the archipelago economy - kjri hamburg · confidential and proprietary any use of this material...

TRANSCRIPT

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of McKinsey & Company is strictly prohibited

The Archipelago Economy:

2015 Outlook and Beyond

June 2015

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of McKinsey & Company is strictly prohibited

McKinsey & Company | 1

3.4

2.1

2.1

2.0

2.0

2.0

1.8

1.8

1.8

1.7

1.7

1.6

1.6

1.5

0.9

0.9

India

Canada

Switzerland

Belgium

New Zealand

France

Norway

Portugal

Australia

Indonesia

China

Poland

South Korea

Average rest

United States

Netherlands

SOURCE: Conference Board Total Economy Database; International Monetary Fund; World Bank; McKinsey Global

Institute analysis

Contrary to most belief, Indonesia has demonstrated consistent growth for

the past decade

3.1

Czech Republic

4.0

South Korea 4.2

Slovakia 4.9

Russia

3.7

Estonia 3.8

Poland 3.9

Turkey

Average rest

Australia 3.1

Israel

1.7

4.9

Indonesia 5.2

India 7.7

China

3.4

South Africa 3.5

Brazil 3.6

Chile

11.5

GDP growth, standard deviation,

annualised, 2000-10 Real GDP growth, 2000-10

Overview of OECD and BRIC plus South Africa development

Percent

▪ Strengthening overall

macroeconomics: lowering

government debt/GDP,

containing inflation, etc.

▪ Not only driven by more

labor input, but also

productivity though still a lot

of room to catch-up

▪ Not only due to resources,

sectors such as retail trade,

transport, and

telecommunications growing

fast

▪ Not only centered in

Jakarta: other areas growing

fast, albeit from a smaller base

Other highlights of Indonesia’s

development

McKinsey & Company | 2

Indonesia is the 16th-largest economy in the world, and has the potential

to be the seventh largest by 2030

SOURCE: McKinsey Global Institute

7th largest economy in the world 16th largest economy in the world

135 million members of the consuming

class

45 million members of the consuming

class

71% of population in cities producing

86% of GDP

53% of population in cities producing

74% of GDP

113 million skilled workers needed 55 million skilled workers

$1.8 trillion market opportunity in

consumer services, agriculture and fisheries,

resources, and education

$0.5 trillion market opportunity in

consumer services, agriculture and

fisheries, resources, and education

INDONESIA TODAY … AND IN 2030

McKinsey & Company | 3

Exports

USD million, monthly

50

100

150

200

250

300

350

400

2015 2014 2013

Indonesia

Thailand Vietnam

Philippines

Singapore

Malaysia

SOURCE: Haver Analytics; McKinsey's Global Economics Intelligence analysis

2015 is a tough year for ASEAN – exports declining due to sluggish

demand and weak commodity price

Price of crude oil

Price of crude palm oil

Price of coal

0

50

100

150

2010 2012 2013 2015 2011 2014

USD/bbl, monthly

0

50

100

150

2014 2011 2010 2013 2015 2012

USD/tonnes, monthly

0

500

1,000

1,500

2013 2011 2010 2014 2012 2015

USD/mt, monthly

McKinsey & Company | 4

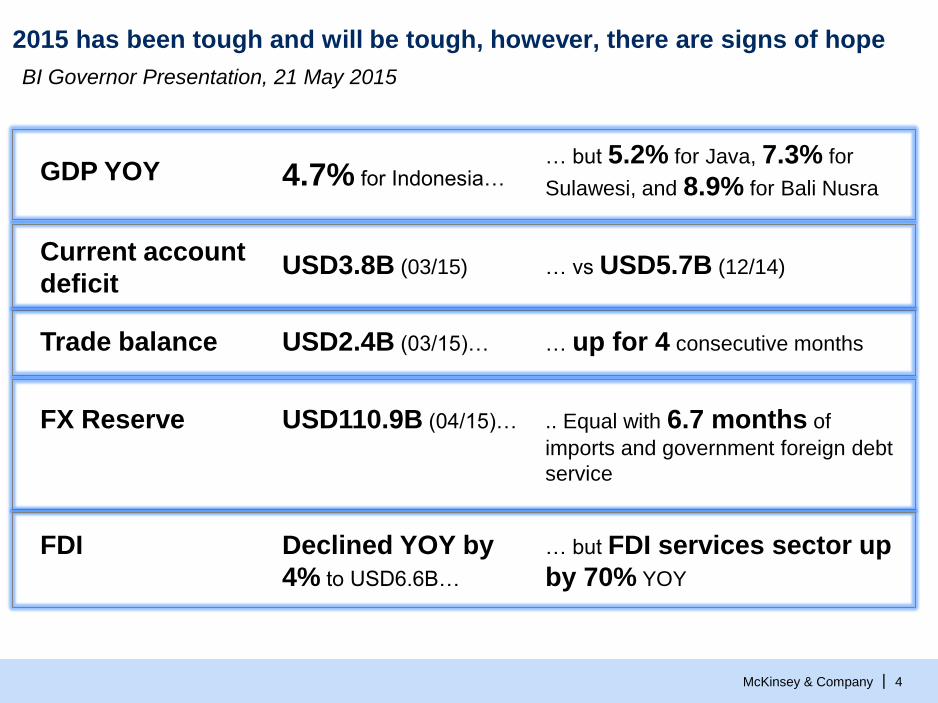

2015 has been tough and will be tough, however, there are signs of hope

FX Reserve

GDP YOY

USD110.9B (04/15)…

4.7% for Indonesia…

.. Equal with 6.7 months of

imports and government foreign debt

service

… but 5.2% for Java, 7.3% for

Sulawesi, and 8.9% for Bali Nusra

Trade balance USD2.4B (03/15)… … up for 4 consecutive months

Current account

deficit USD3.8B (03/15) … vs USD5.7B (12/14)

FDI Declined YOY by

4% to USD6.6B…

… but FDI services sector up

by 70% YOY

BI Governor Presentation, 21 May 2015

McKinsey & Company | 5

Indonesia has a number of opportunities and strengths going in the long

run, but GoI must continue effort to boost sustainable growth

Boosting productivity

Ensuring inclusive growth

Building resilience

Productivity still lags peer countries

USD 6k GDP per person, versus

14k in Malaysia

Unequal growth, rising

inequality – life expectancy in

Yogyakarta is 15 years more

than in West Nusa Tenggara

Rising consuming class

Young population till 2025/30

offers a one-off unique chance to

exploit demographic dividend

Untapped resource potential

Increasing urbanization – 9% p.a.

GDP growth for large middle

weight cities to 2030

Exploiting opportunities

Technologically savvy population –

324m mobile and 93m Internet

users in 2015

Benefitting from inherent strengths

Resource – intensive growth will

pose supply challenges – energy,

food, water

Volatility of world economy

Indonesia

2030

Top 10

economy

SOURCE: McKinsey Global Institute

McKinsey & Company | 6

Indonesia would have ~74 million households in consuming class

by 2030 Consuming class households, 2013–301

Million

SOURCE: McKinsey Global Institute Cityscope database; national statistics offices; McKinsey Global Institute analysis

1 Defined as households with more than $7,500 in annual income (in 2005 purchasing power parity terms). This is the income level at which households

begin to make significant discretionary purchases; Brunei not shown on chart as number of consuming class households in 2030 is only ~0.1 million.

1

1

1

6

3

13

10

11

34

1

2

3

9

9

20

21

23

Laos

Singapore

Cambodia

Malaysia

Vietnam

Myanmar

Philippines

Thailand

Indonesia 74

2030

2013

THE RISE OF ASIA

La

st M

od

ified

5/2

7/2

01

5 1

:33

PM

SE

Asia

Sta

nd

ard

Tim

e

Prin

ted

5/2

6/2

01

5 1

2:2

9 P

M S

E A

sia

Sta

nd

ard

Tim

e

Different regions expected to continue growing – many fast

growing cities are outside Java

SOURCE: 2010 Population Census, Indonesia’s Central Bureau of Statistics; McKinsey Global Institute analysis

Small middleweights

(150,000–2 million)

Large middleweights

(5 million-10 million)

Type of urban area1

1 Urban areas are aggregated areas consisting of cities (kota) and districts (kapupaten) rather than specific city jurisdictions,

GDP compound annual

growth rate, 2010-30 (%)

Less than 5 percent

5 to 7 percent

More than 7 percent

Mid-size middleweights

(2 million–5 million)

Jakarta >10 million

Sumatra

Kalimantan

Java

Sulawesi

Papua

Nusa Tenggara Bali

Maluku

GDP development, 2010-30

INHERENT STRENGTH

McKinsey & Company | 8

2.4

2.9

4.6

7.0

60%

Historical labour

productivity

growth, 2000–

102

Required growth

from labour

productivity,

2010–30

Expected growth

from increased

labour inputs1

GDP growth

target

Achieving Indonesia’s 7 percent annual GDP growth target will require

labour productivity to grow 60 percent faster, in a way that is different

SOURCE: CEIC Data; Indonesia’s Central Bureau of Statistics; Conference Board Total Economy Database; International

Monetary Fund; United Nations Population Division; McKinsey Global Institute analysis

1 Driven by additional workers joining the work force due to demographics and increased participation in work force; productivity assumed to be the

average in 2010–30 based on a business-as-usual growth rate of 5 to 6 percent.

2 Based on an average among national and international data sources.

Annual real GDP growth rates

Percent

Indonesia needs to

boost

productivity in

a way that is

inclusive to the

archipelago, and

resilience to

external shocks and

volatility

McKinsey & Company | 9

Required infrastructure and real estate investment, 2014–301

$ trillion

Infrastructure is one of the key to resolving these challenges: Indonesia

would need investment of ~$2.8 trillion till 2030 in infra and real estate

Transport

Water

Power

Telecom

Commercial

real estate

Residential

real estate

Total

investment

7.0

1.2

1.0

0.6

0.6

0.5

3.1

Others2

0.5

Vietnam

0.7

Singapore

0.7

Malaysia

0.7

Thailand

0.8

Philippines

0.9

Indonesia

2.7

1 In 2013 real dollar terms.

2 Includes Brunei, Cambodia, Laos, and Myanmar.

NOTE: Numbers may not sum due to rounding.

SOURCE: Pike Research; IHS; McKinsey Global Institute analysis

McKinsey & Company | 10 SOURCE: Bank of Indonesia presentation

Government of Indonesia has made infrastructure development a priority

More than 60%

increase in

infrastructure spend

allocation in 2015

revised budget

Acceleration of

execution required

in 2015

McKinsey & Company | 11

With maritime logistic being the focus of the new government for

productivity reform, there can be step change in productivity impact

INFRASTRUCTURE – MARITIME LOGISTIC

2012 current network is point to point with 4 major hubs

Optimized network based on port performance aspirations and

cost-minimization has transshipments and features sub-hubs

SOURCE: MOT, Tg Priok O&D, World Fleet Register Report, Network model output, Team analysis

5,000TEU Major ports

Major regional ports

Current

network

Improved handling

& Cost optimization

41%

0%

274

67%

11%

121

Trans-

shipments

Vessel

utilization

Number of

vessels

Avg vessel

size, TEU ~700 ~1,500

Cost per

TEU, USD 366 191

48%

McKinsey & Company | 12

Shipping

industry

Supporting

industries1

Port industry

The Maritime Logistics study proposes 11 reforms to tackle the challenges

faced today and transform Indonesia in a leading maritime nation

SOURCE: Team analysis

1 Trucking, Logistics centers/ICD, FF and 3PL, Education

3PL Cross cutting themes

▪ National regulatory

reform needed for:

– Harmonization of

regulation across

institutions and regions,

e.g. imports, trucking

circulation

– Investment incentives

▪ Education system will

need to increase

capacity and attract

talents both at sea and

ground

▪ World-class port

operations – incl.

24/7 operations of key

services (e.g. banks,

customs) & provision of

vital supplies (e.g., fuel,

power)

▪ Reducing dwelling

time through:

– Streamlined import

process /better

agency coordination

– Port tariff to reduce

storage at CY

▪ Staged invest-

ments for dredging

or construction of new

sea ports

▪ Acceleration of

implementation of

landlord & concession

models

▪ Improvements in

shipping navigation,

classification, security,

and safety systems

▪ Investments in

– Vessel fleet

– Dockyards

▪ More professionali-

zation and coordina-

tion with ports

– Berth window

– Cut-offs

– Stowage/CWP

▪ Hard land

infrastructure

(logistics centers and

ICDs) and connectivity

to port (e.g. inland

waterways, roads etc)

▪ Professionali-

zation and coor-

dination is required, e.g.

– Choice of network by

FF

– trucking backhaul

utilization

– Warehousing

8 10 1 5

3

4

9

11

2

7

6 $$

Focus today

McKinsey & Company | 13

In summary…

▪ Indonesia has demonstrated consistent growth over the past decade, fueled by strong

fundamentals. We believe that it has the potential to be the top 10 economy in the world in

2030

▪ 2015 is a tough year for ASEAN, and for Indonesia:

– Weak demand and weak commodity price

– Growth projected to slow down to 4.7%, FDI slows down, deficit in current account remains

– Some glimmers of hope, e.g. 70% increase FDI in service sector, trade balance surplus for

four months in a row, inflation under control

▪ There are, however, reasons to be bullish for the long term growth

• Growth of consuming class and young population

• Inherent strengths in natural resources

• Productivity growth must be inclusive and resilience; GoI has recognized this

priority and made conscious effort towards resolving infrastructure, one of the keys for

sustainable productivity

• Recognition that maritime plays a big role in infrastructure – optimized network can

reduce logistic costs by almost half. This effort, however, required movements across port

and adjacent sectors.

• Indonesia is still volatile, however, strong fundamentals say that it remains attractive market.

Thus, to do business in the country means to look for impact beyond profit/return in the

short-term. It means to look for partnership for the long term value creation.

1

3