swoogo.s3.amazonaws.com · slide 1 getting past the bs of marketing productivity measurement ......

TRANSCRIPT

Slide 1

Getting Past the BS of Marketing Productivity MeasurementThe future as suggested by the 60 CMO & marketing leaders of the MMA Boards (and an investment of $3 million)

Mobile Marketing Assoc.Greg Stuart

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 2 “The world is not just changing, it is being reshaped, and is starting to operate differently, in many realms, all at once.”

Thank you for Being Late – Thomas Friedman

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 3

1. Started to solve a problem for mobile… What is the real, proven ROI of Mobile?

2. …Led the board to discover real problem…and that there is huge opportunity for a complete rethink of marketing productivity measurement

3. …and that MTA is the solution (and the curse)Problem is that MTA is early

4. Finally, what we know now in MTA and what we are doing about it

Our Agenda For Today

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 4 First: MMA is Industry Trade Assoc. for Mobile Marketing

Started in 2003; turned around in 2013

Marketer led; plus media sellers, tech and agencies

800+ members worldwide

50+ staff worldwide

Operating in 12 countries

20+ events in 15 countries

MMAAPAC

MMAEMEA

MMALATAM

MMANo. Amer.

4

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 5 Governance: MMA Global Board of Directors

Sanjay GuptaChairCMO

Tim MahoneyExec Comm at Large

CMO

Carolyn EversonGlobal Secretary

VP, Global Mktg Solutions

Luis Di ComoExec Comm at Large

SVP, Global Media

Jack PhilbinExec Comm at Large

Co-Founder & CEO

Greg StuartMMA

CEO Mobile Marketing Association

John CostelloGlobal Chair Emeritus

Former Pres., Global Mktg & Innovation

Stephen McCarthyGlobal Treasurer

CFO(xAd)

Susan CanavariChief Brand Officer

Ilonka LavizGlobal Digital Mktg

Dir., Global eBusiness

Peter McGuinness

Chief Mktg & Brand Officer

Marc MathieuCMO

Karin TimponeGlobal Mktg Officer

Allan ThygesenPresident, Americas

Jeff LucasCRO

Matt DerellaGlobal CRO

Peter HamiltonCEO

John TrimbleCRO

David GodsmanCDO

Suzy DeeringCMO

Rebecca MessinaCMO

Ayesha GilardeCMO

Wanda YoungCMO

Tony RogersCMO

Michael DonnellyNA Regional Rep

SVP, Global Digital Marketing

Louis PaskalisNA Regional Rep.SVP Enterprise Media

Executive Bank Of America

Ernesto EcheverriLATAM Regional Rep

Dir. Mktg USA, Canada & Caribbean

Alberto ‘Banano’ PardoLATAM Regional Rep

Founder & CEO

David LowesEMEA Regional Rep

CMO

Cameron ClaytonCEO & General

Manager

David PorterAPAC Regional Rep

VP, Global Media

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 6 Governance: MMA North America Board of Directors

Kristi ArgyilanAt Large

SVP,Marketing

Target

6

Louis PaskalisChair

SVP, Enterprise Media Executive, Bank of

America

Amit ShahCMO

1-800-Flowers.comGreg Stuart

MMACEO Mobile Marketing

Association

Jack PhilbinChair Emeritus

Co-Founder & CEO, Vibes

Michael DonnellyChair Emeritus

SVP, Digital Experiences Group

MasterCard

Jay AltschulerVP, Media VP,

MediaSamsung

Kim GnattGlobal Group Director

Digital MarketingThe Coca-Cola Company

Josh WetzelSr. Director

Sales & MarketingeBay

Todd PollakManaging Director

US Product Specialist Team

Gail TiffordVP

Media & Digital Engagement

Unilever

Dave SanabriaConnected Consumer

Experiences Ford

Danielle LeeGlobal Head

of Partner SolutionsSpotify

Brad FeinbergSenior Director Media & Digital

MillerCoors

Elizabeth Herbst-BradyHead of NY Ad

SalesSnap Inc.

Tatyana ZlotskyVice President

Digital AcquisitionAmerican Express

OPEN

Theresa AgnewCMO

North AmericaGlaxoSmithKlin

Carrie (Himelfarb) Seifer

VP, CRO, IBM Watson Advertising(The Weather Company)

Ran Ben-YairCEO & Co-Founder

Ubimo

Jay EmmetGM

Open MarketNorth America

Duncan McCall CEO & Co-Founder

PlaceIQ

Steven RosenblattPresident

Foursquare

Jon Suarez-DavisChief Strategy OfficerSalesforce Marketing

Cloud

Rohit TripathiGM

SAP Mobile Services

SAP

Joe PruszHead of Global Sales

Rubicon Partners

Şekip Can GökalpEVP, Exchange

AdColony

Norman DeGreve CMOCVS

Mike RomoffHead of Global

Agency and Channel Sales,

Mark WrightVP Media Services & Sponsorships,

AT&T

Marissa TarletonCMO, RetailMeNot

JP MaheuVP, Twitter

Client Solutions, Americas

Pamela MoyVP of Marketing

Allstate

James KrecklerSVP Digital Media

NBCU

Carla Hassan EVP, Global CMO

Toys R Us

Kristen D’Arcy, Head of

Performance Digital MarketingAmerican Eagle

Amit ShahAt Large

CMO1-800-Flowers.com

Jack PhilbinChair Emeritus

Co-Founder & CEO, Vibes

Michael DonnellyChair Emeritus

SVP, Digital Experiences Group

MasterCard

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

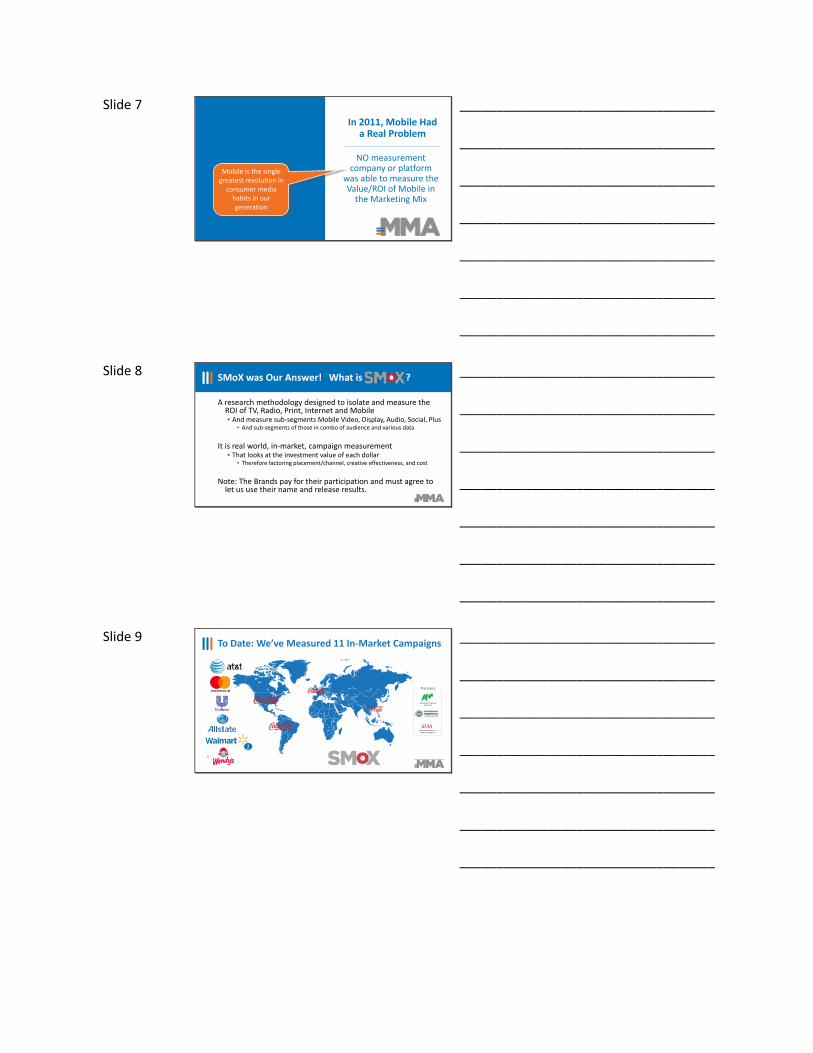

Slide 7 In 2011, Mobile Had

a Real Problem

NO measurement company or platform

was able to measure the Value/ROI of Mobile in

the Marketing Mix

7

Mobile is the single greatest revolution in

consumer media habits in our generation

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 8 SMoX was Our Answer! What is ?

A research methodology designed to isolate and measure the ROI of TV, Radio, Print, Internet and Mobile• And measure sub-segments Mobile Video, Display, Audio, Social, Plus

• And sub-segments of those in combo of audience and various data

It is real world, in-market, campaign measurement• That looks at the investment value of each dollar

• Therefore factoring placement/channel, creative effectiveness, and cost

Note: The Brands pay for their participation and must agree to let us use their name and release results.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 9 To Date: We’ve Measured 11 In-Market Campaigns

9

Association of National Advertisers

American Association of Advertising Agencies

Partners

2

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 10

TV

Internet

FSI

Cinema

Social

Radio

OOH

Mobile DisplayDisplay, video,social

Display, video, native,

location

Display,audio, video social

Display,video, social

Display, video, social

Display, video, social

Display, RM,

Weather targeting,

social, video

Display, Video,

behavioral, retargeting,location,

contextual

Display, Video,

RM, socialContextual, location, daypart10

2014 2015 2015 2015 2016 2016 2016 2016 2017 2017

Each Campaign Measured a Variety of Media Mixes

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 11 Mobile has expanded and become more granular

11

Static Display

300x50300x250

StaticDisplay, Video,Mobile social

Static display,video, Mobile social

Static display,video, Mobile social

Static display,video, Mobile social

Static Display,Audio, Mobile Video

Mobile Social

Static Display, Video, Mobile native,

Location (proximity and HLA)

Static Display 300x50

300x250, Rich Media,

Video Mobilesocial,

Weather targeting, Past user targeting

Static Display, Video, :15 :30, Audio,

:15, :30 Pre-roll,

in banner/ auto play, in

banner/ opt-in,

Contextual targeting

Behavioral, Retargeting,

location(proximity, audience)

Static Display, 300x50

300x250InterstitialRich Media

Video, MobileSocial

Contextual, daypart,Location

proximity, conquesting, historic segments

commuters, coupon

users

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 12

Offline Sales DataFrom customer

Repository of Person Level Data, with PII

information for automated matching

Anonymized and integrated data at the individual level

across all data sources

Complete Dataset to Marketing Evolution

for analytics

Media ExposureAd Agency/Trading Desk/ DSP

Survey Sample Attitudinal metrics &

Psychographics

$ $ $ $

*Alternate processes are available ig LiveRamp is not an option for the customer specific situation.

SMoX: Brings together Audience Viewing Data, with Survey based Brand Attitudes and Sales Data at the USER LEVEL

12

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 13

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0 2 4 6 8 10 12

Poin

t Inc

reas

e in

Sho

ppin

g In

tent

Frequency of Exposure

Broadcast

Cable

Digital Display

Social Media

Mobile Social

Mobile Location

Mobile Native

Target: Moms 18-49, with BTS Shopping IntentSource: Walmart BTS Survey; Data Collected from: 7/18 – 9/8

Basically, What SMoX Provides are ROI Performance Curves by MediumBroadcast, Cable and Digital are all far from saturation, indicating that further campaign spend across channels will continue to drive Intent.

Frequency to Lift ResponseIntent to Shop Walmart for BTS Grocery

Average Media Frequency to Date

Display

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 14 Which is able to produce Optimal Budget Allocation: In this case to drive “Intent to Shop” Brand for Walmart

In an optimal allocation of media dollars, 9% is allocated to Mobile – primarily shifting budget from FSI and Cable TV.

9%

19%

38%

40%

21%

14%24%

6%

12%6%

7%

2014 Full Campaign Optimized

2014 Full Campaign Budget

3%

Broadcast TVCable TV

DigitalMobile

FSI

Social Media

Target: Moms 18-49, with BTS Shopping IntentSource: Walmart BTS Survey; Data Collected from: 7/18 – 9/8Media Mix: Max 2x planned spend, Min ½ planned Spend

People Impacted: 6.2MM+17.3% of the

W18-49 Population

People Impacted: 10.2MM+28.5% of the

W18-49 Population

+64%

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 15 Overall, SMoX Patterns in Optimized Marketing Mixes suggest that Mobile should be 15%-20% of Total Media

15

1%5% 4% 6% 5%

12% 11%16%

26%

20%

15%12%

15% 15%19%

17% 17%

0%

5%

10%

15%

20%

25%

30%

35%

AT&T Gold PeakTea/Coca Cola

MasterCard Walmart 825 Coca ColaChina

Coca ColaBrazil

UnileverMagnum

Allstate Wendys

% of mobile display in the mx (ex search)

Optimal allocations to Mobileas a percentage of total marketing mix

Gap to Optimal

Actual Spend

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 16 And when Mobile is Optimized we see Gains of nearly 20% in Brand metrics and 7% to 60% in Sales

16

18%7% 17% 14% 16%

60%

13% 7%0%

25%

50%

75%

100%

125%

150%

175%

AT&T Gold PeakTea/Coca

Cola

MasterCard Walmart 825 Coca ColaChina

Coca ColaBrazil

UnileverMagnum

Allstate Wendys

% of mobile display in the mx (ex search)

Increase in Key Business Outcomes Based Mobile in the Mix versus No Mobile

Increase in KeyBusiness Outcomes

Sales

SalesSalesSalesSalesBrand

Sales

Image

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 17 SMoX Informed the Case to Drive MTA

What Did SMoX Tell us about the Opportunity

for MTA and it’s importance

17

Measuring Mobile is not the issue. It is

measuring the whole marketing stack, “in all it’s permutations”

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 18

18

Just Looking at Ads, Doesn’t tell us the Whole Story

18

Branding:Aided Awareness/

$ spent*

Sales:ROI

Mobile Displaywith weathertargeting

MobileDisplay

Campaign Average(across all media) 100 100

*Index is based on Number of people who became aware of Magnum per $ spent.

200 147175 ZERO

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 19

*Index is based on Number of people who became more likely to consider Allstate / $ spent

We’ve Consistently Seen How Targeting Improves Performance. But how much?

Mobile Video Targeting Consideration / $ Spent

+ Behavioral targeting

+ Contextual targeting

Demographictargeting 100

19

320191

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 20

Then Suddenly, Everything Changed

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 21

Proprietary & Confidential 21

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

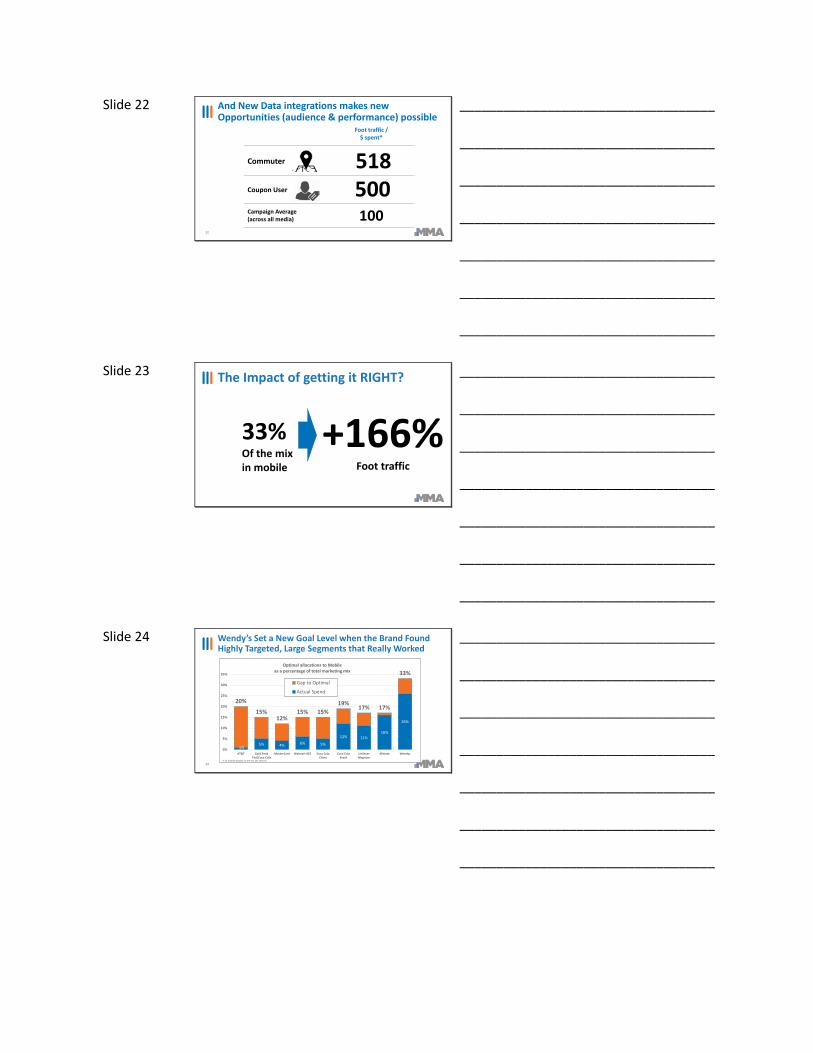

Slide 22 And New Data integrations makes new Opportunities (audience & performance) possible

Foot traffic /$ spent*

Commuter

Coupon User

Campaign Average(across all media) 100

518500

22

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 23 The Impact of getting it RIGHT?

33%Of the mixin mobile

+166%Foot traffic

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 24 Wendy’s Set a New Goal Level when the Brand Found Highly Targeted, Large Segments that Really Worked

24

1%5% 4% 6% 5%

12% 11%16%

26%

20%

15%12%

15% 15%19%

17% 17%

33%

0%

5%

10%

15%

20%

25%

30%

35%

AT&T Gold PeakTea/Coca Cola

MasterCard Walmart 825 Coca ColaChina

Coca ColaBrazil

UnileverMagnum

Allstate Wendys

% of mobile display in the mx (ex search)

Optimal allocations to Mobileas a percentage of total marketing mix

Gap to Optimal

Actual Spend

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 25 Now We have a New Vision for How High, High Could Be

25

18%7% 17% 14% 16%

60%

13% 7%

166%

0%

25%

50%

75%

100%

125%

150%

175%

AT&T Gold PeakTea/Coca

Cola

MasterCard Walmart 825 Coca ColaChina

Coca ColaBrazil

UnileverMagnum

Allstate Wendys

% of mobile display in the mx (ex search)

Increase in Key Business Outcomes Based Mobile in the Mix vs. No Mobile

Increase in KeyBusiness Outcomes

Sales

SalesSalesSalesSalesBrand

Sales

Image

Traffic

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 26

…How else do we assess the value of ad unit combination #159:Or, Mobile video channel targeting men who have visited a dealership in the last 7 days

…Or assess the value of ad unit combination #395:Or, Mobile audio channel targeting women who commute by a QSR regularly over last month

…Versus the dozen’s or hundreds of other ad format, data, target, time of day, context, location, etc. combinations

The issue is that ONLY MTA can get Granular

26

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 27 And by the Way; Click Thru is Fake Measurement

16

81%of marketers use CTR more than any other

metric

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 28 What do We Know

about MTA

Few use it, most are super frustrated,

limited capabilities to assess value; but it’s

important

28

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 29 MMA Board Believes MTA is the Measurement Technique and Tool For the Future

29

Multi-Touch Attribution: The science of using advanced analytics, • on user level data,• to allocate proportional credit,• across a granular list of marketing

touchpoints across many, • and hopefully all, online and offline channels,

leading to a desired customer outcome.

Excluded: Traditional MMM, brand tracking and last-touch attribution methods

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 30 Marketers Want to Adopt But Are Slow

Confidential: Cannot be shared without permission from the Mobile Marketing Association30

Does your company currently use a multi touch attribution (MTA) solution or do you plan to use one in the future? N=343 (2017) N=412 (2016), Total Sample

34% 37%

15% 16%

17%20%

10%11%

25%17%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2016 2017

We don’t plan to use in the near future

We will use in the next 12months

We will use in the next 12months

We will use in the next 6months

We currently MTA

75% 83%

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 31 But that Same Research Showed Huge Dissatisfaction with MTA

Confidential: Cannot be shared without permission from the Mobile Marketing Association

MMA interviews and a quantitative survey reveal the following marketer views on MTA:

Low Satisfaction. Marketers not happy with the data they are getting.*

Fragmented Provider Ecosystem. Ten of 30 providers account for two-thirds of use.*

Mistrust and Hesitation. Marketers have a huge lack of trust, and hesitate to use MTA.**

Minimal Expert Understanding.Marketers don’t have MTA expertise.

Different Approaches. Providers use different analytics methods and data, presenting evidence in different ways.***

Sources:* Quant survey of 118 marketers conducted by the MMA as part of this project** Based on 15 in-depth one-on-one interviews with members*** RFI response analysis

-31%-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

MTA providers have a dismal Net Promoter Score

Overall how likely is it you would recommend your main multi touch attribution (MTA) provider? N=118, Total MTA users

1NPS style calculation created from 10 pt satisfaction question

31

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 32 One, we need to Confirm the Analytics are Right

Confidential: Cannot be shared without permission from the Mobile Marketing Association

1. Agent-based modeling2. Bayesian machine learning3. Bayesian shrinkage4. Control theory5. Counter-factuals6. Doubly robust propensity modeling7. Elastic net8. Ensemble based probabilistic9. Experimental design10. Frequent pattern analysis11. GLM12. Hidden stage Markov models

13. Hierarchical regression14. LASSO15. Last touch16. Logistic regression17. Monte Carlo simulation18. Probability of exposure19. Shapley values20. Structural equation models21. Survey based measurement22. Time decay23. Time series24. Utility theory25. Vector autoregression

32

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 33

1. MTA project starts as a “Big Data” project, but marketers are not data architects

2. Data quality is not validated3. Data completeness is needed, therefore

walled gardens are a challenge4. Marketer expectations are higher than

what providers can deliver when data assets are not in shape

But Two, the Real Problem?YOU [marketers] AREN’T READY FOR MTA!!!

“MTA is first and foremost a big

data project and many big data projects fail”

- MTA Provider

“Until we trust the data no one will accept the

MTA analysis that is built on it”- Marketer

33Confidential: Cannot be shared without permission from the Mobile Marketing Association

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 34

CategoryElements of

Attribution Solutions Educ

atio

n

Def

initi

ons

Nee

ded

Code

of

Cond

uct

Best

Pr

actic

es

Valid

atio

nRe

sear

ch

Stan

dard

s

Audi

ting

Para

met

ers

Data QualityData Quality & Accuracy (and Walled Gardens) X X X X X X

Standardize and Leverage Unified IDs X X X X X

Single Source Linkage to Sales Data X X X X

AnalyticValidity

Experimental Design X X X X

Transparency of Approach X X

Validation of Results and Outcomes X X X

Business Outcomes

Facilitate Agile Marketing X X

Enhance Mobile Readiness X X X X X X X

Prove Lift in Campaign Performance X X X

SolutionCompleteness

Specific Approach for Offline Media X X X X X

Use MTA for Both Brand and Performance Goals X X X

Comprehensive Answers for Planning and Budgeting X X X

34

In Total, There are 12 Elements for Development

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 35 What is the Industry

Doing About MTA

MMA Board believes it’s hard but needs to

be done

35

Truth is, much of our current approach

sucks, and the industry needs to get

to better, business impact proving, measurement

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 36 In September 2016, we Launched…

36

MATT is a community of industry experts committed to rethinkingthe world of marketing measurement and attribution; seeking togive marketers better measurements, tools and confidence inconnecting marketing to business outcomes.

All MMA members are invited to participate in MATT

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 37

Applied to 35% of

Campaigns (on avg.)

38% AlreadyHave an

MTA Solution

MATT’s MTA Mission…This is where we started

-31 NPS!

37 Based on MMA Survey from November 2016.

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 38 Started with “Selecting…”

38* The Decision Guide is available for members only at http://www.mmaglobal.com/matt.

The Report:A comprehensive

guide to MTA

MTA RFI Template

Scoring Tool: To help withevaluation

4-Part MATT MTA Webinar Series

Part 1: Intro to Multi-Touch Attribution

(MTA) Methods

Part 2: Selecting the Best MTA

Provider For Your Needs

Part 3: Making Sense of Attribution

Approaches

Part 4: Leveraging MTA to Improve

Marketing Effectiveness

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 39 MATT’s MTA Focus on Data – Four Part Series

MTA Tactical Success Guide™

Data Acquisition RFI™

Perspective on Walled Gardens™

MTA Data Strategy Guide™

To be released Q2 ‘18To be released Q1 ‘18Released Dec ‘17Released Sept ‘17

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 40

North America

MMA MTA Data Map™

40

Meant to be Single Visual on MTA Strategy

1. Poster-sized framework for complete data picture

2. Companion booklet with “how to” instructions

3. Ensures nothing gets “left out” of the marketer, agency, DMP, and MTA provider strategy discussions

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 41 MATT’s MTA Strategy – How it all fits together…

41

MTA Decision Guide™- MTA Landscape Report- MTA Provider Scoring Tool- MTA Request for Information- 4-Part Intro to MTA Webinar

MTA Tactical Success Guide™

MMA MTA Data Map™

Data Acquisition RFI™

Perspective on Walled Gardens™

MTA Data Strategy Guide™

Part 1: Intro to Multi-Touch Attribution

(MTA) Methods

Part 2: Selecting the Best MTA Provider

For Your Needs

Part 3: Making Sense of Attribution

Approaches

Part 4: Leveraging MTA to Improve

Marketing Effectiveness

QUARTERLY BENCHMARK

SURVEYS

To be released Q1 ‘18

To be released Dec ‘17

To be released Dec ‘17

Released Sept ‘17Released Nov‘16 Released Jan ‘17

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 42

Project Based Initiatives to Accomplish GoalsA. Marketer MTA Journey Map visualB. What CMOs need to know about MTA guideC. Brand vs. Performance Experiment studyD. MTA for Publishers program

Other Supporting ActivitiesA. MATT “Unplugged” (MMA Event on MTA in Nov) B. MMA MTA Benchmark Surveys

MMA’s 2018 Operating Plan for MATT

42

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 43

43

This Overused Phrase Actually Missed the Point

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 44

Age of ReShaping Marketing

44

We Are Really In…

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 45

45

Thanks Greg StuartCEOMobile Marketing [email protected]

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 46 MMA: Leading Marketing Forever

SMoXMobile ROI Research

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 47 Upcoming MMA Events:

47

MMA IMPACT: April 10-11 – New York

MMA Cannes Lions Beach Club: Cannes Lions Festival of Creativity: June 18-22 – Cannes

MMA CEO & CMO Summit: July 15-17 – Sonoma, CA

The Smarties – October 1 – New York

MMA INNOVATE: October 1-2 – New York

MMA MATT/Multi-Touch Attribution Unplugged – TBC – New York

Plus: London, Istanbul, Madrid, Dubai, Sao Paulo, Buenos Aries, Mexico City, Singapore, New Delhi, Jakarta, Shanghai

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 48 MMA’s Focus to Rethink Marketing (and Mobile)

48

USP & Positioning

Economic Value & ROI

Getting it Right/Best

Creative Exploratory & Effectiveness

Building Measure-ment Tools

Organiza-tion Design

MOSTTMarketing Org Structure Think Tank

Wave II

Wave I

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 49

North America

MMA MTA Data Map™

49

Meant to be Single Visual on MTA Strategy1. Poster-sized framework for complete data picture2. Companion booklet with “how to” instructions3. Ensures nothing gets “left out” of the marketer,

agency, DMP, and MTA provider strategy discussions

A version has been sent to your office

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 50

50

Questions?Greg StuartGlobal CEOMobile Marketing [email protected]

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 51

51

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 52 What Else Have We Learned from SMoX

Insights of Note from other SMoX Studies

52

Mobile is not really the challenge or the

issue. It’s what it means to “getting

closer to consumer”

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

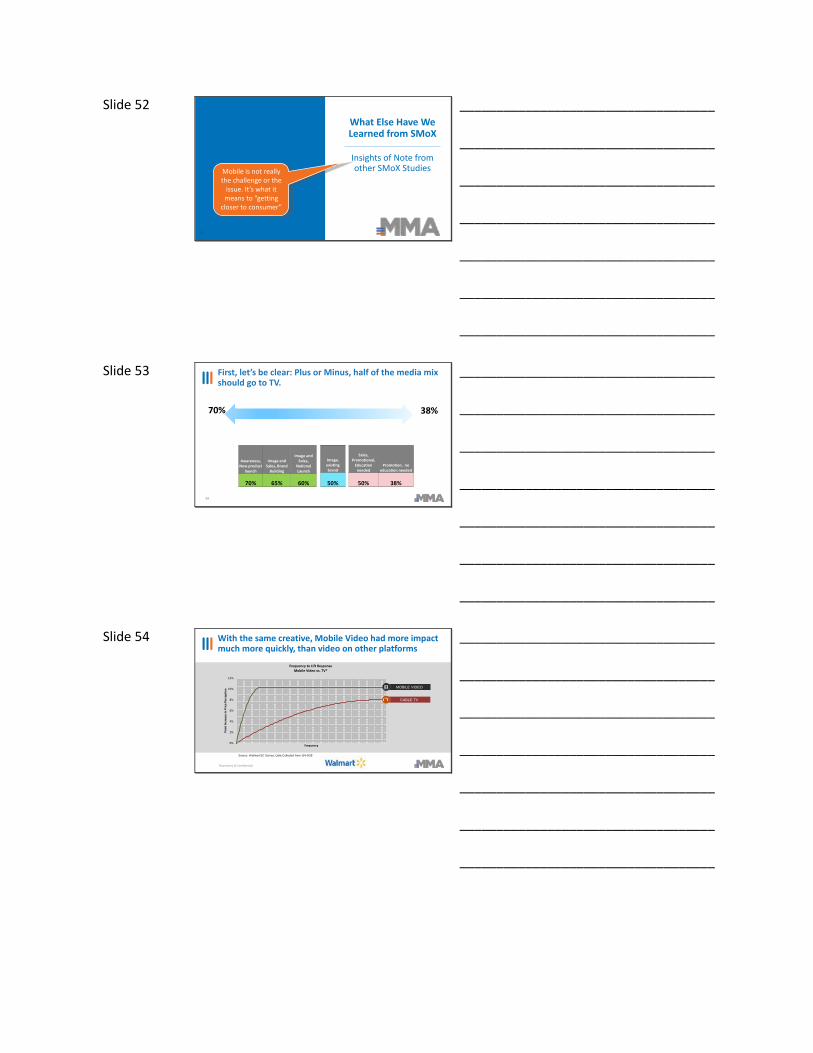

Slide 53 First, let’s be clear: Plus or Minus, half of the media mix should go to TV.

53

70% 38%

Awareness, New product

launch

Image and Sales, Brand

Building

Image and Sales,

National Launch

70% 65% 60%

Image, existing brand

50%

Sales, Promotional,

Education needed

Promotion, no education needed

50% 38%

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 54 With the same creative, Mobile Video had more impact much more quickly, than video on other platforms

Proprietary & Confidential

0%

2%

4%

6%

8%

10%

12%

Poin

t Inc

reas

e in

Pric

e Pe

rcep

tion

Frequency

Frequency to Lift ResponseMobile Video vs. TV*

Source: Walmart SC Survey; Data Collected from: 8/4-9/28

MOBILE VIDEO

CABLE TV

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

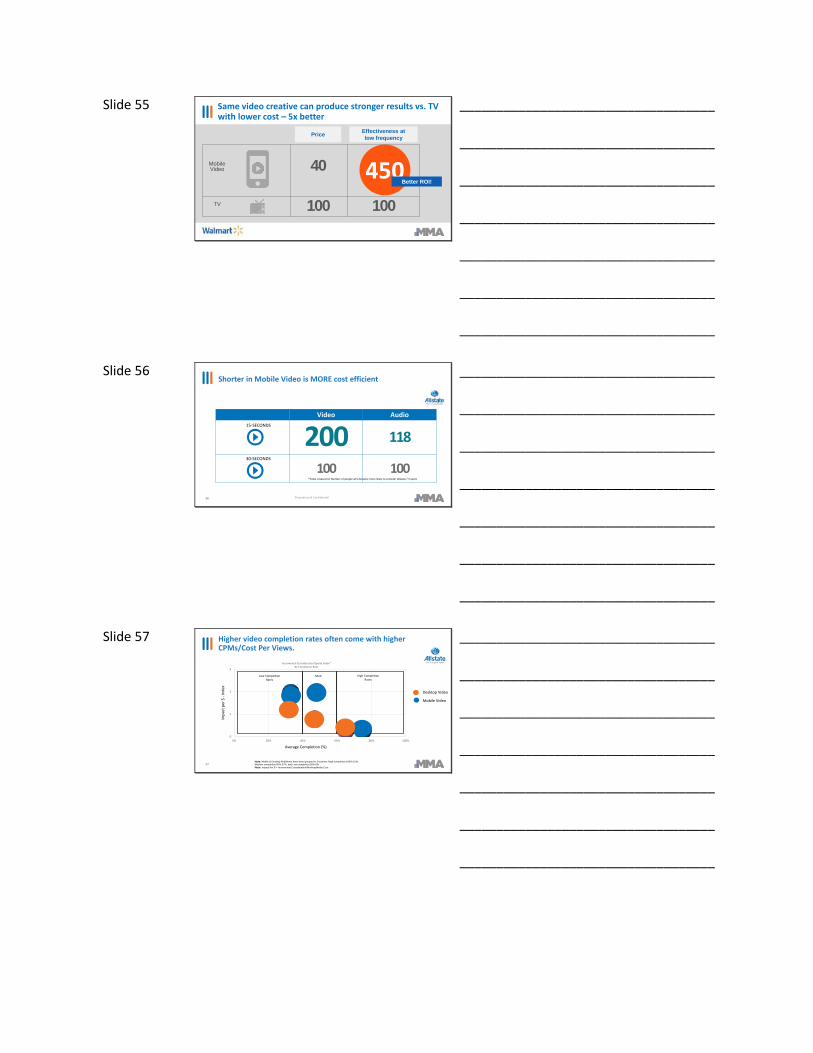

Slide 55

Mobile Video

TV

40

100 100

450Better ROI!

Effectiveness atlow frequencyPrice

Same video creative can produce stronger results vs. TV with lower cost – 5x better

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 56 Shorter in Mobile Video is MORE cost efficient

Proprietary & Confidential56

Video Audio

200 118

100 100*Index is based on Number of people who became more likely to consider Allstate / $ spent

15-SECONDS

30-SECONDS

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 57 Higher video completion rates often come with higher CPMs/Cost Per Views.

57

0

1

2

3

0% 20% 40% 60% 80% 100%

Incremental Consideration/Spend Index*By Completion Rate

Low Completion Rates

Mod High Completion Rates

Note: Mobile & Desktop Publishers have been grouped in 3 buckets: High completion 100%-51%, Medium completion 50%-37%, and Low completion 36%-0% Note: Impact Per $ = Incremental Consideration/Working Media Cost.

Average Completion (%)

Impa

ct p

er $

-In

dex

Desktop Video

Mobile Video

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 58

* Statistical significance at 95%Sources: Walmart Savings Catcher – Combined Publisher report; Walmart Savings Catcher Sub-Segment PerformanceFindings on in-store purchase behavior to come

Expandable Units

Pencil UnitsA

udie

nce

Prox

imity+40%+10%

No Lift +12%

Closer to my Patterns: Getting Location Just Right, Mattered a Lot

58

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

Slide 59 Real time LBA, Proximity targeting and location enhanced creative are the key applications, seen as more valuable

593/12/2018

Q12-01) How often do you use each of the following location strategies:Q12a ) How valuable would you say each of the following location strategies is:

30

35

40

45

50

55

60

65

30 35 40 45 50 55

Beacons Footfall

Non precise Geo

Real time LBA

Historic LBA

Geofencing

Polygon

Geoconquesting

Location enhanced creative Proximity

Perceived as Extremely Valuable

Use Every time I use mobile advertising

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________

___________________________________