the marketpulse volume 6, issue 3 · 2017 oreli i i ti eproduc i i xpres i ii 1 the marketpulse g...

TRANSCRIPT

© 2017 CoreLogic — Proprietary. This material may not be reproduced in any form without express written permission.i

| The MarketPulse g March 2017 g Volume 6, Issue 3

The MarketPulse

MARCH 2017

© 2017 CoreLogic — Proprietary. This material may not be reproduced in any form without express written permission.ii

Table of Contents | The MarketPulse March 2017 Volume 6, Issue 3

Table of Contents

Single-family Rent Growth Faster in Markets with Low Vacancies ...........1

One-percentage point lower vacancy rate leads to 0.5% faster rent growth

Condo Lending Outlook ............................................................................................... 2

The State of House Flipping in 2016 – Part I ....................................................... 3

At the National Level, Flipping Activity is the Second Lowest Since 2012

The State of House Flipping in 2016 – Part II .....................................................4

Texas and Florida Flipping Activities Were Strong in 2016

Charts & Graphs ......................................................................................................................................................7

Home Price Index ...................................................................................................................................................7

Home Price Index State-Level Detail — Combined Single Family Including Distressed January 2017 ................................................................................................................7

In the News ...............................................................................................................................................................7

Peak Foreclosure Inventory for 10 Largest CBSAs From Their Peak to December 2016 ............................................................................................................ 8

Annual National Completed Foreclosures 2000–2016 ....................................................................... 8

Foreclosure Rates for the Ten States with the Highest Peak Foreclosure Rate ..................... 8

CoreLogic HPI® Market Condition Overview............................................................................................ 9January 2017January 2022 Forecast

Variable Descriptions .........................................................................................................................................10

Housing Statistics

January 2017

HPI® YOY Chg 6.9%

HPI YOY Chg XD 5.8%

NegEq Share (Q4 2016) 6.2%

Cash Sales Share

(as of December 2016)

33.1%

Distressed Sales

(as of December 2016)

7.8%

The MarketPulseVolume 6, Issue 3March 2017Data as of January 2017

News Media Contact

Alyson [email protected]

949.214.1414 (offi ce)

© 2017 CoreLogic — Proprietary. This material may not be reproduced in any form without express written permission. 1

The MarketPulse g March 2017 g Volume 6 Issue 3 | Articles

Single-family Rent Growth Faster in Markets with Low VacanciesOne-percentage point lower vacancy rate leads to 0.5% faster rent growth

By Frank E. Nothaft

Rent growth varies across neighborhoods

and over time. For this reason, rent-growth

expectations are important not just for

families who are deciding whether to rent

or own their home, but also for investors

who are trying to forecast net revenue on

their housing investment.

Looking at the types of properties that

renters live in, about 38 percent are

1-family homes. Another 7 percent are

rental condominiums, typically a unit in a

multifamily structure (Figure 1). And if we

include small multi-unit buildings, then 1- to

4-family houses and rental condominiums

account for more than one-half of our

nation’s rental stock.

The importance of single-family rental

homes and condominiums underscores the

need to understand how rents on these

properties vary with market conditions.

Using CoreLogic’s Single-family Rental

Index, we examined rent growth across

28 metropolitan areas over the last year

and compared these with the rental

vacancy rates in these markets.1 We found

that our rent index grew faster in markets

with low vacancy rates: On average,

for each 1-percentage point decline in

the local vacancy rate, rent growth was

about one-half percentage point faster

during 2016 (Figure 2).

This rent-vacancy relationship is important

for property owners and managers. Not

surprisingly, the type of investors who

own single-family properties are very

different from those that own high rises.2

For example, more than 80 percent of 2- to

4-family rental properties are owned by

individuals, but less than 10 percent of rental

properties with 50-or-more apartments are

owned by individual investors (Figure 3).

We would expect that those metros that

have relatively low vacancy rates in early

2017 will also be the markets with more

rapid rent growth during the coming year.

CoreLogic’s Single-family Rental Index found

1 Information on the Single-family Rental Index can be found here

and here.2 For owners of small rental properties, one tenant’s payment

ability can have a large impact on the property’s rental income.

Tenant screening tools, such as MyRental™ from CoreLogic

(https://www.myrental.com), can help property owners and

managers identify top-quality applicants.

FIGURE 1. COMPONENTS OF THE U.S. RENTAL STOCKOccupied Rental Stock (44 Million Homes)

nothaft: fig 1

Multifamily 35%(5 or more units)

2- to 4-family 16%

Manufactured Housing 4%

Condo/Co-op 7%

One-family 38%

Source: U.S. Census Bureau, 2015 American Housing Survey (1-family includes both detached and attached housing)

FIGURE 2. RENT GROWTH FASTER IN LOW-VACANCY MARKETSRent Growth (percent, 2015Q4 to 2016Q4)

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

2% 3% 4% 5% 6% 7% 8% 9% 10% 11%

Rental Vacancy Rate (percent, 2016 average)

nothaft: fig 2

LinearTrend

Source: CoreLogic Single-family Rental Index, U.S. Census Housing Vacancy Survey, 28 metropolitan areas; line represents a univariate regression

Continued on page 6

Dr. Frank Nothaft

Chief Economist

Frank Nothaft is senior vice president and chief economist for CoreLogic. He leads the Office of the Chief Economist and is responsible for analysis, commentary and forecasting trends in global real estate, insurance and mortgage markets.

© 2017 CoreLogic — Proprietary. This material may not be reproduced in any form without express written permission.2

Articles | The MarketPulse March 2017 Volume 6, Issue 3

FIGURE 1. CONDO 1ST LIEN MORTGAGE ORIGINATIONSBillions

$-

$20

$40

$60

$80

$100

$120

$140

$160

Jan

-05

Sep

-05

May

-06

Jan

-07

Sep

-07

May

-08

Jan

-09

Sep

-09

May

-10

Jan

-11

Sep

-11

May

-12

Jan

-13

Sep

-13

May

-14

Jan

-15

Sep

-15

May

-16

+14%

Source: CoreLogic

FIGURE 2. DAYS ON MARKET

0

20

40

60

80

100

120

140

160

180

Jan-00 Sep-01 May-03 Jan-05 Sep-06 May-08 Jan-10 Sep-11 May-13 Jan-15 Sep-16

Source: CoreLogic

Condo Lending Outlook

By Jacqueline Doty

CoreLogic has taken a look at the state

of condominium lending. Where things

stand now… what’s changing and what’s

not…or at least not changing fast enough

for some participants.

Through November of 2016, lending for

condo purchases was running at an annual

rate of $74 billion, or 8 percent of total

purchase originations. Meanwhile, lending

for condo refi nances was running at

approximately the same rate, which means

that in 2016, when all the numbers are

tallied, condo lending will represent around

7 percent of total mortgage originations.

Overall, condo sales were relatively fl at

through the fi rst half of 2016, coming in at

just under 600,000 condos.

The average sale price was $300,000 in

the fi rst half of 2016, up 3 percent when

compared to the prior year. Days on market

was a very fast 78 days (down from 85 days

a year earlier) thanks to a tight supply of

condos on the market, which was running

at about 4.3 months as of December.

For some time now, CoreLogic has been

forecasting that condos will be a bigger part

of the mortgage origination market. Our

outlook is based on the strong demographic

tailwind of fi rst time millennial homebuyers

and down-sizing baby boomers—two large

cohorts that will be gravitating toward the

condo market. The timing of this potential

condo-buying wave has been harder to

predict. But improving employment growth

and continued relatively low interest rates

should begin to change this picture.

As followers of the Insights blog know, there

are some headwinds to condo lending:

mainly the need for lenders to underwrite

the condo project as well as the borrower.

This requires lenders to understand diff ering

investor eligibility requirements and to

deal with the more than 140,000 condo

associations in the US. All of which can add

time, cost and risk to condo lending.

Lenders, condo owners and borrowers all got

some good news last year when Congress

acted to ease rules that have made FHA

condo loans more diffi cult to get. Specifi cally

the new rules lowered the owner-occupancy

threshold from 50 percent to 35 and made

other changes to bring FHA policies in line

with the less-restrictive approach used by

Fannie Mae and Freddie Mac.

Although condos remain a relatively small

slice of the overall single-family market, this

category plays an oversized role when it

come to aff ordable options for fi rst time

buyers, low-to-medium income borrowers

and graying baby-boomers. ■

Jacqueline Doty

VP, Product Management,

Collateral Risk Solutions

Jacqueline Doty is vice president and product line manager at CoreLogic. She is responsible for strategic planning, research and development of innovative products and solutions to collateral risk management problems. She also oversees the CondoSafe and LoanSafe Appraisal Manager off erings, ensuring these CoreLogic solutions provide an accurate, timely and cost-eff ective method of underwriting collateral. Jacqueline earned a bachelor’s degree in economics from the University of Maryland, College Park, and is a graduate of the Mortgage Bankers Association School of Mortgage Banking.

© 2017 CoreLogic — Proprietary. This material may not be reproduced in any form without express written permission. 3

The MarketPulse g March 2017 g Volume 6 Issue 3 | Articles

Continued on page 6

The State of House Flipping in 2016 – Part IAt the National Level, Flipping Activity is the Second Lowest Since 2012

By Bin He

Flipping is the term used when an investor

purchases a property, renovates and repairs

it, and then re-sells it within a short period of

time for a profit. In a blog series I published

a while back, Is Flipping Coming Back?

Part I and Part II, I concluded that in Q1 2016

flipping activity was well below its historical

high at the national level although there

were geographic variations at the metro

level. Now that 2016 is behind us, it’s time

to revisit this topic to see how things have

changed. A little different from the analysis I

did before, a flipped property is now defined

as a property that is bought and sold within

12 months rather than nine months since we

have observed it takes a longer time to flip a

property. Furthermore, non-disclosure states

are now included in the analysis. We aren’t

able to know its price-related metrics but

it is feasible to derive the share of flipped

properties to sales. In Part I of this series we

will focus on the national-level analysis, and

in Part II we will zoom in on metro areas.

At the national level, the ratio of flips to sales

stands at 4.9 percent in 2016, which is well

below the peak value of 7.5 percent reached

in 2005, as shown in Figure 1. As a matter of

fact, this is the second lowest rate of flipping

activity since 2012, as the lowest since 2012

occurred in 2015 with a flipping percentage

of 4.8. It appears that flipping activity has

slowed in the past two years since the start

of the housing recovery, thanks to a five-year

Bin He

Principal Economist

Bin He is a principal economist with the CoreLogic Decision Analytics & Research Team (DART). Bin leads research and development of the CoreLogic Home Price Index and the CoreLogic Real Estate Analytics Suite. Bin is also responsible for the modeling that powers the CoreLogic RiskModel. Before Bin joined CoreLogic, he was director of Credit Analytics for Radian Guaranty, where he was responsible for the development and implementation of mortgage prepayment and default models.

FIGURE 1. THE RATIO OF FLIPS TO SALES OVER TIME AT NATIONAL LEVEL

0%

1%

2%

3%

4%

5%

6%

7%

8%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

He 1: fig 1

Source: CoreLogic Public Records

FIGURE 2. REAL MEDIAN GROSS PROFIT (IN 2016 DOLLARS) PER PROPERTY FLIPPED AND MEDIAN PERCENTAGE GROSS PROFIT ACROSS THE COUNTRY

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

real median gross profit median %gross profit

He 1: fig 2

Source: CoreLogic Public Records

© 2017 CoreLogic — Proprietary. This material may not be reproduced in any form without express written permission.4

Articles | The MarketPulse g March 2017 g Volume 6, Issue 3

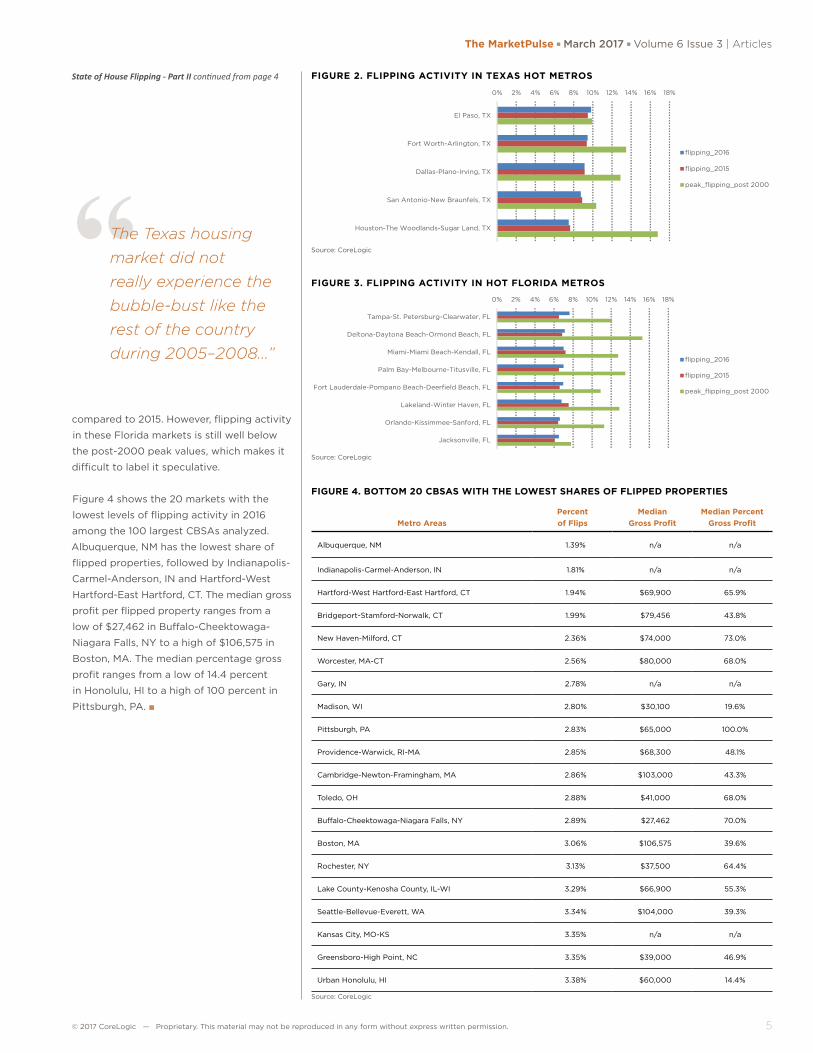

The State of House Flipping in 2016 – Part IITexas and Florida Flipping Activities Were Strong in 2016

By Bin He

In Part I of this blog we discussed flipping

activity in 2016—investors buying homes,

repairing and selling them within a short

period of time for a profit—at the national

level. Here we focus on flipping activity at

the local metro level for 2016. A flipped

property is defined as a property that is

bought and sold within twelve months.

Figure 1 lists the 20 markets, among the

100 largest Core Based Statistical Areas

(CBSAs) that CoreLogic analyzed, with

the highest shares of flipped properties in

2016. Since sale values are not available

for public access in non-disclosure states,

gross profit and percent gross profit are not

available for those CBSAs in these non-

disclosure states. According to CoreLogic

data and analysis, El Paso, TX has the

highest share of flipped properties, followed

by Fort Worth-Arlington, TX and Dallas,

TX. For these 20 CBSAs, the median gross

profit per flipped property ranges from

a low of $29,000 in Birmingham-Hoover,

AL to a high of $130,000 in Los Angeles-

Long Beach-Glendale, CA. The median

percentage gross profit ranges from a low

of 30.7 percent in Birmingham-Hoover, AL

to a high of 66.2 percent in Virginia Beach-

Norfolk-Newport News, VA-NC.

Flipping activity was strongest among Texas

and Florida CBSAs in 2016. Five of the top

10 markets for flipping are in Texas, and

eight of the top 20 markets for flipping

are in Florida. Figure 2 shows that in the

five hot Texas markets flipping activity in

2016 is comparable to activity seen in 2015.

Moreover, in three of those markets, El Paso,

Dallas and San Antonio, flipping activity

in 2016 is not too far from the post-2000

peak values. The Texas housing market did

not really experience the bubble-bust like

the rest of the country during 2005–2008,

and its home price appreciation has been

accelerating. It is worth keeping a close

eye on the Texas market. Figure 3 shows in

all eight hot Florida markets, six of them

had increases in flipping activity in 2016

FIGURE 1. TOP 20 CBSAS WITH THE HIGHEST SHARES OF FLIPPED PROPERTIES IN 2016

Metro AreasPercent of Flips

Median Gross Profit

Median Percent Gross Profit

El Paso, TX 9.82% n/a n/a

Fort Worth-Arlington, TX 9.46% n/a n/a

Dallas-Plano-Irving, TX 9.14% n/a n/a

San Antonio-New Braunfels, TX 8.75% n/a n/a

New Orleans-Metairie, LA 7.93% n/a n/a

Tampa-St. Petersburg-Clearwater, FL 7.64% $55,000 56.4%

Houston-The Woodlands-Sugar Land, TX 7.49% n/a n/a

Virginia Beach-Norfolk-Newport News, VA-NC 7.20% $79,000 66.2%

Deltona-Daytona Beach-Ormond Beach, FL 7.13% $48,000 49.3%

Miami-Miami Beach-Kendall, FL 7.01% $68,000 41.9%

Palm Bay-Melbourne-Titusville, FL 7.01% $56,600 59.3%

Fort Lauderdale-Pompano Beach-Deerfield Beach, FL 6.96% $59,000 42.7%

Fresno, CA 6.95% $62,000 49.0%

Lakeland-Winter Haven, FL 6.80% $49,825 56.5%

Orlando-Kissimmee-Sanford, FL 6.61% $45,000 41.5%

Los Angeles-Long Beach-Glendale, CA 6.52% $130,000 36.2%

Jacksonville, FL 6.51% $54,318 54.2%

Memphis, TN-MS-AR 6.50% $39,900 60.0%

Birmingham-Hoover, AL 6.42% $29,000 30.7%

Phoenix-Mesa-Scottsdale, AZ 6.36% $47,300 32.1%

Source: CoreLogic

Continued on page 5

“According to CoreLogic data and analysis, El Paso, TX has the highest share of flipped properties…”

© 2017 CoreLogic — Proprietary. This material may not be reproduced in any form without express written permission. 5

The MarketPulse g March 2017 g Volume 6 Issue 3 | Articles

FIGURE 4. BOTTOM 20 CBSAS WITH THE LOWEST SHARES OF FLIPPED PROPERTIES

Metro AreasPercent of Flips

Median Gross Profit

Median Percent Gross Profit

Albuquerque, NM 1.39% n/a n/a

Indianapolis-Carmel-Anderson, IN 1.81% n/a n/a

Hartford-West Hartford-East Hartford, CT 1.94% $69,900 65.9%

Bridgeport-Stamford-Norwalk, CT 1.99% $79,456 43.8%

New Haven-Milford, CT 2.36% $74,000 73.0%

Worcester, MA-CT 2.56% $80,000 68.0%

Gary, IN 2.78% n/a n/a

Madison, WI 2.80% $30,100 19.6%

Pittsburgh, PA 2.83% $65,000 100.0%

Providence-Warwick, RI-MA 2.85% $68,300 48.1%

Cambridge-Newton-Framingham, MA 2.86% $103,000 43.3%

Toledo, OH 2.88% $41,000 68.0%

Buffalo-Cheektowaga-Niagara Falls, NY 2.89% $27,462 70.0%

Boston, MA 3.06% $106,575 39.6%

Rochester, NY 3.13% $37,500 64.4%

Lake County-Kenosha County, IL-WI 3.29% $66,900 55.3%

Seattle-Bellevue-Everett, WA 3.34% $104,000 39.3%

Kansas City, MO-KS 3.35% n/a n/a

Greensboro-High Point, NC 3.35% $39,000 46.9%

Urban Honolulu, HI 3.38% $60,000 14.4%

Source: CoreLogic

State of House Flipping - Part II continued from page 4

compared to 2015. However, flipping activity

in these Florida markets is still well below

the post-2000 peak values, which makes it

difficult to label it speculative.

Figure 4 shows the 20 markets with the

lowest levels of flipping activity in 2016

among the 100 largest CBSAs analyzed.

Albuquerque, NM has the lowest share of

flipped properties, followed by Indianapolis-

Carmel-Anderson, IN and Hartford-West

Hartford-East Hartford, CT. The median gross

profit per flipped property ranges from a

low of $27,462 in Buffalo-Cheektowaga-

Niagara Falls, NY to a high of $106,575 in

Boston, MA. The median percentage gross

profit ranges from a low of 14.4 percent

in Honolulu, HI to a high of 100 percent in

Pittsburgh, PA. ■

FIGURE 2. FLIPPING ACTIVITY IN TEXAS HOT METROS

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

El Paso, TX

Fort Worth-Arlington, TX

Dallas-Plano-Irving, TX

San Antonio-New Braunfels, TX

Houston-The Woodlands-Sugar Land, TX

flipping_2016

flipping_2015

peak_flipping_post 2000

He 2: fig 2

Source: CoreLogic

FIGURE 3. FLIPPING ACTIVITY IN HOT FLORIDA METROS

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Tampa-St. Petersburg-Clearwater, FL

Deltona-Daytona Beach-Ormond Beach, FL

Miami-Miami Beach-Kendall, FL

Palm Bay-Melbourne-Titusville, FL

Fort Lauderdale-Pompano Beach-Deerfield Beach, FL

Lakeland-Winter Haven, FL

Orlando-Kissimmee-Sanford, FL

Jacksonville, FL

flipping_2016

flipping_2015

peak_flipping_post 2000

He 2: fig 3

Source: CoreLogic

“The Texas housing market did not really experience the bubble-bust like the rest of the country during 2005–2008…”

© 2017 CoreLogic — Proprietary. This material may not be reproduced in any form without express written permission.6

Articles | The MarketPulse g March 2017 g Volume 6, Issue 3

that rents were up 2.6 percent in December

2016 compared with one year earlier,

measured as an average across 40 metro

areas. Because rental vacancy rates remain

relatively low, we expect that rents will

continue to rise about 2½ to 3 percent in

2017, outpacing inflation, with faster growth

in tight, low-vacancy metros and slower

growth in high-vacancy markets. ■

Single-Family Rent Growth continued from page 1

State of House Flipping - Part I continued from page 3

FIGURE 3. RENTAL PROPERTY OWNERSHIP

87%

10%

1% 1% 1%

9%

77%

1% 12%

1%

Individual Investor

Partnerships andCorporations

Financial Institutions andPension Funds

Nonprofit & Housing Coops

Other

nothaft: fig 3

9%

77%

1% 12%

1%

2- to 4-Unit Properties

50 or More UnitProperties

Source: U.S. Department of Housing and Urban Development and U.S. Census Bureau, U.S. Rental Housing Finance Survey 2012, Table 2a, 2d (Estate Trustees included in Individual Investor category)

“At the national level, the ratio of flips to sales stands at 4.9 percent in 2016…”

“The importance of single-family rental homes and condominiums underscores the need to understand how rents on these properties vary with market conditions.”

high in the rate of home-price appreciation

and still-tight for-sale inventory.

In 2016, the real median gross gain (in

2016 dollars) rose to $54,700 per property

flipped, which is approaching the historical

high of $56,411 (in 2016 dollars) seen in

2005 prior to the housing crash, as Figure 2

shows1. On the other hand, the median

percentage gross gain has declined since

it peaked in 2013. We continue to believe

the decline of the percentage gain might

have something to do with the decline of

the share of distressed sales, which leads to

high acquisition cost. From this CoreLogic

Insights blog posted by Molly Boesel, Cash

and Distressed Sales Update: November

2016, we see that the share of distressed

sales has declined significantly and was just

7.7 percent in October 2016. From Figure 2

we can also see that the median percentage

gross profit was about 20 percent between

1996 and 2008 and then increased to

above 30–40 percent after 2008, which is

largely due to the high acquisition cost on

the investors’ part from 2000 to 2008, as

Figure 3 shows. ■

FIGURE 3. ACQUISITION COST ON THE INVESTORS’ PART IN 2016 DOLLARS

$0

$50,000

$100,000

$150,000

$200,000

$250,000

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

2010

2011

2012

20

13

20

14

20

15

2016

He 1: fig 3

Source: CoreLogic Public Records

1 Gross profits are in real terms of 2016 dollars so that we can

eliminate the impact of inflation over time. CPI is used to derive

the real dollar amount.

© 2017 CoreLogic — Proprietary. This material may not be reproduced in any form without express written permission. 7

The MarketPulse g March 2017 g Volume 6 Issue 3 | Analysis

Home Price Index State-Level Detail — Combined Single Family Including Distressed January 2017

StateMonth-Over-Month

Percent ChangeYear-Over-Year Percent Change

Forecasted Month-Over-Month

Percent Change

Forecasted Year-Over-Year Percent Change

Alabama −0.3% 3.8% 0.0% 3.6%Alaska 0.2% 1.6% 0.1% 5.9%

Arizona 1.0% 6.6% 0.2% 6.4%Arkansas 0.5% 4.6% 0.2% 4.0%California 0.2% 5.8% 0.3% 9.7%Colorado 0.6% 9.1% 0.2% 6.0%

Connecticut 0.2% 0.6% 0.3% 6.0%Delaware 0.5% 1.7% 0.2% 3.5%

District of Columbia 0.7% 5.3% 0.1% 3.3%Florida 0.6% 7.3% 0.2% 6.2%

Georgia 0.2% 6.4% 0.0% 3.4%Hawaii 0.6% 6.7% 0.3% 6.4%Idaho 0.1% 9.0% 0.1% 4.4%Illinois 0.0% 5.6% 0.2% 4.5%

Indiana −0.1% 5.3% 0.1% 4.4%Iowa −0.2% 3.3% 0.0% 3.5%

Kansas −1.0% 5.6% −0.1% 3.6%Kentucky −0.2% 5.6% 0.1% 3.7%Louisiana −0.2% 3.4% −0.1% 2.0%

Maine −2.8% −1.8% −0.3% 3.5%Maryland 0.7% 4.3% 0.2% 4.1%

Massachusetts 0.5% 6.1% 0.2% 5.7%Michigan −0.3% 6.4% 0.0% 5.3%

Minnesota −0.6% 5.4% 0.0% 3.3%Mississippi −0.1% 1.5% 0.0% 2.4%

Missouri −0.1% 4.6% 0.1% 4.1%Montana −1.6% 3.1% −0.2% 4.5%

Nebraska −0.2% 4.6% 0.0% 3.6%Nevada −0.2% 5.3% 0.3% 8.1%

New Hampshire 1.0% 6.0% 0.4% 5.9%New Jersey 0.1% 2.5% 0.2% 4.7%New Mexico 0.6% 5.5% 0.0% 3.8%

New York 2.8% 7.1% 0.4% 4.5%North Carolina 0.3% 5.2% 0.1% 3.6%North Dakota 0.3% 1.0% −0.2% 1.1%

Ohio 0.0% 5.4% 0.1% 4.2%Oklahoma −0.3% 1.6% 0.0% 2.7%

Oregon 0.2% 10.3% 0.3% 5.9%Pennsylvania −0.2% 2.9% 0.1% 3.9%Rhode Island −0.2% 5.6% 0.0% 3.4%

South Carolina 0.6% 6.4% 0.2% 3.6%South Dakota −0.1% 9.1% −0.1% 2.9%

Tennessee 0.2% 7.4% 0.1% 2.8%Texas 0.7% 6.8% 0.1% 2.3%Utah 0.5% 8.0% 0.1% 4.6%

Vermont 1.0% 6.1% 0.1% 3.5%Virginia 0.0% 3.1% 0.1% 3.8%

Washington 0.7% 10.8% 0.2% 5.3%West Virginia −0.7% 1.7% 0.0% 3.9%

Wisconsin 0.1% 5.4% 0.0% 3.9%Wyoming 0.2% 1.1% −0.3% 2.5%

Source: CoreLogic January 2017

In the News

HousingWire, March 21, 2017

CoreLogic: Influx of refis pushes risk

index lower in Q4

Mortgage originations grew safer in the fourth

quarter of 2016, according to CoreLogic, a

global property information, analytics and data-

enabled solutions provider.

Los Angeles Times, March 21, 2017

Southern California home prices jump

again as short supply fuels bidding wars

Low inventory — as well as one fewer day to record

sales last month than in February 2016, which included

a leap day — probably had a role in the 1.7% decline in

sales from a year earlier, CoreLogic said.

Yahoo! Finance, March 21, 2017

The Strongest Housing Market in the US

in 2017 – and the Weakest

Housing values increased 6.9 percent in January

compared with the same month a year ago,

according to the latest figures from CoreLogic.

Home prices also rose month over month by 0.7

percent, the company found.

CNBC, March 21, 2017

Mortgage applications fall 2.7%, as

borrowers turn to riskier loans

Mortgage lending is still conservative. In fact, the

average credit score for borrowers in the third quarter

of last year rose from the previous quarter, according to

CoreLogic, whose quarterly credit-risk index has been

falling steadily. That could change as mortgage rates

rise further, which is expected.

HOME PRICE INDEXPercentage Change Year Over Year

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jan-02 Jul-04 Jan-07 Jul-09 Jan-12 Jul-14 Jan-17

1.77x4.93hpi as of jan 2017

Including Distressed

Source: CoreLogic January 2017

Charts & Graphs

© 2017 CoreLogic — Proprietary. This material may not be reproduced in any form without express written permission.8

Analysis | The MarketPulse g March 2017 g Volume 6, Issue 3

PEAK FORECLOSURE INVENTORY FOR 10 LARGEST CBSAS FROM THEIR PEAK TO DECEMBER 2016

Source: CoreLogic March 2017

2.67x5.01foreclosure jan 2017: peak foreclosure inventory for 10 largest

cbsas from their peak to dec 2016

0% 5% 10% 15% 20% 25%

Miami

Las Vegas

Chicago

New York

Los Angeles

Washington DC

Boston

Denver

Houston

San FranciscoPeak Foreclosure %

December 2016 Foreclosure %

ANNUAL NATIONAL COMPLETED FORECLOSURES 2000–2016Thousands

Source: CoreLogic March 2017

2.62x5.04foreclosure jan 2017: Annual National Completed

Foreclosures 2000‐2016

Number of Completed Foreclosures -

200

400

600

800

1,000

1,200

1,400

2000 2002 2004 2006 2008 2010 2012 2014 2016

FORECLOSURE RATES FOR THE TEN STATES WITH THE HIGHEST PEAK FORECLOSURE RATE

Source: CoreLogic March 2017

2.67x4.59foreclosure jan 2017: Foreclosure Rates for the Ten States with

the Highest Peak Foreclosure Rate

Peak Foreclosure %

December 2016 Foreclosure %

12.51%

8.49%

7.42%

5.61%

5.31%

4.62%

4.42%

4.39%

4.36%

4.36%

1.46%

1.05%

2.88%

1.08%

2.81%

1.42%

1.78%

1.06%

1.71%

0.29%

0% 2% 4% 6% 8% 10% 12% 14%

FL

NV

NJ

IL

NY

CT

ME

MD

HI

AZ

© 2017 CoreLogic — Proprietary. This material may not be reproduced in any form without express written permission. 9

The MarketPulse g March 2017 g Volume 6 Issue 3 | Analysis

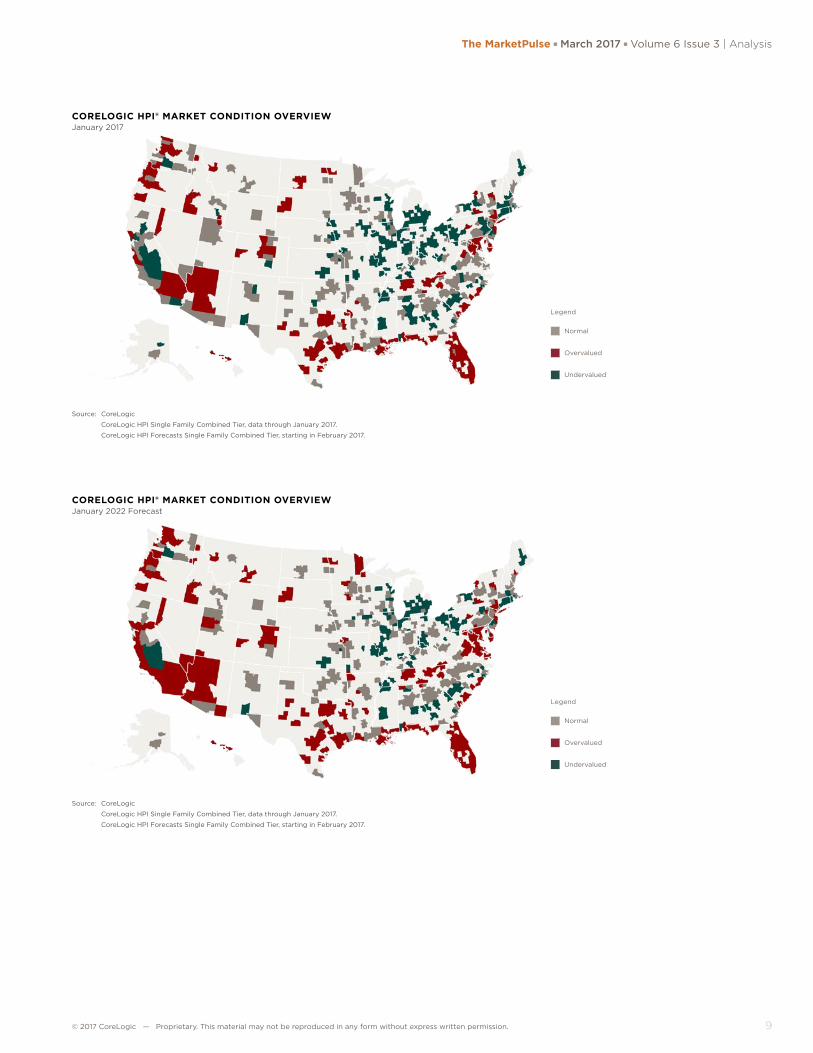

CORELOGIC HPI® MARKET CONDITION OVERVIEWJanuary 2017

Source: CoreLogic

CoreLogic HPI Single Family Combined Tier, data through January 2017.

CoreLogic HPI Forecasts Single Family Combined Tier, starting in February 2017.

Legend

Normal

Overvalued

Undervalued

CORELOGIC HPI® MARKET CONDITION OVERVIEWJanuary 2022 Forecast

Source: CoreLogic

CoreLogic HPI Single Family Combined Tier, data through January 2017.

CoreLogic HPI Forecasts Single Family Combined Tier, starting in February 2017.

Legend

Normal

Overvalued

Undervalued

© 2017 CoreLogic — Proprietary. This material may not be reproduced in any form without express written permission.10

Analysis | The MarketPulse g March 2017 g Volume 6, Issue 3

Variable Descriptions

Variable Definition

Total Sales The total number of all home-sale transactions during the month.

Total Sales 12-Month sum The total number of all home-sale transactions for the last 12 months.

Total Sales YoY Change 12-Month sum

Percentage increase or decrease in current 12 months of total sales over the prior 12 months of total sales

New Home Sales The total number of newly constructed residentail housing units sold during the month.

New Home Sales Median Price

The median price for newly constructed residential housing units during the month.

Existing Home Sales The number of previously constucted homes that were sold to an unaffiliated third party. DOES NOT INCLUDE REO AND SHORT SALES.

REO Sales Number of bank owned properties that were sold to an unaffiliated third party.

REO Sales Share The number of REO Sales in a given month divided by total sales.

REO Price Discount The average price of a REO divided by the average price of an existing-home sale.

REO Pct The count of loans in REO as a percentage of the overall count of loans for the reporting period.

Short SalesThe number of short sales. A short sale is a sale of real estate in which the sale proceeds fall short of the balance owed on the property's loan.

Short Sales Share The number of Short Sales in a given month divided by total sales.

Short Sale Price Discount The average price of a Short Sale divided by the average price of an existing-home sale.

Short Sale Pct The count of loans in Short Sale as a percentage of the overall count of loans for the month.

Distressed Sales Share The percentage of the total sales that were a distressed sale (REO or short sale).

Distressed Sales Share (sales 12-Month sum)

The sum of the REO Sales 12-month sum and the Short Sales 12-month sum divided by the total sales 12-month sum.

HPI MoM Percent increase or decrease in HPI single family combined series over a month ago.

HPI YoY Percent increase or decrease in HPI single family combined series over a year ago.

HPI MoM Excluding Distressed

Percent increase or decrease in HPI single family combined excluding distressed series over a month ago.

HPI YoY Excluding Distressed

Percent increase or decrease in HPI single family combined excluding distressed series over a year ago.

HPI Percent Change from Peak

Percent increase or decrease in HPI single family combined series from the respective peak value in the index.

90 Days + DQ Pct The percentage of the overall loan count that are 90 or more days delinquent as of the reporting period. This percentage includes loans that are in foreclosure or REO.

Stock of 90+ Delinquencies YoY Chg

Percent change year-over-year of the number of 90+ day delinquencies in the current month.

Foreclosure Pct The percentage of the overall loan count that is currently in foreclosure as of the reporting period.

Percent Change Stock of Foreclosures from Peak

Percent increase or decrease in the number of foreclosures from the respective peak number of foreclosures.

Pre-foreclosure FilingsThe number of mortgages where the lender has initiated foreclosure proceedings and it has been made known through public notice (NOD).

Completed ForeclosuresA completed foreclosure occurs when a property is auctioned and results in either the purchase of the home at auction or the property is taken by the lender as part of their Real Estate Owned (REO) inventory.

Negative Equity ShareThe percentage of mortgages in negative equity. The denominator for the negative equity percent is based on the number of mortgages from the public record.

Negative Equity

The number of mortgages in negative equity. Negative equity is calculated as the difference between the current value of the property and the origination value of the mortgage. If the mortgage debt is greater than the current value, the property is considered to be in a negative equity position. We estimate current UPB value, not origination value.

Months' Supply of Distressed Homes (total sales 12-Month avg)

The months it would take to sell off all homes currently in distress of 90 days delinquency or greater based on the current sales pace.

Price/Income RatioCoreLogic HPI™ divided by Nominal Personal Income provided by the Bureau of Economic Analysis and indexed to January 1976.

Conforming Prime Serious Delinquency Rate

The rate serious delinquency mortgages which are within the legislated purchase limits of Fannie Mae and Freddie Mac. The conforming limits are legislated by the Federal Housing Finance Agency (FHFA).

Jumbo Prime Serious Delinquency Rate

The rate serious delinquency mortgages which are larger than the legislated purchase limits of Fannie Mae and Freddie Mac. The conforming limits are legislated by the Federal Housing Finance Agency (FHFA).

© 2017 CoreLogic — Proprietary. This material may not be reproduced in any form without express written permission. 11

The MarketPulse g March 2017 g Volume 6 Issue 3 | Analysis

corelogic.com

End Notes | The MarketPulse g March 2017 g Volume 6, Issue 3

© 2017 CoreLogic, Inc. All rights reserved.

CORELOGIC, the CoreLogic logo, CORELOGIC HPI and MYRENTAL are trademarks of CoreLogic, Inc. and/or its subsidiaries. All other trademarks are the property of their respective holders.

17-MKTPLSE-0317-00

Source: CoreLogicThe data provided is for use only by the primary recipient or the primary recipient's

publication or broadcast. This data may not be re-sold, republished or licensed to any

other source, including publications and sources owned by the primary recipient's parent

company without prior written permission from CoreLogic. Any CoreLogic data used for

publication or broadcast, in whole or in part, must be sourced as coming from CoreLogic,

a data and analytics company. For use with broadcast or web content, the citation

must directly accompany first reference of the data. If the data is illustrated with maps,

charts, graphs or other visual elements, the CoreLogic logo must be included on screen

or website. For questions, analysis or interpretation of the data, contact CoreLogic at

[email protected]. Data provided may not be modified without the prior written

permission of CoreLogic. Do not use the data in any unlawful manner. This data is compiled

from public records, contributory databases and proprietary analytics, and its accuracy is

dependent upon these sources.

For more information please call 866-774-3282

The MarketPulse is a newsletter published by CoreLogic, Inc. ("CoreLogic"). This information is made

available for informational purposes only and is not intended to provide specific commercial, financial or

investment advice. CoreLogic disclaims all express or implied representations, warranties and guaranties,

including implied warranties of merchantability, fitness for a particular purpose, title, or non-infringement.

Neither CoreLogic nor its licensors make any representations, warranties or guaranties as to the quality,

reliability, suitability, truth, accuracy, timeliness or completeness of the information contained in this

newsletter. CoreLogic shall not be held responsible for any errors, inaccuracies, omissions or losses

resulting directly or indirectly from your reliance on the information contained in this newsletter.

This newsletter contains links to third-party websites that are not controlled by CoreLogic. CoreLogic is

not responsible for the content of third-party websites. The use of a third-party website and its content

is governed by the terms and conditions set forth on the third-party’s site and CoreLogic assumes no

responsibility for your use of or activities on the site.

MORE INSIGHTS

The CoreLogic Insights Blog

(corelogic.com/blog) provides an

expanded perspective on housing

economies and property markets,

including policy, trends, regulation

and compliance. Please visit the

blog for timely analysis, thought-

provoking data visualizations and

unique commentary from our team

in the Office of the Chief Economist.

CoreLogic CoreLogic Econ

CoreLogic Insights – On The Go. Download our free App now: