the outlook for transportation fuel prices and .../media/others/events/2017/automotive... · the...

TRANSCRIPT

www.eia.govU.S. Energy Information Administration Independent Statistics & Analysis

The Outlook for Transportation Fuel Prices and Transportation Energy Use: Insights from AEO2017

Twenty-Fourth Annual Automotive Outlook SymposiumJune 1, 2017 | Detroit, MI

ByJohn Staub, Director Office for Petroleum, Natural Gas, and Biofuels Analysis

• Short-term outlook for crude oil and petroleum products

• Overview of the Annual Energy Outlook 2017

• Fuel prices

• Transportation energy consumption

• Projecting light-duty electric vehicle sales in the National Energy Modeling System (NEMS)

Automotive Outlook Symposium June 1, 2017

Outline

2

Forecast

-3

-2

-1

0

1

2

3

4

5

6

84

86

88

90

92

94

96

98

100

102

2012-Q1 2013-Q1 2014-Q1 2015-Q1 2016-Q1 2017-Q1 2018-Q1

Implied stock change and balance (right axis)World production (left axis)World consumption (left axis)

Source: EIA, Short-Term Energy Outlook May 2017

Automotive Outlook SymposiumJune 1, 2017

The global liquid fuels market is expected to be balanced or slightly over-supplied through the end of 2018World liquid fuels production and consumption balancemillion barrels per day (MMb/d) MMb/d

3

Forecast

40

45

50

55

60

65

70

75

80

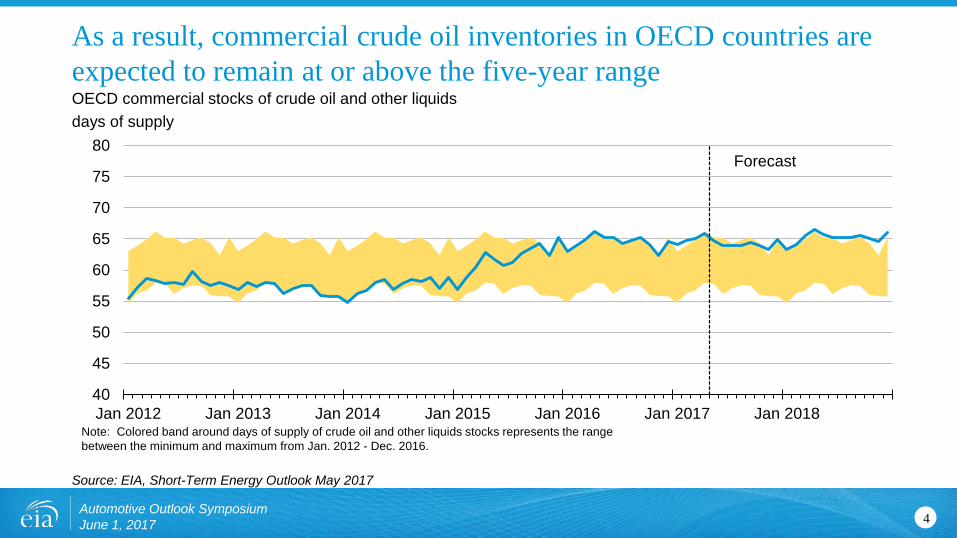

Jan 2012 Jan 2013 Jan 2014 Jan 2015 Jan 2016 Jan 2017 Jan 2018Note: Colored band around days of supply of crude oil and other liquids stocks represents the range between the minimum and maximum from Jan. 2012 - Dec. 2016.

Source: EIA, Short-Term Energy Outlook May 2017

Automotive Outlook SymposiumJune 1, 2017

As a result, commercial crude oil inventories in OECD countries are expected to remain at or above the five-year rangeOECD commercial stocks of crude oil and other liquidsdays of supply

4

-0.6-0.4-0.20.00.20.40.60.81.01.21.4

2016 2017 2018

OPEC countries North America Russia and Caspian Sea Latin America North Sea Other Non-OPEC

Forecast

Source: EIA, Short-Term Energy Outlook May 2017

Automotive Outlook SymposiumJune 1, 2017

North America is projected to be the largest source of liquid fuels production growth over the next two yearsWorld crude oil and liquid fuels production growthmillion barrels per day

5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0U

nite

d S

tate

s

Bra

zil

Can

ada

Rus

sia

Kaz

akhs

tan

Om

an

Nor

way

Mal

aysi

a

Aus

tralia

Syr

ia

Indi

a

Sou

th S

udan

Uni

ted

Kin

gdom

Egy

pt

Vie

tnam

Aze

rbai

jan

Col

ombi

a

Mex

ico

Chi

na

201820172016

Source: EIA, Short-Term Energy Outlook May 2017

Automotive Outlook SymposiumJune 1, 2017

U.S. producers will be the largest source of non-OPEC production growth in 2017 and 2018Non-OPEC crude oil and liquid fuels production growthmillion barrels per day

6

0.0

0.2

0.4

0.6

0.8

1.0

1.2

2016 2017 2018OECD* Non-OECD Asia Former Soviet Union Other

* Countries belonging to the Organization for Economic Cooperation and Development

Forecast

Source: EIA, Short-Term Energy Outlook May 2017

Automotive Outlook SymposiumJune 1, 2017

Growth in global consumption of liquid fuels will be led by non-OECD economies in 2017 and 2018World liquid fuels consumption growthmillion barrels per day

7

-0.30

-0.15

0.00

0.15

0.30

0.45

0.60

0.75

0.90

2015 2016 2017 201817.0

17.5

18.0

18.5

19.0

19.5

20.0

20.5

21.0

Motor gasoline (right axis) Jet fuel (right axis)Distillate fuel (right axis) Other fuels (right axis)Total product supplied (left axis) Product supplied forecast (left axis)

Source: EIA, Short-Term Energy Outlook May 2017

Automotive Outlook SymposiumJune 1, 2017

While U.S. consumption of liquid fuels will increase slightly in 2017 and 2018, led primarily by HGLsU.S. liquid fuels product suppliedmillion barrels per day (MMb/d) annual change (MMb/d)

8

0

20

40

60

80

100

120

140

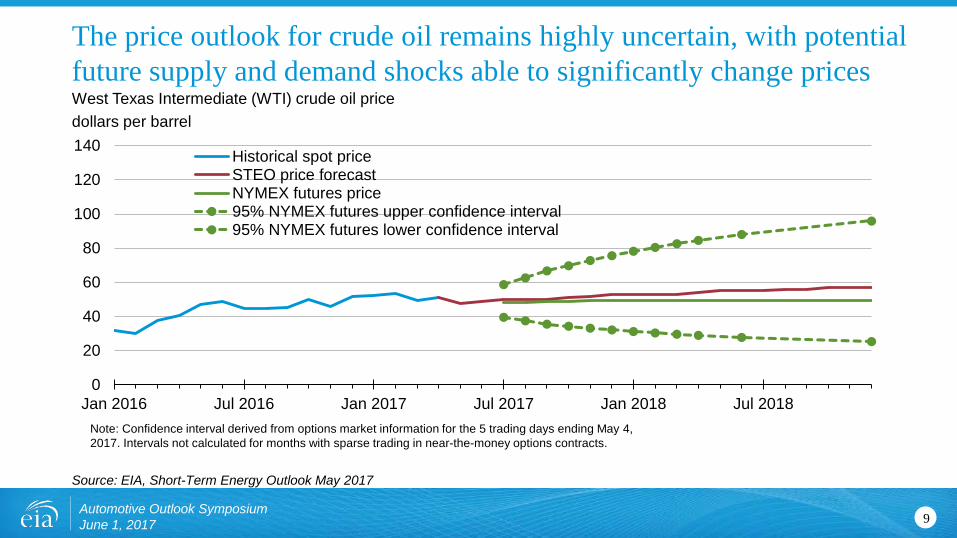

Jan 2016 Jul 2016 Jan 2017 Jul 2017 Jan 2018 Jul 2018

Historical spot priceSTEO price forecastNYMEX futures price95% NYMEX futures upper confidence interval95% NYMEX futures lower confidence interval

Note: Confidence interval derived from options market information for the 5 trading days ending May 4, 2017. Intervals not calculated for months with sparse trading in near-the-money options contracts.

Source: EIA, Short-Term Energy Outlook May 2017

Automotive Outlook SymposiumJune 1, 2017

The price outlook for crude oil remains highly uncertain, with potential future supply and demand shocks able to significantly change pricesWest Texas Intermediate (WTI) crude oil pricedollars per barrel

9

• Oil prices are primarily driven by global market balances that are mainly influenced by factors external to the NEMS model; in the Reference case, oil prices reach $109/b in 2016 dollars, compared to $43/b in the Low Oil Price case and $228/b in the High Oil Price case

• In the High Oil and Gas Resource and Technology case, lower costs and higher resource availability than in the Reference case allow for higher production at lower prices; in the Low Oil and Gas Resource and Technology case, more pessimistic assumptions about resources and costs are applied

• The effects of economic assumptions on energy consumption are addressed in the High and Low Economic Growth cases, which assume compound annual growth rates for U.S. gross domestic product of 2.6% and 1.6%, respectively, from 2016–40, compared with 2.2% annual growth in the Reference case

• A case assuming that the Clean Power Plan (CPP) is not implemented can be compared to the Reference case to show how that policy could affect energy markets and emissions

Automotive Outlook Symposium June 1, 2017

AEO2017 includes side cases with different assumptions of macroeconomic growth, world oil prices, technological progress, and energy policies

10

• Different relative fuel prices

• Faster / slower economic and energy demand growth

• Changing policies and regulations

• Changing consumer preferences

• Faster / slower technology progress

• Technology breakthroughs

Automotive Outlook Symposium June 1, 2017

Why long-term projections might/could/will be wrong

11

0

20

40

60

80

100

120

140

1980 1990 2000 2010 2020 2030 2040

2016history projections High Economic

GrowthLow Oil PriceHigh Oil PriceHigh Oil and Gas Resource and TechnologyReference Low Oil and Gas Resource and Technology Low Economic Growth

Source: EIA, Annual Energy Outlook 2017

Automotive Outlook Symposium June 1, 2017

Energy consumption varies minimally across all AEO cases, bounded by the High and Low Economic Growth cases Total energy consumptionquadrillion British thermal units

12

0

5

10

15

20

25

30

35

40

45

1980 1990 2000 2010 2020 2030 2040

petroleum and other liquidsnatural gas

other renewable energycoalnuclearhydroliquid biofuels

2016history projections

Source: EIA, Annual Energy Outlook 2017

Automotive Outlook Symposium June 1, 2017

Domestic energy consumption remains relatively flat in the Reference case, but the fuel mix changes significantlyEnergy consumption (Reference case)quadrillion British thermal units

13

0

20

40

60

80

100

120

140

1980 1990 2000 2010 2020 2030 2040

High Oil and Gas Resource and Technology High Oil PriceHigh Economic GrowthReference Low Economic GrowthLow Oil PriceLow Oil and Gas Resource and Technology

2016history projections

Source: EIA, Annual Energy Outlook 2017

Automotive Outlook Symposium June 1, 2017

Energy production ranges from nearly flat in the Low Oil and Gas Resource and Technology case, to continued growth in the High Resource and Technology caseTotal energy productionquadrillion British thermal units

14

0

10

20

30

40

1980 1990 2000 2010 2020 2030 2040

dry natural gas

crude oil and lease condensate

coalother renewablesnuclearnatural gas plant liquidshydro

2016history projections

Source: EIA, Annual Energy Outlook 2017

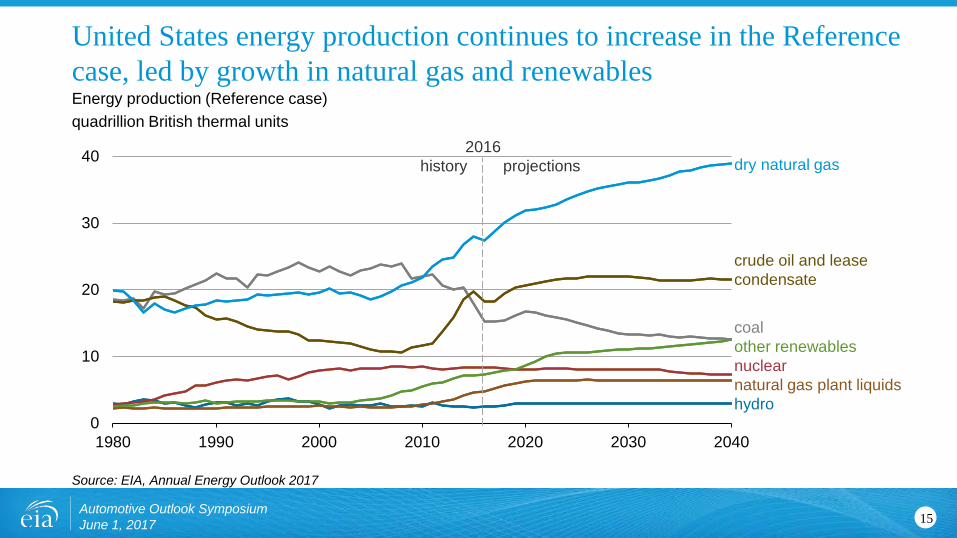

Automotive Outlook Symposium June 1, 2017

United States energy production continues to increase in the Reference case, led by growth in natural gas and renewablesEnergy production (Reference case)quadrillion British thermal units

15

Tight oil dominates U.S. production in the Reference case, but other types of oil production continue to yield significant volumes

Source: EIA, Annual Energy Outlook 2017

02468

1012141618

2000 2010 2020 2030 2040

Crude oil production million barrels per day

U.S. total

tight oil

non-tight oil

2016history projections

2020 2030 2040

2016projections

2020 2030 2040

2016projections

Low Oil and Gas Resource and Technology

Reference High Oil and Gas Resource and Technology

16Automotive Outlook Symposium June 1, 2017

-40

-20

0

20

40

60

80

2000 2005 2010 2015 2020 2025 2030 2035 2040

Low Oil PriceLow Oil and GasResource and TechnologyReference

High Oil Price

High Oil and GasResource and Technology

net imports

net exports

2016history projections

Source: EIA, Annual Energy Outlook 2017

Automotive Outlook SymposiumJune 1, 2017

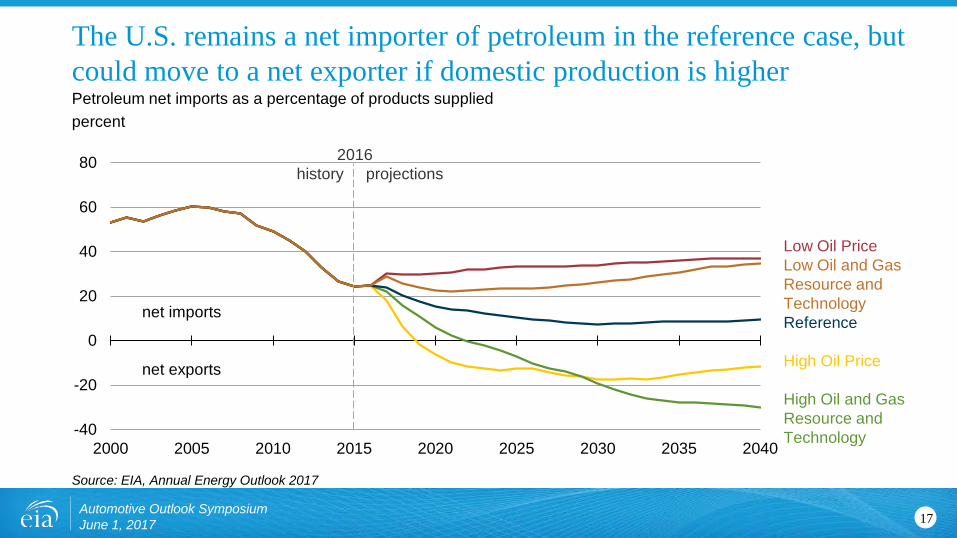

The U.S. remains a net importer of petroleum in the reference case, but could move to a net exporter if domestic production is higherPetroleum net imports as a percentage of products suppliedpercent

17

-30

-20

-10

0

10

20

30

40

2005 2010 2015 2020 2025 2030 2035 2040

2016history projections

solarwindoil and gasnuclearothercoal

additions

retirements

Source: EIA, Annual Energy Outlook 2017

Adam Sieminski, Johns Hopkins SAIS January 5, 2017

Lower capital costs and the availability of tax credits boost near-term wind additions and sustain solar additions; whereas coal-fired unit retirements in the Reference case are driven by low natural gas prices and the Clean Power PlanAnnual electricity generating capacity additions and retirements (Reference case) gigawatts

18

Prices

Automotive Outlook Symposium June 1, 2017 19

0

50

100

150

200

250

2000 2010 2020 2030 2040

North Sea Brent oil price2016 dollars per barrel

2016history projections

0

2

4

6

8

10

12

14

16

18

2000 2010 2020 2030 2040

2016history projections

Crude oil productionmillion barrels per day

Source: EIA, Annual Energy Outlook 2017

In the long-term, there is a wide set of potential outcomes for both crude oil prices and U.S. crude oil production

20Automotive Outlook SymposiumJune 1, 2017

High Oil and Gas Resource and Technology

High Oil PriceReference case

Low Oil PriceLow Oil and Gas Resource and Technology

0.00

1.00

2.00

3.00

4.00

5.00

6.00

0

20

40

60

80

100

120

2015 2020 2025 2030 2035 2040

Motor gasoline (right)

Diesel fuel (right)

North Sea Brent oil price (left)

Real petroleum prices2016 dollars per barrel 2016 $/gallon

Real fuel prices in transportation sector2016 $/MMBtu

Note: Motor gasoline is sales weighted-average price for all grades. Includes Federal, State, and local taxes.Source: EIA, Annual Energy Outlook 2017.

Real fuel prices in the transportation sector are lowest for natural gas, highest for electricity

Automotive Outlook Symposium June 1, 2017 21

0

5

10

15

20

25

30

35

40

45

2015 2020 2025 2030 2035 2040

Motor gasoline

Diesel fuel

Electricity

Natural gas

2016projections

2016projections

0

2

4

6

8

10

12

2000 2010 2020 2030 2040

2016history projections Low Oil and

Gas Resource and TechnologyHigh Oil PriceReference case Low Oil PriceHigh Oil and Gas Resource and Technology

Source: EIA, Annual Energy Outlook 2017

Automotive Outlook SymposiumJune 1, 2017

Natural gas prices also depend on developments in the oil market, with coproduction and substitution linking these marketsHenry Hub natural gas price2016 dollars per million Btu

22

0

5

10

15

20

25

0

2

4

6

8

10

2000 2010 2020 2030 2040

Liquefied natural gas exportstrillion cubic feet billion cubic feet per day

2016history projections

0

1

2

3

4

5

6

7

8

2000 2010 2020 2030 2040

Oil-to-natural gas price ratioenergy-equivalent terms

2016history projections

Source: EIA, Annual Energy Outlook 2017

U.S. LNG export levels vary across cases and reflect both the level of global demand, as well as by the difference between domestic and global natural gas prices

Reference High and Low Oil and Gas Resource and Technology

High and LowOil Price

23Automotive Outlook Symposium June 1, 2017

Transportation Energy Demand

Automotive Outlook Symposium June 1, 2017 24

0

5

10

15

20

25

30

35

2000 2010 2020 2030 2040

Transportation sector consumption quadrillion British thermal units

2016history projections

motorgasoline

distillatefuel oil

jet fuelelectricityother

0

5

10

15

20

25

30

35

2000 2010 2020 2030 2040

Transportation sector consumptionquadrillion British thermal units

2016history projections

light-duty vehiclesmedium-and heavy-duty vehiclesaircommerciallight trucksrailmarineother

Source: EIA, Annual Energy Outlook 2017

Transportation energy use declines between 2018 and 2034 in the Reference case, driven by improvements in fuel economy

25Automotive Outlook SymposiumJune 1, 2017

0

10

20

30

40

50

2000 2010 2020 2030 2040

Light-duty stock fleet fuel economymiles per gallon

car

fleetaverage

truck

2016history projections

20%

30%

40%

50%

60%

70%

2000 2010 2020 2030 2040

Light-duty vehicle sales sharespercent

truck

car

0%

2016history projections

Source: EIA, Annual Energy Outlook 2017

Average light-duty fuel economy improves in the Reference case, even as the share of light-duty trucks increases

26Automotive Outlook SymposiumJune 1, 2017

Source: EIA, Annual Energy Outlook 2017

Automotive Outlook Symposium June 1, 2017

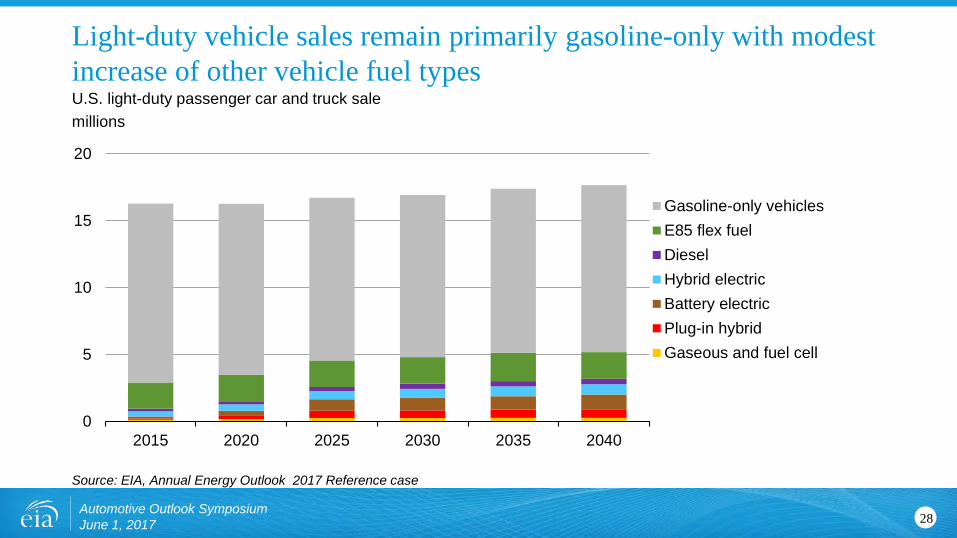

Sales of battery electric, plug-in electric hybrid, and fuel cell vehicles increase in the Reference case because of lower projected battery costs and existing state policiesNew light-duty vehicle sales thousands of vehicles

27

0

5

10

15

20

2015 2020 2025 2030 2035 2040

Gasoline-only vehiclesE85 flex fuelDieselHybrid electricBattery electricPlug-in hybridGaseous and fuel cell

Source: EIA, Annual Energy Outlook 2017 Reference case

Light-duty vehicle sales remain primarily gasoline-only with modest increase of other vehicle fuel typesU.S. light-duty passenger car and truck salemillions

28Automotive Outlook Symposium June 1, 2017

0%

5%

10%

15%

20%

25%

30%

2015 2020 2025 2030 2035 2040

Source: EIA, Annual Energy Outlook 2017 Reference case

Share of vehicles with micro hybrid subsystem increase across the projectionGasoline micro hybrid share of new gasoline vehiclesales

29Automotive Outlook Symposium June 1, 2017

With the second phase of fuel efficiency regulations, medium- and heavy-duty vehicle energy consumption declines over 2027-33 despite continued growth in miles traveled

Source: EIA, Annual Energy Outlook 2017

050

100150200250300350400450

2000 2020 2040

2016history projections

travel indicatorbillion vehicle-miles traveled

0

2

4

6

8

10

12

2000 2020 2040

2016history projections

stock fuel economymiles per gallon

0

1

2

3

4

5

6

7

2000 2020 2040

2016history projections

energy consumptionquadrillion British thermal units

Medium- and heavy-duty vehicle metrics

30Automotive Outlook SymposiumJune 1, 2017

• Ride sharing

• Autonomous vehicle technology in both passenger and freight applications

• Actual uptake of vehicles fueled by electricity and/or hydrogen

• Teleworking and telepresence

• Possible pursuit of deep decarbonization

• Future vehicle efficiency and taxation policies

Automotive Outlook Symposium June 1, 2017

Food for thought – transportation

31

Projecting Light-Duty Electric Vehicle Sales in the National Energy Modeling

System (NEMS)

Automotive Outlook Symposium June 1, 2017 32

• Manufacturers Technology Choice Component (MTCC) – adopt vehicle subsystem technologies (86) for different vehicle fuel types (conventional gasoline,

hybrid, diesel, etc.) based on value of fuel economy and/or performance improvement– alternative fuel vehicles (15)

• Consumer Vehicle Choice Component (CVCC)– determines consumer acceptance (market share) by vehicle fuel type (conventional gasoline,

hybrid, diesel, etc.) – nested multinomial logit model, coefficients vary by size class, for 9 attributes

• Meeting CAFE through the MTCC and CVCC– Application of alternative fuel vehicle credits– CAFE credits and banking– FFV credit limits

Modeling vehicle choice in the NEMS transportation module involves both manufacturers (building) and consumers (buying)

33Automotive Outlook Symposium June 1, 2017

• Historic and Projected vehicle attributes (fuel economy, horsepower, weight, tank size, interior volume, price, footprint) by size class (6), manufacturer (9), and vehicle fuel type (16)

Manufacturer Technology Choice Component (MTCC)—vehicle attributes and size classes

34

Passenger Car Size Class

(interior volume—cubic feet)

Light-Duty Truck Size Class

(test weight—lbs)Mini (<85) Small Pickup (<4500)

Subcompact (85-99) Standard Pickup (>4500)Compact (99-109) Small SUVMidsize (110-120) Standard SUV

Large (>120) Small Van2 seater Standard Van

Automotive Outlook Symposium June 1, 2017

Manufacturer Technology Choice Component (MTCC)—manufacturer groups

35

Passenger CarManufacturer

Light-Duty Truck Manufacturer

Domestic Domestic 1Asian Domestic 2

European Domestic 3Sports/Luxury Import 1

Import 2

Automotive Outlook Symposium June 1, 2017

• Micro and mild hybridization are considered vehicle subsystems

Manufacturer Technology Choice Component (MTCC)—vehicle fuel types

36

Vehicle fuel typeGasoline Gasoline Hybrid

Diesel Dedicated CNGFlex Fuel (ethanol) Dedicated LPG

Electric—100 mile range Bi-fuel CNGElectric—200 mile range Bi-fuel LPG

Plug-in Hybrid Electric—10 mile Methanol Fuel CellPlug-in Hybrid Electric—40 mile

range Gasoline Fuel Cell

Diesel Hybrid Hydrogen Fuel Cell

Automotive Outlook Symposium June 1, 2017

• 86 subsystem technologies available

– Vehicle: Mass Reduction I to V; Aerodynamics I and II; Tires I and II; Low Drag Brakes; Secondary Axle Disconnect

– Transmission: 6 speed Manual; 6, 7, and 8 speed Automatic; Dual Clutch Automated Manual; High Efficiency Gearbox; Aggressive Shift Logic I and II; Early Torque Converter Lockup; Continuously Variable Transmission

– Accessories/Electrification: Electric Power Steering; Improved Accessories I and II; 12V Micro Hybrid; Integrated Starter Generator Mild Hybrid

– Engine (most by cylinder and cam profile): Low Friction Lubricants; Engine Friction Reduction I and II; Cylinder Deactivation; Variable Valve Timing (ICP, CCP, DCP); Variable Valve Lift (DVVL, CVVL); Stoichiometric Gasoline Direct Injection; Turbocharging and Downsizing I, II, and III with cooled EGR

• Technology attributes include fuel economy, cost, horsepower and weight adjustment, and base year (2015) penetration (by manufacturer, by size class)

• Technology synergies, supersede notes, and learning rates

Manufacturer Technology Choice Component (MTCC)—adopting vehicle subsystem technology

37Automotive Outlook Symposium June 1, 2017

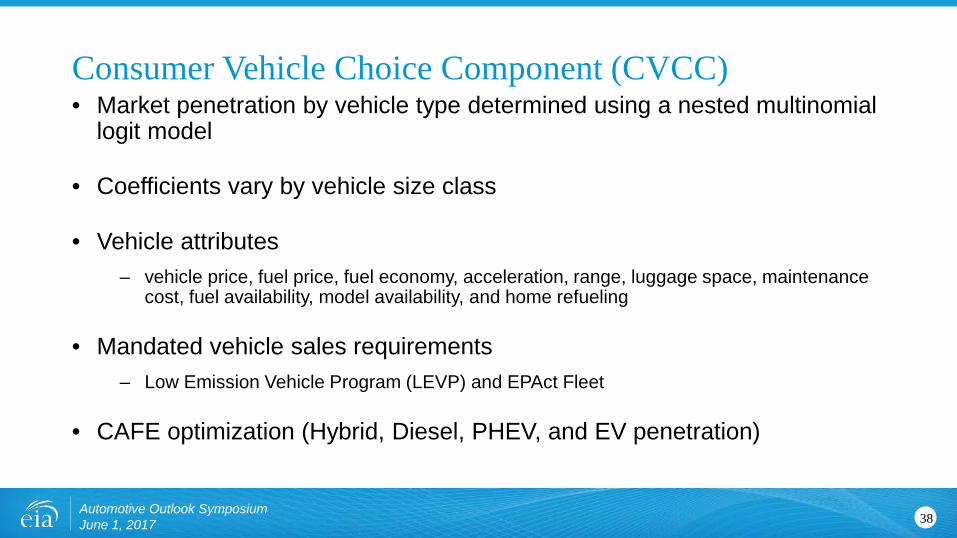

• Market penetration by vehicle type determined using a nested multinomial logit model

• Coefficients vary by vehicle size class

• Vehicle attributes– vehicle price, fuel price, fuel economy, acceleration, range, luggage space, maintenance

cost, fuel availability, model availability, and home refueling

• Mandated vehicle sales requirements– Low Emission Vehicle Program (LEVP) and EPAct Fleet

• CAFE optimization (Hybrid, Diesel, PHEV, and EV penetration)

Consumer Vehicle Choice Component (CVCC)

38Automotive Outlook Symposium June 1, 2017

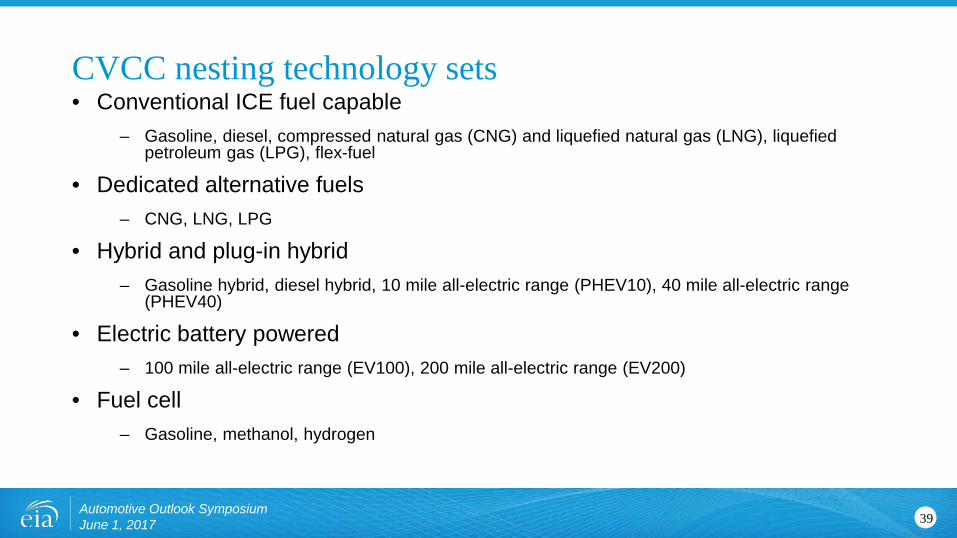

• Conventional ICE fuel capable– Gasoline, diesel, compressed natural gas (CNG) and liquefied natural gas (LNG), liquefied

petroleum gas (LPG), flex-fuel

• Dedicated alternative fuels– CNG, LNG, LPG

• Hybrid and plug-in hybrid– Gasoline hybrid, diesel hybrid, 10 mile all-electric range (PHEV10), 40 mile all-electric range

(PHEV40)

• Electric battery powered– 100 mile all-electric range (EV100), 200 mile all-electric range (EV200)

• Fuel cell– Gasoline, methanol, hydrogen

CVCC nesting technology sets

39Automotive Outlook Symposium June 1, 2017

Nesting structure

40

Vehicle Class

Conventional Fuel ICE

Gasoline, Diesel, FFV,

Bi-Fuel

FFVBi-Fuel

CNG, LPG

Alternative Fuel ICE

CNG, LPG

Hybrid

HEV (gasoline),

HEV (diesel), PHEV10

(gasoline), PHEV40 (gasoline

Electric

EV100, EV200

Fuel Cell

Hydrogen, Methanol, Gasoline

Automotive Outlook Symposium June 1, 2017

• Three passes through the MTCC and CVCC

• Each pass determines CAFE compliance– Pass 1: Add technologies economically– Pass 2: Implement fine for CAFE non-compliance– Pass 3: Reduce horsepower to comply with CAFE

• If not in compliance after third pass, force alternative vehicles for CAFE compliance

CAFE test looping process

41Automotive Outlook Symposium June 1, 2017

Battery Electric Vehicle Assumptions

42Automotive Outlook Symposium June 1, 2017

• Generalized electric-range groups– EV100 (90 actual miles)

– EV200 (200 actual miles)

– PHEV10 (10 all-electric miles)

– PHEV40 (40 all-electric miles)

• Lithium-ion battery costs are modeled for each vehicle type– Base year costs based on literature review

– Cost difference between vehicle types comes from ANL BatPac model

– Projected costs reduce over time as a function of production and a learning curve to generally match projected costs from literature review

Battery Electric Vehicles in NEMS

43Automotive Outlook Symposium June 1, 2017

• Vehicle miles travelled assumed same for all powertrains– VMT per vehicle input by vintage for passenger cars and light trucks

– Total VMT calculated from vehicle stock projections

• PHEV all-electric vs. conventional usage– PHEV10 – 21% of VMT all-electric

– PHEV40 – 58% of VMT all-electric

Battery Electric Vehicles in NEMS

44Automotive Outlook Symposium June 1, 2017

Battery Costs Projected from 2015Lithium-ion retail battery costs 2015$/kW-hr

45

0

200

400

600

800

1,000

1,200

1,400

1,600

2010 2015 2020 2025 2030 2035 2040 2045 2050

PHEV10

PHEV40

EV100

EV200

AEO2016 EV100

Automotive Outlook Symposium June 1, 2017

• California Zero-Emission Vehicle Mandate– Adopted by nine other states

• California AB-32 for GHG Reduction– Further increases electric vehicle share

– Decreases VMT

Battery Electric Vehicle Sales Drivers

46Automotive Outlook Symposium June 1, 2017

• High technology– 10 percent increase in technology fuel economy, 10 percent reduction in technology price

• Low technology– 10 percent decrease in technology fuel economy, 10 percent increase in technology price

• High tech battery case (AEO2012)

• Extended policies case

• Import dependency cases (AEO2013)

AEO transportation scenarios

47Automotive Outlook Symposium June 1, 2017

• Updates to battery electric vehicle models– Non-battery systems costs

– Increase electric-ranges to better represent changing market

Potential updates to AEO2018

48Automotive Outlook Symposium June 1, 2017

For more information

U.S. Energy Information Administration home page | www.eia.gov

Short-Term Energy Outlook | www.eia.gov/steo

Annual Energy Outlook | www.eia.gov/aeo

International Energy Outlook | www.eia.gov/ieo

Monthly Energy Review | www.eia.gov/mer

Today in Energy | www.eia.gov/todayinenergy

49Automotive Outlook SymposiumJune 1, 2017

Backup

50Automotive Outlook SymposiumJune 1, 2017

Although population and economic output per capita are assumed to continue rising, energy intensity and carbon intensity are projected to continue falling in the Reference case

0

50

100

150

200

250

300

350

400

1980 2010 2040

U.S. populationmillion people

2016

history

0

10

20

30

40

50

60

70

80

1980 2010 2040

Gross domestic product per capitathousand dollars/person

2016

history

0

2

4

6

8

10

12

14

1980 2010 2040

Energy intensitythousand British thermal units per dollar

2016

history

0

10

20

30

40

50

60

70

1980 2010 2040

Carbon intensitymetric tons CO2 per billion British thermal units

2016

history

Referencecase

Source: EIA, Annual Energy Outlook 2017

51Automotive Outlook SymposiumJune 1, 2017

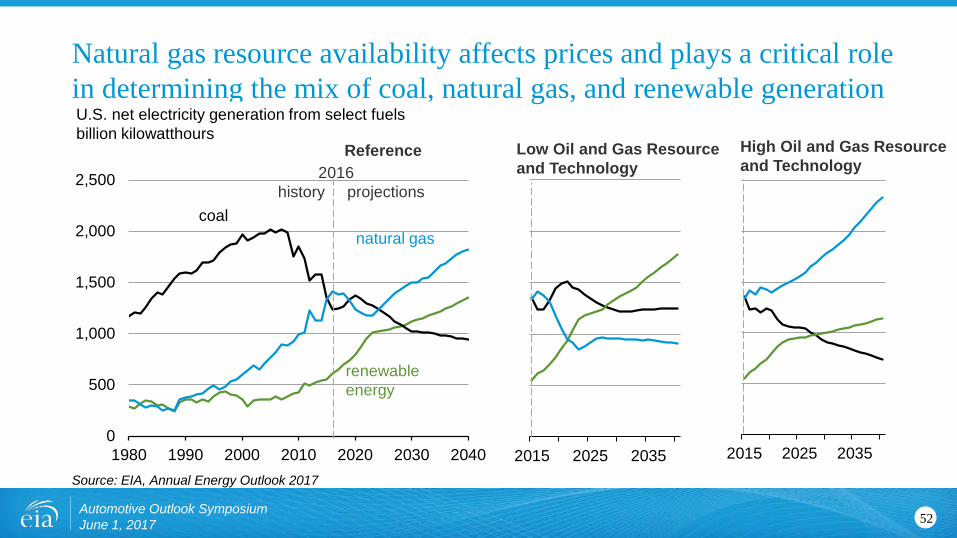

Natural gas resource availability affects prices and plays a critical role in determining the mix of coal, natural gas, and renewable generation

Source: EIA, Annual Energy Outlook 2017

52Automotive Outlook Symposium June 1, 2017

2015 2025 2035 2015 2025 2035

Low Oil and Gas Resourceand Technology

High Oil and Gas Resource and Technology

0

500

1,000

1,500

2,000

2,500

1980 1990 2000 2010 2020 2030 2040

U.S. net electricity generation from select fuels billion kilowatthours

natural gas

2016history projections

coal

renewableenergy

Reference

Natural gas

53Automotive Outlook Symposium June 1, 2017

-3-2-10123456789

2015 2016 2017 201864666870727476788082848688

Federal Gulf of Mexico production (right axis) U.S. non-Gulf of Mexico production (right axis)U.S. net imports (right axis) Total marketed production (left axis)Marketed production forecast (left axis)

Source: EIA, Short-Term Energy Outlook May 2017

Automotive Outlook SymposiumJune 1, 2017

After dropping in 2016, U.S. natural gas production will increase in 2017 and 2018U.S. natural gas production and importsbillion cubic feet per day (Bcf/d)

annual change Bcf/d

54

0

10

20

30

40

50

60

2000 2010 2020 2030 2040

U.S. natural gas production by type trillion cubic feet

shale gas and tight oil plays

tight gasother Lower 48 onshoreLower 48 offshoreother

2016history projections

Source: EIA, Annual Energy Outlook 2017

U.S. dry natural gas production is the result of continued development of shale gas and tight oil plays, alternative assumptions cause significant differences

55Automotive Outlook Symposium June 1, 2017

0

10

20

30

40

50

60

2000 2010 2020 2030 2040

Dry natural gas productiontrillion cubic feet

2016history projections High Oil Price

High Oil and Gas Resourceand Technology Reference case Low Oil PriceLow Oil and Gas Resource and Technology

-3-2-1012345678

2015 2016 2017 20180

102030405060708090

100110

Electric power (right axis) Residential and comm. (right axis)Industrial (right axis) Other (right axis)

Source: EIA, Short-Term Energy Outlook May 2017

Automotive Outlook SymposiumJune 1, 2017

Higher natural gas prices in 2017 will reduce its use for electricity generation compared to 2016U.S. natural gas consumptionbillion cubic feet per day (Bcf/d)

annual change (Bcf/d)

56

0

20

40

60

80

100

0

5

10

15

20

25

30

35

40

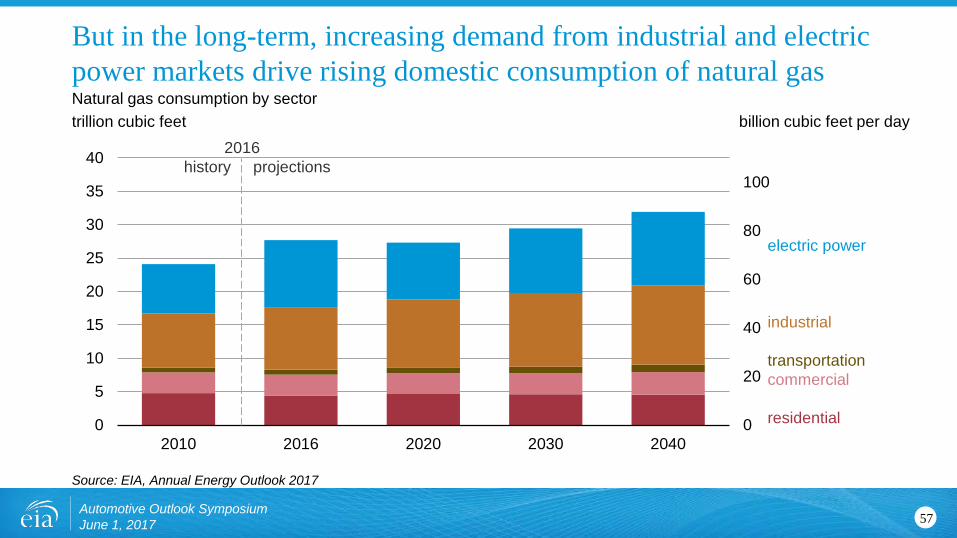

2010 2016 2020 2030 2040

electric power

industrial

transportationcommercial

residential

2016history projections

Source: EIA, Annual Energy Outlook 2017

Automotive Outlook SymposiumJune 1, 2017

But in the long-term, increasing demand from industrial and electric power markets drive rising domestic consumption of natural gasNatural gas consumption by sector trillion cubic feet billion cubic feet per day

57

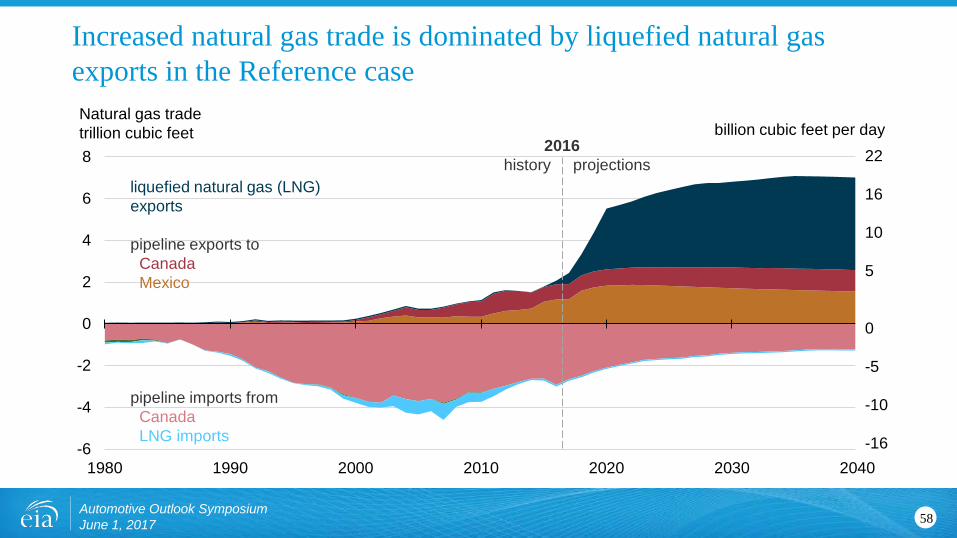

Increased natural gas trade is dominated by liquefied natural gas exports in the Reference case

58

-6

-2

2

6

-6

-4

-2

0

2

4

6

8

1980 1990 2000 2010 2020 2030 2040

Natural gas tradetrillion cubic feet

2016history projections

liquefied natural gas (LNG) exports

pipeline exports to CanadaMexico

pipeline imports fromCanadaLNG imports

billion cubic feet per day22

16

10

5

0

-5

-10

-16

Automotive Outlook Symposium June 1, 2017

Forecast

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

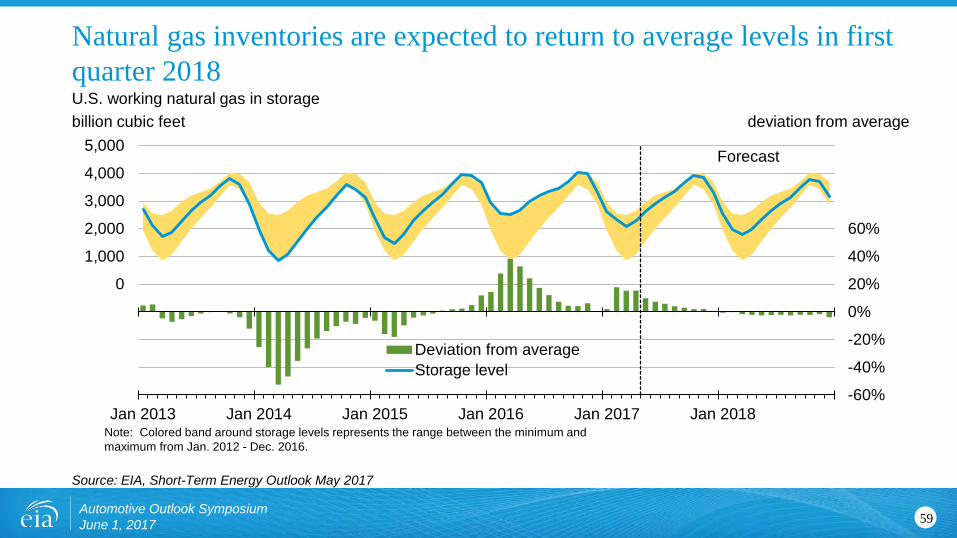

-4,000

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

Jan 2013 Jan 2014 Jan 2015 Jan 2016 Jan 2017 Jan 2018

Deviation from averageStorage level

Note: Colored band around storage levels represents the range between the minimum and maximum from Jan. 2012 - Dec. 2016.

Source: EIA, Short-Term Energy Outlook May 2017

Automotive Outlook SymposiumJune 1, 2017

Natural gas inventories are expected to return to average levels in first quarter 2018U.S. working natural gas in storagebillion cubic feet deviation from average

59

0

1

2

3

4

5

6

7

8

9

Jan 2016 Jul 2016 Jan 2017 Jul 2017 Jan 2018 Jul 2018

Historical spot priceSTEO forecast priceNYMEX futures price95% NYMEX futures upper confidence interval95% NYMEX futures lower confidence interval

Note: Confidence interval derived from options market information for the 5 trading days ending May 4, 2017. Intervals not calculated for months with sparse trading in near-the-money options contracts.

Source: EIA, Short-Term Energy Outlook May 2017

Automotive Outlook SymposiumJune 1, 2017

Future natural gas prices are inherently uncertain, with market participants indicating a range of about $2 to $7 per MMBtuHenry Hub natural gas pricedollars per million Btu

60

• Technology developments – to what extent will they continue to offset depletion of hydrocarbon resources

• Possible pursuit of deep decarbonization, particularly in the electricity generation and buildings sectors

• Geopolitics in key oil and natural gas producing regions – both internationally and within the United States

• Competitiveness of gas-fired generation with other technologies in developing countries where projected electricity demand growth is concentrated

• Technologies and policies affecting vehicle choice, which given dominant role of transportation sector in oil demand can significantly affect markets for oil and natural gas

Automotive Outlook Symposium June 1, 2017

Food for thought – natural gas production and trade

61

• Technology developments – to what extent will they continue to offset depletion of hydrocarbon resources

• Geopolitics in key producing regions – both internationally and within the United States

• Possible pursuit of deep decarbonization, particularly in transportation applications

• Technologies and policies affecting vehicle choice, given dominant role of transportation sector in oil demand

Automotive Outlook Symposium June 1, 2017

Food for thought – hydrocarbon production and trade

62

John Maples | phone: 202-586-1757 | email: [email protected]

David Stone | phone: 202-586-8851 | email: [email protected]

Melissa Lynes | phone: 202-586-5192 | email: [email protected]

Automotive Outlook Symposium June 1, 2017

EIA Transportation analysts

63