the latin american plastics industry market composition ... · the latin american plastics industry...

TRANSCRIPT

The Latin American Plastics Industry Market Composition &

Capital Spending Survey

Presented by:TECNOLOGÍA DEL PLÁSTICO

October, 2014

CONTENTS1.

Latin American Market Overview

2.

Buying Intention Survey

3.

Conclusions

1. LATIN AMERICAN MARKET OVERVIEW

Market Trend Evolution: Plastics Machinery and Molds Imports

Top Exporters of Plastics Machinery and Molds to Latin America

Top Latin American Buyers of Plastics Machinery and Molds

Market Trend Evolution: Raw Materials Imports

Top Exporters of Raw Materials to Latin America

Top Latin American Buyers of Plastics Raw Materials

What does Latin America represent out of the global US exports of plastics

machinery & materials?

Market Trend Evolution: Plastics Machinery and Molds Imports

(USD’000)

* Source: ALADI, the Latin American Integration Association. Figures only include 10 top Latin American economies. Figures based on the limited number of product categories included in this report.

• In terms of Machinery the region showed the following share of imports in 2013:- Injection Machinery: 35%- Others: 22%- Extrusion: 14%- Blow Molding: 8% - Vacuum Molding: 4%- Parts: 22%

• The region grew 21% between 2010 and 2013

Top Exporters of Machinery to Latin America2013‐

(USD’000)

* Source: ALADI, the Latin American Integration Association. Figures only include 10 top Latin American economies. Figures based on the limited number of product categories included in this report.

Germany leads as the top exporting country to Latin America with a 21.3% share of total imports, followed by

China’s 16.9% and USA’s 15.3% share of imports.

Top Exporters of Molds to Latin America2013‐

(USD’000)

* Source: ALADI, the Latin American Integration Association. Figures only include 10 top Latin American economies. Figures based on the limited number of product categories included in this report.

The USA leads as the top exporting country to Latin America with a 24.8% share of total imports, followed by

China’s 19% and South Korea’s 9.4% share of

imports.

Top Latin American Buyers of Plastics Machinery and Molds 2013

* Source: ALADI, the Latin American Integration Association. Figures only include 10 top Latin American economies.Figures based on the limited number of product categories included in this report.

• Mexico is the largest single importing country in Latin America with a significant 58% of the total, followed by Brazil with 24% and ROLA with 18%.

• According to ANIPAC, Mexico beats Brazil in total plastics demand (consumption plus exports), due the higher exports by Mexican companies.

• Brazil has 3X the number of plastics transformers of Mexico, but these companies have lower investments in machinery and equipment, and as such production capacity.

Market Trend Evolution: Raw Materials Imports(USD’000)

* Source: ALADI, the Latin American Integration Association. Figures only include 10 top Latin American economies.Figures based on the limited number of product categories included in this report.

• Polyethylene, PET, Polypropylene and PVC represented 73% of the total imports in 2013.

• In contrast, other materials for more specialized processes such as Polystyrene, Acrylic Polymers, Polyamides, Amino Resins, Silicones and Polymers of Vinyl Acetate represent and important 28% of the market.

• The region is adopting locally more and more their state-of- the-art plastics processing needs!

• Material exports to Latam grew 24.7% between 2010 and 2013!

Top Exporters of Plastics Raw Materials to Latin America2013‐

(USD’000)

* Source: ALADI, the Latin American Integration Association. Figures only include 10 top Latin American economies.Figures based on the limited number of product categories included in this report.

With a 50% share, The USA is the single largest

exporter of plastics raw materials to Latin America

Top Latin American Buyers of Plastics Raw Materials 2013

* Source: ALADI, the Latin American Integration Association. Figures only include 10 top Latin American economies. Figures based on the limited number of product categories included in this report.

Mexico is the largest single importing country in

America Latina of plastics raw materials with a 40% of the total, followed by Brazil with 26%. The rest of Latin

America represents a significant 34% of material

imports.

USA MATERIALS & MACHINERY EXPORTS TO LATAM ‐

USDC

* Source: ALADI, the Latin American Integration Association. Figures only include 10 top Latin American economies. Figures based on the limited number of product categories included in this report.

USA plastics resins, machinery, parts and mold exports to Latin America have grown for four

consecutive years since the global recession hit in 2009, showing a full recovery of the region. Total

USA exports to Latam

reached US$ 13 billion in the 21 product categories tracked in this chart!

Based on July ‘14 exports, the region is bound for growth in 2014!

PRODUCT CATEGORIES / USD EXPORTS 2009 2010 2011 2012 2013 2014 through July3901 Polymers Of Ethylene, In Primary Forms $2,537,487,749 $3,247,766,934 $3,515,463,088 $3,710,623,794 $4,109,491,896 $2,515,308,7373902 Polymers Of Propylene Or Other Olefins, Prim Forms $1,034,437,450 $1,383,456,796 $1,599,599,083 $1,511,285,582 $1,648,374,410 $970,294,0643903 Polymers Of Styrene, In Primary Forms $524,451,216 $697,066,374 $786,102,937 $786,435,210 $764,321,892 $431,910,1333904 Polymers Of Vinyl Chloride Etc., In Primary Forms $693,972,147 $944,467,751 $1,199,484,395 $1,124,456,391 $1,290,442,271 $739,826,3943905 Polymers Of Vinyl Acetate & Oth Vinyl Polym, Pr Fm $179,745,628 $203,342,669 $214,951,227 $234,644,783 $221,529,487 $114,779,6353906 Acrylic Polymers In Primary Forms $453,102,659 $639,881,828 $787,636,087 $768,113,198 $849,946,775 $459,306,0773907 Polyethers, Expoxides & Polyesters, Primary Forms $1,222,268,232 $1,623,969,793 $1,795,850,184 $2,063,322,486 $2,118,194,217 $1,278,161,9213908 Polyamides In Primary Forms $250,483,670 $398,629,070 $463,076,252 $512,151,542 $539,523,968 $327,685,6613909 Amino‐resins, Phenolics & Polyurethanes, Prim Form $344,330,720 $457,765,430 $508,149,473 $508,773,053 $476,448,879 $332,876,0463910 Silicones, In Primary Forms $185,830,716 $235,785,972 $240,962,673 $269,331,660 $282,906,475 $164,234,4773911 Petro Resins, Polysulfides Etc Nesoi, Primary Form $212,608,596 $290,249,318 $281,499,480 $251,944,247 $258,248,049 $169,513,2753912 Cellulose And Chemical Deriv Nesoi, Primary Forms $199,468,646 $191,001,078 $186,085,338 $191,251,732 $193,251,464 $104,858,6853915 Waste, Parings And Scrap, Of Plastics $26,923,383 $38,225,876 $39,158,810 $37,455,958 $39,484,783 $22,891,5148477109025 Inject‐molding Mach For Processing Thermoplastics (no) $67,210,551 $46,746,434 $41,680,662 $48,697,999 $45,204,090 $35,941,1438477200030 Extruders, Single Screw, For Thermoplastics (no) $3,046,014 $5,465,902 $3,034,512 $13,650,926 $7,106,974 $6,056,1258477200060 Extruders For Processing Thermoplastics, Nesoi (no) $5,791,025 $30,649,051 $13,311,431 $12,427,972 $27,022,551 $6,059,6508477300000 Blow‐molding Machines (no) $15,406,072 $13,757,696 $10,974,411 $18,830,762 $18,561,881 $5,070,6498477400100 Vacuum‐mold Mach & Oth Thermoforming Machine Nesoi (no) $8,986,451 $11,488,681 $19,839,100 $19,384,809 $18,780,895 $6,899,8348477900010 Parts Of Injection‐molding Machines (x) $56,447,975 $66,976,308 $63,831,097 $59,375,850 $62,553,999 $36,145,6688477900020 Parts Of Extruders For Rubber Or Plastics (x) $12,117,137 $11,726,965 $16,428,138 $17,719,783 $12,281,168 $12,907,5958477900030 Parts Of Blow‐molding Machines (x) $3,211,703 $7,226,308 $9,144,658 $5,971,472 $4,533,076 $3,778,281

TOTALS $8,037,327,740 $10,545,646,234$11,796,263,036 $12,165,849,209$12,988,209,200 $7,744,505,564VARIATION 31% 12% 3% 7%

USA SHARE OF EXPORTS TO LATAM FROM ITS GLOBAL MACHINARY EXPORTS2013‐

(USD’000)

* Source: ALADI, the Latin American Integration Association. Figures only include 10 top Latin American economies. Figures based on the limited number of product categories included in this report.

2013 USA plastics resins, machinery, parts and molds exports to

Latin America

reached closed to US$13 billion, representing 37% of the USA worldwide exports,

based on the 21 product categories tracked in the prior chart.

Latin America is a key and trusted trading partner of US exporters!

TOTAL US EXPORTS / USD 2009 2010 2011 2012 2013 2014 As of July

TOTAL LATIN AMERICA $8,037,327,740 $10,545,646,234 $11,796,263,036 $12,165,849,209 $12,988,209,200 $7,744,505,564

TOTAL US EXPORTS $25,088,073,369 $32,222,751,014 $35,434,952,398 $34,646,755,622 $35,551,376,075 $21,370,787,430

VARIATION 32% 33% 33% 35% 37% 36%

2. BUYING INTENTION SURVEY

Methodology and reachPlant Capacity Utilization Size of companies by number of employeesMain Markets/Sectors Served 2014‐2015 Projected Investment DistributionInvestment Intentions by Product SegmentBuying Intentions By Country of Origin

METHODOLOGY AND REACH

• E‐mail survey sent to 8,888

Latin

American subscribers of

TECNOLOGIA DEL PLASTICO

magazine.

• Limited to one answer by

company. In‐depth questionnaire.

• The survey obtained 1,094

valid

responses from 23

Latin American

countries, representing a 12%

response rate.

2013 Capacity utilization

Base: 897

• A healthy 38% of companies reported capacity usage of 80% or more.

• Only 13% of companies reported capacity usage of less than 50%

• In Mexico, the investment in capital goods has remained above US$1.6 billion annually since 2005, which confirms the continuing technology renovation and higher productivity of this key Latam country. (ANIPAC)

Size of Latin American Plants Included in the Survey By Number of Employees

Base: 897

• 28% of the sample was comprised of companies with 101+ employees

• 30% was comprised of companies between 21- 100 employees

• 42% was comprised of companies with 20 or less employees

Main Markets/Sectors Served

Base: 1094

• Latin American plastics processors in this sample concentrate mainly in recycling (24%), followed by flexible packaging (22%), products for industrial facilities (19%), rigid packaging (17%), construction (17%) and autoparts (14%).

• In Mexico, the imports of capital goods rose to exceed 2 billion dollars in 2012 and 2,2 billion in 2013.

• This growth can be attributed in part to investments made in the automotive industry, due to new OEM’s and autopart manufacturing plants opening in the past few years (i.e. Honda, VW, Nissan, BMW, Audi, Mazda and others), as well as major Tier-1 suppliers (i.e. Hella, Faurecia, ABC Group, Valeo)

Projected Investment Distribution

Base: 569

A significant 74%

of the sample that

will invest in 2014-

2015, will acquire

new equipment vs.

26% that will buy

used or refurbished

equipment.

Base: 1094

Plastic transformation processes of the companies involved in the survey

The results of the Survey emulate the same pattern that results from the

actual import figures from

ALADI.

Companies who want to invest in equipment / machinery during the

next 12 months (2014‐2015)

Base: 1094

A healthy 69% of the Sample indicated their intention to invest in capital equipment in the next 12 months!

Buying Intention: Auxiliary Equipment

Base: 628

• 57% of the sample indicated their intention to buy Auxiliary Equipment.

• Recycling equipment reported the highest buying intention of the sample.

• All product references show strong 2 percentage digit buying intentions.

Buying Intention: Extrusion Lines

Base: 239

• 22% of the sample indicated their intention to buy Extrusion Equipment.

• The extrusion was one of the first processes used by the Mexican plastics industry and currently accounts for about 31% of the total volume of processed plastics. (ANIPAC)

• In Mexico, the imports of extrusion machinery has grown and now represents 17% of the machinery market in the country. (ANIPAC)

Buying Intention: Hydraulic Injection Molding Systems

Base: 229

• 21% of the sample indicated their intention to buy Hydraulic Injection Molding Equipment.

• In Mexico, around 30% of the total production of plastic components is obtained by plastics injection molding process. (ANIPAC)

• Machinery for injection molding represents the largest category of imports from primary plastics processing machinery. (ANIPAC)

Buying Intention: Molds

Base: 386

• 35% of the sample indicated their intention to buy Molds.

• In Mexico, the molds for injection molding represent over 90% of total imports of molds and tooling. (ANIPAC)

• According to ANIPAC, in 2012 there was an increase in the value of imports of molds and tooling in Mexico, due to a significant increase in injection molds for products/parts of more than 5 kg. (ANIPAC)

• In 2013, the same situation reached a record of more than twice the value recorded in 2000. (ANIPAC)

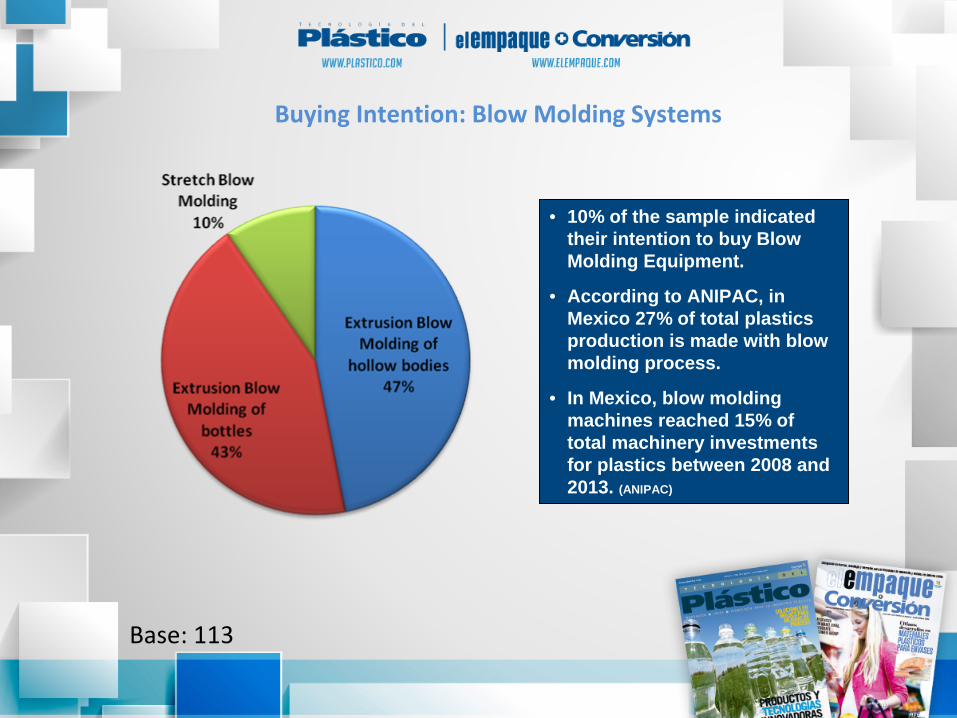

Buying Intention: Blow Molding Systems

Base: 113

• 10% of the sample indicated their intention to buy Blow Molding Equipment.

• According to ANIPAC, in Mexico 27% of total plastics production is made with blow molding process.

• In Mexico, blow molding machines reached 15% of total machinery investments for plastics between 2008 and 2013. (ANIPAC)

Buying Intention: Thermoforming Systems

Base: 68

• 6% of the sample indicated their intention to buy Thermoforming Equipment.

• In Mexico, 3% of the total production of plastics derive from thermoforming processes. (ANIPAC)

• Imports of thermoforming machinery and vacuum forming machinery correspond to no more than 6% of the value of total imports. (ANIPAC)

Base: 569

Buying Intention By Country of Origin

Asian suppliers are the preferred choice with

59% of the buyers indicating they intend to buy from Asia, followed by 36% from Europe and

35% from the USA or Canada.

Conclusions: Positive Market Behavior

38% of the sample reported plant capacity utilization of +80%, showing healthy production levels in the region!

69% of the sample indicated they had the intention to invest in

Capital Equipment in the next 12 months.

Recycling equipment (34%), Feeders & loaders (32%), heating & cooling systems (28%) and measuring & quality

control systems (23%) topped the list of auxiliary equipment the

sample intents to buy in 12 months.

Blown film (37%), pipe and profiles (29%) and solid sheet (14%)

topped the list of extrusion lines the sample

indicated they would buy in the next 12 months.

110‐400 tons (39%), 30 to 100 tons (23%) and 410 to 800 tons (19%) topped the list of hydraulic injection

molding machines the sample indicated they would buy in the next

12 months.

74% of the sample indicated they would buy NEW equipment. Good news for new equipment manufacturers!

A significant 59% of the Buying Intention survey sample expressed interest in buying Asian equipment, vs. 35%

from the USA or Canada and 36% from Europe.

All indicators showed growth for Plastics Machinery, Molds and Material imports from Latin America in 2013!

Mexico is the top importer of Equipment, Molds and Materials in the region!

Latin America represents 37% of the total US exports to the plastics industry!

Conclusions & Final remarks: Latin is going green!

Latin American plastics processors in this sample concentrate mainly in the recycling (24%),

followed by flexible packaging (24%), products for industrial facilities (19%), rigid packaging

(17%), construction products (17%), households products (16%) and autoparts

(14%).

A significant 30% of the sample is involved in recycling processes. Green

mentality is catching

up in Latin America.

According to ANIPAC, the recycling of plastics in Mexico has grown significantly and has

become an indispensable thriving industry.

In 2012, in Mexico recycled about 1.6 million tons of plastic, equivalent to 21.3% of plastic

waste generated.

THANK YOU!¡GRACIAS!

For additional information contact

our Associate Publisher Giovana

Reyes at:

704‐396‐6412

www.plastico.com/media‐kit