tansri datukdr. yusof$basiron$...

TRANSCRIPT

Tan Sri Datuk Dr. Yusof Basiron MALAYSIAN PALM OIL COUNCIL

MPOC FACILITATED EMERGING MARKET OPPORTUNITIES : INNOVATIVE TOOLS TO MEET CHALLENGES IN 2014

OUTLINE OF PRESENTATION

1. Malaysian palm oil trade has performed well

2. Capitalizing on opportuniFes to strengthen or create more market demand

3. Malaysia’s own sustainability system (MSPO)

4. MSPO++

5. Branding Malaysian palm oil to enhance trade

6. Conclusions

1. Malaysia’s Experiences in Global MarkeFng -‐ Scope and Products

Upstream Midstream Downstream Processing Consumer Products

ACTIVITIES • Seed producFon • Nursery • CulFvaFon • HarvesFng • Milling

• • Trading • Crude palm oil bulking

• Refining • FracFonaFon • Oleochemical • EsterificaFon • Refined product storage

• Packaging and branding • Food products • Non – food products

PRODUCTS • DxP seeds • Fresh fruit bunches • Crude palm oil • Palm kernel • Biomass (Empty Fruit Bunches, kernel shell, fronds) • Palm oil mill effluent

• DxP seeds • Fresh fruit bunches • Crude palm oil • Palm kernel • Biomass (Empty Fruit Bunches, kernel shell, fronds) • Palm oil mill effluent

• RBD Palm Oil • Palm Fa]y Acid DisFllate • RBD Palm Olein • RBD Palm Stearin • RBD PK Olein • RBD PK Stearin • Cocoa Bu]er Equivalent • Cocoa Bu]er SubsFtute • Cocoa Bu]er Replacers • Fa]y acid, alcohols, amines, amides • Glycerines • Palm methyl esters

• Cooking oil, frying fats • Margarine • Shortening • VanaspaF • Ice cream, non-‐dairy creamers • Candles, soap • Emulsifiers • Vitamin E supplements • ConfecFonery • Bakery fats • Biodiesel • Energy generaFon • Animal feed

These days, palm oil and derived products are channeled into worldwide industrial and commercial acFviFes to churn out food products as well as non-‐food applicaFons Source: MPOC Publica1ons & USDA Database

1. Source of food (global food security): 80%

2. Oleochemicals: 15%

3. Biofuel : 2%

4. Renewable energy source: Poten1al Remains Largely Untapped through Palm Biomass

1. Malaysian Palm Oil – Export By Region 2001 -‐ 2013

0 1 2 3 4 5 6 7 8 9

10 11 12 13 14 15 16 17 18 19

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

(Million MT)

Africa Americas Asia Pacific

Europe Middle East Sub-‐ConFnent

Export increased by almost 70% since 2001. Palm olein comprises almost 50%, the rest :palm stearin and palm oil

1. Malaysian Palm Oil – Main Markets Ø The biggest markets for Malaysian palm oil are Asia Pacific, Sub ConFnent and Europe

Ø However, in terms of market growth, the two biggest growth regions are the African region and American region

Ø Export to Africa increased from 382,186 MT in 2001 to 1.72 million MT in 2013 (+ 351%)

Ø Export to America increased from 288,000 MT in 2001 to 1.15 million MT in 2013 (+ 299%)

Ø Increase due to efforts of industry and agencies to overcome obstacles eg transfats issue, awareness issue

CPO PRICE VS SBO PRICE

-‐

200

400

600

800

1,000

1,200

1,400

0

500

1000

1500

2000

2500

3000

3500

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

SBO (U

S$/M

T)

CPO (R

M/M

T)

CPO Price (RM/MT) SBO Price (US$/MT))

Source : CPO Price – MPOB SBO Price -‐ Indexmundi

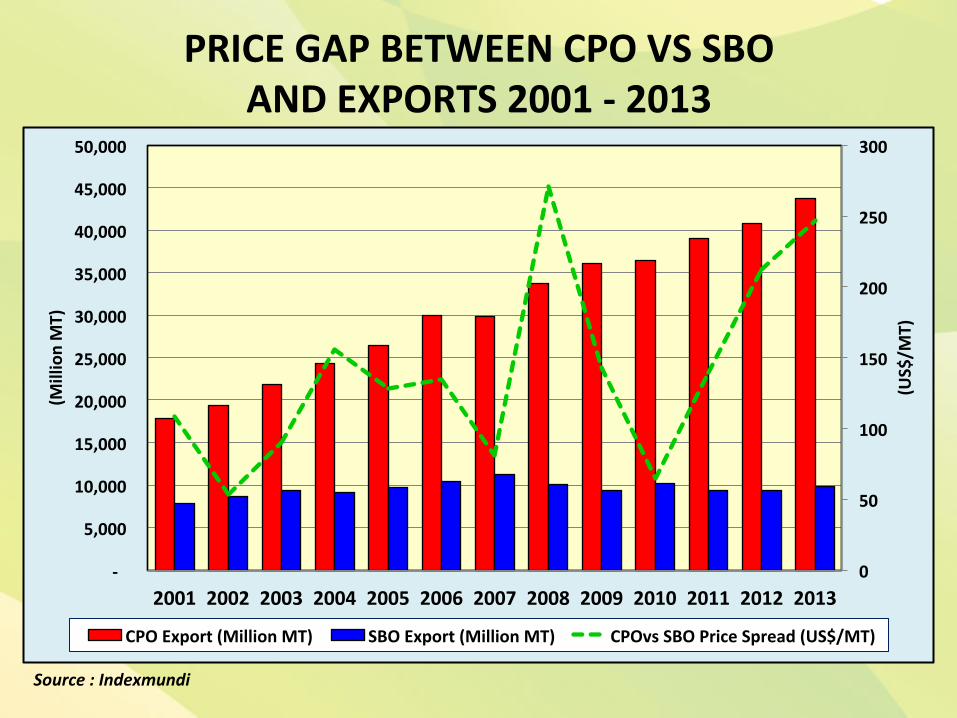

PRICE GAP BETWEEN CPO VS SBO AND EXPORTS 2001 -‐ 2013

Source : Indexmundi

0

50

100

150

200

250

300

-‐

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

(US$/M

T)

(Million MT)

CPO Export (Million MT) SBO Export (Million MT) CPOvs SBO Price Spread (US$/MT)

PRICE GAP BETWEEN CPO VS SBO AND CONSUMPTION 2001 -‐ 2013

Source : Indexmundi

0

50

100

150

200

250

300

-‐

10,000

20,000

30,000

40,000

50,000

60,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

(US$/M

T)

(Million MT)

Palm Oil ConsumpFon (Million MT) Soyoil ConsumpFon (Million MT)

CPOvs SBO Price Spread (US$/MT)

MALAYSIAN PALM OIL EXPORT VS CPO PRICE (RM/MT) 2001-‐2013

0

500

1000

1500

2000

2500

3000

3500

-‐

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

(RM/M

T)

(Million MT)

Export ('000 MT) CPO Price (RM/MT)

Source : MPOB

2. New Market OpportuniFes 1. Expanding markets

Ø Eastern Europe, Iran Ø Russia’s admission into WTO provides an excellent opportunity Ø Philippines

2. Trans fats issue, India, Pakistan Middle East, EU and USA

3. Palm kernel cake

4. Palm biodiesel

5. Palm furniture

MarkeFng palm olein in opaque bo]les Ø MPOC iniFated idea

of markeFng of cooking oil in opaque bo]les or packaging

Ø Highly suitable in regions with temperate climate

Ø Successfully done in Eastern European countries, Iran, Dubai, etc Half the price cf other oils

Philippines Market

Ø New market not well tapped previously

Ø Palm oil to subsFtute coconut oil

Ø MarkeFng of cooking oil in opaque containers

Ø Locals used to buy light colored corn oil

Ø Packing in smaller volumes e.g. 400 or 800ml (usual is 500-‐1,000ml) to meet price affordability

Ø Many countries around the world have banned the use of trans fats in food

Ø The government of India has made it compulsory for food manufacturers to menFon trans fats content on labels

Ø The U.S. Food and Drug AdministraFon is looking to ban trans fats included in food

Ø Harvard scienFsts esFmate that trans fats may contribute to more than 30,000 premature deaths each year

Ø FDA officials esFmate as many as 7,000 deaths and 20,000 heart a]acks would be prevented by eliminaFng trans fats from processed foods

Ø Palm oil is proven to be healthy and trans fats free Ø Opportunity to expand market using this theme

OpportuniFes: Trans Fats in Food

Capitalizing on Trans Fats Issue Big market potenFal that is just emerging

• Solid food formulaFon-‐ trans free Promote sales of palm stearin to make margarines, vasnapa3 and

shortenings, using interesterifica3on • Direct use of RBD palm oil for vanaspa3.. E.g. Pakistan

• Blending soo oils with palm oil, palm olein

Blending so> oils with palm oil E.g. Smart balance to help improve cholesterol ra3o eg in USA Credit goes to MPOB

OpportuniFes: PKC potenFal yet to be tapped fully exploited

2013 2010 2005 2001 Difference 2013 -‐ 2001 (%) 2001-‐2013

EU 827,651 1,000,766 1,559,852 1,534,492 (706,841) (-‐46.06)

NEW ZEALAND 795,642 640,296 225,543 21,018 774,624 3,685.47

SOUTH KOREA 470,156 462,169 165,578 201,221 268,935 133.65

CHINA P.R 202,580 227,008 -‐ 28,856 173,724 602.03

TURKEY 123,949 -‐ -‐ -‐ 123,949 -‐

SAUDI ARABIA 111,546 47,000 -‐ -‐ 111,546 -‐

PAKISTAN 57,062 19,871 -‐ -‐ 57,062 -‐

AUSTRALIA 22,455 4,759 -‐ -‐ 22,455 -‐

O T H E R S COUNTRIES

56,054 43,524 83,027 23,842 32,212 135.11

TOTAL 2,667,096 2,445,393 2,034,000 1,809,430 857,666 47.40

MPOC’s efforts to inform end users of PKC’s use for animal feed which is economically feasible

Ø PKC total metabolizable energy per USD is higher than soymeal, rapeseed and sunflower meal.

Ø For every USD spend on PKC, the energy value is 52.7 MJ which is 29.5%-‐108% higher than that of soya, rapeseed and sunflower meal.

Ø For crude protein, PKC has 22.1%-‐33% lower protein content compared to rapeseed and sunflower meal

Ø However, the crude protein content that can be obtained per USD is the same for soyameal and PKC.

Ø PKC crude fibre content is high at 17%. Ø The high crude fibre content is said to be more suitable for

ruminants than non-‐ruminants.

PKC Advantages

NutriFve and cost advantage of PKC

CP Kg/USD

ME (MJ/USD)

TDN (Kg/USD)

PKC 0.81 52.7 3.57 Soymeal 0.81 25.3 1.42 Rapeseed meal 1.21-‐1.27 33.6-‐40.7 2.42

Sunflower meal 1.04 29.0 2.27

Based on cif Ro]erdam price 2013 Price : PKC –USD199/MT, Soymeal – USD590/MT Rapeseed meal – USD297/MT, Sunflower meal – USD286/MT

CP : Crude protein, ME : Metabolizable energy, CF – Crude Protein TDN : Total Digestable Nutrients

PALM BIODIESEL • At low CPO rela3ve prices, biodiesel is viable, small subsidy

by government, helps increase demand and prices of CPO-‐ beneficial to government /country revenue

• High prices, biodiesel is less viable, subsidy is higher but government can reduce blending ra3o, but s3ll benefit from high palm oil prices to afford the subsidy/ good for country revenue

• Thus B5, B7 or B10 or B3 are possible op3ons, and na3on wide applica3on is possible by July 2014.

ApplicaFons of Oil Palm Biomass

19 19

OIL PALM BIOMASS

BOARD OF VARIOUS KINDS

• MDF • Plywood • Moulded par3cleboard • Sawn lumber

PROPERTIES OF OPT, OPF & EFB FIBRE BUNDLES

• Fibre quality • Fibre morphology • Fibre proper3es • Usable fibre fractions

OTHER PRODUCT TYPES

• Oil palm heart • Carbon products • Carboxymethyl cellulose • Fine chemicals

FIBRE REINFORCING COMPOSITES

• Agrolumber • Plas3c composite

PAPER PULP & PAPER PRODUCTS

• Chemical pulp • Semi-‐mechanical pulp • Mechanical pulp • Moulded paper products • Soilless plan3ng medium

Palm Wood Furniture

MPOC started Palm Wood Promo3on Scheme in 2012. For Furniture China 2012 exhibi3on, confirmed sales were at RM1,500,000

while Furniture China 2013 had RM1,000,000 confirmed sales.

• Standards for MSPO by SIRIM/ MPOB are ready and RSPO can be launched soon

• May be useful to establish MPOCC (CerFficaFon Council) to implement the MSPO cerFficaFon process

• What are the opportuniFes?

3. Malaysia’s own sustainability system (MSPO)

WORLD LAND AREA & DRIVER OF DEFORESTATION

Grains & Oilseeds 10.00%

Ca]le 25.00%

Oil Palm (A Thin Line)

0.10%

Balance 64.90%

2012

WORLD LAND AREA & DRIVER OF DEFORESTATION

Grains & Oilseeds 15.00%

Ca]le 50.00%

Oil Palm (SFll A Thin Line)

0.20%

Balance 34.80%

2050

DistribuFon of Agricultural Area Livestock , 71.27%

Other Crops, 23.17%

Oilseeds, 5.25%

Oil Palm, 0.31%

Total Agricultural Area : 5 Billion Hectares

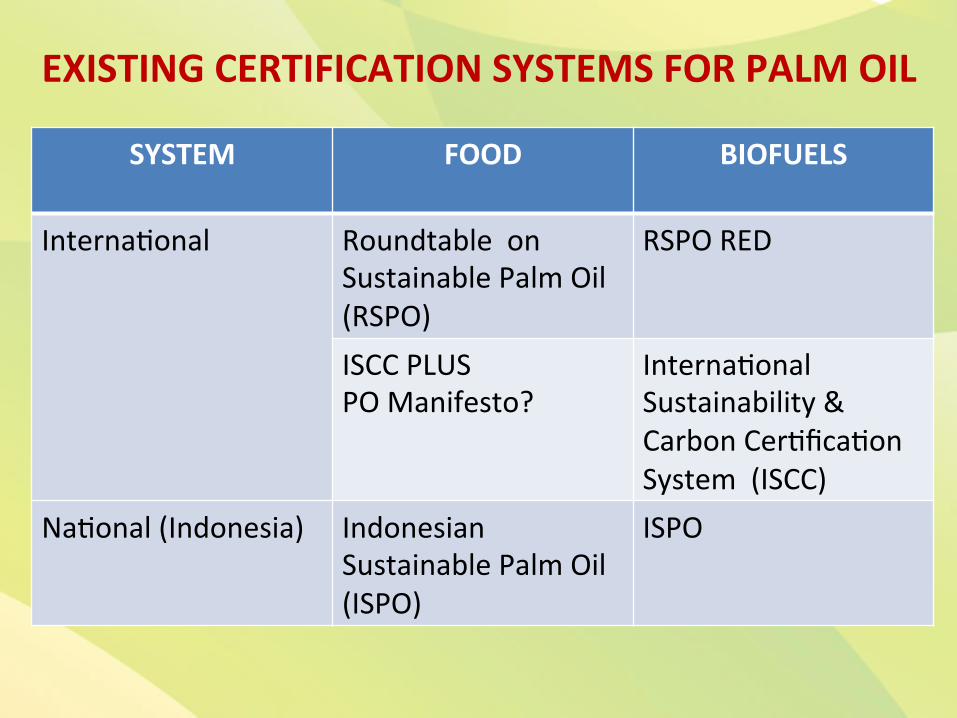

SYSTEM FOOD BIOFUELS

Interna3onal Roundtable on Sustainable Palm Oil (RSPO)

RSPO RED

ISCC PLUS PO Manifesto?

Interna3onal Sustainability & Carbon Cer3fica3on System (ISCC)

Na3onal (Indonesia) Indonesian Sustainable Palm Oil (ISPO)

ISPO

EXISTING CERTIFICATION SYSTEMS FOR PALM OIL

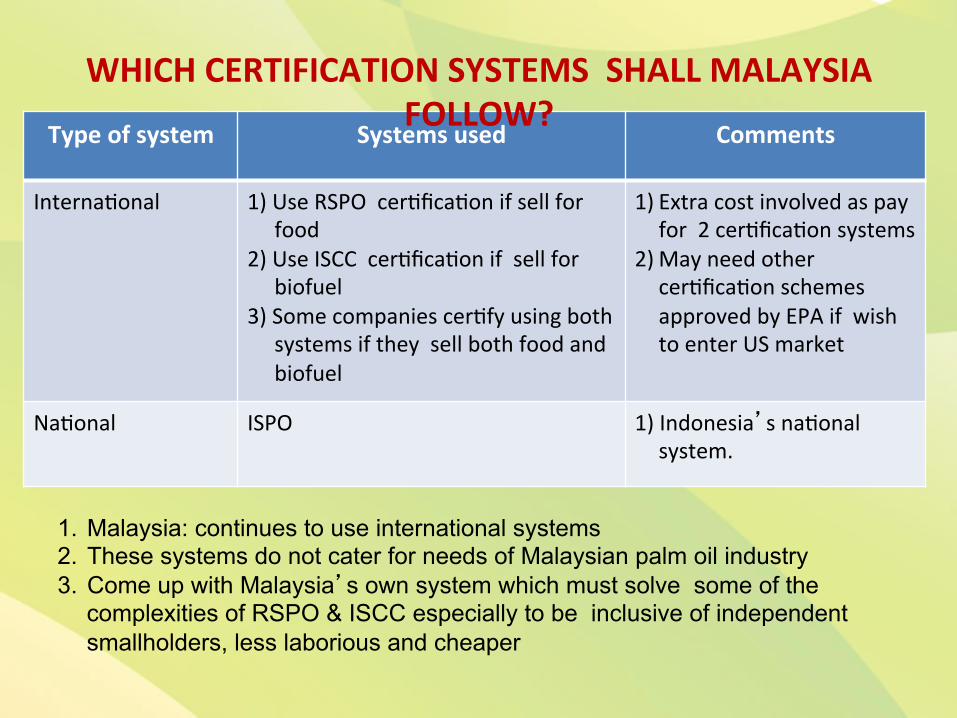

Type of system Systems used Comments

Interna3onal 1) Use RSPO cer3fica3on if sell for food 2) Use ISCC cer3fica3on if sell for biofuel 3) Some companies cer3fy using both systems if they sell both food and biofuel

1) Extra cost involved as pay for 2 cer3fica3on systems

2) May need other cer3fica3on schemes approved by EPA if wish to enter US market

Na3onal ISPO 1) Indonesia’s na3onal system.

1. Malaysia: continues to use international systems 2. These systems do not cater for needs of Malaysian palm oil industry 3. Come up with Malaysia’s own system which must solve some of the

complexities of RSPO & ISCC especially to be inclusive of independent smallholders, less laborious and cheaper

WHICH CERTIFICATION SYSTEMS SHALL MALAYSIA FOLLOW?

• Na3onal Standard or Malaysian Standard

• MS 2530-‐1Part 1: General principles for Malaysian sustainable palm oil

• Part 2: General principles for independent smallholders

• Part 3: General principles for oil palm planta3ons and organised smallholders

• Part 4: General principles for palm oil mills Will be voluntary scheme Cer3fica3on needed

MALAYSIAN SUSTAINABLE PALM OIL (MSPO)

MSPO++ as a Branding Plauorm

Ø Sustainability is no longer an op3on but a necessity for Malaysian palm oil. (based on Survey results) Ø For MSPO to represent Malaysian Palm Oil, it must be applied to all Malaysian palm oil Ø We propose sustainability is men3oned in terms and condi3ons of licenses of all license holders just like in the EU so that all operators are deemed to cross comply to operate responsibly and sustainably, indirectly making sustainability mandatory

CriFcal Issues Ø MSPO as currently proposed may s3ll be burdensome for industry to implement; a simpler and cheaper way is needed for maximum par3cipa3on

Ø Cross compliance and aggregate compliance approaches (MSPO++), like they do in the EU, USA and Canada for their oilseed crops and oils may need to be used at a later stage a>er the launch of MSPO

Ø For other oilseed crops and cafle, they are far behind in sustainability capability, yet they design schemes to overcome their problems.

Ø For example, we can define sustainability at a na3onal level by having more than 35% forest and using less than 35% of land for agriculture.

Ø The 35:35 criterion for sustainability can be easily achieved by Malaysia, Indonesia and other tropical developing countries but not by most developed countries.

Ø In reality, sustainability is a macro measure and not a micro issue because of trade-‐offs involved in achieving the objec3ves.

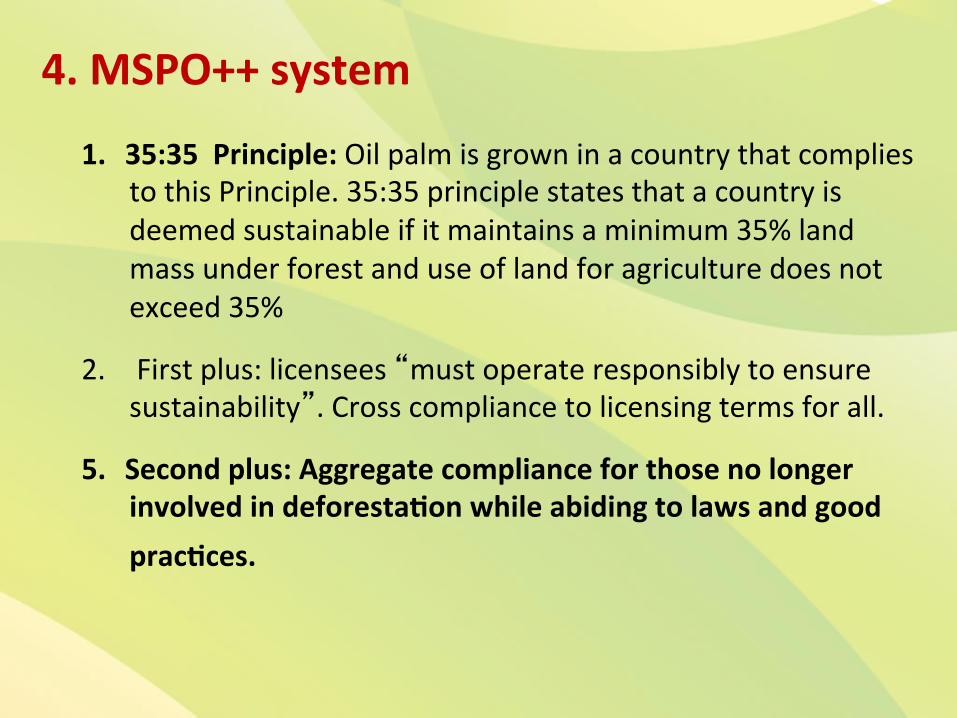

1. 35:35 Principle: Oil palm is grown in a country that complies to this Principle. 35:35 principle states that a country is deemed sustainable if it maintains a minimum 35% land mass under forest and use of land for agriculture does not exceed 35%

2. First plus: licensees “must operate responsibly to ensure sustainability”. Cross compliance to licensing terms for all.

5. Second plus: Aggregate compliance for those no longer involved in deforestaFon while abiding to laws and good pracFces.

4. MSPO++ system

• Company that is already cerFfied under other sustainability schemes

• Admifed into MSPO++ through cross compliance approach

a) Apply to Malaysian Palm Oil Cer3fica3on Council (MPOCC). the new cer3fica3on body/organiza3on that needs to be set up

b) Provide evidence that the company opera3ons is currently cer3fied under one or more of MPOCC recognized sustainability schemes , namely MSPO, RSPO, ISCC and/or ISPO

MSPO++ system

• Company that is not yet cerFfied under other sustainability schemes

Category 1: company with land that is already planted with oil palm, no longer involved in deforesta3on (define cut-‐off year)

Category 2: company with land that is being/will be planted for first 3me with oil palm, including on peat.

MPOCC will admit these Category 1 companies, into MSPO++ cer3fica3on through Aggregate Compliance Approach as they are no longer involved in deforesta3on. They will be judged to see if they also comply to legal and good agricultural prac3ce elements.

MSPO++ system

4. Statutory compliance: Company must comply to all laws of country during conduct of business

5. Good agricultural and management pracFces: Company uses good agricultural & management prac3ces during produc3on process

MPOCC to issue cerFficaFon and recognise cerFficaFon schemes such as RSPO, ISCC, MSPO, ISPO etc

Those operaFng using any of the recognised schemes , cross comply and those falling under the aggregate compliance can be issued cerFficates of compliance (95 % of all players)

Remaining (5%?) Category 2. involved in new planFng must comply to licensing condiFon (sustainable and responsible) and can choose to be cerFfied by any of the recognized cerFficaFon schemes eg MSPO or RSPO

MSPO++ system

UFlizaFon of World’s Agricultural Land

Livestock, 71.27% Oil Palm, 0.29%

Oilseeds, 5.25%

Other crops, 23.17%

Total area: 4.911 bil ha Source: FAO (2011), Oil World, MPOB (2012)

Livestock industry uses the most land and therefore is the main driver for global deforestation. Oil palm has been made a scapegoat

MSPO++ system

No deforestaFon: Applies to companies that are plan3ng oil palm on land for first 3me at 3me of applica3on. Such companies have to undergo a sustainability cer3fica3on. Free to choose any cer3fica3on system recognized by MPOCC.

PlanFng on peat: Applies to companies that are plan3ng oil palm on peat land for first 3me at 3me of applica3on. Such companies have to undergo a sustainability cer3fica3on. Free to choose any cer3fica3on system recognized by MPOCC.

5. MSPO++ as a Branding Plauorm

Ø As for Branding of Malaysian palm oil, the proposed brand tag line is “Malaysia Palm Oil, Responsibly Farmed”.

Ø ‘Responsibly Farmed’ is claimable based on the licensing infrastructure of the Malaysian palm oil industry.

Ø Sustainable claim is tricky as sustainability is subject to different defini3ons in the EU. This issue must be carefully analyzed going forward.

BRAND LOGO

Once Branding Scheme launched, responsibly produced Malaysia Palm Oil will be given a Brand name and logo

• CPO price has retreated from its high. Long term, prices have been remunera3ve

• MPOC con3nues to look for opportuni3es to boost palm oil trade

• Some examples of MPOC facilita3ng the capitaliza3on of such opportuni3es to strengthen markets, find newer markets and tapping on new opportuni3es are shown

• Need to have an overarching system such that all Malaysian Palm Oil can be claimed to be “sustainably” or “responsibly produced”

• MSPO is ready to be launched and MSPO++ can be added subsequently

• MSPO++ can fast-‐track 100% cer3fica3on of Malaysian palm oil, and Branding of Malaysian palm oil will have a strong unified plaiorm for brand support.

• Branding can facilitate trade and afract a premium of Malaysian palm oil

6. CONCLUSIONS

THANK YOU Visit my blog and tweets by visiting MPOC’s website

http://www.mpoc.org.my