the future of burley supply burley stabilization corporation daniel green burley stabilization...

TRANSCRIPT

The Future of Burley Supply

Burley Stabilization CorporationDaniel Green

Overview

Historical Trends Review

U.S. Market Review

Short-term Supply Issues

Long-term Supply Issues

25 Year Production Review

World Production Trends Filler vs. Flavor Production in Flavor Exporters

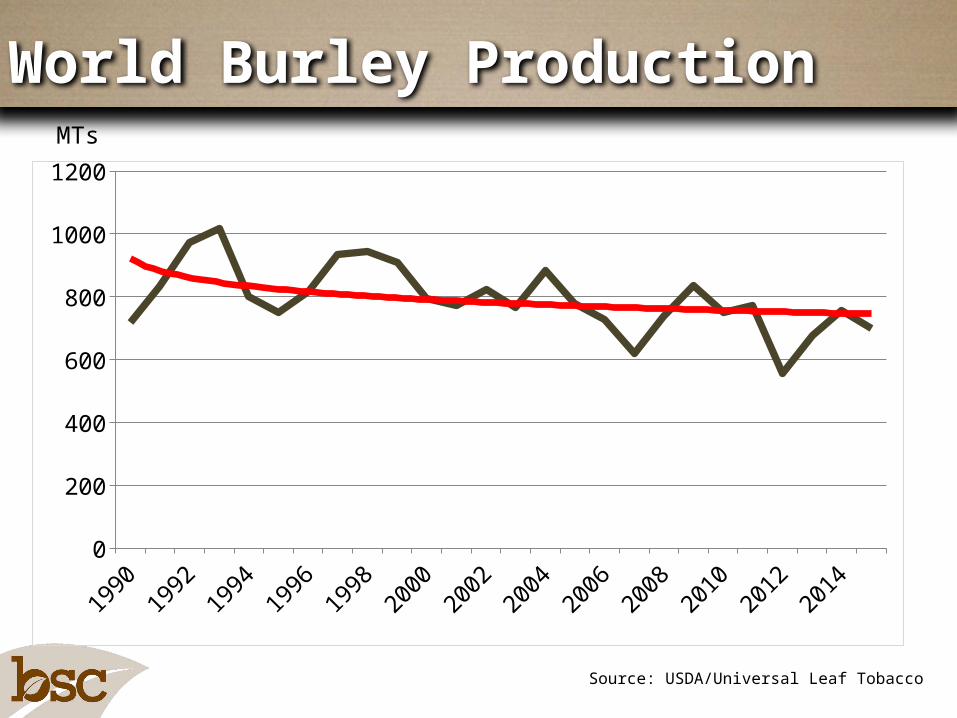

Source: USDA/Universal Leaf Tobacco

World Burley ProductionMTs

19901992

19941996

19982000

20022004

20062008

20102012

20140

200

400

600

800

1000

1200

Source: USDA/Universal Leaf Tobacco

World Burley ProductionMTs

19901992

19941996

19982000

20022004

20062008

20102012

20140

200

400

600

800

1000

1200

Flavor vs. Filler Production

19901992

19941996

19982000

20022004

20062008

20102012

20140%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Flavor

Filler

MTs

Burley Production

19901992

19941996

19982000

20022004

20062008

20102012

20140

50

100

150

200

250

300

350

Argentina Brazil USA

World Burley Production Share

1989 1999 2009 20150.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

USA Brazil ArgentinaMalawi Others

The significant decrease in higher-value flavor burley in recent years exemplifies a relatively rapid shift from traditional flavor producing regions.

Given the much smaller supply of flavor burley, manufacturers are certainly substituting filler for flavor.

Better technology in cigarette production.

Better quality filler tobacco.

Consumer demand for cheaper cigarettes.

Flavor vs. Filler Burley

U.S. Cigarette Taxes

2002200320042005200620072008200920102011201220132014 $-

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

Federal Excise Tax Avg. State Tax

$/Pack

Source:

U.S. Cigarette Retail Price

Source:

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2011 2012 2013 2014 $-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$1.93 $1.85

$1.95 $2.29

$3.29

$3.91 $4.25

$4.14 $4.58

$5.87 $6.00 $6.03 $6.05 $6.10

U.S. Cigarette Production

Source: USDA ERS, TMA

19971998

19992000

20012002

20032004

20052006

20072008

20092010

20112012

20132014

0

100

200

300

400

500

600

700

Domestic Consumption Exports

Billion Pieces

16% since 2009

45% last 10 years

Source: NASS/ERS/USDA2006-2008 Estimates by Univ. KY

KGs

US Burley Trade Balance

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 -

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

US Exports US Imports

American Blend Outlook Approximately 39% of cigarettes consumed worldwide are American blend compared to 53% Virginia and 8% other.

Consumption of American Blend cigarettes is concentrated in USA,

Russia, Japan, Philippines, Ukraine, South Korea and Germany. All are declining markets with approximately 5% decrease in consumption per year the past two years.

Growth markets for American Blend include Egypt, China, Iran, Thailand, Indonesia, Vietnam, Belarus and Taiwan.

While a declining market, American Blend sales declines are not substantially different from Virginia Blend declines and still represent a 2.1 trillion stick market.

Short-Term vs. Long-Term Supply

Short-term factors affecting supply will contribute to excess quantities and general reduction in quality.

Long-term factors contribute to lower capacity to produce flavor burley to meet demand.

U.S. Burley Tobacco

Hectares

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

KY+TN Others

U.S. Burley Tobacco

Hectares

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

KY+TN Others

Actual hectares planted in 2015 may be closer to 31,000

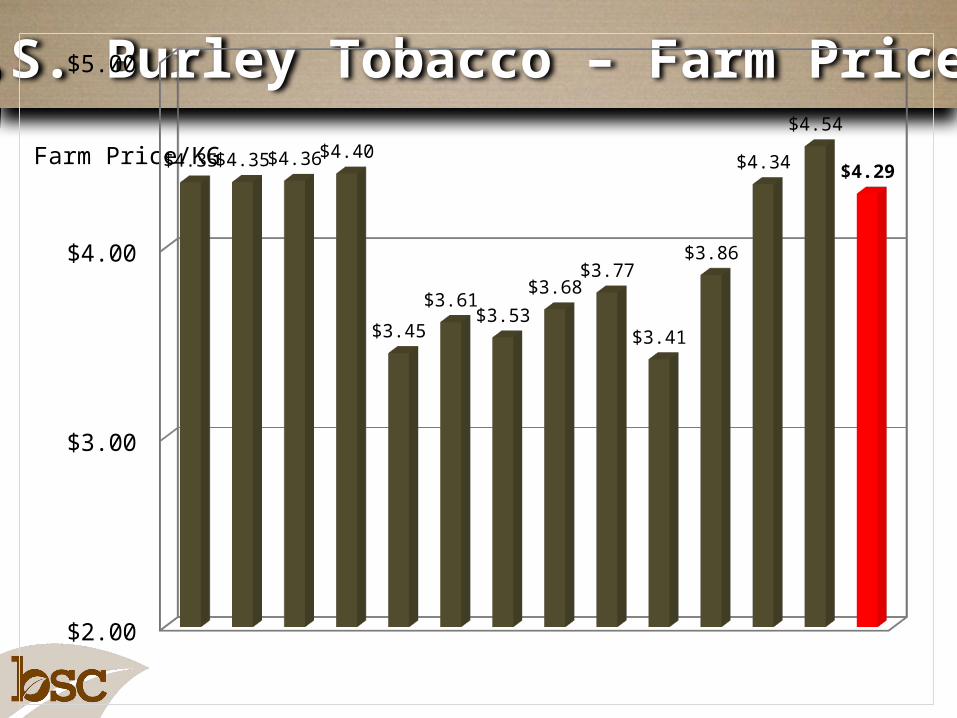

U.S. Burley Tobacco – Farm Prices

Farm Price/KG20

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

14

$2.00

$3.00

$4.00

$5.00

$4.35 $4.35 $4.36 $4.40

$3.45

$3.61 $3.53

$3.68 $3.77

$3.41

$3.86

$4.34

$4.54

$4.29

Burley Production Decision

2014 Contract Volume - 84 MT 2014 Production Volume - 95 MT

2015 Contract Volume - 59 MT

2014 Production Volume - 95 MT

• Growers are planting tobacco without a marketing contract.

• Current incentives to produce are out of line with current burley demand.

• If substantial contract volume reductions and price reductions are in place for 2015, then why are growers overproducing?

Burley Production Decision

Expected Price for Burley

1 acre of burley, 2,000 lb. yield history, 75% coverage

Produced 2,000 pounds of burley grading B4GF

B4GF receives discount factor of 0.60

1-0.6 = 0.4, 0.4 x 2,000 = 800 pounds counting as production

Expected Price for Burley

2014 Guaranty = 0.75 x 2,000 = 1,500 pound guarantee

Indemnity = 1,500 - 800 = 700700 x $2.05 = $1,435

Grower sells tobacco at 3rd quality for $1.90

Expected Price for Burley

Total price received per pound:

$1,435 indemnity + $3,800 sale price

$2.63/LB ($5.78/KG)

Expected Price for Burley - 2015

For 2015, Price election is $1.80/LB

Under same example, expected indemnity for B4GF is $1,260.

If grower expects $1.32/LB or greater for insured non-contract tobacco, non-contract tobacco will average the same as 2014 contract tobacco ($1.95/LB).

Source: US Ag Census, 2012

Average Age of U.S. Burley Growers

Under 251%

25-347%

35-4412%

45-5423%

55-6429%

65+28%

Likelihood of Producing in 10-Years

Source: UT CTGR Survey Data

KY-Burley KY-Dark NC-Flue NC-Burley TN-Burley TN-Dark0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%% Prob or Def will produce % prob or def will not produce

Likelihood of Producing in 10 YRs

Likelihood of Producing in 10-Years

Source: US Ag Census

Number of Tobacco Farms in KY

1992 1997 2002 2007 2012 -

10,000

20,000

30,000

40,000

50,000

60,000

59,373

44,967

29,237

8,113 4,530

15.50%

35.90%17.20%

14.20%

6.20%

11.00%Grain cropsCow/calfBeef CattleHayFruits/Veg.Other

Source: UT CTGR Survey Data

Alternative Crops to Burley Growers

Other Market Outlook Issues

Impact of the WHO – FCTC, FDA regulation and the EU Tobacco Products Directive

Participation of Big Tobacco into the electronic alternatives market

Continued growth in illicit trade – 1 in 10 cigarettes are illicit

Approach of Public Health to electronic cigs/vapor products

Future of Tobacco Regulations

Increased Attack on Combustibles Growth & Acceptance of E-options

Future of Alternatives

Philip Morris iQOS & HeatSticks JTI Ploom & Ploom Pax

Moist Snuff Sales

Source:

Million Pounds

20022003

20042005

20062007

20082009

20102011

20122013

20140

102030405060708090

100110120

E-Cig/Vapor

E-Cigs first on the market less than ten years ago.

Worldwide sales of vapor products totaled $3.5 billion in 2013, with approximately half of the sales in the USA.

E-Cig and Vapor product sales are approximately 2% of the value of cigarette sales in the USA.

Projected to exceed $50 billion per year worldwide by 2030 by Euromonitor.