the domestic production activities deduction and u.s....

TRANSCRIPT

The Domestic Production Activities Deduction and U.S. Employment

A Pete V. Domenici Fellowship White Paper

Fall 2012 Prepared by Dr. Larry Tunnell, Professor of Accounting and Dr. Anthony V. Popp, Professor Emeritus of Economics New Mexico State University Las Cruces, NM

Domestic Production Activities Deduction and U.S. Employment

i

Table of Contents Section Title Page

Table of Contents i List of Tables ii Executive Summary iii

1 Introduction 1 2 Which Industries are favored by the DPAD? 3 3 Which states are more affected by the DPAD? 5 4 Do states more affected by the DPAD also have higher unemployment rates? 6 5 Is the DPAD related to an increase in employment in DPAD-related industries over

time? 6

6 What are the tax treatments of the DPAD for state tax purposes in the various states, and how might the various state tax rates be affecting the effectiveness of the DPAD in those states?

8

7

Conclusions and Policy Implications References

10 12

List of Tables Table Title Page

1 DPAD/Domestic Taxable Income by Industry 4 2 Relative Importance of DPAD to each State 5 3 State DPAD Importance and Unemployment Rate 6 4 Industry DPAD Importance and Employment Change 7 5 State Tax Treatment of the DPAD 8

Domestic Production Activities Deduction and U.S. Employment

ii

The Domestic Production Activities Deduction and U.S. Employment

Pete V. Domenici Fellowship White Paper

Executive Summary

It is widely believed that taxing worldwide income, imposing a relatively high corporate

tax rate and allowing certain foreign income deferrals encourages the offshoring of U.S.

production. One policy alternative that might combat these effects is to extend and expand the

domestic production activities deduction (DPAD) provided for in Internal Revenue Code (IRC)

Section 199. The domestic production activities deduction (DPAD) offers an alternative to

across-the-board tax rate reduction that might be a more effective and less costly form of

corporate tax reform.

Little research on the DPAD has been done to date. Some unanswered questions remain

as to (1) which industries (including energy-related industries) are favored by the DPAD, and by

how much, (2) which states are more affected by the DPAD, (3) do the states more affected by

the DPAD also have higher unemployment rates, and (4) what are the tax treatments of the

DPAD for state tax purposes in the various states, and how might the various state tax rates be

affecting the effectiveness of the DPAD in those states. This study uses Bureau of Economic

Analysis, Census Bureau, and Checkpoint (a tax research program) data to investigate these

questions.

Which industries are favored by the DPAD?

In order to determine which industries are favored by the DPAD, the DPAD/Domestic

Taxable Income ratio was calculated for each industry for 2009. In 2009 the DPAD benefitted

the paper manufacturing industries more than all other industries. The next three industries

benefiting most were the publishing industry, motion picture and sound recording industries, and

electrical equipment, appliance, and component manufacturing industries. Oil and gas

extraction, an important industry to New Mexico and the nation, is combined with non-oil and

gas mining into one category, Mining, in the Statistics of Income (SOI) data. This industry had a

DPAD/DTI ratio of 0.040, a value just above the mean and median for all industries.

Which states are more affected by the DPAD?

In order to determine which states were most affected in 2009 by the DPAD, the

DPAD/DTI ratio for each industry was multiplied by the percent of a state’s GDP that came from

that industry. These products were added together for each state, giving a measure of the

DPAD/DTI ratio for each state. As would be expected, it appears that the DPAD favors states

whose GDP is more concentrated in the production of goods, such as Oregon (computer and

electronic product manufacturing), Louisiana (mining and petroleum products manufacturing),

and Wyoming (mining). States that do not benefit from the DPAD as much have economies that

are less dependent on producing goods, such as Nevada (real estate and accommodations),

Hawaii (real estate and retail trade), and Delaware (Federal Reserve banks, credit intermediation

and related services, and real estate).

Domestic Production Activities Deduction and U.S. Employment

iii

Do states more affected by the DPAD also have higher unemployment rates?

If a purpose of the DPAD is to reduce unemployment, then it would be most effective if it

is most used in states with higher unemployment rates. A simple correlation analysis was

performed to determine the relationship between the incidence of the DPAD in each state and

that state’s unemployment rate. A negative, but insignificant, correlation was found. This may

indicate that states with a higher incidence of DPAD also tend to have a slightly lower

unemployment rate.

Is the DPAD related to an increase in employment in DPAD-related industries over time?

The DPAD was first implemented in 2005 at a rate of three percent of domestic

production taxable income then, increased to six percent in 2007, and nine percent in 2010. The

incentive effects of the DPAD might be expected to result in an increase in the U.S. employment

totals in DPAD-intensive industries over time. The analysis indicated that the more important the

DPAD is to an industry (the higher the DPAD/DTI ratio is), the lower the increase in

employment in that industry over time, an inverse relationship. This would seem to indicate that

the DPAD is actually decreasing employment in the industries in which it is more important – a

counterintuitive result. However, it is more likely that the DPAD is actually targeting the

industries that it was intended to – those in which the U.S. continues to lose jobs. While it is

possible that the DPAD is reducing the job losses in these industries, the other factors (lower

costs and fewer regulations offshore, economic downturn) that are causing these losses are

apparently swamping any positive effect there might be from the DPAD.

What are the tax treatments of the DPAD for state tax purposes in the various states, and

how might the various state tax rates be affecting the effectiveness of the DPAD in those

states?

In all, 21 states conform to the U.S. Federal Income Tax treatment of the DPAD, and 23

states and the District of Columbia do not allow the DPAD as a deduction. Four states (Nevada,

South Dakota, Washington, and Wyoming) do not have a corporate tax against which the DPAD

can be used as a deduction. Given that the DPAD-related tax savings from the federal income tax

is not enough to impact the employment levels in various industries, it not likely that the DPAD-

related tax savings from the smaller state tax rates will have any measurable effect on

employment.

Policy Implications

The primary implication of this study is that in order to effectively offset the other factors

that contribute to offshoring, the DPAD percentage would need to be increased. A doubling of

the DPAD, as the president proposed for advanced manufacturing activities in the last State of

the Union address, would reduce the effective corporate tax rate on such income to 28.7 percent -

close to the 28 percent rate to which Mitt Romney is proposing to reduce the top marginal

corporate tax rate, and close to the top rate suggested by the Simpson-Bowles Commission. This

would seem to be an area in which compromise might be reached.

Domestic Production Activities Deduction and U.S. Employment

iv

Another policy implication of this study is that it illuminates some of the problems

inherent in reducing rates in order to accomplish policy objectives. The reduction of overall

corporate tax rates in order to encourage production in the U.S., without related reductions in

other deductions, would be very expensive from a budget point of view, but might not result in

the desired outcome of reducing offshoring.

The fact that there are so many states that don’t allow the DPAD as a deduction for state

income taxes probably reduces its effectiveness. States that don’t allow the DPAD should

consider making the appropriate changes to allow it.

Domestic Production Activities Deduction and U.S. Employment

1

The Domestic Production Activities Deduction and U.S. Employment

Pete V. Domenici Fellowship White Paper

1. Introduction

It is widely believed that taxing worldwide income, imposing a relatively high corporate

tax rate and allowing certain foreign income deferrals encourages the offshoring of U.S.

production. One policy alternative that might combat these effects is to extend and expand the

domestic production activities deduction (DPAD) provided for in Internal Revenue Code (IRC)

Section 199. Section 199 allows for the deduction of a percentage (currently nine percent) of

taxable income from domestic production activities, and its expansion would provide the U.S. an

opportunity to enact effective corporate rate reductions that are targeted to U.S. producers. In his

2012 State of the Union address President Obama indicated that he would focus on the DPAD

and double it for advanced manufacturing technologies.

Amid growing calls for reform of the corporate income tax, a number of reports have

surfaced comparing the U.S. marginal corporate tax rate to those in other countries around the

world. When Japan lowered its corporate tax rate in April of 2011, the U.S. corporate tax rate of

39.2 percent officially became the highest marginal corporate tax rate in the OECD. In fact, this

is the 20th year in a row that the U.S. marginal corporate tax rate has been higher than the OECD

average (Hodge, 2011). Moreover, a recent study from the CATO Institute estimates that the

current U.S. marginal effective corporate tax rate is around 34.6 percent. (Chen and Mintz,

2011).

Countering these reports are studies that point out that the average effective corporate

rate in the United States is relatively low. A recent New York Times article cites the fact that out

of the 500 companies in the S&P index, 115 paid a total corporate tax rate of less than 20 percent

over the past five years (Leonhardt, 2011). In May 2011, the Boston Globe reported that more

than 25 percent of the 112 profitable publicly traded companies in Massachusetts either paid no

tax or received refunds for the 2010 tax year (Healy, 2011). Many companies claim that their tax

rates are artificially low in recent years due to tax breaks from recently enacted legislation.

Because of the high level of variation in tax burden from one year to the next, recent research

finds that looking at cash taxes paid over several years is a better estimate of tax burden than a

one-year point estimate (Dyreng et al., 2008).

One contributing factor to low average effective corporate tax rates is that over the past

several decades U.S. multinational corporations (U.S. MNCs) have shifted a substantial amount

of business activity offshore.1 As an increasing number of companies choose to offshore

operations, jobs continue their exodus from the U.S. During the 2000s, U.S. MNCs increased

employment in offshore operations by 2.4 million, while cutting workforces domestically by 2.9

million (Wessel, 2011). The result has been a substantial exodus of manufacturing jobs in

particular from the U.S. to foreign locations. Andy Grove, former CEO of Intel, notes that

1 U.S. MNCs shift income offshore for a variety of reasons. In some cases, they may be seeking to expand into

foreign consumer markets. Oftentimes, however, they shift production activities offshore to take advantage of lower

labor and regulatory costs and to benefit from lower corporate tax rates.

Domestic Production Activities Deduction and U.S. Employment

2

manufacturing employment in the American computer industry is smaller today than it was

before the first personal computer was manufactured in 1975 (Grove, 2010).

In December of 2010 the Simpson-Bowles Commission recommended reducing the

corporate tax rate to somewhere between 23 percent and 29 percent, as well as switching to a

territorial rather than a worldwide tax system. After President Obama called for lowering the

corporate tax rate in his State of the Union address in January of 2011, a bipartisan plan put forth

by Ron Wyden and Dan Coats in February of 2011 suggested decreasing the corporate rate to 24

percent2. More recently, House Budget Committee Chairman Paul Ryan (and the Republican

nominee for vice president) proposed lowering the corporate tax rate to 25 percent as part of a

larger budget resolution.

The domestic production activities deduction (DPAD) offers an alternative to across-the-

board tax rate reduction that might be a more effective and less costly form of corporate tax

reform. Internal Revenue Code (IRC) Section 199 (introduced by the American Jobs Creation

Act of 2004) allows for the deduction of a percentage of taxable income derived from domestic

production activities. This provision reduces the effective corporate tax rate on income generated

by domestic production activities, but the currently available deduction of nine percent of

qualified taxable income only reduces the effective tax rate on domestic production income by

just over three percentage points. Expansion of the DPAD would provide Congress an

opportunity to target proposed rate reductions to domestic producers and create stronger

incentives for U.S. MNCs to relocate production to the United States. 3

Morrow, et al., (2011) suggest that selectively reducing the corporate tax rate on

domestic business activity by increasing the DPAD offers a number of advantages. Expanding

the DPAD reduces the cost advantages associated with offshoring production activity.

Moreover, it does so without driving down domestic wages and without relaxing important

environmental, worker safety, and other regulatory controls. Further, focusing the rate reduction

on domestic production activity has the potential to more cheaply attract businesses to the U.S.

than an across-the-board rate reduction would. It could substantially increase federal revenues

by increasing corporate tax revenue (if it drew enough business back to the U.S.). In addition to

possibly increasing corporate tax revenue, every dollar of additional domestic wage income

increases payroll and individual income tax revenues to both federal and state governments, and

local governments would benefit from additional income, property and sales taxes. It is

estimated that resulting increases in individual tax revenues could be sufficiently large so that the

net revenue effect would be positive under various plausible assumptions regarding the amount

of increased domestic production activity stimulated by the proposed change.

However, little research on the DPAD has been done to date. Some unanswered

questions remain as to (1) which industries (including energy-related industries) are favored by

the DPAD, and by how much, (2) which states are more affected by the DPAD, (3) do the states

more affected by the DPAD also have higher unemployment rates, and (4) what are the tax

treatments of the DPAD for state tax purposes in the various states, and how might the various

2 This proposal was previously sponsored by Judd Gregg and Ron Wyden. Judd Gregg chose not to run for re-

election in 2010. 3 The WTO has not challenged the DPAD since its 2004 inception.

Domestic Production Activities Deduction and U.S. Employment

3

state tax rates be affecting the effectiveness of the DPAD in those states. This study uses Bureau

of Economic Analysis, Census Bureau, and Checkpoint (a tax research program) data to

investigate these questions.

2. Which industries are favored by the DPAD?

This question was investigated by analyzing tax return data provided in the Internal

Revenue Service publication Corporation Income Tax Returns (Statistics of Income-2009).

Table 17 of this publication provides tax return data for all corporations with taxable income in

2009, and the data is segregated by the industry in which the corporation does business. In

particular, it provides totals by industry for the DPAD and for taxable income. In order to

determine which industries are favored by the DPAD, the DPAD/Domestic Taxable Income ratio

was calculated for each industry for 2009. Domestic taxable income (DTI) is used to standardize

the industry DPAD amounts because the DPAD is only available for domestic production. The

resulting ratio will vary depending on how much of the domestic taxable income for each

industry is eligible for the DPAD. Domestic taxable income is not explicitly given in the

Statistics of Income (SOI) data, so it was estimated by multiplying taxable income by [(total tax

liability – foreign tax credit)/total tax liability] for each industry. Since (total tax liability –

foreign tax credit) gives an estimate of the U.S. tax on domestic taxable income, dividing that

number by total tax liability will give an estimate of the fraction of total income that consists of

domestic income. Table 1, below, provides the results. In 2009, the DPAD benefitted the paper

manufacturing industries more than all other industries. The next three industries benefiting

most were the publishing industry, motion picture and sound recording industries, and electrical

equipment, appliance, and component manufacturing industries.

Oil and gas extraction, an important industry to New Mexico and the nation, is combined

with non-oil and gas mining into one category, Mining, in the SOI data. This industry had a

DPAD/DTI ratio of 0.040, a value just above the mean and median for all industries.

Domestic Production Activities Deduction and U.S. Employment

4

BEA ID Industry DPAD/DTI BEA ID Industry DPAD/DTI BEA ID Industry DPAD/DTI

129 Paper manufacturing 0.089 111 Construction 0.042 135 Retail trade 0.003

146Publishing industries,

except Internet0.082 127

Textile mills and

textile product mills0.041 163

Administrative and

waste management

services

0.003

147

Motion picture and

sound recording

industries

0.08 130Printing and related

support activities0.041 151

Federal Reserve

banks, credit

intermediation and

related services

0.002

120

Electrical equipment,

appliance, and

component

manufacturing

0.076 106 Mining 0.04 168Ambulatory health

care services0.002

119

Computer and

electronic product

manufacturing

0.066 110 Utilit ies 0.033 170 Social assistance 0.001

131

Petroleum and coal

products

manufacturing

0.06148,

149

Broadcasting and

telecommunications

Information and data

processing services

0.033 162

Management of

companies and

enterprises

0.001

117

Fabricated metal

product

manufacturing

0.057 132Chemical

manufacturing0.026 143

Other transportation

and support

activities

0.001

115

Nonmetallic mineral

product

manufacturing

0.056 105Forestry, fishing, and

related activities0.017 154

Funds, trusts, and

other financial

vehicles

0.001

133

Plastics and rubber

products

manufacturing

0.055 158

Professional,

scientific, and

technical services

0.014 140 Truck transportation 0.001

126

Food and beverage

and tobacco product

manufacturing

0.055 134 Wholesale trade 0.013 152

Securities,

commodity

contracts,

investments

0.001

124Miscellaneous

manufacturing0.053 157

Rental and leasing

services and lessors of

intangible assets

0.01137,

138, 139Air transportation 0

116Primary metal

manufacturing0.052 176

Food services and

drinking places0.009 153

Insurance carriers

and related activities0

114Wood product

manufacturing0.05 172

Performing arts,

spectator sports,

museums, and related

services

0.008 142Pipeline

transportation0

123

Furniture and related

product

manufacturing

0.05 175 Accommodation 0.006 156 Real estate 0

118Machinery

manufacturing0.05 144

Warehousing and

storage0.006 169

Hospitals and nursing

and residential care

facilit ies

0

104Crop and animal

production (Farms)0.048 128

Apparel and leather

and allied product

manufacturing

0.006 173

Amusement,

gambling, and

recreation

0

121, 122

Motor vehicle, body,

trailer, and parts

manufacturing

0.048 166 Educational services 0.004 141

Transit and ground

passenger

transportation

0

Table 1 – DPAD/Domestic Taxable Income by Industry

Domestic Production Activities Deduction and U.S. Employment

5

3. Which states are more affected by the DPAD?

In order to determine which states were most affected in 2009 by the DPAD, the

DPAD/DTI ratio for each industry was multiplied by the percent of a state’s GDP that came from

that industry. These products were added together for each state, giving a measure of the

DPAD/DTI ratio for each state.

As would be expected, it appears that the DPAD favors states whose GDP is more concentrated

in the production of goods, such as Oregon (computer and electronic product manufacturing),

Louisiana (mining and petroleum products manufacturing), and Wyoming (mining). States that

do not benefit from the DPAD as much have economies that are less dependent on producing

goods, such as Nevada (real estate and accommodations), Hawaii (real estate and retail trade),

and Delaware (Federal Reserve banks, credit intermediation and related services, and real estate).

StateGDP/industry-

weighted DPADState

GDP/industry-weighted

DPAD

Oregon 0.0266 Nebraska 0.0165

Louisiana 0.0253 United States 0.0163

Wyoming 0.0238 South Dakota 0.0161

Indiana 0.0204 Tennessee 0.0161

Texas 0.0199 Michigan 0.0161

Oklahoma 0.0197 Georgia 0.0160

Washington 0.0197 Missouri 0.0159

Idaho 0.0194 New Hampshire 0.0159

Alaska 0.0192 Vermont 0.0156

Iowa 0.0192 Montana 0.0155

Mississippi 0.0191 Massachusetts 0.0153

Arkansas 0.0189 Pennsylvania 0.0151

Wisconsin 0.0189 Illinois 0.0149

North Dakota 0.0188 Virginia 0.0147

Kentucky 0.0187 Maine 0.0142

Alabama 0.0186 Arizona 0.0137

Kansas 0.0184 Maryland 0.0128

North Carolina 0.0182 Connecticut 0.0125

New Mexico 0.0180 New York 0.0123

South Carolina 0.0178 New Jersey 0.0119

California 0.0174 Rhode Island 0.0118

Utah 0.0171 Florida 0.0116

West Virginia 0.0169 Nevada 0.0113

Minnesota 0.0169 Hawaii 0.0106

Ohio 0.0166 Delaware 0.0092

Colorado 0.0166

Table 2 – Relative Importance of DPAD to Each State

Domestic Production Activities Deduction and U.S. Employment

6

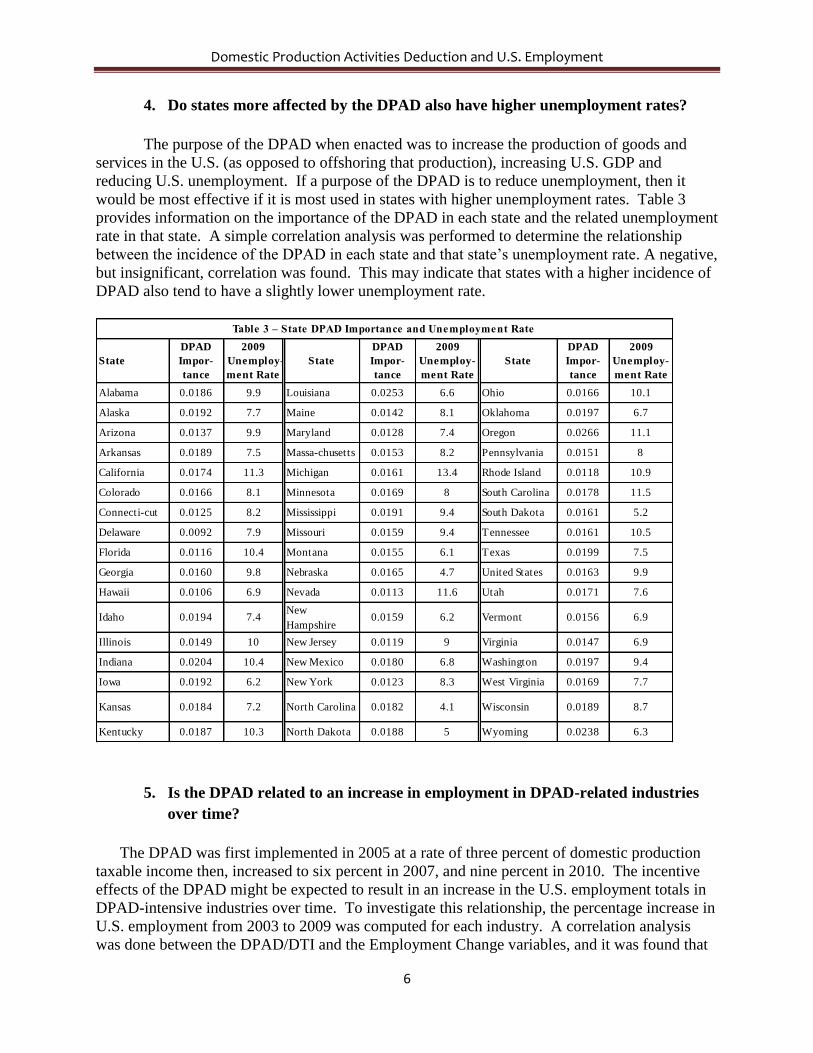

4. Do states more affected by the DPAD also have higher unemployment rates?

The purpose of the DPAD when enacted was to increase the production of goods and

services in the U.S. (as opposed to offshoring that production), increasing U.S. GDP and

reducing U.S. unemployment. If a purpose of the DPAD is to reduce unemployment, then it

would be most effective if it is most used in states with higher unemployment rates. Table 3

provides information on the importance of the DPAD in each state and the related unemployment

rate in that state. A simple correlation analysis was performed to determine the relationship

between the incidence of the DPAD in each state and that state’s unemployment rate. A negative,

but insignificant, correlation was found. This may indicate that states with a higher incidence of

DPAD also tend to have a slightly lower unemployment rate.

5. Is the DPAD related to an increase in employment in DPAD-related industries

over time?

The DPAD was first implemented in 2005 at a rate of three percent of domestic production

taxable income then, increased to six percent in 2007, and nine percent in 2010. The incentive

effects of the DPAD might be expected to result in an increase in the U.S. employment totals in

DPAD-intensive industries over time. To investigate this relationship, the percentage increase in

U.S. employment from 2003 to 2009 was computed for each industry. A correlation analysis

was done between the DPAD/DTI and the Employment Change variables, and it was found that

Alabama 0.0186 9.9 Louisiana 0.0253 6.6 Ohio 0.0166 10.1

Alaska 0.0192 7.7 Maine 0.0142 8.1 Oklahoma 0.0197 6.7

Arizona 0.0137 9.9 Maryland 0.0128 7.4 Oregon 0.0266 11.1

Arkansas 0.0189 7.5 Massa-chusetts 0.0153 8.2 Pennsylvania 0.0151 8

California 0.0174 11.3 Michigan 0.0161 13.4 Rhode Island 0.0118 10.9

Colorado 0.0166 8.1 Minnesota 0.0169 8 South Carolina 0.0178 11.5

Connecti-cut 0.0125 8.2 Mississippi 0.0191 9.4 South Dakota 0.0161 5.2

Delaware 0.0092 7.9 Missouri 0.0159 9.4 Tennessee 0.0161 10.5

Florida 0.0116 10.4 Montana 0.0155 6.1 Texas 0.0199 7.5

Georgia 0.0160 9.8 Nebraska 0.0165 4.7 United States 0.0163 9.9

Hawaii 0.0106 6.9 Nevada 0.0113 11.6 Utah 0.0171 7.6

Idaho 0.0194 7.4New

Hampshire0.0159 6.2 Vermont 0.0156 6.9

Illinois 0.0149 10 New Jersey 0.0119 9 Virginia 0.0147 6.9

Indiana 0.0204 10.4 New Mexico 0.0180 6.8 Washington 0.0197 9.4

Iowa 0.0192 6.2 New York 0.0123 8.3 West Virginia 0.0169 7.7

Kansas 0.0184 7.2 North Carolina 0.0182 4.1 Wisconsin 0.0189 8.7

Kentucky 0.0187 10.3 North Dakota 0.0188 5 Wyoming 0.0238 6.3

Table 3 – State DPAD Importance and Unemployment Rate

State

DPAD

Impor-

tance

2009

Unemploy-

ment Rate

State

DPAD

Impor-

tance

2009

Unemploy-

ment Rate

State

DPAD

Impor-

tance

2009

Unemploy-

ment Rate

Domestic Production Activities Deduction and U.S. Employment

7

these two variables are negatively correlated, with a correlation coefficient of -0.49799

(p=0.0002). This indicates that the more important the DPAD is to an industry (the higher the

DPAD/DTI ratio is), the lower the increase in employment in that industry over time. This

would seem to indicate that the DPAD is actually decreasing employment in the industries in

which it is more important – a counterintuitive result. However, it is more likely that the DPAD

is actually targeting the industries that it was intended to – those for which the U.S. continues to

lose jobs. While it is possible that the DPAD is reducing the job losses in these industries, the

other factors (lower costs and fewer regulations offshore, economic downturn) that are causing

these losses are apparently swamping any positive effect there might be from the DPAD.

Table 4 – Industry DPAD Importance and Employment Change

BEA

Id Industry Name

DPAD/

DTI

Employ-

ment

Change

BEA

Id Industry Name

DPAD/

DTI

Employ-

ment

Change

104 Crop and animal

production (Farms) 0.0481 -6.10% 140 Truck transportation 0.0006 1.88%

105 Forestry, fishing,

and related activities 0.0168 7.80% 141

Transit and ground

passenger transportation

0.0000 13.25%

106 Mining 0.0397 47.97% 142 Pipeline transportation

0.0002 5.74%

110 Utilities 0.0330 -0.72% 143 Other transportation

and support activities 0.0008 0.16%

111 Construction 0.0418 -10.14% 144 Warehousing and

storage 0.0060 25.59%

114 Wood product manufacturing

0.0500 -32.70% 146 Publishing industries, except Internet

0.0817 -13.12%

115

Nonmetallic mineral

product manufacturing

0.0563 -23.82% 147

Motion picture and

sound recording industries

0.0799 1.69%

116 Primary metal

manufacturing 0.0523 -22.18%

148,14

9

Broadcasting and

telecommunications

Information and data processing services

0.0329 -11.90%

117

Fabricated metal

product manufacturing

0.0567 -11.60% 151

Federal Reserve banks, credit

intermediation and

related services

0.0022 -2.79%

118 Machinery

manufacturing 0.0496 -12.20% 152

Securities,

commodity contracts, investments

0.0006 73.36%

119

Computer and

electronic product

manufacturing

0.0660 -17.59% 153 Insurance carriers and related activities

0.0002 3.78%

120

Electrical

equipment,

appliance, and component

manufacturing

0.0762 -20.84% 154

Funds, trusts, and

other financial vehicles

0.0007 117.35%

Domestic Production Activities Deduction and U.S. Employment

8

121, Motor vehicle, body,

trailer, and parts

manufacturing

0.0477 -23.99% 156 Real estate 0.0002 29.88%

122

123

Furniture and related

product

manufacturing

0.0498 -34.53% 157

Rental and leasing

services and lessors

of intangible assets

0.0098 -12.51%

124 Miscellaneous manufacturing

0.0531 -7.06% 158

Professional,

scientific, and

technical services

0.0141 14.21%

126

Food and beverage

and tobacco product manufacturing

0.0546 -3.33% 162

Management of

companies and enterprises

0.0013 15.11%

127 Textile mills and textile product mills

0.0409 -43.80% 163

Administrative and

waste management

services

0.0027 7.39%

128 Apparel and leather and allied product

manufacturing

0.0057 -37.99% 166 Educational services 0.0037 23.99%

129 Paper manufacturing 0.0891 -23.46% 168 Ambulatory health care services

0.0021 24.65%

130 Printing and related

support activities 0.0408 -22.10% 169

Hospitals and nursing and residential care

facilities

0.0002 10.51%

131

Petroleum and coal

products manufacturing

0.0602 -1.39% 170 Social assistance 0.0014 21.46%

132 Chemical manufacturing

0.0260 -11.75% 172

Performing arts,

spectator sports, museums, and related

services

0.0080 17.81%

133 Plastics and rubber products

manufacturing

0.0551 -24.14% 173 Amusement, gambling, and

recreation

0.0000 11.48%

134 Wholesale trade 0.0129 -0.30% 175 Accommodation 0.0062 -0.30%

135 Retail trade 0.0028 -2.58% 176 Food services and

drinking places 0.0088 9.69%

137, 138,

139

Air transportation 0.0002 -13.34%

6. What are the tax treatments of the DPAD for state tax purposes in the various

states, and how might the various state tax rates be affecting the effectiveness of

the DPAD in those states?

Table 5 contains data on the treatment of the DPAD in the various states. In all, 21 states

conform to the U.S. Federal Income Tax treatment of the DPAD, and 23 states and the District of

Columbia do not allow the DPAD as a deduction. Four states (Nevada, South Dakota,

Washington, and Wyoming) do not have a corporate tax against which the DPAD can be used as

a deduction. Kentucky only allows a reduced DPAD of six percent, and Virginia only allows a

Domestic Production Activities Deduction and U.S. Employment

9

reduced six percent DPAD until 2013, after which time a nine percent DPAD will be allowed.

Given that the DPAD-related tax savings from the federal income tax is not enough to impact the

employment levels in various industries, it not likely that the DPAD-related tax savings from the

smaller state tax rates will have any measurable effect on employment. In fact, many of the

states that don’t allow the DPAD as a deduction are the states with higher income tax rates

(California, Washington D.C., Maine, Minnesota, New Jersey), and a number of the states that

do allow it are the states with lower income tax rates (Arizona, Colorado, Florida, Utah). This

combination of associations also makes it unlikely that DPAD-related state corporate income tax

savings will have much effect on employment in the various industries or states.

Table 5 – State Tax Treatment of the DPAD

State Conforms to Federal

Maximum Corp. Rate

Notes, Citations

Alabama Y 6.5%

Alaska Y 9.4%

Arizona Y 6.5%

Arkansas N 6.5%

California N 8.84% No deduction is allowed for the DPAD.

Colorado Y 4.63%

Connecticut N 7.5% For years beginning on or after January 1, 2009, the DPAD is disallowed. [Conn. Gen. Stat. §12-217(a)(1).]

Delaware Y 8.7%

District of Columbia

N 9.975% No deduction is allowed for the DPAD. [D.C. Code Ann. §47-1803.03(a-1).]

Florida Y 5.5%

Georgia N 6% No deduction is allowed for the DPAD. [Ga. Code Ann. §48-1-2(14); Ga. Code Ann. §48-1-2(14.2).]

Hawaii N 6.4% No deduction is allowed for the DPAD. [Haw. Rev. Stat. §235-2.3(b)(14); Hawaii Dept. of Taxation Announcements 2005-12, 08/03/2005.]

Idaho Y 7.4%

Illinois Y 7%

Indiana N 8% No deduction is allowed for the DPAD. [Ind. Code §6-3-1-3.5(b)(8).]

Iowa Y 12%

Kansas Y 7%

Kentucky Y/N 6% For taxable years beginning on or after January 1, 2010, Kentucky limits the deduction percent to 6% (rather than 9%). [Ky. Rev. Stat. Ann. §141.010(13)(c); Ky. Rev. Stat. Ann. §141.010(13)(d).]

Louisiana Y 8%

Maine N 8.93% No deduction is allowed for the DPAD. [Me. Rev. Stat. Ann.36 §5200-A(1)(S); Instructions to Form 1120-ME.]

Maryland N 8.25% No deduction is allowed for the DPAD. [Md. Code Ann. Tax-Gen. §10-305(d)(4) .]

Massachusetts N 8% No deduction is allowed for the DPAD. [Mass. Gen. L.Chapter 63 §1; Mass. Gen. L.Chapter 63 §30(4).]

Michigan N 6% No deduction is allowed for the DPAD. [Mich. Comp. Laws Ann. §206.607(1); Corporate Income Tax FAQ—Corporate Tax Base 1, 11/22/2011.] Michigan Business Tax. No deduction is allowed for the DPAD. [Mich. Comp. Laws Ann. §208.1109(3); Michigan Business Tax FAQ B44, 08/26/2009; Michigan Business Tax FAQ M68, 08/26/2009.]

Minnesota N 9.8% No deduction is allowed for the DPAD. [Minn. Stat. §290.01, Subd. 19c(17).]

Mississippi N 5% No deduction is allowed for the DPAD.

Missouri Y 6.25%

Montana Y 6.75%

Nebraska Y 7.81%

Nevada NCT

New Hampshire N 8.5% No deduction is allowed for the DPAD. [N.H. Rev. Stat. Ann. §77-A:1, XX(l).]

New Jersey N 9% No deduction is allowed for the DPAD. [N.J. Rev. Stat. §54:10A-4(k)(2)(J)., N.J. Admin. Code §18:7-5.2(a)(1)(xx).]

New Mexico Y 7.6%

Domestic Production Activities Deduction and U.S. Employment

10

New York N 7.1% Effective January 1, 2008, no deduction is allowed for the DPAD. [N.Y. Tax Law §208(9)(b)(19); N.Y. Tax Law §210(1)(a); N.Y. Tax Law §210(3)(d); NYCRR20 §3-2.2(b).]

North Carolina N 6.9% No deduction is allowed for the DPAD. [N.C. Gen. Stat. §105-130.5(a)(17) .]

North Dakota N 5.15% No deduction is allowed for the DPAD. [N.D. Cent. Code §57-38-01.3(1).]

Ohio Y 8.5%

Oklahoma Y 6%

Oregon N 7.6% No deduction is allowed for the DPAD. [Or. Rev. Stat. §317.398.]

Pennsylvania Y 9.99%

Rhode Island Y 9%

South Carolina N 5% No deduction is allowed for the DPAD. [S.C. Code Ann. §12-6-50(7), S.C. Code Ann. §12-6-1130(13).]

South Dakota NCT

Tennessee N 6.5% No deduction is allowed for the DPAD. [Tenn. Code Ann. §67-4-2006(b)(1)(L).]

Texas N 1% of taxable margin

No deduction is allowed for the DPAD. [Tex. Tax Code Ann. §171.1011(c)(1); Tex. Admin. Code34 §3.587(d)(1).]

Utah Y 5%

Vermont Y 8.5%

Virginia Y/N 6% Virginia treatment. For tax years 2010, 2011, and 2012, Virginia allows only 2/3 of the IRC §199 deduction, or 6%. For taxable years beginning on or after January 1, 2013, the 9% rate can be used. [Va. Code Ann. §58.1-402; Va. Code Ann. §58.1-301(B)(5) ; Virginia Tax Bulletin 12-1, 02/09/2012.]

Washington NCT

West Virginia N 7.75% No deduction is allowed for the DPAD. [W. Va. Code §11-24-6a.]

Wisconsin N 7.9% For tax years beginning after December 31, 2008, no deduction is allowed for the DPAD. [Wis. Stat. §71.22(4)(um); Wisconsin Dept. Rev. Tax Bulletin 162, 07/01/2009.]

Wyoming NCT

NCT = No corporate tax in the state.

7. Conclusions and Policy Implications

Consistent with its purpose when enacted, the DPAD (as shown in Table 1) appears to be deducted

most heavily in those industries that are more related to production, and less related to the providing of

services. Table 2 shows that the DPAD benefits some states, such as Oregon, Louisiana and Wyoming,

much more on a relative basis than it benefits other states that depend more heavily on services, such as

Nevada, Hawaii, and Delaware. Unfortunately the states that benefit most (on a relative basis) from the

DPAD are not the states with the highest unemployment rates. A negative, but insignificant, correlation

was found between the importance of the DPAD to a state and the unemployment rate in that state.

However, it should be noted that while it might be more desirable for the DPAD and unemployment rates

in the states to be positively correlated, this was not an explicit goal of the DPAD when enacted.

This study also compared the measure of importance of the DPAD to an industry (DPAD/DTI) in

2009 to that industry’s percent growth in employment over the time period 2003-2010 in order to see if

the DPAD had, in fact, had a positive effect on employment in those industries. However, the

DPAD/DTI ratio was actually negatively (correlation coefficient = -0.48799) and very highly (p=0.0002)

correlated with employment increases/decreases in an industry, indicating that the factors that already

contribute to offshoring of production may continue to more than offset the tax savings from the DPAD.

Twenty-one states allow the same DPAD deduction to corporate taxable income that the U.S. tax

code allows. However, 23 states allow no DPAD deduction at all, and some of those states have

relatively higher state income tax rates. A deduction against income at these higher tax rates presumably

would provide more of an incentive to increase production in these states than would a comparable

deduction in low tax states.

Domestic Production Activities Deduction and U.S. Employment

11

Policy Implications. The policy implications of this study are as follows:

1. The primary implication of this study is that in order to effectively offset the other factors that

contribute to offshoring, the DPAD percentage would need to be increased. As currently

constituted, the DPAD is not successful in preventing offshoring in production industries. Even

at a deduction rate of nine percent, the DPAD is only equivalent to a tax rate reduction of 3.15

percent (9% DPAD X 0.35 marginal tax rate = 3.15%). This effectively brings the maximum

U.S. tax rate on U.S. productive activities down to 35-3.15 = 31.85%. A doubling of the DPAD,

as the president proposed for advanced manufacturing activities in the last State of the Union

address, would reduce the effective corporate tax rate on such income to 28.7 percent – close to

the 28 percent rate to which Mitt Romney is proposing to reduce the top marginal corporate tax

rate, and close to the top rate suggested by the Simpson-Bowles Commission. This would seem

to be an area in which compromise might be reached.

2. Another policy implication of this study is that it illuminates some of the problems inherent in

reducing rates in order to accomplish policy objectives. The reduction of overall corporate tax

rates in order to encourage production in the U.S., without related reductions in other deductions,

would be very expensive from a budget point of view, but might not result in the desired outcome

of reducing offshoring. A targeted “rate reduction” such as the DPAD might be a more effective

means of accomplishing this policy objective.

3. The fact that there are so many states that don’t allow the DPAD as a deduction for state income

taxes probably reduces its effectiveness. States that don’t allow the DPAD should consider

making the appropriate changes to allow it. If the state tax rate is eight percent, for example,

allowance of the DPAD is equivalent to a tax rate reduction of .72 percent (8% X 9% DPAD rate

= 0.72%). This is approximately 23 percent of the effective rate reduction from the federal

DPAD deduction – a significant amount.

Domestic Production Activities Deduction and U.S. Employment

12

References

Chen, D. and J. Mintz, 2011. “New Estimates of Effective Corporate Tax Rates on Business

Investment,” CATO Institute, February 2011.

Dyreng, S., M. Hanlon, and E. Maydew, 2008. “Long-run Corporate Tax Avoidance,” The

Accounting Review 83: 61 – 82.

Grove, A. 2010. “How America Can Create Jobs,” Business Week (July 1, 2010).

http://www.businessweek.com/magazine/content/10_28/b4186048358596.htm

Healy, B., 2011. “Millions in Profits and a Tax Bill ($0) to Envy,” The Boston Globe (May 1,

2011).

http://www.boston.com/business/taxes/articles/2011/05/01/millions_in_profits_and_a_tax_

bill_0_to_envy_in_massachusetts/

Hodge, S.A., 2011. “Countdown to #1: 2011 Marks 20th year that U.S. corporate tax rate is

higher than OECD average,” Tax Foundation (March 9, 2011).

Internal Revenue Service. 2009. Corporation Income Tax Returns (Statistics of Income-2009)

Washington, DC 2012.

Leonhardt, D., 2011. “The Paradox of Corporate Taxes,” New York Times (February 1, 2011).

http://www.nytimes.com/2011/02/02/business/economy/02leonhardt.html

Morrow, M., Ricketts, R., and L. Tunnell, 2011. “Effective Corporate Tax Reform: Reducing the

Corporate Tax Burden by Increasing the Section 199 Deduction,” Presented at the 2011

National Meeting of the National Taxation Association (November 14, 2011).

Obama, B., 2011. State of the Union Address. (January 25, 2011).

http://www.whitehouse.gov/the-press-office/2011/01/25/remarks-president-state-union-

address

Wessel, D., 2011. “Big U.S. Firms Shift Hiring Abroad,” The Wall Street Journal (April 19,

2011).

http://online.wsj.com/article/SB10001424052748704821704576270783611823972.html