thailand automotive industry and investment · pdf filethailand automotive industry and...

TRANSCRIPT

ThailandThailandAutomotive Industry andAutomotive Industry andInvestment OpportunitiesInvestment Opportunities

Ms. Ms. SudjitSudjit InthaiwongInthaiwong

Deputy Secretary GeneralDeputy Secretary General

Board of InvestmentBoard of Investment

16 March 200716 March 2007

ThailandThailand

Presentation OverviewPresentation Overview

• Economy and Business Climate Overview

• Infrastructure• Investment Opportunities• BOI Incentives and Outsourcing

services

Overview of ThailandOverview of Thailand’’s Economys Economyand Business Climateand Business Climate

Gross Domestic Product 5% in 2006*Foreign Direct Investment US$ 8.12 billion 2006US $41.34 billion State Budget 2007**Current Account at 6-year high US$ 3.2 billionUnemployment at 1.3% and underemployment at 1.7%Capacity utilization a steady 73.5%

*Revised by NESDB**1.566 trillion baht

Consistent growth and productivityConsistent growth and productivity

$37.88/THB

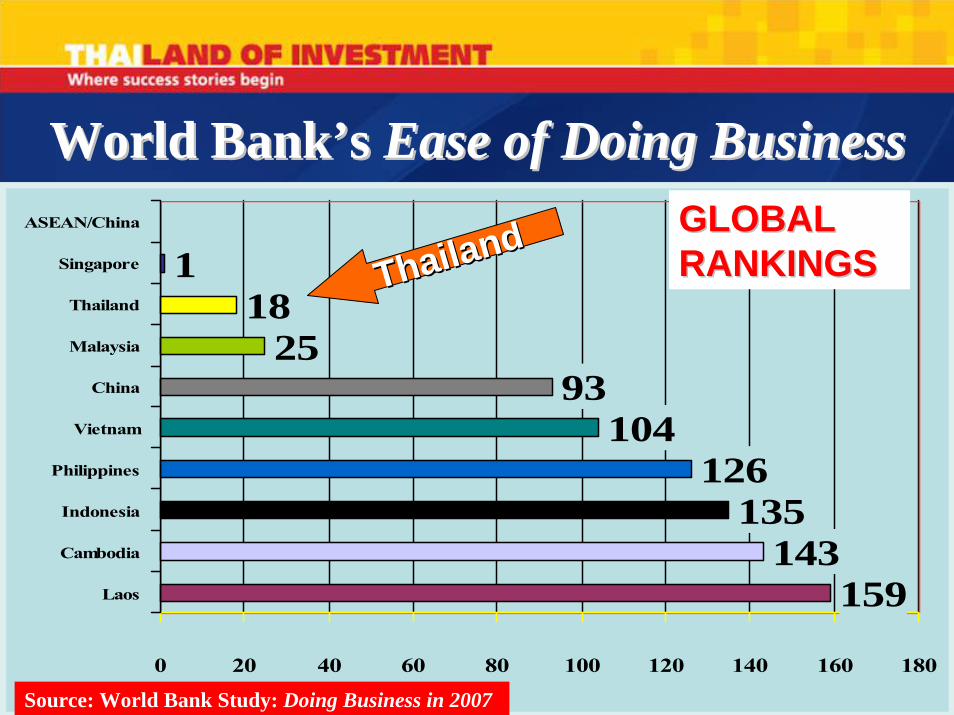

World BankWorld Bank’’s s Ease of Doing BusinessEase of Doing Business

159143

135

10493

2518

1

126

0 20 40 60 80 100 120 140 160 180

Laos

Cambodia

Indonesia

Philippines

Vietnam

China

Malaysia

Thailand

Singapore

ASEAN/China

ThailandThailand GLOBAL GLOBAL

RANKINGSRANKINGS

Source: World Bank Study: Doing Business in 2007

• UNCTAD survey of world’s 325 largest transnational corporations

• Asian region has most positive FDI prospects

• Overall, Thailand ranked #9 in worldVietnamTop 4

South KoreaTop 5

THAILANDTHAILANDTop 3Top 3

IndiaTop 2ChinaTop 1

Ranking of FDI Prospects in Asia

Thailand Rated #3 Most Thailand Rated #3 Most Attractive FDI Location in Attractive FDI Location in Asia by UNCTADAsia by UNCTAD (2005(2005--2008)2008)

UNCTAD Global Investments Prospects Assessment, Sept. 2005

JBIC FY 2006 SurveyJBIC FY 2006 SurveyWhen asked about profitability for each region, including Japan, “the percentage of companies answering “higher” was greatest for Thailand”In E&E, within the ASEAN4, the response to “strengthen or expand” is largest in Thailand.In automotives, “strengthen or expand”stronger in Thailand than any other region, including Southern China and North America.

Ranked 127 in global “Cost of Living Survey*A lowest cost destination within the region and the world

Avg. general industry wage US$146/mth**Avg. Monthly office rent US$11.67/sqm**

“Thailand’s assets include an entrepreneurial population, abundant natural resources and a wonderful lifestyle and, if these strengths are promoted and supported, the country will continue to be a great place to do business”

Grant Thornton International Business Owners Survey 2006

*Mercer Human Resources Consulting**Jetro Survey March 2006

Quality at Low CostQuality at Low Cost

630

33

35

35

48

5097

Singapore

Malaysia

Thailand

China

India

Philippines

Vietnam

Indonesia

Number of days to Number of days to incorporateincorporate

and register new firmsand register new firms

Source: World Bank Group www.doingbusiness.org

ThailandThailand

Low level of bureaucracy

Infrastructure

Enhanced InfrastructureEnhanced InfrastructureTransportationTransportation

National highwayNational highway system: 64,000 km connecting all 76 provincesExpanding connections into Cambodia, Laos, Vietnam and southern China

7 international airportsRail system:Rail system: 4,000 km linking to Malaysia & SingaporeCitywide light rail

US $4.8 billion expansion

CommunicationsMobile phones:Mobile phones: growing 8 million in 2006 to 39 million users, with a 60%+ market penetration rateWiWi--FiFi and broadband accessbroadband access

Shipping8 deep sea ports

Including tanks farms and liquid jetties

Ping Thong Industrial Estate

Hemaraj Land and Development PLC

Amata Industrial Estate

Gateway CityIndustrial Estate

Asia Industrial Estate

PadaengIndustrial Estate

Map Ta Phut Industrial Estate

Laem Chabang Industrial Estate

Wellgrow Industrial Estate

Golf Course

International School& University

Hospital

304 Industrial Park

RojanaIndustrial Park

Percentage of Foreign Investors in Percentage of Foreign Investors in Industrial EstatesIndustrial Estates

Japan

USA

England

Germany

Korea

Singapore

Australia

Taiwan

Belgium

Netherlands

India

Malaysia

China

Hong Kong

Thai Graduates by MajorThai Graduates by Major

Source: Commission on Higher Education; includes BA, MA, and post-graduate degrees

Major 2004 2005

Humanities and Social Sciences

229,561 232,704

Science, Technology, and Engineering

77,329 82,415

Health Science 12,942 17,105

Technology and Business Computer (vocational)

9,085 15,037

TOTAL 319,832 332,224

Thai Graduates in Science, Thai Graduates in Science, Technology, and EngineeringTechnology, and Engineering

Source: Commission on Higher Education; includes BA, MA, and post-graduate degrees

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2004 2005 2006 2007 2008 2009 2010

Investment Opportunities

““Sustainable Sustainable Production BaseProduction Base””

Thailand : The Automotive Hub of AsiaThailand : The Automotive Hub of Asia

Production Center

Exporting Center

Industrial StructureIndustrial StructureThailand Car sales

First-tier

Second-tier

Third-tier

648 Companies

1,641Companies

P a s s e n g e r C a r2 7 %

P P V & S U V7 %

P ic k u p T r u c k 1 to n

6 0 %

O th e r C o m m e r c ia l

C a r6 %

• Auto assembly for local and export markets under AFTA and other FTA arrangements

• Auto part manufacturing to serve domestic and export markets

• Motorcycle production for local and export markets

• NGV 2011 target: 257,000 cars, 533 stations

Investment Opportunities in Automotive Investment Opportunities in Automotive IndustriesIndustries

2010 Target 2010 Target –– WorldWorld’’s Top 10s Top 10• Total production of 2 million units• Domestic sales of 1 million units

1-ton trucks – 700,000 unitsPassenger cars – 250,000 unitsCommercial Veh. – 50,000 units

• Exports of 1 million units1-ton trucks – 800,000 unitsPassanger cars – 200,000 units

• Export opportunity of cars and auto-part OEM

““Production BaseProduction Base””Production Base of One-Ton Pick

Up

• Production Value within the country (GDP share)

• Value added share within country

• Producer opportunity for auto-part REM and Thai Accessories

High Low

70 – 80 % 10 - 50%

World Market Quota Quota

Good Opportunity

Hard to be true

PersistencePersistence Uncertain• Persistence in free trade market

• Thailand product image in foreign market

Sedan Assembly Factory

• Investment value within the country (the whole Cluster)

High Low

Yes No

Thailand: Automotive Hub of ASEANThailand: Automotive Hub of ASEAN

• 2006 production ~ 1,176,840 million units

• 15 assembly plants • Export ~ 539,206 units • Largest in Southeast Asia • Capacity of 2.0 million units by 2010 • Production of pickup trucks ~ 877,890

units – world’s largest one-ton pick-up truck manufacturer

Vehicle Production Vehicle Production 20062006

Source: Thailand Automotive Institute

Passenger Cars 298,678

Trucks 878,162

Motorcycles 2,079,555

Automotive Industry in ThailandAutomotive Industry in Thailand

682,693

539,206

1,176,840

1,177

158

559525434 389

584

459411

327

928

750683

262218

296363

589

485571

409

626

533

144

539

130 152 175 180 233332

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

21 8 1466420

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Production Domestic Export

Thousand Units

Avg. Growth 35% Per Year Avg. Growth 35% Per Year (1998 (1998 –– 2006) 2006)

Vehicle Production in ThailandVehicle Production in ThailandMotorcycles ExcludedMotorcycles Excluded

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Passenger Cars &Off-road PassengerVehiclesPickup and PickupPassenger Vehicles

Total (non-motorcycles)

Source:Thai Automotive Institute

Automotive ProductionAutomotive ProductionTop 15 Manufacturers (2005 data)Top 15 Manufacturers (2005 data)

0

2

4

6

8

10

12

1.U

S2.

Japa

n3.

Ger

man

y4.

Chin

a5.

S.K

orea

6.Fr

ance

7.Sp

ain

8.Ca

nada

9.Br

azil

10.U

K11

.Mex

ico

12.In

dia

13.R

ussia

14.T

hai

15.It

aly

5.6919.08 23.32

32.8846.42 47.42

57.60

76.81

108.26

132.69

13.340

50

100

150

1996 '97 '98 '99 2000 '01 '02 '03 '04 '05 '06

Unit: Million US$

Spare Auto Parts ExportsSpare Auto Parts Exports

$132.69$132.69

1.15 1.49 1.68 3.73 3.17 3.73 3.83 4.53

21.0518.04

18.23

0

10

20

30

1996 '97 '98 '99 2000 '01 '02 '03 '04 '05 '06Unit: Million US$

Vehicle Jig & Die ExportsVehicle Jig & Die Exports

US$18.23US$18.23

0

1000

2000

3000

1996 '97 '98 '99 2000 '01 '02 '03 '04 '05 '06Unit: Million US$

OEM Auto Component Part ExportsOEM Auto Component Part Exports

US$2,124.85US$2,124.85

Thailand Motorcycle ProductionThailand Motorcycle Production

1,414

907

1,328

1,767

2,0801,962

2,378

2,867

2,359

1,1791,050

8187711,047

1,5512,055

527784604

2,027

2,112

9111,236

1,465

1,575

831604585

27226721424513717886

1,338

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Uni

ts (1

,000

)

ProductionDomestic SalesExports

Source: Thai Automotive Institute

Thailand USA• Leader production country

1.2 Million cars 34.1 Million Cars• World Market size

0.4 Million Cars 0.2 Million Cars• Thailand Market size

One-Ton Pick Up

Sedan

0.8 Million cars 7.4 Million cars• Production volume of the leader country

Thailand is SS tt aa rr Thailand is DD oo gg• Analyze as Boston Model

"Global "Global Niche"Niche"

“Global Mass”• Product Positioning in the world market

Market StructureMarket Structure

Automotive Sales and ExportsAutomotive Sales and Exports

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Dom

estic

Sal

es (U

nits

0

100,000

200,000

300,000

400,000

500,000

600,000

Exp

orts

(Uni

ts)

SalesExports

57 Industrial Estates57 Industrial EstatesDeep seaports:Deep seaports:

5 million TEU 5 million TEU capacitycapacity

Suvarnabhumi Airport

Key InfrastructureKey Infrastructure25km

Laem Chabang Port

Eastern Seaboard Industrial A

rea

Many auto firms Many auto firms are located on are located on

ThailandThailand’’s Eastern s Eastern SeaboardSeaboard

Bangkok

Bangchan General Assembly

Y.M.C. Assembly

Thai Honda Manufacturing

Samutprakarn

Toyota Motor Thailand

Isuzu Motors (Thailand)

Siam Nissan Automobile

Siam V.M.C. Automobile

Thai Auto Work

Millennium Motors

Thai Yamaha Motor

Thai Swedish Assembly

Hino Motors (Thailand)

Thonburi Automotive

Assembly

Ayudhaya

Honda Automobile

(Thailand)

Pathumthani

Thai Suzuki Motor

Samutsakorn

Thai Rung Union Car

Rayong

Auto Alliance (Thailand)

General Motors (Thailand)

BMW Manufacturing (Thailand)

Kawasaki Motors Enterprise

(Thailand)

MMC Sittipol

Chachoengsao

Toyota Motor Thailand

Isuzu Motors (Thailand)

1. AUTOMOTIVE CLUSTER

Automotive Manufacturer Location

RayongTotal suppliers: 41

Body Parts: 24%, Engine Parts; Drive, Transmission &Steering Parts: 15% each, Suspension & Brake Parts: 12%, Electrical Parts: 10%, Accessories: 7%, Mold&Die: 2%, Other: 15%

SamutprakarnTotal suppliers: 158

Body Parts: 22%, Electrical Parts: 15%, Engine Parts; Drive, Transmission &Steering Parts: 8% each, Suspension & Brake Parts: 5%, Mold&Die: 4%, Accessories: 3%, Other: 36%

ChonburiTotal suppliers: 55

Body Parts: 25%, Engine Parts: 22%, Drive, Transmission &Steering Parts: 15%, Electrical Parts: 9%, Accessories: 5%, Suspension & Brake Parts: 4%, Mold&Die: 4%, Other: 16%

BangkokTotal suppliers: 232

Body Parts: 9%, Engine Parts; Electrical Parts; Drive, Transmission &Steering Parts; Accessories: 6% each, Suspension & Brake Parts: 4%, Mold&Die: 3%, Other: 60%

PathumthaniTotal suppliers: 39

Body Parts: 18%, Engine Parts; Electrical Parts: 13% each, Suspension & Brake Parts: 10%, Drive, Transmission &Steering Parts; Accessories: 8% each, Other: 31%

Principal Auto Parts Production Sites in ThailandPrincipal Auto Parts Production Sites in Thailand

Thailand is still in need of moulds & dies to produce the following products:

• Moulds for Die Casting- Engine block- Crank shaft- Front case- Oil pan- Gear box – auto- Safety parts : Master pump & Clipper brake

• Moulds for Plastic Injection - Automotive Electronic Control Unit (ECU)- Housing for automotive steering column - Automotive dashboard- Parts for digital camera & cellular telephone- Parts for notebook computer and PDA (personal digital assistant)

• Transfer press dies - Automotive body press die

More More Moulds & Dies Needed in ThailandMoulds & Dies Needed in Thailand

Priority Government PoliciesPriority Government PoliciesPromote NGVs and EcoPromote NGVs and Eco--carcar

Auto assembly for local and export markets under AFTA and other FTA arrangementsAuto part manufacturing to serve domestic and export markets Motorcycle production for local and export marketsNGV segment target: 120,000 NGVs by 2008

Investment Opportunities in Automotive Investment Opportunities in Automotive IndustriesIndustries

Opportunities in Component ProductionOpportunities in Component ProductionPassenger Car EnginesFuel Injection PumpsTransmissionsDifferential GearsInjection NozzlesElectronic SystemsElectronic Control UnitsTurbo ChargersSubstrates for Catalytic ConvertersAnti-Lock Brake Systems

NGV Reduces EnergyNGV Reduces Energy’’s Cost of Thailands Cost of Thailand

NGV station investment cost 43,600 million baht

NGV vehicle investment cost 45,700 million baht

Reduced oil consumption ~10 million liter/day

Increased NGV consumption ~365 million ft3/day

1. For Nation1. For Nation

Dubai Crude Price Level ($/BBL) 50

IRR 32%

NPV@12% 113,600

Reduced import value per year 62,200

Reduced energy’s cost per year 39,500

Unit: Million Baht

Remarks: Project life is 20 year (Investment is during 2006 – 2010).There are 500,000 vehicles with 740 NGV stations.Oil and gas price @ Dubai is $50/BBL.

NGV StationsNGV Stations

Technology for NGV VehicleTechnology for NGV VehicleDIESELDIESEL1. Dedicated NGV

- It uses NGV only.- Most vehicles are produced from manufacturers (OEM) and fitted the additional equipments or adapted the engines (Retrofit, Repowering).- It saves completely because of using NGV only.- The expense is high.

2. Duel Fuel- It uses both NGV and diesel or diesel only.- The vehicles are produced from manufacturers (OEM), fitted additional equipments, or adapted the engines (Retrofit, Repowering).- It has low expense and installs fast.- The duel fuel saves less than dedicated NGV.

Stations

NGV Expansion Target NGV Expansion Target

Type 2006 2007 2008 2009 2010 2011Benzene Car

22,890 52,000 74,700 101,000 128,000 160,000

Diesel Car 2,950 8,850 24,300 50,300 79,600 96,600

Total NGV 25,840 60,850 99,000 151,300 207,600 256,600

Region 2006 2007 2008 2009 2010 2011BKK/vicinity 73 181 212 253 277 285Countryside 31 89 138 172 203 250

Total stations 104 270 350 425 480 535

Vehicles

Technology for NGV VehicleTechnology for NGV VehicleBENZENEBENZENE1. Car with the installation of NGV equipments (Bi Fuel)

- Bi Fuel: It can select to use benzene or NGV.- Installation cost is ~30,000-60,000 baht. The capable distance is 150-200 kilometers.

2. There are two types of manufactured car (OEM) : Dedicated and Bi Fuel.

- Dedicated: It uses NGV only.- Bi Fuel: It can select to use benzene or NGV.-The car price will be added ~ 150,000-200,000 baht. The capable distance is 300-500 kilometers.

Fuel consumption no more than 5 litres/100 kmEmissions standards compliant with Euro4

specification or higherCarbon dioxide emissions no more than 120 gm/km

Safety standards for front and side impact to comply with UNECE Reg. 94 and Reg.95 specifications, or higher

EcoEco--Car Investment PromotionCar Investment Promotion

Project package must be proposed along with:auto assembly, motor manufacture and motor vehicle parts project, andinvestment and manufacture plan for 5-yr period must be included, along with actual production quantity of not less than 100k units/yr from the fifth year

Qualify on MOI energy saving, environmental and safety specifications

General GuidelinesGeneral Guidelinesfor Ecofor Eco--car Incentivescar Incentives

Why? <= 5 L/100 kmWhy? <= 5 L/100 km5L/100km = CO5L/100km = CO22 120g/km for Benzene engine120g/km for Benzene engine

In 1998, EU agreement with automotive companies that by In 1998, EU agreement with automotive companies that by 2008, 2012 cars sold in EU will have an average of 2008, 2012 cars sold in EU will have an average of CO2<=140g/km and 120g/kmCO2<=140g/km and 120g/km

““The European Commission has published an action plan on The European Commission has published an action plan on energy efficiency which restates the threat to the car industry energy efficiency which restates the threat to the car industry that legislation will come if the makers do not meet the EUthat legislation will come if the makers do not meet the EU’’s s carbon dioxide reduction target of 120 g/km by 2012.carbon dioxide reduction target of 120 g/km by 2012.””[European Federation for Transport and Environment, [European Federation for Transport and Environment, October 2006]October 2006]

BOIBOIIncentivesIncentives and outsourcing servicesand outsourcing services

The Board of Investment Basic Incentives and Measures

The Board of Investment The Board of Investment Basic Incentives and MeasuresBasic Incentives and Measures

Land ownership: A promoted company 50% or more foreign owned may apply, per section 27 Investment Promotion ActPermission to bring in technicians and expertsCorporate Tax exemption: 3 to 8 yearsImport duty exemption/reduction on machinery and raw materialsSubsequent 50% reduction of corporate income tax after expiration of exemptionDouble deductionDouble deduction of public utility costsDeductions for infrastructure construction/installation costs

Automotive Industry ClusterAutomotive Industry Cluster: : Assemblers & Suppliers Assemblers & Suppliers

Applying as Package for BOI PromotionApplying as Package for BOI Promotion

• ConditionsTotal investment at least THB 10 billion ($250 million) including component parts manufacturingCovers:

Automotive AssemblingManufacture of Vehicle Parts and Engines

• IncentivesAll Zones: Duty Free Machinery

Local SourcingLocal SourcingBUILDBUILD

Promote and develop supporting industriesStrengthen parts and component marketIncrease capability of Thai suppliersAssist suppliers to tailor parts and components production to the needs of manufacturersStimulate localization – induce manufacturers to source domesticallyAttract foreign investment

BUILD ProgramsBUILD ProgramsVendors meets customers

Suppliers taken directly to assembly plants

VMC Road ShowHannover Fair, MIDEST, MTech

BUILD MarketplaceSuppliers exhibit at domestic trade shows

BUILD Sourcing ProgramLocal sourcing for domestic and global supply chain

SubconSubcon 20072007300 component manufacturers to participate in Subcon Thailand 2007, held alongside Intermach ’07, South East Asia’s Premiere Machinery Exhibition

54

• Date and Time

9-13 May 2007 / 10.00 AM – 07.00 PM

(The exhibition is held during the same period as Intermach 2007)

• Venue

BITEC International Conference and Exhibition Center, Bangkok, Hall 105

• Exhibition Area

6,000 square meters

Show ProfileShow Profile

WWW.BOI.GO.THWWW.BOI.GO.TH