the mexican sugar industry in the context of u.s. policy naamic workshop calgary, may 31 – june 2,...

TRANSCRIPT

The Mexican Sugar Industry in the context of U.S. policy

NAAMIC WorkshopCalgary, May 31 – June 2, 2006

The Mexican Sugar Industry in the Context of U.S. policy

Background/update on Mexico – events since expropriation

Mexican sugar industry balance – looking to the future

Mexican sugar policy framework – protecting prices

U.S. policy environment – access is key

Policy options – buyout and implications

Final thought – policy analysis and market integration

The Mexican sugar industry after the expropriation Brings discipline to the market Congress enacts excise tax on HFCS used in soda pop Sugar prices rebound Companies whose mill expropriated fight in court Government loses legal battle and returns four GAM mills

(2004) Soda pop companies receive injunction allowing for HFCS use

(2005) Agricultural Secretary sells two mill in 2005 Expropriation of Machado mills overturned in 2006 with ruling

undermining legal basis for expropriation of the mills Mexico loses HFCS battle in WTO Government takes expropriated CAZE mills to bankrupcy court Biofuel law in Congress

The Decreto Cañero is revoked, but ?

On January 14, 2005 the Fox Administration revokes the Decreto Cañero The Agricultural Secretariat is to bring sugar industry in line with

the production chain concept that brings together the different players in the market to negotiate policy and programs. A National Committee for the Sugar Cane System is to be established The players negotiate, under the auspices of the Agricultural

Secretariat a 7% increase in sugar cane prices for the 2004/05 harvest Protests led to Congress proposing a new Sugar Law,

incorporating much of the Decreto Cañero. SAGARPA and Congress negotiate changes, but no movement as

of yetIn other words, the situation is still in a state of flux

The Decreto Cañero

Decreto Cañero (Sugar Cane Growers Decree) requires farms, whether they be ejido or private farms, that operated within the sugar mills areas of influence to exclusively produce sugar cane. The decree, in turn, required that the mills buy all the sugar cane produced in their area of influence. This assured a market for farmers’ cane and jobs for rural laborers.

The decree limits the mills ability to adjust purchasing to market conditions. The decree also sets forth a pricing formula for the sugar cane based on a percentage increase of the previous year’s price.

Taken together, the various parts of the Decreto Cañero effectively separated the sugar industry from the market.

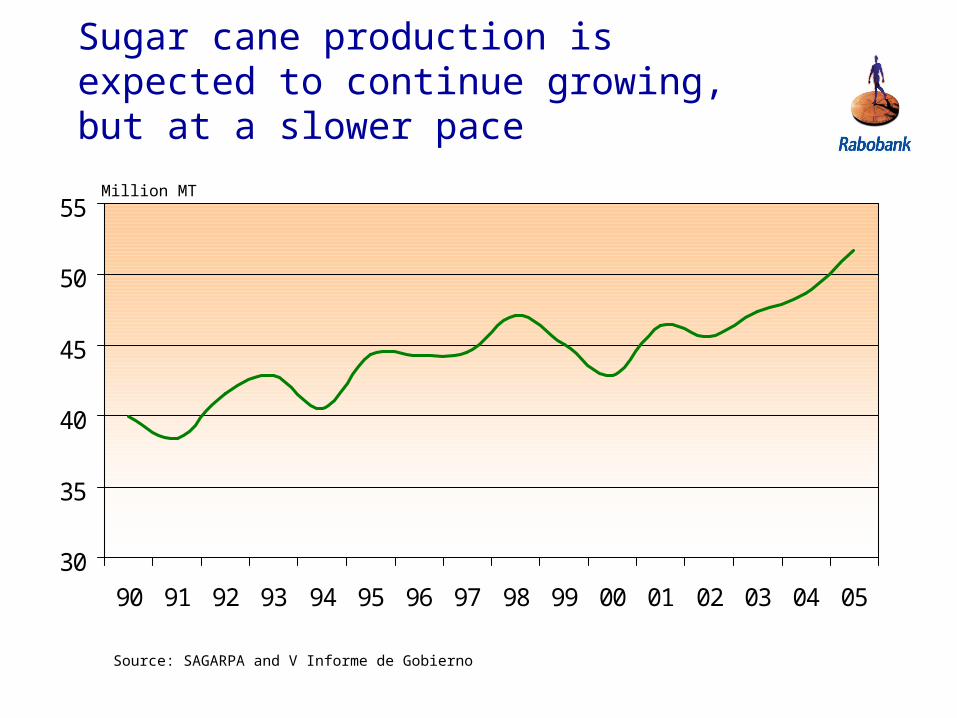

Sugar cane production is expected to continue growing, but at a slower pace

30

35

40

45

50

55

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

Source: SAGARPA and V Informe de Gobierno

Million MT

Recent growth in production has come from higher yields rather than expansion of harvested area

450

500

550

600

650

700

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 0564

68

72

76

80

Area harvested

Yield

‘000 ha. MT per ha.

Source: SAGARPA and V Informe de Gobierno

Sugar production is expected to grow moderately through the rest of the decade based on continued favorable prices

2,000

3,000

4,000

5,000

6,000

83 85 87 89 91 93 95 97 99 01 03 05 07p 09p

‘000 MT

Consumption and end-year inventory

0

1,000

2,000

3,000

4,000

5,000

6,000

84 86 88 90 92 94 96 98 00 02 04e

Consumption

Inventory

‘000 MT

Exports of fructose to Mexico from the U.S. rebounded last year

0

50

100

150

200

250

300

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

‘000 MT

Source: USDA .

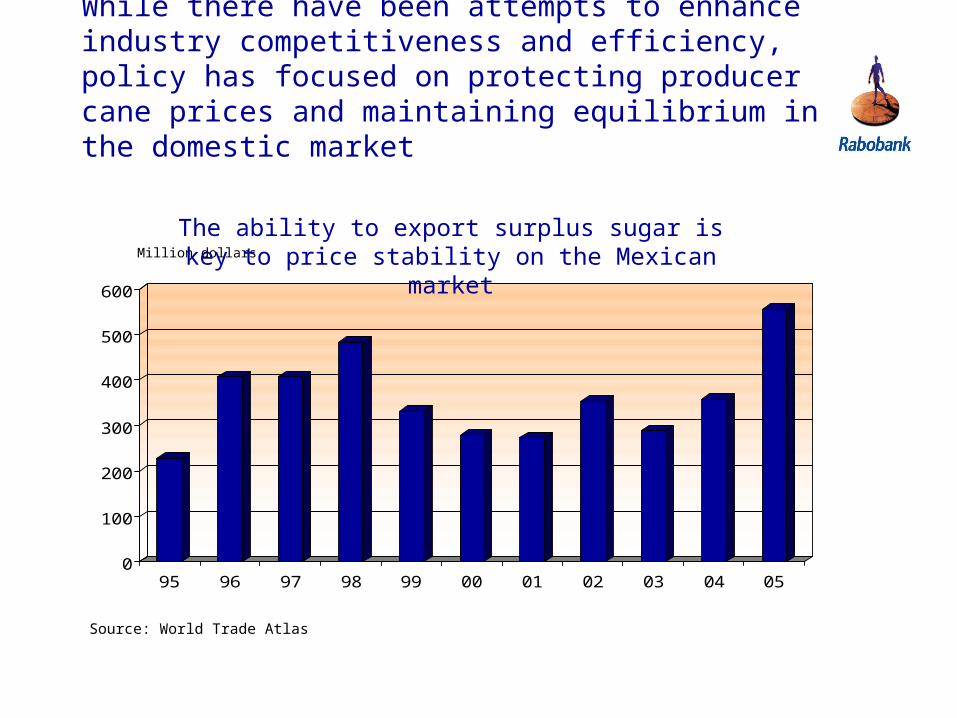

The ability to export surplus sugar is key to price stability on the Mexican market

0

100

200

300

400

500

600

95 96 97 98 99 00 01 02 03 04 05

Million dollars

Source: World Trade Atlas

While there have been attempts to enhance industry competitiveness and efficiency, policy has focused on protecting producer cane prices and maintaining equilibrium in the domestic market

0

100

200

300

400

500

600

95 96 97 98 99 00 01 02 03 04 05

Million dollars

Source: World Trade Atlas

The ability to export surplus sugar is key to price stability on the Mexican market

By the end of the decade Mexico will be looking to export at least 750,000 MT to maintain price stability on the domestic market

0

1,000

2,000

3,000

4,000

5,000

6,000

2006p 2007p 2008p 2009p 2010p

Exports

stocks

Consumption

‘000 MT

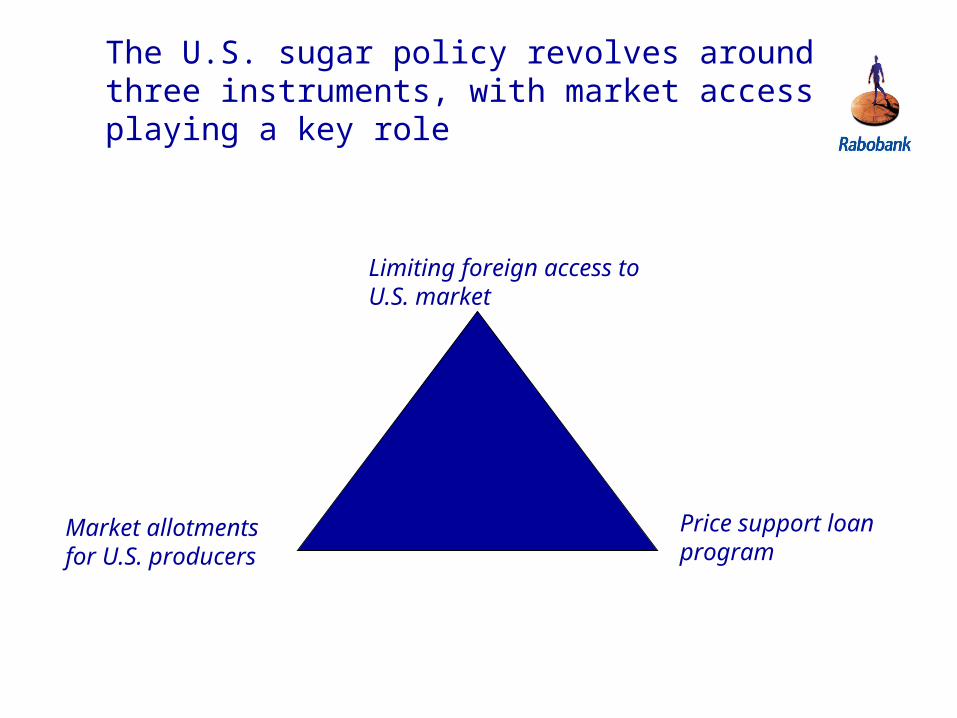

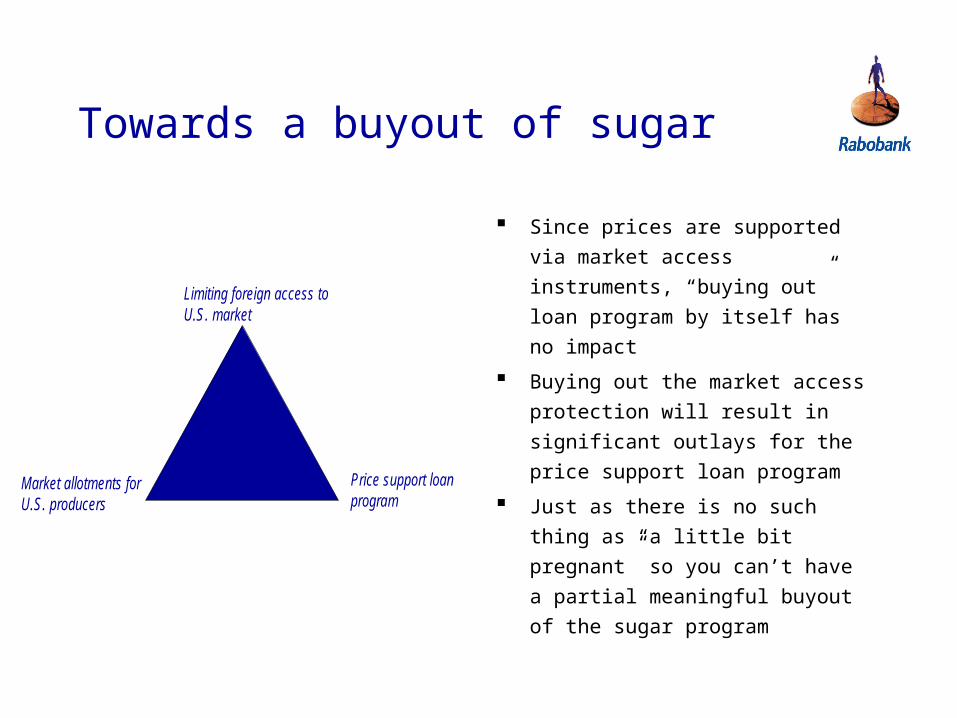

The U.S. sugar policy revolves around three instruments, with market access playing a key role

Limiting foreign access to U.S. market

Market allotments for U.S. producers

Price support loan program

Mexican and U.S. prices for raw sugar although reflecting different market and political conditions, tend to be relatively close

15

16

17

18

19

20

21

22

23

24

25

96 97 98 99 00 01 02 03 04 05 06

Mexico U.S.

US cents per pound

Sources: FORMA, “estándar” for Mexico, USDA for the U.S.

Mexican and U.S. prices for refined sugar are above world prices

0

5

10

15

20

25

30

35

40

45

96 97 98 99 00 01 02 03 04 05 06

Mexico U.S. World

US cents per pound

Sources: FORMA for Mexico, USDA for the U.S.

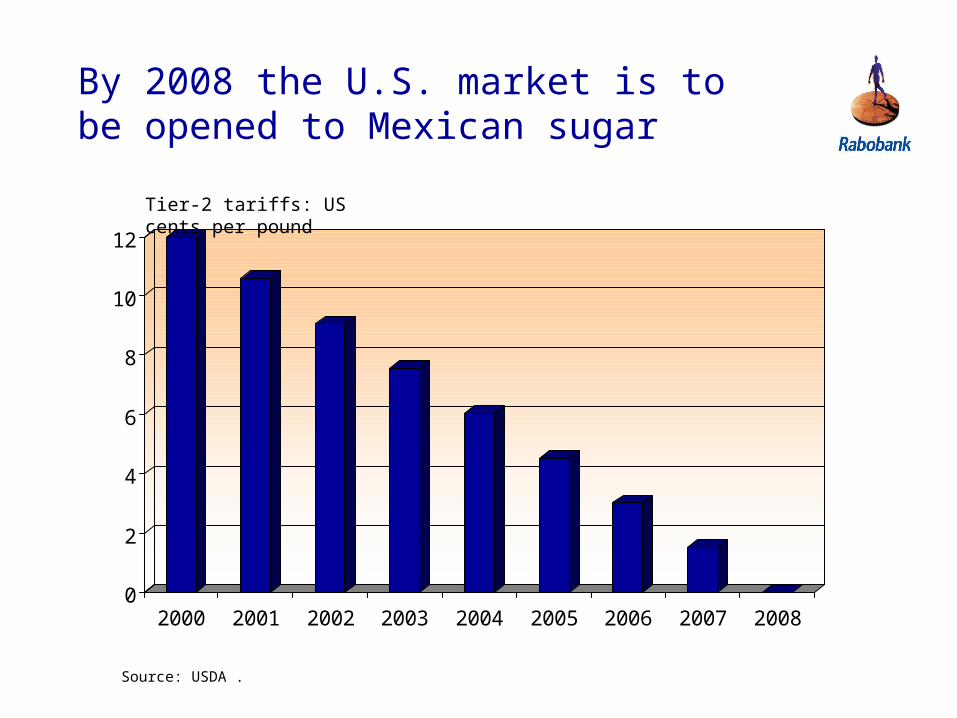

By 2008 the U.S. market is to be opened to Mexican sugar

0

2

4

6

8

10

12

2000 2001 2002 2003 2004 2005 2006 2007 2008

Tier-2 tariffs: US cents per pound

Source: USDA .

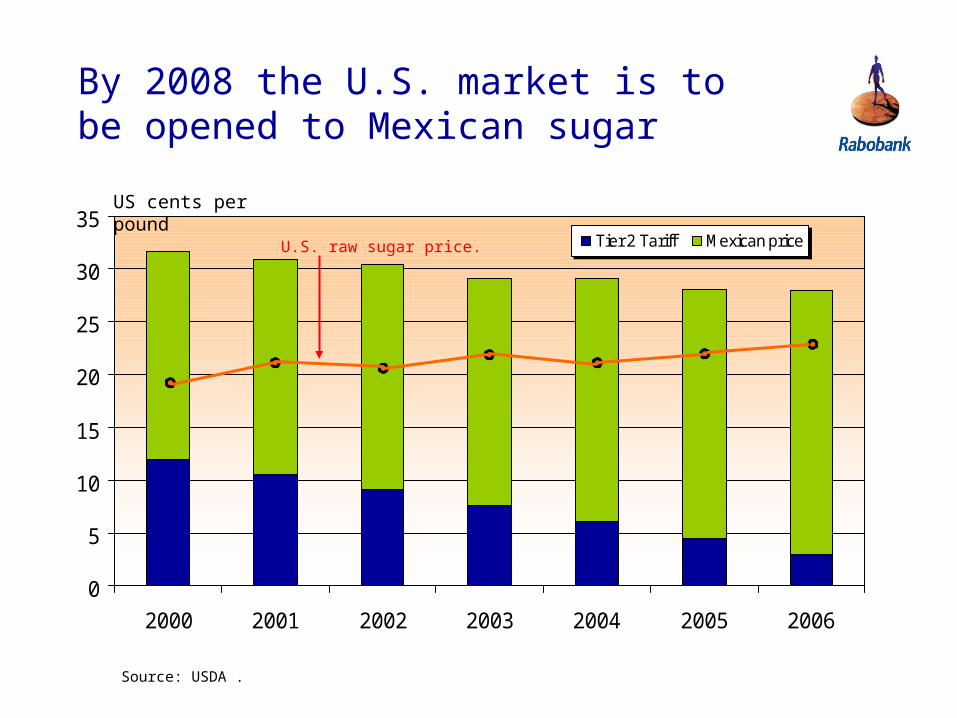

By 2008 the U.S. market is to be opened to Mexican sugar

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005 2006

Tier 2 Tariff Mexican price

Source: USDA .

U.S. raw sugar price.

US cents per pound

Effective price for Mexican sugar producers in the U.S. market: Mexican price less tier two tariff

0

5

10

15

20

25

2000 2001 2002 2003 2004 2005 2006*

Production costs

* March pricesSource: USDA for tariff, FORMA for Mexican prices

US cents per pound

So what will the U.S. do when facing additional and growing imports from Mexico?

0

1,000

2,000

3,000

4,000

5,000

6,000

2006p 2007p 2008p 2009p 2010p

Exports

stocks

Consumption

Renegotiate the NAFTA taking

sugar off the table and/or push a

NAFTA decision into the future}

Look for a non-tariff barrier to

keep Mexican sugar out of the

U.S.

Accept more Mexican sugar by

lowering the quota of third party

countries

Change U.S. sugar policy,

looking to a buyout-type scheme

‘000 MT

Towards a buyout of sugar

Since prices are supported via

market access instruments,

“buying out” loan program by

itself has no impact

Buying out the market access

protection will result in

significant outlays for the price

support loan program

Just as there is no such thing

as “a little bit pregnant” so you

can’t have a partial meaningful

buyout of the sugar program

Limiting foreign access toU.S. market

Market allotments for U.S. producers

Price support loan program

To buyout or not – that is the question

Government intervention is bad,

free markets are good

Makes trade negotiations easier

since sugar no longer problem

Favorable reception by non-sugar

agricultural groups with stake in

export market

Time is right – high world sugar

prices

Ethanol have potential to keep

sugar price high and divert corn

from HFCS

Cheaper sugar for consumers

Support domestic candy market

Sugar policy doesn’t cost government

anything – budgetary outlay

Doesn’t contemplate HFCS

Eliminate potential foreign policy

instrument (sugar quota)

U.S. is high cost producer and

importer – harm/destroy domestic

industry

If world prices remain high consumers

won’t get lower prices

The candy industry will move to lower

cost labor options

No immediate domestic political

benefits from sugar industry

Yes No

And if there is a buyout

Central America is happy Brazil is happy (something for nothing) Canada confectionary market loses

advantage And Mexico…

U. S.

ROW Mexico

Today

U. S.

ROW Mexico

Future

?

• U.S. imports cheap world sugar

• U.S. exports high cost domestic sugar to Mexico

• Tables turned on trade dispute as Mexico claims U.S. not self-sufficient and dumping sugar

Final thought

Market integration requires that policies should at least be analyzed and understood in terms of the impact that they will have on trading partners