the experience of development banks - inct/ppedinctpped.ie.ufrj.br/spiderweb/dymsk_4/4-9s ferraz...

TRANSCRIPT

João Carlos Ferraz Vice President

Central Banks, Financial Systems and Economic Development

The experience of Development Banks

2012 Money and Banking Conference Buenos Aires, October 1st, 2012

Not an exception but very common institution: in countries under different regimes, at different stages of development.

BDC (2009): 235 DIs in 92 countries.

International Benchmark Study on Development Institutions. Business Development Canada, 2009

WB (2012): 90 DIs in 61 countries. By 2009, total assets of US$ 2.01 trillion; loan portfolio of US $1.59 trillion.

Global Survey of Development Banks. Policy Research Working Paper, n. 5969. Washington: World Bank, 2012.

Different types of Development Institutions: Development Banks, Specialized Agencies (Credit, Guarantee or Equity), Development Financing Institutions (usually multilateral)

Development Institutions: very common and most relevant institutions

2

OECD: institutions providing long term loans that are beyond the capacity or the willingness of others to do so.

After 2007/8, “rediscovery” of DBs: Confidence builder, long term financing, risk mitigating institution.

But not at all without controversy! For: Crowding out private industry Having discretionary power (“pick winners”) Being an ambiance conducive to cronyism

Development Banks: what they are

3

Not a homogeneous group, differing in:

Ownership structure (fully vs. partially owned by government)

Target sectors and clients (narrow vs. wide focus)

Lending models (first-tier vs. second-tier)

Credit conditions (subsidized vs. market interest rates)

Regulation and supervision (special regime vs regime applicable to all banks)

Corporate governance (independent vs. government controlled boards)

Development Banks: not one alike

4

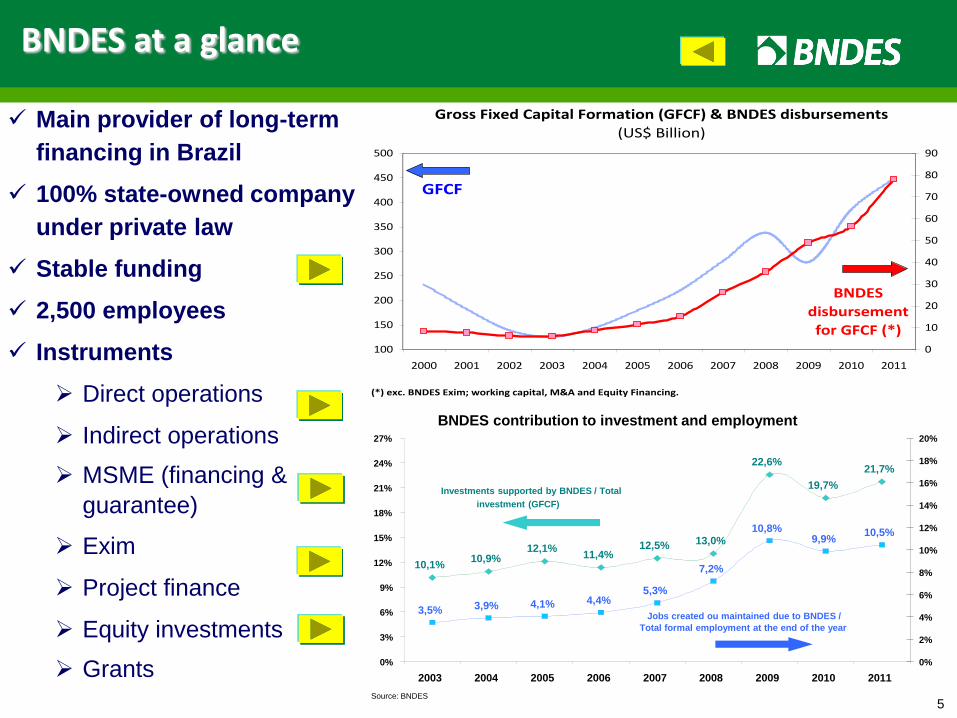

BNDES

Main provider of long-term

financing in Brazil

100% state-owned company

under private law

Stable funding

2,500 employees

Instruments

Direct operations

Indirect operations

MSME (financing &

guarantee)

Exim

Project finance

Equity investments

Grants

BNDES at a glance

Gross Fixed Capital Formation (GFCF) & BNDES disbursements

(US$ Billion)

GFCF

BNDES

disbursement

for GFCF (*)100

150

200

250

300

350

400

450

500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

0

10

20

30

40

50

60

70

80

90

(*) exc. BNDES Exim; working capital, M&A and Equity Financing.

BNDES contribution to investment and employment

10,1% 10,9%

12,1% 11,4%

12,5% 13,0%

22,6%

19,7%

21,7%

3,5% 3,9% 4,1% 4,4% 5,3%

7,2%

10,8% 9,9%

10,5%

0%

3%

6%

9%

12%

15%

18%

21%

24%

27%

2003 2004 2005 2006 2007 2008 2009 2010 2011

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Source: BNDES

Investments supported by BNDES / Total

investment (GFCF)

Jobs created ou maintained due to BNDES /

Total formal employment at the end of the year

5

6

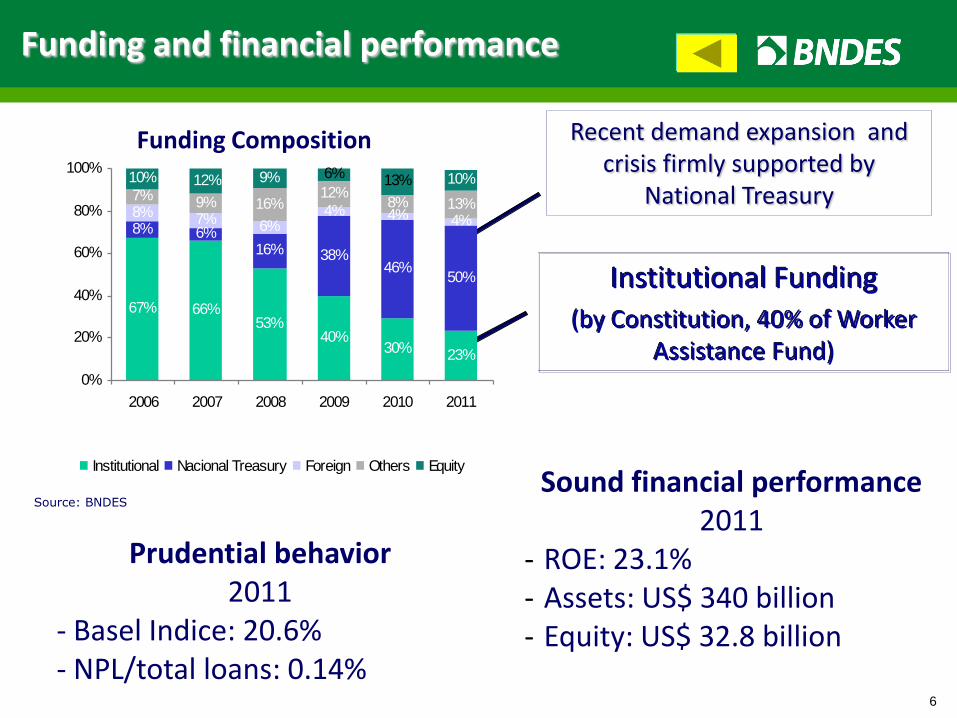

Funding Composition

Prudential behavior 2011

- Basel Indice: 20.6% - NPL/total loans: 0.14%

Source: BNDES

Funding and financial performance

Recent demand expansion and crisis firmly supported by

National Treasury

Institutional Funding

(by Constitution, 40% of Worker Assistance Fund)

Sound financial performance 2011

- ROE: 23.1% - Assets: US$ 340 billion - Equity: US$ 32.8 billion

67% 66%53%

40%30% 23%

8% 6%16% 38%

46%50%

8% 7% 6%4% 4% 4%

7% 9% 16%12%

8% 13%

10%10% 12% 9% 6% 13%

0%

20%

40%

60%

80%

100%

2006 2007 2008 2009 2010 2011

Institutional Nacional Treasury Foreign Others Equity

BNDES annual disbursements

Converted to US dollar on disbursement dates

35,1 4047,1

52,3

64,9

92,2

137,4

168,4

139,7

34

82,3

96,3

71,6

49,8

24,119,813,811,7

0

20

40

60

80

100

120

140

160

180

2003 2004 2005 2006 2007 2008 2009 2010 2011

R$ Billion US$ Billion

Growth rates receding to allow for “crowding-in” of private

industry

Source: BNDES

Share of Direct & Indirect operations (%)

Capillarity ensured by accrediting & providing funds to commercial banks. Risk of

operations is theirs

Disbursements

4434

66

57

4741

4347

4546

5846

46

565753

555442545459

53 43

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 set/11

Direct Operation Indirect Operation7

8

Financing by type of clients

Share of MSMEs in total disbursement

N° of MSMEs supported in 2011

45.83557.480

109.121

176.678

235.984

0

50.000

100.000

150.000

200.000

250.000

2007 2008 2009 2010 2011

Cartão BNDES: - 510,000 active cards - 2011: R$ 7.6 bi - 2012: R$ 11. bi (expected)

85.5% of townships with active operations with BNDES credit card for SMEs

Source: BNDES

21,5%

31,8%

35,9%

41,4%

24,0% 24,8%

15%

20%

25%

30%

35%

40%

45%

2007 2008 2009 * 2010 * 2011 up to march 2012

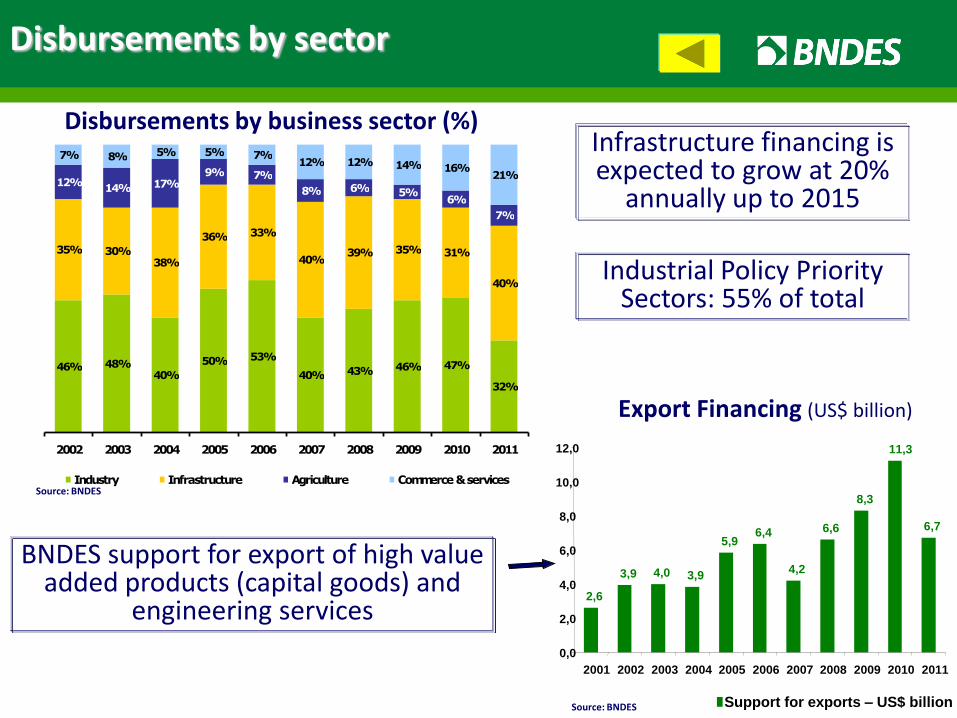

Disbursements by business sector (%)

Source: BNDES

Disbursements by sector

2,6

3,9 4,0 3,9

5,9 6,4

4,2

6,6

8,3

11,3

6,7

0,0

2,0

4,0

6,0

8,0

10,0

12,0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Support for exports – US$ billion

Export Financing (US$ billion)

BNDES support for export of high value added products (capital goods) and

engineering services

Source: BNDES

Infrastructure financing is expected to grow at 20%

annually up to 2015

Industrial Policy Priority Sectors: 55% of total

46% 48%40%

50% 53%

40% 43% 46% 47%

32%

35% 30%38%

36% 33%

40%39% 35% 31%

40%

12%14% 17%

9% 7%

8% 6% 5%6%

7%

7% 8% 5% 5% 7%12% 12% 14% 16%

21%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Industry Infrastructure Agriculture Commerce & services

BNDES as an Investment Bank

Source: BNDES.

BNDES Equity Portfolio (USD million) BNDES Portfolio in PE/VC Funds

USD million (April/2012) – USD/R$ = 1,90

Brazil´s largest investor in PE & VC

BNDES brand attracts new investors

Long experience: 35 years involved with capital markets

66,8

60,5

22,5

28,2

49,7

25,3

59,1

75,6

52,450,848,1

25,1

13,412,28,46,90,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

2005 2006 2007 2008 2009 2010 2011 mar/ 12

US$

billio

n

MARKET VALUE COST VALUE

3718671Education

Fund Focus#

Funds

#

Corps.

All

Commit.

Equity

BNDES

Commit.

Equity

Innovation 9 100 247 95

Infrastruct 7 45 2.176 448

Governance 4 20 482 84

Environment 3 5 745 205

Regional 2 10 79 14

Agribusiness 2 8 598 119

Food 1 4 49 11

Total 29 199 4.562 1.013

3718671Education

Fund Focus#

Funds

#

Corps.

All

Commit.

Equity

BNDES

Commit.

Equity

Innovation 9 100 247 95

Infrastruct 7 45 2.176 448

Governance 4 20 482 84

Environment 3 5 745 205

Regional 2 10 79 14

Agribusiness 2 8 598 119

Food 1 4 49 11

Total 29 199 4.562 1.013

10

11

Finance expansion of capacity, fill gaps, fix failures, induce externalities…

Foster an innovative, sustainable long term financing industry

Contribute to systemic stability (anti-cyclical role)

Appropriate and distribute (to society, via the State) returns of (financial) investment decisions

Scope of potential contributions to development

12

Political priority: The role/mandate of a DB must be enforced at the highest political level

Stable funding: the basic asset to finance long term

Scale and scope: A DB must have the means – resources and instruments- for accomplishing mandates.

Capacity to change: Flexible adaptation to different stages and momentum of a country development.

Competences and values: a servant of public interest; effectiveness and efficiency; team player: an instrument to build the future.

Essential assets and capabilities

Of course, these assets are not “ready made”…

Development Banks, financial industry and economic development

Each Development Bank is a singular institution. No role model exists.

As market based finance has proved to not induce sustainable development, a stronger configuration for a national finance industry is where private and public institutions co-live (But… attention!!! Time and place do matter in defining the mode of relation. Again, no role model exists…)

A Development Bank should not be the vanguard nor the rearguard but the co-guard of development

13

João Carlos Ferraz Vice President

Central Banks, Financial Systems and Economic Development

The experience of Development Banks

2012 Money and Banking Conference Buenos Aires, October 1st, 2012