the effect of organizational culture and ethical orientation on accountants ethical judgments

TRANSCRIPT

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 1/22

The Effect of Organizational

Culture and Ethical

Orientation on Accountants '

Ethical Judgments

Patricia Casey Douglas

Ronald A Davidson

Bill N Schwartz

ABSTRACT. This paper examines the relationship

between organizational ethical culture in two large

international CPA firms, auditors' personal values and

the ethical orientation that those values dictate, and

judgments in ethical dilemmas typical of those that

accountants face. Using an experimental task con-

sisting of multiple judgments designed to vary in

moral intensity (Jones, 1991), and unique as well

as tried-and-true approaches to variable measure-

ments, this study examined the judgments of more

than three hundred participants in our study.

ANCOVA and path analysis results indicate that: {1)

Ethical judgments in situations of high moral inten-

sity are affected by personal values and by environ-

mental variables, such as the professional code of

conduct (direct and indirect effects) and previous

ethics instruction {direct effect only). (2) Corporate

ethical culture, and a relatively strong firm rules-

orientation, affect auditors' idealism but not rela-

tivism, and therefore indirectly affect ethical judg-

ments. Jones' (1991) moral intensity argument is

supported: differences in the characteristics of specific

judgment tasks apparently result in different decision

processes.

KEY WORDS: ethics, ethical judgment, ethical

orientation, moral intensity, organizational ethical

culture, personal values

The accounting community has been concerned

about professional ethics since the American

Association of Public Accountants first adopted

ethical rules in 1905 {Casler, 1964), and accoun-

tants' ethics have been subject to increased

scrutiny over the ensuing decades. Armstrong

(1987, p. 27) described the atmosphere in recent

years as a crisis of confidence and cre dibihty

for the profession. In particular, aspersions of

fraudulent fmancial reporting led the Treadway

Commission (1987, p. 23) to comment on the

combustible mixture of incentives and oppo r-

tunities to commit fraud and suggest that

personal values and codes of conduct are impor-

tant deterrents to such unethical acts {p. 35).

The Commission's recommendations were dis-

cussed more recently under a Wall Street ournal

headline asserting that ethics appear to be a

w rit e off for many executives {Blalock, 1996,

p. C l [discussing Brie f et al., 1996]). Brief et al.

found that the relationship between personal

values, codes of conduct and decisions to engage

in financial misrepresentation are weak at bes t

{p. 184). Arthur Brief (one of the study's authors)

calls this finding really disa ppo intin g {Blalock,

1996, p. Cl), and James Treadway {former SEC

commissioner and head of the Treadway

Co mm ission ) calls it very distressing {p. C1 3) .

Brief et al. (p. 193) also conclude that these

findings imply additional importance for the

Commission's other recommendation: creation of

a strong ethical climate within the organization,

characterized as essential to preventing unethical

acts {Treadway, 1987, p. 56).

This paper reports on a study of ethical

decision-making in public accounting, which

tests the Treadway Commissions' assertions about

the effect of an ethical organizational environ-

ment. The study investigated the effects of

personal values and other factors on accountants'

judgments of ethical dilemmas typical of those

encountered in practice. Factors include demo-

graphic variables, previous ethics instruction,

familiarity with the profession's code of conduct,

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 2/22

102

Patricia Casey Douglas et al.

professional experience, position within the firm

and, most significantly, organizational ethical

culture as it is represented by perceptions of the

firms' shared values and practices.

ackground and hypothesis development

Models of the ethical decision process provide a

general consensus that two influences predomi-

nate in ethical decisions: they share the view -

point that ethical decision making in

organizations is a function of individual as well

as organizational factors (Akaah and Riordan,

1989, p. 113 [emphasis added]). Among the prin-

cipal conceptual models, Trevino (1986) focuses

on Kohlberg's moral development in her identi-

fication of individual influences, but Ferrell and

Gresham's (1985) and Hunt and Vitell's (1986)

models include the person l v lues of the decision

maker. Ferrel and Gresham (p. 89) include values

along with knowledge, attitudes and intentions

as primary influences on jud gm en t; H un t and

Vitell (p. 10) include them with in the dim en -

sions

of personal experiences. Both H unt and

ViteU (1986) and Trevino (1986) exphcitly posit

organizational ethical culture as an organ izational

factor influencing ethical behavior; Ferrell and

Gresham include it with significant others and

professional codes of conduct as secondary influ-

ences on judgment (p. 89).

Personal values

Personal values are a classification of the hun dred s

of thousands of beliefs that individuals con-

sciously or unconsciously hold about the world

in which they live (Rokeach, 1972, p. 1). Values

are distinguished from other beliefs by their

content. They are enduring beliefs that certain

modes of conduct (e.g., fairness) or end-states

of existence (e.g., equality) are preferable to the

alternatives (p. 160). Values guide jud gm en ts and

actions across specific objects and situations and

beyond immediate goals.

Despite such theoretical support, Brief et al.

(1996, p. 184) not e the pauc ity of em pirical

research addressing the potential relationship

between particular values that individuals hol

and engag eme nt in fraudulent behavior. Indee

Brief et al. (1991, p. 380) observed values to

related to ethical decisions only under condition

of low acc ounta bility (i.e., few pressures

justify one's opinions to oth ers [p. 382]). Th e

(1996) attempt to identify which of Rokeach

(1968, Values Survey ) eighteen term ina

(i.e., end -sta te ) values are associated wi

fraudulent financial reporting revealed on

modes t magn itudes of corr elati on (p. 188) an

weak and inconsisten t relationships (p. 19

with subjects' willingness to commit fraud.

Rokeach's Values Survey (1968) provides

generalized assessment of subjects' preferences f

a prosperous life, a world at peace, fami

security, etc. Forsyth's (1980) taxonomy of ethic

ideologies is more specific. As Forsyth describ

it, an individual's ethical orientation (i.e., ethic

value system) may be described most parsimo

niously by his position with respect to two bas

factors. The first factor is the extent to whic

he rejects universal moral rules in favor of

mo re relativist approach to moral decision

Relativists believe that there are many ways t

look at moral issues and are skeptical of specif

ethical principles (p. 175). The second factor

the extent to which an individual assumes th

good consequences always can be obtained (a

idealist approach) rather than adm itting th

consequences are often a mix or good and ba

(p. 176). In general, the stance an individual tak

with respect to these two factors will influenc

the ethical judgments reached (p. 183). Figure

presents the four possible ethical orientation

(i.e.,

combinations of high/low idealism an

relativism), labeled situationism, absolutism, su

jectivism, and exceptionism), with Forsyth's (199

descriptions.

Forsyth's taxonomy has proven useful i

explaining differences in moral judgmen

(Forsyth, 1980, 1992; Ar ringto n and Rec ker

1985;

Douglas and Schwartz, 1999; Douglas an

Wier, 2000) and sensitivity to ethical issue

(Shaub et al., 1993).

Conceptual models of ethical decision-makin

(e.g., Ferrell and Gresham, 1985; Hunt an

Vitell, 1986) suggest and prior research (e.g

Forsyth, 1981, 1992) demonstrates that person

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 3/22

The Effect of Organizational Culture and Ethical Orientation

103

High Idealism

Low Idealism

Adapted from Forsyth (1980, 1992).

High relativism

Situationist

Reject moral rules; ask if the

action yielded the best possible

outcome in the given situation.

Subjectivist

Reject moral rules; base moral

judgments on personal feelings

about the action and the setting.

Low relativism

Absolutist

Feel actions are moral provided

they yield positive consequences

through conformity to moral rules.

Exceptionist

Feel conformity to moral rules is

desirable, but exceptions to these

rules are often permissible.

Figure 1. Taxonomy of ethical ideologies .

values provide the basis for moral judgments.

Previous contradictory fmdings (e.g., Brief et al.,

1991;

Brief et al., 1996) and the specificity of the

judgment task in this study (i.e., ethical dilemmas

specific to public accounting practice) make the

direction of the hypothesized effect an empirical

question. The first hypothesis is based upon this

line of reasoning and stated in the null form:

H Q I : Ethical orientation and ethical judg-

ments are not related.

Jones (1991) argues that differences in charac-

teristics of a moral issue itself its mor l intensity

affect individuals' responses to the issue. Models

of ethical decision-making that fail to consider

details of the ethical issue imply that individual

decisions and behavior are identical for all moral

issues. For exam ple, people will decide and

behave in the same manner whether the issue is

the theft of few^ supplies from the organization

or the release of a dangerous product to the

ma rket (p. 371). This is neithe r intuitively

correct nor consistent with the prior research that

Jones discusses (pp. 371-372).

Jones identifies the six characteristics of moral

issues indicated in Figure 2, which he aggregates

into a single moral intensity construct. Moral

intensity is expec ted to cha nge if there is a

change in any one of its components, although

it is impossible to precisely specify . . . the rela-

tionships between the moral intensity construct

and its co m po ne nts (p. 378). Jones argues that

these characteristics should be aggregated into a

single construct because they are all components

of the moral issue itself and are expected to have

interactive effects. He cautions that me asu re-

ment of moral intensity and its components is

probably possible only in terms of relatively large

distinctions (p. 378). There fore, this study

attempted to represent the moral intensity

variable at only two levels, high (i.e., high on

more than three of the six components) and low.

These variations in moral intensity were repre-

sented in the content of the vignettes developed

for this study as discussed later in this paper's

methodology section.

Becau se differences in jud gm en ts may result

from differences in the moral intensity of the

ethical issues under consideration, two additional

hypotheses were used to test for this effect:

H pla : Ethical orientat ion and ethical jud g-

ments in situations of high moral

intensity are not related.

H o l b :

Ethical orientation and ethical judg-

ments in situations of low moral inten-

sity are not related.

Organizational ethical culture

Organizational culture is, at its core, a system of

common values. Personal values begin to develop

early in Hfe and, like the more general beliefs, are

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 4/22

104

Patricia Casey Douglas et al

1. Magnitude of consequences: the sum of the detriments or bene6ts done to victims or beneficiaries of

the act.

2. Social consensus: the degree of social agreement that the act is good or bad.

3. Probability of effect: the joint probability that the act will actually take place and that it will cause the

detriment or benefit predicted.

4. Temporal immediacy: the length of time between the present and the onset of the act's consequences.

5. Proximity: the feeling of nearness (social, cultural, psychological, or physical) that the moral agent has

for victims (beneficiaries) of the . . . act (p. 376).

6. Concentration of effect: an inverse function of the number of people affected by the act.

Figure 2. Com ponents of moral intensity.

organized into hierarchical systems with describ-

able and measurable properties and observable

behavioral consequences. Because personal values

are mo re central, or close r to [one's] person ality

than other constructs such as attitudes and

opin ion s (Ravlin and M eglino, 1987, p. 156),

they resist change to an even greater degree.

Early social-psychological theories of belief

systems (e.g., Rokeach, 1972) describe value

change as a cognitive process, the result of a

basic human need for cognitive consistency.

Modification of the personal value system was

thought to result from efForts to reduce a per-

ceived inconsistency among an individual's atti-

tudes, values and behavior, or between his and

some significant other's attitudes, values, motives

or behavior (p. 165). More recent belief system

theory (e.g., Grube et al., 1994, p. 156) postu-

lates that change is an ffective process, the result

of a need to feel self-satisfied with one's own

competence and morality. Both the cognitive and

affective perspectives are consistent with the

many studies reviewed in Grube et al. which

demonstrate that personal values can be changed

through a process termed value self confrontation

Individuals presented with feedback concerning

their own and significant others' values, attitudes

and behaviors are motivated to change values,

attitudes and behaviors not consistent and to

maintain those that are consistent with the

referent norm (p. 157). Both perspectives are

consistent with theories of socialization and

organizational culture.

Fogarty (1992, p. 130) defines socialization as

the process by which individuals are molded by

the society to which they seek full membership.

This mo ldin g requires a modification o

reflexes (i.e., person al values, attitude s an

behaviors) through instruction received in th

social environment. Business and profession

organizations shape themselves in response to th

demands of their environment and provid

members with incentives to adopt attributes con

sistent with that milieu. Socialization plays a

even more important part in professional org

nizations like accounting firms, where neith

employee behavior nor output relevant to th

desired performance is measurable. These org

nizations must rely on clan control (Ouchi, 19

1980) or the operation of strong common value

to control possible opportunism and the ineff

ciencies caused by incongruent individual an

organizational goals.

The system of common values that Ouch

(1979,

1980) describes is but part of the overa

organizational culture. Values are the core o

organizational culture, manifested in organiz

tional practices. Values describe what should b

while practices describe what is (Pratt an

Beaulieu, 1992, p. 668). Brief et al (199

p.

193) call it organ ization al climate - the 'fe

of an organization; [that is,] . . . the perception

of organizational members about how organiz

tions function a nd /o r what is imp orta nt in the

organizations. Perceptions of organization

culture are based upo n the conditions peop

experience in their organizations the even

practices, procedures, and rewarded, supporte

and expected behaviors that characterize th

organ ization (p. 194).

Organizational ethical culture or, more speci

ically, the ethical environment within the firm

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 5/22

The Effect

of

Organizational ulture

nd

Ethical Orientation

105

created through management practices and

espoused values,

may be the

most important

deterrent to unethical behavior. The Treadway

Commission's (1987,

p. 56)

study

of

fraudulent

financial reporting concluded with respect to

public accounting firms that the tone that top

management sets is an essential factor in devel-

oping a strong ethical climate within the orga-

nization. In perhaps the only empirical study of

ethical culture or the in public accounting firms

to date. Finn et al (1988) fmd that by discour-

aging unethical behavior top management can

reduce the ethical problems that subordinates

perceive.

Ponemon and Glazer's (1990) results su ggest,

and Douglas

and

Schv^artz (1990) conf irm, that

socialization in the acc oun ting profession actually

begins during college with students' first

exposure to professional values and behavior.

Shaub

et al.

(1993,

p. 153)

find mixed evidence

of the ability of the organization to either

change

an

auditor's ethical orientation

to

match

its own, or to provide an environment that

closely matches an auditor 's norms. Ponem on

(1990, 1992) confirms the existence of a

selection-socialization mechanism operating to

control ethical reasoning

in

public accounting

firms. In essence, selection-socialization causes a

firm to hire and prom ote individuals who fit into

the prevailing firm culture and causes individ-

uals unable to fit into that culture to leave.

Jeffrey and W eatherho lt (1996) fmd no

evidence of differences in moral development

between accountants employed in private enter-

prise

and

those

in

public accounting,

or

among

Big Six auditors employed at different ranks

within their respective firms (i.e.,

no

evidence

of a sociahzation process with respect

to

ethical

decision-making

in

public acco unting firms).

They do find differences across offices of different

firms and across offices within

the

same firm,

suggesting the effect of organizational culture.

These theories

of

value chang e, se lection,

socialization, organizational culture - together

with prior empirical evidence from these and

other studies,' suggest that organizational ethical

culture may act to modify personal values within

the organization. The direction and magnitude

of effect would

be

determined

by

specifics

of

the

culture (i.e., particular practices

and

shared values

espoused). As we know of no previous study of

ethical culture within

CPA

firms that would

provide the specifics necessary to hypothesize the

direction

of

affect,

the

second hypothesis

is

stated

in the null form:

HQ2: Ethical orientat ion and organizational

ethical culture are not related.

Theo ry and evide nce discussed above also

suggest that organizational ethical culture may

affect individuals' judgment in situations with an

ethical component, and that the effect may be

either direct (e.g.,

the

result

of a

rules-vs-indi-

vidual judgment approach

on the

part

of the

firm, previous ethics training, or the strength of

professional codes

of

conduct)

or

indirect (e.g.,

the result of environm ental infiuences a cting to

shape the individual decision-maker's personal

values).

The

direction

of

this hyp othe size d effect

would be determined by the particular culture

and by specifics of the judg me nt task. Therefore,

the third hypothesis

is

also stated

in the

null

form:

H Q

Organizational ethical culture

and

ethical judgments

are not

related.

Again, separate hypotheses were used

to

test

for

the effect of differences in moral intensity:

HQ3a: Orga nizational ethical culture and

ethical judgm ents

in

situations

of

high

moral intensity are not related.

Ho 3b: Orga nizational ethical c ulture and

ethical judgments in situations of lo w

moral intensity

are not

related.

etho ology

Participants

in

this study were practicing accoun-

tants employed by two large, inte rnation al

accounting firms. Three hundred sixty-eight

auditors at various experience levels and positions

within the firms were tested in groups. Sixty-four

failed a man ipulation check built into the

experimental task

or did not

provide comp lete

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 6/22

106

Patricia Casey Douglas

et al.

response sets,^ resulting in a usable sample of 304

(82.6 ).'

Testing of subjects was done under the

auspices

of

a supportive public accounting firm,

who provided access

and

time

for

testing

at

their

regularly-scheduled training sessions. Training

sites

are

located

in

California, Florida,

and

Washington, D.C.; however, participants for these

sessions come from all over the United States.

Data from 103 staff, 136 seniors, and 65

managers are included in this study although dis-

tribution across positions varies by firm. One

firm provided more staff participants; the other

firm, more managers. Experimental materials

comprised an anony mou s, self-administered

questionnaire with multiple measures, generally

considered

to be the

least obtrusive

way to

eUcit

sensitive information. Completion of the ques-

tionnaire took less than 20 minutes, so excessive

length would not be expected to reduce atten-

tion to the materials.

Table

I

presents statistics

or

frequencies

for

demographic variables. The typical particip

was a 26 year-old (range 22 to 37 years), m

(predominates by 56.3 ) Sen ior (45.0 ; Sta

33.5 ; Managers 21.5 ), witho ut

CPA

cert

cation (53.4 ). N ot e that

the

observed betwe

firm demographic differences are driven by th

rank distribution difference:

age,

gender, mar

status, professional certification, and professio

group membership are strongly correlated w

position

p <

0.0001). Of these, only gen

is correlated with a variable of interest h

(ethical orientation) and is discussed later in t

study.

Variables: Measures

of

ethical orientation

Forsyth's (1980) Ethics Position Questionnai

(EPQ, Appendix A) was used to measure ide l

an d relatimsm the tw^o basic factors that m

p a r s i m o n i o u s l y d e s c r i b e an indiv idua l ' s e th i

value sys tem,

as

previou s ly discussed.

The EP

TABLE I

Sample demographics

w =

304*)

Age***

Gender**

Marital status**

Position**

Professional certification**

Professional group membership**

Intend

to

remain with current firm

Intend to remain in public accounting

125 Female

(43.7 )

187 Married

(66.3 )

138

Yes

(46.6 )

165 Yes

(56.9 )

24 7

Yes

(84.6 )

256 Yes

(87.4 )

Mean 26.14 SD 3.06)

Range 22-37

101 Staff (33.5 )

136 Seniors (45.0 )

65 Managers (21.5 )

161 Male

(56.3 )

95 No t marr

(33.7 )

15 8

No

(53.4 )

125 No

(43.1 )

45 No

(15.4 )

37 No

(12.6 )

* Responses may not total 304 due to missing values.

** Be twe en -firm difference significant at p < 0.01 (chi-square test).

*** Between-firm difference significant

zt p <

0.001

(two-tailed f-test).

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 7/22

The Effect of Organizational Culture and Ethical Orientation

107

presents a series of statements with w hich respon-

dents in the current study were asked to agree

or disagree on a nine point scale anchored

1 = Com pletely disagree and 9 = Completely

agree. Response s to idealism- and relativism-

specific statements were suninied to produce the

two variable scores.

The EPQ instrument has been used in prior

studies of both unde rgradu ate and g raduate

college students (Forsyth, 1980; Arrington and

Reckers, 1985; Douglas and Schwartz, 1999) and

practicing auditors (Shaub et al., 1993). AU attest

to the EPQs validity and psychometric proper-

ties.

Forsyth (1980), Arrington and Reckers

(1985), and Douglas and Wier (2000) demon-

strate that the measures can be used to explain

differences in moral judg me nts. Th e ins trum ent

as applied to current data again reveals that the

two dimensions are orthogonal (interscale cor-

relation of -0.10) and that the scales have

adequate internal consistency (Cronbach's alpha

of 0.84 for the idealism scale, 0.81 for relativism).

The idealism and relativism measures were

used to classify individuals into one of the four

ethical orientations, as indicated in Figure 1. This

was done using median splits of the idealism (five

subjects have the median score of 58) and rela-

tivism (15 subjects have the median score of 50)

scores. Because of the duplicated median scores,

the four orientations are not equal in size. The

split into high and low groups was made to make

the groups as equal in size as possible. This clas-

sification method results in 69 Exceptionists, 84

Subjectivists, 77 Absolutists, and 74 Situationists. *

Measures of organizational ethical culture

Hunt et al.'s (1989) five-item Corporate Ethics

Scale (CEP, Appendix B, Panel 1) was used to

measure perce ived organizational ethical culture th e

ethical environment w^ithin the firm created

through management practices and espoused

values - the ton e at the to p of the organiza-

tion. The CEP reflects the extent to which

employees perceive that managers act ethically,

are concerned about ethics in the organization,

and will reward or punish ethical or unethical

behavior (Bearden et al., 1993, p. 253). Hunt et

al. (1989) document the development of the five-

item scale used in the current study from a larger

pool of items (Hunt el al., 1984) and a sample

of over 1,200 respondents. Factor analysis and

coefficient alpha ^vere used to assess the dimen-

sionality and reliability of the scale. The CEP was

adapted for the current study only by substitu-

tion of the word firm for com pany in the

original as a concession to the organizational

structure of public accounting.

The five items in the CEP scale were summed

to form an overall index of organizational ethics

in the current study. Hunt et al. (1989) used a

seven-point response scale, but participants in this

study were asked to agree or disagree with its

statements on a nine-point scale to maintain con-

sistency with the EP Q and jud gm en t m easures.

This adjustment appears not to have affected the

scale's psychometric properties. Hunt et al.

(1989) reports Cronbach's alpha of 0.78, a uni-

dimensional factor structure, and beta coefficients

in models of CEP score and other factors as pre-

dictors of organizational comm itme nt r angin g

from 0.17 to 0.58 {p < 0.01) across four su b-

samples of the data. As applied in the current

study, data reveal Cronbach's alpha of 0 71 and a

unidimensional factor structure. Consistent with

the prior findings, a statistically significant cor-

relation (p = 0.0171) between CEP score and

response to a rough proxy, single-item measure

( intend to remain with current firm ) suggests

the CEP to be a predictor of organizational com-

mitment .

Other injluences

The five CEP questions in the questionnaire were

interspersed with others (Appendix B, Panel 2)

intended to assess and/or control for additional

environmental infiuences on personal values or

judgments suggested by the literature. They (and

their sources) are: explicitness of the firm's

policies, or a management emphasis on rules

versus jud gm en t (Brief et al., 1 991, p. 393); pro-

fessional involvement (Mayer-Sommer and Loeb,

1981,

p. 131); understanding of the profession's

code of conduct (Fulmer and Cargile, 1987,

p.

216); and previous ethics training in college^

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 8/22

108

Patricia Casey Douglas et al.

(Hiltebeitel and Jones, 1991, p. 272; Arm strong,

1993, p. 90). Inclusion of CEP items with these

others provides a less obtrusive way to question

the sensitive area of firm policies and practices.

Measures of judgment

A series of vignettes portraying situations

involving conflicts of interest, confidentiality,

favors for clients, and lowballing were used to

elicit measures of ethical jud gm en t. The se

vignettes were developed using an established

technique for assessing their validity: develop

vignettes based upon the literature, submit

vignettes to a panel of experts, pretest the

vignettes on subjects similar in characteristics to

the sample population (Cavanaugh and Fritzsche,

1985). Each vignette describes a situation and a

fictitious CPA's action, and participants are asked

to agree or disagree with the described action on

the scale previously described.

Some of these vignettes were based upon those

originally developed by Loeb (1971, excerpted

for this study with permission of the Institute of

Professional Accounting) and since used by other

researchers (e.g., Armstrong, 1984); others were

developed by Cohen et al. (1994, used with per-

mission of the authors). The situations described

are typical of those CPA's frequently cite as

ethical problems confronted in practice (i.e.,

conflicts of interest, ind epe nde nce , and f

proble ms [Finn et al., 1988, p. 613]). Th

instrument was pretested on a separate sample

40 accounting practitioners.

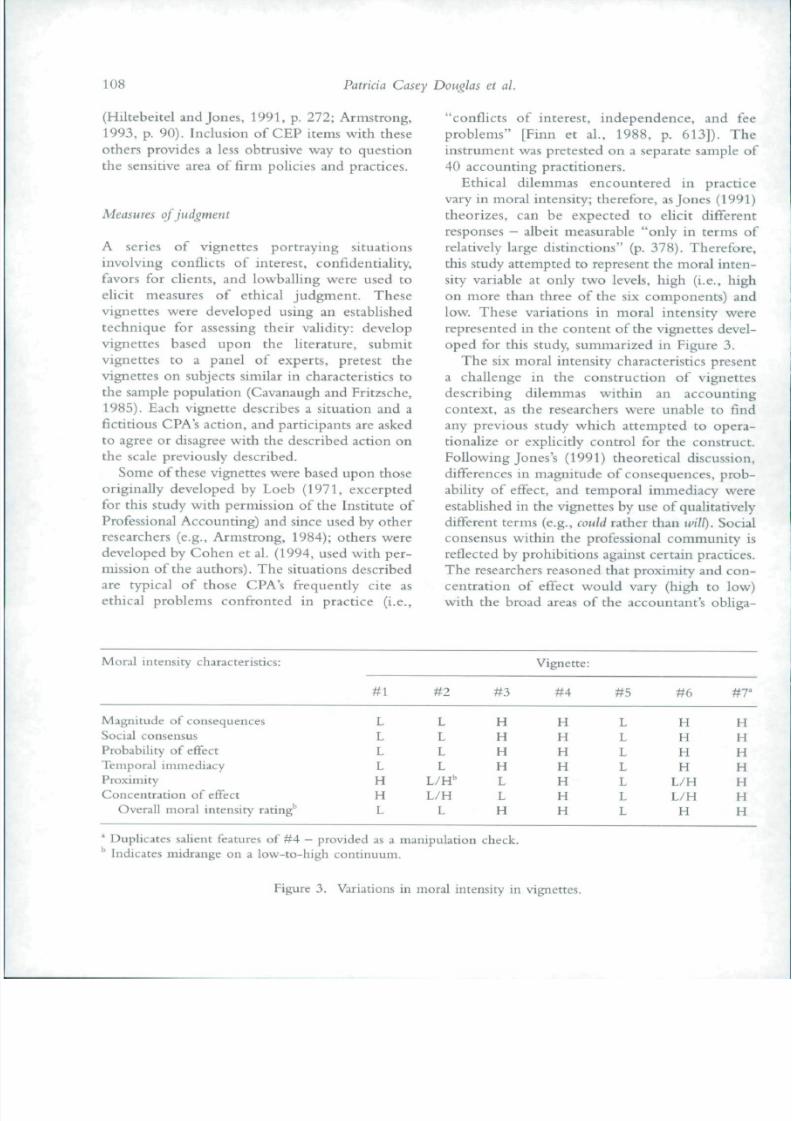

Ethical dilemmas encountered in practi

vary in moral intensity; therefore, as Jones (199

theorizes, can be expected to elicit difFere

responses - albeit measurable only in term s

relatively large distinc tions (p. 378). Th erefor

this study attempted to represent the moral inte

sity variable at only two levels, high (i.e., hig

on more than three of the six components) an

low. These variations in moral intensity we

represented in the content of the vignettes deve

oped for this study, summarized in Figure 3.

The six moral intensity characteristics prese

a challenge in the construction of vignett

describing dilemmas within an accountin

context, as the researchers were unable to fin

any previous study which attempted to oper

tionalize or explicitly control for the construc

Follow ing Jones's (1991) theoretica l discussio

differences in magnitude of consequences, pro

ability of effect, and temporal immediacy we

established in the vignettes by use of quahtative

difFerent terms (e.g., ould rather than wilt . Soc

consensus within the professional community

reflected by prohibitions against certain practice

The researchers reasoned that proximity and co

centration of effect would vary (high to low

with the broad areas of the accountant's oblig

Moral intensity characteristics:

Magnitude of consequences

Social consensus

Probability of effect

Temporal immediacy

Proximity

Concentration of effect

Overall moral intensity rating''

# 1

L

L

L

L

H

H

L

# 2

L

L

L

L

L / H '

L /H

L

# 3

H

H

H

H

L

L

H

Vignette:

# 4

H

H

H

H

H

H

H

# 5

L

L

L

L

L

L

L

# 6

H

H

H

H

L /H

L /H

H

#7

H

H

H

H

H

H

H

Duplicates salient features of #4 - provided as a manipulation check.

'' Indicates midrange on a low-to-high continuum.

Figure 3. Variations in moral intensity in vignettes .

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 9/22

The Effect of Organizational Culture and Ethical Orientation

9

tions represented in specific vignettes: obligations

to clients, to colleagues, and to the public.

The manipulated variable, moral intensity,

requires only two vignettes to represent the high-

versus-low possible states. However, Murphy and

Laczniak (1981, p. 262) suggest that an indi-

vidual s ethical decisions are represen ted best over

a variety of situations and decisions. Replication

also helps control for chance fluctuations in

responses. Therefore, three vignettes representing

each of the two states of moral intensity were

presented. An additional vignette that duplicated

the sahent features of one of the other six was

included to provide a manipulation check. Thus,

seven vignettes were presented to the subjects but

responses to only six comprise the judgments

measure.

Results

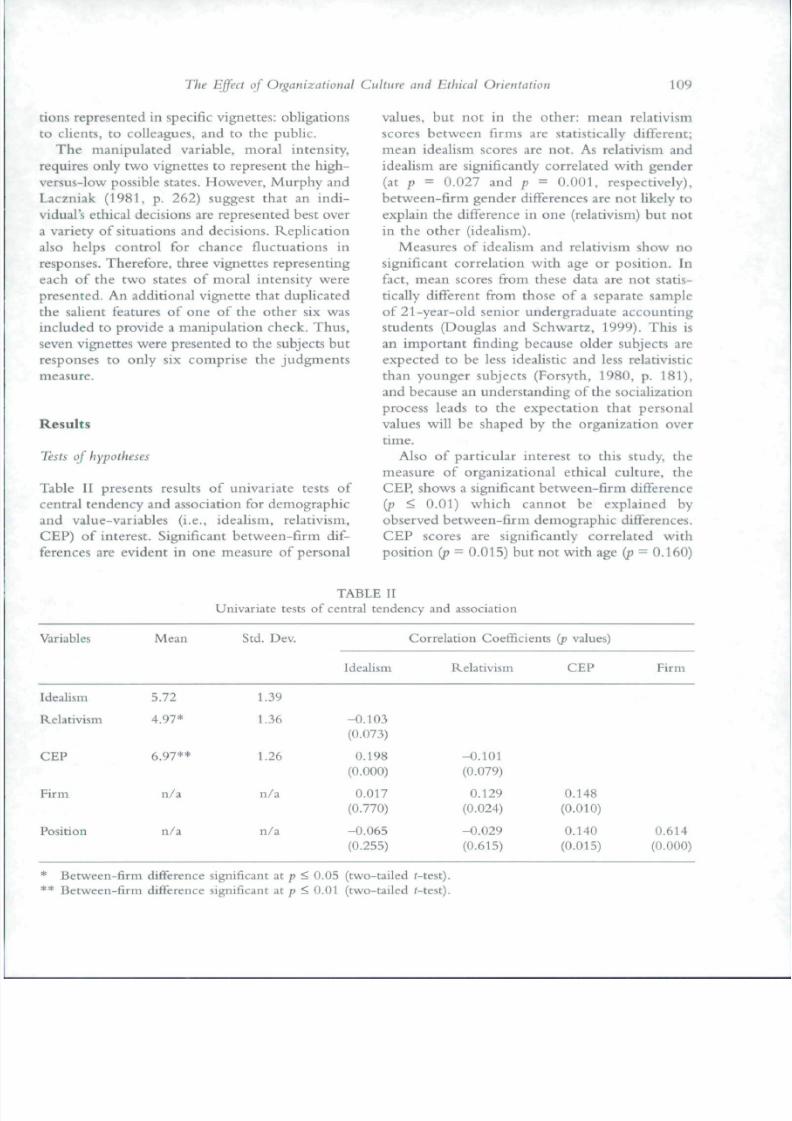

Tests of hypotheses

Table II presents results of univariate tests of

central tendency and association for demographic

and value-variables (i.e., idealism, relativism,

CE P) of interest. Significant betw een -firm dif-

ferences are evident in one measure of personal

values, but not in the other: mean relativism

scores between firms are statistically different;

mean idealism scores are not. As relativism and

idealism are significantly correlated with gender

(at p = 0.027 and p =

0 .001,

respectively),

between-firm gender differences are not likely to

explain the difference in one (relativism) but not

in the other (idealism).

Measures of idealism and relativism show no

significant correlation with age or position. In

fact, mean scores from these data are not statis-

tically different from those of a separate sample

of 21-year-old senior undergraduate accounting

students (Douglas and Schwartz, 1999). This is

an important finding because older subjects are

expected to be less idealistic and less relativistic

than younger subjects (Forsyth, 1980, p. 181),

and because an understanding of the socialization

process leads to the expectation that personal

values will be shaped by the organization over

time.

Also of particular interest to this study, the

measure of organizational ethical culture, the

CEP, show s a significant b etw een -firm difference

{p <

0.01) w hich cann ot be explained by

observed betw een -firm dem ograph ic differences.

CEP scores are significantly correlated with

position p = 0.015) but not with age {p = 0.160)

TABLE II

Univariate tests of central tendency and association

Variables

Idealism

Relativism

C E P

Firm

Position

Mean

5.72

4.97*

6.97**

n /a

n /a

Std. Dev.

1.39

1.36

1.26

n/a

n/a

Idealism

-0.103

(0.073)

0.198

(0.000)

0.017

(0.770)

-0.065

(0.255)

Correlation Coefficients

Relativism

-0.101

(0.079)

0.129

(0.024)

-0 .029

(0.615)

p

values)

CE P

0.148

(0.010)

0.140

(0.015)

Firm

0.614

(0.000)

* Be twe en- firm difference significant t p < 0.05 (tw o-tailed r-test).

** Be twe en-f irm difference significant at ;j < 0.01 (tw o-tailed r-test).

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 10/22

Patricia Casey Douglas et al.

or gender (p = 0.953), despite these three demo

graphic variables' previously noted correlation.

The scores are significantly correlated with the

personal values measure, idealism p < 0.000), and

weakly correlated with relativism (p = 0.079).

This finding might indicate a mo dera ting effect

of organizational environment on personal values

consistent w^ith socialization theory were it not

for the previously discussed evidence implying

that personal values in these firins do not change

over time (i.e., idealism and relativism are not

significantly correlated with position, as would

he expected when values are shaped by an

organization).

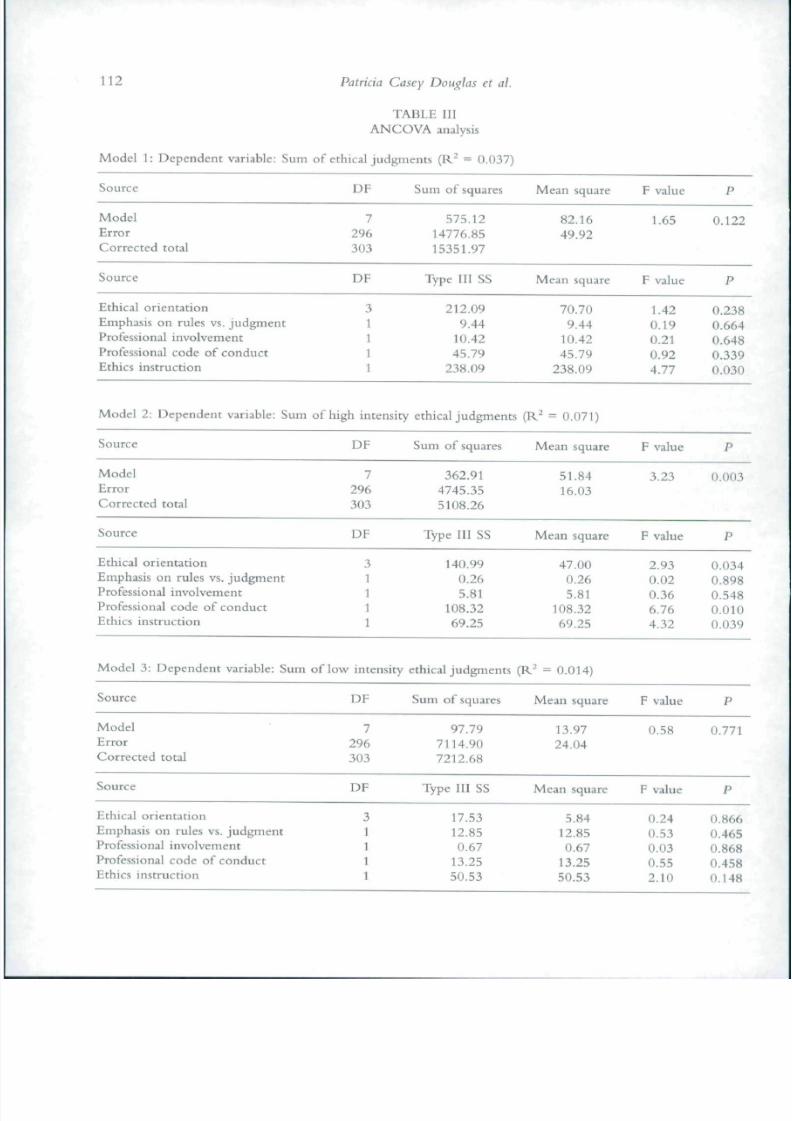

To test H Q I , we used three separate analyses

of covariance (using SAS Proc GLM), as the

judgment score dependent variables are contin-

uous and the independent variable of orientation

is a classification variable while the four measures

of other influences (i.e., management emphasis

on rules versus jud gm en t, professional invo lve-

ment, understanding of the profession's code of

conduct, and previous ethics instruction) are con-

tinuous variables (Table III, Models 1 to 3). Of

the three models, only the model for high inten-

sity ethical judgments is significant (R^ = 0.071;

p

= 0.003). Ethical orientation is significant (F

= 2.93; p = 0.034), even after considering the

effects of other influences. The code of conduct

and ethics instruction variables are also signifi-

cant p < 0.05).

The null hypothesis HQI cannot be rejected in

its entirety: Ethical judgments in situations of

high moral intensity are affected by personal

values (i.e., ethical ideology), by some environ-

mental variables (i.e., understanding of the

professional code of conduct and previous

ethics instruction). Jon es' (1991) moral intens ity

argument is supported: differences in the char-

acteristics of specific judgment tasks apparently

result in different decision processes.

To ensure that the results using the classifica-

tion variable of ethical orientation are not an

artifact of the classification scheme, we reran the

analyses for

H Q I

using the continuous variables

of idealism and relativism instead of the orienta-

tion variable. We also included an interaction

term for idealism and relativism (Table IV).

Comparison of Tables III and IV, Models 1 to

3 indicates that the R^'s are virtually the same f

all models. However, the model for all judgmen

together now is significant

p =

0.044) as is t

interaction term p = 0.028). The only signi

cant ot he r influen ces variable is still ethi

instruction. For the high intensity ethical dec

sions,

the model is still significant

p =

0.004

but the interaction term is not p = 0.166). T

same two other variables are significant. Agai

the model for the low intensity ethical judgmen

is not significant.

Sensitivity analysis indicates that while the u

of ethical orientation produces virtually the sam

R 's and significant oth er influences terms

does use of separate idealism and relativism scor

for all models, there are some differences in t

significance of individual variables. Results f

the high intensity ethical jud gm en t mod

indicate that the classification of subjects in

ethical orientations makes a difference that is n

detected when using the separate value scores

As most studies employing Forsyth's EPQ u

separate idealism and relativism scores and do n

attempt to classify subjects into the four ide

logical groupings (thereby avoiding [as do

Forsyth himself] the attendant issue of what co

stitutes hi gh or low ideahsm and relativis

scores), this finding may indicate serious rese

vations for the less-complicated approach.

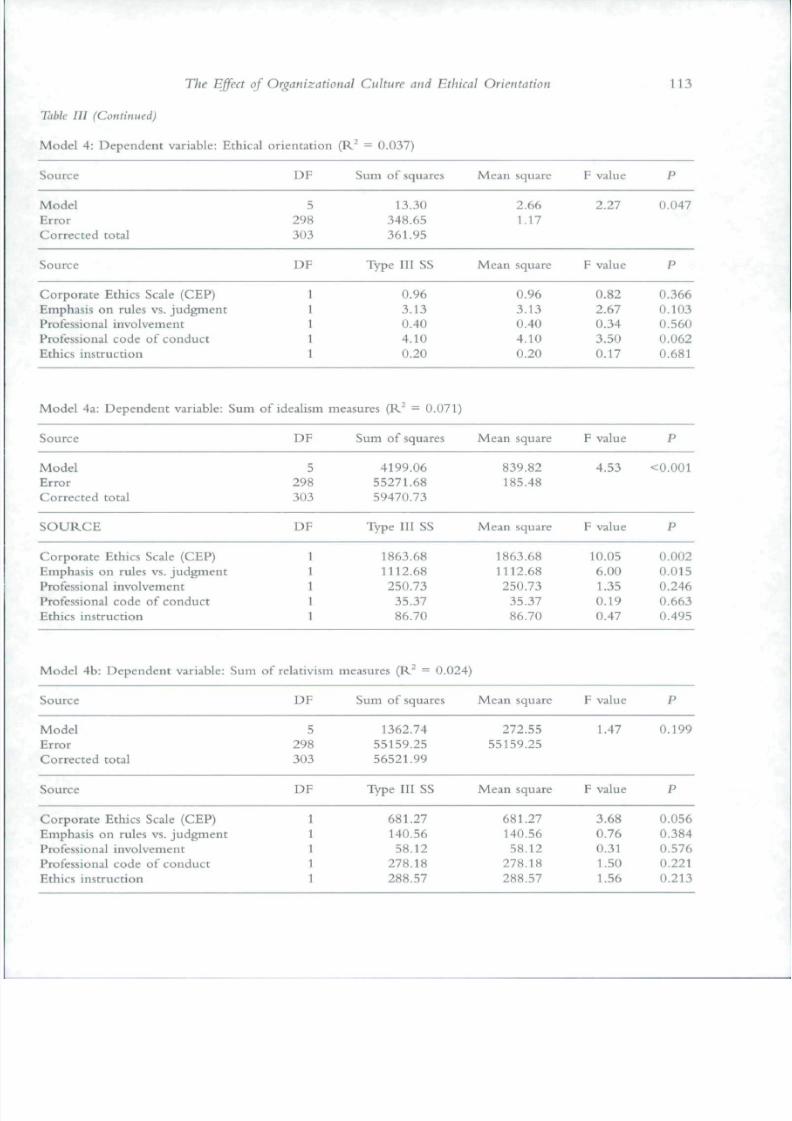

H Q2 was also analyzed with an ANCOV

model (Table III, Model 4). In this model, ethic

orientation is the dependent variable, perceive

organizational ethical culture (CEP) and the fo

other influences variables are the inde pende

variables. This model is marginally significa

(R^

=

0.037;

p =

0.047), but none of t

hypothesized independent variables are signif

cant at p < 0.05. Additional ANCOVA mode

deconstructed the ethical orientation variabl

using summate measures of idealism (Model 4

and relativism (Model 4b) as dependent variable

Model 4a is significant at p < 0.001 (R

=

0.071

CEP and firm emphasis on rules vs. judgme nt a

both significant p = 0.002 and 0.015, respe

tively). Model 4b shows no significant result

Clearly, corporate ethical environment, includin

a relatively strong rules-orientation, affects ind

vidual idealism but not relativism.

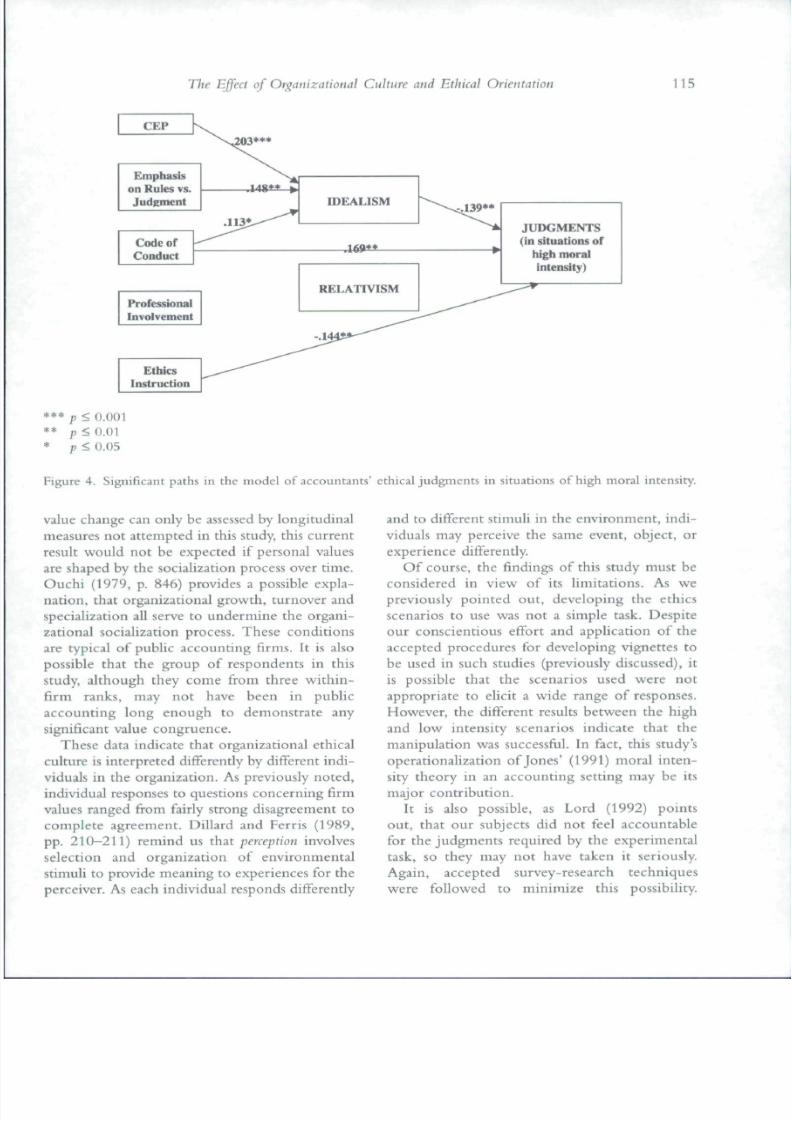

We tested Ho3, in which organizational ethic

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 11/22

The Effect of Organizational Culture and Ethical Orientation

U l

culture is hypothesized to affect individu als'

j udgm en t in situations with an ethical compo-

nent, either directly (as a result of a rules-vs-in di-

vidual judg me nt approach on the part of the

firm, previous ethics training,

or the

strength

of

professional codes of conduct) or indirectly as a

result

of

wo rk-env ironm ent influences acting

to

shape the individual dec ision-maker's personal

values), using path analysis. Figure

4

presents

the

path model supported by these data: a recursive

causal model

of

accountants' ethical judgments,

depicting hypothesized direct and indirect rela-

tionships between corporate ethical culture

(CEP), oth er influences, and judgm ents, here

limited to situations of high m oral intensity. '

Because

the

ethica l ideology con struc t classifies

respondents into one of four categories not

suitable for this type of analysis, the continuous

variables, idealism and relativism, were used in

the path model. Significant paths are indicated

by one-way arrows and path coefficients indic ate

the magnitude of effect.

Table

V

summarizes

the

direct, indirect,**

and

residual effects of significant variables. Consistent

with

HQI

results previously discussed, significant

direct effects on judgments in situations of high

moral intensity

are

shown

for

idealism,

but not

for relativism. Also consistent with HQ2 results,

corporate ethical culture

CEP)

affects idea lism ,

but not relativism. CEP affects judg me nts both

directly

and

indirectly, through

its

effect

on

idealism, although the effect is not statistically

significant at^ < 0.05. Data confirm that the pro-

fessional code of co nd uc t direc tly affects idealism

p

< 0.05) and judgments p < 0.01), and indi-

rectly affects judgments, although again the effect

is not statistically significant p > 0.05). An

emphasis

on

rules

vs.

ju dg m en t directly affects

idealism {p < 0.01) and indirectly affects j ud g-

ments but at p > 0.05), and ethics instruc tion

directly affects judgements p < 0.01) only.

iscussion and conclusions

This study investigated auditors' ethical judg-

ments in situations typical of those they face in

practice. Results indicate that ethical orientation

is related

to

ethical judgments

in

high

but not

low) moral intensity situations. These results

suppo rt Jone s' (1991) issue-continge nt argum ent,

but appear counter to those of Brief et al. (1996)

who found little effect

of

personal values

on

ethical judgments. Brief

et al.

(1991,

p. 393)

observe that personal values

are

related

to

ethical

decisions only under conditions of low account-

ability. As Tetlock (1983,

p. 75)

explains this

phe-

nomena, individuals will tend towards

consistency with the views of those to w h o m

they are accountable if those views are known.

If they are not known , the individual has no

choice but to consider other options and tolerate

inconsistency - perhaps to rely on learned

responses (i.e., personal values).

Perceived organizational ethical culture

is

indirectly related to ethical judgments in our

results,

as

ethical cultur e affects in dividu al values

(i.e.,

idealism) and idealism affects judgments.

Extending Tetlock's (1983) logic,

the

moderating

effect of culture on judgme nt will be more pro-

nounced

if

the cu lture rather explicitly supports

distinct values. Individuals' summed responses to

CEP questions concerning firm values

in

this

study ranged from a m in im um of 13 (largely

to moderately disagree)

to a

maximum

of 45

(completely agree).

The

median score

was 36

(moderately agree) and the interquartile range is

31 (shghtly agree) to 40 (largely agree). These

findings may indicate uncertainty with respect

to what management values, and reliance

on personal values in lieu of organizational

ethical culture. Other environmental influences,

including the professional code of conduct , an

emphasis in the workplace on rules vs. individual

judgment , and previous ethics instruction signif-

icantly influence judgments. These

may

also

indicate

a

reliance

on

prior learned responses

in

the absence

of

a strong ethical culture.

Socialization theory leads us to expect an

eventual convergence of persona l values w ith

those of the organization. Firms mold their

members to fit the organizational environm ent,

or select

and

promote individuals

who

already

fit into the prevailing culture and cause those that

do

not fit to

leave.

The

cross-sectional data

of

this study show no difference in value measure-

ments among participants

at

different pos itions

(i.e.,

experience levels) within

the

firm. While

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 12/22

112

Patricia Casey Douglas et al

TABLE III

ANCOVA analysis

Mo del 1: Dep end ent variable: Sum of ethical judg me nts (R- - 0.037

Source

Model

Error

Corrected total

Source

DF

7

296

303

DF

Sum of squares

575.12

14776.85

15351.97

Type III SS

Mean square

82.16

49.92

Mean square

F value

1.65

F value

P

0.122

P

Ethical orientation

Emphasis on rules vs. judgment

Professional involvement

Professional code of conduct

Ethics instruction

212.09

9.44

10.42

45.79

238.09

70.70

9.44

10.42

45.79

238.09

1.42

0.19

0.21

0.92

4.77

Ethical orientation

Emphasis on rules vs. judgment

Professional involvement

Professional code of conduct

Ethics instruction

0.238

0.664

0.648

0.339

0.030

Model 2:

Source

Model

Error

Corrected

Source

Dependent variable;

total

Sum of high intensity

D F

7

296

303

DF

ethical judgm ents (

Sum of squares

362.91

4745.35

5108.26

Type III SS

R^ = 0.

Mean

51

16

Mean

071)

square

.8 4

.03

square

F

F

value

3.23

value

P

0.003

P

Ethical orientation

Emphasis on rules vs. judgment

Professional involvement

Professional code of conduct

Ethics instruction

3

1

1

1

1

140.99

0.26

5.81

108.32

69.25

47.00

0.26

5.81

108.32

69.25

2.93

0.02

0.36

6.76

4.32

0.034

0.898

0.548

0.010

0.039

Model 3:

Source

Model

Error

Corrected

Source

Dependent variable:

total

Sum of low intensity

DF

7

29 6

303

D F

ethical judgments

Sum of squares

97.79

7114.90

7212.68

Type III SS

( R = 0.014

Mean square

13.97

24.04

Mean square

F

F

value

0.58

value

P

0.771

P

3

1

1

1

1

17.53

12.85

0.67

13.25

50.53

5.84

12.85

0.67

13.25

50.53

0.24

0.53

0.03

0.55

2.10

0.866

0.465

0.868

0.458

0.148

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 13/22

The Effect of Organizational Culture a nd Ethical O rientation 1 1 3

Tabk III Continued)

Model 4: Dependent variable; Ethical orientation (R —

0.037

Source DF Sum of squares Me an square F value

Model

Error

Corrected total

5

298

3 3

13 3

348 65

361 95

2 66

1 17

7

47

Source

DF

Type III SS Mean square F value

Corporate Ethics Scale (CEP)

Emphasis on rules vs. judgment

Professional involvement

Professional code of conduct

Ethics instruction

0.96

3.13

0.40

4.10

0.20

0.96

3.13

0.40

4.10

0.20

82

2 67

34

3 5

17

366

1 3

56

62

681

Model 4a; Dependent variable; Sum of ideahsm measures {R^ = 0.071

Source DF

Sum of squares Mea n square F value

M o d e l

Error

Corrected total

298

3 3

4199 6

55271 68

5947 73

839 82

185 48

4 53 < 1

S O U R C E

DF

Type III SS

Mean square F value

Corporate Ethics Scale (CEP)

Emphasis on rules vs. judgment

Professional involvement

Professional code of conduct

Ethics instruction

1

1

1

1

1

1863 68

1112 68

25 73

35 37

86 7

1863 68

1112 68

25 73

35 37

86 7

1 5

6

1 35

19

47

2

15

246

663

495

Model 4b: Dependent variable: Sum of relativism measures (R^ = 0.024

Source DF

Sum of squares M ean square F value

Model

Error

Corrected total

5

298

3 3

1362 74

55159 25

56521 99

272 55

55159 25

1.47 0.199

Source DF

Type III SS

Me an square F value

Corporate Ethics Scale (CEP)

Emphasis on rules vs. judgment

Professional involvement

Professional code of conduct

Ethics instruction

1

1

1

1

1

681 27

14 56

58 12

278 18

288 57

681 27

14 56

58 12

278 18

288 57

3 68

76

31

1 5

1 56

56

384

576

221

213

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 14/22

114 Patricia Casey ouglas et al

TABLE IV

Sensitivity analyses

Model 1: Dependent variable: Sum of ethical judgments (R^ =

0.047

Source

Model

Error

Corrected total

Source

DF

7

296

303

DF

Sum of squares

724.29

14627.68

15351.97

Type III SS

Mean square

103.47

49.42

Mean square

F value

2.09

F value

P

0.04

P

Idealism

Relativism

idealism*relativism

Emphasis on rules vs. judgment

Professional involvement

Professional code of conduct

Ethics instruction

1

1

3

1

1

1

1

166.07

286.97

241.29

5.15

10.46

39.32

271.88

166.07

286.97

241.29

5.15

10.46

39.32

271.88

3.36

5.81

4.88

0.10

0.21

0.80

5.50

0.06

0.01

0.02

0.74

0.64

0.37

0.02

Model 2:

Source

Model

Error

Corrected

Source

Dependent variable:

total

Sum of high intensity

D F

7

296

303

DF

ethical judgments

Sum of squares

341.97

4766.29

5108.26

Type III SS

(R = 0.067

Mean square

48.85

16.10

Mean square

F

F

value

3.03

value

P

0.00

P

Idealism

Relativism

Idealism*relativism

Emphasis on rules vs. judgment

Professional involvement

Professional code of conduct

Ethics instruction

1

1

1

1

1

1

1

9.55

41.77

31.09

1.29

5.41

101.34

71.67

9.55

41.77

31.09

1.29

5.41

101.34

71.67

0.59

2.59

1.93

0.08

0.34

6.29

4.45

0.44

0.10

0.16

0.77

0.56

0.01

0.03

Model 3:

Source

Model

Error

Corrected

Source

Dependent variable:

total

Sum of low intensity

D F

7

296

303

DF

ethical judgments {

Sum of squares

190.99

7021.70

7212.68

Type III SS

R =

0.026

Mean square

27.28

23.72

Mean square

F

F

value

1.15

value

P

0.33

P

Idealism

Relativism

Idealism*relativism

Emphasis on rules vs. judgment

Professional involvement

Professional code of conduct

Ethics instruction

1

1

1

1

1

1

1

95.98

109.77

99.14

11.59

0.82

14.41

64.36

95.98

109.77

99.14

11.59

0.82

14.41

64.36

4.05

4.63

4.18

0.49

0.03

0.61

2.71

0.04

0.03

0.04

0.48

0.85

0.43

0.10

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 15/22

The Effect of Organizational Culture and Ethical Orientation

115

CEP

Emphasis

on Rules vs.

Judement

Code of

Conduct

Professional

Involvement

IDEALISM

•1691-f

RELATIVISM

JUDGMENTS

in situations of

high moral

intensity)

Ethics

Instruction

** * p < 0.001

p< 0.01

p < 0.05

Figure 4. Significant paths in the mode l of acco untan ts ethical judg me nts in situations of high m oral intensity.

value change can only be assessed by longitudinal

measures not attempted in this study, this current

result would not be expected if personal values

are shaped by the socialization process over time.

Ouchi (1979, p. 846) provides a possible expla-

nation, that organizational growth, turnover and

specialization all serve to undermine the organi-

zational socialization process. These conditions

are typical of pubhc accounting firms. It is also

possible that the group of respondents in this

study, although they come from three within-

firm

ranks,

may not have been in public

accounting long enough to demonstrate any

significant value congruence.

These data indicate that organizational ethical

culture is interpreted differently by different indi-

viduals in the organization. As previously noted,

individual responses to questions concerning firm

values ranged from fairly strong disagreement to

complete agreement. Dillard and Ferris (1989,

pp . 210—211) remind us

thzt per eption

involves

selection and organization of environmental

stimuli to provide meaning to experiences for the

perceiver. As each individual responds differently

and to different stimuli in the environment, indi-

viduals may perceive the same event, object, or

experience differently.

Of course, the fmdings of this study must be

considered in view of its hmitations. As we

previously pointed out, developing the ethics

scenarios to use was not a simple task. Despite

our conscientious effort and application of the

accepted procedures for developing vignettes to

be used in such studies (previously discussed), it

is possible that the scenarios used were not

appropriate to elicit a wide range of responses.

However, the different results between the high

and low intensity scenarios indicate that the

ma nipu lation was successful. In fact, this study s

operationalization of

Jones

(1991) moral inten-

sity theory in an accounting setting may be its

major contribution.

It is also possible, as Lord (1992) points

out, that our subjects did not feel accountable

for the judgm ents required by the experimen tal

task, so they may not have taken it seriously.

Again, accepted survey-research techniques

were followed to minimize this possibility.

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 16/22

116

Patricia Casey Douglas et al.

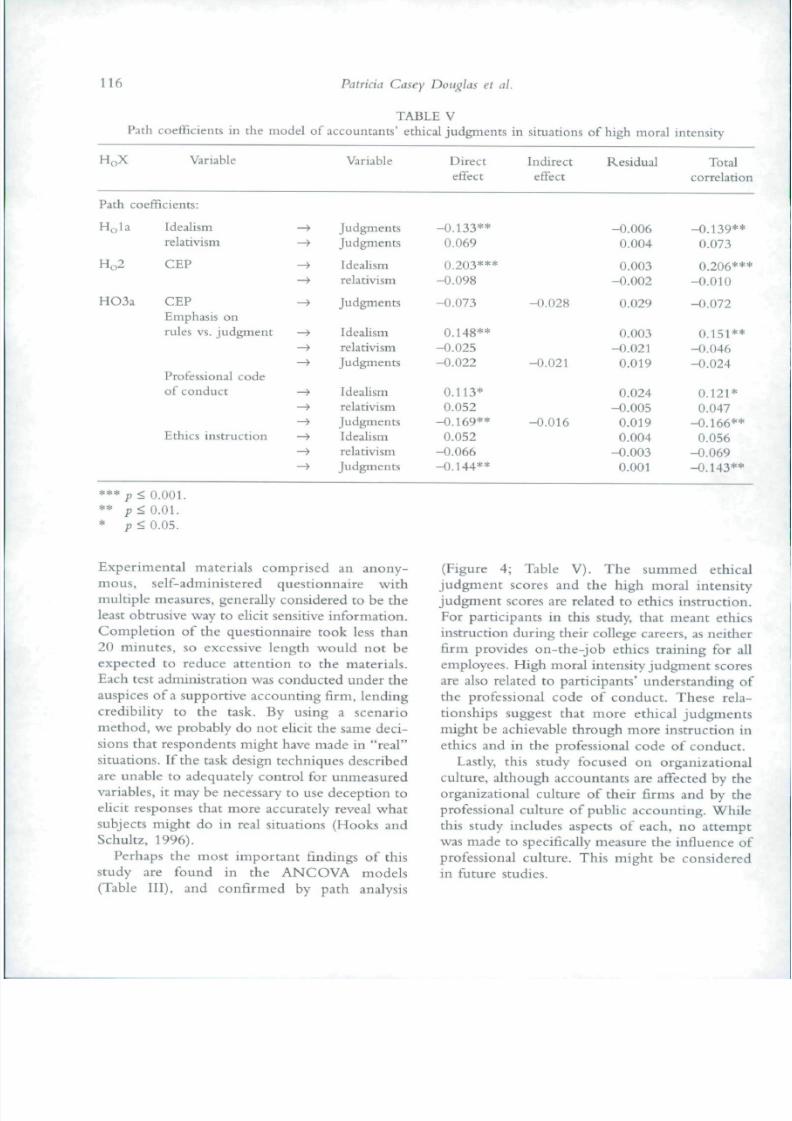

TABLE V

Path coefficients in the m odel of acco untan ts' ethical jud gm ents in situations of high moral intensity

HQX Variable

Path coefficients:

Hola Idealism

relativism

Ho2 CEP

HO3a CEP

Emphasis on

rules vs. judgment

Professional code

of conduct

Ethics instruction

—*

->

—*

>

Variable

Judgments

Judgments

Idealism

relativism

Judgments

Idealism

relativism

Judgments

Idealism

relativism

Judgments

Idealism

relativism

Judgments

Direct

effect

- 0 . 1 3 3 * *

0 069

0.203***

-0 .098

- 0 . 0 7 3

0.148**

-0 .025

-0 .022

0.113*

0 052

-0 .169**

0 052

-0 .066

-0 .144**

Indirect

effect

-0 .028

-0 .021

-0 .016

Residual

-0 .006

0 004

0 003

- 0 . 0 0 2

0 029

0 003

-0 .021

0.019

0 024

- 0 . 0 0 5

0.019

0 004

- 0 . 0 0 3

0.001

Total

correlatio

- 0 . 1 3 9 * *

0 073

0.206**

-0 .010

-0 .072

0.151**

- 0 . 0 4 6

- 0 . 0 2 4

0.121*

0 047

-0 .166**

0 056

-0 .069

-0 .143**

** *

p <

0.001.

* * ; j < 0 0 1

*

p<

0.05.

Experimental materials comprised an anony-

mous, self-administered questionnaire with

multiple measures, generally considered to be the

least obtrusive way to elicit sensitive information.

Completion of the questionnaire took less than

20 minutes, so excessive length would not be

expected to reduce attention to the materials.

Each test administration was conducted under the

auspices ofa supportive accounting firm, lending

credibility to the task. By using a scenario

method, we probably do not elicit the same deci-

sions that respond ents might have made in rea l

situations. If the task design tech niques described

are unable to adequately control for unmeasured

variables, it may be necessary to use deception to

elicit responses that more accurately reveal what

subjects might do in real situations (Hooks and

Schultz, 1996).

Perhaps the most important fmdings of this

study are found in the ANCOVA models

(Table III), and confirmed by path analysis

(Figure 4; Table V). The summed ethica

judgment scores and the high moral intensit

judgment scores are related to ethics instruction

For participants in this study, that meant ethic

instruction during their college careers, as neithe

firm provides on-the-job ethics training for a

employees. High moral intensity judgment score

are also related to participants' understanding o

the professional code of conduct. These rela

tionships suggest that more ethical judgment

might be achievable through more instruction i

ethics and in the professional code of conduct.

Lastly, this study focused on organizationa

culture, although accountants are affected by th

organizational culture of their firms and by th

professional culture of public accounting. Whil

this study includes aspects of each, no attemp

was made to specifically measure the influence o

professional culture. This might be considere

in future studies.

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 17/22

The Effect of Organizational Culture a nd Ethical Orientation 1 1 7

Appendix A: Ethics Position Questionnaire EPQ )

. A person should make certain that their actions never intentionally ha rm a nothe r even to a small degree .

2. Risks to anoth er should never be tolerated, irrespective of how small the risks might be .

3.

Th e existence of potential harm to others is always wrong, irrespective of the benefits to be gained.

4. On e should never psychologically or physically harm ano ther perso n.

5.

On e should not perform an action which migh t in any way threaten the dignity and welfare of ano ther

individual.

6. If an action could harm an inno cen t other, then it should not be don e.

7. Dec iding w heth er or not to perform an act by balancing the positive consequ ences of the act against the

negative consequences of the act is immoral.

8. Th e dignity and welfare of people should be the most imp ortan t conc ern in any society.

9. It is never nece ssary to sacrifice the welfare of others .

10. Moral actions are those whic h closely match ideals of the most "perfec t" action.

11 . Th ere are no ethical principles that are so importa nt that they should be a part of any code of ethics.

12. W hat is ethical varies from one situation and society to another.

13 .

Mo ral standards should be seen as being individualistic; what on e person considers to be moral may be

judged to be immoral by another person.

14. Different types of moralities cannot be com pared as to "rightness."

15 . Qu estio ns of wh at is ethical for every one can never be resolved since wh at is mo ral or imm oral is up to

the individual.

16. Moral standards are simply personal rules which indicate how a person should behave, and are not to be

applied in m aking judgm ents of others.

17 . Ethical considerations in interpersonal relations are so complex that individuals should be allowed to

formulate their own individual codes.

18 .

Rigid ly codifying an ethical position that prevents certain types of actions could stand in the way of better

human relations and adjustment.

19 . N o rule co nce rning lying can be formulated; wh ethe r a lie is permissible or not permissible totally dep ends

upon the situation.

20. W hethe r a lie is judge d to be moral or immoral depends upon the circumstances surrounding the action.

Appendix B: CEP and other influences

Panel 1: Corporate Ethics Scale (Hunt, Wood, and Chonko 1989)

• Manag ers in my firm often engage in behaviors that I consider to be un ethical.*

• In ord er to succeed in my firm, it is often necessary to comp rom ise one's ethics.*

• Top mana gem ent in my firm has let it be know n in no uncerta in terms that unethical behaviors will no t be

tolerated.

• If a ma nag er in niy firm is discovered to have enga ged in une thica l beh avio r that results prim arily in person l

gain (rather than firm gain), he or she will be promptly reprimanded.

• If a man ager in my firm is discovered to have engaged in une thical be hav ior that results prim arily in ftrm

gain (rather than personal gain), he or she will be promptly reprimanded.

Panel 2: Other influences

• M anag em ent generally stresses confo rmin g to rules rather than applying individual jud gm en t.

• I am very active in the profession, atten din g professional me eting s, reading professional public ation s, etc.

• I was exposed to a great deal of ethics or philosophy instruction durin g my college career.

• Th e ethics instruction I received in college was mo re philosophical than practical.

• I have a thoro ugh un derstand ing of the Professional Cod e of Co nd uc t.

Note: items that are reversed scored.

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 18/22

118

Patricia Casey Douglas

et al

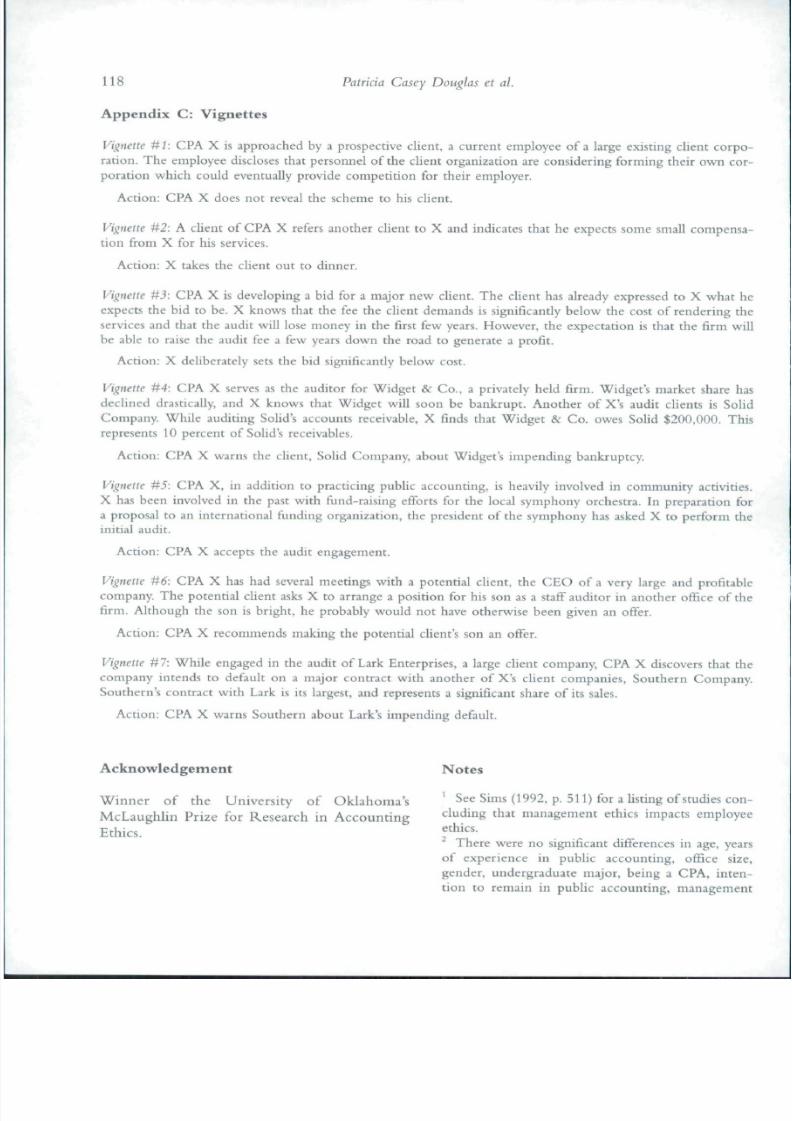

Appendix C Vignettes

Vignette

t: CPA

X is

approached

by a

prospective client,

a

current employee

o fa

large existing client c orp

ration. The employee discloses that personnel of the client organization are considering forming their own co

poration which could eventually provide competition

for

their employer.

Action;

CPA

X does not reveal the scheme to his client.

Vignette

#2 :

A chent of CPA X refers another client to X

and

indicates that he expects some small com pen s

tion from X for

his

services.

Action: X takes the client out to dinner.

Vignette U :

CPA

X is developing a

bid

for a major

new

client. The client

has

already expressed to X what h

expects the bid to

be.

X knows that the fee the chent demands is significantly below the cost of rendering th

services and that the audit will lose money in the first few years. However, the expectation is that the firm w

be able to raise the audit fee a few years down the road to generate a profit.

Action: X deliberately sets the bid significantly below cost.

Vignette

U4:

CPA

X serves as the auditor for Widget &

Co.,

a privately held firm. Widget's m arket share h

declined drastically, and X knows that W idget

wil

soon be bankrupt . Another of

X's

audit clients is So

Company. While auditing Solid's accounts receivable, X finds that Widget & Co. owes Solid 200 ,000. Th

represents 10 percent of Solid's receivables.

Action:

CPA

X warns th e client, Solid Com pany, abou t Widget's impen ding bankrup tcy.

Vignette

#5 : CPA X, in addition to practicing public acc ounting , is heavily involved in community activitie

X has been involved in the past with fund-raising efforts for the local sympho ny orchestra. In preparation fo

a proposal to an interna tional funding orga nization, tbe president of the sym phony has asked X to perform th

initial audit.

Action:

CPA

X accepts the audit engagement.

Vignette U6:

CPA X has had several me etings wit h a potential client, th e CEO of a very large and profita

company. The potential client asks X to arrange a position for his son as a staff auditor in another office of th

firm. Although the son is bright, he probably would not have otherw ise been given an offer.

Action: CPA X recommends making the potential chent's son an offer.

Vignette

#7:

While engaged in the audit of Lark Enterprises, a large client company,

CPA

X discovers that th

company intends to default on a major contract with another of

X's

client companies. Southe rn Compan

Southern's contract with Lark is its largest, and represents a significant share of its sales.

Action:

CPA

X

warns South ern ab out Lark's imp end ing default.

Acknowledgement Notes

Winner

of the

University

of

Oklahoma's

'

See Sims {1992, p. 511) for a listing of studies con

McLaughhn Prize

for

Research

in

A cc ou nti ng eluding tbat management ethics impacts employ

Ethics. fh'' ^-

- There were no significan t differences in

age,

yea

of experience in public a cco unt ing, office siz

gender, undergraduate major, being a CPA, in te

tion

to

remain

in

publ ic account ing, managem e

7/21/2019 The Effect of Organizational Culture and Ethical Orientation on Accountants Ethical Judgments

http://slidepdf.com/reader/full/the-effect-of-organizational-culture-and-ethical-orientation-on-accountants 19/22

The Effect of Organizational Culture and Ethical Orientation

9

emphasis on rules versus jud gm en ts, professional

involvement, and ethics training in college between

the usable and rejected instruments. There were sig-

nificant differences in positio n of respo nde nts, with

rejected instruments coming more from staff and

fewer from higher positions. More rejected instru-

ments came from respondents indicating that they did

not intend to remain with their current f irm.

Rejected respondents also displayed a higher level of

understanding of the Professional Code of Conduct.

This last difference is the only one that is difficult to

understand.

* A t 17 .4 percen t, this is only slightly highe r than the

5 to 15 percen t range of typica l consistency failures

Rest reports of studies using his instrument (Rest,

1987, p. 15). Following the logic of Rest's suggestions

for adapting the reported range to the shorter version

of the DIT, the higher failure rate in the current study

would be expected based only upon the larger

number of items in the instrument developed for this

study.

* As a sensitivity analysis, we also classified res po n-

dents into orientation by a median split but ignoring

the duplicated median scores. This resulted in 65

Exceptionists, 75 Subjectivists, 77 Absolutists, and 67

Situationists. We then reran all the models indicated

in Tables

III

and IV (not shown). Results were not

significantly different.

^ Neither firm provides on-the-job ethics training for

the employee ranks tested in this study.

^ We also conducted a sensitivity analysis using the

64 rejected instruments using the four models shown

in Table III. Results (not shown) were not signifi-

cantly different for any of the four models. We also

recomputed the three regression analyses reported in

Table IV including the 64 rejected instruments. There

were no significant differences in these regression

models.

' Su b- gr ou p analysis was again used to assess the

hypothesized moderating effect of moral intensity

on judgments, as suggested by Sharnia et al. (1981).

As in our previous findings, only the model of