taxation} tax i

TRANSCRIPT

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 1/81

TAX NOTES (LEGAL GROUND)

Lectures of Atty. Japar B. Dimampao

Supplement Bar Material

STATE POLICY

Declared Policy of the State: (CodeRD!"N)

1) to promote sustainable economic growth through the rationalization of the Philippine

internal revenue tax system, incluing tax aministration!") to provie, as much as possible, an e#uitable relief to a greater number of taxpayers in

orer to improve levels of isposable income an increase economic activity!

$) to create a robust environment for business to enable firms to compete better in the

regional as well as the global mar%et!

&) the State ensures that the 'overnment is able to provie for the nees of those uner its

(urisiction an care

T#E !$I$R$

1) Po%er& a'd dtie& of the !IR$

*he B+ shall be uner the supervision an control of the -./ an its powers an uties

shall comprehen: (CODE ACE"P)

1) the assessment!

") collection of all national internal revenue taxes, fees, an charges!

$) the enforcement of all forfeitures, penalties, an fines!

&) execution of (ugments in all cases ecie in favor by the 0* an orinary courts

2) give effect an to aminister the supervisory an police powers conferre to it by the

0oe an other laws

") PO*ERS of the Co++i&&io'er of the I'ter'al Re,e'e$

1) to interpret tax laws an to ecie tax cases 3Sec &)!

") to obtain information an to summon, examine, an ta%e testimony of persons 3Sec 2)!

$) to ma%e assessments an prescribe aitional re#uirements for tax aministration an

enforcement 3Sec 4)!

&) to elegate powers 3Sec 5)!

2) to aminister oaths an ta%e testimony 3Sec 1&)!

4) to ma%e arrests an seizures 3Sec 12)!

5) to assign or re6assign internal revenue officers 3Sec 14 7 15)

RE-UISITES O. A /ALID TAX REGULATION 38+M+**+.9 ./ *; P.<; *.

+9*;P;* *= 8<S)

1) +t must be consistent with the provision of the *ax 0oe") easonable

$) >seful an necessary

&) +t must be publishe in the official gazette or in the newspapers of general circulation

SOURCES O. RE/ENUES

The following taxes, fees and charges are deemed to be national internal revenue taxes :

(CodeIE/PEDO or E/E"PIDO)

1) +ncome tax!

") ;state an onor?s taxes!

$) @alue6ae tax!

&) .ther percentage taxes!

2) ;xcise taxes!

4) -ocumentary stamp taxes! an5) Such other taxes as are or hereafter may be impose an collecte by the Bureau of

+nternal evenue

INCO0E TAX

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 2/81

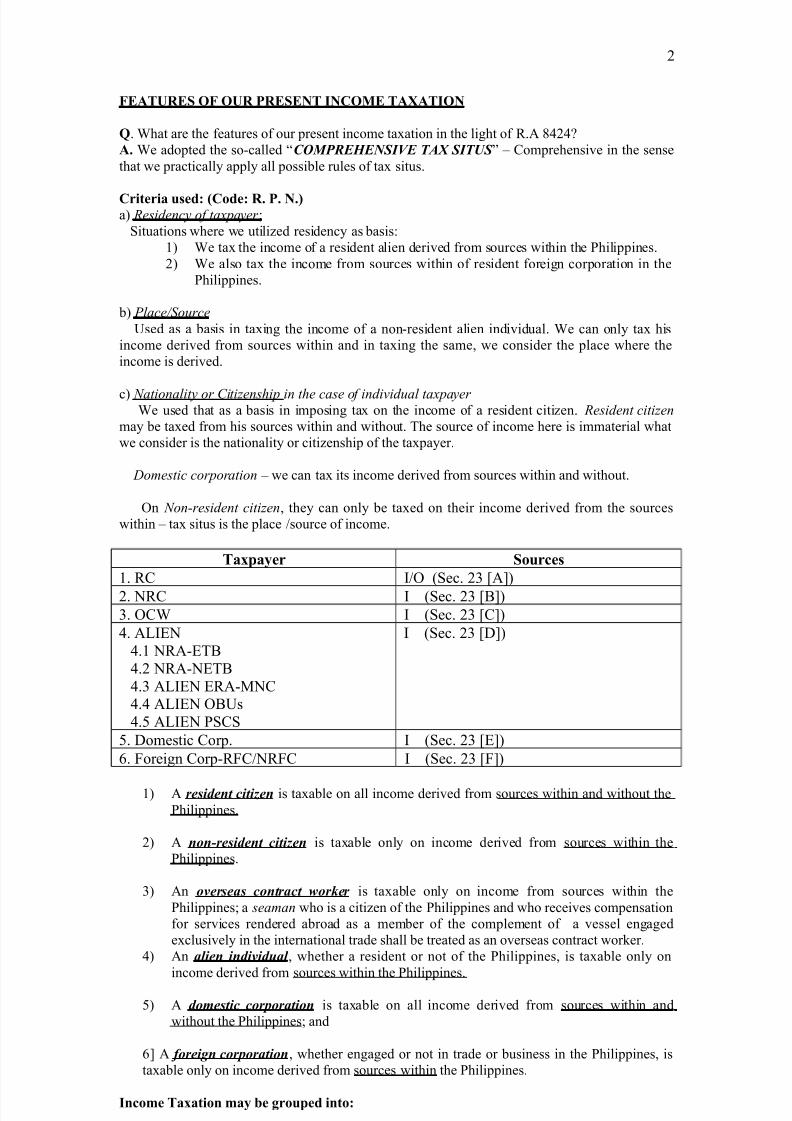

.EATURES O. OUR PRESENT INCO0E TAXATION

- <hat are the features of our present income taxation in the light of A&"&

A$ <e aopte the so6calle C!"#$%&%'()*% TA+ ()T( D E 0omprehensive in the sense

that we practically apply all possible rules of tax situs

Criteria &ed (Code R$ P$ N$)a) Residency of taxpayer!

Situations where we utilize resiency as basis:

1) <e tax the income of a resient alien erive from sources within the Philippines

") <e also tax the income from sources within of resient foreign corporation in the

Philippines

b) Place/Source

>se as a basis in taxing the income of a non6resient alien iniviual <e can only tax his

income erive from sources within an in taxing the same, we consier the place where the

income is erive

c) Nationality or Citizenship in the case of individual taxpayer <e use that as a basis in imposing tax on the income of a resient citizen Resident citizen

may be taxe from his sources within an without *he source of income here is immaterial what

we consier is the nationality or citizenship of the taxpayer

Domestic corporation E we can tax its income erive from sources within an without

.n Non-resident citizen, they can only be taxe on their income erive from the sources

within E tax situs is the place Fsource of income

Ta12ayer Sorce&

1 0 +F. 3Sec "$ GH)

" 90 + 3Sec "$ GBH)

$ .0< + 3Sec "$ G0H)

& 8+;9

&1 96;*B

&" 969;*B

&$ 8+;9 ;6M90 && 8+;9 .B>s

&2 8+;9 PS0S

+ 3Sec "$ G-H)

2 -omestic 0orp + 3Sec "$ G;H)

4 /oreign 0orp6/0F9/0 + 3Sec "$ G/H)

1) resident citi-en is taxable on all income erive from sources within an without the

Philippines

") nonresident citi-en is taxable only on income erive from sources within the

Philippines

$) n overseas contract wor/er is taxable only on income from sources within the

Philippines! a seaman who is a citizen of the Philippines an who receives compensation

for services renere abroa as a member of the complement of a vessel engage

exclusively in the international trae shall be treate as an overseas contract wor%er

&) n alien individual , whether a resient or not of the Philippines, is taxable only on

income erive from sources within the Philippines

2) domestic corporation is taxable on all income erive from sources within an

without the Philippines! an

4H foreign corporation, whether engage or not in trae or business in the Philippines, is

taxable only on income erive from sources within the Philippines

I'co+e Ta1atio' +ay 3e 4ro2ed i'to

"

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 3/81

1) iniviual income taxation

") corporate income taxation

- What are the basic features of individual taxation (S$P$ .$ E$ 0$)

A

5) +niviual income taxation aopte the Schedlar &y&te+ of ta1atio'

Schedlar Sy&te+ of Ta1atio' E is a system employe where the income tax treatment

varies an mae to epen on the %in or category of the taxpayer?s taxable income (an vs! Del

Rosario"!

Characteristics of schedular system of taxation:

a) +t gives or accors ifferent tax treatment on the income of iniviual taxpayer

b) +t classifies income

#anifestations$ 3that uner the iniviual taxation we aopte the scheular system of

taxation)

6C7 !7 P7 D27 I7 R7 R7 D7 A7 P%7 P7 P8

>ner Sec $"3a), income may be categorize as follows:

1) compensation income,

") business income,

$) professional income,&) income erive from ealings in property,

2) interest income,

4) rent income,

5) royalties,

A) iviens,

I) annuities,

1J) prizes,

11) winnings,1") pensions, an

1$) partner?s istributive share from the net income of the general professional partnership

*his is the manifestation that as far as iniviual income taxation, the income is

categorize

98 *he ta1 rate& are 2ro4re&&i,e i' character *his is clear uner Sec "& 3a) Kou will notice

there that the tax base increases as the tax rate increases

:8 0odified 4ro&& i'co+e a& re4ard& co+2e'&atio' ear'er Moifie because in eterminingthe taxable compensation income, the only allowable euctions are personal an aitional

exemption Kou cannot euct the allowable euctions uner Sec $& from gross compensationincome

But as regars those iniviual taxpayers that erive business, trae or professionalincome, we aopte the 'et i'co+e &y&te+$ *his is so because uner Sec $&, allo%a3le

dedctio'& may be claime by iniviual taxpayers who erive business trae an professional

income

;8 <e employ this CPay a& yo .ileD system

<8 >ner certain cases, we employ the C2ay a& yo ear'D system *his applies to Cincome

su%&ect to 'ithholdin tax)!

-$ <hat are the basic features of corporate income taxationA$

58 Glo3al Co'ce2t has been aopte LLL 'lobal system where the tax treatment views

inifferently the tax base an treats in common all categories of taxable income of taxpayer 3*an

vs -el osario)

Characteri&tic& of Glo3al &y&te+ of Ta1atio'

$

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 4/81

a) *niform tax treatment E this is sub(ect to iminishing corporate tax rates of $& 3Nan 1,

1IIA), $$ 3Nan 1, 1III), $" 3Nan 1, "JJJ) See 0hapter +@, Sec "5)

b) Does not cateorize income

98 orporate taxpayer, particularly domestic corporations are entitled to deductions So, insofar

as omestic corporation an resient foreign corporation is concerne, we aopte here the netincome tax system

9ew provisions uner A&"&: 1J tax on improperly accumulate earningsof a corporate taxpayer

:8 Pay a& yo file &y&te+ has also been employe

0orporate taxpayer is allowe to aopt calenar or fiscal year perio 0orporate

taxpayer files corporate income tax return #uarterly n it also files the so6

calle /+98 -N>S*;- ;*>9

+n the case of iniviual taxpayer, the payment shoul not be later than pril 12

of every taxable year +niviual taxpayers are not allowe to aopt the so6calle

/+S08 K; P;+.-

O +ndividual taxpayers are allowe to aopt only the calenar year perio while corporate

taxpayers have the option either the calenar year perio of the fiscal year perio

Cale'dar year 2eriod E this covers the perio of 1"6month commencing from Nan 1 an ening

-ec $1

.i&cal year 2eriod E this is also a 1"6month perio commencing on any month or ening on any

month other than -ec $1

DE.INITION O. CERTAIN TER0S

GROSS INCO0E TAXATION E is a system of taxation, where the income is taxe at gross

*he taxpayers uner this system are not entitle to any euctions

+n general, we aopte the 'et i'co+e ta1atio' because uner Sec $&, taxpayers are allowe to

claim the so6calle 88.<B8; -;->0*+.9S

GROSS INCO0E E means all income erive whatever source, incluing but not limite to thefollowing: 6STP"IRR"DAP"PS8

1 0ompensation for services!

" 'ross income from trae or business or the exercise of a profession!

$ 'ains erive from ealings in property!

& +nterests!

2 ents!

4 oyalties!

5 -iviens!A nnuities!

I Prizes an winnings!

1J Pensions! an

11 Partner?s istributive share from the net income of the general professional partnership

NET INCO0E TAXATION E income is taxe at net *he taxpayer may claim allowableeuctions

INCO0E E all wealth which flows in the taxpayer other than a mere return of capital +t inclues

all income specifically escribe as gain or profit incluing gain erive from the sale or

isposition of capital asset

,*D+C+. D0+N++1N : +t also means gains erive from 31) capital, 3") labor, or 3$) both labor

an capital incluing gains erive from the sale or exchange of capital asset

.OUR (;) Sorce& of INCO0E= 6Cla!S8

a 0apital

b 8abor

c Both labor an capital

&

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 5/81

Sale of property

;xample of income erive from capital LLL +nterest +ncome

;xample of income erive from labor LLL 0ompensation +ncome

;xample of income erive from both capital an labor LLL +ncome of an inepenentcontractor *he inepenent contractor provies wor% force, provies capital an erives income

from such capital

O +n determinin the profit from the sale of property, you shoul always be guie by this

formula:

mount eceive .r ealize 8;SS 0ost of Property P./+*

TAXA!LE INCO0E E 3the ol term is 9et +ncome) E means all pertinent items of gross

income specifie in the *ax 0oe le&& the euctions anFor personal an aitional exemptions,

if any, authorize for such types of income by this 0oe or other special laws 3Sec $1 of the

* of 1II5)

Shoter @ersion: ll pertinent items of ross income less allo'a%le deductions!

-$ <hat are the avantagesFisavantages of gross income taxation an net income taxation

Advantages of gross income taxation0

1 +t simplifies our income taxation *his is so because since no euctions are allowe, it is very

easy to tax the income Kou on?t have to fin out whether euctions or expenses are legitimate

or not because they are not euctible

" *his will generate more revenue to the government

$ +t minimizes cost

Disadvantages of gross income taxation0

1 s far as the taxpayer is concerne, this is ine#uitable because they cannot claim the expenses,

which are incurre in connection with his trae or business or exercise of his profession

" n if this is the system, in all li%elihoo the taxpayers will lose interest to earn more +t will in

effect reuce the purchasing capacity of the taxpayer

$ Since taxpayers cannot claim those legitimate expenses as euctions, they may resort to

frauulent scheme that will minimize their tax ability an this may be one through the

unerstatement of income So, in effect, this will encourage tax evasion

Advantages of net income taxation0

1 s far as the taxpayer is concerne, they will consier this as e#uitable an (ust system

" *his will minimize tax evasion because examiners will be employe to chec% whether

expenses are correct or not

$ *he conse#uence of no " is that this will generate more revenues

Disadvantages of net income taxation0

1 vulnerable to graft an corruption

" vulnerable to tax evasion

$ will give rise to loss of revenues

SOURCES>SITUS O. INCO0E

n income may be an income from within or without the Philippines *he other term for

income within is .ocal +ncome while income without is sometimes calle 2lo%al +ncome or*niversal +ncome

+n determinin 'hether an income is an income 'ithin or 'ithout3 you have to consider

the classification or 4ind of income!

CLASSI.ICATION O. INCO0E 6C7 !7 P7 I7 R7 R7 D7 A7 P7 P7 P81 0ompensation income from services

2

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 6/81

" +ncome erive from business, trae or profession E in this regar, the common forms of

business are merchanising business, farming business, mining business an manufacturing

business

$ +ncome from sale or exchange of property 3either real or personal property)

& +nterest +ncome2 ent +ncome

4 oyalties5 -iviens, which may be receive from omestic or foreign corporation

A nnuities

I Prizes an winnings

1J Pensions

11 Partner?s istributive share in the net income of general professional partnership 3Professional

income of a partner)

? CO0PENSATION INCO0E

*ax Situs: Place 'here services are rendered So, if services are renere within the Phils, that

is a 8ocal +ncome +f it is a payment for services renere outsie the Phils, that is an income

without

0 E income from within an without are taxable 90 E only compensation income from sources within is taxable

E same as 90

? !USINESS INCO0E 60: .8a) Merchanising Business

b) /arming Business ax Situs$ Place 'here these

c) Mining Business %usiness are underta4en

) Manufacturing Business

ax Situs$

31) if the goos are manufacture in the Phils n sol within the phils *his is consiere as

income derived purely within!

3") 'oos manufacture outsie the Phils an sol outsie E income derived purely without.

3$) 'oos manufacture within the Phils an sol outsie the Phils E income partly within and

partly without.

3&) 'oos manufacture outsie the Phils an sol within the Phils E income partly within and

partly without.

? INCO0E .RO0 SALE OR EXC#ANGE O. PROPERTY

+f it involves personal property, in etermining the tax situs, we have to consier

the place of sale

+n the case of sale of transport documents, tax situs is the place where the

transport ocument is sol 3B.0 0ase)

+f it involves real property, the tax situs is the place or location of the real

property So, if the property sol is situate within the Phils, the income erive

from such sale is consiere as income within

? INTEREST INCO0E

*ax Situs: RS+DNC of the D51R

Case$ *here was this contract regaring the construction of ocean6going vessels *here was this

issuance of letter of creit an the payment of ownpayment ll the elements of the transactionstoo% place in Napan *he payment was mae in Napan *he letter of creit was execute in Napan*he elivery was mae in Napan *he de%tor is a domestic corp

+s the interest income on this loan evience by the letter of creit taxable to the Napanese

corp

4

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 7/81

6.D$ '!, because the tax situs of interest income is not the activity %ut the residence of the

de%tor! he place 'here the contract of loan is executed is immaterial!

? RENT INCO0E*ax Situs: the P.C of property su%&ect of the contract of lease!

? ROYALTIES*ax Situs: the P.C 'here the intani%le property is *SD

? DI/IDENDa Received from domestic corp E this is an income purely within

b Received from forein corp E consier the income of the foreign corp in the Phils uring the

last preceing three 3$) taxable years!

rules$31) *he income is purely 'ithin if the income erive from the Phil sources is more than A2

3") +t is purely 'ithout if the proportion of its Phil income to the total income is less than 4J

3$) here should %e an allocation if it is more than 2J but not exceeing A2

? ANNUITIES

*ax Situs: the P.C 'here the contract 'as made

? PRI@ES AND *INNINGS

Prizes may %e iven on account of services rendered E in which case, the tax

situs is the 2lace %here the &er,ice& %ere re'dered

+f these prizes are not iven on account of services, the tax situs is the 2lace

%here the &a+e %a& 4i,e'

ax situs of 'innins is the place where the same was given

?PENSION*ax Situs: P.C 'here this may %e iven on account of services rendered

?PRO.ESSIONAL INCO0E O. PRO.ESISONAL PARTNERS

*ax Situs: P.C 'here the exercise of profession is underta4en

GROSS INCO0E

GROSS INCO0E E means all income erive from whatever source, incluing but not limite

to the following:

)'L()!'0 6code STP"IRR"DAP"PS8

1 compensation for services

" gross income from trae or business or the exercise of a profession

$ gains erive from ealings in property

& +nterests

2 ents

4 oyalties

5 -iviens

A nnuities

I Prizes an winnings

1J Pensions an

5

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 8/81

11 Partner?s istributive share from the net income of the general professional partnership (Sec!

78 of R of 9::;"

%+L()!'( 6code LAGCIR08

1 procees of life insurance policy" amount receive by the insure as return of premium

$ gifts, be#uests, evises or escent& compensation for in(uries or sic%ness

2 income exempt uner treaty

4 retirement benefits, pensions, gratuities

and others: (.7 /7 R7 S7 S7 G)

a retirement benefits receive from foreign institution whether public or private

b veteran?s benefits

c retirement benefits receive from private firms whether iniviual or corporate

separation pay

e SSS

f 'S+S

5 miscellaneous items:

a prizes an awars given in recognition of religious, charitable, scientific, eucational,artistic, literary, or civic achievements

0.9-+*+.9S:

1 the recipient was selected 'ithout any action on his part to enter the contest or

proceeing" the recipient is not re<uired to render su%stantial future services as a conition to

receiving the prize or awar

b income erive by the government or its political subivisions from the exercise of any

essential governmental function or from any public utility

c income erive from investment in the Philippines by foreign government or financing

institutions

prizes an awars in sports competitions

e gain erive from the reemption of shares of stoc% issue by the mutual fun companyf contributions to 'S+S, SSS, P'6+B+', an union ues

g benefits in the from of 1$th month pay an other benefits

h gain erive from the sale, exchange, retirement of bons ebentures or other certificate of

inebteness with a maturity of more than five 32) years 3Sec $" 3b), * of 1II5)

?ALLO*A!LE DEDUCTIONS

1 1ptional Standard Deduction E of ten percent 31J) of the 'ross +ncome available only to

iniviual other than a non6resient alien provie he signifies in his return his intention to elect

.S-, otherwise, itemize euctions apply ;lection mae shall be irrevocable for the taxableyear 3Sec $& 8)

" +temized Deductions E uner Sec $& 6Q, an M$ Personal and dditional Deductions/xemptions under Sec! 7=

? ITE0I@ED DEDUCTIONS 6code ELIT"!DD"CRC8

1 expenses

" loses

$ interest

& taxes

2 ba ebts

4 epreciation

5 epletion of oil, gas wells an mines

A charitable an other contributions

I research an evelopment1J contribution to pension trust

? NON"DEDUCTI!LE ITE0S

1(ec. 23 A4

1 Personal living or family expenses!

" mount pai for new builings or permanent improvements, or betterment to increase the

value of any property or estate!

A

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 9/81

$ ny amount expene in restoring property or in ma%ing goo the exhaustion thereof for

which an allowance is or has been mae! or

& Premiums pai on any life insurance policy covering the life of any officer or employee, or of

any person financially intereste in any trae or business carrie on by the taxpayer , iniviual

or corporate, when the taxpayer is irectly or inirectly a beneficiary uner such policy

1(ec. 23 B4 .osses from sales or exchanes of property directly or indirectly >1 Between members of a family 3brother, sister of half or full bloo, spouse, ascenant, lineal

escenants)!

" ;xcept in case of istributions in li#uiation, between an iniviual an a corporation E more

than 2J in value of the outstaning stoc% of which is owne irectly, by or for such an

iniviual! or

$ ;xcept in case of istributions in li#uiation, between two corporations E more than 2J in

value of the outstaning stoc% of each of which is owne, irectly or inirectly, by or for same

iniviual, if either one of such corporation is a personal holing company or a foreign personal

holing company! or

& Between the grantor an a fiuciary of any trust! or

2 Between fiuciary of a trust an the fiuciary of another trust, if the same person is a grantor

with respect to each trust! or4 Between a fiuciary of a trust an a beneficiary of such trust

TAXA!LE INDI/IDUALS

RESIDENT CITI@ENS (RC)

+ncome from 'ithin and 'ithout E taxable

NON"RESIDENT CITI@ENS (NRC)

+ncome from 'ithin

When an NRC returns to the Phils!3 his income may also %e taxed as ResidentCitizen or Non-Resident Citizen!

+llustration$ , an .0<, arrive in the Phils sometime in Nune 1IIA e will be taxe as a 9on6

esient 0itizen 390) as regars the income that he earne which covers the perio of Nanuary

to Nune 9ow as regars the income that he will erive upon his arrival from Nune to -ecember,

he will be taxe as esient 0itizen 30)

5ut if he is not in the Phils from the perio of Nanuary to -ecember 1IIA, he will be taxe as

90 for the sai perio

+f he will return to the Phils an stay there from Nanuary t -ecember 1III, he will be taxe as

0 for the same perio

? NRC must prove to the satisfaction of the 5+R Commissioner the fact of physical presence

a%road 'ith the intention to reside therein!

? When an NRC decides to return to the Phils!3 he must prove his intention to reside here

permanently!

? No' NRC includes 1@RSS C1NC W1RARS (1CW"3 +##+2RNS3 and those 'ho

SB 1*S+D the Phils! %y virtue of an employment!

RESIDENT ALIEN (RA)1 n iniviual who is not a citizen of the Phils but a resient of the Phils

O +nclues those who consier the Phils as a secon home

OOO ransient tourist who (ust so(ourn, their stay is merely temporary, thus may not be

consiere as

O +f an alien stays in the Phils! for a period of more than one (9" year3 he is considered as R!

SPECIAL NON"RESIDENT ALIEN ENGAGED IN TRADE OR !USINESS (NRA"NET!)

I

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 10/81

O e must be an alien iniviual who is not resiing in the Phils an not engage in trae or

business in the Phils

O 6e is one 'hose stay in the Phis!is not more than 9 days

SPECIAL NON"RESIDENT NOT ENGAGED IN TRADE OR !USINESS (SNRA"NET!)

5 Those employed by0 (ROP)1 egional or rea ea#uarters of Multinational corporations!

" .ffshore Ban%ing >nits!

$ Petroleum Service 0ontractors

NON"RESIDENT ALIEN ENGAGED IN TRADE OR !USINESS (NRA"ET!)

E considered as enaed in trade or %usiness if his stay is more than 9 days

L <e can no longer tax his income from sources without <e can only tax his income from

sources within

ENTITLE0ENT O. DEDUCTIONS

RC E entitle to euctions because the tax base is taxable income

'ross +ncome

8ess: llowable euctions

*axable +ncome

NRC E entitle to euctions because the tax base is taxable income

RA E entitle to euctions because the tax base is taxable income

NRA"T! E entitle to euctions because the tax base is gross income *heir income is sub(ect to"2 tax rate

SNRA"NET! E sub(ect to 12 tax rate on their income in the from of:

S 6 Salaries

# 6 onoraria

O 6 .ther

* 6 <ages

E 6 ;moluments

R 6 emuneration

EXCLUSION .RO0 GROSS INCO0E

PROCEEDS O. LI.E INSURANCEB

(ub6ect to tax if 0

1 the insurer an insure areed that the amount of the procees shall be withhel by the insurer

with the obligation to pay interest in the same, the interest is the one su%&ect to tax!

" there is transfer of the insurance policy!

xample$

transferre to B his life insurance policy *he value of the policy is P1 M B pai a

consieration amounting to P$JJ,JJJ B continue paying the premiums after the transfer suchthat the premiums amounte to P"JJ,JJJ >pon the eath of the insure, the P1 M may be

receive by the heirs

-$ +s the full amount of P1 M exempt

A$ 9., only the consieration given an the total premiums pai may be exclue *hat is, P1 M

less P2JJ,JJJ

1J

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 11/81

Pro%lem$

obtaine a life insurance policy for B B is the presient of ?s corporation 0orp has

an insurable interest in the life of its officers, so premiums may be pai by the employer >pon

the eath of B, his esignate beneficiaries will receive the procees

a +s the amount representing the procees of the life insurance policy taxable

b <hat about the premium pai by the employer -oes this amount form part of thegross compensation income

c -oes the amount representing the procees of life insurance policy from part of the estate

of the eceent

ns'ers$

a 8et us first ma%e t'o (8" assumptions 8et us assume that:

1 the beneficiary esignate is the employer!

" the beneficiary esignate is the heir of the family of the insure

he ax Code ho'ever3 ma4es no distinction! Reardless of the desinated %eneficiary isthe employer or the heirs3 or the family of the insured proceeds of life insurance policy should

al'ays %e excluded!

b Premiums of life insurance policy pai by the employer may form part of compensationincome! hence, taxa%le if the %eneficiary desinated are the heirs or the family or the

employees

+t is not taxa%le compensation income if the desinated %eneficiary is the employer because that is

(ust a mere return of capital

c! Proceeds of life insurance policy may %e excluded from the ross estate of the decedent

under the follo'in cases$1 if the beneficiary esignate is a $r person an the esignation is irrevocable!

" it is a procee of a group insurance policy

owever 3 it is included in the ross estate of the decedent$

1 if the beneficiary esignate in the estate, executor or aministrator of the estate

or the family of heirs of the eceent!" if the beneficiary esignate is a $r person an the esignation is revocable Gsee

Section A2 3e)H

s far as Sec! = (e" is concerned3 an employer may %e considered a 7rd person!

A0OUNT RECEI/ED !Y INSURED AS RETURN O. PRE0IU0Beason for ;xclusion: +t represents a mere return of capital

*he &orce& of thi& retr' of 2re+i+ (L$E$A$)

1 8ife +nsurance Policy

" ;nowment contracts$ nnuity contracts

666Whether the premiums are returned durin or at the maturity of the term mentioned in the

contract or upon surrender of thee contract

Pro%lem$

too% out an enowment policy amounting to P1 M e pai premiums amounting to

PAJJ,JJJ >pon the maturity of the policy, receive that P1Mow much is the taxable amount

ns'er$

*hat is P1,JJJ,JJJ E value of enowment policy

8;SS: P AJJ,JJJ E representing amount of premium

P "JJ,JJJ E taxable amount

11

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 12/81

?GI.TS7 !E-UESTS a'd DE/ISESB

ationale: <hat is contemplate here are onations which are purely ratuitous in character in

orer that it may be exclue

2ifts are exclue because these are sub(ect to donorFs tax

5e<uests and devises are exclue because these may be sub(ect to estate tax

<hat about remuneratory onations Remuneratory donations are su%&ect to

income tax!

%+%#T)!'( to the $ule:LLL the income or fruit of such money given by onation, be#uests

or evise, incluing the income of this gift, be#uest or evise in cases of transfer of ivie

interest

?CO0PENSATION .OR INURIES OR SICNESSBeason for ;xclusion: *his is (ust an indemnification for the in&uries or damaes suffered *his is

compensatory in nature

*he sources are:

1 *he compensation may be paid %y virtue of a suit !

" +t may be paid %y virtue of health insurance3 accident insurance or Wor4menFs Compensation

ct

5ut as reards damaes representin loss of anticipated income3 this is the one that is taxa%le!

+f damaes are in the nature of moral3 exemplary3 nominal3 temperate3 actual and li<uidated

damaes3 as a rule3 these may not %e su%&ect to tax!

;xample:

+f a person suffere in(ury as a result of a vehicular accient, an an action is file in

court, the 0ourt awars the following:

Moral 6 P1JJ,JJJ

;xemplary 6 P1JJ,JJJ

ctual 6 P 4J,JJJ 3hospitalization expenses)

P "J,JJJ 3repair of car)

P 4J,JJJ 3loss of income)

OOO ll damaes a'arded are tax-exempt except damaes of representin loss of income!

Ruestion: re amages aware by the 0ourt on account of breach of contract taxable

nswer: Rualify your answer <ith regars to amages aware on account of loss of earningsof the contracting party, it is taxable

INCO0E EXE0PT UNDER TREATYBeason for the ;xclusion: reaty has o%liatory force of contract

%xception0 s may be provie for in the treaty

?RETIRE0ENT !ENE.ITS7 PENSIONS7 GRATUITIES AND OT#ERSB

*%T%$A'7( B%'%8)T

O *his may be given by the >S ministration

O *he recipient must %e a resident veteran!

B%'%8)T( 9)*%' B: 8!$%)9' A9%')%( !$ )'(T)TT)!'( ;&%T&%$ #BL)

!$ #$)*AT%

'iver: /oreign government agencies or institutions whether public or privateecipient: esient citizen, non6resient citizen or resient alien

1%servation$

1"

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 13/81

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 14/81

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 15/81

O2overnment-o'ned and controlled corporations are no' su%&ect to corporate income tax,

except :

a SSS

b 'S+Sc Phil ealth +nsurance 0orp

P0S.e P'0.

Situation: municipality erive income from holing a fiesta

Rle: *he rule is settle that holing a town fiesta is consiere a proprietary function *herefore,

sai income is sub(ect to tax

Situation: municipality erive income from the operation of public mar%et, electric power

plant an other public utilities

Rle: *hat income is tax exempt

d. )ncome derived from investment in the #hils. 1=4 by foreign government or 1>4

financing institutions, owned, controlled or financed by foreign government, regionalor 124 international financing institutions established by foreign government

;R>+S+*;S:

9! Recipient must %e$a foreign government!

b financing institution owne, finance or controlle by foreign government!

c regional financing institution, international financing institution establishe by

foreign government!

" +t must %e an income derived from investment in the Phils

Sources of such income:

666 +t may be in the nature of bons So, foreign government here may be consiere the creitor E possible income here is the i'tere&t of 3o'd& 9ow, loans may be extene E possible income

here is i'tere&t o' loa'&

666 +f a forein overnment or financin institution mae a eposit in a ban%, Phil currency

eposit E the income here is the nature of i'tere&t i'co+e

666 +f a forein overnment mae an investment in a omestic corporation +t may be consiere a

stoc%holer n a stoc%hler is entitle to ivien ence, the di,ide'd i'co+e receive from

omestic corporation is ta1 e1e+2t

OO +f the recipient of such ivien is a re&ide't forei4' cor2oratio' that is also ta1 e1e+2t +t

is only sub(ect to tax if the recipient of such ivien is a 'o'"re&ide't forei4' cor2oratio'

Ca&e ;=+MB9Q, which is a consortium of Napanese ban%s, extene a loan in the amount of

S"JM to Mitsubishi Metal 0orp, a Napanese corporation *he same amount was extene by

Mitsubishi as a loan to tlas 0orp, a omestic corporation

*he contract entere into between Mitsubishi Metal 0orp is enominate as Ccontract of

loan an saleD +t is a contract of loan because Mitsubishi woul len tlas S"JM +t is a contract

of sale because uner the contract tlas boun itself to sell the concentrates 3this is a mining

corp) that may be prouce by the concentrator machineFe#uipment purchase through the use of

the S"JM for a perio of 12 years

*his being a contract of loan, Mitsubishi is entitle to interest on loan

+SS>;: <hether or not such interest on loan is sub(ect to Phil income tax

R2*#NS : Mitsubishi contene that this is not taxable because:1 *he source of S"JM is a tax exempt entity 3;=+MB9Q is a financing institution controlle

an finance by a foreign government)! an

" Mitsubishi is an agent of ;=+MB9Q, a tax exempt entity

12

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 16/81

;8-: *here was no evience to the effect that Mitsubishi is an agent of ;=+MB9Q +t is a

mere allegation that has not been proven

+n a contract of loan, once the loan is consummate, the amount becomes exclusive property of the borrower +t is no longer consiere the money of ;=+MB9Q ence, the

interest of such loan shoul be sub(ect to tax

*he lener is not a tax exempt entity *he creitor here is Mitsubishi an it is not a tax

exempt entity Such being the case, tax exemption must be strictly construe against the taxpayer

an liberally in favor of the government <hen you claim exemption, you shoul prove it clear

an categorical terms

O *he problem may be moifie by the examiner *he examiner may clearly state the Mitsubishi

is an agent of ;=+MB9Q *he answer is, the interest on loan is tax exempt Mitsubishi then is

consiere as an extension of ;=+MB9Q +t is as if the lener is ;=+MB9Q

e. =2th month #ay and Benefits

O *his applies both to private an public employees

O *otal exclusion shoul not excee P$J,JJJ sub(ect to increase by the Secretary of /inance upon

the recommenation of the B+ 0ommissioner

f. ontributions to 9()(, (((, "%D)A$%, #A9)B)9, and union dues

O *his is a surplusage ;ven if this is not mentione, we cannot tax that

g. (ale, exchange, retirement of bonds, debentures and other certificates of indebtedness

with a maturity of more than 8)*% 1?4 :%A$(

6 +f maturity is less than 2 years, taxable

Rle +nterest on %onds

1 issue by 0B 6 exempt

" if issue by corp6 not exempt

Rle Redemptions of share in mutual funds:

6 only those gains erive from reemption of shares issue by a mutual fun company are

exempt

6 it must emanate from a mutual fun

6 +f the term is not more than 2 years 32 years or less), the gain erive from the sale, exchange

an retirement of the same, may be sub(ect to tax

+llustration:+f you are a creitor, you may sell these bons, ebentures or certificates of inebteness

to another 6indi mo na mahintay an maturity 4asi lon term! +f there is a gain on the sale of the

same, it woul be a tax exempt provie that the bons, etc, have a maturity or term of more than

2 years

etirement of bons, ebenture, etc 666 Na%ayad na Iyun de%tor! *here may be gain

erive from the same, such as interest *his time, since the gain is in the nature of interest, it is

sub(ect to tax But, the gain erive from the sale, exchange or retirement with a term of more

than 2 years, is tax exempt *his is because exemptions are strictly construe against the taxpayer

an liberally in favor of the government +nterests on bons, ebentures, etc are taxable, the

provision is clear +t only covers saleFexchangeFretirement of bons, ebentures an other

certificate of inebteness with a maturity of five years Strict interpretation of tax exemption

TYPES> CLASSI.ICATION O. INCO0E

5$ CO0PENSATION INCO0E an income erive uner an employee6

employer relationship

his may include the follo'in : 3*E!!"DROP)

14

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 17/81

*ages, Emoluments, !onuses, !enefits, Director?s fee, *axable R etirement Benefits, Other

items of income of similar nature, *axable Pensions

O $etirement benefits may be sub6ect to tax , if it oes not comply with the provision of Sec $"

3b) par 4 subpar a

O #ensions may be sub6ect to tax , if it is given not in accorance with the conitions lai ownuner that exclusion provision

O !ther items of income of similar nature may include: (C#A0P)

0lothing allowance, ospitalization allowance, llowances for /oo, Meical allowance, Share

from the Profit sharing plan of the employee

O T%(T( T! D%T%$")'% ;&%T&%$ A' )'!"% )( !"#%'(AT)!' or '!T0

/in out whether it is receive uner an employer6employee relationship

ny payment receive uner an employer6employee relationship is compensation

income

OT%(T( T! D%T%$")'% T&%$% %+)(T( A' %"#L!:%$%"#L!:%% $%LAT)!'(&)#0 1AD4

1 ppointment 3selection an hiring)

" 0ompensation

$ -ismissal power

& 0ontrol test

N$!$ : *he name or esignation of income is immaterial *he basis of the income is immaterial

an the manner by which it is pai, is also not important s lon as it is iven under an

employer-employee relationship3 then that is compensation income

A'%LLAT)!' !8 )'D%BT%D'%(( E 0onsiere as compensation income is the

inebteness ha been cancelle in consieration of the services renere

OOO Share of the employee from the PR10+ S6R+N2 P.N of the employer- 0ompensation

income receive in consieration of services renere

TA+ L)AB)L)T: !8 T&% %"#L!:%% #A)D B: T&% %"#L!:%$ @ 0ompensation income

if pai uner an employer6employee relationship in consieration of services renere

#$%")"( #A)D B: T&% %"#L!:%$ !' T&% )'($A'% #!L): !8 T&%

%"#L!:%% @ 0ompensation income if the beneficiary esignate is the family of heirs of the

employee

OOO he %asis of the income is immaterial ;ven if it is pai in piece wor%, fixe rate or percentage basis as long as it is pai uner an employer6employee relationship

$%<)()T%( 8!$ TA+AB)L)T: !8 !"#%'(AT)!' )'!"% A$%0 (SPR)1 *here must be services, renere uner an employer6employee relationship

" +f payment must be for that services renere

$ +t must be reasonable *he compensation for services renere must be reasonable

#urpose why only a reasonable amount may be taxed as compensation income0

*a%e note on the part of the employer, he can claim such compensation for services aseuction 9ow, only the amount that is reasonable uner the circumstances can be claime as

euction So, if the amount or the value of the services renere is P1J,JJJ but the employee

receive P12,JJJ s far as the employer is concerne, he can only claim the reasonable amountof P1J,JJJ +n the case of an employee, he can consier P1J,JJJ as compensation income *heexcess of P2,JJJ may be treate as other income

OOO Not all payments for services rendered are considered compensation income .nly those

pai uner the employer6employee relationship

T#E .OLLO*ING ARE NOT CO0PENSATION INCO0E (P I)

15

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 18/81

1 0ompensation for services renere by independent service contractor *his may be treate as

trae or business income

" +ncome erive by professionals from the practice of profession uner professional

partnership *his is treate as professional income

OOO 8ringe benefit is considered as compensation income. *his is governe by Sec $$, *

1II5 *his is compensation income in the sense that this is receive uner an employer6employeerelatioship

D!T$)'% !8 A(& %<)*AL%'T

6 you may be pai in cash or in propertyF%in

6 e#uivalent value of property is taxable

? DI..ERENT .OR0S O. CO0PENSATION INCO0E

=. #ropertyind E /air Mar%et @alue (0#@" of the property +f there is a price stipulated3 it is

the price stipulate that will be followe in the absence of contrary evience

>. #romissory 'ote or other evidence of )ndebtedness

a +f it is not discounted , it is the face value of the promissory note b +f it is discounted , it is the fair iscounte value of the promissory note

2. (toc/ @ /M@ of that shares of stoc%

C. ancellation of )ndebtedness @ Cancellation of inde%tedness has the follo'in taxconse<uences$

a +t may amount to taxa%le compensation income if the inebteness has been

cancelle in consieration of the services renere

b +t may amount to taxa%le ift or donation if the inebteness has been

cancelle without any consieration at all *his is not sub(ect to income tax but may amount to taxable gift or onation

c +t may amount to capital transaction if the creitor is a corporation an the

ebtor is a stoc%holer +f creditor corporation condoned the inde%tedness ofthe de%tor stoc4holder , that may amount to taxable capital transaction *his is

the form of irect ivien 9ow, property dividend is su%&ect to tax rates of

HG3 G and 9G! -ivien receive from omestic corporation is nowsub(ect to tax

?. Tax liability of the %mployee paid by the employer in consideration of services

rendered @ amount of tax liability

3. #remiums paid by the employer on the life insurance policy of the employee.

a +t is a taxa%le compensation income if the beneficiary esignate are the heirsof the employee or his family

b +t is not a taxa%le compensation income if the beneficiary esignate is theemployer because it is (ust a mere return of capital

+f the desination of the employer as %eneficiary is indirect 3eg: +t is the creitor

of the employer that is esignate as beneficiary), that is still not taxable compensation

income

xample of +ndirect desination of the employer as a %eneficiary$a Beneficiary is the wife of the Presient of a close corporation

b +f the employer may secure a loan from he insurance policy

1A

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 19/81

Premiums 'ill %e taxed under Sec! 77 par!% no!9 it is state there: C8ife or health

insurance an other non6life insurance premiums or similar amounts in excess of what the

law allows

O +f the payment 'as received %y the employee 'hen he 'as no loner connected 'ith his

employer , it is still consiere compensation income <hat is important here is that itmust be receive uring the existence of the employer6employee relationship ;mployees

may be ismisse by the employer, an they may file complaint for illegal ismissal

against the employer Nugment was renere by the arbiter in favor of the employee llthe wages suppose to be pai 3eg bac%wages) can be taxe as compensation income

<hat about attorney?s fees *hat is exempt

.RINGE !ENE.ITS code (#E/"#I0"E#EL)

8$)'9% B%'%8)T E ny goo, service, or other benefit furnishe or grante in cash or in %in

by an employer to an iniviual employee (except ran4 and file employee" such as but not limiteto the following:

1 ousing!

" ;xpense account!

$ @ehicle of any %in!

& ousehol personnel such as mai, river, others!

2 +nterest on loan at less than mar%et rate to the extent of the ifference between the

mar%et rate an the actual rate grante!

4 Membership fees, ues an other expenses borne by the employer for the employee in

social an athletic clubs or other similar organizations!

5 ;xpenses for foreign travel!

A oliay an vacation expenses!

I ;ucational assistance to the employee or his epenents! an1J 8ife or health insurance an other non6life insurance premiums or similar amounts in

excess of what the law allows!(if contri%ution-exempt"

O &ousing allowance may be exempt from tax if the living uarters are0

a Provie with the premises of the employer

b +t must be mae as a conition of employment

+f sai re#uisites are not present, housing allowance may be taxe as fringe

benefits

O "eal allowance may be exempt from tax if it is provie within the premises of the employer

O #rivilege or purchase discount are tax exempt if it oes not excee of the basic monthly

salary of the employee +f it is more than J3 the excess may be as fringe bene

5 "edical or hospital allowance, clothing allowance, rice allowance may be exempt from tax if

the following reuisites are present0

1 +t must be of relatively small value 3reasonable amount) 3S@)

" +t must be given for the following purposes: 30;')

a *o promote 0ontentment

b *o promote ealth

c *o promote ;fficiency

*o promote 'oowill

O Ta1 E1e+2t fri'4e 3e'efit& (R.7 D07 C7 E17 ECR)

1 5enefits iven to the ran4 and file employees, whether grante uner a collective bargaining

agreement or not

" KDe minimis %enefitsD E means of small amount *hese are benefits relatively of small

amount

1I

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 20/81

$ 0ontributions of the employer for the benefit of the employee to retirement, insurance an

hospitalization benefits plans

& /ringe benefits which are authorize or exempte from tax uner special laws

2 *hose given for the convenience of the employer, incluing those which are re#uire by the

nature of the trae, business or profession of the employer (mployerFs Convenience Rule"

De minimis benefits 3of relatively small value) E limite to facilities or privileges furnishe or

offere by employer to his employees merely as a means of promoting health, goowill,

contentment, or efficiency of employees, such as:

a Monetize unuse vacation leave creits not exceeing ten 31J) ays uring the year!

b Meical cash allowance to epenents of employees not exceeing P52J per semester of

P1"2 per month!

c ice subsiy of P$2J per month!

>niforms!

e Meical benefits

f 8aunry allowance of P12J per month!

g ;mployee achievement awars, for length of service of safety achievement in the form of

tangible personal property other than cash gift certificate, with an annual monetary value

not exceeing month of the basic salary of employee receiving the awar uner an

establishe written plan which oes not iscriminate in favor of highly pai employees!

h 0hristmas an ma(or anniversary celebrations for employees an their guests!

i 0ompany picnics an sports tournaments in the Philippines an are participate in

exclusively by employees! an ( /lowers, fruits, boo%s or similar items given to employees uner special circumstances

on account of illness, marriage, birth of a baby, etc

5#rinciple of %mployer7s onvenience $ule0

6 fringe benefits may be exemptFnot sub(ect to tax if these are given for the benefit

or avantage of the employer

The following are the possible fringe benefits, which may be exempt under the %mployer7s

onvenience $ule0 (# / # 0 T)

a ousing benefit

b @ehiclec ousehol personnel

Membership in a social or athletic club or similar organization

e *raveling expense benefit

O &ousing benefit E in etermining whether the same is exempt uner the employer?s

convenience rule, you have to consier the peculiar nature of the special nees of the employer $euisites for exemption0

1 +t must be mae as a condition for employmentL

" +t must be provided 'ithin the premises of the employer

OOO *his may apply to a supervisor of a plant or a company

O +f the housin or livin <uarters are provided outside the premises of the employer3 even if that

is for the convenience of the employer3 this is only exempt up to =G of the amount So, 2Jtaxable, 2J exempt

O *ehicle E ;xempt but epens upon the peculiar nature of the special nees of the business of

the employer xample$ 8B0 or -8 business

O &ousehold personnel such as maid, driver and others E ;xempt, but epens upon the

peculiar nature of the business of the employer

O "embership in a social club, etc E Peculiar nature re#uirement

"J

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 21/81

O Traveling expense benefit E Peculiar nature re#uirement xample$ ;mployer sent his

employees abroa to atten a particular seminar to improve their technical %now6how

B R>;S*+.9: is a river of 0ongressman Magtanggol an he receive a monthly salary of

P2,JJJ an living #uarter allowance of P",2JJa <hether the P",2JJ living #uarter allowance is exclue or sub(ect to tax

b ssuming the employer is an obstetrician woul your answer be the same

9S<;:

a *hat shoul be sub(ect to tax

b +t shoul be exclue eason: 0onvenience of the employer?s rule

9$ GROSS INCO0E .RO0 !USINESS7 TRADE OR PRO.ESSION

B()'%(( @ ny activity that entails time, attention, effort for purposes of livelihoo or profit

s reards construction %usiness, the taxpayer here must be an inepenent

contractor e may report his income uner the percentage of completion metho

or uner the so6calle complete contract metho

#$!8%(()!'AL )'!"% @ *he recipient of the same must be professionals

ow about those who claim that they are professionals but are not registere in

the P 0, can they still be tax as such

Kes, irrespective of whether they are license or not because of the rule that

gross income erive from whatever source

:$ PASSI/E INCO0E

#A(()*% )'!"% @ *his is the income that is sub(ect to final tax

)ncome sub6ect to final tax are the following0 (codeRPD"*IDS)

1 oyalties

" Prizes

$ <innings

& +nterests on ban% eposit, eposit substitutes, trust funs an

other similar arrangements

2 -ivien receive from omestic corporation, mutual fun insurance company,

regional hea#uarters of multi6national corporation an other corporation

4 Share a partner in the net income after tax of a taxable partnership, (oint account, (oint

venture or concessions

OOO Do not include passive income in the income of your business or profession, or in your

compensation income *his is so because when you receive this income, the tax ha alreay been

impose an eucte

RC7 NRC7 RA NRA"ET! NRA"NET!

"1

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 22/81

ROYALTIES "J except in the

case of literary'or4s3 %oo4s and

musical

compositions 'hich

are su%&ect to 9G final tax

Same as 0, 90,

"2

PRI@ES e1ceedi'4P57$

+f it is P93!

or less3 it is N1 su%&ect to final tax

%ut the same must

%e included in otherincome 3eg

compensation,

business, professional)

"J

"J "2

*INNINGS except

PCS1 M .otto

"J "J "2

INTERESTS ON

!ANDEPOSITS7 etc

"J "J

"2

DI/IDENDS

RECEI/ED fro+do+e&tic cor2$7 etc$

Sub(ect toincreasing rates of

4 if receive in

1IIA! A in 1III!

an 1J in "JJJ

"J "2

S#ARE O. A

PARTNER i' the'et i'co+e after a

ta1 of a ta1a3le

2art'er&hi27 etc

6 o6

4, A 7 1J

"J "2

Ruestion: ow o you treat that share of a professional partner from the net income of a general6

professional partnership

nswer: *his shoul be taxe at the rate provie uner Sec"&, that is, 2 to $&

But as regards the share of a partner in the net income after tax of a taxable or

business partnership, that is one which is sub(ect to final tax

#$)E%( @ may be exempt if given in sports competition an if given primary in recognition ofscientific, artistic, literary, eucational, religious, charitable, or civic achievement

INTEREST

$ules

1 +f it is an interest on forein currency deposit system3 it is exempt

+f the recipient is non6resient iniviual 390, 96;*B, 969;*B)

" +f the recipient is a resident individual (RC3 R"3 that is sub(ect to 52

$ +nterest income is also exempt if it is an interest income on a long6 term eposit or long6term investment 3this must have a term of not less than 2 years)

)f the term is less than ? years it is sub6ect to the following rates:1 & years to less than 2 years 2

" $ years to less than & years 1"

$ 8ess than $ years "J

""

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 23/81

D)*)D%'D $%%)*%D 8$!" D!"%(T) !$#!$AT)!'

1 his is exempt from tax if the recipient is a foreign government, financing institution,

regional financing institution, international financing institution establishe by foreign

government Gsee Sec$" 3B) 35) 3a)H

" +t is also exempt if the recipient of such ivien is another omestic corporation orresient foreign corporation Gsee Sec "A3)35)3)H

A#)TAL 9A)' D%$)*%D 8$!" (AL% !8 (&A$%( !8 (T!

Listed and traded through local stoc/ exchange @ this is not sub(ect to income

tax but sub(ect to percentage tax of of 1 of the gross selling price

'ot listed and traded through local stoc/ exchange E this is the one sub(ect to

income tax

9ot over P1JJ,JJJJJ 2

mount .ver P1JJ,JJJJJ 1J

+f the share of stoc4 is not listed and traded throuh local stoc4 exchane, the

basis of the tax is net capital gain So, you shoul first euct the capital loss

+f listed and traded throuh local exchane, there is no euction allowe

because the basis of the tax rate of of 1 of the gross selling price

he a%ove-mentioned tax rates apply to all individual taxpayers!

5 A#)TAL 9A)' D%$)*%D 8$!" T&% (AL% !8 $%AL #$!#%$T: 6 *he real property involve must be consiere 0P+*8 SS;*

6 *he tax on capital gain erive from the sale of real property is 4 of the gross selling price or

zonal value which ever is higher

O CAPITAL ASSET property held %y the taxpayer 'hether or not connected in his trade or

%usiness except : (code SOUR)

1 Stoc% in trae or other property of any %in which woul be inclue in the inventoryof the taxpayer if on han at the en of the taxable year

" Property primarily hel for sale to customers in the .rinary course of trae or

business

$ Property >se in trae or business sub(ect to epreciation

& eal property use in trae or business

T *he efinition of capital asset says Creal property hel by the taxpayer whether or not

connecte with his trae or business except real property use in trae or businessD So, in

order to %e a capital asset3 the real property must %e one not used in trade or %usiness

T *hat is why, the sale of resiential house an lot is sub(ect to 4 of capital gains because it

is a real property not use in trae or business

T But, sale of real property by a real estate dealer is not a capital transaction because the

property involve is one primarily hel for sale to customer in the orinary course of trae

or business *hat is not a capital asset %ut an ordinary asset

T *his covers not only CsaleD of property! it also covers conitional sale of real property

incluing the so6calle pacto de retro sale uner rt 14J" of the 900, or isposition of property locate in the Phils

T +f the %uyer is the overnment or any of its political su%-divisions or political aencies3

includin overnment o'ned and controlled corporations3 the seller have the option to avail

"$

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 24/81

the 4 or uner Sec "&3), wherein the basis uner sai section is taxable income so

euctions may be allowe *he cost of the property may be eucte but when you avail of

the 4, the basis is gross selling price or zonal value whichever is higher

T +s this a tax on the buyer or the seller +t is a tax on the seller But sometimes, through an agreement, p'ede nilan +-transfer sa

%uyer3 an there?s nothing that can prevent the seller from transferring the tax to the buyer inthe contract of sale

OT#ER INCO0E

O !T&%$ )'!"% includes 6code R$I$D$O$8a ent income other than royalties

b +nterest income other than interest income on ban% eposit

c -ivien income

+ncome from .ther sources an this may inclue: (!IT"CDC)1 Ba ebts recovere

" +llegal gains erive from gambling

$ *ax funs

& 0ompensation for private property expropriate by the

government for public use

2 -amages

4 0ancellation of inebteness

5$ $%'T 6 0ompensation for the use of one?s property

6 *he payment may be in cash or in %in *he property involve is either

personal or real property

6 +n the case of personal intani%le property3 sub(ect to final tax if it involves

intellectual property, copyright, traemar%s etc

T&% 8!LL!;)'9 !'(T)TT%( TA+ABL% $%'T )'!"%0

1 *he re4lar re't may be monthly, semi6annually or annually

" Additio'al re't i'co+e which inclues:

a !bligation of the lessor assumed by the lessee *he following are obligations which

may be assume by the lessee: 6R$I$D$I$O$8a1 eal property taxe on lease premises

a" .bligation to pay insurance premium on the insure lease premises

a$ +f the lessor is a corp, the obligation to istribute -iviens to its stoc%holers

a& .bligation to pay interest on the bons issue by the lessor

a2 .ther obligations of the lessor which may be assume by the lessee

b *alue of permanent improvements on leased premises *his may be reportethrough:

b1 1utriht method at the time of permanent is complete, he may report that as

aitional rent income E /M@ of the builing or permanent improvement

b" Spread out method by allocating the epreciation among throughout the

remaining term of the lease

c. Advance rentals

c1 +f in the nature of the prepai rentals without restriction on the use of the

amount, it is taxa%le

c" +f it is in the nature of security eposit, it is taxa%le rent income if there is aviolation of the term of the lease

c$ +f it is in the nature of a loan to the lessor, it is not taxa%le

>. )'T%$%(T )'!"% E compensation for the use of money6 <hether it is an interest on loan pursuant to the business of a taxpayer or personal

transaction, interest income, except if it is tax exempt, is always taxable *his is so

because the source of income is immaterial, even if it is from an illegal source

"&

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 25/81

6 +nterest income on ban% eposits is sub(ect to final tax

2. D)*)D%'D )'!"% E amount eclare, set asie an istribute by the Boar of -irectors

to stoc%holers, on eman or a fixe perio

lasses of Dividend $ GC$L$I$P$S$S$HCash dividend

.i<uidatin dividend- this is given upon li#uiation of corporate affairs

+ndirect dividend - it is given in other form an this inclues cancellation of

inebteness by the corp of the obligation of stoc%holer

Property dividend - it may be in the form of stoc% other than the stoc% of the corpStoc4 dividend - stoc% issue by the giver corp

Script dividend - +t is given in the form of promissory note or other evience of

inebteness

STOC DI/IDEND @ as a rule not taxable. *his is so because there is no income here +t

merely represents the transfer of surplus account to the capital account

CP+1NS to the Rule:

(toc/ dividend may be sub6ect to tax under the following exceptional cases0 6C OR D8

1 +f there is a 0hange in the stoc%holers interest in the net assets of the corp!

" +f it is one issue by .ther corp <e call that Cdividend stoc/ D

(toc/ dividend vs. dividend stoc/ E Stoc% ivien as a rule is not taxable whereas

ivien in stoc% is taxable

$ eemption of stoc% ivien!

& +f the corp issues -ifferent shares of stoc% +f the corp issues two ifferent classes of

shares of stoc%, the ivien that may be eclare thereafter is taxable

;xample:

!utstanding stoc/ (toc/ dividend Taxable

1 Preferre 0ommon 9*

" 0ommon Preferre 9*

$ Preferre Preferre 9*

& 0ommon 0ommon 9*

2 PreferreF0ommon Preferre *

4 PreferreF0ommon 0ommon *

Disguised dividend @ treasury stoc% ivien eclare out of the outstaning capital stoc%, the

purpose of which is to avoi the effect of taxation 3Commissioner vs! #annin"!

+t is one which is mae to appear as stoc% ivien when the truth of the matter is that it is a

ivien which is illegally eclare, such a case, since the purpose is to evae taxation, it is

taxable

emember, treasury shares of stoc/ are not entitled to dividends.

ALLO*A!LE DEDUCTIONS (SEC$ :;)

As regards individual taxpayers, the following may claim allowable deductions0

1 0

" 90, only those expenses incurre in the Phils because here, we cannot tax his incomeerive from sources without

$ , only those expenses incurre in the Phils

& 96;*B, but only those expenses incurre in the Phils

2 PP 3Professional Partners uner Sec "4)

%xceptions0

1 +* earning 0+ E ;;, ; ;8

"2

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 26/81

" 969*B

$ liens employe

M0

B .B>

0 PS0& 9/0

As regards corporate taxpayers, the following are entitled to claim allowabledeductions0

1 -0, which inclues private eucational institutions, non6profit hospital, government6owne

an controlle corps

" /0

ITE0I@ED DEDUCTIONS 6E7I$T7L7!7D7D7C7R7C81 ;xpenses 4 -epreciation

" +nterests 5 -epletion of oil, gas, wells an mines

$ *axes A 0haritable contributions

& 8osses I esearch 7 -evelopment

2 Ba ebts 1J 0ontribution to Pension *rust

O +n the case of individual taxpayers, they may avail of the optional standard deduction of 9G

of ross income

O Corporate taxpayers are not allowe to claim 1J optional stanar euctions

O ll iniviual taxpayers except the 9 iniviual may claim this optional stanar

euctions

O )temi-ed deduction may apply to corporate taxpayers as well as individual taxpayers

5 8'DA"%'TAL #$)')#L% )' D%DT)!'(

1 *he taxpayer must prove that there is law authorizing euctions

" *he taxpayer must prove that he is entitle to euctionsOOO NR0C are not entitled to claim deductions

5$ EXPENSES

!$D)'A$: F '%%((A$: %+#%'(%(

<hen we spea% of .-+9K, this simply refers to the expenses which are normal, usual orcommon to the business, trae or profession of the taxpayer *his may not be recurring

xample: if an action is file in court, it is but normal to hire the services of a lawyer So, the

taxpayer has to pay attorney?s fees +t is an orinary expense uner this circumstances

9;0;SSK6 +t is one which is useful an appropriate in the conuct of the taxpayer?s trae or profession

.-+9K 7 9;0;SSK ;=P;9S;S

6are those which are incurre or pai in the evelopment, operation management of the business,

trae or profession of the taxpayer

;=*6.-+9K ;=P;9S;S E 'ot Deductible *hese are amortize or in lieu of the same,

you may claim that so6calle allowance for epreciation n if it involves intangible asset, the

wor use is M.*+U*+.9

*here is no har an fast rule n expense may %e ordinary insofar as a particular

taxpayer is concerned and it may not %e an ordinary as reards another taxpayer!

;xample:

+f you have business here in Manila an you also have business in *awi6tawi, what is the

expense that you may incur in *awi6tawi which you may not possibly incur in Manila

+n *awi6tawi, you may nee people to guar your business But here in Manila, you may

nee not because of our new Presient6elect

"4

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 27/81

INDS O. ORDINARY F NECESSARY EXPENSES 6C$A$R$T$E$R$S$8

1 0ompensation for services renere

" vertising 7 promotional expenses

$ ent expenses& *ravelling expenses

2 ;ntertainment expenses4 epairs 7 maintenance expenses

5 Supplies an materials

!""!' $%<)()T%( 8!$ D%DT)B)L)T: of these ordinary F necessary expenses0

6D$I$R$8a #ust %e paid or incurred D*R+N2 the taxa%le year!

+f you incur expenses in 1II5, you cannot carry this over to 1IIA expenses incurre

uring a particular year must be claime as euctions uring this year when the same

were incurre

CP+-D E to signify the fact that the taxpayer uses the 0S

BS+S >ner the 0S BS+S, an expense is recognizewhen it is P+-

C+90>;-D E implies that the taxpayer employs the 00>8

BS+S >ner the 00>8 BS+S, income is recognize

when earne regarless of the receipt of the same an

the expense is recognize when incurre

b #ust %e paid or incurred in connection 'ith the trade3 %usiness or profession of the

taxpayer!

c #ust %e proven %y RC+PS!

SPECIAL RE-UISITES .OR DEDUCTI!ILITY O. T#ESE ORDINARY F

NECESSARY EXPENSES

=. !"#%'(AT)!' 8!$ (%$*)%( $%'D%$%D

*his must be reasona%le, meaning, this must not be ostensible

Ca&e 5: Partnership was sol to a corp an it was agree that the partners will serve the corp an

ma%e it appear that they rener services So, compensation for services was ostensibly mae by

the corp

#eld *hese is a mere ostensible salary or payment for services not actually renere

because that amount really forms part of the properties purchase by the corp

Ca&e 9: 0orporate officers succeee in selling the property of the corp So, profit was erive

therefrom Bonuses were given to these corporate officers

#eld *he rule is settle Bonuses must be given in goo faith *here must be services

renere because bonuses are aitional compensation +n this particular case, there was really no

services renere because that sale was mae through a bro%er *he corp mae it appear that it

was through the efforts of these corporate officers that brought about a successful sale of

property

5onuses must %e iven in ood faith and in determinin 'hether %onuses 'ill form part

of the compensation for services rendered3 you have to consider the 31) nature of the business, 3")the financial capacity of the taxpayer an 3$) the extent of the services renere

>. AD*%$T)()'9 A'D #$!"!T)!'AL %+#%'(%(

6 +t must be reasona%le!

Ca&e: Sugar -ev?t 0orp pai P1"2,JJJJJ to lgue 0orp representing promotional expenses

"5

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 28/81

#eld *his is reasonable uner the circumstances because the particular buget sub(ect for

promotion involves million of pesos n uner that circumstances, the P1"2,JJJJJ is

reasonable as this may coincie with the efforts exerte consiering that the taxpayer has no

venture in that experimental pro(ect to establish that vegetables of investment company an this

involves millions of pesos

2. $%'T %+#%'(% a *he taxpayer must N1 %e the o'ner of the property or he has no e#uitable title over

the property

b *his is su%&ect to 'ithholdin tax! Kou cannot claim that the taxes suppose to be

withhel have not been pai or remitte to B+

C. T$A*%LL)'9 %+#%'(%(

6 *his must be incurred or paid 'hile Ka'ay from home)!

6 K6ome) oes not refer to your resience but to the station assignment or post

xample$ /rom home office to branch office, the traveling expenses incurre are

euctible n this inclues not only the transporatiotion expenses but also meal allowance anhotel accommoations

?. %'T%$TA)'"%'T %+#%'(%(

6 *his must not %e contrary to la'3 morals3 ood customs3 pu%lic policy or pu%lic order

6 ence, %ri%es3 4ic4%ac4s3 and similar payments are not deducti%le

6lso, the expenses incurre by the taxpayer in entertaining gov?t officials in 26star hotel to gain

political influence are not euctible

3. $%#A)$( A'D "A)'T%'A'% %+#%'(%(

6 1nly ordinary or minor repairs are deducti%le!

- xtra-ordinary repairs cannot %e claimed as deduction an in lieu of that, the taxpayer may not

be allowe to claim epreciation

- +f the cost of the repair increases the life of an asset for a period of more than one (9" year3 that

amount is consiere extra6orinary repair 1ther'ise3 it is consiere orinary repair

G. (##L)%( A'D "AT%$)AL(

6his must %e actually consumed durin the taxa%le year!

6 RULE ON SU!STANTIATION simply re<uires that ordinary and necessary expenses must

%e proven *he 2roof& re#uire inclue:

6N$O$R$E$D$8a .fficial receipts

b e#uate ecourse

c mount of ;xpense

-ate an place where such expense is pai or incurre

e 9ature of expense

9$ INTEREST

$%<)()T%( 8!$ D%DT)B)L)T:

1 *his must be pai or incurre ->+9' the taxable year

" *his must be pai or incurre in connection with the trae, business or profession of thetaxpayer

$ *here must be an obligation which is vali an subsisting

& *here must be an agreement in writing to pay interest

Ruestion 1:

<hat about that interest on unclaime salaries of the employees, is that interest

euctions

"A

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 29/81

nswerFel:

9., because there is no obligation or inebteness +t is the fault of the employees in

case they faile to claim their salaries

Ruestion ":

<hat about that interest charge to the capital of the taxpayer, is that euctible

nswer:

+nterest on cost6%eeping purposes is not euctible *his oes not arise uner an interest6

bearing obligation

T&%!$%T)AL )'T%$%(T @ an interest which is compute or calculate, not pai or incurre,

for the purposes of etermining the opportunity cost of investing in a business *his oes not arise

from legally emanable interest6bearing obligation *his is not a deducti%le interest!

Ruestion $:

<hat about interest on preferre stoc%, is this euctible

nswer:

s a rule, interest on preferred stoc/ is not deductible , because there is no obligation to

spea% of +t is in effect an interest on ivien *he reason why it is not euctible is that the

payment is epenent upon the profits of the corp +t will only be pai if the corp earn profitsn woul not be pai of the corp incurs losses

BT if it is not dependent upon corporate profits or earnings, that is deductible +f is

payable on a particular on a particular ate or maturity without regar to the corporate profits, it

is euctible

he Supreme Court mentions W1 (8" 0C1RS$

1 not epenent upon corporate profits! an" agreement as to the ate or term within which payment will be mae

)'T%$%(T !' 9!*7T (%$)T)%( is now taxable.

So, if the taxpayer obtaine a loan from P9B an use the procees in purchasing gov?t

securities, the interest is now taxable 8i%ewise, the interest expense pai on that loan, the

procees of the same, ha been use to purchase gov?t securities is now euctible

-$ <hat about an interest on a loan pai in avance, is this euctible 8et us say that the

taxpayer obtaine a loan from a ban% an it is payable within 2 years *he loan obtaine is

P2J,JJJJJ 9ow, it was eucte in avance, can that be claime as euctions

A$ 9. Kou can only euct the same when the installment is ue a particular year

INTEREST EXPENSES *#IC# ARE NON"DEDUCTI!LE 6PARCAPU81 +nterest expense on P;/;;- S*.0Q!

" <hen there is 9. ';;M;9* in writing to pay interest!

$ +nterest expense on loan entere into between ;8*;- *=PK;S

& +nterest pai or calculate for 0.S*6Q;;P+9' P>P.S;S

2 +nterest pai in -@90;

4 +nterest on obligation to finance P;*.8;>M ;=P8.*+.9

5 +nterest on >908+M;- S8+;S of the employees

$elated taxpayers$

a! mem%ers of the same family 'hich includes$

a1 spouses

"I

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 30/81

a" brothers an sisters

a$ escenants an ascenants

b %et'een t'o (8" corporations o'ned or controlled %y one individual! e must have a

controlling interest over these two corporations ., if one corp is consiere as

personal holing company of another corpc! %et'een a corp! and an individualL that individual o'ns or controls more than =G

of the outstandin capital stoc4 of the such corp! parties to a trust !

1 grant or fiuciary

" fiuciary of one trust an fiuciary of another trust but there is only one

grantor

$ beneficiary an fiuciary

OKour %nowlege of relate taxpayers is also important in etermining whether losses

are euctible or not +f losses 'ere incurred or paid in connections 'ith the

transactions %et'een these related taxpayers3 these are not deducti%le!

Ruestion: ow much interest expense is euctible

nswer: *he interest that may be claime as euctions shall be reuce

by:

a &1 6 Beginning Nanuary 1, 1IIA

b $I 6 Beginning Nanuary 1, 1IIIc $A 6 Beginning Nanuary 1, "JJJ of the income sub(ect to final tax

#P. 10 +NC1# S*5,C 1 0+N. $

1 interest on ban% eposit

" interest on eposit maintaine uner the foreign currency eposit system

So, if the interest income on ban% eposit amounte to P1JJ,JJJJJ n the total interest

expense incurre or pai by the taxpayer is P"JJ,JJJJJ +f this is incurre in 1IIA, &1 ofP1JJ,JJJJJ is P&1,JJJJJ *hat P"JJ,JJJJJ interest expense incurre or pai, shoul be

reuce to P&1 of that P1JJ,JJJJJ to arrive at P12I,JJJJJ which is the interest that may be

claime as euction

P"JJ,JJJJJ

6 &1,JJJJJ

66666666666666666666666 P12I,JJJJJ

*he rule has been establishe that S are N1 1RD+NRB 15.+2+1NS But the

Supreme Court in t'o (8" cases relaxed the distinction %et'een taxes and ordinary o%liations

1 *he interest on deficiency donor7s tax is deductible *he S0 explaine that taxes here areconsiere obligations or inebteness n it rule that we have to relax the istinction

between tax an orinary obligation in this respect

" )nterest on deficiency income tax can also be claimed as deductible interest expense

because taxes here are consiere orinary obligations

:$ TAXES

$%<)()T%( 8!$ D%DT)B)L)T: :

1 *his must be pai or incurre uring the taxable year

" *his must be taxes pai or incurre in connection with the trae, business or profession of thetaxpayer

OOO axes that may %e claimed as deductions may %e national or local taxes!

$J

8/12/2019 Taxation} Tax I

http://slidepdf.com/reader/full/taxation-tax-i 31/81

T&% 8!LL!;)'9 A$% '!'D%DT)BL% TA+%( 6S$I$N$E8

1 SPC+. SSSS#N E tax impose on the improvement of a parcel of lan

" +NC1# E *his inclues foreign income tax +n this regar, the so6calle foreign

income tax may be claime as a euction from gross income or this may be claime as taxcreit against Phil income tax +n the event that he claims that as tax creit, he can no

longer claim the same as euction

$ *axes which are N1 C1NNCD W+6 6 RD3 5*S+NSS 1R PR10SS+1N

10 6 PBR

& S 3 D1N1RFS 3see also iscussion on tax benefit rule)

TA+ A( D%DT)!'( vs. TA+ $%D)T

T *axes as euctions may be claime as euctions from gross income

T *ax creit is a euction from Phil income tax

T *ax as euction inclues those taxes which are pai or incurre in connection with the

trae, business or profession of the taxpayer owever, the sources of a tax creit is foreignincome tax pai, war profit tax, excess profit tax pai to the foreign country

T *he foreign income tax pai to the foreign country is not always the amount that may be

claime as tax creit because uner the limitation provie uner the *ax 0oe, it must not