the mc russian market fund

TRANSCRIPT

THE MC RUSSIAN MARKET FUND

(Sociktk d 'Investissement u Capital Variable incorporated with limited liubility in, and under the laws OJ the Grand Duchy of Luxembourg)

PROSPECTUS

MAY, 2006

VISA 2006/15878-1875-0-PC L'apposition du visa ne peut en auwn d'argument de publicit6 Luxembourg, le 09/06/20 Commission de Surveilla

Subscriptions can be accepted only on the basis of the current Prospectus, which is valid only if accompanied by a copy of the latest SICAV's annual report containing its audited accounts, and of the semi-annual report if this was published after the latest annual report. These reports form an integral part of the present Prospectus.

No person is authorised to give any information or to make any representation other than those contained in this Prospectus, or in the documents as referred to in the Prospectus and which can be consulted by the public.

CONTENTS

DIRECTORS. ADMINISTRATION AND ADVISERS ....................................................................................................... 5

BOARD OF DIRECTORS ........................................................................................................................................................ 5

DEFINITIONS ......................................................................................................................................................................... 7

PRINCIPAL FEATURES ....................................................................................................................................................... 8

THE FUND ............................................................................................................................................................................... 9

INTRODUCTION .................................................................................................................................................................... 9 INVESTMENT OBJECTIVES AND POLICIES ........................................................................................................................ 9 TEMPORARY OR DEFENSIVE INVESTMENTS .................................................................................................................... 9 SUBSIDIARIES ....................................................................................................................................................................... 9 INVESTMENT RESTRICTIONS ............................................................................................................................................ 10 INVESTMENT TECHNIQUES .............................................................................................................................................. 10

APPLICATIONS AND REDEMPTIONS ................... ...................................................................... ~ ............. ~ .... ~ ............. 12

SUBSCRIPTIONS ................................................................................................................................................................. 12 REDEMPTIONS .................................................................................................................................................................... 13 TEMPORARY SUSPENSION OF ISSUE AND REDEMPTION PRICES ................................................................................. 13 ISSUE AND REDEMPTION PRICES ..................................................................................................................................... 13 LISTING ............................................................................................................................................................................... 13

CONVERSIONS BETWEEN SHARE CLASSES .............................................................................................................. 14

VALUATIONS. FEES AND EXPENSES ............................................................................................................................ 14

VALUATIONS ...................................................................................................................................................................... 14 FEES AND EXPENSES ............ ......................................................... 14

Investment Munager and In 14 Custodian ................................................................................................................................... 15 Operating Fees und E.xpen.se.s ............................................................... 15

MANAGEMENT AND ADMINISTRATION .................................................................................................................... 15

DIRECTORS ............... ................................ .................................................. 15 INVES-TMENT MANAGER . ................................................ .................................... 15 INVESTMENT ADVIS .......................................................................................................................... 15 CUSTODIAN ............................................................... .................................................................................... 15

........................................ 16 DISTRIBUTION AGREEMENT ............................................................................................................................................. 16

“THE ROS 30 INDEX” ......................................................................................................................................................... 17

DOMICILIARY, REGISTRAR & TRANSFER AND ADMINISTRATIVE AGENT ........

TAXATION AND EXCHANGE CONTROL ..................................................................................................................... 17

INVESTORS ......................................................................................................................................................................... 17 THE FUND ........................................................................................................................................................................... 17

...................................................................... 17

RISK FACTORS ................................................................................................................................................................... 18

POLITICAL RISKS ............................................................................................................................................................... 1 X ECONOMIC RISKS .............................................................................................................................................................. 18 REGULATORY ENVIRONMENT ......................................................................................................................................... 19 VOLAI’I LlTY AND ILLIQUIDITY ........................................................................................................................................ 19 DISCLOSURE ....................................................................................................................................................................... 19 ACCOUNTING PRACTICE ................................................................................................................................................... 19

2

TAX SYSTEM ...................................................................................................................................................................... 20

EXCHANGE RATES, EXCHANGE CONTROLS AND REPATRIATION RESTRICTIONS ..................................................... 20 SECURITIES MARKET RISKS ............................................................................................................................................. 20 REGISTRATION AND CUSTODY RISK ............................................................................................................................... 20

INVESTMENT PRACTICES AND ILLIQUIDITY OF INVESTMENT ..................................................................................... 21

CURRENCY RISKS .............................................................................................................................................................. 20

PRlVATlSATlON PROCESS ................................................................................................................................................. 21

ENVIRONMENTAL RISKS ................................................................................................................................................... 21 CORRUPTION AND ORGANlSED CRIME ........................................................................................................................... 21 VALUE OF SHARES ............................................................................................................................................................ 22 POTENTIAL CONFLICTS OF INTEREST ............................................................................................................................. 22

DIVIDEND POLICY AND FINANCIAL STATEMENTS ................................................................................................ 22

DIVIDEND POLICY ............................................................................................................................................................. 22 FINANCIAL STATEMENTS .................................................................................................................................................. 22

GENERAL AND STATUTORY INFORMATION ............................................................................................................ 22 1 . Thc Fund ............................................................... 22 2 . Share Capital .............................................................................................. ............................................................... 23 3 . Liquidation - Mergers ......................................................................................................................................................... 23 4 . ........................................................... 23 5 . Publication of Prices ...................................................... ................................................................................................ 24 6 . Directors’ Interests ............................................................................................................................................................. 24 7 . Directors’ Remuneration .................................................................................................................................................... 24 8 . Transactions with Directors ................................................................................................................................................ 24 9 . Indemnities ......................................................................................................................................................................... 24 IO . Dcfinition of US Pcrson .......................................... .............................................................................................. 25 1 I . Miscellaneous ...................... ..................................................................................................................................... 25 12 . .Documents available for lnspcction .............................................................................................................................. 25 13 . Complementary information for thc distribution of the Fund’s sharcs in or from Switzerland ...................................... 26

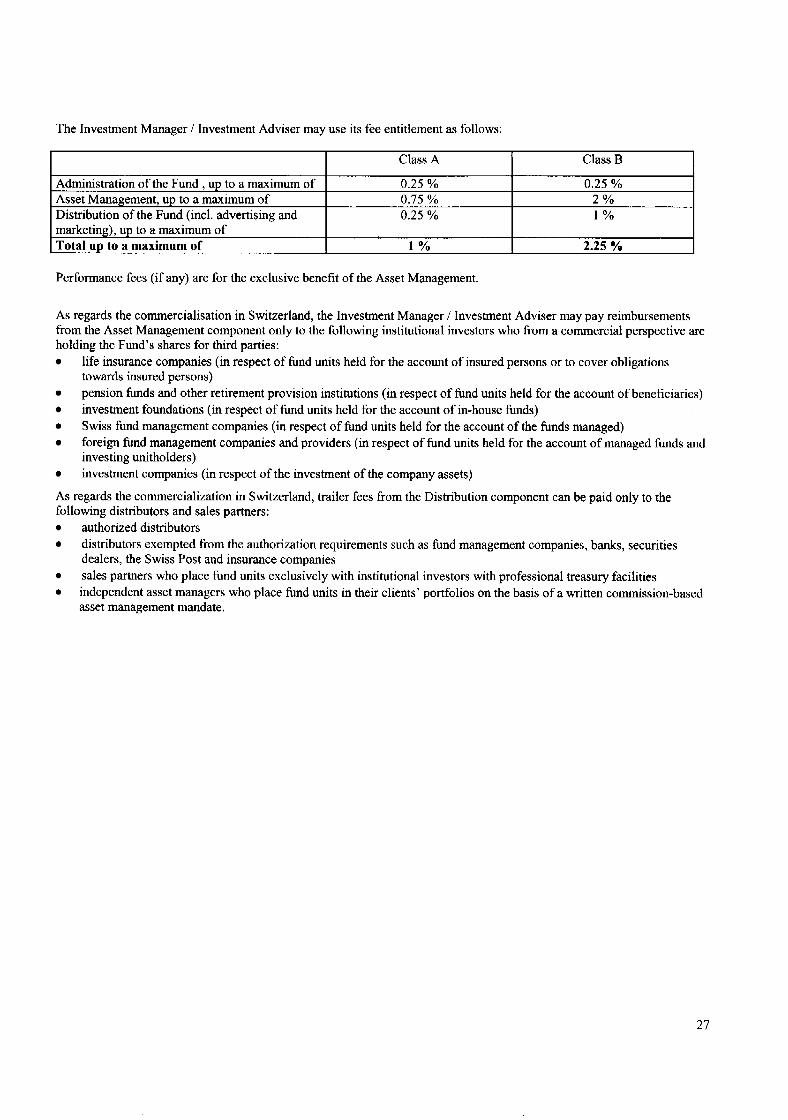

DISTRIBUTION IN SWITZERLAND ..................................................................................................................................... 2~ SWISS REPRESENTATIVE AND PAYING AGENT .............................................................................................................. 26 FEES AND EXPENSES ......................................................................................................................................................... 26 PUBLICATIONS ................................................................................................................................................................... 28 PLACE OF PERFORMANCE AND JURlSDlCTlON ............................................................................................................... 28

APPLICATION FORM ............................ .................................................................................... ........................................ 29

....................................................................................................

Transfer and Compulsory Divestment of Shares ........................................

3

The Directors of the Fund are responsible for the information contained in this document. To the best of the knowledge and belief of the Directors (who have taken all reasonable care to ensure that such is the case) the information contained in this document is in accordance with the facts and does not omit anything likely to affect the import of such information.

The Shares are offered solely on the basis of the information and representations contained in this document and any further information given or representations made by any person may not be relied upon as having been authorised by the Fund or the Directors. Neither the delivery of this document nor the allotment or issue of Shares shall under any circumstances create any implication that there has been no change in the affairs of the Fund since the date hereof.

This document does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorised or to any person to whom it would be unlawful to make such offer or solicitation. The distribution of this document and the offering of Shares in certain jurisdictions may be restricted and, accordingly, persons into whose possession this document comes are required to inform themselves about, and to observe, such restrictions. Prospective investors should inform themselves as to (a) the legal requirements within their own jurisdictions for the purchase, holding or disposal of Shares, (b) any foreign exchange restrictions which may affect them, and (c) the income and other tax consequences which may apply in their own jurisdictions relevant to the purchase, holding or disposal of Shares.

The Fund is not a recognised collective investment scheme for the purposes of the Financial Services Act 1986 of the United Kingdom (the “Act”). This document may only be issued or passed on in the United Kingdom to persons falling within Article I l(3) of the Financial Services Act 1986 (Investment Advertisements) (Exemptions) Order 1995 and the Shares may only be promoted in the United Kingdom by an authorised person under the Act in accordance with the Financial Services (Promotion of Unregulated Schemes) Regulations 1991 as from time to time amended.

The Shares have not been and will not be registered under the United States Securities Act of 1933, as amended (the “1933 Act”) or under the securities (Blue Sky) laws of any state of the United States and, therefore, the Shares may not be ofyered or sold in the United States unless pursuant to an exemption from registration. The Shares being offered hereby have not been approved or recommended by the SEC or any state of the United States or other governmental authority and neither the SEC nor any such authority has passed upon the accuracy or adequacy of this document. Any representation to the contrary is a criminal offence. It is anticipated that the offering and sale will be exempt from registration under the 1933 Act and the various state securities laws.

In addition, the Fund is not and will not be registered under United States Investment Company Act of 1940, as amended (the “1940 Act”). Based on interpretations of the 1940 Act by the staff of the United States Securities and Exchange Commission (the “SEC”) relating to foreign investment companies, if the Company has more than 100 beneficial owners who are US Persons, it may become subject to the 1940 Act. The Directors will not knowingly permit the number of Shareholders who are US Persons to be more than 80. The Investment Manager will not be registered under the United States Investment Advisers Act of 1940, as amended. The attention of United States persons is drawn to the compulsory redemption powers mentioned in paragraph 4 of “General and Statutory Information”.

The Shares are subject to restrictions on transferability and resale and may not be transferred or resold except as permitted under the 1933 Act, and the applicable state securities laws, pursuant to registration or exemption therefrom (for example, to qualified institutional buyers in reliance on Regulation 144A or to non-US Persons in offshore transactions in reliance on Regulation S under the 1933 Act). Investors should be aware that they could be required to bear the financial risb of this investment until the Fund is wound up.

The Shares will not be offered in Russia to Russian residents so as to require permits of the relevant Russian authorities for the transfer of capital and, in addition, neither the Shares nor this document have been registered in Russia under Russian federal or local laws for the purposes of selling Shares in Russia to Russian residents.

The Fund is governed by Part I1 of the Law of 20 December 2002 as it will raise capital without promoting the sale of its Shares to the public within the European Union or any part thereof.

The above information is for general guidance only. Prospective applicants for Shares should inform themselves as to the legal requirements of so applying and any applicable exchange control regulations and applicablc taxes in the countries of their respective citizenship, residence or domicile.

Prospective investors’ attention is also drawn to the “Risk Factors” chapter.

4

DIRECTORS, ADMINISTRATION AND ADVISERS

Board of Directors

Walter FETSCHEm (Chairman)

Gustav STENBOLT

Yves BURRUS

Volker HEMPRICH

Andrea WALTHER

Andre SCHMIT

Investment Manager, Distributor

Investment Adviser

Custodian

Former Swiss Ambassador to Russia

Chairman MCT ASSET MANAGEMENT SA 2-4, Place Molard CH- 1204 Geneva

Board member Anglo Irish Bank (Suisse) S.A. 7, Rue des Alpes 1201 Geneva

MCT ASSET MANAGEMENT SA 2-4, PLACE MOLARD CH-1204 GENEVA

Manager 02 Bankers AG , Churerstrasse 47 8808 Pfaffikon

Premier Fond6 de Pouvoir Kredietrust Luxembourg S.A

L - I I 18 Luxembourg I I , Rue Aldringen

MCT ASSET MANAGEMENT SA 2-4, Place du Molard CH-1204 Geneva

MCT International LTD P.O. Box 3340, Dawson Building, Road Town, Tortola, British Virgin Islands

Kredietbank S.A. Luxembourgeoise 43, boulevard Royal L-2955 Luxembourg

Domiciliary, Registrar Br ‘Transfer and administrative Agent Kredietrust Luxembourg S A . 1 I , rue Aldringen L-2960 Luxembourg

5

Auditors

Legal Adviser as to Swiss law

Price WaterhouseCoopers 400, route d’Esch L- I47 I Luxembourg

Lenz & Staehelin 30, route de ChGne 121 1 Geneve 17

Representative & Distributor in Switzerland MCT ASSET MANAGEMENT SA 2-4 Place Molard 1204 Geneva

Payment agent in Switzerland OZ BANKERS AG Churerstrasse 47 8808 Pfaffikon

6

DEFINITIONS

“Articles” “Business Day”

“CSSF’

“Euroclear System” “Issue Price” “Redemption Price”

“Shares” “Class of Shares”

“Moody’s” “Net Asset Value” or ‘&NAY “OECD’ “Russian Federation” or “Russia” “Russian Companies”

“lndex” “S & P” “Shareholder” “United States”

“US Dollars” or “US$” “US Person” “ E W ’

The Articles of Incorporation of the Fund Any day on which banks are open for business in all of London, Luxembourg-City, MOSCOW, New York and Geneva Commission de Surveillance du Secteur Financier, regulatory body of the financial services sector in Luxembourg Clearing system for Subscriptions and Redemptions The price at which Shares are issued The price per Share at which Shares are redeemed calculated as described in the chapter “Applications and Redemptions” Shares in the Fund of no par value Class A and Class B Shares differentiating themselves by their fee structure and minimum investment level Moody’s Investor Services, Inc. The Net Asset Value of the Fund calculated in accordance with the provisions of the Articles Organisation for Economic Co-operation and Development Those regions, territories, republics, areas and cities which from time to time constitute the geographic area recognised as “Russia” Those corporations, joint stock companies, economic societies, trusts and other entities created, registered and otherwise established in the Russian Federation and those created, registered and otherwise established outside the Russian Federation operating or investing primarily in the Russian Federation or deriving a preponderant part of their income from the Russian Federation The ROS 30 Index Standard & Poor’s Ratings Group, a division of McGraw-Hill, Inc. A holder of Shares as recorded in the Fund’s register of Shareholders The United States of America, any state, territory, or possession thereof, any area subject to its jurisdiction, the District of Columbia, or any enclave of the United States Government or its agencies or instrumentalities The currency of the United States As defined in chapter “General and Statutory Information” The currency of the European Union Member States participating to the Single Currency.

7

PRINCIPAL FEATURES

The following is a summary of the principal features of the Fund and should be read in conjunction with the full text of this document from which it is derived.

The Fund The Fund is an open-ended investment company incorporated with limited liability in Luxembourg on 13 May 1996. The Shares of the Fund are listed on the Luxembourg Stock Exchange.

The investment objective of the Fund is to achieve long-term capital appreciation through investing in Russian Companies, as well as companies in Eastern Europe, the C.I.S. and elsewhere within the limits set forth in the “Investment Restrictions”. The Fund considers the ROS 30 Index as its benchmark, although the Fund does not intend to track this index.

Investment Objective

Subscriptions and Redemptions

Dividend Policy

Taxation

Risk Factors

Shares may be offered on each Business Day at the Issue Price and redeemed on any Business Day at the prevailing Redemption Price. The minimum subscription for class A Shares is US$250.000.- and for class B Shares : US$lO,OOO.-. This minimal amount may be waived at the discretion of the Investment Manager. Details of additional charges payable on the issue of Shares are set out under the Chapter “Applications and Redemptions” .

Capital gains, interest, dividends and other income received will be automatically reinvested, and no dividend will be paid to shareholders, as it is the fund’s objective to achieve long term capital appreciation. Nonetheless, the Board may decide to propose a dividend to the General Meeting of the Shareholders if the Board deems this to be in the best interest of the Shareholders, due for example to changes in the macroeconomic or fiscal environment.

Under current Luxembourg law, the Fund will not be liable to taxation in Luxembourg on its net income or capital gains, nor are dividends paid by the Fund liable to any Luxembourg withholding tax. The Fund is, however, liable in Luxembourg to a tax of 0.05% per annum of its net assets.

An investment in the Fund carries substantial risks. The risks inherent in investment in the Russian Federation are of a nature and degree not typically encountered in investing in securities of companies listed on major security markets worldwide. There can be no assurance that the Fund’s investment objective will be achieved and investment results may vary substantially over time. An investment in the Fund is not intended to be a complete investment programme for any investor. Prospective investors should carefully consider whether an investment in the Fund is suitable for them in the light of their circumstances and financial resources (see further under “Risk Factors” below).

THE FUND

lntroduct ion

d’lnvestissement a Capital Variable number B54.765 and authorized by the CSSF on I7 May 1996.

Investment Objectives and Policies

The objective of the Fund is to achieve long-term capital appreciation through investing at least two thirds of its gross assets after deduction of liquidities in Russian companies or companies exercising their predominant economical activity in Russia.. The Fund may also invest in companies in Eastern Europe, the C.I.S. and elsewhere up to a maximum of one third of the Fund’s total gross assets after deduction of liquidities..

Although the Fund considers the ROS 30 Index when investing, it is not intended that the composition of the Fund’s portfolio reflects the composition or the industry sector weighting of the index. Where the investment manager considers it appropriate and in the interest of the shareholders, the composition of the Fund’s portfolio might significantly deviate from the weighting of the underlying companies and sectors in the index.. In order to achieve its objectives, the Fund may also invest up to 10% of its net assets in undertakings for collective investment (investing their assets or a part of them according to the investment policy of the Fund; the Investment manager of the Fund committing that on a consolidated basis at least two thirds of the gross assets after deduction ot liquidities of the Fund will be invested in Russian companies or companies exercising their predominant economical activity in Russia)

The Fund will not invest in any company where the Investment Manager considers such investment would not be in the best interests of the Shareholders (e.g. the Investment Manager believes the company may not register the Fund’s shareholding).

Whilst the principal investment objective of the Fund is to achieve long term capital appreciation broadly in line with the Index, it is not intended that the Fund be a “tracker fund” as that term is generally understood and used (i.e. the Fund’s investments will not precisely mirror those comprising the Index). In the event that publication of the Index is suspended or the Index ceases to exist, or that the Board of the Fund, in its sole discretion, is of the opinion that the Index is no longer representative of the Russian equity market, the Board may instruct the Investment Manager to substitute another more suitable index.

The Fund was incorporated on 13 May 1996 with limited liability in the Grand Duchy of Luxembourg as a SociCtC

Temporary or Defensive Investments

During periods when the Investment Manager believes that conditions, whether political or economic, are unfavourable, the Fund may, for temporary or defensive purposes (and subject to the principle of risk diversification) invest the available liquid assets in short-term (less than 12 months to maturity) debt securities or hold cash on deposit. These securities will consist of (a) obligations of governments of OECD countries and their respective agencies; (b) bank deposits and bank obligations (including overnight paper, certificates of deposit, time deposits and bankers’ acceptances) denominated in any OECD currency; (c) floating rate securities and other instruments denominated in any currency issued by OECD governments or international or supra-national organisations; (d) corporate commercial paper and other short-term corporate debt obligations; and (e) repurchase agreements with barks and broker-dealers with respect to such securities. The Fund intends to invest in such short-term debt securities rated, at the time of investment, “A” or higher by Moody’s or S&P or, if unrated by either rating agency, in the opinion of the Investment Manager, of equivalent credit quality.

Subsidiaries

Subject to the restriction set out below, the Fund may from time to time invest through wholly-owned subsidiaries incorporated in any appropriate jurisdiction to take advantage of applicable tax treaties. It is intended that such subsidiaries will be audited, to the extent permitted by local laws and regulations, by the auditors of the Fund or its local correspondents and that Directors of the Fund will represent a majority of the directors of each such subsidiary.

In case the Fund invests through a subsidiary, such subsidiary must be wholly owned by the Fund and may not pursue any other activities than holding investmcnts on behalf and for the account of the Fund. The majority of the subsidiaries’ Directors must also be Directors of the Fund. The subsidiaries‘ dnancial statcments must be fully consolidated into the Fund’s financial statements and audited by the same auditors. The Fund’s financial statements must comprise an inventory of all investments held by the Fund through the subsidiaries. The Fund will further take the appropriate measures so as to ensure that the Custodian and tht Auditors are at any time in a position to perform all their obligations in respect of investments held by the subsidiaries in the same way as if they were held directly by the Fund.

9

Investment Restrictions

As a matter of policy in carrying on its investment activities, whether directly or through any subsidiaries, the Fund will

invest more than 10% of its total net assets in any one issuer provided that, in relation to a Russian Company the capitalisation of which represents a percentage greater than 10% of the total capitalisation of the Index, the Fund may invest up to such greater percentage, not exceeding 25%; hold securities representing more than 10% of the total outstanding securities of any class of any one issuer; purchase securities on margin, except such short-term credits as may be necessary for the clearance of transactions; invest in any security, option or financial or forward contract in which the liability of the holder is unlimited; borrow money to a value of greater than 10% of its total net assets; make short sales of securities or maintain a short position; make loans (other than loans to a subsidirvy of the Fund); or invest more than 10% of its total net assets in aggregate in units of undertakings for collective investment, whether closed-ended or open-ended, and will not invest in units of any such undertaking unless it is subject to risk diversification requirements comparable to those of the Fund, always provided that (i) the relevant undertakings pursue an investment policy similar to the one of the Fund, and (ii) no charges, expenses or fees will be debited to the Fund in relation to investments in undertakings for collective investments managed by the Investment Manager; invest more than one third of its total net assets in entities other than companies incorporated in Russia or perfoming a preponderant part of their activities within the Russian Federation. pledge or otherwise charge any of the Fund's assets or transfer or assign them for the purpose of guaranteeing a debt. invest more than 30% of its total assets in securities which are not listed on a stock exchange in Russia or on a stock exchange of an OECD country.

If the restrictions set out under paragraphs (a), (b), (c) or (i) above are exceeded as a result of the exercise of rights attached to investments or for any reason other than the purchase of investments ( e g through capital reductions or market or currency fluctuations), no remedial action will be required.

Investment Techniques

The Fund may use the following techniques and instruments:

(a) investing in stock options in accordance with the following rules:

- investing solely in options listed on a stock exchange or traded on another official market, operating regularly, recognised and open to the public.

- buying, writing or selling call or put options provided:

i. the acquisition cost of options on transferable securities does not exceed, in terms of premiums, 10 9'0 of' the net asset value,

ii. the Fund holds constantly, as cover for call options written and sold either the underlying transferable securities or equivalent call options.

iii. writing or sales of put options relating to settlement operations on put options acquired previously or where it writes put options, the Fund must be covered during the entire duration of the option contract by adequate liquid assets that may be used to pay for securities which could be delivered to it in case of the exercice of the option by the counterpart.

(b) to hedge against the risk of an unfavorable development on stock exchanges the Fund may sell forward exchange contracts, buy put options and sell call options. A sufficiently close connection will exist between the composition of the index used and the portfolio. In addition, total commitments relating to forward exchange contracts and options contracts on stock exchange indexes may not, in principle, exceed the total estimated value of the securities held in the market which corresponds to this index.

10

(c) to hedge against the risk of an unfavorable development in interest rates, the Fund may sell forward exchange contracts, buy put options, sell call options ,carrying out forward rate agreements and interest rate swaps. The forward rate agreements and interest rate swaps must be carried out with first rate financial institutions which are specialised in this type of operation, The total commitments relating to the above- mentioned operations may not exceed the total estimated value of the securities held in the corresponding currency.

Sales of call options on transferable securities with sufficient cover are not taken into account when calculating the above commitments,

(d) total premiums paid to acquire all outstanding call and put may not jointly with the total premiums paid for the options indicated in the above point (a) i., exceed 10 o/o of the net assets.

(e) The Fund may act either as purchaser or seller of repurchase agreements. Its entering into such agreements is however subject to the following rules:

i.It may purchase or sell securities subject to such agreements only if the counterparts are highly rated financial institutions specialised in this type of transactions.

ii.During the lifetime of a repurchase agreement, it may not sell the securities which are the object of the agreement either before the repurchase of the securities by the counterpart has been carried out or the repurchase period has expired.

iii.It must ensure to maintain the importance of such purchase operations at such a level that it is able to meet its obligations to redeem its own shares at all time.

( f , with a view to hedging against the exchange risk, it may carry out operations which relate to contracts to buy or sell currencies foward, financial futures and currency options (selling call options or buying put options). No hedging operation may involve an amount higher than the value of the assets which are the subject of the said hedging nor exceed the time such assets are held. Whcre such assets generate interest at a fixed rate, the hedging may include the interest which is received on maturity; by way of an exception to the above principle, the amount of hedging operations may, on a temporary basis, in the event the value of the assets which are the subject of such operations fluctuates, exceed the value of the asset which has been hedged. In no way may such operations be of a speculative nature. Hedging operations must be carried out in the same currency as the assets to be covered,

(g) all the aforementioned operations, with the exception of over-the-counter operations, must be carried out on an official market, operating normally, recognised and open to the public.

The investments of the Fund in call and put options, financial futures, forward contracts and swap transactions will only be made for the purpose of efkient portfolio management and not for speculative purposes.

(h) it may lend securities in connection with a standard securities lending system organised by a recognised securities clearing body or by a first rate financial institution specialised in this type of operation,

for the purpose of its securities lending operations, the Fund may, in principle, receive a guarantee of a value which, at the time the lending contract is signed, is at least equal to the total estimated value of the securities lent; such guarantee will be given in the form of liquidities and/or securities issued or guaranteed by member states of the O.E.C.D. or by their regional and local authorities or by local, regional and international supranational bodies, frozen in the name of the Fund until the lending contract expires,

the lending operations may not involve over 50 YO of the estimated total value of the securities in the portfolio; however this limit does not apply when the Fund is entitled to obtain termination, at any time, of the contract and refunding of the securities lent; the lending operations may not exceed a period of30 days.

11

APPLICATIONS AND REDEMPTIONS

Subscriptions

by the Fund before 11.30 a.m. (Luxembourg time) on the same Business Day on which the Shares are to be issued.

which should be sent to: European Fund Administration rue d’Alsace B.P. 1725 L- 1725 Luxembourg Fax: (352) 48 65 61 8002 or: MCT ASSET MANAGEMENT SA 2-4, Place du Molard CH 121 I Geneva Fax: (41) 22 716 10 01

Furthermore, Shares of the Fund are eligible for purchase through the Euroclear System provided the investor has an established account with Euroclear. Investors wishing to purchase Shares through the Euroclear System should send a formatted instruction in the form used by the Euroclear System directly to Morgan Guaranty Trust Company of New York, Brussels office as operator of the Euroclear System, quoting the participant’s name and account number with Euroclear and referencing the name of the Fund, the securities Common Code “468902” or the securities ISIN number “LU 0066480616”.

All purchases and redemptions of Shares effected through the Euroclear System are subject to the terms and conditions governing the use of the System, the related operating procedures of the clearing system and applicable law. All securities in the Euroclear System are held on a fungible basis without attribution of specific securities to special securities clearance accounts.

The Euroclear Operator is authorised to disclose to the Investment Manager of the Fund, or its designated agent, the positions held by thc various participants effecting investments in the Fund through the Euroclear System.

When applying for the first time, investors must subscribe US$250,000 for class A Shares and US$ 10,000 for class B Shares or more. This minimal amount may be waived at the discretion of the Investment Manager. No fractions of Shares will be issued. Subscriptions will be rounded down to the nearest whole Share and that part of the subscription monies relating to such rounding down will he retained for the benefit of the Fund.

An initial charge of up to 4% of the Issue Price may be added upon the issue of Shares fbllowing the Initial Offer. This initial charge will be payable to the Investment Manager or intermediaries who agree to subscribe for or arrange for the subscription of‘ Shares.

Applications are subject to the terms of this document, the Articles of the Fund and the Application Form. The right is reserved to refuse any application for any reason.

Payment by telegraphic transfer, net of charges, is due in cleared funds within 2 bank business days in Luxembourg following the applicable Net Asset Value, except as may from time to time be decided by the Directors. Payments should be made in US Dollars

Where subscription monies are not received on the due date, the Directors are not obliged to issue shares on the relevant Business Day. Proceedings may be taken to recover such sums and chargc interest on the overdue monies on a daily basis until payment is received in full at such rate as the Directors consider appropriate.

The Directors may from time to time at their discretion determine that no further Shares will be issued by the Fund if to do so is considered impractical for the efficient operation of the Fund in accordance with its investment policy.

The Fund may agree to issue Shares as consideration for a contribution in kind of securities falling within the investment objectives and policies of the Fund, in compliance with the conditions set forth by Luxembourg law, in particular the obligation to deliver a valuation report from an auditor (“rkviseur d’entreprises agrek”) which shall be available for inspection. Any costs incurred in connection with a contrihution in kind of securities shall be borne by the relevant Shareholders.

Shares may be issued on each Business Day at the prevailing Issue Price. Applications for such Shares must be received

Applications should generally be made on the Application Form (enclosed with this document), in writing or by facsimile,

The securities contributed will be valued at their offer price.

12

Shares will be in registered form only and no certificates will be issued in respect thereof. The register of Shareholders will be kept at the offices of the Registrar and Transfer Agent or his sub-contractor.

Redemptions

A Shareholder may redeem shares on any Business Day at the Redemption Price then ruling. A redemption notice must be received by the Fund before 11.30 a.m. (Luxembourg time) on the same Business Day on which the Shares are to be redeemed. Once given, a redemption notice may not be revoked by Shareholders save where determination of the Redemption Price is suspended in accordance with the terms of the Articles.

Payment of redemption proceeds will be made by cheque in US Dollars which will be dispatched by post at the Shareholder's risk within 10 Business Days after the relevant Redemption Day. Arrangements can be made for Shareholders to receive payment by telegraphic transfer. In these circumstances, Shareholders are advised to specify settlement instructions when making their request for redemption. The cost of any administrative expenses will be borne by the Fund. Contract notes will be dispatched in respect of all redemptions of Shares.

If redemption notices represent, on a Business Day, more than 10% of the total number of Shares in issue, the Directors are entitled to reduce the requests on a prorata basis and carry out only sufficient redemptions which, in aggregate, amount to 10% of the Shares in issue. Redemption notices for Shares which are not redeemed but which would otherwise have been redeemed will be deferred until the next Business Day and will be dealt with (subject to further deferral if a deferred request exceeds 10% of the Shares in issue) in priority to later redemption notices.

Temporary Suspension of Issue and Redemption Prices

circumstances: The Directors may suspend the determination of Issue and Redemption Prices of any Class in any of the following

(a) By reason of the closure, suspension or restriction of trading on any exchange or exceptionally volatile market conditions or for any other reason, circumstances exist as a result of which, in the opinion of the Directors, it is not reasonably practicable fairly to determine the Issue and Redemption Prices; or Where, as a result of exchange restrictions or other restrictions affecting the transfer of funds, transactions on behalf of the Fund are rendered impracticable or if purchases, sales, deposits or withdrawals of the Fund's assets cannot be effected at normal rate of exchange; or

(c) Any other circumstance exists where the Directors consider such suspension to be in the interests of the Fund or the Shareholders.

Any such suspension shall be publicized, if appropriate, by the Fund and may be notified to applicants for Shares in

(b)

respect of whose applications the calculation of the Issue Price has been suspended.

Issue and Redemption Prices

The Issue and Redemption Price of each Class of Shares will be calculated as at each Business Day by:

(a)

(b) ( (c)

Determining the Net Asset Value of the Class of Shares (as described in the chapter " Valuations, Fees and Expenses"); Dividing the result of (a) by the number of Shares then in issue or decmed to be in issue in the concerned Class;

Rounding the result of (b) upwards to the nearest US$O.O 1.

Initial charge An initial charge of up to 4% of the Issue Price will then be added which sum will be payable to the Investment Manager

or intermediaries who agree to subscribe for or arrange for the subscription of Shares.

Listing

The Shares are listed on the Luxembourg Stock Exchange and will be quoted in US Dollars. As it is intended that the Shares will be placed with a limited number of investors, there can be no assurance that there will be an active market in the Shares.

13

CONVERSIONS BETWEEN SHARE CLASSES

Subject to the respective initial minimum investment thresholds, which also apply for conversions, shareholders may request the convertion all or part of their holdings from any share class into another share class at a price equal to the respective Issue Price of each share class.

VALUATIONS, FEES AND EXPENSES

Valuations

Valuations of the net assets of the Classes will be carried out on each Business Day. The Net Asset Value of the Classes will be determined by the Administrative Agent by deducting the liabilities of the Fund (including without limitation, accrued fees and expenses) from the value of the Fund’s gross assets determined on a bid basis in accordance with the Articles. The Net Asset Value will be calculated in US Dollars.

The Fund’s gross assets will be valued in accordance with the following principles: (a) Any security which is listed or quoted on a securities exchange or similar system and regularly traded thereon is

valued at the latest available bid price as quoted in comparable size to the holding maintained by the Fund by a reputable broker as at the relevant Business Day. If a security is listed or traded on several stock exchanges or markets, the latest available bid price on the exchange or market which, in the sole discretion of the Directors, constitutes the principal market for such security shall apply; Any security which is not listed or quoted on any securities exchange or similar electronic system or, if being so listed or quoted, is not regularly traded thereon or in respect of which no prices are described above are available, is valued at its fair bid value as determined by the Directors having regard to its cost price, the price at which any recent transaction in the security may have been effected, the size of the holding having regard to the total amount of such security in issue, and such other factors as the Directors in their sole discretion deem relevant in considering a positive or negative adjustment to the valuation; Deposits are valued at their cost plus accrued interest; Any value (whether of an investment or cash) otherwise than in US Dollars is converted into US Dollars at the rate (whether official or otherwise) which the Directors in their absolute discretion deem applicable as at close of business on the relevant Business Day, having regard, among other things, to any premium or discount which they consider may be relevant and to costs of exchange.

If the Directors consider that any of the above bases of valuation are inappropriate in any particular case, they may adopt such other valuation as they consider better reflects the fair value of the relevant assets. The Directors may delegate to the Investment Manager or the Custodian any of their discretions under the valuation guidelines.

(b)

(c) (d)

Fees and Expenses

Investment Manager and Investment Adviser

The Fund will pay an aggregate managemendadvisory fee of : - for class A Shares, 1 .O% per annum payable quarterly in arrears based and calculated on the average weekly Net Asset

- for class B Shares, 2.25% per annum payable quarterly in arrears based and calculated on the average weekly Net Asset

Furthermore, a performance fee equal to 15% for class A Shares and 10% for class B Shares of any progression of the Net Asset Value of the valuation day compared to the last Net Asset Value which entailed a payment of performance, multiplied by the number of shares, will be charged to the Fund. An accrual for the performance fee is made on each valuation day, when appropriate, and the final performance fee will be payable annually, based on the last valuation day of December in each year. If losses are incurred in the Net Asset Value, the performance fee will not be paid until the losses are recovered and there are new profits. The allocation of the above mentioned fees between the Investment Manager and Investment Adviser will be agreed between the two parties from time to time. In no case the aggregate fees will exceed the aforesaid percentages.

Value of theclass;

Value of the Class.

14

Custodian The fees for KREDIETBANK S.A. Luxembourgeoise's services are charged, in accordance with usual bank fees. The

Custodian will be entitled to a fee expressed on a reducing percentage of the net assets of the-fund, payable monthly, and to a flat transaction fee on all operations relating to receipt or delivery of Portfolio securities. 'This agreement is made for an unlimited duration and may be terminated by either party giving the other three months' notice.

Operating Fern and Expenses The Fund will bear the commission and other costs of all transactions carried out by it or on its behalf including (a) the

charges and expenses of legal advisers and independent auditors, (b) brokers' commissions (if any).and any issue or transfer taxes chargeable in connection with its securities transactions, (c) all taxes and corporate fees payable to governmental agencies, (d) communications expenses with respect to investor services and all expenses of meetings of Shareholders and of preparing, printing and distributing financial and other reports, proxy forms, prospectuses and similar documents, (e) the cost of insurance (if any), (f) litigation and indemnification expenses and extraordinary expenses not incurred in the ordinary course of business and (g) the cost of obtaining and maintaining the listing of the Shares on the Luxembourg Stock Exchange and all other organizational and operating expenses.

MANAGEMENT AND ADMINISTRATION

Directors

The Directors are responsible for the overall management and control of the Fund and will monitor the activities of the entities undertalung the functions for the Fund.

The Directors will review the operations of the Fund at regular meetings and for this purpose will receive periodic reports from the Investment Manager detailing the Fund's performance and providing an analysis of its investments. The Investment Manager will provide such other information as may from time to time be reasonably required by the Directors for the purpose of such meetings.

Investment Manager

By way of a three party agreement dated 01 October 2005 MCT ASSE'P MANAGEMENT SA has been appointed as Investment Manager of the Fund as from 1998 following the retirement on the same date of MC Securities Limited. The Investment Manager shall have full discretion and authority to manage the accounts of the Fund on a day-to-day basis by investing, reinvesting, trading and supervising the Fund's assets in a manner consistent with the investment objectives, policies and restrictions described in this document.

MCT ASSET MANAGEMENT SA is an institutional asset management firm. MCT ASSET MANAGEMENT SA manages a number of investment companies and funds focusing on Russia and Eastern Europe, including ENR Russia Invest SA and Eastern Property Holdings Ltd., listed on the Swiss Stock Exchange and MC Premium SICAV, listed on the Luxembourg stock exchange.

Investment Adviser

By way of a three party agreement dated 1 October 2005 MCT International Ltd has been appointed as Investment Adviser of the Fund. The Investment Adviser will have responsibility for advising in its duties the Investment Manager on all matters including general economic and stock market conditions, overall investment strategy, research and evaluation of potential investments and sectors on investment for inclusion in the portfolio of the Fund and analysis of investments in the portfolio of the Fund.

Custodian

was appointed custodian of the securities of the Fund pursuant to a Custodian Agreement dated July I , 2003 . KREDIETBANK S.A. Luxembourgeoise, societe anonyme, having its head olXce at 43 Boulevard Royal: Luxembourg,

15

The safekeeping of the Fund's assets has been entrusted to the Custodian Bank which shall fulfil the obligations and duties stipulated by law. In accordance with banlung practice, the Custodian Bank may, under its responsibility, entrust all or part of the assets in its custody to other banlung institutions or financial intermediaries. The Custodian must: a)

b)

c) KREDIETBANK S A . Luxembourgeoise is a bank organised as a societe anonyme in and under the laws of the Grand Duchy of Luxembourg. As of 3 1 st December 2003, its capital and reserves amounted to EUR 1,379,897,254.-. The fees for KREDIETBANK S.A. Luxembourgeoise's services are charged, in accordance with usual bank fees. The Custodian will be entitled to a fee expressed on a reducing percentage of the net assets of the fund: payable monthly, and to a flat transaction fee on all operations relating to receipt or delivery of Portfolio securities. This agreement is made for an unlimited duration and may be terminated by either party giving the other three months' notice.

Domiciliary, Registrar & Transfer and Administrative Agent

ensure that the sale, issue, re-purchase and cancellation of shares effected by or on behalf of the Fund are carried out in accordance with the law and the Articles of Incorporation of the Fund, ensure that in transactions involving the assets of the. Fund, the consideration is remitted to it within the usual time limits, ensure that the income of the Fund is applied in accordance with its Articles of Incorporation.

JSREDIETRUST LUXEMBOURG S.A. has its registered office is at 11, rue Aldringen, Luxembourg. KREDIETRUST Luxembourg S.A. is member of the KREDIETBANK-ALMANIJ GROUP. Pursuant to the Domiciliary Agency, Registrar and Transfer Agency and Administrative Agency Agreements dated July 1, 2003. KREDIETRUST LUXEMBOURG S.A. was appointed as Domiciliary Agent to the Fund in Luxembourg, as Registrar and Transfer Agent and as Administrative Agent. These agreements are made for an unlimited duration and may be determined by either party giving the other three months' notice. KREDIETRUST LUXEMBOURG S A . acting as Administrative and Registrar and Transfer Agent is authorised to subcontract, whilst retaining full responsibility, to European Fund Administration, sociCtk anonyme ("EFA"), established in Luxembourg, the execution of all or part of its contractual duties.

Distribution Agreement

Since 1998, MCT ASSET MANAGEMENT SA has been designated as the non-exclusive distributor of the Fund. MCT ASSET MANAGEMENT SA is entitled to delegate its functions to one or more other persons although it shall remain liable for any such person's actions.

In relation to distribution, MCT ASSET MANAGEMENT SA has been appointed to market the sale of shares of the Fund . In consideration of its services as distributor, MCT ASSET MANAGEMENT SA will be entitled to commission equal to the initial charge payable in respect of each share in the Fund for which it procures investors.

The Fund hereby undertakes to indemnify and hold the Distributor harmless from and against all or claims, actions, liabilities, demands, proceedings or judgements ("Proceedings") brought or established against the Distributor by any subscriber or purchaser of any of thc Shares or any subsequent purchaser or transferee of any of the same, or by any other person, governmental agency or regulatory body whatsoever (including without limitation any person to whom it delegates its functions, powers and duties hereunder) and against all losses and all reasonable costs, charges and expenses (including legal fees) which the Distributor may suffer or incur (including, but nor limited to, all such losses, costs. charges or expenses reasonably suffered or incurred in disputing or defending any Proceedings andor in establishing its right to be indemnified andior in seeking advice in relation to any Proceedings) and which in any such case arise directly or indirectly in connection with or out of any breach or alleged breach by the Fund of any of its obligations and undertakings under this Agreement and which does not arise from the negligence or wilful default of the Distributor on any failure by the Distributor to perform its obligations..

It should be noted that prospective and current investors are under no obligation to place subscription or redemption orders through a Distributor and may place such orders directly with the Fund.

16

“THE ROS 30 INDEX”

The ROS 30 Index is a free float-weighted index made up of the 30 largest Russian Companies in terms of market capitalisation and liquidity.

The ROS 30 Index tracks the 30 largest and most liquid Russian Companies. The stock’s liquidity is estimated based on the trading date (number of trades and trading volume) obtained from the Russian Trading System (“RTS”). The Index is composed so that no single sector can dominate (e.g. the total index weighting of companies of a specific sector cannot be greater than 50 %).

The Index is calculated daily, based on mid-market closing price levels as reported by the RTS and other market information systems (such as Bloomberg).

The primary criteria for inclusion in the index are: - -

-

The company is in the top thirty in terms of size The company has been traded on twelve or more days in the previous year The company is not more than 50 9’0 owned by another index constituent.

If the market capitalisation of any one sector exceeds 50 % of the total Index cap for at least 22 days in one quarter, than the smallest company from that sector must be replaced by the next largest company outside the top thirty which satisfies the liquidity criteria.

TAXATION AND EXCHANGE CONTROL

Investors

The receipt of dividends by Shareholders and the redemption of Shares may result in a tax liability for Shareholders according to the tax regime applicable in the various countries of residence. Investors resident in or citizens of certain countries which have anti-offshore fund legislation may have a current liability for the undistributed income and gains of the Fund. Prospective investors should be aware that the Fund does not intend to apply for certification as a “distributing fund” for the purposes of section 760 Income and Corporation laxes Act 1988 ofthc United Kingdom.

Investors should consult their professional advisers on the possible tax and exchange control consequences of their subscribing for, purchasing and holding Shares of the Fund under the laws of their countries of citizenship, residence or domicile.

There can be no guarantee that the tax position or proposed tax position prevailing at the time an investment in the Fund is made will endure indefinitely.

The Fund

(a) Luxembourg Under current law the Fund will not be subject to any Luxembourg tax on its net income or capital gains, nor will

dividends paid by the Fund be subject to any Luxembourg withholding tax. The Fund is, however, liable in Luxembourg to a tax of 0.05% per annum of its net assets, such tax being payable

quarterly and calculated on the Net Asset Value of the Fund at the end of the relevant quarter. No stamp duty or other tax will be payable in Luxembourg on the issue of Shares except a once-and-for-all tax of the equivalent of EUR 1,239.47 paid upon incorporation of the Fund.

(b) Russia At present the withholding tax on dividends and interest is generally 15%, although tax is generally not withheld on

interest payable by the Central Bank of Russia or the Russian Ministry of Finance on Russian government debt obligations.

17

Capital gains realized by foreign entities on sales of securities which are publicly traded in Russia are in general tax exempt.

Generally, the net income of Russian companies is currently taxed at base rates between 20% and 24%. In addition, there are various special fees and taxes that apply either generally, to particular industries, or in local jurisdictions that will increase the effective tax rate. These include value added taxes, other turnover taxes, property taxes, payroll taxes, and taxes on expenses.

(c) United Kingdom Although any profits and gains of the Fund arising in the United Kingdom may be within the charge to UK taxation, it is

expected that neither the Investment Manager or Adviser, as agent of the Fund, nor the Fund itself should be assessable to UK taxation on such profits and gains by reason of exemptions contained in the Finance Act 1995. The Directors of the Fund and the Investment Manager intend to manage the Fund and its investments in such a manner as to ensure that the benefit of those exemptions is available. If any profits and gains arising in the United Kingdom are received by the Fund subject to deduction of tax at source, the Fund will not be entitled to claim from the UK Inland Revenue repayment of the tax deducted.

(d) United Stutes The Directors of the Fund and its Investment Manager intend to manage the affairs of the Fund in such a manner that the

income of the Fund will not be subject to United States federal income tax, other than any income or withholding tax that may be imposed on investment income of the Fund from United States sources. It is not anticipated that the amount of any such United States tax will be material.

RISK FACTORS

Investment in the Russian Federation involves certain risks, including those set out below, not typically associated with investing in securities of companies in more developed and highly regulated environments. Investment in the Russian Federation is thus suitable for investors understanding such risks involved and able to bear the related economic exposure. The Fund can give no assurance that its primary investment objective of capital appreciation will be achieved.

The risks involved in investing in the Russian Federation include the following:

Political Risks

Over the past few years, the government and Parliament of the Russian Federation have enacted reforms aimed at transforming the political and economic system into a more democratic, free market oriented society. This process has resulted in social and economic dislocations accompanied by falling living standards and a growing polarisation of society.

As the democratic process is developing and free elections are taking place, there is ongoing risk that newly-elected andor appointed representatives may not continue the recent economic and political reforms, or will modify them to such an extent that the transformation of the Russian Federation towards political and economic liberalisation will be delayed or even halted. Furthermore, there can be no assurance that the process will not be reversed and that recently privatised industries, particularly those considered of strategic significance, will not be renationalised.

Economic Risks

Investments by the Fund may be affected by the general economic climate in Russia. While the macroeconomic picture over the past years has improved considerably, with moderating inflation, stabilisation of the rouble? and the creation of a balance of payment surplus, there is no assurance that these trends will continue. In addition, while price controls, most export quotas and export taxes have been abolished or significantly reduced, there can be no assurance that some of these liberalisation measures will not be reversed.

The scope, speed and nature of any future economic reforms remains uncertain. High levels of inter-enterprise debt and government borrowing may also have serious economic consequences. Such debt,

in the past, has led to non-payment by Russian companies of company obligations and delay or non-payment of workers' salaries. In addition, the Russian government has financially subsidised a number of companies which are technically insolvent.

18

Investments of the Fund may also be affected by alteration in the fiscal framework, which is currently in a state of change, as well as by an abrogation or modification of the Cyprus-Russia Treaty regarding double taxation of dividends and capital gains.

Regulatory Environment

The Russian securities market is regulated by several different authorities which are often in competition with each other (the Russian Federation Ministry of Finance, the Central Bank of the Russian Federation, the Federal Commission on Securities and Capital Markets and the Russian Federation State Property Committee). The regulations of these various authorities are not always coordinated and may be contradictory. Investments in Russia are generally subject to minimal governmental regulations other than currency regulations. Investors should be aware that unregulated trading implies greater risks, In the absence of exchange or clearing co-operations, the performance of transactions is the responsibility only of the individual member with whom the trader has entered into a contract. .

The overall regulation of joint stock companies generally suffers from the speed and volume at which legislation has been passed, and from the diversity of the authorities regulating both companies and the securities market in general. This situation is aggravated by the lack of a legislative habit of repealing legislation which is outdated or no longer applied. As a result, legislation is frequently inconsistent, contradictory or not applied in practice. Regulations are interpreted and applied with little consistency and the decisions of one government oficial may be overruled or contested by another. Moreover, many of the new Russian laws have never been interpreted by courts or administrative bodies. Both Soviet experience and recent Russian practice suggest that the enforcement of legal rights in Russia will continue to be subject to greater discretion and political influence than is the case in most western jurisdictions. In addition, development of a system of corporate governance and investor protection is still very much in the early stages of its development in Russia.

Investment in Russia by foreigners may require the procurement of a substantial number of regulatory consents, certificates and approvals (including, in some cases, the approval of the board of an investee company). Although it is unlikely that all necessary consents, certificates and approvals will have been obtained by the closing of the Initial Offer, the Investment Manager believes it will obtain all those necessary for the operation of the Fund as described herein. The inability to obtain a particular licence, consent or approval could adversely impact the Fund’s operations.

Volatility and Illiquidity

The value of shares in the Fund may be extremely volatile.. In certain instances, a limited number of the purchases and sales can have a significant impact on the price of securities. In addition, from time to time governments intervene in certain markets often with the intention of influencing prices.

Although shares of companies in the ROS 30 Index are relatively liquid in the context of the Russian equity market, the Fund’s investments may be considered illiquid compared with equity investments in more developed international markets. The Fund may not always be able readily to realise its investments. The sale price for such securities may be lower or higher than the Investment Manager’s most recent estimate of their fair value.

Disclosure

At present, there are limited effective legal or regulatory controls in the Russian securities markets. Consequently, investors operate in an environment which is radically different to that prevailing in the more developed securities markets. Disclosure requirements are rudimentary and investment decisions may therefore be based on information which may subsequently prove to be incorrect or which may not have been available at the relevant time. Therefore, prices which the Fund pays for securities may be affected by trading on material non-public information, market manipulation and similar activities. The reporting, accounting and auditing standards of Russian companies differ from international standards in important respects and may be misleading; and less information is generally available to investors than to investors in securities of companies in the more established markets.

Accounting Practice

Although IAS accounting practices are becoming more common in certain cases, local Russian accounting, auditing and financial reporting standards in Russia are being used. which are very different from, and not equivalent to, those employed under generally accepted international practice. The assets and profits appearing on the financial statements of an issuer in which the Fund may invest may not reflect its financial position or results of operations in the way they would be reflected had the financial statements have been prepared in accordance with generally accepted accounting principles. The quality and reliability of information available to the Fund will in most cases be less than in respect of investments in more highly regulated markets. In addition, the information which is available is not necessarily accurate or comparable. Furthermore, for a company that keeps accounting records in local currency, inflation accounting rules may require, for both tax and accounting purposes, that certain assets and liabilities be restatcd on the issuer’s balance sheet in order to express items in terms of a currency of constant purchasing power.

19

Tax System

Although the Investment Manager will take reasonable steps to mitigate the Fund’s tax liabilities, it should be noted that the current attraction of schemes, such as the use of wholly-owned subsidiaries, to make investments to take advantage of relevant tax treaties could change. This could result in an extra layer of taxation, additional political risks and possible tax liabilities arising from the reorganisation of the structure of the Fund. Investors should appreciate that one of the risks inherent in investing in the Fund is the unpredictability of the tax treatment to which it will be subject in Russia.

Investors’ attention is also drawn to the information under “Taxation and Exchange Control”.

Currency Rish

Although US dollar price quotations are generally available for shares in the ROS 30 Index, these are typically a reflection of underlying rouble prices. The value of the assets of the Fund and its income, as measured in US Dollars, may therefore be affected by fluctuations in currency rates and exchange control regulations. In addition, the rouble is not freely convertible into US Dollars or other currencies outside the Russian Federation and as such it is not internationally traded. Any further depreciation could have an adverse impact on the performance of the Fund. This risk is further enhanced by the fact that the cost of hedging the currency risks may not be economic due to a variety of factors including the almost complete absence of forward and futures contracts, options or other such instruments for hedging against rouble risk.

Exchange Rates, Exchange Controls and Repatriation Restrictions

In recent years, the rouble has experienced a significant depreciation relative to the US Dollar and there has been significant instability in the rouble exchange rate, although this instability has lessened in recent months by means of the Government establishing a band within which the rouble may fluctuate. The Government’s ability to maintain this band will depend on many political and economic factors, including its ability to control inflation and the availability of foreign currency to support the band.

The rouble is not convertible outside Russia. A market exists within Russia for the conversion of roubles into other currencies, but it is limited in size and is subject to rules limiting the purposes for which conversion may be effected. There can be no assurance that such a market will continue indefinitely. Currently, 50% of foreign currency earnings from export sales must be converted into roubles. The recent stability of the exchange rate of the rouble has mitigated risks associated with forced conversion, but no assurance can be given that such stability will continue. Moreover, the banking system in Russia is not yet as developed as its Western counterparts and considerable delays may occur in the transfer of funds within, and the remittance of funds out of Russia. While the current policy of the Government is to allow the repatriation by foreign investors of profits earned in Russia, there are restrictions on such repatriation. Exchange control legislation provides for the Central Bank to promulgate rules regulating certain actions by non-Russian residents owning rouble-denominated securities. Export of such securities is currently not permitted without Central Bank approval.

For the purposes of making equity investments and receiving income on such equity investments, a foreign investor (being a legal entity) may make payments (i) in foreign currency provided that the Russian resident recipient of the foreign currency has a transaction specific licence from the Central Bank of Russia or (ii) in roubles through a rouble I-type account. The types of payments which may be credited to rouble i-type accounts of non-Russian residents are restricted and the repatriation of amounts in rouble I-type accounts (upon conversion) is subject to payment of taxes and duties payable by the I-type account holder.

Securities Market Risks

developed than in many Western countries and, in some cases, is effectively non-existent.

Registration and Custody Risk

Settlement, clearing and registration of securities transactions are subject to significant risks not normally associated with investments in more developed markets. Russian equity securities are generally registered in book-entry form only and Russian enterprises generally do not issue share certificates. The entry in a share register provides the only definitive record of ownership of shares, although the share certificate may provide secondary evidence of ownership. There is no central registration system. Registration services are carried out by many different registrars located throughout Russia or by the internal registrars of the companies themselves, in many cases, in violation of the legal requirements. These registrars are subject to government supervision, although such supervision is often not effectively performed and enforced and it is possible for the Fund or its subsidiaries to lose their registration through fraud, ncgligence or errors.

While the Fund will endeavour to ensure that its interests continue to be appropriately recorded either itSElf or through a correspondent bank or other agent inspecting the sharc registers and by obtaining extracts of share registers through regular audits, these extracts have no legal enforceability as they only provide evidence of what has been registered at some point in

Government supervision of the securities market, and of financial intermediaries and issuers, is considerably less well

20

time. Regulations allow issuers with less than 500 shareholders to control its registrar, which means that the management of a company is often able to exert considerable influence over who can purchase and sell the company’s shares by refusing to record, or discouraging a registrar from recording, transactions on the share register. However, companies with more than 500 shareholders are required to have independent registrars.

Privatisation Process

The transformation of medium and large-scale state enterprises into open joint stock companies and their subsequent privatisation has been carried out at an unprecedented rate. In doing this, much of the responsibility for preparing such enterprises for privatisation and complying with much of the privatisation legislation was imposed on individuals at the enterprise concerned rather than through strict control by state authorities. This has been aggravated in many cases by a lack of legal certainty as to the rules that do or did apply to such privatisation. This increases the risk that there may be illegalities in the privatisation that may lead to full or partial invalidity of the privatisation of the enterprise concerned or government sanctions on that enterprise or its management or employees. Alternatively, an enterprise may not have valid or full title to all of the assets shown on its balance sheet and may be subject to obligations arising from a period prior to its privatisation. As an investor, the Fund may consequently lose all or a part of its investments in such privatised enterprises.

Investment Practices and Illiquidity of Investment

Pursuant to its investment policies, the Fund may make investments and use investment techniques described above under “The Fund’ which bear risks and special considerations. While the Fund will generally only invest in listed or traded securities, the degree of liquidity may not be comparable to that prevailing in more developed secondary securities markets.