the operating costing on hotel,hospital & transport

TRANSCRIPT

[1]

Project Report on

THE OPERATING COSTING ON HOTEL, HOSPITAL

& TRANSPORT

Submitted by

HEMANT DHANRAJ SONAWANE

MASTERS IN COMMERCE SEM-II

(ADVANCE ACCOUNTANCY)

ACADEMIC YEAR 2013-2014

Roll No.6272

Submitted to

UNIVERSITY OF MUMBAI

MULUND COLLEGE OF COMMERCE

S.N ROAD, MULUND (W)-MUMBAI 400 080

[2]

DECLARATION

I, Mr. HEMANT DHANRAJ SONAWANE, the student of MULUND

COLLEGE OF COMMERCE, S.N Road, Mulund (W), Mumbai 400 080,

studying in M.Com part-I (ADVANCE ACCOUNTANCY) here by declaring that

I have completed this project “THE OPERATING COSTING ON HOTEL,

HOSPITAL & TRANSPORT” during the academic year 2013-14. The

information submitted is true and original of best of my knowledge.

Date: Signature:

Place: MUMBAI

[3]

CERTIFICATE

I, Prof. M. S. GANAGI, here by certify that Mr. HEMANT DHANRAJ

SONAWANE of MULUND COLLEGE OF COMMERCE, S.N Road,

Mulund (W), Mumbai 400 080, studying in M.Com part-I (ADVANCE

ACCOUNTANCY) here by declaring that I have completed this project “THE

OPERATING COSTING ON HOTEL, HOSPITAL & TRANSPORT”

during the academic year 2013-14. The information submitted is true and

original of best of my knowledge.

Signature: (Project Guide) Signature (Principal)

Signature: (Co-Ordinator) Signature: (External Examiner)

[4]

ACKNOWLEDGEMENT

I would like to express my sincere gratitude to Principal of Mulund College of

Commerce DR. (Mrs.) Parvathi Venkatesh, Course - Coordinator Prof. Rane and our

project guide Prof. M. S. GANAGI, for providing me an opportunity to do my project

work on “THE OPERATING COSTING ON HOTEL, HOSPITAL & TRANSPORT”.

I also wish to express my sincere gratitude to the non - teaching staff of our college.

I sincerely thank to all of them in helping me to carrying out this project work. Last

but not the least, I wish to avail myself of this opportunity, to express a sense of

gratitude and love to my friends and my beloved parents for their mutual support,

strength, help and for everything.

Date: Name: HEMANT DHANRAJ SONAWANE

Reg. No. Signature:

[5]

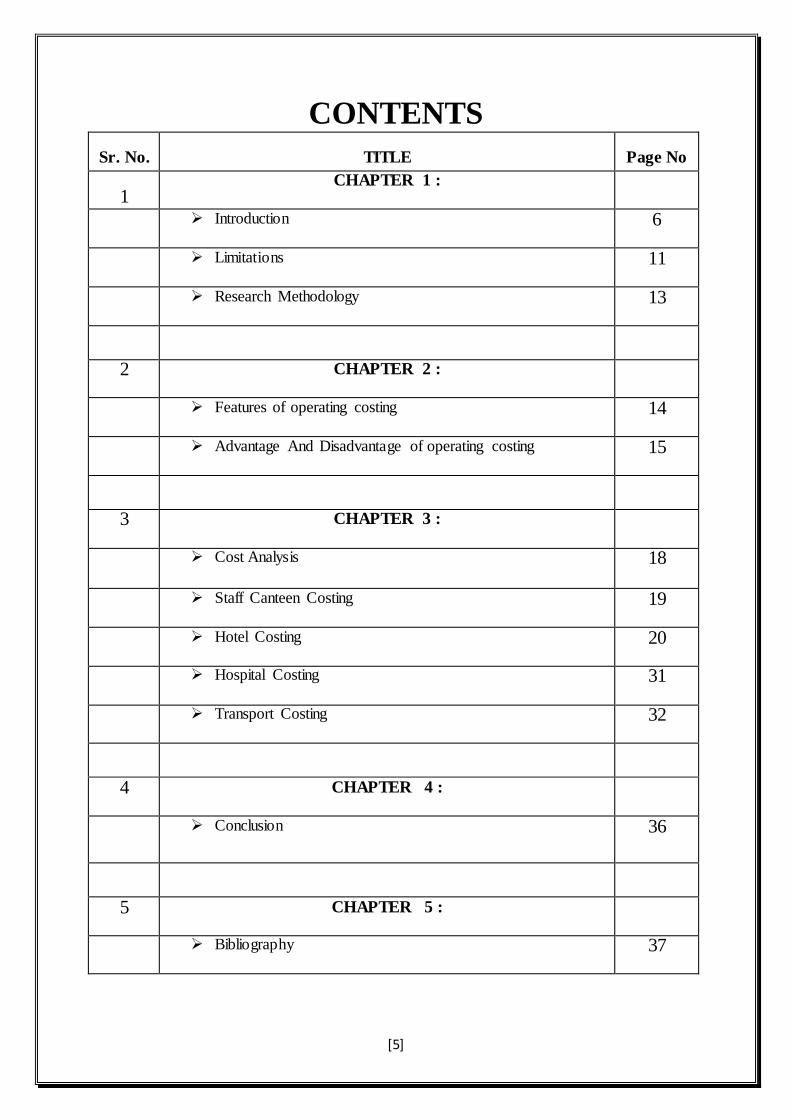

CONTENTS

Sr. No. TITLE Page No

1 CHAPTER 1 :

Introduction 6

Limitations 11

Research Methodology 13

2 CHAPTER 2 :

Features of operating costing 14

Advantage And Disadvantage of operating costing 15

3 CHAPTER 3 :

Cost Analysis 18

Staff Canteen Costing 19

Hotel Costing 20

Hospital Costing 31

Transport Costing 32

4 CHAPTER 4 :

Conclusion 36

5 CHAPTER 5 :

Bibliography 37

[6]

CHAPTER 1

INTRODUCTION

OPERATING COSTING

MEANING

OPERATING COSTING is the method used to ascertain the cost of providing a service

such as transport, hotel, hospital, gas, or electricity. Operating cost denote the cost of

providing a service as opposed to cost of manufacturing a product. CIMA has defined

operating costing as that form of operation costing which applies when standardize service

are provided either by an undertaking or by a service cost centre within an undertaking. Cost

accounting standard -1 by ICWA define operating cost as the cost incurred in conducting a

business activity. Operating cost refer to the cost of undertaking, which do not manufacture

any product but which provide service.

DEFINITION

The day-to–day expenses incurred in running a business, such as sales and administration, as

opposed to production .Also called operating expenses. These are recurring expenses in

operating the business. The expenses can include property maintenance, taxes, and wages.

[7]

APPLICATION:

Operating costing is employed in different types of service industries such as

Transport service e.g. truck operator, road transport, railway, air-line etc.

Municipal service like road maintenance, garbage disposal, street lighting etc.

Supply service such as electricity, steam, gas, water etc.

Welfare service e.g. canteen, hospital, library etc.

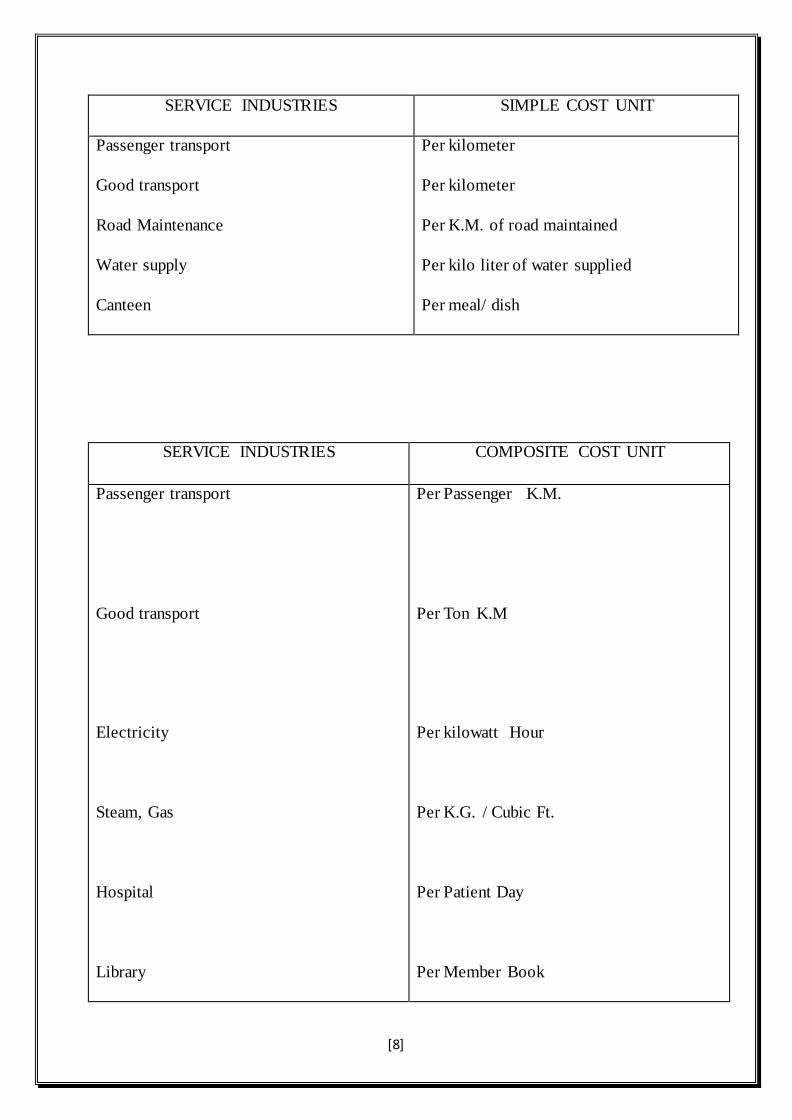

COST UNIT:

For ascertaining cost it is necessary to decide suitable cost unit for each types of

service industry. Basically, operating costing is a types of process costing. Thus it

used the method of process costing when ascertaining the cost of supply of electricity,

steam etc. however, sometime operating costing may adopt a particular job as a unit of

cost as for example when costing a particular trip by a bus so as to quote the charger.

In such cases operating costing used the method of job costing by treating a specific

trip as a separate job. A cost unit under operating costing may be of two types (a)

simple cost unit (b) costing cost unit. Following is the list of different cost unit used in

different types of service.

[8]

SERVICE INDUSTRIES SIMPLE COST UNIT

Passenger transport

Good transport

Road Maintenance

Water supply

Canteen

Per kilometer

Per kilometer

Per K.M. of road maintained

Per kilo liter of water supplied

Per meal/ dish

SERVICE INDUSTRIES COMPOSITE COST UNIT

Passenger transport

Good transport

Electricity

Steam, Gas

Hospital

Library

Per Passenger K.M.

Per Ton K.M

Per kilowatt Hour

Per K.G. / Cubic Ft.

Per Patient Day

Per Member Book

[9]

Thus it can be seen that in operating costing in most cases the cost unit is a compound unit. It

refer to both the quantum of service and period of service. Thus a transport charge for

carrying so much weight (Ton) for so much distance (Km) an electricity company charge one

for use of both the quantum (Kilowatt) and the period (Hour) and so on.

PROCEDURE:

1) DETERMINE COST UNIT: The first in operating costing is the determination of

the cost unit. This is a complex task as explained in para 1.3.

2) ASCERTAIN COST: The next point to be notes is that operating cost are period

cost. The cost of supplying the service for a period are ascertained in the following

manner(taking the example of a transport)

VEHICLE NO.: Each vehicle is treated as accost centre and given a specific number.

All the cost account against this number. A separate account is opened to record the

cost and income of each vehicle.

VARIABLE COST: Variable cost are the running and operating. This included

expenses of variable nature e.g. petrol, diesel, lubricating oil, grease etc. the material

requisition note and time sheet (or Log) bears the vehicle no. the relevant vehicle

account is debited with it direct material and direct labour cost. Direct expenses such

as a fuel are debited to vehicle account on the basic of log book and the cash /

purchase / journal vouchers.

FIXED COSTS: Fixed cost (fixed charge) included garages rent, insurance, road

license fees etc. the fixed charges are apportioned and absorbed by each vehicle no.

[10]

on the basic of overhead absorption rate which may be actual or pre determine. The

fixed cost attributable to the vehicle are debited to the relevant vehicle account.

REVENUE: The revenue from the vehicle is credited to the vehicle account.

PROFIT OR LOSS: the vehicle account at this stage will reveal the profit or loss

made on operating that vehicle. The profit or loss is then transfer to the costing profit

and loss account the total operating cost of a period is divided by the number of cost

unit (KM/Passenger/ Ton)supplied during the period to arrive at the operating cost Per

unit for that period.

3) NO STOCK: In case of a service industry there is no question of any closing stock or

work-in-progress since it is not possible to store a service for future use.

4) ABNORMAL COST: According to cost accounting standard 5 (transportation

cost)abnormal and non recurring cost shall be directly debited to p&l a/c and shall not

form part of operating cost. Example are penalty, detention charge demurrage and

cost related to abnormal breakdown.

[11]

LIMITATIONS

OPERATING COST ACCOUNTING HAS CERTAIN LIMITATIONS

a)Based on estimates: Indirect costs are not charged fully to a product or process. It is

charged to all the products and processes on the basis of estimates. Actual cost varies from

estimated cost. Due to these limitations, all cost accounting results are taken as mere

estimates.

b)Lack of uniformity: Procedures of cost accounting followed by different organizations are

different for different products. There is no uniformity. There is also possibility of

difference in pricing material issues for production. All these lead to different cost results for

the same operation.

c)Many conventions: There are many conventions for classification of costs, pricing of

material issues, apportionment of indirect costs, adoption of marginal or standard cost, etc.

These create difficulty in determining the exact cost, because no one type of cost is suitable

for all. Purposes and in all circumstances.

d)Expensive: Cost accounting is expensive. It involves lots of clerical won for maintaining

various costing records for different purposes. For medium and small size concern, the

benefit derived from costing system may not justify the cost involved.

[12]

e)Result requires reconciliation: Information and results provided b;financial accounting and

cost accounting may be different for the as activity. This requires reconciliation to find out

correctness of the two before taking any decision.

f)Dependent: It is not an independent system of accounting. It depends on other accounting

systems.

g)Does not include all items of expense and income: Items of purely financial nature such as

interest, financial charges, discount and loss on issue of shares and debentures, etc. are not

taken into consideration in Cost Accounting.

h)Not an exact science: Like other accounting system, it is not an exact] science but an art

that has developed through theories and practices.

[13]

RESEARCH METHODOLOGY

One important aspect of analyzing cost data is the challenge of how to present the

findings in a manner that potential users may be able to apply to their own settings.

Consequently, a key question underlying the development of this report is: who are the

potential users of operating cost information and how will the information be used?

Since this analysis has been motivated by informational needs of provincial Ministries

of health, the analysis below assumes that the primary users of the findings will be provincial

Ministries of health and other significant purchasers of health care services, such as the B.C.

Health Services Purchasing Organization (HSPO).

This analysis assumes that the primary users of the methods and findings regarding

operating costs of hospitalizations will be provincial Ministries of health and other significant

purchasers of health care services.

[14]

CHAPTER 2

FEATURES OF OPERATING COSTING

THE MAIN FEATURES OF OPERATING COSTING ARE AS

FOLLOWING

(1) The undertaking which adopts service costing does not produce any tangible goods.

These undertakings render unique services to their customers.

(2) The expenses are divided into fixed and variable cost . Such a classification is necessary

to ascertain the cost of service and the unit cost of service.

(3) The cost unit may be simple or composite. The examples of simple cost units are cost per

unit in electricity supply , cost per liter in water supply, cost per meal in canteen etc.

Similarly cost per passenger kilometers in transport cost per patient-day in hospital, cost per

room-day in hotel etc. are the examples of composite cost unit.

(4) Total cost are averaged over the total amount of service rendered.

(5) Costs are usually computed period-wise. However, in the case of utilization of vehicles,

use of road-rollers etc., the costs are computed order wise.

(6) Service costing can be used for service performed internally or externally.

(7) documents like the daily log sheet, cost sheet etc. are used for the collection of cost data.

[15]

ADVANTAGES & DISADVANTAGES OF OPERATING

COSTING

ADVANTAGES OF OPERATING COSTING:

1. Invest in more training for your employees. Wait-isn't this article about reducing

operating expenses? Well, it is. Investing in more training for employees will reduce

the number of errors that are made, which will inevitably save money for the

company. Not only that, but investing more in your employees will show them that

they are valued. In return, they will be more engaged and produce more (and better)

work.

2. Cut office supply expenses. Reducing supply expenses can significantly reduce your

operating expenses and improve your bottom line. This can be done by going from

paper to electronic whenever possible or ordering supplies in bulk in order to obtain

discounts. In addition, if you purchase all of your supplies at the same outlet, you may

be able to negotiate a better price. At the very least, shop around for lower prices and

any loyalty programs offered by potential suppliers.

3. Cut out travel and entertainment expenses. Although T & E expenses are considered a

"perk," during tough times, these are expenses a business can do without. Instead of

traveling to business meetings, hold conference calls or meetings online. Also, try not

to spend funds on company outings, meals, or other entertainment.

[16]

4. Rent or lease equipment as opposed to purchasing new equipment. Leasing business

equipment and tools preserves capital and provides flexibility. According

to Nolo.com, a legal advice website, the primary advantage of leasing business

equipment is that it allows businesses to acquire assets with minimal initial

expenditures. In addition to this, leasing offers the benefits of improved cash flow, tax

advantages, flexible terms, and the ability to easily upgrade equipment.

5. Reduce marketing and advertising expenses. Business magazine and

websiteEntrepreneur.com suggests that business owners "split advertising and

promotion costs with neighboring businesses. Jointly promote a sidewalk sale, or take

your marketing alliance further by sharing mailing lists, distribution channels and

suppliers with businesses that sell complementary goods or services." If you are

advertising via television or radio ads, look for cheaper time slots as another option.

6. Reduce your staff-well, sort of. This doesn't necessarily mean completely laying off

your workers. Instead, consider rehiring your workers on a contract basis as a

temporary employee. This could save you money on salary expenses as well as

employee benefits until the business gets back on track and is able to rehire workers

on a permanent basis.

[17]

7. Outsource administrative functions. Consider outsourcing functions such as your

accounting and payroll to help reduce your business expenses. This will give you more time

to focus on building your business and costing projects, while possibly reducing the expense

of these functions if you are able to outsource them for cheaper than performing them within

your business.

While cutting expenses may seem like something to do temporarily to maintain your

business, actually implementing these ideas when revenues are increasing will continue to

help your business generate the most profitability possible.

DISADVANTAGES OF OPERATING COSTING:

Start-up businesses are typically more costly and risky since there is no proven

formula.

In order to obtain capital to fund the business, a lengthy detailed business plan must

be put together.

All of the details of starting the business, including licenses, marketing, naming the

business, finding product sources, etc. are the responsibility of the owner

[18]

CHAPTER 3

COST ANALYSIS

The costs incurred in departments rendering services or service organizations are grouped

under the following heads:

1. Fixed or standard charges

2. Semi-fixed or maintenance charges

3. Variable or running charges

To ascertain the cost per unit, these charges are aggregated and divided by the number of

service units during the specified period.

Cost per unit = total cost during the period

Number of service unit during the period

Determination of cost per unit serves the following purposes:

1. It is used for price fixation.

2. It is used for cost control

[19]

STAFF CANTEEN COSTING

Most of the factories have canteens for staff. They are subsidized either partly or wholly. It is

manned by a supervisor who is responsible for running it. The supervisor is accountable to

the works manager or personnel manager. The major accounting headings are

(i) provisions,

(ii) services,

(iii) labor,

(iv) consumable stores and

(v) miscellaneous overheads.

Cost per meal can be calculated on the number of meals served; for other items such as

snacks, on the number of snacks served, and tea/ coffee: no. of tea or coffee served.

A specimen of operating cost statement for a canteen is shown as follow

[20]

HOTEL COSTING

Hotel industry is a service industry and covers various activities as provision for food and

accommodation and providing other comforts like recreation, business facilities, shopping

areas for shopping facilities. In order to provide the service, hotel industry is required to incur

various expenses. Expenses may be fixed or variable. Fixed expenses comprise staff salaries,

repairs and renovations, interior decoration, laundry contract cost, sundries and depreciation

on fixed assets, variable expenses include lighting charges, attendants salaries and power

charges

In order to calculate the room rent to be charged per person, notional profit is added in the

total operating cost and divided by the number of rooms available. The numbers of rooms

available are calculated after taking into consideration various categories of suite, various

seasons and occupancy percentage.

[21]

ELECTRICITY GENERATION

Power houses engaged in electricity generation or steam generation use ‘Power House

Costing.’ Operating cost statement can be prepared by identifying the costs associated with

the power generation or steam generation. Cost unit is different for electricity generation and

steam generation. For electricity generation, cost unit is cost per kilowatt-hour while for

steam it is lb

EXPENSE ACCOUNT

An expense account typically ties to an item making a company spend money, but there also

are non-cash cost accounts that reduce the organization’s income. If you hear finance people

using terms such as cost, expense, charge and outlay, just note they’re referring to the same

thing. Expense accounts run the whole operating gamut, from merchandise cost and interest

to selling, general and administrative outlays. Think of SG&A outlays as anything from rent

and litigation to insurance, office supplies, travel and business entertainment. Non-cash

expense accounts include depreciation, amortization and depletion.

DATA REPORTING

Operating accounts constitute the conceptual fulcrum around which an organization builds its

bookkeeping and financial reporting practices. These accounts help the business publish accurate,

complete financial data summaries at the end of a given period -- say, a month, quarter or fiscal

[22]

year. A full set of accounting reports includes a balance sheet, an income statement, an equity

statement and a cash flow statement.

OPERATING COSTING—MANAGEMENT CONTROL

The operating activity encompasses all the management functions involved in the day-to-day

performance of organizational tasks and missions. As such, it is primarily a lower-echelon

function and is, therefore, of considerable importance to wing/base level managers. In fact, it

can be said that the preponderant portion of a wing/base-level manager’s efforts are expended

in the operating activity. In this regard, many if not most management actions are concerned

primarily with operational effectiveness, mission accomplishment, and the like—

considerations which do not necessarily require cost data. Nevertheless, there are two areas of

operating activity in which managers use cost information: management control and decision-

making.5

In essence, management control is the function of ensuring that management plans and

policies are implemented as intended.6 In performing this function, cost information can help

in three important ways: it can serve as a means of communication; it can be used to

motivate; and it can be used as a yardstick of appraisal.

COMMUNICATION

The communicating role of cost data is inherent in the data themselves. Their very existence

constitutes a record of some activity, and the simple act of transmittal constitutes a report, be

it formal or informal. Perhaps it is this characteristic of cost information that is responsible

[23]

for the interest in cost information for its own sake. A cursory consideration of the

communicating role of cost data could lead to the erroneous argument that, since any and all

cost information by its very nature constitutes a record and/or report, any and all cost

information is of use to management. This argument, however, ignores one of the basic

precepts of communication: to be effective, any communication must convey the intended

thought. In order to be an effective means of communication, then, cost data must be

collected and presented in a fashion suitable for conveying the intended thought. This is

simply another way of stating the introductory premise—cost has no meaning unless the type

of cost is specified. From this discussion it follows that no special category of cost data is

required in performing the communicating function. What is required is that the correct type

of cost data be used, depending on the purpose of the communication.

MOTIVATION

Cost information can be used as an important tool for motivating subordinates. If nothing

else, the mere collection of cost data indicates that management is concerned about costs, and

this fact alone will serve to motivate subordinates to comply with management plans and

policies that can be measured in terms of cost.

At this point it would be appropriate to digress for a moment and consider the importance of

motivation. Motivation, really, is the only way that management can ever accomplish

anything. Mr. Robert Anthony expressed this idea most succinctly:

An obvious and fundamental fact about organizations is that they are made up of human

beings. The management control process in part consists of inducing the people in an

organization to do certain things and to refrain from doing others. Although for some

[24]

purposes an accumulation of the costs of manufacturing a product is useful, management

literally cannot “control” a product or the costs of making a product. What management

does—or at least attempts to do—is control the actions of the people who are responsible for

incurring these costs.8

Regardless of how it is attained, cost control is certainly one of the most important

management objectives.9 But, to repeat, this objective can only be realized by motivating

people. However, “. . . costs can be controlled only on the basis of accurate, comprehensive,

well-coordinated knowledge of their nature, amount, and reason for existence . . .”10 The

logical consequence of these arguments is that, for management control purposes, costs must

be collected and people must be motivated. This twofold requirement can be satisfied by

measuring costs incurred and categorizing them in terms of the person or persons responsible

for incurring the costs. This process will fix responsibility for costs with those individuals

who have control over the costs.11 This concept of measuring and categorizing costs as either

controllable or uncontrollable serves a dual purpose: to collect the required cost data and to

motivate responsible individuals toward cost control and other management objectives,

thereby satisfying the need of cost data for management control.

APPRAISAL

Closely associated with the function of motivation is the appraisal or evaluation function. As

far as people are concerned, the two functions are practically inseparable—a man will be

motivated to perform to the extent that he will be evaluated on his performance. Evaluation,

per se, must be based on much more than just cost performance. Nevertheless, since cost

performance, or efficiency, is a management objective, it must enter into evaluation to some

[25]

extent. The other half of the evaluation coin is effectiveness—how well the job was done. In

the military, effectiveness is rightfully considered to be more important than efficiency, and it

should therefore be given primary consideration in evaluation. The problem, then, is to

motivate toward efficiency and evaluate efficiency without jeopardizing effectiveness. This

may be accomplished by evaluating efficiency in terms of extremes—the very good and the

very bad being identified and evaluated accordingly, and all those in between being evaluated

entirely on effectivenss.12 At any rate, the same cost concepts are applicable to the appraisal

of people as were developed in the preceding discussion on motivation—controllable costs

and uncontrollable costs.

A further application of the appraisal function concerns the evaluation of decisions. Decisions

are often based at least in part on cost considerations. In order to evaluate such decisions it is

necessary to measure results in terms of the cost parameters used in the decision process.13 It

is evident, then, that the same cost considerations and categories will be used in evaluating

decisions as were used in making them, and these will be considered in succeeding

paragraphs.

Suffice it to say in summary that cost information is used in the management control function

of the operating activity in order to communicate, to motivate, and to evaluate, and that these

uses of cost information require that costs be categorized as controllable or uncontrollable. At

any rate, the same cost concepts are applicable to the appraisal of people as were developed

in the preceding discussion on motivation—controllable costs and uncontrollable costs

[26]

OPERATING COSTING—DECISION-MAKING

“There’s more than one way to skin a cat” is a homespun adage which expresses one of the

most basic and most generally accepted truisms of human activity—that there is more than

one way to do anything. One of management’s most basic and most frequently performed

tasks is selecting the best way to do something. This, of course, is the essence of management

decision-making—choosing among alternatives. Moreover, the decision-making process is

one of comparing the relative effects of the various possible alternatives. Any course of

action may be thought of or measured in terms of change, based on the situation existing

before and after the implementation of that course of action. The more a given course of

action improves a given situation (or the less it degrades the situation), the better is that

alternative. Or, in the words of Haynes and Massie, “. . . decisions are based on measuring

the benefits to be derived . . . against the sacrifices (costs) incurred.”14

One of the most important aspects of cost information in the decision-making process is

futurity. Decisions are concerned with the impact of alternatives on future events, not with

past history. It follows, then, that “only those costs not yet incurred are important to a . . .

[management] decision,” and unavoidable costs should never even be considered in the

decision-making process.

COST FOR DECISION-MAKING

The effective communication of cost information for decision-making depends, in large part,

on categorization of costs to reflect those aspects illustrated in the automobile example. The

[27]

first requirement is to separate the costs incurred as a direct result of performing a given task

from those only indirectly related to the task. These aspects may be identified as direct and

indirect costs respectively.16 All the costs listed in Table I are direct costs associated with

owning and operating an automobile. Indirect costs would be incurred for such things as

upkeep of garage and driveway, utilities for the garage, etc.

A further distinction must be made between costs that vary in direct proportion to output and

those that do not, termed “variable” and “fixed” costs respectively.17 In the illustration,

gasoline and lubricants and tire replacements are examples of variable costs, and their

magnitude is determined solely by the number of miles driven. Costs such as depreciation,

registration, garage rent, insurance, etc., are fixed and they remain essentially the same

regardless of how much the car is driven.

Of even more interest in decision-making is the distinction between costs that will be affected

by a particular decision and those that will not, termed “incremental” and “sunk” costs

respectively.18 Returning to our example once more, if the family lives in a house that has a

garage and driveway, the costs of these facilities are sunk costs. They have been incurred and

cannot be reduced by any decision concerning the use of the family car.

Finally, a manager must consider opportunity costs (or opportunity losses). He must consider

that any gain which might have resulted from employing his resources in a manner other than

the one being considered must be foregone if the alternative is selected and is therefore part

of the cost (sacrifice) incurred by choosing the first course of action. This aspect of cost data

has been termed “implicit” cost, as opposed to “explicit” costs, which represent the resources

actually consumed by the alternative selected.19 All the costs listed in Table I, for example,

are the explicit costs of owning and operating the family automobile for one year.

[28]

DESIGNING THE SYSTEM Designing the system begins with product development.

Product development involves determining the characteristics and features of the good (or

service if engaged in a service-oriented industry) to be sold. It should begin with an

assessment of customer needs and eventually grow into a detailed product design. The

facilities and equipment that will produce the product, as well as the information systems

needed to monitor and control performance, are part of this system design process. In fact,

manufacturing process decisions are integral to a system's ultimate success or failure. "Of all

the structural decisions that the operations manager faces, the one with the greatest impact on

the manufacturing operation's success is the process/technology choice, " said Thomas S.

Bateman and Carl P. Zeithaml in Management: Function and Strategy. "This decision

addresses the question 'How will the product be made?' " Product development should be a

cross-functional decision-making process that relies on teamwork and communication to

install the marketing, financial, and operating plans needed to successfully launch a product.

PLANNING THE SYSTEM Planning the system describes how management expects to

utilize the existing resource base created as a result of the production system design. One of

the outcomes of this planning process may be to change the system design to cope with

environmental changes. For example, management may decide to increase or decrease

capacity to cope with changing demand, or rearrange layout to enhance efficiency.

Decisions made by production planners depend on the time horizon. Long-range decisions

could include the number of facilities required to meet customer needs or studying how

technological change might affect the methods used to produce services and goods. The time

horizon for long-term planning varies with the industry and is dependent on both complexity

[29]

and size of proposed changes. Typically, however, long-term planning may involve

determining work force size, developing training programs, working with suppliers to

improve product quality and improve delivery systems, and determining the amount of

material to order on an aggregate basis. Short-term scheduling, on the other hand, is

concerned with production planning for specific job orders (who will do the work, what

equipment will be used, which materials will be consumed, when the work will begin and

end, and what mode of transportation will be used to deliver the product when the order is

completed).

MANAGING THE SYSTEM Managing the system involves working with people to

encourage participation and improve organizational performance. Participative management

and teamwork are an essential part of successful operations, as are leadership, training, and

culture. In addition, material management and quality are two key areas of concern.

Material management includes decisions regarding the procurement, control, handling,

storage, and distribution of materials. Material management is becoming more important

because, in many organizations, the costs of purchased materials comprise more than 50

percent of the total production cost. Questions regarding quantities and timing of material

orders need to be addressed here as well when companies weigh the qualities of various

suppliers.

A budget provides a roadmap for the financial management of the organization including

controlling costs. Historical results along with the effects of current revenue and cost trends

[30]

provide the basis for a budget and can help predict the future financial health of the

organization. It will also provide the benchmark for reporting future financial results.

Monthly reviews of actual financial results compared to budgeted amounts will provide the

information necessary to react quickly to variances to the plan.

[31]

HOSPITAL COSTING

Service costing system is used in ascertaining the cost of operations of a hospital. The

activities of a hospital are divided into a number of cost centers, which are:

i. Out-patient department

ii. Pathology centre

iii. Wards

iv. Operation theatre

v. Laundry

vi. Kitchen

Cost is collected for each such cost centers, and the cost per unit of output is ascertained

with respect to each cost centre. Costs are classified into fixed and variable for preparing

operating cost sheet

Cost unit: Different cost centers have different cost units to measure the output. Cost-

output relationship and all other relevant factors will have to be considered to select a cost

unit. The following cost units are used generally:

“Bed-days” for in-patients department (Ward)

[32]

TRANSPORT COSTING

Service costing method is used to ascertain the cost of services provided by an organization

(transport firm) which uses its vehicles for transporting goods or passengers. In motor

transport costing, the cost unit is tone-km or passenger-km.

OBJECTIVES OF MOTOR TRANSPORT COSTING:

1. Analysis of operating costs, namely, wages, full cost, insurance, repairs and

maintenance.

2. Control of operating and running costs and avoidance of waste of fuel and other

consumable material.

3. Comparison of cost of running and maintenance of different vehicles.

4. Assignment of costs to services provided by each vehicle.

5. To quote hiring rates.

6. To compute cost of idle vehicle and lost running time.

7. Collection and analysis of cost for cost control.

[33]

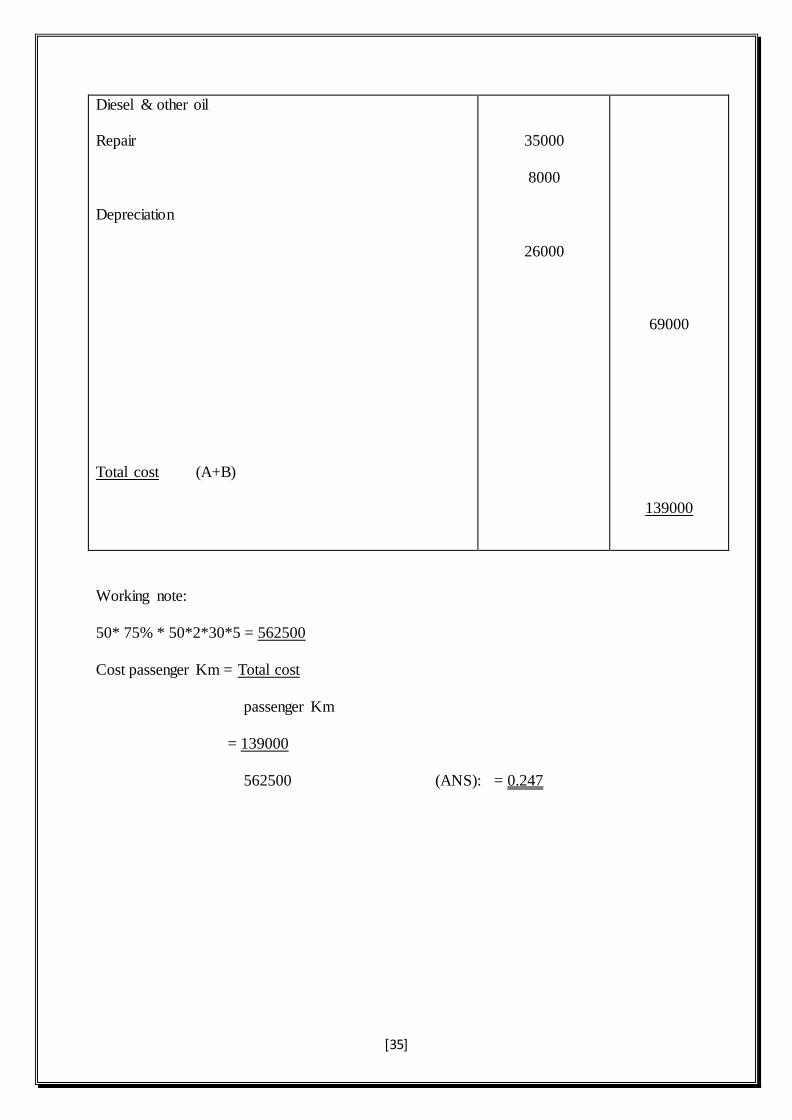

SOLVE THE PROMBLE

TRANSPORTER

A transport company is running 5 bus between 2 town which are 15 Km apart setting capacity

of each bus is 50 passenger the following particular were obtain from the book April 1998.

PARTICULAR AMT

Wages

Salary of office staff

Diesel & other oil

Repair

Taxesation insurance

Depreciation

Interest & other exp

24000

10000

35000

8000

16000

26000

20000

[34]

Additional Information:

Actually passenger carried were 75% of capacity all buses run on all day. If each bus made 1

round trip per day find out cost of per passenger km.

SOLUTION:

PARTICULAR AMT AMT

(A) Fixed cost

Wages

Salary of office staff

Taxesation insurance

Interest & other exp

(B) Variable cost

24000

10000

16000

20000

70000

[35]

Diesel & other oil

Repair

Depreciation

Total cost (A+B)

35000

8000

26000

69000

139000

Working note:

50* 75% * 50*2*30*5 = 562500

Cost passenger Km = Total cost

passenger Km

= 139000

562500 (ANS): = 0.247

[36]

CHAPTER 4

CONCLUSION

Our detailed analysis of operating cost structures leads us to conclude that although the Big4

Indian IT companies offer similar services and operate in same geographies, each of them has

control over and manages their operating costs differently. And this naturally has varying

effects on their operating profits.

We further conclude that the timeless essence of studying each company closely holds true

even when companies are in the same sector.

[37]

CHAPTER 5

BIBLIOGROPHY

www.google.com

www.wikipedia.com

www.icai.com

www.investopedia.com