the handy guide for the expat

TRANSCRIPT

The Handy Guide for the Expat Table of contents Sheet 1 Welcome

2 Gain time, consider the Expat Convenience Package

3 How to open and manage your account

4 Which debit/credit cards are available from KBC

5 Effecting transfers (domestic and international)

5a Filling in your transfer form correctly

6 Using cheques

7 KBC-Phone and KBC-Online

8 Managing investments

9 Application to open an account

10 Renting/buying property

10a Power of attorney

10b Home Insurance Checklist

11 Buying/leasing a vehicle

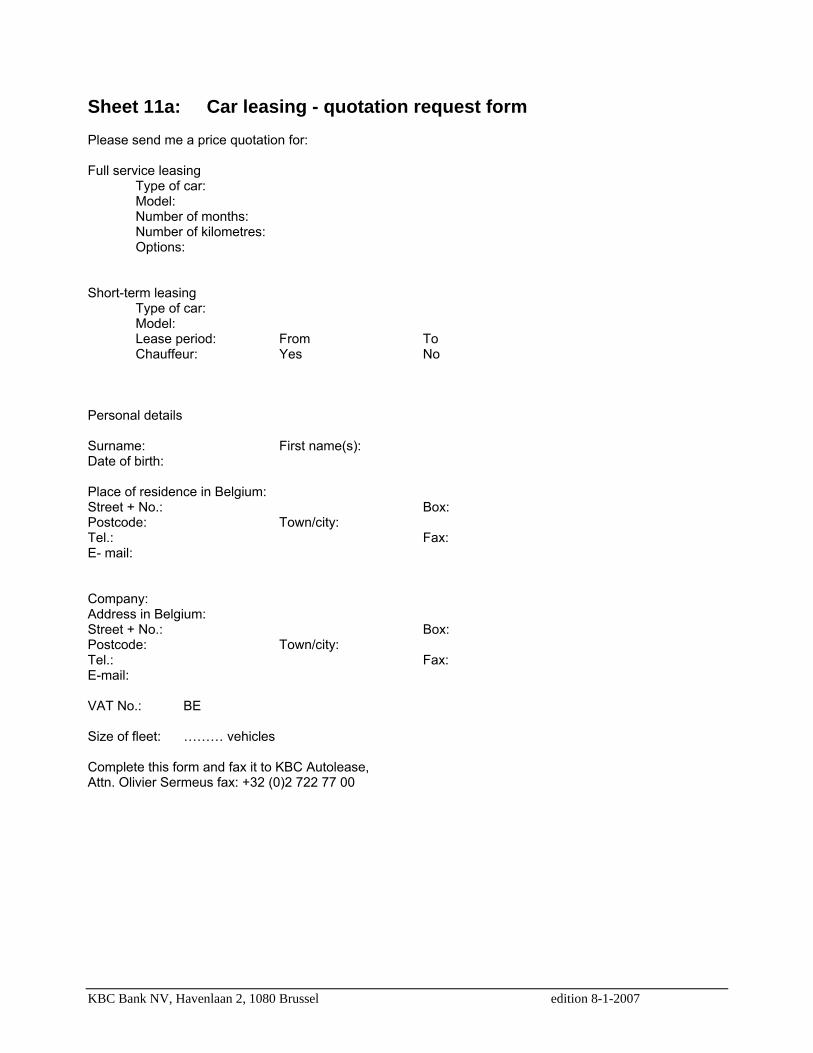

11a Car leasing - quotation request form

12 Personal taxes

13 Frequently Asked Questions

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Sheet 1: Welcome! Congratulations on your new posting and welcome to Belgium! We hope your stay here is both happy and successful. Settling in to a new country, whilst at the same time being able to focus fully on the business challenges ahead of you, isn’t easy. It usually means having to tackle a whole range of important issues - some even before or immediately after your arrival. Many of these are banking- or insurance-related and KBC, with its considerable experience in Expatriate banking in Belgium, would be delighted to assist you in these turbulent times. So welcome also to the KBC 'Handy Guide for the Expat'. KBC provides a convenient and comprehensive financial service for Expats - whether you are already here or in the process of relocating. This handy guide sets out the details for you in a form designed for easy reference. As with our famous Belgian chocolates, you can take the selected assortment or pick & mix! That’s why this guide starts with the KBC Expat Convenience Package, a careful selection taken from KBC's wide range of products and services which are described in more detail in the subsequent sections of this survey. These focus on key decisions you’ll be facing such as opening an account, renting or buying accommodation, and purchasing or leasing a car. Relevant insurance cover however - like the safety net - is dealt with under each section. To keep the guide simple, we have not included all the particulars of charges and rates. These can change from time to time and are readily available from any KBC branch. Moreover, as an Expat, you can benefit from special rates on many products and services. But firstly may we introduce KBC to you. We’re a leading, independent Belgian financial institution providing our customers with a full range of integrated banking and insurance services as well as tailor-made professional advice. Apart from the inherent benefits of our bancassurance concept and high-quality innovative products, other features of our service include convenient business hours and advanced electronic banking facilities via KBC-Online 24 hours a day/7 days a week. But KBC not only offers ‘round-the-clock’ service, we also provide that special ‘round-the-corner’ convenience via our extensive multi-channel network throughout Belgium. In Brussels, Flanders and the German-speaking area under the name KBC, and in Wallonia under the name of our subsidiary, CBC. And of course, there’s the extra dimension of our active presence in more than 30 countries world-wide, notably in the major financial centres. In Central and Eastern Europe, KBC has created a second home market. The bank is active in the Czech Republic, Hungary, Poland, Slovenia and the Slovak Republic, and boasts the biggest market share in the area. It is a true network that assures you of top-class service with, among many other things, the international transfer of funds. In a nutshell, we strive - through customer-friendliness, enterprise, innovation and efficiency - to provide our customers with a unique range of products and services. Whilst you’re busy looking after other people’s interests, we’ll look after yours. Anne Marie Azijn & Leo Verhoeven KBC Expat Adviser Tel.: +32 (0)2 429 18 57 Fax: +32 (0)2 429 11 98 E-mail: [email protected]

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Sheet 2: Gain time, consider the Expat Convenience Package From our experience, we know that your time is at a premium. That’s why we have brought together all the banking services you and your family might need in a single package - the KBC Expat Convenience Package. This currently covers a range of 16 services. You are, of course, not obliged to take this package, nor indeed to utilize all the services. Details of individual products and services are provided in the other sheets. The KBC Expat Convenience Package offers the following five principal benefits, being: 1. comprehensive - providing all the financial services you need in Belgium 2. simple and quick to obtain 3. easy to understand - all documents are in your own language 4. simple to manage - your accounts are easy to keep track of 5. inexpensive – there’s one fixed, ‘all-in’ price A quick overview of the contents The KBC Convenience Package offers the products and services of the KBC Convenience Account plus some extras: The KBC Convenience Account comprises:

• financial management via the current account • free electronic debit transactions and cash withdrawals from KBC/CBC ATMs • access to the KBC-Matic printers and KBC-Matic ATMs • 36 manual payment transactions per year and cash withdrawals from ATMs other than KBC/CBC,

free of charge • a single KBC Bank Card with Proton, Bancontact/Mister Cash (Maestro included) • a second KBC Bank Card with Proton, Bancontact/Mister Cash (Maestro included) at a flat fee of 5

euros • one standard credit card (KBC Visa, KBC MasterCard Business, or a Pinto Visa card1) or

a discount on a KBC Gold MasterCard (including travel cancellation insurance) • a second credit card at a flat fee depending on the kind of card you choose • telephone banking - a subscription to KBC-Phone • PC banking - subscription to the KBC-Online Browser application

The services that come with the KBC Convenience Account are listed in the schedule of rates and charges, which is available for consultation and free copies of which can be obtained at any KBC Bank branch. Extras:

• current accounts in a foreign currency • budget facility on current accounts in euros2

• credit ceiling on credit cards2

• savings account in euros • time deposit account(s) in euros and/or in foreign currencies • international transfers at a flat fee • reappraisal of your insurance cover and of your investment portfolio • assessment of the income tax you’ll have to pay

1 The Pinto Visa card is a credit card which entitles the holder to credit. The card is provided by KBC Pinto Systems through the intermediary of KBC Bank. KBC Bank acts as credit broker for this product. 2 Following a positive credit assessment.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Charges Flat fee For the KBC Convenience Package, a flat fee is charged to the customer’s account at the start of every calendar year. In the first year, the customer will not be charged anything; the remaining of the first year, the package is for free. The flat fee covers all the products and services stipulated. The amount of the flat fee is provided in the schedule of rates and charges, which is available for consultation and free copies of which can be obtained at any KBC Bank branch. As of 1 January 2007, this flat fee is 35 euros per year (that’s less than 3 euros per month!). Unit pricing The flat fee entitles the customer to a basic package of 36 non-electronic debit transactions and cash withdrawals from ATMs other than KBC/CBC. From the 37th transaction, the standard price per transaction will be charged. This price is in the schedule of rates and charges, which is available for consultation and free copies of which can be obtained at any KBC Bank branch. Interest rates The terms and conditions in respect of credit interest on the KBC Convenience Account are given in the schedule of rates and charges, which is available for consultation and free copies of which can be obtained at any KBC Bank branch. Credit interest is settled annually, unless a three-monthly settlement is carried out for debit interest. Credit interest (before withholding tax) on a KBC Convenience Account is 0.25% as of 1.500 euros. Additional information regarding certain of our products and services The current account: an absolute must

The current account is, as it were, the key to managing your finances. You can have all incoming funds, including your salary, credited to it... and you can make all your payments from it. Opening an account at KBC is simple and quick. (For more details see Sheets 3 and 9)

Free electronic banking and cash withdrawal from KBC/CBC ATMs

A few days after opening your current account, you will receive your KBC Bank Card. This card is your key to several functions, including:

• Cash withdrawals in Belgium from ATMs situated in the KBC Bank branches or from any cash dispenser displaying the Bancontact/Mister Cash logo in Belgium (also those displaying the Maestro function abroad).

• Payments in shops or via payment terminals displaying either the Bancontact/Mister Cash or Proton logos in Belgium (and as of 01/01/07 also when displaying the Maestro function abroad).

36 manual payment transactions completely free of charge

You can carry out up to 36 manual (i.e. non-electronic) transactions per year that would otherwise attract a charge. These might include:

• cash withdrawals at a KBC Bank counter • cash withdrawals at a non-KBC/CBC dispenser within the eurozone • paper-based transfers to a payee with a non-KBC account

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Remember that you can avoid these manual transactions by banking electronically. Regularly recurring costs such as rent, gas or electricity can be settled by standing order or direct debit, and why not use your debit or credit cards instead of cheques? Also, manual transfers to payees with a KBC account number are not subject to the above-mentioned limit of 36 transactions.

KBC-Phone and KBC-Online

If you’re abroad or you don’t have time to go to a KBC-Matic Printer, you can always manage your accounts via the telephone (using KBC-Phone) or by the computer (via KBC-Online). Wherever you are, whatever the time! Just about every transaction is now ‘at your fingertips’, day or night - seven days a week. And if you are not yet connected to the Internet, KBC will be happy to help - free of charge, of course.

Current accounts in a foreign currency

If your salary is paid partly in euros and in another currency, then a foreign-currency account would certainly come in handy. There are no costs for opening the account, neither is there any charge for managing it. Of course there is a charge for all non-electronic transactions.

Budget facility on current account in euros and credit ceiling on credit card

To facilitate your cash planning, ask your KBC Bank branch to set up a payment facility linked to your current account. Following a good credit assessment, we can offer you an overdraft facility of 2 500 euros without any problem. Similarly, with a positive credit assessment, we can also offer you a credit ceiling of 2 500 euros on credit cards. In both cases, higher amounts can be arranged via your branch manager.

Savings account in euros and time deposit account(s) in euros and/or in foreign currencies

Although the current account is, as it were, the key to managing your finances, any cash surplus you may have is better invested in a savings account. Or, you could consider using a time deposit account (in the currency of your choice). With the KBC Expat Convenience Package, you can open such an account quickly and it’s free of charge. KBC has also a huge range of successful investment products available. Together, you and your personal KBC investment adviser can compile an individual portfolio for you, tailored exactly to your specific requirements.

International transfers at a flat fee

As an Expat, perhaps you still have to make regular transfers home (mortgage repayments, the children’s school fees, other on-going financial commitments, etc.). Here, too, KBC can make things easier for you. With an Expat Convenience Package, you can transfer money abroad at a low price or even for free: Within the European Union, international transfers up to 12 500 euros, KBC’s EU Transfers are free of charge provided they fulfil the following additional conditions:

• it is not an urgent transfer; • you effect the transfer yourself via KBC-Online (see Sheet 7); • you use the correct IBAN (International Bank Account Number) of the beneficiary and BIC

(Bank Identifier Code) of the beneficiary’s bank. This allows a fully automatic KBC transfer.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

If the transfer is within the EU, but is for an amount over 12 500 euros and/or does not fulfil all the other aforementioned conditions, then an EU Transfer ‘Plus’ will be used which attracts certain fixed charges. Shared cost + 10 euros for an urgent transfer (or extra cost if you want confirmation of payment).

Other countries/currencies:

If you wish to transfer funds outside the European Union and/or in a currency other than euros, then you must effect a standard Cross-border transfer. The associated charges vary according to the amount you transfer, the destination country of the transfer and the cost option (all charges for you, all charges for the beneficiary, or shared). Check first with your KBC branch for more information. With the Expat Convenience Package you benefit from a special service which, for a flat fee of ten euros (+ VAT), allows you to transfer up to 12 500 euros (or the equivalent in another currency) per transfer to a foreign country outside the European Union, nominated by you in advance (e.g. to America). To take advantage of this preferential fee you must:

• inform the branch beforehand (e.g. when opening your account) for which country you wish to have these preferential terms;

• not exceed the per transfer limit of 12 500 euros (or its equivalent); • not specify that the transfer is ‘urgent’; • not link any additional services to the transfer (e.g. confirmation); • remember that any charges from the beneficiary’s bank remain for the recipient of the

moneys.

Reappraisal of your insurance cover and of your investment portfolio and an assessment of the income tax you’ll have to pay.

Your KBC Bank branch is there to help. That’s why we offer you the opportunity to have your insurance portfolio reappraised every year, free of charge. In this way, you can be sure that you have proper and adequate cover without paying excessive premiums. Often, as an Expatriate, you’re squeezed to find the time you need to be able to manage your investments properly. So why not call on the services of a KBC Investment Adviser? He/she will analyse and discuss your investment portfolio with you once a year, free of charge. Your KBC Bank branch will also provide you with one estimate per year of your personal Belgian tax obligations based on your completed tax return (see Sheet 12).

To take advantage of the KBC Expat Convenience Package (or if you have questions about it) contact our expat advisers Anne Marie Azijn and Leo Verhoeven

Tel.: +32 (0)2 429 18 57 Fax: +32 (0)2 429 11 98 E-mail: [email protected]

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Sheet 3: How to open and manage your account Your current account is, as it were, the hub of your cash management system. To open your KBC account, simply drop into any KBC Bank branch and ask to open one! To find the most convenient KBC branch, check the Internet on: www.kbc.be, select ‘E’ for English in the top bar, then ‘Branches’, then click on ‘network’ and enter the name of your preferred town/city. Alternatively, you can look us up in the Yellow Pages, contact us at ‘[email protected]’ or call your expat adviser on +32 (0)2 429 18 57. Of course, there are one or two minor formalities. We need your name and address, for example - but if you don’t yet have an address in Belgium, no problem, we provisionally put your account under your employer’s address. We also require your validated signature. Then, within minutes, you’ll have your account number. If you’re really pressed for time, you might find it more convenient to fill in the application form enclosed (Sheet 9) and post, fax or e-mail it to us. Your account is operational as soon as it is opened. You can deposit cash and have all money transfers, including your salary, paid into it. To have your employer transfer money to your account, all you have to do is notify your account number to your personnel department. You can also withdraw cash from your account at will, besides using it to make all your payments, i.e. rent, loan repayments, telephone, water and electricity bills, etc. As a matter of fact, these regularly recurring bills can be handled by direct debit, whereby you complete the requisite form and return it to the creditor or the KBC branch of your choice. The creditor then arranges everything directly with the bank. This means that your invoices are paid automatically, without you having to worry about them. You can also give the bank a standing order to pay regularly recurring expenses for which you receive no invoice or account (rent, for example). These payments are made at predetermined times and the standing order remains in force until you cancel it. You can, of course, amend the details whenever you wish. Finally, at KBC we make banking easy - 24/7 - for people with busy (often international) schedules. The vast majority of your routine banking transactions can be carried out electronically either via the telephone (with KBC-Phone) or via your PC (through KBC-Online banking). For example, you can set up your own standing orders and then monitor or amend them yourself on your PC. At the same time you can consult any direct debits you arrange with the bank. Managing your KBC account, is made easy thanks to the statements of account which provide you with clear and complete details of all incoming and outgoing payments on your account (see sample statement overleaf). You can print the statements free of charge in the KBC-Matic lobby of any KBC Bank branch, or, for a small fee, have them mailed at pre-determined intervals (daily, weekly, etc.) to an address nominated by you. With KBC-Online, the function ‘Print statement of accounts and annexes’ gives you the opportunity to print out your statements at home or at work. This easy-to-use function will save you a great deal of time and, moreover, these statements have the same legal status as the traditional A6-format statements you can get from the branch. You can also check your account status using KBC-Phone. KBC makes monitoring your account as easy as ABC. Remember that any surplus funds on your current account can be invested or transferred to a savings account and any temporary shortfall in funds can be covered by a credit or budget facility. Note: If you choose the Expat Convenience Package you automatically get a current account, a debit card, a credit card, cheques, transfer forms, etc. For full details see Sheet 2. Alternatively, you can opt to simply open a current account.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Sheet 4: Which debit/credit cards are available from KBC What facilities do I get with a KBC Bank Card? The KBC Bank Card is your debit card, a highly versatile instrument that allows you electronically to access your funds immediately. It offers you four different functions. As some are activated only on request, there is no obligation to use them all. Important facilities for when you’re in Belgium: Proton, Bancontact/Mister Cash, KBC-Matic: 1. Proton - your electronic purse in Belgium Your KBC Bank Card contains your Proton chip. Proton has been specially developed as a fast, convenient and secure means of payment for your small purchases. It cuts out having to carry all that small change around in your trouser pocket or handbag. Loading Proton Loading the Proton chip is simply a matter of transferring an amount of money from your KBC account to the chip on your KBC Bank Card. It can be done:

• at all Bancontact/Mister Cash dispensers and at KBC-Matic ATMs; • at the special Proton loaders in certain KBC-Matic lobbies; • via a Belgacom (the Belgian telephone company) public telephone (i.e. one displaying the Proton

logo). The maximum amount that you can load at any one time is 125 euros; the minimum amount is 5 euros. Just as with a cash withdrawal, details of the transfer appear on your statement of account. Paying with Proton Paying with Proton takes no time at all and is extremely simple. In shops, the trader enters the purchase amount on the Proton payment terminal and, to make the payment, you just place your KBC Bank Card with the Proton chip into the terminal, check the amount, and press the ‘OK’ button. No PIN is required. You can now pay virtually anywhere in Belgium with Proton, not just in most shops, but also at drink vending machines, car-park ticket machines, in Belgacom’s telephone boxes, etc. Checking your Proton balance If you make regular use of the Proton function, you’ll want to keep track of your remaining balance. There are a number of ways to do this:

• at any Proton payment terminal: simply insert your card and press the ‘?’ button; • at any Bancontact/Mister Cash dispenser; • at any KBC-Matic ATM; • at the special Proton loaders in the KBC-Matic lobbies; • at any public Belgacom telephone boxes (displaying the Proton logo), by inserting your card and

pressing the ‘?’ button; 2. Bancontact/Mister Cash Making payments You can use your KBC Bank Card in Belgium to pay in most retail outlets and self-service petrol stations. The advantages of this are that you need no longer carry large amounts of cash, you can shop or refuel at any time of the day or night, and you get a detailed overview of all transactions on your account statement. Important to remember is that, once you have inserted your KBC Bank Card into the payment terminal and entered your secret code (known as your PIN or personal identification number), you are in direct contact with your current account. The payment is thus debited immediately from it.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Withdrawing cash If you need cash, you can use your KBC Bank Card to withdraw banknotes from any cash dispenser in the Bancontact/Mister Cash network throughout the country. These are accessible 24 hours a day, 7 days a week. Simply insert your KBC Bank Card, enter your PIN and follow the English-language instructions on the screen. Please note that your account balance and your card and account limits are checked before the transaction is executed. Consequently, if there are insufficient funds on the account, payment will be refused. 3. KBC-Matic The KBC Bank Card can be used in the KBC-Matic machines located in the self-service lobbies of most KBC branches in Belgium to carry out virtually all basic banking transactions:

• in the KBC-Matic ATMs (Automated Teller Machines), you can withdraw cash, load your Proton chip (see below) and make transfers to other bank accounts;

• in the KBC-Matic printers you can print out your statements of account; • in the KBC-Matic deposit machines you can deposit money (EURO banknotes only) and cheques,

using an envelope. When you’re abroad you have an additional facility at your disposal: Maestro Maestro - Cirrus Your KBC Bank Card automatically offers you the Maestro function for making payments or withdrawing cash when you’re travelling abroad. Making payments You can use your KBC Bank Card to pay for your purchases in any of the 1.5 million retail outlets worldwide that display the Maestro logo. Depending on the type of payment terminal, you either enter your PIN (the same as you use in Belgium) or sign a sales slip. In some countries the PIN linked to a debit card comprises more than four digits, but there too, you simply enter the four digits of your PIN and press OK. Similar to a Bancontact/Mister Cash payment in Belgium, your account balance and card limits are checked. Please remember, however, that a few days elapse before the amount of the Maestro payment is debited from your account. Withdrawing cash Likewise, you can use your KBC Bank Card worldwide to withdraw cash from all cash dispensers displaying the Maestro or Cirrus logo. Again, your account balance and your card and account limits are checked before the transaction is executed. Just as for your payments and cash withdrawals in Belgium, details of each transaction appear on your statement of account. Note 1. Costs are charged for both payments and cash withdrawals made abroad in non-euro countries with the KBC Bank Card (consult your KBC branch for more details). Note 2. The Maestro - Cirrus function is a standard component of the Expat Convenience Package. Your PIN Your PIN is linked to your KBC Bank Card and is used to withdraw cash - so guard it well. Never write it down. Always enter it discretely at the cash dispenser or payment terminal. If you suspect that someone else knows it, change it as quickly as possible. You can do this easily at any time at most cash dispensers. If you forget your PIN, you can always request a new one at your KBC branch. After applying for a new PIN, you can immediately choose your new PIN at our KBC-Matic ATMs.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

FAQ’s: ‘What are credit cards and charge cards and how do they differ from debit cards?’ Whereas payments made with a debit card (your KBC Bank Card) are debited individually and virtually immediately by the bank from your current account, a credit card offers so-called revolving credit where one has the option of paying off some (normally subject to a minimum payment) or all of the balance each month. With a charge card, your payments are debited from your account at one and the same time, once a month. In Belgium most ‘credit’ cards are in fact charge cards. ‘Which charge cards are currently being offered by KBC?’ KBC is currently offering KBC Visa, KBC MasterCard Business and KBC Gold MasterCard. These are a handy, modern and safe means of payment, and give you unrivalled convenience both at home and abroad - plus a host of other advantages. It’s also worth knowing that, via KBC-Online, you can consult your card balance and get a historical overview of your card transactions. You can pay with them wherever the Visa or MasterCard logo is displayed. There are about 6 000 retailers (travel agents, shops, hotels, restaurants, petrol stations, etc.) in Belgium alone that accept them and more than 22 million worldwide. Pay using your secret code or signature KBC charge cards are easy to use and, moreover, no fee is made for their use. You confirm your payment by signing the retailer’s receipt after having checked the amount of your purchase. Increasingly, you’ll be able to confirm your payment by entering your secret code. Reaffirm your code by pressing the ‘OK’ button. The retailer will always give you a copy of the cash ticket, proof of payment that you should keep until you receive your monthly statement. Withdrawing money with your charge card You can also use your KBC charge card to withdraw cash - in Belgium at the Bancontact/Mister Cash dispensers and abroad (local currency) at the banks and ATMs displaying the Visa, MasterCard or Maestro logo. You will, of course, need your PIN, and don’t forget that you will be charged a fee for this service. Note: some ATMs allow longer codes but never add digits to your code. Simply press ‘OK’ when you have entered your code. A favourable exchange rate Your payments and cash withdrawals in a country not a member of the European Monetary Union (EMU) are converted into the currency of your account at a favourable exchange rate based on the indicative rate of the European Central Bank, plus a small exchange margin. Interest-free deferral of payment You receive a detailed statement at the end of each month and the amount due is automatically deducted from your account some days later. This means that you benefit from a deferral of payment which, by the way, is interest-free. Travel cancellation insurance Your KBC Gold MasterCard comes with travel cancellation insurance. This covers:

• the whole family travelling together and individual trips by family members; • all year round; • for an amount of up to 6 000 euros per claim; • in the event, for example, of illness, accident, death, job loss for economic reasons, etc.

Note that it is NOT necessary to pay your trip with the card in order to benefit from the insurance. The terms and conditions of the travel cancellation insurance can be consulted at any KBC Bank branch. If, in addition to your credit card, you also take the KBC-VAB Assistance insurance, you benefit from an extra reduction.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Safer than cheques or cash. Your card is personal, so sign it as soon as you receive it. In the event of loss or theft of your KBC Visa card, KBC MasterCard Business or KBC Gold MasterCard, immediately notify Card Stop (see below). Your liability will then be limited to 150 euros up to the moment of reporting (except in the case of fraud or gross negligence). ‘What actual credit cards are currently being offered by KBC?’ KBC Pinto Visa provides so-called revolving credit to private individuals and is linked to a Visa charge card. The credit can be freely used (i.e. no prior bank approval is required for the expenditure). The repayments are also made when you want to make them. And, once repaid, you can always draw down the credit again up to a previously agreed maximum amount. Note however, that when you use the credit facility, you have to make a minimum monthly repayment of 5% of the line granted. Once in a while unexpected expenses can crop up, such as a down-payment on a car or personal computer, or an unexpected bill. With KBC Pinto, you’ve always got a cash reserve you can fall back on. Moreover, the Pinto Visa card is accepted internationally. Customers also have the option of taking out insurance with the KBC Pinto Visa card. This insurance provides cover in the event of:

• death: on the death of the customer, the insurance will pay back the balance outstanding in principal + interest + charges in full. Consequently, the debt will not become part of the estate.

• disability due to illness or an accident: if, during 60 consecutive calendar days, the customer is unfit for work on account of illness or an accident, the monthly repayments will be met by the insurance company from the first day of disability.

• fraud following the loss or theft of the card (even the deductible is insured). ‘Is there a credit ceiling in force for charge and credit cards?’ Yes there is, so do check this with your KBC branch. The ceiling is generally set at 2 500 euros, but can be adjusted according to your needs and creditworthiness. This is done in discussion with the branch manager. Important! Card Stop To block your card in the event of loss or theft, just call Card Stop on 070 344 344 from within Belgium or + 32 70 344 344 from abroad. The line is open round the clock, 7 days a week. Your card will be blocked immediately, but you should also report the theft or loss to the local police within 24 hours and have a report made up. Tip: Programme the Card Stop emergency number straight away into your mobile phone, so it’s always available. An automated system will order a new card for you, which will be available in your branch after about 4 working days.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Sheet 5: Effecting transfers (domestic and international) Funds may be transferred via a paper trail or electronically. The latter method is faster, cheaper and more secure. ‘What are paper transfer forms and how do you use them?’ The paper transfer form is a document that banks provide their clients so that they can give instructions to transfer money in Belgium or abroad. When completed, it must be delivered to the bank for execution, not to the payee. Transfer forms cannot and should not be accepted in payment. As regards transfers in Belgium, it is important to realize that they are a normal means of payment here, unlike the situation in the United States, for example, where the cheque predominates. Most banks prepare personal transfer forms for their clients, pre-printed with the client’s name, address and account number. All other details have to be filled in by hand, i.e. name, address and account number of the payee (also known as the beneficiary), amount of the payment, date of the order (this can differ from the date the payment has effectively to be made – the so-called ‘memo’ or execution date) and, if required, a textual or standard-format reference (digits only) in the reference zone. And, naturally, the form has to be signed. It will often happen that the payee (e.g., the water company) will send you an invoice together with a payment slip which is virtually completed in advance. The reference, too, will usually be pre-printed and in structured form (a reference number with a control digit with which the payee can easily and automatically identify the payer, also known as the principal). All that is left for you to do is fill in your account number, sign and date the form, and pass it to your KBC branch for payment. The fastest, cheapest and most secure way to deliver your transfers to KBC, is via your pc (KBC-Online). Don’t forget that you can, of course, opt for the domestic direct debit or standing order for those regularly recurring outgoings for rent, loan repayments and the telephone, water and electricity bills, etc. For transfers abroad and other types of transfers, there is another type of transfer form: EU Transfer and EU Plus Transfer. 1 EU Transfer What is it? An EU Transfer is a cross-border, international money transfer with the following features: • the transfer takes place within the European Union1; • the amount of the transfer is denominated in euros; • the amount of the transfer is less than or equal to 50 000 euros; • the IBAN (International Bank Account Number) of the beneficiary and the BIC (previously known as the S.W.I.F.T. address) of the beneficiary’s bank are correct and consistent with each other; • the name and address of the beneficiary are filled in properly; • the principal’s account number is correct and the name and address of the principal are filled in properly; • you have selected a «shared» cost allocation (SHA); • no reference is provided for the principal’s bank or for the beneficiary’s bank (except the INTC code).

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Who is it for? Companies and private persons making/receiving intra-EU money transfers of up to 50 000 euros. Advantages: • Domestic rate of charge; • Simple means of payment; • Efficient, quick and safe; • With KBC Online you can easily execute yourself an EU Transfer. (1) The European Union (EU) comprises: - the 12 countries which have adopted the euro: Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxemburg, Netherlands, Portugal and Spain; - the other EU member states: Denmark, Sweden, United Kingdom, Cyprus, Estonia, Hungary, Latvia, Lithuania, Malta, Poland, Slovakia, Slovenia, Czech Republic; - Northem Ireland, Gibraltar; - French Guyana, Guadeloupe, Martinique and Réunion; - Azores, Canary Islands and Madeira, Ceuta, Melilla. 2 EU Plus Transfer What is it? An EU Transfer ‘Plus’ is a cross-border, international money transfer with the following features: • the transfer takes place within the European Union1; • the amount of the transfer is denominated in euros; • the transfer does not meet all the conditions for an EU Transfer2. (1) The European Union (EU) comprises: - the 12 countries which have adopted the euro: Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxemburg, Netherlands, Portugal and Spain; - the other EU member states: Denmark, Sweden, United Kingdom, Cyprus, Estonia, Hungary, Latvia, Lithuania, Malta, Poland, Slovakia, Slovenia, Czech Republic; - Northem Ireland, Gibraltar; - French Guyana, Guadeloupe, Martinique and Réunion; - Azores, Canary Islands and Madeira, Ceuta, Melilla. (2) For instance: the amount being transferred exceeds 50 000 euros, the payment order cannot be

processed fully automatically (the information is incomplete or incorrect, a reference has been provided for either the principal’s or beneficiary’s bank, etc.) or all charges are paid by the principal (OUR) or by the beneficiary (BEN). The KBC product sheet entitled ‘EU Transfer’ contains more information on this type of money transfer.

Who is it for? Mainly SMEs and large companies with payment flows to/from EU countries (and to a lesser extent private persons). Advantages • Uniform (fixed) charges • Simple means of payment • Efficient, quick and safe

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

3 IBAN Although, in Belgium, all account numbers have the same structure (12 digits, the last two of which are check digits), foreign account numbers are not always that straightforward. Account numbers may vary from country to country and sometimes even from bank to bank. That's why, for payments abroad, the European Committee for Banking Standards (ECBS) has come up with the international standard for account numbers - the IBAN. The account number will be preceded by the word 'IBAN' and split into groups of four digits separated by a space. The ISO code for the country where the account is held (two letters) e.g., BE for Belgium, a check digit (two numbers) and the existing national account number. The IBAN may comprise a maximum of 34 digits, with a fixed number of digits per country. In Belgium, an IBAN comprises 16 digits e.g., the Belgian account number 402-4047601-79 becomes BE58 4024 0476 0179. So, if you have to pay money abroad, specify the IBAN and BIC details shown on the purchase invoice on your international payment instruction. When we carry out your transfer instruction, we'll check those numbers again. This gives you the major benefit of knowing that your payments will be processed more speedily and more securely. ‘Are there other types of transfers?’ If you wish to transfer funds outside the EU, then you must effect a standard Cross-border transfer. The associated charges vary according to the amount you transfer and the cost option (all charges for you, all charges for the beneficiary, or shared). Check first with your KBC branch for more information. As an Expat, however, you can benefit from a special service that comes with the Expat Convenience Package. For a low, flat fee (10 EUR + tax) you can transfer up to 12 500 euros (or the equivalent in another currency) per transfer to a foreign country outside the European Union, nominated by you in advance (e.g., to America) – very useful if you want to repatriate a proportion of your income each month to your home country to cover current financial obligations there (mortgage repayments, the children’s schooling, etc.). To take advantage of this preferential fee you must: • inform the branch beforehand (e.g., when opening your account) for which country you wish to have

these preferential terms; • not exceed the per transfer limit of 12 500 euros (or its equivalent); • not specify that the transfer is ‘urgent’; • not link any additional services to the transfer (e.g. confirmation); • remember that any charges from the beneficiary’s bank remain for the recipient of the moneys. If you want to transfer money back to your own country, ask for your IBAN, if available.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

If you expect a transfer from abroad, then ensure that you provide the principal, at least, with the following information:

• your IBAN bank account number (see your account statement or check out the KBC Web site); • the address of your bank branch; • the BIC (Bank Identifier Code), which for KBC is KREDBEBB.

If your foreign payer uses your IBAN and KBC’s BIC on their payment instructions, then, via a built-in check, their banker carries out an extra check of the data. Thanks to this procedure, payments are credited to your account more speedily and more securely. If you are expecting a transfer from the USA, the money will arrive quicker if the foreign payer uses the following payment instruction: Pay to KBC Bank New York Fedwire number 026008248 for account of KBC Bank Belgium (SWIFT/BIC: KREDBEBB) for further credit to “… your name + iban”.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Sheet 5a: Filling in your transfer form correctly When filling in the form always use blue or black ink (red ink is not permitted). Fill in only one character per space. Always write in block letters. It is better to use a new blank form rather than to change details on a pre-printed form.

You can also execute your payment orders directly via the telephone or via PC. Both are handy and simple methods and permit you to give your instructions when it is most convenient for you. (See Sheet 7)

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Sheet 6: Using cheques Whilst the normal means of paper payment in Belgium is the transfer (see Sheet 5), payment by cheque is also possible. ‘How many types of cheque does KBC supply?’ Two. The ordinary cheque and the travellers’ cheque. The ordinary cheque The ordinary cheque is not linked to a guarantee card. If there are insufficient funds on the account, the bank will not pay out the value of the cheque to the payee. Ordinary cheques are generally used by traders, associations and companies that regularly have to pay substantial sums. It’s a simple matter to pay with a cheque. On the front of the cheque, you fill in the amount in letters and figures, and indicate the currency (the amount in writing is taken as the valid amount, should it differ from that in figures). You also fill in the date and place of issue of the cheque and then, of course, sign it. Cheques written out and payable in Belgium have a ‘presentation term’ of 8 days, which is the grace period for you to ensure that there are sufficient funds on your account to cover the payment. A cheque is valid for six months from the end of this presentation term; thereafter it has no value. In Belgium, because transfers and electronic means of payment have largely replaced cheques, only a small number of cheques are provided to the client at a time. Moreover, they are provided loose and with a single sheet to record transactions, not in a book, as is the case in the United States or the UK, for example. To avoid any misunderstanding, cheques may be written out in English. With a cheque on which the name of the payee is filled in, only this person can cash or endorse the cheque. This is called an order cheque. You endorse a cheque when you want to pass it to someone else. To do this, you write the words ‘to the order of … ‘ with the name of the new payee and your signature on the back of the cheque. A crossed cheque is a cheque with two parallel lines drawn across its face. This indicates that the amount can only be paid into a bank account. Both the person writing it out and the payee can cross a cheque. You can also write the account number of the payee between the parallel lines, indicating that the amount can only be paid into that account. This reduces the risk of financial loss, should the cheque go astray. A cheque represents money, so keep these tips in mind:

• never carry more cheques with you than is necessary; • never sign your cheques in advance; • never leave cheques behind in the car or at the office; • always fill in cheques with indelible ink.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

The travellers’ cheque If you’re travelling abroad, you can also make use of travellers’ cheques to make your payments, besides banknotes, cheques or credit cards. Travellers’ cheques are pre-printed cheques issued by international banks or companies and can be obtained in various currencies and denominations. Your account is debited immediately you buy them (presuming that you use your account for the purpose). When you receive the cheques, you sign them for the first time. When you cash them abroad, you sign them the second time in the presence of the person accepting them, who checks that the two signatures are identical. Travellers’ cheques carry two security guarantees: without the second signature, no-one can use them for payments and you are insured against loss or theft.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Sheet 7: KBC-Phone and KBC-Online KBC offers you the convenience of ‘round-the-clock’ banking ‘round-the-globe’ by means of its telephone and PC banking facilities - KBC-Phone and KBC-Online. Search for all details on these products on our website: www.kbc.be/ebancassurance. KBC-Phone KBC-Phone is available round the clock for all your routine banking transactions (use it to check the balance on your account, effect transfers, etc.). The KBC-Telecenter is there to help you with the more complex banking transactions (e.g., buying shares, ordering foreign currency, etc.) and is manned weekdays – including evenings until 10 p.m. - and Saturdays and Bank Holidays until 5 p.m. Advantages

• Extended opening hours. • 100% security, thanks to the secret PIN (ask for one at your bank branch). Just dial in to KBC-

Phone. • Nothing could be easier. • You'll be able to do your banking business anywhere: at home, at work, even when you're abroad.

All you need is a touch-tone phone or a mobile. • There's no subscription charge for KBC-Phone. All you have to pay is the charge for a local phone

call. • There's no charge for transactions you carry out yourself (using KBC-Phone). • If you require assistance from a member of the KBC-Telecenter team (in the evening, too), charges

will be the same as in your branch. KBC-Phone KBC-Telecenter What do you need? - a touch-tone phone or a mobile

- your customer number and secret PIN (ask for them at your bank branch)

Opening hours 7 days a week, 24 hours a day

Weekdays: 8 a.m. – 10 p.m. Saturdays: 9 a.m. – 5 p.m. Bank holidays: 9 a.m. - 5 p.m.

Transactions Account information (balance, recent transactions and KBC Payments Diary)

√ ☺

Transfer orders √ ☺ Standing transfers, transfers with free-text references

☺

Investments (KBC investment funds, KBC time deposits, KBC certificates, buying/selling shares)

☺

Order forms, foreign currency and traveller's cheques

☺

Change your PIN √ √ = Handle your banking business yourself and save money ☺ = Have a KBC employee take care of things for you If you’re interested, ask for a PIN, customer number and the handy memo booklet at your bank branch, and you can get started straight away.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

If you have any general queries, call the KBC-Telecenter on 03 299 11 44. Another free, KBC service. You won't need a PIN, so you won't be able to carry out any transactions. Naturally, you can always contact or visit your KBC bank branch during banking hours.

KBC-Online What do I need to be able to carry out my banking via my PC? To be able to effect your transactions online and in real-time, in addition to your PC you need access to the Internet. If you’re not yet connected to the Internet, KBC will be happy to help – free of charge, of course! KBC-Online Browser application The KBC-Online Browser application lets you work online and has the following options: Personal financial overview

• an aggregated overview of the assets and obligations, and a summary of the products and services purchased

Basic functions • account information (balances, transactions going back the previous 90 days)

• statement of account print-outs on A4 (legally valid statements of account)

• transfers: • domestic payments between own accounts/to other accounts • manage domestic beneficiaries (max. 30 beneficiaries) • transfers to other accounts abroad

• payments diary administration • display facility • delete facility

• electronic orders • standing orders/automatic savings:

• displaying • enter • manage

• displaying direct debit orders • display credit card billing statement

Investments: • portfolio (investment advice, e-portfolio) • manage • display • optimize

• displaying custody account • KBC Term Investments

• View registered term investments and registered term investments in bearer form which are still running: • KBC Time Deposit and KBC Capitalization Accounts in euros and

in foreign currencies • KBC Deposit Accounts in euros and in foreign currencies • KBC Capitalization Account • KBC Savings Certificates • Time Deposit Account Issues • KBC Subordinated (Plus) certificates and time deposit accounts

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

• Enter term investments: for info on and subscription to term investments: • KBC Time Deposit Accounts in euros and in foreign currencies • KBC Deposit Accounts in euros and in foreign currencies • KBC Capitalization Account • KBC Savings Certificates • KBC Subordinated (Plus) certificates and time deposit accounts

• Change destination of term investments: change of destination (of interest/capital on the payment/redemption date) of term investments

• making additional investments in pension savings account • KBC Investment Funds

• buy-into function • information on infosite • purchases during issue period • view and manage orders

• stock exchange orders: Euronext Brussels, Paris, Amsterdam; Nasdaq Europe; Luxemburg, Frankfurt, London, EuroNM, Nasdaq, NYSE,AMEX:• buy and sell orders • outstanding orders (display, change3, cancel³) • filled orders (display) • cancelled orders (display)

• investment insurance – manage KBC Life Invest Plan • investment plans – overview and management

Insurance: • manage KBC Life Invest Plan • insurance overview

Credits • display credits Financial markets • exchange rates

• stock exchange statistics • most commonly traded shares • key figures, fixing market

• quantity and turnover • hit parade Belgian securities

• key figures second market • quantity and turnover • hit parade Belgian securities • top 5 turnover

Online messages: You can send reports to the bank branch where you have either your KBC-Online subscription or your account.

Internet access: AT&T Internet access (request codes to access Internet). KBC-infosite: Access to a wide range of information via the KBC-infosite.

3 the change and cancel functions can only be used for orders that the client himself has entered via KBC-Online; the display function

is for stock exchange orders that the client has placed via KBC-Online + his KBC Bank branch.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

What does KBC-Online Local have to offer? If you want more options than those offered by the KBC-Online Browser application, you can subscribe to KBC-Online Local, as well. KBC-Online Local allows you to work offline with a host of options – for just 1 euro per month. Beneficiaries: • dividing beneficiaries into groups

• archiving fixed data (amount, reference) • selecting a beneficiary in the transfer form (for instance, via first 3 letters

of the name or by dragging an icon to the file)

Domestic payments: • sending up to 50 orders in one go • saving payment orders if they are not to be transmitted straightaway • overview of payment orders already sent • rapid-transfer mode

Account information: • balance and detailed info relating to account

• wider search function • export info to, for instance, Excel

Reports: for more complex searches using various selection and sorting criteria

Payments diary: save orders offline (orders must be cancelled via the payments diary menu

item in the KBC-Online Browser application)

Profiles: you can use a profile to have certain tasks carried out at regular intervals (e.g., downloading information for a particular account once every week or month)

Remittance folder: all payment orders you prepare are sent to the remittance folder and transmitted to the bank when you establish a connection

Paying online For all information on the KBC payment button and the KBC Shopping Mall, please visit our website www.kbc.be/ebancassurance.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Sheet 8: Managing investments ‘I note that individual advice on investments and portfolio management also comes with the Expat Convenience Package.’ Correct. KBC has built up a solid reputation as an innovator in the investment market and every KBC branch has its own investment adviser, someone whose profession is investment and who is there to provide you with individual advice when you want it. Someone, too, whose first action will be to listen to you, hear what your long- and short-term objectives are, what level of investment you plan and what level of risk you want to accept. Drawing on the huge range of successful investment products available, you and your personal investment adviser, together, can then compile an individual portfolio for you, tailored exactly to your specific requirements. If you have no time to keep close track of your investments or prefer to trust to the judgement of experts, our KBC investment specialists will be happy to manage your portfolio for you, via the exclusive KBC Managed Portfolios service. Once they have determined your aims and personal wishes, they will set them out in a contract and thereafter continually check to see how appropriate your investments are in the light of financial and economic developments. They make investment decisions independently, though naturally on the basis of your aims as set out in the contract. At least twice a year you will receive a status report, an overview of your portfolio and of the transactions carried out during the preceding period. Your adviser will also be quick to anticipate changing market conditions, and is kept fully up to date on the latest interesting opportunities by the KBC’s team of experts and our central information system. Furthermore, you may qualify for ‘non-resident’ status for tax purposes, if it is deemed that your domicile is not in Belgium. Should you then wish to invest in Belgium, the law provides a number of very interesting tax breaks. For example, you will be exempt from paying withholding tax on income from certain investments, and your heirs will not be liable for Belgian estate duty on personal property. Your KBC branch will naturally help you with all the necessary administrative formalities.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Sheet 9: Application to open an account (natural person) If you decide to begin a banking relationship with KBC, call round as we suggest – a person-to-person meeting is always preferable for both parties. Indeed, many problems can be avoided or solved in advance if expats contact us on their preliminary visit to Belgium to make arrangements for their job or accommodation. Failing that you may, of course, simply complete and return this application form if you would like to open an account; this will enable us to prepare the initial documentation and send it off to you (usually by registered post). It may also be there is an existing procedure with your employer for opening an account, so please check first. Surname: First name(s): Sex: male Nationality: Date of birth: Place of birth: In case of a joint account: please also mention your partner’s identity Surname: First name(s): Sex: Nationality: Date of birth: Place of birth: My partner and I are:

O married O living together without being married

Address in your home country: Street + No.: Box No.: Postcode: Town/city: Country: Tel.: Fax: E-mail: Employer/Institution: Function: Tel.: Fax: E-mail: Belgian address to which correspondence should be sent after arrival to Belgium: Street + No.: Box No.: Postcode: Town/city: Country: Belgium Tel.: Fax: E-mail: Address to which account information should be sent for official purposes (e.g., your employer): Street + No.: Box No.: Postcode: Town/city: Country: Tel.: Fax: E-mail: Signature: Place: Date:

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Please send, fax or mail to: KBC Expats Dept. – ASG A.M. Azijn – L. Verhoeven Havenlaan 2 B-1080 Brussels BELGIUM Tel.: 00 32 (0)2-429.18.57 Fax: 00 32 (0) 2 429 11 98 E-mail: [email protected] Please Note Official proof of identity (a photocopy will suffice) mentioning your official address is required to be submitted with this application. The completion and signing of the present form in no way obliges KBC Bank effectively to open an account. The opening of an account can be proceeded to only after the documents submitted have been verified and all enquiries made that KBC Bank deems useful or necessary. Normal practice is that, until there is a person-to-person meeting – which may be no later than 2 months after you return your application form – no cash transactions can take place and a ceiling of 10 000 euros per transaction or per week will apply. The applicant expressly authorizes KBC Bank to obtain from domestic and foreign financial institutions, insurance companies, his/her employer, public and private data bases, governments and all authorities and persons all information that it deems necessary to satisfy itself of the existence and capacity of the applicant. The cost of such enquiries may be charged to the applicant. The applicant will receive a copy of the General Regulations Governing Banking Operations, whose application to all his/her accounts and/or securities deposits he/she is required expressly to accept.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Sheet 10: Renting or buying property Renting General information In order to rent accommodation in Belgium, a lease is a legal requirement. Also, landlords generally require a rent guarantee by way of security deposit equal to three months’ rent, to be put up immediately when the lease is signed. Its main purpose is to cover any damage a tenant may cause to the property rented or any non-fulfilment on the part of the tenant of such obligations as paying the rent and or the charges (water, electricity, etc.). The rule is ‘no guarantee – no key’. To avoid disputes over damage caused during the tenancy, and any subsequent withholding of the rent guarantee by the landlord, it is important to mutually agree on the condition of the property before and after occupation (see Detailed description below). Lease Terms Before signing a lease contract on a property in Belgium, you need to know what the rights and obligations are of both the landlord and the tenant. Have someone with relevant experience read the contract, and remember that, if mutually agreed, the contract can be amended. Duration Standard Belgian leases are for 3-6-9 years. Penalties are liable for termination within the first three years. If the lease is broken after one year, the penalty is three months’ rent; after two years – two months’ rent, and after three years – one month’s rent. After that, no penalties can be invoked. Agree a standard notice period with the landlord and make sure that the lease contains a ‘diplomatic clause’ which will release you from the contract if you have to move abroad at short notice. If you have to break the lease, you must notify the landlord by registered letter as soon as possible. When the lease is approaching the end of its term (e.g., after the first three years), if you do not notify the landlord three months in advance that you are leaving, it will be presumed that you will be continuing to lease the property. Registration You can register the lease at the Ministry of Finance tax office of the commune where the property is located. Registration is in the interest of the tenant because, if the property is sold, the new owner cannot expel the tenant. There is a fee for this registration. Charges Charges normally borne by the tenant include gas, electricity, heating oil, water, local taxes (incl. garbage collection), chimney sweeping, servicing of heating installation (and water softener if fitted) and gardening. The property tax is the responsibility of the landlord. Detailed description (état de lieu/staat van het huis) In order to ensure a fair evaluation of damage versus normal ‘wear and tear’ during a tenancy, and thereby recover a fair proportion of your security deposit (see below), it is very important to get a detailed description of the condition of the property (building and gardens) at the beginning and at the end of the lease term. This can be done by way of a simple written agreement signed and dated by landlord and tenant or, more formally, by a property surveyor (expert). He will inspect the premises thoroughly and submit his report. This service costs in the region of 200 euros. You then normally have one month to add any other damages missed in the surveyor’s report.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Rent guarantee In addition to the fact that your lease will require you to be insured for damage to the property (see below under Home insurance), you are normally required to put up a rent guarantee as a security deposit. This is usually equal to three months’ rent and can be arranged via a bank guarantee or you can transfer the rent guarantee to a blocked bank account specially opened for the purpose. What you opt for depends on your requirements. Note: Neither cash nor securities should be handed directly to the landlord as guarantee. A blocked account bears interest for the tenant and requires both the tenant’s and the landlord’s signature for access. If you choose this option, KBC will issue a deposit certificate. Upon termination of the lease, agreement is reached on the amount to be deducted, if any. The advantages of the blocked account are that it is easy and rapid to open and that, as mentioned, it bears interest for the tenant. To establish a rent guarantee by means of a blocked account offers many advantages, but sometimes (perhaps due to funds being tied up in savings) expatriate tenants may not be able to instantly lay their hands on the amount required to establish the full guarantee. The Pinto Visa card, which is part of the Expat Convenience Package, can provide the solution to this problem as it can be used to withdraw cash for the deposit required for the rent security account. You then settle the debt to Pinto Visa at your own pace, in line with your financial possibilities. Power of attorney If you find your future home prior to taking up your position in Belgium, you may value having a representative here who is authorized, in your absence, to undertake certain important administrative procedures on your behalf. These may include finalizing the rent guarantee, overseeing the detailed description of the property, organizing timely insurance of the property, etc. The representative could be your local personnel manager or a representative from your relocation company. You will find enclosed a copy of the Power of Attorney (Sheet 10a) and Home Insurance Checklist (Sheet 10b). ‘With the Expat Convenience Package, you also offer the possibility of obtaining a KBC Bank rent guarantee. What does that involve?’ The KBC rent guarantee is a bank guarantee in favour of the landlord and for account of the tenant. Please note, however, that a rent guarantee is not given automatically and is not free of charge. A rent guarantee request does incur a file-administration charge and there is also a quarterly fee. Limitations may be built in as regards duration, amount and the conditions under which the guarantor would be released from its obligations. Furthermore, as a bank guarantee is a type of loan, a prior analysis of the credit risk is required and interest (three-monthly) has to be paid on it. The advantage of the bank guarantee is that your funds are not blocked until the end of the rental period, but are free to earn a higher interest or be used for buying furnishings, etc. A number of employers maintain a policy of themselves either providing the bank guarantee or standing security for it vis-à-vis the bank, so consult your employer before making any other arrangements. Utilities ‘Making sure I’m connected to the various utilities and telephone and cable TV services is up to me, as a tenant, isn’t it? Yes. All that we can do is to give you some general information. First of all, you should check with your local municipal authority to find out the names of the companies supplying your gas, electricity and water. Certain of these authorities require one or other document (issued by themselves) certifying that you will be occupying the premises. In any event, have your identity card and the lease with you when you go to collect the document.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Requests for gas and electricity connections should be made to the company concerned in good time - no later than one week before the connection is required. You will need to present your identity card when requesting the connection. You will also need to be available when they come around to hook you up (you’ll be notified of the date in advance), to allow the agent access to the premises and to sign for the connection on completion of the work. If you are not available, you may appoint a proxy to represent you, and that person should be in possession of a photocopy of your identity card. For water, you should write to the company concerned, mentioning the address of the premises, your name and the date the tenancy took effect, as well as the meter reading at that time. The letter should be signed by you and the landlord. A visit by a company agent is necessary only if the meter has been shut off. As regards a phone service, you can opt for a mobile phone (in which case you should get in touch with Mobistar, Proximus, Base, etc.) and/or a connection to the regular telephone network. Although Belgacom is the only company that handles connections, once yours has been installed, you can choose a supplier - Belgacom or Telenet, for instance. Application forms for telephone connection can be obtained from teleboutiques. The telephone company will fix a time for the connection and it is absolutely necessary that someone be present then. Your local municipal authority will also give you the name of your local cable TV distribution company. All TV users (even those without cable TV) are required to pay a TV and radio fee, which is billed separately from the cable TV subscription charge. There are, of course, regularly recurring charges for all these services. As pointed out above, it will often happen that the payee (the water company, etc.) will send you a transfer form virtually fully completed in advance, which you only have to complete and send to your KBC branch for execution. Again, don’t forget that you can opt for the direct debit or standing order to take care of these outgoings, as well as your rent payments. Just ask your KBC branch for details. A final point to note is that some companies require a guarantee for the opening of a meter. The amount involved is generally too small to qualify for a bank guarantee being issued, but can normally be dealt with by means of a direct debit, which companies are happy with. Home insurance ‘I’ve heard that, as a tenant, I need to take out separate home insurance. Is that correct?’ Absolutely. The Belgian Civil Code states that (with three exceptions: act of God, hidden fault in construction, spreading fire) anyone causing damage to the property of another is responsible for that damage, unless it can be proved that he or she was not at fault. On this basis, even though it may seem unusual to the Expat, tenants are responsible for damage caused during their occupancy, including damage caused by fire and water, and broken glass in windows and doors, etc. They must therefore insure against this risk, even though the landlord holds a similar policy. Indeed, the lease may stipulate that the tenant is required to take out liability cover and will sometimes give a precise amount that has to be insured (e.g., 200 000 euros). Occasionally, the landlord may stipulate what in Belgium is known as an ‘abandon de recours contre les locataires’, in which case the tenant does not need to take out liability cover. Your KBC branch or KBC agent will be happy to check this for you and arrange the necessary formalities, if you bring in your lease contract. One thing you should check yourself – if you haven’t already done so, of course – is whether your company pays for its Expats’ tenant liability cover and has already arranged for it. It is in any case important to be sufficiently insured, so that the landlord’s claims for compensation against you can be met in full, if the need arises. One system used for apartments in Belgium to ensure sufficient coverage is to multiply the yearly rent (including charges, but not utilities) by a factor of 20 and take the consequent amount as the property’s value. We do not apply that system at KBC, as we believe that it can lead to your being substantially overinsured. Instead, we use an evaluation grid.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Note: The standard lease contract states that the tenant must provide proof of insurance to the proprietor within 30 days after signature of the lease (a copy of your bank statement detailing payment of the premium for your household policy will suffice). All insurance contracts are for one year and are renewed automatically, unless instructions to the contrary are received. If you leave Belgium before the insurance contract is due to expire, it will be cancelled and your premium refunded pro rata to the day. The KBC Home policy covers your home against ‘all risks’. This means that any unexpected damage is insured, unless it is expressly excluded in the policy. So if you have damage, you never have to prove that this damage is caused by a risk that is insured in the policy. In contrast, the insurer must be able to show that a particular damage is not insured. In other words: the burden of proof lies with the insurer. Another advantage of such an ‘all risks’ policy is that events of loss are also covered that were not even considered when the policy was drawn up. So there are no uncertainties for the future. If you want, the contents of your home can also be insured against ‘all risks’. Even insured against theft and natural disasters The KBC Home policy also covers your home and its contents against earthquake, flooding and theft. The natural disasters insurance protects against disasters even if they are not ‘recognised’ as such by the authorities. The theft cover is not only valid in your home itself. Also outside the home, there is cover of up to a maximum of 5 000 euros against: - theft from your garden, for example of garden furniture; - violent theft in the street, of which yourself, your spouse or members of the family that live with you are the victim, and wherever in the world the theft takes place; - travel theft, for example of baggage or your movables that are temporarily displaced to a holiday residence. Here, there is the condition that the theft must be associated with breaking and entering, violence or threat. A broad cover With a KBC Home policy you are insuring more than just your home. This fire insurance also covers your liability for damage to a holiday residence (hotel room, cottage, etc), to premises or a marquee that you are hiring for family celebrations, to your childrens’ residence during their studies, to the individual garage that you are renting somewhere else for private use. Even the movables that you have moved there temporarily always remain insured. Furthermore, a unique form of assistance is linked to the KBC Home policy with a broad provision of services regarding damage. So, for example, if you need a roof over your head temporarily (hotel or other temporary accommodation), the house is secured, and what remains of your movables is stored safely. You can also count on home help if you have to be admitted to hospital due to an event of loss. Please note, however, that it can only be taken out with KBC as an adjunct to existing insurance cover with us, or if you are transferring an existing policy to us. Another option is family liability insurance (also known as third-person liability), which protects the head of the household against claims for damages by third parties. The cover extends to all persons for whom he or she is responsible, including children of friends staying even temporarily on the household premises or accompanying the household elsewhere; it also extends to pets. The coverage is extensive and includes legal assistance, an important consideration. The KBC Household Policy can also include insurance for domestic help, cover for the head of the household against claims by part-time and occasional employees, such as a baby-sitter, cleaner or a temporary gardener (there is no obligation to name such employees in the policy). Under Belgian law, the employer is responsible for any injury suffered by such persons while they are working or on their way to and from the household premises, and insurance is compulsory. The employer remains legally responsible, even if the individual is working illegally or his or her earnings are undeclared.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Our household policy is thus pretty comprehensive. Besides all the above, there is also cover for damage to real estate caused by burglary, even if you don’t have separate burglary insurance. This basic cover can be extended with additional cover (for theft exterior to the premises, for example). As a tenant, it is important to note that your home is insured for its real value (home insurance, by the way, is often called fire insurance, but there is, in fact, no separate category for fire). Our starting point is always the real cost of the damage, even if it is unexpectedly high. There is also the additional security of free temporary accommodation if your home is so damaged as to be uninhabitable. If necessary, your home will be subject to one or other form of security check during your absence to ensure it does not suffer further damage and that nothing is stolen. Please note that KBC does not itself conduct security checks, but merely pays their cost. Hospitalization insurance A KBC Hospitalization Policy is also available, which provides reimbursement of hospitalization costs not covered by general health insurance, besides having several other interesting features. In the event of hospitalization or a death in the family, you can also count on child-minding facilities and a home-help, if necessary. And if you happen to be abroad at the time of the incident, repatriation is taken care of. Don’t forget, however, to check with your employer whether a hospitalization clause is in your contract.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Buying property ‘Supposing that I opt to buy rather than rent accommodation, what then?’ Buying property in Belgium requires a deed of purchase to be drawn up by a notary public. That apart, very much the same applies as in the case of rented property, meaning that you will require insurance cover (for details, see KBC Household Policy above) and connections with the gas, electricity, water and telephone services, etc. (again, see above for details). You may also wish to take out a mortgage loan. KBC offers you a number of alternatives, again tailored to suit your specific requirements. Before you take out a loan, however, you will receive comprehensive advice and information on loans, covering such items as the monthly repayments, the cost of the deed of loan and any possible government grants or tax limitation schemes. This ensures that you have the full figures in front of you and will not be confronted with any unpleasant surprises in the future. The KBC Home Loan offers three basic repayment alternatives: 1. Equal monthly instalments: each instalment comprises both a payment of interest and a repayment of principal. The initial instalments consist predominantly of interest, and the final instalments predominantly of principal. Formulas are available with either a fixed or variable rate of interest. 2. Equal principal repayments: with this scheme, the interest portion of the instalment naturally diminishes over time, so that the instalment payments will be progressively lower. Compared to a loan with equal monthly instalments, this option means that you will pay less interest overall, although the initial repayments will be higher. Here, too, there are formulas available with either a fixed or variable rate of interest. 3. Lump-sum repayment of principal: in this case, the loan is repaid through monthly instalments comprising interest only and a final instalment comprising interest and the full amount of the principal. Again, formulas are available with either a fixed or variable rate of interest. One specific form of a home loan with lump-sum repayment of the principal is the bridging loan, allowing you to cover the period between the purchase of a new and the sale of an existing property. Variable-rate KBC Home Loans have terms varying from 3 to 30 years. Fixed-rate KBC Home Loans have a maximum term of 20 years. If you select a variable-rate KBC Home Loan, at each contractual interest rate review, we offer you three free options: 1. Switch to another variable-rate option. Say, for example, that you originally chose the option whereby the interest rate is subject to change every 5 years. Then, at the first contractual interest rate review, you can switch – without charge - to an annual interest rate change or opt for the 10-5-5 formula. 2. Change the repayment system. At any contractual interest rate review, you can change from equal monthly instalments to diminishing monthly instalments or vice versa. 3. Either extend or shorten the remaining term of your home loan.

KBC Bank NV, Havenlaan 2, 1080 Brussel edition 8-1-2007

Sheet 10a: Power of attorney With this form you give your local personnel manager or a representative from your relocation company authorization – in your absence – to undertake certain administrative procedures on your behalf. I, ………………………………………., hereby authorize ………………………… to act on my behalf, when necessary, in all matters relating to the rental of my apartment / house, i.e.: