the nutraceuticals battleground - fuld · the nutraceuticals battleground ... an accessible and...

TRANSCRIPT

Fuld & Company

20 Conduit Street | London W1S 2XW | UNITED KINGDOM

phone: +44 (0) 20.7659.6999 | fax: +44 (0) 20.7659.6998

Boston | London | Manila

www.fuld.com

Fuld Webinar | March 28, 2012

The Nutraceuticals Battleground Where Pharma and Consumer Companies Will Clash

Page | 2 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

Founded 1979; over 32 years of intelligence

Completed over 3,500 assignments worldwide

We wrote the book on competitive intelligence

We created industry training “gold standard”

About Fuld & Company

“…an accessible and practical handbook

for reframing the way you think about your

competitors,” – Business Week

Page | 3 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

The 2010 war game revealed that western companies will have to sell a some portion of their business to a Chinese entity in order to participate in the building of China’s Smart Grid.

Alliances to grow WiMax technology, Intel to enter mobile space through PC back door, 2008 The Battle for the Wireless Internet

Second Life will stumble, 2007 The Battle for the Virtual Community, Facebook will need a partner

News Corp revives with a combination of content and Net platform, Apple to introduce iTV, 2006 The Battle for Digital Entertainment Supremacy, LBS

News Corp revives with a combination of content and Net platform, Apple to introduce iTV, 2006 The Battle for Digital Entertainment Supremacy, LBS

Google and Microsoft pursue AOL, 2005 The Battle for Clicks, MIT-Harvard

The electronic medical records industry will see a great deal of consolidation in the coming months and years.

Previous War Game Predictions

Can you “game” the future? Highlights from a public war game:

The Battle for Designer Foods

Page | 5 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

War games vs long-term scenarios

Planning Horizon

Un

ce

rtain

ty o

r c

om

ple

xit

y

Scenario Futuring

War Game

Strategy Workshop

Where should

we play?

How should we play?

“Alternative

futures” possible

Range of players;

known

environment

Known

competitors, more

immediate issues

Page | 6 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

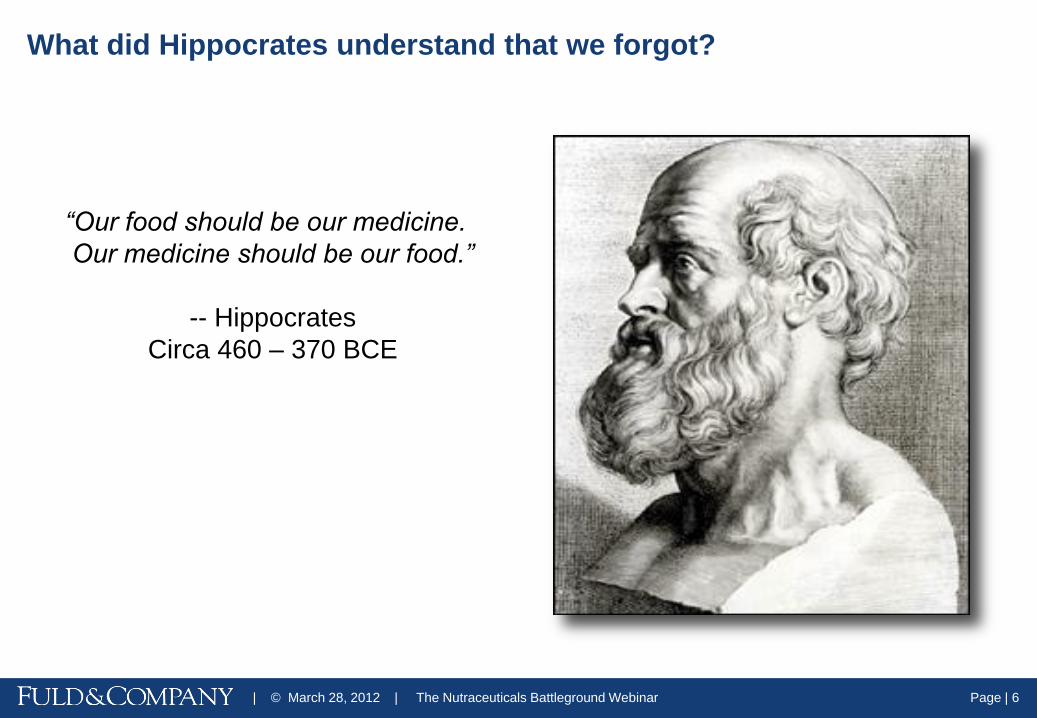

What did Hippocrates understand that we forgot?

“Our food should be our medicine.

Our medicine should be our food.”

-- Hippocrates

Circa 460 – 370 BCE

Page | 7 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

The market for designer foods deserves such a test

U.S. consumers are already

spending $20-30 billion/year

Today designer foods are

approximately 5% of the

overall U.S. market…it’s

projected to reach as much

as 20%

A challenge:

The nutrition industry has

done a poor job marketing

and communicating to

consumers the limitations of

functional foods and

beverages.

Page | 8 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

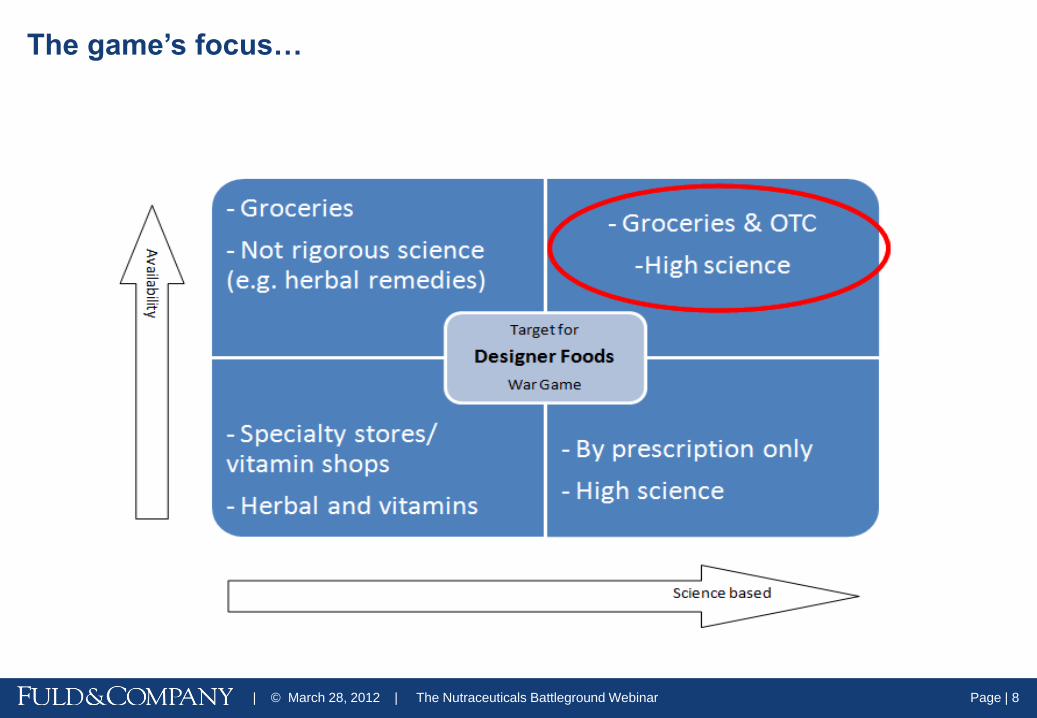

The game’s focus…

Page | 9 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

Team objectives…

3 year horizon…you know the players but may not

understand their strategies!

To articulate and define a strategy that within

the next three years will allow the your

company to both grow its designer foods

business in both the U.S. and in Western

Europe.

What were the predictions

AND

How did we get there?

Page | 11 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

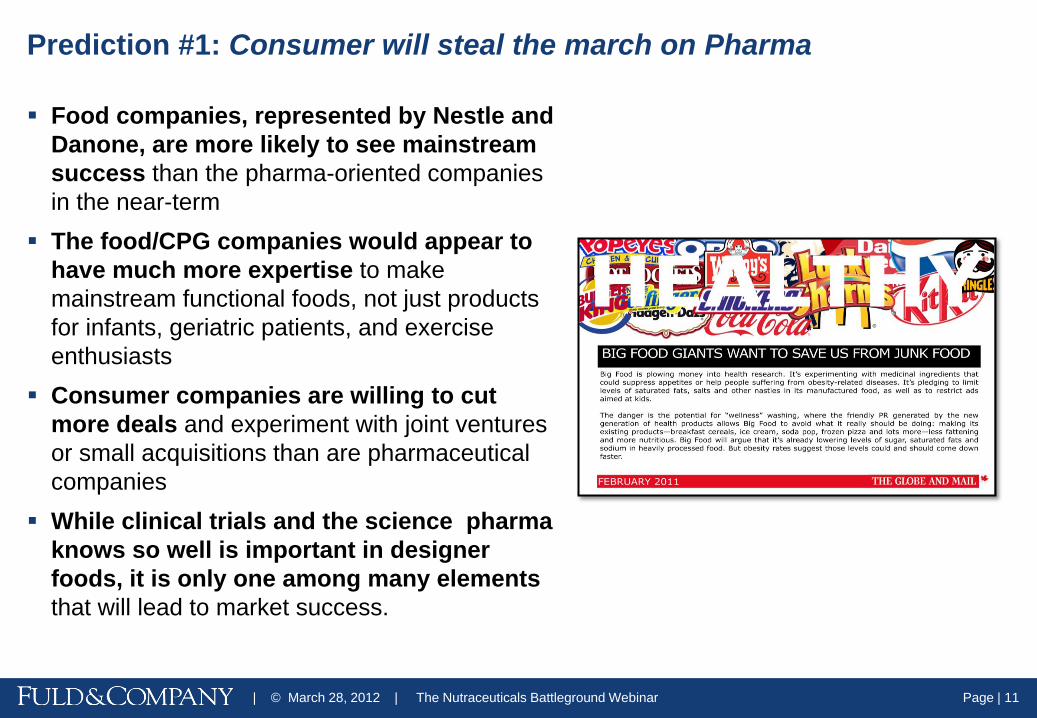

Food companies, represented by Nestle and

Danone, are more likely to see mainstream

success than the pharma-oriented companies

in the near-term

The food/CPG companies would appear to

have much more expertise to make

mainstream functional foods, not just products

for infants, geriatric patients, and exercise

enthusiasts

Consumer companies are willing to cut

more deals and experiment with joint ventures

or small acquisitions than are pharmaceutical

companies

While clinical trials and the science pharma

knows so well is important in designer

foods, it is only one among many elements

that will lead to market success.

Prediction #1: Consumer will steal the march on Pharma

Page | 12 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

Food companies could begin to

incorporate a variety of specialized

ingredients that are already available

– fish oils, plant sterols and stanols,

herbal extracts, vegetable and dairy

proteins, probiotic and other beneficial

bacteria.

CPG companies, especially the major

ones, have been very adept a micro-

segmentation, producing niche

products, accompanied by effective

branding – while pharma companies

have relied heavily on blockbuster

products.

Food/CPG companies are likely to

experiment a bit more than

pharmaceutical firms until something

big catches on

Prediction #2: “Measured steps,” not “high science” will win in the short term

Danone team talked

about “versioning” and

extending the Activia

brand.

The Nestlé team talked

about isolating Nestlé’s

chocolate image by using

other brands like Jenny

Craig, Power Bar, Gerber

Page | 13 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

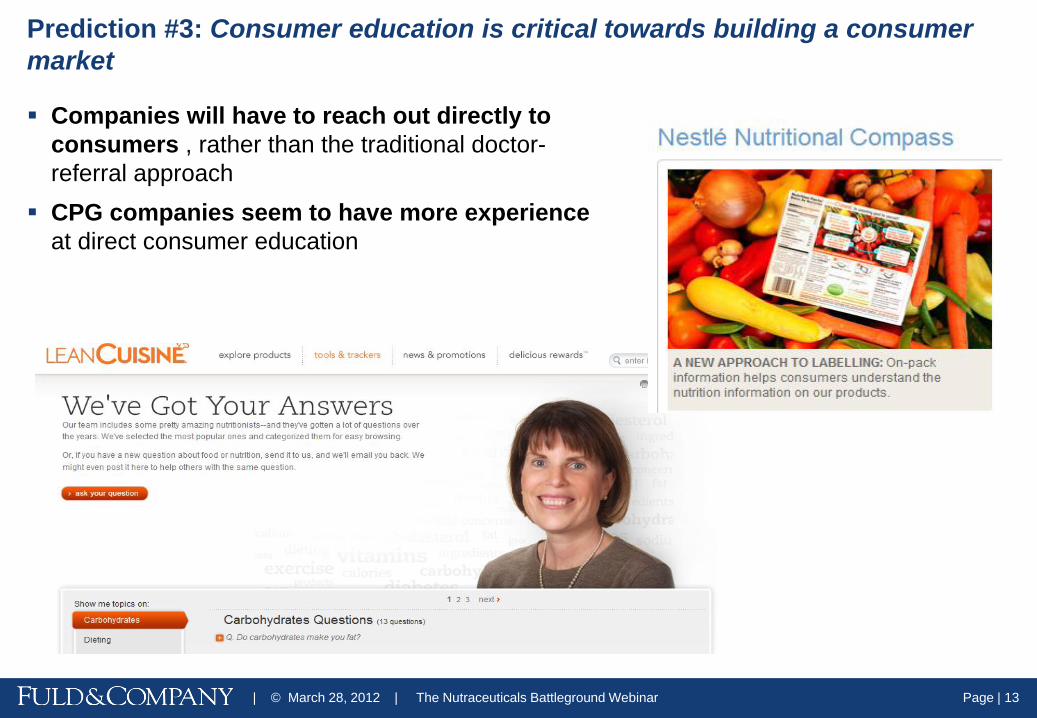

Companies will have to reach out directly to

consumers , rather than the traditional doctor-

referral approach

CPG companies seem to have more experience

at direct consumer education

Prediction #3: Consumer education is critical towards building a consumer

market

Page | 14 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

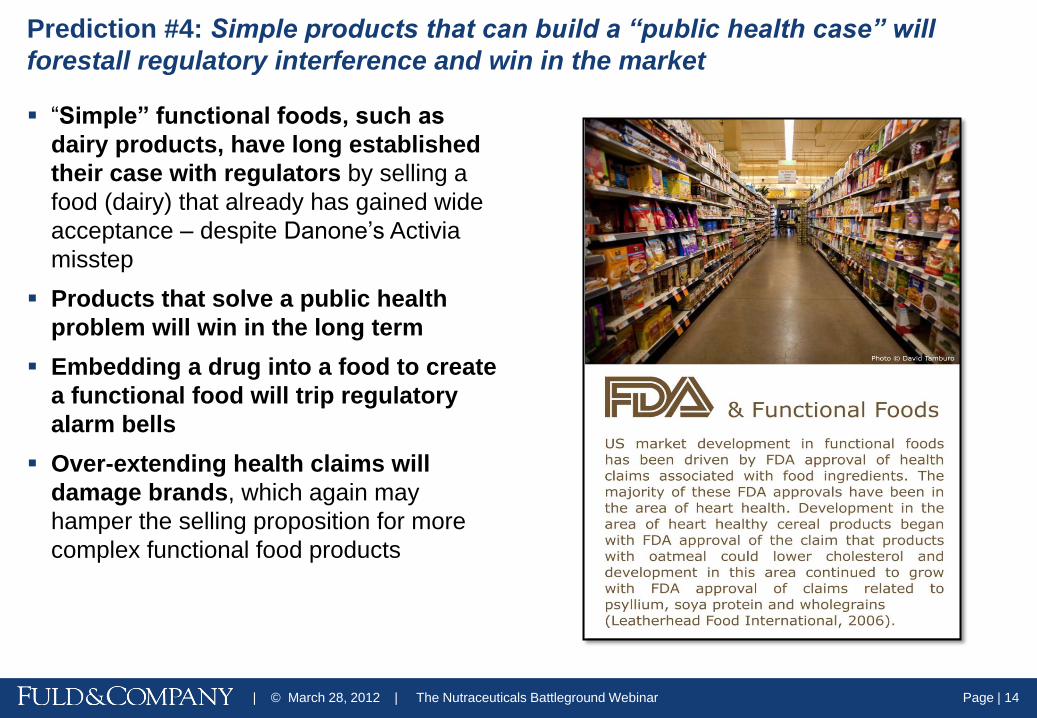

“Simple” functional foods, such as

dairy products, have long established

their case with regulators by selling a

food (dairy) that already has gained wide

acceptance – despite Danone’s Activia

misstep

Products that solve a public health

problem will win in the long term

Embedding a drug into a food to create

a functional food will trip regulatory

alarm bells

Over-extending health claims will

damage brands, which again may

hamper the selling proposition for more

complex functional food products

Prediction #4: Simple products that can build a “public health case” will

forestall regulatory interference and win in the market

Page | 15 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

Competitors will be forced to collaborate in

order to succeed – by building on each others

brands rather than acquire the brand in certain

cases (e.g. Unilever and Starbucks)

Companies must tap into “adjacencies” The

day of only-invented-here is over.

Breakthroughs will come through university and

government laboratory collaborations

(e.g. NIH)

Consumer package goods companies

realize they must acquire their way to

growth – and will do so at a rapid pace

Pharmaceutical companies are risk averse

to merging with a consumer brand,

concerned their science-based brands might be

damaged by CPG corporations

Prediction #5: Mergers will increase but collaboration is the hidden “trump

card”

Page | 16 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

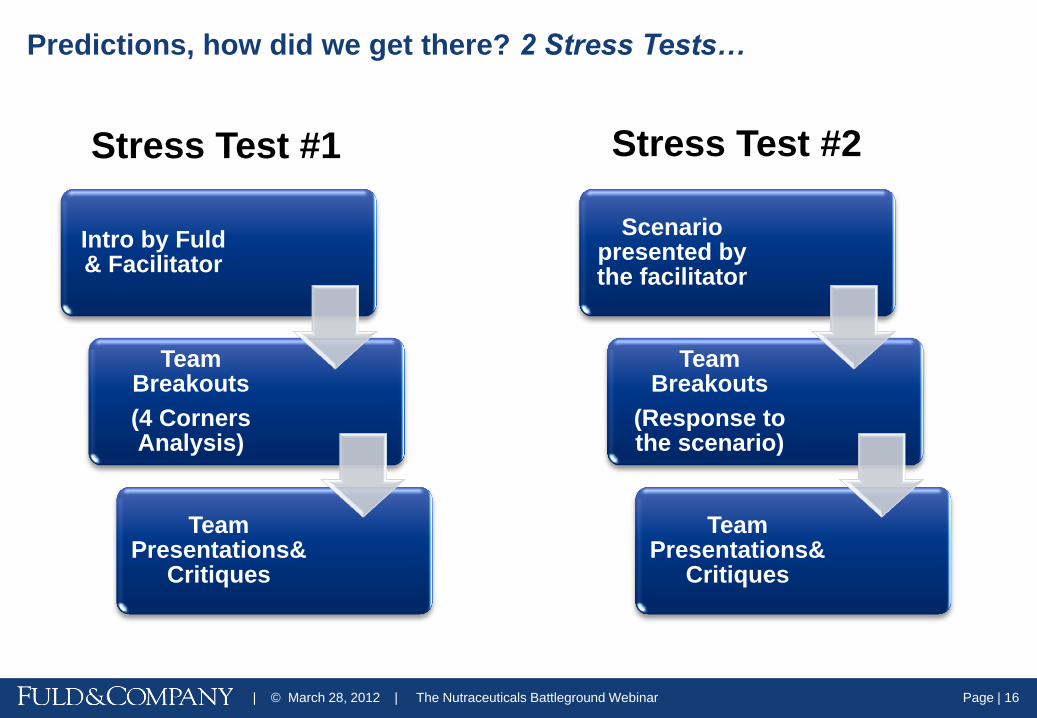

Predictions, how did we get there? 2 Stress Tests…

Intro by Fuld & Facilitator

Team Breakouts

(4 Corners Analysis)

Team Presentations&

Critiques

Stress Test #1

Scenario presented by the facilitator

Team Breakouts

(Response to the scenario)

Team Presentations&

Critiques

Stress Test #2

Round 1

Page | 18 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

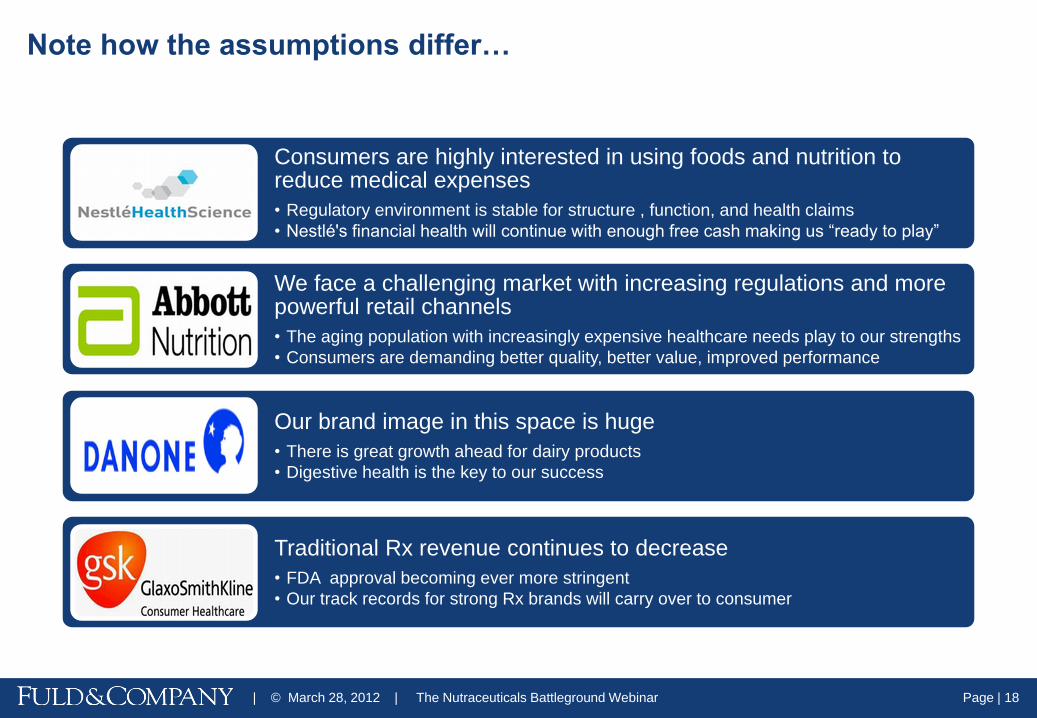

Note how the assumptions differ…

Consumers are highly interested in using foods and nutrition to reduce medical expenses

• Regulatory environment is stable for structure , function, and health claims

• Nestlé's financial health will continue with enough free cash making us “ready to play”

We face a challenging market with increasing regulations and more powerful retail channels

• The aging population with increasingly expensive healthcare needs play to our strengths

• Consumers are demanding better quality, better value, improved performance

Our brand image in this space is huge

• There is great growth ahead for dairy products

• Digestive health is the key to our success

Traditional Rx revenue continues to decrease

• FDA approval becoming ever more stringent

• Our track records for strong Rx brands will carry over to consumer

Page | 19 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

Abbott Danone

GSK Nestle

Moderate

May attempt to claim

ownership over

healthcare professional

channel, but does not

have the in-house taste

and food expertise

Little Overlap

May try to expand within

digestive niche and

claim ownership, but

Nestle could retaliate

Moderate

May compete for smaller

acquisition targets but

lack food/taste capabilities

to convert to market

winners and don’t have

nearly as much free cash

The combination of

Nestle’s size, financial

readiness, and taste

expertise, in

combination with high

science investments

are dominant

Chocolate vs. Science: How can Nestlé truly

offer a credible alternative to traditional

pharmaceuticals?

Are you just a bit too ambitious, expecting to

take this market in such a short timeframe? Do

you truly have the cash? Can you produce

winning [high science] functional food products

in such a relatively short period of time?

Nestlé believes it is in a “sweet spot”

Page | 20 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

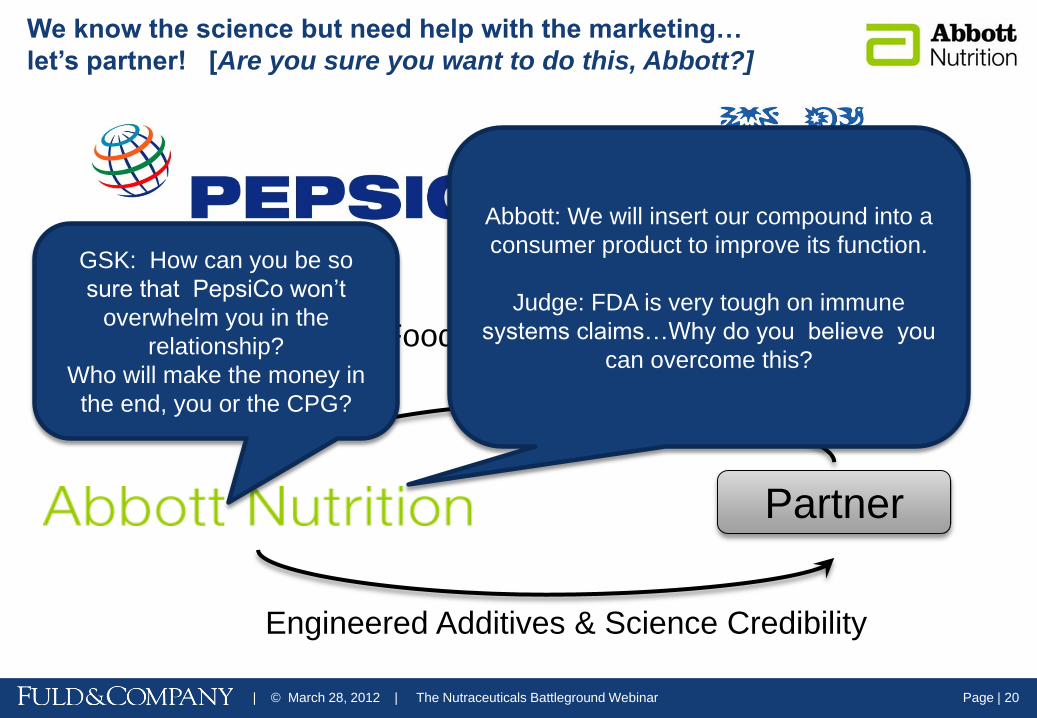

We know the science but need help with the marketing…

let’s partner! [Are you sure you want to do this, Abbott?]

Partner

Food Products & Brands

Engineered Additives & Science Credibility

GSK: How can you be so

sure that PepsiCo won’t

overwhelm you in the

relationship?

Who will make the money in

the end, you or the CPG?

Abbott: We will insert our compound into a

consumer product to improve its function.

Judge: FDA is very tough on immune

systems claims…Why do you believe you

can overcome this?

Page | 21 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

Enhance and Extend the Activia Brand

– Dairy Expansion

– Products

– Addressable Market

– Consumer Packaged Good Licensing

– Mute Activia Health Claims

Increase distribution of Danacol in the US and Western Europe

Medical Nutrition

– Pursue Partnerships with Pharmaceutical Companies

– Increase scientific evidence between diet and disease treatment

Danone will own the “comfort and quality” space…

BUT we must mute Activia claims!

Risk, risk, risk!

What pharmaceutical

company would partner with

you – and increase the risk

with your brand?

Page | 22 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

But you may already have the answer, Danone!

As we say in Cambridge (USA), it’s all about Mahketing.

Page | 23 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

Partner with food producer without science component (“GSK Inside” - Alli)

Refocus some R&D efforts onto nutritional healthcare space

Utilize high science to produce blockbuster products with high margins with high returns

Strategic acquisitions in therapeutic nutrition area

Future Strategy

How do you deal with

the failure of Avandia in

the diabetes space?

Does this not harm your

image?

Blockbusters are difficult

to imagine in the

functional foods market.

How do you intend on

accomplishing this?

Round 2

Page | 25 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

Pepsi announces dual acquisition of

Pfizer’s nutritional unit for $7 billion

and privately-held Agro Farma

(makers of Chobani yogurt) at an

undisclosed amount.

Page | 26 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

Proactively announce focus on nutritional science and shift of R&D resources

Creating compounds that are focused on particular health issues – big markets

In Western Europe – utilize existing nutritional products to build high science brands and

products

In US:

– License with food producer without science component (“GSK Inside” – Alli)

– Expand successful nutritional brands from Western Europe into US market and brand

them effectively

After brand creation focus on partnerships and/or JVs – Kraft as an example with large

reach

Future Strategy - Updated

“Alli Inside!” How do you know

consumers won’t overdose?

GSK: Weak response…”not talking

about active compounds”

Partnering with a consumer

company does make

sense…but only if we can

make “Alli Inside” work.

Page | 27 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

Snacks Drinks Dairy

Complete

Meal

Solutions

Nestle X X

GSK X

Danone X

Pepsi X X

Coke X

Unilever X X X X

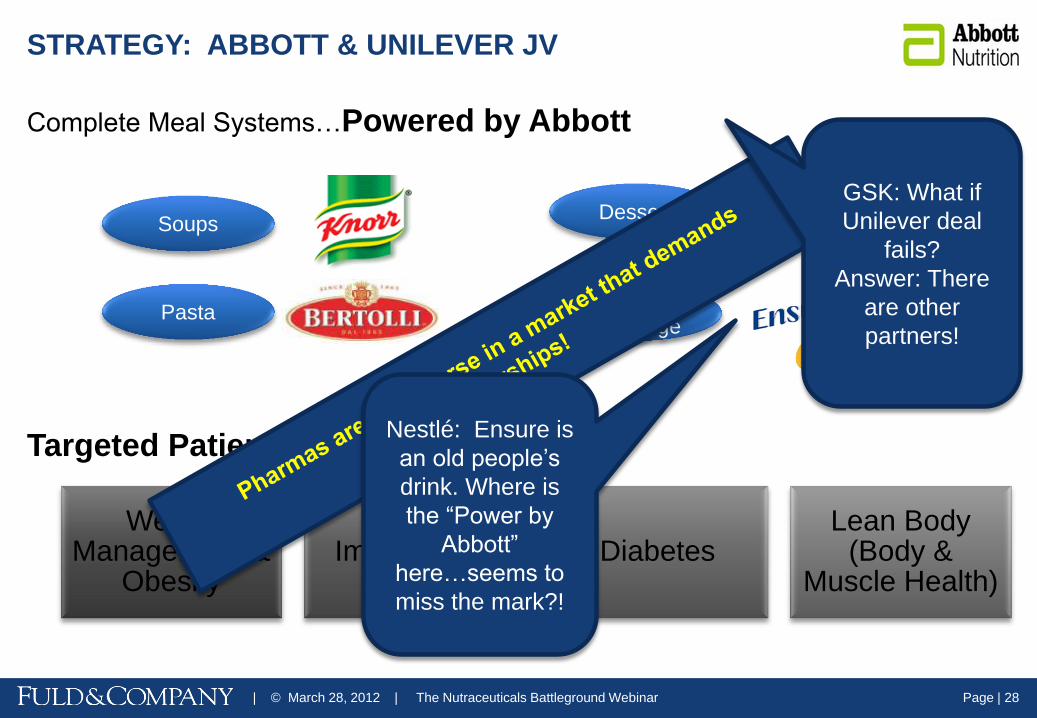

Abbott ponders who should be its partner…Unilever

Page | 28 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

Complete Meal Systems…Powered by Abbott

Targeted Patient Populations

STRATEGY: ABBOTT & UNILEVER JV

Soups

Pasta

Dessert

Nutrition

Beverage

Weight Management &

Obesity Immunology Diabetes

Lean Body (Body &

Muscle Health)

GSK: What if

Unilever deal

fails?

Answer: There

are other

partners!

Nestlé: Ensure is

an old people’s

drink. Where is

the “Power by

Abbott”

here…seems to

miss the mark?!

Page | 29 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

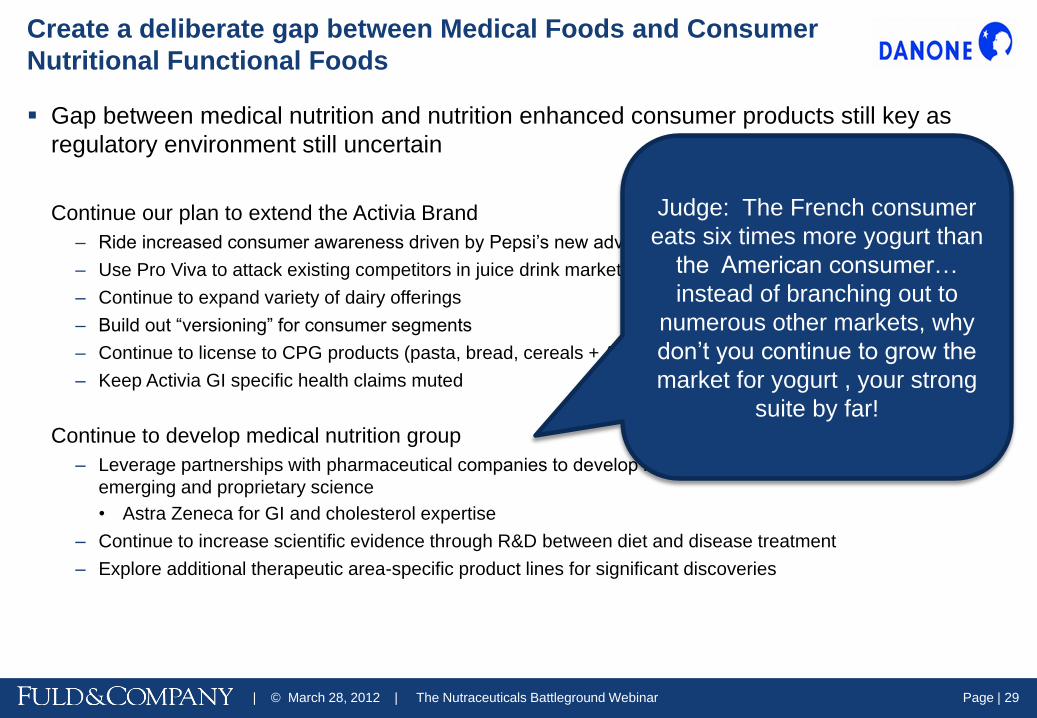

Gap between medical nutrition and nutrition enhanced consumer products still key as

regulatory environment still uncertain

Continue our plan to extend the Activia Brand

– Ride increased consumer awareness driven by Pepsi’s new advertising spend in dairy market

– Use Pro Viva to attack existing competitors in juice drink market in US

– Continue to expand variety of dairy offerings

– Build out “versioning” for consumer segments

– Continue to license to CPG products (pasta, bread, cereals + Activia / probiotic)

– Keep Activia GI specific health claims muted

Continue to develop medical nutrition group

– Leverage partnerships with pharmaceutical companies to develop novel “function” health claims that involve

emerging and proprietary science

• Astra Zeneca for GI and cholesterol expertise

– Continue to increase scientific evidence through R&D between diet and disease treatment

– Explore additional therapeutic area-specific product lines for significant discoveries

Create a deliberate gap between Medical Foods and Consumer

Nutritional Functional Foods

Judge: The French consumer

eats six times more yogurt than

the American consumer…

instead of branching out to

numerous other markets, why

don’t you continue to grow the

market for yogurt , your strong

suite by far!

Page | 30 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

Nestlé is aggressive acquirer/partner!

Analogs:

• Over 100 acquisitions has

yielded largest market cap and

leadership in high-growth tech

and networking platforms

• Danaher spent approx $2B on 18 strategic

acquisitions, and now has a $4B medical

technologies segment

• Imposes the “Danaher Business System”

• 25% return to shareholders over 20 yrs

Aggressive M&A for bolt-on

companies with technology

that Nestle could add value to

immediately (i.e. taste)

Continue to build internally

with existing R&D; act as

internal incubator of

innovations

Leverage Nestle resources to

fuel IP development of

potential innovators, then

consider acquisition

Page | 31 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

When is “high science” too high for today’s market – pushback on Nestlé

Page | 32 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

What core competencies will each side (pharma and cpg) need to tap into in order to

succeed in this market? Have any managed to do this to date? If so, how have they

managed this?

Which functional food categories are likely to become the big sellers?

What consortia need to form in the functional foods arena? Which companies or

government agencies are willing to join such a group?

Can consumer companies, such as Danone create breakout products in the next few

years and build a portfolio beyond dairy products?

Where are the major players investing their R&D monies in functional foods?

What are some of the “hidden” companies corporate development teams are building

relationships with via in-licensing or co-branding efforts?

What role with retail channels play in picking the winners and what will it take for

producers to beat their competition in gaining shelf space in the next few years?

The war game introduced a number of outstanding questions:

Page | 33 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

The War Game Succeeded Because…

Page | 34 | © March 28, 2012 | The Nutraceuticals Battleground Webinar

Thank you for your participation

Fuld & Company

AMERICAS | 25 First Street, Suite 301 | Cambridge, MA 02141 | USA | Phone +1 617.492.5900 | Fax +1 617.492.7108

EUROPE | 20 Conduit Street | London W1S 2XW | United Kingdom | Phone +44 (0) 20.7659.6999 | Fax +44 (0) 20.7659.6998

ASIA PACIFIC | 1206 AIC Burgundy Tower | ADB Avenue | Ortigas Center, Pasig City | Philippines | Phone +63 (2) 706.3292

www.fuld.com

Leonard Fuld

President

Jeanne LaFrance

Senior Vice President