sustained sales and earnings growth - air liquide

TRANSCRIPT

H1 2015

Paris, July 30, 2015

Sustained sales and earnings growth

2015 H1 activityBenoît Potier l Chief Executive OfficerParis, July 30, 2015

Sustained sales and earnings growth

• Sales +8%

• Strong operating margin at 17.4%

• Net profit +12%

• Major new projects and pursued acquisitions

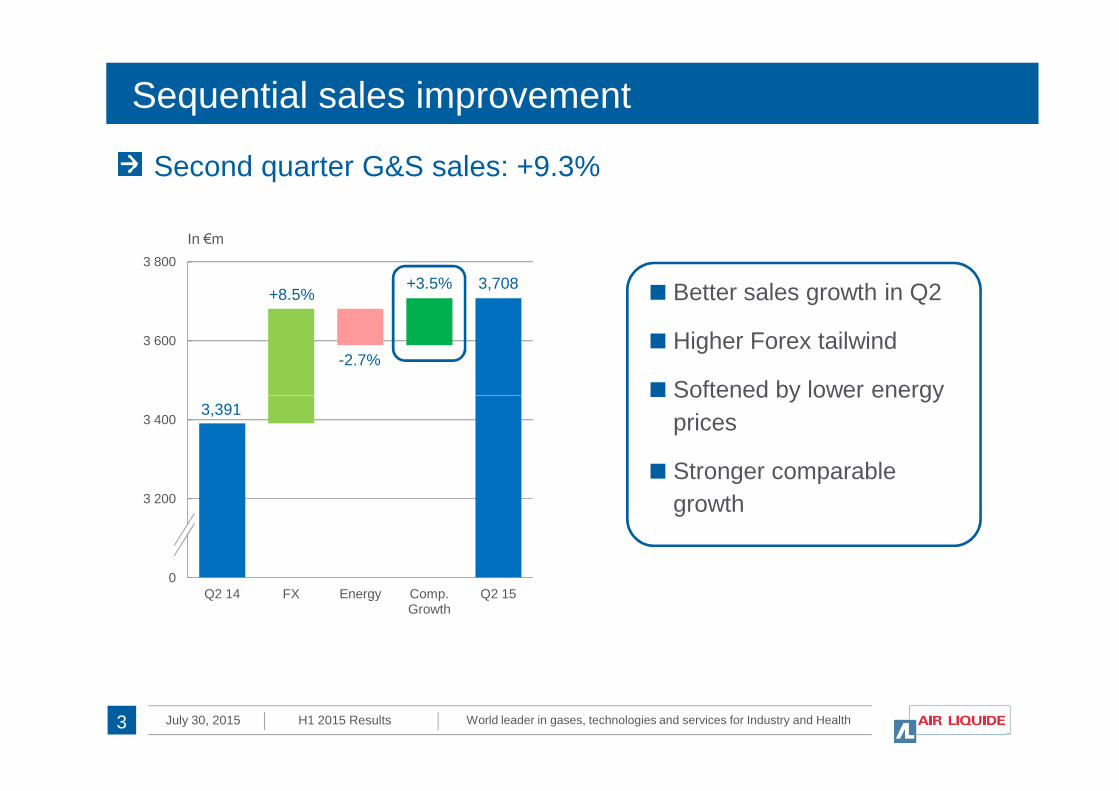

Sequential sales improvement

In €m

3 600

3 800

3,708+8.5%

-2.7%

+3.5%

Second quarter G&S sales: +9.3%

Better sales growth in Q2

Higher Forex tailwind

Softened by lower energy

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results3

3 000

3 200

3 400

Q2 14 FX Energy Comp.Growth

Q2 15

3,391Softened by lower energy

prices

Stronger comparable

growth

An uncertain global economic environment

4

6

8Year on Year in % (3-month rolling average) Softening manufacturing in

China

Low Brazilian economy

Low growth in South East Asia

Industrial Production

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results4

-4

-2

0

2

Source Coe-Rexecode

Low oil price impact in North

America

Weak mining industry in

Australia

Progressive recovery in Europe

World

United States

Euro Zone

Developing Economies

2013 2014 2015

600

800

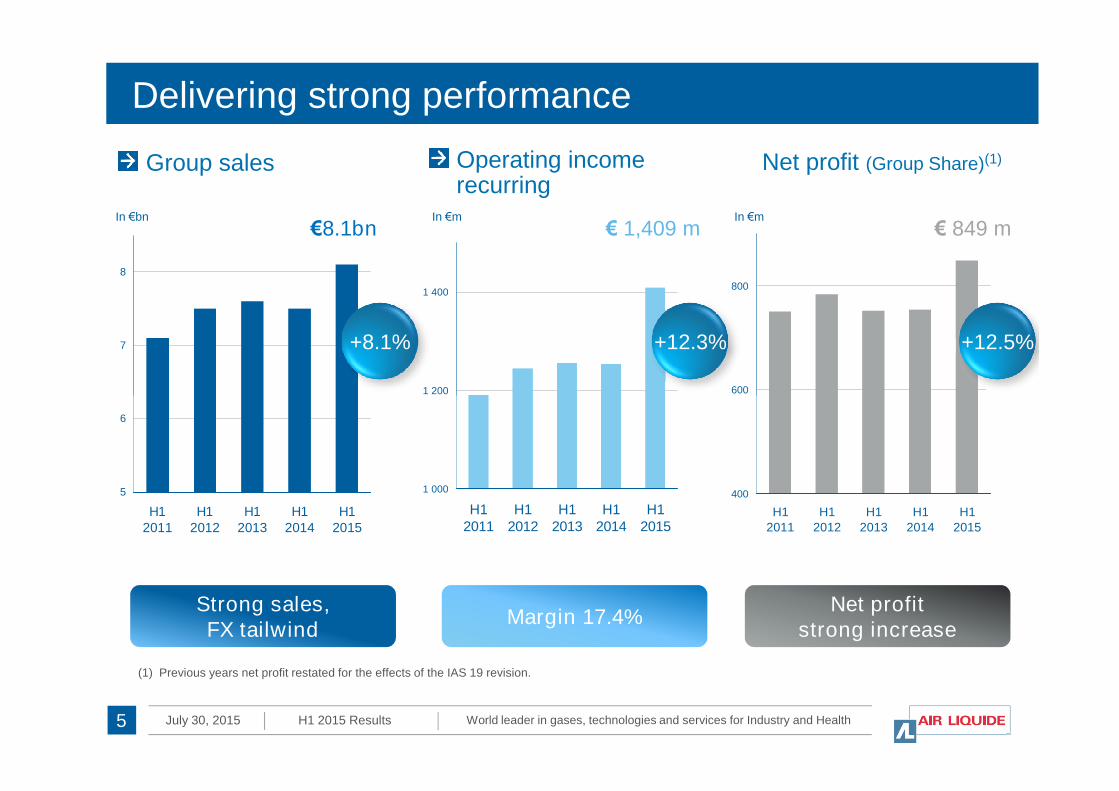

Delivering strong performance

In €mIn €m

Net profit (Group Share)(1)Operating incomerecurring

1 200

1 400

Group sales

7

8

In €bn€8.1bn

+12.5%+8.1% +12.3%

€ 1,409 m € 849 m

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

400

600

H12011

H12012

H12013

H12014

H12015

(1) Previous years net profit restated for the effects of the IAS 19 revision.

1 000

1 200

H12011

H12012

H12013

H12014

H12015

5

5

6

H12011

H12012

H12013

H12014

H12015

Margin 17.4%Net profit

strong increaseStrong sales,FX tailwind

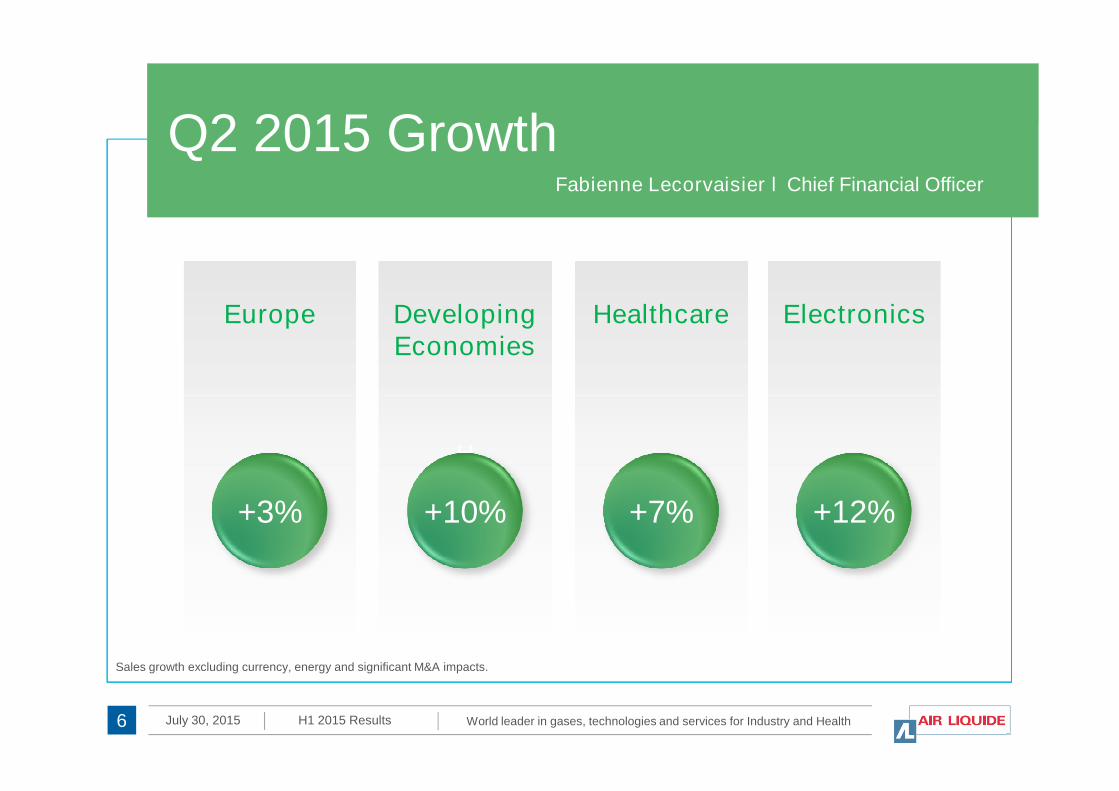

Fabienne Lecorvaisier l Chief Financial Officer

Q2 2015 Growth

Europe DevelopingEconomies

Healthcare Electronics

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

H

6

+10% +7% +12%

Sales growth excluding currency, energy and significant M&A impacts.

+3%

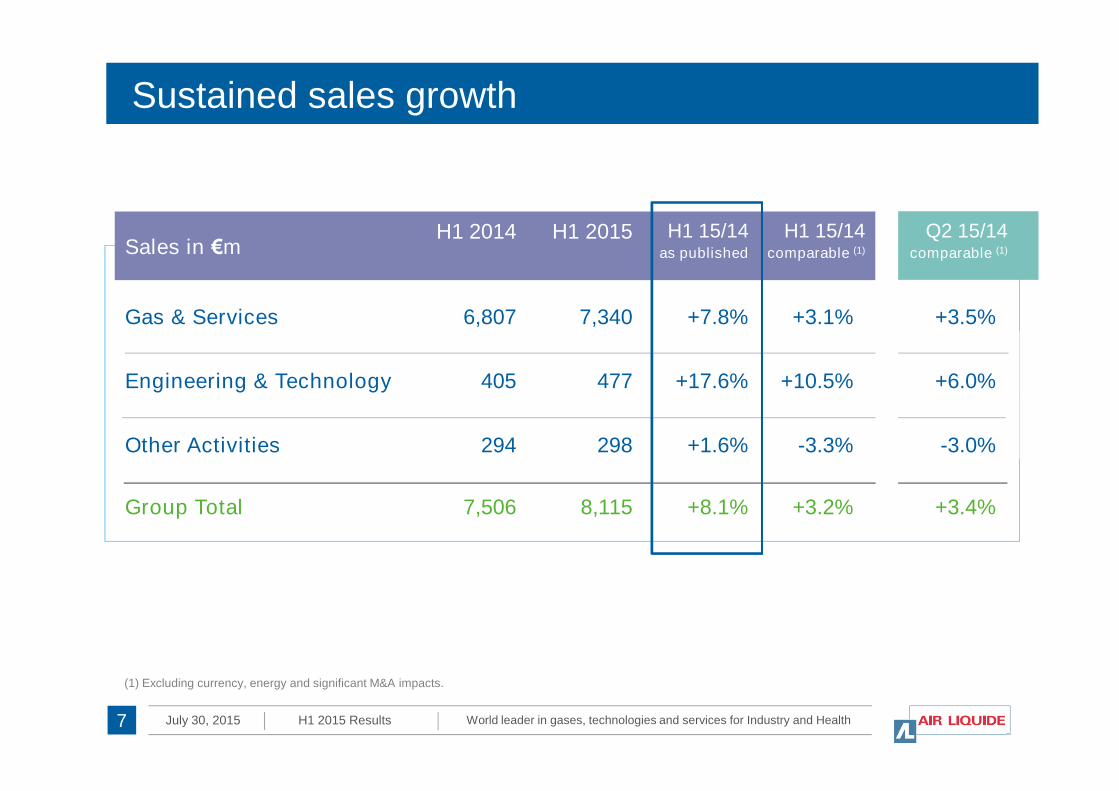

Sustained sales growth

Sales in €mH1 2014 H1 2015 H1 15/14

as published

H1 15/14comparable (1)

Q2 15/14comparable (1)

Gas & Services 6,807 7,340 +7.8% +3.1% +3.5%

Engineering & Technology 405 477 +17.6% +10.5% +6.0%

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results7

Other Activities 294 298 +1.6% -3.3% -3.0%

Group Total 7,506 8,115 +8.1% +3.2% +3.4%

(1) Excluding currency, energy and significant M&A impacts.

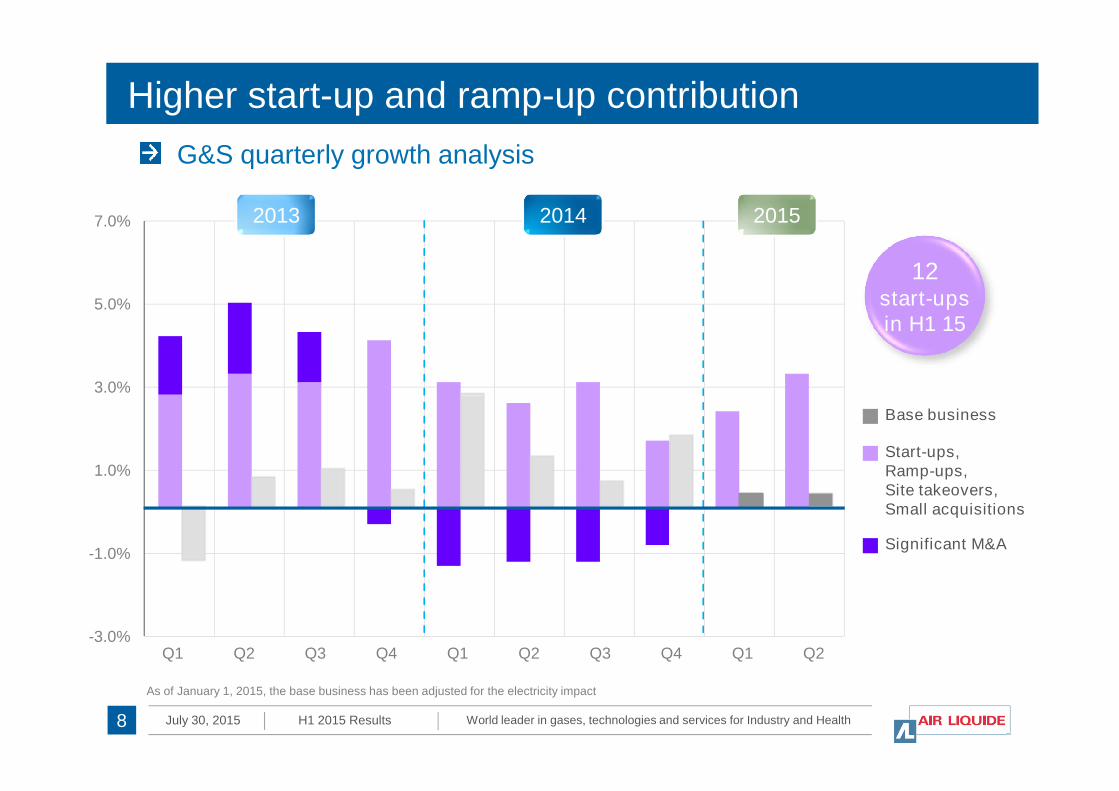

3.0%

5.0%

7.0%

G&S quarterly growth analysis

Higher start-up and ramp-up contribution

12start-upsin H1 15

2013 2014 2015

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

-3.0%

-1.0%

1.0%

3.0%

8

Base business

Start-ups,Ramp-ups,Site takeovers,Small acquisitions

Significant M&A

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

As of January 1, 2015, the base business has been adjusted for the electricity impact

Q2

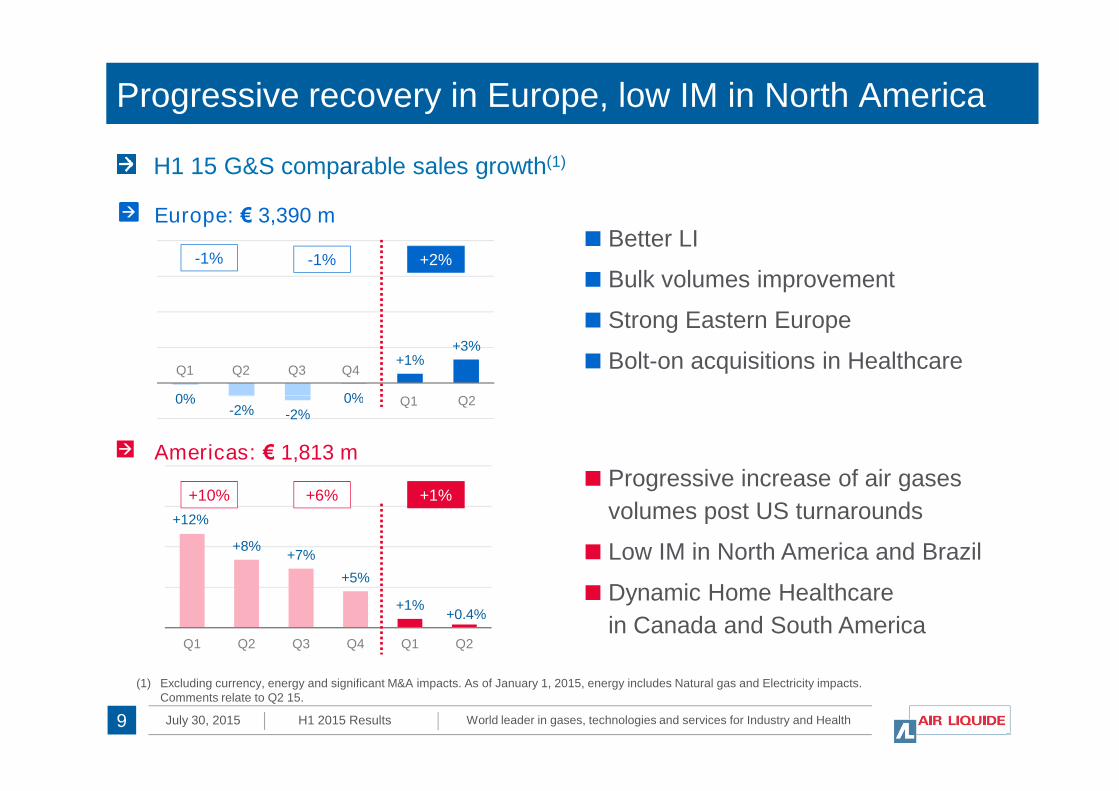

H1 15 G&S comparable sales growth(1)

Progressive recovery in Europe, low IM in North America

Europe: € 3,390 m

0% 0%

+1%+3%

Q2 Q3Q1

Q1

+2%Better LI

Bulk volumes improvement

Strong Eastern Europe

Bolt-on acquisitions in HealthcareQ4

Q2

-1% -1%

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results9

(1) Excluding currency, energy and significant M&A impacts. As of January 1, 2015, energy includes Natural gas and Electricity impacts.Comments relate to Q2 15.

Americas: € 1,813 m

+12%

+8%+7%

+5%

+1%+0.4%

Q1 Q2 Q3 Q4 Q1 Q2

+1%Progressive increase of air gases

volumes post US turnarounds

Low IM in North America and Brazil

Dynamic Home Healthcare

in Canada and South America

0%-2% -2%

0% Q1 Q2

+10% +6%

H1 15 G&S comparable sales growth(1)

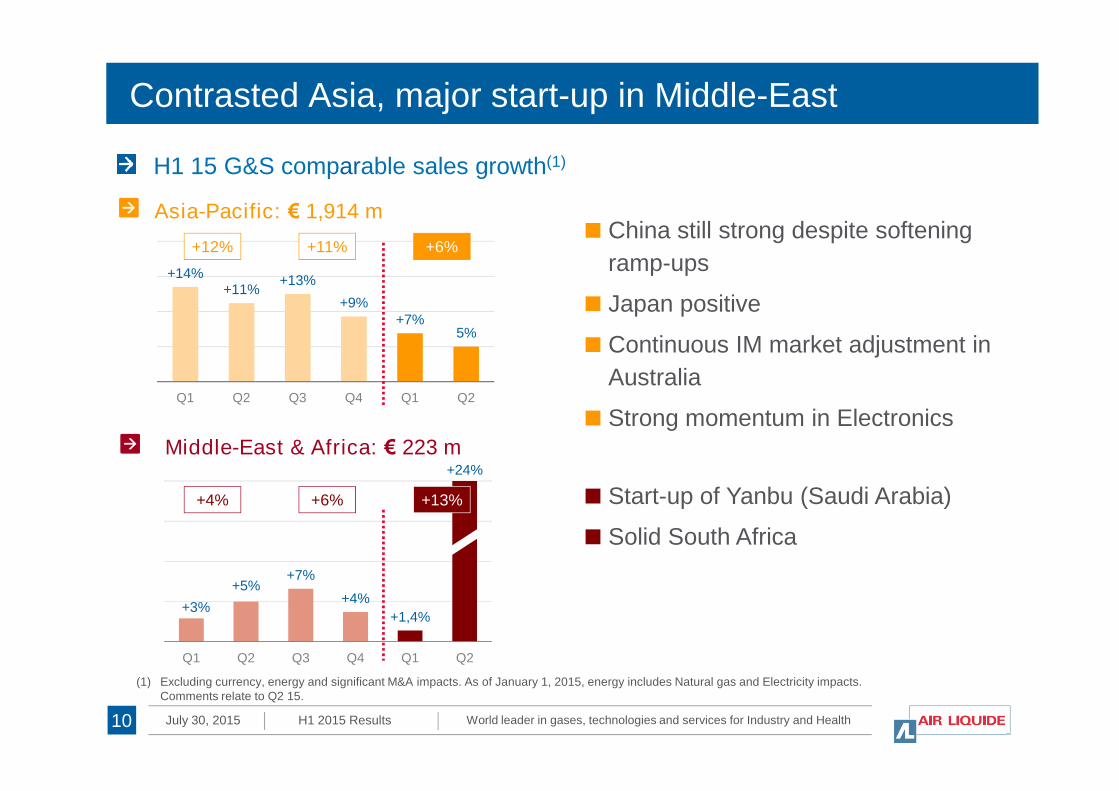

Contrasted Asia, major start-up in Middle-East

Asia-Pacific: € 1,914 m

+14%+11%

+13%

+9%+7%

5%

Q1 Q2 Q3 Q4 Q1 Q2

+6%China still strong despite softening

ramp-ups

Japan positive

Continuous IM market adjustment in

Australia

+12% +11%

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results10

Middle-East & Africa: € 223 m

Q1 Q2 Q3 Q4 Q1 Q2

+3%

+5%+7%

+4%

+1,4%

Q1 Q2 Q3 Q4 Q1 Q2

+13% Start-up of Yanbu (Saudi Arabia)

Solid South Africa

Strong momentum in Electronics

+24%

+4% +6%

(1) Excluding currency, energy and significant M&A impacts. As of January 1, 2015, energy includes Natural gas and Electricity impacts.Comments relate to Q2 15.

19%

10%

H1 15 G&S comparable growth(1)

H1

Strong Healthcare and Electronics

+5%

+3%+4% +3%

+7% +7%

Q1 Q2 Q3 Q4 Q1 Q2

Healthcare: € 1,382 m

Positive impact of bolt-onacquisitions

Strong Home Healthcare andHygiene

Better medical gases

+7%+4% +4%

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

10%

11

H12015

+10%

+13%+12%

+13%+14%

+12%

Q1 Q2 Q3 Q4 Q1 Q2

Electronics: € 733 m

Continued strong momentum

Ramp-ups in China

Advanced materials: +28%

+13%

Q1 Q2 Q3 Q4 Q1 Q2

+12%+12%

(1) Excluding currency, energy and significant M&A impacts. As of January 1, 2015, energy includes Natural gas and Electricity impacts.Comments relate to Q2 15.

+6%

+3% +4%

+1%0%

+5%

H1 15 G&S comparable sales growth(1)

Recovery in Large Industries, slow-down in Industrial Merchant

H135%

Large Industries: € 2,565 m Increasing air gases volumes

(Northern Europe, North America)

Robust growth in China,ramp-up effects softening

Yanbu hydrogen start-up inSaudi Arabia

+3%+3%+5%

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

Q1 Q2 Q3 Q4 Q1 Q2

12

H12015

35%

36%

+4%

+3%+2%

+3%

0%

-1.6%

Industrial Merchant: € 2,660 m

Low Oil & Mining activity inAdvanced Economies

Weak manufacturing environmentin North America

Continued growth in China

Pricing: +0.9%

-0.7%+2%+4%

Q2 Q3Q1 Q1Q4

Q2

(1) Excluding currency, energy and significant M&A impacts. As of January 1, 2015, energy includes Natural gas and Electricity impacts. Comments relate to Q2 15.

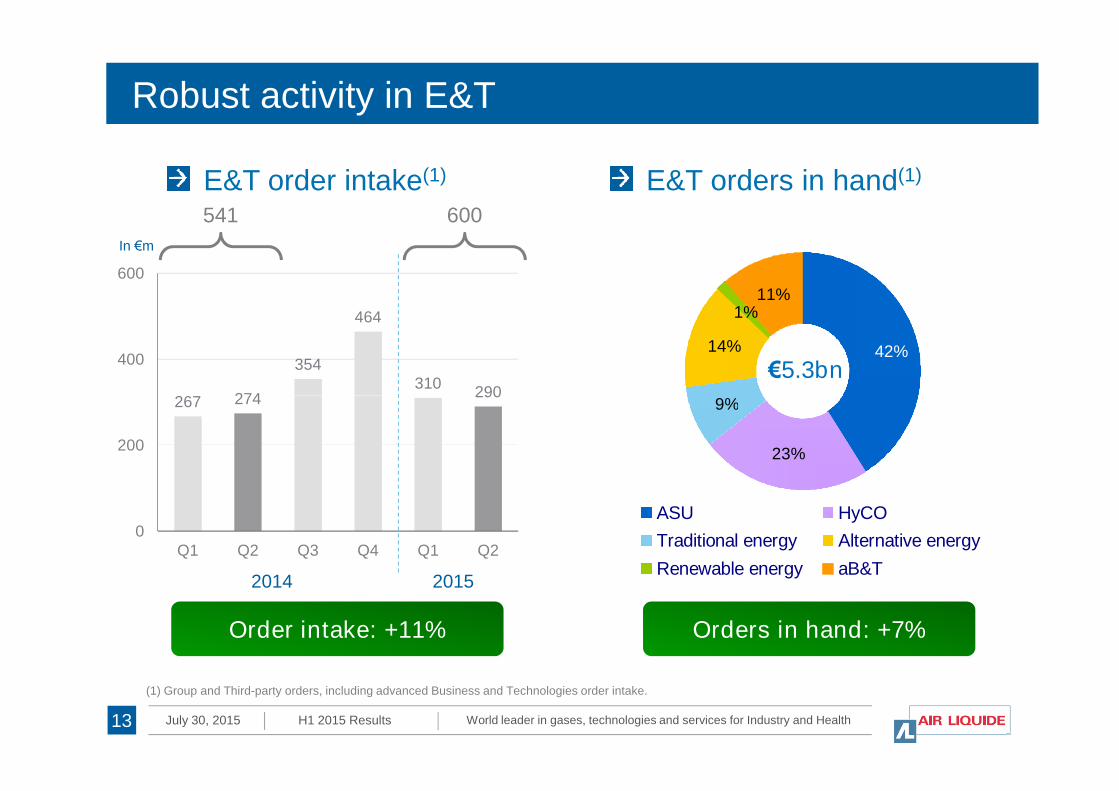

E&T order intake(1) E&T orders in hand(1)

541

In €m

267 274

354

464

310290

400

600

Robust activity in E&T

600

9%

14%

1%11%

42%

€5.3bn

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

(1) Group and Third-party orders, including advanced Business and Technologies order intake.

Order intake: +11%

267 274 290

0

200

Q1 Q2 Q3 Q4 Q1 Q2

2014 2015

13

23%

9%

ASU HyCO

Traditional energy Alternative energy

Renewable energy aB&T

Orders in hand: +7%

Fabienne Lecorvaisier l Chief Financial Officer

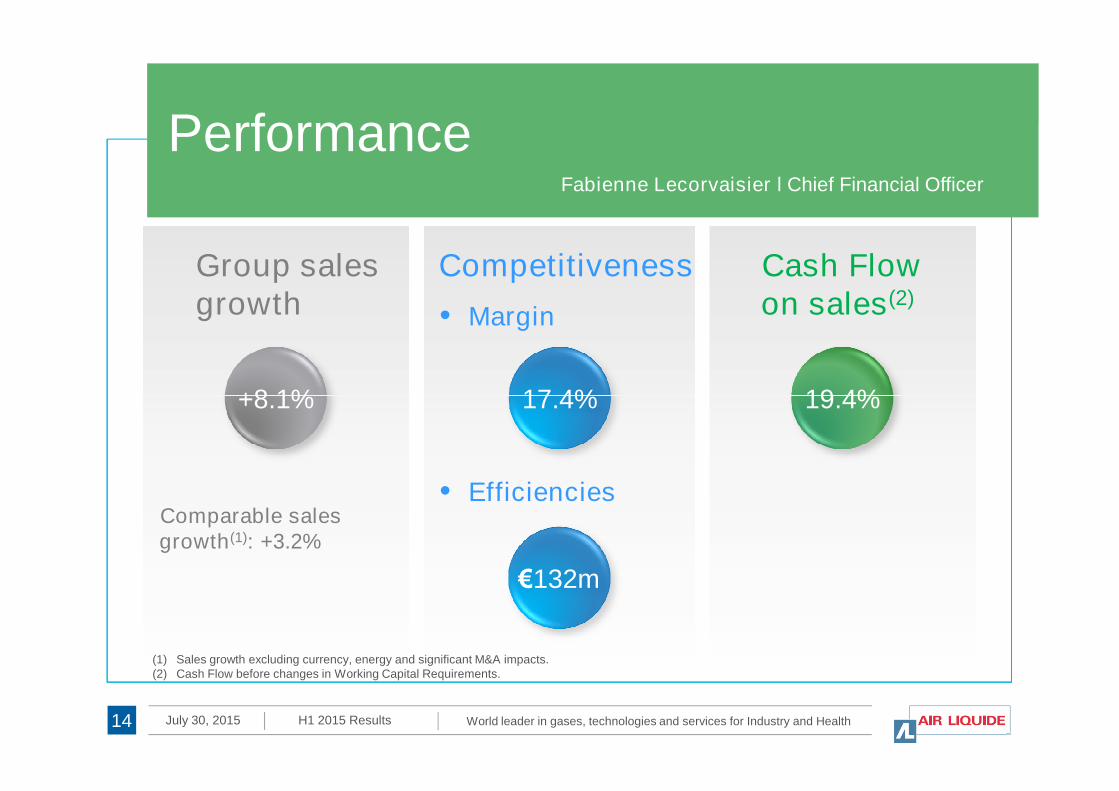

Performance

• Margin

+8.1% 17.4% 19.4%

Group salesgrowth

Competitiveness Cash Flowon sales(2)

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results14

(1) Sales growth excluding currency, energy and significant M&A impacts.(2) Cash Flow before changes in Working Capital Requirements.

Comparable salesgrowth(1): +3.2%

+8.1%

€132m

17.4%

• Efficiencies

19.4%

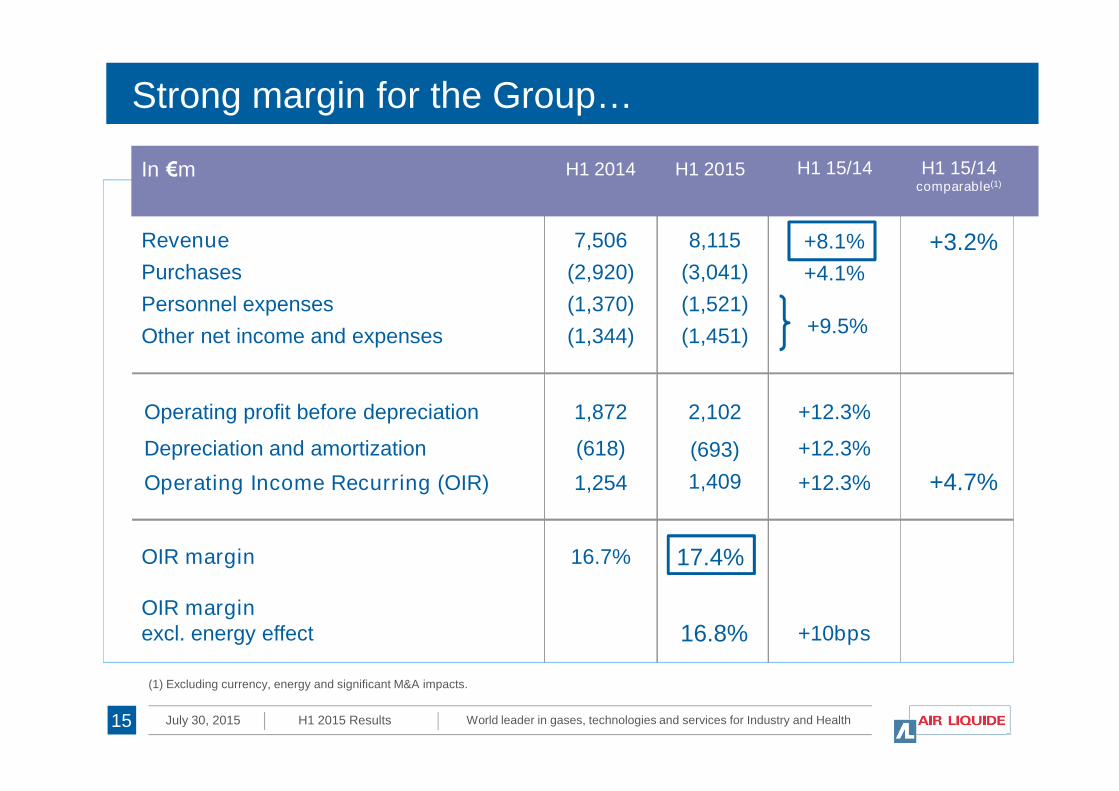

Strong margin for the Group…

In €m H1 2014 H1 2015 H1 15/14

Revenue

Purchases

Personnel expenses

Other net income and expenses

7,506

(2,920)

(1,370)

(1,344)

8,115

(3,041)

(1,521)

(1,451)

+8.1%

+4.1%

+9.5%

H1 15/14comparable(1)

+3.2%

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results15

Operating profit before depreciation 1,872 2,102 +12.3%

Depreciation and amortization

Operating Income Recurring (OIR)

(618)

1,254

(693)

1,409

+12.3%

+12.3%

OIR margin

OIR marginexcl. energy effect

16.7% 17.4%

16.8%

(1) Excluding currency, energy and significant M&A impacts.

+10bps

+4.7%

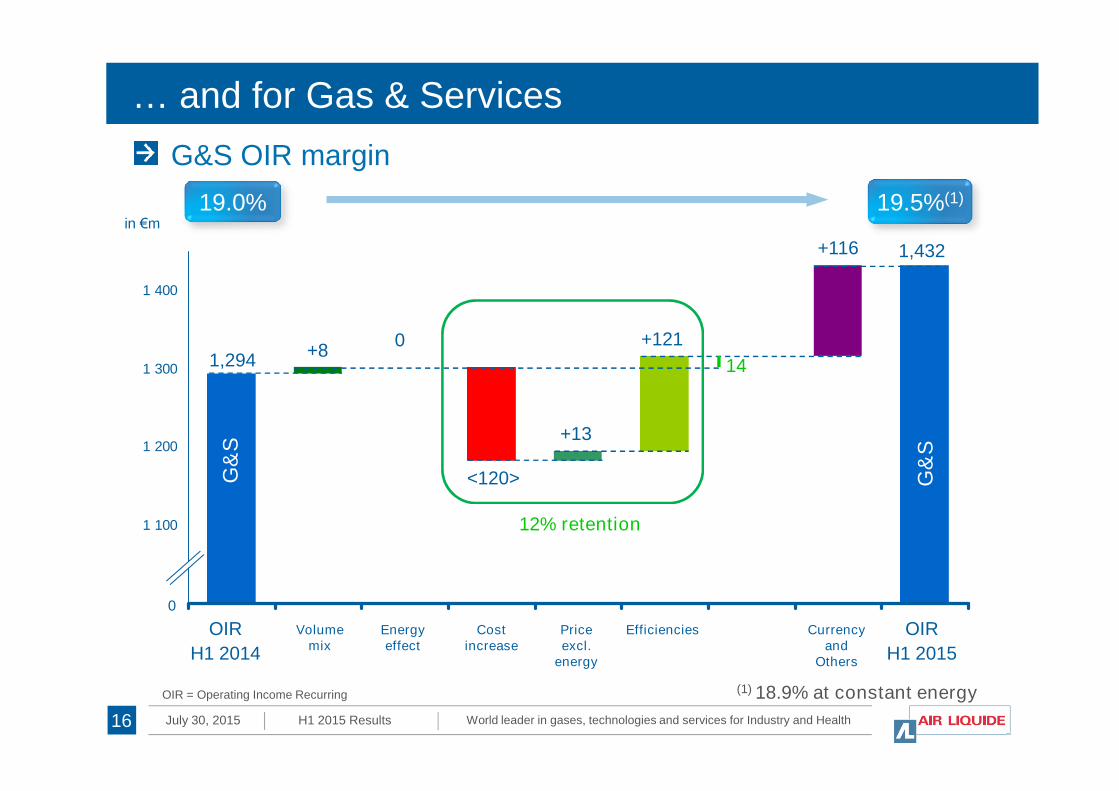

… and for Gas & Services

1 300

1 400

in €m

1,432

+121+8

1,2940

+116

19.5%(1)19.0%

G&S OIR margin

14

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results16

1 000

1 100

1 200

OIR = Operating Income Recurring (1) 18.9% at constant energy

0

OIR

H1 2015

<120>G&

S

G&

S

OIR

H1 2014

Volumemix

Energyeffect

Costincrease

Priceexcl.

energy

+13

Efficiencies Currencyand

Others

12% retention

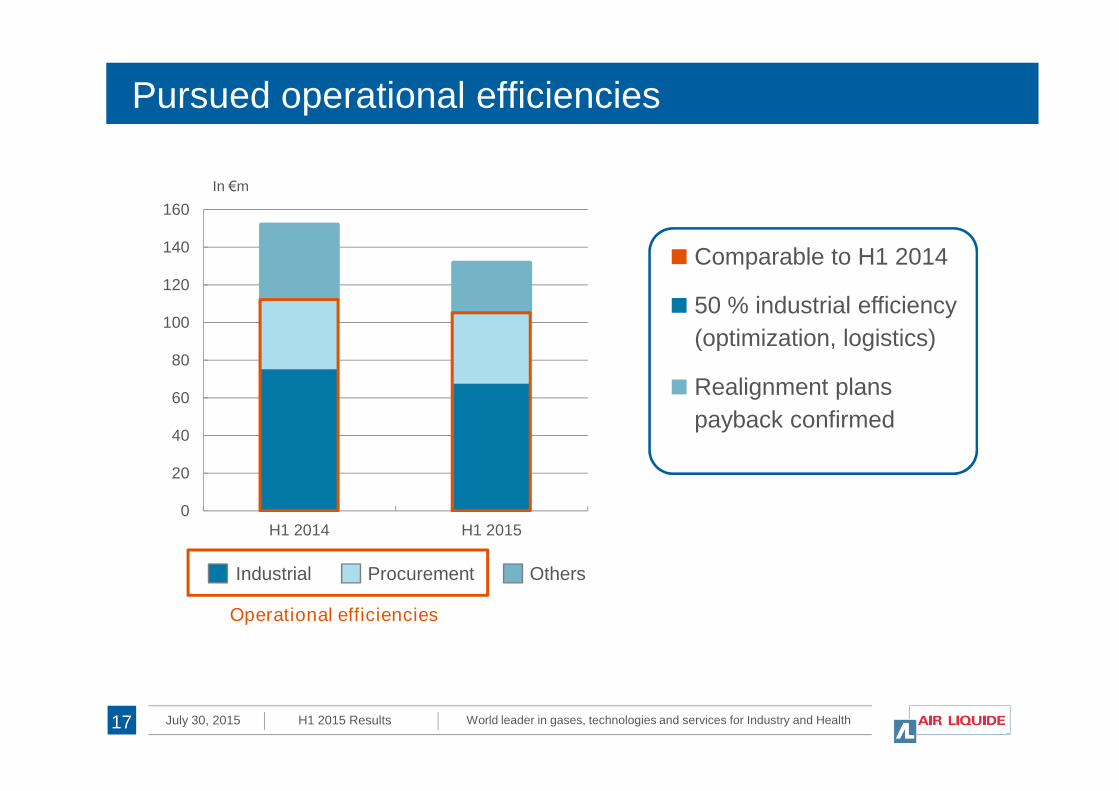

Pursued operational efficiencies

In €m

Comparable to H1 2014

50 % industrial efficiency

(optimization, logistics)

Realignment plans60

80

100

120

140

160

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results17

Realignment plans

payback confirmed

0

20

40

60

H1 2014 H1 2015

Industrial Procurement Others

Operational efficiencies

In €m 2012 2013

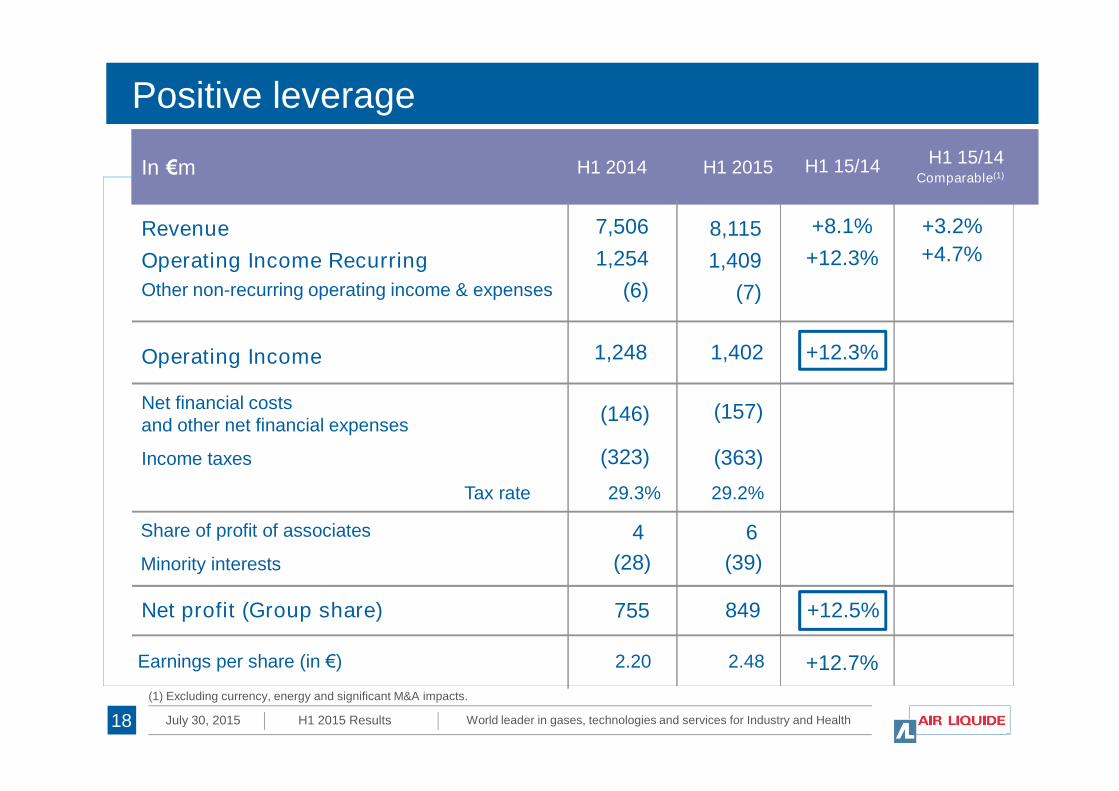

Positive leverage

Revenue

Operating Income Recurring

Other non-recurring operating income & expenses

7,506

1,254

(6)

8,115

1,409

(7)

+8.1%

+12.3%

Operating Income 1,248 1,402 +12.3%

Net financial costs

In €m H1 2014 H1 2015 H1 15/14 H1 15/14Comparable(1)

+3.2%

+4.7%

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results18

Net financial costsand other net financial expenses

Income taxes

Net profit (Group share)

Earnings per share (in €) 2.20 2.48

Tax rate 29.3% 29.2%

Share of profit of associates

Minority interests

(146)

(323)

4

(28)

755 849 +12.5%

(157)

(363)

(39)

6

(1) Excluding currency, energy and significant M&A impacts.

+12.7%

In €m

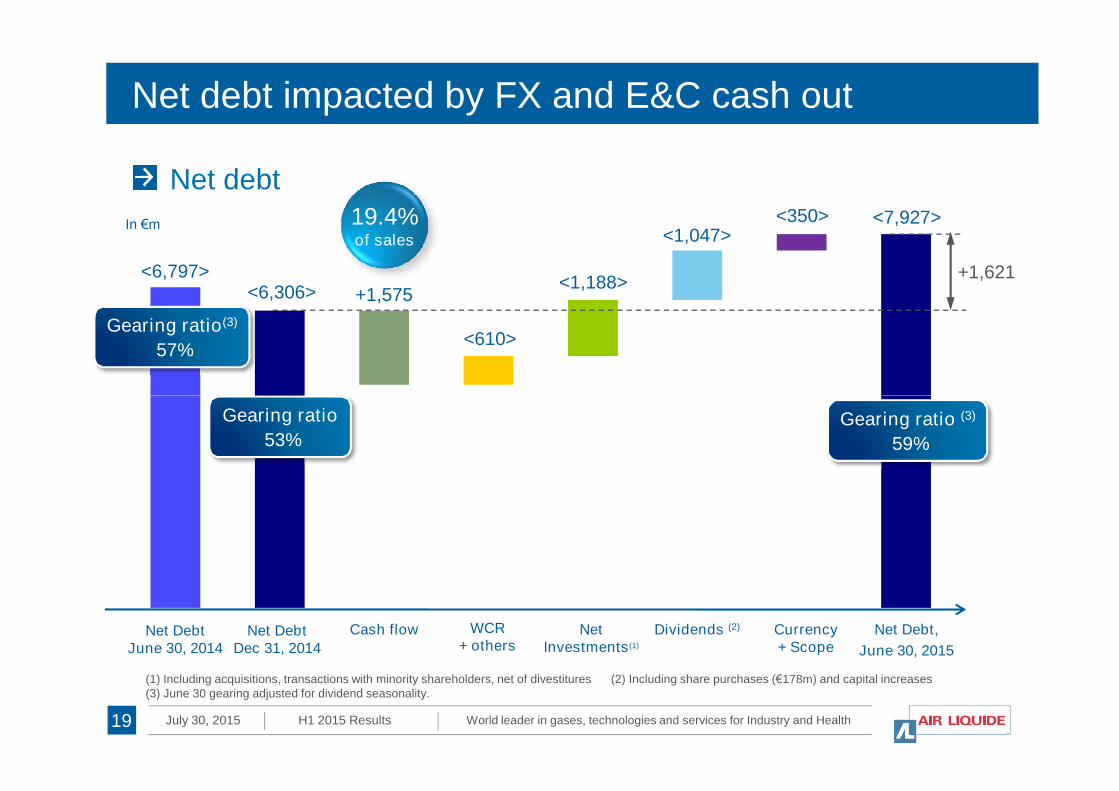

Net debt impacted by FX and E&C cash out

<6,306>

<7,927>

+1,575<1,188>

<1,047><350>

<610>

In €m

Net debt

+1,621<6,797>

Gearing ratio(3)

57%

19.4%of sales

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results19

Net Debt,

June 30, 2015

Cash flow NetInvestments(1)

Currency+ Scope

Net DebtDec 31, 2014

WCR+ others

(1) Including acquisitions, transactions with minority shareholders, net of divestitures (2) Including share purchases (€178m) and capital increases(3) June 30 gearing adjusted for dividend seasonality.

Dividends (2)

Gearing ratio

53%Gearing ratio (3)

59%

Net DebtJune 30, 2014

Major new projects and pursuedacquisitionsParis, July 30, 2015 Benoît Potier l Chief Executive Officer

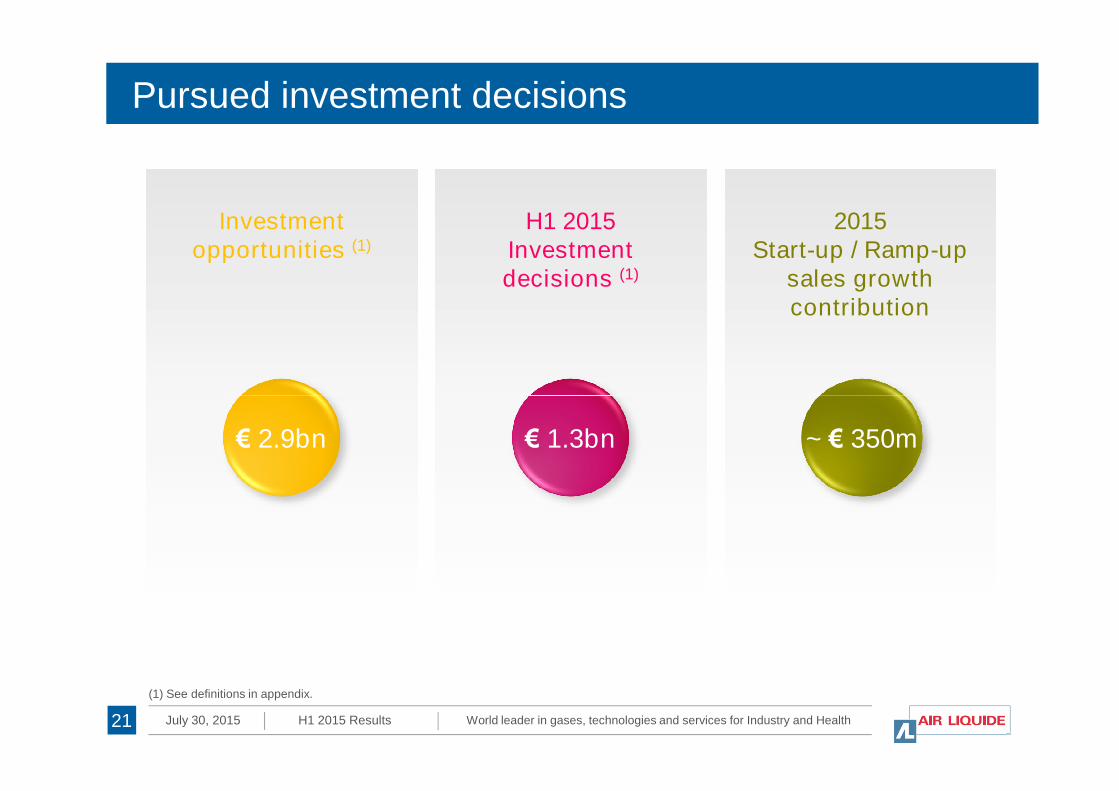

Pursued investment decisions

Investmentopportunities (1)

H1 2015Investmentdecisions (1)

2015Start-up / Ramp-up

sales growthcontribution

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results21

€ 2.9bn € 1.3bn

(1) See definitions in appendix.

~ € 350m

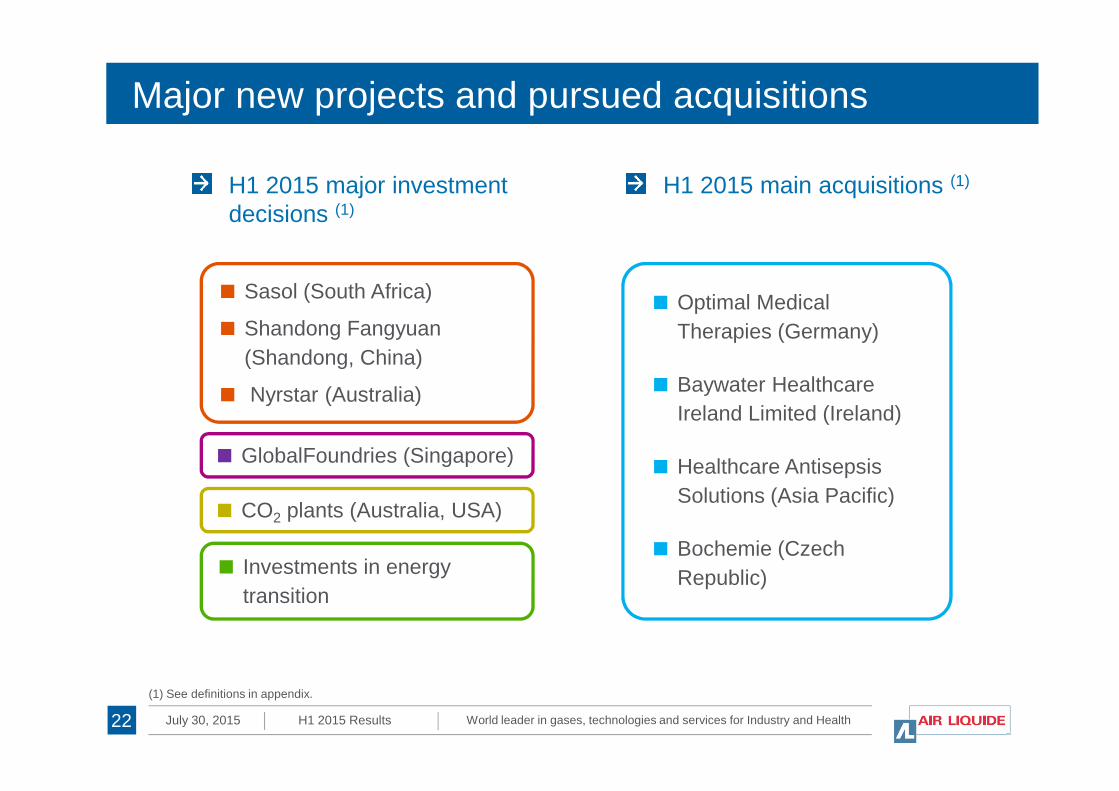

Major new projects and pursued acquisitions

Optimal Medical

Therapies (Germany)

Baywater Healthcare

Sasol (South Africa)

Shandong Fangyuan

(Shandong, China)

Nyrstar (Australia)

H1 2015 major investmentdecisions (1)

H1 2015 main acquisitions (1)

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results22

(1) See definitions in appendix.

Baywater Healthcare

Ireland Limited (Ireland)

Healthcare Antisepsis

Solutions (Asia Pacific)

Bochemie (Czech

Republic)

Nyrstar (Australia)

GlobalFoundries (Singapore)

CO2 plants (Australia, USA)

Investments in energy

transition

Major state-of-the-art syngas plant start-ups in H1 2015

Dormagen (Germany) Yanbu (Saudi Arabia)

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results23

Carbon monoxide for Bayer

Achieved flexibility in line with

customer’s expectations

Hydrogen by-product

exported to pipeline network

Hydrogen for Yasref

Tested feedstock to date:

natural gas, butane and mixture

Ramp-up in line

Investment backlog adjusting due to major start-ups

€ 2.8bn

Decisions Start-ups

Investment backlog H1 2015

€ 2.7bn

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results24

Dec 2012 Dec 2013 Dec 2014 Decisions Start-ups Investmentbacklog

June 2015

€ 2.8bn

€ 2.1bn

Yearly salesbacklog

after full ramp-ups

See definitions in appendix.

€ 2.7bn

€ 2.3bn

~ €0.9bn

H1 2015

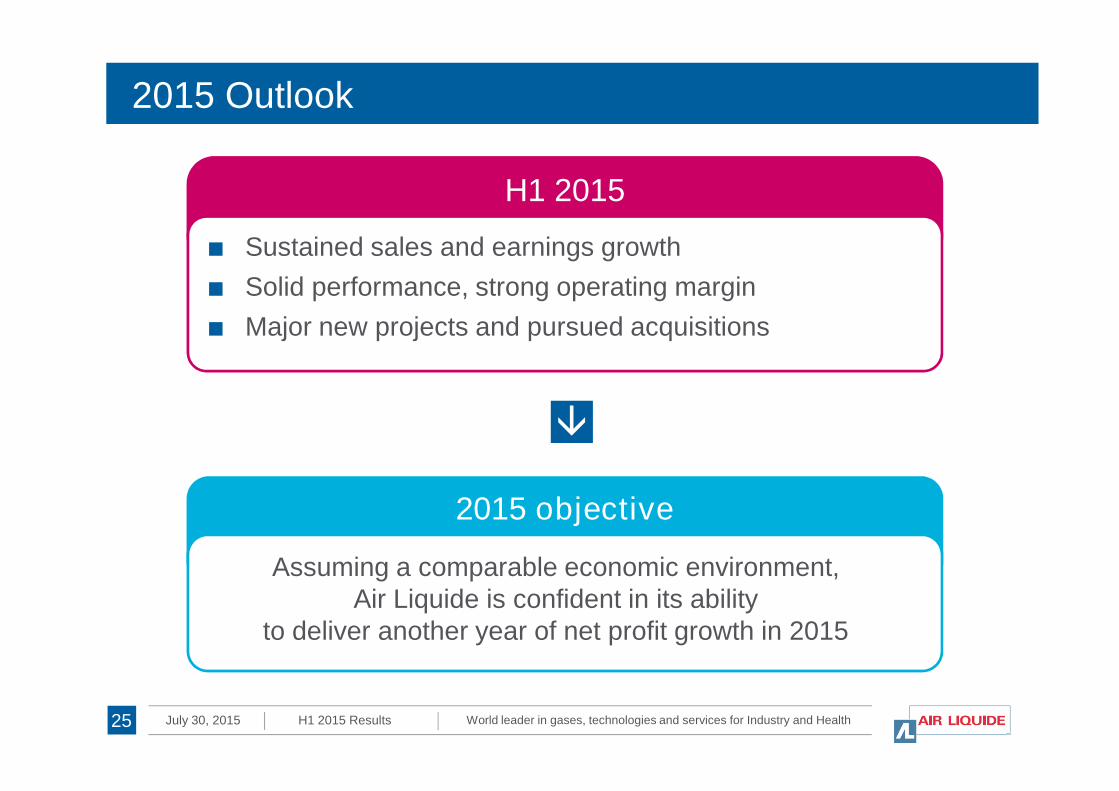

2015 Outlook

■ Sustained sales and earnings growth

■ Solid performance, strong operating margin

■ Major new projects and pursued acquisitions

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

2015 objective

25

Assuming a comparable economic environment,Air Liquide is confident in its ability

to deliver another year of net profit growth in 2015

AppendixH1 2015

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results27

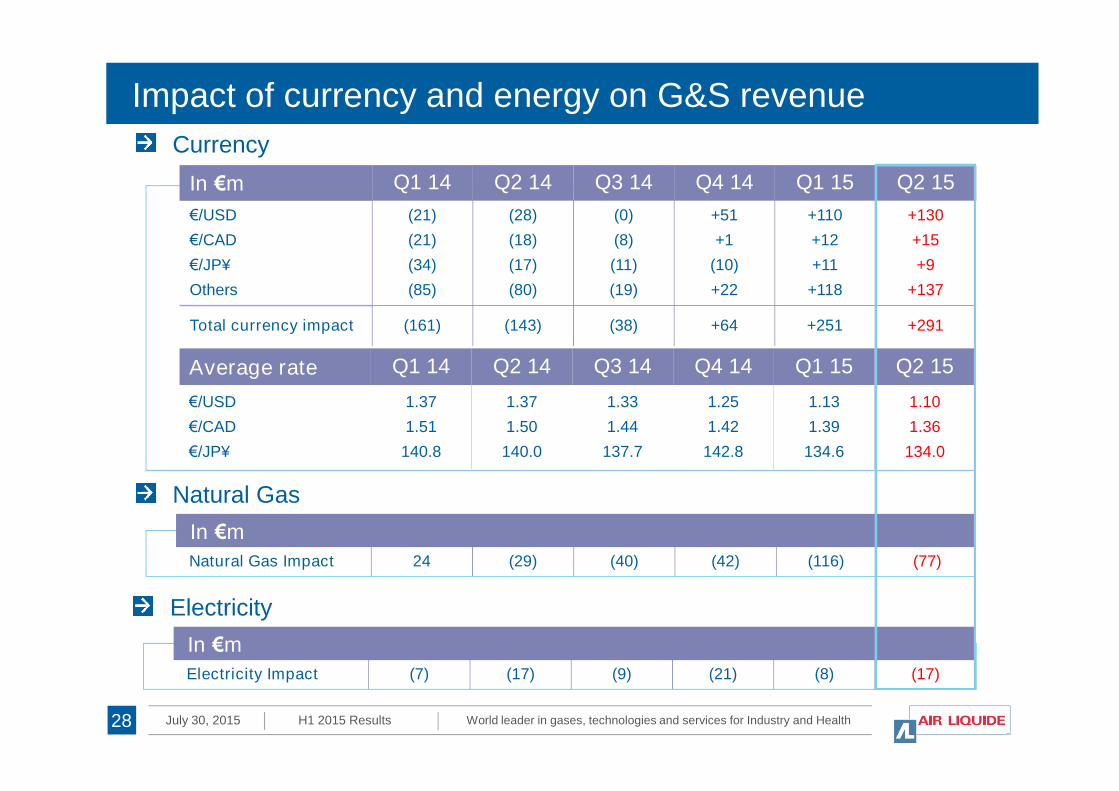

Impact of currency and energy on G&S revenue

In €m Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15

€/USD

€/CAD

€/JP¥

Others

(21)

(21)

(34)

(85)

(28)

(18)

(17)

(80)

(0)

(8)

(11)

(19)

+51

+1

(10)

+22

+110

+12

+11

+118

+130

+15

+9

+137

Total currency impact (161) (143) (38) +64 +251 +291

Average rate Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15

€/USD 1.37 1.37 1.33 1.25 1.13 1.10

Currency

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results28

Natural Gas Impact 24 (29) (40) (42) (116) (77)

In €m

€/USD

€/CAD

€/JP¥

1.37

1.51

140.8

1.37

1.50

140.0

1.33

1.44

137.7

1.25

1.42

142.8

1.13

1.39

134.6

1.10

1.36

134.0

Natural Gas

Electricity Impact (7) (17) (9) (21) (8) (17)

In €m

Electricity

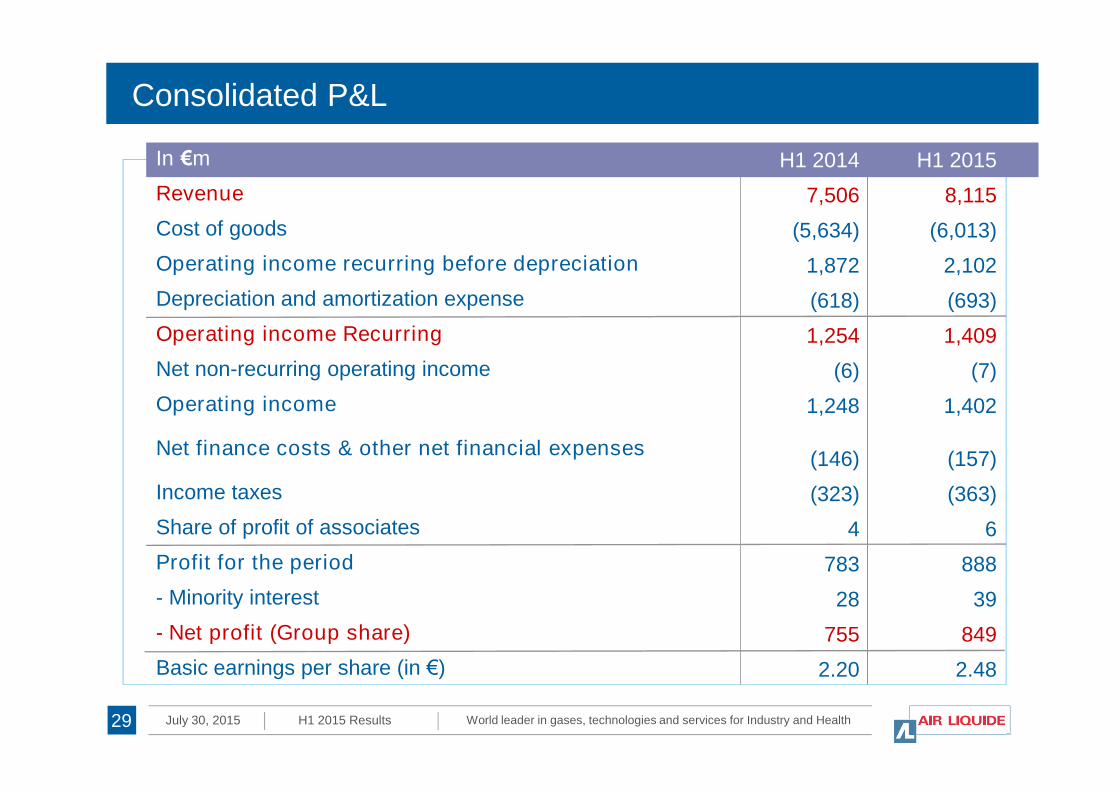

Consolidated P&L

In €m H1 2014 H1 2015

Revenue 7,506 8,115

Cost of goods (5,634) (6,013)

Operating income recurring before depreciation 1,872 2,102

Depreciation and amortization expense (618) (693)

Operating income Recurring 1,254 1,409

Net non-recurring operating income (6) (7)

Operating income 1,248 1,402

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

Operating income 1,248 1,402

Net finance costs & other net financial expenses(146) (157)

Income taxes (323) (363)

Share of profit of associates 4 6

Profit for the period 783 888

- Minority interest 28 39

- Net profit (Group share) 755 849

Basic earnings per share (in €) 2.20 2.48

29

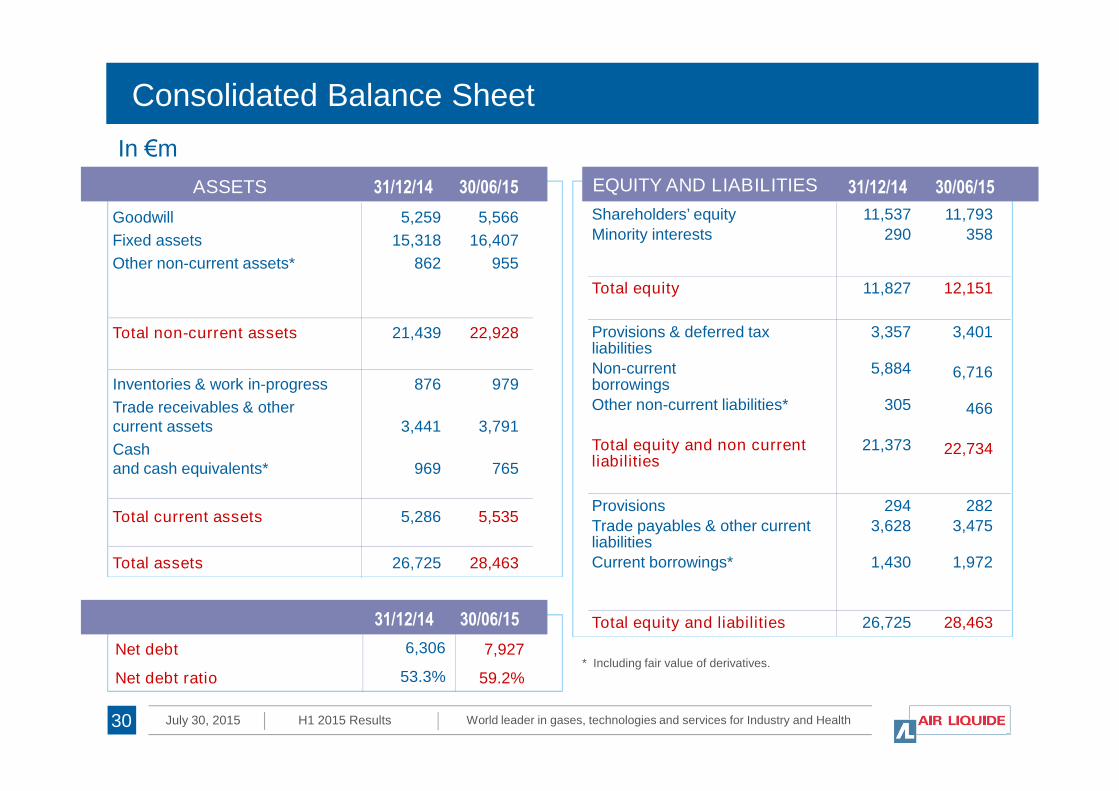

Consolidated Balance Sheet

ASSETS 31/12/14 30/06/15

Goodwill

Fixed assets

Other non-current assets*

5,259

15,318

862

5,566

16,407

955

Total non-current assets 21,439 22,928

Inventories & work in-progress 876 979

EQUITY AND LIABILITIES 31/12/14 30/06/15

Shareholders’ equity

Minority interests

11,537

290

11,793

358

Total equity 11,827 12,151

Provisions & deferred taxliabilities

Non-currentborrowings

3,357

5,884

3,401

6,716

In €m

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

Trade receivables & othercurrent assets

Cashand cash equivalents*

3,441

969

3,791

765

Total current assets 5,286 5,535

Total assets 26,725 28,463

Other non-current liabilities*

Total equity and non currentliabilities

305

21,373

466

22,734

Provisions

Trade payables & other currentliabilities

Current borrowings*

294

3,628

1,430

282

3,475

1,972

Total equity and liabilities 26,725 28,46331/12/14 30/06/15

Net debt 6,306 7,927

Net debt ratio 53.3% 59.2%

30

* Including fair value of derivatives.

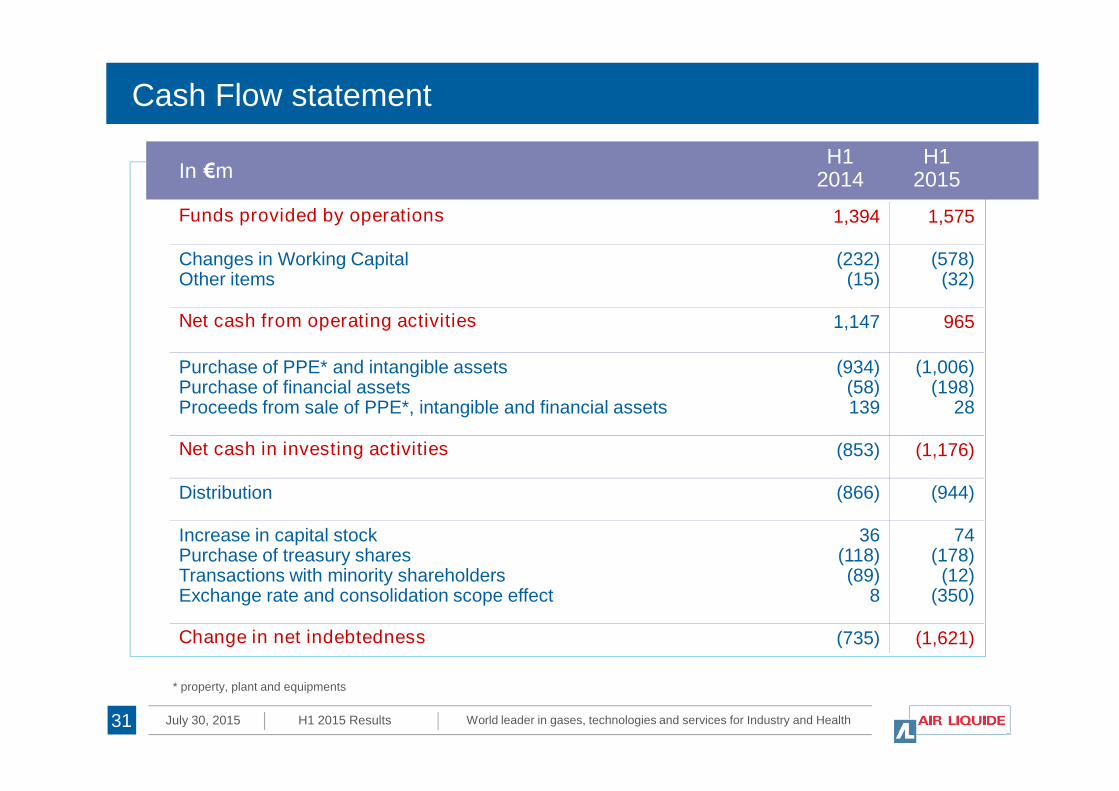

Cash Flow statement

In €mH1

2014H1

2015

Funds provided by operations 1,394 1,575

Changes in Working CapitalOther items

(232)(15)

(578)(32)

Net cash from operating activities 1,147 965

Purchase of PPE* and intangible assetsPurchase of financial assets

(934)(58)

(1,006)(198)

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

Purchase of financial assetsProceeds from sale of PPE*, intangible and financial assets

(58)139

(198)28

Net cash in investing activities (853) (1,176)

Distribution (866) (944)

Increase in capital stockPurchase of treasury sharesTransactions with minority shareholdersExchange rate and consolidation scope effect

36(118)(89)

8

74(178)(12)

(350)

Change in net indebtedness (735) (1,621)

* property, plant and equipments

31

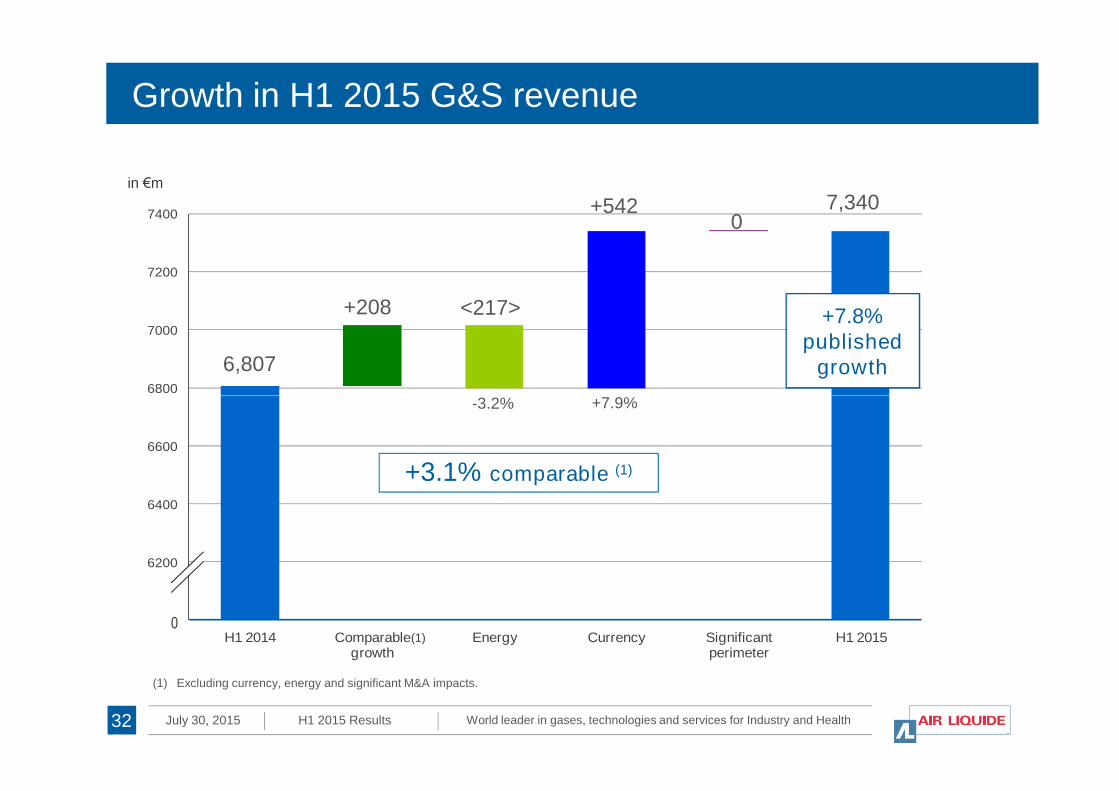

Growth in H1 2015 G&S revenue

6800

7000

7200

7400

in €m

<217>

0

+7.8%published

growth6,807

+208

7,340+542

-3.2% +7.9%

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

6000

6200

6400

6600

6800

H1 2014 Comparablegrowth

Energy Currency Significantperimeter

H1 20150

32

+3.1% comparable (1)

(1) Excluding currency, energy and significant M&A impacts.

-3.2% +7.9%

(1)

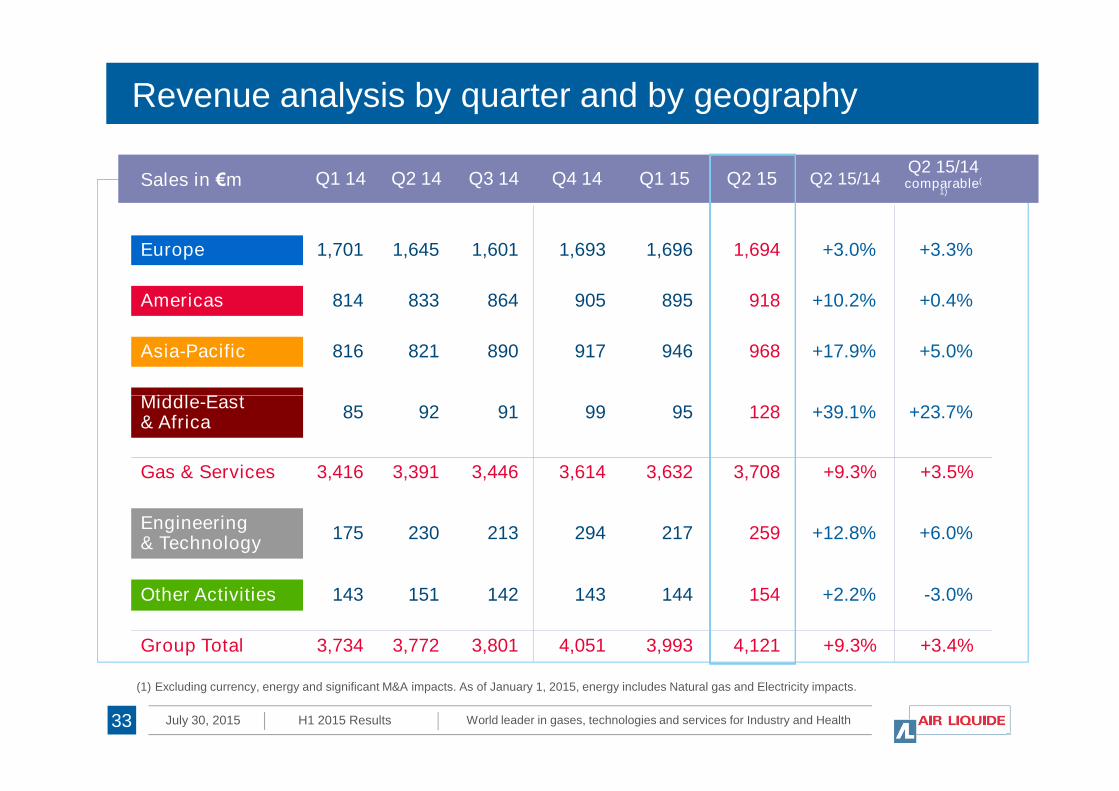

Revenue analysis by quarter and by geography

Sales in €m Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q2 15/14Q2 15/14comparable(

1)

Europe 1,701 1,645 1,601 1,693 1,696 1,694 +3.0% +3.3%

Americas 814 833 864 905 895 918 +10.2% +0.4%

Asia-Pacific 816 821 890 917 946 968 +17.9% +5.0%

Middle-East

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results33

Middle-East& Africa

85 92 91 99 95 128 +39.1% +23.7%

Gas & Services 3,416 3,391 3,446 3,614 3,632 3,708 +9.3% +3.5%

Engineering& Technology

175 230 213 294 217 259 +12.8% +6.0%

Other Activities 143 151 142 143 144 154 +2.2% -3.0%

Group Total 3,734 3,772 3,801 4,051 3,993 4,121 +9.3% +3.4%

(1) Excluding currency, energy and significant M&A impacts. As of January 1, 2015, energy includes Natural gas and Electricity impacts.

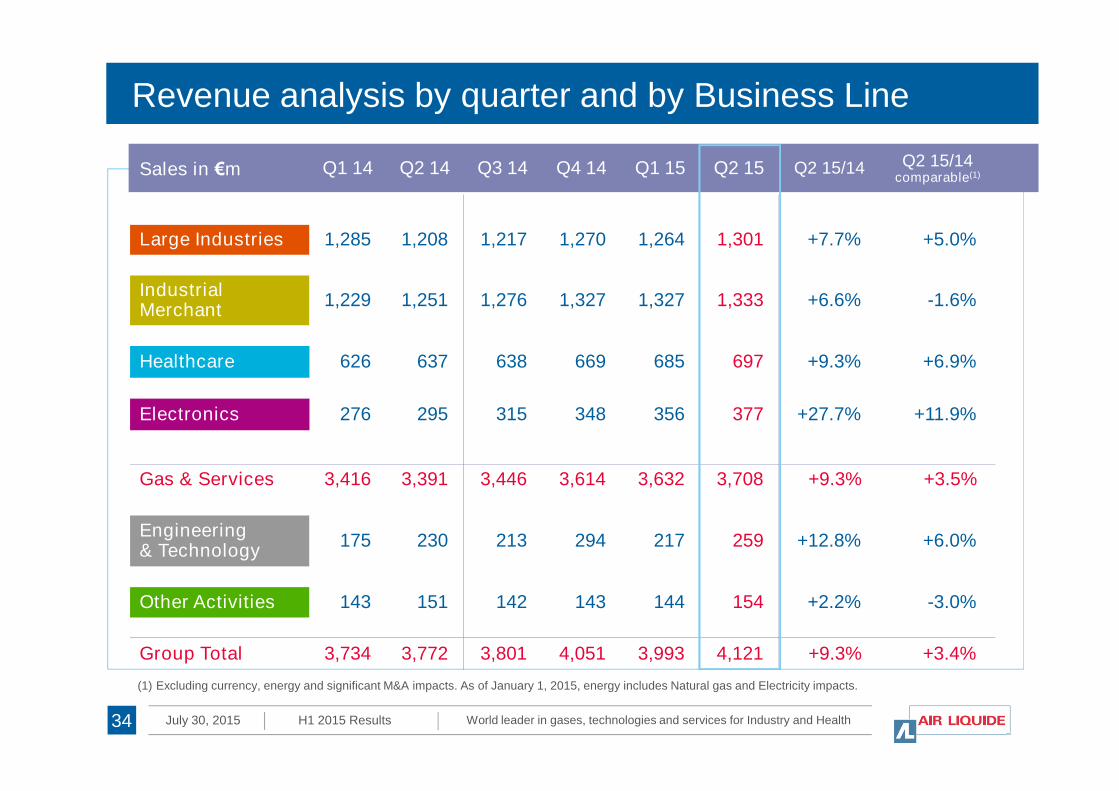

Revenue analysis by quarter and by Business Line

Sales in €m Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q2 15/14 Q2 15/14comparable(1)

Large Industries 1,285 1,208 1,217 1,270 1,264 1,301 +7.7% +5.0%

IndustrialMerchant

1,229 1,251 1,276 1,327 1,327 1,333 +6.6% -1.6%

Healthcare 626 637 638 669 685 697 +9.3% +6.9%

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results34

Electronics 276 295 315 348 356 377 +27.7% +11.9%

Gas & Services 3,416 3,391 3,446 3,614 3,632 3,708 +9.3% +3.5%

Engineering& Technology

175 230 213 294 217 259 +12.8% +6.0%

Other Activities 143 151 142 143 144 154 +2.2% -3.0%

Group Total 3,734 3,772 3,801 4,051 3,993 4,121 +9.3% +3.4%

(1) Excluding currency, energy and significant M&A impacts. As of January 1, 2015, energy includes Natural gas and Electricity impacts.

G&S Revenue growth by quarter and by impact

Growth aspublished

NaturalGas

Electricity Currency Significantperimeter

Comparablegrowth(1)

Q3 2013 - 1.3% - 0.6% - 5.8% + 1.2% + 3.9%

Q4 2013 - 2.1 % - 1.0% - 5.2% - 0.4% + 4.4%

Q1 2014 + 0.3% + 0.7% - 4.7% - 1.4% + 5.7%

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results35

Q2 2014 - 2.5% - 0.8% - 4.1% - 1.3% + 3.7%

Q3 2014 + 0.1% - 1.2% - 1.1% - 1.3% + 3.6%

Q4 2014 + 3.0% - 1.2% + 1.8% - 0.9% + 3.3%

Q1 2015 + 6.3% - 3.4% - 0.2% + 7.3% 0,0% + 2.6%

Q2 2015 + 9.3% - 2.2% - 0.5% + 8.5% 0,0% + 3.5%

(1) Excluding currency, energy and significant M&A impacts. As of January 1, 2015, the energy impact includes electricity impact in addition to the natural gas effect.

H1 2015 Revenue breakdown by region

Americas: € 1.8 bn Asia: € 1.9 bnEurope: € 3.4 bn

Middle-East and Africa

AmericasEurope

Asia

Gas & ServicesH1 2015 Revenue: € 7,340 m

3%

26%

25%

46%

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

24%

33%

4%

39%

Americas: € 1.8 bn Asia: € 1.9 bnEurope: € 3.4 bn

32%

34%31%

3%

36

35%

10%

45%

10%

Large Industries ElectronicsHealthcareIndustrial Merchant

31%

34%

32%

3%

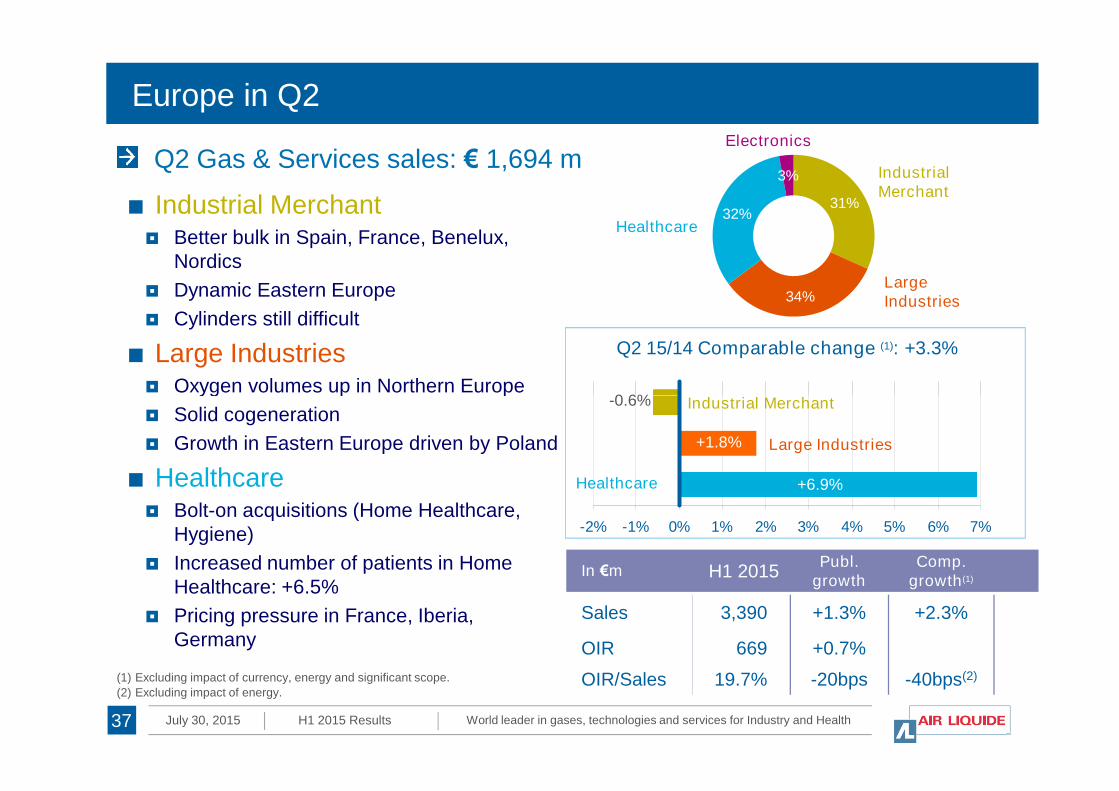

Europe in Q2

Q2 Gas & Services sales: € 1,694 m

Q2 15/14 Comparable change (1): +3.3%

■ Industrial Merchant Better bulk in Spain, France, Benelux,

Nordics

Dynamic Eastern Europe

Cylinders still difficult

■ Large Industries Oxygen volumes up in Northern Europe

IndustrialMerchant

Electronics

LargeIndustries

Healthcare

Industrial Merchant-0.6%

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

-2% -1% 0% 1% 2% 3% 4% 5% 6% 7%

Oxygen volumes up in Northern Europe

Solid cogeneration

Growth in Eastern Europe driven by Poland

■ Healthcare Bolt-on acquisitions (Home Healthcare,

Hygiene)

Increased number of patients in HomeHealthcare: +6.5%

Pricing pressure in France, Iberia,Germany

In €m H1 2015Publ.

growthComp.

growth(1)

Sales 3,390 +1.3% +2.3%

OIR 669 +0.7%

OIR/Sales 19.7% -20bps -40bps(2)

Industrial Merchant

Large Industries

-0.6%

+1.8%

Healthcare +6.9%

37

(1) Excluding impact of currency, energy and significant scope.

(2) Excluding impact of energy.

45%

35%

10%

10%

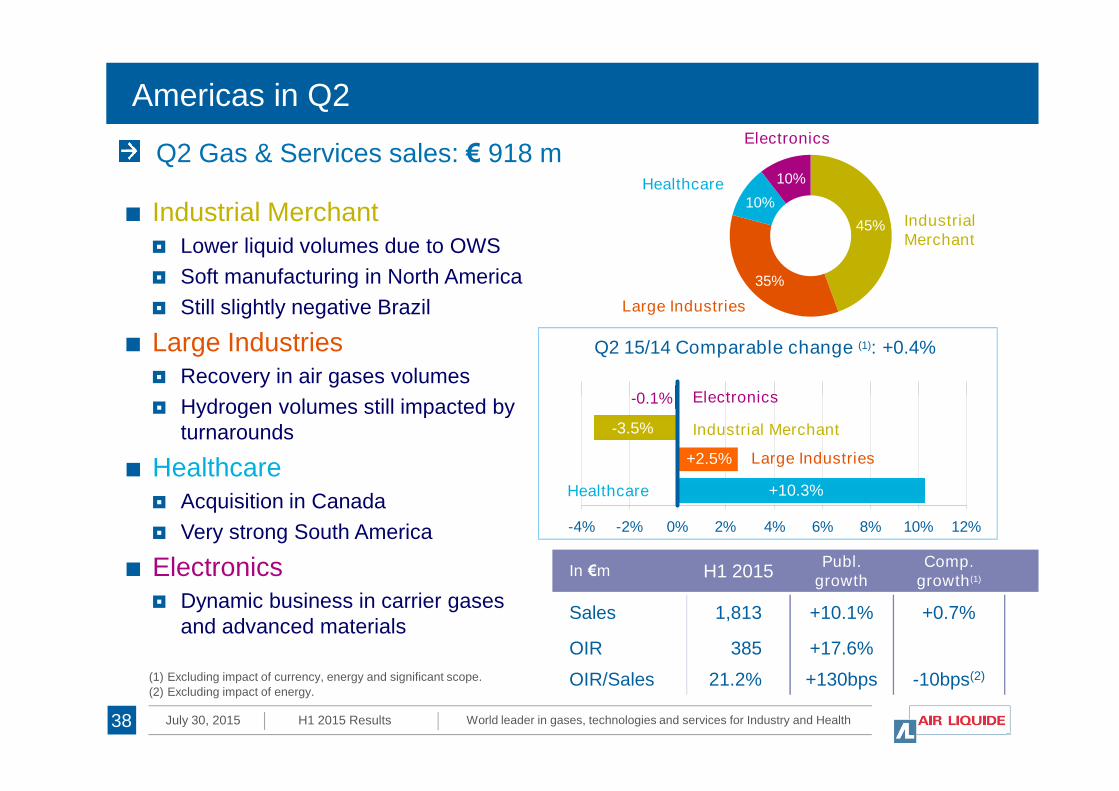

■ Industrial Merchant Lower liquid volumes due to OWS

Soft manufacturing in North America

Still slightly negative Brazil

■ Large Industries Recovery in air gases volumes

Hydrogen volumes still impacted by

Americas in Q2

Q2 Gas & Services sales: € 918 m

Q2 15/14 Comparable change (1): +0.4%

Electronics

Large Industries

Healthcare

Electronics

-0.1%

IndustrialMerchant

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

-4% -2% 0% 2% 4% 6% 8% 10% 12%

Hydrogen volumes still impacted byturnarounds

■ Healthcare Acquisition in Canada

Very strong South America

■ Electronics Dynamic business in carrier gases

and advanced materials

Industrial Merchant

Large Industries+2.5%

Electronics

Healthcare

In €m H1 2015Publ.

growthComp.

growth(1)

Sales 1,813 +10.1% +0.7%

OIR 385 +17.6%

OIR/Sales 21.2% +130bps -10bps(2)

38

+10.3%

-3.5%

-0.1%

(1) Excluding impact of currency, energy and significant scope.

(2) Excluding impact of energy.

33%

39%

4%

24%

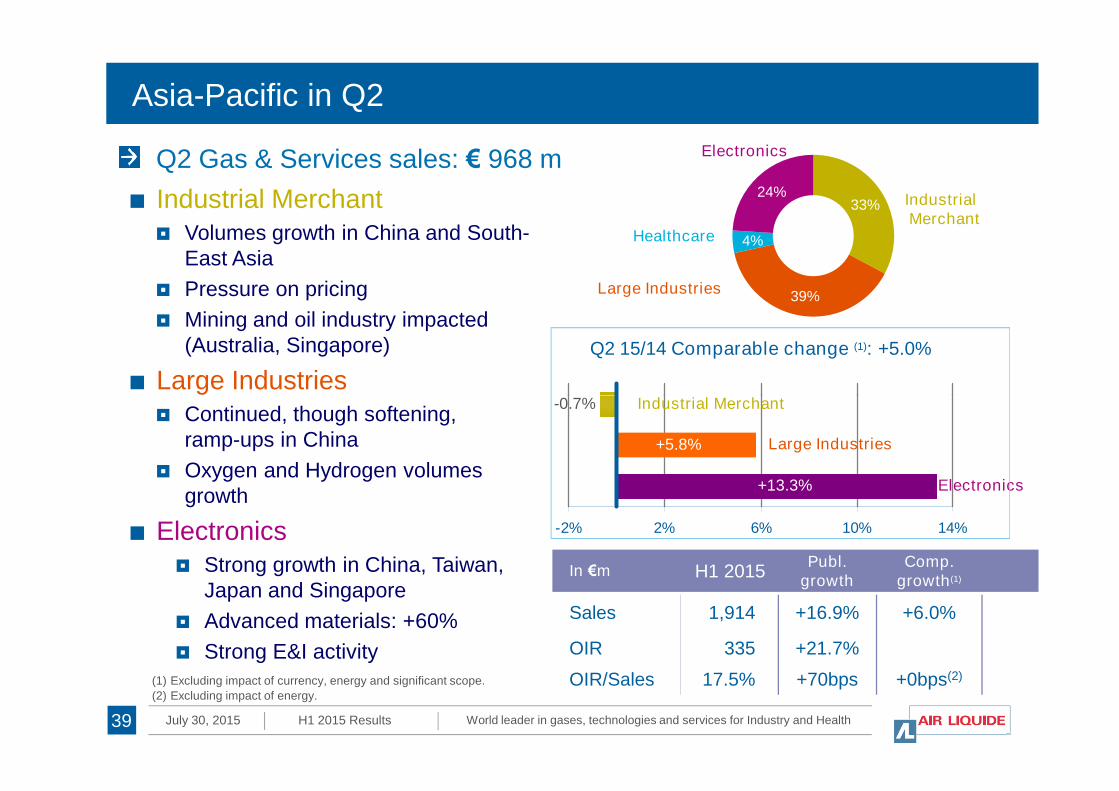

Asia-Pacific in Q2

Industrial Merchant-0.7%

Q2 Gas & Services sales: € 968 m

Q2 15/14 Comparable change (1): +5.0%

■ Industrial Merchant Volumes growth in China and South-

East Asia

Pressure on pricing

Mining and oil industry impacted(Australia, Singapore)

■ Large Industries

IndustrialMerchant

Large Industries

Healthcare

Electronics

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

-2% 2% 6% 10% 14%

Industrial Merchant

Large Industries

Electronics

-0.7%

+5.8%

+13.3%

■ Continued, though softening,

ramp-ups in China

Oxygen and Hydrogen volumesgrowth

■ Electronics Strong growth in China, Taiwan,

Japan and Singapore

Advanced materials: +60%

Strong E&I activity

In €m H1 2015Publ.

growthComp.

growth(1)

Sales 1,914 +16.9% +6.0%

OIR 335 +21.7%

OIR/Sales 17.5% +70bps +0bps(2)

39

(1) Excluding impact of currency, energy and significant scope.

(2) Excluding impact of energy.

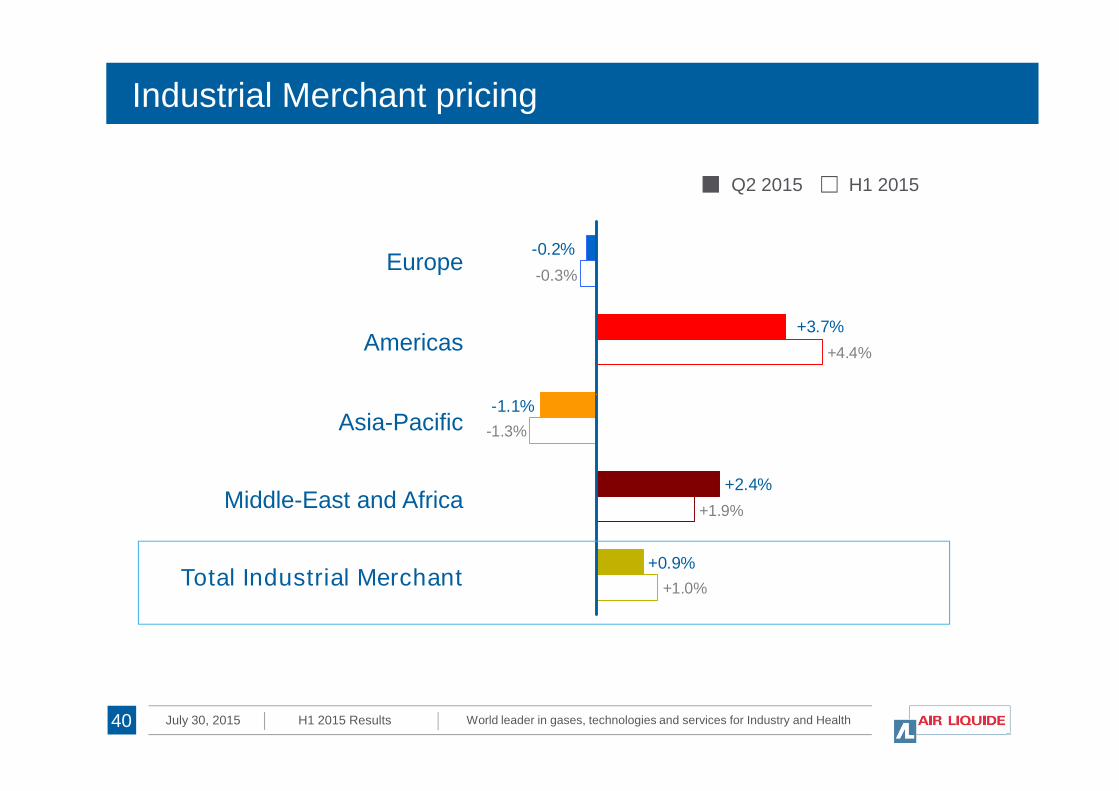

Industrial Merchant pricing

+4.4%

-0.2%

+3.7%

Europe

Americas

Q2 2015 H1 2015

-0.3%

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

+1.0%

+1.9%

-1.3%

-1.1%

+2.4%

+0.9%

Asia-Pacific

Middle-East and Africa

Total Industrial Merchant

40

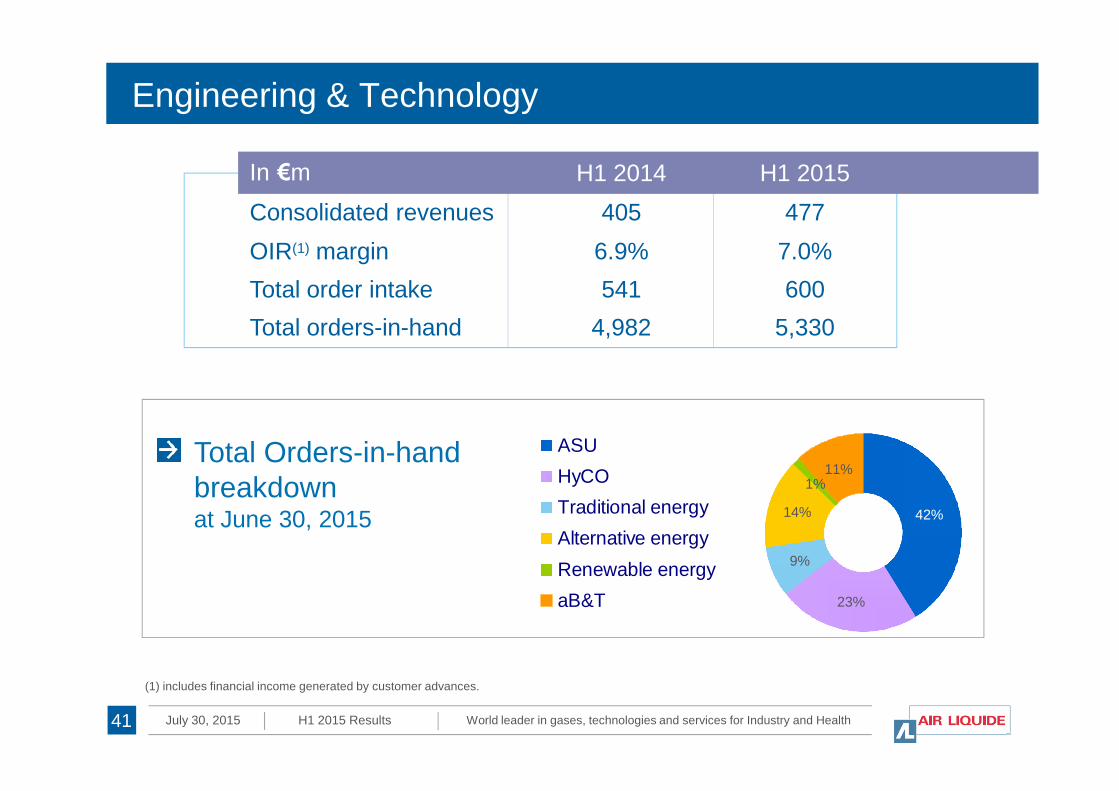

Engineering & Technology

In €m H1 2014 H1 2015

Consolidated revenues 405 477

OIR(1) margin 6.9% 7.0%

Total order intake 541 600

Total orders-in-hand 4,982 5,330

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

23%

9%

14%

1%11%

42%

ASU

HyCO

Traditional energy

Alternative energy

Renewable energy

aB&T

Total Orders-in-handbreakdownat June 30, 2015

(1) includes financial income generated by customer advances.

41

Operating margin – energy effect

Group, in €m H1 2014 H1 2015

Revenue 7,506 8,115

Incl. energy (217)

Operating income recurring 1,254 1,409

Operating margin 16.7% 17.4%

Operating margin excluding energy 16.8%

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

Gas and services, in €m H1 2014 H1 2015

Revenue 6,807 7,340

Incl. energy effect (217)

Operating income recurring 1,294 1,432

Operating margin 19.0% 19.5%

Operating margin excluding energy 18.9%

42

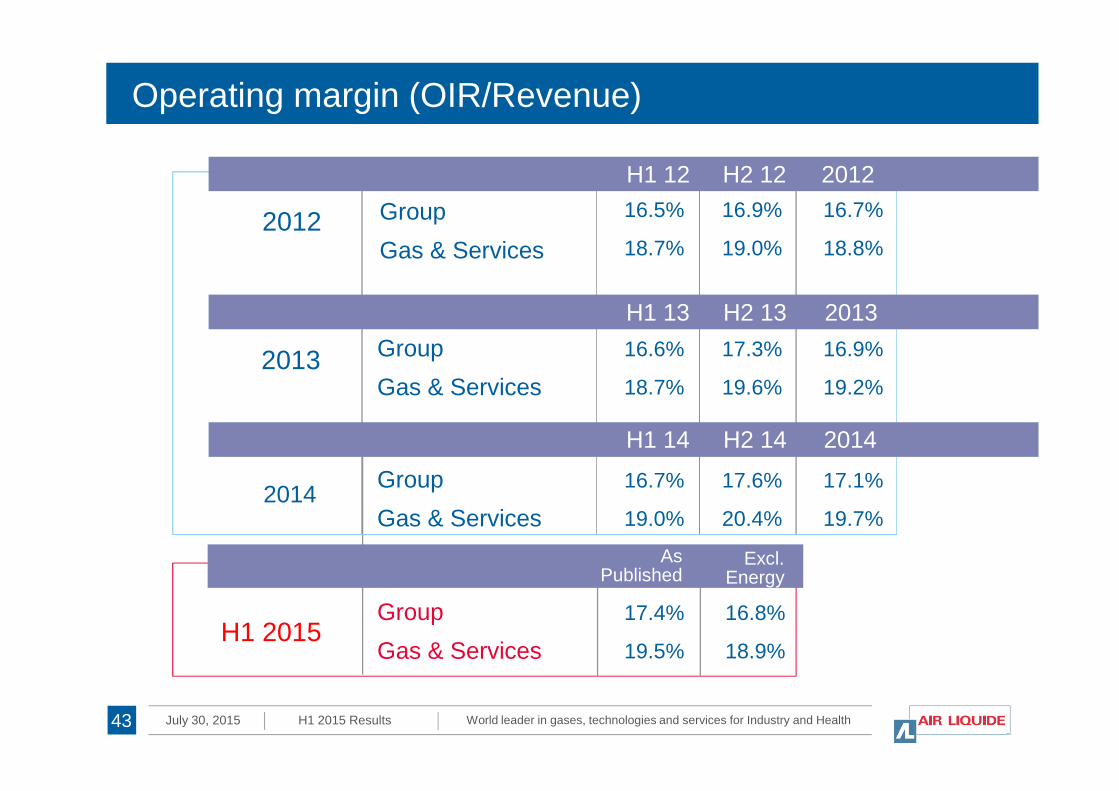

Operating margin (OIR/Revenue)

Group

Gas & Services2012

H1 12 H2 12 2012

16.5%

18.7%

16.7%

18.8%

16.9%

19.0%

Group

Gas & Services

16.6%

18.7%

H1 13 H2 13 2013

17.3%

19.6%

16.9%

19.2%2013

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

Group

Gas & Services

16.7%

19.0%

H1 14 H2 14 2014

17.6%

20.4%

17.1%

19.7%2014

43

Gas & Services 18.7% 19.6% 19.2%

Group

Gas & Services

17.4%

19.5%

Excl.Energy

16.8%

18.9%H1 2015

AsPublished

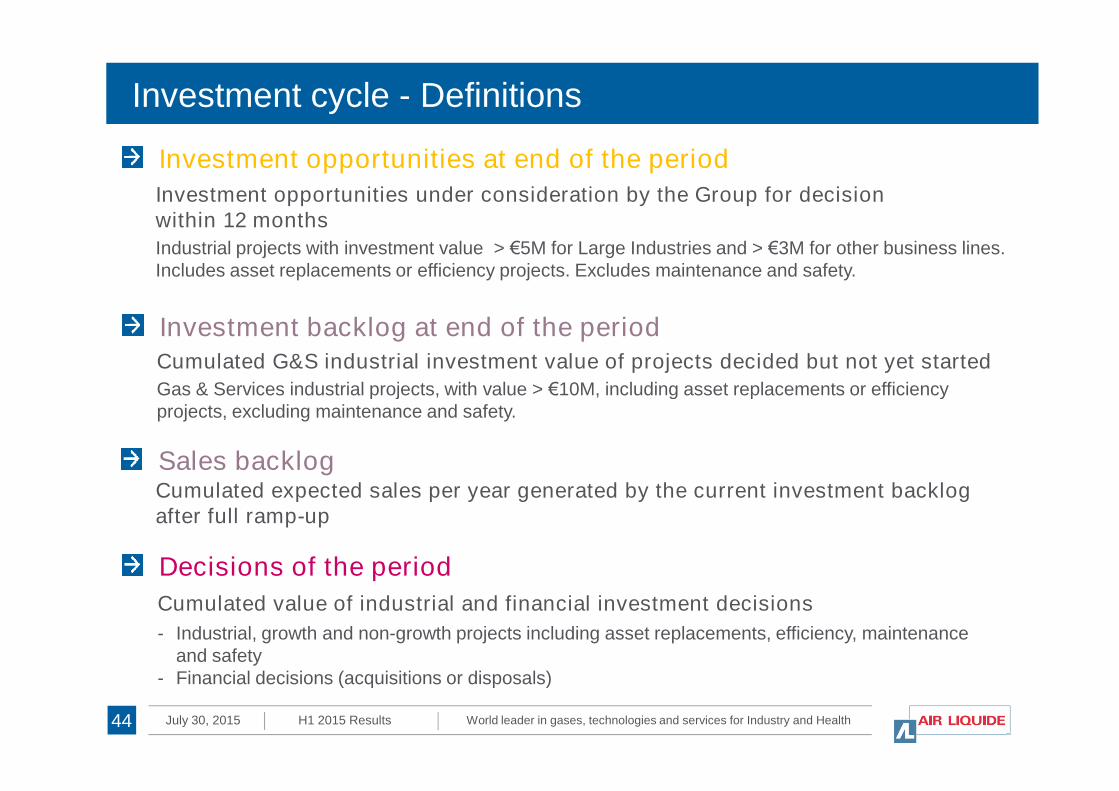

Investment cycle - Definitions

Investment backlog at end of the periodCumulated G&S industrial investment value of projects decided but not yet started

Gas & Services industrial projects, with value > €10M, including asset replacements or efficiency

Investment opportunities at end of the period

Investment opportunities under consideration by the Group for decisionwithin 12 months

Industrial projects with investment value > €5M for Large Industries and > €3M for other business lines.Includes asset replacements or efficiency projects. Excludes maintenance and safety.

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results44

Decisions of the period

Cumulated value of industrial and financial investment decisions

Gas & Services industrial projects, with value > €10M, including asset replacements or efficiencyprojects, excluding maintenance and safety.

- Industrial, growth and non-growth projects including asset replacements, efficiency, maintenanceand safety

- Financial decisions (acquisitions or disposals)

Sales backlogCumulated expected sales per year generated by the current investment backlogafter full ramp-up

5%

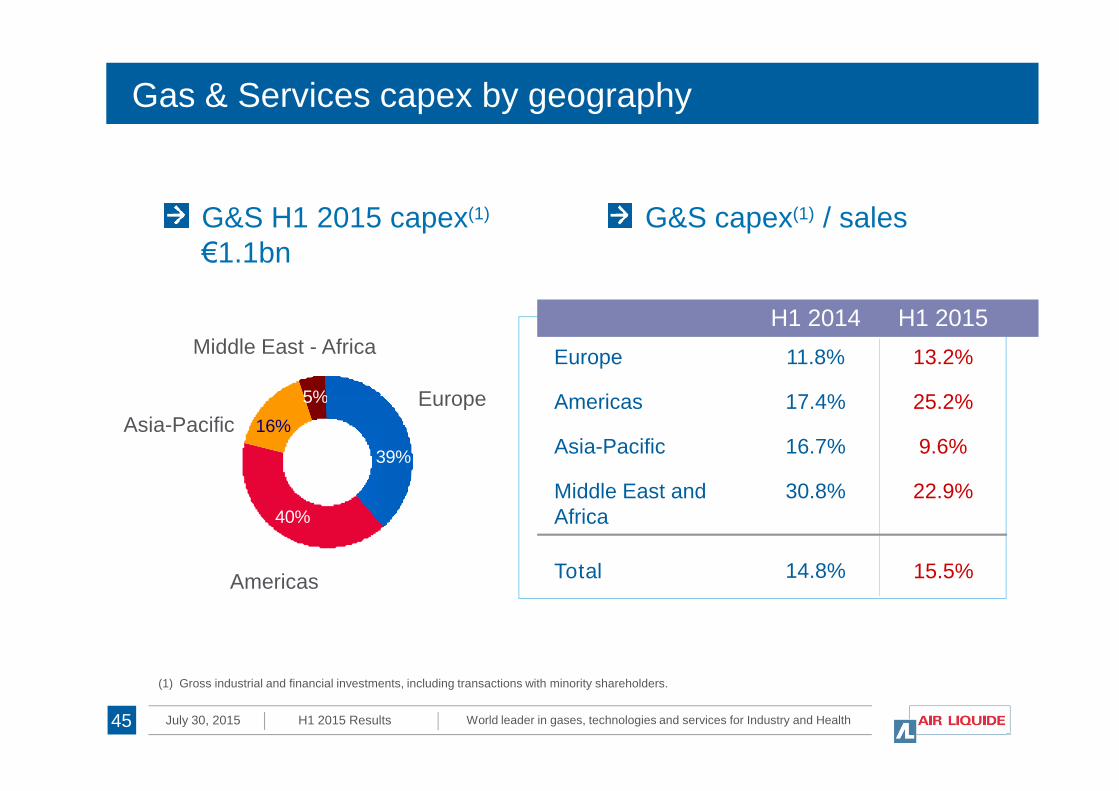

Gas & Services capex by geography

H1 2014 H1 2015

Europe

Americas

11.8%

17.4%

13.2%

25.2%Europe

Middle East - Africa

G&S capex(1) / salesG&S H1 2015 capex(1)

€1.1bn

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

39%

40%

16%

5% Americas

Asia-Pacific

Middle East andAfrica

17.4%

16.7%

30.8%

25.2%

9.6%

22.9%

Total 14.8% 15.5%

Europe

Americas

Asia-Pacific

(1) Gross industrial and financial investments, including transactions with minority shareholders.

45

Financing structure

Bankdebt

Others(1)

Commercialpaper

70%

At 30 June 2015

Fixed rate

6000

7000

8000

9000

1%15%

Fixed/variablerates

Sources MaturityIn €m

> July 1st,2020

Marketdebt:82%

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

Bonds

Privateplacements

paper

30%

Variable rate

0

1000

2000

3000

4000

5000

6000

48%14%

22%

From July 1st

2016 toJune, 30th

2020

< June, 30th

2016

(1) Others: Finance leases and put options granted to minority shareholders.

46

(2) Les billets de trésorerie sont reclassés aux échéances des lignes de crédit qui les garantissent.

Regular and sustained performance

0

2 500

5 000

7 500

10 000

12 500

15 000

19841986198819901992199419961998200020022004200620082010201220140

1

2

3

4

5

6

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Revenue (in €m)

+5.6% CAGR over 30 years(2)

EPS (1) (in €)

+7.7% CAGR over 30 years(2)

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results47

0

500

1 000

1 500

2 000

2 500

3 000

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 20140.00

0.50

1.00

1.50

2.00

2.50

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Cashflow (in €m)

+6.9% CAGR over 30 years(2)

Dividend (1) (in € per share)

+9.3% CAGR over 30 years(2)

(1) Adjusted for the 2-for-1 share spilt in 2007 and free share attributions. (2) Calculated according to prevailing accounting rules over 30 years.

For further information, please contact:

Investor Relations

Aude Rodriguez + 33 (0)1 40 62 57 08

Louis Laffont + 33 (0)1 40 62 57 18

Jérôme Zaman + 33 (0)1 40 62 59 38

Communications

Anne Bardot + 33 (0)1 40 62 50 93

Annie Fournier + 33 (0)1 40 62 51 31

www.airliquide.com Follow us on Twitter @AirLiquideGroup

World leader in gases, technologies and services for Industry and HealthJuly 30, 2015 H1 2015 Results

L’Air Liquide S.A.

Corporation for the study and application of processes developed by

Georges Claude with registered capital of 1,897,386,986.00 euros

Corporate headquarters:

75, Quai d’Orsay

75321 Paris Cedex 07

Tel : +33 (0)1 40 62 55 55

RCS Paris 552 096 281

48