the lean and agile bss the difference between success and ... · white paper: the lean bss 3...

TRANSCRIPT

‘Thought Leaders in Quadruple P lay and Emerging Wireless Technologie s’

The Lean and Agile BSS The difference between success and failure for smaller carriers

A White Paper by Rethink Technology Research

Lead author: Caroline Gabriel, Research Director September 2016

In association with

White paper: The lean BSS

2

Executive Summary In a world of rising competition, spiraling data demands and the threat from over-the-top services, the challenges facing communication service providers (CSPs) have never been greater. For the smaller CSPs which sit outside tiers 1 and 2, the landscape looks even more daunting. At a time of operator consolidation and huge infrastructure investments, is the day of the regionally or vertically focused provider over? Looking at the trends in the market, the answer is a resounding ‘no’. The smaller CSPs still account for as many as 20% of mobile and fixed connections worldwide, and in some areas their role is expanding, especially as over-the-top services and the Internet of Things (IoT) usher in new business models for highly specialized operators. And these smaller CSPs have advantages which larger players do not. They have lower overheads and greater ability to change quickly, and they often understand their customers very deeply. Their challenge is to play to their strengths, which do not lie in the price wars and economies of scale of the giants. Instead, they must seek new ways to differentiate themselves, and to develop new sources of revenue growth, which are clearly distinct from those of the tier 1 carriers. In a survey of about 40 smaller CSPs round the world, conducted for Amdocs by Rethink Technology Research, three areas of differentiation emerged as critical:

A sharp business focus and well-targeted services, which concentrates resources on areas where the CSP can add value

Agility to introduce new services, promotions and tariffs in response to customer needs and so behave more like an over-the-top (OTT) player

Highly personalized customer service All these are areas with which larger organizations often struggle, but the smaller CSPs are well aware that they will only achieve these goals if their platforms are aligned to the more agile, targeted approach. In this, a new-style BSS will be the most important investment many providers will make in the 2016-2018 period (and 73% will invest in a new or upgraded system in that time). For 28% of the respondents, a lean and flexible BSS will be the most important enabler of their competitive strategy, and they are looking to the industry to deliver a BSS which is specifically tailored to the needs of the smaller player, with a heavy focus on total cost of ownership, automation and support for granular personalization. In addition, the adoption of cloud-based BSS will be particularly important in transforming smaller CSPs’ cost base and business agility. A cloud approach promises the advantages of significantly lower software licensing and infrastructure costs, combined with real time data which can support agile business decisions and customer responsiveness – all key competitive elements. This paper examines the key business strategies of smaller CSPs in the 2016-2018 timeframe and the systems they believe they will need to achieve their goals.

White paper: The lean BSS

3

Amdocs’ Viewpoint Midsized Communication Businesses (MCBs) are in the midst of a battle for survival. Faced with rising competition, as well as the challenges of falling ARPU, lower profits, increased regulation and changing customer expectations, the need to differentiate has never been more crucial. To better understand the issues MCBs are facing, we engaged Rethink Technology Research to canvas a broad set of service providers within this segment, and ask them about their path to the future. This included the current key growth opportunities and what they need to do in order to achieve their goals. From this research, it emerged that a modern and flexible BSS, support for customer experience management and the ability to deploy in the cloud are the most important enablers for creating differentiated offerings and driving new revenues. The research reaffirms the premise behind the creation of Amdocs Optima, a digital customer management & commerce platform, which can rapidly and securely monetize any product or service. This new offering provides unprecedented agility and ease in configuration to support any level of complexity. Deployed in the cloud or on premise, the solution can handle all customer types – from residential service providers and small businesses to enterprises operations – and offers profitable ways to grow beyond the current supported business models. With 73% of respondents expecting to invest in a new or updated BSS in the next 2-3 years, we hope the following research will provide some insights into what your colleagues worldwide are doing to survive and thrive profitably into the future. For more information on how Amdocs can help you, please contact your local Amdocs representative or visit Amdocs Optima at www.amdocsoptima.com Meri Christenson Product Marketing Manager Amdocs Optima

Table of Contents Amdocs’ Viewpoint 3 Introduction: The market landscape 4

1. Where are the growth opportunities for smaller CSPs? 4 2. The differentiation challenge 6 3. The advantages and challenges for smaller CSPs 8 4. The importance of the BSS to the business case 10 5. The optimal BSS for smaller CSPs 11

Conclusion 13

White paper: The lean BSS

4

Introduction: The market landscape The tier 1 communication service providers (CSPs) may grab most of the headlines, but smaller operators still account for a substantial share of the market for mobile, fixed and converged internet services. At the start of 2015, about 19% of fixed and mobile connections were managed by operators outside Tiers 1 and 2. 1 Indeed, as Internet connectivity becomes pervasive in every part of life, that share may well increase, as more specialized providers emerge, serving a particular application, user group or vertical. There are various ways to define the different operator tiers, such as subscriber numbers, geographical reach, or the degree to which they rely on other carriers’ infrastructure. For the purposes of this paper, we will focus on those falling below tier 2, excluding MVNOs. This is a very varied group, but its members have certain attributes in common:

Subscriber numbers or connections below 10 million Regional or local reach, sometimes national in small countries Owning their own infrastructure in their coverage area

Traditionally, these smaller carriers have been associated with simple voice and data services (fixed or mobile) for a limited geographical area or user group. However, the range of business models in this group is diversifying rapidly. For instance, some CSPs target a particular vertical sector which has distinctive requirements for performance, applications or support and built their networks primarily to address those. This will become more common as the Internet of Things (IoT) evolves with its wide range of vertical-focused use cases The profile of the smaller CSPs is also changing in response to the rise of OTT services. They need to mimic the agility and cost-effectiveness of those providers, while continuing to offer their customers additional value – which may mean investment in quality of service or in new applications. In some cases, smaller operators may partner with OTT firms to offer ‘the best of both worlds’.

1. Where are the growth opportunities for smaller CSPs? Despite the challenges, there is clearly room for smaller carriers to increase their market share and the value/profitability of the services they offer. Indeed, in a survey of small CSPs conducted by Rethink in December 2015, there was a high level of confidence that the smaller carriers could outperform the overall market, in terms of revenue growth. Assuming an annual growth rate of 3.1% in mobile2 communications and minus 2% in fixed services3 between 2015 and 2020, a full 24% of smaller carriers expected to outperform those figures and only 12% expected to underperform.

1 Rethink Technology Research estimates January 2016 2 GSMA, ‘Global Mobile Economy Report 2015’ http://www.gsmamobileeconomy.com/GSMA_Global_Mobile_Economy_Report_2015.pdf 3 Ovum, ‘Telecoms Media and Entertainment Outlook 2015’, http://info.ovum.com/uploads/files/Ovum_Telecoms_Media_and_Entertainment_Outlook_2015.pdf

White paper: The lean BSS

5

This paper will examine the key opportunities they perceive, and what they need to deploy in order to turn that potential into commercial reality. It is clear that, for operators of all sizes, a key challenge is that ARPU and profit are under pressure from factors including rising competition, the decline of paid-for voice and messaging, challenges from over-the-top services and so on. Increasingly, those CSPs – in any tier – which continue to grow their revenue and margins are doing so by:

Achieving greater market share in ‘basic’ services (voice and data access), through consolidation or competitive services

Bundling a larger number of services to extend the subscriber relationship, with multi-play offerings, increasingly personalized to the user or company

Creating incremental revenue streams on top of data access and voice, such as enterprise, cloud or content applications

Targeting specific user groups which will pay a premium for services that meet their particular requirements, e.g. for high security, excellent quality of service, etc.

Smaller CSPs need to be able to deploy these weapons just as national and international carriers are doing, and they are well aware that their service and revenue mix will have to change in order to achieve their growth objectives. This is clear from the survey results (see Figure 1). The respondents were asked to name their top three sources of revenue now, and what they expect to deliver the greatest growth in the 2016-2018 period.

Figure 1. % of respondents placing each use case in their top 3 current sources of revenue, and top 3 targeted to deliver incremental growth in 2016-2018

0

10

20

30

40

50

60

70

80

90

100

% o

f re

spo

nd

ents

Current Growth

White paper: The lean BSS

6

Currently, mobile and/or fixed voice and data are the major revenue sources – and will remain so, but the growth potential will slow and so other services will need to be added too. Already, triple play, enterprise and video services are cited as top three revenue generators by at least 20% of the operators. Those are also the elements which will drive the greatest new growth, along with multi-play services (combinations of fixed-line and mobile voice, video and data services with, increasingly, other modules such as connected car or smart home services). Cloud services, vertical market applications and content are also expected to be more important to future growth than they are to the current revenue mix. The changing mixture of revenue streams is similar in pattern to that seen among Tier 1 and 2 providers, which are also relying more heavily on targeted, vertical or added value services. This presents new competitive challenges for smaller CSPs, since they are targeting similar new revenue streams but with smaller resources. Therefore, smaller CSPs that want to be competitive will have two key commercial challenges:

To sustain growth and profit in conventional voice and data services, by lowering the cost of delivery, bundling and gaining market share (organically or through acquisitions). This also means seeking differentiation by means of quality of service, or well-targeted bundles – not by price alone

To generate new revenues from additional business models such as enterprise and multi-play services

In order to compete on more than just price, they will also need to adopt platforms which allow them to differentiate themselves clearly from their larger or over-the-top rivals.

2. The differentiation challenge The survey found that there are three key ways in which smaller CSPs will differentiate themselves from larger rivals:

Agility – launching new services, tariffs and bundles more quickly and in response to customers’ changing demands

Focus – concentrating resources on a particular service, vertical market, or community where they have specialized understanding and can add significant value

Personalized service– harnessing local or market knowledge to provide personalized services and bundles, and a high level of advanced customer support, including smart self-service

These three strategies will be examined in more detail below, with regard to the demands they will make on the providers’ business systems, but they add up to a significantly new approach for smaller providers to punch above their weight with creative approaches to differentiation. The survey shows that many smaller CSPs want to change the way they differentiate to attract new users, reduce churn and improve their margins. The basic competitive elements of price and data speed will remain important, of course, but if they are the only differentiators, they create price wars which are very hard for smaller carriers to win.

White paper: The lean BSS

7

They have far greater advantages in the critical areas of agility, focus and personalization, especially as new markets and services open up new ways to attract and retain customers. These may include offering specialized applications for certain vertical sectors, such as smart energy monitoring for utilities, or personalized customer service for enterprises, for instance. Here they can offer something different from their competitors, whether those are larger operators (or subsidiaries of large groups) on one hand, or MVNOs on another. One example is an increased focus on selected vertical services where the CSP can offer specialized support. In its survey, Rethink found that, between 2012 and 2015, consolidation among localized providers has been offset by the emergence of vertically targeted firms4. These most commonly offer a full range of services – fixed, mobile and sometimes value added offerings like cloud – to a particular vertical market, or group of verticals. At the end of 2015, 25% of smaller CSPs were focused only on business markets (corporate, SMB or vertical), with 5% of them specializing in just one or two verticals (see Figure 2). That was up from 21% the previous year. Vertical specialists included, for example, CSPs offering voice and data services to emergency services workers, sailors, factories and farmers – all user groups with particular requirements in terms of remote customer support, network quality agreements, and tailored data and applications - which might not be cost-effective for a tier one operator to address.

Figure 2. CSPs below tier 2 by business model (% of CSPs). Source: Rethink Technology Research global operator survey, December 2015

Figure 3 highlights a broader shift in thinking among smaller carriers, in terms of how they need to differentiate themselves and so improve their performance. Currently, the differentiators which are most commonly placed in the top three are data speed, price and level of customer support. These are the only factors cited by more than 50% of respondents, though almost 40% also ranked network quality of service (QoS) and special promotions, such as a high value device or a bundled content subscription, in their top three. 4 Rethink Technology Research RAN Research Service www.rethinkresearch.biz

52

11

12

14

65

Consumer mobile Household fixed Household multiplay SMB Corporate Vertical

White paper: The lean BSS

8

Then the operators were asked to rank the same factors, in terms of future importance for generating improved revenues and profits. This showed a shift away from price and raw speeds, towards service-related differentiators, with almost 60% believing that good customer support and QoS would be in their top three, in terms of importance to the business model, by 2018. Other factors which are expected to have an increased impact by 2018 include innovative bundles, specific business applications, the agility to deliver new services quickly, support for self-service, and customized offerings.

Figure 3. % of respondents placing each differentiator in their top three for now, and in 2018

3. The advantages and challenges of smaller CSPs In creating a business model around these differentiators, the smaller providers have some natural advantages over those in the top tiers. In many cases they may have:

Greater agility, because their small size allows them to implement change quickly Deeper understanding of their customers, and closer relationships with them, because they are

more specialized, either in geography or type of customer Lower costs of operation in some areas with limited overhead even while lacking economies of

scale In other words, scale is a double-edged sword. Smaller CSPs may not have the budgetary resource to invest in the same range of tools as a larger player – but this can be turned to their advantage. Large operators have often built hugely complex systems to handle their escalating numbers of events and transactions, which come with high operating costs. Smaller CSPs do not need this level of complexity – for instance, they generally do not need to support multi-country languages and tax regimes.

0

10

20

30

40

50

60

70

80

90

% o

f re

spo

nd

ents

Now 2018

White paper: The lean BSS

9

The risk is that smaller CSPs find themselves having to invest in systems that are over-specified for their needs (23% of respondents said their existing BSS had more functionality than they require) due to the lack of options available. But if they can select a flexible, configurable tool, whose functions can be mapped (and adapted) to their actual business processes and volumes, they can often achieve a better ratio of cost:revenue than larger players. As we will see later, cloud-based solutions are increasingly being identified by smaller CSPs as a means to achieve the flexibility they require. Another important aspect of cost-effective BSS is the availability of tools and application programming interfaces (APIs) to support simple integration with third party products to add functionality in a streamlined way. These examples highlight the criticality of mapping cost to volume and revenue, and having the flexibility to scale up and down if required. Cost-related issues emerged as the most critical ones in the CSP survey (see Figure 4). When asked to name the key challenges to achieving their business goals of new revenue streams and enhanced differentiators, the factors which were most frequently placed in the top three all related to cost:

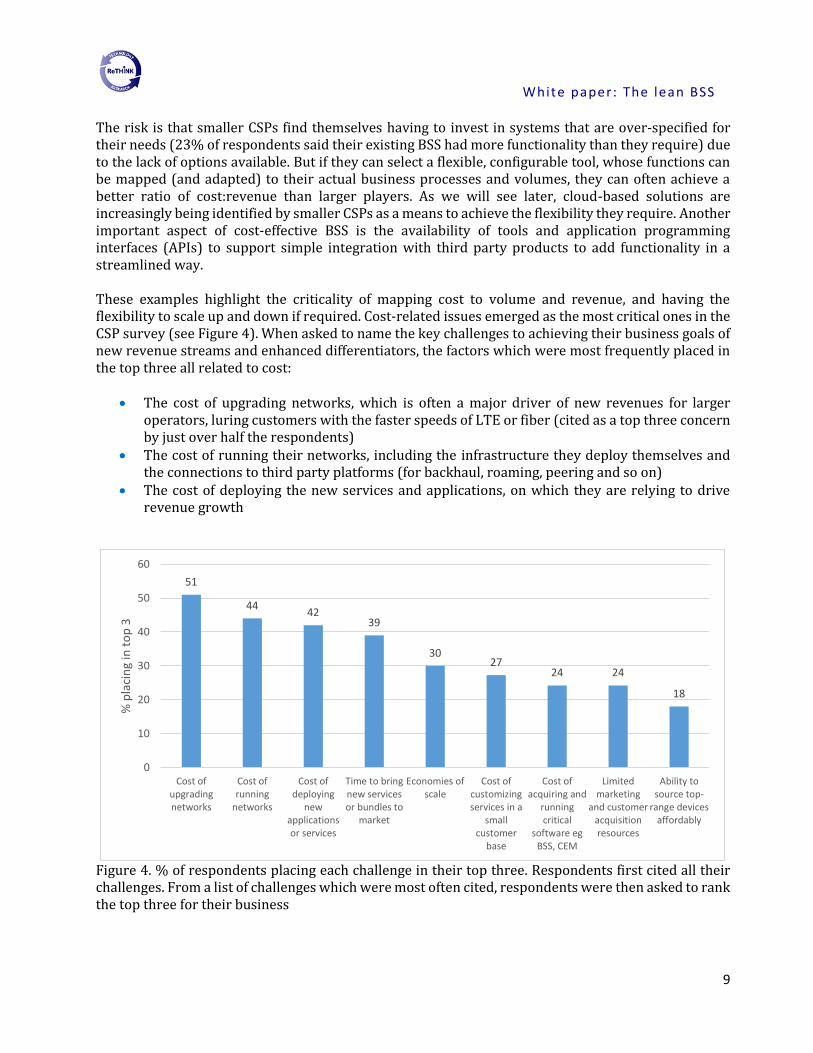

The cost of upgrading networks, which is often a major driver of new revenues for larger operators, luring customers with the faster speeds of LTE or fiber (cited as a top three concern by just over half the respondents)

The cost of running their networks, including the infrastructure they deploy themselves and the connections to third party platforms (for backhaul, roaming, peering and so on)

The cost of deploying the new services and applications, on which they are relying to drive revenue growth

Figure 4. % of respondents placing each challenge in their top three. Respondents first cited all their challenges. From a list of challenges which were most often cited, respondents were then asked to rank the top three for their business

51

4442

39

3027

24 24

18

0

10

20

30

40

50

60

Cost ofupgradingnetworks

Cost ofrunning

networks

Cost ofdeploying

newapplicationsor services

Time to bringnew servicesor bundles to

market

Economies ofscale

Cost ofcustomizingservices in a

smallcustomer

base

Cost ofacquiring and

runningcritical

software egBSS, CEM

Limitedmarketing

and customeracquisitionresources

Ability tosource top-

range devicesaffordably

% p

laci

ng

in t

op

3

White paper: The lean BSS

10

Other important challenges include time to market for new services, economies of scale, the cost of supporting customization, and limited resources for marketing or device procurement. In other words, smaller CSPs need to reduce their costs in relation to their revenues dramatically. And they also need to compensate for their limited scale by demonstrating high levels of agility and innovation, taking advantage of their nimbleness and their keep knowledge of their particular customer bases.

4. The importance of the BSS to the business case Among all the systems at a CSP’s disposal, one is of paramount importance to maximizing flexibility, agility and resource efficiency. That is the business support system (BSS). In the survey, 28% - the largest percentage - said a modern, flexible BSS will be the most important enabler of the competitive

strategy. Smaller CSPs need a BSS which has been designed with their specific needs in mind. It is just as important for a smaller CSP to invest in new networks and back office systems as its larger rivals, but their pockets

are less deep, and so it is even more challenging to fund these major deployments, without sacrificing investments in other areas. They need to focus on systems which are agile and flexible, rather than massive ‘big bang’ upgrades, so they can maximize the business impact of every dollar invested.

Figure 5. Most important enabler of new revenues and differentiators, per % of response

28

19

17

14

14

8

Flexible BSS to support targetedservices

Customer experience managementsystem

Hosted/cloud systems for keyfunctions

Improved customer analytics

Upgraded RAN e.g. LTE-A

New network architecture e.g. HetNet

Almost three-quarters (73%) of CSPs below Tier 2 expect to invest in a new or upgraded BSS in the coming 2-3 years

White paper: The lean BSS

11

A flexible BSS is the most important enabler of respondents’ plans to introduce new services and differentiators (see Figure 5), along with greater reliance on hosted/cloud services (17%) and customer experience management (CEM) systems (19%). These were more important than network-related developments such as heterogeneous networks or LTE-Advanced. Although CSPs of all sizes need to invest in network upgrades, they are unlikely to be at the cutting edge in this area, and place greater importance on differentiating at service level rather than network level

5. The optimal BSS for smaller carriers The BSS is a major source of CAPEX and OPEX expense, and so smaller carriers have sometimes been hesitant to invest in a heavy platform, or have been deterred by solutions which are overkill for their needs. But increasingly they recognize that this is a question of return on investment, not just upfront cost. The BSS not only supports all the operator’s key business processes, but also makes the difference between effective and ineffective service delivery, customer support and innovation. Therefore, holding back from investment is a false economy, but the maximum ROI will come from a new breed of BSS. The old-style BSS will no longer meet all the needs of a modern operator, and it certainly does not deliver the stringent cost and agility requirements of the smaller carrier, as described above. In the new age of multi-play, IoT, OTT and other diverse services, operators of all sizes need to:

provide differentiated digital content or services support transactions and commerce create customized bundles of services for specific

users or groups enable different methods of billing and charging, for different user and application

requirements support rapid deployment of new and sometimes highly targeted services

Many legacy BSS offerings cannot do all this, since they were developed for a simpler market focused on voice and data access, not a wide range of ever-changing services. In many cases, they are based around data siloes, with little integration between the systems that run the various charging methods and services, and even less integration with customer data. By contrast, in order to compete with larger carriers on one side, and MVNOs or Wi-Fi providers on the other, CSPs need a unified, real time BSS solution which can manage and offer flexible billing for multi-play bundles, content, on-demand services, subscription services and applications. For the smaller carriers, in particular, this BSS must be

Cost optimized – lean; requiring limited in-house team; perhaps outsourced or virtualized Automated – to reduce cost and speed up delivery of new services Agile – to enable the CSP to offer new bundles, services or tariffs highly flexibly, with very

short time-to-market

The top requirements of a new-style BSS:

Low TCO (47% place in their top three critical requirements)

Customer self-service (36%)

Automation (34%)

Ability to personalize services or bundles (33%)

White paper: The lean BSS

12

A new breed of solutions is emerging which ticks these boxes, delivering the business benefits of a modern BSS without the need for a huge platform upgrade process. They may be offered as a traditional on premise solution or hosted in the cloud, for ease of deployment and maintenance with the option for support to be outsourced and a predictable monthly fee. Typically, these solutions are very lean and modular, and allow the operator to deploy just the capabilities they need for their business case at any one time, adding further modules as that case changes in future, with all the integration carried out by the vendor. For instance, the Rethink survey found that, at the current time, total cost of ownership (TCO), automation and flexibility are the most important requirements for smaller CSPs moving to a more agile model (see Figure 6). Integration with other software, such as big data analytics, and virtualization, are of interest, but less urgent at this stage – but the platform must be sufficiently open and future-proof that these priorities can change in future, without the CSP needing a new BSS.

Figure 6. % of respondents placing each BSS characteristic in their top three requirements

47

3634 33

31

25 25

22 22

14

11

0

5

10

15

20

25

30

35

40

45

50

% p

laci

ng

in t

op

3

White paper: The lean BSS

13

Among the capabilities which emerged as most important to the CSPs, apart from low TCO, are:

Web-based self-service interfaces for customer empowerment automation to streamline business processes, reduce cost of delivery and drive flexibility flexible service creation platform to maximize market agility and support personalization the option of a hosted cloud solution, which can have an important impact on the economics of

their business (see below) ability to support dynamic bundling of different options, and special promotions or upselling,

on the fly, to maximize monetization links to customer data in CRM and CEM systems, so that services and promotions can be

tailored to individuals or groups, and advertising revenues generated links to OSS and RAN data, so that customer experience can be monitored on a real time basis APIs to support links to third party networks and apps offering the flexibility needed to solve

future business requirements Increasingly, these key requirements are being most effectively met by cloud-based solutions. In the December survey, almost one-third of smaller CSPs said a cloud-based system was a top three requirement for a new BSS. When the question was asked again six months later, that percentage had risen to 38%, reflecting that the cloud is becoming a priority for a rising number of providers. And an even higher percentage, 68%, expected to deploy some element of cloud BSS within two years.5 This was above the result for the entire community, at 61%, showing that smaller CSPs are leading the way. The initial reasons to prefer a cloud solution reflect the key challenges and BSS criteria outlined above – increased OPEX efficiency and cost predictability; increased flexibility in fulfilment and assurance; more agile response to customer requirements. Longer term, some CSPs are looking for additional value from a cloud approach including the improved ability to introduce new types of services, ad support for a new line of business or offer ‘as-a-service’ options for customers. Conclusion A BSS which can support all these capabilities, while remaining affordable and easy to deploy/manage, will be the key enabler of success for many smaller CSPs, allowing them to innovate in the services and business models they offer, while keeping their costs low. This will be more significant to the survival and growth of smaller CSPs than any other investment, and will drive intense interest in this sector over the coming 2-3 years. In that time, at least73% of CSPs below tier 2 expect to invest in a new or updated BSS, whether in-house or hosted, and among those, only 5% do not plan to have any cloud-based elements. These CSPs will look for platforms with the flexibility to offer them access to the very best functionality, but mapped to their actual processes and volumes, so that costs are in line with business returns. In many cases the cloud will be the enabler of such systems, and they can be expected to drive a new wave of service innovation for smaller operators around the world.

5 Rethink Technology Research ‘Cloud OSS/BSS migration plans’ June 2016

White paper: The lean BSS

14

About Rethink Technology Research Rethink Technology Research is a specialized research and consulting firm with 14 years’ experience in surveying wireless, broadband, over-the-top and quad play operators. This has resulted in a broad research base of over 100 service providers (MNOs, telcos, cable and satellite operators, over-the-top providers) worldwide. These organizations are surveyed on a regular basis about their network infrastructure and business plans, and have a relationship of trust with Rethink. Together with that unique research base among CSPs, Rethink has deep relationships with the telecoms ecosystem (vendors, technology developers, integrators, regulators etc), and is perceived as a thought leader in many areas of the telecoms and media sectors. Rethink provides input to business models and strategic reviews for operators, vendors and the investment community, and its research, forecasts and deep analysis support critical decision making throughout the mobile and wireless ecosystem. For more on Rethink’s services and publications, visit www.rethinkresearch.biz.

About Amdocs Amdocs is the market leader in customer experience software solutions and services for the world’s largest communications, entertainment and media service providers. For more than 30 years, Amdocs solutions, which include BSS, OSS, network control, optimization and network functions virtualization, coupled with professional and managed services, have accelerated business value for its customers by simplifying business complexity, reducing costs and delivering a world-class customer experience. The Amdocs portfolio enables service providers to capture the world of digital immediacy by operating across digital dimensions to engage customers with personalized, omni-channel experiences; creating a diversified business to capture new revenue streams; becoming data empowered to make business and operational decisions based on insight-based and predictive analytics; and achieving service agility to accelerate the fast rollout of new technologies and hybrid network services. Amdocs and its more than 24,000 employees serve customers in over 90 countries. Listed on the NASDAQ Global Select Market, Amdocs had revenue of $3.6 billion in fiscal 2015. Amdocs: Embrace Challenge, Experience Success.

Rethink Technology Research Ltd Research Director: Caroline Gabriel [email protected] Unit G-5, Bristol and Exeter House, Lower Station Approach, Temple Meads, City of Bristol, BS1 6QS Telephone: +44 (0)1794 521411.