tennis research 2015 state of the industry the bright spots in the tennis industry association’s...

TRANSCRIPT

mong the bright spots in the Tennis Industry Association’s 2015 “State of the Industry” report are a slight rise in overall tennis participation, growth in the number of youth tennis players, and 14.6 million Americans who, while not tennis players currently,

express an interest in playing the sport.But the annual report also indicates the industry

faces a number of challenges, including declining levels of consumer spending on equipment, a lower “core player” participation level, and an aging base of core players.

The TIA’s 2015 annual report, based on year-end 2014 research and data, puts the overall “tennis economy” at $5.73 billion, up 3.2% from a year earlier, and giving the sport a 104 on the TIA Economic Index scale, which is determined by factors such as expenditures for participation, facilities, programs, equipment, ad revenue, sponsorships, etc.

2015 State of the Industry

Tennis Research

While the latest TIA research shows some gains, the State of the Industry report points out a number of challenges we must address.By Peter Francesconi

A100

101 101

98

101 101

104

95

96

97

98

99

100

101

102

103

104

105

2008 2009 2010 2011 2012 2013 2014

TIA Economic Index 2008-2014

TOTAL TENNIS ECONOMYMeasuring the value of the tennis marketplace

$5.73 B

TOTAL PARTICIPATION 17.9 MTENNIS EQUIPMENT INDEXWholesale performance of racquets, balls and strings

Monitoring growth and tennis demographics

115

TIA STATE OF THE INDUSTRY

TENNIS INDUSTRY KEY INDICATORS

2 0 1 5 E D I T I O N

Tennis Industry Association—TennisIndustry.org Page 1

The full, 16-page 2015 State of the Industry report is available to all TIA members.

For membership information, visit TennisIndustry.org/Membership.

ParticipationOverall U.S. tennis participation is at 17.9 million players, up 1% from 2013, according to data from the Physical Activity Council (PAC) 2015 Participation Study, the largest single-source independent sports participation project in the U.S.

However, “core” tennis players, who play 10 or more times a year, dipped 1% to 9.91 million in 2014. Core tennis players account for an estimated 90% of total expenditures in the sport. Also, the percentage of adult core players in the 18-to-24 age segment dropped nearly 3%, while core players ages 55-plus increased 1%.

A significant opportunity exists for the industry to convert a “latent demand” by 14.6 million Americans who indicate they are interested in playing tennis. Plus, another 12 million consider themselves tennis players, but haven’t played in the last year. “As we move ahead with our collaborative efforts to grow this sport, we’re looking

Total Play Occasions (Millions) – PAC Study

21+ times 4-20 times 1-3 times Total

355.8 356.3 372.7 352.5

89.3 79.6 84.6

83.0

7.3 6.6 6.6

7.5

452 443464

443

0

100

200

300

400

500

2011 2012 2013 2014

Total Tennis Economy .........................................$5.73 BillionTotal Participation ................................................17.9 MillionYouth Tennis Participation Ages 6-12 ................................................................2.14 Million Ages 13-17 ..............................................................2.23 MillionCore Tennis Players (10+ times a year) ..........9.91 MillionCardio Tennis .........................................................1.62 Million

Manufacturer Year-End Wholesale Shipments (units)Tennis Racquets ....................................................2.96 MillionTennis Balls .............................................................124 MillionRed, Orange, Green Balls ....................................5.54 MillionTennis Strings ........................................................3.16 Million

Top Reasons People Played MORE Tennis in Previous Year:1. Had more time.2. Found someone/new people

to play with.3. Joined a tennis league.4. Took tennis lessons.

Top Reasons People Played LESS Tennis in Previous Year:1. Injury/health problem.2. Not enough time.3. No one to play with at my skill level.4. Moved where courts/players were

less accessible.

U.S. Tennis Participation – Physical Activity Council (PAC) Study (2007-2014)

15.75 17.75 18.55 18.72

17.77 17.02 17.68 17.90

0

2

4

6

8

10

12

14

16

18

20

2007 2008 2009 2010 2011 2012 2013 2014

Millio

ns of

Play

ers

The Industry at a Glance (2014 data)

2014

Tennis Players and Latent Demand – PAC Study

17.90 M

12.04 M

14.62 M

Latent Demand (number of non-playerswho are interested in tennis)Intermittent (consider themselves players)

Total Active Tennis Players

Tennis Research

For full report contact the TIA at [email protected] or call 866-686-3036.

Tennis Industry Association—TennisIndustry.orgPage 2

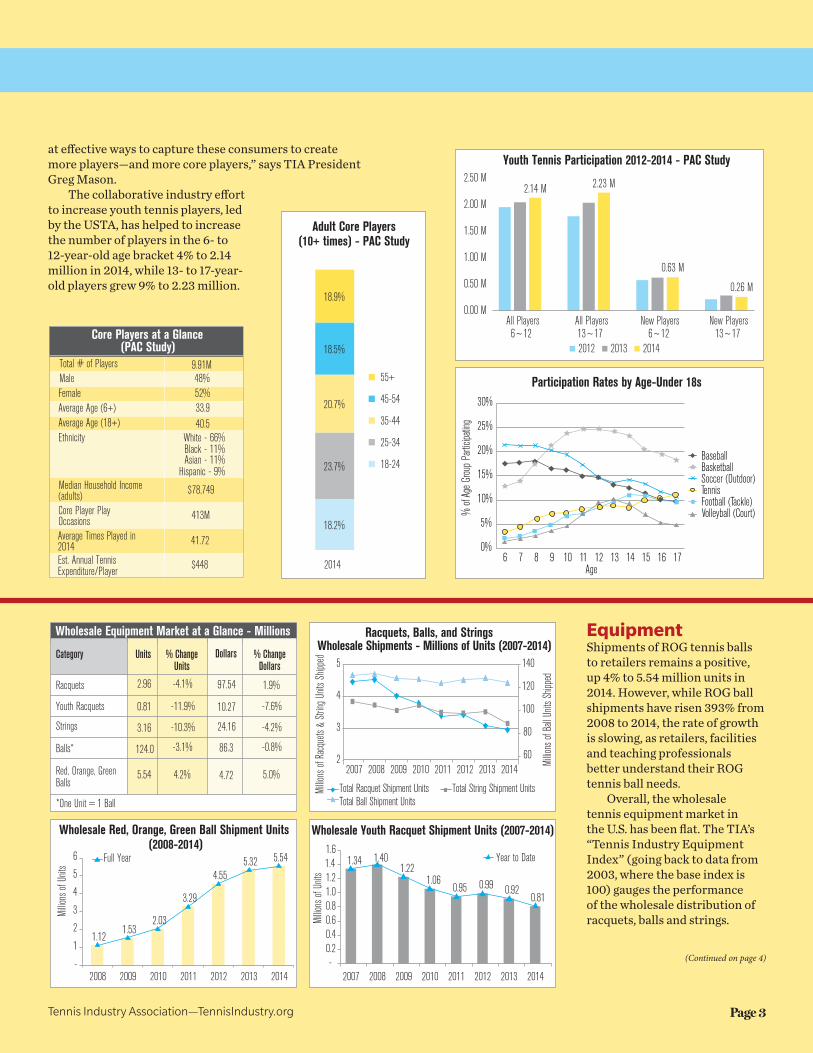

EquipmentShipments of ROG tennis balls to retailers remains a positive, up 4% to 5.54 million units in 2014. However, while ROG ball shipments have risen 393% from 2008 to 2014, the rate of growth is slowing, as retailers, facilities and teaching professionals better understand their ROG tennis ball needs.

Overall, the wholesale tennis equipment market in the U.S. has been flat. The TIA’s “Tennis Industry Equipment Index” (going back to data from 2003, where the base index is 100) gauges the performance of the wholesale distribution of racquets, balls and strings.

18.2%

23.7%

20.7%

18.5%

18.9%

2014

Adult Core Players(10+ times) - PAC Study

55+

45-54

35-44

25-34

18-24

Core Players at a Glance (PAC Study)

Female 52%Average Age (6+) 33.9Average Age (18+) 40.5Ethnicity White - 66%

Hispanic - 9% Asian - 11% Black - 11%

(adults) $78,749

Core Player Play Occasions 413M

Average Times Played in 2014 41.72

Est. Annual TennisExpenditure/Player $448

Median Household Income

Total # of Players 9.91MMale 48%

0%

5%

10%

15%

20%

25%

30%

6 7 8 9 10 11 12 13 14 15 16 17

% of

Age

Grou

p Pa

rticipa

ting

Age

Participation Rates by Age-Under 18s

Baseball Basketball Soccer (Outdoor) Tennis Football (Tackle) Volleyball (Court)

0.00 M

0.50 M

1.00 M

1.50 M

2.00 M

2.50 M

All Players6~12

All Players13~17

New Players6~12

New Players13~17

Youth Tennis Participation 2012-2014 - PAC Study

2012 2013 2014

2.14 M 2.23 M

0.63 M

0.26 M

Wholesale Equipment Market at a Glance - Millions

Category Units % ChangeUnits

Dollars % ChangeDollars

Racquets 2.96 -4.1% 97.54 1.9%

Youth Racquets 0.81 -11.9% 10.27 -7.6%

Strings 3.16 -10.3% 24.16 -4.2%

Balls* 124.0 -3.1% 86.3 -0.8%

Red, Orange, GreenBalls

5.54 4.2% 4.72 5.0%

*One Unit = 1 Ball

Racquets, Balls, and Strings Wholesale Shipments - Millions of Units (2007-2014)

60

80

100

120

140

2

3

4

5

2007 2008 2009 2010 2011 2012 2013 2014

Millio

ns of

Ball

Unit

s Ship

ped

Millio

ns of

Rac

quets

& S

tring U

nits S

hippe

d

Total Racquet Shipment Units Total String Shipment UnitsTotal Ball Shipment Units

Wholesale Red, Orange, Green Ball Shipment Units (2008-2014)

Millio

ns of

Unit

s

Wholesale Youth Racquet Shipment Units (2007-2014)

1.12 1.53

2.03

3.29

4.55 5.32 5.54

-

1

2

3

4

5

6

2008 2009 2010 2011 2012 2013 2014

Full Year

1.34 1.40 1.22

1.06 0.95 0.99 0.92

0.81

- 0.2 0.4 0.6 0.8 1.0 1.21.4 1.6

2007 2008 2009 2010 2011 2012 2013 2014

Millio

ns of

Unit

s

Year to Date

(Continued on page 4)

at effective ways to capture these consumers to create more players—and more core players,” says TIA President Greg Mason.

The collaborative industry effort to increase youth tennis players, led by the USTA, has helped to increase the number of players in the 6- to 12-year-old age bracket 4% to 2.14 million in 2014, while 13- to 17-year-old players grew 9% to 2.23 million.

Tennis Industry Association—TennisIndustry.org Page 3

Teaching Pros, Facilities and Court BuildersIn 2014, about 52% of teaching pros rated their business as “strong” or “very strong,” the highest since the survey began five years ago. Teaching professionals reported a 10% increase in the cost of private lessons, while the average group lesson and clinic charges increased 25% and 24%, respectively.

Overall, the average number of private lessons taught each week rose 4% in 2014, while the number of weekly group lessons surged 34%. For 2015, more than half of all tennis-teaching pros project their business to increase.

The TIA’s Court Activity Monitor (CAM) surveys 500 bellwether facilities across the country, and from late-season 2014 results, nearly 60% of facilities saw an increase in new 10U players. All other CAM components—including total courts used/book, new first-time adult players, rejoining adults, youth and adult tournament play and league play—also showed net gains.

Court builders also are optimistic about the current and future states of their business, with 44% rating it “strong” or “very strong,” and 65% expecting business to increase in 2015. For 2014, 65% of court contractors reported increased business, vs. 57% in 2013.

Pro/Specialty RetailersPro shop and specialty tennis retailers saw a drop in overall racquet unit sales of 1.9% in 2014, after a particularly tough 7% drop in the third quarter, which in part can be attributed to a work slowdown in West Coast ports that resulted in major delays in about 70% of U.S. imports from Asia.

While specialty retailers continue to express concerns over competition from online-only retailers, there is optimism over new “smart” technology which uses sensors in the racquet. “Players, coaches and teaching professionals can use this data to facilitate tennis instruction and improvement,” says TIA Executive Director Jolyn de Boer. “It can make tennis more enjoyable for players at all levels.”

The 2014 Equipment Index is unchanged from 2013 in “nominal dollars,” at 115, and dropped to 90 in “real dollars,” from 91 in 2013.

For year-end 2014, wholesale tennis racquets were down 4.1% to 2.96 million units, youth tennis racquets dropped 11.9% to 810,000 units, total tennis balls (which include ROG balls) were down 3.1% to 124 million, and tennis strings declined 10.3% to 3.16 million.

Long-term, the decline is more pronounced: from 2008 to 2014, total wholesale racquet shipments have dropped 35%, with the largest drop in mass merchants and chain stores, and in racquets at the low end of the price scale.

Pro/Specialty Retail Racquet Unit Sales - 2007-2014 (Thousands)

143 143 115 126 121 139 120 118

209 207 188 194 188 198 185 182

282 280 253 242 249 238

230 215

188 164 169 158 161 157

156 163

822 795 724 720 719 731

690 677

0

100

200

300

400

500

600

700

800

900

2007 2008 2009 2010 2011 2012 2013 2014

Thou

sand

s

Q1 Q2 Q3 Q4 Total

1. Very weak 2. Weak 3. Average 4. Strong 5. Very strong MeanCurrent State of the Tennis Teaching Business

1% 1% 2% 1% 2% 1% 13% 13% 10% 13% 16%

8%

48% 47% 47% 45% 39% 39%

35% 37% 37% 34% 39% 44%

3% 3% 4% 7% 4% 8%

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

ES 2010 LS 2010 2011 2012 2013 2014

Mean

Rati

ng

% of

Teac

her r

espo

nden

ts

3.503.27 3.28 3.31 3.32 3.27

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

ES 2010 LS 2010 2011 2012 2013 2014

% of

contr

actor

resp

onde

nts

1. Very weak 2. Weak 3. Average 4. Strong 5. Very strong Mean

13% 11% 9% 3%2%

53%

36%29%

30%

2% 6%

20%

39%49% 35%

50% 50%

13% 14% 14%

30%44%

32%

3% 2%12%

2.32.6 2.7

3.0

3.4 3.5

Current State of the Tennis Court Construction Business

Mean

Tennis Research

Tennis Industry Association—TennisIndustry.orgPage 4

(Continued from page 3)