the increasingly important connection between the e-world and the p-world adventis perspective and...

TRANSCRIPT

The Increasingly Important Connection Between the e-World and the p-World

ADVENTIS Perspective and Prescriptions

Fall 2000

ADVENTIS CORPORATION

200 Berkeley Street, 22nd FloorBoston, MA 02116

Telephone: 617.421.9990Fax: 617.421.9994

ADVENTIS CORPORATION

200 Berkeley Street, 22nd FloorBoston, MA 02116

Telephone: 617.421.9990Fax: 617.421.9994

The Increasingly Important Connection Between the e-World and the p-World

ADVENTIS Perspective and Prescriptions

Fall 2000

1. Introduction To ADVENTIS

4Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

ADVENTIS: Heritage and Horizons

We were founded in 1993 to provide expert management and strategy consulting focused on the converging global information industries.We were founded in 1993 to provide expert management and strategy consulting focused on the converging global information industries.

Since our inception, we have maintained industry leading growth and financial performance. We have consistently achieved 60% annual growth and now have over 200 consultants and offices in Boston, Chicago, London, New York, San Francisco, and Washington, D.C.

Since our inception, we have maintained industry leading growth and financial performance. We have consistently achieved 60% annual growth and now have over 200 consultants and offices in Boston, Chicago, London, New York, San Francisco, and Washington, D.C.

To mark our March 2000 separation from our former parent Renaissance Worldwide, and to underscore our expertise in applying Real Economy Values to Next Economy Strategies, we changed our name in October 2000 to ADVENTIS.

To mark our March 2000 separation from our former parent Renaissance Worldwide, and to underscore our expertise in applying Real Economy Values to Next Economy Strategies, we changed our name in October 2000 to ADVENTIS.

Our new name captures the essence of who we are and what we do for clients every day, anticipating and harnessing convergence, enabling breakthrough results in the Next Economy.

Our new name captures the essence of who we are and what we do for clients every day, anticipating and harnessing convergence, enabling breakthrough results in the Next Economy.

5Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

The Premier Strategy and Management Consultancy to the Global Information Industries

• We Make Strategy Work, By Helping Clients Harness Convergence

• We Are Not Generalists—We Focus on the Converging Global Information Industries:

- Communications- Computing - Commerce- Content

• Six Global Offices:- Boston- London- San Francisco

• Entrepreneurial Growth- Established in 1993- 60% compound annual revenue growth - Over 200 staff

- Chicago- New York- Washington

Applying Real Economy Values to

Next Economy Strategies™

Blue Chip and New Chip Clients

Breakthrough Capabilitieswith Measurable Impact

PeerlessIndustry Focus

6Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

ADVENTIS: Our Core Values Enable Us to Relentlessly Pursue Our Mission

Our MissionOur Mission

To Help Clients Apply Real Economy Values to Next Economy Strategies by Harnessing the Power of Convergence

To Help Clients Apply Real Economy Values to Next Economy Strategies by Harnessing the Power of Convergence

Our ValuesOur Values

• FocusedWe are deeply specialized in the converging 4Cs of the Next Economy.

• SmartWe bring clarity to alarming complexity.

• CreativeWe see the whole picture and we are blazing new paths to a convergent future we are helping to create.

• FlexibleWe are rigorous and disciplined yet adapt adroitly to our client’s changing needs.

• FriendlyWe enjoy working with our clients and take our work very seriously, but we don’t take ourselves all that seriously.

• DependableWe are trustworthy, dedicated, and professional. We do whatever it takes to get the job done. Period.

• FocusedWe are deeply specialized in the converging 4Cs of the Next Economy.

• SmartWe bring clarity to alarming complexity.

• CreativeWe see the whole picture and we are blazing new paths to a convergent future we are helping to create.

• FlexibleWe are rigorous and disciplined yet adapt adroitly to our client’s changing needs.

• FriendlyWe enjoy working with our clients and take our work very seriously, but we don’t take ourselves all that seriously.

• DependableWe are trustworthy, dedicated, and professional. We do whatever it takes to get the job done. Period.

7Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

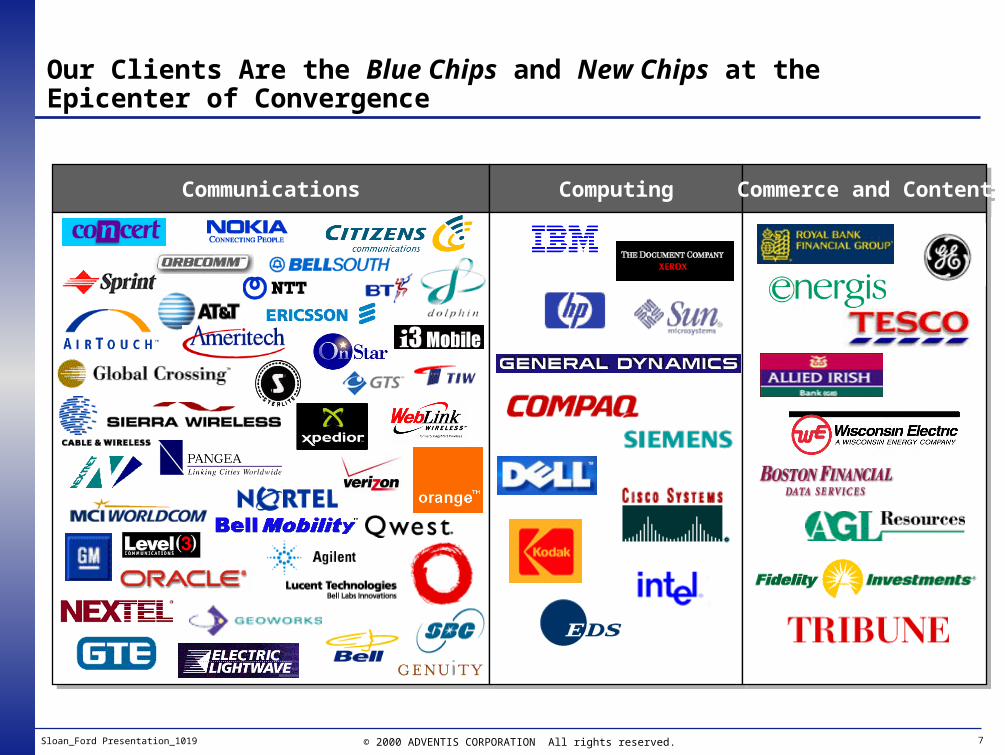

Our Clients Are the Blue Chips and New Chips at the Epicenter of Convergence

CommunicationsCommunications ComputingComputing Commerce and ContentCommerce and Content

8Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

ADVENTIS Expert Commentary on the New Economy’s Issues Is Frequently Featured in the World’s Leading Business Media

We provide penetrating and provocative commentary on key industry developments and original thinking on breakthrough strategies and approaches

We provide penetrating and provocative commentary on key industry developments and original thinking on breakthrough strategies and approaches

9Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

ADVENTIS Helps Business Leaders Establish and Implement Their Convergence Destination, Navigation, and Mobilization

Business CreationBusiness CreationBusiness RenewalBusiness Renewal

• Newco Future Mapping• e-Business Strategy Blueprint• Ecosystems Beachhead Mapping• ASP Market Blueprint

• Strategic Architecture• Opportunity Blueprint

• Market Segmentation• Solutions Growth Blueprint• Technology Commercialization

• Newco Future Mapping• e-Business Strategy Blueprint• Ecosystems Beachhead Mapping• ASP Market Blueprint

• Strategic Architecture• Opportunity Blueprint

• Market Segmentation• Solutions Growth Blueprint• Technology Commercialization

• Enterprise Scan• e-Commerce Engine• M-Commerce Blueprint

• Business Model Redesign• Best Practices Benchmarking

• Rapid Strategy Realization• Business Engine Re/Design • Activity Based Management• Integrated Supply Chain

• Enterprise Scan• e-Commerce Engine• M-Commerce Blueprint

• Business Model Redesign• Best Practices Benchmarking

• Rapid Strategy Realization• Business Engine Re/Design • Activity Based Management• Integrated Supply Chain

Performance ManagementPerformance Management

• Strategic Performance Management Scorecard• Shareholder Value Creation • Knowledge Enabled Processes

• Quick Hit and Breakthrough Implementation• Change Management• Leadership and Skills Development

• Strategic Performance Management Scorecard• Shareholder Value Creation • Knowledge Enabled Processes

• Quick Hit and Breakthrough Implementation• Change Management• Leadership and Skills Development

ConvergenceDestination

ConvergenceDestination

Convergence Navigation

Convergence Navigation

Convergence Mobilization

Convergence Mobilization

Power Tools

2. ADVENTIS Viewpoint On Winning Strategies to Connect the e-World and the p-World

11Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

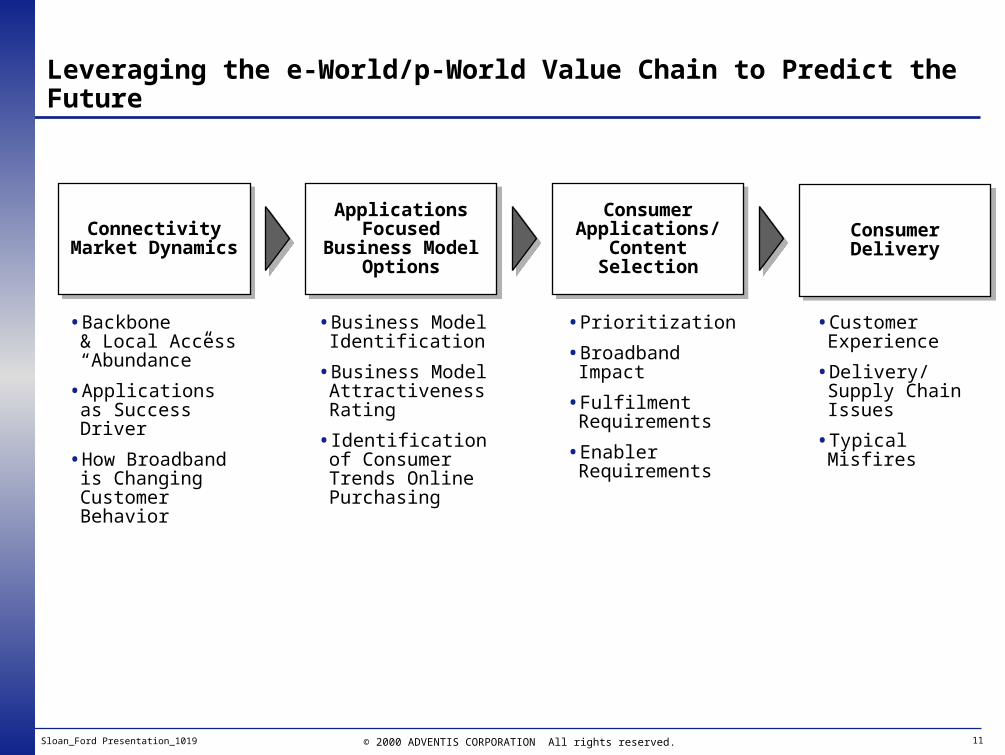

Leveraging the e-World/p-World Value Chain to Predict the Future

Connectivity Market Dynamics

Connectivity Market Dynamics

Applications Focused Business

Model Options

Applications Focused Business

Model Options

Consumer Applications/

Content Selection

Consumer Applications/

Content Selection

• Backbone & Local Access “Abundance”

• Applications as Success Driver

• How Broadband is Changing Customer Behavior

• Business Model Identification

• Business Model Attractiveness Rating

• Identification of Consumer Trends Online Purchasing

• Prioritization

• Broadband Impact

• Fulfilment Requirements

• Enabler Requirements

Consumer DeliveryConsumer Delivery

• Customer Experience

• Delivery/Supply Chain Issues

• Typical Misfires

12Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

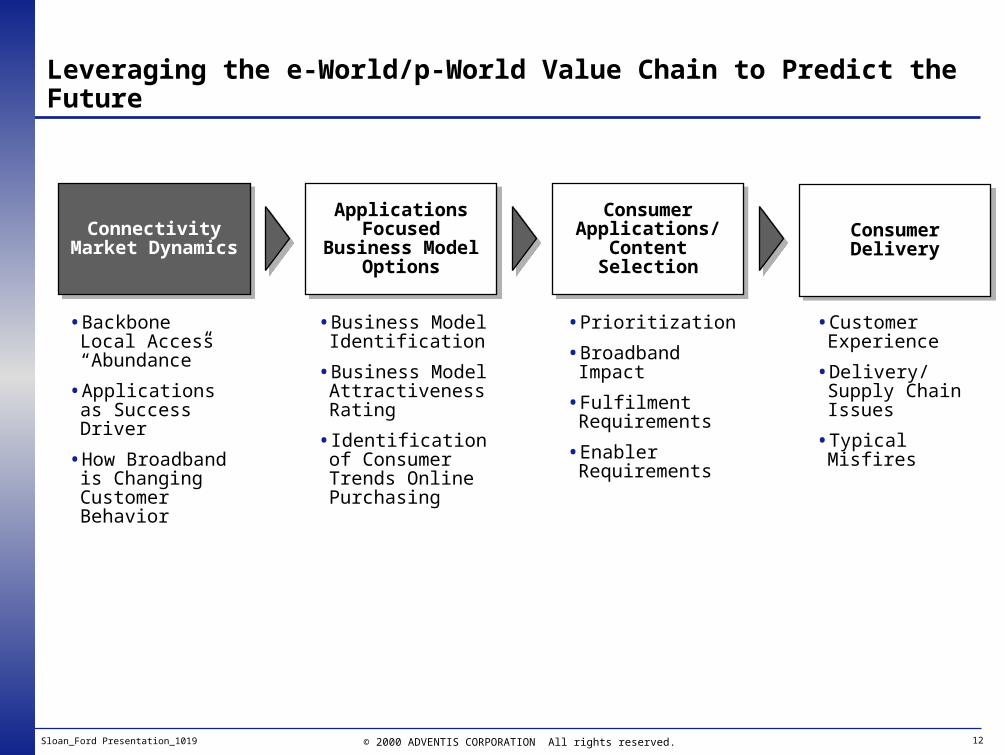

Leveraging the e-World/p-World Value Chain to Predict the Future

Connectivity Market Dynamics

Connectivity Market Dynamics

Applications Focused Business

Model Options

Applications Focused Business

Model Options

Consumer Applications/

Content Selection

Consumer Applications/

Content Selection

• Backbone Local Access “Abundance”

• Applications as Success Driver

• How Broadband is Changing Customer Behavior

• Business Model Identification

• Business Model Attractiveness Rating

• Identification of Consumer Trends Online Purchasing

• Prioritization

• Broadband Impact

• Fulfilment Requirements

• Enabler Requirements

Consumer DeliveryConsumer Delivery

• Customer Experience

• Delivery/Supply Chain Issues

• Typical Misfires

13Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Capital Abundance is Driving Bandwidth AbundanceCapital Abundance is Driving Bandwidth Abundance

Source: Brokers Reports, Textlines, Annual Reports, ADVENTIS Analysis

Fibers and Fibers Lit by Major Carrier 1999-2004

US NetworksUS Networks

Total # Fibers

(Incl. Not Lit)

TotalFibers Lit

1999

TotalFibers Lit

2004

0

100

200

300

400

500

600

SprintFrontierGTEMCI

AT&T

IXC

Williams

Qwest

Level (3)

508

1836

Nu

mb

er o

f F

iber

s

Capacity Build-Up On the Internet Is Disrupting Supply/Demand Balance–Pure Transport Players Will Be Threatened in This Environment

US Demand and Supply (Tbps)1999–2004Tbps

Demand

SupplyScenario 1

SupplyScenario 2

0

5

10

15

20

1999 2000 2001 2002 2003 2004

9 Tbps

18 Tbps

11 Tbps

Source: Renaissance Analysis, Telegeography, P Budde Communications Ltd, OECD, Pioneer Group, Brokers Reports, Textlines, Annual Reports

Scenario 1: One fiber pair lit, with no increase from 1999Scenario 2: Extra fiber pair lit by most players in 2000

14Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

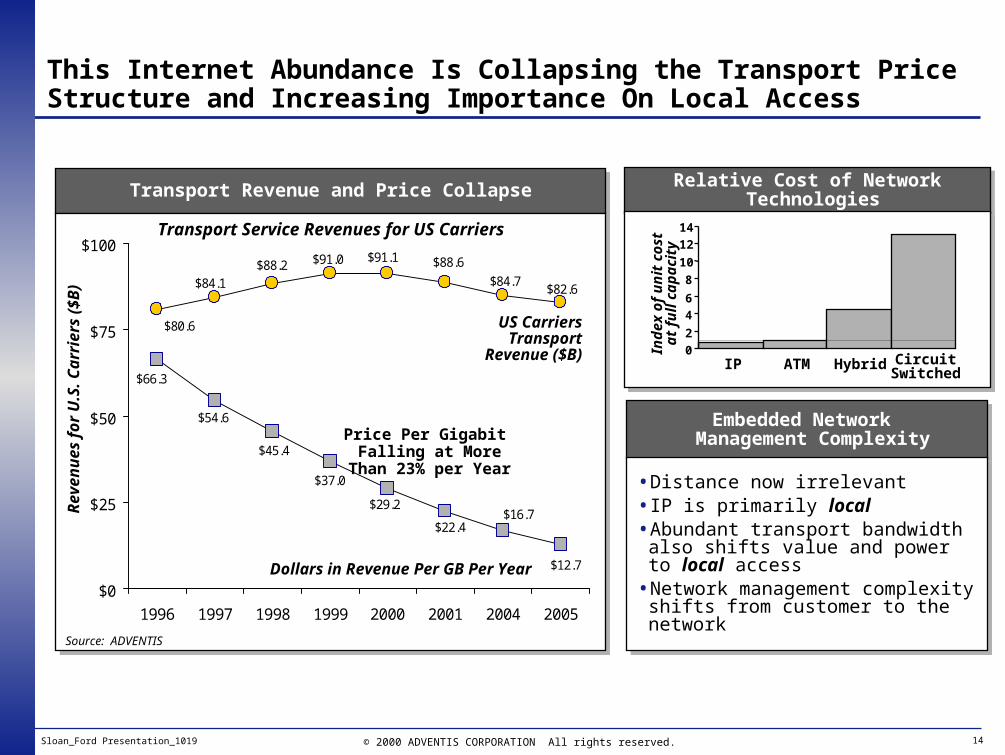

Transport Revenue and Price CollapseTransport Revenue and Price Collapse

Transport Service Revenues for US CarriersTransport Service Revenues for US Carriers

Embedded Network Management ComplexityEmbedded Network

Management Complexity

• Distance now irrelevant• IP is primarily local• Abundant transport bandwidth also

shifts value and power to local access• Network management complexity shifts

from customer to the network

• Distance now irrelevant• IP is primarily local• Abundant transport bandwidth also

shifts value and power to local access• Network management complexity shifts

from customer to the network

Re

ve

nu

es

fo

r U

.S.

Ca

rrie

rs (

$B

)

$12.7

$16.7

$45.4

$22.4

$29.2

$37.0

$66.3

$54.6

$82.6$84.7

$88.6$91.1$91.0$88.2$84.1

$80.6

$0

$25

$50

$75

$100

1996 1997 1998 1999 2000 2001 2004 2005

Price Per Gigabit Falling at More

Than 23% per Year

US Carriers Transport

Revenue ($B)

Dollars in Revenue Per GB Per Year

Relative Cost of Network TechnologiesRelative Cost of Network TechnologiesRelative Cost of Network Technologies

0

2

4

6

8

10

12

14

IP ATM Hybrid CircuitSwitched

Ind

ex o

f u

nit

co

stat

fu

ll c

apac

ity

Source: ADVENTIS

This Internet Abundance Is Collapsing the Transport Price Structure and Increasing Importance On Local Access

15Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Source: J.D. Power and Associates 2000 National Internet Service Provider Customer Satisfaction Study

Customer Satisfaction Index Weights: Internet/On-Line Service

The Present Focus on Price Has Is Leading Broadband Internet Access Towards Commoditization

Annual Local Access Revenue per Subscriber

$889

$391

$0

$200

$400

$600

$800

$1,000

1999 2003

Broadband Household Penetration

4.5

40.9

0

10

20

30

40

50

1999 2003

Households (millions)

Broadband Subscriber Revenue Growth

$16B

$4B

05

101520

1999 2003

Revenue (billions)

CAGR = 41.4%

CAGR = 73.6%

2000 2003

2000 2003

2000 2003

16Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

The Market Is Relatively Concentrated With AT&T Owning a 25% Share – With a Stock Price Reflecting a Commodity Position

Broadband SubscribersBroadband Subscribers

Source: Company Announcements, CyberData

• Facilities based players are the clear leaders

• Profitability of operators is questionable

• Operational issues (provisioning billing etc.) abound

• Equity markets no longer looking favorable on segment

• Facilities based players are the clear leaders

• Profitability of operators is questionable

• Operational issues (provisioning billing etc.) abound

• Equity markets no longer looking favorable on segment

0 200 400 600 800

Rythyms

Northpoint

Bell South

Adelphia

US West

Covad

Verizon

Comcast

Shaw

SBC

AT&T Broadband

Thousands

Q2-00

Q4-99

17Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Current Internet Users Reasons for Wanting BroadbandCurrent Internet Users Reasons for Wanting Broadband

Compelling Applications Increase Perceived Value of Broadband by Seven Fold– But Few Compelling Applications Exist

Source: The Yankee Group and ADVENTIS

Key Messages Propelling

Growth

Key Messages Propelling

Growth

Overall Penetration

Overall Penetration

Consumer Reaction

Consumer Reaction

SpeedSpeed Always OnAlways On Compelling ApplicationsCompelling

Applications

3 % Penetration3 % Penetration

Attractive to power users and home office workers

Attractive to power users and home office workers

10 % Penetration10 % Penetration 20 % Penetration20 % Penetration

Of the 22.5% of homes with multiple lines 32.2% say that they would drop one for “always on” high speed internet access

Of the 22.5% of homes with multiple lines 32.2% say that they would drop one for “always on” high speed internet access

Understand compelling power of:

• Productivity Applications

• Communications Application

• Entertainment Applications

Understand compelling power of:

• Productivity Applications

• Communications Application

• Entertainment Applications

New Application FocusNew Application Focus

• Development in Value Added Services and content offerings that demand a price premium and fill bandwidth supply

• Partnerships and alliances across the industry spectrum as providers team up with content providers to be able to give their customers the unique value proposition needed for them to switch to Broadband

• Content Providers are developing applications in an attempt to be the first to market with “the killer app” to make broadband real

• Investment in user infrastructure is necessary to utilize these applications and to create the “need” for broadband

• Development in Value Added Services and content offerings that demand a price premium and fill bandwidth supply

• Partnerships and alliances across the industry spectrum as providers team up with content providers to be able to give their customers the unique value proposition needed for them to switch to Broadband

• Content Providers are developing applications in an attempt to be the first to market with “the killer app” to make broadband real

• Investment in user infrastructure is necessary to utilize these applications and to create the “need” for broadband

18Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Leveraging the e-World/p-World Value Chain to Predict the Future

Connectivity Market Dynamics

Connectivity Market Dynamics

Applications Focused Business

Model Options

Applications Focused Business

Model Options

Consumer Applications/

Content Selection

Consumer Applications/

Content Selection

• Backbone Local Access “Abundance”

• Applications as Success Driver

• How Broadband is Changing Customer Behavior

• Business Model Identification

• Business Model Attractiveness Rating

• Identification of Consumer Trends Online Purchasing

• Prioritisation

• Broadband Impact

• Fulfillment Requirements

• Enabler Requirements

Consumer DeliveryConsumer Delivery

• Customer Experience

• Delivery/Supply Chain Issues

• Typical Misfires

19Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

There Are Five Business Model Internet Providers Are Using To Establish Stable Connection With the Consumer

Key Business Model Attributes

Key Business Model Attributes

Revenue ModelRevenue Model

OptionsOptions

Subscription, Advertising, Transactional Subscription, Advertising, Transactional

Product OwnershipProduct Ownership Owned, OutsourcedOwned, Outsourced

Service OfferedService Offered Connectivity, Context, Commerce, ApplicationsConnectivity, Context, Commerce, Applications

Stable Business ModelsStable Business Models

1. Wholesale Connectivity

2. Content Network

3. Portal Model

4. e-Commerce Model

5. Full-Service Network

1. Wholesale Connectivity

2. Content Network

3. Portal Model

4. e-Commerce Model

5. Full-Service Network

Target CustomersTarget Customers Mass, High EndMass, High End

20Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Bu

sin

ess

Mo

del

Bu

sin

ess

Mo

del

1. Content Network

1. Content Network

Business Models Add Value Through Distinct Combinations Of Activities

Provide Connectivity

Provide Connectivity

DevelopContent,

Commerce, and Applications

DevelopContent,

Commerce, and Applications

AggregateContent, Commerce,

and Applications

AggregateContent, Commerce,

and ApplicationsMarket and SellMarket and Sell Provide Customer

ServiceProvide Customer

Service

2. Wholesale Connectivity

2. Wholesale Connectivity

3. Portal Model3. Portal Model

- Consumer Service Value Chain -

4. eCommerce Model

4. eCommerce Model

5. Full Service Network

5. Full Service Network

ShipShip

21Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

1. Wholesale Connectivity

Pure-Play Connectivity Is Only Viable For Low Cost Providers

DescriptionDescription

• Pure-play connectivity consists solely of wholesale arrangements with Internet service providers and other customers, including enterprise and competing telecommunications providers

• Pure-play connectivity consists solely of wholesale arrangements with Internet service providers and other customers, including enterprise and competing telecommunications providers

PlayersPlayers

• Covad

• Northpoint

• Rythms Netconnection

• Covad

• Northpoint

• Rythms Netconnection

Service OfferedService Offered

ConnectivityConnectivity ContentContent CommerceCommerce ApplicationsApplications

Target SegmentsTarget Segments Target SegmentsTarget Segments Target SegmentsTarget Segments Target SegmentsTarget Segments

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Re

ve

nu

e M

od

el

Re

ve

nu

e M

od

el

Tra

nsa

ctio

nT

ran

sact

ion

Ad

vert

isin

g A

dve

rtis

ing

Su

bsc

rip

tio

n S

ub

scri

pti

on

Pro

du

ctP

rod

uct

Pro

du

ct P

rod

uct

Pro

du

ctP

rod

uct

Ou

tso

urc

edO

uts

ou

rced

O

wn

ed

Ow

ned

Ou

tso

urc

edO

uts

ou

rced

O

wn

ed

Ow

ned

Ou

tso

urc

edO

uts

ou

rced

Ow

ned

Ow

ned

22Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

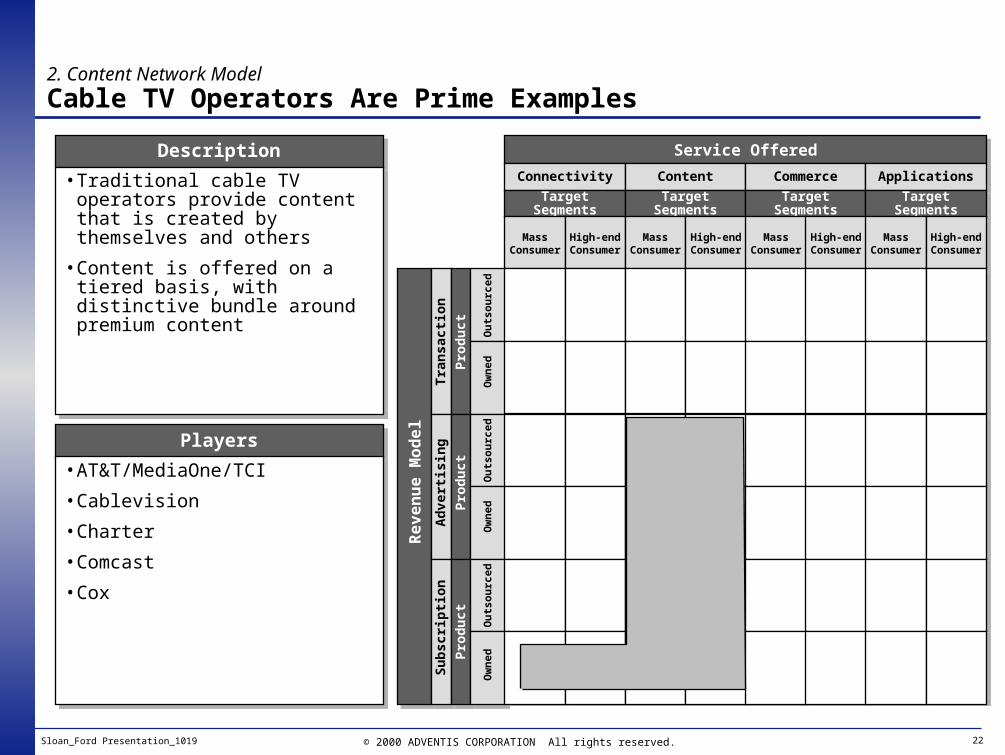

2. Content Network Model

Cable TV Operators Are Prime Examples

DescriptionDescription

• Traditional cable TV operators provide content that is created by themselves and others

• Content is offered on a tiered basis, with distinctive bundle around premium content

• Traditional cable TV operators provide content that is created by themselves and others

• Content is offered on a tiered basis, with distinctive bundle around premium content

PlayersPlayers

• AT&T/MediaOne/TCI

• Cablevision

• Charter

• Comcast

• Cox

• AT&T/MediaOne/TCI

• Cablevision

• Charter

• Comcast

• Cox

Service OfferedService Offered

ConnectivityConnectivity ContentContent CommerceCommerce ApplicationsApplications

Target SegmentsTarget Segments Target SegmentsTarget Segments Target SegmentsTarget Segments Target SegmentsTarget Segments

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Re

ve

nu

e M

od

el

Re

ve

nu

e M

od

el

Tra

nsa

ctio

nT

ran

sact

ion

Ad

vert

isin

g A

dve

rtis

ing

Su

bsc

rip

tio

n S

ub

scri

pti

on

Pro

du

ctP

rod

uct

Pro

du

ct P

rod

uct

Pro

du

ctP

rod

uct

Ou

tso

urc

edO

uts

ou

rced

O

wn

ed

Ow

ned

Ou

tso

urc

edO

uts

ou

rced

O

wn

ed

Ow

ned

Ou

tso

urc

edO

uts

ou

rced

Ow

ned

Ow

ned

23Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

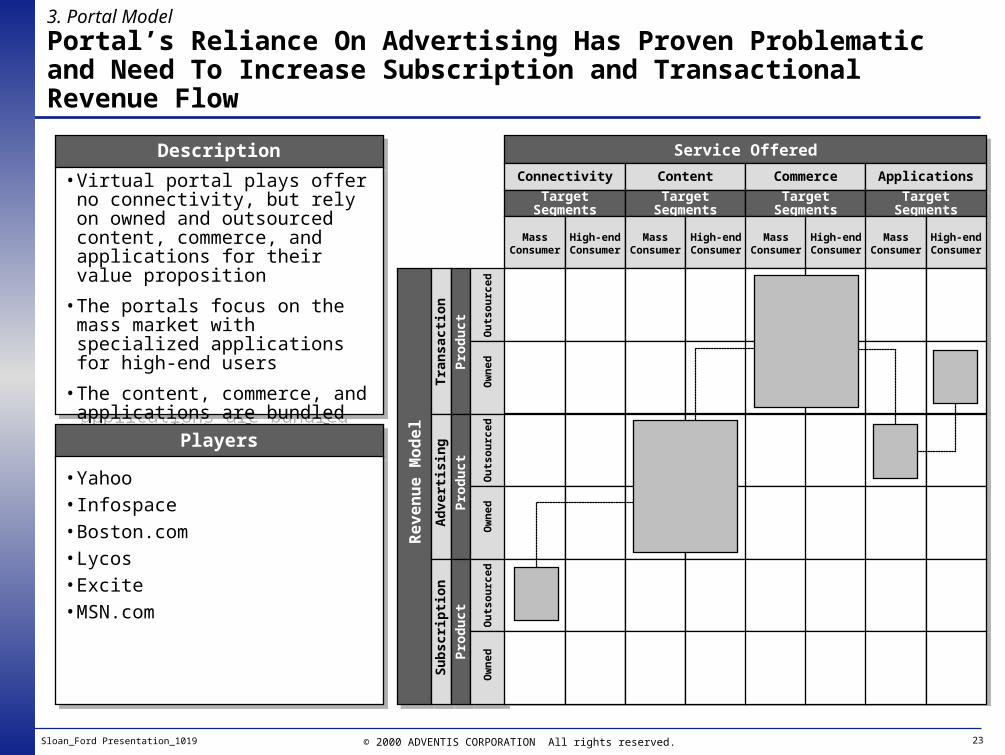

3. Portal Model

Portal’s Reliance On Advertising Has Proven Problematic and Need To Increase Subscription and Transactional Revenue Flow

DescriptionDescription

• Virtual portal plays offer no connectivity, but rely on owned and outsourced content, commerce, and applications for their value proposition

• The portals focus on the mass market with specialized applications for high-end users

• The content, commerce, and applications are bundled in a traditional portal format

• Virtual portal plays offer no connectivity, but rely on owned and outsourced content, commerce, and applications for their value proposition

• The portals focus on the mass market with specialized applications for high-end users

• The content, commerce, and applications are bundled in a traditional portal format

PlayersPlayers

• Yahoo• Infospace• Boston.com• Lycos• Excite• MSN.com

• Yahoo• Infospace• Boston.com• Lycos• Excite• MSN.com

Service OfferedService Offered

ConnectivityConnectivity ContentContent CommerceCommerce ApplicationsApplications

Target SegmentsTarget Segments Target SegmentsTarget Segments Target SegmentsTarget Segments Target SegmentsTarget Segments

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Re

ve

nu

e M

od

el

Re

ve

nu

e M

od

el

Tra

nsa

ctio

nT

ran

sact

ion

Ad

vert

isin

g A

dve

rtis

ing

Su

bsc

rip

tio

n S

ub

scri

pti

on

Pro

du

ctP

rod

uct

Pro

du

ct P

rod

uct

Pro

du

ctP

rod

uct

Ou

tso

urc

edO

uts

ou

rced

O

wn

ed

Ow

ned

Ou

tso

urc

edO

uts

ou

rced

O

wn

ed

Ow

ned

Ou

tso

urc

edO

uts

ou

rced

Ow

ned

Ow

ned

24Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

4. E-Commerce

Amazon.com Is A Leading Example

DescriptionDescription

• E-Commerce players offer unique content, commerce, and applications

• The content, commerce, and applications are bundled to secure advertising and transaction revenues

• E-Commerce players offer unique content, commerce, and applications

• The content, commerce, and applications are bundled to secure advertising and transaction revenues

PlayersPlayers

• Amazon

• Dell

• Peapod

• Buy.com

• Citysearch / Tickemaster

• Priceline

• Amazon

• Dell

• Peapod

• Buy.com

• Citysearch / Tickemaster

• Priceline

Service OfferedService Offered

ConnectivityConnectivity ContentContent CommerceCommerce ApplicationsApplications

Target SegmentsTarget Segments Target SegmentsTarget Segments Target SegmentsTarget Segments Target SegmentsTarget Segments

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Re

ve

nu

e M

od

el

Re

ve

nu

e M

od

el

Tra

nsa

ctio

nT

ran

sact

ion

Ad

vert

isin

g A

dve

rtis

ing

Su

bsc

rip

tio

n S

ub

scri

pti

on

Pro

du

ctP

rod

uct

Pro

du

ct P

rod

uct

Pro

du

ctP

rod

uct

Ou

tso

urc

edO

uts

ou

rced

O

wn

ed

Ow

ned

Ou

tso

urc

edO

uts

ou

rced

O

wn

ed

Ow

ned

Ou

tso

urc

edO

uts

ou

rced

Ow

ned

Ow

ned

25Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

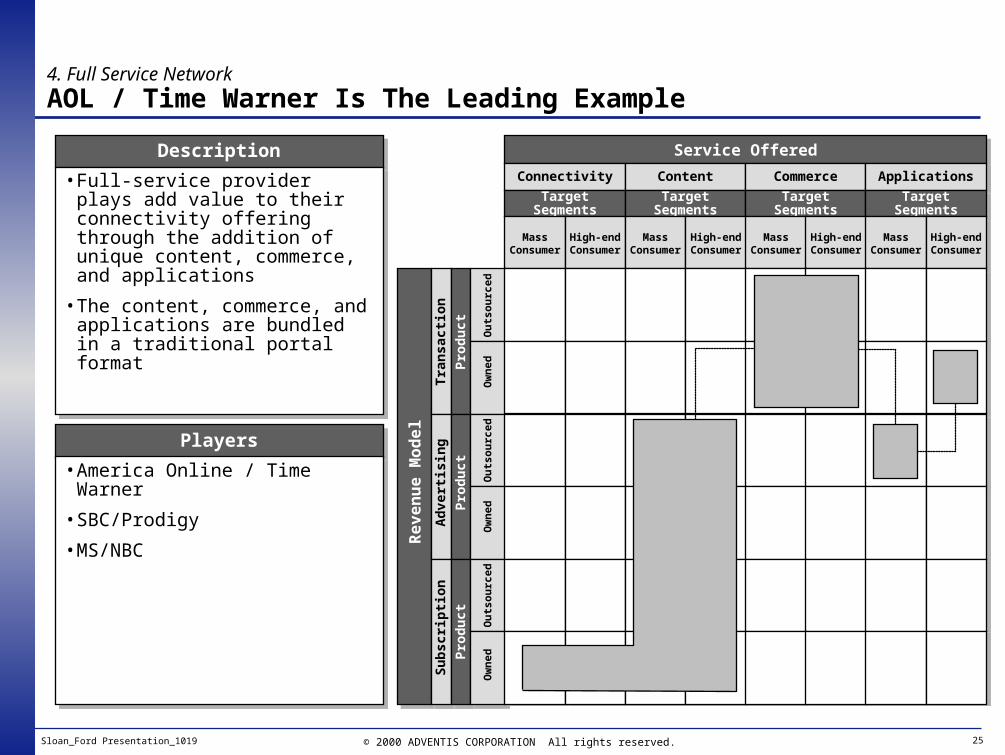

4. Full Service Network

AOL / Time Warner Is The Leading Example

DescriptionDescription

• Full-service provider plays add value to their connectivity offering through the addition of unique content, commerce, and applications

• The content, commerce, and applications are bundled in a traditional portal format

• Full-service provider plays add value to their connectivity offering through the addition of unique content, commerce, and applications

• The content, commerce, and applications are bundled in a traditional portal format

PlayersPlayers

• America Online / Time Warner

• SBC/Prodigy

• MS/NBC

• America Online / Time Warner

• SBC/Prodigy

• MS/NBC

Service OfferedService Offered

ConnectivityConnectivity ContentContent CommerceCommerce ApplicationsApplications

Target SegmentsTarget Segments Target SegmentsTarget Segments Target SegmentsTarget Segments Target SegmentsTarget Segments

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Mass Consumer

Mass Consumer

High-end Consumer

High-end Consumer

Re

ve

nu

e M

od

el

Re

ve

nu

e M

od

el

Tra

nsa

ctio

nT

ran

sact

ion

Ad

vert

isin

g A

dve

rtis

ing

Su

bsc

rip

tio

n S

ub

scri

pti

on

Pro

du

ctP

rod

uct

Pro

du

ct P

rod

uct

Pro

du

ctP

rod

uct

Ou

tso

urc

edO

uts

ou

rced

O

wn

ed

Ow

ned

Ou

tso

urc

edO

uts

ou

rced

O

wn

ed

Ow

ned

Ou

tso

urc

edO

uts

ou

rced

Ow

ned

Ow

ned

26Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Market Value Segmentation

Note: Revenues are estimates for 2000 and Market Capitalization is for October 17, 2000

DescriptionDescription

1. Wholesale Connectivity1. Wholesale Connectivity

Example CompanyExample Company

CovadCovad

Market CapMarket Cap

$2,848$2,848

RevenueRevenue

$2,671$2,671

Market Cap/ Revenue

Market Cap/ Revenue

10.6610.66

2. Content Network Model 2. Content Network Model ComcastComcast $38,500$38,500 $873$873 4.414.41

3. Portal Model 3. Portal Model YahooYahoo $50,866$50,866 $1,045$1,045 48.6848.68

4. eCommerce Model4. eCommerce Model AmazonAmazon $8,924$8,924 $2,816$2,816 3.163.16

4. Full Service Network4. Full Service Network AOL / TWAOL / TW $116,800$116,800 $38,243$38,243 3.053.05

27Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Leveraging the e-World/p-World Value Chain to Predict the Future

Connectivity Market Dynamics

Connectivity Market Dynamics

Applications Focused Business

Model Options

Applications Focused Business

Model Options

Consumer Applications/

Content Selection

Consumer Applications/

Content Selection

• Backbone Local Access “Abundance”

• Applications as Success Driver

• How Broadband is Changing Customer Behavior

• Business Model Identification

• Business Model Attractiveness Rating

• Identification of Consumer Trends Online Purchasing

• Prioritisation

• Broadband Impact

• Fulfillment Requirements

• Enabler Requirements

Consumer DeliveryConsumer Delivery

• Customer Experience

• Delivery/Supply Chain Issues

• Typical Misfires

28Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Applications Are The Best Way To Reverse These Trends and Increase Broadband Service Take-up Rate

Computing IndustryComputing Industry Communications IndustryCommunications Industry

Increased Performance

Increased Requirements

The Win/TelVirtuous

Circle

Data Processing/

Retrieval Capabilities

Data Processing/

Retrieval Capabilities

Application Complexity and

Processing Requirements

Application Complexity and

Processing Requirements

Increased Performance

“The big opportunity is to think up new services to be delivered over this suddenly cheap, plentiful and still unregulated channel”

—John Chambers, CEO Cisco Systems

“The big opportunity is to think up new services to be delivered over this suddenly cheap, plentiful and still unregulated channel”

—John Chambers, CEO Cisco Systems

Increased Requirements

Connectivity / Storage

Capabilities

Connectivity / Storage

Capabilities

Application Complexity and

Processing Requirements

Application Complexity and

Processing Requirements

Broadband Applicatio

ns and Content

Broadband Applicatio

ns and Content

“Classic” Services &

Content

“Classic” Services &

Content

29Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Market Attractiveness Rating Screen For Priority Application/Content/Commerce Services

Market PotentialMarket Potential

• Determination of a market’s expected future profitability based on a combination of the following factors:

- current market size

- forecasted growth

- revenue model sustainability

• Determination of a market’s expected future profitability based on a combination of the following factors:

- current market size

- forecasted growth

- revenue model sustainability

“Established”6. News

11. Gambling

18. Low Value, Low Tactile, Physical Goods

19. Low Value, High Tactile, Physical Goods

20. High Value, Low Tactile, Physical Goods

22. Shopping for Software

23. Shopping for Music

24. Shopping for Videos

25. Shopping for Books“Finished”

3. Personal Productivity

13. Recruiting

16. Government Services

26. Search Engines

“Hottest”2. Personal Finance

4. Communications

7. Professional Services

8. Video Entertainment

9. Audio Entertainment

10. Online Video Games

21. High Value, High Tactile Physical Goods

“Dormant”1. Media Sharing and

Manipulation

5. Information Storage

12. Distance Learning

14. Content / Community

15. Remote Security / Surveillance

17. Event Planning

High

Low

Low High

Ma

rke

t P

ote

nti

al

Attractiveness to aNew Entrant

— Market Attractiveness Screen —

Attractiveness to a New Entrant

Attractiveness to a New Entrant

• Determination of a market’s attractiveness to a new entrant based on a combination of the following factors:

- market concentration

- barriers to entry

- competitive intensity

• Determination of a market’s attractiveness to a new entrant based on a combination of the following factors:

- market concentration

- barriers to entry

- competitive intensity

30Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Revenue Forecasting for Attractive Services

$0

$5,000

$10,000

2000 2003

Source: IDC, Jupiter, Frost & Sullivan, Forrester, Renaissance

CAGR

Personal Finance29%

Communications108%

Video Entertainment138%

Audio Entertainment321%

Online Video Games73%

High Value, High TactileeCommerce

69%

48% Professional Services Key TakeawaysKey Takeaways

• Highest growth areas are in the entertainment segments with audio entertainment leading the pack with a 321% CAGR

• Projected size for the entertainment segments for 2003 is only $2.6 billion; however, these markets are expected to maintain their growth rates for several years and grow to be large markets as broadband and other enabling technologies improve

• Highest growth areas are in the entertainment segments with audio entertainment leading the pack with a 321% CAGR

• Projected size for the entertainment segments for 2003 is only $2.6 billion; however, these markets are expected to maintain their growth rates for several years and grow to be large markets as broadband and other enabling technologies improve

$2,924

$11,037

$484$577$900

$1,030

$1,078

$3,414

$3,535

Million

31Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Other ADVENTIS Research Confirms That Broadband and Wireless Are The Top Enablers for Priority Application/Content/Commerce Services

File Compression

Security

Non-PC Devices

Number of Priority Services Benefiting from Each Key Enabler 1 2 3 4 5 6 7

Wireless Devices

Broadband

Smart Cards

Key Enablers Frequency

• Broadband service and wireless devices will be the top enablers for mass adoption

• Wireless devices give consumers anytime, anywhere access to applications

• Non PC devices will create a demand for priority services by utilizing new devices and advanced online connectivity

• Service providers have an opportunity to leverage relationships with enabler firms

• co-operative marketing agreements to get customers from enabler

• revenue sharing as existing customers are up-sold to new technologies by enabler

• increased customer loyalty and usage through a superior offering due to the enabler technology

Service Providers Should Leverage Broadband and Other Key Enablers to Deliver Differentiated, Value-Added Offerings to Consumers

32Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

E-Commerce Processes Such As Researching & Ordering Are Greatly Affected by Broadband and Wireless

Sites VisitedSites VisitedIn Stock

Information Available?

In Stock Information Available?

Upsell Recommendation

Made?

Upsell Recommendation

Made?

Complementary Product

Complementary Product

Time to Confirm Order

Time to Confirm Order

Quality of Confirm

Quality of Confirm

Time Order Until Receipt

Time Order Until Receipt

1. Value America 1. Value America YesYes YesYes Only received email congratulating me on becoming a member

Only received email congratulating me on becoming a member

Link to Value America

Link to Value America

6-10 days for one item and 9 days for the other

6-10 days for one item and 9 days for the other

2. SpotShop 2. SpotShop YesYes NoNo 2 days after placing order2 days after

placing orderOrder # and order

dateOrder # and order

date5-10 days after order

was placed5-10 days after order

was placed

3. Circuit City 3. Circuit City YesYes YesYes 20 minutes-1 hour after

placing order

20 minutes-1 hour after

placing order

Order #, order date, price, delivery

method, address

Order #, order date, price, delivery

method, address3-11 days after order

was placed3-11 days after order

was placed

4. CDW 4. CDW YesYes YesYes 1 hour afterplacing order1 hour after

placing orderOrder #, items, price, sales linkOrder #, items, price, sales link

Very inconsistent see report for details

Very inconsistent see report for details

5. Egghead 5. Egghead YesYes YesYes Ranged from 10 minutes to 2

hours

Ranged from 10 minutes to 2

hours

Order #, address, items, price,

customer svc. links

Order #, address, items, price,

customer svc. linksBetween 1-4 days after order

was placedBetween 1-4 days after order

was placed

6. Outpost 6. Outpost NoNo YesYes 30 minutes-2 hours after placing order

30 minutes-2 hours after placing order

Order #, address, items, price

Order #, address, items, price

2-7 days after order was placed

2-7 days after order was placed

7. Amazon 7. Amazon YesYes20 minutes- 2

hours afterplacing order

20 minutes- 2 hours after

placing order

Order status link, address, items

and price

Order status link, address, items

and price4-5 days after order

was placed4-5 days after order

was placed

8. CDNow 8. CDNow YesYes YesYes 1-3 hours after placing order

1-3 hours after placing order

Order #, shipping method, items,

price and address

Order #, shipping method, items,

price and address5-8 days for the first item and 6 days for the other

5-8 days for the first item and 6 days for the other

9. eToys 9. eToys YesYes YesYes 5 minutes-6 hours after placing order

5 minutes-6 hours after placing order

Order #, items, price, address and customer service

link

Order #, items, price, address and customer service

link

5-8 days after order was placed

5-8 days after order was placed

10. Buy.com10. Buy.com YesYes NoNo 15-30 minutes after placing order

15-30 minutes after placing order

Order #, items, tracking link,

support link and 800#

Order #, items, tracking link,

support link and 800#

6-9 days for the first item and 7 days for the other

6-9 days for the first item and 7 days for the other

11. NECX11. NECX YesYes NoNo 1 hour-2 days after placing order

1 hour-2 days after placing order Order #Order # 1-4 days after the order

was placed1-4 days after the order

was placed

Yes

Yes

Yes

Yes

No

Yes

Yes

Yes

Yes

Yes

Yes

No

12. Dell 12. Dell YesYes NoNo 6 hours after placing order6 hours after placing order

Order #, items and price

Order #, items and price

3 days after order was placed

3 days after order was placedYes

33Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Leveraging the e-World/p-World Value Chain to Predict the Future

Connectivity Market Dynamics

Connectivity Market Dynamics

Applications Focused Business

Model Options

Applications Focused Business

Model Options

Consumer Applications/

Content Selection

Consumer Applications/

Content Selection

• Backbone Local Access “Abundance”

• Applications as Success Driver

• How Broadband is Changing Customer Behavior

• Business Model Identification

• Business Model Attractiveness Rating

• Identification of Consumer Trends Online Purchasing

• Prioritisation

• Broadband Impact

• Fulfillment Requirements

• Enabler Requirements

Consumer DeliveryConsumer Delivery

• Customer Experience

• Delivery/Supply Chain Issues

• Typical Misfires

34Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Profile of Value America Customer Experience: Round 1-4 Order Process

1. Place Order

1. Place Order

2 . Order Confirmation

2 . Order Confirmation

4 . Receive Order

4 . Receive Order

5 . Return Product

5 . Return Product

3 . Order Status

3 . Order Status

Round 1Round 1

Round 2Round 2

Round 3Round 3

Round 4Round 4

• Submitted order on August 4th

• Received e-mail congratulating me on becoming a member one day after order was placed

• Never received order confirmation

• Never received order status

• Submitted order on August 4th

• Submitted order on August 5th

• Submitted order on August 9th

• Received e-mail congratulating me on becoming a member one day after order was placed

• Never received order confirmation

• Received order confirmation 5 hours after order was placed

• Received e-mail congratulating me on becoming a member

• Never received order confirmation

• Never received order status

• Order was canceled, but not followed up by cancellation confirmation e-mail

• Never received order status

• Order was successfully canceled

• Order was successfully canceled

• Received Palm IIIX on August 16th

• Received Renaissance Art Book on August 17th via UPS Ground

• Received order on August 11th via UPS Ground

• ValueAmerica set up FedEx to pick up package

• Returned order via FedEx with RA #

• Received order on August 11th via UPS Ground

• ValueAmerica set up FedEx to pick up package

35Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

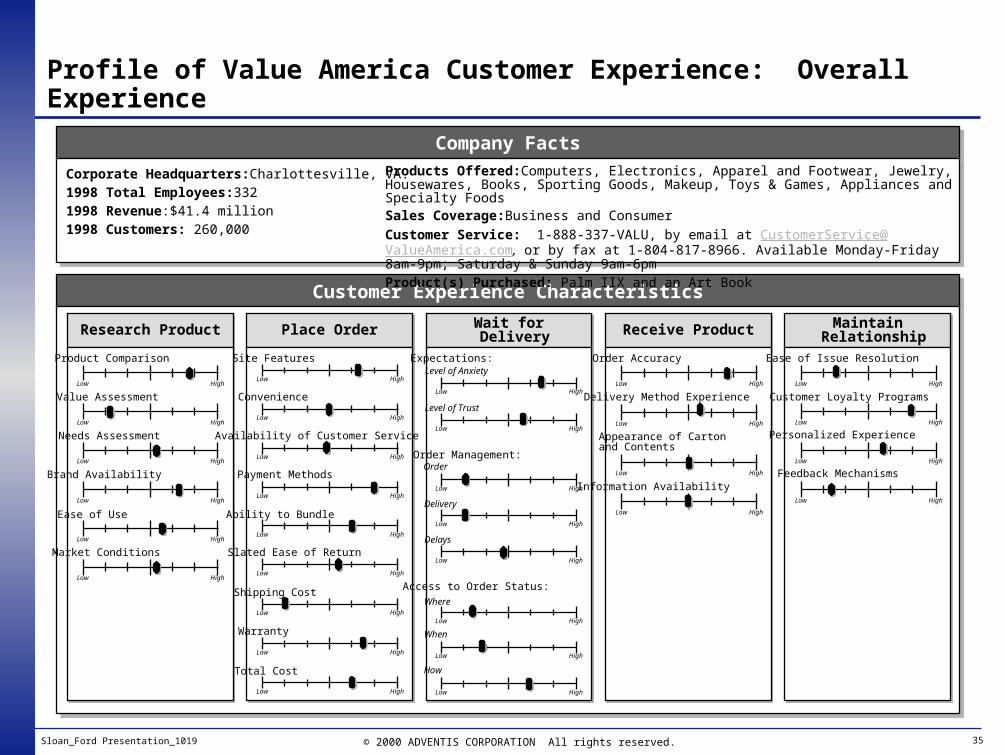

Customer Experience CharacteristicsCustomer Experience Characteristics

Profile of Value America Customer Experience: Overall Experience

Company FactsCompany Facts

Corporate Headquarters:Charlottesville, VA.1998 Total Employees:3321998 Revenue:$41.4 million1998 Customers: 260,000

Corporate Headquarters:Charlottesville, VA.1998 Total Employees:3321998 Revenue:$41.4 million1998 Customers: 260,000

Products Offered:Computers, Electronics, Apparel and Footwear, Jewelry, Housewares, Books, Sporting Goods, Makeup, Toys & Games, Appliances and Specialty FoodsSales Coverage:Business and ConsumerCustomer Service: 1-888-337-VALU, by email at [email protected], or by fax at 1-804-817-8966. Available Monday-Friday 8am-9pm; Saturday & Sunday 9am-6pmProduct(s) Purchased: Palm IIX and an Art Book

Research ProductResearch Product Place OrderPlace Order Wait for DeliveryWait for Delivery Receive ProductReceive Product Maintain RelationshipMaintain

Relationship

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Low High

Product Comparison

Value Assessment

Needs Assessment

Brand Availability

Ease of Use

Market Conditions

Site Features

Convenience

Availability of Customer Service

Payment Methods

Ability to Bundle

Slated Ease of Return

Shipping Cost

Warranty

Total Cost

Expectations:Level of Anxiety

Level of Trust

Order Management:

Delivery

Where

When

Access to Order Status:

How

Delays

Order

Order Accuracy

Delivery Method Experience

Appearance of Carton and Contents

Information Availability

Ease of Issue Resolution

Customer Loyalty Programs

Personalized Experience

Feedback Mechanisms

36Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Sites VisitedSites Visited

Interim CommunicationInterim Communication

Update?Update?

Waiting for Delivery and Receiving Product Affect Customer Experience At Least As Much as the Web Experience Does

Shipping Info?Shipping Info?

Interim CommunicationInterim Communication

Received on or Before

Date Expected

Received on or Before

Date ExpectedQuality of Box and Materials

Quality of Box and Materials

Return Information

Provided

Return Information

ProvidedQuality of

InvoiceQuality of

InvoicePresence of

Other MaterialsPresence of

Other Materials

1. Value America 1. Value America NoNo

2. SpotShop 2. SpotShop 50% 50%

3. Circuit City 3. Circuit City YesYes

4. CDW 4. CDW YesYes

YesYes

75% 75%

50% 50%

NoNo

No

50%

Yes

Yes

5. Egghead 5. Egghead YesYes Y/NY/NYes

6. Outpost 6. Outpost YesYes

7. Amazon 7. Amazon YesYes

8. CDNow 8. CDNow YesYes

9. eToys 9. eToys YesYes

10. Buy.com10. Buy.com YesYes

11. NECX11. NECX YesYes

YesYes

NoNo

YesYes

YesYes

50% 50%

YesYes

50%

Yes

Yes

Yes

Yes

Yes

12. Dell 12. Dell YesYes Y/NY/NYes

37Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Po

ten

tial

Pro

ble

ms

Po

ten

tial

Pro

ble

ms

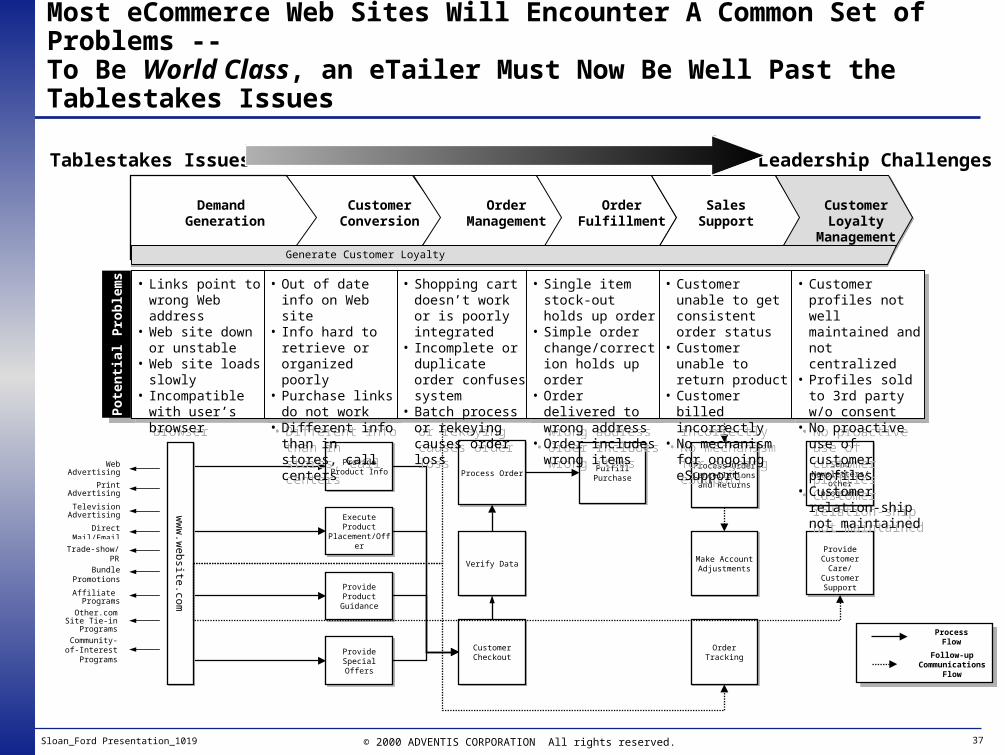

Demand Generation

Demand Generation

Customer ConversionCustomer

ConversionOrder

ManagementOrder

ManagementOrder

FulfillmentOrder

FulfillmentSales

SupportSales

Support

Most eCommerce Web Sites Will Encounter A Common Set of Problems -- To Be World Class, an eTailer Must Now Be Well Past the Tablestakes Issues

Customer Loyalty

Management

Customer Loyalty

ManagementGenerate Customer Loyalty

Affiliate Programs

PrintAdvertising

Direct Mail/Email

Verify DataVerify Data

Customer CheckoutCustomer Checkout

Send Newsletters/

other programs

Send Newsletters/

other programs

ww

w.w

ebsite.comw

ww

.website.com

Provide Product Info

Provide Product Info

Execute Product Placement/OfferExecute Product Placement/Offer

Provide Product Guidance

Provide Product Guidance

Trade-show/PR

Other.com Site Tie-in Programs

BundlePromotions

Provide Special Offers

Provide Special Offers

Process Order Cancellations and Returns

Process Order Cancellations and Returns

Make Account Adjustments

Make Account Adjustments

Order TrackingOrder Tracking

Process OrderProcess Order Fulfill PurchaseFulfill Purchase

Community-of-Interest

Programs

WebAdvertising

TelevisionAdvertising

ProcessFlow

Follow-upCommunications

Flow

ProvideCustomer Care/

Customer Support

ProvideCustomer Care/

Customer Support

• Links point to wrong Web address

• Web site down or unstable

• Web site loads slowly

• Incompatible with user’s browser

• Links point to wrong Web address

• Web site down or unstable

• Web site loads slowly

• Incompatible with user’s browser

• Out of date info on Web site

• Info hard to retrieve or organized poorly

• Purchase links do not work

• Different info than in stores, call centers

• Out of date info on Web site

• Info hard to retrieve or organized poorly

• Purchase links do not work

• Different info than in stores, call centers

• Shopping cart doesn’t work or is poorly integrated

• Incomplete or duplicate order confuses system

• Batch process or rekeying causes order loss

• Shopping cart doesn’t work or is poorly integrated

• Incomplete or duplicate order confuses system

• Batch process or rekeying causes order loss

• Single item stock-out holds up order

• Simple order change/correction holds up order

• Order delivered to wrong address

• Order includes wrong items

• Single item stock-out holds up order

• Simple order change/correction holds up order

• Order delivered to wrong address

• Order includes wrong items

• Customer unable to get consistent order status

• Customer unable to return product

• Customer billed incorrectly

• No mechanism for ongoing eSupport

• Customer unable to get consistent order status

• Customer unable to return product

• Customer billed incorrectly

• No mechanism for ongoing eSupport

• Customer profiles not well maintained and not centralized

• Profiles sold to 3rd party w/o consent

• No proactive use of customer profiles

• Customer relation-ship not maintained

• Customer profiles not well maintained and not centralized

• Profiles sold to 3rd party w/o consent

• No proactive use of customer profiles

• Customer relation-ship not maintained

Tablestakes Issues Leadership Challenges

38Sloan_Ford Presentation_1019 © 2000 ADVENTIS CORPORATION All rights reserved.

Customers Generally Prefer the eTailers Who Follow These Best Practices in Creating a Quality eCommerce Customer Experience

1. Research Products

1. Research Products

2. Make Buying Decision

2. Make Buying Decision

3. Place Order

3. Place Order

4. Wait for Delivery

4. Wait for Delivery

5. Receive Product

5. Receive Product

6. Maintain Ongoing Relationship

6. Maintain Ongoing Relationship

7. Utilize Customer Support

1.1 Site loads quickly - “More

than 1/3 of consumers give-up on purchasing on line because

of slow download times.”

1.1 Site loads quickly - “More

than 1/3 of consumers give-up on purchasing on line because

of slow download times.”

2.1 Product Availability

Information is clearly indicated and frequently

updated

2.1 Product Availability

Information is clearly indicated and frequently

updated

3.1 Site uses historical purchase

information for suggestive selling

3.1 Site uses historical purchase

information for suggestive selling

4.1 Timely, personalized

stream of information is provided from

order placement until order receipt

4.1 Timely, personalized

stream of information is provided from

order placement until order receipt

5.1 Product arrives in a

clearly labeled package

5.1 Product arrives in a

clearly labeled package

6.1 Personal Information is collected and

USED to make shopping

experience more intimate

6.1 Personal Information is collected and

USED to make shopping

experience more intimate

1.2 Layout, Categories and

Navigational Tools facilitate

use by the “lowest common

denominator”

1.2 Layout, Categories and

Navigational Tools facilitate

use by the “lowest common

denominator”

3.2 All costs are readily available to the customer

PRIOR to entering any

payment information

3.2 All costs are readily available to the customer

PRIOR to entering any

payment information

4.2 Change or Cancel Order is

handled efficiently irregardless of

channel used by Customer

4.2 Change or Cancel Order is

handled efficiently irregardless of

channel used by Customer

5.2 Automated returns process requires minimal customer effort

(all information is included)

5.2 Automated returns process requires minimal customer effort

(all information is included)

6.2 Purchasing History and

Survey data is used for

suggestive selling - Creating a

“virtual handshake”

6.2 Purchasing History and

Survey data is used for

suggestive selling - Creating a

“virtual handshake”

1.3 Consumers are able to get to

the level of information

necessary to make an informed buying decision

1.3 Consumers are able to get to

the level of information

necessary to make an informed buying decision

2.2 A consumer will make a

purchase from a site they trust (Brand, Prior

Experience) in lieu of making a

pure price decision

2.2 A consumer will make a

purchase from a site they trust (Brand, Prior

Experience) in lieu of making a

pure price decision

6.3 Privacy is Respected

6.3 Privacy is Respected

3.3 Site clearly indicates

estimated time of delivery

3.3 Site clearly indicates

estimated time of delivery

7.2 Automated responses clearly indicated anticipated wait times for Customer Support. Loads are balanced between channels so that customer is not

“penalized” making the “wrong” choice

7.2 Automated responses clearly indicated anticipated wait times for Customer Support. Loads are balanced between channels so that customer is not

“penalized” making the “wrong” choice

7.1 Customer Service provides both Pre and Post Sales service through multiple channels - 800 numbers, E-mail, Chat, Instant Messenger

7.1 Customer Service provides both Pre and Post Sales service through multiple channels - 800 numbers, E-mail, Chat, Instant Messenger

5.3 Post-receipt “Thank-you” for your purchase

provides opportunity for

customer feedback and “soft sell” of additional products

5.3 Post-receipt “Thank-you” for your purchase

provides opportunity for

customer feedback and “soft sell” of additional products

The enclosed material is confidential and proprietary to ADVENTIS CORPORATION and is for the internal use of addressee only.

For further information please contact:

Ford Cavallari, Executive Vice President

ADVENTIS CORPORATION

200 Berkeley Street, 22nd FloorBoston, MA 02116

Tel: 617.421.9990 Fax: 617.421.9994

The enclosed material is confidential and proprietary to ADVENTIS CORPORATION and is for the internal use of addressee only.

For further information please contact:

Ford Cavallari, Executive Vice President

ADVENTIS CORPORATION

200 Berkeley Street, 22nd FloorBoston, MA 02116

Tel: 617.421.9990 Fax: 617.421.9994