the abcs of retail

TRANSCRIPT

Michael Stevens, AICPExecutive Director

Capitol Riverfront BID

The ABCs of RetailIDA Caribbean Conference

February 24, 2008Nassau, Bahamas

The economic development process is not a sprint, it is a marathon race.

Retail attraction is not about “immediate gratification”, it is a process that takes years to realize results.

Michael StevensCapitol Riverfront BID

“To plan is human…to implement is divine.”Andrew Altman, former President & CEOAnacostia Waterfront Corporation

Retail Attraction is a Process Involving:

Players – public & private stakeholders & organizationsResources – a commitment of process, staff and $$$$$Priorities – the establishment of realistic goals Political Will – commitment of the local government (Mayor, City Council, County)Incentives – “carrots” to bring retailers to you Collective Vision – a plan of action based on visionPerseverance – staying the course although players may change over timePassion – belief in what you are doing it is rightImplementation – action items, strategies & tactics

Retail “Morphing”: Full Circle in 40 Years

Downtownswere the shopping destination

Shift to neighborhood strip shopping centers in the early sixties w/trolleys & autos

Regional mallsbecame the destination of choice

Power Centersemerged for convenience shopping & “bulk buying”

Suburban town centersdeveloped using design principles of downtown (create community)

Retail Recycles, Reinvents, & Evolves…

Retail venues can, & should be, recycled into new uses as retail reinvents itselfDept. stores are “reborn” as book stores & furniture storesRetail space becomes restaurants, sports clubs, electronics stores, independent retailers, etc.Retail mix is an organic process & evolutionary

Retail Can Be a Catalyst

Retail can be catalytic & attract other uses to cluster nearby - creating critical mass - although it tends to follow other land uses/activity generatorsGrocery stores are an excellent example of this “co-tenancy”, as are big box retailers

Retail’s Evolving Role

Retail has become more than just the purchase of consumer goods:

- It is experiential street theater- It is community engagement- It is restaurants & dining- It is “edutainment”- It is social interaction/therapy

Other Uses Can Attract Retail

As a follower of other activities, retail will cluster around sports arenas, theaters, museums, resorts, restaurants, i.e. other major activity anchors or pedestrian generators

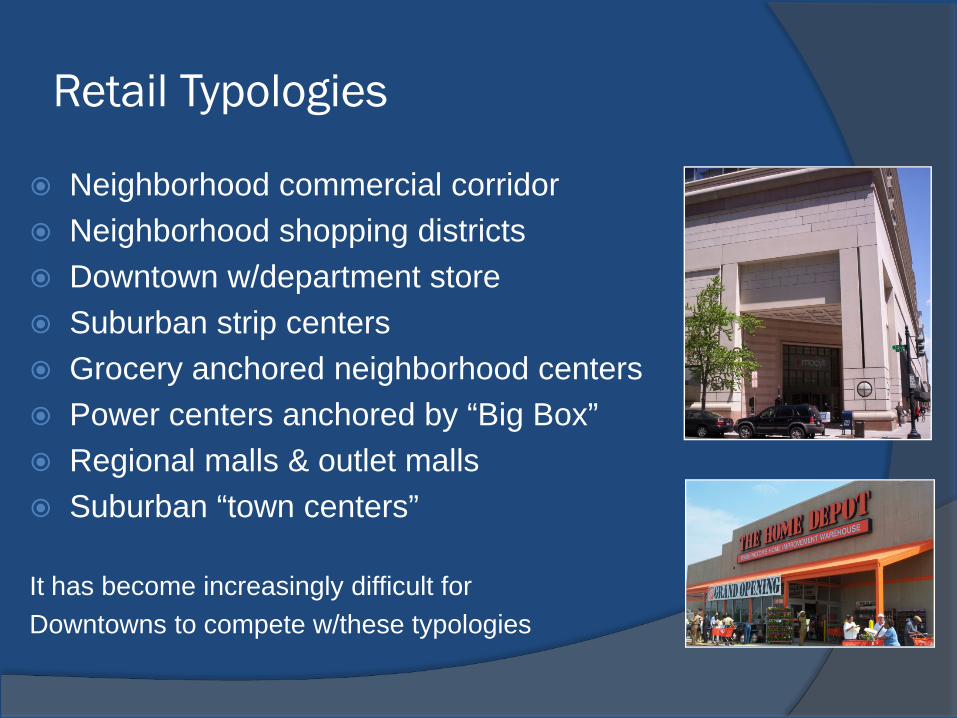

Retail Typologies

Neighborhood commercial corridorNeighborhood shopping districtsDowntown w/department storeSuburban strip centersGrocery anchored neighborhood centersPower centers anchored by “Big Box”Regional malls & outlet mallsSuburban “town centers”

It has become increasingly difficult forDowntowns to compete w/these typologies

Typologies Share Similarities

Successful mix of retailers (size, product, etc.)Variety of choices & even experiencesMost rely on plentiful, free parkingMany exhibit high quality & controlled public realmSuccessful typologies have a critical mass of retail & variety (stand alone big boxes are exception)Food offerings & convenience retail are present (banks, laundry, post office, FedEx/Kinko’s, etc.)Accessibility is a key to success – auto, transit, walking, etc.

What Downtowns Can Offer (as acompetitive advantage):

A variety of shoppers – employees, residents, visitors, conventioneers & studentsAuthenticity in environment & historyCompelling architecture built over timeDensity & diversity – everyone’s neighborhoodA larger mix of uses, experiences – museums, theaters, sports arenas, office, residential, hotels & convention facilities, art galleries, etc.A “walkable urbanity” & transit accessibility

Downtown/Urban Market Challenges

Crime, security & homeless issuesConvenient & inexpensive parkingMultiple property ownerships – land assembly is difficult & adds to costsQuality of public realmParcel or building sizes – size, depth & width constraintsOff street loading for trucksLack of residential density

Fundamentals of Retail Attraction

Market AnalysisInventory & Understand Retail OpportunitiesIdentify Your Retail MixApproach the RetailersImplement a Process

Market Analysis

1. Prepare a retail market analysisIdentify existing retail supply, demand & gaps in the provision of retail (consumer goods)Identify household income & what that income is used to purchaseIdentify “leakage” from communityIdentify sub-markets & competitionIdentify retailers that fill “gaps”Who is the market?

Know Your Retail Opportunities

2. Develop a retail opportunities inventoryIdentify all retail opportunities – sites, lease space & projects sitesResearch & understand those opportunities- Size - Location - Ownership- Access - Zoning - Traffic & pedestrian countsUnderstand their “position” in the marketplaceBegin the process of matching retailers to those various opportunitiesDevelop database of opportunities & publications to support

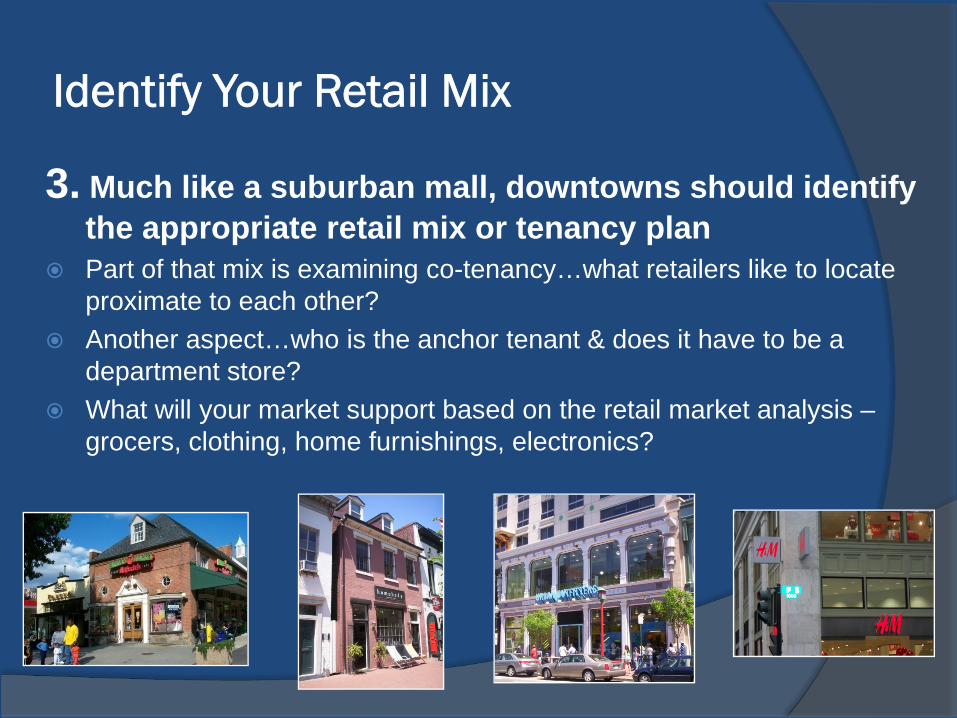

Identify Your Retail Mix

3. Much like a suburban mall, downtowns should identify the appropriate retail mix or tenancy planPart of that mix is examining co-tenancy…what retailers like to locate proximate to each other?Another aspect…who is the anchor tenant & does it have to be a department store?What will your market support based on the retail market analysis –grocers, clothing, home furnishings, electronics?

Approach the Retailers

4. Develop a plan of action w/tacticsIdentify retailers that meet needs & match-up with opportunity sites – have specific sitesResearch retailer contacts, operations, & store requirementsIdentify local brokers & developers who have worked with these targeted retailersContact by e-mail and phone…it will take multiple attemptsUse ICSC conferences & conventions for face to face meetingsPrepare support materials – print & electronic summaries on sites, demographics, incentives

Implement a Process (embrace the horror)

5. Approach retail attraction as a processEstablish a year-round schedule of contacting retailersUtilize ICSC events & conferences to meet in person & market opportunitiesInvite retailers to your city for toursContinuously update database on opportunities, demographics, other researchSell the product – market using publications, website, etc.

Basic Assumptions on Retail Attraction

Most downtown & inner city markets are underservedGrocery stores, restaurants & drug stores are often first “national” retailers that will go into these markets“Big box” retailers are rethinking their footprints & formats to adapt to urban environments (smaller sites)Retailers follow “rooftops” – residential densities & disposable incomesLocation decisions based on accurate information Retail attraction based on relationship building

National Retailers OK as a Starting Point

Nationals help legitimize your marketNationals, especially food, provide a familiarity & comfort level for traveling visitors (families)Nationals have staying power while market builds that independents often do not haveNationals help prove purchase power of market

What do retailers look for?

First & foremost…to make money…lots of $$$$Opportunities for stores – sites, lease space, development projects, commercial corridors, etc.Accurate Information on the market:- Population growth - Household incomes - Age distribution- Household expenditures - Neighborhood profiles (1 – 3 mile rings)- Traffic counts - Building permits - Competition- Parking & transit access - Incentives - Critical mass

Contacts who know the development processConsistent & predictable review/permit processIncentives to reduce market entry costs

Retail in Urban MarketsCities are often extremely underserved markets: - Less retail per capita per sq. ft. than surrounding suburbs (U.S. average is 17 sq. ft., DC is 9, VA/MD suburbs is 24 )- Residents have to cross municipal or state lines to purchase basic goods and services- Cities lose millions in sales tax revenues (DC is $1.5 billion)- They often lack apparel stores, home furnishings, electronics, grocery stores, big box retailers, etc.

Giant Foods

Future Giant

Future Harris Teeter

Magruders

Safeway

Future Safeway

Future Trader Joes

Whole Foods

NW

NE

SE

SW

Major DC Grocery Stores

Some Reasons Retailers Leave

Constraints of a city’s development patterns/standards1. Shortage of large parcels for development, multiple ownerships2. Constraints of commercial corridors (setbacks, ownership, pkg.)3. Lack of parking in downtown & commercial corridors“Nimbyism” towards retail issues – traffic, density, etc.Riots of 1968 & damage done to commercial corridorsLack of population base with significant disposable incomesEasier to develop in suburbs on “Greenfield” sitesPopulation decline over thirty years in many citiesLack of free parking supply

But Cities Demographics Are Compelling…

Density – more residents per square mileAverage household incomes are risingDaytime workforce populations w/disposable incomeConvention & visitor business New housing starts – back to the city movementStudent populations w/incomeHidden “cash economies” of inner city & minority markets

Goal of Retail AttractionPolitical will of Mayor/City – retail attraction should be fundamental economic development goal of cityNew retail stores benefit a city in a number of ways:1. Stores enhance property tax & sales tax revenues2. New retail provides opportunities to hire residents, thereby adding to income tax revenues3. More retail enhances residential attraction effortsCity governments can stimulate the process by providing sites for development & incentives for retail storesCity governments can be major partners in the process

Retail Attraction is a Partnership

Retail attraction as a public/private partnership between City Govt., retail brokers, BIDs, property owners & commercial developersRetail attraction partnership based on four components:1. Organization – an organization or entity to oversee & manage the attraction effort2. Process – using ICSC conferences as a platform for attraction, relationship building, & a year-round effort3. Deal Making – using incentives to attract retailers & commercial developers, city government involved in deal making for retail4. Information – accurate info on sites, demographics, neighborhood profiles, etc.

Retail Attraction Strategy – Washington, DC Economic Partnership

The Washington, DC Economic Partnershipwas created in 2000 as an independent entity to manage retail attraction & promote development opportunities1. WDCEP is a public/private partnership that interfaces with government, the local broker community & developers

2. WDCEP serves as the first point of contact for information on sites, incentives, the development process, data & demographics

3. WDCEP is a 501(c)(3) nonprofit that can serve as a confidential first point of contact & access to the DC Govt. 4. WDCEP serves as the coordinating entity for the District’s local, regional & national retail attraction efforts

Retail Attraction as a Process

Year-round effort Involves research, marketing materials, attendance at ICSC conventions & trade shows, networks with brokers/developers/retailers, etc.Marketing materials can include…1. Neighborhood Retail

Opportunities Book2. Neighborhood Profile Sheets3. DC Main Street SheetsICSC in DC, New York & Las Vegas

Retail Attraction Strategy – ICSC Events

ICSC events can be foundation of retail attraction strategy:1. Best platform to enter the retail attraction process & quickly “legitimize” city’s efforts2. Mayor can be your best ambassador for retail attraction3. Conventions allow Mayor & Council to meet with retailers, brokers & developers face to face 4. Cities use booths & a range of publications to market opportunities

ICSC Conferences & Conventions

ICSC spring convention in Las Vegas is major opportunity to meet with retail communityUse a variety of tactics to meet retailers, brokers & commercial developers & establish relationships1. Reception for retailers, brokers, developers, etc. 2. Retailers dinner3. Developers dinner4. Booth to host meetings with retailers Sponsors help underwrite costs of booth, materials, reception & dinners – public/private partnershipOther ICSC conferences throughout USA –regional & state IDEA Exchanges, Alliance programs, etc.NY IDEA Exchange is 2nd largest ICSC conventionwww.icsc.org

ICSC Conferences & Conventions

Do not necessarily need a booth to be successfulDo set appointments w/retailers & brokers at least 2 months in advanceWalk the floor to meet retailers, brokers & developers at their boothsAttend receptions & educational sessions to make contactsFollow-up after conventions

Retail Attraction - Summits

Retail summits part of a year-round attraction strategy that extends the attraction process1. City can host retail summits each year to extend cycle2. Each summit focuses on a different retail cluster –restaurants, apparel, home furnishings, grocers/big boxes, etc. – where city has definitive needs3. Opportunity to host retail decision makers for a day in your city that involves tours of opportunities & neighborhoods4. Summits bring retail decision makers from ICSC conventions to your city for a closer look & to meet key players in the process

Retail Attraction Strategy - Research

Cities can serve as an information clearinghouse for data collection and research on retail attraction1. WDCEP collects and publishes data on development activity in DC:

- building permits - sites - development projects- housing units - incentives

2. WDCEP partnered with DC Government to conduct research on DC’s market potential and cash economy – Social Compact project3. WDCEP partners with broker & development community for information on retail opportunities4. WDCEP partners with DC Main Street program to document existing retail conditions in commercial corridors

Research & Information Systems

Goal of making the city the definitive information clearinghouse on demographics, development, opportunities, etc.Interactive websites reach national audiences Retail opportunities interactive databaseDevelopment projects interactive databaseBuilding permit informationCensus & demographic info on neighborhoodsMapping capacity – GIS systemCore economy research

Capitol Riverfront

3,9121,97428%

$67,567$73,627$27,837

$5,680,000$5,973,000$9,253,000$5,839,000$4,060,000

$23,600

Source: ESRI Business Information Solutions (2005 Estimates and Projections)

Capitol Riverfront: Demographics

DemographicsPopulationHouseholdsOwner-occupied

IncomeAverage Household IncomeMedian Net WorthMedian Disposable Income

Consumer ExpendituresApparelEntertainment & HobbyFood at HomeMeals at RestaurantsHome FurnishingsTotal Avg. Per HH

204,43889,159

35%

$57,845$87,992$29,221

$223,472,000$230,002,000$369,287,000$229,026,000$153,716,000

$20,500

0 - 0.5 miles

24,96313,668

40%

$78,212$126,238$38,605

$45,378,000$47,667,000$74,498,000$47,018,000$32,261,000

$27,400

0 - 1 mile 0 - 3 miles

Capitol Riverfront: DC Bldg. Permits

Source: Department of Consumer and Regulatory Affairs (1/2002 – 12/2005)

* 3 mile radius

2002200320042005Totals

Permits Issued

4,3144,5805,0854,563

18,542

2002200320042005Totals

Valuation

$1,435 m$1,209 m

$647 m$855 m

$4,146 m

National Mall

NavyYard

BollingAirforce

Base

Maryland

National Mall

NavyYard

SaintElizabeth’s

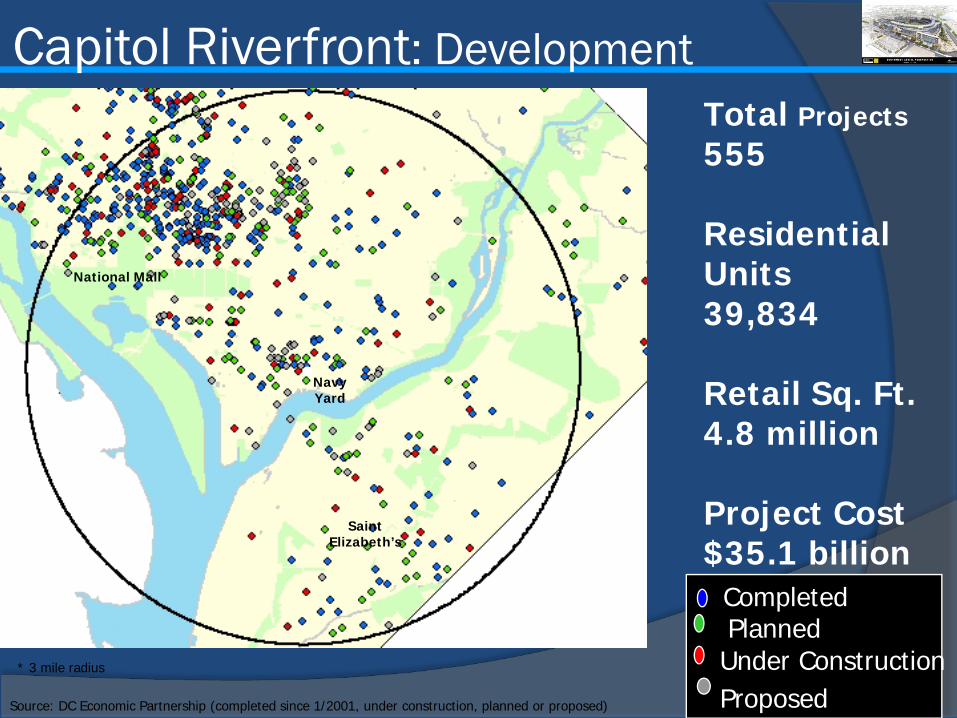

Capitol Riverfront: Development

Source: DC Economic Partnership (completed since 1/2001, under construction, planned or proposed)

* 3 mile radius

Total Projects555

Residential Units39,834

Retail Sq. Ft.4.8 million

Project Cost$35.1 billion

Completed

Under ConstructionPlanned

Proposed

National Mall

NavyYard

BollingAirforce

Base

SaintElizabeth’s

National Mall

NavyYard

SaintElizabeth’s

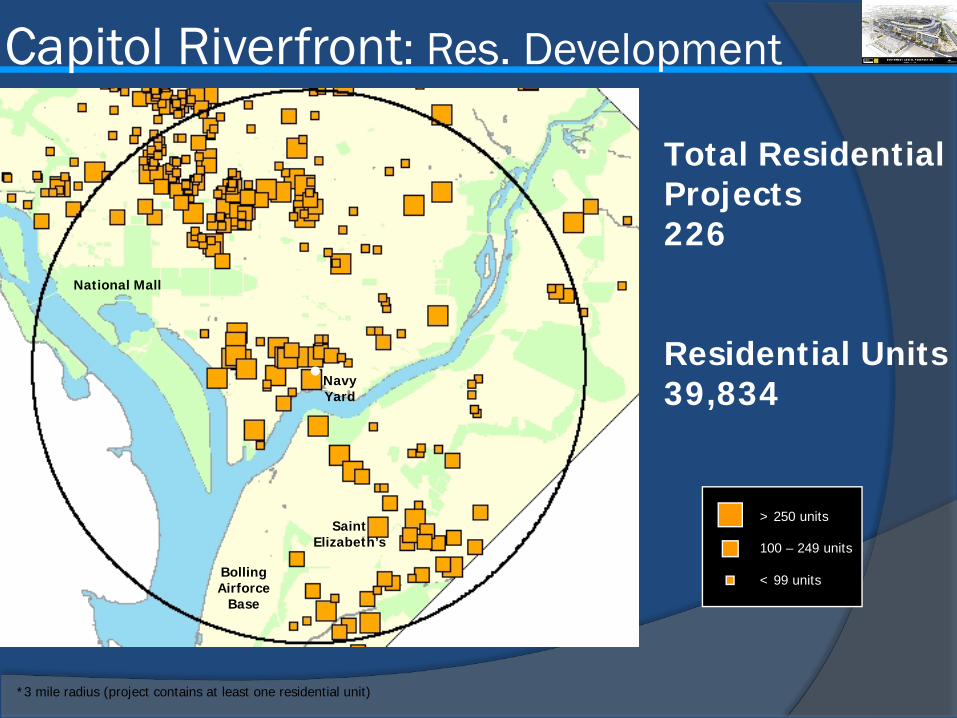

Capitol Riverfront: Res. Development

*3 mile radius (project contains at least one residential unit)

Total ResidentialProjects226

Residential Units39,834

< 99 units

100 – 249 units

> 250 units

National Mall

NavyYard

BollingAirforce

Base

SaintElizabeth’s

Proposed PlannedUnder

ConstructionCompleted(since 1/2001)

TOTAL

No. of Projects

Total Sq. Ft.

Office Sq. Ft.

Retail Sq. Ft.

Resdntal. Units

Project Cost

83

36,911,246

15,041,836

1,454,156

9,654

$9.2 billion

122

40,453,360

21,181,196

1,460,996

14,601

$10.4 billion

92

18,416,635

9,527,379

500,735

5,180

$5.7 billion

258

41,856,416

19,253,358

1,469,208

10,399

$9.8 billion

555

137,637,657

65,003,769

4,885,095

39,834

$35.1 billion

*Located within three miles (projects have a minimum valuation of one million dollars)

Capitol Riverfront: Development Data

Capitol Riverfront: Retail Sites

Baseball Stadium30,000 sq. ft.

Arthur/Capper Hope V51,000 sq. ft.

U.S. Dept. of Transportation

M Street

Sout

h Ca

pito

l St

reet

Canal Park75,000 sq. ft.

Capitol Hill Towers

The Yards300,000 sq. ft.

Jefferson at New Jersey6,000 sq. ft.

Half Street50,000 sq. ft.

Retail Attraction Strategy:Incentives for Retailers

Retail attraction incentives/entitlements can include:1. Grocery store tax abatement program2. TIF financing for mixed use projects3. Government sites for development4. Job training funds5. Retail research efforts6. EZ incentive programs7. Downtown Retail TIF program8. Streetscape improvements9. CDBG funds

Incentives – Grocery Tax Abatement

DC very underserved market for grocery stores with Safeway & Giant dominating marketDC Government can award property and sales tax abatements for grocery stores locating in the DistrictAbatement is awarded on a deal-by-deal process & must be approved by DC Council – viewed as catalytic projectsAmount of abatement and length awarded on case-by-case basis

Grocery Store Tax Abatement

Incentive had multiple goals:1. Attract grocers to underserved neighborhoods2. Stabilize areas & attract additional development 3. Attract additional housing & retail stores4. Provide basic goods & services while capturing future sales & property taxes

Incentives – Retail Research Efforts

Social Compact researchResearch examines “intown” neighborhood clusters and documents:1. Hidden cash economy of neighborhoods2. Spending potential of consumers3. Retail “leakage” to adjacent jurisdictions4. Uncounted population Census missed5. Building ownership in neighborhoodsData is used in retail attraction efforts to illustrate spending power

Incentives – Downtown Retail TIF Program

Downtown Retail TIF Program focuses on attracting retail to an identified Downtown retail districtGoals of the program are as follows:1. Attract high quality/unique retail to retail TIF district2. Provide tenant finish-out funds to property owner to make retail deals happen3. Create a critical mass of destination retail that will attract more retailers to district

Downtown Retail TIF Program

How the program works – the mechanics of the deal…1. $30 million is available in the TIF fund2. Retailers must locate in an identified Downtown TIF district3. Property owners apply for funds and use for tenant finish-out, reducing costs to retailer4. Fund is repaid by future sales tax generated5. TIF funds are available to apparel, home furnishings, general merchandise & specialty retailers6. Applications reviewed by TIF committee based on criteria, Deputy Mayor has final approval

Retail Attraction – Marketing Assets

Retail Attraction – Marketing Assets

• Market segment sheets

• Neighborhood profile sheets

• DC Main Street sheets

• Print ads • Summary sheets on incentives• Website w/interactive databases & publications

• Monthly electronic newsletters

Marketing Development Dynamic

Benefits of Research

You are doing “homework” for retailersYou are establishing your organization as a reliable “information clearinghouse”You are speeding up the processYou can provide information from government that retailers/brokers cannot always accessYou are creating value & gaining trust

District Retail Success Stories

A variety of new retail stores have located or signed leases in the District:- Home Depot - Gap- H & M Retail - Target- Jos. A. Banks - Costco- The Container Store- Whole Foods, Giant & Safeway - Loehman’s - Trader Joe’s- Best Buy - Bed, Bath & Beyond- Cost Plus - Harris Teeter- Fresh Grocer - West Elm

Lessons Learned…

Establish a process based on a collective vision Identify the right players in the processDo you homework – research market conditions & feasibility for new retailDevelop a plan of action but allow for flexibility in tactics & processPrioritize retailers you want to pursue, as well as opportunity sitesDevelop inventory of retail opportunities & leverage government owned properties Provide incentives as a part of the attraction process

Lessons Learned…

Establish political will & partnerships among entities & private stakeholdersHonestly assess strengths, weaknesses, opportunities & threats of the marketBase strategies & plans on those market realitiesEstablish a achievable goals, benchmarks & action itemsMarket your resources at every opportunityUse ICSC events & other trade shows as part of year-round attraction process

Retail Projects: DC USA

Location: Columbia Heights, NW

Type: Regional retail center

Developer(s): Grid Properties Inc

Total SF: 540,000

Retail SF: 540,000 (Target)

Project Status: Under Construction

Targeted Delivery: March 2008

Project received a TIF to fund parking garage development

Retail Projects: Gallery Place

Location: Downtown, NW

Type: Downtown mixed-useDestination retail/entertainment

Developer(s): Western Dev. & JohnAkridge Companies

Total SF: 1,100,000

Office SF: 237,000

Residential Units: 192

Retail SF: 260,000

Project Status: CompletedProject received a $73 million TIF

Retail Projects: Tivoli Square

Location: Columbia Heights, NW

Type: Grocer anchored, mixed-use

Developer: Horning Brothers

Total SF: 175,000

Office SF: 28,000

Residential: 38 townhouses

Retail SF: 77,000

Project Status: Completed 2005

Stevens Contact Information

Michael Stevens, AICPExecutive Director

Capitol Riverfront BID1100 New Jersey Avenue, SE

Suite 1000Washington, DC 20003

(202) [email protected]