the goals of finance 1.to simplify finance systems and business processes 2.to adopt a gaap...

Post on 19-Dec-2015

215 views

TRANSCRIPT

1

The Goals of Finance

1. To simplify finance systems and business processes

2. To adopt a GAAP (Generally Accepted Accounting Principles) compliant "single source of truth" in all financial reporting

3. To build and develop a strong team of high quality professional staff in finance roles across the University

4. To develop a responsive, helpful, customer-friendly culture

5. To improve the quality of financial management and planning, positioning Finance as the trusted adviser of decision-makers at all University levels

2

Stephen ReesDirector of Finance

3

The Way Forward Janz Reinecke ~ Finance Division

4

Agenda

• The need and support for transformation

• How the transformation is going to happen

• What’s in it for you?

• Our systems

• What are the changes?

• Next steps

• Questions?

5

Decision Support:Distrust of Financial Information

Informal framework

NOW

Stewardship & Compliance:Confusing rules and inconsistent accounting treatments

Little accountability and ownership

Transaction Processes:Journal rework

Offshore purchases are complex and slow

Low degree of automation

Decision Support:Customer service focus

High degree of Financial Management

Improved decision making

AHEAD

Stewardship & Compliance:Appointment of Finance Managers

Consistent reporting

More reliably phased budgets

Transaction Processes:Reduced number of transfer journals

Procedures performed at an appropriate level

The need for transformation

6

The support for improvement

• Analysis of project balances shows that approx. 40% of Projects are in deficit (by value compared to budgets)

• Non-standardised, conflicting reports used for review of Faculty, School and Divisional financial performance

• Variable ownership and accountability of Faculty and Divisional budgets across the University

• Inconsistent accounting treatment (non-GAAP) operating across different levels of the University

• High levels of resource dedicated to journal re-work, reporting dispute and correction related activities

7

How?

Alignment of NS Financials with

Calumo

Substituting Commitment Control with

active financial management

Standard monthly reporting

framework to discuss operating results to budget

Budget model established on

common platform to AIFRS

Consistent accounting rules across all areas

Regular review and discussion on

financial performance &

forecast position

Review of business

processes which impact customers

Development of Customer Service

standards

Ongoing monitoring of service quality

through customer feedback

Finance assisting with

implementation of improvements

Finance Managers supporting areas of the University

Clear advice and quality services to

support the UNSW community

8

What’s in it for you?

• Financial information which is meaningful, clear and friendly

• A focus on advice and guidance tailored to the needs of your business

• The removal of non-value add activities (such as removing 100,000 plus budget transfer journal entries across faculties, elimination of over 2,000 redundant research reports)

• Reliable management reports aligned to the needs of the business

• Provision of strong finance capabilities embedded into the organisation to support local decision making

• A more customer-centric service culture across every area of Finance

/

9

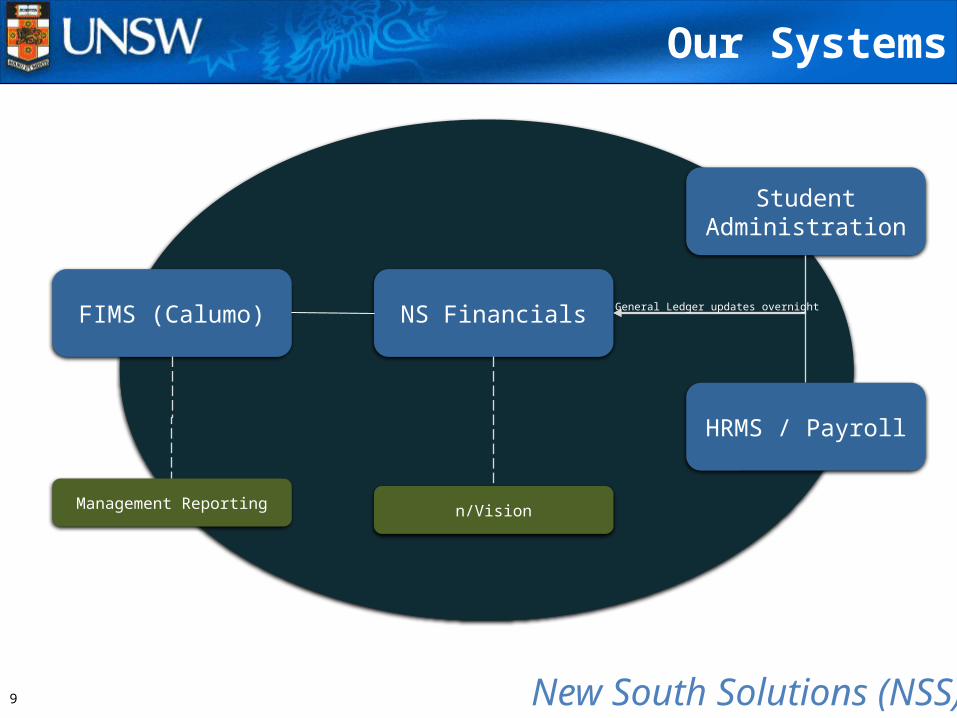

Our Systems

FIMS (Calumo) NS Financials

n/VisionManagement Reporting

Student Administration

HRMS / Payroll

General Ledger updates overnight

New South Solutions (NSS)

10

General Ledger

Asset Management

Accounts Payable

eProcurement

Accounts Receivable

NS Financials

Purchasing Billing

Credit Card

Expenses

11 /

• Commitment Control

• Fund Code Reduction

• Chart of Accounts Review

• Reporting

• AIFRS

• Budget Management

How does this impact you?

12

Commitment Control

13

Commitment Control

What is Commitment Control?

Commitment Control is used for budgetary control. It refers to the process of defining and tracking the actual expenses incurred through each module.

Commitment control blocks a transaction that would cause a pre-set budget limit to be exceeded.

Myths about Commitment Control

Commitment Control flags an issue too lateA very useful tool to assist management in managing budgets

BELIEFS EVIDENCE TO THE CONTRARY

Prevents over spending At 31 Aug 09, in value terms approx 40% of projects over budget

Keeps budget owners below budget Over 40% of projects are in deficit

Allows more time to spend on Research type activities and less time managing the finances

Considerable time is spent on adjusting misdirected transactions to resolve commitment control issues

Without Commitment Control there would be a “spending frenzy”

Commitment Control wasn’t applying to people related costs (which accounts for 80% of total costs)

Necessary part of UNSW Areas of UNSW have operated without commitment control for some time

Financial performance would go down hill if not for Commitment Control

Commitment Control ‘budgets’ total $29.7 million above Official UNSW Budget

14

15

Commitment Control signals issues too late

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec0

500

1000

1500

2000

2500

-400

-300

-200

-100

0

100

200

300

400

500

600

Revenue (LHS) Total Costs (LHS) Net Result (RHS)

Commitment Control limit set

Commitment Control "de-tects" expenditure above

budget.

16

Active budgetary control works better

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

-400

-300

-200

-100

0

100

200

300

400

500

600

Net result Budget Net Result

Net result at end of year below by same amount as suggested in April and identified in August.

Aware throughout the year that per-formance is trending below expecta-tions (budget)... Shortfall identified much

sooner through active man-agement of results.

Corrective action can be taken sooner to avoid

adverse budget outcome

17

• Budget checks will no longer fail

• Processing transactions will be easier (and more accurate)

• Less adjustments will be necessary

• Misdirection of expenditure will be reduced

• Budget management can now actively be performed by the budget

owner

No Commitment Control

/

18

Fund Code Reduction

19

The Challenges

• Size & Complexity

• Combination of organisational structure, project structure (to add a detailed fund structure - 5 funds grew into about 40 over time)

• Informal rules developed around the use of one fund vs another

• Transfers between fund categories diminished their intended purpose

• Historically balances and different treatments resulted making comparing them difficult

20

Fund Code Outcomes

Consolidated Operating Strategic Capital Restricted

Reduced from 33 codes to just one:

OP001

Commercial Activities

12 codes of 35 remain for 2010

Remaining 23 codes transferred

toOP001 and

retired

SIR and SPF codes remain

LT001 will stay until 2011

CPF01 remains

USG01 codes retired

380 codes reduced to 180

codes

Maintained for HERDC purposes

Ongoing review to identify further

reductions

/

21

Chart of AccountsReview Update

22

Chart of Accounts

Account Names & Descriptions

Accounting Guidelines

Process Clarity & Communication

Structural Issues

• Large volume of accounts, many with similar/indistinguishable descriptions making their use unclear or confusing

• No clarity on the use of specific accounts such as contractors, contract services and little clarity on accounting rules for internal transfers, cost recoveries, etc

• What is the process for getting new account opened? Who do I contact? / Who do I ask for assistance? Who are communications sent to?

• Cleanup of old projects, departments and funds long overdue

23

“Chartfield”

PHASE ONE(in Finalisation stage)

Chart of Accounts

Expenses

Revenue

B/Sheet

Business Unit

Accounts

Departments

Funds

Projects

Program

Class

24

“Chartfield”

PHASE TWO(revenue accounts)

Chart of Accounts

Revenue

Expenses

B/Sheet

Business Unit

Accounts

Departments

Funds

Projects

Program

Class

25

What are the Revenue account changes?

71Accounts

Accounts not used for 2-4 years will be made inactiveAccounts Not Used

95Accounts

Account Name & detailed description will be amended to improve clarity & consistency of revenue allocation

Account Name Changes

50Accounts

• These accounts will be inactivated• Historical data to these accounts will not change• No transfers necessary

Redundant Accounts and redirects

15Accounts New accounts to enhance clarity and consistencyNew Accounts

26

Major changes

• Naming convention has been developed

• Redirects / Redundant accounts

• Changes to existing coding practice

• Reference guides have been created for Revenue Accounts (to compliment the existing guide for Expenses)

27

Naming convention

28

Redirect Example – Teaching Income

0903Fees Non Award Student Activity

0909Fees Non Award Local Misc.

0910Fees Non Award Math Skills

0911Fees Voluntary Subjects

0913Fees Continuing Education

0911Teaching – Cont Ed’n Subjects

0913Teaching – Cont Ed’n Courses

2009

2010

29

What do you need to do?

Identify accounts that are applicable to you and ensure the transactions that are allocated to these accounts are applicable under the revised user guidelines, if not establish what the appropriate account is

Identify if any of the accounts you use are listed to be redirected and ensure any concerns are addressed

Review information on the www.fin.unsw.edu.au

Remember that the Chart of Accounts Review is a work in progress and we welcome user feedback

30

CoA Website

www.fin.unsw.edu.au

/

31

Reporting

32

Reporting – The Challenges

• Reports disconnected between total Faculty / Division balances and project related balances

• Unclear from reports what was excluded and how reconciles to other reports

• Context biased towards funds & project balances rather than organisation structure (department)

• Project level budget values not at a level which can be used to manage specific expense categories

• Abundance of project codes largely due to Commitment Control

• Needed informative reports on what we spend our revenue on

33

Reporting - 2009

Faculty / Division reportsStudent revenue allocated

Budget at summary account level

Faculty / Division reportsNo student revenue allocatedNo budget detail by account type

No project reportsProject level detailOne line budget

Executive ReportingNo Executive Reporting

NSF Calumo

34

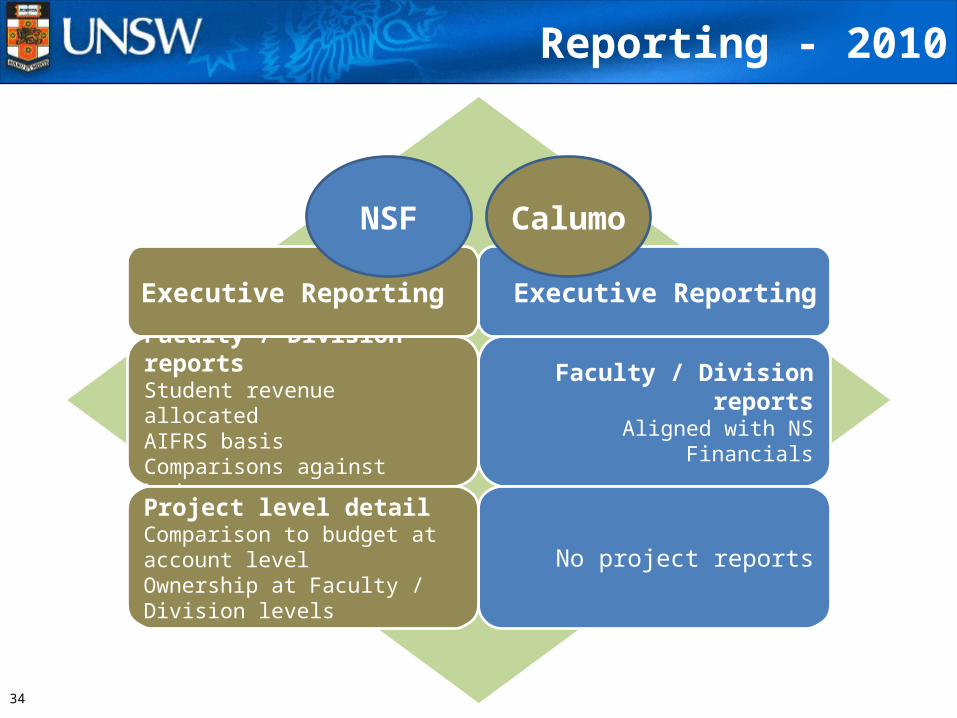

Reporting - 2010

Faculty / Division reportsAligned with NS Financials

Faculty / Division reportsStudent revenue allocatedAIFRS basisComparisons against budget

No project reports

Project level detailComparison to budget at account levelOwnership at Faculty / Division levels

Executive ReportingExecutive Reporting

NSF Calumo

35

Report ID: ????? Scope Name: ALL ACCOUNTS Accounting Period: 7

$'000 Jul 08 YTD

Actual Budget Variance Actual Budget Variance Actual Forecast Budget Variance Costs

People CostAcademic 33.7 33.4 (0.3) 202.3 204.1 1.8 341.0 368.1 355.0 (13.1)General 29.6 27.8 (1.8) 170.6 170.1 (0.5) 663.5 301.3 293.8 (7.5)Other people's cost 1.1 0.5 (0.6) 2.9 3.2 0.3 4.8 4.3 5.4 1.1

Total people cost 64.4 61.7 (2.7) 375.8 377.4 1.6 1,009.3 673.7 654.2 (19.5)Other Costs

Scholarship expenses 4.7 4.5 (0.2) 32.3 31.5 (0.8) 49.8 58.6 54.0 (4.6)Contract & consulting services 5.3 6.3 1.0 35.5 44.4 8.9 70.4 71.1 76.1 5.0Entertainment 0.3 0.3 - 2.4 2.0 (0.4) 4.4 4.5 3.4 (1.1)Marketing 0.2 0.6 0.4 3.5 4.4 0.9 8.6 7.5 7.5 -Overheads 0.8 1.2 0.4 7.4 8.6 1.2 12.0 13.9 14.8 0.9Repairs and maintenance 3.2 2.1 (1.1) 19.1 14.8 (4.3) 29.6 29.1 25.4 (3.7)Consumables 3.8 3.2 (0.6) 19.0 22.3 3.3 34.2 36.4 38.2 1.8Travel 2.7 2.3 (0.4) 14.9 16.3 1.4 29.8 26.8 28.0 1.2Equipment non capital 3.6 2.2 (1.4) 13.2 15.5 2.3 26.4 24.7 26.5 1.8Other expenses 4.3 6.6 2.3 42.6 45.9 3.3 64.8 83.4 78.7 (4.7)Internal expense 10.7 2.9 (7.8) 29.5 20.6 (8.9) 46.4 39.0 35.3 (3.7)Interest expense 0.2 0.1 (0.1) 2.5 0.8 (1.7) 5.2 5.3 1.4 (3.9)

Total other costs 39.8 32.3 (7.5) 221.9 227.1 5.2 381.6 400.3 389.3 (11.0)Transfer from Reserves (0.1) 0.1 - - - - 1.0 - (1.0)

TOTAL COSTS 104.1 94.0 (10.1) 597.7 604.5 6.8 1,390.9 1,075.0 1,043.5 (31.5)

Result before depreciation 24.2 (3.9) 48.3 110.9 42.2 55.1 6.0 106.5 67.8 101.7

Depreciation 7.1 6.8 (0.3) 50.4 47.3 (3.1) 83.6 88.5 81.1 (7.4)

Operating Result 17.1 (10.7) 27.8 60.5 (5.1) 65.6 (77.6) 18.0 (13.3) 31.3

UNSW Total

UNSWFinancial Statement

Jul-09

LOGOJuly 09 (Month) July-09 YTD FY 2009 Forecast

Aligned with Calumo

New nVision Reports

Actuals and Accrue_Add

36

New nVision Reports

Report name Executive Faculty / Division

School / Unit Project

F1_Standard Financial Statement (P&L)

F2_Summary Financial Statement (P&L)

F3_Summary Financial Statement Fund Grp

F4_Detailed Financial Statement (P&L)

F5_Trial Balance

D1_Project results (Dept Summary)

D2_Summary P&L by Dept

P1_Standard Project P&L

P2_Life to date Project report

P3_Project results summary - Dept/Fund

“Old” nVision reports still available

Reports available from early 2010

37

AIFRS

38

AIFRS

Australian International Financial Reporting Standards

www.aasb.com.au (Australian Accounting Standards Board)www.iasb.org (International Accounting Standards Board)

39

Accounting Manual

/

New/Updated Policies:

Financial Reporting Foreign Currency Translation Taxes Inventories Intangible Assets Property, Plant & Equipment Impairment of Assets Non-current Assets held for Sale and Discontinued Operations Investments in Associates and Joint-Ventures Investments and Other Financial Assets Leases Payables and Borrowings Trade Receivables Provisions and Employee Benefits Revenue Recognition

40

AIFRS

Student Fees

Employee Costs

Research

Other

Government Grants

Revenue

41

Revenue – Teaching & Learning

DEEWR revenue allocated to Faculties in

NS Financials, then reported in Calumo

DEEWR revenue allocated to Faculties in

Calumo not in NS Financials

Revenue recognised based on ACTUAL

student enrolments (accrued as earned)

Revenue recognised on CASH basis

&End of year accrual

Student Fees

Employee Costs

Research

Other

Government Grants

Revenue

2009 2010

www.fin.unsw.edu.au

42

Student related income in NS Financials

600m

2009 2010

NilMED

UNSW

SCI

ARTS

Nil

Nil

150

220

230

Sum of below(600m)

etc… … …

Same balances

in NS Financials & Calumo

Split down to School

level

Derived from

Student Financial System

Student Fees

Employee Costs

Research

Other

Government Grants

Revenue

www.fin.unsw.edu.au

43

Research

No reclassification required

Re classification of grants based on the

nature at Central

Monthly deferral/accrual at

Faculty level

Monthly deferral/accrual at

Central level

Coding to relevant income accounts

Coding to limited set of specific accounts at

Faculty level

Student Fees

Employee Costs

Research

Other

Government Grants

Revenue

2009 2010

www.fin.unsw.edu.au

44

Expenses – Employee costs

Annual leave:No charge when taken;

Charged to Faculties when entitlement accrues

Annual leave:Charged to Faculties when

taken; Charged to Central when

entitlement accrues

2009 2010

More constant Annual Leave expense from period to period

Highly variable Annual Leave expense from period to period

On-costs reflected in Faculty / Division results

Related on-costs not reflected in Faculty / Division results

Standard charge for Annual Leave based on statutory rate of 20 days per year per employee

Salary / wages that would otherwise be charged to S&W

account, charged to AL expense

Student Fees

Employee Costs

Research

Other

Government Grants

Revenue

More transparency for Faculties and DivisionsLow level of transparency

www.fin.unsw.edu.au

45

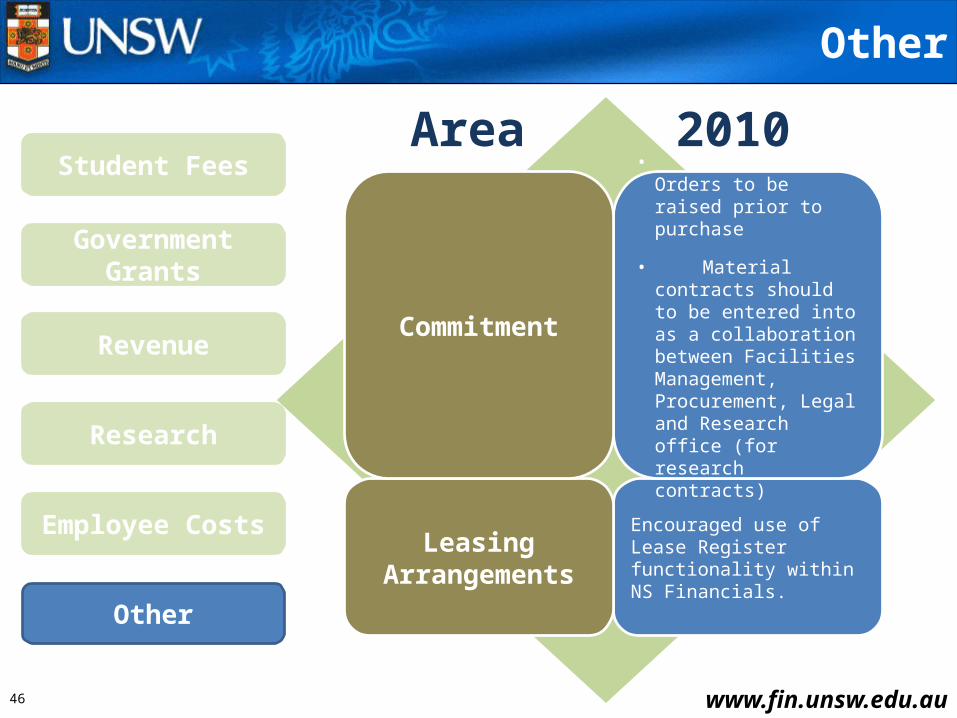

Other

More formalised and collaborative 'capital assessment‘ process in order to capture additional costs of a capital nature

Capital/ Construction projects

IT expenditure capitalisation

• All asset acquisitions through POs to enable capture of 'accruals' & 'commitments' info

• Tagging & Stocktake performed for assets costing $5,000 or more

Computers, Motor vehicles , Other

Plant & Equipment

Contingent Assets & Liabilities

Better guidance embodied in the procedure

Student Fees

Employee Costs

Research

Other

Government Grants

Revenue

Area 2010

www.fin.unsw.edu.au

46

Other

Encouraged use of Lease Register functionality within NS Financials.

Leasing Arrangements

2009 2010• Purchase Orders to be raised prior to purchase

• Material contracts should to be entered into as a collaboration between Facilities Management, Procurement, Legal and Research office (for research contracts)

Commitment

Student Fees

Employee Costs

Research

Other

Government Grants

Revenue

Area 2010

www.fin.unsw.edu.au

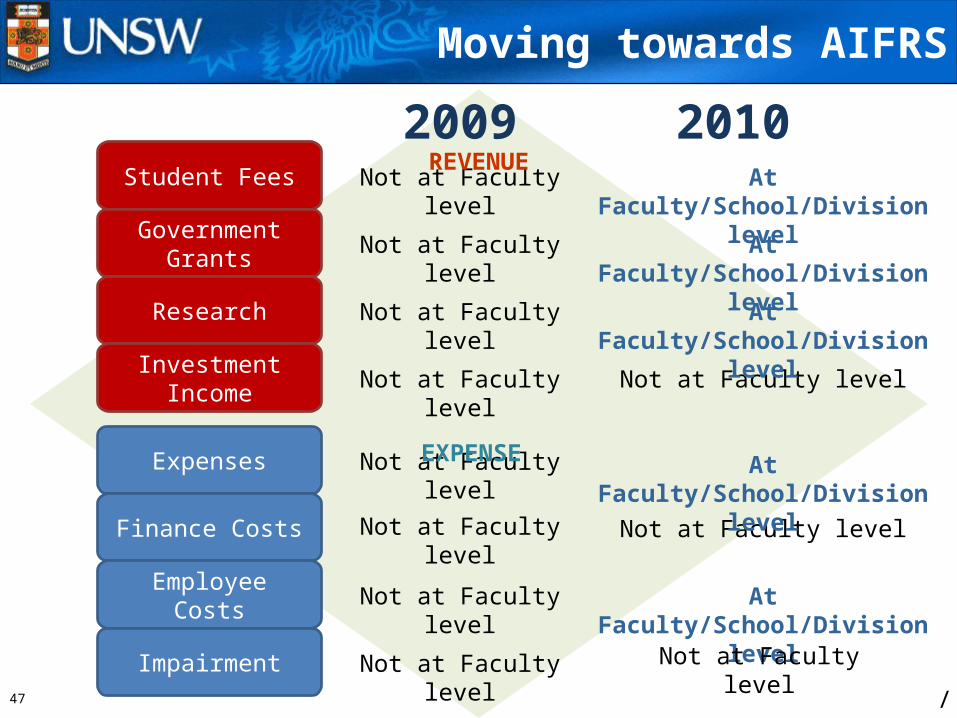

47

Not at Faculty level

Not at Faculty level

Not at Faculty level

Not at Faculty level

Not at Faculty level

Moving towards AIFRS

Not at Faculty level

Not at Faculty level

At Faculty/School/Division level

Not at Faculty level

Not at Faculty level

Not at Faculty level

At Faculty/School/Division level

At Faculty/School/Division level

At Faculty/School/Division level

At Faculty/School/Division levelREVENUE

EXPENSE

Student Fees

Government Grants

Research

Investment Income

Expenses

Finance Costs

Employee Costs

Impairment

/

20102009

Not at Faculty level

48

Budget Management

49

Impact on Budgeting

Budgeting Minimal impact; budgets prepared at

summary fund levels

Reporting Fund codes that have been reclassified

as operating will be re-mapped

Fund Codes

Monthly management reports and nVision reports will contain consistent data; reconciliation no longer required

Reporting

Minimal impact on UNSW’s formal budget setting process

Commitment Control

50

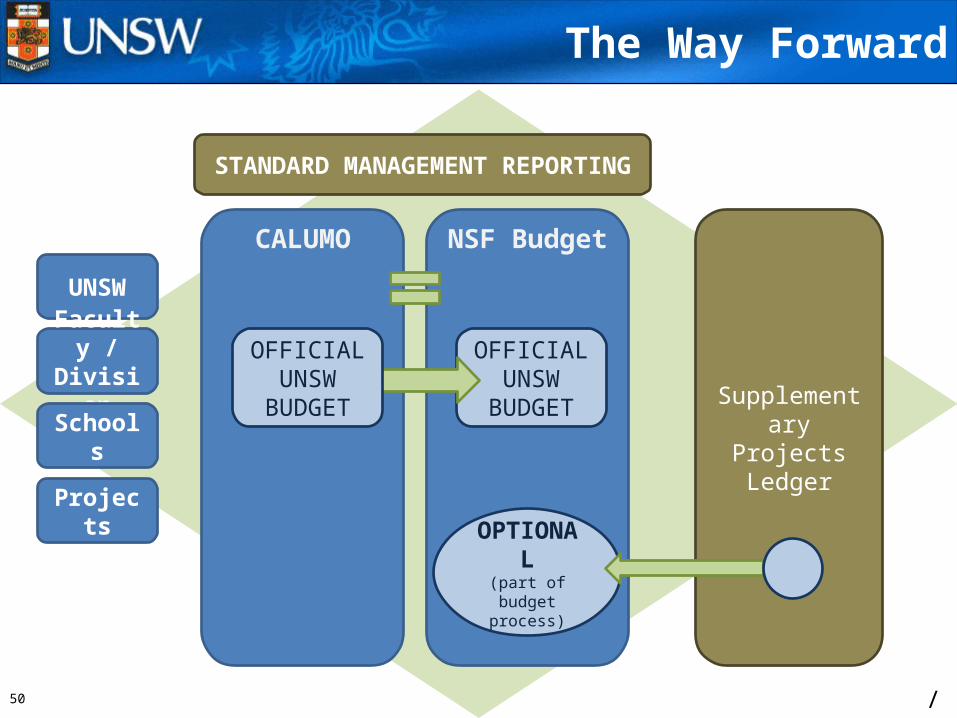

The Way Forward

/

OPTIONAL(part of budget

process)

UNSW

Faculty / Division

Schools

Projects

Supplementary Projects Ledger

OFFICIAL UNSW

BUDGET

STANDARD MANAGEMENT REPORTING

CALUMO NSF Budget

OFFICIAL UNSW

BUDGET

51

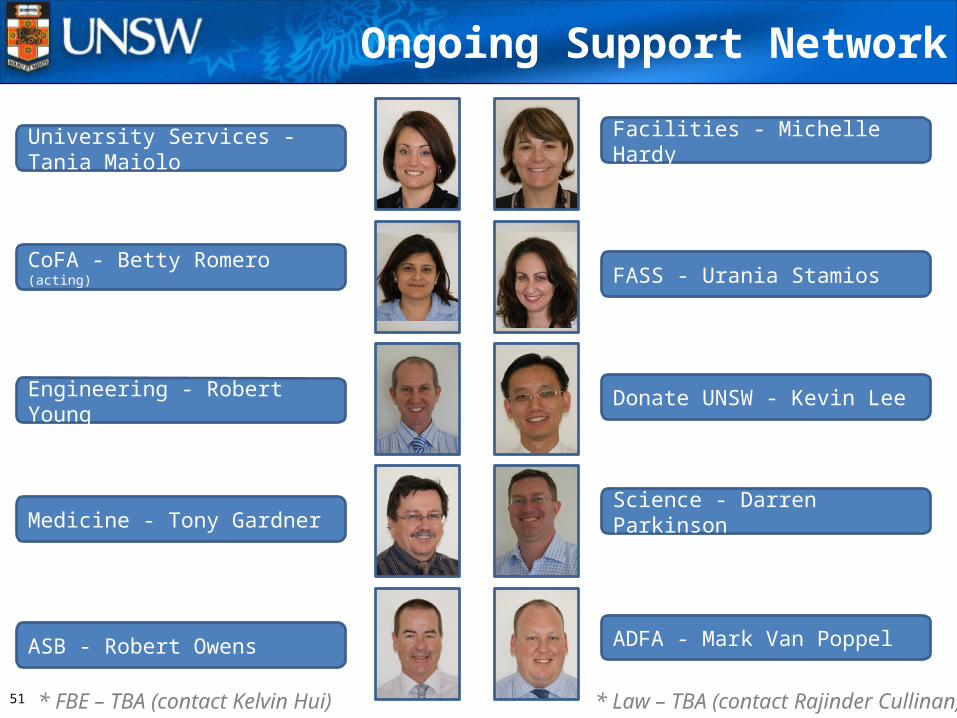

Ongoing Support Network

FASS - Urania Stamios

Science - Darren Parkinson

ASB - Robert Owens

Engineering - Robert Young

ADFA - Mark Van Poppel

Medicine - Tony Gardner

CoFA - Betty Romero (acting)

Facilities - Michelle Hardy

Donate UNSW - Kevin Lee

University Services - Tania Maiolo

* FBE – TBA (contact Kelvin Hui) * Law – TBA (contact Rajinder Cullinan)

52

Next Steps

• 1st of a series of informational briefings

• Reports are under development for release in early 2010

• Frequently Asked Questions to follow on website

• Future sessions are envisaged targetted at the specific needs of individual faculties / divisions

• Accounting Manual (including procedures)

• Get to know your Finance Managers

• Evaluation form

/

53

Any Questions?

Please start your questions with:

1. Your name

2. Your Faculty / Division

3. Your role

Grant CooleyDEPUTY DIRECTOR OF FINANCIAL CONTROL

54

Handouts

• AIFRS details summary

• 2010 nVision Report Wuick Reference Guide

• CoA Quick Reference Guide – Expense Accounts• CoA Quick Reference Guide – Revenue Accounts• CoA Revenue Accounts Summary of changes• CoA Revenue Accounts Detailed list of changes• Expense Accout Detailed list of changes

• Customer Service Charter

• Web Page

• Who Can Help

/