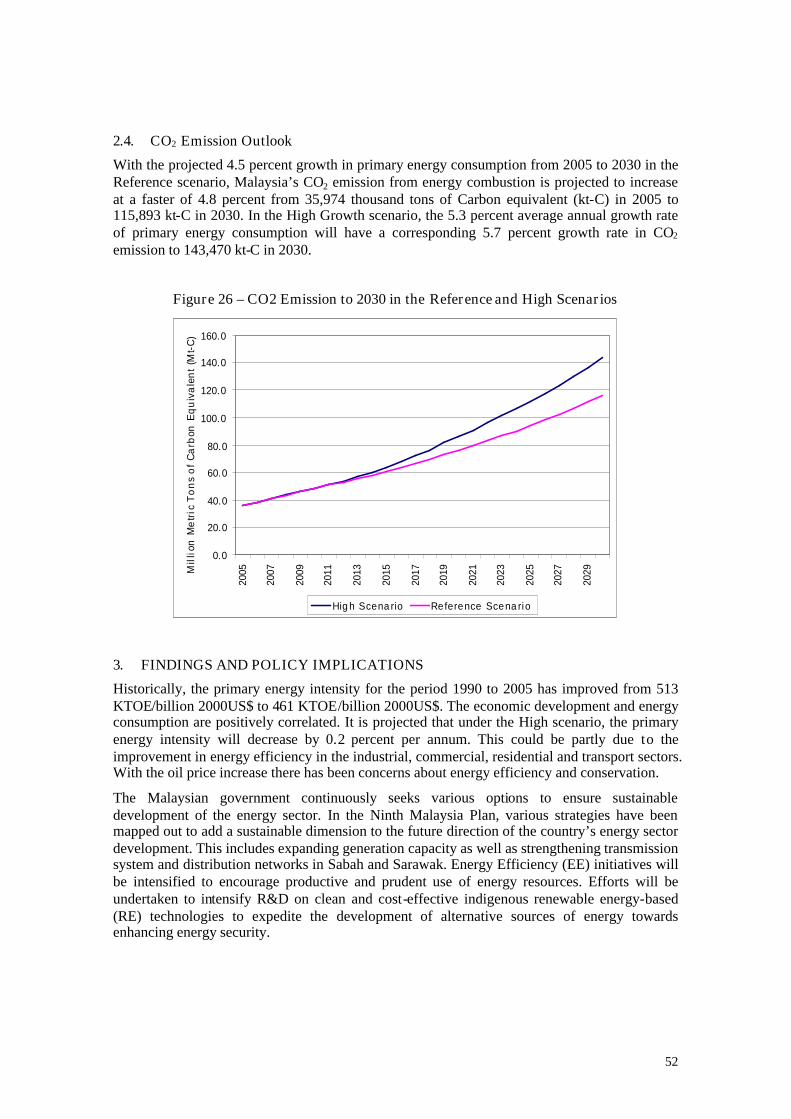

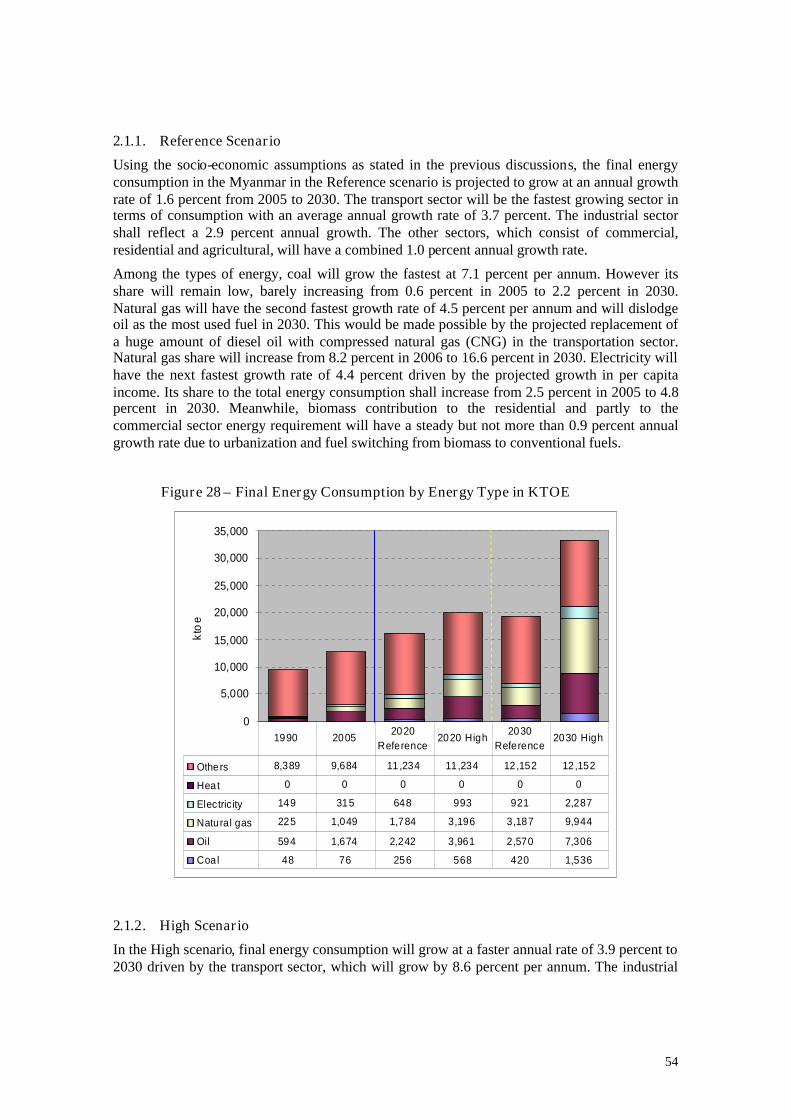

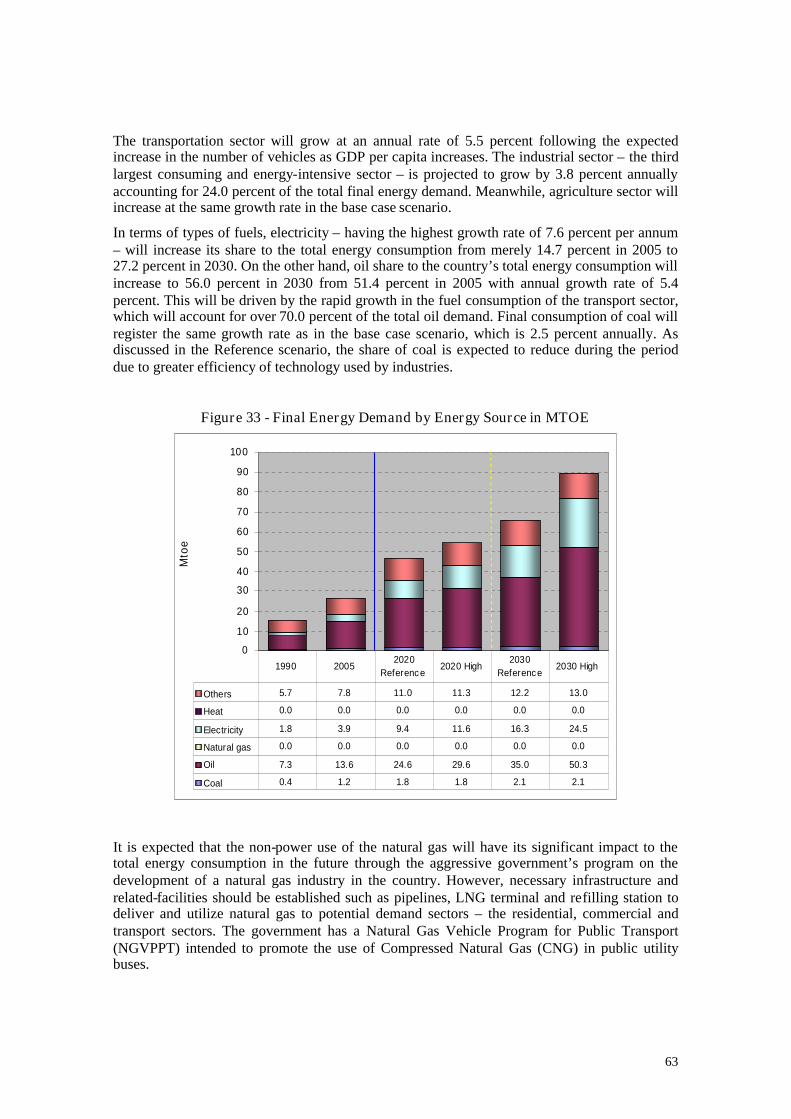

the 2nd asean energy outlook revapr14 - commend: community for

TRANSCRIPT

The 2nd ASEAN Energy Demand Outlook

Prepared in conjunction with theEnergy Supply Security Planning

for the ASEAN (ESSPA)

Prepared byThe Energy Data and Modeling Center

The Institute of Energy Economics, Japan,

The ASEAN Center for Energy

andThe National ESSPA Project Teams

for theASEAN SOE Leaders

and theMinistry of the Economy, Trade and Industry, Japan

March 2009

DISCLAIMER

This report was prepared as part of the activity under SOME-METI Programme onEnergy Supply Security Planning for the ASEAN (ESSPA). The data and assumptionsused were discussed and agreed on by the representatives of the participating ASEANmember states to enable harmonization of forecasting techniques and assumptions.These assumptions and modeling approaches may differ from those used in eachmember states. Therefore, the projections presented here should not be viewed asofficial national projections of the ASEAN member states.

i

FOREWORD

Japan has been involved in two cooperation programs in ASEAN region based on the SOME-METI Energy Cooperation Program. They are:

a. Energy Supply Security Planning in the ASEAN (ESSPA)

b. Promotion on Energy Efficiency and Conservation (PROMEEC)

This report contains the results of “2nd Energy Demand Supply Outlook in ASEAN” project,one of ESSPA activities, which was started in December 2007.

In order to evaluate past and current energy security situation in ASEAN region, Japan assistedthe ASEAN CENTER FOR ENERGY (hereafter referred to as ACE), the representative body ofASEAN region regarding energy issue, to develop the ASEAN Energy Database from year2001 to 2003, in order to maintain consistent annual historical energy data of the membercountries. Japan also conducted the project for forecasting future energy security situation inASEAN region based on future energy demand projected using the energy demand outlookmodel from 2003 to 2005. However, the main purpose of this cooperation program is capacitybuilding, thus The Institute of Energy Economics, Japan (hereafter referred to as IEEJ)transferred its technical know-how on energy demand supply outlook work to ASEANparticipants of this project in 2007 and the participants implemented the practical workthemselves. It was marvelous that all the participants which included even beginners couldreach the final step, in other words, succeeded to simulate energy outlook up to year 2030 usingthe model.

This report is the 2nd version of the outlook project. Differences from the 1st version of thereport are break-down of petroleum products, incorporation of refinery process and treatment ofindigenous production, and so on. In other words, the 2nd version of the ASEAN energy outlookmodel is enriched with more precise details than the 1st version. The participants prepared themain part of this report - the country discussions – while IEEJ and ACE worked on the otherparts.

I hope that this report would contribute as one of the references for policy decision making inmaintaining future energy security of Japan as well as the ASEAN.

Shigeru KimuraSenior Research FellowThe Energy Data and Modelling CenterThe Institute of Energy Economic, Japan

March 2009

ii

ACKNOWLEDGEMENT

The 2nd Energy Demand and Supply Outlook in the ASEAN is a project under the SOME-METIEnergy Cooperation Program on the Energy Supply Security Planning in the ASEAN. Thisoutlook is a product of a joint effort between ASEAN Member States, ASEAN Centre forEnergy (ACE) and Institute of Energy Economy Japan (IEEJ) to develop an energy demand andsupply outlook model for the ASEAN region up to 2030 and at the same time to enhance thecapacity building of ASEAN people in energy modeling.

We would like to acknowledge and express our sincere gratitude for all the supports providedby everyone who were involved as follows:

1. Mr. Kiyoshi Mori, Director, International Affairs Division, Agency for NaturalResources and Energy, METI, Japan, for the provision of the funding support necessaryto realize this activity and to release the publication,

2. Mr. Yukinori Seki, Section Chief, METI, for his full support in approving and realizingthe implementation of this activity under ESSPA Work Programme 2007 – 2008,

3. Dr. Weerawat Chantanakome for his support and advice on this activity in his role asACE Executive Director during the initial phase of ESSPA Programme 2007 – 2008,

4. Mr. Shigeru Kimura, Research Fellow, General Manager of the Energy Data andModeling Centre (EDMC), IEEJ, for his expertise, continuous guidance and advices,encouragement, and patience in proposing, negotiating, implementing and finalizing thesecond publication of Development of Energy Demand Supply Outlook in the ASEANfrom 2007 to 2009.

5. Mr. Edito Barcelona, Senior Researcher of IEEJ, for his kind guidance and advices toall the participants of ASEAN member states and for his patience in directing theparticipants as well as his editing of this report,

6. Mrs. Cecilya Malik Sastrohartono, Energy Expert from the Agency for the Assessmentand Application of Technology on her capacity as ACE representative, for her expertisein managing, implementing, reporting and finalizing the second publication ofDevelopment of Energy Demand Supply Outlook in the ASEAN and for her strong andsincere commitment to cooperate with IEEJ since 2003,

7. SOE Leaders of Brunei Darussalam, Cambodia, Indonesia, Lao PDR, Malaysia,Myanmar, Philippines, Singapore, Thailand and Vietnam for approving the 2nd EnergyDemand and Supply Outlook in the ASEAN and continuously supporting the activitiesunder ESSPA Work Programme until now,

8. ESSPA / REPP-SSN Focal Points for their cooperation in approving and providingappropriate technical personnel to participate in the 2nd Energy Demand and SupplyOutlook in the ASEAN,

9. Ms. Noor Dina Zharina Yahya, Ms. Adelina Jaya and other Brunei personnel for theirhard work in modeling and finalizing the Brunei Energy Demand and Supply Outlook,

10. Mr. Heng Kunleang, Mr. Sok Chandareth and other Cambodia personnel for their hardwork in modeling and finalizing the Cambodia Energy Demand and Supply Outlook,

11. Mr. Golfritz Sahat, Ms. Fifi Indarwati and other Indonesia personnel for their hard workin modeling and finalizing the Indonesia Energy Demand and Supply Outlook,

iii

12. Mr. Khamso Kouphokham, Ms. Sengdeuane Vonginh and other Lao PDR personnel fortheir hard work in modeling and finalizing the Lao PDR Energy Demand and SupplyOutlook,

13. Ms. Yuzlina Mohd. Yusop, Mr. Zaharin Zulkifli, Ms. Marhaini binti Mat and otherMalaysia personnel for their hard work in modeling and finalizing the Malaysia EnergyDemand and Supply Outlook,

14. Mr. Zaw Aung, Mr. U Kyaw Min Thu for their hard work in modeling and finalizingthe Myanmar Energy Demand and Supply Outlook,

15. Mr. Danilo Javier and Mr. Michael Sinocruz for their hard work in modeling andfinalizing the Philippines Energy Demand and Supply Outlook,

16. Ms. Latha R. Ganesh and other Singapore personnel for their hard work in modelingand finalizing the Singapore Energy Demand and Supply Outlook,

17. Ms. Supit Padprem, Mr. Wattanapong Kurovat, and other Thailand personnel for theirhard work in modeling and finalizing the Thailand Energy Demand and Supply Outlook,

18. Mr. Nguyen Minh Bao, Ms. Pham Thi Quynh Nga for their hard work in modeling andfinalizing the Vietnam Energy Demand and Supply Outlook,

19. Mr. Akhmad Nidlom, Ms. Andini Desita Ekaputri, and other ACE personnel for alltheir support and commitment in the initiation, implementation, proofreading andfinalization of the 2nd Energy Demand and Supply Outlook in the ASEAN,

20. Other experts and personnel from, among others, IEEJ, APERC, ASEAN member stateswho participated and provided valuable inputs from the initiation, implementation, andfinalization of the 2nd Energy Demand and Supply Outlook in the ASEAN.

Nguyen Manh Hung

Executive Director

ASEAN Centre for Energy

iv

ABBREVIATIONS AND ACRONYMS

ACE – ASEAN Center for EnergyAEEMTRC – ASEAN-EC Energy Management Training and Research CenterAPSA – ASEAN Petroleum Sharing AgreementASEAN – Association of Southeast Asian NationsCCGT – Combined-cycle gas turbineCDM – Clean Development MechanismCNG – Compressed natural gasCO2 – Carbon dioxideEDMC – The Energy Data and Modeling CenterESSPA – Energy Supply Security Planning for the ASEANGDP – Gross domestic productGTL – Gas-to-liquidGVA – Gross value addedIEA – International Energy AgencyIEEJ – The Institute of Energy Economics, Japankt-C – Thousand tons of Carbon equivalentKTOE – Thousand tons of oil equivalentLEAP – Long-range Energy Alternative Planning SystemLNG – Liquefied natural gasMETI – Ministry of the Economy, Trade and Industry, JapanMTOE – Million tons of oil equivalentOECD – Organization for Economic Cooperation and DevelopmentR&D – Research and developmentSOE – Senior Official on EnergyTOE – Tons of oil equivalentTWh – Terawatt-hourUSD – United States Dollar

v

TABLE OF CONTENTS

Foreword iAcknowledgement iiAbbreviations and Acronyms iv

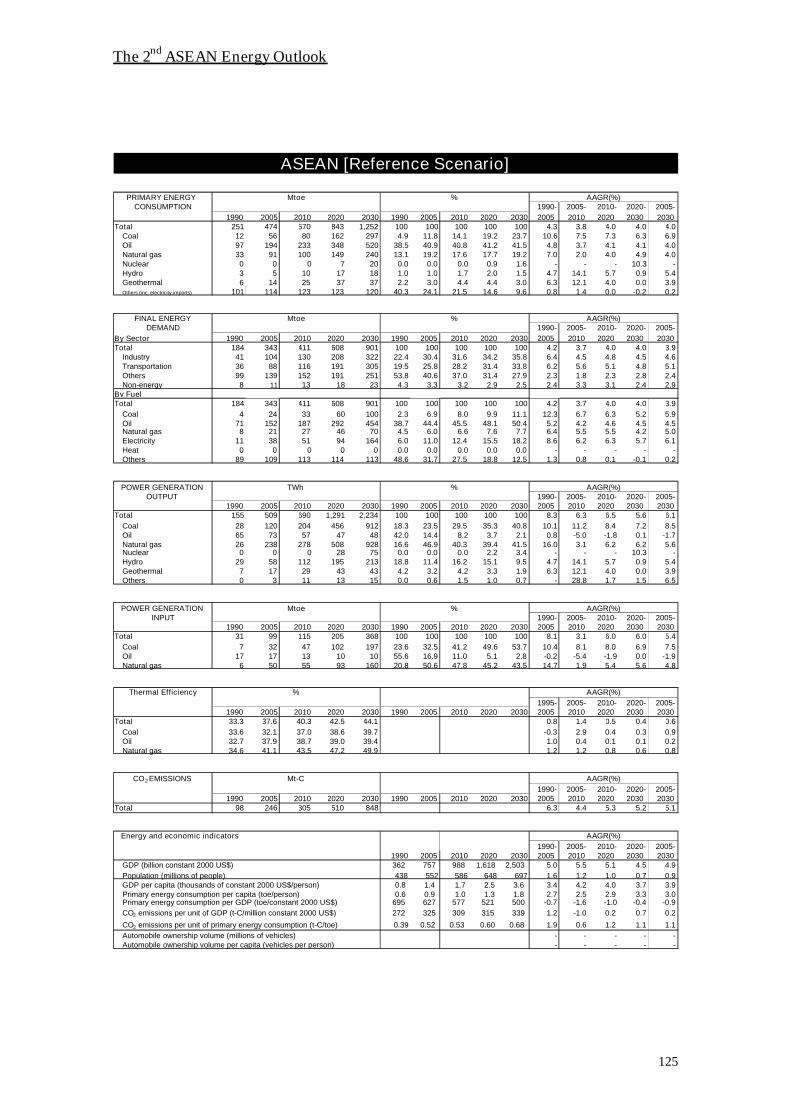

Executive Summary 1Introduction 3Socio-Economic and Energy Situation in the ASEAN in 2005 5Methodological Framework 6Forecast Assumptions 9Energy Demand and CO2 Emission Outlook 12

Final Energy Consumption 12Primary Energy Supply 14Power Generation 16CO2 Emission Outlook 17

Implications and Policy Recommendations 18

Annex 1 – Country Reports 21Brunei Darussalam 23Cambodia 29Indonesia 35Lao PDR 41Malaysia 47Myanmar 53Philippines 59Singapore 69Thailand 75Vietnam 81

Annex 2 – Final Energy Demand Equations 87Annex 3 – Naming Conventions for Sectors, Energy and Key Variables 121Annex 4 – Results Summary Tables 123

vi

LIST OF FIGURES

Figure 1 – Structure of the ASEAN Energy Model 7Figure 2 – Nominal Oil Price Assumption 11Figure 3 – Projected Final Energy Consumption in ASEAN by Sector 12Figure 4 – Projected Final Energy Consumption in ASEAN by Fuel Type 13Figure 5 – Primary Energy Requirements in ASEAN 15Figure 6 – CO2 Emissions in the Reference and High Scenarios, in Mt-C 17

LIST OF TABLES

Table 1 – Work Schedule of the ESSPA energy Demand Outlook ModelActivities 5

Table 2 – Average Annual GDP Growth Assumptions, Reference Scenario, inPercent 10

Table 3 – Average Annual GDP Growth Assumptions, High Scenario, in Percent 10Table 4 – Average Annual Population Growth Assumptions, in Percent 11Table 5 – Electricity Production in ASEAN (Reference and High Scenarios), in

TWh 16Table 6 – Fuel Inputs to Power Generation in ASEAN, in MTOE 16

THE 2ND ASEAN ENERGY OUTLOOK

EXECUTIVE SUMMARY

The 2nd ASEAN Energy Outlook is an update of the 1st ASEAN Energy Outlook prepared in2005 in conjunction with the SOME-METI joint cooperation program on capacity building forEnergy Supply Security Planning in the ASEAN. The intention was to develop an energydemand outlook model in ASEAN while at the same time provide capacity building to ASEANenergy analysts in energy demand modeling.

This outlook has covered all the 10 member states of the ASEAN while the 1st outlook was onlyable to cover 6 member states due to limitations in data availability for 2 states andunavailability of technical staff that could participate in the forecasting work from 2 other states.

This work is a joint output of Japan being represented by The Institute of Energy Economics,Japan (IEEJ) and 10 national energy outlook teams from the 10 member states with thecoordination and logistics work handled by the ASEAN Centre for Energy (ACE).

The energy data used in the modeling work were taken from the Energy Balances for Non-OECD Members Countries that is published by the International Energy Agency annually. Theeconomic and social indicators were obtained from the World Bank’s World DevelopmentIndicators that is also published annually. Other relevant data that are not available from thispublication are obtained from national sources.

The assumptions used were proposed by IEEJ which includes GDP growth rate for theReference scenario, population growth rate obtained from UN Department of Economic andSocial Affairs, crude oil price assumptions and GDP deflators which were projected by IEEJ.

The methodology applied for the final energy demand forecasting was econometrics while theestimation of primary energy consumption used an engineering based model but thedevelopment programs of each member states were the major inputs used in the models. Themodeling work was carried out in three 1-week working/training meetings and in sets ofhomework given to each national team after every meeting.

As results of the foregoing, the following are the energy and CO2 emission outlook in the nexttwo and a half decades:

Final energy consumption in ASEAN will grow at an average annual rate of 3.9 percentfrom 343 MTOE 2005 to 901 MTOE 2030 in the Reference scenario with thetransportation sector experiencing the highest growth in consumption of 5.1 percent perannum. The industry sector consumption will grow at an annual rate of 4.6 percentwhile the consumption of the combined residential, commercial and agriculture sectorswill have a slower growth of 2.4 percent per annum. Electricity will have the highestgrowth rate among the energy consumed in the final consumption sector at 6.1 percentper annum. This is followed by coal at 5.9 percent, natural gas at 5.0 percent and oil at4.5 percent. Biomass will have a slow growth rate of 0.2 percent per annum.

The corresponding primary energy consumption will have a faster growth rate of 4.0percent per annum with coal having the fastest annual growth rate of 6.9 percent. This isdue to the projected rapid growth in electricity consumption that will be met largely bycoal-fired generation. Hydropower will have the second fastest growth rate of 5.4percent as countries in the Great Mekong Sub-region decide to develop their vasthydropower potential. Oil and natural gas will have the next fastest growth rates of 4.0

2

percent per annum. Oil will remain as the major source of energy in the region evenincreasing its share to the total primary energy supply from 40.9 percent in 2005 to 41.5percent in 2030. Nuclear energy will be introduced in the region before 2020 and willhave a 0.9 percent share of the total by 2020 which will increase to 1.6 percent in 2030.Geothermal energy will be developed in the Philippines and Indonesia which will resultto 3.9 percent annual growth rate in the primary energy supply. Biomass will continueto grow albeit at a slow pace of 0.2 percent per annum. The growth in energyconsumption will increase per capita energy consumption from 0.9 TOE per person in2005 to 1.8 TOE per person in 2030. However, energy consumption per unit of GDPwill decrease from 627 TOE/million US dollars1 (USD) in 2005 to 500 TOE/millionUSD in 2030, a reduction of 20.3 percent over a 25-year period.

The above growth in primary energy consumption will result to a corresponding 5.1percent annual growth in CO2 emission. This is due to the faster growth rate in theconsumption of carbon-based energy sources than in the growth of carbon-free sourcessuch as nuclear and renewable energy. As a result, CO2 emission per unit of energyconsumption will increase from 0.52 tons of carbon equivalent (kt-C)/TOE in 2005 to0.68 kt-C/TOE in 2030. CO2 emission per unit of GDP will also increase at averageannual rate of 0.2 percent from 325 kt-C/million USD in 2005 to 339 kt-C/million USDin 2030

The abovementioned findings raised implications to the energy supply security and globalenvironmental stability. There was an agreement among the national teams that the followingmeasures need to be taken to face the future challenges posed by rapidly increasing energyconsumption:

Utilize CDM to mitigate climate change

Diversify the energy mix to reduce overdependence on certain energy sources andincrease utilization of indigenous energy, such as low-grade coal, to decreasedependence on imported energy.

Promote technology transfer and development on clean coal technology from thedeveloped world and encourage R&D in renewable energy, energy efficient and cleantechnologies as well as alternative fuels.

Promote energy efficiency and conservation by encouraging modal shift in thetransportation sector, use more efficient technologies to reduce consumption of biomassand intensify energy efficiency and conservation program in the short- and long-termsacross all sectors.

Accelerate development of clean energy such as renewables and alternative energy byencouraging the use of alternative fuels from biomass, enhancing renewable energy toreplace oil consumption in the final sector, increasing renewable energy and attain amore balanced mix in electricity generation, utilizing alternative fuels such as CNG inthe transportation sector., and formulating policies to promote the utilization ofrenewables, alternative fuels and nuclear energy.

Create an energy investment climate conducive to investors by formulating appropriatepolicies and incentives to encourage investment to develop geothermal, hydropower aswell as hydrocarbon resource potential.

Strengthen regional cooperation especially in sharing best practices in energydevelopment and utilization

1 All US dollar (USD) values are in constant 2000 prices unless specified

3

1. INTRODUCTION

This section explains the circumstances that resulted to the publication of the ASEAN EnergyOutlook in 2005. Discussion on the preparation of the energy outlook in the ASEAN arosewhen ACE with the assistance of IEEJ started to analyze the energy supply security in theregion.

After this introductory section the methodological framework follows with the basicassumptions of the model coming next. The next section discusses in detail the energy outlookof the ASEAN region with the energy outlooks of individual participating member statesdiscussed in Annex 1. The implications of the outlook outcomes to energy security of the regionare also discussed. The policy recommendation to address the emerging energy security as wellas environmental problems will be presented in the last part of the main body of the report.

1.1. Energy Supply Security Planning in the ASEAN (ESSPA) and Development of theASEAN Outlook Model

On January 1, 1999, ASEAN established the ASEAN Centre for Energy (ACE) as a successorof the 10-year old organization AEEMTRC (ASEAN-EC Energy Management training andResearch Centre) established jointly by the ASEAN and the European Union (EU) in 1988.

As a full-pledge ASEAN body, ACE conducted specific projects on energy in the region. Oneof the activities conducted by ACE was ESSPA. This activity is part of the SOME-METI jointCooperation Program on energy initiated in 2000 and agreed by the ASEAN and Japan SOELeaders during their First SOME-METI Consultation.

This ASEAN-Japan Energy Security Cooperation program was established on the basis of thefollowing:

A stable energy supply is indispensable to economic growth, and oil is and will be a mainplayer in energy.

Future high economic growth will inevitably increase energy use. Though there are someAsian countries which produce oil, Asia as a whole, as well as ASEAN, will rapidlyincrease oil imports from outside Asia. Therefore, securing a stable supply of energy,particularly oil, is important for policy makers in Asia.

Recent trends show a high volatility in the volume and price of oil. The increase of oilimports may aggravate the fragility of the ASEAN economy against oil supply disruptionsand fluctuations in oil price.

Securing a stable trade in oil, in terms of volume and price, is an essential task of thegovernments. There must be mechanisms and infrastructure to cope with this issue.

Japan has experienced two oil shocks, and the Japanese Ministry of Economy, Trade andIndustry (METI), previously Ministry of International Trade and Industry (MITI), has beenformulating and improving its energy policy.

These experiences in Japan may be useful for ASEAN in considering the strengthening ofits energy security by revising the ASEAN Petroleum Sharing Agreement (APSA) and othermeasures such as emergency preparedness and stockpiling.

The scope of the cooperation program covers the following:

Information exchange and seminars for energy policy experts of ASEAN and Japan.

Visits to facilities and study of the mechanisms in Japan by ASEAN energy policy officials.

4

Initiate joint research on how to strengthen energy security in ASEAN, which willcontribute to the revision of APSA, and the establishment of emergency preparedness andnecessary infrastructure such as oil stockpiling.

Recognizing the importance of energy supply security in ASEAN, the Energy Supply SecurityProgram in ASEAN (ESSPA) was then conducted by establishing a working group responsiblefor analyzing energy security in ASEAN with ACE and IEEJ as implementing agencies.Because future energy demand is a key factor for evaluating energy security in ASEAN, ESSPAfocal points decided to develop an ASEAN Energy Demand Model as part of the ESSPAactivities for 2004-2005.

The objectives for conducting the Energy Demand Outlook Model activity for 2004-2005 weretwo folds. First was capacity building to increase and enhance the participating membercountries capability in developing energy demand outlook model based on econometricapproach. Second, the objective was to develop the outlook model of these participatingmember countries in order to forecast their energy demand up to year 2030 and study theimplications in securing future energy supply of ASEAN through comparison between theforecasted energy demand and energy supply planning information.

The Energy Demand Outlook Model was conducted focusing only on the six major ASEANcountries namely Indonesia, Malaysia, Myanmar, Philippines, Thailand and Vietnam. Theoutcome of which was published in 2006 with the title Final Report on the Development ofEnergy Demand Outlook Model for the ASEAN Project.

1.2. The 2nd Energy Demand Outlook Model Project

To update the ASEAN energy demand outlook model of 2005, the ESSPA activities for 2007-2008 focused on the 2nd energy demand outlook model project. The coverage of the secondoutlook demand outlook model expanded to include the remaining four ASEAN membercountries. Thus, Brunei Darussalam, Cambodia, Laos and Singapore joined the modelingactivities in addition to the previous six ASEAN member countries, Indonesia, Malaysia,Myanmar,Philippines, Thailand and Vietnam.

Prior to development of the 2nd ASEAN energy demand outlook model, a pre-meeting wasconducted in Vietnam on 28 February to 1 March 2007. The objective of the pre-meeting was toexplain the works conducted in the initial ASEAN demand outlook mainly to the four newlyparticipating countries and also to share and understand purposes and outcomes of 2nd EnergyDemand Outlook:

Estimate demand by each petroleum product

Collect local energy prices & activity data and apply them for estimation of demandfunction

Collect future national energy plans, such as electricity and gas

Reconstruct power generation module

Incorporate refinery module

Other transformation like GTL, LNG

As in the first ASEAN energy demand model outlook development, the implementation of thisproject was also in phases consisting of training and homework in model development, modelimprovement, model simulation and finally report writing. There were three meetings organizedin 2007 to monitor and evaluate the model development process. These were:

5

a. Kick-off Meeting conducted on 3 - 5 December 2007, in Jakarta, Indonesia.

b. Follow-Up Meeting conducted on 30 January - 1 February 2008 in Bangkok, Thailand

c. Final Meeting conducted on 17-18 March 2008 in Singapore.

Table 1 shows the working schedule for the 2nd Energy Demand Outlook Model Project. Thisreport on the 2nd Energy Demand Outlook of ASEAN is the outcome of the Energy DemandOutlook Model Project.

Table 1 - Work Schedule of the ESSPAEnergy Demand Outlook Model Activities

Month Training Home Work

3-5 December, 2007(Kick-off work meeting)

Import the data into MICOFIT,understand how to use MICROFITand confirm the model structure

December 2007- January2008

Estimate energy demandequations using MICROFIT,complete the model systemand confirm it to IEEJ

End of January 2008(Follow-up work meeting)

Finalize future assumption,understand to use LEAP and completeBAU scenario

February – March 2008 Future simulation of severalscenarios by LEAP andsummarize energy demand to2030

Middle of March 2008(Review work meeting)

Finalization of future energy demandand Extraction of implications

By the end of May 2008 Prepare country report basedon the finalized energyoutlook and the extractedimplications

2. SOCIO-ECONOMIC AND ENERGY SITUATION IN THE ASEAN IN 2005

The Association of Southeast Asian Nations or ASEAN is a regional organization that wasestablished on 8 August 1967 in Bangkok by the five original Member Countries, namely,Indonesia, Malaysia, Philippines, Singapore, and Thailand2. Brunei Darussalam joined on 8January 1984, Vietnam on 28 July 1995, Laos and Myanmar on 23 July 1997, and Cambodia on30 April 1999.

The ASEAN region’s total land area covers 4.33 million square kilometers equivalent to 3.3percent of the world’s land area (bigger than India but is less than half of Brazil). It has a totalpopulation of 552 million in 2005 which is about 8.5 percent of the total world population. TotalGDP was 757 billion USD and per capita GDP among the 10 member states ranged from 260 to26,000 USD during the same period.

2 http://www.aseansec.org/64.htm

6

The region’s economy has experienced a rapid growth during the past two and a half decadeswith GDP growing at an average annual rate of 5.5 percent from 1980 to 2005. The populationgrew at an average rate of 1.7 percent per annum during the same period indicating acorresponding growth in per capita GDP.

Total primary energy consumption in 2005 reached 474 MTOE which grew at an averageannual rate of 4.3 percent from 1990. Per capita primary energy consumption stood at 0.9 TOEper person in 2005 while the region’s primary energy intensity was 627 TOE/million USD.Energy to GDP elasticity from 1990 to 2005 was 0.86 indicating that energy consumption isgrowing at a slower rate than GDP.

The region collectively, exported 74.8 MTOE of coal and 60.7 MTOE of natural gas in 2005. Itused to be a net oil exporter but has become a net importer since 1995 and in 2005, 30 percentof its total oil requirements has to be imported.

The 2nd Energy Demand Outlook for the ASEAN now covers the ten ASEAN member states;i.e.: Brunei Darussalam, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines,Singapore, Thailand and Vietnam.

3. METHODOLOGICAL FRAMEWORK

The energy demand projections of all the member states up to 2030 were estimated using theeconometrics approach wherever possible. Historical energy demand data were taken from theEnergy Balances for Non-Organization for Economic Cooperation and Development (Non-OECD) Countries of the International Energy Agency (IEA). The economic indicators used inenergy modeling such as Gross Domestic Products (GDP) and Gross Value Added (GVA) weretaken from the World Development Indicators Publication of the World Bank. Other socioeconomic data such as numbers of households and vehicles were obtained from national sources.

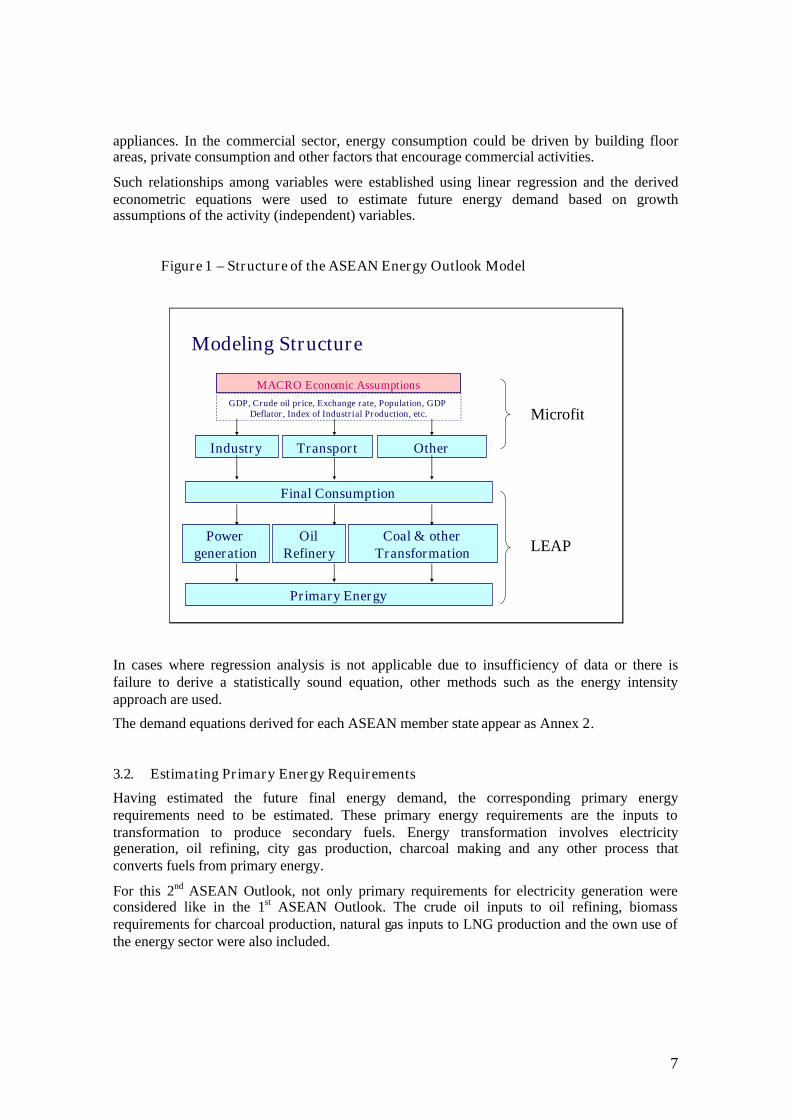

Energy modeling involved the estimation of final energy consumption (FEC) and thecorresponding primary energy requirements or supply. Figure 1 shows the model structure fromfinal energy demand projection and estimation of transformation inputs to arrive at the primaryenergy requirements including the computer software used in the modeling work.

3.1. Forecasting Final Energy Demand

The method applied in forecasting final energy demand as mentioned earlier was theeconometric approach. The historical correlation between energy demand as well asmacroeconomic and activity indicators were derived by regression analysis using Microfit3.

The future energy demand for various energy sources were estimated using assumed values ofthe macro-economic and activity indicators. Future values of these indicators were also derivedusing historical data depending on the sufficiency for such analysis.

In the model structure, energy demand is modeled as a function of activity such as income,industrial production, number of vehicles, number of households, number of appliances, floorarea of buildings and etc. In the residential sector for example, the demand for electricity couldbe a function of number of households, disposable income and penetration rate of electrical

3 Microfit is a computer program that offers an extensive choice of data analysis options. It is a versatileaid in evaluating and designing of advanced univariate and multivariate time series models. It is aninteractive, menu-driven program with a host of facilities for estimating and testing equations, forecasting,data processing, file management, and graphic display.

7

appliances. In the commercial sector, energy consumption could be driven by building floorareas, private consumption and other factors that encourage commercial activities.

Such relationships among variables were established using linear regression and the derivedeconometric equations were used to estimate future energy demand based on growthassumptions of the activity (independent) variables.

Figure 1 – Structure of the ASEAN Energy Outlook Model

Modeling Structure

MACRO Economic Assumptions

Industry

Primary Energy

GDP, Crude oil price, Exchange rate, Population, GDPDeflator, Index of Industrial Production, etc.

Transport Other

Final Consumption

Powergeneration

OilRefinery

Coal & otherTransformation

Microfit

LEAP

In cases where regression analysis is not applicable due to insufficiency of data or there isfailure to derive a statistically sound equation, other methods such as the energy intensityapproach are used.

The demand equations derived for each ASEAN member state appear as Annex 2.

3.2. Estimating Primary Energy Requirements

Having estimated the future final energy demand, the corresponding primary energyrequirements need to be estimated. These primary energy requirements are the inputs totransformation to produce secondary fuels. Energy transformation involves electricitygeneration, oil refining, city gas production, charcoal making and any other process thatconverts fuels from primary energy.

For this 2nd ASEAN Outlook, not only primary requirements for electricity generation wereconsidered like in the 1st ASEAN Outlook. The crude oil inputs to oil refining, biomassrequirements for charcoal production, natural gas inputs to LNG production and the own use ofthe energy sector were also included.

8

The Long-range Energy Alternatives Planning System (LEAP)4 is used to estimate primaryenergy consumption and produce the energy balance tables.

3.2.1. Electricity Generation

Electricity can be produced using various technologies and fuels. In ASEAN, the most commonsource of electricity is oil power plants which exist in all of the 10 member states. The nextmost common source is hydroelectric power plants followed by natural gas and coal powerplants. Geothermal power plants also exist in 3 member states and there is also an increasingcapacity of wind and solar photovoltaic power plants. Biomass-powered plants also exist inThailand

Electricity generation requires fuels to produce outputs and this section covers how these fuelsare calculated. The calculation of the primary energy requirements for electricity generationinvolves the following steps:

Estimating total electricity generation requirements

The total electricity generation requirement is greater than the final electricity demand tocover the electricity consumption in the power stations and the expected losses in thetransmission and distribution systems. The additional requirement among ASEAN memberstates is generally above 10 percent of the total final demand.

Estimating electricity generation capacity requirements

This involves two processes. First is estimating total capacity requirements which is thecapacity needed to meet the peak demand. The total capacity requirement is the peakdemand plus the assumed reserve margin which is a percentage of the peak demand.Reserve margin is the preferred amount of available capacity above the peak demand inorder for the electrical system to ensure that there is no or minimal disruption in the supply.

The second process is determining the power plants that should be added when the totalcapacity of the existing power plants cannot meet the peak demand. In five of the ASEANcountries, it is assumed that power plants for the base load should be coal-fired power plantsin view of its relatively low operating costs. For intermediate and peak loads, it is assumedthat these will be met by natural gas power plants. Myanmar is one of the exceptions inview of its government policy of developing the vast hydroelectric potential of the country.Viet Nam, Lao PDR and Cambodia are also developing a sizeable amount of their hydroresources. In Brunei Darussalam and Singapore, future electricity demand will be met bynatural gas power plants. Oil power plants are considered only in isolated areas that cannotbe connected economically to the electricity grids.

There is no strict criterion for determining the amount of coal and natural gas additions inview of the flexibility of the CCGT technology which could be used to supply theintermediate and peak requirements.

Estimating generation by each type of power plant

Generation by individual types of power plants is assumed to follow the order of ascendingoperating costs. That is, the power plant with cheapest operating cost are made to generateat maximum available capacity before the next cheapest power plant is made to produceelectricity. This order is followed until the generation requirement is met. In this case,

4 LEAP or the Long-range Energy Alternatives Planning System is an energy policy analysis and climatechange mitigation assessment software developed at the Stockholm Environment Institute. For moreinformation see: http://www.energycommunity.org/default.asp?action=47

9

hydroelectric, wind and geothermal power plants which have zero marginal costs areassumed to operate first before nuclear, coal, natural gas and oil power plants.

The operating cost is derived from the formula below:

i

iii Efficiency

CostFuelCostMOVariableCostOperating

__&__ ,

where i are the types of power plants

Estimating fuel inputs

Finally, the information of electricity generation together with conversion efficiencyvariables or the thermal efficiencies are used to calculate the input fuels required by powerplant for the amount of calculated output. This can be derived from the simple formulabelow:

i

ii Efficiency

GenerationyElectricitInputFuel

__

3.2.2. Oil Refining and other Transformation

In oil refining, the amount of crude oil and other inputs is calculated from capacity, capacityutilization, efficiency information and auxiliary fuels. Auxiliary fuels are the fuels needed forthe operation of the refinery. The estimation of primary energy requirements for othertransformation uses the same information as those in oil refining.

3.3. Projection Scenarios

Two scenarios were forecasted in the modeling work as follows:

The first scenario which was agreed upon by the members of the ASEAN technicalworking group is identified as the Reference scenario or the base case scenario. Thescenario used historical trends (1980 to 2000) of GDP, GVA, population, number ofvehicles in forecasting their future values. It is assumed that the future growth trends wouldfollow the historical development paths.

The other scenario is the High GDP Growth scenario, which will be known as Highscenario from this point onwards. In this scenario, the growth rates of GDP were takenfrom the official targets of each of the 10 ASEAN member states, which incidentally arehigher that the growth rates in the Reference scenario.

4. FORECAST ASSUMPTIONS

4.1. GDP Growth

The GDP growth assumptions for the Reference scenario were derived by IEEJ and weresuggested to the working group during the second working meeting in January 2008 in Bangkok.Table 2 shows these GDP Growth assumptions. These growth rates are basically derived fromlong-term trends obtained from historical data.

10

As mentioned above, the assumptions for the High GDP growth scenario were collected by theworking group members from their respective countries and are these shown in Table 3. Most ofthese growth rates are economic growth targets of ASEAN member states.

Table 2 – AverageAnnual GDP Growth Assumptions, Reference Scenario, inPercent

2005-2010 2010-2020 2020-2030 2005-2030Brunei Darussalam 4.2 3.8 3.5 3.8Cambodia 7.5 5.3 4.3 5.3Indonesia 6.0 4.5 4.0 4.6Lao PDR 7.5 5.3 4.3 5.3Malaysia 5.4 4.4 4.2 4.5Myanmar 7.5 5.3 4.3 5.3Philippines 5.5 4.7 4.0 4.6Singapore 4.7 3.7 3.9 4.0Thailand 4.8 4.8 4.6 4.7Vietnam 7.0 6.5 6.0 6.4ASEAN 5.5 5.1 4.5 4.9

Source: EDMC/IEEJ.

Table 3 –AverageAnnual GDP Growth Assumptions, High Scenario, in Percent

2005-2010 2010-2020 2020-2030 2005-2030Brunei Darussalam 5.2 4.8 4.5 4.8Cambodia 10.4 7.0 6.7 7.6Indonesia 6.5 6.5 6.5 6.5Lao PDR 7.2 7.5 7.4 7.4Malaysia 5.5 6.0 5.0 5.5Myanmar 7.1 13.1 9.8 10.6Philippines 5.8 6.3 6.0 6.1Singapore 5.5 5.0 4.8 5.0Thailand 6.2 5.8 5.3 5.7Vietnam 9.9 9.6 9.8 9.8ASEAN 6.2 6.4 6.1 6.2

Sources: EDMC/IEEJ, National Project Teams

4.2. Population Growth Rates

Population growth assumptions are obtained from the United Nations Department of Economicand social Affairs, Population Division Homepage5. From Table 4 below, there is a wide rangeof growth projections from 0.4 percent per annum in Thailand to 2.4 percent per annum inBrunei Darussalam.

5 http://esa.un.org/unpp

11

Table 4 – AverageAnnual Population Growth Assumptions, in Percent

2005-2010 2010-2020 2020-2030 2005-2030Brunei Darussalam 2.1 1.7 1.3 1.6Cambodia 1.1 1.0 0.8 0.9Indonesia 1.2 0.9 0.6 0.9Lao PDR 1.1 1.0 0.8 0.9Malaysia 1.7 1.4 1.0 1.3Myanmar 1.1 1.0 0.8 0.9Philippines 1.9 1.6 1.2 1.5Singapore 1.9 1.6 1.2 1.5Thailand 0.6 0.4 0.2 0.4Vietnam 1.3 1.1 0.8 1.1ASEAN 1.2 1.0 0.7 0.7

Source: UN Department of Economic and Social Affairs, Population Division

4.3. Crude Oil Price Assumptions

Nominal crude oil price, which is based on Japan CIF (includes cost of insurance and freight) isprojected to increase gradually from 53.8 US$/barrel in 2005 to 112.6 US$/barrel in 2030.

From these assumptions, the nominal domestic prices are calculated using exchange rates.These prices are converted to constant prices using GDP Deflators.

Figure 2 – Nominal Oil Price Assumption

0

20

40

60

80

100

120

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

$/b

arre

l(n

om

ina

l)

Source: EDMC/IEEJ.

12

5. ENERGY DEMAND AND CO2 EMISSION OUTLOOK

5.1. Final Energy Consumption

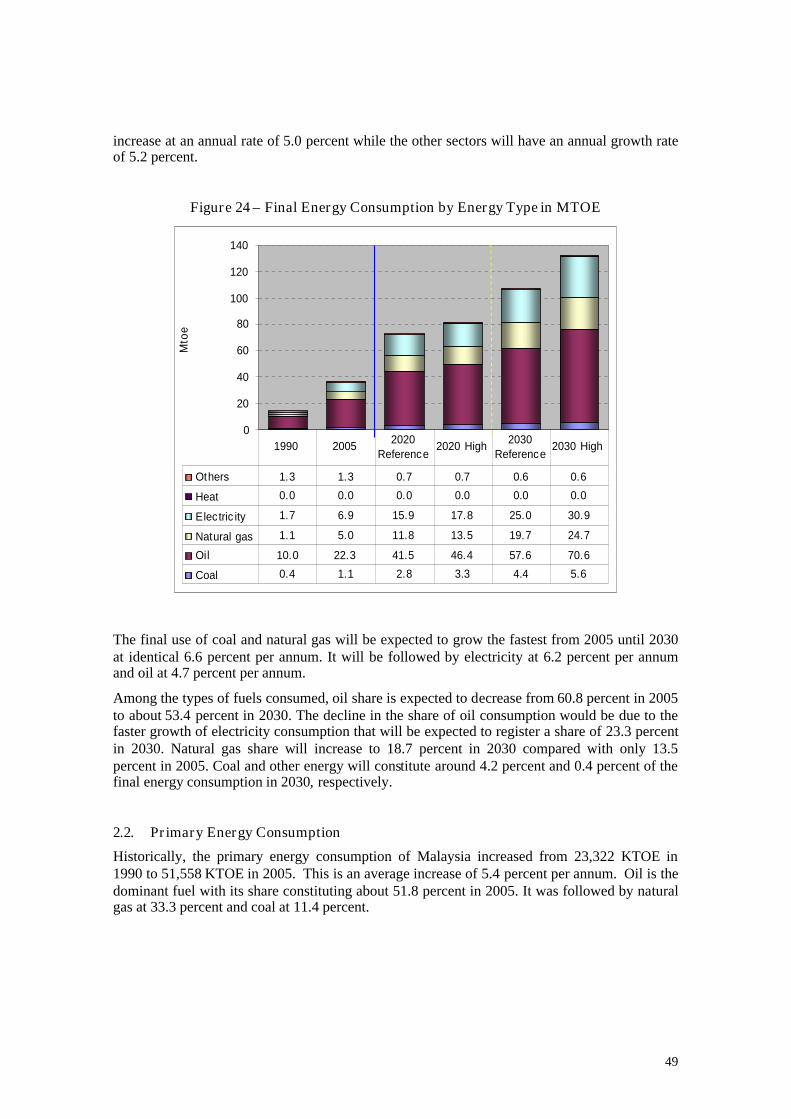

The total ASEAN final energy consumption increased to 343 MTOE in 2005 growing at anaverage annual growth rate of 4.2 percent over the 1990 to 2005 period. On a sectoral basis, thetransport sector contributed around 19.5 percent of the total ASEAN demand in 1990 while theindustry and the other sectors contributed 22.4 percent and 53.8 percent respectively. From thento 2005, the transport and industrial demand had been growing rapidly almost at the same rate.Industry grew at a slightly faster average annual growth rate of 6.4 percent per year while thetransport demand growth was 6.2 percent per year. The rapid growth of these sectors resulted inan increase of their shares in the total ASEAN demand to 25.8 percent and 30.4 percentrespectively in 2005. The consumption of the other sectors, which comprise of commercial,residential and agricultural sub-sectors, grew the slowest at 2.3 percent per annum, reducing itsshare in the total demand to 40.6 percent from 53.8 percent in 1990.

Figure 3 – Projected Final Energy Consumption in ASEAN by Sector

0

200

400

600

800

1,000

1,200

Mto

e

Others 107 150 209 220 274 317

Trans po rt 36 88 191 218 305 394

Indus try 41 104 208 231 322 412

1990 20052020

Reference2020 High

2030Reference

2030 High

Non-energy use accounted only around 4.3 percent of the total ASEAN final energyconsumption in 1990 and its share decreased to 3.3 percent in 2005. The average annual growthof energy consumption as feedstock was 2.4 percent over the 1990 to 2005 period.

5.1.1. Reference Scenario

For the future, under the Reference scenario, the total final energy consumption of the ASEANis projected to grow at a slower annual rate of 3.9 percent from 2005 to 2030. The transportsector consumption will grow the fastest during the period with annual growth projected at 5.1percent driven by the increasing per capita income. The industrial sector consumption will

13

grow at 4.6 percent and other sectors which include residential, commercial and agriculturalsectors will have an average annual growth of 2.4 percent. Non-energy consumption will growat an average rate of 2.9 percent per annum.

Figure 4 – Final Energy Consumption in ASEAN by Fuel Type

0

200

400

600

800

1,000

1,200

Mto

e

Others 89 109 114 114 113 112

Heat 0 0 0 0 0 0

Electrici ty 11 38 94 108 164 214

Natural gas 8 21 46 50 70 87

Oil 71 152 292 328 454 573

Coal 4 24 60 69 100 136

1990 20052020

Re ference2020 High

2030Reference

2030 High

Among the types of energy, electricity will grow the fastest, at 6.1 percent per annum in view ofthe projected growth in industrial GDP. This result corresponds to the result in the first ASEANoutlook published in 2005. Electricity share to the total will consequently increase from 11.0percent in 2005 to 18.2 percent by 2030. Coal will have the second highest growth rate of 5.9percent per annum. Its share will increase from 6.9 percent in 2005 to 11.1 percent in 2030.Natural gas consumption will be growing at a slower average rate of 5.0 percent per annum overthe 2005 to 2030 period.

Oil will remain as the most used fuel and is projected to grow at 4.5 percent per annum over theforecast period. Its share to the total consumption mix will also increase from 44.4 percent in2005 to 50.4 percent in 2030. This is driven by the rapid growth in consumption of thetransport sector, which is largely fuelled by oil products.

Consumption of other fuels, which are mostly biomass, will increase at an average annual rateof 0.2 percent resulting to a decreased share to the total consumption from 31.7 percent in 2005to 12.5 percent in 2030.

5.1.2. High Scenario

In the High scenario, final energy consumption will grow at a faster annual rate of 4.9 percentdriven by the transportation sector consumption, which will grow by 6.2 percent per annum.Those of the industrial and other sectors will have annual growth rates of 5.7 percent and 3.0percent, respectively.

14

As in the Reference scenario, oil share will increase reaching 51.1 percent in 2030. This is dueto faster growth rate of the transport sector demand compared to the Reference scenario.

Final consumption of electricity will however post the highest growth rate at 7.2 percent. Itsshare will subsequently increase from 11.0 percent in 2005 to 19.1 percent in 2030. Likewise,coal share will increase from 6.9 percent in 2005 to 12.1 percent brought about by the growth inconsumption of 7.2 percent annually.

Consumption of biomass which is largely used in the residential sector in rural areas is projectedto grow at a very slow rate of 0.1 percent per annum. Consequently, its share to the total finalenergy consumption will decline from 31.7 percent in 2005 to 10.0 percent in 2030. This wouldbe made possible by fuel switching to more convenient fuels such as LPG for cooking as percapita income increases.

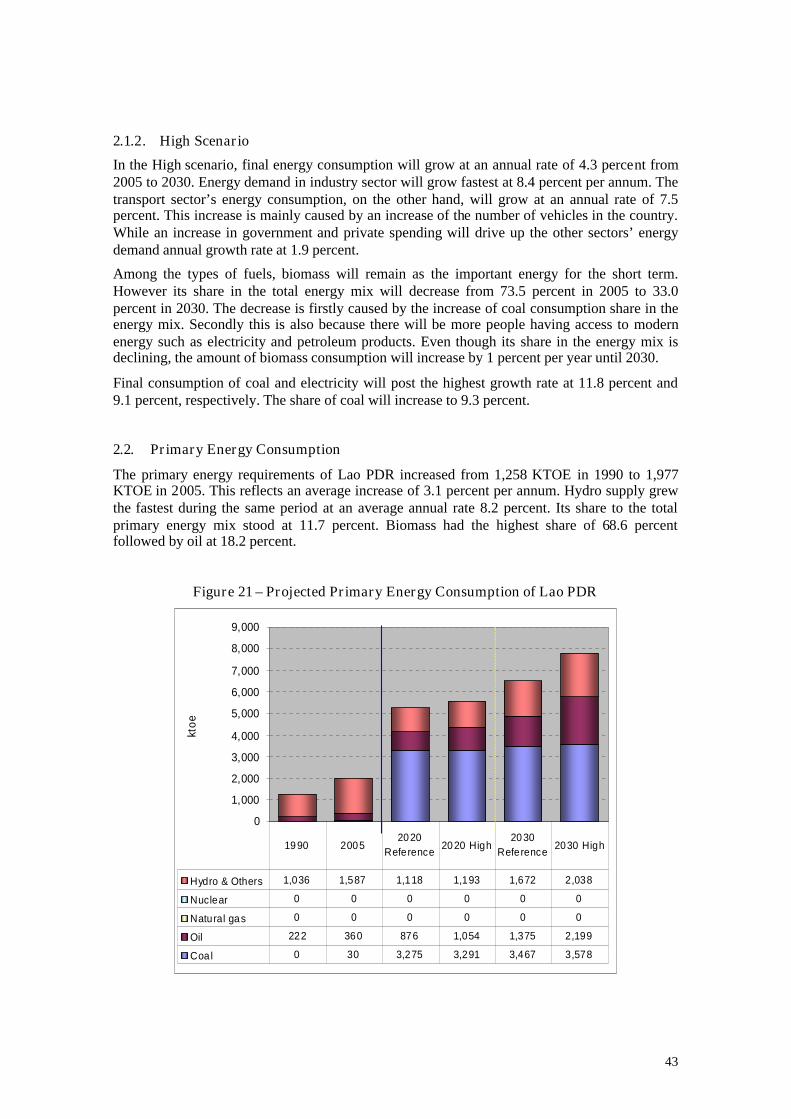

5.2. Primary Energy Supply

Historically, the total primary energy supply in the ASEAN increased from 251 MTOE in 1990to 474 MTOE in 2005. This is an average increase of 4.3 percent per annum. Indonesia has thelargest share, amounting to 41 percent of the total primary energy requirement in 1990 butdecreasing to 38 percent in 2005. This decreased share of Indonesia’s primary energy supply isdue to the rapid increase of the requirement of Singapore and Thailand that grew at similaraverage annual rates of 5.6 percent and Malaysia at 5.4 percent.

Coal supply grew the fastest during the same period at 10.6 percent per annum due to the rapidgrowth in the consumption of the industrial sector and the construction of coal-fired powerplants. Gas supply grew at a slower rate of 7.0 percent per annum which is largely due to thecoming-on-stream of natural gas power plants in Malaysia, the Philippines, Singapore andThailand

5.2.1. Reference Scenario

The primary energy requirements in the ASEAN will grow at an annual rate of 4.0 percent from474 MTOE in 2005 to 1252 MTOE in 2030. Among the energy sources, coal will have thehighest annual growth rate of 6.9 percent per annum due to the increasing demand for fuel forelectricity generation and the industrial sector. From 56 MTOE in 2005, primary coal supplywill increase to 297 MTOE in 2030.

Oil supply, in view of the fast growth rate of the transport sector will grow by 4.0 percentannually. Gas will have a similar annual growth rate of 4.0 percent. Gas for power generationwill comprise 67 percent of the total gas requirements in 2030. Its share to the total primaryenergy mix will remain at 19.2 percent in 2030.

Hydropower share in the total primary energy supply in ASEAN is small, only 1.0 percent in2005. The growth of hydropower however, will be significant at 5.4 percent per annum over the2005 to 2030 period. This is due to the plan for aggressive development of hydroelectricpotential in the Great Mekong Sub-region. Among the states in this sub-region, Cambodia willhave the fastest growth of hydropower supply at almost 12.6 percent per annum followed byLao PDR at 11.0 percent per annum. Hydropower development in Lao PDR is due largely to theplanned increase in electricity exports mainly to Thailand. For Myanmar, electricity is mainlyhydropower based (almost 100%). The hydropower supply in Myanmar will experience fastgrowth at an average rate of 9.2 percent per annum as the state also plans to export excesselectricity generation in the future. Vietnam electricity generation from hydropower will grow atan average annual rate of 5.8 percent and will account for at least 25 percent of the country’s

15

total power generation in 2030. From outside of the sub-region, Malaysia, with its Bakunhydropower development will increase its hydropower supply at an average growth of 4.7percent per annum.

Philippines and Indonesia are the two countries in ASEAN having geothermal resources forpower generation. The share of geothermal energy to total requirement in the region is 3 percent.This is projected to grow at an average growth of 3.9 percent per annum from 2005 to 2030. Itsshare to the total will however remain at the same level as in 2005.

Indonesia, the Philippines and Vietnam plan to construct nuclear power plants to meet demandfor electricity from 2020 onwards. As a result, nuclear energy could take a 1.6 percent share ofthe total ASEAN primary energy supply in 2030.

Other energy will have a slower growth rate of 0.2 percent per annum. This covers mostlybiomass that is used by the final sector, supply of other renewables such as bio-fuels, wind,solar, etc.

Figure 5 – Primary Energy Requirements in ASEAN

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Mto

e

Others 101 114 123 122 120 117

Geothermal 6 14 37 37 37 37

Hydro 3 5 17 18 18 22

Nuclear 0 0 7 7 20 19

Natural gas 33 91 149 169 240 307

Oil 97 194 348 383 520 639

Coal 12 56 162 189 297 405

1990 20052020

Reference2020 High

2030Re ference

2030 High

5.2.2. High Scenario

In the High scenario, total energy requirement will reach 1,548 in 2030, 23.6 percent higherthan in the Reference scenario. Coal supply will exhibit the fastest growth at 8.3 percent perannum in view of the more rapid increase in the requirements for electricity generation in thisscenario. Natural gas will grow at 5.0 percent per annum almost similar to the growth of the oilrequirements (4.9 percent per annum).

Hydropower will grow at 6.2 percent per annum. Its share to total primary energy requirementwill increase to 1.5 percent, similar to that of the Reference scenario. Other fuels will be

16

growing at a slightly lower rate of 0.1 percent as compared to its growth rate in the Referencescenario as higher per capita GDP in this scenario is expected to result to lower consumption ofbiomass in the households.

5.3. Power Generation

Electricity production increased from 155 TWh in 1990 to 509 TWh in 2005. This is equivalentto an average annual growth rate of 8.3 percent over the same period. In the future, electricityproduction is projected to increase to 2,234 TWh in the Reference scenario and 2,923 TWh inthe High scenario or at average annual growth rates of 6.1 percent and 7.2 percent, respectively.

Both gas and coal will continue to form the bulk of the supply for power generation in theReference and High scenarios. Coal share will reach 40.8 percent in the Reference scenario and42.8 percent in the High scenario by 2030. Natural gas share will be 41.5 percent in theReference scenario and 42.1 percent in the High scenario.

Table 5 - Electricity Production in ASEAN (Reference and High Scenarios), in TWh

By TYPE 1990 20052030

(Reference)2030

(High)Thermal 119 431 1,888 2,530Nuclear 0 0 75 74Hydro 29 58 213 262Geothermal 7 17 43 43Other 0 3 15 15Total 155 509 2,234 2,923

Oil share will decrease significantly from 14.4 percent in 2005 to 2.1 percent by 2030 in theReference scenario and 1.6 percent in the High scenario. This indicates that the role of oil inpower generation will become minimal due to the diversification program for alternative fuelsin most of the ASEAN member states. In addition, the renewable portfolio standardimplemented in some ASEAN states recently has also reduced the role of oil in powergeneration.

Hydropower will grow at an average annual growth rate of 5.4 percent in the Reference scenarioand 6.2 percent in the High scenario. Geothermal will also grow but at a slower pace of 3.9percent due mainly to resource constraint.

In regards to fuel inputs for power generation, oil formed the bulk of supply in 1990 at 55.6percent. In 2005, natural gas became the main fuel input for power generation in the region at50.6 percent. Oil was reduced to 16.9 percent of the total while coal increased from 23.6 percentin 1990 to 32.5 percent in 2005.

Coal and natural gas are expected to continue to dominate the future fuel mix for powergeneration. In the Reference scenario, coal share will increase to 53.7 percent while gas sharewill be 43.5 percent in 2030. In the High scenario, coal share will be 55.1 percent while that ofgas will be 42.8 percent.

In view of the increasing utilization of coal and natural gas which could be used in new andmore efficient technologies for power generation, thermal efficiency of the region is expected toincrease from 38 percent in 2005 to 44 percent in 2030 for both the Reference and Highscenarios.

17

Table 6 - Fuel Inputs to Power Generation in ASEAN, in MTOE

1990 20052030

(Reference)2030

(High)Coal 7 32 197 270Oil 17 17 10 10Gas 6 50 160 209ThermalEfficiency 33% 38 % 44 % 44 %

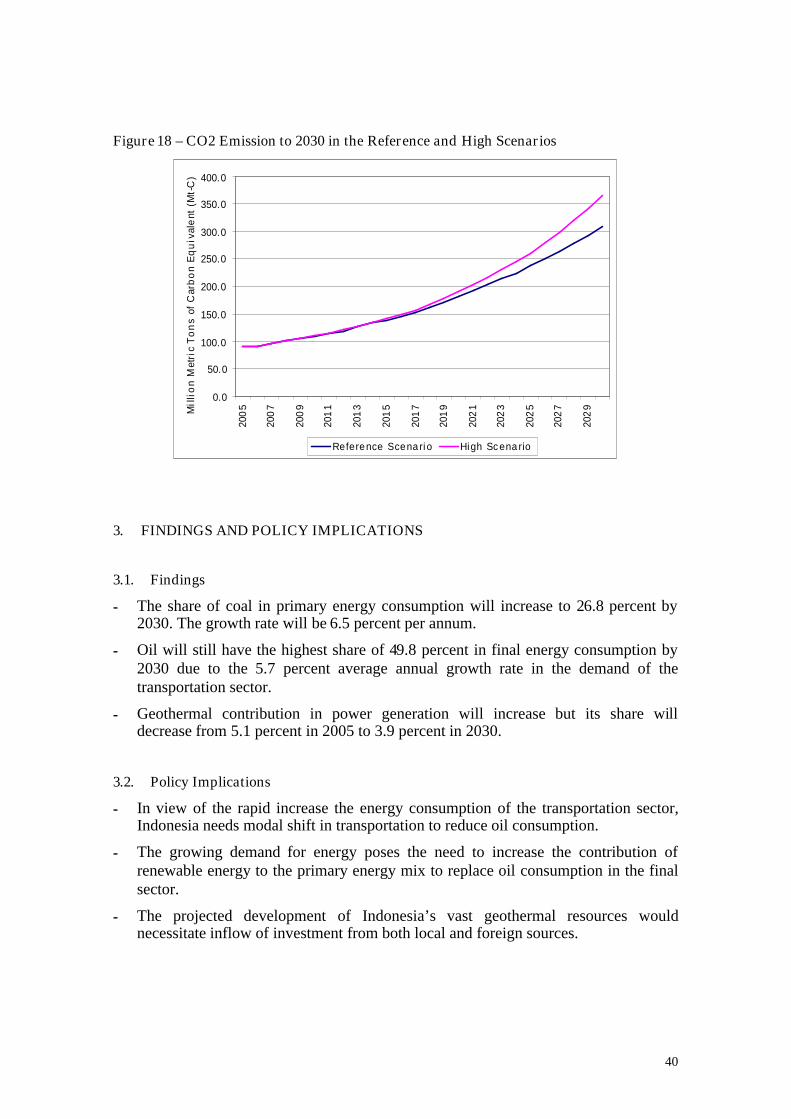

5.4. CO2 Emission Outlook

The 4.0 percent annual growth in primary energy consumption in the Reference scenario willresult to a corresponding 5.1 percent growth in CO2 emission. This is due largely to theprojected 6.9 percent annual escalation of coal consumption which is the most carbon-intensivefossil fuel. The similar 4.0 percent annual growth rates in oil and natural gas consumption willalso contribute to this increasing emission.

Figure 6 – CO2 Emission in the Reference and High Scenarios, in Mt-C

0

200

400

600

800

1,000

1,200

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029M

illi

on

Met

ric

Ton

so

fCar

bo

nE

quiv

alen

t(M

t-C)

High Scena rio Reference Scena rio

In the High scenario, CO2 emission will have a faster annual growth rate of 6.2 percent. This isdue to the projected 8.3 percent annual growth in coal consumption and the 5.0 percent and 4.9percent annual growth of natural gas and oil consumption, respectively.

18

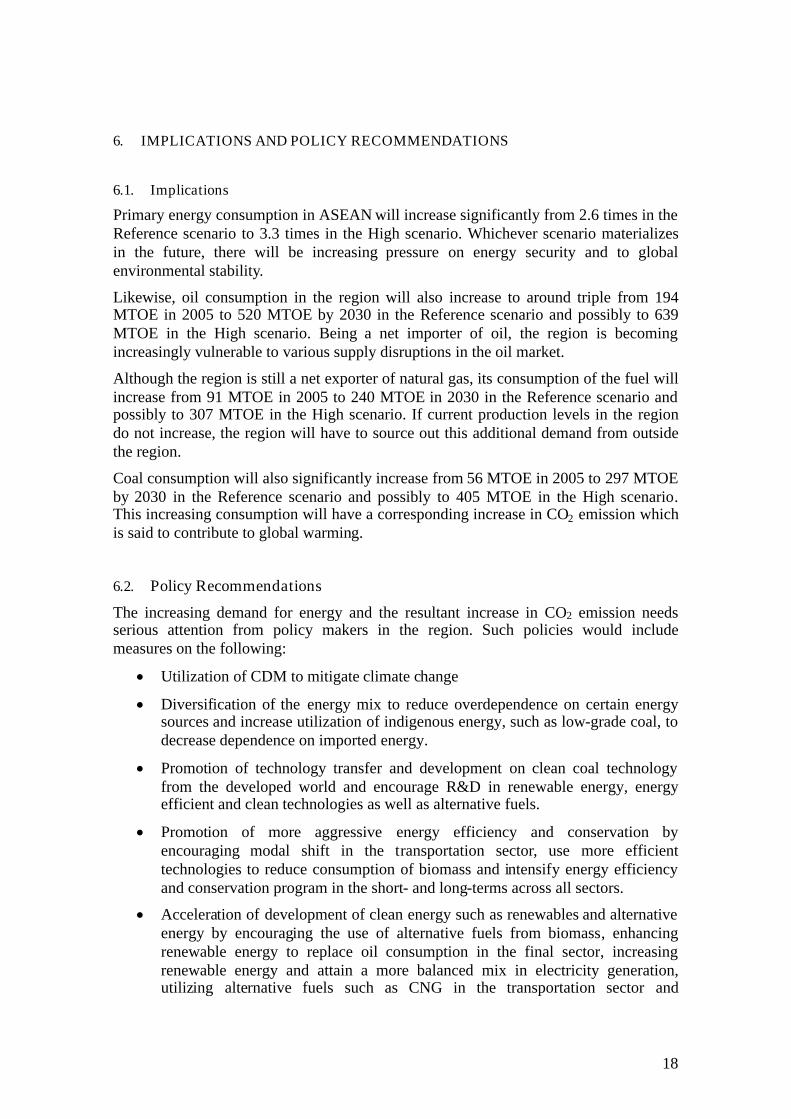

6. IMPLICATIONS AND POLICY RECOMMENDATIONS

6.1. Implications

Primary energy consumption in ASEAN will increase significantly from 2.6 times in theReference scenario to 3.3 times in the High scenario. Whichever scenario materializesin the future, there will be increasing pressure on energy security and to globalenvironmental stability.

Likewise, oil consumption in the region will also increase to around triple from 194MTOE in 2005 to 520 MTOE by 2030 in the Reference scenario and possibly to 639MTOE in the High scenario. Being a net importer of oil, the region is becomingincreasingly vulnerable to various supply disruptions in the oil market.

Although the region is still a net exporter of natural gas, its consumption of the fuel willincrease from 91 MTOE in 2005 to 240 MTOE in 2030 in the Reference scenario andpossibly to 307 MTOE in the High scenario. If current production levels in the regiondo not increase, the region will have to source out this additional demand from outsidethe region.

Coal consumption will also significantly increase from 56 MTOE in 2005 to 297 MTOEby 2030 in the Reference scenario and possibly to 405 MTOE in the High scenario.This increasing consumption will have a corresponding increase in CO2 emission whichis said to contribute to global warming.

6.2. Policy Recommendations

The increasing demand for energy and the resultant increase in CO2 emission needsserious attention from policy makers in the region. Such policies would includemeasures on the following:

Utilization of CDM to mitigate climate change

Diversification of the energy mix to reduce overdependence on certain energysources and increase utilization of indigenous energy, such as low-grade coal, todecrease dependence on imported energy.

Promotion of technology transfer and development on clean coal technologyfrom the developed world and encourage R&D in renewable energy, energyefficient and clean technologies as well as alternative fuels.

Promotion of more aggressive energy efficiency and conservation byencouraging modal shift in the transportation sector, use more efficienttechnologies to reduce consumption of biomass and intensify energy efficiencyand conservation program in the short- and long-terms across all sectors.

Acceleration of development of clean energy such as renewables and alternativeenergy by encouraging the use of alternative fuels from biomass, enhancingrenewable energy to replace oil consumption in the final sector, increasingrenewable energy and attain a more balanced mix in electricity generation,utilizing alternative fuels such as CNG in the transportation sector and

19

formulating policies to promote the utilization of renewables, alternative fuelsand nuclear energy.

Creating an energy investment climate that is conducive to investors byformulating appropriate policies and incentives to encourage investment todevelop geothermal, hydropower and hydrocarbon resource potential as well asnuclear energy.

Strengthening regional cooperation especially in sharing best practices in energydevelopment and utilization

The foregoing implications are big hurdles but they also offer a lot of opportunities suchas: technological advancement to improve energy efficiency in the demand and supplysides, technology transfer from the developed to less developed countries, possibleimprovement of investment regimes in each ASEAN member states and increased flowof foreign investments for energy resource development and electricity generation.

Likewise, as these implications are common to all member states, collaborative actionsto address these issues would deepen the ties among the member states.

20

21

ANNEX 1: Country Reports

22

23

BRUNEI DARUSSALAM

1. BACKGROUND

Brunei Darussalam is situated on the northwest end of the Island of Borneo in South East Asia,covering a total land area of 5,765 square kilometers. The population of Brunei Darussalam in2005 stood at 370,100 registering an increase of 2.9 percent from 2004.

Brunei Darussalam has one of the highest per capita incomes among the countries in the Asia-Pacific region owing mainly to its significant natural gas and oil resources. The economicactivity in the country is dominated by oil and gas sector production. The share of these tworesources alone accounted for 66 percent of GDP in 2005. Brunei Darussalam’s economicgrowth rate was 3 percent in 2005 compared with 1.7 percent in 2004. The rate of inflation asmeasured by the consumer price index (CPI) rose by 1.1 percent in 2005 compared with 0.9percent in 2004. The higher rate in 2005 was mainly a reflection of the increase in transportationcost.

2. ENERGY DEMAND AND CO2 EMISSION OUTLOOK

2.1. Final Energy Consumption

In 2005, Brunei Darussalam’s total final energy consumption (TFEC) was 719 KTOE. Thetransport sector was the largest consumer accounting for 56.2 percent (404 KTOE) of TFEC.This is followed by the residential/commercial with 32.8 percent (236 KTOE). BruneiDarussalam’s industry sector accounted for 11.0 percent (79 KTOE) of TFEC.

Taking into account the socio-economic assumptions which were previously set accordingly, wehave simulated the two scenarios i.e. reference case and high growth case using the LEAPmodel. As such the following shows the summarized results based on the assumptions.

2.1.1. Reference Scenario

In the reference scenario, Brunei Darussalam’s total final energy consumption is projected togrow at an average annual growth rate of 3.8 percent from 2005 to 2030. This escalation isexpected to be contributed mainly by Brunei Darussalam’s transport sector as well as the othersectors, which comprise of the combined sectors of residential/commercial and agriculture. Bothof these sectors are projected to increase at an average annual growth rate of 3.9 percent untilthe end of the planning period. These are driven by the increasing economic growth in view ofthe nation’s aspiration to further its development.

The industrial sector final energy consumption shall reflect a 2.3 percent annual growth rateduring the projected period. This reflects the anticipated development of Brunei Darussalam’spetrochemical industries in particular, in the future. This is an effort of the Government ofBrunei Darussalam to make full use of its oil and gas resources and further expand its economy.

Among the types of energy, it is expected that oil and electricity will remain as the two mainenergy types during the projection period.

24

Figure 7 – Final Energy Consumption by Sector to 2030

0

500

1,000

1,500

2,000

2,500kt

oe

Others 101 236 425 491 620 787

Transport 226 404 714 830 1,044 1,351

Indus try 60 79 105 119 141 179

1990 20052020

Reference2020 High

2030Reference

2030 High

Figure 8 – Final Energy Consumption by Fuel Type to 2030

0

500

1,000

1,500

2,000

2,500

ktoe

Others 0 0 0 0 0 0

Heat 0 0 0 0 0 0

Electricity 87 234 428 500 633 820

Natural gas 0 0 0 0 0 0

Oil 300 485 816 940 1,172 1,497

Coa l 0 0 0 0 0 0

1990 20052020

Reference2020 High

2030Reference

2030 High

Oil will account for approximately 65 percent of the future energy source for TFEC, thusmaintaining the largest share for fuel usage. It is projected that the average annual growth rate

25

will be around 3.6 percent. Electricity however, will account for the remaining 35 percent oftotal energy source. Although it reflects the smaller share, it is foreseen to have the fastergrowth rate of 4.1 percent. All this growth is a result of the process of urbanization and also inview of emerging commercial and industrial activities in the future.

2.1.2. High GDP Growth Scenario

In the High GDP Growth scenario (High scenario from this point onwards), the total finalenergy consumption is expected to grow at a faster annual rate of 4.8 percent as compared to theReference scenario. This is expected to be driven mainly by the transport sector as well as theresidential/commercial and agriculture sector which will grow at identical average annualgrowth rates of 4.9 percent. The industrial sector energy consumption is expected to grow at anannual rate of 3.3 percent.

Among the types of fuels, oil is expected to remain as the most used fuel and is projected togrow at an annual average rate of 4.6 percent. Its share of the TFEC will however decreasefrom 67.5 percent in 2005 to 64.6 percent in 2030. This is because electricity’s share of theenergy mix will increase from 32.5 percent in 2005 to 35.4 percent in 2030, which will begrowing at a much faster annual growth rate of 5.1 percent.

2.2. Primary Energy Consumption

In 2005, Brunei Darussalam’s primary energy requirements were around 2,435 KTOE, with oiland gas as its only energy sources. Natural gas accounted for the highest percentage share of thetotal final energy requirement with 75.6 percent with the remaining having been supplied by oil.

In general, Brunei Darussalam uses around 20 percent of its gas production for its domestic usewhilst the remaining 80 percent is exported as liquefied natural gas. Whereas oil produced aremostly exported. Only a small percentage (around 6 percent of the daily production) is refinedin Brunei Darussalam. The petroleum products are mostly used in its transport sector, whereautomobiles (cars) are the main mode of transportation.

2.2.1. Reference Scenario

From 2005 to 2030, oil and natural gas are projected to remain as Brunei Darussalam’s primaryenergy sources. Primary energy requirement will increase to 4,165 KTOE in 2030 at an averagegrowth rate of 2.2 percent per annum between 2005 and 2030.

Oil is projected to grow faster with an annual growth rate of 4.0 percent per annum driven bythe transport sector. Oil share in the total energy requirements will also increase from 24.4percent in 2005 to 38.2 percent in 2030.

Natural gas will remain as the main source for primary energy requirement increasing from1,840 KTOE in 2005 and 2,575 KTOE in 2030 despite of its reducing share in the total primaryenergy requirements. Natural gas held 75.6 percent of the total primary energy requirementshare in 2005 and projected to contribute a lower 61.8 percent of the total mix in 2030.

2.2.2. High Scenario

Increase in the GDP growth will cause the total primary energy requirement to grow more thandouble in 2030 from 2,435 KTOE in 2005 with an annual average growth of 3.1 percent. Oilwill grow at a more rapid rate throughout the projection period with an average growth of 5.2

26

percent per year from 2005 to 2030. Similar to the Reference scenario, natural gas share in thetotal primary energy requirement mix is projected to decline from 75.6 percent in 2005 to 59.6percent in 2030, as a result of a lower 2.1% annual growth rate.

Figure 9 - Primary Energy Consumption by Energy Type

0

1,000

2,000

3,000

4,000

5,000

6,000

ktoe

Others 0 0 0 0 0 0

Hydro 0 0 0 0 0 0

Nuclear 0 0 0 0 0 0

Natural gas 1,676 1,840 2,208 2,442 2,575 3,089

Oil 122 595 1,050 1,238 1,590 2,093

Coa l 0 0 0 0 0 0

1990 20052020

Reference2020 High

2030Reference

2030 High

2.3. Power Generation

Electricity production was at 2,907 GWh in 2005 and is projected to increase to about 7,867GWh in the Reference scenario and 10,185 GWh in the High scenario.

Table 7 – Projected Electricity Production to 2030, in GWh

By Type 2005 2030 (Reference) 2030 (High)

Natural Gas 2,890 7,845 10,156

Oil 17 22 29

Total 2,907 7,867 10,185

Power generation in Brunei Darussalam is almost solely being sourced from natural gas as fueland is projected to remain as the only major fuel input to power generation in Brunei until 2030.

In view of the installation of more efficient technologies for electricity generation, thermalefficiency of Brunei is expected to increase from 25.5 percent in 2005 to 40 percent in 2030 forboth the Reference and High scenarios.

27

Table 8 – Fuel Inputs for Power Generation to 2030, in KTOE

By Type 2005 2030 (Reference) 2030 (High)

Natural Gas 976 1,686 2,183

Oil 4 5 7

Total 980 1,691 2,190

2.4. CO2 Emissions

In 2005 Brunei Darussalam’s CO2 emissions reached 1,392 thousand tons of Carbon equivalent(kt-C), 30.6 percent of which were derived from oil-based fuels while the remaining 69.4percent were from natural gas. Based on the estimated demand growth for these fuels, CO2

emissions will increase at an average annual rate of 2.5 percent. This growth rate is higher thanthe growth of primary energy consumption of 2.2 percent. The reason for this disparity ingrowth is the faster growth of oil consumption which has higher carbon content than natural gas.

In the High scenario, CO2 emission will increase at a faster rate of 3.4 percent faster than thegrowth rate of primary energy consumption of 3.1 percent. Again, this is attributed to the fastergrowth rate of oil consumption.

Figure 10 - CO2 Emissions in the Reference and High Growth Scenarios

0

500

1000

1500

2000

2500

3000

3500

200

5

200

7

200

9

201

1

201

3

201

5

201

7

201

9

202

1

202

3

202

5

202

7

202

9

Th

ous

and

Met

ric

To

ns

ofC

arb

on

Eq

uiv

ale

nt(k

t-C

)

High Scena rio Reference Scenario

28

3. FINDINGS AND POLICY IMPLICATIONS

The total final energy consumption in Brunei Darussalam is expected to grow at a faster rate of3.8 percent compared to its final energy requirement that will grow at 2.2 percent from 2005 to2030 in the reference scenario. Natural gas will remain as the main source of fuel for finalenergy requirement throughout the projection period, whereas for final energy consumption oilwill continue to be the main source of energy. The purely oil-based transport sector is thecurrent largest consumer in Brunei Darussalam and this is projected to grow at an annual rate of3.9 percent. Electricity generation will grow at 4.1 percent per annum with natural gas as its solesource of fuel.

Thus with the projected increase in final energy consumption, there is an urgency for BruneiDarussalam to reduce its final energy consumption. Various efforts have already been put inmotion such as adopting energy efficiency and conservation (EEC) techniques and technologieswithin the nation. Having only oil and natural gas for its main sources for energy, it is alsoimperative for Brunei Darussalam to diversify its energy sources to alternative and renewableenergy resources not only for final energy requirement, but also for its electricity generation.Diversification of its energy mix would result in a less dependent energy sector on the currentfossil fuels and an enhanced energy security for the country. As Brunei Darussalam is highlydependent on oil-based automobile for transportation, a shift in mode of transportation to a lessenergy intensive mode would help reduce the nation’s consumption in the transport sector.

29

CAMBODIA

1. BACKGROUND

The Kingdom of Cambodia is located in the tropical region of Southeast Asia’s Lower Mekongregion. It has 800 km border with Thailand in the west, 450 km with Lao PDR in the north,1,250 km with Viet Nam in the east and a coastline of 440 km long in the south. The physicallandscape is dominated by the lowland plains around the Mekong River and the Tonle Sap Lake.Of the country’s total land area 181,035 km2, approximately 49 percent remains covered byforest. There are about 2.5 million hectares of arable land and over 0.5 million hectares ofpasture land.

The GDP recorded a growth rate of 8.4 percent in 2000, and in 2004 and 2005, growth rateswere recorded at 10.0 percent and 13.4 percent, respectively. Investments are financedpredominantly from foreign sources, which accounts for 21.6 % of GDP. More than half ofthem are made up by grants, with the remaining parts consisting of Foreign Direct Investmentand soft loans. Public investment grew by 5.2 %, with national budget and funding from theWorld Bank, Asian Development Bank (ADB), and assistance from other countries focusing onpriority areas including agriculture, rural development, education, health care, and physicalinfrastructure. The Royal Government of Cambodia (RGC) considers the private sector, bothdomestic and foreign, as the major sources of investment, and thus an engine for growth.Consequently the RGC has doubled efforts to create favourable conditions and a climate ofconfidence for investors. The population of Cambodia in the year 2005 was 14.07 million, whileGDP per capita was around US$451/person at constant 2000 US$ values.

Cambodia has substantial hydropower resources and indications of oil, gas and coal deposits;there is an urgent need to assess the extent of these energy resources. Other renewable energysources are available and their use is being started, such as biomass, solar and mini-hydro. Theproblem is to diversify the sources of supply, and intensify the exploration for natural gas andthe development of renewable energy resources.

2. ENERGY AND CO2 EMISSION OUTLOOK

2.1. Final Energy Consumption

The total final energy consumption of Cambodia increased from 3,278 KTOE in 1995 to 4,530KTOE in 2005, growing at an average annual rate of 3.3 percent. The other sectors, whichconsist of residential, commercial and agricultural sectors, consumed the largest portion ofenergy with a share 89.4 percent in 2005. The transportation sector was the next largestconsumer with 9.5 percent of the total with the industrial sector taking the remaining 1.1 percent.

2.1.1. Reference Scenario

Using the basic assumptions as mentioned in the previous section, final energy consumption inCambodia is projected to grow at an annual growth rate of 2.6 percent from 2005 to 2030. Forthe simulation period, the industrial sector final energy consumption is expected to increase atan average annual growth rate of 6.3 percent while the transport sector energy consumption isprojected to increase at an average annual growth rate of 5.0 percent. The combined

30

commercial and residential sectors final energy consumption is expected to increase at anaverage annual growth rate of 2.1 percent until the end of the planning period, 2030.

Figure 11: Sectoral Final Energy Consumption (Reference and High Scenarios)

0

2,000

4,000

6,000

8,000

10,000

12,000

ktoe

Others 2,991 4,050 5,511 5,990 6,862 7,954

Transport 284 429 883 1,255 1,436 2,333

Indus try 3 51 133 204 236 415

1990 20052020

Reference2020 High

2030Reference

2030 High

Electricity consumption will grow at an annual growth rate of 6.1 percent in the period 2005-2030. Its share to total energy consumption is expected to increase from 1.4 percent in 2005 to3.3 percent by 2030. Final consumption of oil will increase at an average rate of 4.8 percentannually and will form 35.1 percent of the total consumption by 2030 increasing from 20.5percent in 2005. Meanwhile, biomass consumption will grow at a relatively low rate of 1.6percent per annum over the simulation period. However, its share, although decreasing, will stillbe substantial at 61.6 percent in 2030.

2.1.2. High Scenario

In the High scenario, final energy consumption will grow at an annual rate of 3.5 percent to2030 driven by the industry sector, which will grow by 8.7 percent per annum. The transportsector energy consumption and the other sectors will grow at annual rates of 7.0 percent and 2.7percent, respectively.

Among the types of fuels consumed, biomass share will decrease from 78.1 percent in 2005 toabout 49.1 percent in 2030. The decline in the biomass consumption would be due to theincreasing use of electricity.

31

Figure 12: Final Energy Consumption by Energy Type

0

2,000

4,000

6,000

8,000

10,000

12,000kt

oe

Others 2,901 3,536 4,442 4,442 5,258 5,258

Heat 0 0 0 0 0 0

Electricity 9 64 161 279 279 562

Natural gas 0 0 0 0 0 0

Oil 369 930 1,924 2,727 2,997 4,881

Coa l 0 0 0 0 0 0

1990 20052020

Reference2020 High

2030Reference

2030 High

2.2. Primary Energy Supply

The primary energy supply of Cambodia was about 4,812 KTOE in 2005. It increased at anaverage annual rate of 3.6 per annum from 3,385 KTOE in 1995. The bulk of the primaryenergy supply in 2005 came from biomass which formed 73.5 percent of the total or 3,536KTOE. Oil supply was 1,272 KTOE or 26.4 percent and the remaining amount of 4 KTOE (0.1percent) came from hydro.

2.2.1. Reference Scenario

Cambodia’s primary energy requirements will grow at an annual rate of 2.4 percent from 2005to 2030. Primary energy consumption per capita will increase from 0.34 to 0.41 toe, which isstill significantly lower as compared to majority of the member states of the ASEAN.

Among the energy sources, hydro will have the highest annual growth rate of 12.6 percent perannum from 2005 to 2030. This is due to the planned construction of hydropower plants tosupply the projected increasing electricity demand.

Oil, in view of the fast growth rate of 3.5 percent per annum will increase its share to the totalprimary energy supply from 26.4 percent in 2005 to 34.2 percent in 2030. Other energy, whichis mostly biomass will have growth rate of 1.6 percent.

Coal and natural gas are envisioned to figure in the energy mix in the future as fuel forelectricity generation. Their combined shares will however be low at 2.2 percent in 2020 and 4.9percent in 2030. Biomass will remain as the major energy source with a share of 60.0 percent in2030.

32

Figure 13: Primary Energy Consumption by Energy to 2030

0

2,000

4,000

6,000

8,000

10,000

12,000

kto

e

Others 2,901 3,536 4,442 4,442 5,258 5,258

Hydro 0 4 24 69 74 176

Nuclear 0 0 0 0 0 0

Natural gas 0 0 33 86 97 217

Oil 484 1,272 1,924 2,727 2,997 4,881

Coa l 0 0 112 298 333 747

1990 20052020

Reference2020 High

2030Reference

2030 High

2.2.2. High Scenario

In view of the higher economic growth assumption in this scenario, primary energy supply willgrow at a faster rate of 3.5 percent per annum. Per capita primary energy consumption willincrease from 0.34 TOE to 0.63 TOE by 2030.

Hydro will exhibit the fastest growth in supply at 16.6 percent per annum from 2005 to 2030.Oil will also grow faster at 5.5 percent per year. Coal and natural gas will garner higher sharesin view of higher demand for electricity. Their combined shares will be 5.0 percent in 2020 and8.5 percent in 2030.

2.3. Power Generation

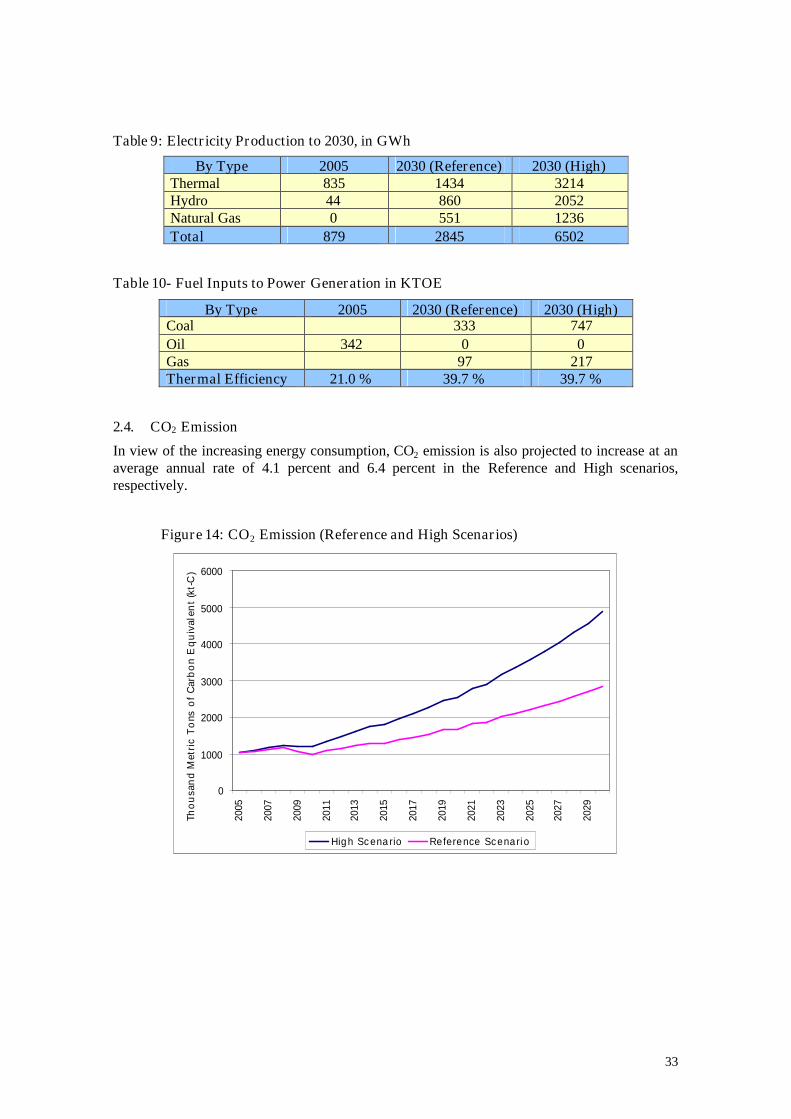

Electricity production was 879 GWh in 2005. In the future, electricity production is projectedto increase to 2,845 GWh in the Base Case with an annual growth rate of 4.8 percent and 6,502GWh in the High scenario posting an annual growth rate of 8.3 percent.

As regards, fuel inputs to power generation, coal and natural gas are projected to replace oil forboth the Reference and High scenarios.

In view of the shift from old oil power generating facilities to technologies using coal andnatural gas with higher efficiencies, thermal efficiency of Cambodia is expected to increasefrom 21.0 percent in 2005 to 39.7 percent in 2030 in the both scenarios.

33

Table 9: Electricity Production to 2030, in GWh

By Type 2005 2030 (Reference) 2030 (High)Thermal 835 1434 3214Hydro 44 860 2052Natural Gas 0 551 1236Total 879 2845 6502

Table 10- Fuel Inputs to Power Generation in KTOE

By Type 2005 2030 (Reference) 2030 (High)Coal 333 747Oil 342 0 0Gas 97 217Thermal Efficiency 21.0 % 39.7 % 39.7 %

2.4. CO2 Emission

In view of the increasing energy consumption, CO2 emission is also projected to increase at anaverage annual rate of 4.1 percent and 6.4 percent in the Reference and High scenarios,respectively.

Figure 14: CO2 Emission (Reference and High Scenarios)

0

1000

2000

3000

4000

5000

6000

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

Tho

usa

nd

Met

ric

To

nso

fC

arb

on

Eq

uiv

alen

t(k

t-C

)

High Scena rio Reference Scenario

34

3. FINDINGS AND POLICY IMPLICATIONS

3.1. Findings: