tax treaties: a curse or a blessing?

TRANSCRIPT

Tax Trea'es A curse or a blessing?

Research on Developing Countries JUDr. Tomas Balco, LL.M., ACCA Ministry of Finance of Slovakia

ICTD

Introduc'on • Chartered Cer'fied Accountant – ACCA (FCCA) • 3 law degrees

– Doctor in Law (Interna'onal Law) – Magister in Law – Postgraduate LL.M. in Interna'onal Tax Law (Vienna)

• Work Experience – Slovakia (MoF), Kazakhstan (KIMEP University & CATRC, PwC), Netherlands (IBFD),

Czech Republic (MoF, DeloiWe),Chile (MoF), Belgium (European Commission)

• Other – Since 2008 – Member of SubcommiWees -‐ UN CommiWee of Experts – Projects (World Bank, IFC, USAID, EU)

• Focus of Research and Tax Policy Work – Interna'onal Taxa'on, Extrac've Industry, Financial Sector

• Proud to teach – ITC Leiden University (Netherlands), KIMEP University (Kazakhstan), IBDT Brazil,

African Ins'tute – University of Pretoria (SA), University of Lausanne (CH)

Rela'onship with ICTD • Introduced to Mick Moore by Sol PiccioWo in Spring 2014 • Draa Working Papers

– Introduc'on to Extrac've Industry Taxa'on – Tax Treaty Issues in Extrac've Industry

• hWp://www.un.org/esa/ffd/tax/tenthsession/CRP3_AWachmentE_TreatyIssues.pdf

• New Tax and Development Short course at IDS, in partnership with ICTD and ATAF – Interna'onal Taxa'on and Extrac've Industry

• Monday 26th – Thursday 29th January 2015, IDS (Brighton, UK) • hWp://www.ids.ac.uk/tax-‐course

• REDE Project proposals – Protec'ng the Source Tax Base (Pilot Project – 3 months) – Extrac've Industry Taxa'on

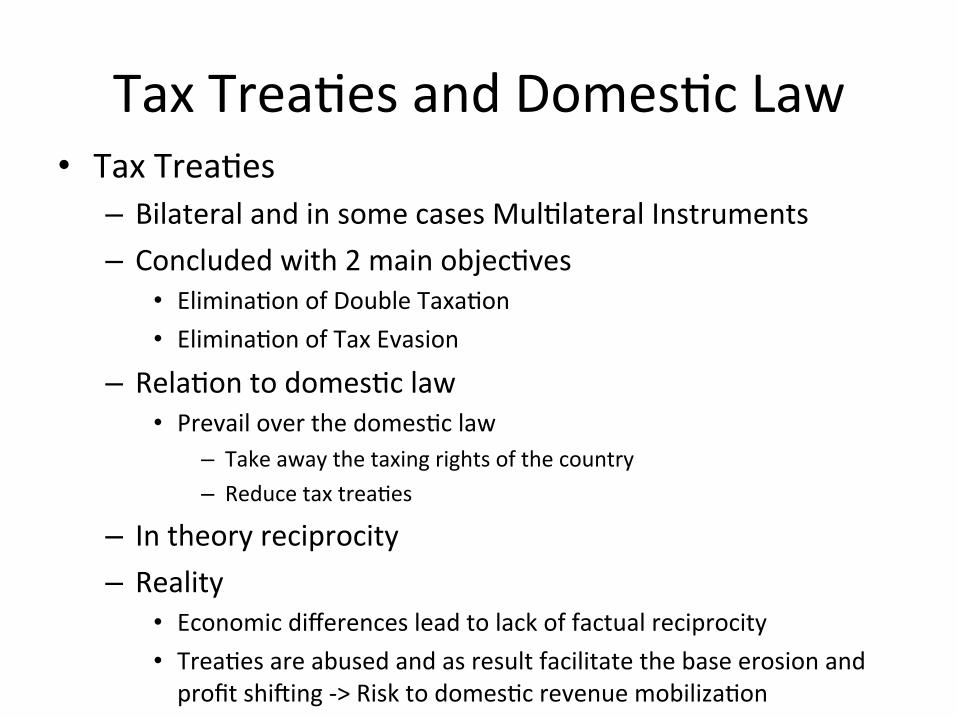

Tax Trea'es and Domes'c Law • Tax Trea'es

– Bilateral and in some cases Mul'lateral Instruments – Concluded with 2 main objec'ves

• Elimina'on of Double Taxa'on • Elimina'on of Tax Evasion

– Rela'on to domes'c law • Prevail over the domes'c law

– Take away the taxing rights of the country – Reduce tax trea'es

– In theory reciprocity – Reality

• Economic differences lead to lack of factual reciprocity • Trea'es are abused and as result facilitate the base erosion and profit shiaing -‐> Risk to domes'c revenue mobiliza'on

Domes'c Law – Source Taxa'on • Can a good tax treaty solve the problem?

– No – it starts by domes'c law • Where domes'c law comes short – treaty does not remedy

• Taxa'on of income having a source in the country • Payments made from country • Ac'vi'es carried in the country • Deduc'ons made in the country • Other nexus to the jurisdic'on (e.g. Capital Gains from Indirect transfer of shares)

• Cri'cal factors – Defini'on of income having source in country

• Absence of defini'on – no tax liability – Tax Collec'on and enforcement mechanism

• Absence of collec'on mechanism = non-‐compliance – An'-‐abuse provisions

• An'-‐base erosion and profit shiaing rules

Domes'c Law & DTT Overlap

Domes'c Law – Source Taxa'on

Collec'on mechanism

Tax Treaty

Tax Trea'es

• Benefits of Tax Trea'es • Poten'al Loss of Revenue • Examples of Treaty Abuse • How to stop the Abuse? • Tax Treaty Applica'on

– Issues Arising – Refund and Automa'c Applica'on

• Tax Policy and Administra'on Considera'ons

Benefits of Tax Trea'es (Elimina(on of Double Taxa(on)

– Exclusive Taxing Rights (Usually state of residence) • But…Country of Source (Usually the Developing Country) is loosing the right to tax

– In theory reciprocity… but in reality…. Flow of investment vs. oumlow of resources, profits and tax base…

– Credit and Exemp'on • But… can be achieved by domes'c law the Country of Residence (Country of investor)

– Mutual Agreement Procedure • But… countries may oaen have different perspec'ves and agreement may not be reached

Benefits of Tax Trea'es (Comba(ng tax evasion)

• Exchange of Informa'on – Yes, but oaen 'mes limited ability to determine what informa'on is needed

• And limits on what informa'on may be provided – Can be achieved by special agreements on Exchange of Informa'on

• Assistance in Collec'on of Tax Claims – Yes, but s'll rarely used by developing countries

• Can be also achieved by specialized administra've agreements

Poten'al Implica'ons of DTT (for source country)

• Ar'cle 7 – Taxa'on of Business Profits – Loss of Taxing rights on provision of services or commercial ac'vi'es below the Permanent Establishment threshold

• Ques'on? Where/how high is the threshold?

• Ar'cle 8 – Profits of companies carrying out interna'onal transporta'on – These companies may take advantage of special tonnage or other regimes and pay very low tax

• Ar'cle 10, 11, 12 – Reduced Tax Rates on income in form of dividend, interest, royalty – Can also lead to Zero rates if trea'es nego'ated wrongly

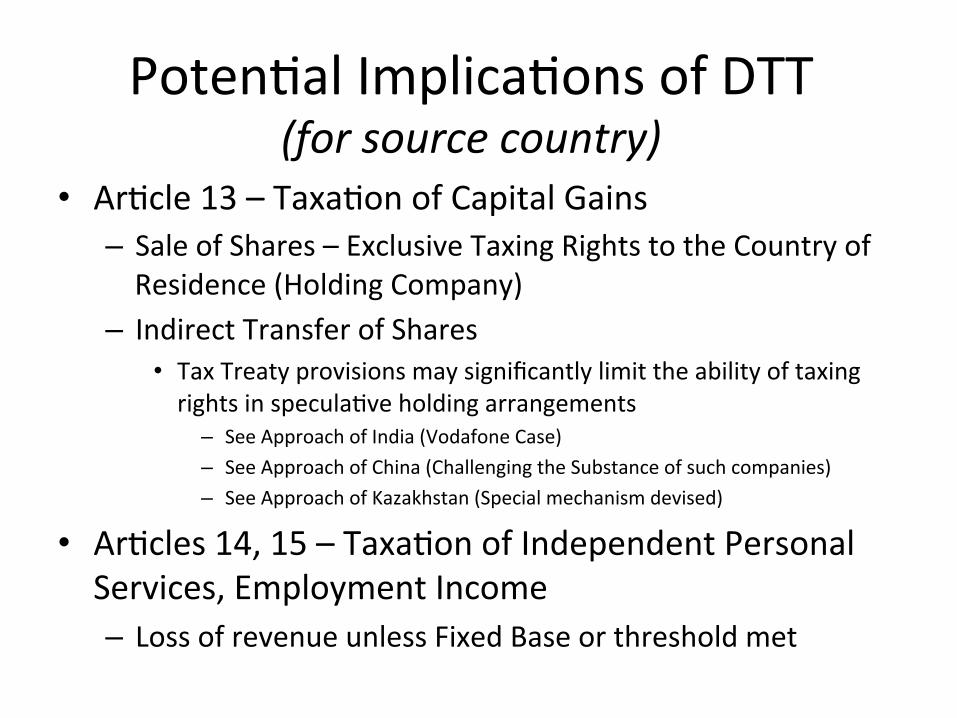

Poten'al Implica'ons of DTT (for source country)

• Ar'cle 13 – Taxa'on of Capital Gains – Sale of Shares – Exclusive Taxing Rights to the Country of Residence (Holding Company)

– Indirect Transfer of Shares • Tax Treaty provisions may significantly limit the ability of taxing rights in specula've holding arrangements

– See Approach of India (Vodafone Case) – See Approach of China (Challenging the Substance of such companies) – See Approach of Kazakhstan (Special mechanism devised)

• Ar'cles 14, 15 – Taxa'on of Independent Personal Services, Employment Income – Loss of revenue unless Fixed Base or threshold met

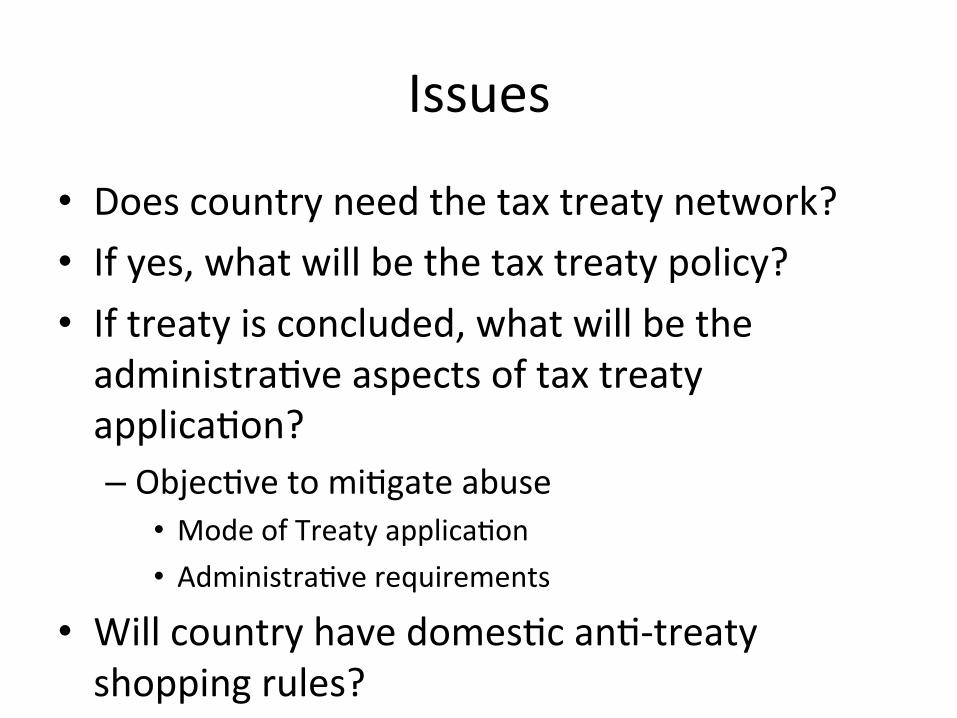

Issues

• Does country need the tax treaty network? • If yes, what will be the tax treaty policy? • If treaty is concluded, what will be the administra've aspects of tax treaty applica'on? – Objec've to mi'gate abuse

• Mode of Treaty applica'on • Administra've requirements

• Will country have domes'c an'-‐treaty shopping rules?

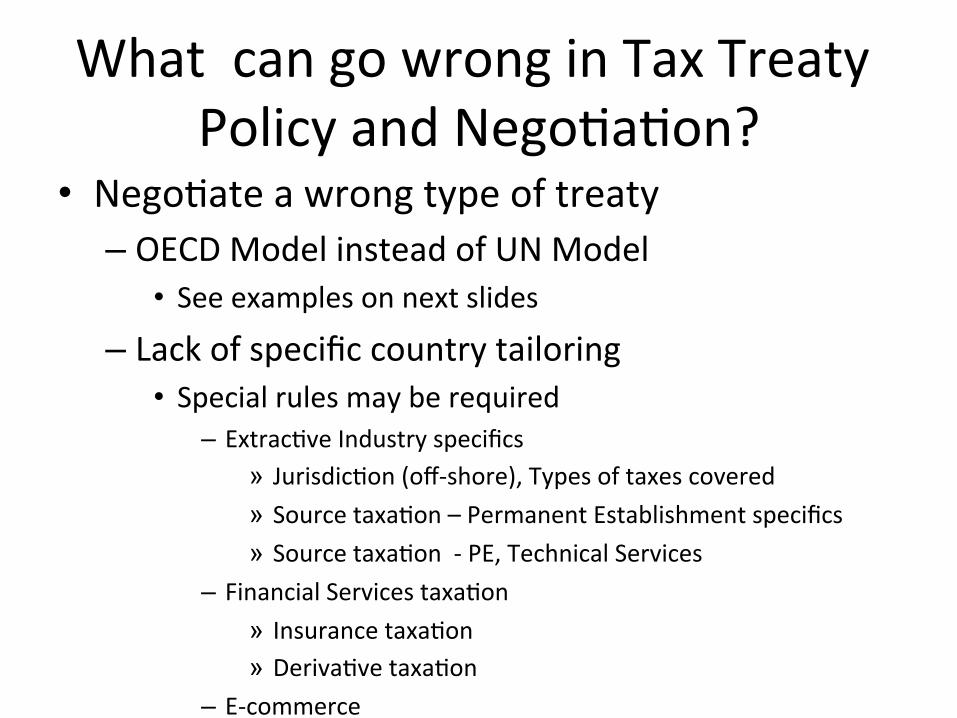

What can go wrong in Tax Treaty Policy and Nego'a'on?

• Nego'ate a wrong type of treaty – OECD Model instead of UN Model

• See examples on next slides

– Lack of specific country tailoring • Special rules may be required

– Extrac've Industry specifics » Jurisdic'on (off-‐shore), Types of taxes covered » Source taxa'on – Permanent Establishment specifics » Source taxa'on -‐ PE, Technical Services

– Financial Services taxa'on » Insurance taxa'on » Deriva've taxa'on

– E-‐commerce

Example – Mongolia Outcome of 2011 ADB Seminar -‐ Tokyo

Example of Fatal Error -‐ Dividends (Mongolia – Netherland’s DTT)

15

Paragraph 3 effectively reverses – paragraph 2 Paragraph 2 – looks like very good deal for developing country

Paragraph 3 – takes it down to Zero – most likely only one country will benefit from this provision

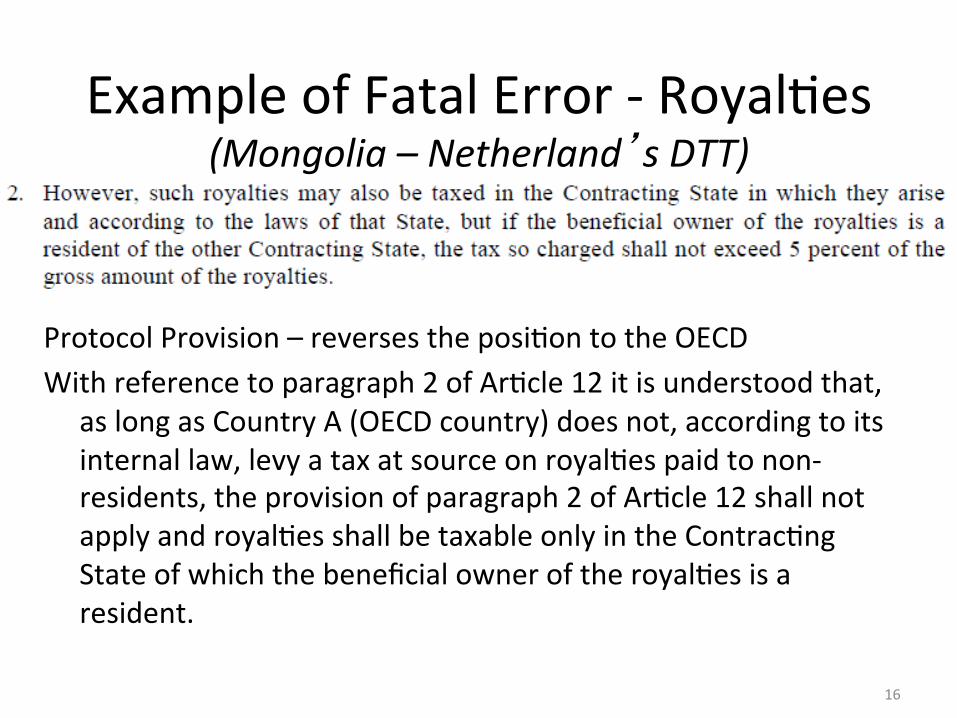

Example of Fatal Error -‐ Royal'es (Mongolia – Netherland’s DTT)

Protocol Provision – reverses the posi'on to the OECD With reference to paragraph 2 of Ar'cle 12 it is understood that,

as long as Country A (OECD country) does not, according to its internal law, levy a tax at source on royal'es paid to non-‐residents, the provision of paragraph 2 of Ar'cle 12 shall not apply and royal'es shall be taxable only in the Contrac'ng State of which the beneficial owner of the royal'es is a resident.

16

What to do? • Why did developed country put developing country in such a posi'ons – is it dealing with equals? Ethics?

• Op'ons? – Renego'ate the tax treaty – Terminate the treaty – Teach them a lesson

• Offer route to the global tax community to access the tax free distribu'on of dividend from this country, which so “fairly” treated the developing country

– May speed up the renego'a'on… 17

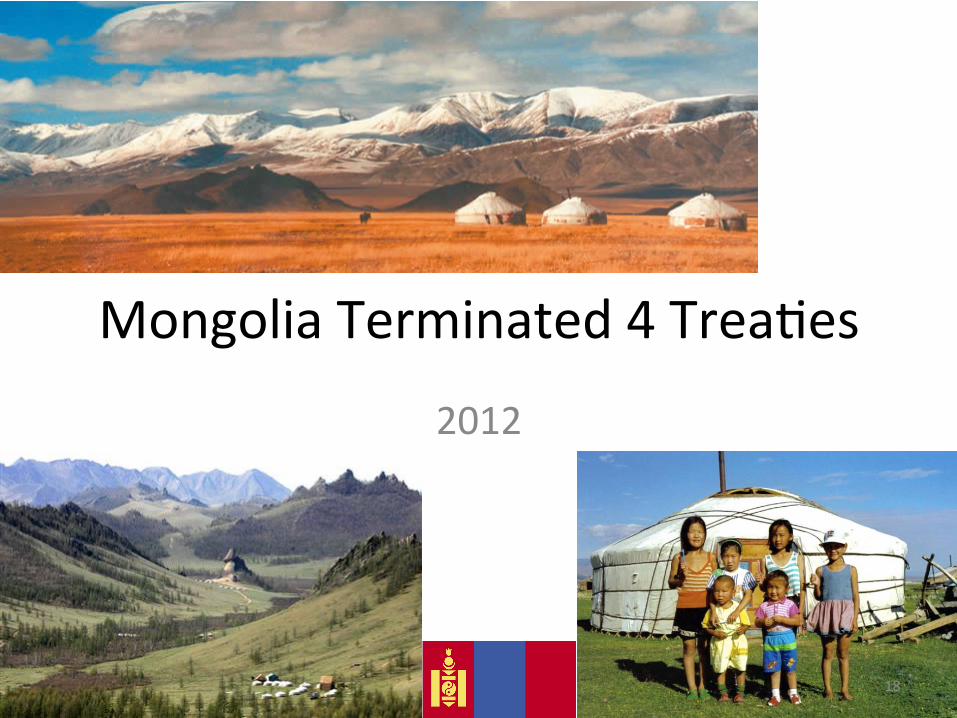

Mongolia Terminated 4 Trea'es

2012

18

How was it solved? Termina'on of 4 Tax Trea'es by Mongolia

• Mongolia has recently (28.11.2012) adopted a law to terminate 4 tax trea'es: – Netherlands (effec've 1.1.2014) – Luxemburg (effec've 1.1.2014) – Kuwait (effec've 1.1.2015) – UAE (effec've 1.1.2015)

19

Reasons? Netherlands

– Art 10 (2) – 15% WHT / However (10/3) 0% if BO of the dividends is a company the capital of which is wholly or partly divided into shares …(?)

– Art 12 (2) – 5% WHT / However (Protocol) as long as under internal law NL does not levy WHT on royalty – Exclusive taxing to country of residence

– Ar'cle 13 – Sale of shares – Exclusive Taxing right to State of Residence

20

Reasons? Luxemburg

– Art 10 (2) – 5% / 15% WHT / However (10/3) 0% if BO holds > 25% of shares for longer than 12 months

– Art 11 (2) – 10% WHT / However (11/3) 0% for any bank loans, commercial debt and bank deposits

– Ar'cle 13 – Sale of shares – Exclusive Taxing right to State of Residence

21

Reasons? Kuwait and UAE

Kuwait UAE Dividend 5% (Gov

exemp'on) 0%

Interest 5% (Gov exemp'on)

0%

Royalty 10% 10% Capital Gains

Exclusive -‐ Residence

Exclusive -‐ Residence

22

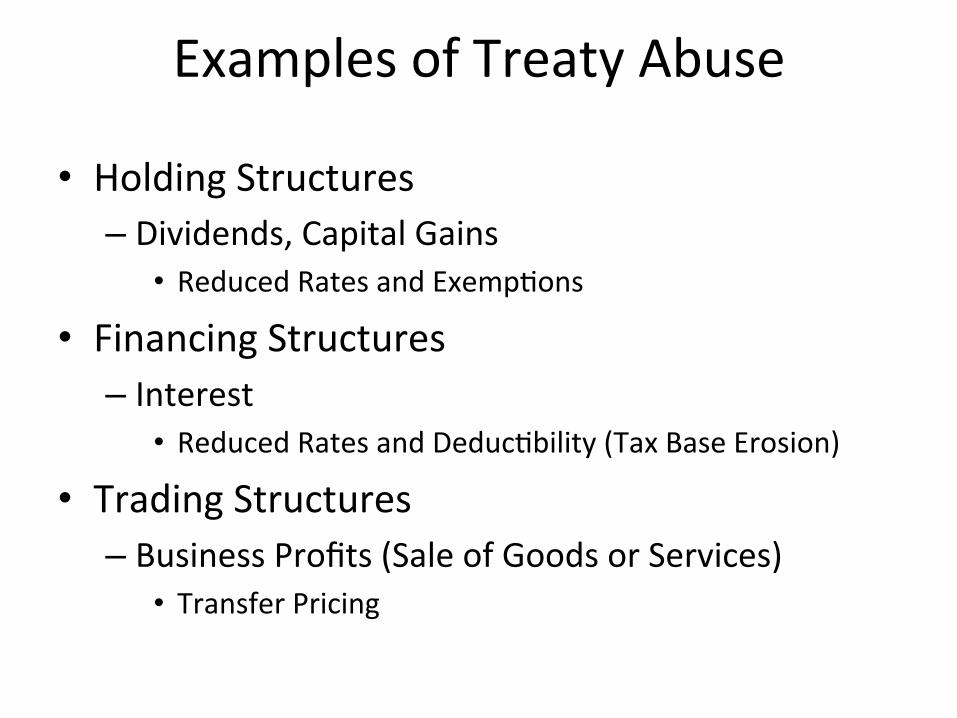

Examples of Treaty Abuse

• Holding Structures – Dividends, Capital Gains

• Reduced Rates and Exemp'ons

• Financing Structures – Interest

• Reduced Rates and Deduc'bility (Tax Base Erosion)

• Trading Structures – Business Profits (Sale of Goods or Services)

• Transfer Pricing

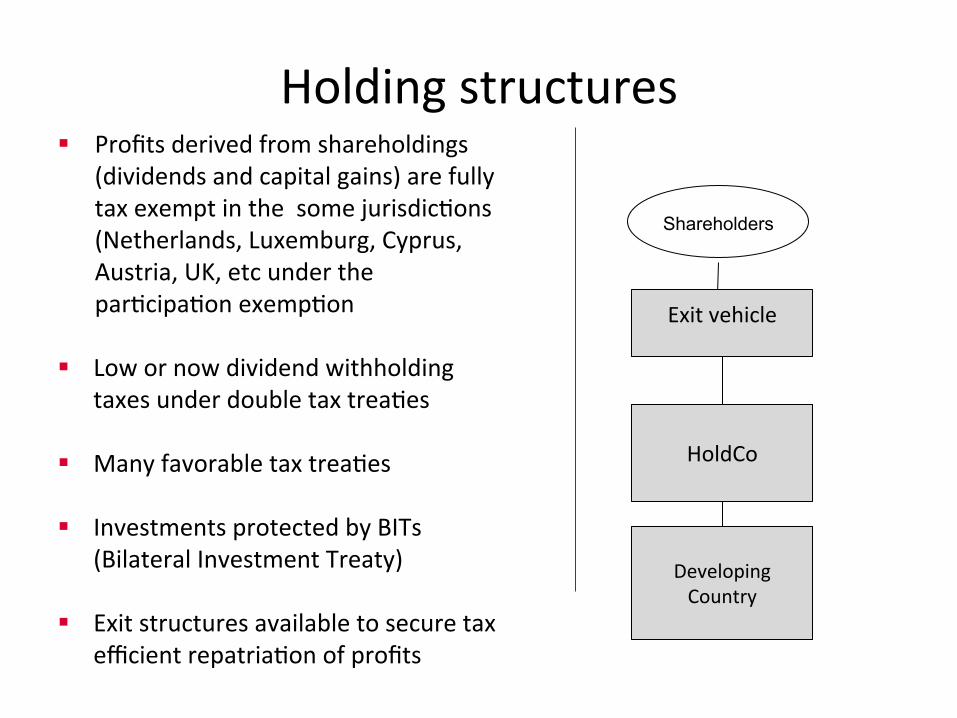

Holding structures § Profits derived from shareholdings

(dividends and capital gains) are fully tax exempt in the some jurisdic'ons (Netherlands, Luxemburg, Cyprus, Austria, UK, etc under the par'cipa'on exemp'on

§ Low or now dividend withholding taxes under double tax trea'es

§ Many favorable tax trea'es

§ Investments protected by BITs (Bilateral Investment Treaty)

§ Exit structures available to secure tax efficient repatria'on of profits

Shareholders

HoldCo

Developing Country

Exit vehicle

Example 1 – Direct Sale of Shares

• Company A sells shares in C to company B

• DTT 13 (4) missing • DTT between A – C takes away taxing right from Country C -‐> no taxa'on in country C, Country A exempts Capital Gains from tax under domes'c rules -‐> double non-‐taxa'on

C

B A

Example 2 – Indirect Transfer of Shares

• Indirect transfer of shares in C via sale of shares of company D – Country C may loose the taxing right, since the shares that are sold

are not shares of C, but that of D – outside of the jurisdic'on – Extra-‐territorial Capital Gain

• India (Vodafone Cas) • China approach • Kazakhstan rules

– OECD vs UN DTT Model rules – Cri'cal aspects:

• Tax Treaty provisions – UN vs. OECD

• Domes'c Law – Broader Source Defini'on – Immovable property defini'on

A

D

C

B

Financing, Royalty, Services structures § Interest, Royalty, Services deduc'ble in the country of source § Intermediary company in Tax Treaty jurisdic'on – using the tax treaty, the country of source either losses the taxing right (services) or the WHT may be limited (also down to Zero). Cri'cal factor for success – the intermediary jurisdic'on does not levy WHT on these payments (either based on domes'c law or DTT) § Mi'ga'on? § Consistent tax treaty network,

limita'on to deduc'bility

Loan or Hybrid Instrument

Loan or Equity

Intermediatry Company

Off-‐shhore

Opera'ng Companies

Source – Atlas Tax Lawyers

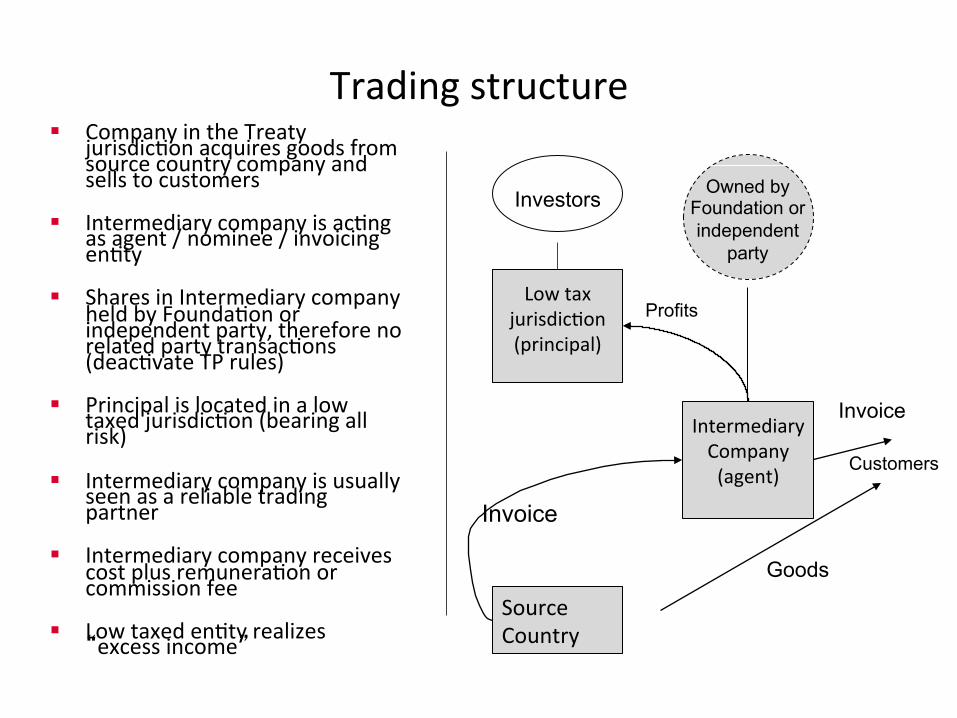

Trading structure § Company in the Treaty

jurisdic'on acquires goods from source country company and sells to customers

§ Intermediary company is ac'ng as agent / nominee / invoicing en'ty

§ Shares in Intermediary company held by Founda'on or independent party, therefore no related party transac'ons (deac'vate TP rules)

§ Principal is located in a low taxed jurisdic'on (bearing all risk)

§ Intermediary company is usually seen as a reliable trading partner

§ Intermediary company receives cost plus remunera'on or commission fee

§ Low taxed en'ty realizes “excess income”

Investors

Source Country

Invoice

Invoice

Low tax jurisdic'on (principal)

Intermediary Company (agent)

Goods

Customers

Owned by Foundation or independent

party

Profits

Tanzanian Tax Treaty Network (9+ DTT’s) Dividends Interest Royalties

Individuals, companies

Qualifying companies

(%) (%) (%) (%) Canada 25 20 15 20 Denmark 15 15 12.5 20 Finland 20 20 15 20 India 10 5 10 10 Italy 10 10 15 15 Norway 20 20 15 20

South Africa 20 10 10 10

Sweden 25 15 15 20 Zambia 0 0 0 0

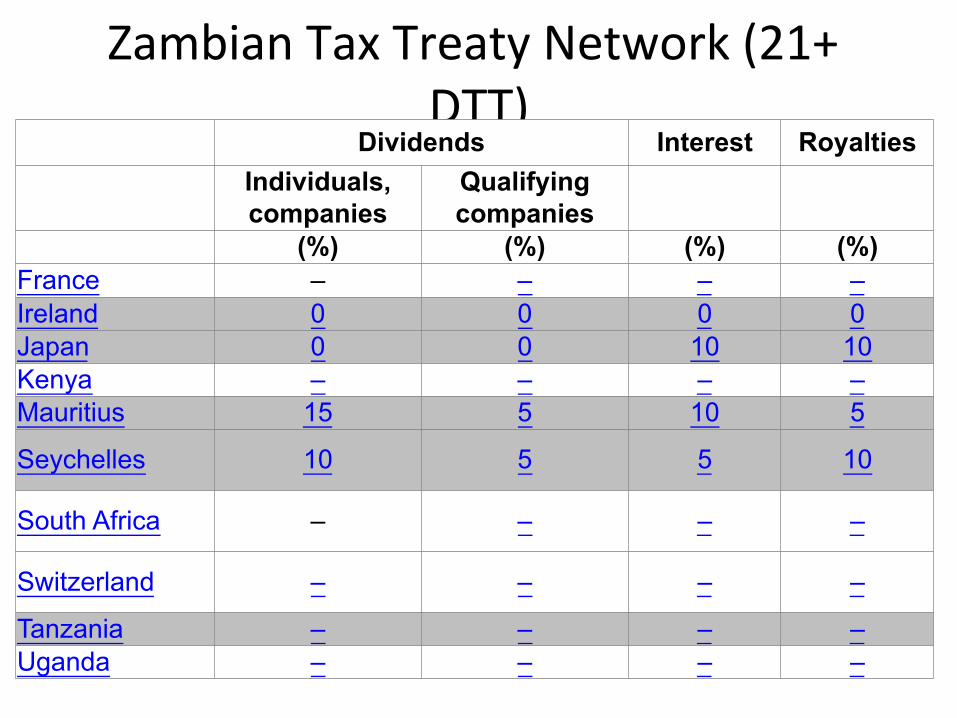

Zambian Tax Treaty Network (21+ DTT)

Dividends Interest Royalties

Individuals, companies

Qualifying companies

(%) (%) (%) (%) France – – – – Ireland 0 0 0 0 Japan 0 0 10 10 Kenya – – – – Mauritius 15 5 10 5

Seychelles 10 5 5 10

South Africa – – – –

Switzerland – – – –

Tanzania – – – – Uganda – – – –

South African Tax Treaty Network (73 DTT) Dividends Interest Royalties

Individuals, companies

Qualifying companies

Cyprus 0 0 0 0 Grenada – – – – Hungary 15 5 0 0 Ireland 10 5 0 0 Kuwait 0 0 0 10 Luxembourg 15 5 0 0 Malawi – – – 0 Mauritius 15 5 0 0 Netherlands 10 5 0 0 Norway 15 5 0 0 Seychelles 10 5 0 0 Sierra Leone – – – – Zambia – – 0 – Zimbabwe – – – –

How to limit the abuse? • Domes'c An'-‐Abuse Provisions

• General An'-‐avoidance Rule • Many Developing Countries do not have them

• Special rules • Domes'c law based An'-‐treaty shopping • Transfer Pricing, • Thin-‐Cap and other deduc'on limita'on rules • WHT on payments to Tax Havens -‐ Black list

• Tax Treaty Based An'-‐Avoidance Rules • Limita'on of Benefits Clause

• Ac'on 6 BEPS -‐ recommenda'on • Beneficial Ownership requirement

• Only limited to Ar'cles 10, 11, 12

Refund vs. Automa'c Applica'on

• Issue • Inappropriate applica'on of DTT

• Lack of en'tlement • Transparent en'ty? • Exempt en'ty • En'ty in Special Economic Zone • En'ty ac'ng as agent/intermediary

• SoluEon • Special procedures for applica'on of DTT

• Refund mechanism (Subject to administra've review) • Approval process • Automa'c applica'on (subject to requirements) • Automa'c applica'on (no-‐requirements)

• Minimum requirements – Requirement of Cer'ficate of Residence

– Extreme – always with Apos'l or Legaliza'on – Affidavit on Beneficial Ownership

Tax Treaty Applica'on

• 3 Approaches – Detailed regula'ons and procedures

• Most aspect of Treaty Applica'on regulated in detail – Some degree of guidance and regula'on

• Providing some sporadic guidance – Refund vs. Automa'c Treaty Applica'on

– Hardly any guidance • Minimum – level – establishing the role of trea'es in rela'on to Tax Code

• No proper guidance, no proper forms

Tax Policy and Tax Administra'on Considera'ons

• Different levels of aWen'on to DTT • Level of Capacity

– To Legislate and Nego'ate Tax Trea'es • Limited knowledge of the concepts and principles

– To Administer and Audit • Lack of qualified staff • Limited systems (sources of informa'on)

– To resolve disputes • Limited competencies to nego'ate MAP • Mostly absence of Arbitra'on provisions

– Where they exist – they are not ac'vated as required

– Challenge in form of harmful tax compe''on – Conflic'ng interest of different countries

Focus of Source Tax Base Protec'on Project • Stage 1

– Country specific research -‐ Throw a net and collect a sample of issues – Country specific problems in domes'c law – shortcomings in defini'ons, collec'on mechanism,

lack of an'-‐abuse provisions – Country Specific Good or Genius prac'ces – developing countries some'mes tend to come up

with some original ideas on how to deal with challenges (Tax Collec'on mechanism, Defini'ons, Limita'ons to deduc'bility)

• Stage 2 – Analyze, Summarize and Generalize

• What are the common issues and problems? • What are the areas requiring further study/research – is something missing in OECD BEPS project?

• Stage 3 – Recommenda'ons

• Country Specific and also General Recommenda'ons

• Stage 4 – Findings dissemina'on

• Policy Maker mee'ngs, delivery of recommenda'on, contribu'on to regional discussion