the global solar power market shines again

TRANSCRIPT

Global Solar Power Market Solar PV is Becoming a High-growth Mainstream Energy Source in

Emerging Markets

MA28-14

June 2014

2 MA28-14

Contents

Section Slide Number

Executive Summary 4

Market Overview 11

Solar Power Market -

• Drivers and Restraints 20

• Forecasts and Trends 29

• Market Share and Competitive Analysis 58

CEO’s 360 Degree Perspective 67

North America Analysis 69

Europe Analysis 91

Asia-Pacific Analysis 113

Latin America Analysis 135

Middle East and Africa Analysis 157

The Last Word 178

Appendix 181

3 MA28-14

CEO’s Perspective

2 The Asia-Pacific market is the fastest and

largest market for industrial, commercial, and

residential solar PV systems.

3 FiT incentives, subsidies, and supportive

government legislation have increased solar

power market attractiveness.

4

Demand is fast emerging in the Latin

America region and the Middle East and

Africa (MEA) region due to rapid growth and

unreliable electric grid networks.

5 Aggressive expansion by Chinese PV

module manufacturers has led to global

overcapacity and market consolidation.

1

Prices of solar PV modules are expected to

decline further or, at best, stabilise because

most companies still have high inventory

levels.

Source: Frost & Sullivan

4 MA28-14

Key Findings

• Frost & Sullivan estimates that the global solar market revenue decreased by 12.9% in 2013 compared to the previous year. Market revenue is estimated to reach $137.02 billion in 2020 growing at a compound annual growth rate (CAGR) of 12.6%. The market is expected to follow a positive growth pattern throughout the forecast period despite economic uncertainty in the global market.

• As a result of significant overcapacity and price decline of photovoltaic (PV) modules, the market registered negative growth in 2013 and larger global suppliers of PV panels struggled to make a profit, with some of them filing for bankruptcy.

• In 2013, the industrial and public projects segment accounted for the majority of the annual installed capacity at 50% and will be the fastest-growing segment for annual capacity installed at a CAGR of 10.2%.

• One of the key drivers for this market has been defining the structure of feed-in tariffs (FiTs) for solar PV-generated power. Favourable legislation should continue to propel the growth of the industry as a whole.

• A number of government-sponsored initiatives are expected to boost the proportion of energy coming from green sources, and political willingness will also be a key driver of this market throughout the forecast period. With climate change high on the agenda for most governments, renewable energy has come to the forefront as one of the solutions proposed to combat global warming.

Source: Frost & Sullivan

5 MA28-14

• Growth in the solar power market is impacted by the level of insolation that a region receives. Insolation is defined as the amount of solar energy reaching the earth, which is usually strongest on and around the equator and is measured in kWh/m2/day.

• Higher latitudes have lower insolation levels, therefore, some regions are unattractive markets for solar PV.

Key Findings (continued)

• According to the European Photovoltaic Industry Association (EPIA), ‘‘China and India will lead the way as PV prices fall and economies rapidly develop in countries located ±35° around the equator.’’ China and India have become the most attractive markets over the last 5 years. Most large PV module manufacturers are building up their capabilities with tie-ups and alliances in these countries. Increased investment into this market is a result of the likely introduction of FiT systems, adequate solar radiation, and increasing awareness of renewable technologies.

• With increased technological efficiency, the cost of generating solar energy has decreased significantly, though the installation and maintenance costs still remain relatively high. Therefore, incentive mechanisms are an important factor encouraging investments for growth of the solar power market.

Key: kWh/m2/day = kilowatt hour/square metres/day Source: Frost & Sullivan

Solar Power Market: Solar Radiation Map, Global, 2013

Image Source: http://meteonorm.com

6 MA28-14

Key Findings (continued)

• The reduction of emissions from greenhouse gases (GHGs) and other pollutants is a priority for many countries, while energy efficiency is one of the most cost-effective ways to enhance security of energy supply. In many ways, energy sufficiency is one of the drivers impacting growth of the solar power market.

• The competitive landscape of the solar power market has been extremely dynamic with companies registering high growth at one point and declaring bankruptcy a few years later.

• Low manufacturing costs in Asia, particularly China, have resulted in the liquidation of some industry pioneers such as BP Solar, Photowatt (one of the first PV companies to become profitable), and Evergreen Solar (which closed its solar division, as was the case for BP). Q-Cells also closed down (although it was later rescued by BMW heir, Quandt). Suntech declared bankruptcy in March 2013.

• However, the market currently looks quite buoyant and Frost & Sullivan expects the market revenue to reach $74.79 billion in 2014, an increase of 25% over 2013.

Source: Frost & Sullivan

7 MA28-14

Drivers and Restraints

Solar Power Market: Key Market Drivers and Restraints, Global, 2014–2020

Dri

ve

rs

Re

str

ain

ts

Dri

ve

rs

Re

str

ain

ts

Greater demand for

energy sustainability

drives opportunities

for solar PV.

Recession-triggered

price declines will

accelerate

installations. Government

incentives promote

the solar power

market.

High reliance on

government support

impedes development.

Lower energy return on

invested (EROI) compared

to conventional energy

systems reduces growth

potential.

Economic downturn and

global instability still

discourage significant

capital investments in the

market.

The wider market for other

renewable energy

technologies restrains

uptake of solar PV systems.

Denotes long-term impact

Denotes current impact Source: Frost & Sullivan

Increasing environmental

awareness and

decreasing dependency

on fossil fuels will drive

the market.

Technological

improvements and

advances in

efficiency create

new opportunities.

Key Takeaway: Energy sustainability, price declines, and environmental awareness drive the market.

8 MA28-14

Revenue Forecast Discussion

0

20

40

60

80

100

120

140

160

2013 2020

Revenue 59.84 137.02

Reve

nu

e (

$ B

illi

on

)

Solar Power Market: Revenue Forecast, Global, 2013 and 2020

• The global solar power market revenues are expected

to increase from $59.84 billion in 2013 to $137.02 billion

by 2020.

• The market is driven by increasing the focus to curb

emissions, drafting strict clean energy regulations, and

offering adequate subsidies to the renewable energy

sector. Solar power finds applications across

residential, commercial, industrial, and public projects.

• As a result of significant overcapacity in the solar power

market, larger global suppliers of PV panels in the

emerging markets were struggling to make profits. The

market witnessed drastic changes in the supply-

demand pattern, regional policies, and tariff cuts.

• The market is largely influenced by pricing patterns of

PV modules and the ability of the global suppliers to

exploit short-term revenue opportunities.

• Because the market is likely to be driven by the

emerging markets, it is important that the solar PV

value chain is adequately integrated such that suppliers

and project developers can adjust project deployment

between different countries and regions on short notice.

Note: All figures are rounded. The base year is 2013. Source: Frost & Sullivan

Year

9 MA28-14

Annual Installed Capacity Forecast Discussion

0

10,000

20,000

30,000

40,000

50,000

60,000

2013 2020

Annual Installed Capacity

28,528 54,190

An

nu

al

Ins

tall

ed

Cap

ac

ity (

MW

)

Solar Power Market: Annual Installed Capacity Forecast, Global, 2013 and

2020

• Frost & Sullivan estimates that the global solar

market annual installed capacity decreased by 9.1%

in 2013, compared to 2012. The annual installed

capacity is estimated to reach 54.2 GW in 2020,

growing at a CAGR of 9.6%.

• A total of almost 45 GW of solar PV capacity is

expected to be added every year until 2020. The

price decline of PV modules will be a key market

driver supporting the penetration of solar power,

especially in emerging markets.

• The solar market is sure to benefit from various

incentive schemes in the forms of tradable green

energy certificates, FiTs, and tax rebates for the use

of renewable energy for power generation. However,

it continues to remain very heterogeneous and solar

PV penetration varies widely and is dependent on

local and regional policies.

• Policy decisions will drive the market during the

forecast period. Environmental policies, along with

upgrades and modifications of the electricity grid, will

continue to have a heavy influence on the electricity

prices for final consumers.

Note: All figures are rounded. The base year is 2013. Source: Frost & Sullivan

Year

10 MA28-14

Market Structure

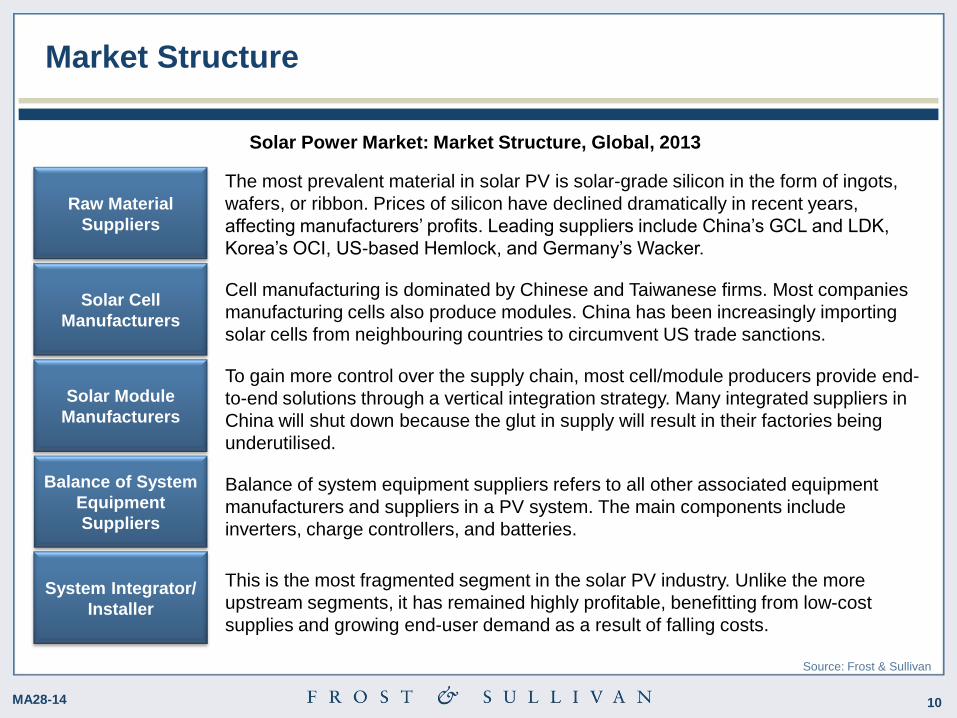

The most prevalent material in solar PV is solar-grade silicon in the form of ingots,

wafers, or ribbon. Prices of silicon have declined dramatically in recent years,

affecting manufacturers’ profits. Leading suppliers include China’s GCL and LDK,

Korea’s OCI, US-based Hemlock, and Germany’s Wacker.

Cell manufacturing is dominated by Chinese and Taiwanese firms. Most companies

manufacturing cells also produce modules. China has been increasingly importing

solar cells from neighbouring countries to circumvent US trade sanctions.

To gain more control over the supply chain, most cell/module producers provide end-

to-end solutions through a vertical integration strategy. Many integrated suppliers in

China will shut down because the glut in supply will result in their factories being

underutilised.

Balance of system equipment suppliers refers to all other associated equipment

manufacturers and suppliers in a PV system. The main components include

inverters, charge controllers, and batteries.

This is the most fragmented segment in the solar PV industry. Unlike the more

upstream segments, it has remained highly profitable, benefitting from low-cost

supplies and growing end-user demand as a result of falling costs.

Solar Power Market: Market Structure, Global, 2013

Raw Material

Suppliers

Solar Cell

Manufacturers

Solar Module

Manufacturers

Balance of System

Equipment

Suppliers

System Integrator/

Installer

Source: Frost & Sullivan

11 MA28-14

Distribution Channels

Solar PV Cell/Module

Manufacturers

End User

Company-owned

Dealers/Distributors

Independent Accredited

Installers

Agents

Partners

Direct Sales

Superstores

EPC Sales

Solar Power Market: Distribution Channel Analysis, Global, 2013

Key: EPC = engineering, procurement, and construction

Source: Frost & Sullivan

30%

Key Takeaway: Independent accredited installers are dominant in the distribution system.

10%

25%

15%

5%

5%

10%

12 MA28-14

Pricing Analysis

Solar Power Market: Price Component

Structure, Global, 2013

Component

Per cent of

Overall

Capital Costs

Trend

PV module/panels 40–55%

Inverters 20–35%

Mounting Frame 8–12%

Balance of Systems 6–8%

Planning and

Installation 10–20%

• The PV module is a critical component of the solar

PV system. Modules are clusters of PV cells

incorporated into a unit usually under a sheet of

glass.

• The inverter is used to convert direct current (DC)

electricity produced by the PV module into alternating

current (AC) electricity.

• A mounting frame’s purpose is to hold the modules

together. Frames can vary in design and materials,

depending on the type of installation: roof-mounted,

pole-mounted, or ground-based. Also, tracking

systems can be used to optimise the angle of the PV

module relative to the sun, increasing the yields by

25% to 40%

• Batteries can be used mainly for off-grid systems.

Deep-cycle batteries in solar power systems are

designed to be discharged constantly, over longer

time periods.

• The balance of system components includes meters,

switches, and the cables.

Note: All figures are rounded. The base year is 2013. Source: Frost & Sullivan

Trend Decreasing Stable Increasing

13 MA28-14

Pricing Trends

Solar Power Market: Price Trends, Global,

2001–2020

• The continued panel price reduction and

the volatility of legislative policies make

it difficult to predict the future of solar

PV price movements. Frost & Sullivan

forecasts that the price of PV modules

is, at best, likely to stabilise, if not

reduce further.

• Although the price of solar systems has

decreased in the last few years, the

costs are still high for an investor with

no incentives.

• High costs lead to lengthy payback

periods that may deter investments in

solar power.

• Moreover, several original equipment

manufacturers (OEMs) from the United

States and Europe are likely to

penetrate the untapped Southeast Asia

market to survive competition.

• FiTs are the most popular form of

government support.

Source: www.statista.com; Frost & Sullivan

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Pri

ce

Pe

r P

ea

k W

att

($)

PV Cells PV Modules

Year

14 MA28-14

LCOE Analysis

LCOE, $/MWh Green energy

Total Lifetime Expenses

Energy Output, MWh

Resource Availability

Rated Power of Equipment

Equipment Lifetime

Equipment Availability

Capital Costs

O&M Costs

Discount Factor

Equipment Lifetime

Discount Factor

Comparison with

‘grid’ electricity

Solar Power Market: LCOE, Global, 2013

• The LCOE is defined as the total life cycle cost of a PV system / total lifetime energy production. Massive

regional variations and assumptions exist on every element of the LCOE equation. Capital costs and

resource availability are the main factors affecting LCOE for solar energy.

• The LCOE for PV solar electricity ranges between $0.10 and $0.20 per kilowatt hour (kWh). A few

renewable energy sources are already competitive with conventional generation. However, solar is still

above grid parity at present.

• The price reduction of PV modules, FiT incentive schemes, and net metering policies that are adopted

globally are likely to reduce LCOE and make it comparable with other conventional/renewable energy

sources. Source: Frost & Sullivan Note: operations and maintenance (O&M)

15 MA28-14

Solar Power Market: Solar PV Technology Curve, Global, 2013

Technology Analysis

Maturity Development Growth Decline

Time

Source: Frost & Sullivan

Dye-sensitised solar

cell (DSSC)

Ma

rke

t P

en

etr

ati

on

an

d C

om

me

rcia

lis

ati

on

Organic Cell

Hybrid HIT Cell

2nd Generation PV (thin-film based)

1st Generation PV

(crystalline based)

Third-generation solar cells aim to achieve high

efficiency but still use thin film and second-

generation deposition methods. This should be

done with only a small increase in area costs and;

thus, reduced cost per watt peak.

Thin-film solar technologies primarily use non-

semiconductor materials including copper, cadmium,

and tellurium to create PV cells. Second-generation

solar cells are cheaper than first-generation solar

cells but have lower efficiency. They have lower cost

per watt and are effective under low light conditions.

First-generation solar cells dominate

the commercial market because they

have higher efficiencies. There is likely

to be a sustained demand for this solar

PV technology because it is cheaper,

reliable, tested, and proven over the

years.

3rd Generation PV

16 MA28-14

Technology Trends

• Polysilicon-based technologies are the most widespread, but thin-film technologies have been gaining

market share. However, the on-going price falls of polysilicon have eroded some of the cost advantages

of thin film as its market share has remained at about 14% of the annual installed capacity in 2013.

• The maximum recorded lab cell efficiency is about 20% for polysilicon-based technologies and 15% for

thin-film solar cells. However, scientists at Empa, the Swiss Federal Laboratories for Materials Science

and Technology, announced in early 2013 that they had developed thin-film solar cells with a new

efficiency record of 20.4%.

• According to the Fraunhofer Institute for Solar Energy Systems, material usage for silicon cells has

been reduced significantly during the past 5 years from about 16 grams per Watt-Peak (g/Wp) to 6 g/Wp

due to increased efficiencies and thinner wafers.

Source: Frost & Sullivan

• Until now, adoption of the first-generation technology (i.e.,

polycrystalline cells and modules) has dominated the solar power

market. This includes both the on-grid and off-grid markets.

• There is a slow and steady demand for thin-film solar cells,

especially amorphous silicon cells and modules.

• Extensive research and development (R&D) spending in recent

years, combined with mass market development leading to scale

economies, has led to dramatic declines in the cost of solar PV

modules, estimated at up to 75% from pre-recession levels.

17 MA28-14

Solar Power Market: Life Cycle Assessment, Global, 2013

Regional Life Cycle Assessment

Maturity Development Growth Decline

Time

Source: Frost & Sullivan

North

America

Ma

rke

t V

alu

e

Latin America

MEA

APAC

Europe

Middle East: Power demand and supply gaps and demand from

infrastructure projects have created a market for solar PV.

Africa: The African market is in a growth stage. The oil and gas

and construction sectors are driving demand for solar PV. Major

power outages in these regions will lead to increased demand for

energy security.

APAC: The power supply gap and demand for

adequate electricity have created a need for

solar PV in APAC. India, China, and South

Asia have become attractive destinations for

market expansion.

Europe: The European market

is in the late growth stage.

European participants are

considering geographical

expansion and improving

technological efficiency.

North America: The expiration of the 1603

program in the United States will affect new

system installations. Industry participants are

convinced that the market in the Americas will

grow, albeit at a slower rate.

Latin America: Latin American

countries are highly reliant on

hydroelectric power. During

droughts, the demand for solar

power increases.

18 MA28-14

Strategic Analysis—Five Forces Model

Source: Frost & Sullivan

Intensity of Rivalry: High

Opportunities are well known; therefore,

many suppliers compete to enter bids in

a good position.

Bargaining Power of

Customers: Medium-

High

In the current environment,

the bargaining power of end

users is high due to a large

number of suppliers in the

market.

Bargaining Power

of Suppliers: Low

The market is end-user

oriented for solar PV,

and competition is fierce

among suppliers to win

projects.

Threat of New Entrants: High The increasing activities by regional manufacturers, chiefly in the

APAC market, have resulted in price competition and increased

threats to large global participants of solar modules.

Threat of Substitutes: Medium-High Most substitutes come in the form of other renewable and distributed

generation technologies, such as gensets. The flexibility of the

technology and support incentives are key decision drivers for solar.

Solar Power Market: Five Forces Model, Global, 2013

19 MA28-14

The Last Word—3 Big Predictions

2 APAC will continue to be the largest region for solar power. Most manufacturers are

likely to build up manufacturing capabilities either organically or through partnerships

and alliances in the region.

3 The solar PV supply chain participants are likely to develop new technologies that will

integrate PVs with flexible infrastructure grids. Solar PV power will mature into a

mainstream technology with the help of efficient grid integration and management.

1 Effective policies and regulatory frameworks, the low cost of solar modules, and

active participation and high awareness among customers will drive the growth of the

global solar power market.

Source: Frost & Sullivan

20 MA28-14

Research Team

Lead Analyst Research Director

John Raspin Partner

Energy and Environment

(+44) 20 7915 7814

Pritil Gunjan Industry Analyst

Energy and Environment

(+44) 20 7915 7832

Contributing Research Manager

Alina Bakhareva Research Manager

Energy and Environment

(+44) 20 7915 7829