the main planning metrics of long term care planning

DESCRIPTION

The Main Planning Metrics of Long Term Care Planning. Wednesday July 28, 2010 D. Corey Rieck, MBA, CLTC. Certified in Long-Term Care Program www.ltc-cltc.com. The Main Planning Metrics of Long Term Care. Your Presenter: D. Corey Rieck, MBA, CLTC President, Founder, LTCcompass - PowerPoint PPT PresentationTRANSCRIPT

The Main Planning Metrics The Main Planning Metrics of Long Term Care Planningof Long Term Care Planning

Wednesday July 28, 2010Wednesday July 28, 2010D. Corey Rieck, MBA, CLTCD. Corey Rieck, MBA, CLTC

Certified in Certified in Long-Term Care Long-Term Care

ProgramProgramwww.ltc-cltc.comwww.ltc-cltc.com

The Main Planning The Main Planning Metrics of Long Metrics of Long Term CareTerm Care

Your Presenter:Your Presenter:

D. Corey Rieck, MBA, CLTCD. Corey Rieck, MBA, CLTCPresident, Founder, LTCcompassPresident, Founder, LTCcompassPhone: (678) 990-3664Phone: (678) 990-3664Email: Email: [email protected]: Website: www.ltccompass.com

CLTC 2 Day Master Class Instructor since CLTC 2 Day Master Class Instructor since 20032003

CLTC LTC Partnership Training Instructor CLTC LTC Partnership Training Instructor since 2008since 2008

Thousands of agents trained since 2003 in Thousands of agents trained since 2003 in the LTC arenathe LTC arena

Personal LTCI producer since 1999Personal LTCI producer since 1999

Results to be achieved Results to be achieved from today’s webinar:from today’s webinar:

How systematic, processed based LTC How systematic, processed based LTC Education can help you as it relates to Education can help you as it relates to expectation settingexpectation setting

Educational DeliveryEducational Delivery Obtain additional insight as to how to Obtain additional insight as to how to

choose the LTC Planning Metrics choose the LTC Planning Metrics – Daily Benefit AmountDaily Benefit Amount– Benefit PeriodBenefit Period

Results to be achieved Results to be achieved from today’s webinar:from today’s webinar:

Obtain additional insight as to how Obtain additional insight as to how to choose the LTC Planning Metrics:to choose the LTC Planning Metrics:– InflationInflation– Claims Payment OptionsClaims Payment Options– Home Care Percentage optionsHome Care Percentage options– Elimination PeriodElimination Period

Results to be achieved Results to be achieved from today’s webinar:from today’s webinar:

Case Design and Set upCase Design and Set up A new way to consider LTC A new way to consider LTC

PlanningPlanning Co-insuringCo-insuring

What is What is your your education delivery education delivery system?system?

Have you committed it to paper?Have you committed it to paper?

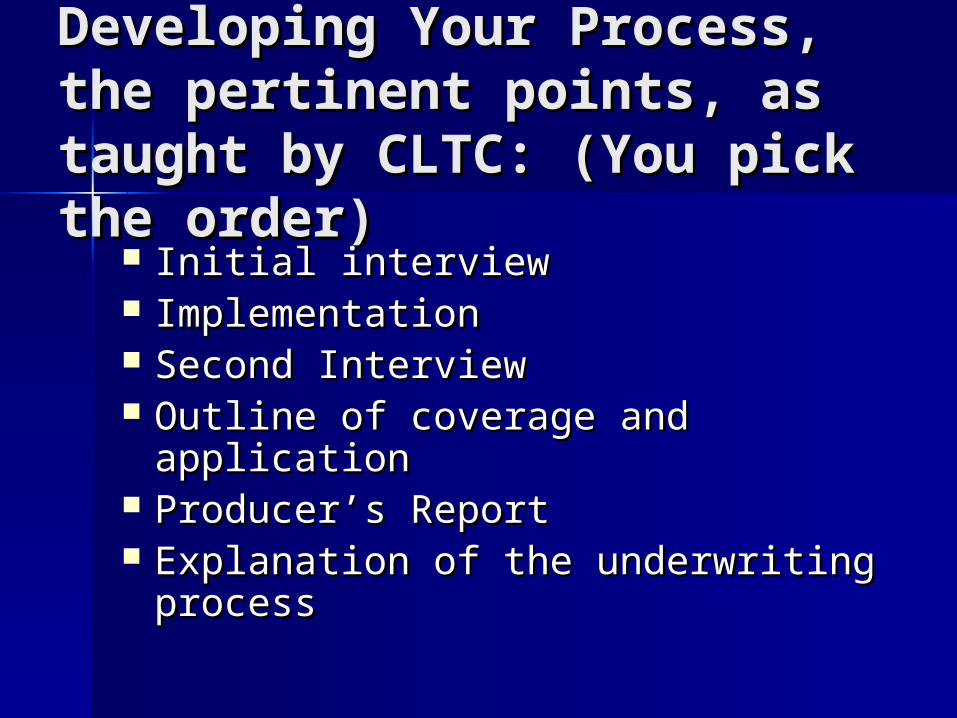

Developing Your Process, Developing Your Process, the pertinent points, as the pertinent points, as taught by CLTC: (You pick taught by CLTC: (You pick the order)the order)

Initial interviewInitial interview ImplementationImplementation Second InterviewSecond Interview Outline of coverage and applicationOutline of coverage and application Producer’s ReportProducer’s Report Explanation of the underwriting Explanation of the underwriting

processprocess

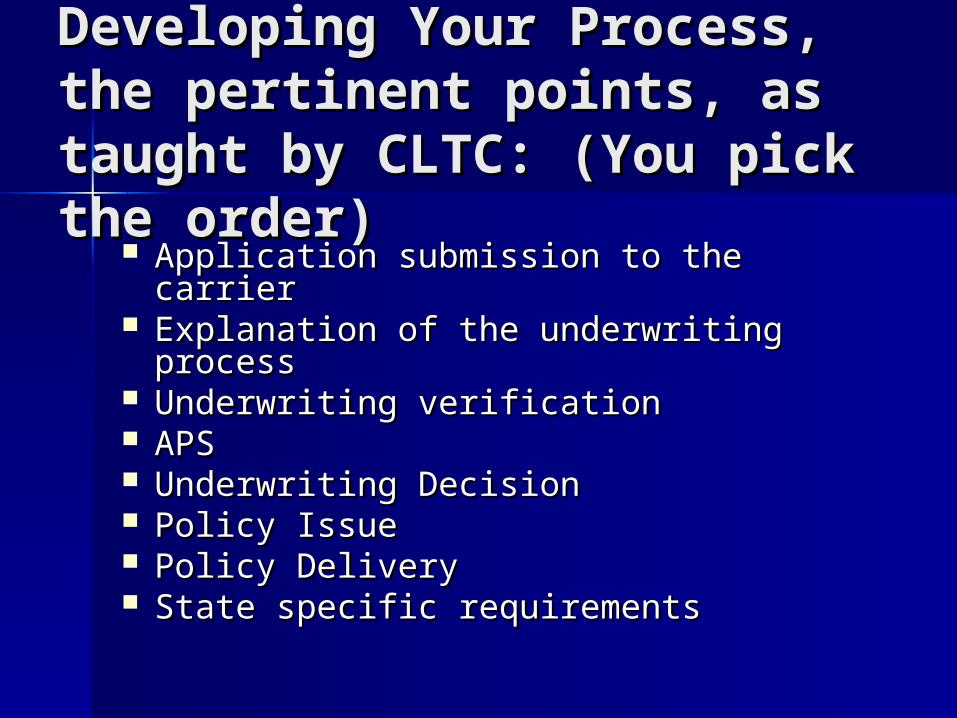

Developing Your Process, Developing Your Process, the pertinent points, as the pertinent points, as taught by CLTC: (You pick taught by CLTC: (You pick the order)the order)

Application submission to the carrierApplication submission to the carrier Explanation of the underwriting Explanation of the underwriting

processprocess Underwriting verificationUnderwriting verification APSAPS Underwriting DecisionUnderwriting Decision Policy IssuePolicy Issue Policy DeliveryPolicy Delivery State specific requirementsState specific requirements

Systematic, Processed Based LTC Systematic, Processed Based LTC Education/Assistance:Education/Assistance:– Education/DiscoveryEducation/Discovery– Underwriting/Expectation SettingUnderwriting/Expectation Setting– ImplementationImplementation

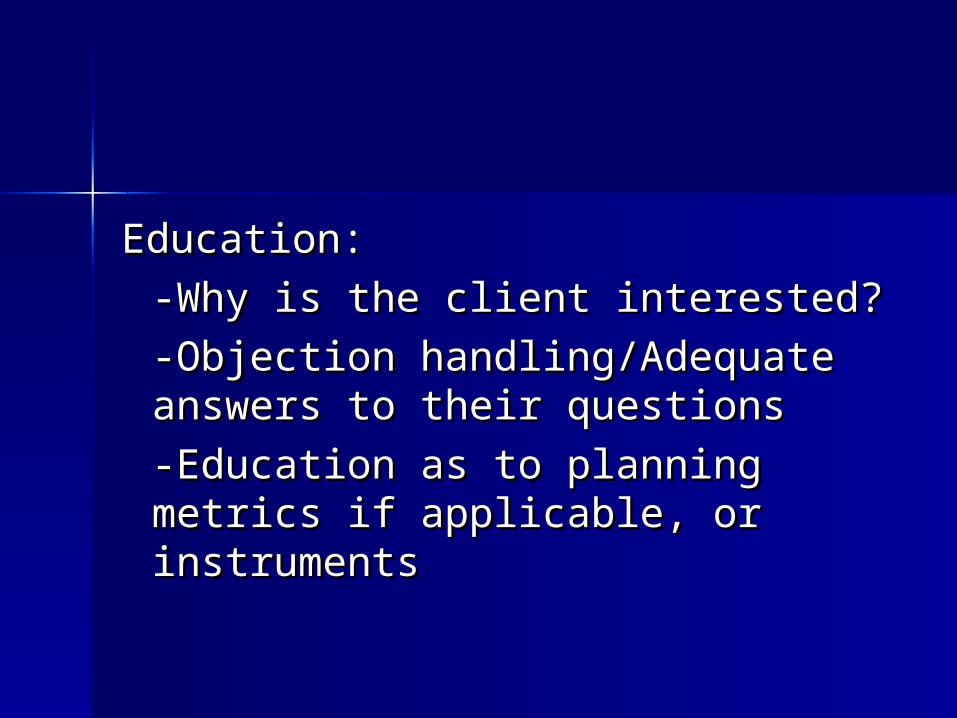

Education:Education:

-Why is the client interested?-Why is the client interested?

-Objection handling/Adequate -Objection handling/Adequate answers to their questionsanswers to their questions

-Education as to planning -Education as to planning metrics if applicable, or metrics if applicable, or instrumentsinstruments

Discovery:Discovery:– How do you determine if you How do you determine if you

can help the client after you can help the client after you have educated them?have educated them?

– Two step process or one Two step process or one step?step?

– Are they insurable?Are they insurable?

Discovery:Discovery:– Underwriting:Underwriting:

10 year medical history10 year medical history10 year surgical history10 year surgical historyMedicationsMedicationsUnderwriting differentiationUnderwriting differentiation

Discovery:Discovery:– Framing the options they may Framing the options they may

have, based on what they tell youhave, based on what they tell you– Expectation settingExpectation setting– Commitment to the process if one Commitment to the process if one

person from a couple is person from a couple is uninsurableuninsurable

– Analogous to the Dentist’s “Full Analogous to the Dentist’s “Full mouth x-ray and exam”mouth x-ray and exam”

Credibility:Credibility:

If your process is committed to paper, If your process is committed to paper, you can email it to the clients after you can email it to the clients after your discussion.your discussion.

Once you have done this, you can Once you have done this, you can refer to it during your educational refer to it during your educational process.process.

If you have a website, you may post it If you have a website, you may post it therethere

If you can’t health qualify, If you can’t health qualify, what difference does the what difference does the premium you would be premium you would be willing to pay make?willing to pay make?

Don’t get too caught up in Don’t get too caught up in the premium until the premium until underwriting is complete; underwriting is complete; keep the options open……keep the options open……

Underwriting/Expectation Underwriting/Expectation Setting:Setting:– Does the client present with Does the client present with

significant or multiple significant or multiple medical issues?medical issues?

– Do you work with more than Do you work with more than one carrier or instrument?one carrier or instrument?

Here is where the case is Here is where the case is won or lostwon or lost

Underwriting/Underwriting/Expectation Setting:Expectation Setting:

Scenario:Scenario:– Is Is youryour process committed to paper? process committed to paper?

Tell the client what you are going to tell Tell the client what you are going to tell themthem

Tell themTell them Use your process that is committed to Use your process that is committed to

paper to tell them what you told them.paper to tell them what you told them. Refer to it during the processRefer to it during the process

Considerations:Considerations:

What kind of client/prospect do What kind of client/prospect do you have?you have?– Prior Experience with LTC?Prior Experience with LTC?– Next Logical Step in Financial Next Logical Step in Financial

Planning?Planning?– Wealthy?Wealthy?

Considerations:Considerations:

What kind of client/prospect do What kind of client/prospect do you have?you have?– How do they present from an How do they present from an

underwriting perspective?underwriting perspective? What carriers make the most sense?What carriers make the most sense? What instruments make the most What instruments make the most

sense?sense?

– Retail?Retail?– Wholesale?Wholesale?

How CLTC can help:How CLTC can help:

CLTC V 8 Text:CLTC V 8 Text:– Appendix 7 Top 20 ProspectsAppendix 7 Top 20 Prospects– Appendix 8 CLTC Planning Process Appendix 8 CLTC Planning Process

workbookworkbook– Appendix 9 CLTC Client Interview Appendix 9 CLTC Client Interview

Road mapRoad map

How CLTC can help:How CLTC can help:

Graduate WebsiteGraduate Website

Power Point PresentationsPower Point Presentations

One Page Tax GuideOne Page Tax Guide

Ask The ExpertsAsk The Experts

How CLTC can help:How CLTC can help:

Have you shared with your Have you shared with your client/prospect the CLTC 3 step client/prospect the CLTC 3 step process?process?

Decision Area I:Decision Area I:

Traditional Health Long Term Care?Traditional Health Long Term Care?Asset Based Long Term Care?Asset Based Long Term Care?

Carrier Considerations?Carrier Considerations?

Client pre-dispositionsClient pre-dispositionsWholesale/Retail CaseWholesale/Retail Case

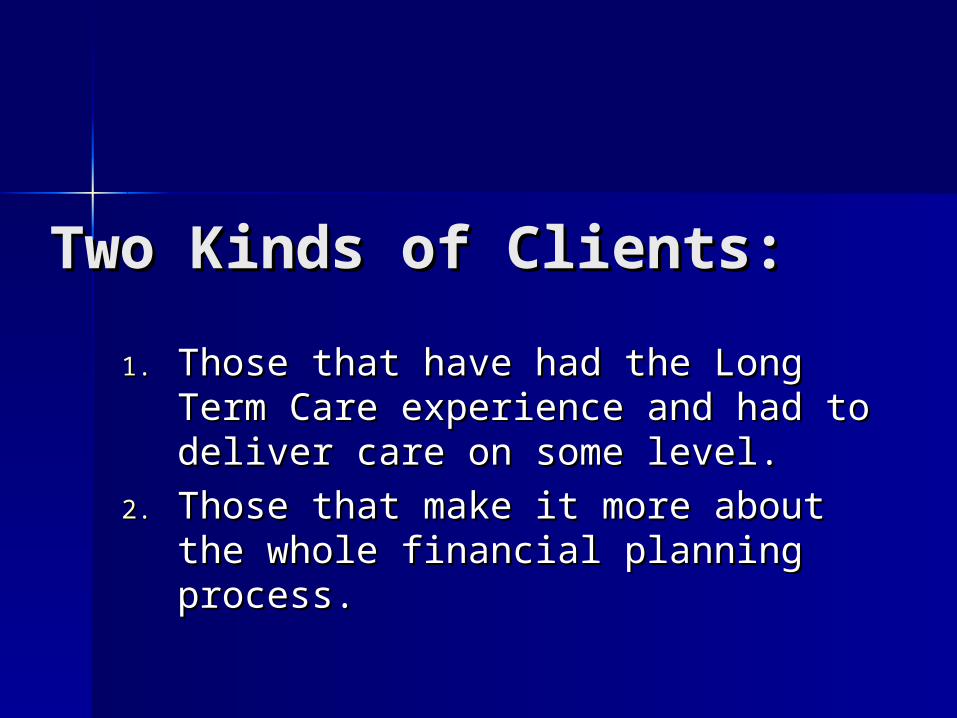

Two Kinds of Clients:Two Kinds of Clients:

1.1. Those that have had the Long Term Those that have had the Long Term Care experience and had to deliver Care experience and had to deliver care on some level.care on some level.

2.2. Those that make it more about the Those that make it more about the whole financial planning process.whole financial planning process.

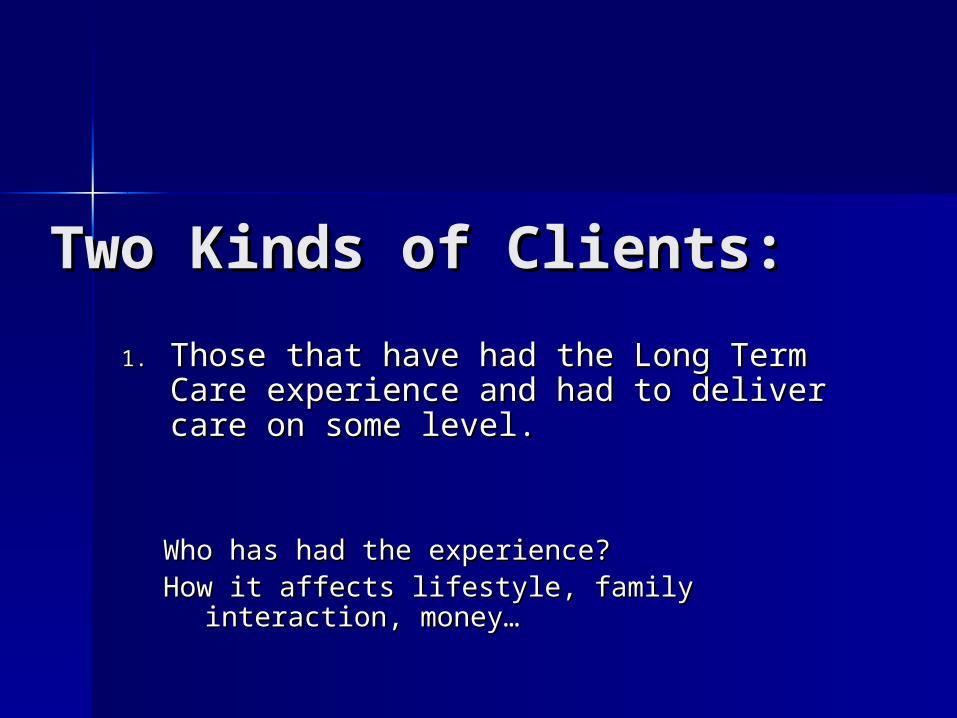

Two Kinds of Clients:Two Kinds of Clients:

1.1. Those that have had the Long Term Care Those that have had the Long Term Care experience and had to deliver care on experience and had to deliver care on some level.some level.

Who has had the experience?Who has had the experience?How it affects lifestyle, family interaction, How it affects lifestyle, family interaction,

money…money…

7474 3232

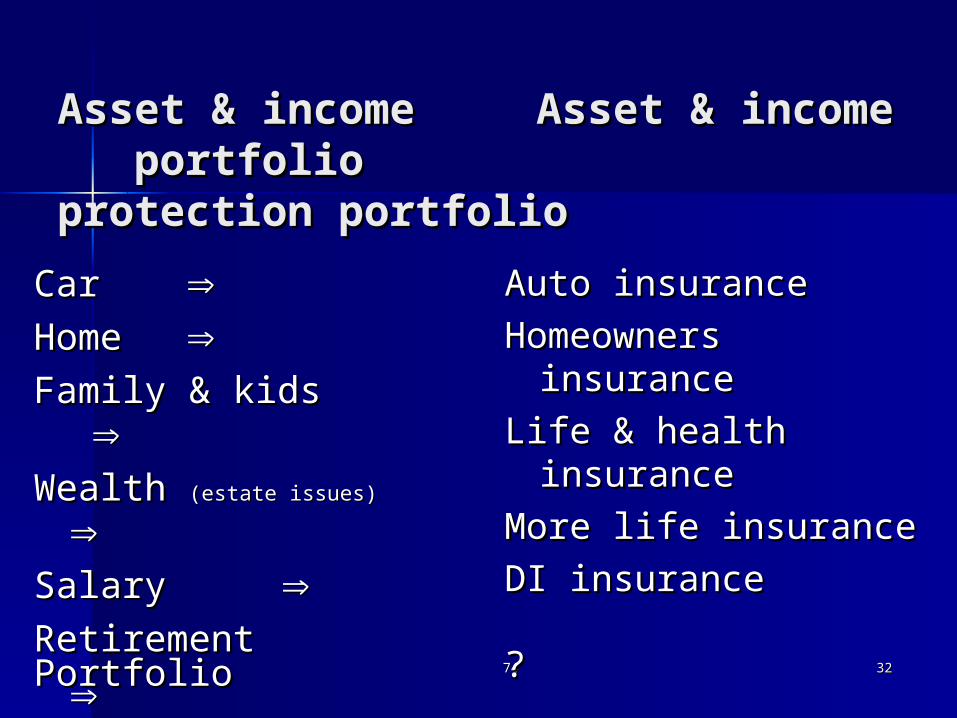

Asset & incomeAsset & income Asset & incomeAsset & income portfolio portfolio protection protection portfolio portfolio

CarCar HomeHome

Family & kids Family & kids Wealth Wealth (estate issues) (estate issues) SalarySalary Retirement Retirement PortfolioPortfolio

Auto insuranceAuto insurance

Homeowners Homeowners insuranceinsurance

Life & health Life & health insuranceinsurance

More life insuranceMore life insurance

DI insuranceDI insurance

??

Educational Delivery:Educational Delivery:

A Timeline Process that may work A Timeline Process that may work for you for you

Applicable Underwriting Applicable Underwriting Expectations:Expectations:

Why is this relevant?Why is this relevant?

Steps/considerationsSteps/considerations

Rocks in the riverRocks in the river

How underwriting could possibly How underwriting could possibly affect the individual planning affect the individual planning metricsmetrics

Planning Metric Number Planning Metric Number I:I:

Daily Benefit AmountDaily Benefit Amount

Daily Benefit Amount :Daily Benefit Amount :

Considerations:Considerations:-Health of the client?-Health of the client?-Wealth of the client?-Wealth of the client?-Are you helping a single person or -Are you helping a single person or

a couple?a couple?-Which instrument?-Which instrument?-Which carriers?-Which carriers?

Long Term Care Planning Metric Long Term Care Planning Metric Number 1: Daily Benefit AmountNumber 1: Daily Benefit Amount(DBA)(DBA)

Dollar Amount from $50--$500Dollar Amount from $50--$500 Study what the following costs are for your area:Study what the following costs are for your area:

– Home Health Care: (Hourly)Home Health Care: (Hourly)– Nursing HomeNursing Home (Daily) (Daily)– Assisted LivingAssisted Living (Monthly) (Monthly)

Geography is criticalGeography is critical– Where do you live now?Where do you live now?– More importantly, where will you live?More importantly, where will you live?

– The more daily benefit you buy, the more premium you investThe more daily benefit you buy, the more premium you invest

Daily Benefit Amount :Daily Benefit Amount :

Considerations:Considerations:-Geography:-Geography:

-where is your client living now?-where is your client living now? -where will your client live?-where will your client live? -do they own multiple homes?-do they own multiple homes? -if so, where are they most likely -if so, where are they most likely

receive care?receive care?

Daily Benefit Amount :Daily Benefit Amount :

Considerations:Considerations:

-Geography:-Geography:

-what if they want to live over -what if they want to live over seas?seas?

Daily Benefit Amount :Daily Benefit Amount :

Considerations:Considerations:

-Carrier Surveys that discuss:-Carrier Surveys that discuss:

-Nursing Home Costs-Nursing Home Costs

-Assisted Living Costs-Assisted Living Costs

-Home Care Costs-Home Care Costs

-Adult Day Care Costs-Adult Day Care Costs

Daily Benefit Amount :Daily Benefit Amount :

Considerations:Considerations:-Carrier Surveys that discuss:-Carrier Surveys that discuss: -Give client a copy for their records…-Give client a copy for their records…

Don’t they need to know what they Don’t they need to know what they could be “on the hook for” if they could be “on the hook for” if they don’t follow through with your advice?don’t follow through with your advice?

ComplianceCompliance

Daily Benefit Amount :Daily Benefit Amount :

Considerations:Considerations:-How much of the risk does the -How much of the risk does the

client want to take on?client want to take on?-What kind of risk tolerance do they -What kind of risk tolerance do they

have if you manage investments?have if you manage investments?-Co-insuring the risk-Co-insuring the risk

-getting to that amount -getting to that amount

Planning Metric Number Planning Metric Number II:II:

Benefit PeriodBenefit Period

Benefit Period:Benefit Period:

Considerations:Considerations:-Step 1 of the 3 step process-Step 1 of the 3 step process-Longevity in client/prospect family:-Longevity in client/prospect family:

-Parents-Parents -Grand parents-Grand parents -Siblings-Siblings -Aunts-Aunts

Benefit Period:Benefit Period:

Considerations:Considerations:-Longevity:-Longevity:

-Uncles-Uncles -Other applicable family members-Other applicable family members

Does the client think they could Does the client think they could live a long life?live a long life?

Benefit Period:Benefit Period:

Considerations:Considerations:

-Risk Tolerance-Risk Tolerance

-Co-insuring considerations-Co-insuring considerations

-Benefit Period issues:-Benefit Period issues:

-Finite benefit issues-Finite benefit issues

-Carrier trends toward benefit -Carrier trends toward benefit periodperiod

Planning Metric Number Planning Metric Number III:III:

InflationInflation

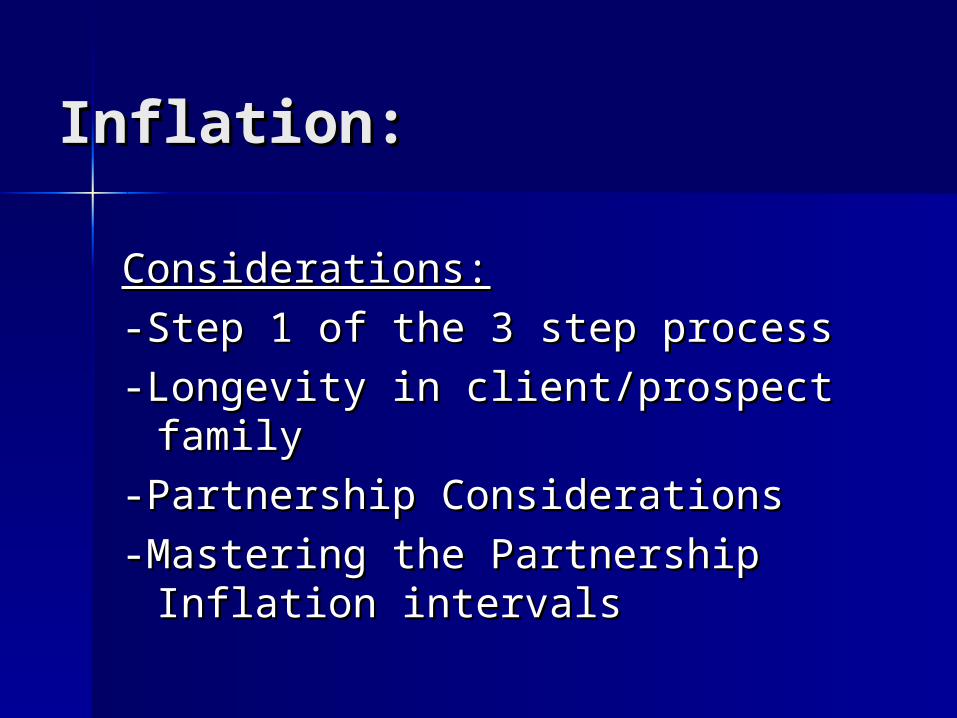

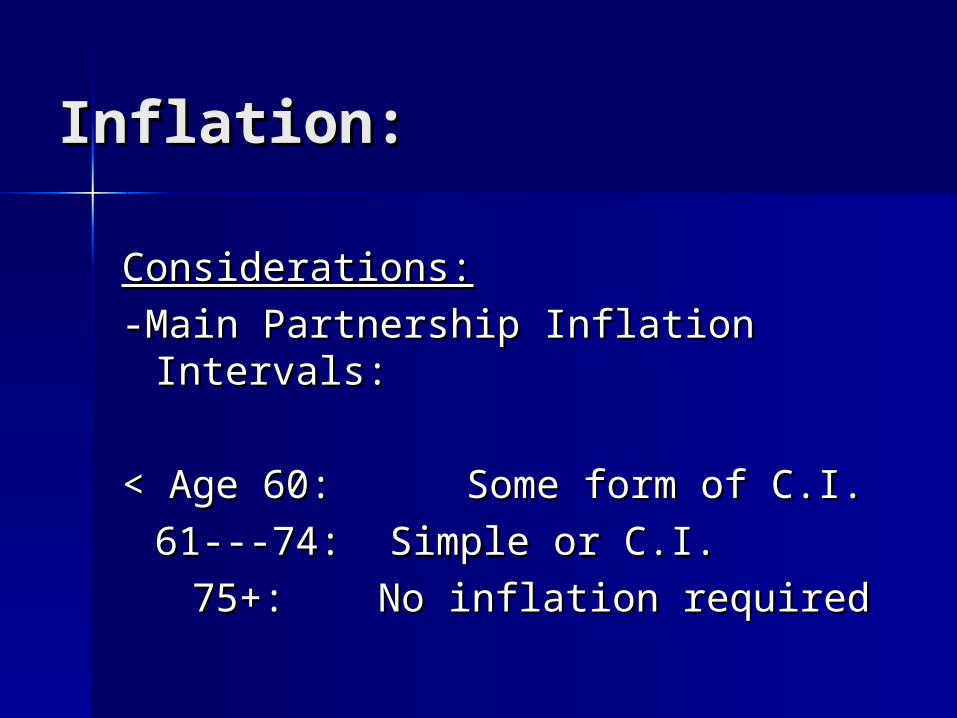

Inflation:Inflation:

Considerations:Considerations:

-Step 1 of the 3 step process-Step 1 of the 3 step process

-Longevity in client/prospect family-Longevity in client/prospect family

-Partnership Considerations-Partnership Considerations

-Mastering the Partnership Inflation -Mastering the Partnership Inflation intervalsintervals

Inflation:Inflation:

Considerations:Considerations:

-Main Partnership Inflation Intervals:-Main Partnership Inflation Intervals:

< Age 60:< Age 60: Some form of C.I. Some form of C.I.

61---74: Simple or C.I.61---74: Simple or C.I.

75+:75+: No inflation required No inflation required

Inflation:Inflation:

Considerations:Considerations:-Risk Tolerance-Risk Tolerance-How much cost sharing are they -How much cost sharing are they

contemplating?contemplating?-Compound, Simple, CPI, GPO/FPO -Compound, Simple, CPI, GPO/FPO

main considerationsmain considerations-Can vary by state -Can vary by state

Planning Metric Number Planning Metric Number IV:IV:

Claims Payment Options:Claims Payment Options:

Claims Payment OptionsClaims Payment Options

ReimbursementReimbursement– DailyDaily– MonthlyMonthly

IndemnityIndemnity CashCash

Claims Payment OptionsClaims Payment Options

Assume: $100 per day contract Assume: $100 per day contract purchased.purchased.

Assume $25 of expenses incurred on Assume $25 of expenses incurred on that daythat day

Claims Payment OptionsClaims Payment Options

Reimbursement:Reimbursement:– Contract language says you will be reimbursed up to $100 Contract language says you will be reimbursed up to $100

per day. If you don’t spend it you don’t get it for that day.per day. If you don’t spend it you don’t get it for that day.– You will be reimbursed $25 for that dayYou will be reimbursed $25 for that day– Have to get care on a day by licensed agency to be paidHave to get care on a day by licensed agency to be paid– Most cost effective of all of the claims payment options Most cost effective of all of the claims payment options

alternativesalternatives– Geo StormGeo Storm

Claims Payment OptionsClaims Payment Options

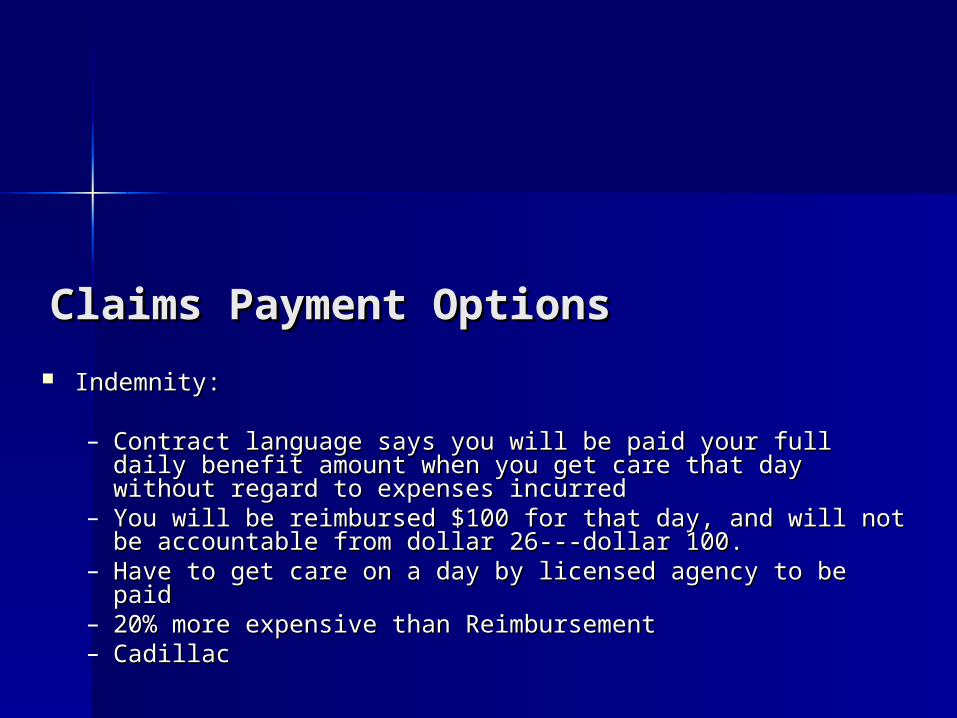

Indemnity:Indemnity:

– Contract language says you will be paid your full daily Contract language says you will be paid your full daily benefit amount when you get care that day without regard benefit amount when you get care that day without regard to expenses incurredto expenses incurred

– You will be reimbursed $100 for that day, and will not be You will be reimbursed $100 for that day, and will not be accountable from dollar 26---dollar 100.accountable from dollar 26---dollar 100.

– Have to get care on a day by licensed agency to be paidHave to get care on a day by licensed agency to be paid– 20% more expensive than Reimbursement20% more expensive than Reimbursement– CadillacCadillac

Claims Payment OptionsClaims Payment Options

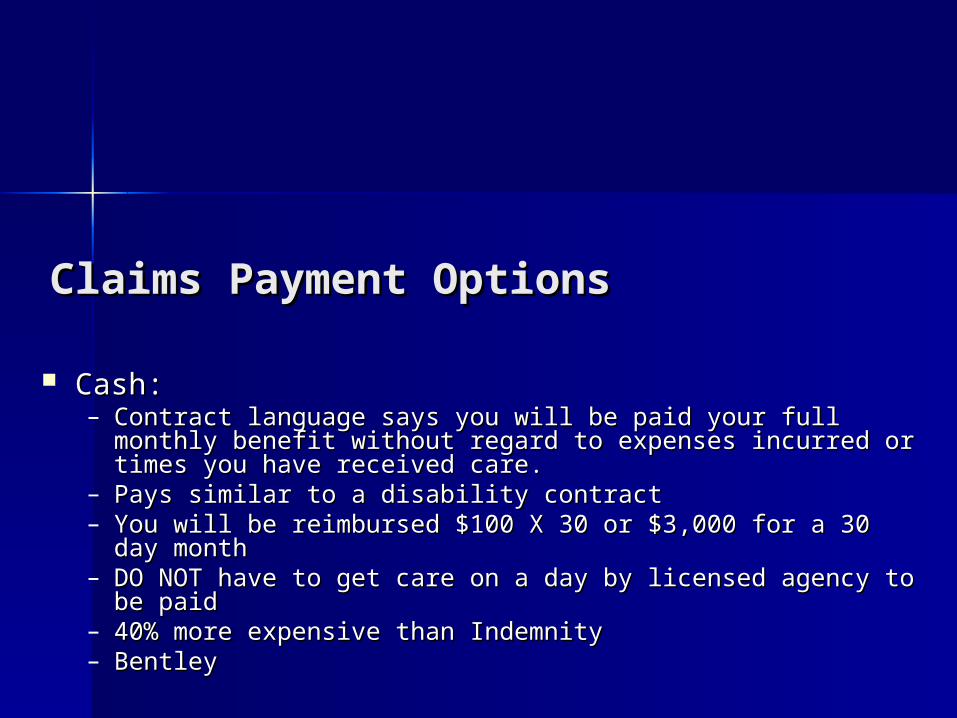

Cash:Cash:– Contract language says you will be paid your full monthly Contract language says you will be paid your full monthly

benefit without regard to expenses incurred or times you benefit without regard to expenses incurred or times you have received care.have received care.

– Pays similar to a disability contractPays similar to a disability contract– You will be reimbursed $100 X 30 or $3,000 for a 30 day You will be reimbursed $100 X 30 or $3,000 for a 30 day

monthmonth– DO NOT have to get care on a day by licensed agency to be DO NOT have to get care on a day by licensed agency to be

paidpaid– 40% more expensive than Indemnity40% more expensive than Indemnity– BentleyBentley

Claims Payment OptionsClaims Payment Options

Taxation of Benefits:Taxation of Benefits:– One Page CLTC Tax GuideOne Page CLTC Tax Guide– Reimbursement benefits are not included in incomeReimbursement benefits are not included in income– Indemnity benefits are not included in income, Indemnity benefits are not included in income,

except those amounts which exceed the greater of:except those amounts which exceed the greater of: Total Qualified LTC expenses ORTotal Qualified LTC expenses OR $290 per day (in 2010)$290 per day (in 2010)

Planning Metric Number Planning Metric Number V:V:

Home Care Percentage Election:Home Care Percentage Election:

Home Care Percentage Election Home Care Percentage Election Considerations:Considerations:

-Available Family Infrastructure-Available Family Infrastructure-Part B of CLTC V8-Part B of CLTC V8-Who could potentially quarterback -Who could potentially quarterback

care?care?-if there is no infrastructure, then -if there is no infrastructure, then

what?what?

Home Care Percentage Election Home Care Percentage Election Considerations:Considerations:

-Percentage to elect?-Percentage to elect?

-Risk Tolerance-Risk Tolerance

-Geography-Geography

-State filing issues-State filing issues

Comprehensive or Facility OnlyComprehensive or Facility Only

Two components to these Two components to these contracts:contracts:– Facility Component:Facility Component:

Nursing HomeNursing Home Assisted LivingAssisted Living

Comprehensive or Facility OnlyComprehensive or Facility Only

Two components to these contracts:Two components to these contracts:– Home (HCBS) Component:Home (HCBS) Component:

Home Care Home Care Adult Day CareAdult Day Care Community Based ServicesCommunity Based Services

– Meals on WheelsMeals on Wheels

Comprehensive or Facility OnlyComprehensive or Facility Only

You must elect a % on the Home Care You must elect a % on the Home Care (HCBS) Component of the contract(HCBS) Component of the contract

The main choices are 100%, 75% or The main choices are 100%, 75% or 50%50%

Comprehensive or Facility OnlyComprehensive or Facility Only

Assume $100 dollar a day contract is purchasedAssume $100 dollar a day contract is purchased On the HCBS (Home Care) component, if you elect a On the HCBS (Home Care) component, if you elect a

percentage of anything other than 100%, you take percentage of anything other than 100%, you take that percentage and multiply it by the Daily Benefit that percentage and multiply it by the Daily Benefit Amount and that is the dollar amount that you have Amount and that is the dollar amount that you have available to you for the Home (HCBS) componentavailable to you for the Home (HCBS) component

For instance, if you chose 75% home care in this For instance, if you chose 75% home care in this example, you would have $75 to use in the example, you would have $75 to use in the components that make up the HCBS part of the components that make up the HCBS part of the contract. (NOT $100)contract. (NOT $100)

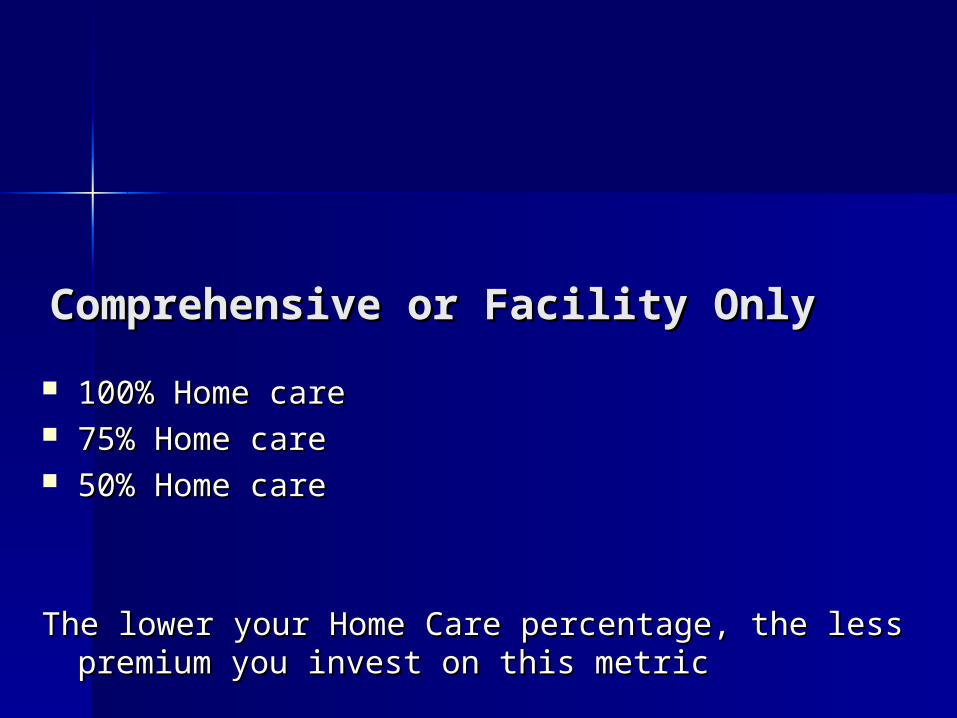

Comprehensive or Facility OnlyComprehensive or Facility Only

100% Home care 100% Home care 75% Home care75% Home care 50% Home care50% Home care

The lower your Home Care percentage, the less The lower your Home Care percentage, the less premium you invest on this metricpremium you invest on this metric

Planning Metric Number Planning Metric Number VI:VI:

Elimination Period:Elimination Period:

Elimination Period:Elimination Period:

Considerations:Considerations:

-Risk Tolerance-Risk Tolerance

-Cash flow-Cash flow

-Co-insuring considerations-Co-insuring considerations

-Cost of care progression-Cost of care progression

-Inflation choices-Inflation choices

Elimination Period:Elimination Period:

Considerations:Considerations:

-What we know about the age of -What we know about the age of our populationour population

The Elimination PeriodThe Elimination Period

(E.P.)(E.P.) This is your deductible, expressed in the number of days that This is your deductible, expressed in the number of days that

you pay for your care for yourself out of your pocketyou pay for your care for yourself out of your pocket In Georgia, the longest your E.P. can be is 60 daysIn Georgia, the longest your E.P. can be is 60 days Choices range from zero to 60 days generallyChoices range from zero to 60 days generally State Filing issueState Filing issue The closer to zero your elimination period is, the more The closer to zero your elimination period is, the more

premium you investpremium you invest

Elimination Period:Elimination Period:

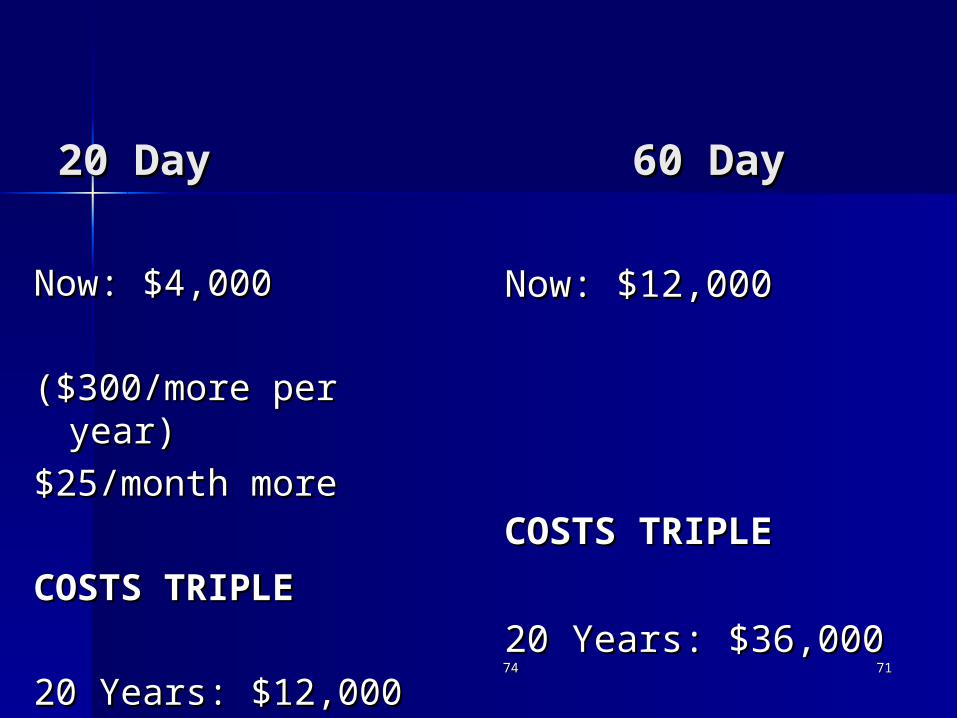

An Exercise:An Exercise:

-Assume: -Assume:

-$200/Day is the cost of care-$200/Day is the cost of care

-Cost of care projected to triple in 20 -Cost of care projected to triple in 20 yearsyears

-Difference between 20 and 60 day E.P. -Difference between 20 and 60 day E.P. is $25/Monthis $25/Month

-What that means….-What that means….

7474 7171

20 Day20 Day 60 Day60 Day

Now: $4,000Now: $4,000

($300/more per year)($300/more per year)

$25/month more$25/month more

COSTS TRIPLECOSTS TRIPLE

20 Years: $12,00020 Years: $12,000

Now: $12,000Now: $12,000

COSTS TRIPLECOSTS TRIPLE

20 Years: $36,00020 Years: $36,000

Elimination Period:Elimination Period:

An Exercise:An Exercise:

-Would you pay $6,000 to -Would you pay $6,000 to potentially get $24,000?potentially get $24,000?

Elimination Period:Elimination Period:

Considerations:Considerations:

-What will the client remember about -What will the client remember about what you told them?what you told them?

-Warning about Medicare Part A and -Warning about Medicare Part A and what it does pay for?what it does pay for?

-Very cost effective to consider shorter -Very cost effective to consider shorter for the value it could potentially for the value it could potentially deliverdeliver

Case Design and Setup Case Design and Setup considerations:considerations:

Traditional Health LTCTraditional Health LTCAsset BasedAsset BasedTimelineTimelineUnderwritingUnderwritingCarrier ConsiderationsCarrier ConsiderationsMarket ExplorationMarket ExplorationInstrument AccessInstrument Access

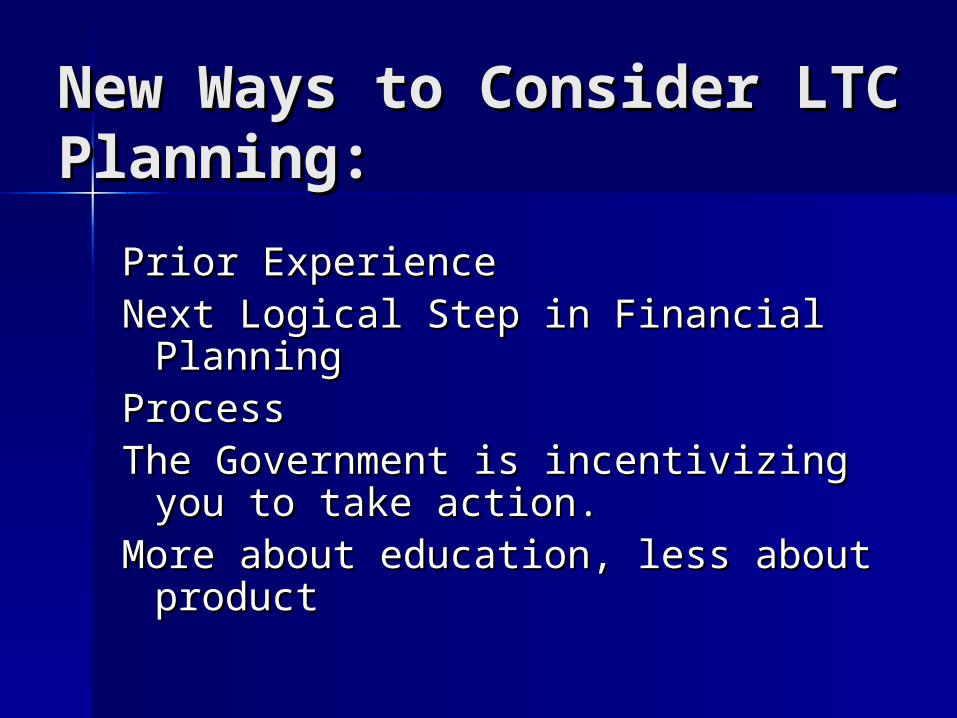

New Ways to Consider New Ways to Consider LTC Planning:LTC Planning:

Prior ExperiencePrior ExperienceNext Logical Step in Financial Next Logical Step in Financial

PlanningPlanningProcessProcessThe Government is incentivizing The Government is incentivizing

you to take action.you to take action.More about education, less about More about education, less about

productproduct

New Ways to Consider New Ways to Consider LTC Planning:LTC Planning:

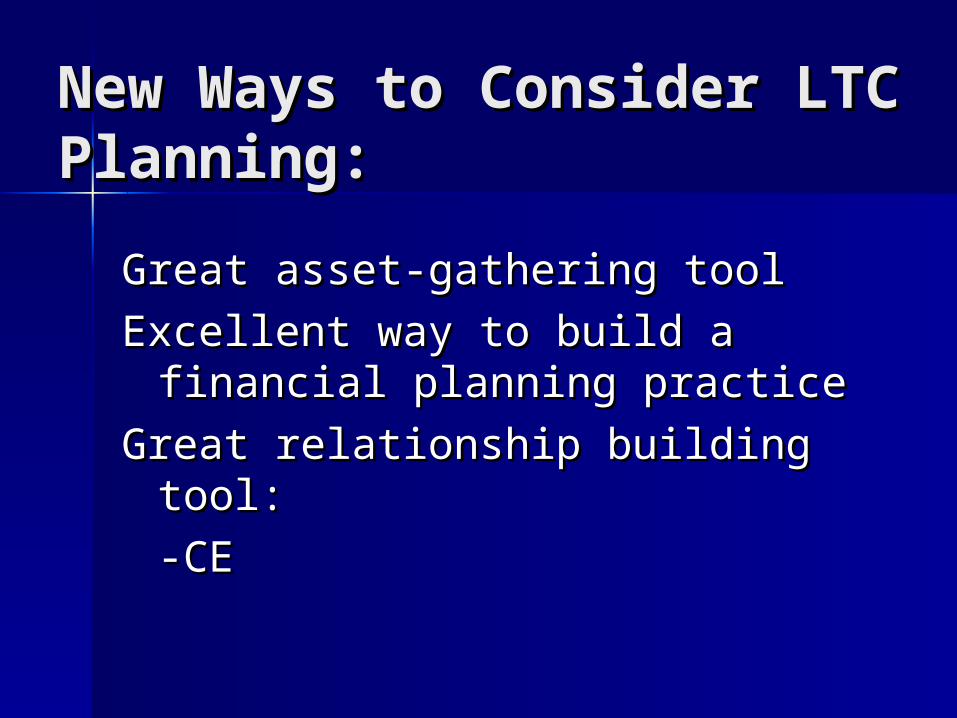

Great asset-gathering toolGreat asset-gathering tool

Excellent way to build a financial Excellent way to build a financial planning practiceplanning practice

Great relationship building tool:Great relationship building tool:

-CE-CE

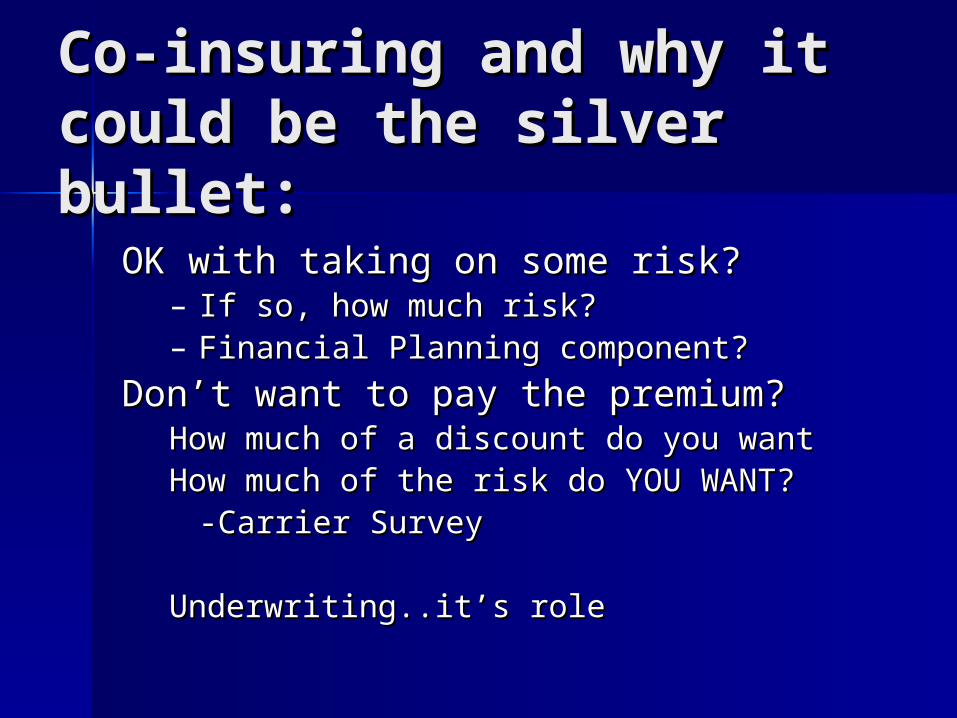

Co-insuring and why it Co-insuring and why it could be the silver could be the silver bullet:bullet:

OK with taking on some risk?OK with taking on some risk?– If so, how much risk?If so, how much risk?– Financial Planning component?Financial Planning component?

Don’t want to pay the premium?Don’t want to pay the premium?How much of a discount do you wantHow much of a discount do you wantHow much of the risk do YOU WANT?How much of the risk do YOU WANT?

-Carrier Survey-Carrier Survey

Underwriting..it’s roleUnderwriting..it’s role

Co-insuring and why it Co-insuring and why it could be the silver could be the silver bullet:bullet:

Wealthy PeopleWealthy People

StrategyStrategy

Why multiple steps in the planning Why multiple steps in the planning process can serve you wellprocess can serve you well

Questions/Follow-up:Questions/Follow-up:

Questions?Questions? How can I help you further?How can I help you further? Corey Rieck:Corey Rieck:

– Phone: (678) 990-3664Phone: (678) 990-3664– Email: Email: [email protected]

Do you need more?Do you need more?

Please feel free to contact Corey Please feel free to contact Corey at:at:

– [email protected]@ltccompass.com