tax administrations in a post beps environment 20 & 21 april 2015 jeffrey owens

TRANSCRIPT

Tax Administrationsin a post BEPS environment

20 & 21 April 2015 Jeffrey Owens

Table of Contents:

The Changing Relationship in taxpayer, tax administration and tax advisor interaction

Pressures vs Opportunities in the international tax world BEPS Exchange of Information Country by Country Reporting

The Role of Technology

How to benefit from a more transparent and cooperative environment

Moving Forward: What will tax administrations look like in 10 years

The taxpayer, tax administration and tax advisor: A changing relationship

The new cooperative way of building tax compliance: The old model:

Operating only by reference to legal requirements Limited disclosure and no signals of uncertainty Low levels of trust

Towards an enhanced cooperative relationship: Establishing and sustaining mutual trust Disclosure and transparency from taxpayers Revenue body approach based on commercial awareness,

openness and responsiveness.

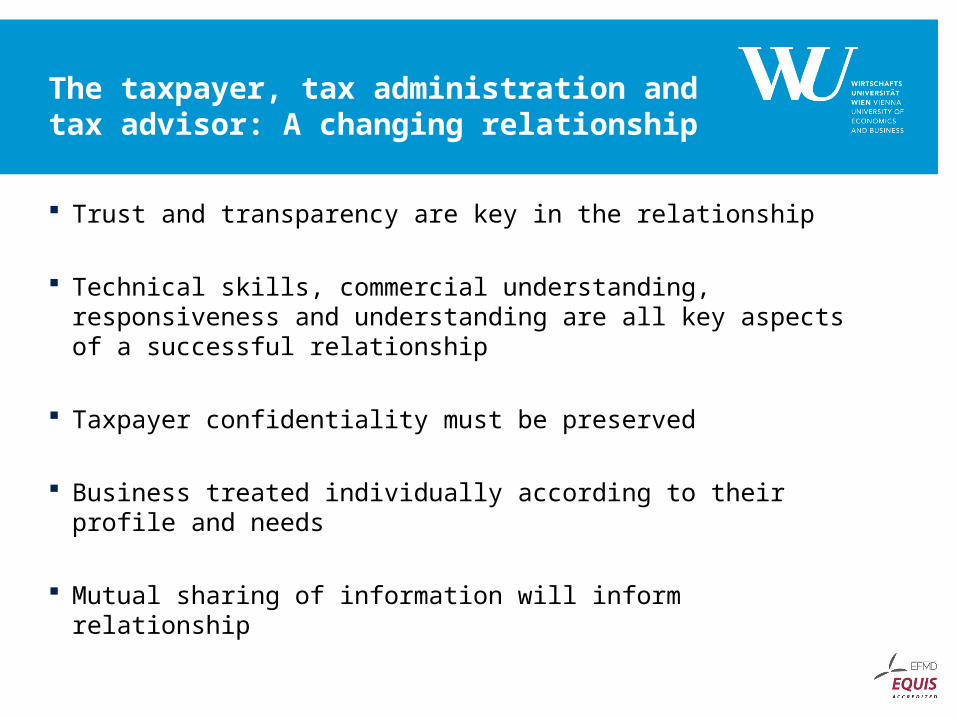

The taxpayer, tax administration and tax advisor: A changing relationship

Trust and transparency are key in the relationship

Technical skills, commercial understanding, responsiveness and understanding are all key aspects of a successful relationship

Taxpayer confidentiality must be preserved

Business treated individually according to their profile and needs

Mutual sharing of information will inform relationship

Pressures vs opportunities in the international tax world

BEPS

Exchange of Information

Country by Country Reporting

Technology Development

Reflection Points: Are tax administrations geared up to use this information?

How could tax administrations benefit from a more cooperative environment?

BEPS

EMERGING NEW INTERNATIONAL STANDARDS: A CHALLENGE FOR MNES

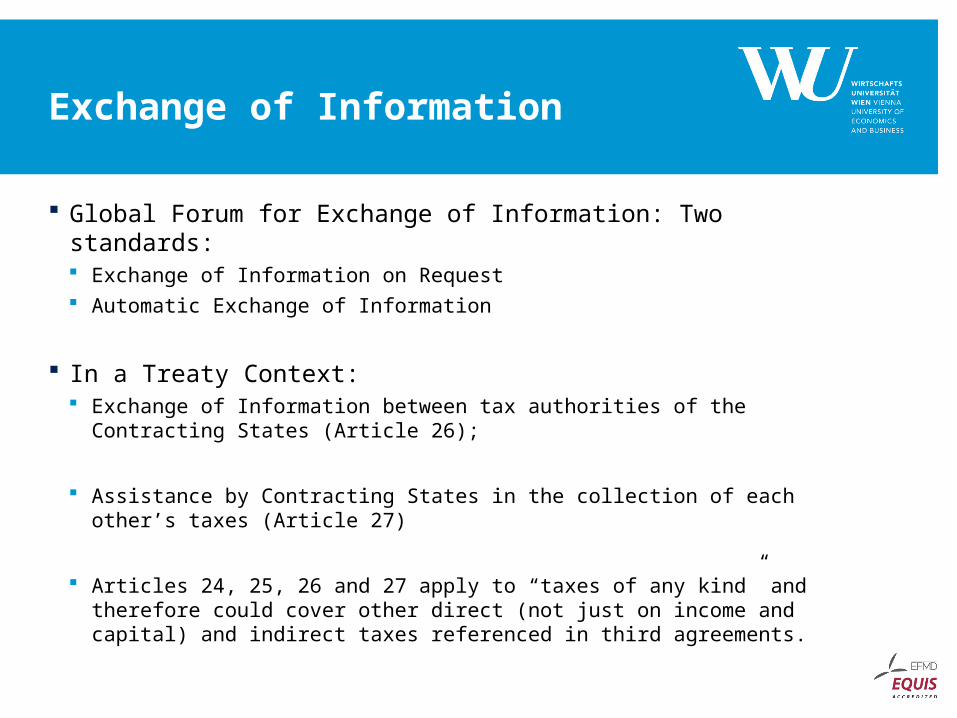

Exchange of Information

Global Forum for Exchange of Information: Two standards: Exchange of Information on Request Automatic Exchange of Information

In a Treaty Context: Exchange of Information between tax authorities of the Contracting

States (Article 26);

Assistance by Contracting States in the collection of each other’s taxes (Article 27)

Articles 24, 25, 26 and 27 apply to “taxes of any kind” and therefore could cover other direct (not just on income and capital) and indirect taxes referenced in third agreements.

Country by Country (CbC)

Reporting

CbC reporting: getting a good look inside

What it is: Companies will have to provide tax authorities with country-specific allocation of profits, revenues, employees and assets; worldwide adoption expected by 2017, though specific adoption deadlines will vary by country.

What it is not: Not intended as a substitute for a full transfer pricing analysis, nor is it intended for use in formulary apportionment-based adjustments. But it will feed into tax audits.

Fully understand the requirements and how those requirements could be met with your current reporting efforts. Do a thorough analysis to understand what reporting gaps you might have and devise a strategic plan that allows enough time to ensure proper and accurate reporting.

Why this is an early focus: Because of the level of complexities involved with cross-border transactions, and data collection and management, many companies should begin preparing now, testing and validating processes and technologies. This will allow time to take mitigating steps – e.g., ensuring profit margin consistency (Inter-Company Effectiveness) and minimizing potential controversy..

Next steps:

TP Master file

TP Local file

CbC report

CbC Reporting

Country by Country (CbC) Reporting

Key considerations

How to source the data

Rapid flow of new reporting and disclosure requirements have left both tax departments and software houses rushing to catch up

Many companies approaching on a phased basis (Excel spreadsheet versus systems integration)

Vendor market will catch up

Moving from year 1 to sustainability – investment, integration, analytics

How to assess the data – the search for anomalies. For example:

Should parent company or local company GAAP be used as a basis for reporting?

How can the company avoid misinterpretation of data, such as reporting ordinary profits in addition to profits after extraordinary items?

Does the company have accurate information on global operations - including headcount, revenues and profits by country?

Has the company identified features listed as potentially indicative of transfer pricing risk?

Does the company have significant transactions with a low tax jurisdiction?

Does the company have transfers of IP to related parties?

Has the company experienced a business restructuring?

OECD CbC template – main reporting table

– country aggregated data

Tax jurisdiction

Revenues

Profit (loss) beforeincome tax

Cash tax paid (CIT and WHT)

Current year tax accrual

Stated capital

Accumulated earnings

Tangible assets other than cash and cash equivalents Number of

employees

Unrelated party

Related party Total

1.

2.

3.

4.

5.

6.

7.

Etc. Notes:► Aggregated rather than consolidated data► Flexibility in data sources allowed► Entity data aggregated on the basis of tax residence► Revenue defined to include turnover, royalties, property, interest► Revenue specifically excludes intercompany dividends► Profit/loss before income tax includes extraordinary items► Cash tax paid includes tax withheld by other parties on payments to the constituent entity► Current year tax accrual is tax on current year operations only► Number of employees may include external contractors

OECD CbC template – table 2

– entity details

Notes:► Constituent entities rather than legal entities► Multiple activities may be chosen

Tax jurisdiction

Constituent entities resident in the tax jurisdiction

Tax jurisdiction of organization or incorporation if different from tax jurisdiction of residence

Main business activity(ies)

R&D

Holding or managing IP

Purchasing or

procurement

Mfg or production

Sales, mktg or distribution

Admin., mgmt or support services

Provision of services to unrelated parties

Internal group finance

Regulated financial services

Insurance

Holding shares or other equity instruments

Dormant

Other

1.

2.

3.

1.

2.

3.

Etc.

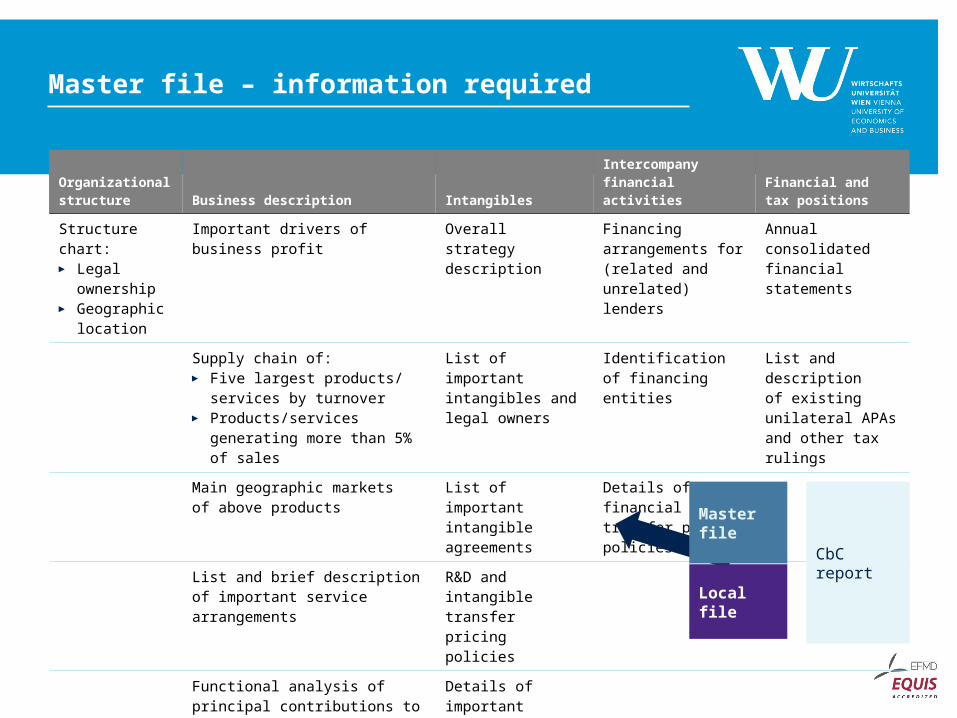

Master file – information required

Organizational structure Business description Intangibles

Intercompany financial activities

Financial and tax positions

Structure chart:► Legal

ownership► Geographic

location

Important drivers of business profit

Overall strategy description

Financing arrangements for (related and unrelated) lenders

Annual consolidated financial statements

Supply chain of:► Five largest products/

services by turnover► Products/services generating

more than 5% of sales

List of important intangibles and legal owners

Identification of financing entities

List and description of existing unilateral APAs and other tax rulings

Main geographic markets of above products

List of important intangible agreements

Details of financial transfer pricing policies

List and brief description of important service arrangements

R&D and intangible transfer pricing policies

Functional analysis of principal contributions to value creation by individual entities

Details of important transfers

Business restructuring/ acquisitions/divestitures during fiscal year

Master file

Local file

CbC report

Other analysis

► Global footprint by business activity

► Comparison of profit margins

► Pie charts to illustrate “absolute amounts”

► Filters

► Income per head► Tax rate comparison► Related-party revenues

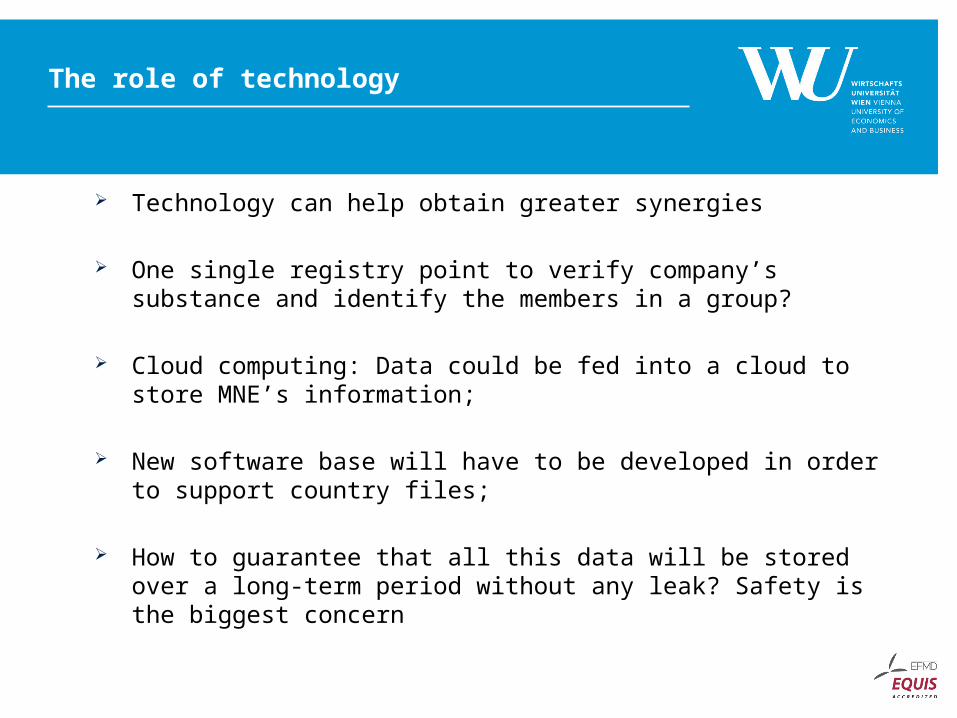

The role of technology

Technology can help obtain greater synergies

One single registry point to verify company’s substance and identify the members in a group?

Cloud computing: Data could be fed into a cloud to store MNE’s information;

New software base will have to be developed in order to support country files;

How to guarantee that all this data will be stored over a long-term period without any leak? Safety is the biggest concern

How to benefit from a more cooperative

and transparent environment?

► Main Advantage for Governments:► Transparency and disclosure by business► Willingness to go beyond respecting just the strict letter of the law► Volunteering information which may highlight significant differences of

opinion and interpretation► Willingness of business to educate tax administrations on the realities

of new business models► Cooperation in tax assessment

► Main advantage for business:► Greater certainty and predictability► Commercial and business awareness in tax administrations► Access to decision makers in tax administrations► Consultation on tax policy issues► Speedy conflict resolution system

Moving forward: What will tax administrations

look like in 10 years

Tax administrations will be stripped of policy functions; Leaner and flatter tax administrations by making use of technology; Assessment and collection functions will be outsourced Good taxpayer service Constructive and transparent dialogue between taxpayers, tax authorities and

their advisors Tax will focus on prevention rather than detection and non-compliance Move away from a tax-by-tax approach to a more taxpayer by taxpayer approach Special units to deal with groups of taxpayers i.e. large business units, SMEs, etc. More sophisticated approach to risk management, based on new technology

resources and segmentation Behavioural approach towards compliance (help taxpayers who want to be

compliant and target those who do not)

Moving forward: What will tax

administrations look like in 10 years

Financial institutions will become an integrated part of the tax assessment process

Pre-audit settlements will become the norm Joint multilateral audits will become the norm amongst different tax

administrations National fiscs will operate as global bodies Bilateral agreements will be substituted by multilateral agreements Global system of tax arbitration to resolve issues not handled by competent

authorities Non-revenue function of tax administrations will develop – they will raise to the

new role of global regulators.

Thank you!

Jeffrey Owens

Director WU Global Tax Policy Center

Institute for Austrian and International Tax Law

WU Vienna University of Economics and Business