t4 - part b - case study yj - oil and gas industry case ... docs/2010 syllabus docs/t4... · tullow...

TRANSCRIPT

©The Chartered Institute of Management Accountants 2014

Note: This report is far more comprehensive than would be expected from a candidate in exam conditions. It is more detailed for teaching purposes.

T4 - Part B - Case Study

YJ - Oil and gas industry case - March 2014

REPORT

To: YJ Board

From: Management Accountant

Date: 25 February 2014

Review of issues facing YJ Contents 1.0 Introduction 2.0 Terms of reference 3.0 Prioritisation of the issues facing YJ 4.0 Discussion of the issues facing YJ 5.0 Ethical issues and recommendations on ethical issues 6.0 Recommendations 7.0 Conclusions Appendices: Appendix 1 SWOT analysis Appendix 2 PEST analysis Appendix 3 NPV of carrying on production at CCC Appendix 4 Forecast costs of drilling for EEE Appendix 5 YJ total cash forecast for one year period ending February 2015 on its own

(without farm-out proposal with Q) and with farm-out proposal with Q Appendix 6 Revenue valuation of EEE reserves Appendix 7 Part (b) – Email to Board members on the differences between profit and cash

and the significance of cash flow in the oil and gas exploration and production industry and the merits of the farm-out proposal with Q

1.0 Introduction YJ is a small E & P oil and gas company which was listed on the AIM in 2007. It has been reasonably successful to date and already has three oil and gas fields in production (AAA, BBB and CCC). It was recently awarded the licence for EEE, an oil and gas field off the coast of an African country. Furthermore, YJ has received a farm-out proposal from a multi-national company, Q, to share this new oil and gas field with it in return for payment of fees. YJ is also currently awaiting the outcome of three further licence applications for potential oil and gas fields it has identified and carried out surveys on.

March 2014 Page No: 2 T4 Part B Case - Answer

YJ‟s share price has fallen to its lowest level for two years following the announcement that field CCC has been temporarily shut down following the build-up of gas pressure at the production well on 13 February 2014. Until CCC is operational again, investors are unwilling to invest further equity finance through a rights issue. As a small company, YJ has limited access to the vast amount of cash required for drilling costs in order to bring the newly licensed oil and gas field EEE into production. However, YJ has been approached by a global oil and gas company Q with a proposal for it to take a 48% share in EEE through a farm-out agreement. Tullow Oil plc is an independent oil and gas exploration company based in the Republic of Ireland. It has grown from a small company which won its first licence in Senegal, Africa in 1986, to become one of the largest independent oil and gas companies in Europe with production assets and interests in over 90 licences spread across 23 countries. 2.0 Terms of reference I am the Management Accountant appointed to write a report to the YJ Board which prioritises, analyses and evaluates the issues facing YJ and makes appropriate recommendations. I have also been asked by Orit Mynde, Chief Financial Officer (CFO), to draft an email to Board members on the differences between profit and cash and the significance of cash flow in the oil and gas exploration and production industry and the merits of the farm-out proposal with Q. This is included in Appendix 7 to this report. 3.0 Prioritisation of the issues facing YJ 3.1 Top priority – CCC shut down The top priority is the current shut down of oil and gas field CCC due to safety reasons following the dangerously high level of gas pressure at the production well. This is justified to be the top priority issue as this is affecting shareholder confidence as evidenced by YJ‟s share price and urgent action is required to decide what actions are required to bring CCC back into production. The possible need to drill a new production well at a cost of US$ 50.0 million, is a very large level of expenditure and would significantly affect both profits and cash generated from operations. Alternatively this oil and gas field could be shut down permanently. 3.2 Second priority – Farm-out proposal This is considered to be the second priority as the proposal from Q for a farm-out arrangement would enable Q to gain 48% share of the newly licensed oil and gas field EEE in exchange for fees. This would enable YJ to share the cost of test and production drilling and the farm-out would also generate a large one-off payment of US$ 75.0 million. This would provide much needed cash to help YJ to bring this oil and gas field into production sooner than would have been possible for YJ to do on its own. 3.3 Third priority – EEE licence awarded The third priority is considered to be the new licence for EEE and the range of potential sizes of the oil and gas reserves in EEE. Additionally there is the consideration as to whether YJ should wait until CCC is back in operation in order to raise the required finance to commence test and then production drilling at this new oil and gas field and retain 100% rights over all future revenues, rather than sharing the revenues with Q in the farm-out proposal.

March 2014 Page No: 3 T4 Part B Case - Answer

3.4 Fourth priority – Recruitment problems This issue is considered to be the fourth priority as YJ‟s growth will be limited by its ability to recruit and retain adequate numbers of operational managers. There is also the discussion concerning whether there is a need to change the company‟s remuneration policy to either include a share of profits or to establish an employee share scheme, or whether a salary increase alone would help resolve this problem. It should be noted that the security issue could be ranked in the top 4 but this will depend on whether there have been any real life examples of terrorist activities, which could raise its importance on exam day. It is considered only as an ethical issue in this suggested answer. A SWOT analysis summarising the strengths, weaknesses, opportunities and threats facing YJ is shown in Appendix 1. A PEST analysis is shown in Appendix 2. 4.0 Discussion of the issues facing YJ 4.1 CCC shut down On 13 February 2014, a routine daily safety check identified that the natural gas pressure at CCC was much higher than normal and subsequently the gas pressure rose to a higher level than allowed by safety regulations. Therefore, Lee Wang, Director of Health, Safety and Environment, advised that production at CCC should be ceased immediately. In this industry, safety is a top priority as the implications of even a minor accident could have an enormous impact on the safety of the workers on these off-shore production well sites and also on the environment. If there were to be an explosion at CCC then this could cause severe long-term damage to YJ‟s reputation. Safety must be the top issue here and the production well at CCC must remain shut down until it is considered safe to start production again, using the existing production well or possibly a new production well within the CCC oil and gas field. The Deepwater Horizon oil spill in the Gulf of Mexico in April 2010 started after high-pressure methane gas from the well expanded into the drilling riser and was released onto the drilling rig where it ignited and exploded. This massive explosion resulted in the deaths of 11 workers on the drilling platform and the subsequent spillage of around 4.9 million barrels of oil into the sea over several months before it was brought under control and officially sealed in September 2010, months after the start of the oil spill. This has had huge reputational damage and cost implications to BP and Transocean, BP‟s outsourced oil and gas rig contractor. Safety and environmental factors must be the top priority issue and therefore YJ has been responsible in closing down operations at CCC before the gas pressure situation worsened. The prevention of a possible major accident by YJ personnel should be welcomed. However, shareholders are more interested in the delay in oil and gas production and the temporary shut down which is adversely affecting revenues and cash flows. The shut down of CCC has resulted in lost revenues totalling US$ 115,000 each day. This is cash that YJ needs to help finance its other E & P opportunities. Additionally, the temporary shut down of CCC is affecting shareholder confidence, YJ‟s share price has fallen to its lowest level for two years and investors have advised that they are not willing to invest further in a rights issue to raise finance for the newly licensed oil and gas field

March 2014 Page No: 4 T4 Part B Case - Answer

EEE until the situation at CCC is resolved. Therefore, YJ‟s management need to urgently decide what options it has in order to bring CCC back into production. When YJ‟s management has decided what it is to do about CCC, then it needs to advise its shareholders. Shareholders have not yet been informed of the full implications of the temporary shut down of CCC. YJ‟s management are considering three alternative options, which are:

1. Re-starting production using the existing oil and gas production well if the gas pressure reduces to a safe level.

2. Closing off the existing oil and gas well and to drill a new production well in a different location within the licensed area of CCC.

3. Closing down CCC permanently.

The analysis and cost implications for these three alternatives are shown as follows: Re-starting production using the existing well The case material states that Adebe Ayrinde, Director of Drilling Operations, and Lee Wang both consider that re-starting production using the current production well would NOT be safe. They both consider that the safest way to continue production at CCC is to close off the existing well. Therefore this alternative is not a viable proposal due to safety considerations. An explosion or oil spillage at CCC could severely affect the long-term future of the entire company. Therefore this option is dismissed. Closing off the existing oil and gas well and to drill a new production well in CCC The possible need to drill a new production well is forecast to cost US$ 50 million plus a further US$ 5 million to close off the dangerous production well. This is a large amount of expenditure and currently YJ does not have this level of finance available. It has a cash balance of only US$ 25.6 million at 1 March 2014. However, YJ‟s existing other two oil and gas wells that are in production (AAA and BBB) are generating substantial cash from operations (US$ 52.0 million per year before tax and finance costs). However, YJ has the requirement to invest in the newly licensed oil and gas field EEE. Therefore, YJ needs cash to bring EEE into production as well as to drill a new production well for CCC. This is a huge cash requirement, especially with shareholders currently not willing to invest new equity finance, resulting in a difficult situation. Appendix 3 shows that it is financially worthwhile to drill a new production well to carry on with production at CCC. Even with the required capital investment costs totalling US$ 55.0 million over the next year (Year 1) for drilling costs and closure of the dangerous well, the future discounted net cash flows of US$ 21.0 million per year results in a positive NPV of US$ 68.3 million. Appendix 3 also shows an alternative NPV calculation, which excludes the cost of US$ 5.0 million for closing the current dangerous well, is a positive US$ 72.9 million. It could be argued that the cost of closing off the dangerous production well would be required anyway, irrespective of whether YJ chose to drill a new production well or not. Therefore it is financially viable, under either of the alternative calculations, to try to get CCC back into production even after the extra cost of drilling a new production well.

March 2014 Page No: 5 T4 Part B Case - Answer

However, the dilemma for YJ‟s management is how to finance the required US$ 55.0 million capital expenditure, especially with competing cash requirements for the newly licensed oil and gas field EEE. If YJ were to drill a new production well at CCC, it would not be operational until the end of February 2015, a year from now. This is a long time and investors should be brought up to date and advised of this timescale if the decision to drill a new production is taken. The issue concerning Ullan Shah, Chief Executive Officer, instructing to Orit Mynde, Chief Financial Officer, to re-assure investors about CCC and to effectively lie to investors concerning the temporary short-term nature of the problem is discussed in the Ethics section of this report in paragraph 5.3 below. Shutting down CCC permanently YJ has a third alternative which is to shut down CCC permanently. This would require capital expenditure of only US$ 5.0 million in order to close off the dangerous oil and gas well. However, it would result in YJ giving up future net cash flows of US$ 21.0 million each year for the remaining 9 years of productive life at CCC. This does not make economic sense when the NPV is so high at US$ 68.3 million, even after the additional drilling costs of US$ 50.0 million. Therefore the option to permanently close down CCC is not financially viable and should be rejected. Summary The problem remains that finance needs to be found to bring CCC into production, which will be difficult with the newly licensed field EEE which needs to be taken into production. With shareholders showing a lack of confidence in YJ, it would be impossible to have a rights issue. YJ could attempt to farm-out CCC, in order to gain some finance to bring this back into production. Alternatively if YJ were to farm-out EEE, as discussed in the next paragraph, then some of the cash generated from this farm-out arrangement could be used to finance bringing CCC back into production. Appendix 5 shows that there would be adequate cash to bring CCC back into production if YJ were to farm-out 48% of EEE to Q. 4.2 Farm-out proposal YJ has recently been awarded the licence for oil and gas field EEE, which is a potentially very significant development for YJ. This field has a 50% probability of generating 3,000 bopd and 2,500 boepd, which would make this oil and gas field the largest of all of YJ‟s current licensed fields. YJ‟s has two oil and gas fields currently in production (but CCC is shut down at present) which are generating large sources of cash. These could be categorised as „Cash Cows‟ using the BCG matrix, as they are cash generators and profitable and that these profits can be used to support other aspects of the company that are in their development stage. Under the terms of the licence, this field needs to be brought into production within a two year period by the end of December 2015. Therefore YJ needs to identify and secure adequate finance to undertake both test drilling and production drilling within this potential large oil and gas field.

March 2014 Page No: 6 T4 Part B Case - Answer

YJ has funded the drilling costs for all of its current three oil and gas fields through equity and debt finance and has never before undertaken a farm-out arrangement. Therefore this is a major strategic decision for YJ. However, in the current situation with CCC temporarily shut down and investors unwilling to invest further via a rights issue, YJ may have little choice but to accept a farm-out agreement. Farm-out and farm-in arrangements are commonly used in the oil and gas industry with many large multi-national companies taking a stake in oil and gas fields identified and licensed to small E & P companies. For example, BP plc is involved in a number of farm-in arrangements. A farm-in is defined as acquiring an interest in a licence from another E & P company. In Brazil, BP has acquired a 30% interest in five deep-water exploration fields held by an international oil company. The fees payable for farm-out arrangements vary greatly, with some multi-national companies paying large annual fees in order to obtain a share of the licensed oil and gas fields identified and managed by other smaller E & P companies. Forecast drilling costs The forecast drilling costs total US$ 125.1 million, as shown in Appendix 4. This comprises:

US$ 38.04 million for two test wells at US$ 19.02 million each

US$ 87.06 million for three production wells at US$ 29.02 million each This is a huge cost for YJ to try to finance on its own which is hampered significantly by three factors. These three factors are:

1. With CCC temporarily shut down, YJ has lower cash being generated from operations.

2. Secondly, with CCC shut down, YJ‟s shareholders are not prepared to invest further through a rights issue.

3. With CCC shut down, raising new loan finance is unlikely to be successful (as stated in

the unseen case material). Therefore, YJ needs to either delay starting drilling at EEE or to accept the farm-out proposal from Q. If YJ were to delay drilling in this newly licensed field until CCC was back in operation, this would be the end of February 2015. This would not allow sufficient time to then raise new finance in order to bring EEE into production before the licence deadline date of the end of December 2015. This means that Orit Mynde‟s preferred approach to delay EEE is highly risky. Risk of EEE not being economic to go into production According to the probabilities assigned to the size of the oil and gas reserves following YJ‟s survey work, there is also the 10% risk that EEE will not be economic to go into production. Although this is a low probability, it is still possible. The test drilling is forecast to cost US$ 38.04 million. If YJ were to agree to the farm-out proposal with Q, then this cost and the associated risk would be shared with Q. It should be noted that the one-off up-front farm-out fee of US$ 75.0 million would not be payable at all if EEE were proved to be uneconomic to go into production following test drilling. However, by agreeing to a farm-out with Q, this would reduce YJ‟s share of test drilling costs from US$ 38.04 million down to US$ 19.8 million.

March 2014 Page No: 7 T4 Part B Case - Answer

Farm-out proposal from Q

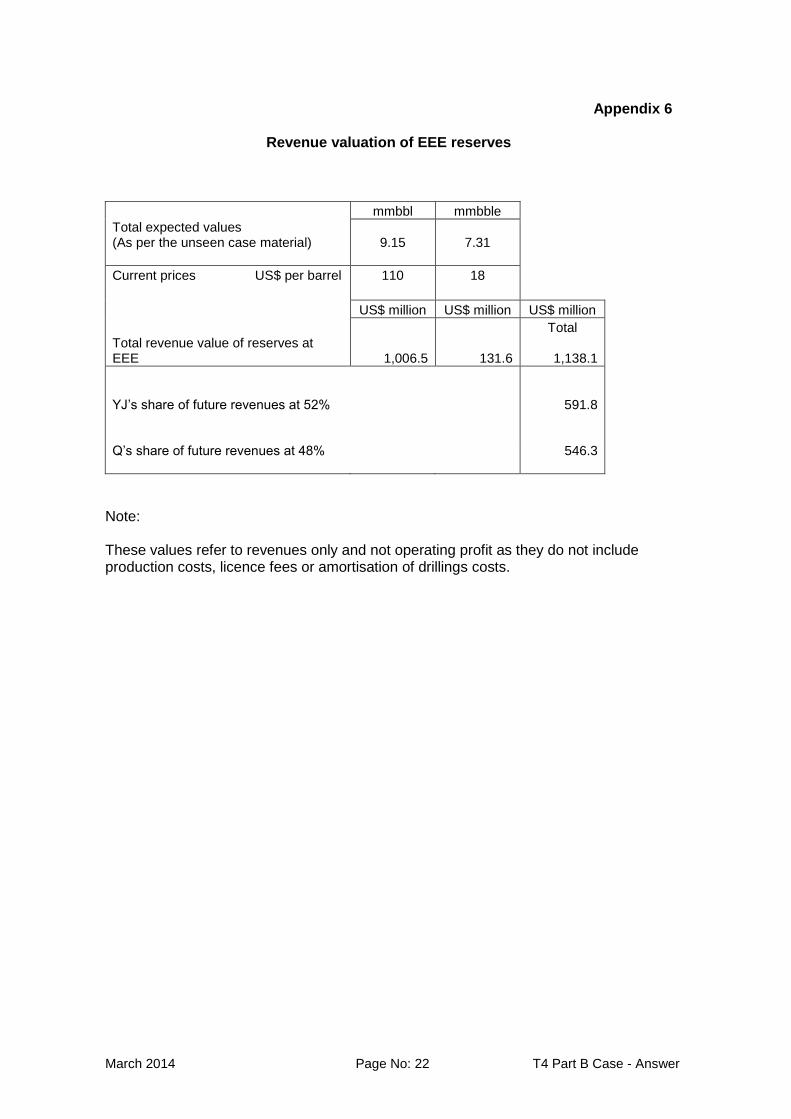

The farm-out proposal would give Q a 48% share of the newly licensed oil and gas field EEE. This would result in YJ only retaining 52% of all of the oil and gas reserves in EEE and would reduce YJ‟s future revenues and cash flows. However, the farm-out proposal would help YJ to share the cost of test and production drilling and it would generate a large one-off payment of US$ 75.0 million from Q. This would generate much needed cash to help YJ to bring this oil and gas field into production sooner than would have been possible for YJ on its own. Without the farm-out proposal YJ would have a cash deficit of US $ (126.0). This is shown in Appendix 5. This includes the cost of bringing CCC back into production. The unseen material states that due to the problems at CCC, trying to raise new loan finance or a rights issue would not be successful, so YJ has no other alternative way to raise the required finance. Therefore, the farm-out proposal looks very appealing. The oil and gas field at EEE is potentially very large with reserves valued at US$ 1,138 million as shown in Appendix 6. Therefore, there is room to negotiate with Q on either its percentage share for the farm-out or the up-front one-off fee payable by Q for a share of EEE. Perhaps the offer of US$ 75.0 million could be negotiated up to US$ 100.0 million. Alternatively, the level of the one-off fee could be based on the size of reserves after test drilling has been completed as the reserves can be assessed with more certainty then, rather than the current forecast range of probabilities based on survey work alone. YJ’s manpower shortage The forecast number of days required for YJ‟s management of drilling operations would be 2,200 days per production well which totals 6,600 days for EEE in total. This equates to 30 managers. As discussed in paragraph 4.4 below, YJ has a shortage of skilled managers and that Q has offered to allow 15 of its own skilled managers to work on EEE if the farm-out proposal were to be agreed. So this would be another key advantage of agreeing to the farm-out proposal. Summary If YJ were to accept the proposed farm-out agreement with Q, then this would enable YJ to have sufficient cash to bring CCC back into production and also to bring EEE into production well before the deadline date of 31 December 2015. This is shown in Appendix 5 and demonstrates that with the farm-out proposal, YJ would have a small cash surplus of US$ 9.0 million. Another advantage of the farm-out arrangement with Q is the offer from Q to allow 15 of its skilled managers to work on EEE. YJ would need to recruit 30 managers (for the 6,600 man days) to manage the production drilling process for this additional oil and gas location. Currently, YJ has adequate manpower to manage the test drilling process. As there is a skill shortage making recruitment difficult in this industry, this proposal from Q would mean that half of the extra 30 managers would be provided to YJ. This would result in YJ only having to recruit the other 15 managers, which is a more realistic challenge. Therefore the farm-out proposal from Q would help YJ to overcome the two shortages that it currently has, which are cash and manpower resources. In summary this proposal could be assessed using the Johnson, Scholes and Whittington model as follows: Suitability – The proposal to accept the farm-out proposal from Q is suitable for YJ as this would generate adequate cash and manpower resources in order to bring EEE into production.

March 2014 Page No: 8 T4 Part B Case - Answer

Acceptability – the proposal appears to be acceptable to YJ as YJ has no alternative ways to generate the required cash in order to bring EEE into production before the deadline date in the licence. Furthermore, YJ has a shortage of skilled managers and the offer from Q of a loan of 15 skilled managers makes the operational aspects of the farm-out agreement acceptable. Feasibility – This farm-out proposal with Q is feasible as it generates adequate finance for YJ in order to bring EEE into production. 4.3 EEE licence awarded The forecast sizes of the oil and gas reserves at EEE are potentially very large with an expected volume of 9.15 mmbbl for oil and 7.31 mmbble for gas. However, there is a 50% probability that this could be higher at 10.95 mmbbl for oil and 9.13 mmbble for gas. There is also a 10% probability that the reserves could be very high at 14.6 mmbbl and 10.95 mmbble. Until the recent problem at CCC, YJ had three oil and gas fields operational (AAA, BBB and CCC) with a total reserves of 9.198 mmbbl for oil and 12.780 mmbble for gas. Therefore the size of EEE is potentially as large as, or perhaps even larger than, YJ‟s total reserves at all three of its licensed fields. YJ has just been awarded the licence for EEE and the company is gaining a good track record for oil and gas exploration like Afren plc, which has added significant oil and gas reserves to its asset base following successfully being awarded licences in specific areas within Nigeria.

However, there is a 10% risk that EEE would not be economic to go into production, as surveys have shown that there is a 10% probability that the reserves could be only 80 bopd for oil and 40 boepd for gas. If YJ were to test drill EEE on its own (without the proposed farm-out with Q) and find that it was not economic to go into production, then YJ would have incurred test drilling costs at the two test drilling sites within EEE totalling US$ 38 million. This would need to be written off to the Profit or Loss Statement. This write-off would have a huge impact on YJ‟s profitability. As discussed above, due to this 10% risk of EEE not being economic to go into production, a more cautious route would be to proceed with the farm-out arrangement with Q, as at least Q would pay 48% of the test drilling costs, which would be just over US$ 18 million.

There is a proposal from Orit Mynde, Chief Financial Officer, that YJ should wait until CCC is back in operation in order for YJ to then raise finance to commence test and then production drilling at EEE. This would enable YJ to retain 100% rights over all future revenues from EEE, rather than sharing the future revenues with Q in the farm-out proposal. However, it may take until February 2015 to get CCC operational. Therefore, this would not allow adequate time to raise finance and then to commence test drilling and then production drilling in order to bring EEE into production before the deadline in the licence of December 2015. So the opportunity to wait is not realistic and runs the risk of YJ losing the licence at EEE. It would be better for YJ to accept the farm-out proposal from Q and to retain only 52% of the oil and gas from EEE rather than run the risk of losing the licence at EEE, which could happen as YJ does not have sufficient finance to bring EEE into production before the licence runs out in December 2015, due to its current problems at CCC, which were not foreseen. With CCC shut down and not productive, YJ faces the challenge of having to finance drilling a new production well at CCC as well as missing out on cash generated from CCC. This is leaving YJ with a severe cash crisis and no alternative way to raise adequate finance in the short-term for EEE. Without the problems at CCC, investor confidence would be high and additional loan or equity finance could have been raised. This is not available due to the problems at CCC. Long-term To ensure that YJ does not face such financing problems in the future, it is further suggested that YJ should consider seeking a listing on the full stock exchange in order to have access to a

March 2014 Page No: 9 T4 Part B Case - Answer

wider pool of investors in order to be able to raise money for financing drilling costs at future newly licensed oil and gas fields. However, undertaking a full stock exchange listing will take around 18 months and utilise a large amount of management time. This would be a huge distraction for YJ‟s management team at present and would not generate cash in sufficient time to finance drilling costs for EEE. Additionally, with YJ‟s share price being the lowest for two years, due to the shut down at CCC, investor confidence would need to be restored before YJ commenced a full stock exchange listing. However, it is something that YJ should plan to undertake in the future. 4.4 Recruitment problems As the whole of the oil and gas industry is suffering from a skill shortage, if YJ is going to continue to grow and compete with other small E & P companies as well as the multi-national oil and gas companies, it will have to reward its employees based on competitive salaries and other benefits. The employees of YJ and their skills are behind the success of YJ, which is already generating revenues of US$ 174.0 million in the last financial year, within 10 years of the start of the company. YJ is a fast growing company like Afren plc, which only held a minority interest in a single oil and gas field 10 years ago, but the company has grown rapidly and Afren now holds interests in almost 30 oil and gas fields spread across 12 countries. Afren has grown very rapidly and it has been able to recruit a wide range of skilled managers to help manage the volume of growth in its business. The Board of YJ needs to agree how to establish a suitable pay and reward structure in order to be able to recruit and retain its managers. Otherwise, YJ‟s growth will be limited by its ability to recruit and retain adequate numbers of operational managers. There is an industry wide skill shortage and if YJ is to grow as fast as it hopes it will, especially with the success it has achieved with surveying and being awarded licences to date, the lack of adequate skilled managers could threaten its future success. YJ has recently been awarded a licence for field EEE and is currently awaiting the outcome of three further licence applications. If YJ were to be successful in winning further licences, then it would need to recruit even more experienced managers.

There is a need for the Board to discuss and agree whether salary alone is adequate to retain and also to recruit the number of new managers that YJ will need in order for it to grow. Adebe Ayrinde, Director of Drilling Operations, considers that it may be necessary to offer free shares in YJ, linked to achieving performance related objectives, as the only way to attract new managers. YJ needs to recruit 30 new managers in order to manage production drilling operations at the newly licensed field EEE, which is the equivalent of the forecast 6,600 man days. Adebe Ayrinde considers that if YJ does not change its current remuneration policy, it may struggle to be able to recruit this required number of new managers in order to meet the deadlines required to bring EEE into production. It should be noted that if the farm-out with Q were to be agreed, then Q has offered to allow 15 of its managers to work on EEE. Therefore, this would reduce the recruitment problem for YJ down to just 15 new managers to be recruited. However, this is still a large number of new employees to be recruited over the next few months. If YJ were to accept the offer from Q for the farm-out proposal and the loan of 15 of its managers to work on EEE, then Q‟s managers would be working alongside YJ‟s managers. It is likely that YJ‟s managers would discuss pay and conditions with Q‟s managers and this could alert YJ‟s managers to the fact that they YJ do not currently receive any performance related pay, which Q‟s managers possibly do. This could lead to the de-motivation of YJ‟s managers and possibly some of YJ‟s managers could decide to leave and move to competitors.

March 2014 Page No: 10 T4 Part B Case - Answer

Ullan Shah, CEO, has stated that he considers that only directors should be shareholders in YJ and that a slight salary increase should be enough to attract new managers and retain YJ‟s existing managers. Ullan Shah is a key stakeholder with high power and high interest as categorised in Mendelow‟s stakeholder analysis. YJ has three alternatives:

1. It could increase the pay for managers.

2. It could offer its managers free shares annually for meeting or exceeding agreed performance objectives.

3. It could establish and operate an apprentice scheme to try to “grow” its own future

managers. YJ‟s share price when it was listed on the AIM in 2007 was only US$ 6.00 per share but this had grown to US$ 26.80 by December 2013, a growth of 347% over 7 years. However, with the shutdown of CCC, YJ‟s share price has currently fallen. Even with the fall in share price, there has been a material capital gain as the company has grown and identified potential oil and gas fields and won licences and then brought these oil and gas fields into production. The potential for future capital growth is also good as the company‟s oil and gas reserve assets grow as each new licence is awarded to YJ. Therefore, there is an opportunity to establish an employee share scheme, whereby YJ‟s managers could be rewarded with free shares in YJ for meeting set down and agreed performance related targets each year. These targets could be partly specific employee targets as well as company wide targets such as meeting specific dates within a project, such as drilling deadlines or YJ‟s planned profits or the target number of barrels of oil and gas equivalents each day. By rewarding managers with shares, this would align the managers‟ objectives with the company‟s objectives and they would share in the company‟s future share price growth. Therefore this would help to achieve goal congruence and encourage managers to consider the long-term effects of their decisions. This would help ensure that short-termism is not their main focus. This is especially relevant in the oil and gas industry where the process from identifying a potential oil and gas field through to the start of production can take many years. However, Ullan Shah‟s proposal is for YJ to only pay a slight salary increase. This could be considered to be a temporary solution and may possibly work in the short-term but will not address the underlying skill shortage and the need for YJ to retain the best employees and to encourage these employees to stay loyal to YJ. The Board of YJ needs to consider the cost of losing and recruiting new managers and possible delays caused by skill shortages if a small salary increase were to be agreed, rather than the bolder step of establishing a share scheme and achieving long-term loyalty and motivation towards achieving company-wide objectives. The potential difference between these two alternative plans could be huge, although the cost differential may not be that great. YJ is a young growing company and offering its managers free shares is a tangible benefit that will act as a motivator to retain managers and also help to attract the required numbers of new managers. Additionally, another more long-term way to address the industry skill shortage would be for YJ to recruit graduate trainees, to establish an apprentice scheme and to train them in YJ‟s business. This would help YJ to “grow” its own future managers. However, there is no guarantee that these YJ trained managers would stay, as they could move to competitors.

March 2014 Page No: 11 T4 Part B Case - Answer

5.0 Ethical issues and recommendations on ethical issues 5.1 Range of ethical issues facing YJ There are two ethical issues that will be discussed and recommendations made, which are:

1. Security 2. Ullan Shah, Chief Executive Officer, pressurising Orit Mynde, CFO

5.2 – Security 5.2.1 Why this is an ethical issue This is an ethical issue as YJ is proposing to renew the security company contract at a lower cost. Therefore this renewed contract would provide an inferior level of security at YJ‟s oil and gas locations and it would not continue to provide security for YJ‟s employees and outsourced personnel travelling to and from the drilling sites. This exposes YJ‟s employees and outsourced personnel to greater personal risk. It places costs and the need for higher profits above the safety of its employees. YJ has a duty of care to protect its employees and outsourced contractors from possible terrorist actions. 5.2.2 Recommendations for this ethical issue It is unfair to cut security costs when the threat of international terrorism remains a significant problem. Just because there has not been any incident to date does not mean that they will not occur in the future. It is recommended that the security contract is renewed at the same level as the previous year. It is also recommended that all employees undergo safety awareness training regularly. It is also recommended that all outsourced personnel employed at YJ‟s drilling rigs undergo rigorous security checks so that its sites are not exposed to any foreseeable terrorist threat. It is also recommended that YJ‟s management liaise closely with the European government agencies on possible terrorist alerts as well as the governments of the countries in Asia and Africa, in which YJ‟s licensed oil and gas fields are located. 5.3 – Ullan Shah, Chief Executive Officer (CEO), pressurising Orit Mynde, CFO 5.3.1 Why this is an ethical issue This is considered to be an ethical issue as Ullan Shah, CEO, should be supportive of Orit Mynde, CFO. There are two separate instances of where the CEO is not acting in a responsible and ethical manner. These are: 1. Ullan Shah has instructed Orit Mynde that he must tell investors that the shut down of CCC

is very temporary and keep them re-assured if he is to be retained on the Board of YJ. The CEO of YJ should not be asking his CFO, Orit Mynde, to lie to its key institutional investors.

2. Additionally, Ullan Shah is blaming Orit Mynde for his inability to have adequate finance in

place for test drilling at the newly licensed oil and gas field EEE. This is not the sole responsibility of the CFO. It is a Board decision of how and when to raise new equity and debt finance externally.

Furthermore, it would have been difficult to raise external finance any sooner, as shareholders would want to await the outcome of any licence applications before they chose to invest in new equity finance, in the form of a rights issue.

March 2014 Page No: 12 T4 Part B Case - Answer

It appears that Ullan Shah, who has recently joined YJ, is unsupportive of the CFO and he is dealing with a fellow Board member in an irresponsible and derisive manner and not showing due respect. Ullan Shah‟s threat to have Orit Mynde removed from the Board is not possible unless the majority of the members of the Board decided that they did not have confidence in Orit Mynde‟s ability to carry out the CFO role. There is no evidence that Orit Mynde has not got the full support of his colleagues. The CEO‟s bullying behaviour is unacceptable. 5.3.2 Recommendations for this ethical issue It is recommended that Orit Mynde should speak to one or more of the non-executive directors or the Non-executive Chairman, Jeremy Lion, or alternatively the Chairperson of the audit committee to express his concerns over Ullan Shah‟s behaviour towards him. After seeking advice, Orit Mynde should inform his fellow Board members about these instances, so that they are all aware of the comments made to him by the CEO. At the next Board meeting, an apology should be minuted to confirm that the Board has the confidence in the CFO‟s ability to manage YJ‟s finances. Furthermore, Orit Mynde and all Board members should inform YJ‟s shareholders honestly and truthfully concerning the current shut down of CCC and to explain that the shut down was required due to the risk of explosion. The shareholders should be advised that a decision on how and when CCC will go back into production will be announced as soon as the YJ Board has made the decision as to what action it will be taking. 6.0 Recommendations 6.1 – CCC shut down 6.1.1 Recommendation It is recommended that YJ should close the current production well at a cost of US$ 5.0 million and write off the remaining capitalised drilling costs. It is recommended that CCC should be brought back into operation by drilling a new production well. Therefore, it is recommended the cost of US$ 50 million is approved by the YJ board and that drilling commences as soon as possible. It is also recommended that when the YJ Board has made a decision on CCC, the decision should be announced to investors. 6.1.2 Justification The justification as to why YJ should close the current production well is that both the Director of Drilling and the H & S and Environment Director consider that this is the safest route. It is considered to be too risky to carry on using the current production well as an explosion could occur which could have serious long-term damage to YJ‟s reputation and could endanger the lives of workers. The current value of capitalised drilling costs would need to be written off in accordance with accounting standards. This would have a huge impact on profits in the current financial year, 2013/14. It is probable that a profits warning would need to be issued to investors, due to this substantial write-off. Whilst there are no cash flow implications for this write-off of capitalised drilling costs, this would result in lower tax being payable on the reduced profits for the current financial year.

March 2014 Page No: 13 T4 Part B Case - Answer

The justification as to why CCC should be brought back into operation by drilling a new production well is that this would generate a NPV of US$ 68.3 million positive. Therefore CCC should not be permanently closed. However, independent expert advice should be obtained to try to ensure that the location within the CCC field for the new production well is likely to be safe and that the existing problem will not re-occur. The justification as why to YJ should make an announcement to investors is that until CCC is back in production, investors‟ confidence may be lost. Investors need to be told the truth and Orit Mynde should not be put under pressure to re-assure investors that the shut down is only a very temporary problem, as drilling a new production well will take a further year before CCC is back in production. 6.1.3 Actions to be taken

1. YJ needs to identify funding in order to finance the recommended action which would require US$ 50 million for drilling plus US$ 5.0 million for closure costs, totalling US$ 55.0 million, in order to bring CCC back into production.

2. Financing for the new production drilling costs could come from cash generated from

operations over the next 12 months, but this would have implications on the start of drilling at EEE.

3. Safety to continue to be a top priority at CCC and gas pressures should be monitored

closely at the new production well to be drilled.

4. If the farm-out proposal for EEE with Q were to be accepted, then YJ would have

enough cash to drill at CCC and also at EEE. See recommended actions below in paragraph 6.2.3.

6.2 – Farm-out proposal 6.2.1 Recommendation It is recommended that the farm-out proposal with Q is accepted. It is also recommended that YJ should try to negotiate the one-off fee of US$ 75.0 million from Q to a higher figure, due to the forecast large volume of the reserves. Based on expected values, the reserves are forecast to generate revenues totalling US$ 1,138 million over the next 10 years (at current prices). The recommendation is to link the one-off payment to the size of the reserves identified after test drilling. It is further recommended that YJ accept the offer for Q to allow 15 of its managers to work on EEE. 6.2.2 Justification The justification as to why the farm-out with Q should be accepted is that it generates cash from the one-off fee which will help YJ to have sufficient finance to bring EEE into production in the next year and also to bring CCC back into production. Without the farm-out arrangement, YJ would not have adequate cash, using its current cash balance and generated by operations, to take CCC and EEE into production within the next year, as it is forecast that it would have a cash deficit of US$ (126.0) million, as shown in Appendix 5. With the recommendation to accept the farm-out arrangement with Q, it is forecast that this would result in YJ having a cash surplus of US$ 9.0 million after paying finance costs and tax.

March 2014 Page No: 14 T4 Part B Case - Answer

Furthermore, the justification for YJ agreeing to a farm-out proposal at present, with its cash shortage, is that Q would share the test drilling costs of US$ 38 million irrespective of whether the oil and gas field shows that it could be taken into production or not. There is a 10% chance that the test drilling will show that oil reserves are not economic for production. This farm-out agreement would allow YJ to see how well this commonly used arrangement could work for the company. YJ‟s skills lie in identifying potential new oil and gas reserves and it does not currently have the financial strength to bring the potential oil and gas fields into production on its own. The justification as to why the one-off fee of US$ 75.0 million should be negotiated is that it is probably based on the expected value of EEE‟s reserves which are given in the case material as 9.15 mmbbl and 7.31 mmbble. However, for example, there is a 50% probability that the reserves will be higher at 10.95 mmbbl and 9.13 mmbble. Therefore, it is recommended that the one-off fee should be a minimum of US$ 75.00 million and increased if the forecast level of reserves after test drilling has been completed shows a higher level than the current expected level of reserves. A further justification as to why the farm-our proposal should be accepted is that Q would also help YJ with the shortage of managers for the production of outsourced drilling operations. Q‟s offer to allow 15 of its skilled production managers to work on the EEE oil and gas field should be accepted as this would reduce the number of new managers YJ would need to recruit for EEE. 6.2.3 Actions to be taken

1. Before accepting the farm-out proposal with Q, YJ should establish whether there are any other global oil and gas companies willing to compete for this farm-out opportunity.

2. Assuming the farm-out agreement is going to be accepted with Q, then YJ should negotiate over the level of the one-off fee payable after test drilling and to try to get this increased and perhaps linked to the forecast value of reserves established after test drilling rather than the expected value based on survey data.

3. Agree timetable for funding of test drilling costs.

4. Agree timetable for secondment of 15 managers when EEE goes into the production

drilling phase

5. Orit Mynde to prepare updated cash flow forecast to be presented to the Board including the farm-out agreement.

6. Drilling costs should be closely monitored and reported against forecast costs to ensure financing can be put in place if there should be any cost over-runs.

6.3 – EEE licence awarded 6.3.1 Recommendation It is recommended that EEE is test drilled and brought into production as soon as possible. YJ does not have the financial resources to do this without a farm-out agreement. Therefore, it is recommended that the farm-out proposal from Q should be accepted. It is further recommended that YJ should try to negotiate the value of the farm-out one-off payment from Q. It is recommended that the one-off payment should be linked to the forecast size of the oil and gas reserves that are established after test drilling, as there is a wide variation in the size of reserves and the probabilities established from YJ‟s surveys.

March 2014 Page No: 15 T4 Part B Case - Answer

6.3.2 Justification The justification for starting test drilling as soon as possible, using a farm-out arrangement with Q, is that any delay to the start of test drilling at EEE, in order to bring CCC back into production, would significantly delay the start of test and production drilling at EEE and this could exceed the licence conditions of bringing EEE into production before the end of December 2015. It is too risky to delay the start of test drilling. The justification for trying to negotiate to link the one-off payment from Q to the size of the reserves established after test drilling is that probabilities and possible sizes of the reserves at EEE are quite varied. There is a 50% probability of 3,000 bopd for oil and 2,500 boepd for gas ranging up to a 10% probability of a high level of 4,000 bopd for oil and 3,000 boepd for gas. 6.3.3 Actions to be taken

1. The Board to accept the farm-out agreement with Q.

2. Test drilling work should start as soon as possible to identify the forecast level of oil and gas reserves at EEE.

3. YJ‟s management should negotiate the one-off fee payable by Q and link the fee to the

volume of reserves established after test drilling. 6.4 – Recruitment problems 6.4.1 Recommendation It is recommended that YJ should establish a share ownership scheme for all of YJ‟s management level employees, as proposed by Adebe Ayrinde. It is also recommended that the proposed farm-out arrangement with Q is accepted, and that the offer from Q to allow 15 of its skilled production managers to work in EEE is accepted. It is further recommended that YJ should establish an apprentice scheme and should recruit graduate trainees and train them in all areas of YJ‟s operations. 6.4.2 Justification The justification for establishing a share ownership scheme is that YJ is a young and growing company which has already been granted four licences to drill and is awaiting the outcome of three more licence applications. Therefore, the company is on the edge of future high growth. YJ will only be able to exploit the opportunities if it has adequate manpower in place. YJ needs to overcome the recruitment problem for its skilled employees, as well as to trying to retain its key employees. Skilled employees in the oil and gas industry are in short supply and therefore it is important for YJ to be able to offer an attractive package, including shares, to enable it to be able to recruit the best individuals to meet YJ‟s growing needs. Even in these recessionary times where some companies do not now pay performance related pay, the oil and gas industry is extremely specialised and there is a shortage of skilled managers resulting in the need to offer attractive packages to enable YJ to recruit talented managers. The justification for accepting the offer from Q to allow 15 of its skilled production managers to work in EEE is that the newly licensed oil and gas field EEE will require a total of 30 managers, and therefore this would reduce the number of managers that YJ would need to recruit to only 15 managers.

March 2014 Page No: 16 T4 Part B Case - Answer

The justification for establishing an apprentice scheme is that the oil and gas industry is facing a shortage in skilled workforce, and therefore it is imperative to YJ‟s long term success that it retains its employees and that it grows its future management team. 6.4.3 Actions to be taken

1. YJ Board decision to proceed with establishing a share scheme.

2. YJ Board decision on establishing an apprentice scheme.

3. A framework for the share scheme would need to be established to determine how and when shares are to be awarded to managers.

4. It is recommended that a fixed percentage of YJ‟s post-tax profits each year is used to purchase shares on the open market. These shares would then be awarded to managers for free to those that met or exceeded agreed performance related targets.

5. Establish a range of performance related targets and the timescale for measuring and reporting of these targets.

6. Establish a timetable for the introduction of performance related targets and agreement with each manager of the range of targets to be met or exceeded in order to be eligible for free shares.

7.0 Conclusions YJ faces a challenging but exciting future. With the newly licensed oil and gas field EEE, the company could be significantly expanding its production output and sales revenue within the next two years. However, in order to bring EEE into production, the company faces a major cash deficit, mainly due to the current problem at CCC, which has been shut down. Therefore, for the first time in YJ‟s history it is recommended that it accepts a farm-out agreement with Q in order to generate enough cash to finance the drilling costs at EEE and also to cover the drilling costs for a new production well to bring CCC back into production. YJ also needs to change the reward structure to enable YJ to be able to retain and recruit managers in the industry.

March 2014 Page No: 17 T4 Part B Case - Answer

Appendix 1 SWOT analysis

Strengths

Experienced Board members

New CEO with a reputation for bringing new oil and gas fields into production swiftly

Good track record of bringing three of the four oil and gas fields into production, with only one unsuccessful field

Strong revenues and profits after early years of losses

Successful in winning new licences

Just been awarded one licence for EEE

Weaknesses

Lack of financing for expansion of the company

Investors not willing to invest in EEE due to current problems with CCC

Bank not willing to loan additional finance due to current problems with CCC

Current shut down of CCC in order to prevent a serious accident, resulting in a lack of cash flows from this oil and gas field

Shortage of experienced managers

Opportunities

To bring EEE oil and gas field into production

EEE is potentially a very large oil and gas field

YJ could secure funding from Q in a farm-out arrangement for EEE

YJ is waiting to hear whether it will be awarded three further licences in Asia

To identify more potential new oil and gas fields in the future

Further farm-out arrangements in the future to help finance drilling costs with other multinational oil companies

Future full stock market listing

To gain new managers by offering YJ‟s managers an employee share scheme

To establish an apprentice scheme

Threats

Shortage of cash for investment in test and production drilling at the newly licensed oil and gas field EEE and for possible new production drilling at CCC

Possible permanent closure of CCC

Threat of explosion at CCC

Shortage of skilled oil and gas manpower, which is an industry wide problem

YJ‟s inability to recruit sufficient managers to enable the company to grow

Terrorist activities

Note: The above SWOT analysis is detailed for teaching purposes. However, in exam conditions a SWOT containing fewer bullet points, which cover the main issues from the case and the unseen material, is expected.

March 2014 Page No: 18 T4 Part B Case - Answer

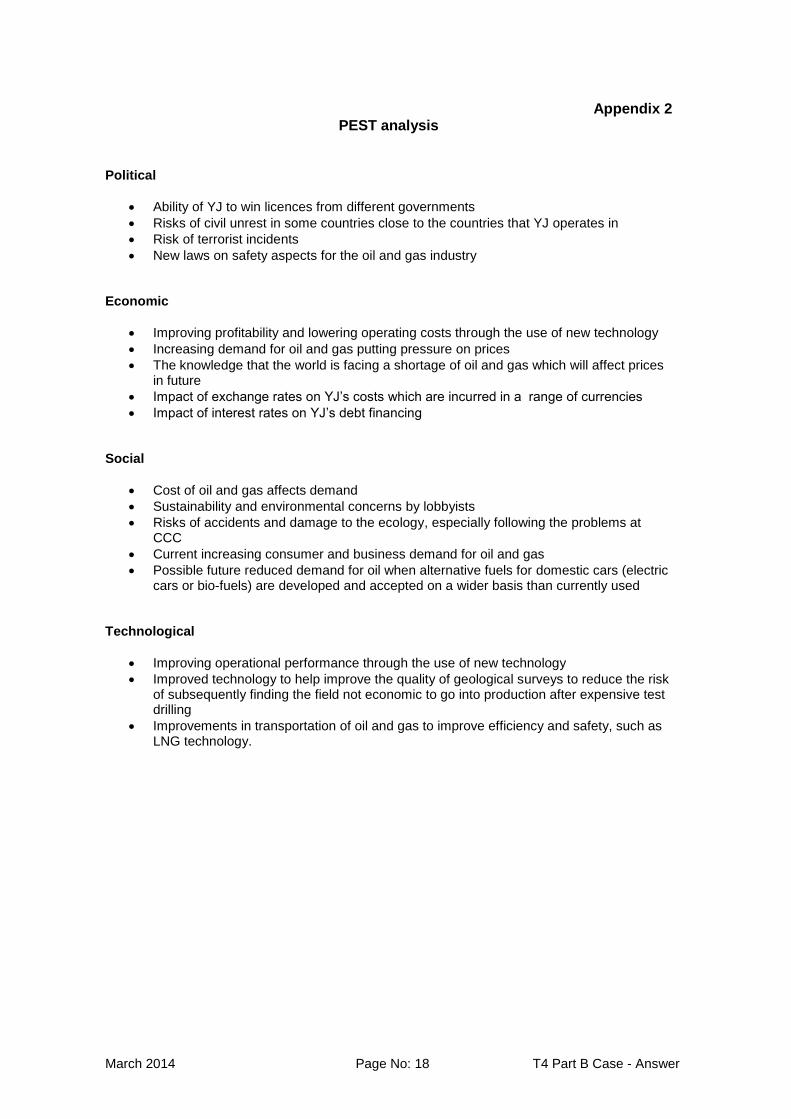

Appendix 2 PEST analysis

Political

Ability of YJ to win licences from different governments

Risks of civil unrest in some countries close to the countries that YJ operates in

Risk of terrorist incidents

New laws on safety aspects for the oil and gas industry Economic

Improving profitability and lowering operating costs through the use of new technology

Increasing demand for oil and gas putting pressure on prices

The knowledge that the world is facing a shortage of oil and gas which will affect prices in future

Impact of exchange rates on YJ‟s costs which are incurred in a range of currencies

Impact of interest rates on YJ‟s debt financing

Social

Cost of oil and gas affects demand

Sustainability and environmental concerns by lobbyists

Risks of accidents and damage to the ecology, especially following the problems at CCC

Current increasing consumer and business demand for oil and gas

Possible future reduced demand for oil when alternative fuels for domestic cars (electric cars or bio-fuels) are developed and accepted on a wider basis than currently used

Technological

Improving operational performance through the use of new technology

Improved technology to help improve the quality of geological surveys to reduce the risk of subsequently finding the field not economic to go into production after expensive test drilling

Improvements in transportation of oil and gas to improve efficiency and safety, such as LNG technology.

March 2014 Page No: 19 T4 Part B Case - Answer

Appendix 3

NPV of carrying on production at CCC

(Assuming drilling a new production well)

CCC Year 1

Years 2 - 10

Year 10

US$ million US$ million US$ million

Post-tax net cash flows (55.0) 21.0 (5.0)

DR 0.926 5.784 0.463

DCF (50.9) 121.5 (2.3)

NPV

+ 68.3

The following alternative answer, which excludes the cost of closing off existing dangerous well, would also be acceptable:

CCC Year 1

Years 2 - 10

Year 10

US$ million US$ million US$ million

Post-tax net cash flows (50.0) 21.0 (5.0)

DR 0.926 5.784 0.463

DCF (46.3) 121.5 (2.3)

NPV

+ 72.9

Note: This alternative NPV of US$ 72.9 million reflects the correct NPV of investing in a new production well as the closure costs of the existing dangerous well would need to be incurred irrespective of whether YJ were to drill a new production well or not.

March 2014 Page No: 20 T4 Part B Case - Answer

Appendix 4

Forecast costs of drilling for EEE

Costs of drilling: Cost per

No. of relevant

Per test

No. of relevant

Per production Total

day days well days well costs

US$

US$

million US$

million US$

million

H & S 10,000 183 1.83 275 2.75

Hire of drilling rig 42,000 183 7.69 275 11.55

Hire of drilling team 35,000 183 6.41 275 9.63

YJ management of drilling 700 732 0.51 2,200 1.54

YJ survey team liaison 900 366 0.33 0 0.00

Other one-off costs: Contract fees, H & S and Security 0.75 0.75

Contingency 1.50 2.80

Forecast per well 19.02 29.02

Number of wells to be drilled

2

3

Total forecast

38.04

87.06

125.10

If farm-out agreement with Q:

US $ million

US $ million

Q‟s share of drilling costs at 48%

18.26

41.79

60.05

YJ‟s share of drilling costs at 52%

19.78

45.27

65.05

March 2014 Page No: 21 T4 Part B Case - Answer

Appendix 5

YJ total cash forecast for one year period ending February 2015 on its own (without Q farm-out proposal) and with Q farm-out proposal

Cash forecast for next 12 months (1 March 2014 to 28 February 2015) On own -

Without With

Q Farm-out

Q Farm-out

US$ million US$ million

Opening cash balance 1 March 2014 25.6 25.6

Cash generated from operations with CCC shut down 52.0 52.0

Cash up-front payment from Q for farm-out agreement 0.0 75.0

Total cash available

77.6 152.6

Cash required:

EEE:

Test drilling 38.0 19.8

Production drilling 87.1 45.3

Sub-total: EEE drilling costs 125.1 65.1 CCC:

Current production well closure costs 5.0 5.0

Drilling of new production well 50.0 50.0

Other cash items:

Finance costs 15.4 15.4

Tax payable 8.1 8.1

Total cash required

203.6 143.6

Cash deficit at 28 February 2015 (126.0)

Cash surplus at 28 February 2015 9.0

March 2014 Page No: 22 T4 Part B Case - Answer

Appendix 6

Revenue valuation of EEE reserves

mmbbl mmbble

Total expected values (As per the unseen case material)

9.15

7.31

Current prices US$ per barrel 110 18

US$ million US$ million US$ million

Total Total revenue value of reserves at EEE

1,006.5 131.6 1,138.1

YJ‟s share of future revenues at 52%

591.8

Q‟s share of future revenues at 48%

546.3

Note: These values refer to revenues only and not operating profit as they do not include production costs, licence fees or amortisation of drillings costs.

March 2014 Page No: 23 T4 Part B Case - Answer

Appendix 7

Part (b) – Email to Board members on the differences between profit and cash and the significance of cash flow in the oil and gas exploration and production

industry and the merits of the farm-out proposal with Q To: YJ Board members From: Management Accountant Date: 25 February 2014 Differences between profit and cash:

1. Profit is an accounting term which takes account of sales made and revenue expenditure incurred using the accruals concept and does not include any working capital requirements or capital expenditure or reflect the timing of sales receipts.

2. Profit includes non-cash items such as depreciation and the amortisation of the capital expenditure of drilling costs.

The significance of cash flow in the oil and gas exploration and production industry:

3. In the oil and gas industry, large amounts of cash are required for exploration, surveys and drilling before any revenues can commence. It may take years from the start of cash outflows before any revenues are generated and therefore there are significant timing differences between cash flow and profit.

4. Cash is the life blood of an organisation and a small E & P company like YJ has limited

access to the large amounts of cash required to finance drilling costs on its own. Merits of the farm-out proposal with Q:

5. Shares the risk of test drilling as there is a 10% probability that EEE will not be economic to go into production.

6. Shares the cost of test and production drilling as instead of YJ having to finance total

drilling costs of US$ 125.1 million, YJ would only need to finance 52% which would be US$ 65.05 million.

7. With CCC currently shut down due to risk of explosion, additional equity or new loan

finance is not available at present.

8. The farm-out proposal gives Q 48% of all future oil and gas production and the associated profits but will allow YJ to go into production at EEE sooner.

9. Without the farm-out proposal, YJ would not be able to bring CCC back into production

as well as bringing EEE into production, as it is forecast that there would be a US$ (126.0) million cash deficit.

Recommendation:

10. It is recommended that YJ agrees to the farm-out arrangement with Q although it should try to negotiate the one-off fee upwards from US$ 75.0 million to perhaps nearer to US$ 100.0 million due to the forecast large value of the oil and gas reserves at EEE.

End of answer