the indian hotels - smifs.com the company has built a vibrant porolio catering to ... ministry of...

TRANSCRIPT

&

The Indian Hotels C o m p a n y L i m i t e d

Initiating Coverage Report

20 March 2018

Research Analyst:

Sarthak Mukherjee

Over 100 years in owning, operating & managing hotels

&

The Indian Hotels Company Ltd

Contents

3

3-6

7-9

10-15

16

17

18-19

20

20

21

22

Page No.

IHCL at an Inflec�on Point

Investment Ra�onale

Indian Hospitality Industry

Company Overview

Financing Strategy to Support Growth

Strength backed by Customer Needs

Asset Management & Focus Areas

Aspira�on 2022

23

Upcoming Development

Recent Awards

Leadership

Outlook & Valua�on

25-27

28-29

Financial Details

Disclaimer & Disclosure

Key Risks 24

&

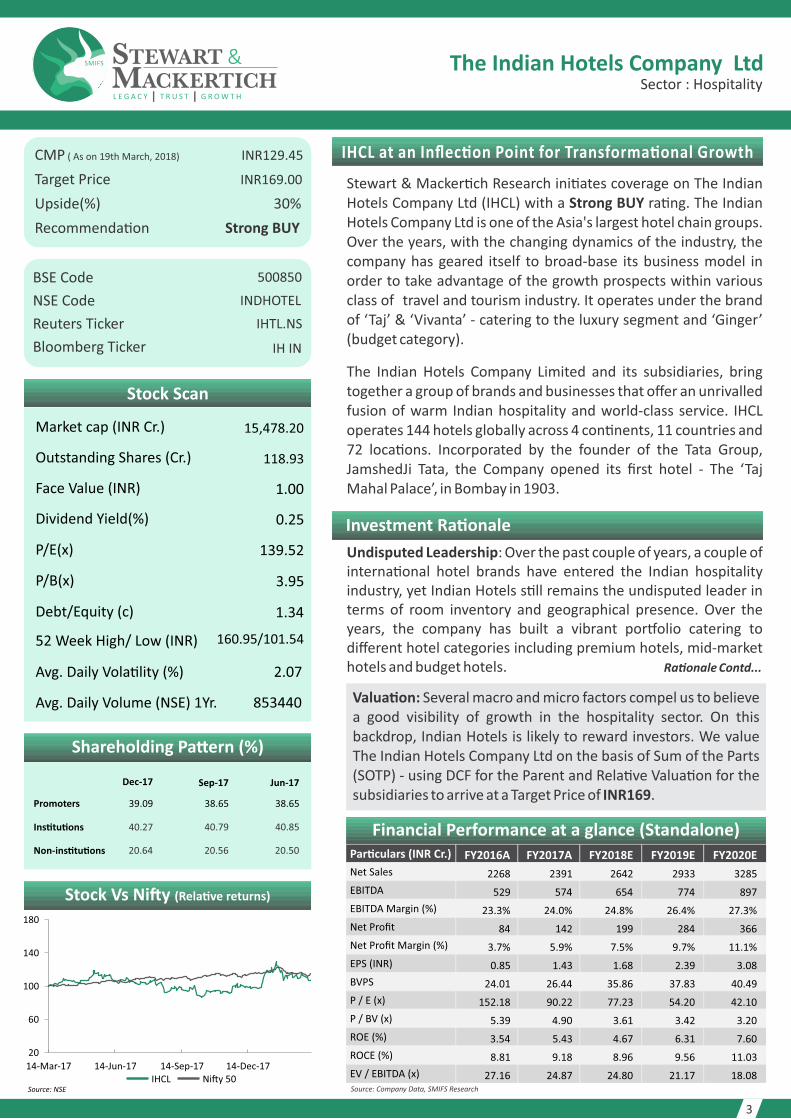

CMP ( As on 19th March, 2018) INR129.45

INR169.00 Target Price

Upside(%) 30%

Recommenda�on Strong BUY

BSE Code

NSE Code

Reuters Ticker

Bloomberg Ticker

500850

INDHOTEL

IHTL.NS

IH IN

IHCL at an Inflec�on Point for Transforma�onal Growth

Shareholding Pa�ern (%)

Promoters

Ins�tu�ons

Non-ins�tu�ons

Dec-17

39.09

40.27

20.64

Sep-17

38.65

40.79

20.56

Jun-17

38.65

40.85

20.50

Stock Scan

Market cap (INR Cr.) 15,478.20

Outstanding Shares (Cr.) 118.93

Face Value (INR) 1.00

Dividend Yield(%) 0.25

P/E(x) 139.52

P/B(x) 3.95

Debt/Equity (c) 1.34

Avg. Daily Vola�lity (%) 2.07

52 Week High/ Low (INR) 160.95/101.54

3

Stewart & Macker�ch Research ini�ates coverage on The Indian Hotels Company Ltd (IHCL) with a Strong BUY ra�ng. The Indian Hotels Company Ltd is one of the Asia's largest hotel chain groups. Over the years, with the changing dynamics of the industry, the company has geared itself to broad-base its business model in order to take advantage of the growth prospects within various class of travel and tourism industry. It operates under the brand of ‘Taj’ & ‘Vivanta’ - catering to the luxury segment and ‘Ginger’ (budget category).

The Indian Hotels Company Limited and its subsidiaries, bring together a group of brands and businesses that offer an unrivalled fusion of warm Indian hospitality and world-class service. IHCL operates 144 hotels globally across 4 con�nents, 11 countries and 72 loca�ons. Incorporated by the founder of the Tata Group, JamshedJi Tata, the Company opened its first hotel - The ‘Taj Mahal Palace’, in Bombay in 1903.

Valua�on: Several macro and micro factors compel us to believe a good visibility of growth in the hospitality sector. On this backdrop, Indian Hotels is likely to reward investors. We value The Indian Hotels Company Ltd on the basis of Sum of the Parts (SOTP) - using DCF for the Parent and Rela�ve Valua�on for the subsidiaries to arrive at a Target Price of INR169.

Sector : Hospitality

Investment Ra�onale

Undisputed Leadership: Over the past couple of years, a couple of interna�onal hotel brands have entered the Indian hospitality industry, yet Indian Hotels s�ll remains the undisputed leader in terms of room inventory and geographical presence. Over the years, the company has built a vibrant por�olio catering to different hotel categories including premium hotels, mid-market hotels and budget hotels. Ra�onale Contd...

Source: NSE

Stock Vs Ni�y (Rela�ve returns)

The Indian Hotels Company Ltd

20

60

100

140

180

14-Mar-17 14-Jun-17 14-Sep-17 14-Dec-17IHCL Ni�y 50

Avg. Daily Volume (NSE) 1Yr. 853440

Source: Company Data, SMIFS Research

Financial Performance at a glance (Standalone)Par�culars (INR Cr.) FY2016A FY2017A FY2018E FY2019E FY2020E

Net Sales 2268 2391 2642 2933 3285

EBITDA 529 574 654 774 897

EBITDA Margin (%) 23.3% 24.0% 24.8% 26.4% 27.3%

Net Profit 84 142 199 284 366

Net Profit Margin (%) 3.7% 5.9% 7.5% 9.7% 11.1%

EPS (INR) 0.85 1.43 1.68 2.39 3.08

BVPS 24.01 26.44 35.86 37.83 40.49

P / E (x) 152.18 90.22 77.23 54.20 42.10

P / BV (x) 5.39 4.90 3.61 3.42 3.20

ROE (%) 3.54 5.43 4.67 6.31 7.60

ROCE (%) 8.81 9.18 8.96 9.56 11.03

EV / EBITDA (x) 27.16 24.87 24.80 21.17 18.08

&

4

3 R’s-Re-structuring, Re-engineering and Re-imaging: The management wants to expand through asset light model, thus focusing primarily on management contracts. The company also plans to reduce its energy costs, payroll costs through op�mized organiza�on structure and shared services, admin and general expenses through reducing commissions. It also plans to reduce its imports and carbon footprint.

The Indian Hotels Company Ltd is going to focus on the topline, margin enhancement, guest-sa�sfac�on and employee engagement. To improve topline, the company would rely on support and partnership from Tata companies’ legacy of strong rela�onships with corporates, travel trade, diploma�c missions, shop rentals from Spa, Starbucks, etc.

The Company is looking to mone�ze its land parcels and other none core assets to further reduce its debt level and thus increasing the profit margins. Building alliances with group companies, selling property such as apartments owned by the company and engaging with more management contracts instead of buying hotels, are some of the ways in which the company would be improving its margins.

IHCL, a 144-hotel chain company would be taking its room inventory to 24,000 by 2022 from current 17000. It also plans to expand its exis�ng proper�es to leverage / develop over 1 million square feet of unu�lized floor space index (FSI).

With occupancy levels at about 64%, Indian Hotels claims to have a 20% market share in the domes�c hospitality industry. We believe Indian Hotel’s thrust to future performances will be backed by asset light model and de-leveraging of the balance sheet.

Infrastructure status to the Hospitality sector: Hospitality segment lobby group Federa�on of Hotels and Restaurants Associa�on of India (FHRAI) was long trying to get the Infrastructure status to the sector. They even sent a memorandum to the government ahead of the 2018 budget seeking infrastructure and industry status for all projects worth INR25 Cr and more. The Government is currently working on a proposal to grant infrastructure status to hotel projects worth INR50 crore and more. The move is aimed to encourage small and mid-segment hotel projects in the country. The tourism ministry has already finalized a proposal to this effect and is now awai�ng Cabinet clearance. This will provide easier access to long-term funding and lower interest rates for hotel projects over INR50 crore.

Expand Margins

Embrace Technology

Engage People

Re-engineer

Re-structure

Scale up Inventory

Simplify Holding Structure

Sell Non Core Assets

Manoeuvre Excellence

Manage Brand-scape

Mul�ply Por�olio

Re-imagine

Ra�onale Con�nued...

The Indian Hotels Company Ltd

&

5

Beginning of an up-cycle: The five-year period marked by oversupply in the Indian hospitality sector is coming to an end and the market is witnessing an up-cycle with expecta�ons of a robust revival in demand. The revenue per available rooms is expected to witness impressive improvements over the next two years on the back of the rising demand.

Presence in premium and mid-market a boon: Historically, an increase in demand is followed by increase in supply by the industry players but se�ng up premium and mid category hotels require considerable �me (funding, permissions, land acquisi�on etc.). The Company has dominant presence in premium and mid-market hotel categories (where se�ng up supply takes �me). This will be a boon for the company.

Significant tariff growth a�er 9 years: In 2018 a�er a gap of nine years, branded hotels are seeing a double digit growth in tariffs. Hotels have been able to nego�ate and take the tariff growth significantly up in the contracts with corporate clients through which half of the revenue is generated for most of the branded hotels. According to Hospitality consul�ng firm ‘Hotelivate’ expects tariffs to go up by double digits across most markets this year. Being a leader in the Indian hospitality space, IHCL is likely to make the most out of this development. It needs to be looked at how the management reaps benefit out of this as the fes�val and tourist season is far away.

Avia�on Industry’s PLF at a life�me high: There is a posi�ve correla�on between the airline passenger growth and hotel occupancy. Indian avia�on sector is in an up cycle and opera�ng at life�me high PLFs (passenger load factor). The occupancy levels are rising on a year on year basis. The Indian avia�on sector is in an up cycle, the sector is opera�ng at life�me high passenger load factors coupled with a passenger growth rate which is increasing at the rate of over 17-18% over the past 18 months. This bodes well for the hospitality sector.

Introducing Tech pla�orms and 24-hour command centre: The Indian Hotels Company (IHCL) has moved into the digital game in hospitality and a concerted effort over the past year has led to a 27% boost in its online revenue, 30% increase in room bookings, as well as addi�onal dining reserva�ons of around 25,000 tables over the past few months. Localized content like French, German, UK English, Spanish, simplified Chinese, etc. to drive direct booking from source markets. With the rise in usage of data and increase in no. of people going online, this strategic move is likely to yield posi�ve results for the company.

Preferred Choice for Heads of States,

Celebri�es and Dignitaries

68.9

63.7

72

77.3 75.1 74.673.3

7982.8

84.3

50

60

70

80

90

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Pax Load Factor

Passenger (Pax) Load Factor

The Indian Hotels Company Ltd

In the year 2017, a total of 16.97 lakh foreign

tourists arrived on e-Tourist Visa as compared

to 10.80 lakh in 2016, registering a growth

of 57.2%

Foreign Exchange Earnings(FEE) during 2017

were US$ 27.693 billion with a growth of 20.8%

over 2016. Whereas, the FEEs during 2016 were US$

22.923 billion with a growth of 8.8% over 2015

&

6

IHCL looks to enter into branded homes business: Following the likes of Four Seasons, Ritz Carlton and Grand Hya� who lend their brands and provide hospitality services to luxury residen�al apartments, IHCL is also evalua�ng strategies to foray into the residen�al space. It would be a strategic move to expand its brand and improve on the cash flows. Besides, developing branded residen�al projects over land parcels it owns could also help unlock the value of the land assets at different strategic loca�ons.As per the management, the company has a land bank of 759 acres, out of which IHCL is planning to mone�ze around 6%, i.e. 44 acres.

Demand-Supply Mismatch: Robust growth in the sector is awai�ng since there is a demand - supply mismatch in terms of required room inventory. According to Ministry of Tourism, India is short of around 2 lakh tourist hotel rooms and India is projected to be the fastest growing na�on in the wellness tourism sector. Tourist arrivals have been seeing a robust growth due to introduc�on of e-visas.

The drive to promote India as a tourist des�na�on and increase in global growth has also lead to larger travel to India by global tourists.

Turnaround inevitable: Stock valua�on lies in the ability of a company to generate posi�ve free cash flows on a consistent basis. The company has lagged on this parameter, besides some other factors, which has led the company to underperform the benchmarks and some peers for several years. Nevertheless, the �de is expected to turn favorable for the company led by sector trends which are turning posi�ve across several parameters and the company’s ini�a�ves in recent years which is likely help generate posi�ve free cash flows on a sustainable and incremental basis, an a�rac�on for long term investors.

The consolidated Net Debt is at INR1967 cr at the end of 9 months FY18 from INR3151 cr at the beginning of FY18. Similarly Net Debt to Equity is down at 0.47 compared to 1.25 at the beginning of FY18 according to latest filings by the company and is projected to come down further in FY19. The company’s recently closed rights issue has been used partly to bring down debts.

Strong Sales Offices Network and Healthy Geo Sources backed by strong

Leadership

The Indian Hotels Company Ltd

Net Debt (INR-Cr)

4216

3151

1967

2016 2017 2018(YTD)

Net Debt

Supply Growth +3.2%

Demand Growth +5.6%

Demand > Supply

&

7

The Indian hospitality industry has been instrumental in contribu�ng to the na�on’s economic growth. This trend is expected to con�nue especially with the introduc�on of e-visa for foreign tourists and with the domes�c economy improving, there are clear signs of increased domes�c travel. Tourism in India has significant poten�al considering the rich cultural and historical heritage, variety in ecology, terrains and places of natural beauty spread across the country. The growth rate in room demand (5.7%) has been consistently outpacing the supply (3%) growth in India in H1 (2017-18) as compared to the same period last year. All key markets have shown good growth in room demand with no key markets lagging as compared to last year.

Indian Hospitality Industry

The Indian tourism and hospitality sector is a key driver to the service sector in India. It is also a large employment generator besides being the third largest foreign exchange earner. India's Foreign Exchange Earnings (FEE) during 2017 were US$ 27.693 billion with a growth of 20.8% over 2016. Whereas, the FEEs during 2016 were US$ 22.923 billion with a growth of 8.8% over 2015.

Domes�c Tourist Visits (DTVs) to the States/Union Territories went up by 15.5% y-o-y to 1.65 billion during 2016 with the top 10 States/UTs contribu�ng about 84.2% to the total number of DTVs, as per Ministry of Tourism. This trend is expected to con�nue with increasing disposable income. Similarly with increasing number of working women, double income households are on the rise.

Foreign Tourist Arrival (FTAs) in the year 2017 were 101.77 lakh with a growth of 15.6% over 2016, compared to FTAs of 88.04 lakh with a growth of 9.7% is 2016 over 2015 as per Ministry of Tourism. As per the ministry of Tourism, Foreign tourist arrivals in India have shown growth in each quarter for past 6 years.

One in every Eleven people worldwide is

employed by Tourism & Hospitality sector

Contribu�on to GDP(%)

9

9.5

10

10.5

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Contribu�on to GDP

Domes�c Air Passenger Traffic has doubled over the past five years

20%

23%

17%

-5%

0%

5%

10%

15%

20%

25%

2015 2016 2017

Growth

-2%

4.4%

9.8%

0

200

400

600

800

1000

1200

1400

2012 2013 2014

Passengers (lakhs)

25%

16% 15% 15%17%

20%

12%

16% 17%21%

17%18% 19%

0%

5%

10%

15%

20%

25%

30%

0

40

80

120

160

Passenger (lakhs) Growth

Domes�c Air passenger growth 2017 (YoY)

FTA (Jan'17-Jan'18)

0%

5%

10%

15%

20%

25%

0

2

4

6

8

10

12

14

FTA (lakhs) YoY growth (%)

Source : Company data, SMIFS Research, DGCA, Ministry of Tourism

The Indian Hotels Company Ltd

&

8

India is expected to move into the top five business travel market by 2030, as business travel spending in the country will see a robust growth in the near future. Hotel chains will likely increase their expansion and investment plans in India. The tourism and hospitality sector is among the top 10 sectors in India to a�ract the highest Foreign Direct Investment.

India is a large market for travel and tourism. It offers a diverse por�olio of niche tourism products - cruises, adventure, medical, wellness, sports, MICE, eco-tourism, film, rural and religious tourism. India has been recognized as a des�na�on for spiritual tourism for domes�c and interna�onal tourists. Total contribu�on of travel and tourism sector to India’s GDP is expected to increase to US$ 275.2 billion in 2025. India ranked third among 184 countries in terms of travel & tourism’s total contribu�on to GDP in 2016. The Government of India has planned to take the FTA figure to 20 million by 2020 and double the foreign exchange earnings as well.

The launch of several marke�ng ini�a�ves by the Government of India like “A�thi Devo Bhava” and “Incredible India” has paced up the growth of the sector. Incredible India 2.0 campaign was launched in September 2017. The Indian government has also released medical visa to encourage medical tourism in the country. India has been making serious efforts to boost investments in the sector. The hotel and tourism sector, 100 per cent FDI is allowed through the automa�c route. A five-year tax holiday has been offered for 2, 3 and 4 star category hotels located around UNESCO World Heritage sites (except Delhi and Mumbai).

India has moved up 13 posi�ons from 65 to 52 in the Tourism & Travel Compe��ve Index according to reports. The ease of doing business in India according to World Bank has moved from 130 in 2017 to 100 in 2018 Levels, the recent upgrade of India’s Sovereign ra�ng by Moody’s is likely to a�ract more business travel to the country, benefi�ng Indian Hotels. Foreign tourist arrivals in the 1st half of FY2018 increased by 16% compared to the FY2017.

Branded room supply in major ci�es of India like Mumbai, Delhi and Bangalore is much lesser than in other Asian ci�es like Hong Kong, Shanghai and Tokyo. We believe the huge gap is likely to be filled going forward, raising occupancy and room rates of leading branded hotels, including Indian Hotels Ltd.

India is projected to be the fastest growing na�on in the well-ness tourism sector in the next five years, clocking over 20% gains annually through 2017, according to some studies.

0

2

4

6

8

10

12

14

Jan Feb Mar Apr May Jun July Aug Sep Oct Nov Dec

2015 (in lakhs) 2016 (in lakhs) 2017 (in lakhs)

Foreign Tourist Arrival

Foreign Exchange Earnings (INR Cr.)

0%

5%

10%

15%

20%

25%

30%

0

5,000

10,000

15,000

20,000

25,000

FEE (INR Crores) YoY growth (%)

Source : Company data, SMIFS Research, DGCA, Ministry of Tourism

The Indian Hotels Company Ltd

FTAs in the year 2017 were 101.77 lakh with a growth of 15.6% over 2016,

compared to FTAs of 88.04 lakh with a growth of 9.7% is 2016

over 2015

According to latest presenta�on by the Indian Hotels, the Indian hospitality industry is experiencing increase in occupancies leading to upward pressure on RevPARs (revenue per available room). The growth in demand is outpacing supply for the past three years.

The occupancy levels across the hotels in the country has stabilized between 65% to 68%. The sector is expec�ng a revival in the room rates that have largely been subdued for past few years. As per the industry experts, occupancy levels are expected to shoot up to 70% in the near future.

Branded hotels in the sector are seeing a double digit growth in tariffs in 4QFY18. Hotels have been able to nego�ate a significant tariff increase in the contracts with corporate clients through which, half of the revenue is generated for most of the branded hotels. This will benefit the industry immensely if the global and domes�c economy performs well.

&

9

Hotels in India

Occupancy 64% (+2.3%)

Avg. Room Rate ₹5,520 (+1.7%)

RevPAR ₹3, 516 (+4.1%)

Growing Markets

Ahmedabad, Jaipur,Chandigarh, Pune,

Hyderabad, Bengaluru, Mumbai, New Delhi,

Chennai, Goa, Kolkata

The Indian Hotels Company Ltd

&

10

Company Overview

Crea�ng value by opera�ng Best-in-class por�olio of hospitality brands in India & select overseas des�na�ons

Owned Hotels Managed Hotels Leased / Licensed Hotels

By Business Por�olio

Subsidiary Companies

Associate Companies

By Legal En�ty

Joint Ventures

IHCL

0

5000

10000

15000

20000

Room Inventory

Room Inventory

62 6676 82 88

99 103 107 112 118 125 131 138 137 139 144

40

60

80

100

120

140

160

No. of Hotels

Number of Hotels

Owned Leased Owned Leased Owned Leased

No. of Hotels 60 23 9 7 31 7

Inventory of Rooms 8,165 2,545 1,474 1,160 3,043 461

Revenue(INR / Cr) 3,637 828 1,535 541 156 16

EBITDA (INR/ CR) 784 215 106 85 17 6

Domes�c Interna�onal Ginger

Indian Hotels Company Ltd

Par�culars

* Figures are in line by line addition of all the properties under IHCL, Subsidiaries and JVs. Inventory as on September 30,2017

Source : Company data

The Indian Hotels Company Ltd

&

11

Major Subsidiaries, JV & Associates

The Indian Hotels Company Ltd

The Indian Hotels Company Ltd

Joint Ventures

Taj SATS Air Catering Ltd (51.0%)

Taj GVK Hotels & Resorts Ltd (25.52%)

Taj Madras Flight Kitchen Pvt Ltd (50.0%)

Taj Kerala Hotels & Resorts Ltd (28.30%)

Taj Karnataka Hotels & Resorts Ltd (44.27%)

Taj Safaris Ltd (28.96%)

Kaveri Retreat & Resorts Ltd (50%)

IHMS (SA) Pty Ltd (50%)

TAL Hotels & Resorts Ltd (27.49%)

Subsidiaries

Piem Hotels Ltd (51.57%)

TIFCO Holdings Ltd (100%)

Benares Hotels Ltd (51.68%)

United Hotels Ltd (55.0%)

Roots Corpora�on Ltd (63.25%)

Skydeck Proper�es Pvt Ltd (100%)

IHOCO BV (100%)

United Overseas Holdings, Inc (100%)

St James Court Hotel Ltd (72.25%)

Associates

Oriental Hotels Ltd (35.67%)

Lanka Island Resorts Ltd (24.66% ) TAL Lanka Hotel PLC (24.62%)

Source : Company data

&

12

IHCL - A $ 1.2 Billion Revenue Group

The Indian Hotels Company Ltd is one of the Asia's largest hotel chain groups. Over the years, with the changing dynamics of the industry, the company has geared itself to broad-base its business model in order to take advantage of the growth prospects within various class of the travel and tourism industry. It operates under the brand of Taj & Vivanta - catering to the luxury segment, Vivanta-catering to the upscale segment and Ginger-catering to the budget category.

TAJ: Spanning world-renowned landmarks, modern business hotels, idyllic beach resorts, authen�c palaces and rus�c safari lodges, each Taj hotel reinterprets the tradi�on of hospitality in a refreshingly modern way to create unique experiences and lifelong memories.

VIVANTA: Work hard and play hard. Relax and energize. Ideate and confer. Evolve and transform. Revel in a spirit that presents the normal with an unexpected twist. Stylish and sophis�cated, Vivanta by Taj delivers experiences with imagina�on, energy and efficiency.

THE GATEWAY: The Gateway Hotels and Resorts are designed for the modern traveler. Which is why they have a 24X7 a�tude across services like dining and fitness. So, when one feels like a quick bite at 1 A.M or a heart pumping jog at 4 A.M, they are ready to serve you.

GINGER: IHCL’s revolu�onary concept in hospitality for the budget segment in India is also its largest. Ginger Hotels are designed and operated with the ethos of providing reliable, safe and clean rooms that provide guests with a res�ul sleep experience coupled with a refreshing and reviving start to each day.

The Indian Hotels Company Limited (IHCL) and its subsidiaries, bring together a group of brands and businesses that offer an unrivalled fusion of warm Indian hospitality and world-class service. IHCL operates 144 hotels globally across 4 con�nents, 11 countries and 72 loca�ons.

Revenue Breakup

46%

38%

1%4%

7%4%

Room Income Food, Restaurant & Banquet

Shop rentals Membership fees

Management and opera�ng fees Other Opera�ng Income

Food and beverages consumed Employee benefit expenses

Power & Fuel Cost Other Opera�ng & Servicing Cost

Selling and Administra�on Expenses Miscellaneous Expenses

12%

10%

34%19%

25%

1%

Cost Break Up

2374 24452722

30213383

2016 2017 2018E 2019E 2020E

TOTAL REVENUE

Revenue from Opera�ons (INR Cr.)(Standalone)

Source : Company data, SMIFS Research

The Indian Hotels Company Ltd

&

13

The Indian Hotels Company Limited-A Brand

Taj Innercircle Re-launch: A loyalty programme applicable across all brands globally with addi�onal features and enhancements. It is characterized with easy redemp�on process with facili�es such as accommoda�on, restaurants, spas and no expiry of points for ac�ve members.

Enrolment

120%

Ac�ve Members

50%

Revenue from Loyalty Program

100%

Source : Company data

The Indian Hotels Company Ltd

&

14

Taj-ness - Guest Experience

Taj Culture and Tajness to be the bedrock of all experiences

Efficiency and consistency in delivering Product and Service Standards

Recogni�on and Personaliza�on

Pioneering Food and Beverage Experience

New Products and Cuisines

Leveraging Iconic restaurants and celebrity chefs Collabora�ons with Renowned Chefs

Authen�c Regional Cuisine crea�ng a sense of place

Taj Signature offerings

Bespoke Weddings’ Experience

Preferred Choice for Conferences and Events

Source : Company data

The Indian Hotels Company Ltd

9000 12000 15000 17000

35000

72000

121000

159000

2008 2012 2017 2021

Taj Others

&

15

Inventory Trend

IHCL—Por�olio

Room Supply Growth in the

Industry w.r.t various segments

7000 1700033000 46000

1500030000

53000

70000

22000

36000

49000

59000

2008 2012 2017 2021

Luxury Upperscale Upscale - Upper midscale Midscale - Economy

Increasing trend of Inventory to

con�nue with increased focus on management

contracts

Holding Company Group Company

Management Contract

25%

50%

25%

Inventory by Contract Inventory by Brand

38%

26%

14%

22%

Taj/Luxury Vivanta

Gateway Ginger

Source : Company data

The Indian Hotels Company Ltd

&

16

Financing Strategy to Support Growth while Improving Balance Sheet

Reduc�on in debt has been primarily on account of repayment of borrowings from the proceeds of Rights Issue by the management.

IHCL has allo�ed approx, 20 crore shares i.e., 1999.84lakh shares in October 2017.

Aggregate Rights Issue Proceeds of INR1,499.88 crore was raised.

Promoters Shareholding has increased from 38.65% to 39.09%, post conclusion of the Rights Issue.

Out of the Total Proceeds, INR1,273 crore was proposed to be used for repayment.

The cost of debt has reduced as some of the loans have been re-financed by raising debt at a lower cost.

Credit ra�ng on the borrowings : “AA+” by CARE & “AA” by ICRA.

Net Debt (INR-Cr)

4216

3151

1967

2016 2017 2018(YTD)

Net Debt

6.47

4.74

2.97

1.27 0.970.47

2016 2017 2018(YTD)

Net Debt:EBITDA Net Debt : Equity

Debt Ra�os

Brand Ginger-the budget segment where cash requirement is high, requires support from IHCL and from poten�al partners.

Piem, Oriental Hotels & other associates to operate on a self reliant manner.

Special acquisi�ons needs to be looked into separately and strategically.

IHCL standalone cash flows to be used for renova�on.

Standalone Balance Sheet is likely to sweat to fund expansion within IHCL and partly for Ginger.

Growth envisaged via combina�on of Equity Raising, Divestment, Partnerships and SPV/REITs.

Cash Flow from Opera�ons (INR Cr.)

469.35 457.15 429.40 528.86

706.39

FY2016A FY2017A FY2018E FY2019E FY2020E

Total Opera�ng Cashflow

Source : Company data, SMIFS Research

The Indian Hotels Company Ltd

&

17

Strength Backed by Customer Needs

Business segment

Loca�on

Efficiency Safety Hygiene

Personaliza�on

� Strong network across different price points

Ability to leverage Palace & Leisure por�olio

Leisure segment

Overall well being

Relax Fun & Family �me

� Key loca�ons & pioneering new des�na�ons

both local and global markets

Largest domes�c leisure operator

Jiva Spa

Palaces

Authen�city

Experience of a life �me

� Restora�ve ethics & ability to run living

palaces, heritage proper�es, curated

experience and connectedness with

owners

Source : Company data

The Indian Hotels Company Ltd

&

18

Asset Management & Focus Areas

Capital Alloca�on

� Maintain market leadership with quality products

Priori�ze investment in product renova�on for areas and ci�es with maximum returns

Contract Management

� Regular review and analysis of contracts to extend tenure of good performing hotels

Exit hotels with sustained losses and low poten�al

Build Synergies

� Op�mize overheads across mul�ple en��es

Capitalize on enterprise scale for achieving lower costs on products and services

Unlock Capital

� 3/4th of the current inventory is under freehold/ leasehold, evalua�ng & unlocking of capital through sale and lease back models or through special purpose vehicles

Source : Company data

The Indian Hotels Company Ltd

&

19

Domes�c Focus Interna�onal Focus

Taj

City Hotels: All key ci�es in the top 15 states by GDP

Resorts: Established des�na�ons with good access

Palaces: Authen�c Palaces with easy access

Safaris: Loca�ons near key na�onal wild life parks

Taj

Target the growing, high spending outbound tourists familiar with our brand

Currently MENA and South East Asia get the highest outbound traffic from India, making them a natural choice for our expansion overseas

Customer Crossover

Vivanta

City Hotels :Top 40ci�es (basis of popula�on, connec�vity, commercial importance) Resorts: Key resort des�na�ons as part of a circuit

Taj

The large Indian Diaspora in various markets such as Singapore,

Thailand, Malaysia, MENA region, South Asia, con�nue to be ambassadors for

the brand Taj

Ci�es with large Indian Diaspora

Ginger

City Hotels: Top 80 ci�es (basis popula�on, connec�vity, commercial

importance)

Taj

Certain markets like Myanmar, Africa etc. are poised to

grow and are a poten�al opportunity before they get saturated

Growth Markets

Source : Company data

The Indian Hotels Company Ltd

&

20

Aspira�on 2022

Aspira�on 2022: Indian Hotels Company has charted a strategy to improve its EBITDA margin to 25% by 2022. The company plans to mone�se its non-core assets. It aims to go in the direc�on of asset-light model and hold less ownership (60% of its assets will not be owned by the company by 2022), reducing its dependence on the luxury segment and moving the hotels por�olio of some of the group companies to the holding company.

Upcoming Development-Next 12 months

The Indian Hotels Company Ltd

Hotel

Udaipur - Management Contract :125 rooms

Rishikesh - Management Contract : 79 rooms

Shimla - Management Contract : 95 rooms

Tirupa� - Management Contract : 102 rooms

Taj Mansingh Bid

Source : Company data

Ginger

Patna– Roots Corpora�on : 70 rooms

Aurangabad - Roots Corpora�on: 64 rooms

Surat - Management Contract : 94 rooms

Taj Lands End & Sea Rock Hotel

IHCL to connect Taj Land’s

End and Sea Rock Hotel with a

Bridge reducing overhead costs and

increase revenue through F&B

Iconic Five Star Property

Strategic Loca�on

294 rooms

Iconic and

ProfitableHospitalityCompany

Re-structureScale, Simplify,

Sell

Re-engineerMargins, Technology,

People

Re-imagineService, Brandscape,

Por�olio

Culture Strong Brand Equity High Customer Engagement

Pan-India Footprint Market Leaders in Leisure & Palaces Segment

TRUST, AWARENESS, JOYINTEGRITY, EXCELLENCE, UNITY, RESPONSIBILITY, PIONEERING

VALU

ES

ENABLE

RS

INIT

IATI

VES

ASPIR

ATIO

N 2

022

Source : Company data

&

21

Recent Awards

Business Today Award for Best Companies to Work For in India -2017

Six Time Winner India's top 50

People Capital Index

Business Traveller UK Awards

GALLUP GREAT WORKPLACE AWARD

DUN & BRADSTREET CORPORATE AWARDS

ALL INDIA INVESTOR RELATIONS AWARD

CONDÉ NAST TRAVELER US READERS' CHOICE AWARDS

Best Business Hotel Chain in India: Taj Hotels Palaces Resorts Safaris

50 Best Hotels in the World include : Rambagh Palace, Jaipur

Umaid Bhawan Palace, Jodhpur

Taj Diploma�c Enclave, New Delhi

Source : Company data

The Indian Hotels Company Ltd

&

22

Leadership

Name Designa�on Details

N. Chandrasekaran Chairman

PUNEET CHHATWAL MD & CEO

PRABHAT VERMA Sr. V.P -Opera�ons

CHINMAI SHARMA Chief Revenue Officer

GIRIDHAR SANJEEVI CFO

Natarajan Chandrasekaran is the chairman of Tata Sons. Chandrasekaran took over as the

CEO of Tata Consultancy Services on November 6, 2009 prior to which he was COO and

execu�ve director of TCS.

On the 6th of November,2017, Mr. Puneet Chhatwal joined IHCL as the Managing

Director and Chief Execu�ve Officer. He is a global professional with over three decades of

leadership experience at highly-acclaimed hotel groups in Europe and North

America.Prior to this, Mr. Chhatwal was the Chief Execu�ve Officer and Member of the

Execu�ve Board of Steigenberger Hotels AG – Deutsche Hospitality. He was also the Chief

Development Officer of The Rezidor Hotel Group – Carlson Hotels Worldwide. Mr.

Chhatwal is a graduate of both Delhi University and Ins�tute of Hotel Management,

Delhi. He has completed an MBA in Hospitality from ESSEC, Paris and an Advanced

Management Program from INSEAD.

Mr. Prabhat Verma, a hotel management graduate from IHMCTAN, Kolkata joined Taj

group in the year 1990 as a Management Trainee and has held key posi�ons like General

Manager of Taj Malabar, Cochin, and Taj Coromandel, Chennai. He was re-located as

Hotel Manager to Crowne Plaza, St. James Court and 51 Buckingham Gate, the London

proper�es of the Taj. He subsequently took over as General Manager - Crowne Plaza, St.

James and 51 Buckingham gate, London. Mr. Verma has won numerous industry

accolades including Young General Manager of the Year 2005, 5 Star Deluxe category by

FHRAI and the 'Interna�onal Coopera�on between the UK and India Award' (2012) by

Asian Voice.

As the Chief Revenue Officer for the Taj Group, Chinmai's responsibili�es include Brand

Management, Digital Pla�orms, Loyalty programs, Public Rela�ons, Customer Analy�cs,

Global Sales and Revenue Management. Chinmai is a seasoned industry professional

with nearly two decades of progressive hospitality experience in the fields of Strategic

Marke�ng, Revenue Management and Electronic Distribu�on. Chinmai was named as

one of the 'Top 20 Extraordinary minds within Sales, Marke�ng and Technology' by

Hospitality Sales & Marke�ng Associa�on Interna�onal (HSMAI), Europe in 2015. Before

joining Taj, Chinmai was with Starwood Capital Group, based in Paris as the Global head of

Revenue, Distribu�on and eCommerce for Louvre Hotels Group's en�re por�olio of six

hotel brands with 1,100 plus hotels spread across 45 countries

Giri is a Chartered Accountant (An All India Ranker) and an MBA from IIM Ahmedabad

(class of 1987) .Giri joined The Indian Hotels Company Limited from Merck & Co, the

American Pharma company, where he was the CFO for South Asia and the Business

Head for Pakistan, Bangladesh, Srilanka and Nepal. Giri started his career in ITC Ltd,

where he did a variety of roles across businesses in India and the Middle East.

Subsequently, Giri was with IL&FS as an Investment Banker and head of M&A. In

addi�on, he was also the Head of the opera�ons at Eastern India.

Source : Company data

The Indian Hotels Company Ltd

&

23

Outlook And Valua�on

Several macro and micro factors compel us to believe a good visibility of growth in the hospitality sector backed by booming tourism and increase in tariffs a�er a gap of 9 years accompanied by demand growth greater than supply growth. Moreover, the newly charted strategy will help The Indian Hotels Company Ltd in its profitability alongside increasing occupancy levels and average room rates.

On this backdrop, Indian Hotels Company Ltd being the largest player in the Indian hospitality sector, is perfectly poised to reap benefits from the macroeconomic factors. The pullbacks in the sector caused by GST and De-mone�za�on fading away will boost the sector further.

We, value The Indian Hotels Company Ltd on the basis of Sum of the Parts (SOTP) - using DCF for the Parent and Rela�ve Valua�on for the subsidiaries to arrive at a Target Price of INR169.

Free Cash Flow (INR Cr.)

979.59 1,063.13

522.95

930.90 993.61

569.39 673.38

362.85

673.13 760.83

FY 2016 FY 2017 FY 2018E FY 2019E FY 2020E

FCFF FCFE

The Indian Hotels Company Ltd

9504

9360

9562

9308

10213

8800

9000

9200

9400

9600

9800

10000

10200

10400

2013 2014 2015 2016 2017

Average room rent

Source : Company data, SMIFS Research

ARR has by 10% in 2017

63%

64% 64%

65%

66%

62%

62%

63%

63%

64%

64%

65%

65%

66%

66%

67%

2013 2014 2015 2016 2017

Occupancy (%)

Occupancy has by 200 bps since 2015

&

24

Entry of global hospitality players: Many global players are entering the hospitality industry in India. They are being backed by private equity players. This may put pressure on the market share of the Indian Hotels Company Ltd. Their main focus lies in asset light model.

Exchange Rate Risk: The Company has mul�-country opera�ons and is prone to the currency fluctua�ons. This is likely to impact the revenue from foreign markets.

Success of subsidiaries: The Indian Hotels Company’s success primarily depends on the performance of its subsidiaries as the subsidiaries are in losses.

Taj Mansingh Bid: The New Delhi Municipal Council (NDMC) has decided to e-auc�on the Taj Mansingh Hotel. Indian Hotels, had been granted the license for the Taj Mansingh in 1976 for 33 years. The license had expired in 2011, but the company was given many extensions. Although Indian Hotels is also bidding to retain the property, but the Company may lose the property due to s�ff compe��on from other players. The 294-room property accounts for less than 2% of Indian Hotel's total revenues . The auc�on has been ge�ng postponed due to several issues related to the bidding terms.

Economic Ac�vity: The hospitality industry is dependent both on the domes�c and foreign economic ac�vity. IHCL bears a risk of economic downturn. In case of recession the industry will experience lower occupancy levels along with downward pressure on the tariffs leading to a significantly lower RevPAR impac�ng profitability adversely.

Geo-poli�cal Tensions: In case of any geo-poli�cal tension cropping up in any of the loca�ons of IHCL’s existence, it will badly impact the business.

Key Risks

Entry of global hospitality players may put pressure on

the market share of the Indian Hotels Company Ltd

Economic downturn may hamper the

hospitality business

The Indian Hotels Company Ltd

&

25

Financial Details

The Indian Hotels Company Ltd

Income Statement (Standalone)

FY2016A FY2017A FY2018E FY2019E FY2020E

2,268 2,391 2,642 2,933 3,285

106 54 79 88 99

2,374 2,445 2,722 3,021 3,383

210 220 238 266 301

180 167 206 223 243

615 633 691 756 835

346 370 396 428 474

488 464 520 558 617

7 16 16 16 17

1,846 1,871 2,067 2,247 2,487

529 574 654 774 897

23.3% 24.0% 24.8% 26.4% 27.3%

126 151 168 186 213

403 423 486 587 684

243 198 180 150 121

160 225 307 437 563

-7 34 0 0 0

153 259 307 437 563

69 117 107 153 197

84 142 199 284 366

Par�culars (INR Cr.)

[+] Service Income

[+] Other Income

Total Revenues

Food and beverages consumed

Employee benefit expenses

Power & Fuel Cost

Other Opera�ng & Servicing Cost

Selling and Administra�on Expenses

Miscellaneous Expenses

Total Expenses

Opera�ng Profit/EBITDA

Opera�ng margin(%)

[ - ] Deprecia�on

EBIT

[-] Interest

PBT before excep�onal item

Excep�onal Items

PBT

[-] Income Tax Expense

PAT (before share of associates & JVs)

Revenues

Opera�ng Expenses

Source: Company Data, SMIFS Research

&

26

Balance Sheet (Standalone)

The Indian Hotels Company Ltd

Source: Company Data, SMIFS Research

Parameters (INR Cr.)

2016

2017

2018E

2019E

2020E

Assets

Property, plant and equipment

2,101

2,149

2,249

2,421

2,642

Capital work-in-progress

55

108

130

130

78

Intangible assets

41

38

32

27

19

Intangible assets under development

0

0

0

0

0

Investments

1,819

2,875

3,200

3,400

3,400

Loans

1,057

38

500

500

500

Other financial assets

56

59

62

59

60

Advance income tax (net)

48

65

49

54

56

Other non-current assets

250

256

291

323

361

Inventories

45

48

48

46

41

S.T Investments

136

53

207

132

131

Trade receivables

162

214

227

262

285

Cash and cash equivalents

21

14

488

64

56

Other balances with banks

8

8

8

8

8

Loans

1

1

1

1

1

Other financial assets

123

120

132

125

126

Other current assets

42

49

53

59

66

TOTAL

5967

6094

7676

7610

7830

Equity and liabili�es

Equity share capital

99

99

119

119

119

Other equity

2277

2517

4146

4380

4696

Equity a�ributable to owners

2376

2616

4265

4499

4815 Liabili�es

Borrowings

1569

1495

1317

1051

878 Other financial liabili�es

298

253

283

278

272

Provisions

49

49

42

46

46

Deferred tax liabili�es (net)

229

288

243

254

262

S.T Borrowings

7

7

9

12

15

Trade payables

173

177

187

202

223

Other financial liabili�es

921

883

1036

947

955

Provisions

78

86

75

80

88

Other current liabili�es 267 239 218 241 278 TOTAL LIABILITIES 3592 3478 3411 3111 3015 TOTAL Equity and liabili�es 5967 6094 7676 7610 7830

&

27

Source: Company Data, SMIFS Research

FY2016A FY2017A FY2018E FY2019E FY2020E

95.5% 97.8% 97.1% 97.1% 97.1%

4.5% 2.2% 2.9% 2.9% 2.9%

23.3% 24.0% 24.8% 26.4% 27.3%

3.5% 5.8% 7.3% 9.4% 10.8%

12.0% 5.4% 10.5% 11.0% 12.0%

11.2% 3.0% 11.3% 11.0% 12.0%

12.8% 8.7% 13.9% 18.3% 15.9%

202.7% 68.7% 40.4% 42.5% 28.7%

81.4% 78.2% 78.2% 76.6% 75.7%

21.5% 19.4% 19.7% 19.0% 18.8%

37.3% 36.4% 76.2% 47.0% 45.8%

35.8% 35.3% 44.3% 42.7% 42.2%

3.7% 5.7% 5.8% 6.5% 7.9%

2.1% 3.5% 4.1% 5.1% 6.5%

66.4% 57.4% 31.1% 23.6% 18.5%

Par�culars

Service

Other Income

EBITDA Margin

PAT Margin

Service

Revenue

EBITDA

PAT

Cost of services and sales

Selling, general and administra�ve

Current Ra�o

Quick Ra�o

ROAE

Post Tax ROACE

Debt/ Equity

Growth Rates: Y-o-Y

As a % of Sales

Liquidity Ra�o

Return Ra�o

Leverage Ra�o

Revenue Mix

Profit Margins

Key Ra�os (Standalone)

Cash Flow Statement (Standalone)

FY2016A FY2017A FY2018E FY2019E FY2020E

469 457 429 529 706

311 -97 -992 -480 -55

-1043 -367 1036 -473 -660

-262 -7 474 -424 -8

283 21 14 488 64

21 14 488 64 56

Par�culars (INR Cr.)

Total Opera�ng Cashflow

Total Inves�ng Cashflow

Total Financing Cashflow

Net change in Cash Flow

Cash Flow at the beginning of the year

Cash Flow at the end of the year

The Indian Hotels Company Ltd

Members: NSE | BSE | MCX | NCDEX | NSDL | CDSL | Repository (For Disclosures and Disclaimers please follow the page below)

Bloomberg Ticker for Stewart & Macker�ch Research: SMIF<Enter>

Website: www.smifs.com | Email: [email protected]

MUMBAI Mr. Vaibhav Wadke

Office No. 5G, New Marine Lines, Court Chamber, Mumbai - 400 020,

Maharashtra, India Phone: +91 -9967642795

BHUBANESHWAR

Mr. Jeetendra Nath Sahoo

Plot No. 15 -B, Bapuji Nagar, Unit-I, Ashok Nagar,

Bhubaneswar - 751009, Odissa, India. Phone: +91 9668257514

BANGALORE Mr. S. Srikanth

No.153, 2nd Floor, Sheela Arcade, 7th Block Koramangala, (Opp.—Sai Baba Mandir)

Bangalore - 560095, India. Phone: +91 9845020017

KANPUR

Mr. Amit Kumar Gupta

Office No.212 - 213, 2nd Floor, KAN Chamber, Adjacent to UP Stock Exchange, 14/113, Civil Lines, Kanpur - 208001, U�ar Pradesh, India.

Phone: +91 9151104767

REGISTERED OFFICE Mr. Sandipan Cha�erjee

Vaibhav, 4 Lee Road,

Kolkata 700020, India. Phone: +91 33 30515400 / 40115400

Fax No: +91 9748899161

Mr. Ashiwini Kumar Tripathi Director [email protected]

+91 33 30515415 / 40115415 Mobile: +91 9831155058

Mr. Shivaji Roy Sr. VP - Retail Sales [email protected] +91 33 30515400/40115400 Mobile: +91 9830173200

Mr. Jaydeep Pa�anayak Plot No. 15-B, Bapuji Nagar, Unit-I, Ashok Nagar, Bhubaneswar - 751009, Odissa, India. jaydeep.pa�[email protected] Phone: +91 9583099025

NEW DELHI Mr. Rajesh Kumar Jha

6th Floor, 654, Aggarwal Metro Heights, Netaji Subhash Place, Pitampura,

New Delhi – 110034, India. Phone: +91 9999243622

PATNA Mr. Ram Singh

606/A, Ashiana Plaza, Budha Marg, Patna – 800001, Bihar, India.

Phone: +91 9570507409

LUCKNOW Mr. Ashish Verma

6 Park Road, UGF 4, Hazratganj, Lucknow - 226001, U�ar Pradesh, India.

Phone: +91 9559378972

PATHANKOT

Ms. Anuradha Marwaha SCO G -

Pathankot - 145001, Punjab, India. Phone: 0186 - 2222201/ 2222205

CHENNAI

Mr. K.K.Raja Gopalan New No.4/2, Bajaj Apartments,

Seethamal Colony, 1st Cross Corner, Alwarpet,

Chennai – 600018, India. Phone: +91 9383931590

NOIDA

Mr. Prakash Srivastava

1st, Floor, Wave Silver Tower, Sector -18, Noida - 201301, U�ar Pradesh, India.

Phone: +91 9910497783

Research & Development Strategies

Mr. Ajay Srivastava Associate VP - Research [email protected] +91 33 30515400 Mr. Kapil Joshi

Research Analyst Infrastructure/Power [email protected] +91 33 40115468

Mr. Sarthak Mukherjee Research Analyst Avia�on/Hospitality/Logis�cs [email protected] +91 33 40115474

Mr. Saurabh Ginodia Associate VP - Research & Strategies

[email protected] +91 33 30515407

Ms. Mononita Mitra

Research Analyst Agro/Chemicals [email protected] +91 33 40115468 Mr. Anupam Goswami Research Analyst Building Products/Capital Goods/

Construc�on Equipment [email protected] +91 33 40115474

Ms. Sutapa Biswas Sr. Research Analyst Economy [email protected] +91 9836020612 Mr. Debjit Maji

Research Analyst Auto & Auto Ancillary/Telecom [email protected] +91 33 40115474

Mr. Rahul Agarwal

Research Associate BFSI [email protected] +91 33 40115400

Mr. Abhishek Roy Research Analyst

FMCG/Retail/Consumer Durables [email protected] +91 33 40115468 Mr. Anmol Das

Research Analyst Metals and Mining [email protected] +91 33 40115474 Mr. Vivek Sethia

Research Analyst [email protected] +91 33 40115400

Mr. Pra�m Roy

Research Analyst Oil & Gas/Tex�les pra�[email protected] +91 33 40115400 Mr. Anik Mitra Research Analyst IT/ Pharmaceu�cals

[email protected] +91 33 40115400

Mr. Dipanjan Basuthakur Sr. Research Analyst [email protected] +91 33 30515486

Sales Leadership Team

Contact Details

Mr. Monal Desai Sr. VP - Ins�tu�onal Sales [email protected] +91 2242005555 Mobile: +91 9821137303

Mr. Taj Mohammad 6th Floor, 654, Aggarwal Metro Heights, Netaji Subhash Place, Pitampura, New Delhi – 110034, India. [email protected] Phone: +91 9818754786

Mr. Vishal Prabhakar Sr. VP - PMS & PCG [email protected] +91 33 30515400 / 40115400 Mobile: +91 9831554477

Mr. Sohil I Khan Office No. 5G, New Marine Lines, Court Chamber, Mumbai - 400 020, Maharashtra, India Phone: +91 9930294893

Mr. Saurasanta Biswas Vaibhav, 4 Lee Road, Kolkata - 700020, India. [email protected] Phone: +91 9883604672

Mr. Deepankar Saha Research Assistant [email protected] +91 33 30515468

Ms. Debjani Sen Officer – Investor Rela�ons [email protected] +91 33 30515401

Investor Rela�ons and Data Support

Mr. Ajay Jaiswal President: Strategies and Head Research

[email protected] +91 33 30515408 / 40115408 Mobile: +91 9836966900

Mr. Rajesh Basu Majumdar Head Equi�es - Ins�tu�onal

[email protected] +91 33 30515400 / 40115400 Mobile: +91 9830267133

Mr. Rahul Kayan Director [email protected]

+91 33 30515419 / 40115419

Mr. Jaydeb Dey

Technical Analyst Equi�es [email protected] +91 33 30515433

Mr. Sam Nair

AVP - Commodi�es [email protected] +91 81138 52263

Commodity Research Technical Research

Research Team

Stock Recommenda�on Expected absolute returns (%) over 12 months

Strong Buy >20%

Buy between 12% and 20%

Accumulate between 6% and 12%

Hold between 0% and 6%

Sell 0 to <-10%

Neutral No Ra�ng

Mr. Nadim Heyat VP - Distribu�on [email protected] +91 33 30515400 / 40115400 Mobile: 9831253842/9674965154

28

&

29

&