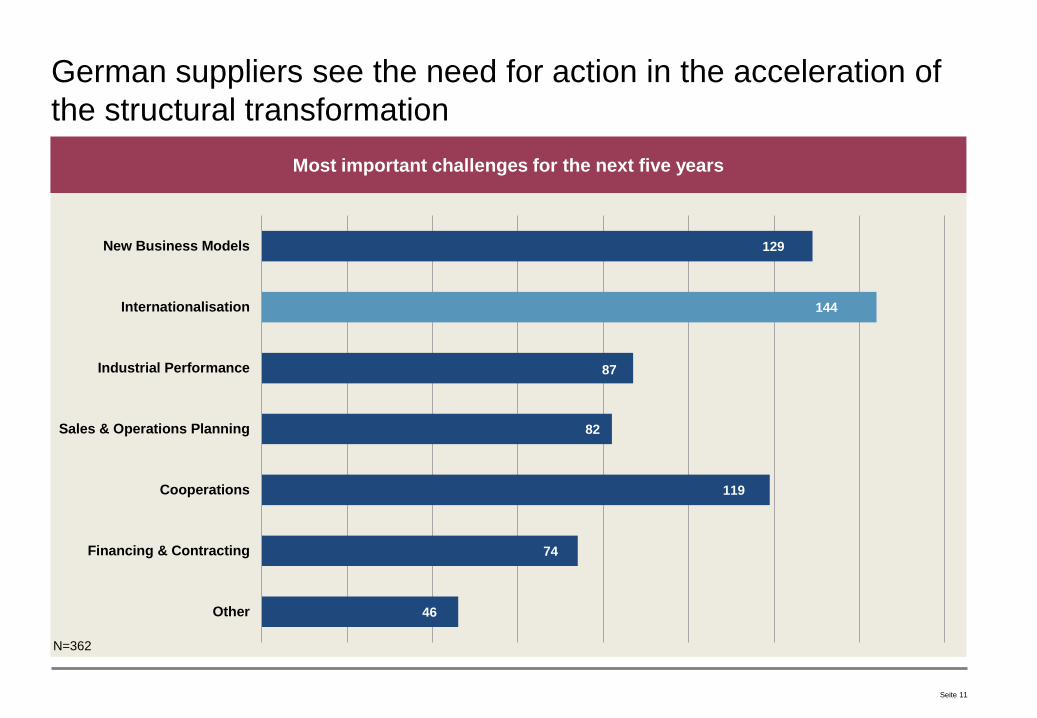

German suppliers see the need for action in the acceleration of

the structural transformation

Most important challenges for the next five years

N=362

129

144

87

82

119

74

46

New Business Models

Internationalisation

Industrial Performance

Sales & Operations Planning

Cooperations

Financing & Contracting

Other

Seite 12

224

0

60

11

124

194

88

150

188

255

155

181

153

61

86

113

196

247

190

190

220

127

127

127

Internationalisation has been identified as the biggest challenge

of the industry

The German aerospace industry is already present in most parts of the world

Seite 13

224

0

60

11

124

194

88

150

188

255

155

181

153

61

86

113

196

247

190

190

220

127

127

127

Germany is still the most important target market

Alternative: Target markets for sales, manufacturing and procurement

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Sales

Manufacturing

Procurement

Seite 14

224

0

60

11

124

194

88

150

188

255

155

181

153

61

86

113

196

247

190

190

220

127

127

127

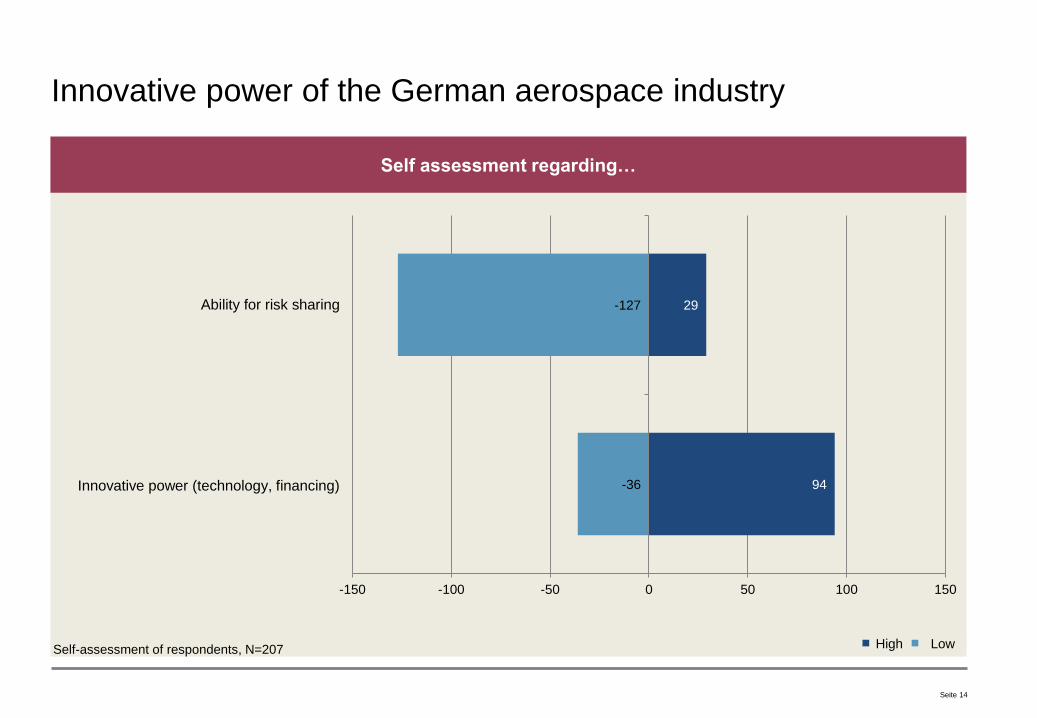

Innovative power of the German aerospace industry

Self assessment regarding…

Self-assessment of respondents, N=207

94

29

-36

-127

-150 -100 -50 0 50 100 150

Innovative power (technology, finanzing)

Ability for risk sharing

Hoch GeringHigh Low

Innovative power (technology, financing)

Seite 15

224

0

60

11

124

194

88

150

188

255

155

181

153

61

86

113

196

247

190

190

220

127

127

127

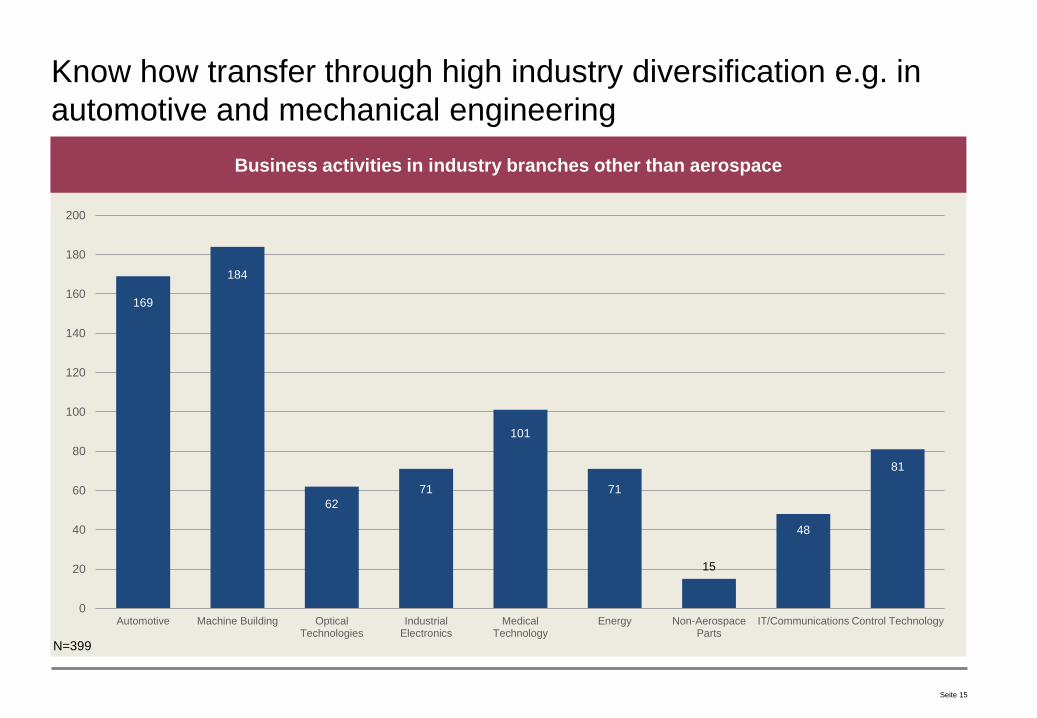

Know how transfer through high industry diversification e.g. in

automotive and mechanical engineering

Business activities in industry branches other than aerospace

N=399

169

184

62

71

101

71

15

48

81

0

20

40

60

80

100

120

140

160

180

200

Automotive Machine Building OpticalTechnologies

IndustrialElectronics

MedicalTechnology

Energy Non-AerospaceParts

IT/Communications Control Technology

Seite 16

224

0

60

11

124

194

88

150

188

255

155

181

153

61

86

113

196

247

190

190

220

127

127

127

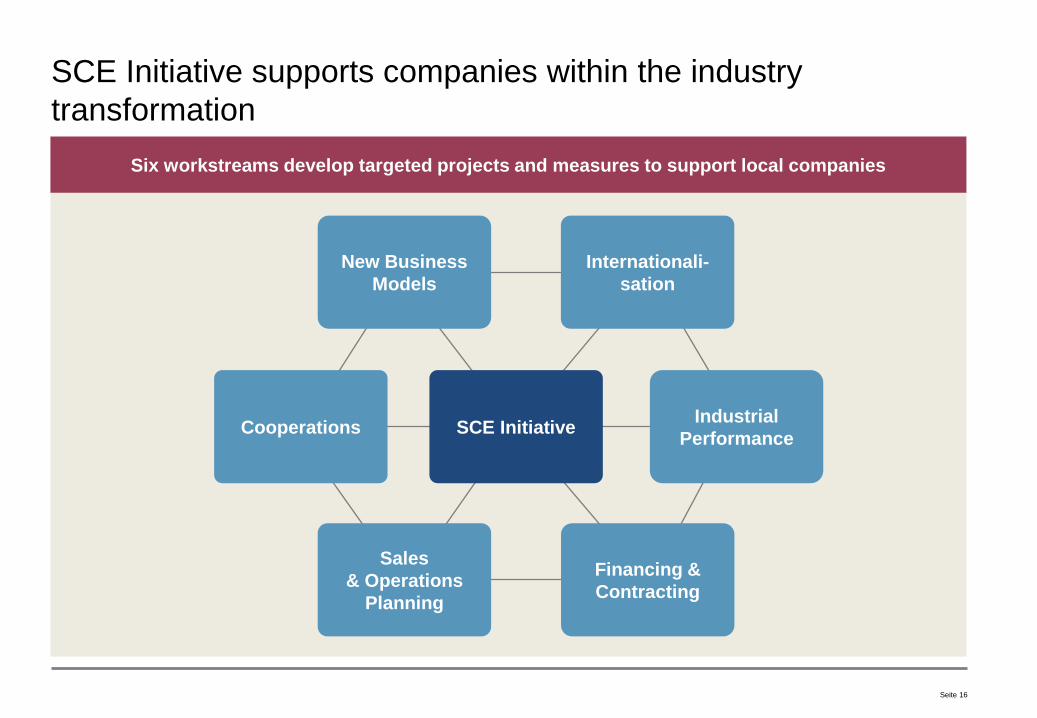

SCE Initiative supports companies within the industry

transformation

Six workstreams develop targeted projects and measures to support local companies

SCE Initiative Cooperations

Internationali-

sation

Sales

& Operations

Planning

New Business

Models

Financing &

Contracting

Industrial

Performance

An initiative by

Thank you!