tangled governance: international regime complexity in … · tangled governance: international...

TRANSCRIPT

Tangled Governance: International Regime Complexity in the Euro Crisis

C. Randall Henning American University

Presented to the International Relations Faculty Colloquium, sponsored by the Department of Politics, Niehaus Center for Globalization and Governance and

European Union Program, Princeton University, November 3, 2014

C. Randall Henning, November 2014

Questions

1. What explains the institutional form of the financial rescue?

2. How do states strategize the complex of institutions?

3. Is the regime complex for crisis finance fragmenting?

C. Randall Henning, November 2014

0

5

10

15

20

25

30

35

40

45

50

01/0

1/08

02/2

6/08

04/2

2/08

06/1

7/08

08/1

2/08

10/0

7/08

12/0

2/08

01/2

7/09

03/2

4/09

05/1

9/09

07/1

4/09

09/0

8/09

11/0

3/09

12/2

9/09

02/2

3/10

04/2

0/10

06/1

5/10

08/1

0/10

10/0

5/10

11/3

0/10

01/2

5/11

03/2

2/11

05/1

7/11

07/1

2/11

09/0

6/11

11/0

1/11

12/2

7/11

02/2

1/12

04/1

8/12

06/1

3/12

08/0

8/12

10/0

3/12

11/2

8/12

01/2

3/13

03/2

0/13

05/1

5/13

07/1

0/13

09/0

4/13

10/3

0/13

12/2

5/13

Greece Ireland Portugal

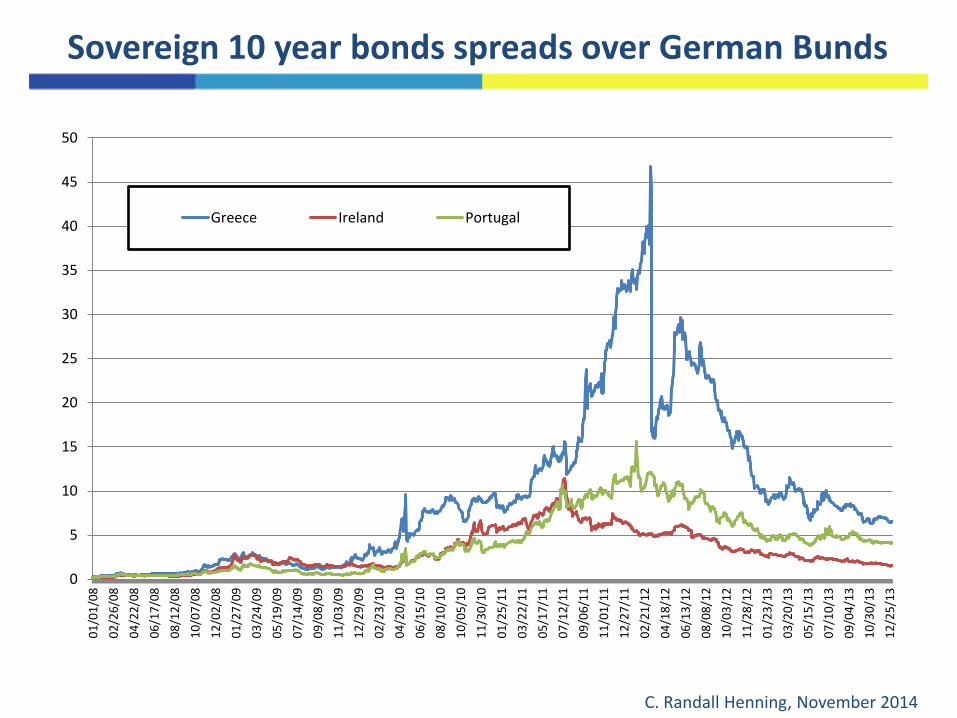

Sovereign 10 year bonds spreads over German Bunds

C. Randall Henning, November 2014

Sovereign 10 year bonds spreads over German Bunds

0

1

2

3

4

5

6

701

/01/

0802

/26/

0804

/22/

0806

/17/

0808

/12/

0810

/07/

0812

/02/

0801

/27/

0903

/24/

0905

/19/

0907

/14/

0909

/08/

0911

/03/

0912

/29/

0902

/23/

1004

/20/

1006

/15/

1008

/10/

1010

/05/

1011

/30/

1001

/25/

1103

/22/

1105

/17/

1107

/12/

1109

/06/

1111

/01/

1112

/27/

1102

/21/

1204

/18/

1206

/13/

1208

/08/

1210

/03/

1211

/28/

1201

/23/

1303

/20/

1305

/15/

1307

/10/

1309

/04/

1310

/30/

1312

/25/

13

France Spain Italy Netherlands Finland

C. Randall Henning, November 2014

Opposition to IMF Involvement

“We don’t need to call in the IMF. We have more than enough instruments in the treaty to tackle a situation like the one we’re faced with at the moment in Greece.”

Joaquín Almunia, Commissioner for Economic and Monetary Affairs, February 9th, 2010.

“I do not believe that it would be appropriate to introduce the IMF as a supplier of help through standby arrangements or through any such kind of help.”

Jean-Claude Trichet, President, European Central Bank, March 4th, 2010.

. . . “absurd” . . . “It’s not a matter of having the IMF designing the exit strategy as far as public finances are concerned.”

Jean-Claude Juncker, President, Eurogroup, February 16th, 2010.

C. Randall Henning, November 2014

Opposition to IMF (cont.)

“What’s clear is that this is a matter for the Europeans. There is no doubt that Greece is not a question for the International Monetary Fund.”

Wolfgang Schäuble, Minister of Finance, Germany, February 9th, 2010.

“Nous ne sommes pas….. en situation de faire appel au Fonds monétaire international. On en est pas là du tout.”

Christine Lagarde, Minister of Finance, France, February 12th, 2010.

C. Randall Henning, November 2014

IMF Inclusion is Over-determined

The reasons adduced for euro area leaders to include the Fund:

1. Expertise and credibility in designing, negotiating and monitoring programs;

2. Financial resources;

3. Skeptical of the European Commission, faith in IMF (to be tough);

4. Deflection of political backlash against austerity.

C. Randall Henning, November 2014

International Monetary Fund

European Central Bank

Program Negotiations

European Commission

Eurogroup and Euro Summit

Finance Minister and Central Bank Governor of Borrowing Country

Troika and Member States – Complex Indeed

UK

PRC

J

US

Non-European and non-Euro States

...

ES EL IT

FR DE

BE AT

Euro Area Member States

...

European Stability

Mechanism

C. Randall Henning, November 2014

Greece May 2010

Ireland November 2010

Portugal May 2011

Greece March 2012

Spain Financial Sector Program

July 2012

Cyprus May 2013

European Commission

€80bn through Greek Loan Facility

€22.5bn EFSM, €17.7bn EFSF

€26bn EFSM, €26bn EFSF

€144.7bn EFSF in conjunction with

PSI

€100bn EFSF and ESM €9bn ESM

European Central Bank

“In liaison with" European

Commission (and UMP)

In liaison with European

Commission (and UMP)

In liaison with European

Commission (and UMP)

In liaison with EC (ELA, eventually restores regular

access to refinancing)

Technical assistance in liaison with EC and EBA (financial

assistance via UMP)

In liaison with EC (restores regular

access to refinancing)

International Monetary

Fund €30bn SBA €22.5bn EFF €26bn EFF €28bn EFF

Technical assistance,

monitoring and informal input on program design

€1bn EFF

Notes

Replaced by second program in 2012 after disbursing

€73bn (Eurozone share €52.9bn; IMF

€20.9bn)

Exits in December 2013 without a precautionary

program

Exits in June 2014 without a

precautionary program

Exits European program in

December 2014, IMF in March 2016

Exits in January 2014 Exits in May 2016

Source: IMF and European Commission program documents

Summary of Troika Programs 2010-2014

C. Randall Henning, November 2014

Spanish Banking Sector Program

Included among these cases because:

a) Spain’s access to the capital markets was endogenous to the institutional solution;

b) Program was in reality “full”: fiscal, structural as well as banking. Administered through a decentralized, but coordinated, variation on the troika.

C. Randall Henning, November 2014

Spain (cont.)

This mix was chosen owing to:

a) Size, which i. Placed a premium on ECB putting its balance sheet in play ii. Made euro-area-wide policy (e.g., monetary policy, banking union)

critical to success of any IMF program, prompting demands for adjustments

b) Domestic party politics i. Rajoy replaced Zapatero prior to the program ii. Merkel had confidence, Spanish officials orthodox

Key creditors thus maximized preferences by keeping the IMF as a shadow member of the troika.

C. Randall Henning, November 2014

Cyprus

1) IMF contributes only 1/10th of the financing

2) Program does not cover the financing gap

3) IMF insists on closing insolvent banks

4) Prevails because it is backed by the most powerful euro area member state

C. Randall Henning, November 2014

Underlying Explanation

1. Expertise and credibility in designing, negotiating and monitoring programs;

2. Financial resources;

3. Skeptical of the Commission, faith in IMF;

4. Deflection of political backlash against austerity;

Preference heterogeneity and intergovernmentalism.

C. Randall Henning, November 2014

Prediction

Preference heterogeneity + unanimity = IMF involvement

As long as EAMS take decisions on financial assistance to sovereigns by unanimity, the euro area will continue to request that the IMF participate in crisis resolution.

The Spanish program could be a template for future programs. But complete exclusion of the IMF from a sovereign rescue by unanimity would falsify this prediction.

C. Randall Henning, November 2014

Germany

1. Economic preferences rooted in international position, remarkably consistent over the decades

2. Abiding fear of the costs of mistakes of others, overshadowing benefits from monetary union

3. Anticipated cases being brought to the Federal Constitutional Court, which insisted on Bundestag review and votes (adept two-level strategy)

4. IMF protected the government’s right flank, maintaining a working legislative majority for programs

C. Randall Henning, November 2014

United States

Caught between two imperatives:

1) Stabilize the euro crisis to prevent contagion across the Atlantic and a double-dip recession

2) Force euro area member states to bear the cost of fighting the crisis and completing the institutional architecture to stabilize the monetary union.

These were sometimes at odds: US sometimes withholds support to prod EAMS to pony up; but ultimately prioritizes stabilization.

C. Randall Henning, November 2014

Unexpected Outcomes

1) U.S. official position shifts from moral support with private skepticism of Europe’s monetary union to firm endorsement of completing the project. a) A lurching shift, not gradual b) Motivated by financial spillover c) Abandons concerns about balance of payments constraints or

currency competition; weakness of the euro area a greater threat

2) IMF supports creation of the ESM and completion of the euro project a) Against its narrow bureaucratic interest b) In deference to its non-European members

C. Randall Henning, November 2014

Cooperation mixed with conflict

1) Troika cooperates on financial assistance while competing on economic analysis, simultaneously.

2) Awkward for troika officials, but explained by states’ incentives.

3) Lending function contains distinctly negative spillovers, while competition on analysis carries positive spillover, from the standpoint of states.

4) Resonates with Johnson and Urpelainen (2012) thesis re regime separation and integration.

C. Randall Henning, November 2014

Strategizing Complexity

1) States can use complexity to manage agency drift.

2) Especially when they are the arbiters of institutional conflict.

3) Germany tolerated disagreements with the Fund because it was in such a position, along with other key creditors.

4) Inter-institutional conflict does not necessarily portend breakdown in the troika; it is integral to the control mechanism.

C. Randall Henning, November 2014

Is the regime complex fragmenting?

1) Yes, but less than meets the eye

2) Informal coordination sustains cooperation despite an increasing number of institutions

3) States’ control strategies ensure that informal mediation of institutional deadlock will continue to be necessary

4) The effectiveness of informal coordination hinges on convergence of preferences among key states

5) Which cannot be taken for granted, especially in contingencies outside Europe, in the future

C. Randall Henning, November 2014

Thank you

C. Randall Henning, November 2014