surviving the nuclear winter presentation to mineafrica london december 1 st 2008

TRANSCRIPT

Surviving the Nuclear Winter

Presentation to MINEAfricaLondon December 1st 2008

Plastics – Need I say more!

Metal Prices in retreat

Copper (-59.0%)

Nickel (-81.3%)

Gold (-19.0%)

Platinum (-62.5%)

FTSE Mining Index plunges by 64% since July

The Collapse of the Aim MarketMining Index down 80% since July

The Impact upon Junior Mining Co’s• Collapse of market valuations

• No access to equity capital markets

• No credit available

• Deterioration of project economics

– Producers

– Developers

– Explorers

• Project financings under pressure

• Need to conserve cash

• Consolidation trend accelerates

• Exposure to predators

The Impact upon Africa

• Low creditworthiness shelters impacts

• Exposure to commodity markets

• Evaporation of inward investment

• Collapse of Government revenues and employment

• Effects of poor infrastructure

• Heightened social disruption

• China – Africa love-affair end

• Contract renegotiation pressures weaken

The Impact upon AfricaBotswana 20% reduction of diamond production by Debswana

Junior resource companies under financial pressure.

DR of Congo Collapse of cobalt concentrate exports as metal price plungesCamec ceases production. Relationship with China cools.Revisitation process peters out.

Madagascar $3 billion Ambatovy project shelved by Sherritt

Mozambique

Aluminium price fall slashes Mozal revenuesFinancial restructuring at Kenmare

Namibia Weatherley closes mines and cuts back at TsumebDiamond revenues fall

South Africa Misplaced optimism by Government although Rand depreciation mitigates impact. Platinum prices collapse. Ferro alloy markets trashed. Gold price holding up relatively well.

Zambia Retrenchment of copper mining operations and workforce.

Zimbabwe Economic and political crisis intensifies. Bindura nickel placed on care and maintenance.

How bad will it get? The Kondratieff Wave

•A Kondratieff Winter would extend beyond 2010

Is there any good news?

• Credit crunch has speeded up adjustment– Retrenchment of production– Shelving of projects

……this could accelerate recovery

• Capital and operating costs are falling and equipment lead-times are reducing

• Even in Great Depression, metal prices started to recover

• Long term commodity supercycle might still be intact

– Resumption of growth for BRIC economies

Copper S Curve – Income v Consumption

Japan

USA

Taiwan

S.Korea

EU/EEA

Canada

AustraliaMalaysia

India

China

Russia

Brazil

GDP/capita (2007 000$)

kg/c

apita

Cu

cons

umpti

on

Source: CRU Strategies

Data: LME, CRU

Early 70s boom,

ended by 1st oil crisis

Early 70s boom,

ended by 1st oil crisis

Mine capacity surge follows

second oil crisis

Mine capacity surge follows

second oil crisis

Global recovery,

Bougainville crisis and Zambian decline

Global recovery,

Bougainville crisis and Zambian decline

End of recessionEnd of

recession

Early 90s recessionEarly 90s recession

Hamanaka scandalHamanaka scandal

Asian crisisAsian crisis

Supply response fails to meet

booming demand from China

Supply response fails to meet

booming demand from China

Financial crisis

Financial crisis

Real and Nominal Cu Prices since 1970

So who will survive the Nuclear Winter?

Access to cash

Supportive shareholders

High quality projects

Strong and responsive management

Likely Survivors – The Invulnerable

• Impervious to radiation and cold

• Inaccessible

• Omnivorous

Namely, private companies with an untrashed market value , sound projects and financially secure owners

Likely Survivors – The Predators

• Top of food chain• Sharp claws and teeth• Reserves of fat• Fur coat

Namely, the cashed up, low geared, majors with operations in the lowest quartile should be able to acquire assets cheaply

Predator No 1 - Rio Tinto

on hearing that

BHP Billiton had withdrawn its bid

Predator No 2 – BHP Billiton

on watching

Rio Tinto’s

share-price collapse after

the bid was withdrawn

• Lesotho assets acquired in 2004

• Two adjacent kimberlite pipes

Satellite Pipe – 1.0 hectare with high grade (68 cpht) but low value (~$44 per carat) placed into production 2005.

Main Pipe – 8.6 hectares , with good grade (39 cpht) and value ($86 per carat), rediscovered by Kopane 2004-8

– Multiphase mineralisation

– 76 million tonnes now delineated containing 29.6 million tonnes with a value of $2.54 million.

– DFS currently in progress – publication mid 2009

• Recovered to date 340,000 carats and sold 292,000 carats, realising $16.1 million, equal to $55 per carat , including boart.

Kopane’s Liqhobong Assets

The Liqhobong Pipes

Alrosa cuts rough supplies

to market by 40%

The Crisis in the Diamond Industry

Diamond prices

plunge by 40-50%Indian diamantaire to lay-off 300 cutters

Gem Diamonds closes capacity in DRC

India calls for 1 month freeze

on diamond rough imports

Debswana Plans 20% Cut in

Diamond Production in 2009

The Collapse in Diamond Shares

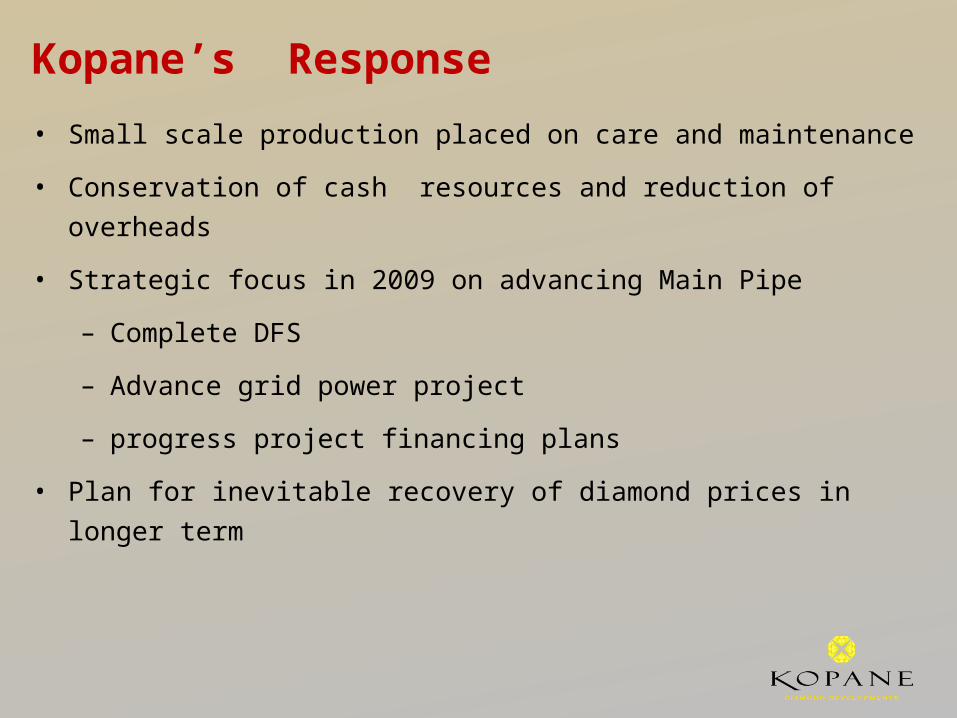

• Diamond prices have fallen by 30-50% in last four weeks• Liqhobong’s small scale plant not currently economic

Kopane’s Response

• Small scale production placed on care and maintenance

• Conservation of cash resources and reduction of overheads

• Strategic focus in 2009 on advancing Main Pipe

– Complete DFS

– Advance grid power project

– progress project financing plans

• Plan for inevitable recovery of diamond prices in longer term

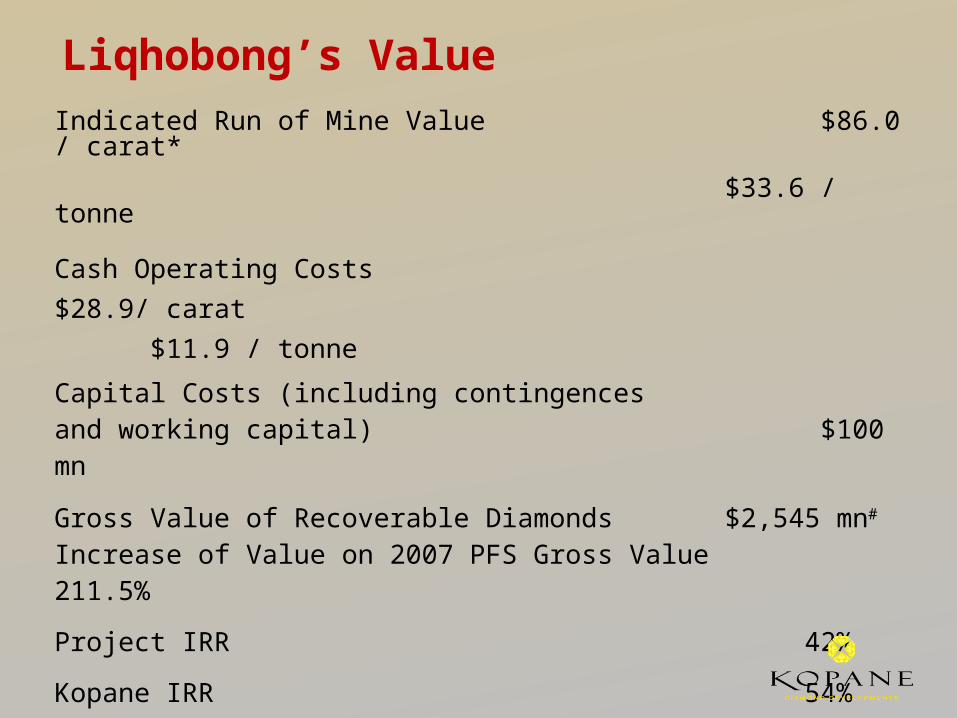

Liqhobong’s ValueIndicated Run of Mine Value $86.0 / carat*

$33.6 / tonne

Cash Operating Costs

$28.9/ carat

$11.9 / tonne

Capital Costs (including contingences and working capital) $100 mn

Gross Value of Recoverable Diamonds $2,545 mn# Increase of Value on 2007 PFS Gross Value 211.5%

Project IRR 42%

Kopane IRR 54%

Capital Payback < 2 years

* based on a bulk sample of 12,512 carats in August 2008# New interim KDD Resource model