table of contents (english version)

TRANSCRIPT

1

Chronicle of a Crisis Foretold:

The New Middle Class Strikes Back

Coordination: Marcelo Cortes Neri

September 16th, 2009

Version 1.0

2

TABLE OF CONTENTS (ENGLISH VERSION)

1. Introduction

2. Counter-Attack Against the Crisis

3. The Score

4. January Undertow

5. The Middle Path

6. Bibliography

3

Chronicle of a Crisis Foretold:

The New Middle Class Strikes Back

Fundação Getulio Vargas

Coordinator: Marcelo Cortes Neri

1. Introduction

The Center for Social Policies at the Getulio Vargas Foundation

(CPS/IBRE/FGV) has shown in successive studies the emergence of a new middle class

in Brazil: from 2003 to 2008, 27 million people have ascended to classes ABC. After

the external crisis hit Brazil in September 2008, our studies chronicled the crisis,

inquiring about the evolution of recently acquired living standards during this critical

period. The new Brazilian middle class became a macroeconomic asset to make up for a

decrease in exports as a result of the global economic retraction. With data that goes up

to July 2009, we continue monitoring the evolution in the population composition in its

various economic strata (ie., classes E, D, C and AB) as well as its close determinants

such as income inequality and mobility and its respective labor-related components.

A Social Draw – Nine months after the crisis began, there is a clearer vision of its

effects on Brazilians in the six largest metropolises. Income inequality - that had

undergone a serious deterioration when part of the previous years’ gains were lost in

January alone – has come back to the same pre-crisis’ levels. Even class AB that earns

more than 4800 reais per month and had lost more with the crisis (-2,7% in January),

today is only 0,5% below the level one year ago (14,97% of the population is in class

AB, with almost 55% of the income). Class C has a positive result with a gain of 2,5%

in 12 months (the prevalent class in terms of population size: 53,2%). If this draw may

be considered a good results in times of crisis, it also hides a sudden halt in the previous

improvement in indicators: from July 2003 to July 2008, Class AB grew 35,7%, class C

increased 23,1% and income inequality decreased as never before in the Brazilian

statistical series.

New Agenda – In the same way as we updated our traditional series, we have

introduced some innovations. Our strategy has that we shall strive to introduce a new

4

dimension to the analysis of the middle-class at each research update: access to

consumer goods, entrepreneurship and microcredit, quality education, among others;

exploring a new perspective with each research. In the present research, following the

impacts from the financial bubble burst, we explore the demand for insurance by the

low-income population and by the groups that recently emerged to new economic

classes. Micro-insurance as an agenda only now emerges in the world, just as

microcredit had done in the last two decades. They are natural sequences of the same

process; as microcredit enables an improvement in people’s lives, micro-insurance helps

decrease people’s vulnerability to adverse shocks such as unemployment, disease,

accident, theft, death, among others. During last years’ improved income distribution,

we have handed out the poor population to consumer markets. Now we aim to hand the

market out to poor producers as we explore the entrepreneurship and productive credit

agendas as in previous researches, as the quality education agenda in the next

researches, and in the current demand for micro-insurance. Placing low-income people

as agents of change in their lives, integrating social and economic aspects and exploring

public-private interactions form the new generation of social policies for the next

decade.

Work plan: this study presents new data on the evolution of inequality and poverty

rates and economic classes in Brazil and the mobility of Brazilian income until July

2009. We also present a short compilation of the studies produced this year about the

impacts of the crisis on the income of Brazilians, its causes and the debate on public

policy propositions.

5

The research website www.fgv.br/cps/contraataque provides a large data bank with

user-friendly and interactive search tools. You will be able to assess the evolution of

economic classes in the six main metropolitan regions in the country, acquiring a

detailed vision of the mobility between different income classes through longitudinal

data following the same people through time. As it relies on information updated till

July 2009, it is possible to capture the impacts of the crisis. The analysis ranges from

the evolution of economic classes in Brazil through to a detailed decomposition of

income mobility.

6

2. Counter-Attack Against the Crisis

President Lula recently said that Brazil is doing relatively well despite the crisis

even before he called up “Pelé to play”. In his analogy, Pele would be the reduction of

Selic, the basic interest rate of the economy and reduction in bank spreads. We focus

here on the importance of summoning another greater player, good and old Tostão (he

played alongside Pelé in the Brazil national team during the 1970s World Cup). Tostão

literally means in Portuguese “a small coin like a Dime or a Shilling”. In this sense,

direct income transfer to the poor. Family Grant reaches the lower income groups that

consume a good share of the resources, which is a double-effect measure: it is good in

equity terms and in terms of heating the aggregate demand, apart from facilitating

monetary transactions in remote places, neutralizing in part the credit crunch that affects

the sophisticated parts of the system. That is: Tostao is good on his own, playing on the

left, but makes a great pair with Pele.

In truth, based on above arguments we may list eleven factors that may cushion

the impacts of external crisis in Brazil and some related risks. In the football analogy,

these would be the best players to be called up to the Brazilian Team.

Defensive and Offensive Attack Instruments:

1. High international reserves

2. Fiscal Policy

• Established fiscal responsibility

• High tax load (may fall, e.g. car tax)

RISK: quantitative and qualitative lack of control of public accounts.

There has to be a selection of the best income sources from the

efficiency point of view and from impact on demand. They must go

hand in hand.

3. Monetary policy

• High interest rates (may fall)

• High Spreads may fall)

• High compulsory deposits (may fall)

• competition instrument for public banks interest rates

• Salary-bound credit (pensions in a high, and frontier of

remaining benefits

7

4. Financial system

• Regulated and healed private banking system (Proer

program in the late 1990s heed that)

• Strong public banks presence - established and healed

(developed countries began to nationalize banks where

governance is not well established)

5. Very closed economy (still reducing the impacts of shocks)

6. Food exporter (Foreigners will not reduce as much the purchases

of staple items during a recession)

7. Good demography (the share of adult young workers is high)

8. Brazilians' adaptability to crises (Brazilians ared used to it!)

9. Social safety nets

• Family Grant (Ex: food crisis led to increase in benefits

and now an increase of 17 reais per capita in the elegibility

criteria)

• Public pensions linked to the Minimum Wage

(Readjustment of the minimum wage in 2009 of 6,5% real on

the basis of the dsitribution and close to zero for the

remaining pensionners)

RISK: besides those above, there is the issue of permanence. Today

we need to generate more aggregate demand to back up higher

private spending, but in a more transitory fashion. We are presently

all Keynesian now, but we should emphasize the importance of using

the right instruments to each context (fine tuning)

10. Booming Domestic market

11. Public Investments

PAC has a double function of improving the logistics in the country but at the

same time enhancing public demand in the system. A sort of new deal made in Brazil

conceived when the crisis had not appeared in the economists' radar.

Just as in times of World Cups, 180 million Brazilians become aspiring football

managers with possible solutions for the team’s victory, during the crisis we all become

experts in economics. Therefore, to build a list of 11 players always leave room for

discussion. There is no equivalent to the Washington Consensus. It is always risky to

8

disagree with the president, the late Joao Saldanha (the coach of the great 1970 World

Cup team) would say it, but for me the real Pelé, our number 10 player in the Brazilian

team, is the high domestic market, in a double act with Tostão, as the Family grant,

whose resources will be entirely used in the consuming market. This is the double act

that will meet our hunger for goals.

More than just calling up the good players, it is necessary to acknowledge those

who are already in the pitch and can play better, more in tune with the crisis. We still

have to avoid taking for granted certain aspects (remember the 1966 fiascos even with

Pele and Garrincha n the field) but we need above all to adopt a tactical system that

favours the potential of the Brazilian talents ensemble. In the same way as ten years ago

we created the magical tripod in macroeconomy: inflation tagets, fluctuating exchange

rate and fiscal responsibility - which are the basis of our macroeconomic defense - we

also have interesting isolated innovations in the social areas that can be integrated into a

sole tripod, namely: family grant, PAC and actions of access to markets for poor

producers. In the integration of these isolated advances, and with a macroeconomic

defense against the crisis is that we have the most expected returns. The Family Grant

(Bolsa-Familia) has created a platform of service delivery to the poorestthat talt can and

probably will make the difference now. The Family Grant leads the poor to

consumption markets, which is not wrong but it is necessary to go further: give the

market to the poor. In terms of creating the exit door out of the Family Grant it is worth

noting that it may be more constructive to emphasize entry doors to the markets. The

poor do not have to be protected from the market, but to be integrated into it through

educational measures, microcredit, microinsurance and marketing of their products and

services. There are some successful experiences of microcredit in Brazil, in particular

CrediAmigo from Banco do Nordeste, which is not widely known despite reaching 2/3

of the Brazilian microcredit market and increasing the productor's family consumption

in 28% with less than 1% default rate without incurring in public subsidies. CrediAmigo

was ellected in 2008 as the best microcredit experience in Latin America by IADB

(Inter-American Development Bank). We have defended the use of family grants as a

collateral for credit since the 2002 World Cup (This scheme was later adopted in

consignation of public pensions and terired benefits consignation). We are treading new

ways in this integration of microcredit with the Family Grant platform. President Lula

should call it up to play.

9

Strategic work to enhance the poor groups access to markets is in its embryo

phase in Brazil given ideological obstacles, but it gains exceptional relevance in the

current time of demand shortage and countercyclical policies. In particular, there lacks a

clear vision about two questions: 1) changes in the economy, who loses, who gains,

demand as a result of the crisis and actions against it (expanding family grant,

readjusting minimum wage, etc.). 2) lack of policies that allow producers to find their

demand niches. Not only studying what creates demand, but how supply meets the new

demand is necessary. In short, the injection of the necessary demand is the key point in

the Brazilian society now but we may be looking at things at an aggregate way (without

seeing the details of the emerging and sub-emerging groups) while looking at producers

in a passive way (the rationale is not only to lead people to the market, consumers and

credit, but deliver the market to the producers).

It is still necessary to integrate the social agenda into a scheme that works harder for

the equality of opportunities (people's assets) and less for immediate results (e.g.

income). Observe, once more, that we are not talking much about leading the poor to the

consuming markets, but of delivering the consumer markets to excluded producers,

giving the markets to producers, for instance through a policy of commercialization, or

microcredit, targeting the low income producer - but, above all, by virtue of education

of quality for all. This process calls for the creation of integrated actions in the long

term. That magical tripod in the social area above mentioned is an essential part of the

tactical scheme to be implemented to fight the external crisis.

3. The Score

Economic Classes and the Demand for Protection

Traditionally, sociological studies and more recently Thomas Friedman’s work

have alleged that being middle-class does not depend to a certain extent on the person’s

current situation but relies more on his hoping for a future social rise. More than being

in a certain situation, the essential characteristic of a new middle class would be to have

a plan of upward mobility. This perspective mirrors the entrepreneurship rationale,

whereby a person rises in life on account of his efforts and productive potential. In this

sense, in order to identify emerging producers among the population it would be

necessary to separate the subsistence production at any level from activities with a

capital accumulation and growth potential. We argue here that this kind of approach is

10

relatively less present in Brazil than in other countries such as the United States, or even

India. In India, establishing an IT shop in Bangalore permeates people’s plans (at least

of those people who say that they want to be a millionaire). In the current view in

Brazil, the new middle-class also relates to the future, but Brazilians not only basically

plan their rise, they also focus on avoiding a social downward movement. That is, new

emergent classes wish above all not to recede to their previous status in the future.

Brazilians aim for greater security by being formally employed with the employment

registration booklet (carteira de trabalho) or preferably through public service or even

under the protection of state-sponsored social programs. Brazilians demand and receive

State protection in larger proportions than Indian or Chinese people.

Furthermore, doesn’t the Brazilian State already meet the demand for protection

through social insurance? The problem of the State, contrary to George Orwell’s Big

Brother, is that it does not have eyes everywhere, and there are risks that only someone

at risk may notice. The present study finds itself in the arena of the supply and demand

for protection in this public-private interaction that has characterized the Brazilian

situation in the last years. Brazil has reconciled a respect to market rules with an active

social policy. For over a decade, the Brasília Consensus has not been the same as that of

Washington or Caracas. We tread a sort of Middle Path, not so much to the State nor to

the market. A true market social economy.

There are many possible perspectives to help define the middle-class, including

supply and demand elements. The first aspect looks at the individual as an income

generator, particularly through income from his work. This type of concern leads to

class criteria such as inclusion in the labor market and education, as applied in England,

Portugal and India. We have used this approach given the large data availability in

frequent surveys such as PNAD (household survey) on an annual basis or the PME on a

monthly basis. Besides measuring the evolution of the new middle class in Brazil from

the producer’s point of view, we may define E, D, C, B and A economic classes for

their consumption potential. The so-called Brazil Criterion uses access to and number of

durable goods (TV sets, radio, washing machines, fridges and freezer, VCR or DVD

player), bathroom, as well as hiring a housekeeper and the level of education of the

household head. This criterion estimates the weights based on a Mincerian income

equation. Since Robert Hall’s 1977 seminal work, we have known that current

11

consumption levels ideally contain all the relevant information about future

consumption patterns.

A more general methodology could also combine both above mentioned aspects

including other symbols of middle-class, such as the employment registration booklet

(carteira de trabalho), entering university or entering the digital age through the

internet. Social status aspects related to the private demand for goods, that were

previously a monopoly of the State, such as social security, education, health and

housing credit could also be included here. The composition of these expenses is also

important, thus the need to separate hedonism from productive capacity to a certain

level of people’s expenses. According to La Fontaine’s fable, one has to distinguish

between the productive ants and the consumer grasshoppers. In other words, we

approach the demand for insurance by different economic classes – which, at the base of

the income distribution pyramid, give origin to the micro-insurance industry that begins

to flourish in some parts of Brazil. Another objective of the present work is to update

the economic classes series based on income (E, D, C and AB) and its close

determinants including income inequality and its labor-related components.

Aggregate Movement of Economic Classes

The main feature of the approach used here is its level of disaggregration in four

income groups. We look at the evolution of the participation of the population in each

class. Making a long story short (described below) in objective numbers, we have next

the limits of the economic classes measured in terms of total household income from all

sources per month1:

1 Values are calculated based on household per capita income. When applied to the PME compatible with the income from work for the population 15 to 60 years old.

12

Definition of Economic Classes

We have extended here the period of analysis of the previous researches until

July 2009, highlighting the same month in all years in order to deal with seasonal

fluctuations within the years. We also present the values of the period after the worse

moment of the crisis, from September 2008, with an emphasis on the following months,

until July 2009, the period of this research.

Class C is the most numerous, with half of the population (53,2%), although

from an income point of view, AB is the dominating class, where 14,97% of the

population own almost 55% of income. We present in the table below the distribution

across different layers since 2002:

Source: CPS/FGV based on PME/IBGE microdata

13

We open data from the above table into two variations that cover the pre- and

post-crisis periods, according to the graphs below. Temporal comparisons point to a

growth in class C, that is in its record rate in July 2009, when compared to the same

month in each year since 2002 (or 1992 by PNAD). Classes D and E are also at their

lowest levels in July in the PME series. Class AB is also a bit smaller (-0,5%) in 2009 in

relation to the same month last year.

Variation of Economic Classes Pre and Post-crisis

Source: CPS/FGV based on PME/IBGE microdata

Next, we open the post-crisis period in terms of variations. In the immediate

post-crisis period, from September to December 2008, we did not see any qualitative

change in this scenario except for the small accumulated reduction of -0,6% in class AB

(that represented a sudden halt because, as we saw previously, such class had been

growing more than others). The dynamics of the remaining classes were maintained:

class C keeps growing, at 1.2% in the period, and classes D and E keep their decreasing

trend, -2,5% and -1,2%, respectively in the period.

14

Variation of Economic Classes - Post-crisis

Source: CPS/FGV based on PME/IBGE microdata

In January, we observed a strong reversion of the previous trend, with a

retraction of the highest classes: class AB drops -2,7% and class C – which had been

growing – decreases -2,2%. In January alone, around 760 thousand people from classes

AB and C return to classes D and E. On the other hand, classes D and E increase 3,03%

and 6,73% in one month. That is, all the observed trends get inverted as if bouncing off

a solid object. January appears as the critical point in terms of the transition in the

composition of economic classes. Crisis starts in stock markets abroad and hits ordinary

citizens in the country in the first month of the year.

From February to April, there is a similar profile to the period from September

to December 2008, as Class AB keeps decreasing discreetly. As a result of the turn of

the year’s event, the accumulated trend of the post-crisis becomes a crisis scenario as

people get displaced from higher to lower classes.

15

Description of the Databases: PME

The Brazilian Institute of Geography and Statistics (IBGE) implemented the Monthly Employment Survey (PME) in 1980. PME is a monthly survey about workforce and work earnings, and includes the six main metropolitan areas in Brazil: Belo Horizonte, Porto Alegre, Recife, Rio de Janeiro, Salvador and São Paulo.

PME is a panel survey and replicates the US’s Current Population Survey aiming to collect information from the same household eight times during a 16-month period. It is carried out on a rotating basis through monthly interviews with families during 4 consecutive months, withdrawing them from the sample during eight months and then interviewing them again for four more months. Between 4500 and 7500 families are interviewed per month in each of the six metropolitan areas, totaling approximately 35000 families. In August 1988, the size of the sample was reduced to around 30000 families per month. PME’s longitudinal aspect – that is, it follows the same people through time – enables the analysis of the individual occupational and income risk. Since the start of the PME, there have been changes in the survey aiming to better capture the characteristics of the population in working active age and their inclusion in the productive system. Themes have become wider encompassing the short-term effects and changes in the labor market. General questions about demography and work are the same since February 1982.

The availability of monthly information based on the Monthly Employment

Survey (PME) would allow us to work with annual averages, avoiding seasonal problems, besides allowing a detailed analysis of the process dynamics. PME’s main restriction lies in the breadth of its income concept, once it only considers income from work.

Through PME, like PNAD, we may analyze the evolution of income and the composition of population groups with the advantage of being a monthly activity, thus becoming an important monitoring tool.

A 360o Revolution

The graph shows that in the pre-crisis period, last years’ trends were inverted:

classes that had earned greater participation began to lose more and vice-versa. In the

pre-crisis period, upper income strata increase and so does the room of more poor

people: the accumulated increase since July 2003 until July 2008 of classes AB and C

was 35,7% and 23,1% respectively, with an equivalent reduction in the participation of

classes D and E, of -15,5% and -37%. Next, when considering the period up to 2009,

including the post-crisis period (September 2008 to July 2009), observed an

accumulated decrease in class AB (-0,5%) followed by a slight increase in class C

(2,5%) and a reduction in class D (-4,1% in the period). Class E (-3,3%) is more

constant. We may call the liquid result of these movements a”360 revolution.

In aggregate terms, if we calculate the income variations in the last years (all the

series until July 2009) we see that there has been an improvement in Brazilians’

16

purchasing power in large metropolises: the accumulated increase since July 2003 of

classes AB and C was 35% and 25% respectively, with the corresponding reduction in

the participation of classes D and E of -19% and -39%. This displacement, that moves

masses of people from the base to the peak of the distribution of income, was

proportionally stronger at the extremes of the distribution with an emphasis on the

greater relative growth of classes in relation to class C – for the new emerging middle

class and for the reduction in Class E, the poorest.

PME and the Recent Evolution of Living conditions The tradition among research institutes like IBGE is to use data from the Monthly Employment Survey on individual levels, and not at the household level. Typically, processing indicators such as unemployment rate, formality and average income from work. Nevertheless, PME is a household survey comparable to the National Household Sample Survey PNAD and may be used as such. This point deserves attention, as the evaluation of the socioeconomic conditions must consider the process of resources division within households. For instance, the fact that the income of an adult worker may benefit other members of his family, like children. Or being benefited by the spouse’s income, which offers a social insurance of a family nature. In this sense, the most adequate concept to assess the poverty level would be the household per capita income of individuals, which corresponds to the sum of income of all people in the households divided by the total number of members. Likewise, when we want to quantify the extension of the middle class in order, for instance, to assess the power to purchase family goods, such as homes, the adequate concept is the total income received by all household members. Both concepts sum up a series of factors operating on family members, such as level of occupation and revenue, received formally or informally, but whose effects are shared or added by the total number of members. The main issue here is to improve the monitoring of the living conditions of the Brazilian population. How do we assess the social and economic performance by using only the PNAD/IBGE, whose data is on average 18 months late in relation to the time of the collection? For instance, today there has been 22 months since the last national snapshot taken based on PNAD. PNAD went to the field in the first week of October 2008 and will become known only in September 2009, when the crisis’s effects would be at their peak and data collection will happen in prosperous times.

The increase in speed is a necessary requisite to help design an operational monitoring system and evaluation of social targets. This includes both managerial systems within public administrations, as well as monitoring income fluctuations for each group of society. For companies that want to adjust to the business cycle fluctuations in order to adjust their production and to niche their demand, the urgency is no smaller. As a result of these needs, we suggest using the PME microdata which, thanks to its agile timing, helps to diminish PNAD’s lag of one and a half year to a bit more than a month and a half (NERI; CONSIDERA,1996).

Below, we present graphs with the complete monthly series since March 2002

for each economic class. Each graph contains levels followed by another with the

respective mobile averages.

17

Evolution of Class E – Moving Average

Population 15 to 60 years old

Household Per Capita Income from Work

Source: CPS/FGV based on PME/IBGE microdata

Evolution of Class D Population 15 to 60 years old

Household Per Capita Income from Work –

Evolution of Class E Population 15 to 60 years old

Household Per Capita Income from Work

18

Source: CPS/FGV based on PME/IBGE microdata

Evolution of Class C Population 15 to 60 years old

Household per Capita Income from Work

Evolution of Class D – 12-Month Moving Average Population 15 to 60 years old

Household Per Capita Income from Work

19

Source: CPS/FGV based on PME/IBGE microdata

Evolution of Class AB Population 15 to 60 years old

Household per Capita Income from Work

Evolution of Class C – 12-Month Moving Average Population 15 to 60 years old

Household per Capita Income from Work

20

Source: CPS/FGV based on PME/IBGE microdata

Evolution of Class ABC Population 15 to 60 years old

Household per Capita Income from Work

Evolution of Class AB – 12-Month Moving Average Population 15 to 60 years old

Household per Capita Income from Work

21

Source: CPS/FGV based on PME/IBGE microdata

PME on a weekly basis

In this section, we open the monthly survey in weekly bases to better trace the

weekly chronology of the crisis, until the last week of July 2009. Illustratively, it refers

to the mobile average of four weeks concerning the participation of extreme classes in

our spectrum of economic strata, that is, classes E and AB through the last 17 months.

We focus the analysis on the last point in the series, the last week in July as an

antecedent (unbiased) indicator of the future trend. By comparing the last point in the

series (in the graphs below), we notice that class E has remained stable (18,3% reflects

Evolution of Class AB – 12-Month Moving Average Population 15 to 60 years old

Household per Capita Income from Work

22

the whole month) but Class AB would keep its decreasing trend at a slower pace

(13,9%, 1 percentage point below the monthly average) according to this criterion.

Evolution of Class E – Moving Average 4 weeks

Population 15 to 60 years old

Household per capita income from work -

Habitual

Evolution of Class AB – Moving Average 4 weeks

Population 15 to 60 years old

Household per capita income from work - Habitual

Inequality

23

Income inequality, that underwent a strong deterioration with its increase in

January that compromised last years ’improvements, came back to the pre-crises’ levels

in July: Gini index of household per capita income from work is 0,5815 in the last

month, just 0,3% above the index a year before, hence prior to the crisis.

Theil’s Inequality Index, which is more sensitive to changes at the bottom of the

distribution, shows a similar movement, with increases at the beginning of the year that

are being reverted now. Despite that, in July 2009, levels are still higher (0,6807) to the

pre-crisis period in July 2008 (0,6688).

We present monthly series of the Gini and Theil-T indexes adopting the

individual and per capita concepts.

Source: CPS/FGV based on PME/IBGE microdata

Next: variation data for the many concepts in the previous table. The widest

concepts that include null incomes tend to present a result close to the null variation by

comparing July in both years, while those partial concepts tend to show an

improvement, for not capturing the effects of adverse changes in the occupation and

unemployment.

24

Source: CPS/FGV based on PME/IBGE microdata

Graphs below illustrate variations from July 2003 to July 2008 and from this

month until July 2009 for the concept of household per capita income, including null

values.

Source: CPS/FGV based on PME/IBGE microdata

The next graph opens last year into sub-periods, identifying the strong

deterioration in January followed by a movement in the contrary direction to the

following six months.

25

Source: CPS/FGV based on PME/IBGE microdata

When analyzing the graphs of mobile averages, we clearly observe an influence

of the result from the beginning of the year, showing a decrease observed since the

series started – a result that has been reverted in the last months, according to the series

below.

Source: CPS/FGV based on PME/IBGE microdata

26

Source: CPS/FGV based on PME/IBGE microdata

Source: CPS/FGV based on PME/IBGE microdata

27

Source: CPS/FGV based on PME/IBGE microdata

Income Risk

PME uses a rotating panel methodology that seeks to collect information in the

same households in the months t, t+1, t+2, t+3, t+12, t+13, t+14, t+15, in a total of 8

interviews through a period of 16 months. The initial approach used here consists of

calculating the probability of transitions into and out of the four groups in society, and

the non-transition between these groups, between pairs of observation of the same

people in periods 12-months apart, starting March 2002. The last of the groups analyzed

begins in December 2007 and end in January 2008. The longitudinal aspect of the

household per capita income from work data will give us the basic empirical evidence

about the social mobility pattern observed in practice.

We open the destinations of the transitions from each economic class per year.

In the last line of the table, we present 2008 and 2009 information, available until July,

which could be a way to measure the possible impacts of the crisis on the transitions

among classes. Data show that years 2004 and 2008 stand out in the statistics, with just

59,5% and 59,91% of class E that remains class E, one year after the first observation

(collected in 2003 and 2007, respectively). If we look at what happened in the first

month in 2009 in view of the same period one year before, there was an increase of 0

percentage point in the number of people who remained class E (60,67%).

28

Source: CPS/FGV based on PME/IBGE microdata

Generally, the year 2008 stood out for the transitions from class E towards

classes D and C; the relative presence of transitions in relation to the class, following

the same person during a year. When analyzing the extreme opposite, those who

remained in class AB began to show negative growth in 2008 and 2009, as measured

until June. It had grown strongly and begins to lose ground in relative and absolute

terms.

Source: CPS/FGV based on PME/IBGE microdata

Was AB initially

*until July 2009

Matrix of transition of class AB 6 Main metropolitan regions

Per capita income from work - 15 to 60 years old (PIA) Mobility Annual

Final Period (1 year later) Class E Class D Class C Class AB

Pe río d o I n ic ia l 2002 8.50 1.15 25.47 64.88 2003 5.38 0.75 20.21 73.66 2004 2.77 0.47 17.06 79.70 2005 3.16 0.47 16.26 80.11 2006 2.96 0.39 14.32 82.34 2007 3.20 0.43 16.93 79.44 2008* 4.02 0.45 20.65 74.88

Was initially class E

*until July 2009

Matrix of Transition of Class E 6 Main Metropolitan Regions

Per capita income from work Habitual - 15 to 60 years old (PIA) Mobility Annual

Final Period (1 year later) Class E Class D Class C Class AB

Pe r í o d o I n i c i a l 2002 61.47 16.80 18.18 3.55

2003 59.50 18.64 18.34 3.522004 61.16 19.07 17.12 2.652005 64.10 18.00 16.07 1.832006 63.31 18.48 16.12 2.092007 59.91 17.60 19.00 3.49

2008* 60.67 17.35 18.97 3.01

29

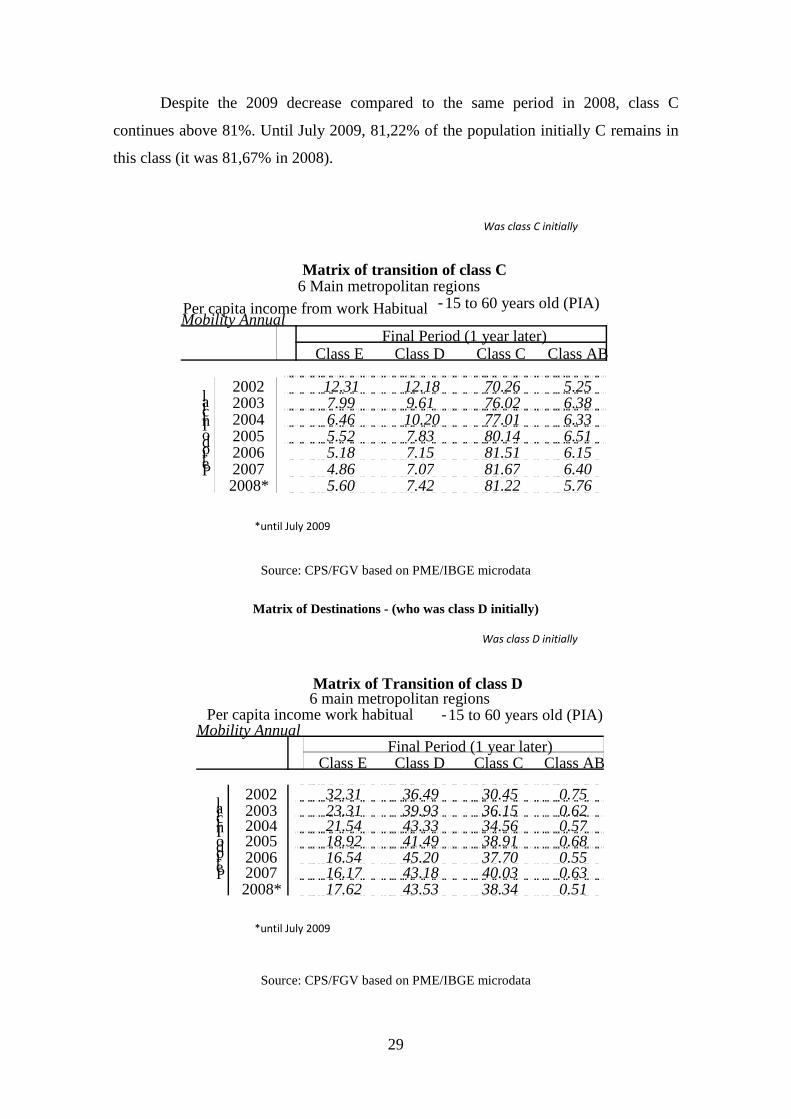

Despite the 2009 decrease compared to the same period in 2008, class C

continues above 81%. Until July 2009, 81,22% of the population initially C remains in

this class (it was 81,67% in 2008).

Source: CPS/FGV based on PME/IBGE microdata

Matrix of Destinations - (who was class D initially)

Source: CPS/FGV based on PME/IBGE microdata

Was class D initially

*until July 2009

Matrix of Transition of class D 6 main metropolitan regions

Per capita income work habitual - 15 to 60 years old (PIA) Mobility Annual

Final Period (1 year later) Class E Class D Class C Class AB

P e r í o d o I n i c i a l 2002 32.31 36.49 30.45 0.75 2003 23.31 39.93 36.15 0.62 2004 21.54 43.33 34.56 0.57 2005 18.92 41.49 38.91 0.68 2006 16.54 45.20 37.70 0.55 2007 16.17 43.18 40.03 0.63 2008* 17.62 43.53 38.34 0.51

Was class C initially

*until July 2009

Matrix of transition of class C 6 Main metropolitan regions

Per capita income from work Habitual - 15 to 60 years old (PIA) Mobility Annual

Final Period (1 year later)Class E Class D Class C Class AB

P e r í o d o I n i c i a l 2002 12.31 12.18 70.26 5.25 2003 7.99 9.61 76.02 6.38 2004 6.46 10.20 77.01 6.33 2005 5.52 7.83 80.14 6.51 2006 5.18 7.15 81.51 6.15 2007 4.86 7.07 81.67 6.40 2008* 5.60 7.42 81.22 5.76

30

We analyze here the transitions into and out of the four income groups. The

reader may analyze changes in social classes in pre- and post-crisis periods through the

previous matrices or by different socio-demographic groups, in the Social Mobility

Panorama available on the research website.

Mobility Panorama: On our research, there is a social mobility panorama through which it is possible to obtain the proportion of individuals that enter and leave each economic class, by different socio-economic characteristics. The information in the table tells the probabilities of transitions. For that, pick a period (annual or crisis) and the initial class for analysis. To compare more than one period, press Ctrl

Regional Changes

We present next the evolution of class ABC in the main Brazilian metropolises.

As we could observe, when considering the period in the last seven years, all

metropolises present an accumulated growth in rate. Generally, Sao Paulo Metropolitan

area has the best indexes in all years, reaching in July 2009, 73% in population ABC.

Between July 2007 and 2008, growth reached 5,3% in one year, and remained stable

now in the last year (July 2009). In the meantime, Belo Horizonte metropolitan area

presents the best relative performance, gaining new positions in the rankings of class

ABC. Third in class size, accumulated growth was 52,5% since 2003 (3,94% in the last

year), reaching in July 2009, 70,7% of the population in this group. In the remaining

regions, we see Porto Alegre that continues second in the ranking, with 71,1% of the

population in class ABC in the last month (growth of 2,64% between 2008 and 2009).

Rio de Janeiro with 66,98% in July grow 2,76% in the last year. Next, Salvador and

Recife are in the two last places respectively with 61,2% and 47,8% despite the good

performance (over 50% growth in seven years). In the presentation (attached) it is

possible to find the same regional tables for the remaining income classes.

31

32

33

The Brazilian Dream Even before the discussion about who is the new Brazilian middle class came up, an FGV study had planned to launch a subjective measure of the middle class. Middle class would be a state of mind in which life is expected to improve in the future. We have shown in the research entitled “Jovens, Educação, Trabalho e o Índice de Felicidade Futura” that, among 132 countries, Brazilians present the highest expectations of happiness for 5 years into the future. In a scale from 0 to 10 reported directly by the interviewees, the average grade for satisfaction with life in 2011 was 8,78 in Brazil, surpassing the United States (9th place in the ranking) and Denmark, the world leader of current happiness, but the 3rd one in terms of future happiness. The worst in this ranking is Zimbabwe.

Source: CPS/FGV based on the Gallup World Poll 2006 – IADB Project

Source: CPS/FGV processed the Gallup World Poll 2006 microdatta – in an FGV project for the IADB

N o t a Mé d i a d e

F e l ic i d a d e F u t u r a

d o s jo v e n s (

d e 0

a 1 0 , d a q u i a

5 a n o s ) 4 . 5

- 6 , 56 . 5

- 7 . 5

7 . 5 - 8 . 5

8 . 5 - 9

9 - 1 0 N o D a t a

FUTURE HAPPINES YOUNG PEOPLE FROM 15 TO 29 YEARS OLD

zimbabwe 4,04cambodia 4,86paraguay 5,04haiti 5,10bulgaria 5,13ethiopia 5,22uganda 5,31

Future

Future Happiness (Five years )

Total population

–

Menos

Future

brazil 8,78venezuela 8,52denmark 8,51ireland 8,32jamaica 8,25canada 8,14

Future Happiness (Five years) total Population

–

Mais

34

The research website www.fgv.br/cps/crisis offers a wide data bank where the

user may explore the extension of groups as the mobility between them, open by a wide

range of socio-economic attributes (gender, race, etc.) labor (formally employed,

education) and spatial (location) aspects. The databank allows each one to see the

average path of people with the same features, in a kind of recent hindsight. We present

in the end, three appendices with the analysis of aspects from this databank. In the first,

we make a profile of the middle class by their main socio-demographic attributes. In the

second, we compare the evolution of the middle class and poverty for each metropolitan

area. In the third we present estimated statistical models for simulators:

www.fgv.br/cps/crisis

35

36

4. January Undertow

January subverted the trends of the last five years: those economic classes who had

increased their participation began to lose more and vice versa.

In the last few weeks, we heard about the GDP contraction of 10 percentage

points between the third and fourth trimester in 2008 (6,3% to -3,6%), a loss equivalent

to the Chinese-like rate of growth observed during the economic boom. Manufacture

and formal employment data from CAGED also indicate a sudden halt in the Brazilian

economy (tsunami). Nonetheless, trade and services data point only to a modest

contraction (smaller wave). There is a marked dichotomy in the growth paths among the

segments more or less connected with the globalized world, more or less formal, and

with larger or smaller incomes.

The problem, for the analysts, is that the multiple shocks have, in different

moments, hit different databases, released with different time lags. To make matters

worse, each database emphasizes different parts of a given diverse and unequal society,

like Brazils. IBGE’s PME (employment monthly survey) provides an overview of the

different outlooks in the major Brazilian cities. We noticed that, in the immediate post-

crisis period, despite the spectacular fluctuations in financial markets, Brazilian

metropolitan workers experienced a relative calm in their accounts on the whole, in

particular those with a smaller income.

January subverted the trends of the last five years: those classes that had gained

more participation began to lose more, and vice-versa. The income variations in the five

years pre-crisis reveal a strong improvement in the purchasing power of the Brazilians

living in big metropolises, as higher income groups grow and poorest ones diminish: the

accumulated growth since February 2003 in classes AB and C was 35% and 25%,

respectively, with a reduction in the participation of classes D and E of -15,9% and

40,3%. If we consider the pre-period crisis, after 2004, the growth in classes AB and C

was even bigger, 43% and 26%.

In the immediate post-crisis period, or September to December 2008, we did not

observe a qualitative change in the Picture, except for the small accumulated reduction

of -0,6% in class AB (which is a sudden halt because, as we saw before, class AB was

growing more than others), but with the maintenance of the movement of other classes:

37

class C kept growing at 1.2% in the period, and classes D and E kept their decreasing

trend, -2,5% and -1,2% respectively, in this period.

Following a chronological sequence to the analysis of the crisis period, as we

isolate January, we notice a strong reversion of the previous trend with the retraction of

the higher strata: class AB falls -2,74%, class C (which had been untouched by this fall,

but had grown), falls -2,17%. This decreased is matched by an increase in the lower

segments of the income distribution, classes D and E (which had been falling) grow

3,03% and 6,73% in January alone. That is, all the observed trends inverted the previous

trends, as if they had bounced off from a solid object.

JANUARY UNDERTOW

Obs: accumulated and monthly variation coincides in this case

February, the last month in this series, shows a similar profile to the period

September to December 2008, with a continuous slight fall in class AB. As a result of

the turn of the year events, the accumulated post-crisis trend becomes a crisis situation

with a displacement of people from higher to lower income groups. Taking the period

from September 2008 to February 2009, the accumulated decrease in class AB was

3,8%, followed by a decrease of 0,9% in class C, and a consequent growth in classes D

(1,1%) and E (5,1%).

If we calculate the income variations in February in the last five years up to

February 2009, there was an improvement in the purchasing power of Brazilian citizens

living in big metropolises: the accumulated increase since February 2004 was 39,7%

and 25%, respectively, in classes AB and C, with a reduction of -18,2% e -38,4% in the

Distribution of Economic Classes - Accumula te d Vari ation (%)

S ource: CPS/FGV base d on PME m icrodata/IBGE

Dec 2008 a Jan 2009

-2.7

%

-2.2

%

3.0

%

6.7

%

Class AB Class C Class D Class E

C la ss A B C lass C C lass D C la ss E

38

participation of classes D and E. This movement, which places low-income people at

the top of the income distribution, was proportionally stronger at the extreme points of

the income distribution pyramid, with a relatively stronger growth of classes AB than

class C - the new middle class - and a reduction in the class E, i.e. the poorest one.

LAST FIVE YEARS, EVEN WITH CRISIS

Distribution of Economic Classes - Accumulated Vari ation (%)

Source: CPS/FGV based on PME microdata/IBGE

Feb 2004 a Feb 2009

39.7

%

25.0

%

-18.

2%

-38

.4%

Class AB Class C Class D Class E

Cla ss A B C lass C C lass D C lass E

39

Bibliography

BACHA, E. L., AND TAYLOR, L.. “Brazilian income distribution in the 1960s: Tacts’ model results and the controversy.” Journal of Development Studies, Vol. 14, Issue 3, pages 271 – 297, 1978 BANERJEE, ABHIJIT V. AND DUFLO, ESTHER ”What is middle class about the middle classes around the world?”, mimeo, MIT December 2007. BARROS, R.P. de; MENDONÇA, R. A evolução do bem-estar e da desigualdade no Brasil desde 1960. Rio de Janeiro: IPEA, 1992. (Texto para discussão, nº. 286). BARROS, R.P. de; HENRIQUES, R.; MENDONÇA, R. Desigualdade e pobreza no Brasil: a estabilidade inaceitável. In: HENIQUES, R. (Ed.). Desigualdade e pobreza no Brasil. Rio de Janeiro: IIPEA, 2000. BARROS, R. P. Foguel, M. N. ULYSSEA G. (Orgs.). Desigualdade de Renda no Brasil: uma análise da queda recente. Rio de Janeiro: IPEA, 2007. BARROS,Ricardo Paes; MENDONÇA, Rosane; NERI, Marcelo C. The duration of poverty spells. In: III Encontro Nacional de Estudos do Trabalho, ENABET, Anais..., 1996. BARROS, Ricardo Paes; MENDONÇA, Rosane; NERI, Marcelo C. Pobreza e inflação no Brasil: uma análise agregada. In: Economia Brasileira em Perspectiva 1996, Rio de Janeiro: IPEA, 1996, v.2, p.401-420. BIRDSALL, NANCY, CAROL GRAHAM, AND STEFANO PETTINATO “Stuck In Tunnel: Is Globalization Mudding The Middle Class?” Brookings Institution, Center on Social and Economic Dynamics WP No. 14, 2000. BOOT, H. M. (1999) “Real Incomes of the British Middle Class, 1760-1850: The Experience of Clerks at the East India Company”, The Economic History Review, 52(4), 638-668. BONELLI, R.P. de; SEDLACEK, G.L. Distribuição de renda: evolução no último quarto de século. In: SEDLACEK, G.L.; BARROS, R.P. de. Mercado de trabalho e distribuição de renda: uma coletânea. Rio de Janeiro: IPEA, 1989. (Série Monográfica 35). CARDOSO, E.; BARROS, R.; URANI, A. Inflation and unemployment as determinants of inequality in Brazil: the 1980s, Chapter 5. In: DORNBUSCH, R.; EDWARDS, S. (Eds.), Reform, recovery and growth: Latin America and the Middle-East, Chicago: University of Chicago Press for the NBER, 1995. DOEPKE, M.AND F. ZILIBOTTI (2005)”Social Class and the Spirit of Capitalism”, Journal of the European Economic Association 3, 516-24.

40

DOEPKE, M AND F. ZILIBOTTI (2007)”Occupational Choice and the Spirit of Capitalism”, NBER Working Paper. ESTERLY, WILLIAM (2001) “The Middle Class Consensus and Economic Development”, Journal of Economic Growth, 6(4), 317-335. FERREIRA, F.; LANJOUW, P.; NERI, M. A Robust poverty profile for Brazil using multiple data sources. Revista Brasileira de Economia 57 (1), p. 59-92, 2003. FISHLOW, A. (1972): “Brazilian Size Distribution of Income”, American Economic Association: Papers and Proceedings 1972, pp.391-402 FREDERICK, JIM (2002) “Thriving in the Middle Kingdom ”, TIME Magazine, Nov 11. GASPARINI, L. Different lives: inequality in Latin America the Caribbean, inequality the state in Latin America the Caribbean World Bank LAC Flagship Report 2003. Washington, D.C.: World Bank, 2003. Mimeografado. GOLDMAN SACHS - WILSON, DOMINIC AND DRAGUSANU, RALUCA “The Expanding Middle: The Exploding World Middle Class and Falling Global Inequality” - Goldman Sachs Economic Research/Global Economics Paper nº 170, July 2008 HOFFMAN, R. A evolução da distribuição de renda no Brasil, entre pessoas e entre famílias, 1979/86. In: SEDLACEK, G.; BARROS R.P. de. Mercado de trabalho e distribuição de renda: uma coletânea. Rio de Janeiro: IPEA/Inpes, 1989. HOFFMANN, R. As transferências não são a causa principal da redução da desigualdade, Econômica 7, no.2, 335-341: Rio de Janeiro, Brazil, 2005. IPEA. Sobre a queda recente da desigualdade no Brasil, 2006. (Nota técnica). KAKWANI, N., SON, H. Measuring the Impact of price changes on poverty. International Poverty Centre, Brasília, 2006. (Working paper # 33). KAKWANI, N.; NERI, M.; SON, H. Linkages between pro-poor growth, social programmes labour market: the recent brazilian experience. International Poverty Centre, Brasília, 2006a. (Working paper # 26). ______. Desigualdade e Crescimento: Ingredientes Trabalhistas em Desigualdade de Renda no Brasil: uma análise da queda recente. Ricardo Paes de Barros, Miguel Nathan Foguel, Gabriel Ulyssea (orgs), Rio de Janeiro, 2007. vide http://www.fgv.br/cps/pesquisas/propobre/ LANDES, DAVID. The Wealth and Poverty of Nations. New York: Norton, 1998. LANGONI, C. Distribuição da renda e desenvolvimento econômico do Brasil. Rio de Janeiro: Fundação Getúlio Vargas (FGV), 3a edição 2005, 1973

41

MURPHY, KEVIN M., ANDREI SCHLEIFER AND ROBERT VISHNY (1989) “ Industrialization and the Big Push”, Journal of Political Economy, 97(5), 1003-1026. NERI, Marcelo C.; CONSIDERA, Cláudio; PINTO, Alexandre. A evolução da pobreza e da desigualdade brasileiras ao longo da década de 90. In: Revista Economia Aplicada, Ano 3, v. 3, p.384-406, jul.-set. 1999. NERI, Marcelo C. O reajuste do salário mínimo de maio de 1995. In: XIX ENCONTRO BRASILEIRO DE ECONOMIA, SBE, Recife. Anais... dez. 1997, v. 2, p. 645-666. NERI, Marcelo C.; CONSIDERA, Cláudio. Crescimento, desigualdade e pobreza: o impacto da estabilização. In: Economia Brasileira em Perspectiva 1996, Rio de Janeiro: IPEA, 1996, v.1, p. 49-82. NERI, M. C. Diferentes histórias em diferentes cidades. In: REIS VELLOSO, J.P.; CAVALCANTI, R. (Eds.). Soluções para a questão do emprego. Rio de Janeiro: José Olimpio, 2000. ______. Eleições e “Expanções”, mimeo, vide http://www.fgv.br/cps/pesquisas/pp2/, 2006a. (also available in English) ______. Miséria em queda: mensuração, monitoramento e metas. mimeo Rio de Janeiro: FGV, vide: http://www3.fgv.br/ibrecps/queda_da_miseria/inicio_q.htm . 2005. ______. Miséria, desigualdade e políticas de rendas: o Real do Lula, mimeo, Rio de Janeiro: FGV, 2007. (also available in English) ______. Miséria, desigualdade e estabilidade in Desigualdade de Renda no Brasil: uma análise da queda recente. Ricardo Paes de Barros, Miguel Nathan Foguel, Gabriel Ulyssea (orgs), Rio de Janeiro, 2007a. see: <http://www.fgv.br/cps/pesquisas/site_ret_port/ (also available in English) ______. A Nova Classe Média, mimeo, Rio de Janeiro: FGV, 2008a. see: http://www.fgv.br/cps/classe_media/ (also available in English) ______. Miséria, e a nova classe média na década da igualdade, mimeo, Rio de Janeiro: FGV, 2008b. see: http://www.fgv.br/cps/desigualdade/ (also available in English) ______. Miséria, desigualdade e estabilidade in Desigualdade de Renda no Brasil: uma análise da queda recente. Ricardo Paes de Barros, Miguel Nathan Foguel, Gabriel Ulyssea (orgs), Rio de Janeiro, 2007a. see: <http://www.fgv.br/cps/pesquisas/site_ret_port/ ______. A Dinâmica da Redistribuição Trabalhista em Desigualdade de Renda no Brasil: uma análise da queda recente. Ricardo Paes de Barros, Miguel Nathan Foguel, Gabriel Ulyssea (orgs), Rio de Janeiro, 2007b.

42

______. (org) Microcrédito, o mistério nordestino e o Grameen brasileiro: perfil e performance dos clientes do CrediAMIGO”, Editora da Fundação Getulio Vargas, 370pag, Rio de Janeiro, 2008 NERI, M. C.; CAMARGO, J. Distributive effects of Brazilian structural reforms. In: BAUMANN, R. (Ed.). Brazil in the 1990s: a decade in transition, Palgrave. Macmillan's Global Academic Publishing, UK, 2001. NERI, M. C.; GIOVANNI F, Negócios nanicos, garantias e acesso a crédito in Revista de Economia Contemporânea, Rio de Janeiro, v.9, n.3, pp 643-669, setember-december 2005. RAMOS, Lauro; BRITO, M. O funcionamento do mercado de trabalho metropolitano brasileiro no período 1991-2002: tendências, fatos estilizados e mudanças estruturais. Boletim Mercado de Trabalho, Conjuntura e Análise, Rio de Janeiro: IPEA, nº 22, p. 31-47, nov. 2003. ROCHA, S. Pobreza no Brasil: afinal do que se trata? Rio de Janeiro: Ed. FGV, 2003. SOARES, S. “Análise de bem-estar e decomposição por fatores da queda na desigualdade entre 1995 e 2004.” Econômica, v. 8, n. 1, p. 83-115. Rio de Janeiro, 2006.