the international tropical timber organization global outlook for the tropical timber trade and...

TRANSCRIPT

THE INTERNATIONAL TROPICAL TIMBER ORGANIZATION

Global Outlook for the Tropical Timber Trade Global Outlook for the Tropical Timber Trade

and Furniture Export Markets and Furniture Export Markets

Where are the Emerging Markets?Where are the Emerging Markets?

Trends in Tropical Timber Exports

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

Val

ue (

Billi

ons

US

D)

Primary Secondary

19961997

19981999

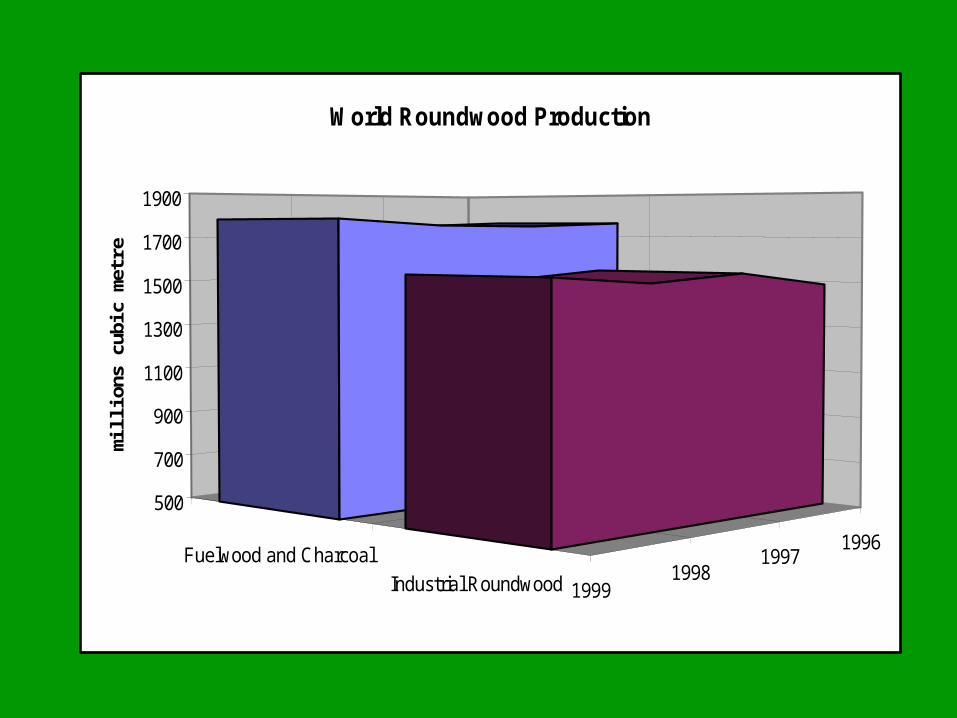

Fuelwood and Charcoal

Industrial Roundwood

500

700

900

1100

1300

1500

1700

1900

mill

ions

cub

ic m

etre

sWorld Roundwood Production

19951996

19971999 Fuelwood and

CharcoalIndustrialRoundwood

0

200

400

600

800

1000

1200

1400

1600

mil

lio

ns c

ub

ic m

etr

es

Developing Country Roundwood Production

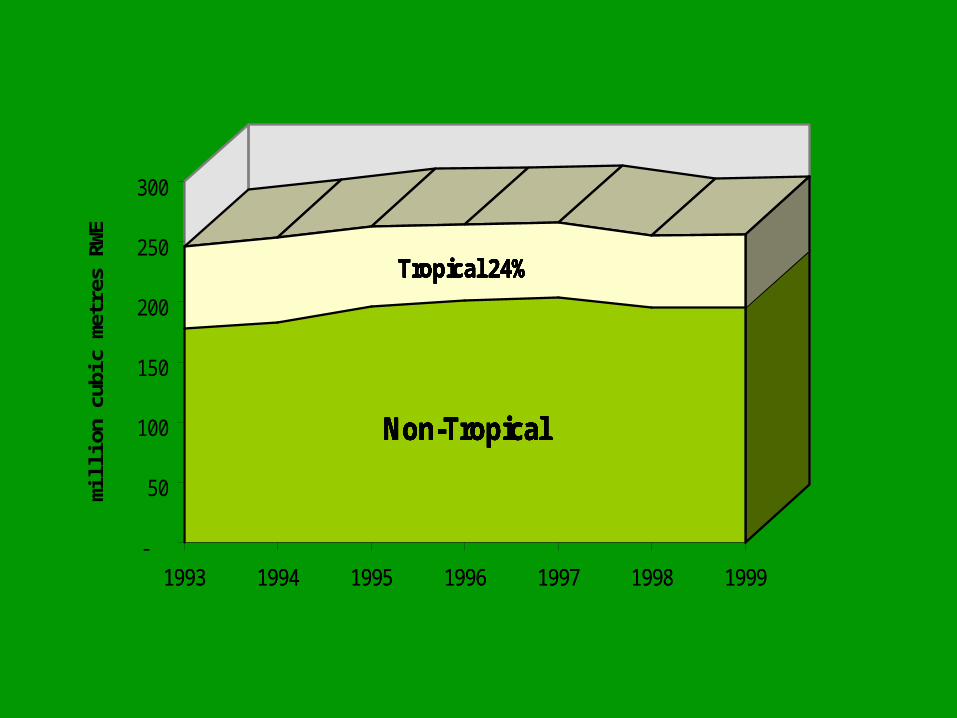

1993 1994 1995 1996 1997 1998 1999

Non-Tropical

Tropical 24%

Non-Tropical

Tropical 24%

Non-Tropical

Tropical 24%

Non-Tropical

Tropical 24%

Non-Tropical

Tropical 24%

Non-Tropical

Tropical 24%

Non-Tropical

Tropical 24%

Non-Tropical

Tropical 24%

-

50

100

150

200

250

300

mill

ion

cubi

c m

etre

s R

WE

1993 1994 1995 1996 1997 1998 1999

Composition of Exports By Region

0

10

20

30

40

50

60

Logs Sawnwood Veneer Plywood

Asia Pacific Latin America Africa

Imports of Tropical Timber 1996-2000

0

5000

10000

15000

20000

25000

1996 1997 1998 1999 2000

000'

s c

ub

ic m

etr

es

Japan EU 15 China

Japan's Tropical and Non-tropical Timber Imports

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1993 1994 1995 1996 1997 1998 1999 2000

RWE

Thou

sand

s

Tropical Non-tropical

China's Tropical and Non-tropical Timber Imports

0

2,000

4,000

6,000

8,000

10,000

12,000

1993 1994 1995 1996 1997 1998 1999 2000

RWE

Thou

sand

s

Tropical Non-tropical

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

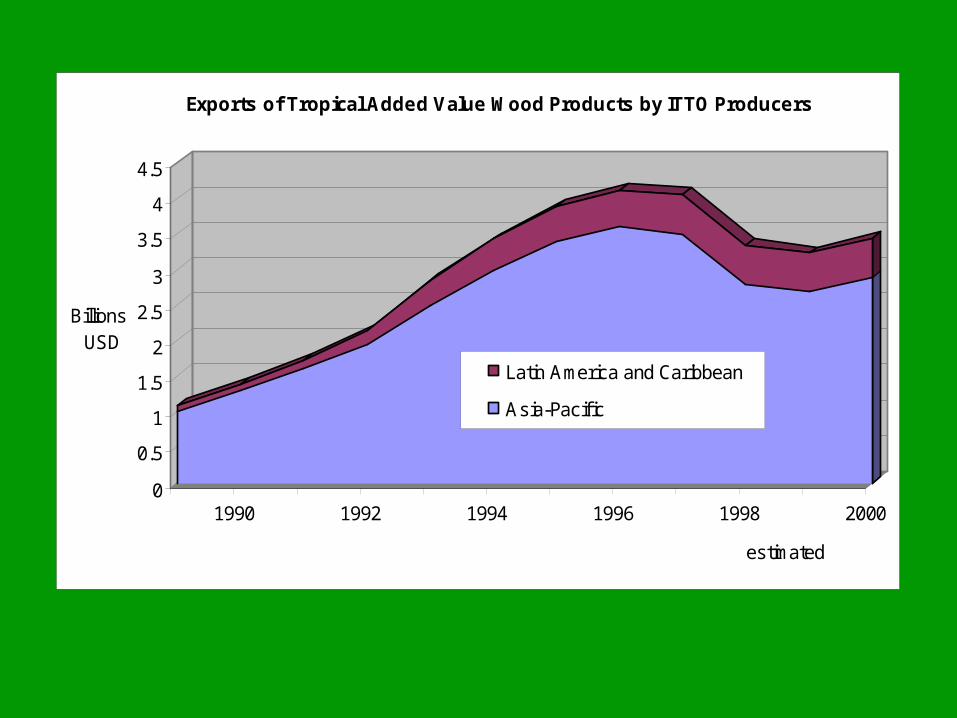

Billions USD

1990 1992 1994 1996 1998 2000

estimated

Exports of Tropical Added Value Wood Products by ITTO Producers

Latin America and Caribbean

Asia-Pacif ic

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

Billions USD

1990 1992 1994 1996 1998 2000

estimate

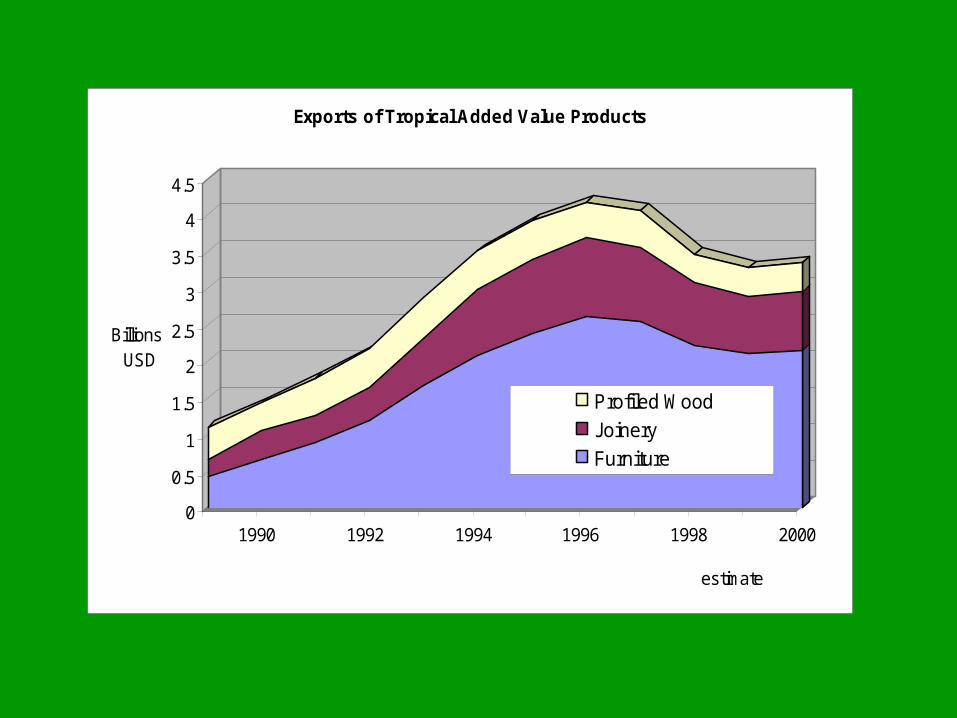

Exports of Tropical Added Value Products

Profiled Wood

Joinery

Furniture

0.00

0.50

1.00

1.50

2.00

2.50

Billion USD

1990 1992 1994 1996 1998 2000

estimate

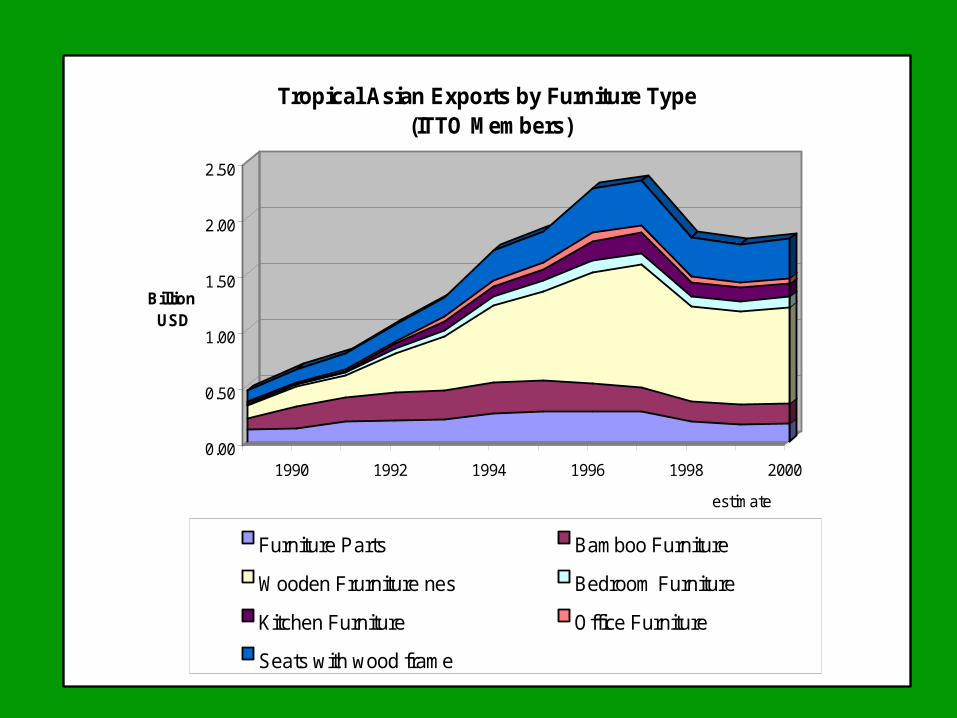

Tropical Asian Exports by Furniture Type (ITTO Members)

Furniture Parts Bamboo Furniture

Wooden Frurniture nes Bedroom Furniture

Kitchen Furniture Office Furniture

Seats with wood frame

World Furniture Production

Other Developed countries

18%

UK4%

Canada3%

Other Developing Countries

13%

Poland1%

Mexico3%

United States25%

Germany11%

Italy9%

France4% Japan

9%

Furniture Market Trends

• US, Germany and Japan not expected to grow

• Italy, France, UK, Brazil, Spain and Mexico to grow moderately

• Only China expected to show high growth

• Amongst other 40 markets

• India, Chile Ireland and Malaysia in high growth group

• General optimism of last year replaced by a more guarded posture

• US the engine of growth for the international furniture trade - demand for imported furniture has grown

• however the slowing US economy may put export trade under pressure, especially for medium-low priced furniture

• producers must prepare for weaker demand in major markets

• seek new niche markets, distribution systems and promotional tools

• introduce market specific designs and regularly launch new ranges

The Import “iceberg”

• Explosion of furniture imports to the US - account for 34% of all furniture sales

• 29% of all furniture imports from China - 1992 USD 69mil, over 2000 USD 1.8 bil.

• In 10 years just a handful of US domestic manufacturers

and in China

• Asia Pacific main force reshaping furniture trade

• China single most important country in region dynamics

• Chinese market holds promise for expanding trade in added value products

• house ownership encouraged

• home getting bigger

• imported brands favoured

• reduced domestic timber supply

• economy opening - WTO entry

• China market not lived up to expectations

• within a decade domestic production created stiff competition

• Now an aggressive exporter with non tariff barriers

• distribution channels, unclear customs and import licensing rules

Winning Market Share

• Added value exports will continue to grow at expense of primary product trade

• will expand at annual rate of 8-10%

• USD5 billion in 2001, USD 6.6 billion in 2003

• Win market share in OECD countries

• Widening base of sustainably produced timbers

• wage cost differentials and improving managerial skills

• advanced technologies and targeted promotion

• supportive institutions

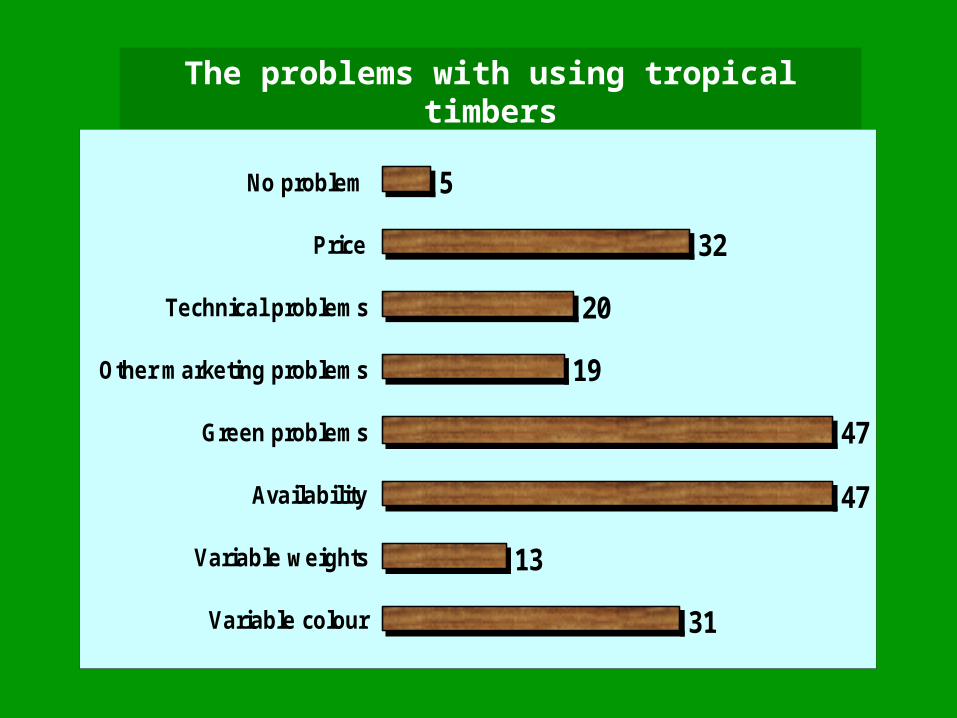

The problems with using tropical timbers

31

13

47

47

19

20

32

5

Variable colour

Variable weights

Availability

Green problems

Other marketing problems

Technical problems

Price

No problem

Which tropical country has scored greatest success with tropical added value exports?

43

18

8

2

3

1

2

Malaysia

Indonesia

Brazil

Chile

China

Taiwan

Ghana

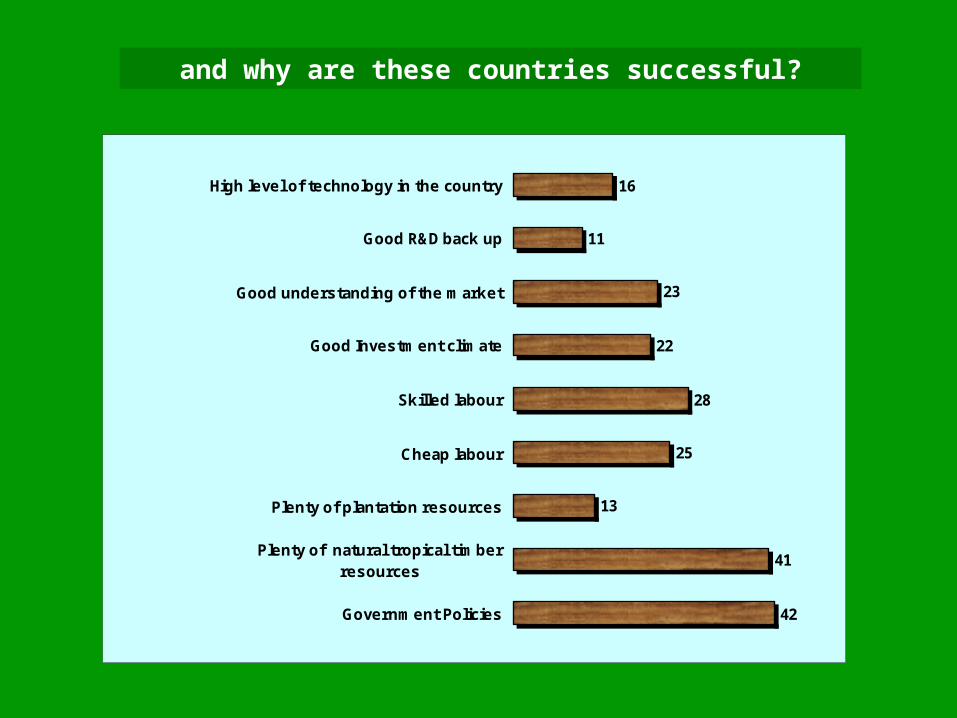

and why are these countries successful?

42

41

13

25

28

22

23

11

16

Government Policies

Plenty of natural tropical timberresources

Plenty of plantation resources

Cheap labour

Skilled labour

Good Investment climate

Good understanding of the market

Good R&D back up

High level of technology in the country

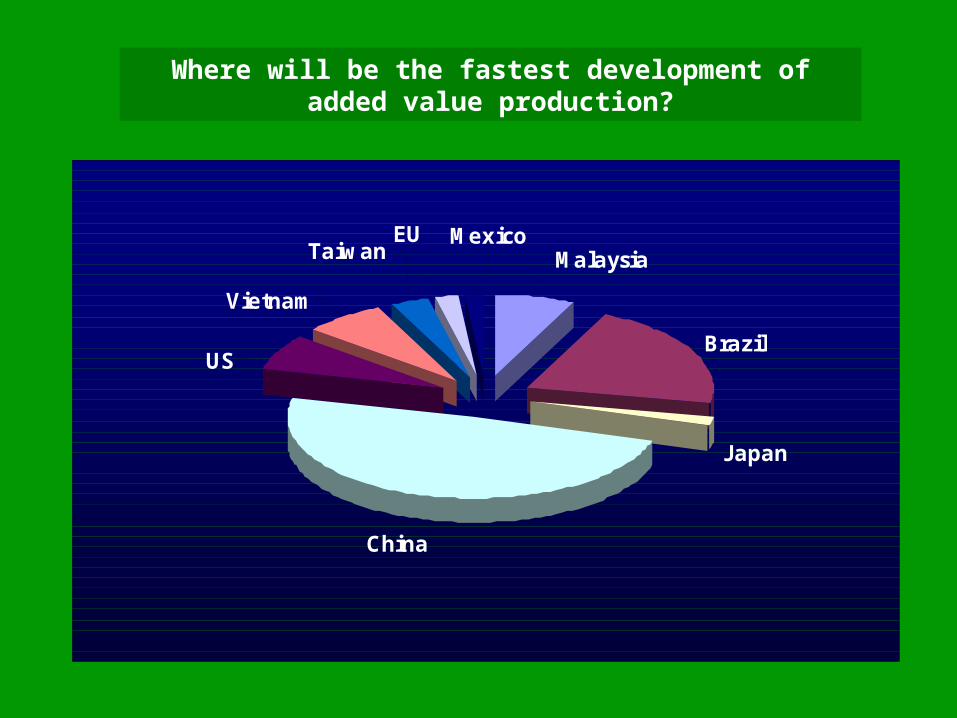

Where will be the fastest development of added value production?

Brazil

Japan

China

MalaysiaTaiwanMexicoEU

Vietnam

US

Forecast Trends in Exports of Primary and Secondary Tropical Products

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

estimated

Valu

e (B

illio

ns U

SD)

Primary Secondary