the greenhouse gas impact of exporting coal - sightline institute

TRANSCRIPT

The Greenhouse Gas Impact of Exporting

Coal from the West Coast An Economic Analysis

Dr. Thomas M. Power Executive Summary

As the use of coal to generate power in the United States has declined, coal companies have increasingly turned their attention to the export market, particularly the fast-growing economies of Asia, and particularly China. Because there currently is no infrastructure that would allow coal exports from the West Coast of the United States, the growing interest in export has led to proposals to build new private coal export terminals in Washington. The first two such projects are seeking permits for infrastructure that would allow close to 110 million tons of coal export annually. For context, burning 110 million tons of Powder River Basin coal is roughly equivalent to the annual carbon emissions of 40 million cars. These projects have generated intense local and state-wide controversy, particularly given Washington State’s historic leadership in setting progressive policies intended to address greenhouse gas emissions and their effect on the global climate.1

Proponents of the coal export terminals consistently claim that the decision to authorize them will have no effect on the total amount of coal that is burned globally, and hence on the global climate. In their view, opening up the West Coast to the export of Powder River Basin coal will only change the source of the coal burned in Asia—not the total amount. This white paper explains why these arguments are incorrect, and inconsistent with both the basic principles of economics as well as the abundant literature regarding energy use and consumption patterns in Asia. This paper concludes that the proposed coal export facilities in the Northwest will result in more coal consumption in Asia and undermine China’s progress towards more efficient power generation and usage. Decisions the Northwest makes now will impact Chinese energy habits for the next half-century; the lower coal prices afforded by Northwest coal exports encourage burning coal and discourage the investments in energy efficiency that China has already undertaken. Approving proposed coal export facilities would also undermine Washington State’s commitment to reducing its own share of greenhouse gas emissions.

• Coal exports from the Northwest mean lower prices and higher consumption in Asia. Opening the Asian import market to dramatic increases in U.S. coal will drive down coal prices in that market. Several empirical studies of energy in China have demonstrated that coal consumption is highly sensitive to cost. One recent study found that a 10 percent reduction in coal cost would result in a 12 percent increase in coal consumption. Another found that over half of the gain in China’s “energy intensity” improvement during the 1990s was a response to prices. In other words, coal exports will mean cheaper coal in Asia, and cheaper coal means more coal will be burned than would otherwise be the case.

1 United States Environmental Protection Agency, Coalbed Methane Outreach Program, Interactive Units Converter. http://www.epa.gov/cmop/resources/converter.html

1

• Prices now determine energy use for decades. Lower coal prices reduce the incentives to retire older, inefficient, coal-using production processes and discourage additional investments in the energy efficiency of new and existing coal-using enterprises. As those lower prices flow through to consumers, it also reduces the incentives to shift to more energy efficient appliances. Furthermore, lower coal costs will encourage investments in new coal-burning facilities in Asia—which in turn create a 30- to 50-year demand for coal.

• China responds to higher prices by improving efficiency. Concerns over rising energy costs have led the Chinese government to develop tighter energy efficiency standards throughout the economy. The rise in world oil prices, for example, led the Chinese government to announce strict five-year energy conservation goals including limiting the growth of coal consumption to about 4 percent per year, far below the expected expansion of the economy.

• Potential for energy efficiency remains largely untapped. Energy usage per unit of GDP across the Chinese economy is almost four times that in the United States and almost eight times that in Japan. The Chinese government and the large state-owned enterprises that produce, distribute, and use larger amounts of energy are well aware of the burden that high and rising energy cost can impose on the economy. The energy policies embodied in the last several five-year plans have focused heavily on improving overall energy efficiency in order to effectively control energy costs. Lowering coal costs to China would undermine these valuable energy efficiency efforts.

• Washington’s role in global greenhouse gas emissions. Washington State, like other West Coast states, has been a leader in reducing greenhouse gas emissions and supporting innovative projects to protect the climate. That leadership role is directly threatened by the proposed coal export terminals. A decision by Washington to play a key role in expanding coal use in Asia would also weaken the national and international drive to reduce global greenhouse gas emissions.

Energy use in Asia, and particularly China, is a highly complex issue, and there are many political, economic and cultural influences on the energy planning decisions that are made there. The decision as to whether to make available large volumes of coal from the Powder River Basin is, of course, not going to determine their total coal use. But neither is it correct to say that it will have no influence at all. To the contrary, building coal export terminals in Washington State and elsewhere on the West Coast will ultimately lower coal prices, increase coal consumption, and over the long term create incentives towards more coal use than would be the case if these terminals are not built. NOTE: This analysis focuses primarily on the expected net carbon emissions of coal exports to Asia, given the known dynamics of supply, price, and demand in coal and other markets. It does not address a variety of other factors that should be considered in evaluating the costs and benefits of coal export, including: the costs of human health and environmental impacts, economic impacts on other users of rail, port, and other capacity, impacts on communities due to environmental and logistical impacts, opportunity costs due to foreclosed economic opportunities, economic damages associated with accelerated climate change and toxic emissions, and others.

2

1. Export of Powder River Basin Coal through West Coast Ports Will

Reduce the Cost of Using Coal in Asia

There are currently two proposals pending in the Pacific Northwest to build new private ports: one in Longview, Washington (proposed by a Millennium Bulk Logistics, which is jointly owned by Ambre Energy and Arch Coal), and another being developed by SSA Marine (a Carrix company). The Millennium facility is expected to be able to ship up to 60 million tons of coal annually, and the SSA facility proposes to ship up to 48 million tons of coal. SSA has already signed an agreement with Peabody Energy, the world’s largest coal company, to export 24 million tons through the terminal 2 As discussed further below, there is ample reason to believe additional export terminals in Washington, Oregon, British Columbia and even Alaska will be proposed in the months ahead. To provide some context as to what 100 million tons of Powder River Basin coal represents in terms of greenhouse gas emissions, it is the equivalent to the annual carbon emissions of 40 million automobiles.3

In 2009, the total seaborne thermal coal sales to East Asia were 354 million tons.4 The East Asian5 thermal coal imports for 2010 are expected to rise to about 370 million tons.6 Most of those thermal coal exports to East Asia have previously come from Australia and Indonesia.7 Clearly, with just two of the proposed West Coast coal terminals expecting to export over a hundred million tons of coal, coal port proponents in the U.S. expect to make major inroads in East Asian markets, capturing a significant share of the seaborne thermal trade.

It is important to point out that while Japan, South Korea, and Taiwan almost exclusively rely on imports to provide the coal they consume, that is not true of China. China is the world’s largest coal producer and until recently was a net exporter of coal. China’s current imports, while quite significant in terms of East Asian seaborne coal trade, still represent a relatively small fraction (about 3% in 2009)8 of its total consumption. China currently is largely self-sufficient in terms of its coal consumption but still represents a substantial market for coal exporters.

Ambre, Arch, Peabody, and other western North American coal companies eyeing East Asian coal markets see the greatest growth potential in China. Projections for the growth in demand for thermal coal in Japan (previous to the nuclear crisis), South Korea, and Taiwan are quite modest or flat9. China’s consumption of coal, on the other hand, is projected to expand dramatically. Ambre, Arch, Peabody, and other western North American coal companies also hope to compete successfully with domestic Chinese sources of thermal coal in delivering coal to the coastal areas of China. China also has potential overland coal import opportunities from Russia and Mongolia that U.S. coal companies expect to undersell.

To be successful in competing with the current primary sources of coal in East Asia, Australia, and Indonesia, and from Chinese domestic sources, Millennium and SSA Marine’s investors and customers, like Arch Coal and Peabody

2 http://www.marketwatch.com/story/peabody-hopes-to-boost-us-coal-exports-2011-03-01 3 United States Environmental Protection Agency, Coalbed Methane Outreach Program, Interactive Units Converter. http://www.epa.gov/cmop/resources/converter.html4 The combined steam coal imports of Japan, China, South Korea, and Chinese Taipei. http://www.worldcoal.org/coal/market-amp-transportation/ 5 This testimony will focus on East Asian coal markets, primarily Japan, South Korea, Taiwan, and China. India’s coal production, consumption, and imports is not the focus because of India’s distance from U.S. West Coast ports. South African coal fields are much closer to India. 6 This number comes from the rate of growth projected by EIA in Asia from 2009-2010 applied to the worldcoal.org number stated earlier. http://www.eia.doe.gov/oiaf/ieo/coal.html 7 http://www.eia.doe.gov/cabs/Australia/Coal.html (Australia) http://www.eia.doe.gov/cabs/Indonesia/Coal.html (Indonesia) 8 China consumed 3.5 billion short tons of coal in 2009 and produced 3.4 billion tons. http://www.eia.doe.gov/cabs/China/Coal.html 9 “The countries of non-OECD Asia account for 95 percent of the projected increase in world coal consumption from 2007 to 2035” http://www.eia.doe.gov/oiaf/ieo/coal.html

3

Energy, will have to be able to deliver coal at a lower price, deliver coal that is less costly to use, or in some other way reduce the importing country’s coal costs.

Thus far, U.S. coal companies have emphasized to their investors that they believe that they can deliver western U.S. coal to East Asia more cheaply than Australia can and more cheaply than northern and western domestic Chinese coal can be delivered to China’s southeastern coastal population and industrial centers. U.S. coal producers expect to under-bid existing East Asian supplies and reap significant profits.10 Of course, Ambre Energy, Arch Coal, and Peabody Energy will not be the only western North American coal companies seeking to enter the East Asian coal market and compete for a significant market share. The Port Metro Vancouver (British Columbia) terminals are planning significant expansions as is the Ridley Terminal in Prince Rupert, British Columbia, to serve East Asian countries with coal. Alaska coal mines are planning expansion including the building of new coal ports to serve the same markets.

Millennium and SSA Marine will be competing not only with existing Australian and Asian sources of coal but also with other North American sources of coal. This competition will drive the cost of coal to East Asian countries, including China, downward. The handsome profit margins on coal exports to East Asia that western U.S. coal companies are currently calculating, based on competing only with existing Asian sources of supply, will be squeezed by competition among North American coal companies to gain market share in East Asian thermal coal markets as competing companies cut their prices.

This result--that international competition to serve particular import markets will lower the prices that the importing countries have to pay--should not be startling. One of the major benefits of international trade is that it allows countries access to lower cost sources of supply.11

Competition to serve coal import markets does not only take place on the basis of price. Competition can also take place on the basis of coal quality. The differences in the heat content of different coals can be taken into account by calculating the cost of the coal per million BTUs rather than per ton. The impurities in the coal that may be released during combustion are also likely to be quite important since air quality regulations restrict emissions of sulfur and mercury to protect human health and biological systems. Emission control technologies can be installed to reduce such emissions but that equipment is costly and its operation reduces the net efficiency of the coal-fired system. Often those costs of using coal can be reduced by burning coal low in the contaminants of concern or blending highly contaminated coal with less contaminated coal. Those emission control concerns have put a premium, for instance, on low sulfur coal such as the Powder River Basin produces.

In that sense, PRB coal can help reduce the cost of meeting air quality standards in Asia and hence lowering the cost of operating those coal-fired facilities. Burning PRB coal or blending it with domestic Asian sources may especially lower the emission control costs of older coal-fired electric generating and other industrial facilities, allowing them to continue to operate when, in the absence of PRB coal, there may be pressure on such facilities to close. Since such plants often have much lower fuel efficiency, this may have implications for carbon emissions.

The primary use of thermal coal in Asia is to fuel electric generators. Electricity, by its nature, is not easily stored. It has to be produced as needed. Electric delivery grids have to keep electric supply and electric demand in balance almost second by second. This puts a very high premium on the reliability of electric generating plants. For coal-fired generators, this means that the reliability of coal supply is also important. Because of its bulk, coal is costly to store. Typically coal supply is maintained by almost continuous deliveries of coal. The reliability of those deliveries is important.

10 Platts Energy Week, Coal Trader, December 6, 2010, “Peabody projections show lucrative Chinese market for PRB coal,” Regina Griffin; December 15, 2010, “Coal terminal challenge seen as a test case for West Coast ports, Peter Gartrell. 11 “Cost” here is being used to refer to the private commercial cost that is paid. The impact of international trade on social costs, including environmental costs is more complex and a source of controversy.

4

As the recent torrential rains and flooding in Australian coal fields dramatized, unexpected events can disrupt particular coal sources putting the stream of delivered coal at risk. One way of reducing the costs associated with interrupted supplies is to draw on a variety of different supplies. Such geographic diversity of supply can help minimize the costs associated with supply disruption.

The huge production potential of the PRB coal fields is an attractive feature of that coal source to East Asian customers. It helps them diversify their coal supply and reduce the costs of relying on coal as a fuel. The Millennium and SSA Marine coal export terminals in Washington can contribute to the reduction in the cost of coal to East Asian customers in that sense too.12

The conclusion I draw from this analysis is that the PRB coal exports facilitated by the proposed coal ports will reduce the price of coal to Asian markets, the cost of using coal there, and the long-term price and supply risks that planners take into account when making long-term energy infrastructure investment decisions. Coal export will encourage the continued, rapid expansion of coal-fired electric generation capacity. Consequently, as I discuss in Section 6 below, the impacts of coal export will be much larger than the annual capacity of the port facilities would suggest, because it will encourage investments in new coal-burning facilities in Asia and their associated 30-50 year combustion of coal.

2. Coal Export from the Powder River Basin Will Increase Coal

Consumption in Asia

Lower coal prices and lower costs of using coal, in general, encourage higher levels of consumption while higher prices and costs discourage consumption. That is why demand curves depicting how price influences the quantity demanded are drawn sloping down to the right. In that context, the downward pressure of the proposed coal export facilities will put on Asian coal prices and costs would lead to levels of coal consumption above those that otherwise would exist.

In the past some have suggested that when it comes to energy, there is an exception to this typical response of the quantity demanded to changes in price. One asserted reason for energy use not being sensitive to changes in price is that energy is a necessity for economic activity and, even, human survival, with no alternatives or substitutes available. Such objections may have some validity in the very short run but are in error when a longer time frame is considered.

The sensitivity of the level of use of a primary input to an industrial process to changes in price or cost depends on the flexibility of that production process. Consider electric generation. For any given coal-fired electric generator, coal consumption is largely proportional to electric generation. A certain amount of coal is necessary for any given level of output. Changes in the cost of the coal cannot change that physical relationship. Higher or lower coal costs would raise or lower the cost of producing electricity and that could lead to higher or lower electric prices. Electric customers could change their electric usage in response, but electric customers might also be locked into using electricity in a particular pattern by the electric appliances they own and depend upon: cooking, water heat, clothes washing and drying, home heating, computers, entertainment, etc.

The way that energy-using technology in-place significantly dictates the level of energy consumption, making that energy use a “necessity” not easily adjusted can significantly reduce the sensitivity of energy usage to changes in price or cost. These potential short run constraints on coal or electric use in response to price changes can be contrasted with what was once a common situation where industrial plants dependent on process heat had the capability of using

12 For a discussion of the value of diversity of supply and the role that PRB coal can play in that regard in Asian markets see “PRB coal could provide diversity”, Paul McAfee, Inside Coal, Issue #233, February 23, 2011, p. 2,

5

any one of several fuels, e.g. natural gas, fuel oil, residual oil, biomass. In that setting, a change in the relative price of one of the fuels could lead to a quick substitution of one fuel for another.

The fact that technology in place can often dictate energy usage because there is little flexibility other than increasing or decreasing production, does not mean that energy use, in general, is insensitive to price changes. It simply means that the impact of price changes is likely to work through the adjustment in the technology deployed and that adjustment in technology cannot take place instantaneously. In the short run, meaning until adjustments can be made in the technology deployed, energy usage may be relatively insensitive to price changes, but in the longer run the technology deployed will adjust to relative prices, and with that technology adjustment, energy usage will adjust.

Some have also expressed doubts about the sensitivity of energy use to energy prices based on a casual overview of American energy consumption habits over the last forty years when, despite ongoing increases in energy prices, Americans adopted more energy intensive technologies such as larger motor vehicles and a larger number of energy-using electronic appliances. That sort of casual empiricism misunderstands what is meant by economic demand. Economic demand refers to the determinants of the level of consumption of any given product. Price is not the only determinant of our level of consumption. Price is an important determinant but just one of several. Other important determinants are the level of income, tastes and preferences, and technological developments. While higher prices depress demand, higher incomes increase demand. It is always possible that the impact of higher incomes will swamp the impact of higher prices and lead consumption to rise despite the higher prices. The important point, however, is that even when that happens, the higher price will have reduced consumption below what it would otherwise have been if price had been constant but the rise in income had been the same.

In addition, it is important to measure price changes in terms of monetary units of constant purchasing power. That is, the effect of general price inflation has to be removed. Because inflation makes the price of almost everything steadily rise as the purchasing power of the dollar shrinks, that purely inflationary trend has to be removed so that prices can be stated in terms of dollars of constant purchasing power. When that is done, the apparent trajectory of energy prices can change significantly. Rather than seeing energy prices constantly rising, we find that energy prices periodically rise steeply in real terms but then go through long periods during which they are actually declining in terms of the purchasing power we sacrifice to buy them.

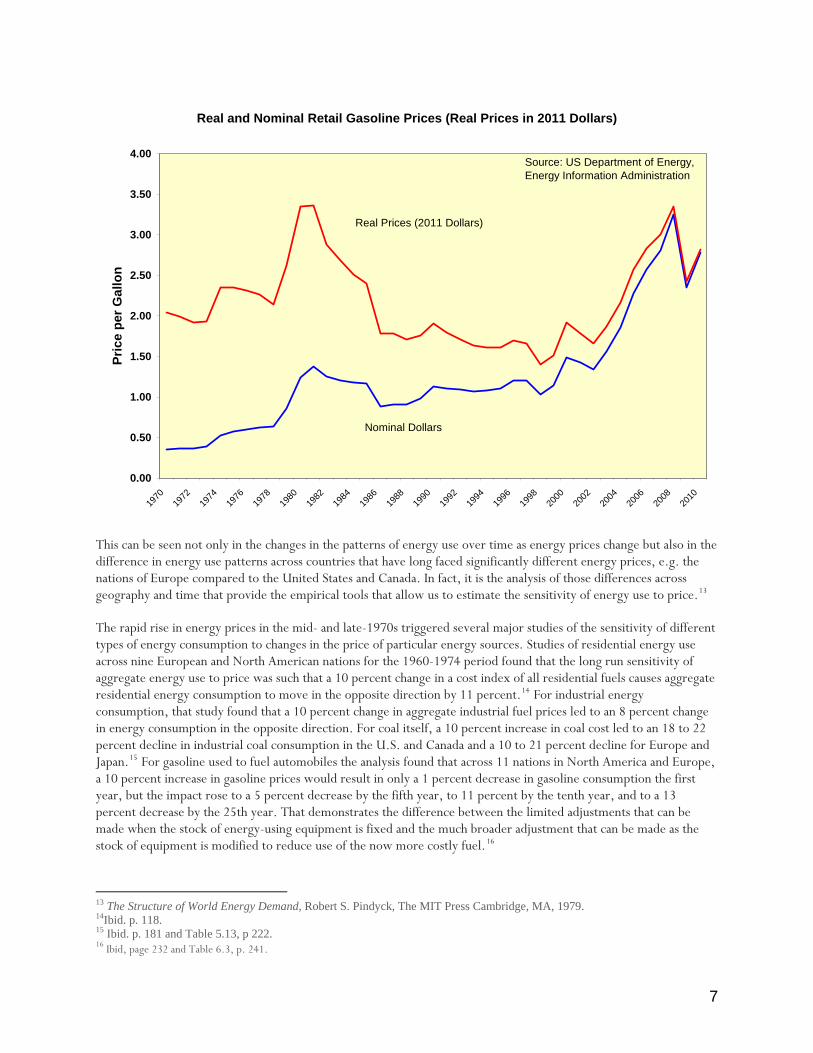

If, for instance, we look at retail gasoline prices in nominal terms, with some fluctuations, gasoline prices rose significantly between 1970 and 2008. Immediately after the price shock of the late 1970s, Americans did turn to smaller cars to reduce fuel expenditures. Note the deployment of a different technology to allow that adjustment. But then Americans turned back to larger vehicles, beginning with the minivan and then SUVs and finally truck-like vehicles. It would be easy to argue that Americans were ignoring the price of gasoline. But between 1981 and 1998 gasoline prices in real terms fell dramatically. In 1998 real gasoline prices were lower than they had ever been in the twentieth century and 60 percent below the peak prices of 1981. Real gasoline prices remained below those peak levels until 2008. The steep rise in real gasoline prices in the 2000s renewed Americans’ interests in more fuel efficient cars, including hybrids, diesels, and smaller conventional cars. Prices mattered, but those prices have to be expressed in terms of constant purchasing power to see that. See the figure below.

In order to accurately observe adjustments in the use of energy to changes in energy prices, we must look beyond the very short run when technology locks in usage; we must statistically isolate the effect of price changes from the effect of changes in income, technology, tastes, etc.; and we must measure energy prices after general inflation has been removed from them. When that is done, empirical analysis of energy usage over the last four or more decades documents that energy consumption is in fact sensitive to price: higher prices or costs decrease consumption while lower prices or costs increase energy consumption.

6

Real and Nominal Retail Gasoline Prices (Real Prices in 2011 Dollars)

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

Pric

e pe

r Gal

lon

Real Prices (2011 Dollars)

Nominal Dollars

Source: US Department of Energy, Energy Information Administration

This can be seen not only in the changes in the patterns of energy use over time as energy prices change but also in the difference in energy use patterns across countries that have long faced significantly different energy prices, e.g. the nations of Europe compared to the United States and Canada. In fact, it is the analysis of those differences across geography and time that provide the empirical tools that allow us to estimate the sensitivity of energy use to price.13

The rapid rise in energy prices in the mid- and late-1970s triggered several major studies of the sensitivity of different types of energy consumption to changes in the price of particular energy sources. Studies of residential energy use across nine European and North American nations for the 1960-1974 period found that the long run sensitivity of aggregate energy use to price was such that a 10 percent change in a cost index of all residential fuels causes aggregate residential energy consumption to move in the opposite direction by 11 percent.14 For industrial energy consumption, that study found that a 10 percent change in aggregate industrial fuel prices led to an 8 percent change in energy consumption in the opposite direction. For coal itself, a 10 percent increase in coal cost led to an 18 to 22 percent decline in industrial coal consumption in the U.S. and Canada and a 10 to 21 percent decline for Europe and Japan.15 For gasoline used to fuel automobiles the analysis found that across 11 nations in North America and Europe, a 10 percent increase in gasoline prices would result in only a 1 percent decrease in gasoline consumption the first year, but the impact rose to a 5 percent decrease by the fifth year, to 11 percent by the tenth year, and to a 13 percent decrease by the 25th year. That demonstrates the difference between the limited adjustments that can be made when the stock of energy-using equipment is fixed and the much broader adjustment that can be made as the stock of equipment is modified to reduce use of the now more costly fuel.16

13 The Structure of World Energy Demand, Robert S. Pindyck, The MIT Press Cambridge, MA, 1979. 14Ibid. p. 118. 15 Ibid. p. 181 and Table 5.13, p 222. 16 Ibid, page 232 and Table 6.3, p. 241.

7

A study focused specifically on the use of coal as an energy source in the United States was published in 1986.17 The sensitivity of coal use by electric utilities in the U.S. to changes in price was estimated to be such that a 10 percent increase in coal costs would result in a 4 to 5 percent decline in coal use in the short run and a 6 to 9 percent decline in use in the long run.18 These estimates were compared to earlier estimates for U.S. industrial use of coal that found the adjustment to a 10 percent increase in coal cost to range from a 6 to a 22 percent decline in coal consumption.19

The U.S. Department of Energy funded a review of all of the studies that had been done of the sensitivity of American energy usage to energy prices as of 1993. That analysis was done to support the development of the National Energy Modeling System, the energy modeling system that the Energy Information Administration continues to use and develop today. For coal the conclusions of this 1993 review were similar to the 1978 and 1984 reviews: a change in the price of coal would have an impact on coal consumption in the opposite direction that would be about the same size in percentage terms, possibly a little smaller, possibly a little larger. 20

In more recent years, energy research has focused on the use of petroleum products in the U.S. A study published in 2010 focused on the important role played by changes in oil prices relative to previous maximum prices as opposed to fluctuations up and down between relatively high prices. It found that a 10 percent increase in price over a previous maximum led to a 15 to 19 percent decline in petroleum consumption in the long run.21

A recent study of the sensitivity of coal use to price changes in China estimated that a 10 percent change in coal cost resulted in a 12 percent change in coal consumption in the opposite direction.22 An earlier study of the sensitivity of Chinese coal consumption to price estimated a smaller change in coal consumption attributable to a 10 percent change in coal cost: 6 percent.23 A study of the decline in the energy intensity (or a rise in energy productivity) within the Chinese economy in the 1990s concluded that over half of the measured decline in energy intensity was a response to rising energy prices. Research and development activity, shifts in the structure of the Chinese economy towards less energy intensive sectors, and improvements in management incentives were each responsible for less than a sixth of the decline in energy intensity.24 Energy prices have important economic consequences, even in a nation such as China where the government still exercises considerable control over those prices.

There is nothing startling or controversial about these results. Price and cost matter. Lower prices and costs encourage consumption. Higher prices and costs discourage consumption.

17 Coal in Appalachia: An Economic analysis, Curtis E. Harvey, Lexington, KY: University Press of Kentucky, 1986. 18 Ibid.Table 15, p.156. 19 Ibid. Table 14, p. 155. 20 “A Survey of Energy Demand Elasticities in Support of the Development of the NEMS, C. Dahl, Contract No. DE-Apo1-93EI23499 (Washington, DC, October 1993), pp. 60-63.http://mpra.ub.uni-muenchen.de/13962/. 21 “Short- and long-run adjustments in U.S. petroleum consumption,” Hillard G. Huntington, Energy Economics 32(2010):63-72. 22 “The structural break and elasticity of coal demand in China: empirical findings from 1980-2006, Jiao, J-L, Fan, Y. and Wei, Y-M, International Journal of Global Energy Issues 31(3/4):331-344, 2009, p. 340.. 23 China’s energy economy: Technical Change, factor demand and interfactor/interfuel substitution,” Hengyun Ma, Les Oxley, John Gibson, Bonggeun Kim, Energy Economics 30 (2008): 2167-2183Table 5, p.2179. 24 “Technology development and energy productivity in China,” Karen Fisher-Vanden, Gary H. Jefferson, Ma Jingkui, and Xu Jianyi, Energy Economics, 28 (2006): 690-705, pp. 695-696 and Table 1. It should be pointed out that after 2002 the energy intensity of the Chinese economy began to increase as production in energy intensive industries such steel, aluminum, paper, chemicals, cement, etc. grew rapidly.

8

3. China’s Consumption of Coal Responds to Changes in Coal Prices and

Costs

The Chinese energy market responds to changes in coal prices. Although past research indicated that the Chinese energy market was insulated from traditional price pressures due to the role of centralized Chinese planning, this is no longer the case.

3.1 Old Studies of Chinese Energy Markets Claim the Market was Insulated from Price

Pressures

A recent paper argued that reducing the price of coal or the cost of using coal in China might have little impact on the consumption of coal in China due to the role of central planning, which makes prices and costs largely irrelevant. In other words, since China remains politically dominated by the Chinese Communist Party and its strategic direction is guided by periodic five-year plans developed by the Chinese government, it might seem plausible to argue that changes in prices are largely irrelevant to resource use decisions in China.

For example, one recent analysis of Chinese energy consumption and future energy imports concluded “it is not helpful to use data on fuel prices as an input into a forecast study. Market signals appear to have had little effect on Chinese energy use and related investment. Chinese energy prices are administered and, though there have been some efforts at deregulation, so far they do not reflect underlying market scarcities.”25 The citation in support for this assertion was to a 2005 report from the Foreign Policy Centre in London on “Energy and Power in China.” That report asserted that “the current [Chinese] energy regulatory system is characterized by…[p]rice signals that have negligible effect on consumer behavior and investment…”26

However, both of these recent studies were tied to analysis of Chinese data and conditions before 2003 and were focused heavily on petroleum products over which the Chinese government has exerted fairly strict price controls. Given the changes that have taken place in Chinese energy policy over the last decade and our focus on coal, which has been partially exposed to market pricing for many years, the quotes above about the irrelevance of energy prices in China appear to be misleading assertions if applied to the second decade of the twenty-first century.

3.2 The Role of Energy Prices in the Chinese Economy

As pointed out in the previous section, empirical studies of the consumption of coal and other energy sources in China have demonstrated that coal consumption is sensitive to the cost of coal. Also as pointed out above, analysis of the decline in the energy intensity of the Chinese economy during the 1990s estimated that over half of that improvement in energy productivity was a response to the increases in energy costs. As that latter study concluded:

“In particular, rising energy prices and technology development activity are the principal determinants of gains in energy efficiency.” But that technology development may also be driven by energy prices: “Very preliminary results involving the interaction of technology development expenditure and energy prices suggest that rising energy prices may be motivating the innovation and deployment of energy-saving

25 “Modeling and forecasting energy consumption in China: Implications for Chinese energy demand and imports in 2020,” F. Gerard Adams and Yochanan Schachmurove, Energy Economics 30 (2008), pp. 1265-6, citation excluded. 26 “Energy and Power in China: Domestic Regulation and Foreign Policy,” Angie Austin, Foreign Policy Centre, London, UK, April 2005.

9

technologies as well as motivating substitutions of capital and labor for energy within a static, short-run context.”27

In addition, recent studies of the relationship between the prices of various energy products in China indicate that movements in energy prices demonstrate the correlations that one would expect if national and regional markets were coordinating the production and sale of those energy products. The study looked to see, for instance, whether gasoline and diesel prices moved together as well as coal and electric prices. In addition it looked to see if common prices emerged for each of these products within particular geographic areas, indicating that market exchanges were creating a uniform price. The analysis focused on the 1995-2005 time period and found that by 1997-1999 gasoline and diesel prices were moving together and that by 2002-2005 so were coal and electric prices. By the end of the period all four energy prices were behaving as if there were integrated energy markets in operation in China.28

This is not surprising. China abandoned fully state-controlled energy prices in the reforms of the late 1970s and 1980s. Under those reforms only energy prices within state planned industries were controlled while energy prices to other enterprises were left to the market. One result was that an increasing portion of total coal produced was produced by small town and village enterprises sold at market determined prices. In 1978 only 15 percent of Chinese coal production came from these small firms. By 1997 over half of total national coal production came from these small mines, guided by market forces rather than central planners.29 By 1997 even coal producers selling to electric generators were allowed to bargain with the electric firms to determine coal sale prices. The result was that coal prices increased sharply, and the regulated price of electricity had to be regularly adjusted to reflect the cost of building and operating those power plants. As a result, electric prices rose too.30 In that sense, familiar market forces were determining coal and electric prices even if the government was seeking to smooth those price adjustments and avoid what it perceived to be disruptively volatile prices.

Chinese economic planners may have had legitimate concerns about the highly decentralized and fragmented Chinese coal industry and the consequences in terms of efficiency, safety, environmental impacts, and market price volatility. While a few large coal mining companies have come to dominate the U.S. industry, in the early 2000s there were 81,000 coal mining companies in China. This was reduced to about 25,000 by 2003 and 15,000 by 2009 as a smaller number of large coal enterprises were encouraged to consolidate Chinese coal production into larger, more efficient, safer, and less polluting coal mines. By 2008, 268 such large, high-efficiency, mines out of about 15,000 total mines, were responsible for a third of total Chinese coal production.31 Besides this horizontal consolidation, the Chinese government also encouraged vertical integration between coal mines and electric generation as well as coal mines, rail transportation, and other coal-intensive industries in order to lessen the impact of volatile coal market prices on major industries.32

Coal buyers in China also have indicated that coal prices affect their coal sources. Electric generation firms have to negotiate with coal producers over quantity and price wherever they operate in China. In addition, coal buyers in China’s major urban and industrial centers on China’s southeast coast, where much of the industrial manufacturing is located, have access to foreign sources of coal, e.g. Indonesia, Australia, and Vietnam. Coastal Chinese coal buyers can compare the cost of coal delivered from domestic sources in the north and west of China against the cost of delivered coal from available foreign sources. If rising market prices for domestic coal and the transportation costs to

27 Op. cit. Fisher-Vanden et al., “Technology development and energy productivity in China,” pp. 700-701. 28 “The integration of major fuel source markets in China: Evidence from panel and cointegration tests,” Hengyun Ma and Les Oxley, Energy Economics, 32(5): 1139-1146. 29 “Remaking the World’s Largest Coal Market: The Quest to Develop Large Coal-Power Bases in China,” Huaichuan Rui, Richard K. Morse, and Gang He, Program on Energy and Sustainable Development, Working Paper #98, December 2010, p. 6-7. 30 Ibid. pp. 1140-1141. 31 “Understanding the Chinese Coal Industry,” Syd S. Peng, Coal Age, 115(8):24-29, August 2010. 32 “Remaking the World’s Largest Coal Market: The Quest to Develop Large Coal-Power Bases in China,” Huaichuan Rui, Richard K. Morse, and Gang He, Program on Energy and Sustainable Development, Working Paper #98, December 2010; “Understanding the Chinese Coal Industry,” Syd S. Peng, Coal Age, August 26, 2010.

10

deliver it to the southeastern coast rise too high, coastal coal buyers can turn to foreign sources. That appears to be exactly what they did in 2009 and have continued to do through 2010. While foreign sources of coal were “out of the money” relative to domestic Chinese sources in 2008, by late 2009, Indonesian coal was as much as $40 per ton cheaper than delivered domestic Chinese coal. Australian coal, with a longer transportation path, was as much as $29 per ton cheaper. As a result, coal imports into China skyrocketed, and that continued into 2010. As one analysis of that surge in imports put it “We conclude China’s coal buying behavior follows the logic of a ‘cost minimizer’…” Chinese coal imports are simply tied to a comparison of the delivered cost of coal to these southern coastal cities from alternative sources of supply.33

Even within a government planning framework where the government controls some prices, those administered prices can be designed to reflect costs and control demand. Electric prices have continued to be set by economic planners in China. But the pricing strategy often has been similar to what economists have urged in developed market economies. The Foreign Policy Center report quoted above as saying that energy prices in China had negligible impacts on energy consumption and investments also pointed out that beginning in 2004 the Chinese government has used electric price increases in order to dampen surging demand and prevent power shortages. Prices during peak demand periods have been increased in many Chinese economic centers while reduced prices were used to encourage off-peak power usage. The loads placed on the electric grid by electric-intensive industries have also been restricted by higher electric demand charges as well as placing limits on the loads those industries can place on the grid. In regions dependent on hydroelectric facilities, the government varies electric prices between wet and dry seasons, charging lower rates when electricity is plentiful and higher rates when that hydroelectric production declines during the dry season.34

Concerns over rising energy costs have also led the Chinese government to develop tighter energy efficiency standards throughout the economy. The rise in world oil prices in response to the unrest in North African and Mideast countries in early 2011, for instance, led the Chinese government to announce strict five-year energy conservation goals aimed at limiting the growth of coal consumption to about 4 percent per year, far below the expected expansion of the economy.35 This expected change in the five-year plan represents a shift away from just targeting an overall reduction in the energy used per unit of output produced toward actually imposing a cap on coal use. Last year, in order to meet the previous five-year plan target of reducing the energy intensity of the economy by 20 percent, the Chinese Premier vowed he would use an “iron hand” to enforce compliance. He followed through with relatively drastic measures such as ordering inefficient production lines to shutdown at more than two thousand factories.36

Even what appear to be economically irrational pricing policies by the Chinese government can create incentives that improve the efficiency and productivity of production processes. When the government abandoned controls on coal prices but retained controls on electric prices, the electricity firms saw their profits squeezed by rising coal costs that they could not pass forward to customers. Analysts studying this serious contradiction between market forces and central planners’ prices point out that managers of the electric generators offset some of the coal cost increases by tightening up cost control and enterprise efficiency within the electricity sector. They also point out that once the government allowed electric prices to rise with coal costs, those higher coal and electricity prices encouraged optimizing behavior by firms that improved the efficiency with which energy resources were used.37

33 “The World’s Greatest Coal Arbitrage: China’s Coal Import Behavior and Implications for the Global Coal Market,” Richard K. Morse and Gang He, Program on Energy and Sustainable Development, Stanford University, Working Paper No. 94, August 2010. 34 Op. Cit. “Energy and Power in China,” Angie Austin, 2005. 35 Zhang Guobao, China’s recently retired longtime energy czar was quoted by the New York Times as saying that coal consumption would be restricted to growing from the 3.2 billion tonnes in 2010 to only 4 billion tonnes by 2015. New York Times, March 4, 2011, Keith Bradsher, “China Reportedly Plans Strict Goals to Save Energy.” 36 Ibid. 37 “Economic analysis of coal price-electricity price adjustment in China based on the CGE model,” Y.X. He, S.L. Xhang, L.Y. Yand, Y.J. Wang, and J. Wang, Energy Policy 38 (2010): 6629-6637.

11

4. China Has Tremendous Potential to Reduce Dependence on Coal, but

Coal Exports from the U.S. Will Reduce Incentives to Capture that

Potential

4.1 Chinese Efforts to Improve the Energy Efficiency of the Economy38

The Chinese government and the large state-owned enterprises that both produce, distribute, and use larger amounts of energy are well aware of the burden that high and rising energy costs can impose on the overall economy and the viability and success of individual enterprises. The energy policies embodied in the last several five-year plans have focused heavily on improving overall energy efficiency in order to effectively control energy costs.

Like energy planners within government as well as within autonomous enterprises around the world, Chinese energy planners do not simply arbitrarily “make up” their energy efficiency targets. Rather they look at energy costs and the costs of implementing and operating different energy-using technologies and pursue the most cost-effective measures currently available. The value of the energy cost savings (along with potential environmental, health, and safety benefits) are weighted against the cost of the efficiency improvements. In that sense energy costs (including external social costs) drive the investment in efficiency.

Past Chinese efforts to improve the energy efficiency of the economy have focused on:39

• Boosting the energy efficiency of coal-fired electric generation by building larger generating plants with more fuel efficient conversion of fuel into electricity, retrofitting older power plants, and shutting down small thermal plants with low thermal efficiency. These efforts reduced the coal used per kwh generated by almost a quarter between 1978 and 2008.

• Increasing the energy efficiency of the electric transmission and distribution system resulting in almost a 30 percent reduction in line losses over the same time period.

• Consolidating coal mining into larger enterprises that can make use of safer and more energy- and coal-efficient technologies.

• Shutting down outdated production lines in major energy-using industrial sectors including, besides electricity and coal, steel, cement, non-ferrous metals, paper, and coke. Steel production in China, for instance, uses two to three times as much coke per ton of steel produced than the rest of the world and releases disproportionately larger volumes of greenhouse gases as a result.40 That is one of the reasons efforts are being made to close the many older, smaller, and less efficient steel production facilities.

38 For a discussion of recent energy efficiency efforts and the potential yet to be realized written by researchers from both Chinese and American energy research laboratories see “Integrated resource strategic planning in China,” Zhaoguang Hu et al., Energy Policy 38 (2010): 4635-4642. 39 Ibid. 40 “China’s steel Industry: An Update,” Yu, Hong and Yang, Mu, Energy Information Administration Background Brief No. 501,, U.S. Department of Energy, Jan 14, 2011.

12

4.2 The Remaining Potential for Improving the Chinese Energy Efficiency

The cost-effective energy-saving potential within the Chinese economy, however, remains largely untapped. Energy usage per unit of GDP across the Chinese economy is almost four times that in the United States and almost eight times that in Japan.41 See the figure below. Note the dramatic improvements between 1980 and 2000 and the deterioration since then. A return to a declining energy intensity path could “fund” much of China’s economic expansion.

Energy Intensity (Total Primary Energy Consumption per Dollar of GDP)

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

1980 1985 1990 1995 2000 2005

Year

Btu

per

(200

0) U

.S. D

olla

rs U

sing

Mar

ket E

xcha

nge

Rat

es

China

U.S.

Japan

Analysis of the energy efficiency of the relatively small Chinese Township and Village Enterprises indicates that for four energy intensive industrial sectors (brick making, metal foundries, coke-making, and cement manufacturing), the per unit average energy use was 30 to 60 percent higher than in their larger counterparts within China’s state-owned enterprise sectors. Those state-owned enterprises, themselves, had much higher energy use than in developed countries and some developing countries.42

Clearly there is massive room for improvements in energy efficiency.43 One analysis by energy analysts within and outside of China noted that in the very areas where the Chinese government has been concentrating its attentions, reductions in the energy intensity of the economy and the environmental impacts associated with energy production

41 EIA International Energy Annual 2006, Table E.1g, World Energy Intensity, Total Primary Energy Consumption per Dollar of Gross Domestic Product. In Op. cit. “Energy and Power in China,” Angie Austin, 2005, p. x, it is asserted that Chinese energy intensity is five times that in the U.S. and twelve times that in Japan. 42 “A model approach for analyzing trends in energy supply and demand at country level: Case study of industrial development in China,” Sergio M. Miranda-da-Cruz, Energy Economics 29(2007):913-933, p. 923. 43 Life-cycle energy consumption and greenhouse gas emissions for electricity generation and supply in China,” Xunmin Ou, Yan Xiaoyu, and Xiliang Zhang, Applied Energy 88(2011):298-297, p. 295.

13

and use present substantial opportunities for additional efficiency gains.44 In addition there is substantial energy savings potential on the customer demand side. Those opportunities would sound familiar to anyone who has worked on energy efficiency issues in the United States: a more substantial shift from incandescent to fluorescent lamp and from induction ballasts with electronic ballasts in those fluorescent lamps; improvements in the efficiency of electric appliances including refrigerators, television sets, and air conditioners; peak demand shaving measures that shift loads that contribute to short duration peaks. Such shifting of loads in time both reduces the need for additional electric capacity while serving those loads with base-load generators that operate with higher energy efficiency.45

4.3 Conclusion

Chinese energy producers, users, and planners do not ignore energy prices and costs. In particular, coal prices and costs matter: They influence the quantity of coal consumed. When coal costs are high and/or rising they increase the incentive to find ways of reducing coal costs. This leads to improvements in the efficiency with which coal is used through better management and investments in new technology. When higher coal costs are passed on in the price or cost of products produced using coal, there is also an incentive to reduce the use of those products by reducing waste and finding less coal-intensive substitutes. Higher coal costs also lead government planners to act to limit the impact of those higher costs on the overall economy by tightening energy efficiency standards, adjusting energy pricing, and increasing conservation targets.

With higher incomes and a more urbanized population, planners are also emphasizing the need for the Chinese economy to shift away from over-reliance on energy intensive heavy industry and towards the provision of services to businesses and citizens. This broadening of the structure of the Chinese economy would also reduce the energy intensity of the GDP while focusing more on Chinese citizens’ needs. It could also reduce the vulnerability of the Chinese economy to international business cycles.

Lowering the price of coal or the cost of using it in China has the opposite impact: It encourages higher levels of coal use than otherwise would exist. It reduces the incentives to retire older, inefficient, coal-using production processes. It reduces the justification for additional investments in the energy efficiency of new and existing coal-using enterprises. As those lower prices flow through to consumers, it also reduces the incentives to purchase more energy efficient appliances as well as reducing the range of energy efficient appliances available.

5. PRB Coal Exports Will Not Reduce U.S. Coal Consumption Significantly

Because national and international coal markets are linked, a theoretical argument could be made that Chinese purchases of PRB coal involve an implicit competition between China and existing American buyers of PRB coal for that coal. Such competition could drive up the domestic price of coal in the United States. In addition, expanding coal production in the PRB could involve developing more costly coal deposits, i.e. those that are thinner, deeper, have more overburden to remove, or are of poorer quality in terms of energy content and/or the presence of contaminants. If that were the case, the domestic cost of using that coal in the United States might also rise. Such increases in coal prices and costs could be expected to discourage coal consumption in the United States just as the downward pressure on coal prices in China encourages increased consumption. That is, reduced American coal consumption could more or less offset increased Asian coal consumption due to the competition of PRB coal for Asian markets.

This section explores that theoretical possibility. It will conclude that in reality this will not happen to any significant degree because coal use is stabilizing in the United States and other OECD countries for reasons that are largely

44 Op. cit. Zhaoguang Hu, et al, Integrated resource strategic planning in China, 2010. 45 Ibid.

14

unrelated to coal prices but tied to increasing environmental concerns and regulation associated with coal combustion. While coal-fired electric capacity in the U.S. is decreasing in order to improve environmental performance and not primarily in response to coal prices, coal-fired electric capacity in Asia is expanding dramatically. Therefore, shifting supply to Asia provides an economic “green light” in the economies where coal-burning infrastructure is most likely to be developed, with large impacts on emissions that last for decades.

5.1 U.S. Coal Consumption Is Being Limited by Environmental Costs

It is not the domestic price of coal in the U.S. that has led dozens of proposed coal-fired plants to be abandoned and dozens of existing coal-fired plants to be prematurely shutdown. Rather, it is the rising costs of environmental regulation and the uncertainty about that regulation that is discouraging the combustion of coal in the United States and other OECD countries.

The potential that carbon emissions will be regulated in the United States and the reality of that regulation in other OECD countries and some American states, have increased the risks and costs associated with relying on the most carbon-intensive of the fossil fuels, coal. Cap-and-trade and carbon tax proposals as well as proposals to regulate carbon emissions as hazardous pollution under the Clean Air Act have created considerable uncertainty about the economic viability of new coal-fired generation in the United States and other OECD countries. Large developing countries such as China and India are also aware of the challenges that coal combustion represent for greenhouse gas emissions and climate change in addition to other pollutants. As Fred Palmer, a senior vice-president of Peabody Coal and current chairman of the World Coal Association, said in a March 2011 interview:46

I think the concern over carbon is a constant…It’s here to stay. We respect that. We don’t denigrate it. We don’t diminish it…There’s a concern over carbon in all parts of the world, particularly western Europe, where there’s deep concern. In the US, there’s concern: it’s clearly fallen back, but it could come back to being a top issue…In China, the leadership has embraced concern over carbon so it’s a constant. The leaders of China, the US and Europe have embraced carbon as a driver, some with more intensity than others…But if you want to put in a new [coal-fired] plant today [in the US] you have to have a carbon answer so we have to develop the technology to do that.

In addition, new concerns have been raised about mercury emissions and the environmental dangers associated with fly ash and other liquid effluents from coal-fired generators.47 At the same time, long-standing concerns about sulfur and particulate emissions from older coal-fired generators that had previously been relatively lightly regulated as “grand-fathered” facilities have been the focus of new proposals to more strictly regulate those plants’ emissions. The cost of retrofitting those older plants with state-of-the-art emission control devices has led to proposals to simply retire many of those facilities.48 By one energy consulting firm’s estimate, as much as 20 percent of U.S. coal-fired electric generation, mostly merchant generators, might be retired rather than make the investment to upgrade these older, smaller, and less efficient plants.49

46 Guardian (UK), March 8, 2011, Leo Hickman, “Fred Palmer interview.” http://www.guardian.co.uk/environment/2011/mar/08/china-coal-new-middle-east47 Electric Advisory Committee, U.S. Department of Energy, “The Utility Challenge 2010-2020: Environmental and Climate Regulation, Legislation and Litigation, October 29, 2010, p. 8. http://www.oe.energy.gov/DocumentsandMedia/Shea_DOE_EAC_10-29-2010_2.pdf 48 “Reaching Retirement, Robert Peltier, Power, February 1, 2011. http://www.powermag.com/coal/Reaching-Retirement_3369.html Also see “Coal’s Burnout, Steven Mufson, Washington Post, January 2, 2011. http://www.washingtonpost.com/wp-dyn/content/article/2010/12/31/AR2010123104110.html 49 Metin Celebi et al., The Brattle Group, “Potential Coal Plant Retirements under Emerging Environmental Regulations,” December 8, 2010, http://www.brattle.com/_documents/UploadLibrary/Upload898.pdf

15

In general, high coal prices have not been what has been discouraging new commitments to coal-fired electric generation in the United States. Part of the shift away from coal can be explained by falling natural gas prices, increasing use of renewable energy which has now surpassed nuclear power in the U.S., and the much more optimistic and expansive estimates of domestic natural gas supplies that have offered a reasonably cost-effective alternative fuel for electric generation.50

Between the costs and risks associated with environmental regulation and the availability of relatively inexpensive alternative fuels, electric utilities have been shying away from coal-fired generation in the United States.51 This presents PRB coal mines with a relatively static domestic market for their coal. As Bud Clinch, Executive Director of the Montana Coal Council, located in one of the PRB states, stated: “The markets [for PRB coal] nationally are questionable, but it’s unquestionable the demand that exists overseas—a wide variety of countries and into the foreseeable future.”52

The U.S. Department of Energy’s Energy Information Administration (EIA) in its Annual Energy Outlook 2011 projects exceedingly slow growth in coal consumption in the United States: 0.2 percent per years between 2005 and 2035. That is a total expansion of about six percent over the entire 30 year period. EIA’s international projections of coal consumption show even less growth for all of the OECD countries (including the United States): Zero annual percentage growth between 2007 and 2035.53 See the figure below which shows the past trends and current projections of coal use in different groups of countries. ExxonMobil’s 2010 Annual Energy Outlook released at the beginning of 2011 projected that “in OECD countries, demand for coal is projected to decline through 2030, driven by initiatives to increase the cost of CO2 emissions and difficulties in obtaining licenses to build new coal power plants.” ExxonMobil’s projections show coal consumption declining in North America, Europe, and other OECD countries (including Japan, South Korea, Australia, and New Zealand).54

The important conclusion to be drawn from these analyses is that coal consumption in the United States and other OECD countries is projected to stabilize and then decline because of concerns over the environmental impacts associated with coal combustion rather than because coal prices are expected to be too high. Public concern, and with it public policy, has shifted towards the pursuit of cleaner ways to meet our energy needs than the combustion of coal. That is clear in the states of Washington, Oregon, and California and many other states where commitments are being made to reduce the impact of coal combustion on the local, regional, and global environment.55 The focus of this report is to understand how facilitating the export of coal for combustion elsewhere in the world affects these public policy efforts to reduce the impacts of coal combustion on the global atmosphere and climate.

50 Energy Information Administration Annual Energy Outlook, 2011, Natural Gas, http://www.eia.gov/pub/oil_gas/natural_gas/data_publications/natural_gas_annual/current/pdf/nga2009_sum_hghlght.pdf. See also http://arstechnica.com/science/news/2011/07/renewable-power-booms-in-developing-world-as-it-tops-nuclear-in-the-us.ars 51 Energy Information Administration Annual Energy Outlook 2011, Early Release Overview: US Coal http://www.eia.doe.gov/forecasts/aeo/early_elecgen.cfm . 52 Billings Gazette, Montana, November 17, 2010, Matthew Brown. 53 International Coal Outlook 2010, EIA, Figure 60, http://www.eia.doe.gov/oiaf/ieo/coal.html . 54 P. 41. 55 Senate Bill 5769 which was passed by the Washington Senate on March 5, 2011, It would reduce the gas air emissions from the only coal-fired plant in Washington, the Centralia plant owned by TransAlta, and shut down the plant entirely by 2025. The legislation has been described by some as making Washington the first “coal-free” state. http://www.chronline.com/article_2b8dfe96-479c-11e0-acb2-001cc4c03286.html However, even if these plants are shut down as proposed, Puget Energy would still be serving its customers from Puget’s 33 percent share of the four coal-fired Colstrip plants in Montana.

16

0

50

100

150

200

250

1980 1995 2007 2020 2035

World consumption by country grouping, 1980-2035(quadrillion Btu)

ProjectionsHistory

Total

Non-OECD

OECD

EIA, International Energy Statistics database (as of November 2009), web site www.eia.gov/emeu/international. Projections: EIA, World Energy Projection System Plus (2010).

5.2 Shifting the U.S. Coal Supply from Flat and Declining Markets to Booming Asian

Markets

As demand for coal in the U.S. and other OECD countries stabilizes or declines in order to meet environmental objectives, more of that coal is available to facilitate increased coal consumption in Asia. China’s booming economy has placed considerable strain on its coal production, coal transportation, and electricity system as well as on other coal-using heavy industry. China has struggled to reorganize its coal industry and transportation infrastructure to feed its burgeoning demand for electricity. This has been a race between a galloping demand for coal and a limping supply that has led to higher coal and electricity prices and periodic shortages of electricity. Chinese planners are aware of the fact that they have got to get rising energy demand under control or face energy bottlenecks and economic disruption.

Facilitating the export of coal from the U.S. where demand is flat or declining to China where the demand is high and rising would help the Chinese meet their energy needs with a “business as usual” strategy: Increase the supply, take some of the pressure off of rising Chinese energy prices, and continue to energize the Chinese economy by burning more coal. Facilitating access to Powder River Basin coal, a new, very large, and relatively cheap source of coal supply that also has low sulfur content, could make the continued building of new, long-lived, coal-burning industrial infrastructure in China easier to justify. It helps keep coal prices lower than they otherwise would be; it diversifies supply; and it helps reduce the pollution control costs associated with coal-fired generation. These impacts unavoidably make it easier for Chinese industrial leaders to make huge ongoing investments in coal-burning facilities that will emit greenhouse gases for the next 30 to 50 years. Such an enhancement of the coal supply available to Asia unavoidably provides a positive economic signal to expand coal combustion. Additionally, any further decrease in U.S. coal consumption would not offset a booming Asian market.

17

5.3 Conclusion

Significant exports of PRB coal to Asia from the West Coast will not trigger decreases in domestic coal consumption that will offset the massive increases in coal consumption in Asia caused by those exports. Coal consumption in the United States is not constrained by coal costs but by the environmental costs associated with coal combustion. However, coal consumption in Asia is expanding rapidly, so shifting PRB supplies to Asia moves them from a flat or declining market to a rapidly expanding market, facilitating the ongoing rapid expansion of coal combustion in China. By relaxing coal supply constraints in China, this effectively encourages higher levels of greenhouse gas emissions with accompanying climate change implications.

6. The Impacts of the Proposed Coal Ports Will Be Significant and Long-

Lasting

6.1 Introduction

In the previous sections of this report, we have dealt with a set of interconnected economic arguments that have been used by some to suggest that exporting Powder River Basin coal through West Coast ports will have no impact on Asian coal consumption. We have showed that that will not be the economic outcome because PRB coal can gain market share in Asia only by underselling existing suppliers including domestic Chinese coal suppliers. Firms like Arch and Peabody will have to compete against other nations currently supplying Chinese markets as well as other American coal companies who will also be seeking a share of that Asian market. That competition will put downward pressure on Asian coal prices, pushing them lower than they would otherwise have been. The lower prices and costs brought on by that competition will encourage a greater commitment to coal-fired generation in Asia and will discourage the adoption of coal- and electricity-displacing improvements in technology. Asian coal consumption will be increased over what it otherwise would have been if PRB coal was not actively competing for a share of Asian coal markets.

In addition to this particular argument that PRB coal exports through West Coast ports will not have any impact on Asian coal consumption, other arguments have been made to insist that the pending coal port proposals will have trivially small environmental impacts. We now take up with those other arguments. The analysis that follows yields the following conclusions:

• The impacts will be much larger than the annual capacity of the port indicates because access to this coal will encourage investments in new coal-burning facilities in Asia and their associated 30- to 50-year demand for coal. The impacts from those long-term investments will accumulate as will the burden on the global climate system. It will also lead to cumulative impacts in Wyoming and Montana where the coal will be strip-mined as well as along the routes of the coal trains and in the port cities.

• It has been argued that whatever the impact associated with the state of Washington facilitating the export and burning of coal overseas, that impact will be small compared to all the coal being burned in Asia and all of the greenhouse gases being released worldwide. For that reason, those impacts can be appropriately ignored. This type of argument reflects a “free rider” mentality that can be the source of the often-discussed “Tragedy of the Commons” in which everyone ignores the relatively small impacts they have individually as they seek to get as much of the benefits as they individually can from exploiting an open access common property resource, in this case, the earth’s atmosphere. As a result, that open access resource may be over-used and damaged with the result that almost everyone is worse off. This is a serious and widely recognized economic problem.

18

• This outcome can be avoided through a wide variety of cooperative behavior. One way individuals can indicate their interest in a cooperative solution to what otherwise could be individually destructive behavior involves individuals signaling their intentions to take their own impacts into account and take actions to reduce those impacts. That type of behavior can lay the basis, ultimately, for negotiated agreements to protect the threatened open access common property resource.

• The state of Washington’s public policies on climate change and greenhouse gas reduction as well as other pollution reduction efforts can be interpreted as exactly this sort of signaling of its willingness to cooperate with others to avoid a “tragedy of the commons” outcome. Ignoring the increase in coal consumption caused by the state facilitating the export of coal to Asia could undermine Washington’s existing policies to reduce its own carbon footprint and encourage others to do the same. That would not be an insignificant outcome.

6.3 Other Coal Export Proposals in the Northwest

In evaluating the impact of coal exports on Asian coal consumption, the region will not only be considering the two pending coal export plans—there are very likely to be others. In Oregon, Ambre Energy, through its subsidiary Coyote Island Terminal LLC, has entered into a one year lease option agreement with the Port of Morrow for potential coal handling.56 Other Wyoming and Montana coal mines are exploring coal exports Oregon, Washington and British Columbia. Two Washington ports that have been approached by coal exporters, Tacoma and Kalama, have decided, for now, not to open their ports to coal exports. To the extent that Washington ports begin competing with each other for coal exports, Tacoma and Kalama may reconsider. There is also evidence that other ports and counties are actively negotiating with coal exporters, including St. Helens, OR, Coos Bay, OR, and Everett, WA.

The cumulative impact of these coal port proposals on coal consumption in Asia could be much larger than even that implied by the two pending proposals. If Arch, Peabody, and other western U.S. coal producers’ projections of the competitiveness of western coal in Asia are correct, facilitating the opening of the development of West Coast coal ports could have a very large impact on the supply of coal to China and the rest of Asia.

6.4 The Long-term Implications of Fueling Additional Coal-Fired Electric Generation

Although the economic life of coal-fired generators is often given as 30 or 35 years, a permitted, operating, electric generator is kept on line a lot longer than that, as long as 50 or more years through ongoing renovations and upgrades. Because of that long operating life, the impact of the lower Asian coal prices and costs triggered by PRB coal competing with other coal sources cannot be measured by the number of tons of coal exported each year. Those lower coal costs will lead to commitments to more coal being burned for a half-century going forward.

That time-frame is very important. During exactly this time frame, the next half-century, the nations of the world will have to get their greenhouse gas emission stabilized and then reduced or the concentrations of greenhouse gases in the atmosphere may pass a point that will make it very difficult to avoid massive, ongoing, negative climate impacts. Taking actions now that encourage fifty-years of more coal consumption around the world is not a minor matter. Put more positively, allowing coal prices to rise (and more closely approximate their full cost, including “external” costs) will encourage extensive investments in improving the efficiency with which coal is used and the shift to cleaner sources of energy. This will lead to long-term reductions in greenhouse gas emissions that will also last well into the next half-century.57

56

Seattle Times, June 15, 2011 http://seattletimes.nwsource.com/html/localnews/2015330653_aporcoalterminals1stldwritethru.html; Longview Daily News, http://tdn.com/news/local/article_28aa69f4-97cd-11e0-a0ba-001cc4c002e0.html 57 “China Energy: A Guide for the Perplexed,” Daniel H. Rosen and Trevor Houser, China Strategic Advisory, May 2007, pp. 15 and 44.

19

6.5 Impacts in Wyoming and Montana and along the Railroad Corridor

The coal that would be exported to Asia will be coming from the coal fields of Wyoming and Montana. Although Arch operates in Wyoming, it has also purchased the rights to develop a new mine in Montana in the Tongue River Valley, the Otter Creek Tracts. That mine would also require that a railroad line be built into that valley. Ambre has indicated in the coal mining press that it is seeking to buy another mine in Montana, the idle East Decker mine, south of the Otter Creek Tracts in the upper Tongue River Valley just north of the Montana-Wyoming state line.

In 2009 Montana produced a little less than 40 million tons of coal. Mining twenty million additional tons would represent a 50 percent increase in Montana coal production. Mining an additional eighty million tons of coal per year would represent a tripling of Montana coal production.

Wyoming coal production, however, has been over ten times that of Montana, 431 million tons in 2009. The percentage increase in mining to serve the build-out of the Millennium and the Gateway Pacific coal ports would be a lower percentage of total PRB production, but would still take several new large strip mines since the average mine size was about 7 million tpy in Montana and 22 mm tpy in Wyoming in 2009.58 The environmental disruption associated with those additional strip mines and the transportation infrastructure to support them would be significant.

Finally, the cumulative nature over the life of the coal port of the coal trains transporting coal from eastern Montana to the west coast of Washington and the cumulative impact of decades of off-loading, storage, and re-loading of the coal on the ships at the port site also has to be taken into account. Coal dust escaping from coal cars can be a serious problem as BSNF railroad has explained.59

7. One State’s Actions Can be Effective and Economically Rational in the

Context of a Global Problem: Avoiding Free Riders and the Tragedy of the

Commons

In discussions of greenhouse gas emissions policy, it is regularly pointed out that if a particular local, state, or national government acts on its own to reduce its emissions, the impact on global climate will be insignificantly small since it is total emissions around the world that matter. The costs associated with a government unilaterally acting to reduce its emissions, however, may well not be small, especially when projected foregone economic activity is taken into consideration. In that setting it can be asserted that the costs vastly exceed the benefits and the government should not act alone. Instead, it should recognize that the climate change effects of its relatively small reductions in greenhouse gas emissions will be trivially small given the total build up of greenhouse gases and it should, therefore, wait for others to solve the problem. But even then, if others have effectively reduced greenhouse gas emissions, there would be little harm associated with any individual government deciding to enjoy the common benefits of stabilized climate while not contributing to the reduction in emissions. From a narrow economic rationality perspective, it is in any individual government’s interest to “free ride” on the efforts of others and continue to take maximum advantage of the common property resource, the earth’s atmosphere, for waste disposal purposes.

The economic incentives for individuals to maximally exploit open access common property resources, is the source of the concern over the “tragedy of the commons,” the over-use and damage to common property resources. The consequences of the absence of individual property rights and a way of enforcing those property rights is regularly used in economics texts and popular discussions of natural resource and environmental problems to dramatize the

58 Energy Information Administration, Report No: DOE/EIA-0584 (2009), Table 1, Updated February 3, 2011. 59 http://www.bnsf.com/customers/what-can-i-ship/coal/coal-dust.html#2 .

20

role of property rights and the rule of law in encouraging the efficient use of resources. However, the privatization and creation of markets for scarce and valuable resources is not always possible and even where it is, that is not the only solution to the “free rider” and “tragedy of the commons” problems. For much of human history, other social arrangements have often been relied on to solve this social problem.

The likely “tragedy” associated with these open access situations is often dramatized by some version of the “prisoner’s dilemma” where implicit cooperation between the prisoners would lead to the best outcome for both of them, but, because communication between them is not allowed, each prisoner has to contemplate the outcome if the other acts in her own individual interest rather than in their joint interest. The result is that both act in their individual interests and both are much worse off than they would have been if they had implicitly cooperated. The pursuit of “rational” self-interest by each leads to a much worse outcome.