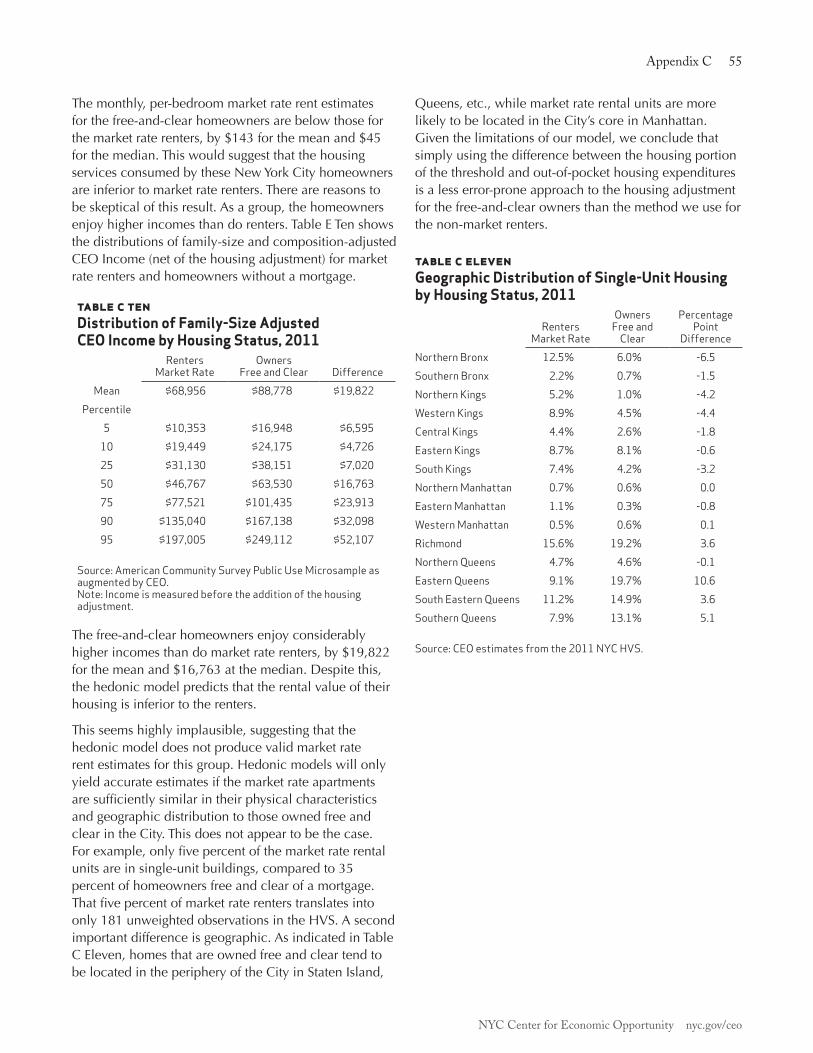

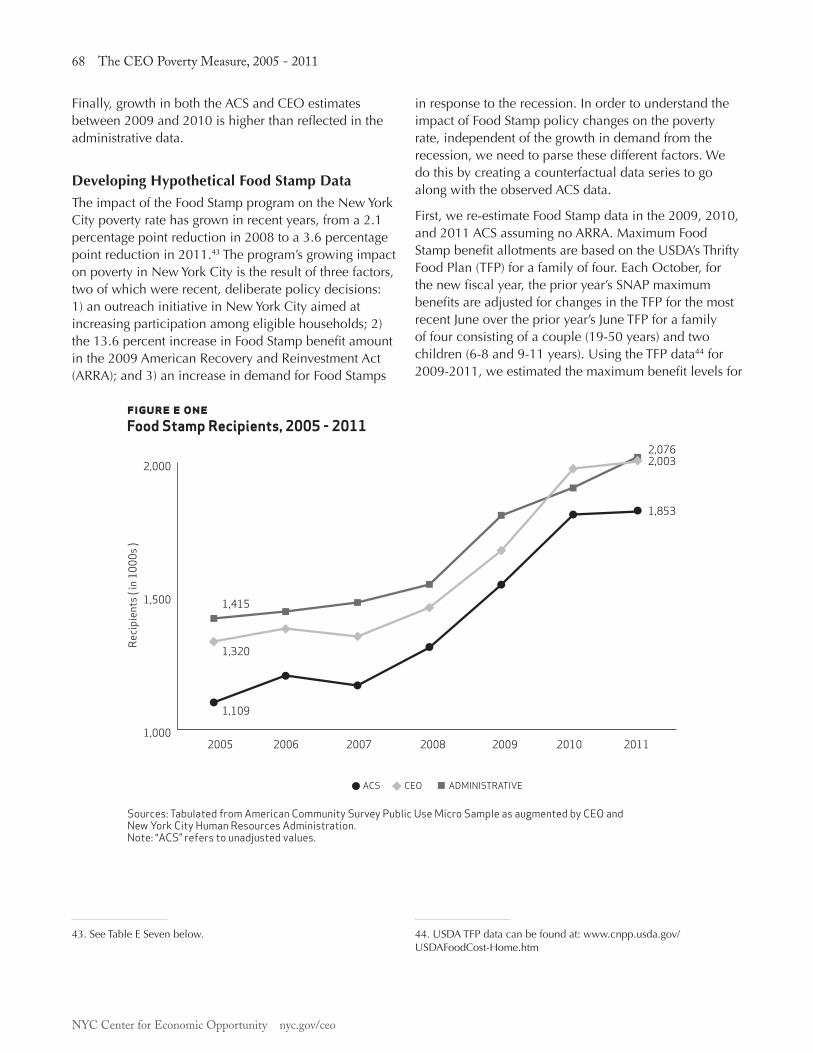

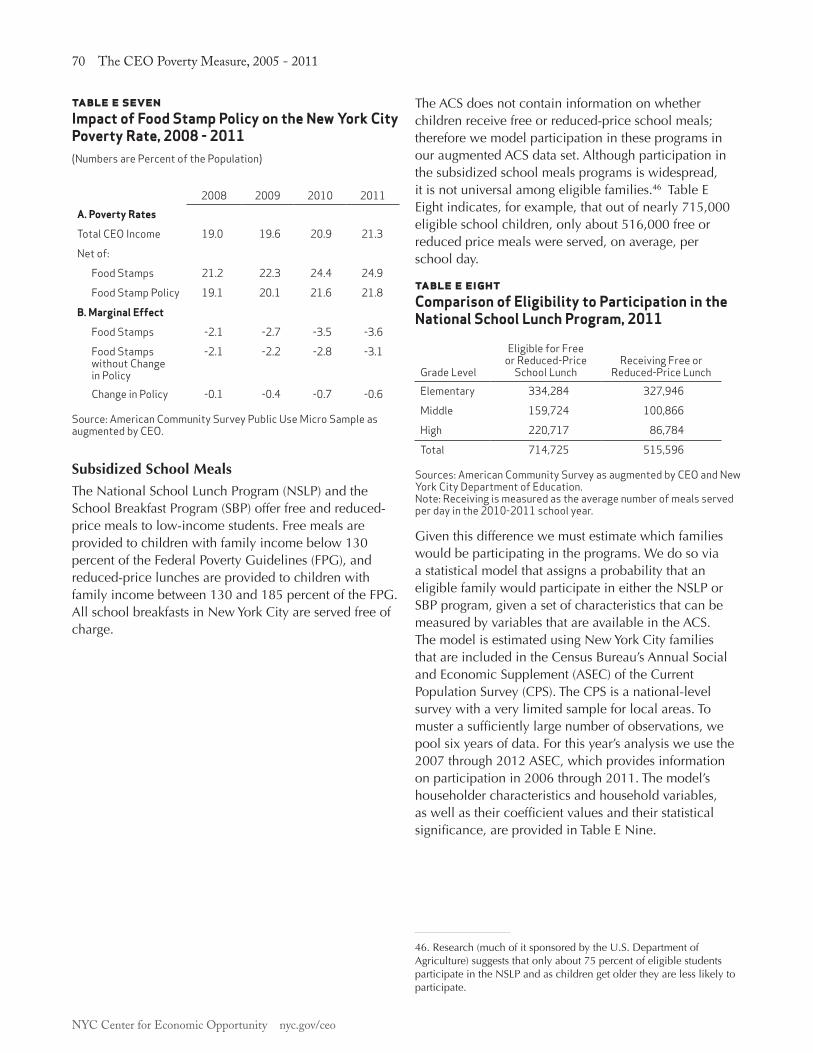

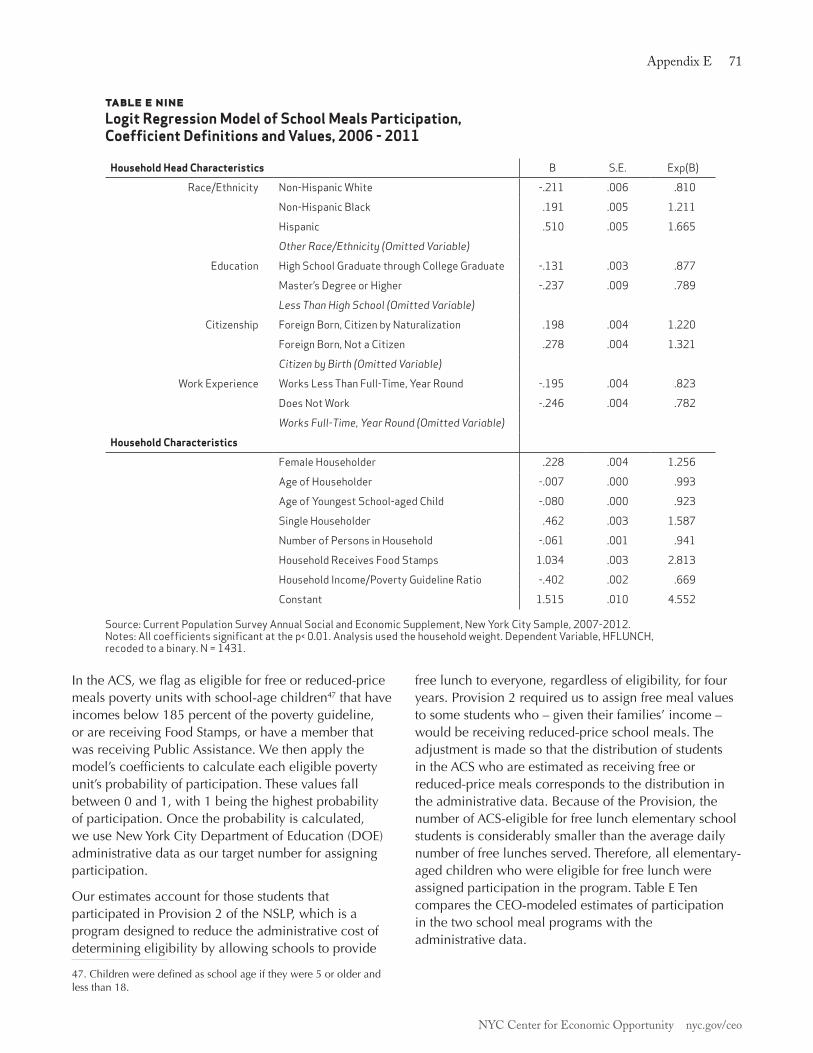

the ceo poverty measure, 2005 - 2011 - new york city

TRANSCRIPT

The CEO Poverty Measure, 2005 - 2011

An Annual Report by the NYC Center for Economic Opportunity

April 2013

The CEO Poverty Measure, 2005 - 2011

An Annual Report by the NYC Center for Economic Opportunity

April 2013

Table of ConTenTs

PREFACE AND ACKNOWLEDGMENTS ............................................................................................. i

EXECUTIVE SUMMARY ................................................................................................................... iii

I. INTRODUCTION .......................................................................................................................... 1 1.1TheOfficialPovertyMeasure ............................................................................................. 1 1.2TheNationalAcademyofSciences’Alternative ................................................................. 2 1.3TheSupplementalPovertyMeasure ................................................................................... 2 1.4CEO’sAdoptionoftheNAS/SPMMethod .......................................................................... 2 1.5ComparingPovertyRates ................................................................................................... 5 1.6TheNewYorkCityLaborMarket ....................................................................................... 6 1.7KeyFindingsinThisReport................................................................................................7

II. POVERTY IN NEW YORK CITY, 2005 - 2011 ................................................................................ 9 2.1NewYorkCityPovertyRates,2005-2011 ......................................................................... 9 2.2TheDepthofPovertyandExtentofNearPoverty ............................................................. 13 2.3TheEffectofNon-CashResourcesontheCEOPovertyRate............................................. 14

III. CEO POVERTY RATES IN DEMOGRAPHIC DETAIL, 2005 - 2011 ............................................. 19 3.1PovertyRatesbyDemographicCharacteristicoftheIndividual ........................................ 19 3.2PovertyRatesbyFamilyCharacteristic ............................................................................. 22 3.3PovertyRatesbyBorough ............................................................................................... 25

IV. ALTERNATIVE POVERTY MEASURES IN THE U.S. AND NEW YORK CITY ................................ 27 4.1PovertyRatesbyAgeGroup ............................................................................................ 27 4.2ExtremePoverty ............................................................................................................... 28 4.3ChangesintheSPMandCEOPovertyRates,2009-2011 ............................................... 28

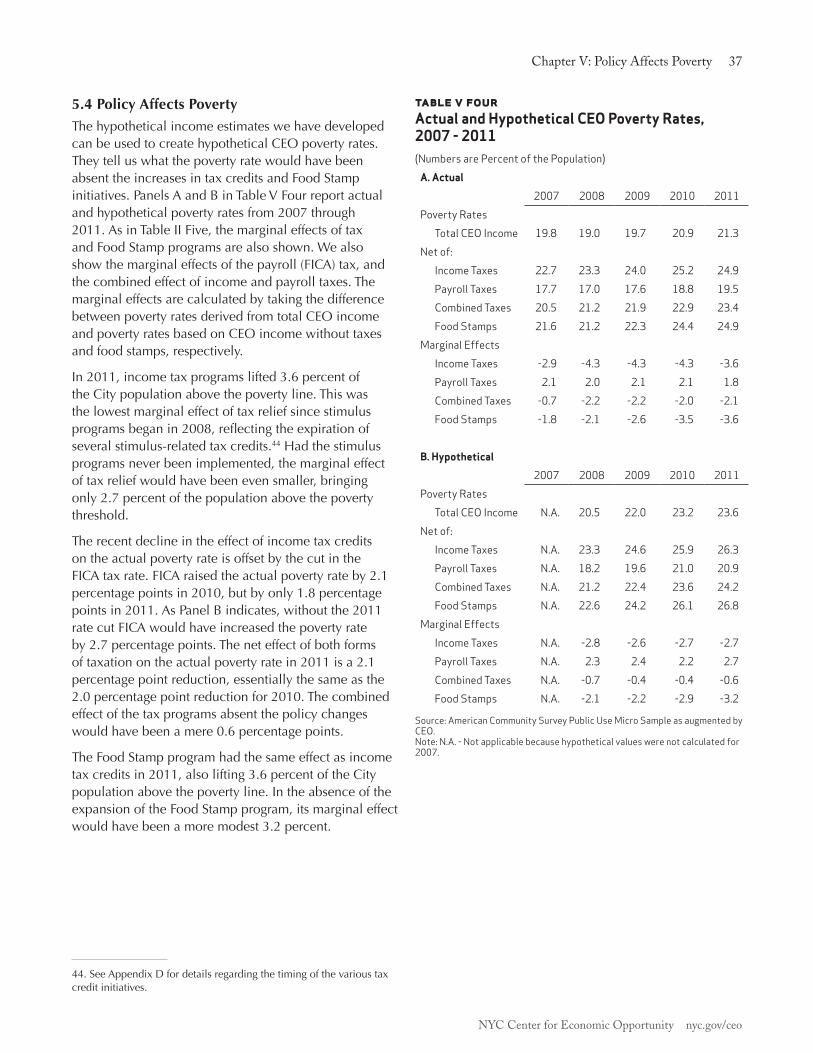

V. POLICY AFFECTS POVERTY ....................................................................................................... 31 5.1MeasuringtheEffectsofNewandExpandedTaxCredits .................................................. 31 5.2MeasuringtheEffectofChangesinFoodStampPolicy .................................................... 34 5.3PolicyAffectsIncome ...................................................................................................... 35 5.4PolicyAffectsPoverty ....................................................................................................... 37

VI: IN CONCLUSION ..................................................................................................................... 39

APPENDIX A: THE POVERTY UNIVERSE AND UNIT OF ANALYSIS ............................................... 41 APPENDIXB:DERIVINGAPOVERTYTHRESHOLDFORNEWYORKCITY .................................. 43 APPENDIX C: ADJUSTMENT FOR HOUSING STATUS .................................................................. 47 APPENDIX D: THE CEO TAX MODEL ............................................................................................. 56 APPENDIX E: ESTIMATING THE VALUE OF NUTRITIONAL ASSISTANCE ...................................... 64 APPENDIXF:ESTIMATINGTHEVALUEOFHEAPBENEFITS ......................................................... 76 APPENDIX G: WORK-RELATED EXPENSES .................................................................................... 78 APPENDIX H: MEDICAL OUT-OF-POCKET EXPENDITURES .......................................................... 84 APPENDIX I: ACCURACY OF THE DATA ........................................................................................ 88

Preface & Acknowledgments i

NYC Center for Economic Opportunity nyc.gov/ceo

PrefaCe and aCknowledgmenTs

In2006,NewYorkCityMayorMichaelR.BloombergconvenedaCommissiononEconomicOpportunity,directingittocraftinnovativeapproachestoreducingpovertyintheCity.TheCommissionmemberstookabroadviewoftheirmandate.What,theyasked,arewetryingtoreduce?Howdoweknowifwearesucceeding?Toanswerquestionslikethese,policymakersneedbroadsocialindicators.TheCommissionerssoonlearnedwhatsocialscientistshaveknownfordecades:thenation’sfifty-year-oldmeasureofpovertynolongerprovidesusefulinformation.Inthe1960s,thepovertymeasurewasafocalpointforthenation’sgrowingconcernaboutpoverty.Overthedecades,societyevolvedandpolicieshaveshifted,buttheofficialpovertymeasureremainsfrozenintime.Asaresult,ithassteadilylostcredibilityandusefulness.TheCommissionersconcludedthat,alongwithnewprograms,theCityneededtodevelopanewmeasureofpoverty.MayorBloombergembracedtheCommission’srecommendationandthedevelopmentofanimprovedmeasureofpovertybecameaprojectoftheorganizationhecreatedtoimplementtheCommission’srecommendations,theNewYorkCityCenterforEconomicOpportunity(CEO).

TherehasbeennoshortageofproposalsforimprovingthewayAmericacountsitspoor.Themostinfluentialofthesewasdeveloped,attherequestofCongress,bytheNationalAcademyofSciences(NAS).AlthoughtheNAS’sproposalwasissuedin1995,neithertheFederalnoranyotherbranchofgovernmenthadadoptedthisapproachuntil2008whenCEOreleaseditsfirstworkingpaperonpovertyinNewYorkCity.Thisstudy–ourfifth–continuesourpracticeofissuingannualupdatesofourmeasure.

Wehavenotbeenaloneinthiswork.Inrecentyears,CEOhasbeenjoinedbyotherstateandlocalpovertymeasurementinitiatives.Todate,NAS-style,state-levelpovertymeasureshavebeendevelopedforNewYork,Connecticut,Georgia,Illinois,Massachusetts,Minnesota,andWisconsin,alongwiththecity(andmetroarea)ofPhiladelphia.Alltheseprojectshavebeenenormouslyhelpfultoourwork.WehavebenefitedfromthewisdomofGeorgeFalcoandJihyunShinattheNewYorkStateOfficeofTemporaryandDisabilityAssistance;MarkSternoftheUniversityofPennsylvania;LindaGiannarelli,LauraWheaton,andSheilaZedlewskiattheUrbanInstitute;andJuliaIsaacsandTimothySmeedingattheUniversityofWisconsin’sInstituteforResearchonPoverty.

In2011,theU.S.BureauoftheCensusbeganreleasingannualreportsonpovertyintheUnitedStatesusinganewSupplementalPovertyMeasure,whichisalsobasedontheNASrecommendations.ToenhancethecommensurabilityofourworkwiththenewFederalmeasure,CEOrevisedsomeelementsofourapproach.OurcolleaguesattheCensusBureau,DavidJohnson,KathleenShort,andTrudiRenwick,aswellasThesiaGarnerattheBureauofLaborStatistics–friendsoftheCEOprojectsinceitsinception–havebeenparticularlyhelpfulinthiswork.

Fromtheearlieststagesofoureffort,wehavebenefitedfromopportunitiestopresentourworktootherscholarsandpolicypractitioners.TheBrookingsInstitutionCenteronChildrenandFamilieshostedanumberofmeetings,someatCEO’srequest,wheremanyofthenation’sleadingpovertyexpertsnotonlysharedtheirwork,butofferedusadviceforimprovingourmeasure.WeneedtorecognizethegenerosityofRonHaskins,theCenter’sCo-Director,aswellasthewisdomofthosewhohaveattendedtheseevents.CEOhasalsopresentedourworkatanumberofconferences,includingannualmeetingsoftheAssociationforPublicPolicyandManagement,theNationalAssociationforWelfareResearchandStatistics,theAmericanStatisticalAssociation,theInternationalAssociationforResearchinIncomeandWealth,andtheAdministrationforChildrenandFamilies’WelfareResearchandEvaluationConference.ThankstoagrantfromtheRIDGECenterforNationalFoodandNutritionAssistanceResearchattheUniversityofWisconsin’sInstituteforResearchonPoverty,wewereabletopresentourworkonvaluingFoodStampbenefitstoexpertsinthisfield.Inthecourseofallthiswehaveamassedaconsiderabledebt.Inadditiontothosementionedabove,wewishtoacknowledgeJessicaBanthin,RichardBavier,DavidBetson,RebeccaBlank,GaryBurtless,ConstanceCitro,SharonO’Donnell,IrvGarfinkel,MarkGreenberg,AmyO’Hara,NathanHutto,JohnIceland,DottieRosenbaum,IsabelleSawhill,KarlScholz,ArlocSherman,SharonStern,JaneWaldfogel,andJamesZiliak.

Closertohome,VickyVirgin,demographicanalystatthePopulationDivisionofNewYorkCityDepartmentofCityPlanning,hasmadeimportantcontributionsthroughouttheproject.Shedeservesspecialthanks,asdoesDr.JosephSalvo,thePopulationDivision’sDirector.ManyothercolleaguesinCitygovernmenthavesharedtheirexpertiseaboutpublicpolicy,theCity’sadministrationofbenefitprograms,andagency-leveldata.SondraSanchez,DirectorofHEAPandTraceyThorne,DirectorofProgramandPolicyAnalysis,Office

NYC Center for Economic Opportunity nyc.gov/ceo

ii The CEO Poverty Measure, 2005 - 2011

ofEmergencyandInterventionServicesattheCity’sHumanResourcesAdministration,provideddataandinsightontheHomeEnergyAssistanceProgram;RobertDeschak,attheDepartmentofEducation’sOfficeofSchoolSupportServices,shareddataonschoolmeals;andJacksonP.Sekhobo,Director,EvaluationandAnalysisUnit,DivisionofNutrition,NewYorkStateDepartmentofHealth,provideddataonparticipationintheWICprogram.ThanksarealsoduetoRobertDoar,Commissioner;AngelaSheehan,DeputyCommissionerforEvaluationandResearch;andHildyDworkin,librarian,attheCity’sHumanResourcesAdministrationfortheircontinuedsupport.

Staffatothergovernmentagenciesthatalsoassistedusinclude:RamchalKaveeta,MetropolitanTransitAuthority;ToddGoldman,PortAuthorityofNewYorkandNewJersey;JessicaSemega,HousingandHouseholdEconomicStatisticsDivision,U.S.BureauoftheCensus;MahdiSundukchi,DemographicStatisticalMethodsDivision,U.S.BureauoftheCensus;andLyndaLaughlin,Social,EconomicandHousingStatisticsDivision,U.S.BureauoftheCensus.

OvertheyearswehavealsoamassedaconsiderabledebttopastandpresentCEOcolleagues,includingDavidBerman,AllegraBlackburn-Dwyer,CoreyChambliss,KateDempsey,PatrickHart,AnnelHernandez,CarsonHicks,SusanneJames,SineadKeegan,MosesMagali,CarmenGenao-Maria,EmmaOppenheim,ArturoReyes,DorickScarpelli,CarlUrness,JoshuaWheatley,andJeromeWhite.LastsummerwewerejoinedbystudentinternsNikhilGahlawatandMayaOrtiz.Wethankthemfortheirveryableassistance.AdebtofgratitudeisalsoowedtoKristinMisner,ChiefofStafftotheDeputyMayorforHealthandHumanServices.

ThisreportwasauthoredbyChristineD’Onofrio,Ph.D.,JohnKrampner,DanielScheer,andToddSeidel,alongwithmyself.Sinceitsinception,ourworkreliedontheleadershipofVeronicaWhite,CEO’sfoundingExecutiveDirector.Hercommitmenttothisprojectwassimplyindispensible.ThisyearwegratefullyacknowledgetheleadershipandsupportofKristinMorse,CEO’scurrentExecutiveDirector.WeextendourlastthankyoutoLindaGibbs,NewYorkCityDeputyMayorforHealthandHumanServices.Hercommitmenttothisprojecthasbeensteadfast,enthusiastic,andessential.

MarkLevitan,Ph.D. DirectorofPovertyResearch OnbehalfoftheNewYorkCityCenterforEconomicOpportunity

desi

gn: P

urpl

e Ga

te D

esig

n w

ww.

pur

pleg

ated

esig

n.co

m

Executive Summary iii

NYC Center for Economic Opportunity nyc.gov/ceo

exeCuTive summary

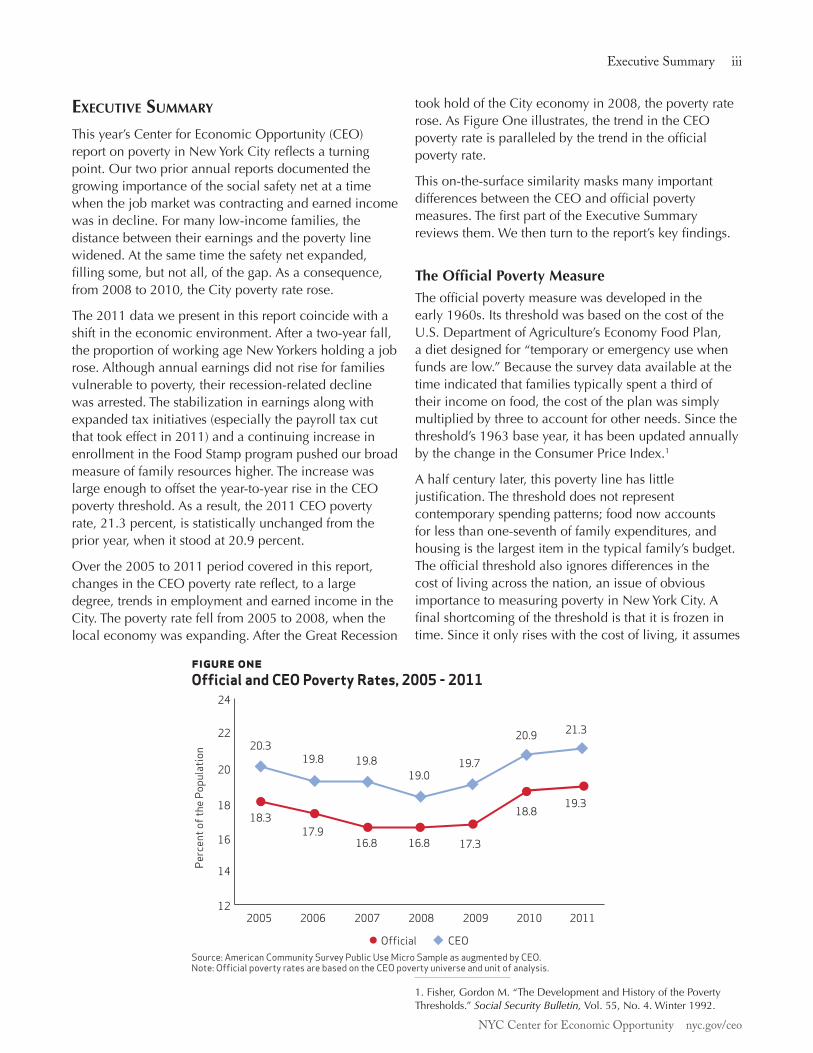

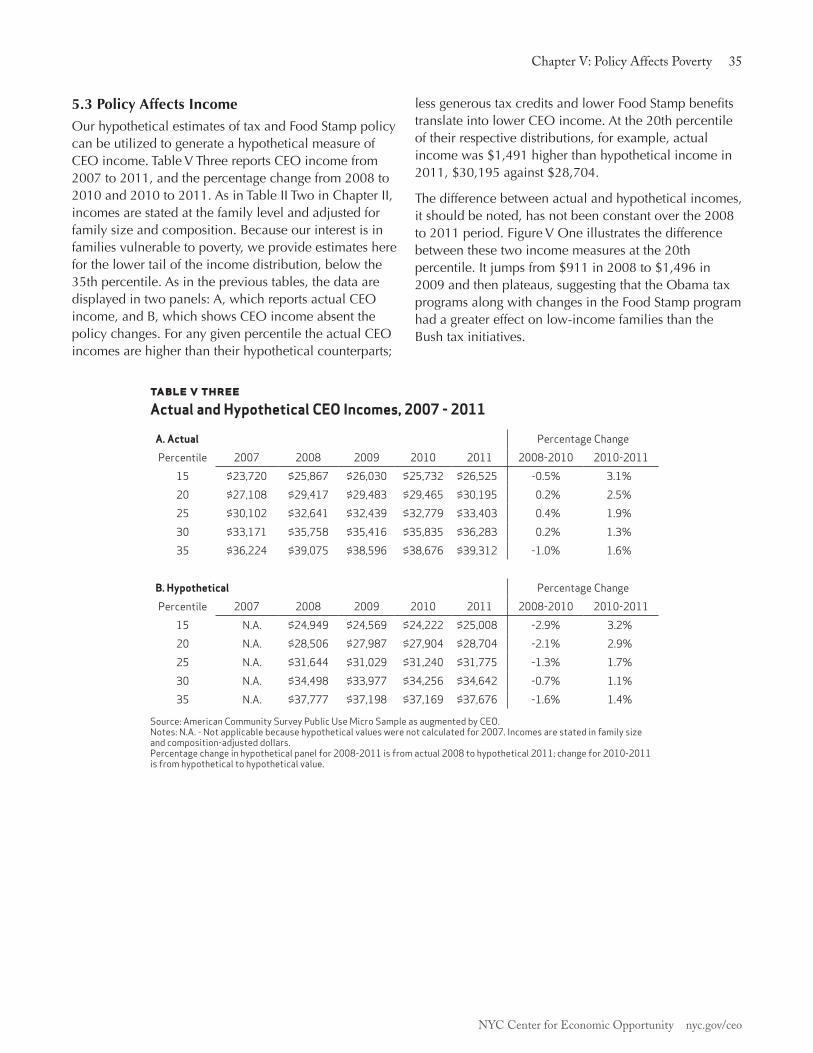

Thisyear’sCenterforEconomicOpportunity(CEO)reportonpovertyinNewYorkCityreflectsaturningpoint.Ourtwopriorannualreportsdocumentedthegrowingimportanceofthesocialsafetynetatatimewhenthejobmarketwascontractingandearnedincomewasindecline.Formanylow-incomefamilies,thedistancebetweentheirearningsandthepovertylinewidened.Atthesametimethesafetynetexpanded,fillingsome,butnotall,ofthegap.Asaconsequence,from2008to2010,theCitypovertyraterose.

The2011datawepresentinthisreportcoincidewithashiftintheeconomicenvironment.Afteratwo-yearfall,theproportionofworkingageNewYorkersholdingajobrose.Althoughannualearningsdidnotriseforfamiliesvulnerabletopoverty,theirrecession-relateddeclinewasarrested.Thestabilizationinearningsalongwithexpandedtaxinitiatives(especiallythepayrolltaxcutthattookeffectin2011)andacontinuingincreaseinenrollmentintheFoodStampprogrampushedourbroadmeasureoffamilyresourceshigher.Theincreasewaslargeenoughtooffsettheyear-to-yearriseintheCEOpovertythreshold.Asaresult,the2011CEOpovertyrate,21.3percent,isstatisticallyunchangedfromtheprioryear,whenitstoodat20.9percent.

Overthe2005to2011periodcoveredinthisreport,changesintheCEOpovertyratereflect,toalargedegree,trendsinemploymentandearnedincomeintheCity.Thepovertyratefellfrom2005to2008,whenthelocaleconomywasexpanding.AftertheGreatRecession

tookholdoftheCityeconomyin2008,thepovertyraterose.AsFigureOneillustrates,thetrendintheCEOpovertyrateisparalleledbythetrendintheofficialpovertyrate.

Thison-the-surfacesimilaritymasksmanyimportantdifferencesbetweentheCEOandofficialpovertymeasures.ThefirstpartoftheExecutiveSummaryreviewsthem.Wethenturntothereport’skeyfindings.

The Official Poverty MeasureTheofficialpovertymeasurewasdevelopedintheearly1960s.ItsthresholdwasbasedonthecostoftheU.S.DepartmentofAgriculture’sEconomyFoodPlan,adietdesignedfor“temporaryoremergencyusewhenfundsarelow.”Becausethesurveydataavailableatthetimeindicatedthatfamiliestypicallyspentathirdoftheirincomeonfood,thecostoftheplanwassimplymultipliedbythreetoaccountforotherneeds.Sincethethreshold’s1963baseyear,ithasbeenupdatedannuallybythechangeintheConsumerPriceIndex.1

Ahalfcenturylater,thispovertylinehaslittlejustification.Thethresholddoesnotrepresentcontemporaryspendingpatterns;foodnowaccountsforlessthanone-seventhoffamilyexpenditures,andhousingisthelargestiteminthetypicalfamily’sbudget.Theofficialthresholdalsoignoresdifferencesinthecostoflivingacrossthenation,anissueofobviousimportancetomeasuringpovertyinNewYorkCity.Afinalshortcomingofthethresholdisthatitisfrozenintime.Sinceitonlyriseswiththecostofliving,itassumes

1.Fisher,GordonM.“TheDevelopmentandHistoryofthePovertyThresholds.”Social Security Bulletin, Vol.55,No.4.Winter1992.

figure oneOfficial and CEO Poverty Rates, 2005 - 2011

Source: American Community Survey Public Use Micro Sample as augmented by CEO. Note: Official poverty rates are based on the CEO poverty universe and unit of analysis.

Perc

ent o

f the

Pop

ulat

ion

2005 2006 2007 2008 2009 2010 2011

Official CEO

12

14

16

18

20

22

24

18.317.9

16.8 16.8 17.3

18.819.3

20.9 21.3

19.719.0

19.819.820.3

NYC Center for Economic Opportunity nyc.gov/ceo

iv The CEO Poverty Measure, 2005 - 2011

thatastandardoflivingthatdefinedpovertyintheearly1960sremainsappropriate,despiteadvancesinthenation’sstandardoflivingsincethattime.

Theofficialmeasure’sdefinitionoftheresourcesthatarecomparedagainstthethresholdispre-taxcash.Thisincludeswages,salaries,andearningsfromself-employment;incomefrominterest,dividends,andrents;andsomeofwhatfamiliesreceivefrompublicprograms,iftheytaketheformofcash.Thus,paymentsfromUnemploymentInsurance,SocialSecurity,SupplementalSecurityIncome,andpublicassistanceareincludedintheofficialresourcemeasure.

Giventhedataavailableandthepoliciesinplaceatthetime,thiswasnotanunreasonabledefinition.Butinrecentyearsanincreasingshareofwhatgovernmentprogramsdotosupportlow-incomefamiliestakestheformoftaxcredits(suchastheEarnedIncomeTaxCredit)andin-kindbenefits(suchasFoodStamps).

Measures of Poverty

Official: The current official poverty measure was de-veloped in the early 1960s. It consists of a set of thresh-olds that were based on the cost of a minimum diet at that time. A family’s pre-tax cash income is compared against the threshold to determine whether its mem-bers are poor.

NAS: At the request of Congress, the National Academy of Sciences issued a set of recommendations for an im-proved poverty measure in 1995. Although the proposal did not become the new official poverty measure, staff at the Census Bureau, Bureau of Labor Statistics, and other researchers created a body of research that was based on the NAS proposal.

SPM: In March 2010 the Obama Administration an-nounced that the Census Bureau, in cooperation with the Bureau of Labor Statistics, would create a Supple-mental Poverty Measure based on the NAS recommen-dations, subsequent research, and a set of guidelines proposed by an Interagency Working Group. The first report on poverty using this measure was issued by the Census Bureau in November 2011.

CEO: The Center for Economic Opportunity released its first report on poverty in New York City in August 2008. CEO’s poverty measure is based on the NAS recommen-dations and the guidelines from the SPM Interagency Working Group.

Ifpolicymakersorthepublicwanttoknowhowthese programsaffectpoverty,theofficialmeasurecannotprovideananswer.

The National Academy of Sciences’ AlternativeDissatisfactionwiththeofficialmeasurepromptedCongresstorequestastudybytheNationalAcademyofSciences(NAS).TheNAS’srecommendationsforanimprovedmeasurewereissuedin1995.2Theysparkedfurtherresearchandgarneredwidespreadsupportamongpovertyexperts.3TheNAStookaconsiderablydifferentapproachtoboththethresholdandresourcesideofthepovertymeasure.Itspovertythresholdreflectstheneedforclothing,shelter,andutilitiesaswellasfood.Itisestablishedbyselectingasub-groupoffamiliesasreferencefamilies,4calculatingtheirspendingontheseitems,andthenchoosingapointintheresultingexpendituredistribution.5Asmallmultiplierisappliedtoaccountformiscellaneousexpensessuchaspersonalcare,householdsupplies,andnon-work-relatedtransportation.Thethresholdisupdatedeachyearbythechangeinthelevelofthisspending.Thisconnectsthethresholdtothegrowthinlivingstandards.Infurthercontrasttotheofficialmeasure,theNASproposedthatthepovertylinebeadjustedtoreflectgeographicdifferencesinhousingcosts.

Ontheresourceside,theNASmeasureisdesignedtoaccountfortheflowofincomeandin-kindbenefitsthatafamilycanusetomeettheneedsrepresentedinthethreshold.Thiscreatesamuchmoreinclusivemeasureofincomethanpre-taxcash.Thetaxsystemandthecash-equivalentvalueofin-kindbenefitsforfoodandhousingcreateimportantadditionstofamilyresources.Butfamiliesalsohavenon-discretionaryexpensesthatreducetheincomeavailabletomeettheirotherneeds.Theseincludethecostofchildcare,commutingtowork,andmedicalcarethatmustbepaidforoutofpocket.Thisnon-discretionaryspendingisaccountedforasdeductionsfromincome.

2.Citro,ConstanceF.andRobertT.Michael(eds).Measuring Poverty: A New Approach.Washington,DC:NationalAcademyPress.1995.3.MuchoftheresearchinspiredbytheNASreportisavailableat:www.census.gov/hhes/povmeas/methodology/nas/index.html4.TheNASreferencefamiliesarethosecomposedoftwoadultsandtwochildren.Thethresholdforthisfamilyisthenscaledforfamiliesofdifferentsizesandcompositions.SeeAppendixB.5.TheNASsuggestedthatthispointliebetweenthe30th and35thpercentile.CitroandMichael,p.106.

Executive Summary v

NYC Center for Economic Opportunity nyc.gov/ceo

CEO’s Adoption of the NAS/SPM MethodLikeCEO’smeasure,theCensusBureau’snewSupplementalPovertyMeasure(SPM)isalsoshapedbytheNASrecommendationsalongwithasetofguidelinesprovidedbyanInteragencyTechnicalWorkingGroupinMarch2010.6TheguidelinesincorporatedworkbyresearchersattheCensusBureau,BureauofLaborStatistics,andotherssubsequenttotheoriginalNASreport.Manyoftheserecommendationsarereflectedinourmeasure.

CEObasesourNewYorkCity-specificpovertythresholdontheU.S.-widethresholddevelopedfortheSPM.Weadjustthenational-levelthresholdtoaccountfortherelativelyhighcostofhousinginNewYorkCitybyapplyingtheratiooftheNewYorkCitytotheU.S.-wideFairMarketRentforatwo-bedroomapartmenttothehousingportionofthethreshold.7In2011,ourpovertylineforthetwo-adult,two-childfamilycomesto$30,949.WerefertothisNewYorkCity-specificthresholdastheCEOpovertythreshold.The2011officialpovertythresholdforthecorrespondingfamilywas$22,811.

Poverty Thresholds

Official: The official threshold was developed in the early 1960s and was based on the cost of a minimum diet at that time. It is updated each year by the change in consumer prices. It is uniform across the United States.

CEO: The CEO poverty threshold is a New York City-specific threshold derived from the U.S.-wide thresh-old developed for the Federal Supplemental Poverty Measure. The threshold is based on what families spend on basic necessities: food, clothing, shelter, and utilities. It is adjusted to reflect the variation in housing costs across the United States.

6. Observations from the Interagency Technical Working Group on Developing a Supplemental Poverty Measure.March2010.Availableat:www.census.gov/hhes/www/poverty/SPM_TWGObservations.pdf7.DetailsofthecalculationaregiveninAppendixB.

Measuring Income

Official Income: The official poverty measure’s defini-tion of family resources is pre-tax cash. This includes income from all sources such as earnings, interest, and government transfer payments that take the form of cash. Thus, Social Security benefits are included in this measure, but the value of in-kind benefits such as Food Stamps or tax credits such as the Earned Income Tax Credit are not counted.

CEO Income: Based on the NAS recommendations, CEO income includes all the elements of pre-tax cash plus the effect of income and payroll taxes, and the value of in-kind nutritional and housing assistance. Non-discre-tionary spending for commuting to work, childcare, and out-of-pocket medical care are accounted for as deduc-tions from income.

Obviously,ifthisweretheonlychangeCEOhadmadetothepovertymeasure,itwouldleadtoapovertyratehigherthantheofficialrate.But,asdescribedabove,CEOalsousesafardifferentmeasureofincometocompareagainstthepovertythreshold.Althoughourmeasureincludessubtractionsaswellasadditionstoresources,CEOincomeishigherthanpre-taxcashincomeatthelowerrungsoftheincomeladder.Atthe20thpercentile,forexample,CEOincomewas$30,195in2011.Thecorrespondingfigureforpre-taxcashwasonly$22,944.Thus,ifamorecompleteaccountofresourceshadbeentheonlychangewehadmadetothepovertymeasure,theCEOpovertyratewouldfallbelowtheofficialmeasure.FigureTwoillustratesofficialandCEOincomes,thresholds,andpovertyratesfor2011.TheeffectofthehigherCEOthreshold(35.7percentabovetheofficial)outweighstheeffectofCEO’smorecompletedefinitionofresources(whichis31.6percenthigher,atthe20thpercentile,thantheofficialresourcemeasure),resultinginahigherpovertyrate.In2011,theCEOpovertyratestoodat21.3percentwhiletheofficialratewas19.3percent,a2.0percentagepointdifference.

NYC Center for Economic Opportunity nyc.gov/ceo

vi The CEO Poverty Measure, 2005 - 2011

figure twoOfficial and CEO Thresholds, Incomes, and Poverty Rates, 2011

Source: U.S. Bureau of the Census and American Community Survey Public Use Micro Sample as augmented by CEO. Notes: Incomes are measured at the 20th percentile and stated in family size and composition-adjusted dollars. Official poverty rates are based on the CEO poverty universe and unit of analysis.

Tomeasuretheresourcesavailabletoafamilytomeettheneedsrepresentedbythethreshold,ourpovertymeasureemploysthePublicUseMicroSamplefromtheCensusBureau’sAmericanCommunitySurvey(ACS)asitsprincipaldataset.Theadvantagesofthissurveyforlocalpovertymeasurementarenumerous.TheACSisdesignedtoprovidemeasuresofsocio-economicconditionsonanannualbasisinstatesandlargerlocalities.ItoffersarobustsampleforNewYorkCity(roughly25,000households)andcontainsessentialinformationabouthouseholdcomposition,familyrelationships,andcashincomefromavarietyofsources.

But,asnotedearlier,theNAS-recommendedpovertymeasuregreatlyexpandsthescopeofresourcesthatmustbemeasuredinordertodeterminewhetherafamilyispoor.Unfortunately,theACSprovidesonlysomeoftheinformationneededtoestimatetheseadditionalresources.CEOhasdevelopedavarietyofmodelsthatestimatetheeffectoftaxation,nutritionalandhousingassistance,work-relatedexpenses,andmedicalout-of-pocketexpendituresontotalfamilyresourcesandpovertystatus.Wereferencetheresultingdatasetasthe“AmericanCommunitySurveyPublicUseMicroSampleasaugmentedbyCEO”andwerefertoourestimateoffamilyresourcesas“CEOincome.”

This Year’s ReportThefocusofthisyear’sCEOworkingpaperisonpovertyinNewYorkCitysince2008,aperiodofrecession,thenlingeringweakness,and,mostrecently,recoveryintheeconomy.From2008to2010,labormarketindicatorsforCityresidentspointedsouth.Adecliningproportionoftheworkingagepopulationwasemployed.AsFigureThreeillustrates,theshareofNewYorkers18through64yearsofagewhowereholdingajobatthetimetheyweresurveyedpeakedin2008at70.8percent.Thatproportiondeclinedto66.4percentby2010.Butin2011,itroseto67.0percent.

figure threeEmployment/Population Ratios, 2005 - 2011

Source: American Community Survey Public Use Micro Sample.

Becausepovertystatusisdeterminedbyannualincome,employmentoverthecourseofayearisaparticularlysalientlabormarketindicator.FigureFourshowsthattheshareoftheworkingagepopulationwithsteadywork,definedas50ormoreweeksintheprior12months,declinedfrom59.8percentin2008to56.3percentin2010,whiletheproportionofthepopulationthathadnoworkatallgrewfrom23.5percentin2008to27.3percent2010.Thisindicatorstabilizedin2011.

$22,811

OfficialThresholds Incomes Poverty Rates

$22,944

$30,945

CEO Official CEO Official CEO

$30,195

19.3% 21.3%

Perc

ent o

f 18

thro

ugh

64-Y

ear-

Olds

2005 2006 2007 2008 2009 2010

67.068.7 69.3

70.868.2

66.4

2011

67.0

50

55

60

65

70

75

Executive Summary vii

NYC Center for Economic Opportunity nyc.gov/ceo

figure fourWeeks Worked in Prior 12 Months, 2008 - 2011

Source: American Community Survey Public Use Micro Sample.

The2008to2010declineinweeksworkedisreflectedinmeasuresofearnings.TableOnereportsperfamilyearningsforthosefamilieswhoseearningswouldputthemneartheCEOpovertythreshold(betweenthe25thand40thpercentileoftheearningsdistribution).Thedeclinesrangefrom14.6percentto11.2percentfrom2008to2010.Thedeclineinearningsendsin2011,alsoechoingthepatterninweeksworked.

Thejobmarketplaysanimportant roleinyear-to-yearchangesintheCEOpovertyrate.Butitseffecttakesplacewithinthebroadscopeofourmeasureoffamilyresourcesandthecontextofpublicpoliciesintendedtobolsterfamilyincomes.Inadditiontoearnings,low-incomefamilies’abilitytomeettheirneedsisdeterminedbypublicbenefitprograms.Overthelastseveraldecadestherehasbeenanimportantshiftinthecompositionoftheseprograms,especiallyforthenon-elderlypopulation.Asnotedabove,asmallerproportionofmeans-testedassistancetakestheformofcashpayments,suchaspublicassistance,whilealargerproportioniscomposedoftaxcreditsandin-kindbenefits.ThetrendhasbeenreinforcedbytheBushandObamaAdministrations’economicstimulusprograms.Ataxprogram,theEconomicRecoveryRebate,wasakeyfeatureoftheBushAdministration’sresponsetotheonsetoftherecession.NewandexpandedtaxcreditprogramsandanincreaseinFoodStampbenefitlevelswereimportantelementsinPresidentObama’sAmericanRecoveryandRebuildingAct.

TheexpandingroleoftaxcreditsandtheFoodStampprogramareafocusoftheanalyticalsectionsofthisyear’sreport.Inordertoidentifytheimpactoftherecentpolicychanges,wecomparetrendsinCEOincomeandpovertyratesagainsthypotheticalestimates,toidentifywhatwouldhaveoccurredintheabsenceofthenewtaxandFoodStampinitiatives.

0

20

40

60

80

100

Perc

ent o

f 18

thro

ugh

64-Y

ear-

Olds

23.5

2008

59.8

16.7

2009 2010

24.6 27.3

16.5

56.3

2011

27.0

16.6

56.3

17.1

58.3

At Least 50 Less Than 50 No Weeks

table oneAnnual Family-Level Earned Income, 2008 - 2011

Year Percentage ChangePercentile 2008 2009 2010 2011 2008-2010 2010-2011

25 $18,701 $17,945 $16,122 $16,029 -13.8% -0.6%

30 $25,460 $24,226 $21,741 $21,970 -14.6% 1.1%

35 $31,815 $30,506 $27,818 $27,682 -12.6% -0.5%

40 $38,218 $36,707 $33,922 $33,301 -11.2% -1.8% Source: American Community Survey Public Use Micro Sample as augmented by CEO. Notes: Earnings are stated in family size and composition-adjusted dollars. They are not adjusted for inflation. Persons in families with no earnings are included.

NYC Center for Economic Opportunity nyc.gov/ceo

viii The CEO Poverty Measure, 2005 - 2011

Key Findings Inthecontextofalabormarketthatisrecoveringfromatwo-yearslump,wefindthat:

Afterrisingfrom19.0percentin2008to20.9percentin2010,theCEOpovertyratestoodat21.3percentin2011,statisticallyunchangedfromtheprioryear.Anequivalent8officialpovertyratefollowedasimilarpath,risingfrom16.8percentin2008to18.8percentin2010.Theofficialpovertyratein2011was19.3percent,alsostatisticallyunchangedfrom2010.

AlthoughtheCEOpovertyrateexceedstheofficialrateineachyearforwhichwehavedata,theCEOmethodologyfindsthatasmallerproportionoftheCity’spopulationislivinginextremepoverty–below50percentofthepovertythreshold–thandoestheofficialmethod(5.6percentcomparedto7.9percentin2011).Bybothmeasures,extremepovertyrosefrom2008to2010.Theproportionofthepopulationlivingbelow50percentoftherespectivethresholdswasunchangedfrom2010to2011.SeeFigureFive.

ThetrendinCEOpovertyratesbydemographiccharacteristicssuchasage,familystatus(i.e.,numberofparentsinthefamilyunit),andboroughgenerallyfollowstheriseintheCitywidepovertyratefrom2008to2010anditsstatisticalstabilityfrom2010to2011.Comparing2011to2008,wefindstatisticallysignificantincreasesinthepovertyrateforchildrenunder18andworkingageadults(SeeFigureSix);Non-HispanicWhites,Asians,andHispanics(SeeFigureSeven);andCitizensbyBirthandNon-Citizens(SeeFigureEight).Therearefewstatisticallymeaningfulchangesinpovertyratesfrom2010to2011.Animportantexceptionisthedeclineinthepovertyrateforpersonslivinginasingle-headedfamilywithchildren,from33.4percentin2010to30.9percentin2011.SeeFigureNine.

8.Tomakecomparisonsmoreuseful,theofficialpovertyratesgiveninthereportarebasedontheCEOpovertyuniverseandunitofanalysis.SeeTextBoxFourinChapterIfordetails.

figure fivePercent of the Population in Extreme Poverty, 2008 - 2011

Source: American Community Survey Public Use Micro Sample as augmented by CEO. Note: Official poverty rates are based on the CEO poverty universe and unit of analysis.

0

1

2

3

4

5

6

7

8

6.97.3

7.7 7.9

Official CEO

5.14.8

5.6 5.6

Perc

ent o

f the

Pop

ulat

ion

2008 2009 2010 2011

Executive Summary ix

NYC Center for Economic Opportunity nyc.gov/ceo

figure six CEO Poverty Rates by Age Group, 2008, 2010, and 2011

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

figure sevenCEO Poverty Rates by Race/Ethnicity, 2008, 2010, and 2011

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

0

5

10

15

20

25

30

23.1

Under 18

25.6 24.7

18 through 64 65 and Older

16.919.3 19.9

22.7 22.421.1

Perc

ent o

f the

Pop

ulat

ion

2008 2010 2011

13.215.4 15.4

Non-Hispanic White

Non-Hispanic Black

Non-Hispanic Asian

Hispanic, Any Race

Perc

ent o

f the

Pop

ulat

ion

2008 2010 2011

0

5

10

15

20

25

30

20.8 21.5 21.422.4

26.1 26.5

23.524.6 25.3

NYC Center for Economic Opportunity nyc.gov/ceo

x The CEO Poverty Measure, 2005 - 2011

figure eightCEO Poverty Rates by Nativity/Citizenship, 2008, 2010, and 2011

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

figure nineCEO Poverty Rates for Families with Children, 2008, 2010, and 2011

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

0

5

10

15

20

25

30

17.7

Citizen by Birth

19.9 19.7

Naturalized Citizen Not a Citizen

18.2 17.819.1

24.7

28.927.5

Perc

ent o

f the

Pop

ulat

ion

2008 2010 2011

0

5

10

15

20

25

30

35

20.3

All Families with Children

23.0 22.4

Two-Parent Families

Single-Parent Families

14.4

17.8 17.8

31.1 30.933.4

Perc

ent o

f the

Pop

ulat

ion

2008 2010 2011

Executive Summary xi

NYC Center for Economic Opportunity nyc.gov/ceo

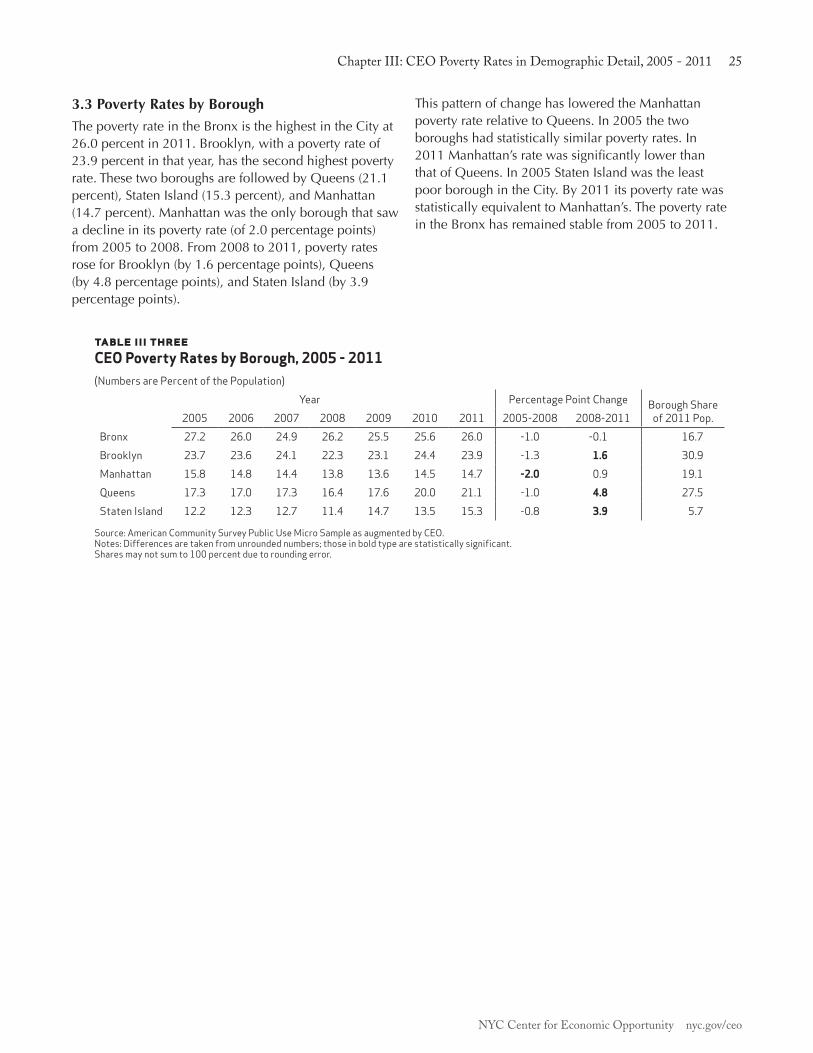

From2008to2011,povertyratesincreasedinthreeoutoffiveoftheCity’sboroughs:Brooklyn(by1.6percentagepointsto23.9percent),Queens(by4.8percentagepointsto21.1percent),andStatenIsland(by3.9percentagepointsto15.3percent).SeeFigureTen.

ThepatterninpovertyratesfortheUnitedStatesbasedonthenewFederalSupplementalPovertyMeasureresemblestheCEOpatternforNewYorkCity.Acrosstheentirepopulation,thetwoNAS-basedpovertymeasuresfindahigherincidenceofpovertythandotheofficialmeasures.IntheU.S.,theratein2011is16.1percentasopposedto15.1percent.InNewYorkCity,thetwopovertyrateswere21.3percentand19.3percentinthatyear.Becausetheycountthevalueofnon-cashassistance,however,boththeSPMandCEOmeasuresofpovertyamongchildrenarelowerthanchildpovertyratesbasedontheofficialmethod:18.1percentcomparedto22.3percentforthenation;24.7percentratherthan28.7percentfortheCity.SeeFigureEleven.

26.2 25.6 26.0

22.324.4 23.9

13.8 14.5 14.716.4

20.021.1

11.413.5

15.3

Bronx Brooklyn Manhattan Queens Staten Island

Perc

ent o

f the

Pop

ulat

ion

2008 2010 2011

0

5

10

15

20

25

30

figure tenCEO Poverty Rates by Borough, 2008, 2010, and 2011

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

NYC Center for Economic Opportunity nyc.gov/ceo

xii The CEO Poverty Measure, 2005 - 2011

Theanalyticalsectionsofthisyear’sreportfocusontrendsinthreefamily-levelmeasuresofincome:earnings,pre-taxcash,andCEOincome.Comparisonsindicatetheextenttowhichtherecession-relateddeclinesinearnedincomewereoffsetbycashandnon-cashbenefitprograms.Wefindthat:

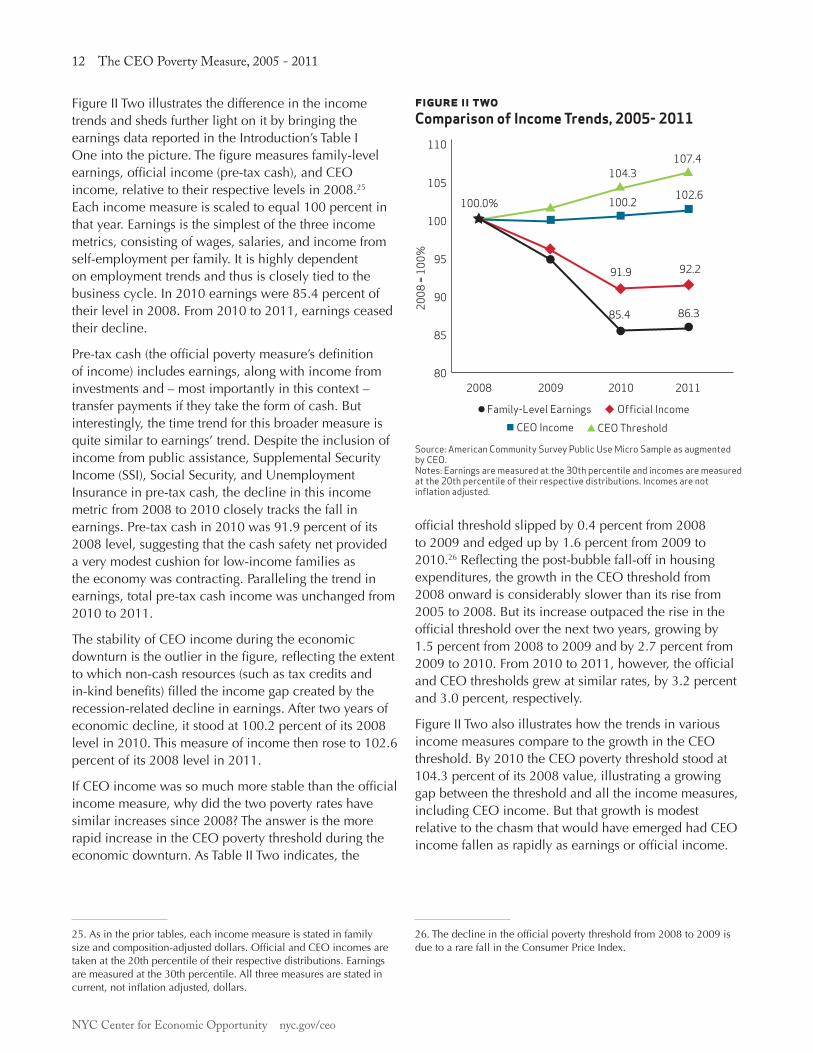

In2010,earnedincomestoodatonly85.4percentofits2008level.Pre-taxcash,themeasureofincomeusedintheofficialpovertymeasure,equaled91.9percentofits2008levelinthatyear.Bycontrast,CEOincomedidnotdeclinefrom2008to2010.From2010to2011,bothearningsandpre-taxcashwerestatisticallyunchanged,whileCEOincomeroseto102.6percentofits2008level.ThedramaticallystrongerperformanceoftheincomemeasureusedtodeterminetheCEOpovertyratecomparedtotheincomemeasureusedtodeterminetheofficialpovertyrateistheresultofCEO’sinclusionofnon-cashsocialsafetynetprogramsthatareuncountedintheofficialpovertymeasure.SeeFigureTwelve.

figure twelve Comparison of Income Trends, 2008 - 2011

Source: American Community Survey Public Use Micro Sample as augmented by CEO. Notes: Earnings are measured at the 30th percentile and incomes are measured at the 20th percentile of their respective distributions. Incomes are not inflation-adjusted.

Official

United States

SPM

15.1

22.3

13.7

8.7

16.118.1

15.5 15.1

Perc

ent o

f the

Pop

ulat

ion

0

10

15

5

20

25

15

5

25

30

Total Under 18 18 - 64 65 and Older

New York City

Official CEO

19.3

28.7

17.5

21.3

24.7

19.922.4

Perc

ent o

f the

Pop

ulat

ion

0

10

20

30

16.5

figure elevenComparison of Poverty Rates in the U.S. and NYC, 2011

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

Official IncomeFamily-Level Earnings CEO Income

2008

= 10

0%

100.0% 100.2%

91.9%

85.4%

102.6%

92.2%

86.3%

2008 2009 2010 201180

95

100

105

90

85

110

Executive Summary xiii

NYC Center for Economic Opportunity nyc.gov/ceo

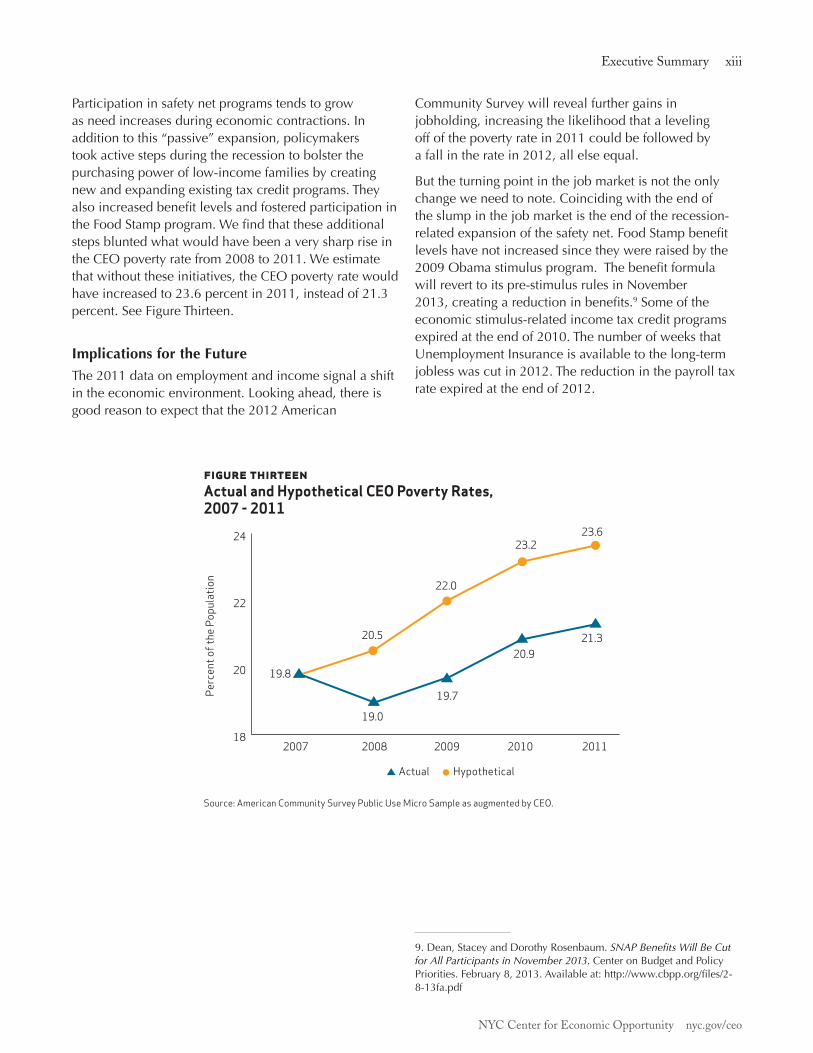

Participationinsafetynetprogramstendstogrowasneedincreasesduringeconomiccontractions.Inadditiontothis“passive”expansion,policymakerstookactivestepsduringtherecessiontobolsterthepurchasingpoweroflow-incomefamiliesbycreatingnewandexpandingexistingtaxcreditprograms.TheyalsoincreasedbenefitlevelsandfosteredparticipationintheFoodStampprogram.WefindthattheseadditionalstepsbluntedwhatwouldhavebeenaverysharpriseintheCEOpovertyratefrom2008to2011.Weestimatethatwithouttheseinitiatives,theCEOpovertyratewouldhaveincreasedto23.6percentin2011,insteadof21.3percent.SeeFigureThirteen.

Implications for the FutureThe2011dataonemploymentandincomesignalashiftintheeconomicenvironment.Lookingahead,thereisgoodreasontoexpectthatthe2012American

CommunitySurveywillrevealfurthergainsinjobholding,increasingthelikelihoodthataleveling offofthepovertyratein2011couldbefollowedby afallintheratein2012,allelseequal.

Buttheturningpointinthejobmarketisnottheonlychangeweneedtonote.Coincidingwiththeendoftheslumpinthejobmarketistheendoftherecession-relatedexpansionofthesafetynet.FoodStampbenefitlevelshavenotincreasedsincetheywereraisedbythe2009Obamastimulusprogram.Thebenefitformulawillreverttoitspre-stimulusrulesinNovember2013,creatingareductioninbenefits.9Someoftheeconomicstimulus-relatedincometaxcreditprogramsexpiredattheendof2010.ThenumberofweeksthatUnemploymentInsuranceisavailabletothelong-termjoblesswascutin2012.Thereductioninthepayrolltaxrateexpiredattheendof2012.

9.Dean,StaceyandDorothyRosenbaum.SNAP Benefits Will Be Cut for All Participants in November 2013.CenteronBudgetandPolicyPriorities.February8,2013.Availableat:http://www.cbpp.org/files/2-8-13fa.pdf

figure thirteen Actual and Hypothetical CEO Poverty Rates, 2007 - 2011

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

20082007 2009 2010 2011

HypotheticalActual

Perc

ent o

f the

Pop

ulat

ion

19.7

20.5

19.0

22.0

23.2

20.9

23.6

21.3

18

20

22

24

19.8

NYC Center for Economic Opportunity nyc.gov/ceo

xiv The CEO Poverty Measure, 2005 - 2011

Thesequester–thecutsinFederalgovernmentspendingthatbeganonMarch1,2013–alsothreatensprogramsimportanttolow-incomeAmericans.UnemploymentInsurancebenefitlevelsforthelong-termjoblesswhoarereceivingFederally-fundedbenefitscouldfallby11percent.10TheCenteronBudgetandPolicyPrioritiesestimatesthatbetween575,000and750,000womenandchildrenwillbedeniedWICbenefitsbytheendofthecurrentFederalfiscalyear.11FundingforFederalhousingprograms,thebackboneofthemeans-testedhousingassistancesovitaltolow-incomeNewYorkers,willalsosufferstiffreductions.12

Insum,thedynamicthatspurred,butalsolimited,therecentriseinpoverty–decliningearningsbufferedbyanexpandedsafetynet–isshifting.InthecontextofpoliticalstalemateinWashingtonandapolicyenvironmentthatisfocusedonreducingtheFederalbudgetdeficit,progressinreducingpovertywilldependtoalargedegreeonarisingeconomictideliftingenoughboats.ProgresswillalsorestonthecontinuedeffortsbyCitypolicymakerstobuild“on-ramps”toanexpandingjobmarketforthosegroupsofNewYorkersthatprosperitysooftenleavesbehind.

10. The Sequester’s Devastating Impact on Families of Unemployed Workers and the Struggling Unemployment Insurance System.NationalEmploymentLawProject.BriefingPaper.February27,2013.Availableat:http://www.nelp.org/page/-/UI/2013/Briefing-Paper-Sequester-Unemployment-Insurance.pdf?nocdn=111.Neuberger,ZoeandBobGreenstein.The Impact of the Sequester on WIC: 575,000 to 750,000 Eligible Low-Income Women and Children at Nutritional Risk Could Be Denied Benefits.CenteronBudgetandPolicyPriorities.March5,2013.Availableat:www.cbpp.org/files/2-26-13fa.pdf12. Estimated Cuts in Federal Housing Assistance and Community Development Programs Due to Sequestration, 2013.CenteronBudgetandPolicyPriorities.March5,2013.Availableat:www.cbpp.org/files/1-28-13hous.pdf

Chapter I: Introduction 1

NYC Center for Economic Opportunity nyc.gov/ceo

ChaPTer i: inTroduCTion

Ithasbeenahalfcenturysincethedevelopmentofthecurrentofficialmeasureofpoverty.Intheearly1960sthemeasurerepresentedanimportantadvance,servingasafocalpointforthepublic’sgrowingconcernaboutpovertyinAmerica.Butoverthedecades,discussionsaboutpovertyincreasinglyincludedcriticismofhowpoorlyitwasbeingmeasured.Societywasevolvingandpublicpolicyhadshifted,yettheCensusBureauwasstillmeasuringpovertyasifnothinghadchanged.

DissatisfactionwiththeofficialmeasurepromptedCongresstorequestastudybytheNationalAcademyofSciences(NAS).TheNAS’srecommendations,issuedin1995,sparkedfurtherresearchandgarneredwidespreadsupportamongpovertyexperts.13However,neithertheFederalnoranystateorlocalgovernmenthadadoptedtheNASapproachuntilCEO’sinitialreportonpovertyinNewYorkCityinAugust2008.14Thisyear’sstudy,ourfourthannualreport,continuesourpracticeofissuingyearlyupdatesofourmeasure.Usingthemostrecentdataavailable,itprovidespovertyratesfor2005 through2011.

Thisintroductorychaptersetsthecontextforourfindings.Itbeginswithanoverviewoftheofficialmeasureanditsweaknesses.Wethendescribeouralternative,whichisbasedontheNASrecommendationsandthedevelopmentofthenewFederalSupplementalPovertyMeasure(SPM),firstissuedinNovember2011.15 Thesecondpartoftheintroductionshiftsthediscussionfrommethodologytothelocaleconomy.Followingtherecessionandcontinuedweaknessinthelocaleconomyfrom2008to2010,thedatafor2011indicatesomeimprovementintheCity’sjobmarket.Theintroduction’sfinalsectionsummarizesthereport’sprincipalfindings.

1.1 The Official Poverty MeasureTheofficialmeasure’spovertythresholdwasdevelopedintheearly1960sandwasbasedonthecostofthe

13.Citro,ConstanceF.andRobertT.Michael(eds).Measuring Poverty: A New Approach.Washington,DC:NationalAcademyPress.1995.MuchoftheresearchinspiredbytheNASreportisavailableat:www.census.gov/hhes/povmeas/methodology/nas/index.html14.NewYorkCityCenterforEconomicOpportunity.The CEO Poverty Measure: A Working Paper by the New York City Center for Economic Opportunity.August2008.Availableat:www.nyc.gov/html/ceo/downloads/pdf/final_poverty_report.pdf15.U.S.BureauoftheCensus.The Research Supplemental Poverty Measure: 2010.November2011.Availableat:www.census.gov/hhes/povmeas/methodology/supplemental/research/Short_ResearchSPM2010.pdf

U.S.DepartmentofAgriculture’sEconomyFoodPlan,adietdesignedfor“temporaryoremergencyusewhenfundsarelow.”Becausethesurveydataavailableatthetimeindicatedthatfamiliestypicallyspentathirdoftheirincomeonfood,thecostoftheplanwassimplymultipliedbythreetoaccountforotherneeds.Sincethethreshold’s1963baseyear,ithasbeenupdatedannuallybythechangeintheConsumerPriceIndex.16

Ahalfcenturylater,thispovertylinehaslittlejustification.Thethresholddoesnotrepresentcontemporaryspendingpatterns;foodnowaccountsforlessthanone-seventhoffamilyexpenditures,andhousingisthelargestiteminthetypicalfamily’sbudget.Theofficialthresholdalsoignoresdifferencesinthecostoflivingacrossthenation,anissueofobviousimportancetomeasuringpovertyinNewYorkCity.Afinalshortcomingofthethresholdisthatitisfrozenintime.Sinceitonlyriseswiththecostofliving,itassumesthatastandardoflivingthatdefinedpovertyintheearly1960sremainsappropriate,despiteadvancesinthenation’sstandardoflivingsincethattime.

Theofficialmeasure’sdefinitionoftheresourcesthatarecomparedagainstthethresholdispre-taxcash.Thisincludeswages,salaries,andearningsfromself-employment;incomefrominterest,dividends,andrents;andsomeofwhatfamiliesreceivefrompublicprograms,iftheytaketheformofcash.Thus,paymentsfromUnemploymentInsurance,SocialSecurity,SupplementalSecurityIncome(SSI),andPublicAssistanceareincludedintheofficialresourcemeasure.

Giventhedataavailableandthepoliciesinplaceatthetime,thiswasnotanunreasonabledefinition.Butinrecentyearsanincreasingshareofwhatgovernmentdoestosupportlow-incomefamiliestakestheformoftaxcredits(suchastheEarnedIncomeTaxCredit)andin-kindbenefits(suchasFoodStamps).Ifpolicymakersorthepublicwanttoknowhowtheseprogramsaffectpoverty,theofficialmeasurecannotprovideananswer.

16.Fisher,GordonM.“TheDevelopmentandHistoryofthePovertyThresholds.”Social Security Bulletin,Vol.55,No.4.Winter1992.

NYC Center for Economic Opportunity nyc.gov/ceo

2 The CEO Poverty Measure, 2005 - 2011

Measures of Poverty

Official: The current official poverty measure was developed in the early 1960s. . It consists of a set of thresholds that were based on the cost of a minimum diet at that time. A family’s pre-tax cash income is compared against the threshold to determine whether its members are poor.

NAS: At the request of Congress, the National Academy of Sciences issued a set of recommendations for an improved poverty measure in 1995. The NAS threshold represents the need for clothing, shelter, and utilities as well as food. The NAS income measure accounts for taxation and the value of in-kind benefits.

SPM: In March 2010 the Obama Administration an-nounced that the Census Bureau, in cooperation with the Bureau of Labor Statistics, would create a Supplemental Poverty Measure based on the NAS recommendations, subsequent research, and a set of guidelines proposed by an Interagency Technical Working Group. The first report on poverty using this measure was issued by the Census Bureau in November 2011.

CEO: The Center for Economic Opportunity released its first report on poverty in New York City in August 2008. CEO’s poverty measure is largely based on the NAS rec-ommendations, with modifications based on the guide-lines from the Interagency Technical Working Group.

1.2 The National Academy of Sciences’ AlternativeNAS-basedmethodstakeaconsiderablydifferentapproachtoboththethresholdandresourcesideofthepovertymeasure.Thepovertythresholdreflectstheneedforclothing,shelter,andutilities,aswellasfood.Itisestablishedbyselectingasub-groupoffamiliesasreferencefamilies,17calculatingtheirspendingontheseitems,andthenchoosingapointintheresultingexpendituredistribution.18Asmallmultiplierisappliedtoaccountformiscellaneousexpensessuchaspersonalcare,householdsupplies,andnon-work-relatedtransportation.Thethresholdisupdatedeachyearbythechangeinthelevelofthisspending.Thisconnects

17.ThereferencefamilyproposedbytheNASiscomposedoftwoadultsandtwochildren.Thethresholdforthisfamilyisthenscaledforfamiliesofdifferentsizesandcompositions.SeeAppendixB.18.TheNASsuggestedthatthispointliebetweenthe30thand35thpercentileofthedistribution.CitroandMichael,p.106.

thethresholdtothegrowthinlivingstandards.Infurthercontrasttotheofficialmeasure,theNAS-stylepovertylineisalsoadjustedtoreflectgeographicdifferencesinhousingcosts.

Ontheresourceside,theNAS-basedmeasureisdesignedtoaccountfortheflowofincomeandin-kindbenefitsthatafamilycanusetomeettheneedsrepresentedinthethreshold.Thiscreatesamuchmoreinclusivemeasureofincomethanpre-taxcash.Thetaxsystemandthecash-equivalentvalueofin-kindbenefitsforfoodandhousingareimportantadditionstofamilyresources.Butfamiliesalsohavenon-discretionaryexpensesthatreducetheincomeavailabletomeettheirotherneeds.Theseincludethecostofcommutingtowork,childcare,andmedicalcarethatmustbepaidforoutofpocket.Thisspendingisaccountedforasdeductionsfromincome.

1.3 The Supplemental Poverty MeasureTheCensusBureau’sSupplementalPovertyMeasureisshapedbytheNASrecommendationsandasetofguidelinesprovidedbyanInteragencyTechnicalWorkingGroup(ITWG)inMarch2010.19Revisionstothe1995NASrecommendationscenteronthethresholdsideofthepovertymeasure.Themostimportantoftheseare:

1.Anexpansionofthetypeoffamilyunitwhoseexpendituresdeterminethepovertythreshold,from two-adultfamilieswithtwochildrentoallfamilieswithtwochildren.

2.Useofafive-year,ratherthanthree-year,movingaverageofexpendituredatatoupdatethepovertythresholdovertime.

3.Creationofseparatethresholdsbasedonhousingstatus:whetherthefamilyownsitshomewithamortgage;owns,butisfreeandclearofamortgage;orrents.

1.4 CEO’s Adoption of the NAS/SPM MethodCEOhasfollowedthefirsttwooftheserevisionstotheNASrecommendations.However,wedonotfollowtheSPM’screationofthresholdsthatvarybyhousingstatus.Weaccountforalldifferencesinhousingstatus– includingresidenceinrent-regulatedapartmentsandparticipationinmeans-testedhousingassistance

19. Observations from the Interagency Technical Working Group on Developing a Supplemental Poverty Measure.March2010.Availableat:www.census.gov/hhes/www/poverty/SPM_TWGObservations.pdf

Chapter I: Introduction 3

NYC Center for Economic Opportunity nyc.gov/ceo

programs–ontheincomesideofthepovertymeasure.20 ByapplyingtheratioofNewYorkCitytoU.S.-wideFairMarketRentforatwo-bedroomapartmenttothehousingportionofthethreshold,weadjustthenational-levelSPMthreshold(regardlessofhousingstatus)toaccountfortherelativelyhighcostofhousinginNewYorkCity.In2011,ourpovertylineforthetwo-adult,two-childfamilycomesto$30,949.WerefertothisNewYorkCity-specificthresholdastheCEOpovertythreshold.(SeeAppendixB.)

Poverty Thresholds

Official: The official threshold was developed in the early 1960s and was based on the cost of a minimum diet at that time. It is updated each year by the change in consumer prices. It is uniform across the United States.

CEO: The CEO poverty threshold is a New York City-specific threshold derived from the U.S.-wide thresh-old developed for the Federal Supplemental Poverty Measure. The threshold is based on what families spend on basic necessities: food, clothing, shelter, and utilities. It is adjusted to reflect the variation in housing costs across the United States.

Tomeasuretheresourcesavailabletoafamilytomeettheneedsrepresentedbythethreshold,ourpovertymeasureemploysthePublicUseMicroSamplefromtheCensusBureau’sAmericanCommunitySurvey(ACS)asitsprincipaldataset.Theadvantagesofthissurveyforlocalpovertymeasurementarenumerous.TheACSisdesignedtoprovidemeasuresofsocioeconomicconditionsonanannualbasisinstatesandlargerlocalities.ItoffersarobustsampleforNewYorkCity(roughly25,000households)andcontainsessentialinformationabouthouseholdcomposition,familyrelationships,andcashincomefromavarietyofsources.

But,asnotedearlier,theNAS-recommendedpovertymeasuregreatlyexpandsthescopeofresourcesthatmustbemeasuredinordertodeterminewhetherafamilyispoor.Unfortunately,theACSprovidesonlysomeoftheinformationneededtoestimatetheadditionalresourcesrequiredbytheNASmeasure.CEOhasdevelopedavarietyofmodelsthatestimatetheeffect

20.TherationaleforthisdecisionisprovidedinAppendixBoflastyear’sreport.See:The CEO Poverty Measure, 2005 – 2010: A Working Paper by the NYC Center for Economic Opportunity.Availableat:www.nyc.gov/html/ceo/downloads/pdf/CEO_Poverty_Measure_April_16.pdf

oftaxation,nutritionalandhousingassistance,work-relatedexpenses,andmedicalout-of-pocketexpendituresontotalfamilyresourcesandpovertystatus.Wereferencetheresultingdatasetasthe“AmericanCommunitySurveyPublicUseMicroSampleasaugmentedbyCEO”andwerefertoourestimateoffamilyresourcesas“CEOincome.”

Measuring Income

Official Income: The official poverty measure’s definition of family resources is pre-tax cash. This includes income from sources such as wages and salaries, as well as government transfer payments, provided that they take the form of cash. Thus, Social Security benefits are included in this measure, but the value of in-kind benefits, like Food Stamps or tax credits such as the Earned Income Tax Credit, are not counted.

CEO Income: Based on the NAS recommendations, CEO income includes all the elements of pre-tax cash plus the effect of income and payroll taxes, as well as the value of in-kind nutritional and housing assistance. Non-discretionary spending for commuting to work, childcare, and out-of-pocket medical care are deductions from income.

Belowisabriefdescriptionofhowthenon-pre-taxcashincomeitemsareestimated.Moredetailsontheseproceduresandanyrevisionswehavemadetothemsinceourlastreportcanbefoundintheappendices.

Housing Adjustment:ThehighcostofhousingmakesNewYorkCityanexpensiveplacetolive.TheCEOpovertythreshold,wenotedabove,isadjustedtoreflectthatreality.ButsomeNewYorkersdonotneedtospendasmuchtosecureadequatehousingasthehigherthresholdimplies.ManyoftheCity’slow-incomefamiliesliveinpublichousingorreceiveahousingsubsidy,suchasaSection8housingvoucher.AlargeproportionofNewYork’srentersliveinrent-regulatedapartments.Somehomeownershavepaidofftheirmortgagesandowntheirhomesfreeandclear.Wemakeanupwardadjustmenttothesefamilies’incomestoreflecttheseadvantages.

TheACSdoesnotprovidedataonhousingprogramparticipation,however.TodeterminewhichhouseholdsintheACSwouldbeparticipantsinrentalsubsidyorregulationprograms,wematchhouseholdsintheCensus

NYC Center for Economic Opportunity nyc.gov/ceo

4 The CEO Poverty Measure, 2005 - 2011

Bureau’sNewYorkCityHousingandVacancy Surveywithhousehold-levelrecordsintheACS. (SeeAppendixC.)

Taxation:CEOhasdevelopedataxmodelthatcreatestaxfilingunitswithintheACShouseholds;computestheiradjustedgrossincome,taxableincome,andtaxliability;andthenestimatesnetincometaxesafternon-refundableandrefundablecreditsareapplied.ThemodeltakesaccountofFederal,State,andCityincometaxprograms,includingallthecreditsthataredesignedtoaidlow-incomefilers.ThemodelalsoincludestheeffectoftheFederalpayrolltaxforSocialSecurityandMedicare(FICA).(SeeAppendixD.)

Nutritional Assistance:WeestimatetheeffectofFoodStamps,21theNationalSchoolLunchprogram,theSchoolBreakfastProgram,andtheSupplementaryNutritionProgramforWomen,Infants,andChildren(WIC).ToestimateFoodStampbenefits,wemakeuseofNewYorkCityHumanResourcesAdministrationFoodStamprecords,imputingFoodStampcasesto“FoodStampUnits”weconstructintheACSdata.WecounteachdollarofFoodStampbenefitsasadollaraddedtofamilyincome.

Thelikelihoodofparticipationintheschoolmealsprogramsiscalculatedbyaprobabilitymodel.ParticipationisassignedtoeligiblefamiliestoreplicatedataonmealsservedbytheCity’sDepartmentofEducation.WefollowtheCensusBureau’smethodforvaluingtheincomefromtheprogramsbyusingtheper-mealcostofthesubsidy.WeidentifyparticipantsintheWICprograminasimilarmanner,matchingenrollmentintheprogramtoparticipationrateestimatesbytheNewYorkStateDepartmentofHealth.BenefitsarecalculatedusingtheaveragebenefitlevelperparticipantcalculatedbytheU.S.DepartmentofAgriculture.(SeeAppendixE.)

Home Energy Assistance Program: TheHomeEnergyAssistanceProgram(HEAP)providesassistancetolow-incomehouseholdsthatoffsetstheirutilitycosts.InNewYorkCity,householdsthatreceivecashassistance,FoodStamps,orarecomposedofasinglepersonreceivingSSIbenefitsareautomaticallyenrolledintheprogram.Otherlow-incomehouseholdscanapplyforHEAP,butadministrativedatafromtheCity’sHumanResourcesAdministrationindicatethatnearlyallHEAPhouseholdscomeintotheprogramthroughtheirparticipationintheseotherbenefitprograms.WeidentifyHEAP-

21.TheFoodStampprogramwasrecentlyrenamedtheSupplementalNutritionalAssistanceProgram(SNAP).Sincetheprogramismorewidelyrecognizedbyitsformername,wecontinuetouseit.

receivinghouseholdsbytheirparticipationinpublicassistance,FoodStamps,andSSI,andthenaddtheappropriatebenefittotheirincome.For2011,wealsomakeuseofHEAPreceiptreportedintheHousingandVacancySurvey.(SeeAppendixF.)

Work-Related Expenses:Workersmusttraveltoandfromtheirjobs,andwetreatthecostofthattravelasanon-discretionaryexpense.Weestimatethenumberoftripsaworkerwillmakeperweekbasedontheirusualweeklyhours.WethencalculatethecostpertripusinginformationintheACSabouttheirmodeoftransportationandadministrativedata(suchassubwayfares).Weeklycommutingcostsarecomputedbymultiplyingthecostpertripbythetripsperweek.Annualcommutingcostsequalweeklycoststimesthenumberofweeksworkedoverthepast12months.

Familiesinwhichtheparentsareworkingmustoftenpayforthecareoftheiryoungchildren.Likethecostofcommuting,theCEOpovertymeasuretreatschildcareexpensesasanon-discretionaryreductioninincome.BecausetheAmericanCommunitySurveyprovidesnoinformationonchildcarespending,wehavecreatedanimputationmodelthatmatchestheweeklychildcareexpendituresreportedintheCensusBureau’sSurveyofIncomeandProgramParticipation(SIPP)toworkingfamilieswithchildrenintheACSdataset.Childcarecostsareonlycountediftheyareincurredinaweekinwhichtheparents(orthesingleparent)areatwork.Theyarecappedbytheearnedincomeofthelowestearningparent.(SeeAppendixG.)

Medical Out-of-Pocket Expenditures (MOOP):Thecostofmedicalcareisalsotreatedasanon-discretionaryexpensethatlimitstheabilityoffamiliestoattainthestandardoflivingrepresentedbythepovertythreshold.MOOPincludeshealthinsurancepremiums,co-pays,anddeductibles,aswellasthecostofmedicalservicesthatarenotcoveredbyinsurance.Inamannersimilartothatforchildcare,weuseanimputationmodeltomatchMOOPexpendituresbyfamiliesintheAgencyforHealthcareResearchandQuality’sMedicalExpenditurePanelSurveytofamiliesintheACSsample.(SeeAppendixH.)

FigureIOnesummarizesthediscussionthusfar,contrastinghowtheofficialandCEOpovertymeasuresestablishathresholdandaccountforfamilyresources.

Chapter I: Introduction 5

NYC Center for Economic Opportunity nyc.gov/ceo

1.5 Comparing Poverty RatesAsnotedabove,theCEOpovertythresholdforatwo-adult,two-childfamilyin2011was$30,949.Theofficialpovertylinefortheequivalentfamilywas$22,811inthatyear.Obviously,ifthisweretheonlychangeCEOhadmadetothepovertymeasure,itwouldleadtoapovertyrateabovetheofficialmeasure.But,asdescribedabove,CEOalsousesafardifferentmeasureofincometocompareagainstthepovertythreshold.Althoughourmeasureincludessubtractionsaswellasadditionstoresources,CEOincomeishigherthanpre-taxcashincomeatthelowerrungsoftheincomeladder.Atthe20thpercentile,forexample,CEOincomewas$30,195in2011.22Thecorrespondingfigureforpre-taxcashwasonly$22,944.Thus,ifamorecompleteaccountofresourceshadbeentheonlychangewemadetothepovertymeasure,theCEOpovertyratewouldfallbelowtheofficialmeasure.FigureITwoillustratesofficialandCEOincomes,thresholds,andpovertyratesfor2011.TheeffectofthehigherCEOthreshold(35.7percentabovetheofficial)outweighstheeffectofCEO’smorecompletedefinitionofresources(whichis31.6percenthigheratthe20thpercentilethantheofficialresourcemeasure),resultinginahigherpovertyrate.In2011,the

22.Throughoutthisworkingpaper,wereportincomeinfamilysizeandcomposition-adjusteddollars.Thismakestheincomemeasuresdirectlycomparabletothetwo-adult,two-childreferencefamilypovertythreshold.

CEOpovertyratestoodat21.3percentwhiletheofficialratewas19.3percent,a2.0percentagepointdifference.

Official Poverty Rates

The official poverty rates reported in this study differ from those provided by the Census Bureau. To make them more comparable to the CEO poverty rates, they are calculated using CEO’s poverty universe and unit of analysis. CEO excludes all members of the group quar-ters population and includes all members of the house-hold population in its universe of persons for whom a poverty status is determined. The CEO poverty unit of analysis expands the notion of the family unit to include more members of the household than just those related by blood, marriage, or adoption. Unmarried partners, for example, are treated as members of the family unit. Both these changes lower the poverty rate. In 2011, for example, the Census Bureau’s official poverty rate for New York City is 20.1 percent. The 2011 official poverty rate for the City that we report is 19.3 percent. See Ap-pendix A for further explanation.

figure i oneComparison of Poverty Measures

Official CEO

Threshold

Established in mid-1960s at three times the cost of “Economy Food Plan.”

Equal to 33rd percentile of family expenditures on food, clothing, shelter, and utilities, plus 20 percent more for miscellaneous needs.

Updated by change in Consumer Price Index.

Updated by change in expenditures for the items in the threshold.

No geographic adjustment. Inter-area adjustment based on differences in housing costs.

Resources

Total family pre-tax cash income (includes earnings, cash assistance, Social Security, etc.)

Total family after-tax income.

Include value of near-cash, in-kind benefits such as Food Stamps.Housing status adjustment.Subtract work-related expenses such as childcare and transportation costs.Subtract medical out-of-pocket expenditures.

NYC Center for Economic Opportunity nyc.gov/ceo

6 The CEO Poverty Measure, 2005 - 2011

figure i twoComparison of Thresholds, Income, and Poverty Rates, Official and CEO, 2011

Sources: U.S. Bureau of the Census and American Community Survey Public Use Micro Sample as augmented by CEO. Note: Incomes are measured at the 20th percentile and stated in family size and composition-adjusted dollars.

1.6 The New York City Labor MarketPovertyratesareinfluencedbytheeconomicenvironment.AfocusofthisreportisonthechangeintheCEOpovertyratesince2008.Thenationaleconomybegantocontractsharplyinearly2008,markingDecember2007asthepriorhighwatermarkintheU.S.-widebusinesscycle.23Thus,U.S.-levelstudiestrackingtheeffectsoftherecentrecessionandsubsequentperiodofsluggishemploymentgrowthhaveused2007astheirpointofcomparison.ButtherecessioncamelatertoNewYorkCity.Here,employmentdidnotbegintodeclineuntilthefallof2008,makingthatyearthelastforwhichannualindicatorsfindincreasesinemployment,earnings,andincome.

From2008to2010,labormarketindicatorsforCityresidentspointdecidedlysouth.Asmallerproportionoftheworkingagepopulationwasholdingajob.AsFigureIThreeillustrates,theemployment/populationratio–theshareofNewYorkers18through64yearsofagewhowereholdingajobatthetimetheyweresurveyed– peakedin2008at70.8percent.Thatproportiondeclinedto66.4percentby2010.Thedownward trend,however,isbrokenbythe2011uptickinthe ratio(of0.6percentagepoints)to67.0percent.

Becausepovertystatusisdeterminedbyannualincome,employmentoverthecourseofayearisaparticularlysalientlabormarketindicator.FigureIFourshowsthat theshareoftheworkingagepopulationwithsteady

23.TheNationalBureauforEconomicResearchdatesthestartoftherecentrecessionatDecember2007.

figure i threeEmployment/Population Ratios, 2005 - 2011

Source: American Community Survey Public Use Micro Sample.

work,definedas50ormoreweeksintheprior12months,declinedfrom59.8percentin2008to56.3percentin2010,whiletheproportionofthepopulationthathadnoworkatallgrewfrom23.5percentin2008to27.3percent2010.Thelatestdataidentifyalevelingoffofthedeclineinweeksworked;theshareoftheworkingagepopulationwithyear-roundwork,forexample,heldsteady.

figure i fourWeeks Worked in Prior 12 Months, 2008 - 2011

Source: American Community Survey Public Use Micro Sample.

Thetrendinweeksworkedisreflectedinmeasuresofearnings.TableIOnereportsearningsperfamilyforthosefamiliesthatareinthelowerhalfoftheearningsdistribution.Afterregisteringsharpdeclinesfrom2008to2009and2009to2010,thechangesinearningsfrom2010to2011aretoosmalltobestatisticallysignificant.

Perc

ent o

f 18

thro

ugh

64-Y

ear-

Olds

2005 2006 2007 2008 2009 2010

67.068.7 69.3

70.868.2

66.4

2011

67.0

50

55

60

65

70

75

0

20

40

60

80

100

Perc

ent o

f 18

thro

ugh

64-Y

ear-

Olds

23.5

2008

59.8

16.7

2009 2010

24.6 27.3

16.5

56.3

2011

27.0

16.6

56.3

17.1

58.3

At Least 50 Less Than 50 No Weeks

$22,811

OfficialThresholds Incomes Poverty Rates

$22,944

$30,945

CEO Official CEO Official CEO

$30,195

19.3% 21.3%

Chapter I: Introduction 7

NYC Center for Economic Opportunity nyc.gov/ceo

Thelabormarketdatasuggestthatthe2011ACSdescribesaneconomyataturningpoint.Thereisamodestuptickinemploymentlevelsandanendtotherecession-relateddeclineinweeksworkedandannualearnings.Thecontrastbetweentheimprovementintheemployment-populationratioandthestabilityofthelattertwoindicatorsislikelyduetothewayinwhichtheACSsampleiscollected.Theemployment-populationratioindicatesrespondents’statusatthetimetheyaresurveyed.Bycontrast,theweeksworkedandannualearningsdataareretrospective,lookingbackovertheprior12months.Thustheemployment-populationratioreflectsconditionsincalendaryear2011,whiletheannualindicatorsareasrepresentativeofconditionsin2010astheyareof2011.

Calendar Years and ACS Survey Years

The American Community Survey (ACS) is conducted as a rolling sample gathered over the course of a calendar year. Approximately one-twelfth of the total sample is collected in each month. Respondents are asked to pro-vide information on work experience and income during the 12 months prior to the time they are in the sample. Households that are surveyed in January of 2011, for example, would report their income for the 12 months of 2010, households that are surveyed in February 2011 would report their income for February 2010 through January 2011, and so on. Consequently, estimates for poverty rates derived from the 2011 ACS do not, strict-ly speaking, represent a 2011 poverty rate. Rather, it is a poverty rate derived from a survey that was fielded in 2011. Readers should bear in mind this difference as they interpret the findings in this report.

1.7 Key Findings in This Report Inthecontextofalabormarketthatisrecoveringfromatwoyearslump,wefindthat:

Afterrisingfrom19.0percentin2008to20.9percentin2010,theCEOpovertyratestoodat21.3percentin2011,statisticallyunchangedfromtheprioryear.Theofficialpovertyratefollowedasimilarpath,risingfrom16.8percentin2008to18.8percentin2010.Theofficialpovertyratein2011was19.3percent,alsostatisticallyunchangedfrom2010.

AlthoughtheCEOpovertyrateexceedstheofficialrateineachyearforwhichwehavedata,theCEOmethodologyfindsthatasmallerproportionoftheCity’spopulationislivinginextremepoverty–below50percentofthepovertythreshold–thandoestheofficialmethod(5.6percentcomparedto7.9percentin2011).

ThetrendinCEOpovertyratesbyindividualcharacteristicssuchasage,familystatus(i.e.,numberofparentsinthefamilyunit),andboroughgenerallyfollowstheriseintheCitywidepovertyratefrom2008to2010anditsstatisticalstabilityfrom2010to2011.Lookingoverthe2008to2011timeperiod,wefindstatisticallysignificantincreasesinthepovertyrateformales,females,childrenunder18,workingageadults,Non-HispanicWhites,Asians,andHispanics.Therearefewstatisticallymeaningfulchangesinpovertyratesfrom2010to2011.Animportantexceptionisthedeclineinthepovertyrateforpersonslivinginasingle-headedfamilywithchildren,from33.4percentin2010to30.9percentin2011.

From2008to2011,povertyratesincreasedinthreeoutoffiveoftheCity’sboroughs:Brooklyn(by1.6percentagepointsto23.9percent),Queens(by4.8

table i one Annual Family-Level Earned Income, 2008 - 2011

Year Percentage Change

Percentile 2008 2009 2010 2011 2008-2009 2009-2010 2008-201120 $12,311 $11,116 $9,673 $10,157 -9.7% -13.0% 5.0%25 $18,701 $17,945 $16,122 $16,029 -4.0% -10.2% -0.6%30 $25,460 $24,226 $21,741 $21,970 -4.8% -10.3% 1.1%35 $31,815 $30,506 $27,818 $27,682 -4.1% -8.8% -0.5%40 $38,218 $36,707 $33,922 $33,301 -4.0% -7.6% -1.8%45 $44,640 $43,131 $40,305 $40,322 -3.4% -6.6% 0.0%50 $51,271 $50,019 $46,505 $47,000 -2.4% -7.0% 1.1%

Source: American Community Survey Public Use Micro Sample as augmented by CEO. Notes: Earnings are stated in family size and composition-adjusted dollars. They are not adjusted for inflation. Persons in families with no earnings are included.

NYC Center for Economic Opportunity nyc.gov/ceo

8 The CEO Poverty Measure, 2005 - 2011

percentagepointsto21.1percent),andStatenIsland(by3.9percentagepointsto15.3percent).

ThepatterninpovertyratesfortheUnitedStatesbasedonthenewFederalSupplementalPovertyMeasureresemblestheCEOpatternforNewYorkCity.Acrosstheentirepopulation,thetwoNAS-basedpovertymeasuresfindahigherincidenceofpovertythandotheofficialmeasures.IntheU.S.,theratein2011is16.1percentasopposedto15.1percent.InNewYorkCity,thetwopovertyrateswere21.3percentand19.3percentinthatyear.Becausetheycountthevalueofnon-cashassistance,however,boththeSPMandCEOmeasuresofpovertyamongchildrenarelowerthanchildpovertyratesbasedontheofficialmethod:18.1percentcomparedto22.3percentforthenation;24.7percentratherthan28.7percentfortheCity.

Theanalyticalsectionsofthisyear’sreportfocusontrendsinthreefamily-levelmeasuresofincome:earnings,pre-taxcash,andCEOincome.Comparisonsindicatetheextenttowhichtherecession-relateddeclinesinearnedincomewereoffsetbycashandnon-cashbenefitprograms.Wefindthat:

In2010,earnedincomestoodatonly85.4percentofits2008level.Pre-taxcash,themeasureofincomeusedintheofficialpovertymeasure,equaled91.9percentofits2008levelin2010.Bycontrast,CEOincomedidnotdeclinefrom2008to2010.From2010to2011,earningsandpre-taxcashwerestatisticallyunchanged,whileCEOincomeroseby2.5percent.ThedramaticallystrongerperformanceoftheincomemeasureusedtodeterminetheCEOpovertyratecomparedtotheincomemeasureusedtodeterminetheofficialpovertyrateistheresultofCEO’sinclusionofnon-cashsocialsafetynetprogramsthatareuncountedintheofficialpovertymeasure.

Participationinsafetynetprogramstendstogrowasneedincreasesduringeconomiccontractions.Inadditiontothis“passive”expansion,policymakerstookactivestepsduringtherecessiontobolsterthepurchasingpoweroflow-incomefamiliesbycreatingnewandexpandingexistingtaxcreditprograms.TheyalsoincreasedbenefitlevelsandfosteredparticipationintheFoodStampprogram.WefindthattheseadditionalstepsbluntedwhatwouldhavebeenaverysharpriseintheCEOpovertyratefrom2008to2011.Weestimatethatwithoutthesesteps,theCEOpovertyratewouldhaveincreasedto23.6percentin2011,insteadof 21.3percent.

Theremainderofthisreportproceedsasfollows:ThenextchapterprovidesanoverviewoftrendsintheofficialandCEOpovertyratesfrom2005to2011.Inthatcontextwetracehowchangesinthethresholdandresourcesidesofthetwomeasuresdeterminedchangesintheirrespectivepovertyrates.ChapterIIIdetailspovertyratesinNewYorkCitybydemographiccharacteristic,familystatus,andborough.InChapterIV,wecompareofficialandCEOpovertyratesforNewYorkCitytoofficialandSupplementalPovertyMeasureratesfortheUnitedStates.Thefollowingchapterexploresthedegreetowhichcashandnon-cashpublicbenefitprogramsoffsetrecession-relateddeclinesinearnedincome.Thereport’sfinalchapterofferssomethoughtsontheimplicationsofourfindings.Asetofappendicesprovidemoredetailabouthowourpovertyestimates arecreated.

Chapter II: Poverty in New York City, 2005 - 2011 9

NYC Center for Economic Opportunity nyc.gov/ceo

ChaPTer ii: PoverTy in new york CiTy, 2005 - 2011TheIntroductionnotedthattheCEOpovertyrateexceedstheofficialratein2011.Indeed,itdoessoineachoftheyearsforwhichwehavecomparabledata.Thefocusofthischapter,however,isnotonthedifferentlevelsofpovertyderivedfromthetwoapproaches,butonhowandwhytheychangeovertime.TheofficialandCEOpovertyrateshavetakenparallelpathsduringtheseven-yeartimespancoveredbythisreport.From2005to2008,whentheCityeconomywasexpanding,thetwomeasuresregisterdeclinesofsimilarmagnitude.From2008to2011,theyrecordnearlyequalincreases.

ThischapterbeginswithanoverviewofhowandwhytheofficialandCEOpovertyrateschangedfrom2005to2011.Thesimilarityintheirtrendmasksimportantdifferencesbetweenthemeasures.From2008to2010,recession-relateddeclinesintheofficialmeasureofincome–pre-taxcash–aredramatic.Overthesametimeperiod,CEOincomewasremarkablystable.From2010to2011,officialincomewasunchangedwhileCEOincomerose.

Asecondsectioninthechapterexploresthedepthofpoverty,thedegreetowhichthepoorarelivingclosetoorfarbelowthepovertythreshold,aswellastheextentofnearpoverty(thedegreetowhichthepopulationthatresidesabovethepovertylineisuncomfortablyclosetoit).BecauseCEO’spovertymeasureprovidesamoreinclusivedefinitionofincome,itfindsasmallerproportionofthepopulationinextremepovertythandoestheofficialmeasure.Ontheotherhand,becauseeligibilityformeans-testedbenefitsendsandthevalueoftaxcreditsphaseoutasincomesrise,theCEOmeasurefindsalargershareofthepopulationlivinginnearpovertycomparedtotheofficialmeasure.

Thechapter’sthirdsectionexplorestherolethatnon-cashresourcesandnon-discretionaryexpensesplayintheCEOpovertymeasure.Wefindthatsince2008,taxprogramsandFoodStampshavebecomeincreasinglyimportantresourcesforlow-incomefamilies.Thisisnotsimplya“passive”outcomereflectinggreaterneedinabadeconomy.Itisalsoaresultofpolicychoices,atopicweexploreinChapterFive.

2.1 New York City Poverty Rates, 2005 - 2011ChangesintheofficialandCEOpovertyratefrom2005to2011moveintandemwiththelabormarketconditionsdescribedintheIntroduction.Povertydeclinesduringtheexpansionandrisesafter2008.FigureIIOneillustratestheofficialandCEOpovertyratesforNewYorkCityovertheseven-yeartimespancoveredinthisreport.

figure ii oneOfficial and CEO Poverty Rates, 2005 - 2011

Source: American Community Survey Public Use Micro Sample as augmented by CEO. Note: Official poverty rates are based on the CEO poverty universe and unit of analysis.

TableIIOneprovidestheseratesandadditionally,reportsdifferencesbetweenthemandchangesovertime.Asnotedabove,theCEOpovertyrateexceedstheofficialrateineachyear,adifferencethatrangesfrom2.0to3.0percentagepoints.However,changesinthetworatesovertimeareremarkablysimilar.WhiletheCityeconomywasgrowing,from2005to2008,theofficialpovertyratedeclinedby1.5percentagepointswhiletheCEOpovertyratefellby1.3percentagepoints.From2008to2010,asemploymentandearningscontracted,theofficialpovertyrateroseby2.1percentagepointsto18.8percent,andtheCEOpovertyrateclimbedby1.9percentagepoints,reaching20.9percentin2010.Themostrecentdatareflectastabilizinglabormarket;neitherpovertyrateexperiencedastatisticallysignificantchangefrom2010to2011.

Perc

ent o

f the

Pop

ulat

ion

2005 2006 2007 2008 2009 2010 2011

Official CEO

12

14

16

18

20

22

24

18.317.9

16.8 16.817.3

18.8

20.9

19.719.0

19.819.820.3

21.3

19.3

NYC Center for Economic Opportunity nyc.gov/ceo

10 The CEO Poverty Measure, 2005 - 2011

table ii oneOfficial and CEO Poverty Rates, 2005 - 2011(Numbers are Percent of the Population)

Year Official CEO

Percentage Point

Difference*2005 18.3 20.3 2.0

2006 17.9 19.8 1.9

2007 16.8 19.8 3.0

2008 16.8 19.0 2.3

2009 17.3 19.7 2.3

2010 18.8 20.9 2.1

2011 19.3 21.3 2.0

Percentage Point Change* Official CEO

2005-2008 -1.5 -1.3

2008-2010 2.1 1.9

2010-2011 0.5 0.4 *Differences and changes are measured in percentage points and are taken from unrounded numbers; those in bold type are statistically significant. Source: American Community Survey Public Use Micro Sample as augmented by CEO. Note: Official poverty rates are based on the CEO poverty universe and unit of analysis.

TableIITwoexploresthechangesinpovertyratesfromthevantagepointofchangesontheincomeandthresholdsideoftheirrespectivepovertymeasures.24 Asthetable’sPanelAreports,theofficialmeasureofincome–pre-taxcash–roseineachyearfrom2005 to2008,growingby17.7percentacrossthethree years.From2008to2010,pre-taxcashplungedby 8.1percent.Thismeasureofincomewasunchangedfrom2010to2011.

24.Tomaketheincomefiguresinthetablecomparabletothetwo-adult,two-childfamilypovertythresholds,theyareadjustedforfamilysizeandcomposition.Pre-taxcashandCEOincomesarebothreportedatthe20thpercentileoftheirrespectivedistributionsandbotharestatedincurrent,notinflationadjusted,dollars.

Changesinincometellastoryaboutpovertyrateswhentheyarecomparedagainstchangesinthepovertythreshold.Inthe2005to2008period,year-to-yearchangesinpre-taxincomeexceededthechangeintheofficialthreshold.From2006to2007,forexample,thismeasureofincomeroseby7.8percentwhiletheofficialthresholdedgedupby2.9percent.Asaconsequence,theofficialpovertyratedeclinedby1.2percentagepoints.Inthetwo-yearperiodfrom2008to2010,bycontrast,thesteepfallinincome(by8.1percent)wascoupledwithamodestriseintheofficialthreshold(by1.3percent),leadingtoariseintheofficialrateof2.1percentagepoints.The3.2percentclimbintheofficialthresholdfrom2010to2011outpacedtheessentiallyunchangedmeasureofincome,whichgeneratedanarithmeticriseintheofficialpovertyrateby0.5percentagepoints.Thisincrease,however,wasnotlargeenoughtobestatisticallysignificant.

PanelBinthetableprovidesthesameinformationforCEOincome,thresholds,andpovertyrates.Thepatternofrisingincomesandgrowthinthepovertythresholdsitdescribes,from2005to2008,mimicsthepatternfortheofficialmeasure.The20.9percentriseinCEOincomefrom2005to2008outpacedthe17.5percentincreaseintheCEOthreshold,leadingtoafallinthepovertyrateby1.3percentagepoints.

From2008to2010theCEOpovertyrateroseby1.9percentagepoints,roughlyequaltotheclimbintheofficialrate.Butthesimilarityinthetwopovertyrateincreasesmasksimportantdifferencesontheincomesideofthepovertymeasure.CEOincomeisremarkablymorestablethanofficialincome;itwasessentiallyunchangedfrom2008to2010.From2010to2011,itroseby2.5percent,asomewhatmoremodestpacethanthe3.0percentincreaseintheCEOthreshold.Thisresultedinasmall,butnotstatisticallysignificant,uptickintheCEOpovertyratefrom2010to2011.

Chapter II: Poverty in New York City, 2005 - 2011 11

NYC Center for Economic Opportunity nyc.gov/ceo

table ii two Income, Thresholds, and Poverty Rates, Official and CEO, 2005 - 2011

A. Official Income, Thresholds, and Poverty Rates

Income (Pre-tax Cash) Threshold Poverty Rate

Year LevelPercentage

Change* LevelPercentage

Change* Level

Percentage Point

Change*2005 $21,154 $19,806 18.3%

2006 $22,339 5.6% $20,444 3.2% 17.9% -0.3

2007 $24,083 7.8% $21,027 2.9% 16.8% -1.2

2008 $24,896 3.4% $21,834 3.8% 16.8% 0.0

2009 $24,087 -3.2% $21,756 -0.4% 17.3% 0.6

2010 $22,873 -5.0% $22,113 1.6% 18.8% 1.5

2011 $22,944 0.3% $22,811 3.2% 19.3% 0.5

Percentage Change

Percentage Change

Percentage Point Change

2005-2008 17.7% 10.2% -1.5

2008-2010 -8.1% 1.3% 2.1

B. CEO Income, Thresholds, and Poverty Rates

Income Threshold Poverty Rate

Year LevelPercentage

Change* LevelPercentage

Change* Level

Percentage Point

Change*2005 $24,332 $24,532 20.3%

2006 $25,711 5.7% $25,615 4.4% 19.8% -0.5

2007 $27,108 5.4% $26,979 5.3% 19.8% 0.0

2008 $29,417 8.5% $28,822 6.8% 19.0% -0.8

2009 $29,483 0.2% $29,265 1.5% 19.7% 0.6

2010 $29,465 -0.1% $30,055 2.7% 20.9% 1.2

2011 $30,195 2.5% $30,945 3.0% 21.3% 0.4

Percentage Change

Percentage Change

Percentage Point Change

2005-2008 20.9% 17.5% -1.3

2008-2010 0.2% 4.3% 1.9 *Change from prior year.Source: American Community Survey Public Use Micro Sample as augmented by CEO.Notes: Official poverty rates are based on the CEO poverty universe and unit of analysis.Incomes are measured at the 20th percentile and are stated in family size and composition-adjusted dollars. They are not adjusted for inflation. Differences in poverty rates are measured in percentage points and are taken from unrounded numbers; those in bold type are statistically significant..

NYC Center for Economic Opportunity nyc.gov/ceo