the evolving broadcast sector (review report)

TRANSCRIPT

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 1

DATAMONITOR VIEW

CATALYST

Competition across the digital TV sector is now greater than ever before, prompting operators to develop their offerings to

both attract and retain subscribers. Operators are increasingly embracing new technologies to achieve this goal –

Datamonitor expects 2006 to be a watershed year for new services such as high-definition TV, IPTV and mobile TV.

SUMMARY

The five components of the evolving broadcast sector theme provide an overview of developments across the digital TV

sector, including a focus on the potential impact of technologies including high definition, PVRs and mobile TV.

• Digital TV markets: Europe & the US (Market Focus)

• Technology developments in the digital TV sector (Technology Focus)

• Digital TV development - major European TV markets and the US (Databook)

• Digital TV development - small European TV markets (Databook)

• Technology developments in the digital TV Sector (Databook)

METHODOLOGY

Industry opinion research Interviews with leading market participants.

Market data Historic and current market values are based on Datamonitor’s ongoing research into the media sector.

REVIEW REPORT

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) Driving the transition to digital

Reference Code: DMTC1195

Publication Date: June 2006

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 2

EXECUTIVE SUMMARY

Introduction

This report combines the two briefs from the evolving broadcast sector theme for Q2 2006. While the market focus

section provides an overview of key developments across the digital TV sector, the technology focus brief

considers developments with regard to the deployment of technologies such as high definition, PVRs and mobile

TV. Three databooks showcasing relevant datasets from the interactive model are also included.

Digital TV markets: Europe & the US (Market Focus)

The Market Focus section discusses key recent developments across the European and US digital TV markets.

The European and the US digital TV markets are expected to show strong growth by the end of the decade, with

the emergence of IPTV acting to boost levels of competition and add new impetus to the plans of established

operators. The rate and nature of market development will continue to differ considerably between individual

country markets, although all will show a significant increase in the penetration of digital services by the end of

2010. Key findings of this brief include:

• strong digital growth expected across Europe;

• IPTV set to shake up the digital TV competitive environment;

• consolidation continues to have an impact on market dynamics.

Technology developments in the digital TV sector (Technology Focus)

The Technology Focus section examines the potential impact of technologies – including high definition, PVRs

and mobile TV – on the digital TV sector. Competition across the broadcast sector is now greater than ever

before, prompting operators to develop their offerings to both attract and retain subscribers. Operators are

increasingly embracing new technologies to achieve this goal – Datamonitor expects 2006 to be a watershed year

in Europe for new services such as high-definition TV, IPTV and mobile TV, while uptake of PVR technology is set

to increase rapidly over the next five years. Key findings of this brief include:

• high definition expected to become a major service differentiator;

• increasing penetration of PVRs could disrupt existing broadcast business models;

• mobile TV offers new opportunities for broadcasters.

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 3

Databooks

The final section provides datasets relating to the evolving broadcast sector theme. Three databooks are included

in this review report:

• Digital TV development: major European TV markets and the US (Databook) – provides a breakdown

of digital households by both platform (satellite, cable, DTT and IPTV) and operator across major

European TV markets (France, Germany, Italy, Spain and the UK) and the US.

• Digital TV development: small European TV markets (Databook) – provides a breakdown of digital

households by both platform (satellite, cable, DTT and IPTV) and operator across the smaller European

TV markets (Austria, Belgium, Denmark, Finland, the Netherlands, Norway, Portugal, Sweden and

Switzerland).

• Technology developments in the digital TV Sector (Databook) – provides forecast market data relating

to the penetration of PVR, high definition and mobile TV technologies across western Europe and the

US.

Sources used for this research include:

• interviews with leading market participants;

• Datamonitor’s ongoing research into the media sector.

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 4

TABLE OF CONTENTS

DATAMONITOR VIEW 1

CATALYST 1

SUMMARY 1

METHODOLOGY 1

EXECUTIVE SUMMARY 2

Introduction 2

Digital TV markets: Europe & the US (Market Focus) 2

Technology developments in the digital TV sector (Technology Focus) 2

Databooks 3

DIGITAL TV MARKETS: EUROPE & THE US (MARKET FOCUS) 8

Summary 8

Strong digital growth expected across Europe 8

IPTV set to shake up the digital TV competitive environment 15

Consolidation continues to have an impact on market dynamics 20

TECHNOLOGY DEVELOPMENTS IN THE DIGITAL TV SECTOR (TECHNOLOGY FOCUS) 24

Summary 24

High definition expected to become a major service differentiator 24

Increasing penetration of PVRs could disrupt existing broadcast business models 32

Mobile TV offers new opportunities for broadcasters 36

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 5

DIGITAL TV DEVELOPMENT: MAJOR EUROPEAN MARKETS & THE US (DATABOOK) 42

Introduction 42

Market development comparison: Europe & US 43

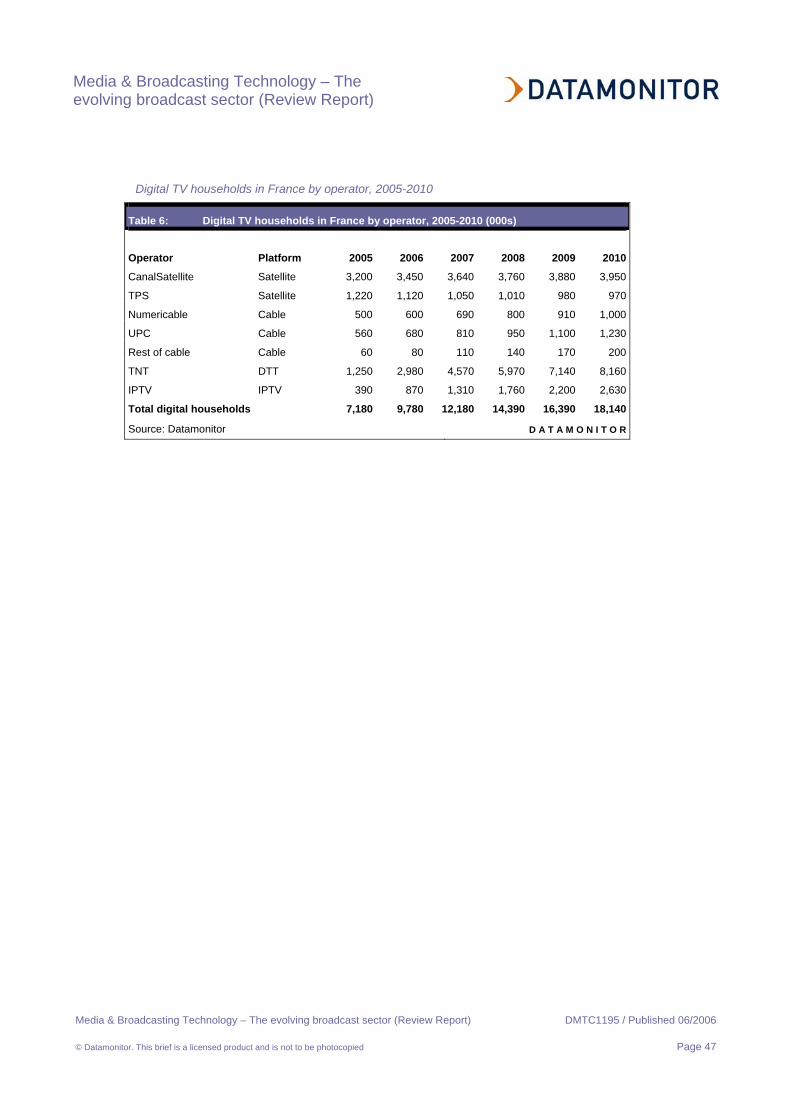

Digital TV growth in France 46

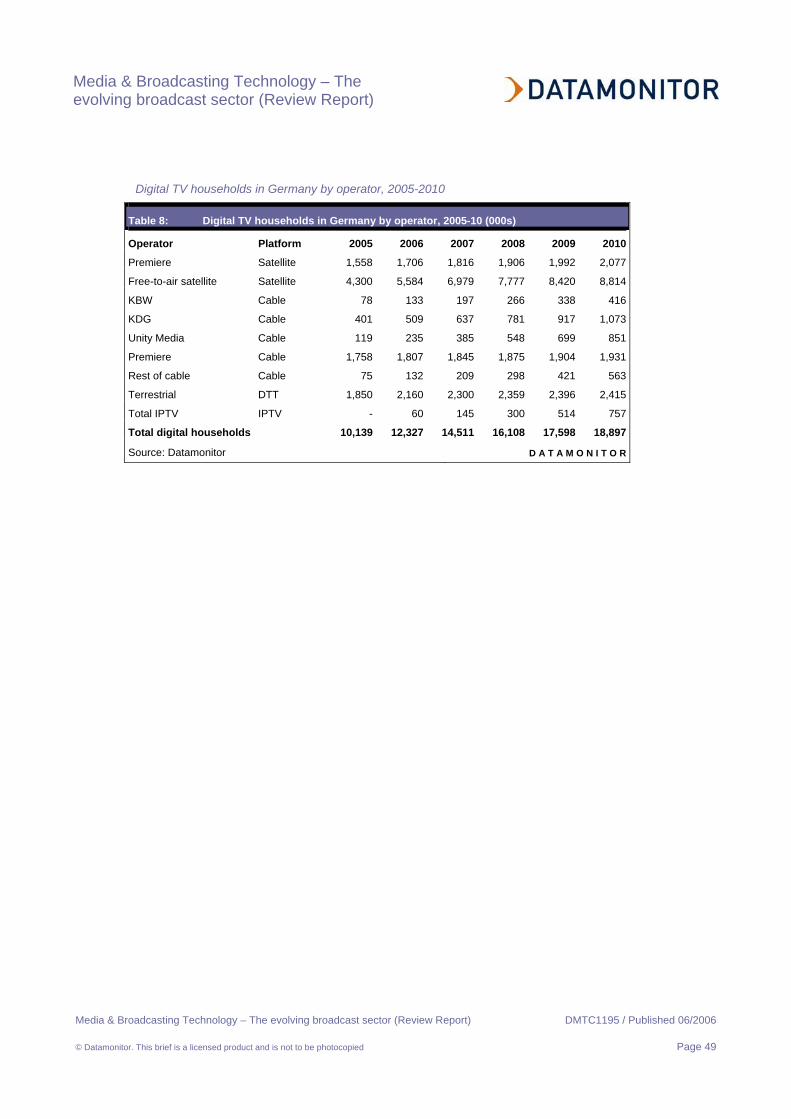

Digital TV growth in Germany 48

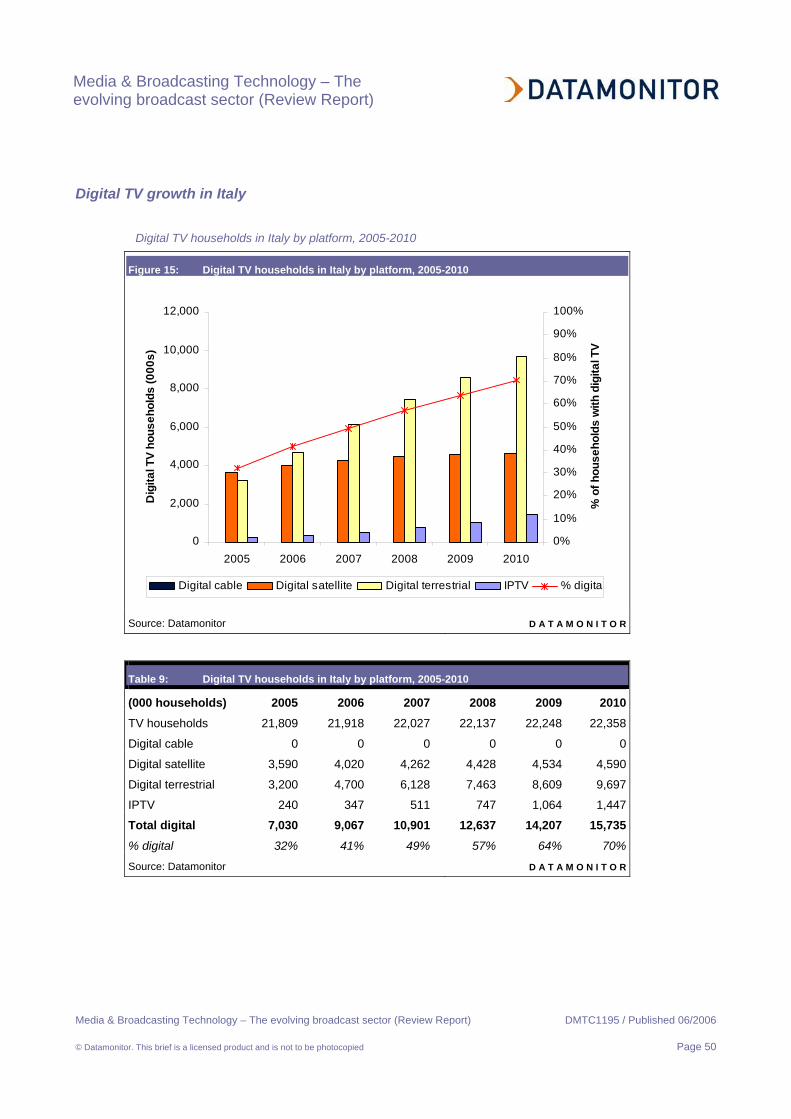

Digital TV growth in Italy 50

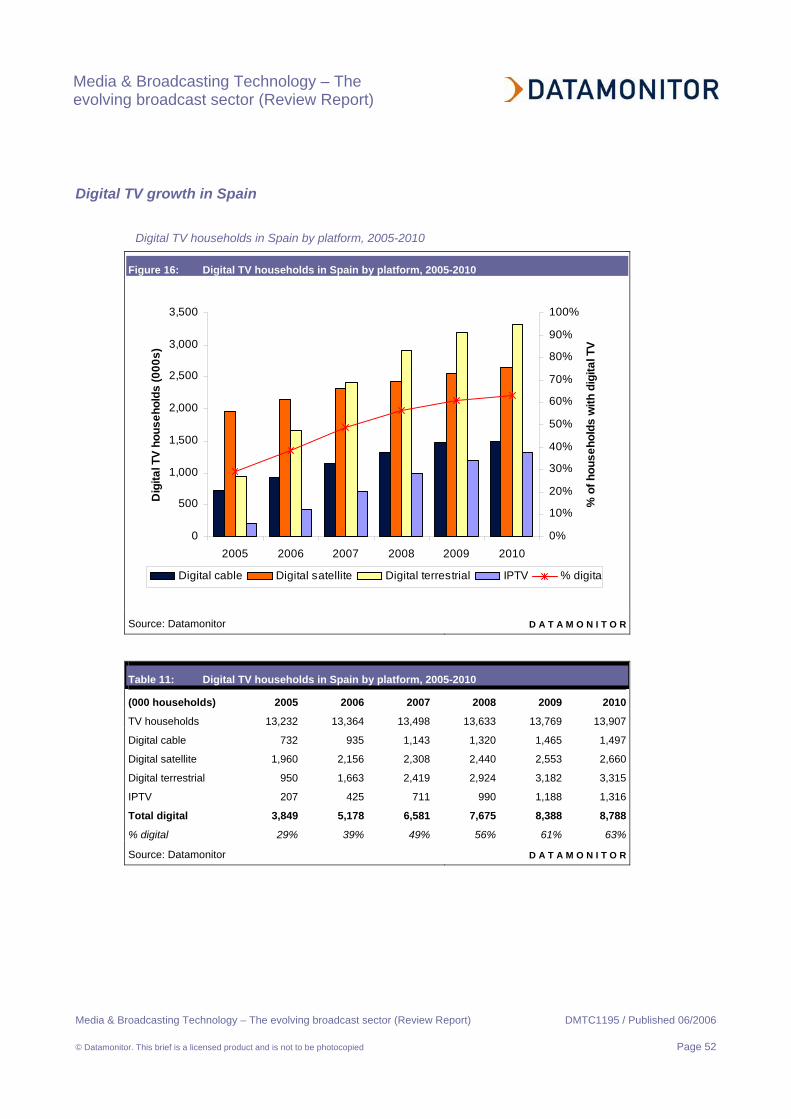

Digital TV growth in Spain 52

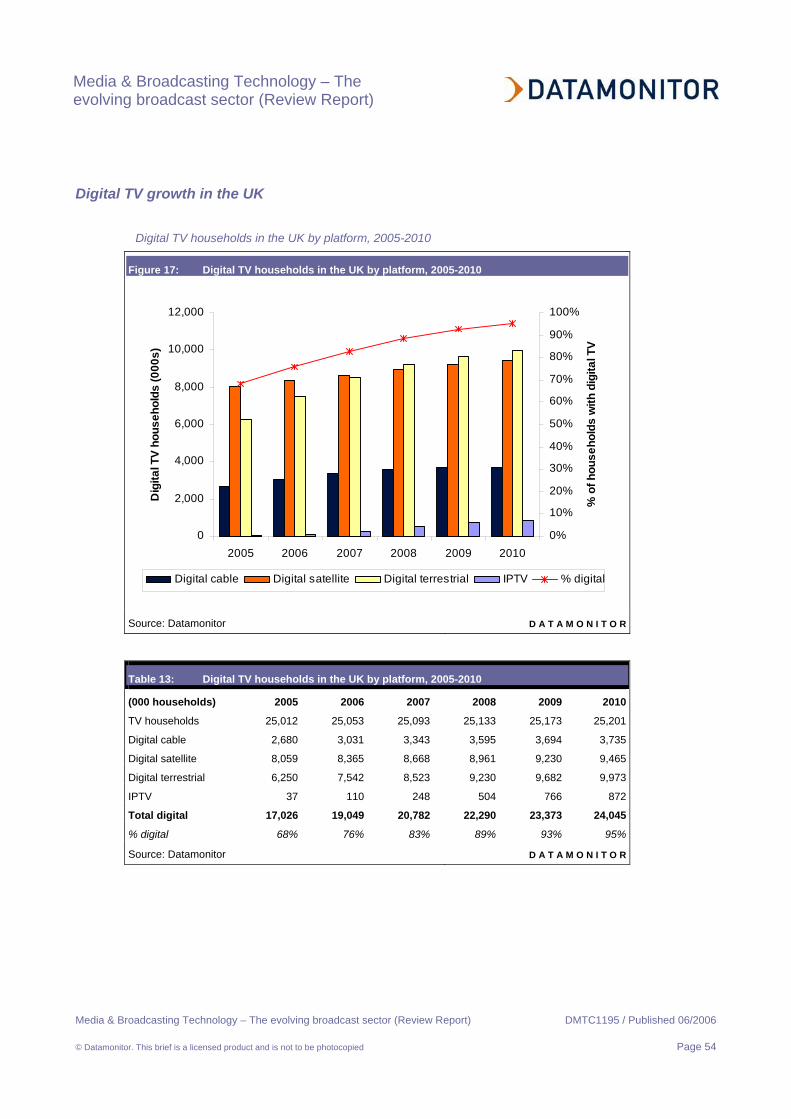

Digital TV growth in the UK 54

Digital TV growth in the US 56

DIGITAL TV DEVELOPMENT: SMALL EUROPEAN TV MARKETS (DATABOOK) 58

Introduction 58

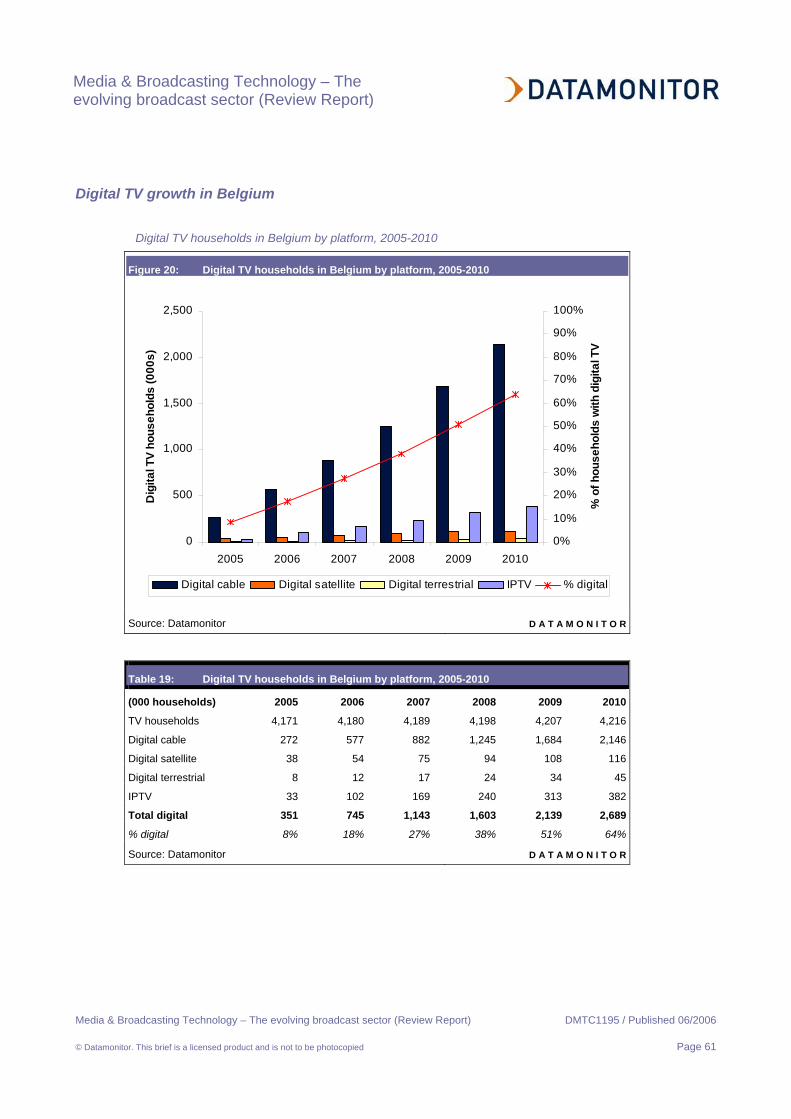

Digital TV growth in Austria 59

Digital TV growth in Belgium 61

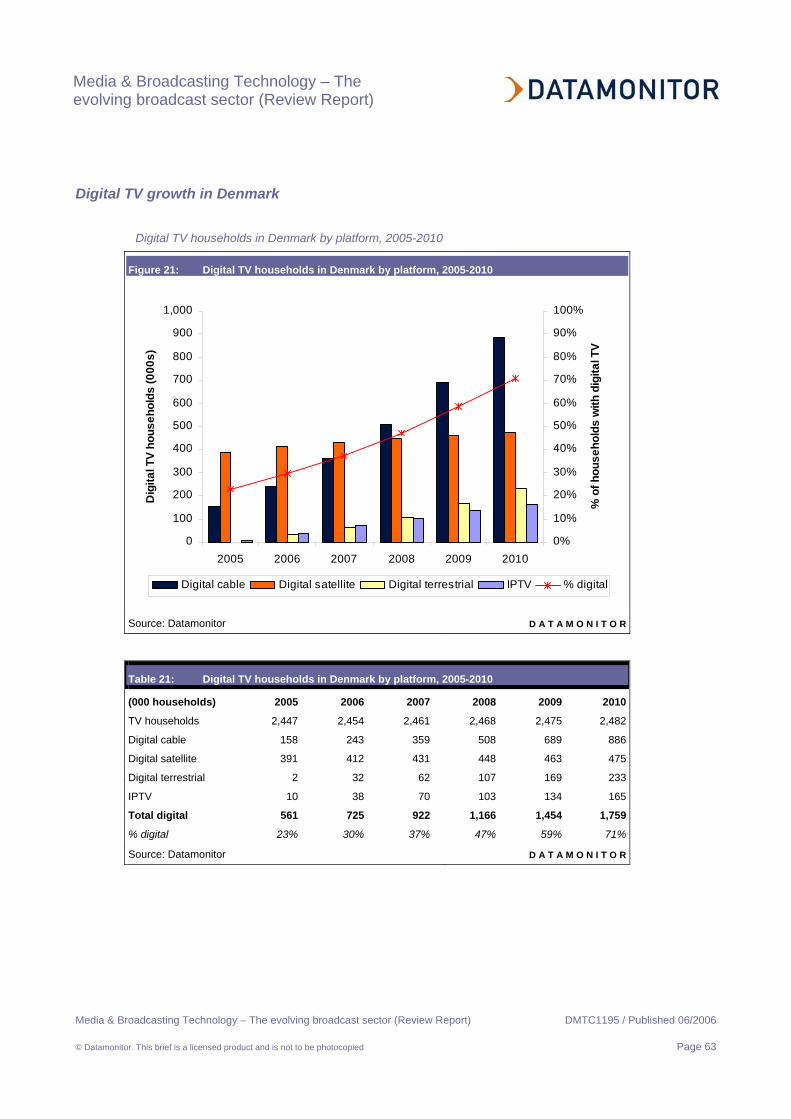

Digital TV growth in Denmark 63

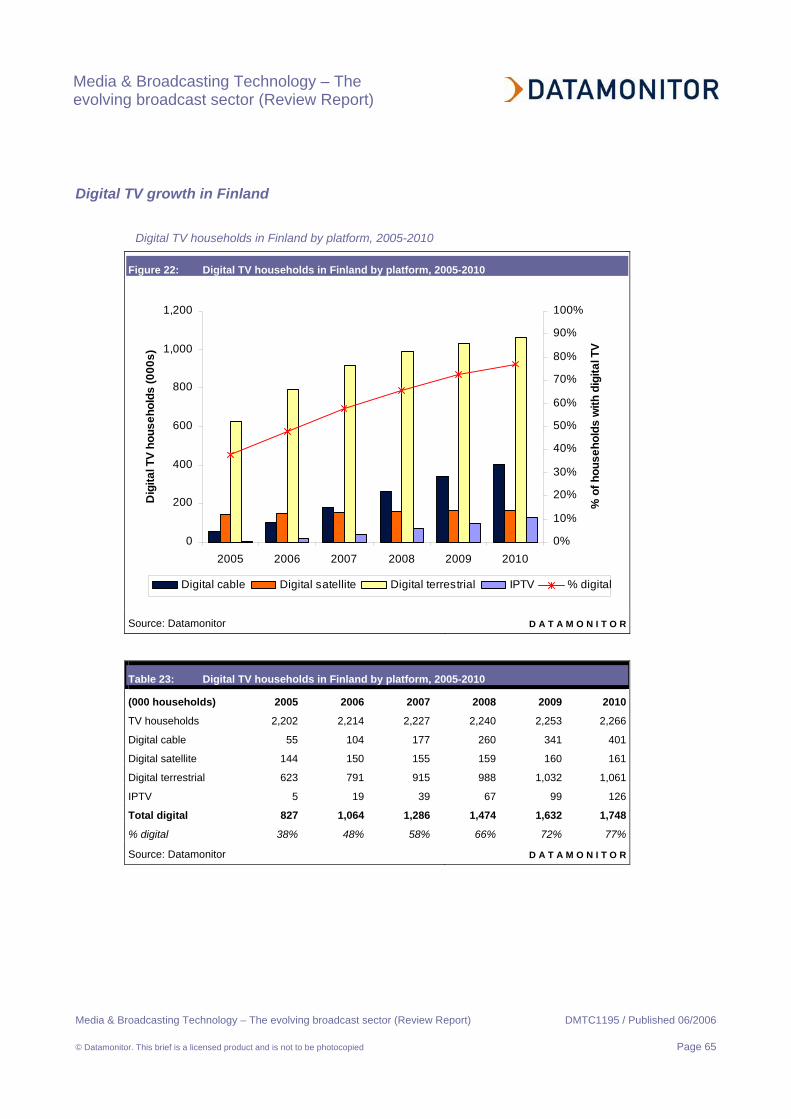

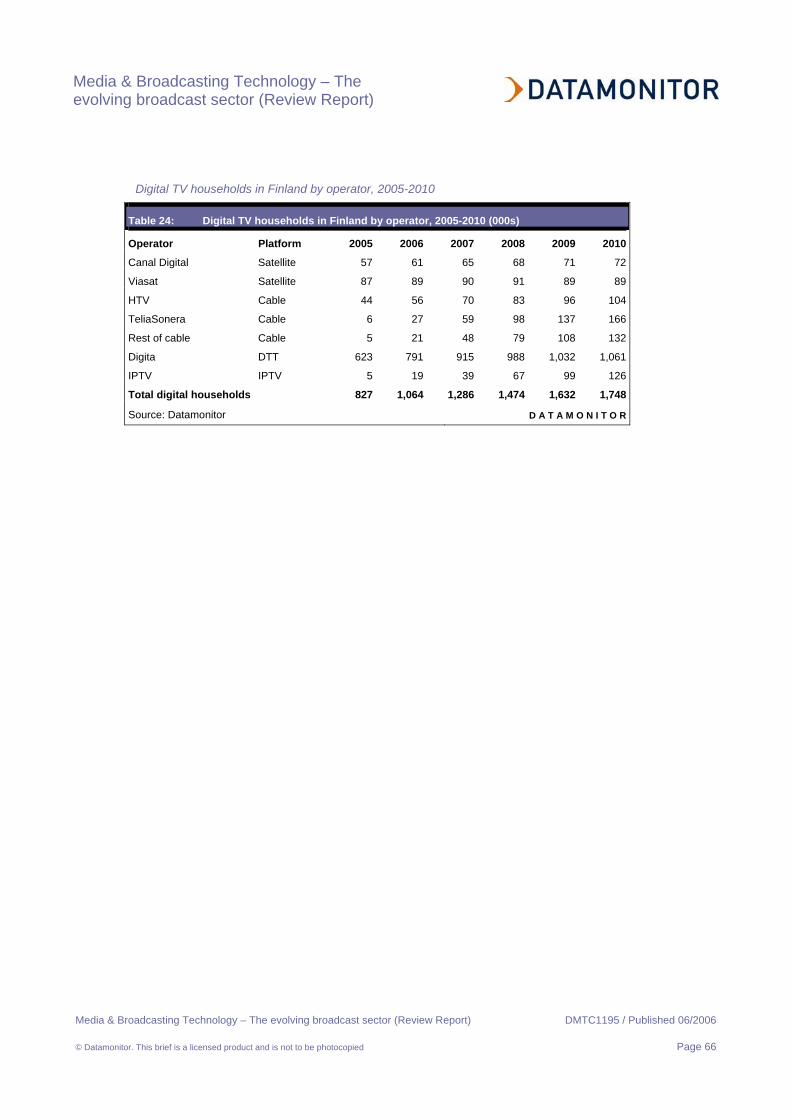

Digital TV growth in Finland 65

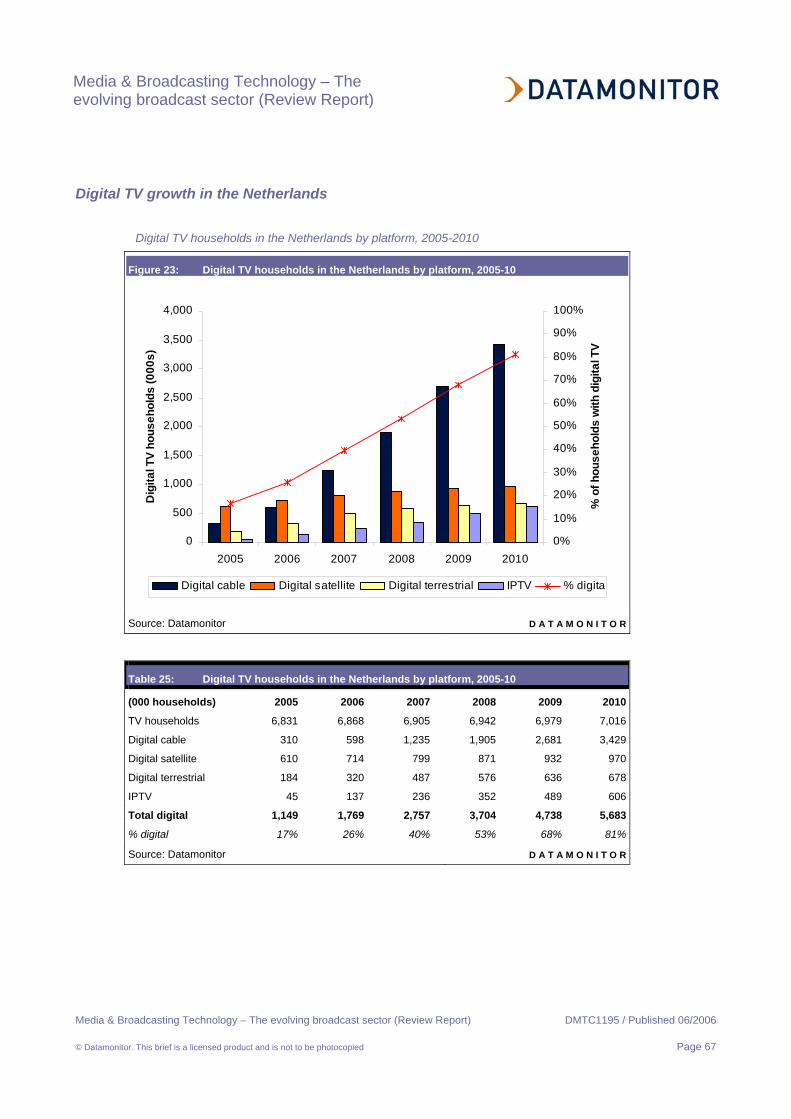

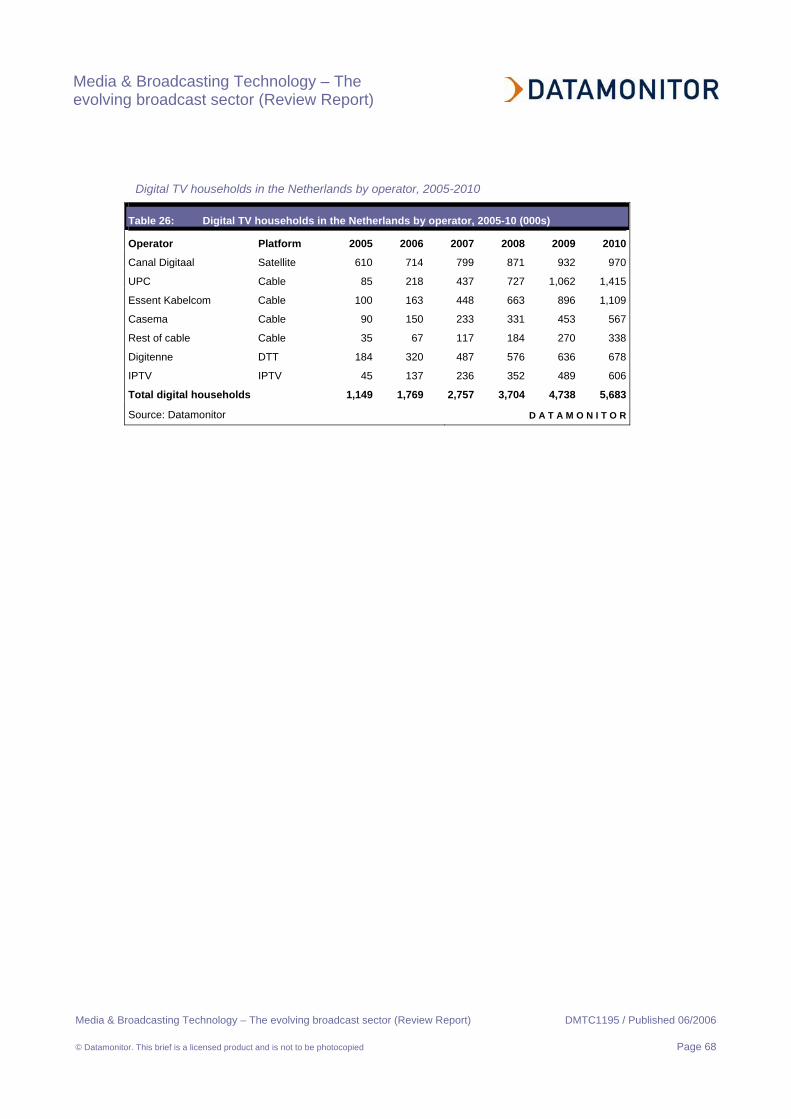

Digital TV growth in the Netherlands 67

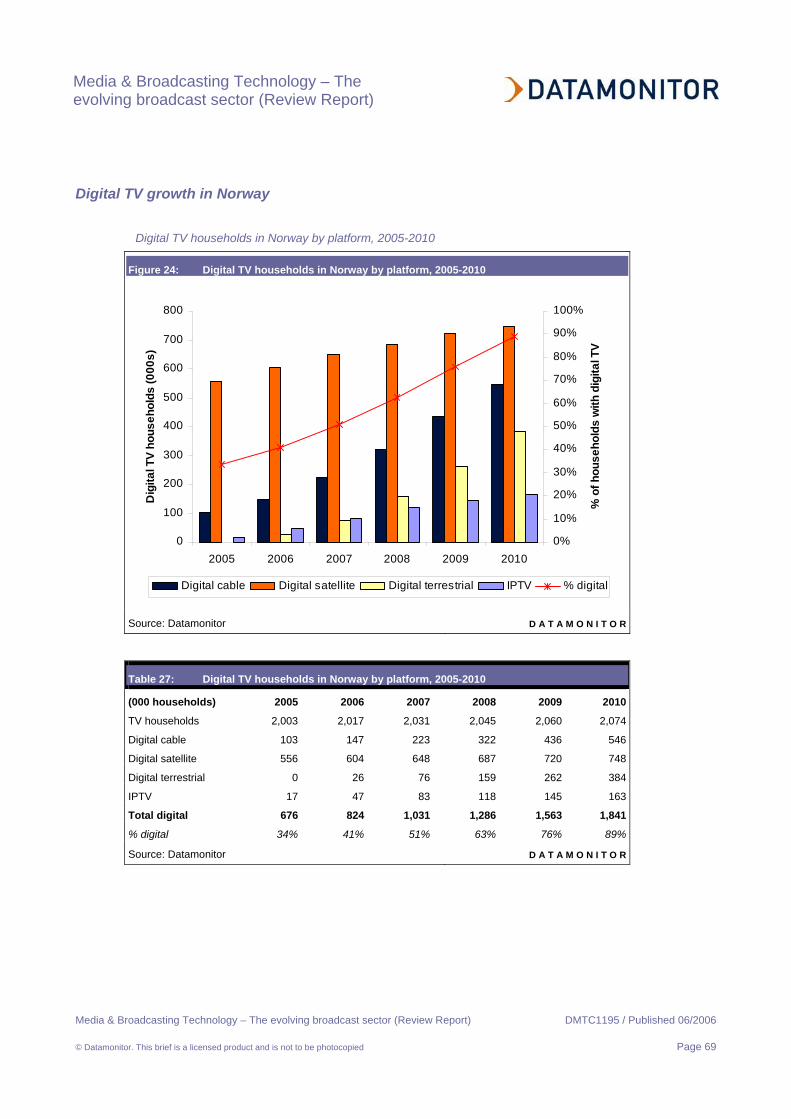

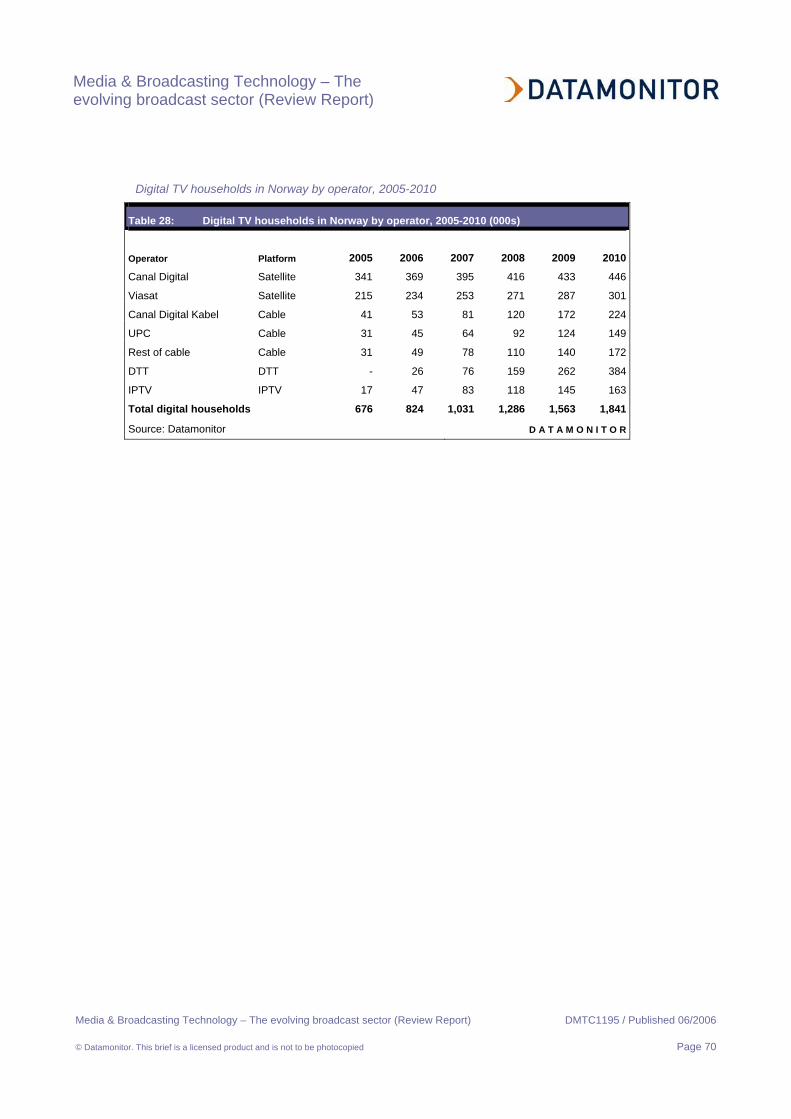

Digital TV growth in Norway 69

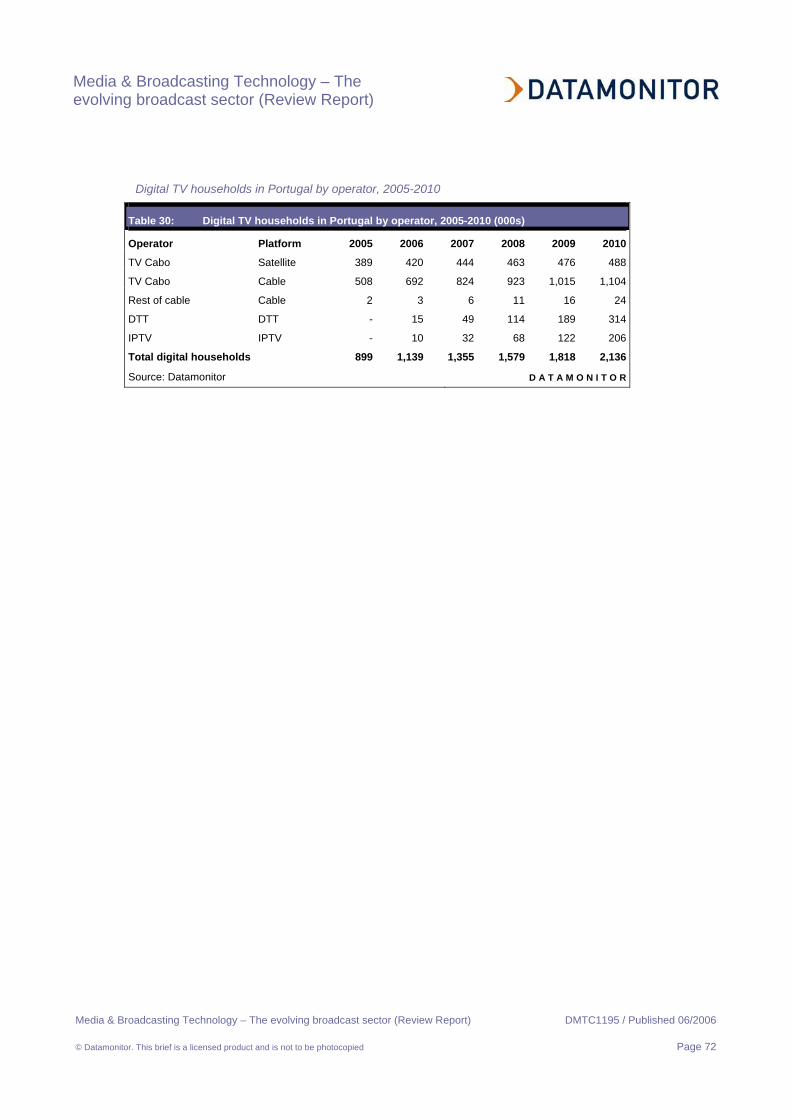

Digital TV growth in Portugal 71

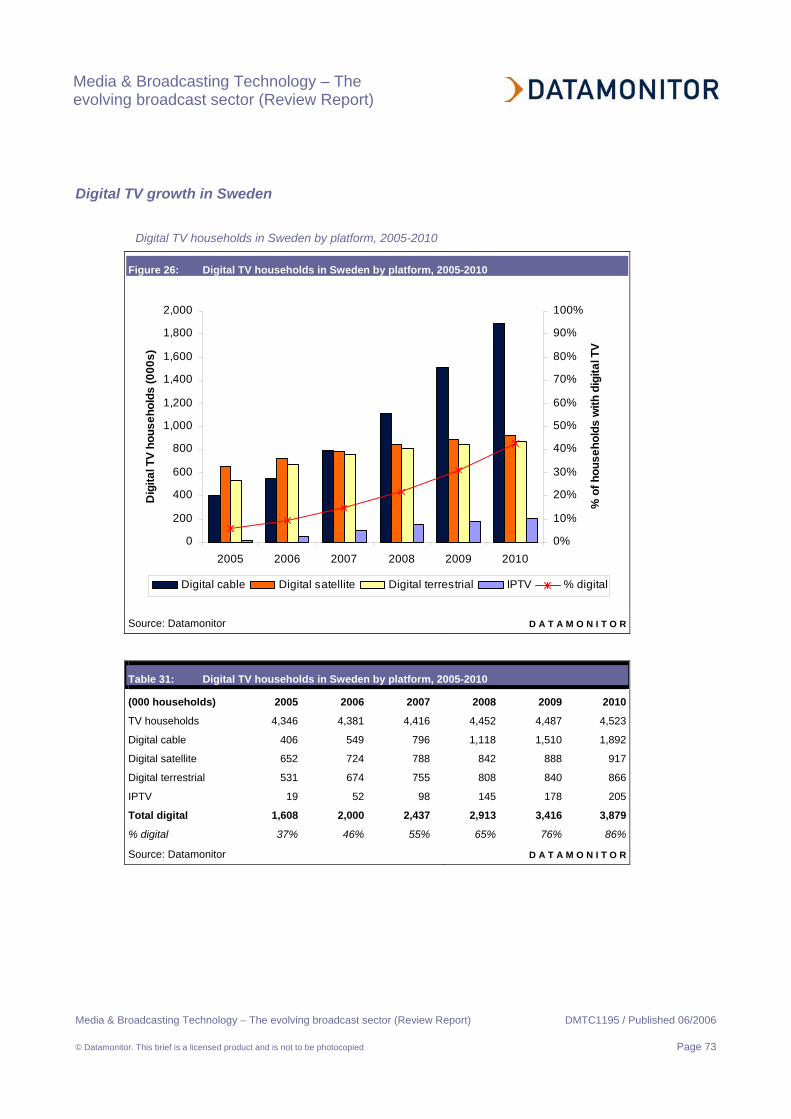

Digital TV growth in Sweden 73

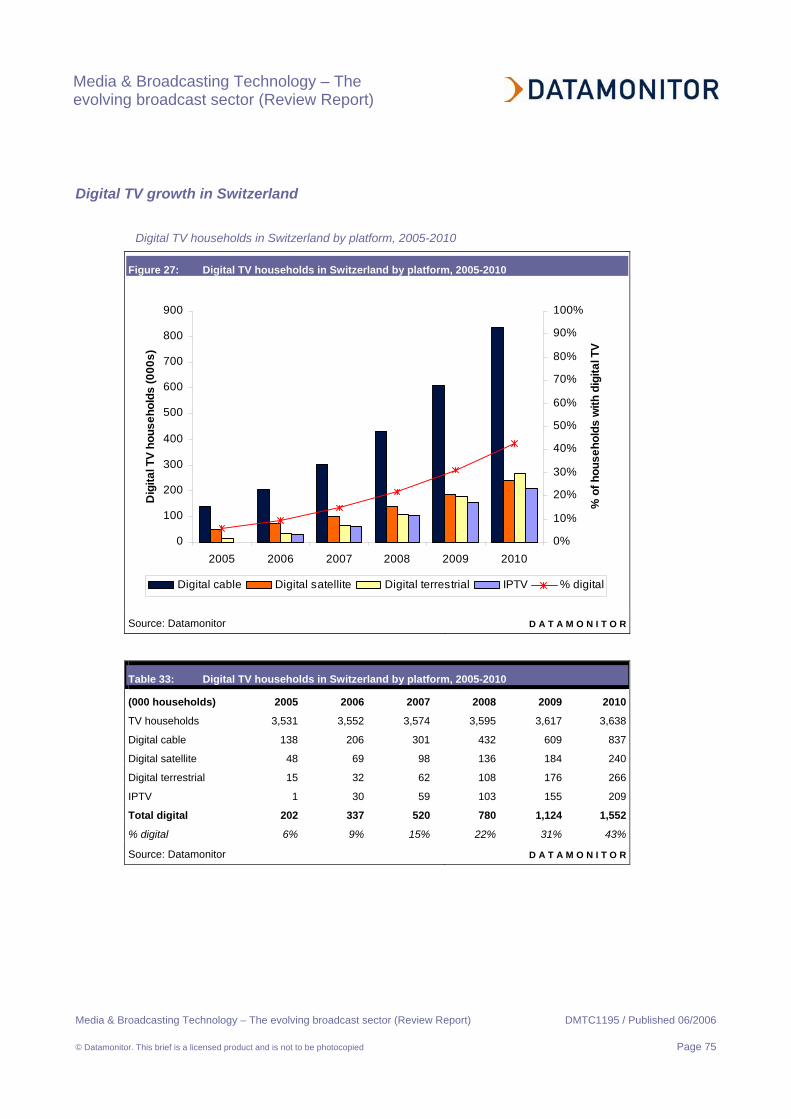

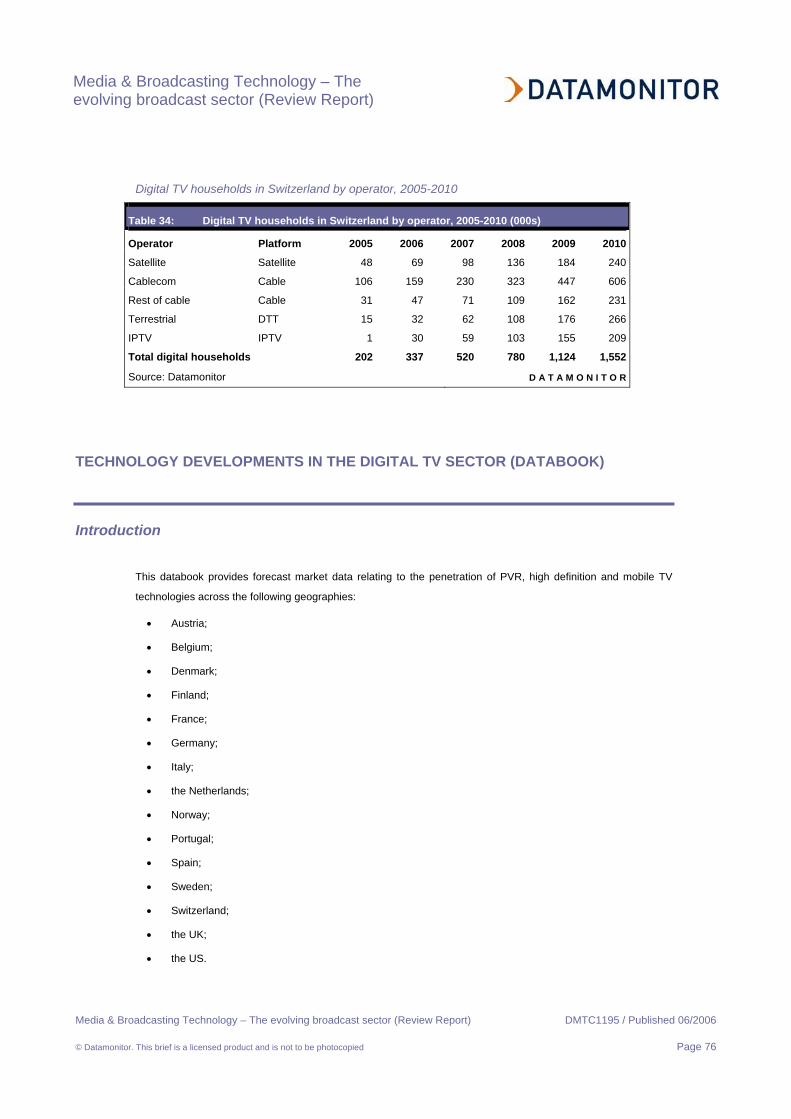

Digital TV growth in Switzerland 75

TECHNOLOGY DEVELOPMENTS IN THE DIGITAL TV SECTOR (DATABOOK) 76

Introduction 76

High definition uptake comparison: Europe vs. the US, 2006-2010 78

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 6

High definition TV households in Austria, 2006-2010 79

High definition TV households in Belgium, 2006-2010 80

High definition TV households in Denmark, 2006-2010 81

High definition TV households in Finland, 2006-2010 82

High definition TV households in France, 2006-2010 83

High definition TV households in Germany, 2006-2010 84

High definition TV households in Italy, 2006-2010 85

High definition TV households in the Netherlands, 2006-2010 86

High definition TV households in Norway, 2006-2010 87

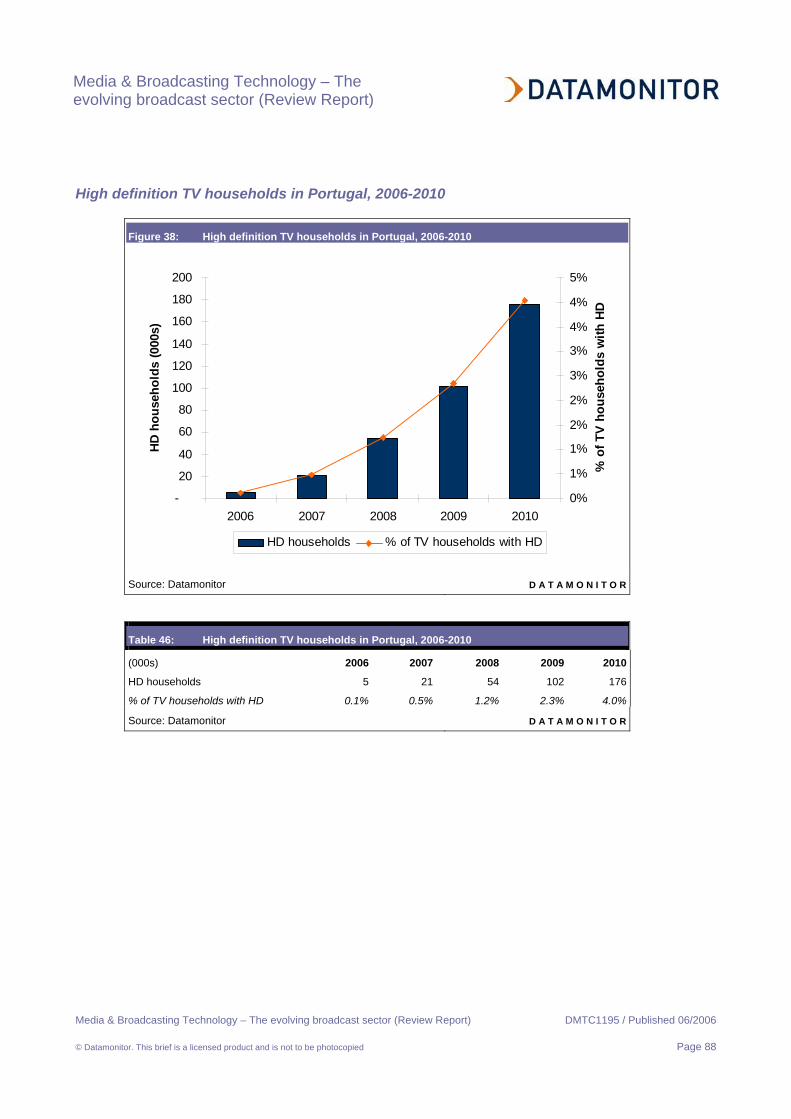

High definition TV households in Portugal, 2006-2010 88

High definition TV households in Spain, 2006-2010 89

High definition TV households in Sweden, 2006-2010 90

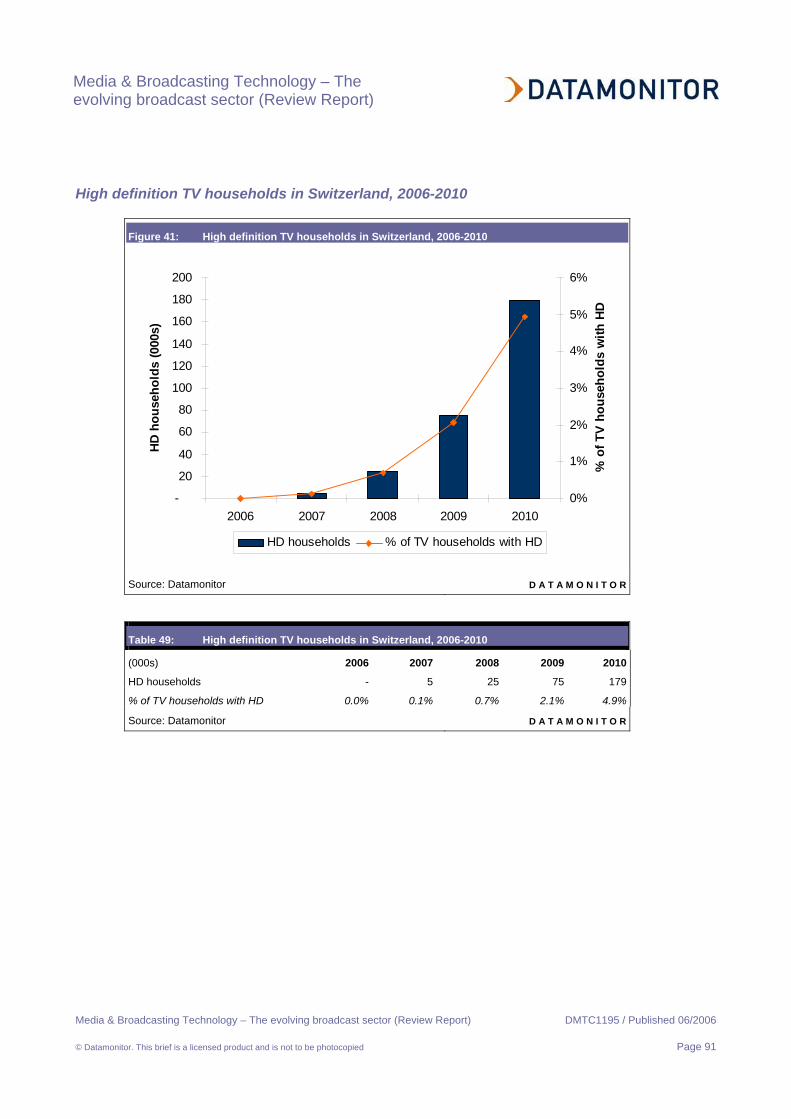

High definition TV households in Switzerland, 2006-2010 91

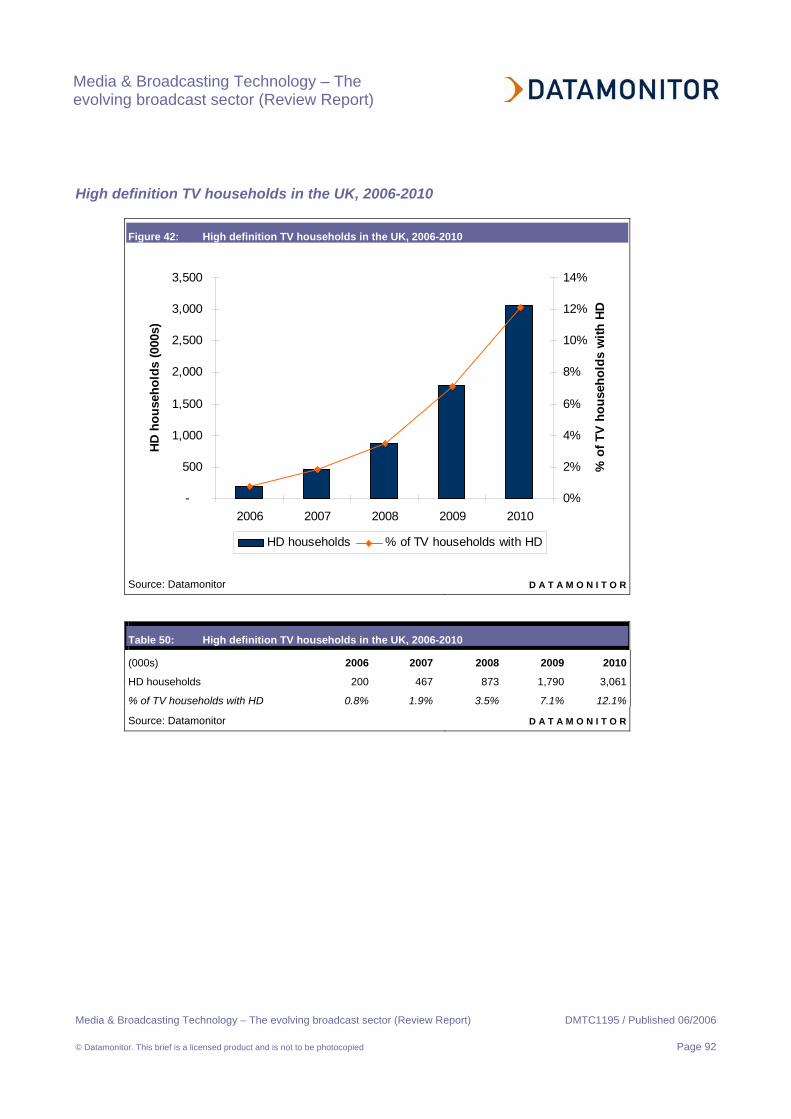

High definition TV households in the UK, 2006-2010 92

High definition TV households in the US, 2006-2010 93

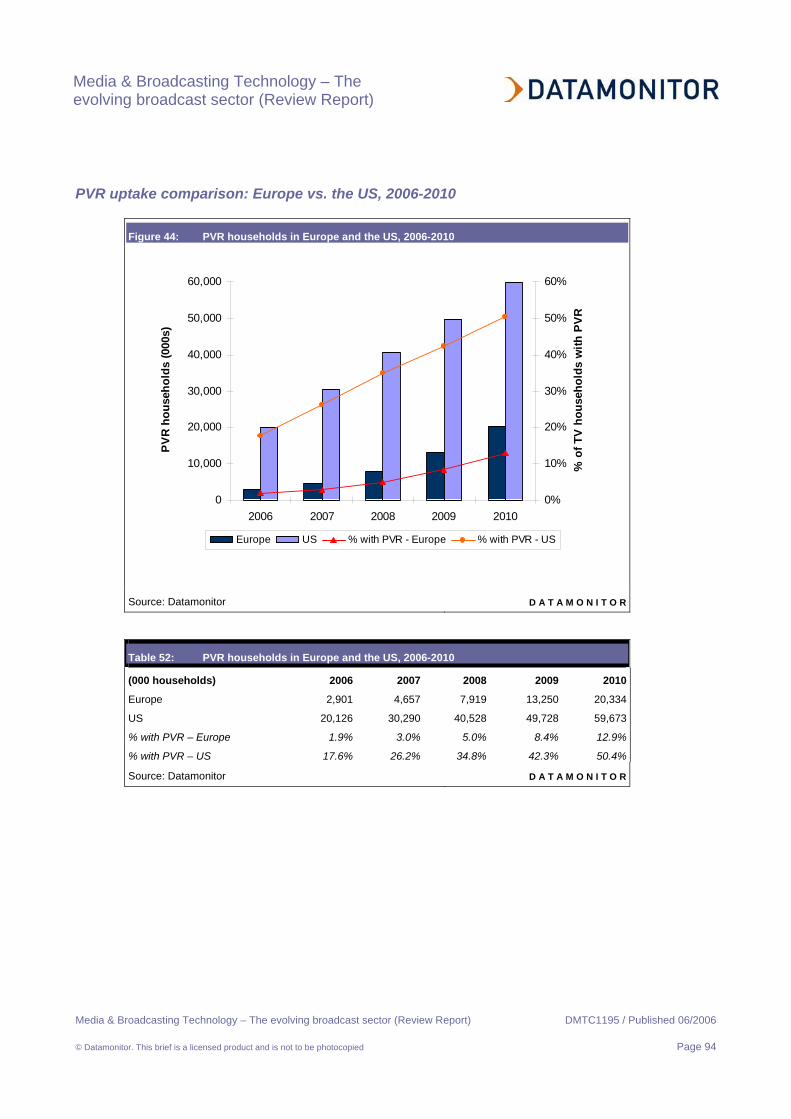

PVR uptake comparison: Europe vs. the US, 2006-2010 94

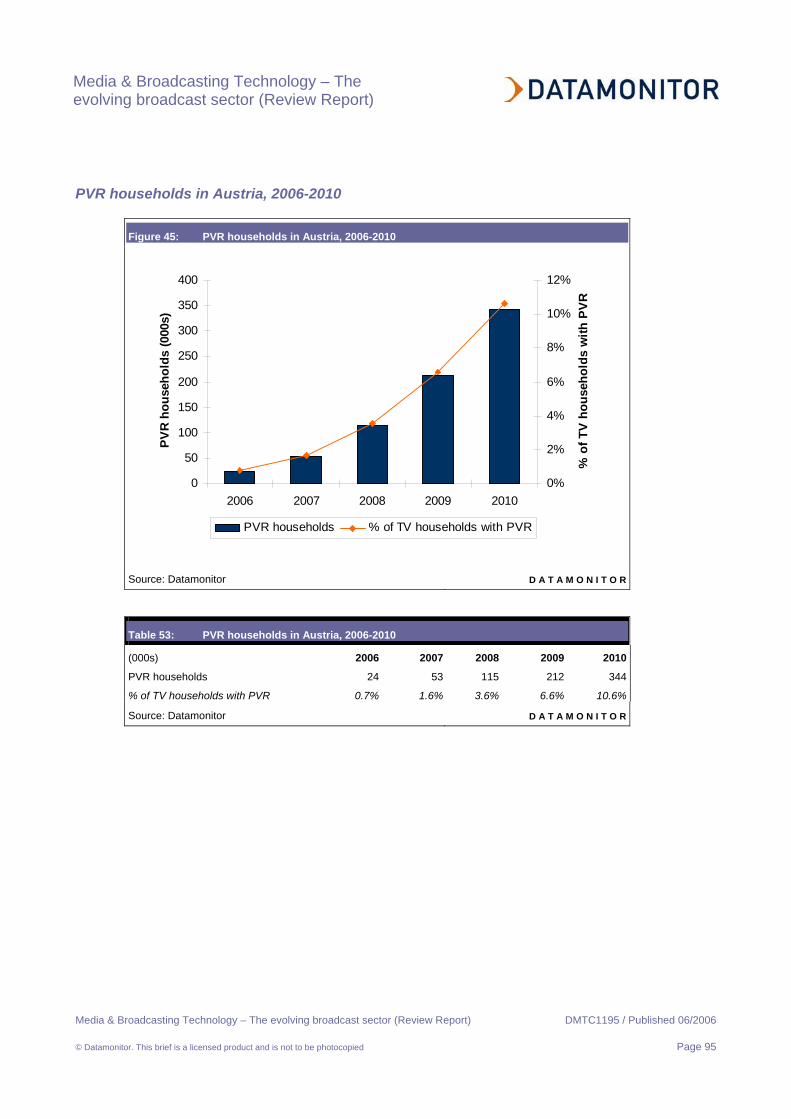

PVR households in Austria, 2006-2010 95

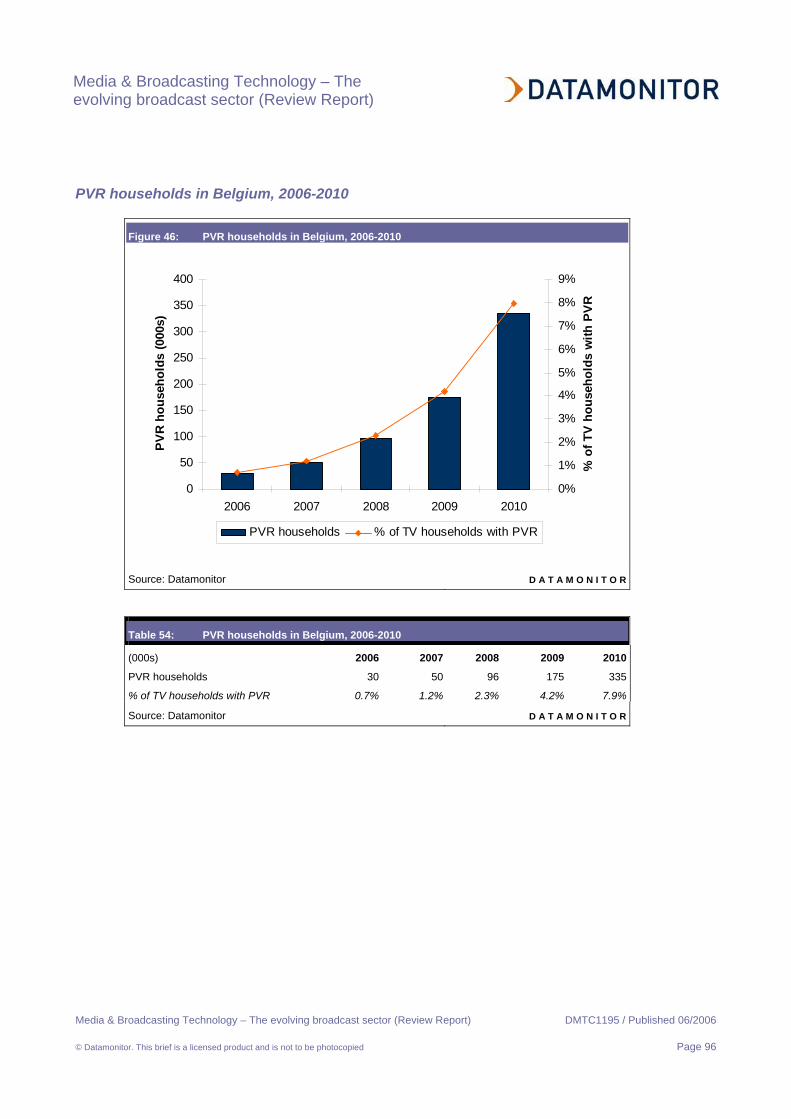

PVR households in Belgium, 2006-2010 96

PVR households in Denmark, 2006-2010 97

PVR households in Finland, 2006-2010 98

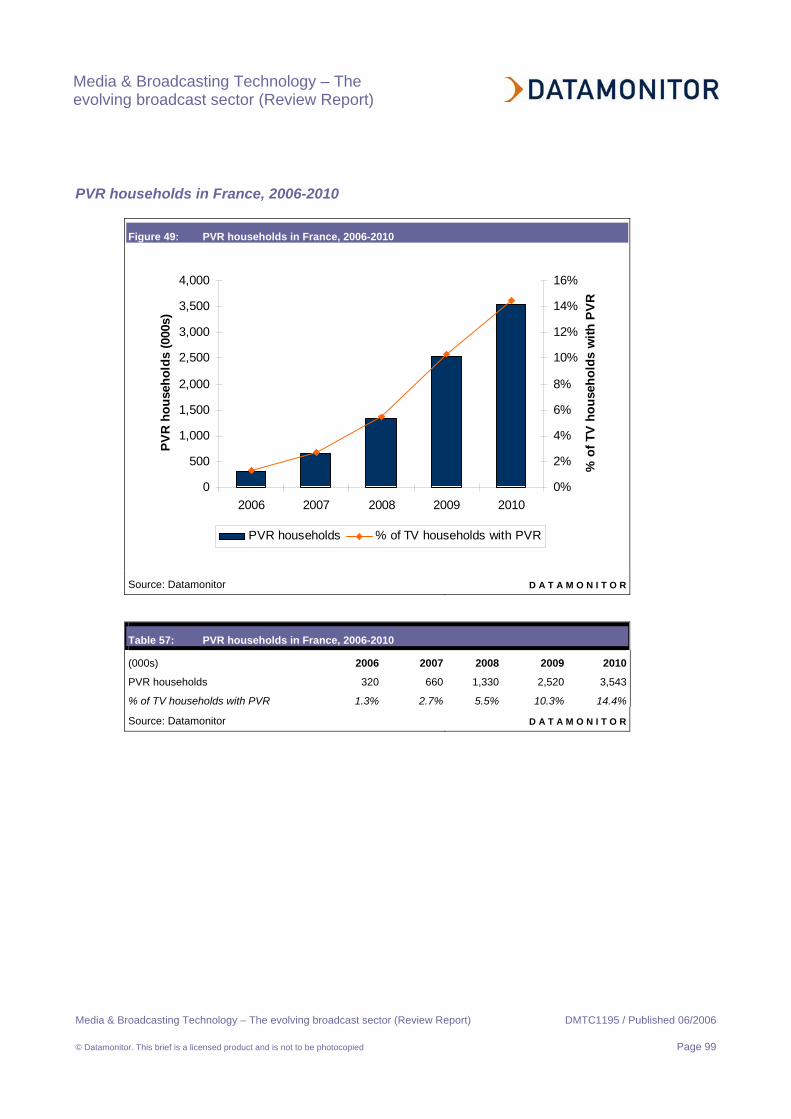

PVR households in France, 2006-2010 99

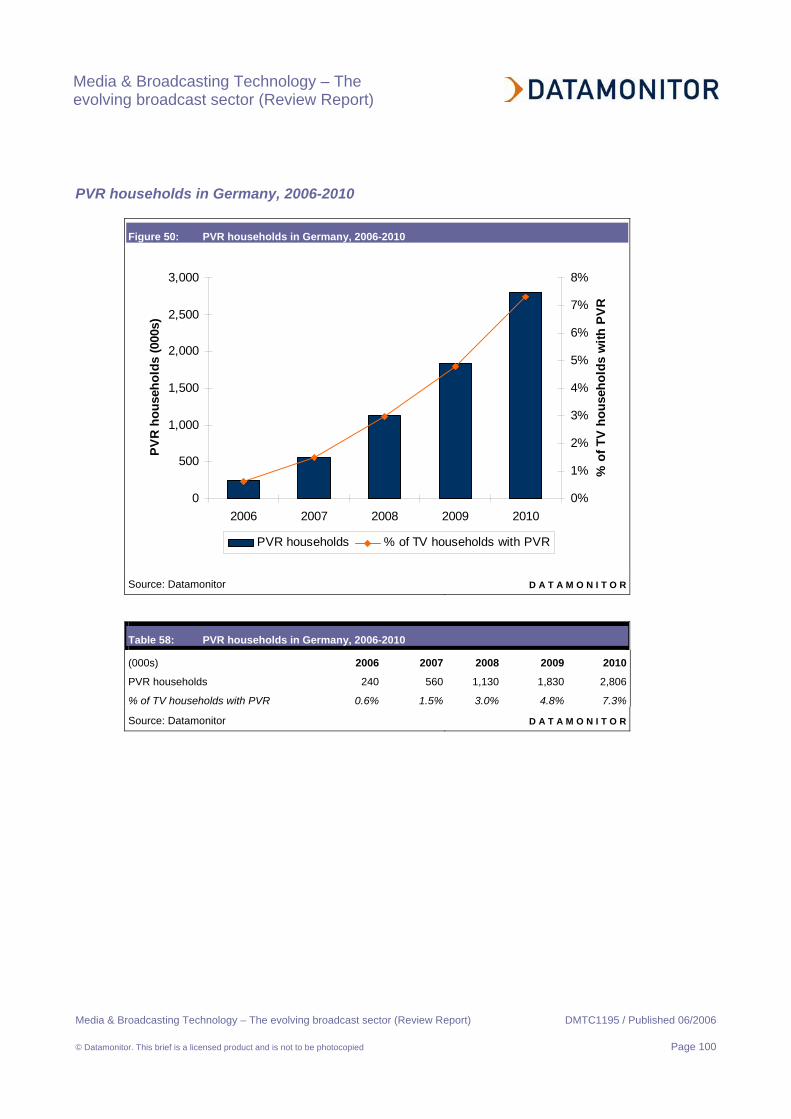

PVR households in Germany, 2006-2010 100

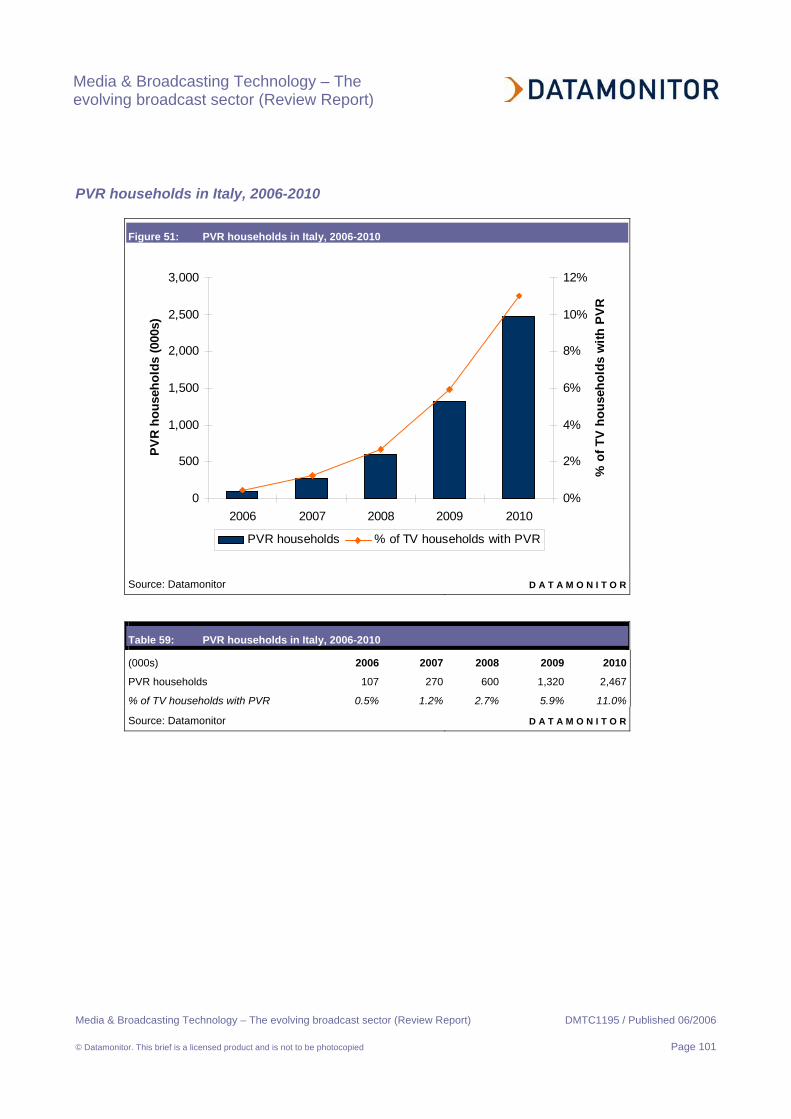

PVR households in Italy, 2006-2010 101

PVR households in the Netherlands, 2006-2010 102

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 7

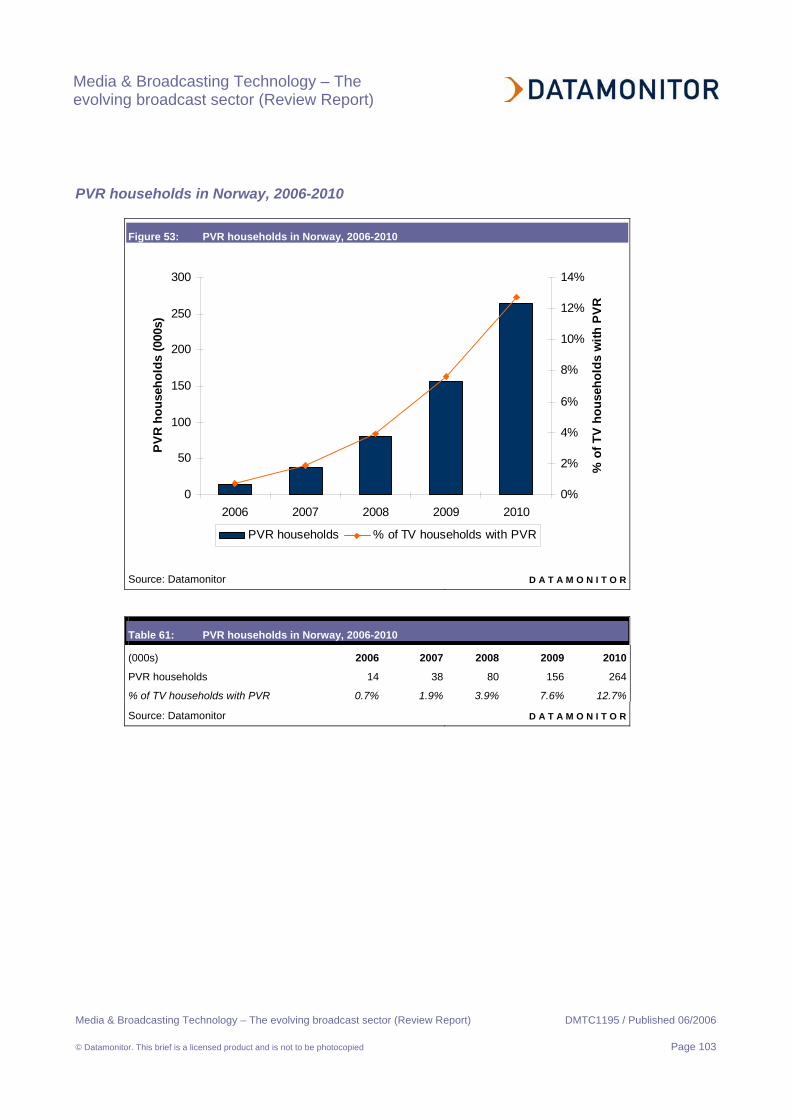

PVR households in Norway, 2006-2010 103

PVR households in Portugal, 2006-2010 104

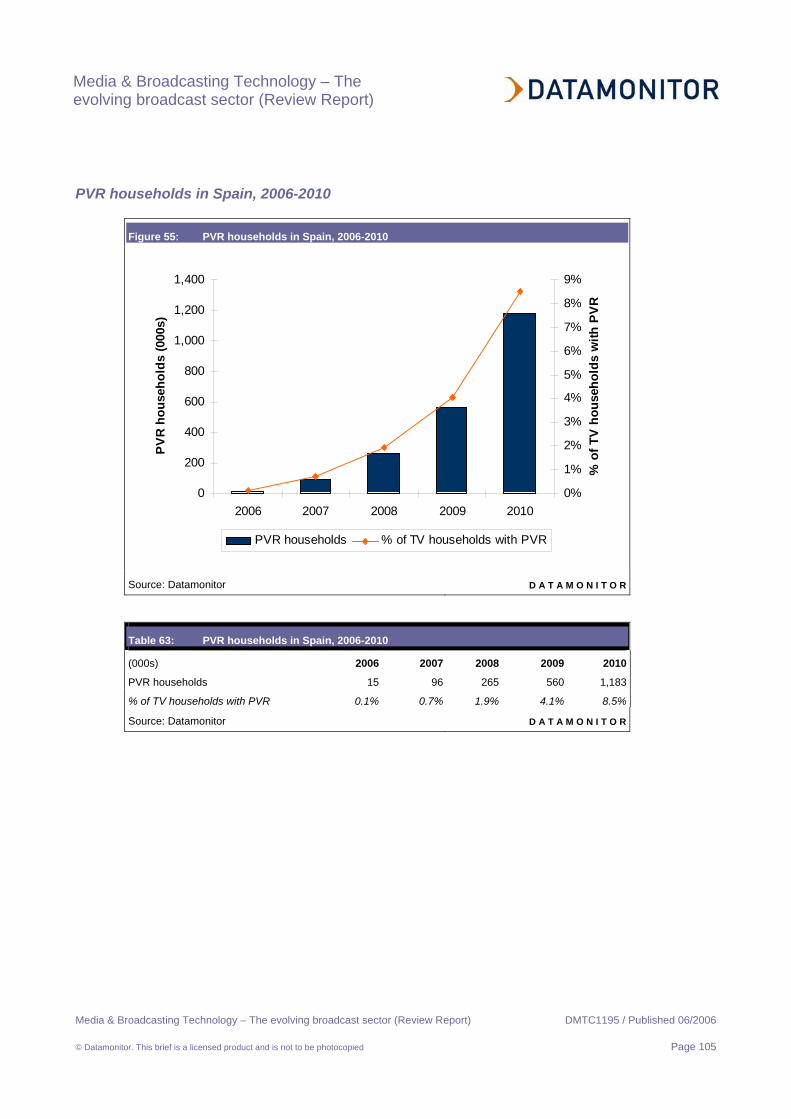

PVR households in Spain, 2006-2010 105

PVR households in Sweden, 2006-2010 106

PVR households in Switzerland, 2006-2010 107

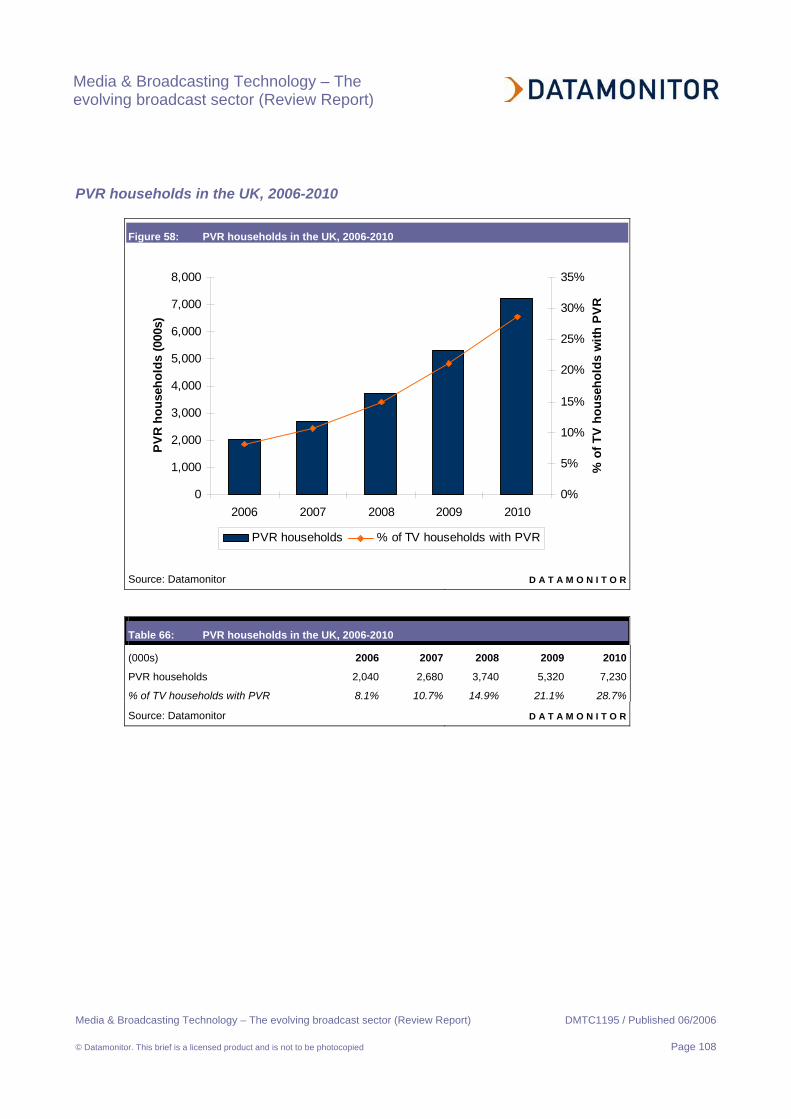

PVR households in the UK, 2006-2010 108

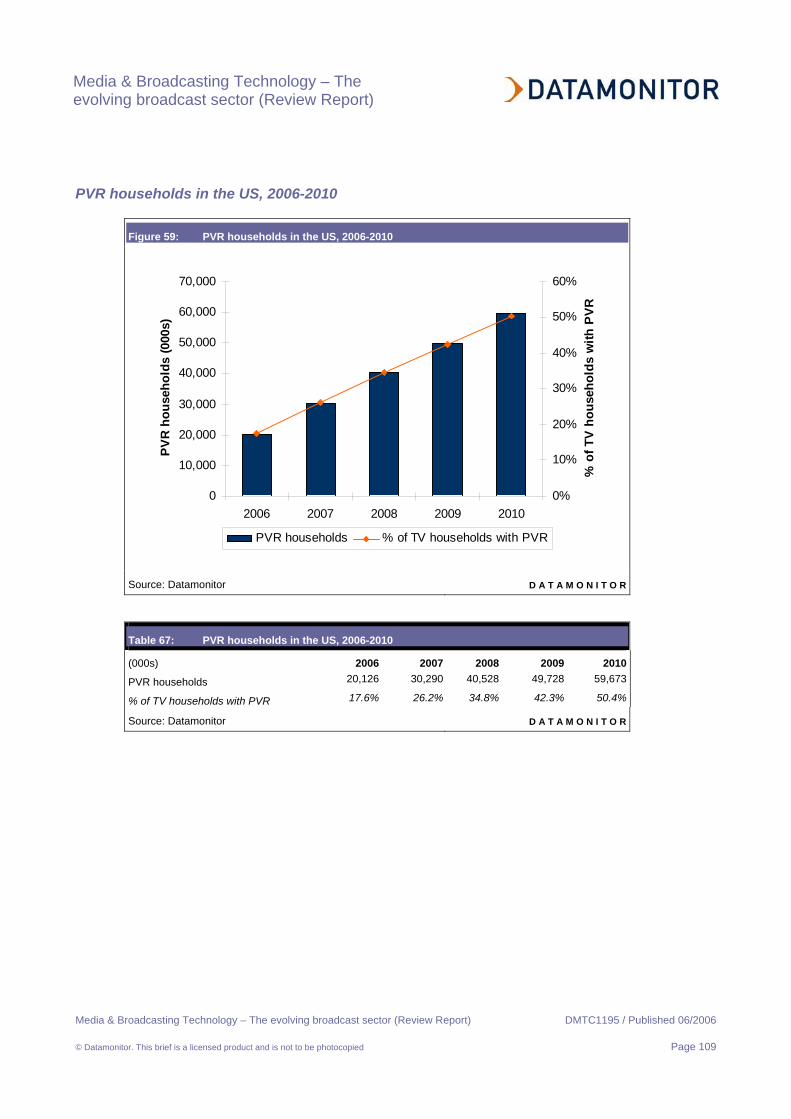

PVR households in the US, 2006-2010 109

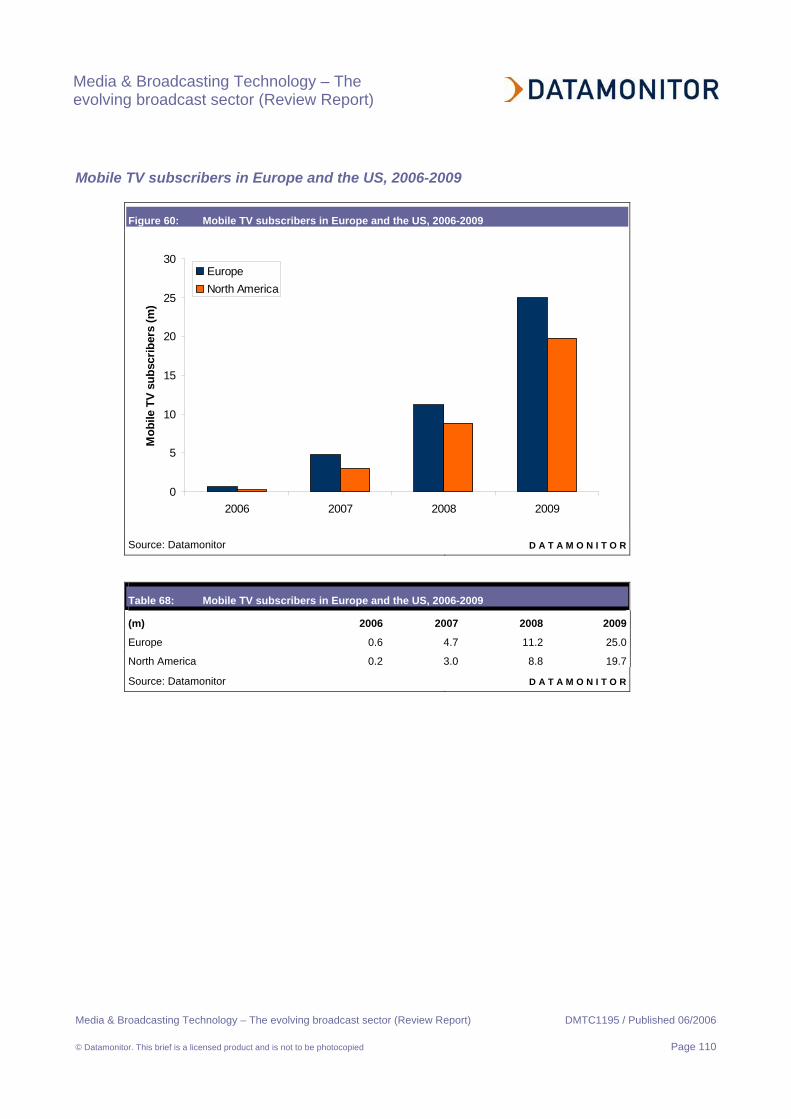

Mobile TV subscribers in Europe and the US, 2006-2009 110

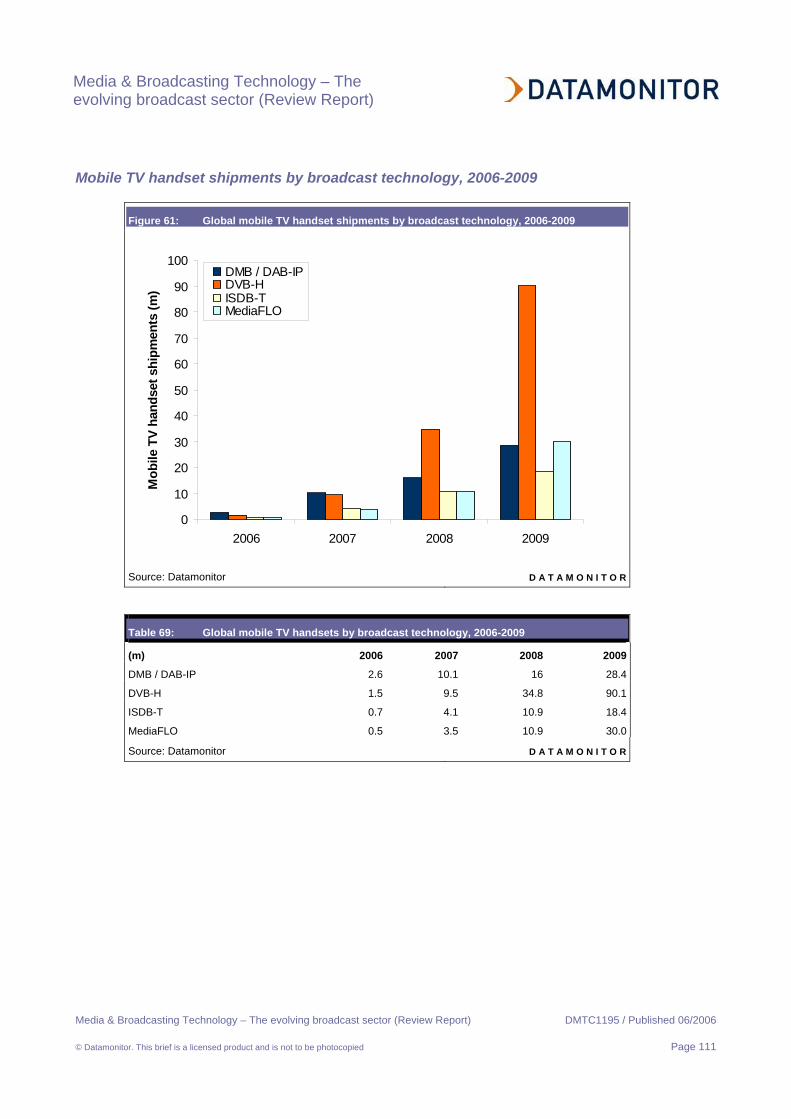

Mobile TV handset shipments by broadcast technology, 2006-2009 111

APPENDIX 112

Definitions 112

Further reading 113

Ask the analyst 113

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 8

DIGITAL TV MARKETS: EUROPE & THE US (MARKET FOCUS)

Summary

The European and the US digital TV markets are expected to show strong growth by the end of the decade, with

the emergence of IPTV acting to boost levels of competition and add new impetus to the plans of established

operators. The rate and nature of market development will continue to differ considerably between individual

country markets, although all will show a significant increase in the penetration of digital services by the end of

2010. Key findings of this brief include:

• strong digital growth expected across Europe;

• IPTV set to shake up the digital TV competitive environment;

• consolidation continues to have an impact on market dynamics.

Strong digital growth expected across Europe

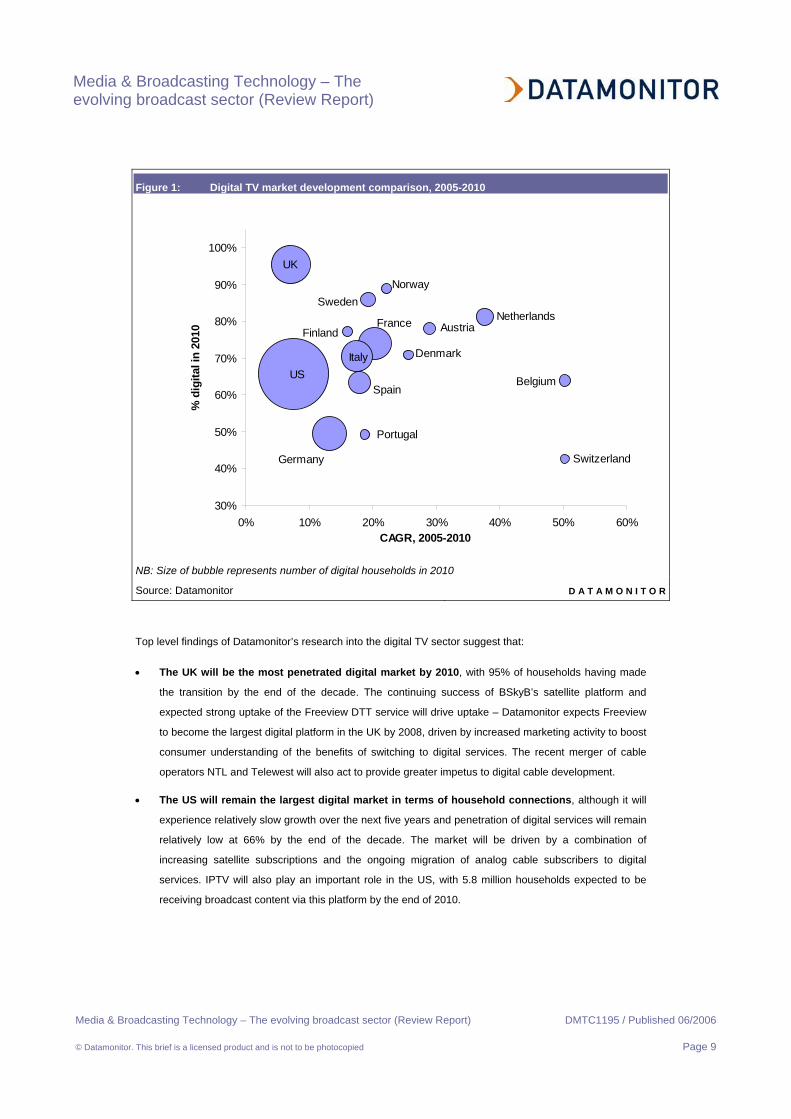

The digital TV market continued to exhibit strong growth across Europe and the US in 2005, with more than 100

million households across the two regions having made the transition from analog services by the end of the year.

However, the pace of progress with regard to the penetration of digital services continues to vary significantly

between individual country markets, with the UK remaining the only market where more than half of households

had made the transition by the end of 2005. The following figure compares current and future development in

Western Europe and the US from 2005 to 2010, highlighting the fact both expected uptake of digital TV services

and the rate at which individual markets will grow over the forecast period will continue to differ considerably.

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 9

Figure 1: Digital TV market development comparison, 2005-2010

Italy

Germany

Portugal

Denmark

Finland France

Spain

Netherlands Austria

Switzerland

Sweden Norway

Belgium US

UK

30%

40%

50%

60%

70%

80%

90%

100%

0% 10% 20% 30% 40% 50% 60%CAGR, 2005-2010

% d

igita

l in

2010

NB: Size of bubble represents number of digital households in 2010

Source: Datamonitor D A T A M O N I T O R

Top level findings of Datamonitor’s research into the digital TV sector suggest that:

• The UK will be the most penetrated digital market by 2010, with 95% of households having made

the transition by the end of the decade. The continuing success of BSkyB’s satellite platform and

expected strong uptake of the Freeview DTT service will drive uptake – Datamonitor expects Freeview

to become the largest digital platform in the UK by 2008, driven by increased marketing activity to boost

consumer understanding of the benefits of switching to digital services. The recent merger of cable

operators NTL and Telewest will also act to provide greater impetus to digital cable development.

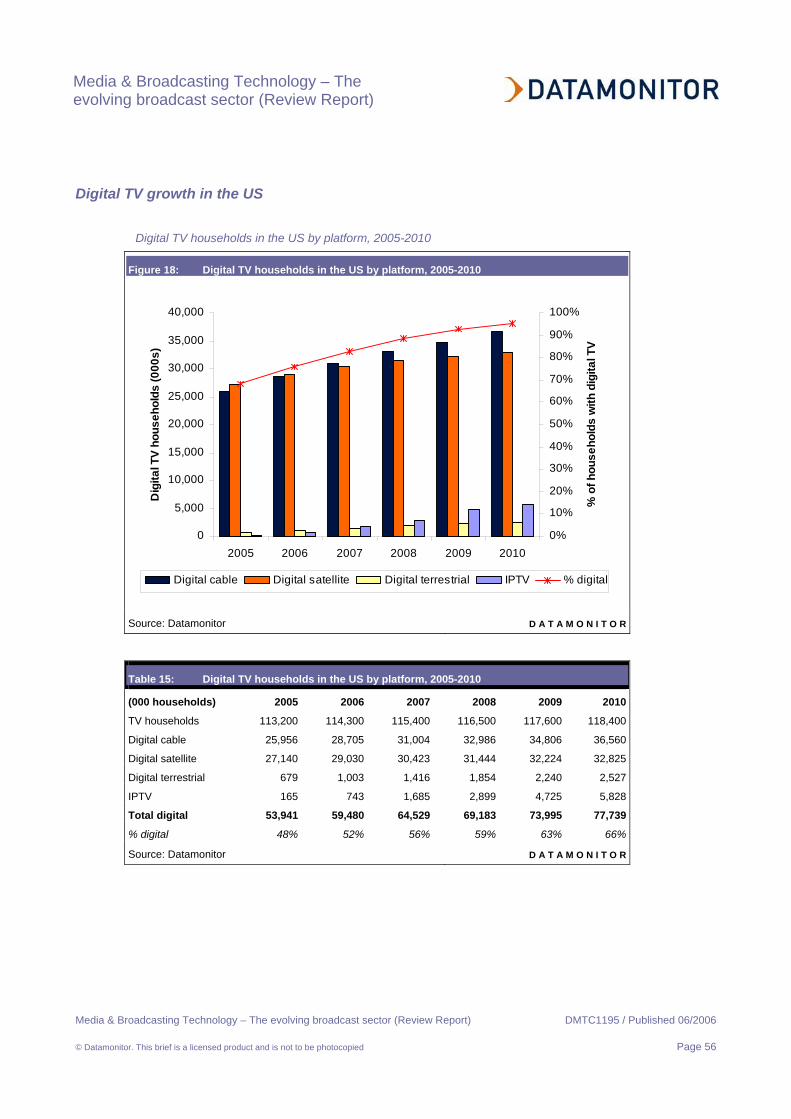

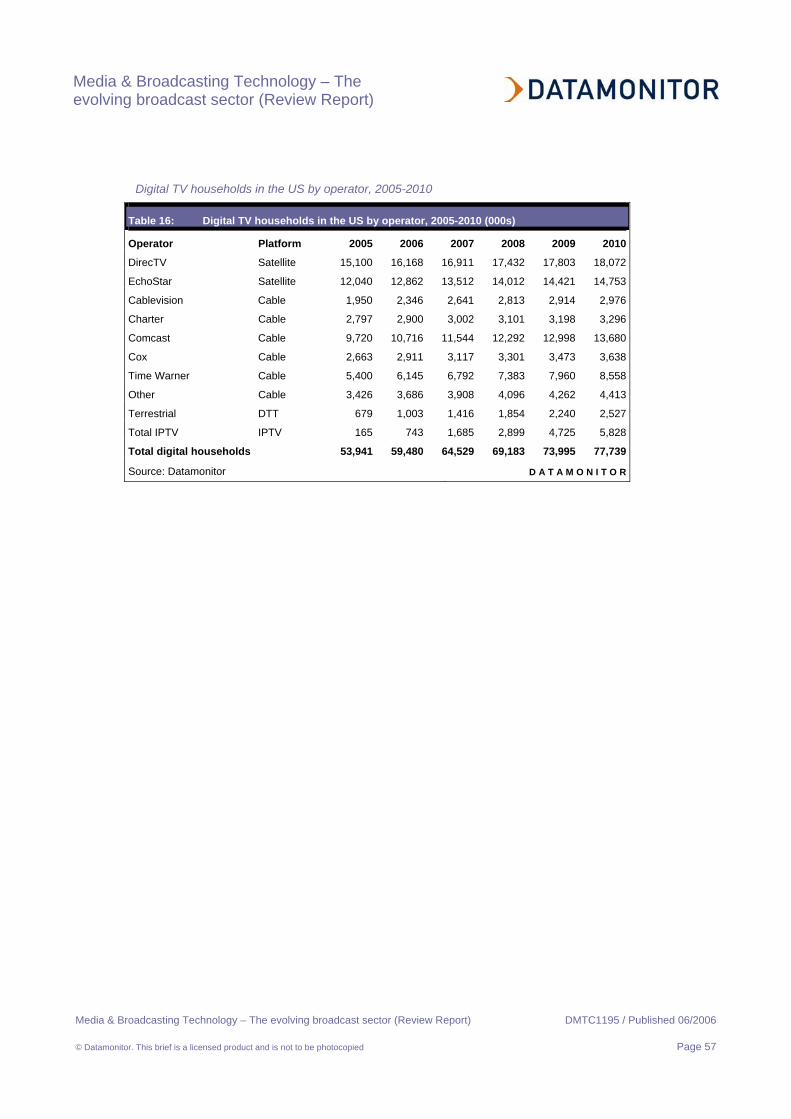

• The US will remain the largest digital market in terms of household connections, although it will

experience relatively slow growth over the next five years and penetration of digital services will remain

relatively low at 66% by the end of the decade. The market will be driven by a combination of

increasing satellite subscriptions and the ongoing migration of analog cable subscribers to digital

services. IPTV will also play an important role in the US, with 5.8 million households expected to be

receiving broadcast content via this platform by the end of 2010.

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 10

• Belgium will experience the strongest growth over the forecast period, driven by the development

of the digital cable sector, which is currently very underdeveloped. IPTV will also have an impact on the

Belgian market, with over 300,000 households expected on Belgacom’s platform by the end of 2010.

• In Germany, Europe’s largest TV market, the digital value proposition has proved less powerful

than in many markets – the sizable multi-channel subscriber base that currently receives a broad

range of channels via analog cable services is in no rush to migrate to digital, making rapid

infrastructure investment an unattractive option for operators. However, Datamonitor believes that

recent cable consolidation will to drive digital development plans, helping to boost digital penetration to

nearly 50% of households by the end of 2010.

Europe set to overtake the US in 2006

Digital TV penetration in Europe is currently lower than that in the US, where cable and satellite operators are in

intense competition. In the US, there 27 million satellite subscribers at the end of 2005, compared with around 26

million digital cable households – the penetration of digital services among cable operators’ total subscriber bases

continues to grow, with approaching half of many cable operators’’ subscribers having made the transition to

digital service by the end of 2005. In contrast, many European cable operators are only just making their first

tentative steps with regard to digital services, holding back digital penetration levels.

Figure 2: Digital TV uptake comparison: Europe vs. the US, 2005-2010

0

20,000

40,000

60,000

80,000

100,000

120,000

2005 2006 2007 2008 2009 2010

Digi

tal T

V h

ouse

hold

s (0

00s)

0%

10%

20%

30%

40%

50%

60%

70%

80%

% o

f hou

seho

lds

with

dig

ital T

V

Europe US % digital - Europe % digital - US

Source: Datamonitor D A T A M O N I T O R

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 11

As shown in the figure above, Datamonitor expects the European digital TV market to overtake the US in absolute

terms by the end of 2006, at which point almost 65 million households across the region will have made the

transition to digital TV services. However, digital penetration will remain higher in the US until the end of 2009 – at

this point, around 63% of households in both the US and Europe will be receiving digital TV services. The key

driver of European digital TV uptake over the forecast period is expected to be DTT, which will to drive uptake to

109 million by the end of 2010 – compared to 78 million in the US at the same period.

European market growth dependent on DTT and migration to digital cable services

Across Europe as a whole, cable infrastructure is slowly being upgraded to digital, with customer migration to

digital services proving to be rather limited in many markets. However, strong growth is expected across Europe,

driven by a number of key factors:

• Strong growth in DTT in France, Italy, Spain and the UK, driven by the EU analog switch-off dates.

All of these major TV markets have a relatively strong reliance on terrestrial reception compared to

other more cable-centric markets, and hence migrating analog households to DTT will be a key

requirement over the next five years.

• Increasing migration of analog cable subscribers to digital services, driven by operators’ desire to

deploy triple play services in order to strengthen their competitive offerings relative to both satellite and,

increasingly, IPTV.

• Continued growth of satellite services in the UK, Italy, Spain and the Nordics, driven by the

deployment of new services (HD in particular) and the strong content offerings that these operators

provide.

• The emergence of IPTV services, which are already gaining a foothold in a number of markets

including France, Spain and Italy. Datamonitor expects strong growth across this platform as incumbent

operators seek to strengthen their market position by adding TV services to their service portfolios.

In contrast, the US market will be largely driven by the continuing migration of analog cable subscribers to digital

services, with over 10 million households expected to make this transition between 2005 and 2010. IPTV will also

become a significant platform over the forecast period, with almost 6 million households connected by the end of

the forecast period. The following section highlights expected progress across the three established platforms for

digital TV (cable, satellite and DTT).

Digital cable: slow progress continues in core European cable markets

The European digital cable market has continued its slow progress in 2005. Datamonitor retains high hopes for

strong growth in many of the key cable markets over the next few years, although there remains a lack of interest

on the part of both consumers and operators to make the transition in many markets. The UK is expected to

continue to lead the European market in terms of digital penetration of cable services, with Telewest reaching

93% digital penetration by the end of 2005 and expecting to switch off analog services in 2006. Strong growth is

expected in heavily cable markets including the Netherlands and Belgium, although German digital development

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 12

remains relatively sluggish. However, Datamonitor expects recent consolidation of the German cable market to

help to drive migration to digital services, with greater economies of scale within operators helping to boost

investment levels.

Digital penetration reaches almost 50% in US cable sector

In the US, digital penetration among cable subscribers is approaching the 50% mark: Comcast, the largest cable

operator in the US, had migrated around 46% of its subscribers to digital services by the end of 2005, while the

innovative Cablevision is approaching the two-thirds mark. Despite this healthy position, Datamonitor expects

relatively slow progress over the next five years, with approximately 60% of cable subscribers using digital

services by the end of 2010. However, the need to free up capacity for the further development of HD services is

likely to prompt operators to boost their efforts in this regard. The emergence of IPTV services – not just in the US

but also across Europe – is also likely to prompt greater focus on driving digital adoption, with the need to offer

VOD services to compete on an even footing with new competitors becoming increasingly important.

Digital satellite: steady, if unspectacular progress

The digital satellite market remains dominated by pay-TV operators, with the only significant exception being

Germany where FTA satellite services are commonplace. Around 24 million European households and 27 million

US households now receive digital satellite services, with continued growth anticipated by the end of 2010.

Datamonitor expects the strongest satellite growth to occur in Germany, where the number of digital households

will increase to almost 11 million by the end of 2010, driven primarily by the FTA market which will double in size

over the forecast period. In the other major European markets, Datamonitor expects relatively slow growth – the

pay-TV markets in France, Spain the UK are nearing saturation point, with further digital growth expected to come

primarily from FTA services. Free-to-air satellite services are already commonplace in Germany, while plans are

afoot to launch a FreeSat service in the UK – although the huge success of FTA DTT services has resulted in

plans being delayed for the foreseeable future.

Solid growth anticipated for US satellite

The US satellite market continues to grow, with over 2 million subscribers added in 2005. Datamonitor expects

around 5.7 million more subscribers to be added by DIRECTV and EchoStar over the forecast period, with around

33 million households accessing pay-TV services via digital satellite by the end of 2010, representing nearly 28%

of all US TV households. With subscriber growth beginning to slow, Datamonitor expects the operators to focus

increasing efforts on increasing ARPU levels via investment in HD programming and PVR technology, while a

merger of the rival providers remains a possibility.

Digital terrestrial television (DTT): Europe’s largest platform by 2008

DTT continues to be a major success story in the markets where it has launched on a FTA basis – the strong

uptake of services seen in the UK has been followed by substantial growth in other key terrestrial-dominated

markets including France, Italy and Spain. However, DTT services have yet to be fully launched in a number of

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 13

European markets including Austria, Belgium and Denmark – in these markets, there is little compelling reason to

invest heavily in DTT services due to the high penetration of cable and satellite services. In Belgium, for example,

the dominance of cable (over 90% of households receive TV content via this platform) and the emergence of IPTV

services means that there is no real incentive to deploy widespread DTT services. Datamonitor believes that the

most significant opportunities for DTT provision across Europe have already been exploited, with remaining

markets having limited reliance on analog terrestrial reception and hence less significant need for DTT rollout.

Overall, however, DTT will be the largest digital platform by the end of 2008, with over 30 million households using

the platform as their primary means of receiving digital TV services by this time.

DTT will remain a niche proposition in the US

In contrast to the European market, DTT is expected to have a minimal impact in the US – only around 10% of

households use analog terrestrial as their primary reception method for TV services. However, with around 11

million households reliant on terrestrial services, transitioning households to digital services will be increasingly

important – many channels are already being broadcast in digital, with a market for DTT programming developing

as a result of the increasing propensity for new TVs to come ready equipped with a digital tuner (the FCC has

mandated that digital tuners must be integrated into all new TVs by the summers of 2007). The USDTV pay-TV

service is also likely to attract some subscribers – the $20 per month service, which offers around 30 channels,

was launched in Dallas in November 2005 following trials in three other markets.

A switch-off date of April 7th 2009 has been approved by the US Senate Commerce Committee – following the

cessation of analog broadcasts, the frequencies are set to be returned to the government for resale, and are

expected to reach up to $10 billion at auction. The Senate bill includes a $3 billion fund for set-top box subsidies,

considerably more than the $1 billion previously proposed by the House of Energy and Commerce Committee.

Datamonitor believes that high subsidy levels will help to ensure a smooth transition to DTT services in the US.

Football rights remain an essential component of European pay-TV strategies

The provision of high value content is a key driver across the pay-TV sector – consumers will understandably opt

for services that provide them will a broad range of popular and sought-after content. Across the European pay-

TV sector, top-flight football rights remains the most prized of assets – the success of many satellite providers,

including BSkyB and Premiere, has been attributed by many to the availability of exclusive football coverage.

However, recent developments in both Germany and UK have acted to disrupt the current monopolies that the

operators previously held over football rights, potentially having a significant impact on the dynamics of these pay-

TV markets.

Premiere seeking to repair the damage caused by Bundesliga rights loss

Germany’s leading pay-TV operator, Premiere, lost the rights to top-flight German football to Unity Media (a

holding company of the cable operators iesy, ish and Tele Columbus) in December 2005. Unity Media paid

€1.26bn ($1.52bn) for the rights from 2006-9; Premiere’s bid was actually higher, but the operator demanded that

a popular highlights show on public broadcast channel, ARD, was moved to a later time slot. Clubs, realizing the

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 14

importance of sizable FTA audiences to their sponsors, opted to support the lower, but less restrictive, Unity

Media bid. Premiere’s share price fell by around 45% when the news was announced, highlighting the huge

importance of the rights to its business. The loss of the highly prized football rights could also have a major impact

on its subscriber base – while Premiere itself expects to lose about 10% of its 3.4 million subscribers if it is unable

to sub-license the rights from Unity, Datamonitor believes that the actual figure could be closer to 20%, such is the

importance of the rights.

In an attempt to repair the damage caused by the rights loss, Premiere has reached a deal with Deutsche

Telekom that will allow the operator’s customers to watch coverage over the Internet – Deutsche Telekom holds

the Internet rights for Bundesliga coverage. Under the terms of the deal, Bundesliga games will be available to

Premiere subscribers that have a DT broadband connection – currently estimated to be around half of the pay-TV

operator’s customer base. Although the deal will help Premiere to repair some of the damage wrought by the loss

of pay-TV football rights, Datamonitor believes that the operator will need to negotiate a deal with Unity Media in

order to regain access to matches across its cable and satellite platforms. Although not yet confirmed, Unity

Media is expected to sub-license its rights to other operators in order to recoup some of its initial investment –

whether Premiere is one of these remains to be seen.

EC decision weakens BSkyB’s hold on UK football rights

Premiere is not the only European operator to have lost control of football rights in the past year. It was confirmed

in March 2006 that English Premiership TV rights for the 2007-2010 seasons would be sold in 6 packages, with no

single broadcaster able to buy more than 5 of these. Despite the enforced loss of Sky’s exclusivity, the English

Premier League rights auction in the UK generated £1.7bn ($3.1bn), up around 65% on the previous deal. As

expected, BSkyB has retained a strong position with regard to the 2007-2010 rights, winning 4 of the 6 rights

packages on offer, while Setanta has gained control of the remaining 2 packages. Overall, Sky has won the rights

to 92 matches (including the elite Sunday afternoon games) at a cost of around £4.8 million ($8.6m) per match,

while Setanta took the remaining 46 at an average cost of £2.8 million ($5m).

For the first time, the rights are platform neutral, meaning that the rights winners will be able to simulcast

programming via non-TV channels, including broadband – Datamonitor expects Sky in particular to exploit this

opportunity over the course of the next few years in order to extend consumer reach. Setanta has already

confirmed that it is planning to screen live matches over broadband and across all digital TV platforms (including

DTT); should Premier League coverage be made available through Freeview via the Top Up TV pay-TV services,

it would provide a major boost to the DTT platform, which is already in around c7 million UK homes. Rumors also

persist that BSkyB will offer some coverage on Top Up TV, possibly via a monthly subscription – this would be a

significant departure from the operator’s existing strategy, whereby it sells access to Premier League matches as

part of a package of channels through cable and satellite.

IPTV operators start to compete for football rights

Although satellite (and to an extent, cable) operators have historically been the primary acquirers of football rights,

a number of IPTV providers have taken an aggressive approach to their content strategies to win exclusive rights.

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 15

Belgacom has acquired the rights to the Belgian football league and Dutch telco, Versatel, has acquired the rights

to the Dutch football league. Both operators currently lack the necessary scale to make the deals profitable

without sub-licensing the rights to other operators (Belgacom provides some matches to satellite provider Canal

Digitaal, Versatel to a number of cable operators) – however, Datamonitor expects the situation to change as the

operators’ IPTV subscriber bases increase to the point where they can retain exclusivity in a cost-effective

manner. BT’s acquisition of ‘near live’ Premier League rights in the UK for its forthcoming VOD service further

underlines the high value of football rights across the pay-TV sector.

IPTV set to shake up the digital TV competitive environment

Increasing competition drives need for service expansion

IPTV remains one of the biggest subjects of discussion and speculation across the digital television industry

today. The emergence of a fourth platform is making executives across the cable, satellite and terrestrial sectors

uneasy as they prepare to meet the challenge of increased competition from telecoms providers. Telecoms

operators across the US and Europe are coming under increasing pressure from cable operators with regard to

the provision of triple play services, and in many cases are reacting by launching triple play services by adding

IPTV to the plethora of services already being delivered over their broadband networks.

European operators begin to embrace IPTV

Initial IPTV development has been faster in Europe than the US, with the majority of early deployments over

existing DSL broadband connections and product offerings relatively simple. Of the incumbent telecoms operators

in Europe, Belgacom, France Telecom, KPN, Austria Telecom, Telecom Italia, Telia, Telefonica and TDC have all

launched IPTV services to date, with BT planning to roll out its combined DTT/VOD service in the Autumn of

2006. Deutsche Telekom has recently announced that it will launch an IPTV service over VDSL in 2007, while

Swisscom’s IPTV plans have been delayed as a result of technical issues. Both France Telecom and Telefónica

have already established a strong foothold in their domestic markets, while other major services providers are

stepping up their efforts in an attempt to compete with their cable and satellite rivals, as outlined below.

• France Telecom’s IPTV service attracted 200,000 subscribers by the end of 2005, representing strong

progress over the course of the year. The service has now been extended – from February, customers

have been able to opt for the ‘Le Bouquet’ package, which provides access to over 200 channels and

the potential to access premium content from TPS and Canal+. Competition in the French IPTV market

is strong, with Neuf Cegetel, Free and Telecom Italia France all offering services, in some cases for

free when consumers subscribe to broadband services – the combination of low price points and pay-

TV operators’ willingness to provide content for the services have acted to drive uptake.

• Telefónica had attracted around 200,000 subscribers to its Imagenio service by the end of 2005. In

December 2005, the first true rival to Imagenio in Spain was launched by Superbanda, while Jazztel is

also set to enter into direct competition with the incumbent telco when it launches its IPTV service

nationally.

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 16

• Telecom Italia launched its Alice Home TV service in December 2005. Initially available in 4 cities to

around 2 million households, coverage was extended to 4 million homes by the end of January and will

be further increased to 8 million by the end of 2006. The operator plans to invest around €2.1 billion

($2.6bn) on broadband-related deployment and services over the next two years, with €350 million

($440m) of this spent on developing IPTV services. However, with FastWeb already well established in

what is arguably Europe’s most developed IPTV market, combined with satellite’s current pay-TV

dominance and the strong growth of DTT services, Datamonitor believes that Telecom Italia may

struggle to drive significant growth in the short-term. In order to succeed, the operator will need to

stress the convenience and cost advantages of opting for a triple play offering, an area in which

FastWeb is currently the only major competitor.

• Belgium – Belgacom launched its IPTV services in June 2005, beating cable rival Telenet to the punch

with regard to launching a digital TV service. Currently, around 62% of Belgian households are able to

receive TV services, with the combination of ADSL2+ and VDSL deployments likely to result in an

increase to nearer 80% by the end of 2006. By securing exclusive football rights in Belgium for both

domestic games and Italian Serie A matches, Belgacom has gained a strong position – the fact that the

operator does not force consumers to subscribe to a raft of other channels before being able to access

the football coverage is also seen as a positive move which is a marked departure from the strategy of

cable operators. Belgacom extended its VOD offering in December through a partnership with

DreamWorks which provides a catalog of around 300 movies.

• KPN – Dutch service provider KPN launched its IPTV service in May 2006 under the brand name

‘Mine’. At launch, subscribers will have access to 48 TV and 60 radio channels, with an expansion to 60

TV channels planned over the following months. The service also includes a VOD movie service

offering 300 titles, with KPN partnering with major content providers such as Warner Bros and

Blockbuster to provide the service. KPN expects to sign up around 10,000 subscribers by October, but

will have to compete with rival IPTV provider Versatel, which has acquired rights to the Dutch football

league.

• Deutsche Telekom has partnered with Microsoft in preparation for a planned launch of IPTV services

from mid-summer onwards; Initially, the service will only be provided in 10 German cities. For Microsoft,

it is the biggest IPTV deal in Europe and its second biggest global deal (the largest being with AT&T in

the US). The transition to digital services in Germany has been hindered by the availability of a large

number of popular channels which are provided for free, limited the appeal of paid services. German

IPTV providers have the opportunity to provide a new range of services (interactivity and VOD, for

example) that will convince consumers to make the switch from basic cable services.

• Telekom Austria, which had approximately 575k broadband subs at the end of 2005, launched Aon

Digital TV in January 2006 in Vienna – previously, it had offered PC-based video services via its Aon

TV service, but the latest offering extends connectivity to TVs. Aon Digital TV offers 50 channels and

VOD content.

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 17

• BT will launch its BT Vision service in the autumn, the first offering to combine IP-based VOD content

and free-to-air DTT through a single STB. Datamonitor believes that this will prove to be an attractive

combination, providing consumers with the ability to buy premium content without paying a subscription

fee for access to more mainstream broadcast programming. In preparation for the launch, BT has

boosted its broadband network capacity, and has agreed content deals with a number of major

providers including DreamWorks, Paramount, Warner Music and the FA Premier League (it has won

the ‘near live’ rights to top-flight football coverage from the 2007 season).

Despite strong support from European service providers, Datamonitor believes that IPTV will remain a relatively

niche proposition across much of Europe, with the platform facing stiff competition from existing cable and satellite

services and, increasingly, DTT – around 9.5 million IPTV subscribers are expected across the region by the end

of 2010, with fewer than 9% of digital households connecting via this means.

DTT – IPTV’s friend or foe?

Although DTT is expected to be the largest digital platform in the Europe by the end of 2010 with over 37 million

households connected, the core focus of the platform is likely to remain on free-to-air services – although pay-TV

services are available (TopUp TV in the UK, for example), the vast majority of households will not pay a monthly

subscription fee for DTT. As a result, Datamonitor suggests that the success of DTT can be leveraged by IPTV

operator in some markets.

In countries where DTT is growing rapidly, telcos have sought to partner in order to gain access to a broad range

of popular content. In France, for example, the TNT DTT channels are available via France Telecom’s IPTV

service, while Telefonica provides DTT channels via its hybrid IPTV set-top boxes. BT in the UK is the latest major

service provider to announce a tie-in with DTT – its IPTV strategy will be based around VOD content, with live

broadcast content delivered via Freeview. In other markets such as Sweden and Italy, Datamonitor believes that

DTT services are likely to provide higher levels of competition to IPTV services – in the case of Sweden, the pay-

TV DTT service is in direct competition with both cable and IPTV services, while Italian DTT benefits from access

to top-flight football coverage and a €70 ($88) subsidy per household for STB acquisition.

US market starting to gain traction

In the US, the IPTV market is starting to gather momentum and is now starting to develop beyond the rural

telephone companies who have been delivering TV content over DSL infrastructure for several years – today,

more than 200 US and Canadian telephone companies offer TV-based services over broadband IP networks. All

of the major US carriers have announced their IPTV development roadmaps and are currently undertaking either

limited market tests or technical trials, as outlined below.

• Verizon launched its FiOS TV service in September 2005 – the service is now available in 5 states

including Texas and Florida. The service currently offers 350 broadcast channels (including 20-22 HD

channels) and VOD. The service provider operators an unusual hybrid network that employs IP delivery

for VOD but QAM modulated signals (similar to cable networks) for broadcast TV – the choice of these

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 18

technologies was based on the telco’s desire to use proven technologies, rather than wait for IPTV-

specific technologies to reach maturity. Verizon’s fiber-to-the-home network is capable of delivering up

to 100Mbps to each home, meaning there is no need for advanced coding, even with HD.

• AT&T’s ‘Project Lightspeed’ aims to provide consumers with around 25Mbps capacity through which

television, telephony, and Internet access services will be offered. The project’s goal is to reach 18

million homes in 13 states by the first half of 2008. Unlike Verizon, AT&T uses fiber-to-the-node to feed

ADSL2+ copper networks in last mile. AT&T is in the process of introducing its U-Verse TV service

across this network.

• BellSouth’s IPTV plans are similar in nature to those of AT&T – the carrier intends to provide

consumers with at least 12Mbps of capacity via fiber to the node, fiber to the curb and DSL. BellSouth

doesn’t intend to deploy fiber all the way to the consumers’ premises, making the deployments less

capital intensive than Verizon’s offering. With AT&T set to acquire BellSouth, the latter’s IPTV plans

may fall by the wayside, although Datamonitor expects the deal to help drive developments of TV-

based services in the longer term.

Verizon had connected around 3 million homes with fiber at the end of 2005 and expects to add around 3 million

per year. Datamonitor believes that its strategy is a safe, but ultimately expensive and time consuming one.

Furthermore, the IP-centric plans of AT&T and BellSouth – which employ switched video technology – are likely to

prove more flexible in the long term, allowing an almost unlimited number of channels to be offered and potentially

enabling connectivity with other devices. Problems could arise with this infrastructure, however, when considering

the future need to deliver multiple HD feeds to a household – subscribers wanting to connect either a second TV

set or an HD PVR (which would require two concurrent HD feeds) could easily use up available bandwidth, forcing

the operators to deploy advanced compression technologies to reclaim capacity.

Datamonitor expects the US to be a more difficult market than Europe for IPTV, with high levels of pay-TV

penetration and expected strong price competition from established cable and satellite providers. IPTV operators

will need to pay particular attention to ensuring that their services are not only price competitive, but also deliver

services that are at least as good as existing offerings in terms of reliability, customer services and functionality.

Early suggestions indicate that the major US telcos are seeking to provide similar products to those already

available via cable and satellite – in such an intensely competitive industry, Datamonitor does not expect such

offerings to be hugely successful.

Europe set to maintain its early lead over the US

As illustrated in the following figure, the number of IPTV households is expected to grow rapidly in both Europe

and the US, with a combined 15 million subscribers expected across the two regions by the end of 2010. By the

end of the forecast period, IPTV will account for approximately 8.6% of digital households in Europe and 7.5% in

the US. Datamonitor expects IPTV to make further inroads into the digital TV sector beyond 2010, although

success will depend heavily on content availability and pricing strategies relative to established platforms.

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 19

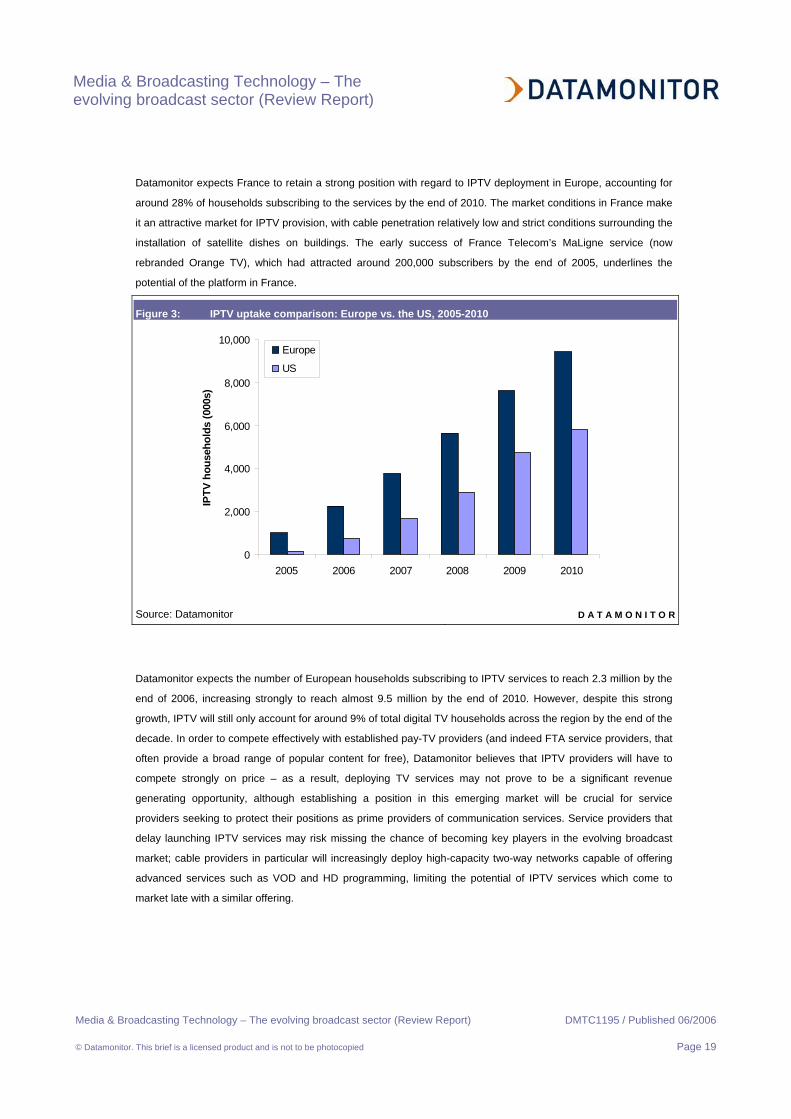

Datamonitor expects France to retain a strong position with regard to IPTV deployment in Europe, accounting for

around 28% of households subscribing to the services by the end of 2010. The market conditions in France make

it an attractive market for IPTV provision, with cable penetration relatively low and strict conditions surrounding the

installation of satellite dishes on buildings. The early success of France Telecom’s MaLigne service (now

rebranded Orange TV), which had attracted around 200,000 subscribers by the end of 2005, underlines the

potential of the platform in France.

Figure 3: IPTV uptake comparison: Europe vs. the US, 2005-2010

0

2,000

4,000

6,000

8,000

10,000

2005 2006 2007 2008 2009 2010

IPTV

hou

seho

lds

(000

s)

Europe

US

Source: Datamonitor D A T A M O N I T O R

Datamonitor expects the number of European households subscribing to IPTV services to reach 2.3 million by the

end of 2006, increasing strongly to reach almost 9.5 million by the end of 2010. However, despite this strong

growth, IPTV will still only account for around 9% of total digital TV households across the region by the end of the

decade. In order to compete effectively with established pay-TV providers (and indeed FTA service providers, that

often provide a broad range of popular content for free), Datamonitor believes that IPTV providers will have to

compete strongly on price – as a result, deploying TV services may not prove to be a significant revenue

generating opportunity, although establishing a position in this emerging market will be crucial for service

providers seeking to protect their positions as prime providers of communication services. Service providers that

delay launching IPTV services may risk missing the chance of becoming key players in the evolving broadcast

market; cable providers in particular will increasingly deploy high-capacity two-way networks capable of offering

advanced services such as VOD and HD programming, limiting the potential of IPTV services which come to

market late with a similar offering.

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 20

Can telcos succeed in the pay-TV environment?

The key challenge for telecoms operators seeking to deploy IPTV services is to take market share from

established cable and satellite providers who have already gained a strong foothold in the pay-TV sector. In this

regard, Datamonitor has identified two main barriers for IPTV providers, as outlined below.

• Industry knowledge – the TV market is a new business area for most telecoms operators, requiring

strong partnerships with content providers to be developed. In order to combat this, a variety of

strategies have been employed by operators; while Belgacom has hired media specialists (its CEO is

the former head of RTL Group), Swisscom has acquired Cinetrade (a pay-TV and cinema group to

develop its media know-how. Datamonitor expects industry knowledge issues to become less apparent

over the coming years as operators ramp up their internal resources in this regard, while content will be

made widely available by content providers as the IPTV market develops.

• Technical issues – in order to compete effectively with digital cable and satellite services, IPTV

offerings need to provide the high picture quality that consumers demand. Minor issues currently being

experienced with some operators are likely to be quickly resolved, while Datamonitor also expects

installation times to fall as operators become more used to physical deployment and overcome initial

obstacles. Another current issue is the fact that it is currently difficult to service multiple-TV households

– indeed, network capacity constraints often prevent operators from providing IPTV services to more

than one TV set. However, Datamonitor expects such issues to be resolved as higher capacity

networks are deployed and new compression technologies are implemented.

Datamonitor sees IPTV primarily as a defensive move by the major service providers rolling out services. While

such services have the potential to generate additional revenues for operators, the key driver of deployment – in

the short term at least – will be improving customer loyalty and adding greater depth to the services provided to

consumers over ADSL networks. In some cases, IPTV may prove to be a financial loss leader, albeit an essential

one if telcos are to retain a significant position with regard to provision of consumer communication and

entertainment services. In the longer term, service providers will need to invest heavily on their network

infrastructure – Datamonitor believes that upgrading to either ADSL2+ or VDSL will become essential if a broad

range of services are to be deployed. When the cost of content acquisition, CPE subsidization and marketing are

factored in, it is difficult to see how the majority of operators will generate significant profit margins from IPTV in

the short term – especially considering the need to be competitive on a pricing basis to generate interest among

consumers.

Consolidation continues to have an impact on market dynamics

Cable consolidation boosts market potential

Consolidation of the European cable industry has continued over the past year, with resultant economies of scale

likely to enable operators to provide increased competition to both satellite operators (in terms of TV-based

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 21

services) and telecoms operators (in terms of both telephony and data services). Some of the more recent

developments in this regard are outlined below.

• French cable consolidation – the French cable market has undergone considerable consolidation

over the last two years. Now, pending terms and regulatory approval, the French network will come

under the ownership of a single company. In March, Liberty Global signed a letter of intent to sell its

cable business to Altice and Cinven. UPC France, which acquired its competitor Noos in 2004, was

valued at €1.25 billion ($1.55bn) – considerably higher than its cash flow. Shortly after the acquisition of

Noos by UPC France, Altice and Cinven acquired the cable businesses of France Telecom (FT Cable)

and Canal+ (Numéricable). Upon completion of the acquisition, Altice and Cinven hold a dominant

position in the French cable network.

• Unity in the German cable market – there was much needed consolidation of the German cable

market in 2005, with first iesy and ish merging under the Unity Media brand, and the combined operator

then acquiring level 4 operator Tele Columbus. The deals mark the first major step in the consolidation

of level 3 and 4 networks in Germany, creating a combined company that will directly provide around

4.5 million households with TV services. Datamonitor believes that such activity is crucial if the German

cable market is to generate the economies of scale needed to provide impetus for digital development.

• ONO acquires Auna – ONO, in partnership with a consortium of private equity partners, acquired the

cable assets of Auna in August 2005 for €2.5 billion ($3.1bn). The two companies had been closing in

on a merger for over a year, with ONO rebuffing a €2.4 billion ($3bn) offer from Auna in November

2004 before tables were ultimately turned with this deal. The merger of the companies’ cable

operations extends combined reach to 6 million Spanish homes, or around 40% of total households.

However, with strong competition from both Digital+ and Telefónica, Datamonitor believes that the

operators will need to compete strongly on price in order to gain market share.

• NTL and Telewest merge at last – the UK pay-TV market has also seen consolidation activity in the

last year with the two leading cable operators, NTL and Telewest, finally agreeing to merge in August

2005. NTL purchased Telewest in a deal worth around £3.4 billion ($6.1bn), creating a company that

has around 5 million subscribers. The merger was essential for the prospects of the UK cable sector;

without the economies of scale created by this move, the companies would doubtless have continued

to struggle to compete with Sky (on a pay-TV basis) and BT (on a telephony and Internet basis).

• Liberty Global now has operations in Switzerland (following it acquisition of Cablecom), the

Netherlands and Belgium. Although the group has recently sold its interests in UPC France and UPC

Sweden, it remains an important player across the European cable sector. Datamonitor expects Liberty

Global to focus its efforts on its Eastern European investments, while its French exit is in line with its

gradual withdrawal from ‘sub-scale’ markets where there are limited opportunities for significant growth.

UPC Sweden was sold to Providence Equity Partners and Carlyle Group, which has also acquired

ComHem to create a strong position in the Swedish market.

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 22

• Adelphia still awaiting sale to be finalized – midway through 2002, Adelphia, a cable operator with

approximately 5 million US subscribers filed for Chapter 11 bankruptcy protection. A significant level of

debt forced the company to undertake a significant restructuring process, including delisting from the

NASDAQ. As a result, Time Warner cable and Comcast agreed to purchase the majority of Adelphia’s

assets in 2005 to the value of $17.6bn in cash and stock. While the deal has not yet been finalized,

Adelphia has asked the bankruptcy court to expedite matters, with completion by the end of July 2006

now widely anticipated.

Satellite consolidation expected in France

There has been significant consolidation activity in the French cable market, the French satellite market is also

seeing some of the action, with Canal+ and TPS expected to merge their operations in 2006. The merger of

Group Canal+ and TPS in France would be controlled by Vivendi Universal (85% share), TF1 (9.9%) and M6

(5.1%). At this stage, only a draft commercial agreement has been signed by the relevant parties – any

subsequent approval of that draft would still leave the merger subject to approval from the French competition

authorities, the French broadcasting authority and relevant unions. However, with similar moves in the Italian,

Spanish and UK satellite markets proving successful in terms of driving digital adoption, Datamonitor expects the

potential merger to occur with few problems. Pooling resources would allow the satellite operators to combat the

growing threat from telco- and Internet-based TV services, with the a merger helping to prevent the costly content

wars that have impacted upon profitability over recent years, while providing greater negotiating power with

content owners and offering improved economies of scale.

In the US, DirecTV is still believed to be interested in buying rival US satellite operator EchoStar, although

regulators seem unlikely to allow such a deal to take place in the short term at least. The two companies tried to

merge in 2002, but the deal was blocked by the FCC, who felt that it would be anti-competitive – with little having

changed in the past 4 years with regard to market structure, Datamonitor believes that similar restrictions will

remain in place. A merger would enable the satellite operators to compete more effectively with cable operators,

and could have a major impact on the dynamics of the US digital TV market – successful satellite mergers across

a number of European markets (including Italy, Spain and the UK) have highlighted the benefits of consolidation

with regard to improving economies of scale and increasing rates of uptake.

Pay-TV operators are seeking to extend the scope of their offerings via acquisitions

While a number of deals have acted to increased levels of consolidation across the pay-TV sector, several

acquisitions aimed at allowing operators to develop their strategies in what are currently non-core areas have

taken place over the course of the past 12 months. Developments in the UK in particular highlight the fact that

pay-TV operators are seeking to extend the scope of their offerings to offer the potential to launch new services

and gain a greater share of consumer spending with regard to communication and entertainment services.

• NTL acquires Virgin Mobile – in early 2006, NTL agreed to acquire MVNO Virgin Mobile for £962

million ($1.7bn), creating the first quad-play offering in the UK. Virgin TV – as the combined company is

expected to be rebranded later in the year – will offer consumers cable TV, broadband and both fixed-

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 23

line and mobile telephony services. The strategy of offering a bundled solution of this type is not a new

one, nor is it limited to the UK – mobile operator Sprint, for example, provides mobile phone services to

customers of the main cable operators in the US via a series of partnerships. However, this acquisition

is a notable development due to the level of investment undertaken by NTL – other deals have been on

a partnership basis rather than involving an actual purchase.

• BSkyB branches into broadband with Easynet purchase – in late 2005, BSkyB acquired UK

broadband operator Easynet for £211 million ($380m) in a move that is the first step towards the

company’s goal of deploying a full triple play of entertainment and communications services. Easynet

has made more progress than most of its rivals in terms of exploiting local loop unbundling

opportunities, with its equipment now residing within around 250 BT exchanges. Sky will be able to

leverage its considerable content assets to offer IPTV and VOD services to extend coverage to those

households that cannot access satellite service, notably those in multi-tenant units and those without

necessary line-of-site – having access to Easynet’s expanding network will allow Sky to offer these

services without having to rely on third party network providers. BSkyB is already offering its

subscribers access to a PC-based VOD offering, although this is only likely to be a short-term measure

in preparation for a true VOD service.

Datamonitor believes that more deals of this type will emerge over the coming 2-3 years as pay-TV operators

seek to extend their coverage and develop their distribution strategies. Offering triple- or quad-play services will

become increasingly crucial as competition for subscribers continues to grow – the ability to offer bundled

services, whereby consumers are offered discounted rates for taking multiple services, is likely to be particularly

crucial. Datamonitor believes that US satellite operators will increasingly seek to offer triple-play services,

although the local loop unbundling regulations seen across Europe are not evident in the US, making it

problematic for DirecTV and EchoStar to exploit DSL-related opportunities without partnering with existing

providers. Industry speculation suggests that DirecTV is looking at WiMAX broadband wireless technology as a

potential way to circumvent this obstacle, while EchoStar is considering a range of options including two-way high-

speed satellite and developing marketing relationships with telcos. Satellite operators in particular are also

expected to follow BSkyB’s lead and evolve their strategies in order to offer a more comprehensive range of

services to meet the changing demands of consumers.

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 24

TECHNOLOGY DEVELOPMENTS IN THE DIGITAL TV SECTOR (TECHNOLOGY FOCUS)

Summary

Competition across the broadcast sector is now greater than ever before, prompting operators to develop their

offerings to both attract and retain subscribers. Operators are increasingly embracing new technologies to achieve

this goal – Datamonitor expects 2006 to be a watershed year in Europe for new services such as high-definition

TV, IPTV and mobile TV, while uptake of PVR technology is set to increase rapidly over the next five years. Key

findings of this brief include:

• high definition expected to become a major service differentiator;

• increasing penetration of PVRs could disrupt existing broadcast business models;

• mobile TV offers new opportunities for broadcasters.

High definition expected to become a major service differentiator

High-definition TV (HDTV) offers a significant improvement in quality of broadcast TV content – in many respects

it is the first step-change in picture quality since the advent of color TV. While HDTV broadcasting has been

available in the US since 1998, European operators are only just starting to roll out commercial services.

Datamonitor believes that HD will become an increasingly crucial component of pay-TV operators’ digital

strategies, with the availability and range of HD programming providing an important differentiator over the next

few years as competition for new subscribers increases.

The US leads the way with regard to high definition

In the US, sales of HD TV sets are around three years ahead of the European market, with approaching 20% of

US households believed to own an HD-capable TV by the end of 2005 – 87% of US households are already

passed by at least one cable operator offering HD services. In contrast, there were only around 2 million ‘HD

ready’ (i.e. with an HD-capable TV) households in Europe at the end of 2005, although the vast majority of these

sets not connected to HD programming due to very limited rollout of service. This, coupled with the fact that the

difference in quality between standard definition and HD programming is not as noticeable in Europe as it is in the

US due to differences between the broadcast technologies used, is likely to result in a continued gap between

development in the two regions. In addition, the fact that average screen sizes are larger in the US means that

demand for HD services are likely to be greater, with picture quality improvements more noticeable on bigger

screens.

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 25

Satellite operators playing catch-up in the US

Over the course of the past two years, both DirecTV and EchoStar have been investing heavily in preparation for

expansion of their HD services. Overall, satellite continues to be at a disadvantage over cable for HD as both

operators build out infrastructure and await a greater supply of MPEG-4 STBs. To date, the satellite operators

have matched cable with regard to national HD services, but have lagged behind in terms of local programming

due to capacity constraints. Datamonitor expects the local HD advantage that cable currently holds to be erased

as both satellite operators deploy true local HD channels using MPEG-4 compression and increasing capacity

coming online from recent satellite deployments. Approximately 50% of satellite households are expected to be

covered with local HD services by the end of 2006; at CES 2006, EchoStar announced that it would offer local HD

programming to 50 markets in 2006, while DirecTV has similar expectations.

Pricing and programming selection will become increasingly important

Pricing will remain an important factor in the US HD market. At present, DirecTV charges $399.99 for an HD-DVR

devices, plus $9.99 per month for HD channel access, while many cable operators currently offer devices for no

upfront fee and provide a basic level of channels for no fee, highlighting the current advantage that cable currently

holds in this regard. However, in the long term, it will be the quality and quantity of HD programming available that

will differentiate services – Datamonitor believes that satellite operators hold the long-term advantage here, with

DirecTV expecting to be providing 150 national HD channels by 2007 – in order for cable operators to match this,

they are likely to have to reclaim analog spectrum in order to provide sufficient capacity, which would involve

increased capital spending and a major push towards digital migration across their subscriber bases. It seems

likely that both DirecTV and EchoStar will have a significant lead over cable operators once upgrades have been

undertaken, with increased capacity enabling the rollout of a far broader portfolio of HD programming than is

currently available.

World Cup boost for European HD market

European operators are well behind their US counterparts with regard to HD development – Euro 1080 was the

first operator to broadcast in high definition in Europe, but its rather limited content portfolio has restricted

consumer demand. However, more mainstream pay-TV operators are now starting to roll out services – both

Telewest and Premiere launched initial services in late 2005, while BSkyB and Sky Italia are now providing

services. A number of European operators and broadcasters have launched HD services in time for the football

World Cup – Premiere, TPS, Sky Italia, Canal Digital and the BBC all broadcast games in HD. With the European

pay-TV market beginning to reach maturity, operators have high hopes for HD as a way to increase ARPU,

reduce churn and increase subscriber numbers – indeed, BSkyB sees HD as a key element of its mission to reach

10 million subscribers by 2010.

The 2006 football World Cup has acted as a catalyst for the first meaningful stage of HD development in Europe –

Datamonitor expects steady adoption over the next two years, with only early adopters willing to invest in the

devices and subscriptions needed to receive HD content. The price of flat-screen HDTV sets is set to fall

significantly over the next few years, providing incentive for households to make the transition – current average

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 26

HDTV prices of around $1,800 in Europe are too high to prompt mass-market development, with this price

probably needing to drop by almost 50% before strong market growth can be expected.

European satellite operators pushing ahead with HD

As expected, early developments in the European HD market have been primarily on satellite platforms – satellite

operators have historically been the first to offer new technologies to their subscribers. Although the cable sector

has often lagged behind satellite with regard to technology development, some cable operators have kept pace in

terms of deployment of HD services, notably Telewest in the UK and UPC in the Netherlands. Some of the main

HD service launches to date are highlighted below.

• Premiere was the first major European pay-TV operator to launch a commercial HD service – the

German satellite operator launched its HD service in November 2005, featuring three specialist

channels for sport, film and documentary programming. However, a shortage of necessary STBs and

limited sales of HD-capable screens has resulted in relatively limited uptake of the service to date.

• Telewest was the first UK operator to launch a nationwide HD service in the UK. The service, which is

available to over 4.5 million homes and costs an extra £10 ($18) per month, requires subscribers to

upgrade to the new TVDrive PVR device, which incorporates a 160GB hard drive. While rival pay-TV

operator Sky offers HD services via a number of dedicated channels, Telewest’s HD content is

currently only available via its on-demand service, Teleport. BSkyB launched its HD service in May –

subscribers to the service will need to pay £299 ($540) for the Sky HD set-top box and an additional

£10 ($18) per month on top of their existing subscription fee.

• TPS’s HD service, jointly promoted by the operator and Sony, was originally planned for 2005, but was

delayed due to an MPEG-4 chip shortage – 10,000 pre-registered subscribers finally received their

HDTV decoders in March. The HD STB costs subscribers an additional €5 ($6) per month compared to

the standard TPS decoder – Datamonitor believes that this is a relatively small premium to pay for HD

services, and should, therefore, help to drive strong interest across TPS’s subscriber base. Rival

French satellite provider, CanalSat, rolled out HD service in time for the World Cup, with a full bouquet

of HD channels expected over the coming months.

• UPC Netherlands have rolled out an HD service in time for the World Cup in partnerships with STB

manufacturer Philips. For a one-off activation fee of €49.99 ($63), UPC’s digital TV subscribers receive

a Philips HD STB and access to two HD channels (one movie channel, one sport). The two companies

are jointly marketing the service alongside Philips’ range of HD-ready flat screen TVs.

• Sky Italia launched its HD service on May 17th with coverage of the European Champions League

football final. Following its coverage of the World Cup, Sky Italia will launch its HD channel bouquet,

which will cost subscribers an extra €7 ($9) per month.

European operators have struggled to date to obtain sufficient numbers of HD-capable STBs – delays relating to a

shortage of the necessary MPEG-4 chipsets have restricted availability, with Sky in the UK believed to be

particularly affected by the problem. Sky was forced to delay the installation of HD in around 17,000 homes

Media & Broadcasting Technology – The evolving broadcast sector (Review Report)

Media & Broadcasting Technology – The evolving broadcast sector (Review Report) DMTC1195 / Published 06/2006

© Datamonitor. This brief is a licensed product and is not to be photocopied Page 27

following early delivery issues with STBs from partner Thomson. The operator has announced that around 40,000

consumers signed up for the service in the first three weeks after launch, although admitted that some of these

would not have the necessary equipment installed prior to the start of the World Cup – a major reason why many

subscribers would have made the investment in the first place. Hence, although the World Cup could have

provided a perfect catalyst for HD development in Europe, the opportunity is likely to be somewhat missed –

although the long term future of HD in Europe is unlikely to be unduly affected, current supply issues could

certainly act to restrict uptake in 2006.

HD services unlikely via DTT in the short term

Although HD services are unlikely to emerge on DTT platforms in the short term due to a lack of available

spectrum prior to analog switch-off, a number of trials are ongoing across Europe to assess the viability of such

services. In the UK, major broadcasters (including the BBC, ITV, Channel 4 and Channel 5) are undertaking a six-

month DTT HD trial, using local frequencies to showcase a selection of HD programming including World Cup

coverage. Trials are also anticipated in France following regulatory approval for a 9-month test phase in a number

of key cities. Once spectrum is available, Datamonitor expects DTT to rapidly become a key platform for HD

services, with the FTA focus of digital terrestrial services in most markets helping to establish HD as a

mainstream, rather than pay-TV, service.

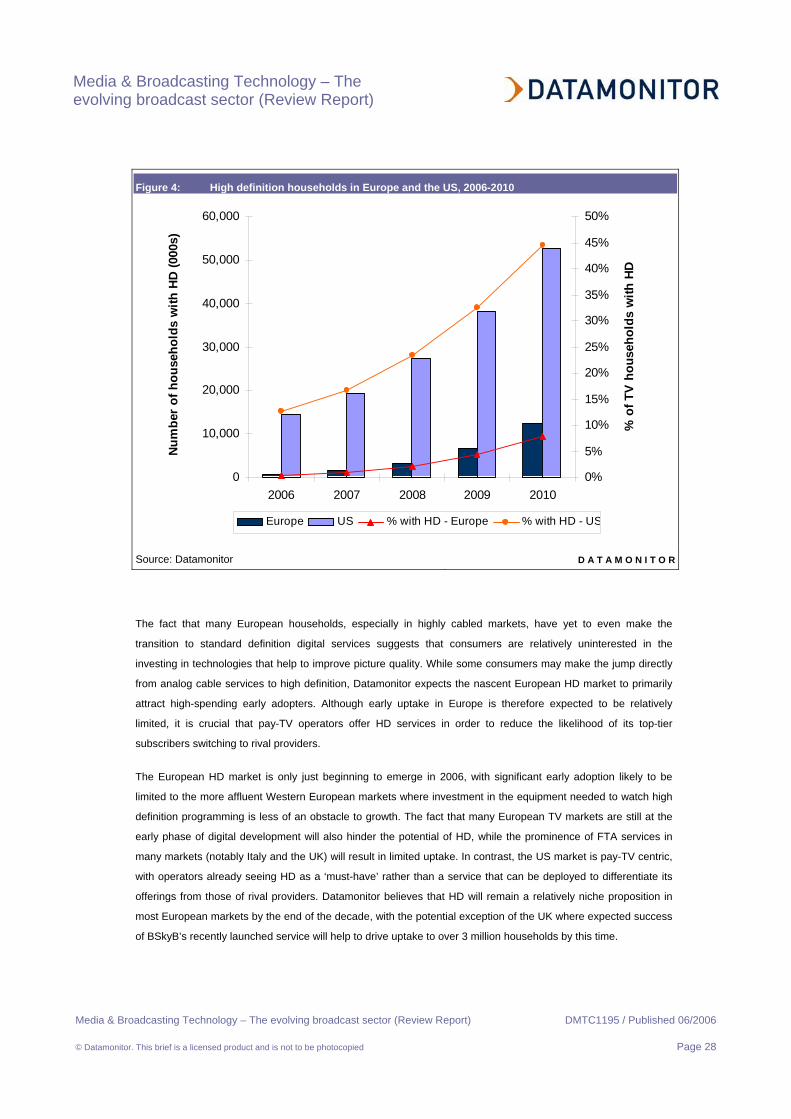

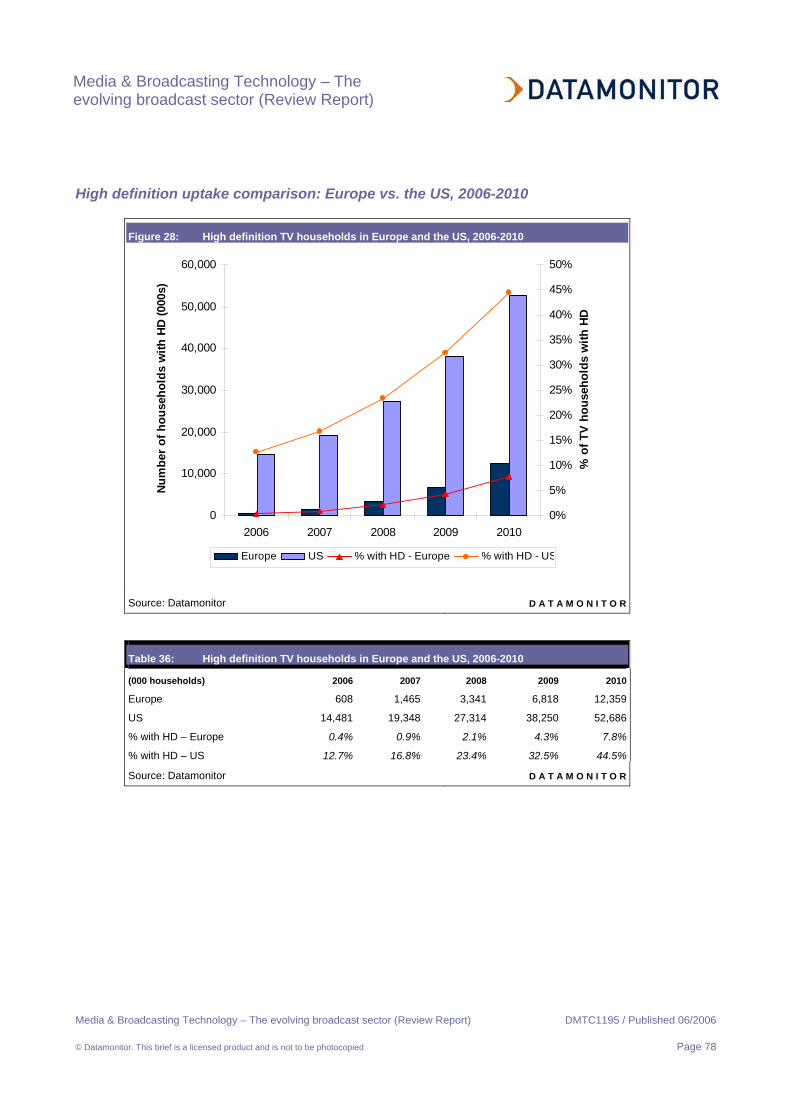

The US will retain its early HD lead over Europe

As shown in the figure below, Datamonitor expects the US to retain its significant lead over Europe with regard to

the penetration of HD services by the end of the decade. By the end of 2010, over 50 million US households will

be viewing HD programming (i.e. they will have invested in an HD-capable television and the necessary STB and

subscription needed to receive HD), representing almost 45% of all TV households across the country. In contrast

only 12 million (or c8% of TV households) will have made the transition by this time.