the outlook for automotive

TRANSCRIPT

Outlook For Automo,ve

Dennis Cuneo Fisher & Phillips LLP Southern Economic Development Roundtable January 24, 2014

US ProducDon

Vehicles (million) CumulaDve Increase

2009 5,611,800 2013 11,000,000 E +5,388,200

US Light Vehicle Produc,on Doubled Since Recession

Source: United States Auto report, BMI

5.4M incremental vehicles ! Equivalent 27 assembly plants

Why No New U.S. Assembly Plants?

• Automakers focused on using & expanding exis,ng capacity – 3 shiX opera,ons (adds 33% capacity) – Investments to eliminate bo\lenecks – Adding new assembly capacity to exis,ng facili,es e.g. Subaru, Toyota

• Mexico à expanding hub for new auto plants

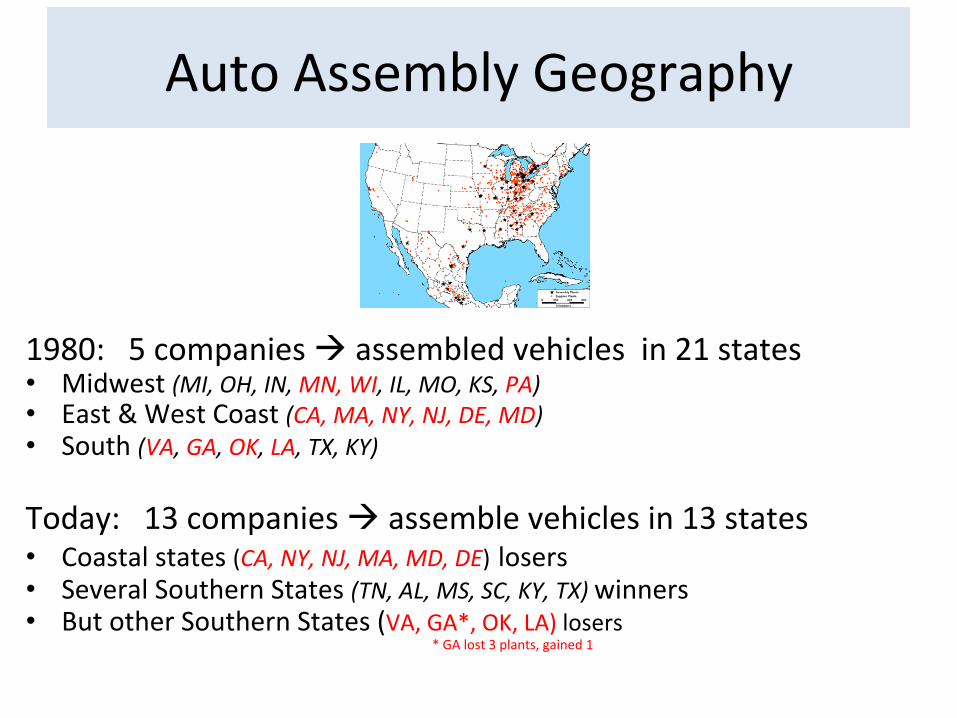

Auto Assembly Geography

1980: 5 companies à assembled vehicles in 21 states • Midwest (MI, OH, IN, MN, WI, IL, MO, KS, PA) • East & West Coast (CA, MA, NY, NJ, DE, MD) • South (VA, GA, OK, LA, TX, KY) Today: 13 companies à assemble vehicles in 13 states • Coastal states (CA, NY, NJ, MA, MD, DE) losers • Several Southern States (TN, AL, MS, SC, KY, TX) winners • But other Southern States (VA, GA*, OK, LA) losers

* GA lost 3 plants, gained 1

Southern Assembly Plants Closed Over Past 2 Decades

• GM Shreveport (2012) • GM Doraville (2008) • Ford Norfolk (2007) • GM OKC (2006) • Ford Atlanta (2006) • GM Lakewood (1990)

3 decade shiX to “Auto Alley”

Detroit 3 pulled back to upper Midwest core

Foreign automakers built new plants along I-‐65/ I-‐75 corridor: Canada to South

But There Are New Challenges As Well As New Opportuni,es

For the Southern States

South Emerged As Major Automo,ve Manufacturing Hub For Foreign Automakers

2 decades of Investment by Foreign Automakers

Source: Thomas Klier, Federal Reserve Bank of Chicago

But the South faces new challenges & new opportuni,es as the auto industry restructures

Canada $3.2 billion

Total $51.7 billion

U.S. Great Lakes

$23.9 billion United States

$35.8 billion

Mexico $12.7 billion

South $8.2 billion

U.S. Great Lakes includes: IL, IN, KY, MI, MO, and OH South includes: AL, FL, GA, MS, SC, TN, and TX

North American Automaker Investments 2010-‐2013 Source: CAR Research, Book of Deals

Since the Great Recession Mexico Has Outpaced U.S. Southern Region

24 month comparisons Oct 2010 – Sept 2012 * States include TN, MS, AL, GA, NC, SC, FL & TX

Mexico • More trade agreements • Cheaper labor • Growing Parts Infrastructure

Automaker investments in

Mexico 2010 – 2013 $12.7 billion

Automaker Investments in Southern States 2010 – 2013 $8.2 billion

What does the future hold?

Map Source: Thomas Klier, Federal Reserve Bank of Chicago

New Assembly in Mexico

• Nissan, Honda, Audi, Mazda, (w Toyota produc,on) building new plants.

• Chrysler, Ford, GM adding capacity at exis,ng plants.

• BMW & Hyundai reportedly in talks with Mexican government.

• Volkswagen: majority of $7B NA investment in Mexico.

Another Challenge for the South

UAW currently targe,ng: – Volkswagen Cha\anooga – Nissan Canton – Mercedes Tuscaloosa

UAW Campaign At Nissan

Center for Automo,ve Research Southern AutomoDve Research

Alliance

Iden,fying & Exploi,ng Opportuni,es Southern Automo,ve Industry

1. Alabama 2. Kentucky 3. Louisiana 4. Mississippi 5. South Carolina 6. Tennessee - - - - - - - - - - - - - - - - - - - - - - - - - • Duke Energy • CU-ICAR • University of Alabama • AAMA • MAMA • SCMA • TAMA • GAMA

-

Participation by six states

Supporting contributions and in-kind participation by Duke Energy and various Universities & AMA’s

Southern AutomoDve Research Alliance (SARA)

Southern AutomoDve Research Alliance (SARA)

Opportunities to Grow Southern Auto Industry • Expand Supply Base • Enhance Automotive R&D in the Region

Auto Parts Suppliers Still Concentrated In Upper Midwest

Thomas Klier, Federal Reserve Bank of Chicago

Assembly

Tier 1

Tier 2

Tier 3

Includes Alabama, Georgia, Mississippi, North Carolina, South Carolina, and Tennessee.

Source: CAR 2010

Includes: Illinois, Indiana, Michigan, Ohio, Pennsylvania, and Wisconsin

Opportunity

Less Lower Tier Supplier Jobs in the South

Job Impact US MS Outside MS

Region Outside Region

Direct 2000 2000 -‐-‐-‐ 2000 -‐-‐-‐ Supplier 5133 1857 3276 2603 2530 Total Direct +Supplier

7133 3857 3276 4603 2530

Spin-‐off 8680 1713 6967 3871 4809

Total (Direct + Supplier+ Spin-‐off)

15,813 5570 10,243 8474 7339

Es,mated Impact Toyota Tupelo Assembly Plant

Source: Center For Automo,ve Research: “ContribuXon of Toyota To the U.S. in 2010”

Opportunity 46% out-‐of-‐region jobs

Opportunity 65% out-‐of-‐state jobs

Fuel Economy

Source: CAR 2013

ConnecDvity/AutomaDon Electronics Safety

Bio-‐Based Materials/ Fuels

LightweighDng

New Automo,ve Technology Brings New Opportuni,es

Porsche

High-‐Tech Automo,ve Systems

Next genera,on high strength steels Foamed metals

Aluminum and magnesium alloys Corrosion protec,on

Bio-‐based materials Advanced plas,cs and composites Mold in color/Films/Other for plas,cs Alterna,ve automo,ve trim cover insert and/or bolster fabrics

Recycled low cost filler materials Coa,ng technology

Non-‐destruc,ve tes,ng methods Robo,cs simula,on soXware Forming high strength steels

New laser technology for trimming, piercing and cupng

New joining technologies Tool rapid hea,ng and cooling Mul,-‐material joining technologies Low cost fine blanking alterna,ves

Materials and Processes Powertrain and Fuels Connected Vehicles Gasoline direct injec,on Turbochargers and superchargers Dual-‐clutch transmissions

Higher-‐speed automa,c transmissions (8-‐ or 9-‐speed) Con,nuously variable transmissions

Vehicle electrifica,on: motor assist, hybrid electric vehicles, plug in hybrid electric vehicles, extended range electric vehicles, or ba\ery electric vehicles

Alterna,ve fuels: natural gas, biofuels (E85 and B20), and hydrogen

Dedicated Short Range Communica,ons (DSRC); 3G, 4G, LTE Cellular; Wi-‐Fi; Bluetooth; and Global Posi,oning System Infotainment (e.g. Sync, Uconnect, and Cue) Human machine interface Collision warning and avoidance

Lane departure warning Blind spot and pedestrian detec,on Road condi,on and event no,fica,on

Adap,ve route guidance with real-‐,me traffic informa,on Signal phase and ,ming

Tolling and E-‐payment Loca,on-‐based services

Efficiency monitoring and carbon footprint accoun,ng Infrastructure investment planning and condi,on monitoring Fleet management

Prognos,cs and diagnos,cs

Advanced Driver Assistance Radar, light detec,on and ranging (LiDAR), and cameras Forward collision warning systems

Automa,c emergency braking and steering Back-‐up and rear-‐view assistance systems

Lane departure and lane-‐keeping assistance systems Adap,ve cruise control and adap,ve cruise control with lane-‐keeping

Blind spot and pedestrian detec,on systems Parking assistance and automated parking systems Adap,ve headlights and adap,ve high beams

Source: CAR 2013

Loca,on of Automaker & Supplier R&D…Design…Engineering

Nissan HQ

Other opportuniDes???

Ques,ons Comments