the commonwealth natural resources forum

TRANSCRIPT

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 2

Contents

Introduction 3

Opening address - Kamalesh Sharma, Commonwealth Secretary General 4

Welcome Message from Ransford Smith, Deputy Secretary General 7

Welcome Message from José Maurel, Director, Special Advisory Services Division 8

Purpose of the Forum, Daniel Dumas, Adviser and Head, Economic and Legal Section 9

Section 1: Creating a sustainable investment climate

Legal frameworks for sustainable investment in natural resources

Investor attraction and selection process: international industry perspective

Bid round process and practice – The Trinidad & Tobago Experience

Open discussion

10

12

13

16

Section 2: Effective risk allocation

Contract design and negotiation: companies’ perspective

Issues in contract negotiation

Negotiating Mineral Agreements: The Pakistan Experience

Dispute Prevention and Resolution

Open discussion

17

20

21

22

24

Section 3: Issues in taxation of natural resource projects

International benchmarking of fiscal regimes in natural resources

Issues in taxation of natural resource projects: an industry perspective

Fiscal issues and challenges in developing countries: the case of Belize

Open discussion

26

28

29

31

Section 4: Natural resource revenue administration and management

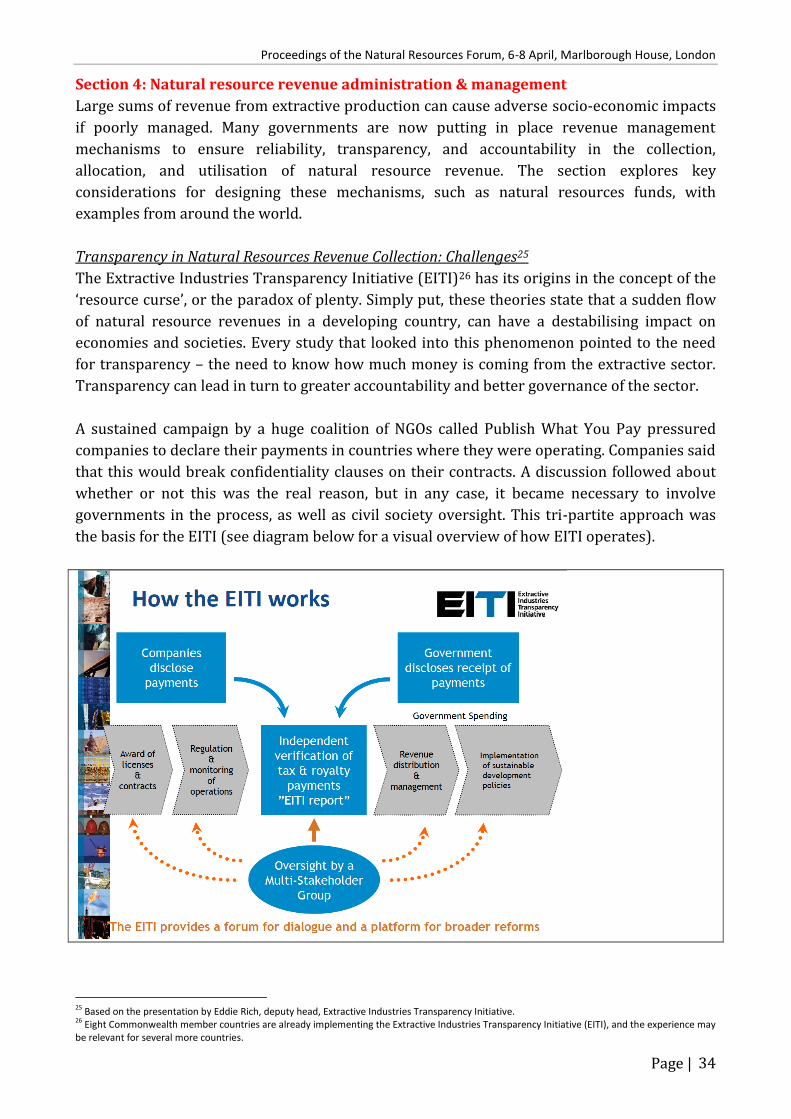

Transparency in Natural Resources Revenue Collection: Challenges

Natural resources revenue management

Transfer pricing, issues and challenges

Implementation challenges and lessons from Tanzania

Open discussion

33

34

37

39

40

Section 5: Managing environmental and social risks

Managing the environmental impacts of offshore oil and gas developments

Regulatory framework for environmental financial risk management

The demand for an ‘environmental protection bond’ and implications for

upstream petroleum licensing

Open discussion

43

45

48

48

Conclusions 50

List of acronyms 51

Appendix A – Participant feedback 53

Appendix B – About ELS 55

Appendix C – About this report 60

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 3

Introduction

The Natural Resources Forum was held between 6-8 April, 2011, at Marlborough House in

London. This was the first Forum of its type organised by the Economic and Legal Section of

the Commonwealth Secretariat’s Special Advisory Services Division. It provided an

opportunity for senior government officials from 18 countries across the Commonwealth to

meet and exchange ideas on the critically important subject of natural resource development.

It also provided an opportunity to share the work of the ELS team1 and show some of the

support available to member states. A fuller discussion of the objectives of the Forum follows

the welcoming messages.

The forum was organised around five half-day sessions, and this report follows the same

structure. This report is not a full, formal set of minutes of the proceedings. Rather it seeks to

capture the main points made by the presenters and a flavour of the rich discussions that

followed each section, reflecting the highly dynamic and rapidly evolving field of natural

resources management. A series of appendices provides further information about the

organisers. Electronic versions of all the presentations, together with further copies of this

report, are available from the ELS on request.

1 A full description of the ELS team, including biographies, is available in Appendix B.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 4

Opening address

Kamalesh Sharma, Commonwealth Secretary General

“Deputy Prime Minister, distinguished delegates, it is a great pleasure to welcome you all to

Marlborough House, and to the very first Commonwealth Secretariat Natural Resources

Forum.

We are a Commonwealth in microcosm: some 18 of our 54 member countries are here, from

virtually every continent. In conveying my appreciation to Daniel Dumas and my

Commonwealth Secretariat colleagues in the Special Advisory Services Division who have

organised this event, I also recognise other Commonwealth colleagues who will play their part

in their own areas of expertise, and applaud other international players from both public and

private sector who will bring us their own perspectives, and indeed four countries in

particular – Belize, Pakistan, Tanzania, and Trinidad & Tobago – who will share their

experience in detail.

This is another landmark for the Commonwealth Secretariat in its efforts – unfolding for over

thirty years now – to assist member countries to develop their natural resources sector, be it

in oil, gas or mining. At the core of what we discuss today is something supremely ethical. It

concerns our stewardship of the earth and our sharing of its bounty; it concerns not so much

what we inherit from our ancestors, as what we borrow from our children, and all

generations.

We humans and our complex, convoluted world are infinitesimally small, in the face of nature

and natural history. Commonwealth countries – like Zambia and Papua New Guinea – produce

a fifth of the world’s copper that we use to conduct heat and electricity in our houses, our cars.

But copper has been in use for thousands of years – smelted to make tools and artefacts.

The natural world is as old as time: we are the recent arrivals, who need to know where we

have come from, and when we might be headed – if only we knew.

So it is only right that this Commonwealth of values – for that, above all else, is what we are –

should bring both its wisdom and its wherewithal; its best policy and best practice – to so

fundamental a part of national and international life.

We sometimes forget that some of the more developed Commonwealth countries, such as

Canada and Australia, initially achieved their development and wealth to a large extent

because of the role that natural resources played in their economies. Indeed, if managed

properly, the natural resources sector is probably the only economic sector that can, on its

own, help lift a country out of underdevelopment in a relatively short period of time, if wisely

used.

For unfortunately the reverse situation is also equally significant. Mismanaged, revenues from

the natural resources sector can destabilise an economy, fuel conflict and war and corruption.

So, too, can they have a very negative impact on the environment, and create lasting damage

to human habitat.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 5

I have spoken of the sweep of history, and of resources that have been with us for centuries

and centuries. But so, too, must I speak of the start of the second decade of the 21st Century,

and challenging times in the field of natural resources. Oil and gas prices continue their

upward climb, as growth in demand for conventional energy sources outstrips growth in

supply of these finite commodities. In the case of the mining sector, after a huge drop in

demand for metals in 2008, prices have returned to their pre-recession levels, and demand

remains strong.

So the main objective of this Commonwealth Forum on Natural Resources is to provide an

avenue for our member Governments to discuss key issues in the development and

management of their natural resources.

The Secretariat has been providing assistance to Commonwealth member Governments in the

area of Natural Resources for almost 30 years. In visits to places like Namibia, Botswana,

Tanzania, Belize, I hear of our holistic work – not just advising on managing resources, but on

the legal and fiscal frameworks and rules which underpin successful resource management.

The Secretariat has gained significant experience and expertise, and has built a solid

reputation of “honest broker” in the field. We do so typically with hands-on assistance, on a

country-by-country basis, offering tailor-made expertise from the Economic & Legal team

within our Special Advisory Services Division.

But Natural Resource development is an area of ever-greater complexity, with more and more

at stake as the scale of potential social and economic impacts increase. It is an area tailor-

made for the Commonwealth, and its networks. Just as Commonwealth Trinidad and Tobago

can advise Commonwealth Ghana on stewarding its new-found resource of oil and gas, so can

Commonwealth countries in this room stand side by side in meeting their individual and

collective challenges.

My preface to your discussions is the simple observation that – from a global perspective – the

natural resources challenges we all face are twofold. In essence, they are about ensuring

availability of supply on the one hand; and ensuring acceptability and sustainable

development on the other.

Allow me to say a few words on these two issues.

First, a look at availability of supply.

As we know, many of the world’s largest oil fields are now past their peak, and on their way to

depletion. Added to the growing economies of the world, this is putting enormous pressure on

energy security, and obviously on prices. New oil-rich Commonwealth Countries such as

Ghana, Sierra Leone, Belize and Uganda are now coming into play, in a world of oil prices of

$100 a barrel, rather than $25.

But the real issue nowadays is not just prices, but rather one of security of supply.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 6

Around the world, companies have been courting countries to secure access to their

resources. Sometimes, this is done by exercising pressure. This is why we believe that the

work we are doing in putting in place adequate legal and commercial frameworks, strong

institutions and good governance principles is essential.

Second, to look at what we are calling ‘acceptability’, which is now at the forefront of the

natural resources debate.

Climate change is a major issue, as the world is struggling to find ways significantly to reduce

carbon emissions. The awful recent events in Japan have reintroduced questions concerning

nuclear energy – one of the few major sources of energy with a relatively small carbon-

footprint. Although in the very long run, nuclear energy will arguably still be necessary (and

this may be in the interest of Commonwealth countries such as Namibia, Botswana and

Malawi as uranium producers), in the medium-term, Liquefied Natural Gas (LNG) will

certainly regain strength.

As you may be aware, with the development of their LNG industry, Tanzania and Papua New

Guinea, among others will soon join Trinidad & Tobago as significant LNG producers. Finally,

in addition to renewable energy, new sources are being looked at, such as Coal-Bed methane

in Botswana. To keep up with the increasing demand in most minerals, the pursuit of new

sources of extraction has intensified, as we are seeing in the in Deep-Sea Mining now

happening in the Cook Islands and Papua New Guinea.

Acceptability also means greater awareness of environmental, social and accountability

issues. The recent Gulf of Mexico oil spill – and the serious environmental damage caused by

the accident – has had profound implications for offshore petroleum development. This is

why our work focuses more and more on environmental issues such as decommissioning of

mining or petroleum facilities, drafting environmental legislation (such as we are currently

doing in Ghana).

Last but not least, acceptability also pushes for greater transparency in the extractive

industries, so that Governments can be held to account regarding the management of natural

resource revenues. There is a growing realisation on the part of governments that while the

extractive process is purely converting a country’s mineral wealth into financial assets, this

wealth is finite. Provisions must therefore be made to secure some of these financial assets, so

that future generations also benefit from the country’s endowment in Natural Resources.

The Commonwealth Secretariat recognises the implications attached to these developments,

and has introduced transparency and revenue management principles in the assistance it has

been providing to member countries.

As such, the Secretariat is currently considering further collaboration with other

organisations, such as with the Extractive Industries Transparency Initiative (EITI).

Our objective is to ensure that, through the transparent and accountable management of

revenues accruing from natural resources, countries can benefit from increased growth,

achieve economic development and poverty reduction, and transform their societies.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 7

In closing, I hope that you will benefit from this Forum and by discussing the most

internationally acceptable and sustainable practices in the design of policy, legislation, and

contracts in the oil, gas and mining sectors. One of the great values of the Commonwealth is

sharing our experience and supporting each other: hence the title of our Forum – ‘Shared

Practice, Enhanced Wealth’.

I end where I began, with the Commonwealth of Values. If our brains and our hearts are our

own, ‘human’, natural resources, then let us use them. We have seen that ‘physical’ natural

resources can make us or break us: it depends on how we use our human natural resources,

to treat them. Our brains and our hearts should tell us how to treat them – and telling each

other is what this conference is about.

Once again, I thank you for being here this week, and I wish you a pleasant and rewarding stay

in London.”

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 8

Welcome Message

Ransford Smith, Deputy Secretary General

It gives me great pleasure to welcome you to the very first Commonwealth Natural Resources

Forum. I strongly believe in the potential of natural resources to transform societies for the

better. Given the right conditions, the extractive industry can create jobs, strengthen the

domestic private sector, fund public service improvements and contribute significantly to

infrastructure development. Oil, gas and mineral resources can also contribute to inflows of

foreign investment, export earnings, government revenues and national income.

However, we are also mindful of the fact that fulfilling this potential is neither assured nor

automatic. The extraction of non-renewable natural resources (notably, oil, gas and minerals)

has often led to political instability, revenue management challenges, corruption and

increased social tension. It is therefore necessary for resource-rich countries to improve their

legislative and regulatory frameworks, build institutional capacity and strengthen

governance. These are major challenges.

This Forum comes at an exciting time for the extractive industries. Extractive industry

commodity prices surged between 2003 and 2008, and then dipped during the global

financial crisis and recession, only to continue in their upward direction from the latter part of

2009. These factors have contributed to an increase in pressure on the governments of

producing countries.

Balancing the need to optimise the benefits from natural resources whilst considering the

need to secure and sustain much needed foreign investment continues to pose a formidable

challenge for countries. This is one of the main reasons for this Forum. I do hope you find the

discussions useful.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 9

Welcome Message

José Maurel, Director, Special Advisory Services Division

As you may know, the Commonwealth Secretariat has been providing technical assistance

with regard to issues in natural resource management and maritime boundaries for a number

of years. In fact, we have been involved in assisting governments in negotiations and in

establishing legal, fiscal and commercial frameworks for more than 25 years.

The provision of advisory services to Commonwealth Governments on oil, gas and mineral

resource development policies and strategies is a core activity and key competence of SASD.

We maintain the requisite in-house expertise to provide such support and we are assisted

where necessary, by external experts in respect of certain specialised areas.

While many of our member countries such as Belize, Ghana, Sierra Leone and Uganda have

recently discovered oil, many others have had to address issues related to new areas, such as

coal-bed methane (Botswana), and deep sea mining (Cook Islands). Issues related to the

environment, revenue management and transparency are now also key aspects of our work.

We strongly believe that the key to successful management of Natural Resources requires

three essential components: well-enforced legislative and regulatory frameworks, strong

institutions with adequate capacity and a clear role, and good governance according to

widely-shared principles. The Forum will try to address some of these components.

SASD remains committed to assisting countries in making natural resources a blessing to our

member countries, not a curse. I wish you all a fruitful week at the Forum.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 10

Purpose of the Natural Resources Forum

Daniel Dumas, Adviser and Head, Economic and Legal Section

The ELS has over the years gained significant experience and expertise in the provision of

advisory and technical assistance in natural resources to Commonwealth member

governments. ELS’s primary mode of operation in this regard has centred on adapting its

international know-how to country specific economic and legal challenges in the management

of natural resources.

While member governments have benefited from this approach, it was felt that there was a

need for a central medium for sharing experiences and learning contemporary practices. This

led to the idea to develop the Commonwealth Natural Resources Forum as a capacity building

initiative, for senior Commonwealth member government officials to share and learn with ELS

advisers and industry experts.

Objective of the Forum

The event sought to provide a high-level discussion forum on today’s petroleum and mining

issues for both governments and investors. The sessions took participants through the

fundamentals of developing sound modern and sustainable policy, legislation and agreements

in line with international contemporary practice.

Relevance to Commonwealth Member Countries

In April 2009, ELS successfully launched a report titled “Minerals Taxation Regimes: a review

of issues and challenges in their design and application”, in conjunction with the International

Council on Mining and Metals (ICMM). It was pointed out by DSG Smith in his opening

remarks that such opportunities to interact in this regard did not happen enough. One of the

key recommendations by participants at the launch was for a forum which would foster

interaction on contemporary developments in natural resources between industry

practitioners and governments.

The ELS report ‘Transforming Society through the Extractive Industries’ identified weak

institutional capacity as a significant impediment to sustained development in the petroleum

and mineral sectors of many member countries. While most agencies and technical assistance

programmes focus on developing proper frameworks, countries often do not have sufficient

institutional capacity to properly implement and maintain them. A significant proportion of

ELS’ work focuses on establishing such frameworks. It is felt that additional effort now needs

to be geared towards enhancing institutional capacity. This is the primary focus of the Forum.

The comparative advantage of ELS stems from the interactive hands-on style the team

maintains while working with government officials. There is significant value in the access

which government officials gain into the ‘institutional memory’ of ELS as well as its

international knowledge-base, in addition to a high level of trust which ELS has gained from

experience in advising numerous Commonwealth countries over time.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 11

Section 1: Creating a sustainable investment climate

Attractive geological prospectivity of a natural resource is a primary consideration for

investment in the extractive sector. However, if a country is seeking to attract investors with

proven technical, financial and operational competence, for the development of its extractive

natural resources, it is critical to demonstrate the presence of suitable legal, fiscal, and

commercial arrangements. This section explores these arrangements, looking at the issues

from the perspectives of both a host government and an investor.

Legal frameworks for sustainable investment in natural resources2

Sustainable investment implies the allocation of resources in the most judicious manner in

order to achieve benefits for both present and future generations. This in turn requires an

effective legal framework, comprising the following elements:

- The constitution: There may be special provisions in the constitution relating

specifically to natural resources, including, crucially their ownership. Generally natural

resources are owned by the state, or a mix of public and private owners.

- National policy: A policy is simply a signpost or a roadmap. There are different policy

models available, including the ‘institutional model’ involving the judiciary or

executive branch of government or the ‘process model’, which involves a broader set of

stakeholders.

- Natural resources laws and regulations: These provide stability and are either

integrated, multidimensional or sector-specific. The Kenyan Energy Act is an example

of an integrated, multidimensional law, dealing with electricity, including rural

electrification, petroleum and natural gas as well as renewable energy, energy

efficiency and conservation. Sector-specific laws can be fragmented and may cover the

oil & gas sector, or mining environmental laws. There is no common denominator

across countries, though in all cases the quality of the regulation is measured in terms

of its ability to strike the right balance between attracting investment and providing

welfare gains to the host country.

- Contracts: These define the legal and commercial relationship between the host

government and the investor. It is important to understand the difference between a

contract (usual in common law, it means the basis of the relationship cannot be

changed); and an administrative permit (usual under continental law, and subject to

alteration). Different contractual models include a concession (royalty/tax licensing

system); a Production Sharing Agreement/Contract (where the government receives

some of the production); Risk Service Contracts; or hybrids. The box below, ‘Varying

contractual models across different oil and gas jurisdictions’, demonstrates the

diversity of approaches available to governments. Bid rounds should be relatively

short3, they should reflect geological prospectivity and socio-economic circumstances,

and they should be robust enough to allow for changing domestic or global socio-

economic and political circumstances.

2 Based on the presentation by Ibibia Worika, Adviser (legal), ELS. 3 Though sufficient time should be allowed for an investor to prepare a bid, bearing in mind that there may be several dozen other bid rounds underway around the world at any one time. Trinidad & Tobago allows companies four months’ preparation time. See box ‘Bidding rounds – an investor perspective’ on page 10.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 12

- Regulatory institutions: Regulatory institutions are responsible for the implementation

and compliance enforcement of regulations and contracts. There can be well-

developed laws and contracts but without the implementation capacity provided

through regulatory institutions, little can be achieved. If they are well developed,

regulatory institutions can facilitate natural resource development; if not, they may

stifle it. Enforcement can take place via line ministries, agencies or departments (for

more specific elements such as licensing procedures), and independent agencies,

which have some level of autonomy but whose remit is circumscribed by law. State-

owned enterprises may sometimes have regulatory powers, though this can lead to a

conflict of interests.

Varying contractual models across different oil and gas jurisdictions

There are many challenges to effective regulatory enforcement, including conflicting policy

goals, for example the encouragement of extractive sector development combined with

conservation laws. Whenever goals are unclear, the agency may become ineffective. There

may also be ambiguity in regulatory language which can make enforcement difficult.

Investors place a premium on the legal framework being stable and predictable, with clear

mechanisms to encourage good behaviour and punish bad practice. Political stability is also

crucial to investors, and a growing issue, as well as transparency and accountability. Other

important issues include revenue management, the quality of infrastructure, the skill level

among the country’s labour force, and the openness or receptivity of the country to foreign

investors. Regional economic development (or ‘regionalism’ – through organisations such as

SADC4, ECOWAS, the EU) is also critical as it creates a ‘bulwark’ for investors by increasing the

4 A list of acronyms appears at the end of this report.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 13

size of the market as well as developing a common set of rules which guarantees at least a

minimal level of democratic governance.

Investor attraction and selection process: international industry perspective5

Petroleum licensing is a highly complex process involving the constitution, ownership of

resources and reserves, multiple stakeholders, prospectivity, bid rounds, changes of

circumstances, economic stability, regulatory institutions and an educated workforce6. The

four main groups (or ‘stakeholders’ or ‘co-operants’) affected by the licensing process are the

host community7, the host government (or rights-holder), the investor, and the environment,

including future generations. A balance of interest should be sought between these four

groups.

These four groups are affected by risk, prospectivity and competition. The search for

petroleum is about management (as opposed to minimisation) of risk. There is a huge body of

research on petroleum risk. An industry maxim sates: ‘if you don’t like risk, you’re in the

wrong business’. Regarding prospectivity, there are commonly five types:

- technical prospectivity, which is subject to rapid changes (10 yrs ago, Uganda had

limited prospectivity in the oil industry, now it is considered a ‘hot area’);

- legal/contractual prospectivity, to do with the stability of the legal framework;

- fiscal prospectivity, which relates to prices, and subject to rapid change;

- geopolitical prospectivity, which can be important, for example knowing whether or not

there is a secure, safe pipeline route to the coast; and

- environmental prospectivity, which is a significant issue especially since the BP

Macondo spill8.

Each company accords different weights to the five elements. A valuable element of

prospectivity for investors is whether or not they will be granted bookable reserves. This is

the case in countries including the UK, Norway, Netherlands, US, parts of Latin America, the

UAE and Oman. In other countries including Iran, Iraq and Kuwait, reserves are not bookable.

There is tendency away from awarding investors this right as it is seen as an intangible

essence of a nation state, or a sovereignty issue.

Future challenges include the growing role of increasingly vocal and politically active host

communities, environmental considerations, and the potential for citizens to act as de facto

‘regulators’ (for example by protesting against extractive activity if there is no local social

licence to operate). Islamic law may also have a growing effect on the sector, as could ‘buy-

back’ type contracts as resource nationalism9 takes a greater hold. Prospectivity changes over

time, for example regimes with a low geopolitical prospectivity can improve their rating

surprisingly quickly as investors revise their risk assessments.

5 Based on the presentation by Mike Bunter, B and R Co, Petroleum Consultants. 6 The right licensing policy creates the conditions for an educated workforce: an estimated 350,000-500,000 people are directly or indirectly working as a consequence of a sound licensing regime for the North Sea oil & gas sector. 7 Because of the demands of transparency, host communities are de facto involved in licensing processes. 8 A participant later suggested the addition of a sixth type, ‘corruption prospectivity’, given the increasing level of discussion of this issue across the sector. 9 Resource nationalism is the trend whereby governments claim ownership of natural resources. Venezuela recently announced that foreign investors can no longer book reserves, and Bolivia followed suit shortly afterwards.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 14

Investors are looking for the largest amount of acreage for the longest period of time for the

lowest cost. By contrast, governments offer the smallest possible acreage for smallest period

in return for the maximum amount of money. These mutually exclusive objectives clearly

require compromise on both sides10. Governments want to attract a large number of investors

into a licensing round - the bigger the market, the better the deal. The government wants to

assess whether investors are suitable for involvement in the territory so they ask for a bid

that includes financial and technical capability as well as management capability. They use a

point scoring system for tender evaluation to make sure investors are suitable. Then the

dialogue between governments and investors can begin.

Bidding rounds – an investor perspective

Investors need to have sufficient time to be able to consider each opportunity as it arises. At

the time of the forum, there were 39 bidding rounds underway around the world, including 10

in Africa, 8 in south-east Asia, 12 in Latin America. For each bidding round that an investor is

considering becoming involved in, the process followed is roughly:

- a company analyst or researcher is requested to provide information for the

management board to be able to make a preliminary decision about whether or not to

enter the bidding round

- if the company decides to take the investment opportunity further, they work out

whether or not to partner with another company and spread the project risk

- if they decide to partner, the new ventures manager (or equivalent) will talk to his

colleagues in other companies to see who is interested

- money is found to fund in-depth evaluation of the opportunity

- the opportunity is evaluated and an offer is made

All of these stages require time and management effort, and compressing the timescale may

cause an investor to walk away from the opportunity.

Bid round process and practice – The Trinidad & Tobago Experience11

Trinidad & Tobago is a small country in the southern Caribbean, covering around 1864m2. Its

current gas production is 4.1bcf/day and although its oil production is declining it would like

to increase it in order to balance oil and gas production. Petroleum production began 102

years ago, so it has a very well-established governance structure. The petroleum industry is

governed by the Petroleum Act (1969), which has had several amendments and is currently

being revised to align it with contemporary circumstances (but without any major upheavals).

The minister is responsible for determining the areas to be made available for petroleum

exploration and development. The minister invites applications for the right to explore and

produce petroleum. Competitive bidding and one-on-one negotiations have both been used

but competitive bidding is now preferred. This has been the policy since 1987 – ‘in a

competitive environment, you get the best out of companies’, notes Helena Inniss. A number

of licences are issued including (rarely) an exploration licence; an exploration and production 10 ‘Relinquishment provisions’ provide part of the solution to this conundrum, see Trinidad & Tobago experience, page 14. 11 Based on the presentation by Helena Inniss, Director, Ministry of Energy and Energy Affairs, Trinidad & Tobago

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 15

licence (more common and gives a company the exclusive right to develop an area); or a

Production Sharing Contract (PSC). Before 1995, there were few PSCs; since then there have

been many more. A PSC doesn’t preclude the option of using the licensing regime, for example

in two big offshore areas which have been under development since the 1970s. Generally

however PSCs are used now, on land as well as offshore.

The PSC approach has been refined since 1995 with changes including allowing more time to

explore in deep water, in recognition of the technical challenges of operating in these areas.

The exploration programme is biddable – the government has its own internal benchmark but

in their experience, when they publish this, the companies tend to stick to it. They have found

that it is better to allow the companies to say what opportunity is worth. The duration of

contracts is 25 years for shallow water, 30 years for deep water (400m or more). The

duration is flexible for gas because it has to include a market development phase. This

additional time is added to the term of contract, and companies are happy with this approach.

There are also ‘relinquishment provisions’ in PSCs because the government doesn’t want

companies retaining acreage indefinitely. At the end of each project phase companies

relinquish acreage until what they get to keep is the discovery that is commercially viable. In

some cases they can ask for acreage to be retained, up to 20%, but the government doesn’t

allow the company to keep acreage anyway – this is a lesson from past experience.

The country has attractive gas provisions and a lot of companies are involved in bidding

rounds. Over time they have chosen to have a fixed cost recovery limit, which is 60% in deep

water, 55% in average depth and 50% in shallow water. The government’s share of profit

petroleum is biddable, and it is price and production sensitive. When these are low, the

government gets a smaller take; when price and production are higher, the government gets a

higher take. The country has had a mixed experience of competitive bidding rounds, though

they have been mostly successful. They are highly dependent on the global environment,

including issues such as supply and demand, and energy security.

There are good perceptions of prospectivity of acreage in Trinidad & Tobago because it has a

stable operating environment, even though the technical prospectivity is lower than in

Venezuela12. The prospectivity of acreage is very important, especially in deep water.

Incentives have been built into PSCs, such as a reduction in petroleum profit tax from 50% to

35%, and an uplift of 40% on CAPEX for exploration drilling. There is a windfall profits tax if

oil prices go over US$90/bbl. The royalty is flexible, between 0% and 12%. With the windfall

profit, companies used to complain that the government took all of the upside, this has now

changed so that companies get a share in the upside. There is also an escrow account which

the investor pays into from start of development (the payment comes from the contractor’s

profit oil – 0.25c per boe). Five years before the operation ends, companies are required to

draw up a plan and bring it to the government, showing the cost of the plan. If more money is

required, the company needs to start paying it in at that stage. If less money is required, the

12 Some companies with offices in Venezuela have moved to Trinidad & Tobago, demonstrating that security of the operating environment is a big factor for investors.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 16

government keeps the money, since the company operates on a cost recovery basis. The

country has tried to reduce front-end costs to companies and cost recovery has been set at

60%.

The competitive bidding process begins with a technical review of open acreage, which is

sometimes done in the ministry, but tends to be outsourced for deepwater areas. Companies

nominate the acreage they want, and the information is kept confidential to avoid overheating

the bid round. The country decides how many blocks to offer based on its strategic interests

and then makes recommendations to cabinet on the blocks and the terms and conditions of

the bid.

The competitive bidding order by which bids are invited is a very structured process, which

sets out prerequisites and terms and conditions. The bid form is totally self-assessable, there

is a point system and companies can work out what they are likely to receive for different

elements. Up to now, this stage has taken two months. A lot of evaluation time is required to

analyse different numbers and pick the best bid on the basis of this analysis. The contract can

be up to 40 years so the information needs to be correct from the outset.

The government is hoping for the process to take nine months, which includes four months

for companies to evaluate the area and receive internal approvals, and then five months for

the government’s own process. Negotiating the PSC can take a long time, as both parties

sometimes hold hard to elements that are dear to them. In response, the government has

started publishing the model contract and asking for comments. The discussion takes place in

the public domain. The government then responds to comments from companies and others,

trying to take on board as much as possible, and then asks companies to sign a schedule

indicating exceptions to the provisions of the model contract. One month after the award of

contract, the government wants the PSC signed. This approach brings all the big issues up

front, so when negotiations begin, there is a limited number of issues to cover so the process

doesn’t end up too time intensive.

Challenges include completing the process in the stated time; the dynamic, volatile global

environment; and accidents and environmental considerations. Deep water drilling will begin

for the first time fairly soon. Bids have been received and are currently being evaluated. The

future of the oil industry in Trinidad & Tobago will be focussed on deepwater production.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 17

Open discussion

What are the pros and cons of signature bonuses?

- There are none in Trinidad & Tobago for deep water, to try and keep front end costs

down13. For shallow water, where there is more competition, a signature bonus was

required, in the range of US$2m - US$12.8m.

- Signature bonuses are currently US$0.5bn in Angola for 6000sq km of deep water

acreage, per contract area. Angola is regarded as highly prospective. For a less

prospective area, signature bonuses may not be appropriate.

- Many NGOs dislike signature bonuses because it represents a large cash payment

which could be misused – it presents an opportunity for corruption.

What does it mean for citizens to act as regulators?

Communities may feel resentful about the presence of oil in their territory and citizens may

end up acting as ‘regulators’. For example the Wessex basin in the UK is a petroleum

prospective area and official ‘area of outstanding natural beauty’. The government in London

licenced acreage to a foreign oil company and failed to bring the local community along in the

process. When the first seismic trucks turned up, people lay down in the road to stop them.

Why do some governments provide incentives for gas exploration rather than for oil?

There is a lot of ‘stranded gas’ around the world, often in very remote, intercontinental areas.

If the pipeline is sufficiently long and selling price sufficiently low, it is possible for the gas to

have no commercial value, so an incentive is required to make it commercially viable.

13 Rig costs can approach US$1m/day for deepwater production.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 18

Section 2: Effective risk allocation

Investors in the natural resources sector prefer to be able to operate within the context of an

established legislative framework, but also expect that certain key issues of importance to

them will be substantially negotiable. This section focuses on contract design and

negotiations. The first part will address issues such as what should be set by law versus

contract, which parameters should be fixed or open for negotiation, and how to best handle a

negotiation process. The second part of the session will focus on elements most frequently

raised during negotiations between governments and companies, such as provision for

discretionary power, stabilisation clauses, and dispute prevention and resolution.

Contract design and negotiation: companies’ perspective14

There is often a sense of frustration among investors that they struggle to convey their

messages to governments. This is not due to translation difficulties but rather to differences of

culture – ‘what happens when worlds collide’, according to Peter Roberts. A number of issues

come up time and again in negotiations between investors and governments, these are

described below.

Local content

When investors say that ‘local content rules must be sensible and proportionate’, they mean

that ‘it will be impossible to do the work if the rules are unrealistic about what skills and

materials can be procured locally’. One example was a requirement to make pipelines using

only materials from Indonesian steel mills, but local producers lacked the technical capacity to

undertake the high pressure, high temperature welding required, making it impossible for the

company to adhere to the requirements.

Tax rates

When investors say that ‘taxes should be favourable to the investor’, they mean that ‘tax terms

should be favourable, but at the very least, they should not be worse or less attractive than

anyone else’s tax terms (including local companies).’ Tax stabilisation clauses or other

measures can be used to guarantee equal and fair treatment. This principle can be applied

across all fiscal issues.

Government take

When investors say that ‘there should be a proportionate allocation of profits and

hydrocarbons between the government and the investor’ this means that the cost recovery

element should not be blocked by the requirement to pay an early royalty (though investors

are mindful that the government wants some kind of early economic benefit) (also, see

comment box on ‘Domestic market obligations’, below).

14 Based on the presentation by Peter Roberts, Ashurst LLP

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 19

Domestic Market Obligations

Many developing countries, particularly those facing fuel shortages or energy security issues,

may require companies to sell a proportion of oil and gas that they produce to the domestic

market under a domestic market obligation (DMO). The prices offered domestically may well

be lower than the price on the international market, which means that investors do not like

these obligations from a financial point of view (though they may accept the need for such

obligations).

An investment strategy is based on selling products at the best price available on the

international market, so the obligation to sell at an artificially low price reduces a company’s

profits. When setting the rate of DMOs, governments should therefore be mindful of the

impact on the investor’s overall profitability and maintain the obligations at a fairly low level.

Change in law/regulatory application risk

Legal stability is important to investors. They worry that at some point there might be a

change in the way regulations are applied to the project, which will have an adverse effect on

the investment. They would like upfront protection from this, which means stabilisation

provision (treaty protection), to protect them from expropriation of their interests.

‘Expropriation’ in this case refers to everything from an asset seizure to ‘creeping

expropriation’ whereby the regime changes subtly. Investors want governments to exercise

their power objectively and fairly, but recognise that governments may react negatively to

this view since it sounds like it is a curtailment on its sovereign powers. The investor’s view is

that, if there is re-regulation of the sector, it should affect all companies (including local ones)

equally.

There is a split view among investors on the value of termination payments (whereby an

investor takes money from the government in the event of a loss of the project), with some

seeing them as a useful form of insurance, and others more tentative because the government

may see an opportunity to sequestrate the project and buy out the project.

Remittability

Investors believe there should be free remittability of cash and hydrocarbons from the

country, which means that cash generated by the investor should be remittable without

exchange controls, and hydrocarbons should be exportable (subject to domestic market

obligations).

Dispute resolution

There should be some mechanism to ensure that disputes are resolved fairly, amicably,

objectively, and in a way that doesn’t stultify continuing operation of the project. This could

be undertaken under local government law rather than international law, but disputes need

to be settled via an international panel in a place outside country (e.g. via ICSID – see section

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 20

on dispute resolution later in this report). This means that the host government needs to

agree to abide by the findings of an international process/arbitral award.

Government control

The investor must be free to operate the project as it sees fit15. This does not mean ignoring

local standards, or reporting and data sharing requirements, but rather, being free to operate

in the best interests of itself, its shareholders, and the local communities affected by the

operations. Governments should have no say in key decision making, particularly:

- initial commerciality of the project: this refers to circumstances where an investor may

decide that there is not enough oil to be commercially recoverable, but the government

might disagree, pointing to high oil prices, and insist on production regardless of

whether the finances hit internal rates (there can be similar debates about the size of

blocks);

- ongoing production: this refers to times where, because of high tax rates and low

prices, investors are inclined to buy gas in rather than producing it, but the

government insists that the facility runs regardless of the investment climate; and

- final decommissioning: at the end of the life of project, whose argument prevails about

what ‘end of life’ means – the company may see a decline in production and announce

end of project, the government might disagree and say that there is plenty of resource

left.

Government participation

Investors say that government participation in a project is not necessary, but if it happens, it

should be on fair and reasonable terms. For example a government may reserve the right for a

national oil company to back into a contract and take 10% of the equity. The concern for an

investor is that a government will seek to exercise this because they are concerned about how

the block is being operated by the investor, and what information is being provided to the

government (the true extent of hydrocarbon plays, the difficulty of the geology, whether or

not it is a viable project, etc.).

The investor view is that if the concession is set up so there is enough information flowing,

and the domestic market obligation is being fulfilled, there’s no need for a government to back

into the concession. If it happens, investors want to know that government participation will

be ‘full value’, that is, they need to pay to participate, and if there are carried interests (which

the investor would rather not have) then they should be hard/repayable, preferably with

interest.

Recognition of international standards

The government should recognise the investor’s imperatives towards upholding international

standards, and investors like to see wording in the contract referring to ethical standards

including bribery prevention. Investors also like to be seen to be upholding critical corporate

responsibility standards, with an external audit to demonstrate that they are doing so.

15 Makbul Rahim (see next section) makes the following point: ‘It is important to minimise government discretion to the bare minimum of circumstances where critical public interest is involved. In those cases, there should be clear objective criteria on how this discretion will be exercised.’

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 21

Issues in contract negotiation16

The key question in this section is how a contract, as an instrument, relates to a country’s

legal and regulatory regime. A basic principle of a contract is that it cannot be inconsistent

with the law – not only the petroleum/mining law but also the environmental law. The

licensing regime sets out minimum terms and conditions in law – the government wants to set

out core non-negotiable principles and make them generally applicable. There may be some

provisions which allow some flexibility, for example regarding the rate of relinquishment, or

the retention period in natural gas projects. However in general the law is non-negotiable and

there is a need for a contract in order to be able to tailor projects to the requirement of an

investor. A contract is therefore an instrument that seeks to provide a degree of

assurance/stability to the overall project.

A negotiation process might begin with a model contract which is synchronised with the law,

indicating to investors how they are expected to carry out a project, what provisions apply to

them and so on17. If there is competitive bidding, involving a licensing round, followed by

evaluation of bids, the conclusion is a selection of bids with which the government negotiates.

In mature oil and gas countries, cash auctions may be the best approach, but they may not be

applicable in new markets. In such cases, a negotiation process coupled with a competitive

bidding process may be more appropriate.

A concern for an investor relates to ancillary rights such as a drilling permit. Often, in

negotiations the company may draw up a very long list of ancillary rights. The government

should negotiate a procedure in which all ancillary rights are granted to investors, while

fulfilling those rights in the respective legislation. Subject to those rights being met, the

institutional arrangements can be worked out, for example by convening a coordinating

committee of the investor and relevant ministries.

Contractual considerations often boil down to risk management – if there are risks that are

better managed by the company, they will take responsibility. If there are projects risks that

governments have control over, these will be of concern to the company.

During contract negotiations governments are keen to enhance national capacity. One way to

do this is through participation. This is not just about an equal balance of fiscal responsibility

but also includes issues such as technology transfer, provision of employment, local content,

encouraging local businesses, training and skills development, local processing.

Negotiating Mineral Agreements: The Pakistan Experience18

Pakistan is relatively new to large-scale mining. A model mining agreement has been

developed which addresses the concerns of governments, communities, mining companies

and other stakeholders. It provides clarity over the basis for negotiations, sets out the

substantive rights and obligations of mining companies under law. It also acts as a legal

16 Based on the presentation by Makbul Rahim, MMR Consultants 17 Trinidad & Tobago’s practice of allowing a four-month period for investors to critique model contracts was welcomed by the audience. 18 Based on the presentation by Irshad Ali Khokhar, Director General Minerals, Ministry of Petroleum and Natural Resources, Pakistan.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 22

instrument to provide stability, assurance, and investment security for mining activity in the

country. Governments are bound to the agreed terms for the duration of the agreement unless

amendments are mutually agreed.

Mining agreements are not the usual way to regulate a mining operation and their use is

restricted to large-scale operations involving foreign investors. It provides a mechanism to

clarify how much of the regime should be fixed in legislation and how much should be left

open for negotiation. Pakistan’s model mining agreement covers a wide range of areas

including rights and obligations; investment protection; financing, royalties and taxation;

corporate social responsibility; and protection of environment and reclamation.

Located in western Pakistan, Reqo Diq is the world’s fifth largest copper deposit with

estimated reserves of 2.20 billion tonnes of copper ore. The first agreement to develop the

deposit was signed in 1993 and ownership has shifted a number of times since then. Most

recently a series of scoping, feasibility and Environmental and Social Impact Assessment

(ESIA) studies have been undertaken, for a total investment of US$435m, of which US$214m

covers exploration activities. The draft mineral agreement covers fiscal systems, dispute

resolution, regulatory issues and infrastructure, setting out such details as the life of the mine

(56 years), and involving the government of Balochistan as regulator, the government of

Pakistan as guarantor and regulator, and the investor (Tethyan Pakistan).

There are a number of important commercial terms set out in the draft agreement. These

include a reduction in corporate tax from 35% to 25% and stability for the full life of the mine.

50% of tax payments can be withheld by the company in return for specified infrastructure

obligations. Regarding royalty: the investor will pay 2% of gross sales proceeds for the life of

the agreement, with 50% of the tax available as an offset as above. The infrastructure

obligations cover power supply, a road connection from Gwadar Port, and a rail connection

from Karachi to locations near to the deposit.

The agreement is based on a number of precedents from power and petroleum sectors as well

as from competitors. There are however a number of new elements that the government has

not dealt with before, including the infrastructure obligation, the use of an export processing

zone for the life of mines, and a dispute resolution mechanism.

A detailed review process has been undertaken for the mineral agreement over the course of

the last few years, between the three main parties involved. Many amendments and reviews

have taken place over this time. For example the company sought to self-govern mining

operations in a number of areas, but this proposal was blocked by the government. Other

counter-proposals were made by the government parties in the areas of infrastructure, tax

exemption and dispute resolution (for example, the use of ICSID19 for international

arbitration). There was also detailed negotiation about the split between investor take and

government take.

19 The International Centre for the Settlement of Investment Disputes.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 23

Many of the outstanding issues have been settled via the input of a high-level, 13-person

steering committee headed by the Minister for Petroleum & Natural Resources and including

government representatives from a range of departments at national and regional levels. The

steering committee is currently meeting for the second time with a view to resolving

outstanding issues including the settlement of the royalty rate, the operational obligations

relating to social development, and value addition up to the final refining stage. Pakistan is in

a strong position at this pre-agreement stage because of the mineral potential and the

international competitiveness of its regimes. The government hopes to conclude negotiations

with TCCP (the investor) in the very near future.

Dispute Prevention and Resolution20

Dispute resolution is a critical matter that investors expect to be taken into consideration

when they are deciding whether or not to invest. The ideal is for disputes to be resolved in an

orderly, lawful and amicable manner, while preserving the contractual relationship if

possible. A number of different dispute resolution options exist, with an overall trend towards

harmonisation under international law. ELS assists member countries to address dispute

resolution issues, including through the development of model contracts and agreements.

Disputes often arise over an interpretation or application of an agreement or contract

between a government and an investor. These are known as ‘mixed disputes’ (public-private

disputes, as opposed to disputes between two private parties). The extractive industries

require high capital outlays, long contracts, a range of technical issues, and sovereign risk - all

of which creates a broad scope for dispute. It is therefore vital for the government and the

investor to consider in advance, within the contract, how disputes will be resolved, for

example through the use of a model contract or agreement. Such documents reflect

internationally agreed standards and practices.

There is a continuum of options from highly informal through to formal, adversarial, rules-

based processes. The majority of disputes are resolved informally through negotiations,

which are the most efficient way to deal with concerns and allow the contractual arrangement

to continue. When negotiation fails, the first fallback position is usually to seek third party

intervention, whose central tenet is for the parties to consent to be bound by the findings of

the process. International arbitration is a last resort. The categories further break down as

follows:

Fact-finding: This model helps to clarify issues and resolve a dispute before it gets out of hand.

It results in report limited to findings of fact, and parties are free to decide how to give effect

to the report.

International conciliation: Under this model, parties agree to appoint a conciliator or

commission to clarify issues and secure agreement. This is a formal process which doesn’t

involve rendering of a binding award. It ends with a report containing recommendations, and

if parties have agreed on plan of action, that report can contain the agreement. Conciliation is

20 Based on the presentation by Joshua Brien, Adviser (Legal), ELS.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 24

less adversarial than arbitration and more and more international organisations have applied

this approach.

Expert determination: This model is often used in conjunction with arbitration and features a

qualified expert who resolves issues, especially those of a technical nature for example

regarding the payment of royalties. This can be an informal process (which is quick and

cheap) and results in binding determination by the expert, unless parties have agreed

otherwise. ELS has worked with the government of the Seychelles on a clause on expert

determination, designed as an adjunct to formal dispute process – the two elements can work

together.

International arbitration: This is the most costly and time-consuming model, but some

disputes can’t be resolved by any other means. It involves the appointment of an arbitrator or

tribunal which issues an award to the parties to resolve the matters in dispute, and results in

a decisive outcome –the rendering of a binding and enforceable award.

The best known rules covering dispute resolution have been developed under the United

Nations and are known as UNCITRAL21. They cover all procedural issues. A number of bodies

apply international arbitration rules, such as the Permanent Court of Arbitration (which was

originally established for state-to-state disputes, but now works on mixed disputes, including

those relating to natural resources). ICSID provides another forum for the resolution of mixed

disputes under the Washington Convention. There are 157 parties to the convention,

including 41 commonwealth member countries.

ICSID provides an international agreed mechanism for the resolution of disputes between

states, and mixed disputes. Awards are binding and may be reviewed, revised (or annulled).

ICSID is increasingly popular and has such a full case-load (many of which are from Latin

America) that resolution of cases has slowed down. Many cases brought before ICSID involve

natural resources, such as the cancellation of oil concession. If a company succeeds in

characterising a dispute as an investment dispute they are able to have it heard at ICSID.

21 United Nations Commission on International Trade Law.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 25

Open discussion

Comment from a participant:

The challenge for most developing countries is that they have laws which are old and require

updating, hence, many countries do not have agreements for reciprocal investment and

protection of the government. Contracts are often negotiated at different times, under

different circumstances, which is why at particular times certain concessions may be offered.

However, investors often allude to precedent and attempt to circumvent the new policies of a

government, being reluctant to enter into new or revised agreements. It must also be

remembered that the mining and petroleum industry are distinct. Hence, laws and model

documents/agreements should be tailored accordingly.

Does being a signatory to ICSID allow a host government to be involved in the arbitration

process?

Any country that is a party to the treaty which established ICSID has an opportunity to put

forward their concerns, and be involved in many of the processes surrounding the arbitration,

including the selection of the panel and forum

Is it possible to write into law the method by which disputes will be handled?

There can be and there are instances when countries have laws which require and refer to

arbitration, yet when they don’t have such laws in place, resolution of the dispute is usually

decided on an ad hoc basis. In this regard, in order to prevent such ad hoc resolution of

matters, it is prudent to include dispute resolutions provisions in model law or contract which

will form part of negotiations between the investor and host governments.

The Trinidad & Tobago PSC example showed that one can go outside the ambit of the law, to

the extent that matters can be negotiated for, even if the law has not yet been amended or

revised to address such prevailing issues at that time.

The government often encourages investors to be involved in the country, yet at times when the

government wants to be involved in critical decision making situations the investors declare that

the government should not be involved. In this regard, how can government know and be

assured that the interest of the country is being taking into account?

Citizens are the stewards of a country’s natural resources, hence, although investors are often

ignorant of the public interest and may adopt aggressive negotiation tactics, there is a need

for investors to be aware of what is reasonable, what is unreasonable and how to be sensitive

to negotiations.

A balance needs to be attained between the objectives that an investor wants to achieve and

the matters where the government wishes to stand firm. Robust and open negotiations from

the outset, which allow for clear channels of communication between the government and

investor throughout the project, can help to avoid difficulties further down the line.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 26

There is often a conflict between government objectives and investor objectives and a

government will need to provide for and balance the rules and legislative provisions that

support the public interest and yet, can attract investment.

There is a perception that the investor does not want local content, but can’t these requirements

benefit the investor as well as the government?

Local content can benefit investors over the long term in a number of ways, for example

through increasing the size and diversity of the domestic private sector (and therefore the

quality of the supply base), or through increasing the pool of skilled employees available for

recruitment to the company. Both of these elements may in turn reduce the investor’s costs

because it becomes cheaper to access these resources locally as compared with bringing them

in from an international location. However, in the short term, meeting local content targets

usually represents a cost to the investor because it requires capacity building for local

businesses or potential employees. These costs can sometimes be shared between companies

and governments (and international development organisations).

Usually an investor decides to invest depending on geology of area and legal framework, but

what are the other critical features of a regulatory regime that foster investment?

The legal framework of a country should be clear and stable but also dynamic, in relation to

policy changes. Generally, at any given time law is evolving, however, it cannot or should not

be developed to respond retrospectively to new policies and prevailing issues at a particular

time.

Does ICSID waiver sovereign immunity?

There is immunity from suit and immunity from execution. ICSID removes the immunity from

suit to the extent that an arbitration award is to be treated as akin to a final judgment of a

court of competent jurisdiction. However, execution against government assets is an entirely

different matter which is not under the purview of ICSID.

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 27

Section 3: Issues in taxation of natural resource projects

Many resource-rich countries have special fiscal regimes relating to the extractive sector,

given the unique nature of the industry. Where governments choose to set up these regimes,

they are faced with a range of complex questions. The first part of this section covers the main

considerations for taxation of the extractive sector, making a case for why they should be

taxed differently, and discussing various tax instruments and the main characteristics of an

effective fiscal regime. The second part will consider the question of government take and

international fiscal competitiveness.

Tax administration of extractive natural resources has presented significant challenges for

governments. The problem is often not in the fiscal regime itself but in the failure to enforce

fiscal rules. This section explores tax administration practices that can help a government

maximise its revenue collection, including the appropriate determination of tax liability,

transfer pricing, tax filing, and auditing.

International benchmarking of fiscal regimes in natural resources22

When considering different fiscal regimes and comparing competitiveness, the conventional

wisdom is that the more competitive a country’s fiscal system, the more likely it should be

that the country will attract investment. This is because of the perspective that international

capital is mobile, and investors will go elsewhere if the regime is uncompetitive. However, as

of 2008, in the oil sector, about 150 countries were offering investment opportunities and 200

companies were pursuing these opportunities. The assumption that the bargaining power lies

with the company is increasingly not the case (see comment box, below: ‘Negotiation power

swings back to governments?’).

The Commonwealth Secretariat’s benchmarking work in this area helps governments to

assess the quality of their fiscal regimes by comparing practices with a range of peers. This

helps countries stay abreast of good practice and ensures that countries are not

comparatively short-changed. This is based on the idea that a country’s bargaining position is

enhanced when it is clear what’s on offer from peer countries.

Negotiating power swings back to governments?

The view that the competitiveness of a fiscal regime is a critical determining factor in its

success held sway for a long time when prices were relatively low and resources and reserves

appeared plentiful. During these periods governments were wary of asking for too much from

companies. In the last few years, however, bargaining power appears to have shifted back into

the hands of governments.

Chinese oil demand alone (11bn barrels per day) is driving the market in an unprecedented

way and its demand will soon be higher than that of the US. Meanwhile it costs US$70/barrel

to produce oil from Canadian tar sands. Therefore, as demand increases, and the quality of the

remaining oil diminishes, a company’s options are limited.

22 Based on the presentation by Ekpen Omonbude, ELS Economic Adviser

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 28

The point was underscored by Andre Cho, director of petroleum for the government of Belize,

who agrees that countries are in a strong position with respect to negotiating terms, and that

governments often underplay their hand. His view was that, as the number of oil fields

worldwide dwindles, companies will increasingly have to accept the terms that they are

offered by government.

There have been three broad periods of fluctuation in oil prices since the mid-1970s (see

diagram below). During the period up to the early 1980s, this was a period of increased

government revenues as the profitability of projects went up. This coincided with a period of

nationalisation, and the prevailing philosophy was to try and get more out of project

revenues. Between the early 1980s and the turn of century, there was an increase in countries

offering acreage, lower prices, and better technology allowing companies to go offshore. This

resulted in a shift in bargaining power from governments to investors.

From the period 2003 to the present, the high spike in oil prices has led to a growing shift in

ownership of acreage from companies to governments. Increased oil prices have returned

increasing revenues to projects. Governments signed deals when prices were low and there

have been questions over the amount of revenue earned, and a general tendency to want to

bring investors back to table and re-think contracts. There has been a temporary slowdown in

the renegotiation drive, but as prices go up again, so will the renegotiations.

Three phases of oil price fluctuation since the 1970s

The diagram shows that, in general, when oil prices are high, a government’s negotiating

position is stronger than when oil prices are lower.

The benchmarking exercise comprises three phases. The analyst selects a group of countries

with similar technical, legal, fiscal and environmental characteristics. The ‘fiscal burden’ is

assessed in order to identify the level of government take and measure the impact of the

regime on government cash flow, as generated by a hypothetical extractive sector project. The

next step is to identify the main sources of government revenue and assume a field size

Proceedings of the Natural Resources Forum, 6-8 April, Marlborough House, London

Page | 29

(including import duties, royalties, income tax, additional dividends etc). The model does not

include minor fees such as rents, licence fees, bonuses and so on, even though signature

bonuses can reach into the hundreds of millions of dollars.

The next step is to determine the fiscal burden – if revenues are received later rather than

earlier, the government may have to find other sources to meet budget commitments, through

raising taxes, reducing expenditures, increasing government borrowing and so on. This can

also be analysed from the perspective of budget surplus and the development of a sovereign

wealth fund which may bring a return to the government. There is also an opportunity cost in

making the investment at the current time rather than later, and this is considered in the

model.

Next the model considers how long it would take investor to recoup cost of investment, and

the responsiveness of the government take – how much does the government get in return as

the profitability of the project increases? In reviewing a number of different regimes, it shows

that a number of oil regimes are progressive and a number are regressive, but in the mining

sector only two or three regimes are progressive. In a progressive regime, as profitability

increases, so does the government take. Different measures can be used to delay or speed up

the incidence of fiscal burden. For example the front-end burden can be reduced, which is

valuable from an investor’s perspective, but may not be so good for the government as it is

often looking for early signs of benefit from a project’s presence.

Having undertaken the benchmarking exercise a country can identify the areas where

adjustment is required in order to ensure at least a minimal revenue to government. Simple,

profit-based regimes are effective from the point of view of being low-maintenance and