the philippine electric distribution...

TRANSCRIPT

The Philippine Electric Distribution Sector

April 29, 2014

Wallace Business Forum Quarterly Roundtable

1

Outline of the discussion

• Overview of the Electric Distribution Subsector

• Power Prices

• Supporting Economic Development

2

SUPPLY CHAIN OF THE PHILIPPINE POWER SECTOR

National Power

Corporation (NPC),

Privatized Generation

Companies,&

Independent Power

Producer Administrators

(IPPAs), etc.

Wholesale

Electricity Spot

Market (WESM)

Independent

Power

Producers (IPPs)

National Grid

Corporation of

the Philippines

(NGCP)

Generation Transmission

Distribution &

Supply

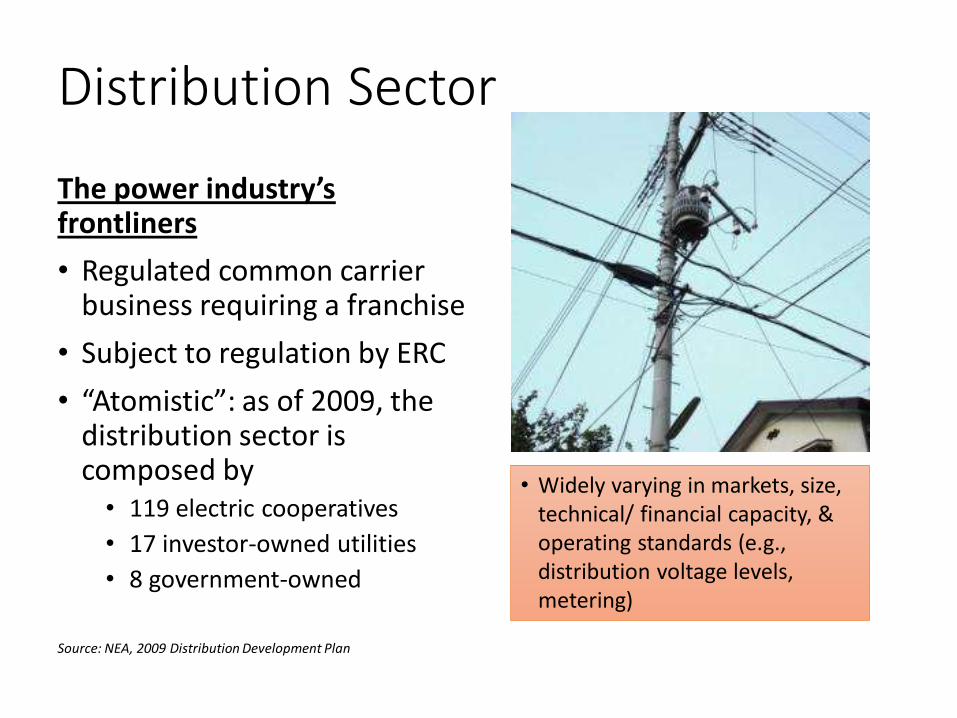

Distribution Sector

The power industry’s frontliners

• Regulated common carrier business requiring a franchise

• Subject to regulation by ERC

• “Atomistic”: as of 2009, the distribution sector is composed by• 119 electric cooperatives

• 17 investor-owned utilities

• 8 government-owned

Source: NEA, 2009 Distribution Development Plan

• Widely varying in markets, size, technical/ financial capacity, & operating standards (e.g., distribution voltage levels, metering)

Background: Investor-owned distribution utilities

• Serves political & economic centers• Example: cities of

Dagupan, Angeles, Tarlac, Cebu, Iloilo, Davao, Cagayan de Oro

Angeles Electric

San Fernando Electric

Tarlac Electric

Dagupan Electric

Cabanatuan Electric

La Union Electric

Ibaan Electric

Subic Enerzone

Clark Electric

Meralco

Davao Light

Cagayan Electric

Iligan Light

Cotabato Light

Visayan Electric

Mactan Electric

Panay Electric

Bohol Light

Background: electric cooperatives (NEA general information & statistics, 2013)

1st Sem2013

National

No. of operational ECs 119

Consumers served 9,923,725

Gross Revenue (thousand pesos)

57,276,326

Sales (GWh) 6,887

Peak Load (MW) 3,057

Total Workforce 21,562

Total Circ. Kms of line 314,088

6

2013 AveNational

Ave Revenue/EC/Month 84 M

Ave Connection/EC 84,393

Ave kms of line constructed/EC

2,617

Ave conns/circ km of line 32

Ave MWh sales/EC/mo 10,069

Ave monthly kWhconsumption/connection

116

Ave System Loss 12.15%

Ave No of Employees/EC 189

Electric cooperatives and their markets are generally small

Meralco serves a strategic market

• Powers more than five (5) million customers in 33 cities and 78 municipalities

• The country’s center of commerce & industry• About 50% of the

country’s GDP• An estimated 60% of

manufacturing output• More than 30

manufacturing economic zones

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

23,834 24,660 24,806 25,078

26,219 27,049 27,516

30,247 30,592

32,771

34,084 GWh

4.0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

4.054.21

4.32 4.39 4.464.57

4.704.85

5.035.19 5.37 m 3.4%

ENERGY SALES

CUSTOMER COUNT

CONSOLIDATED

Ave. Growth: 2009-13: 3.7%

2003-13: 4.8%

Ave. Growth: 2009-13: 2.9%

2003-13: 3.3%

Market has been steadily growing

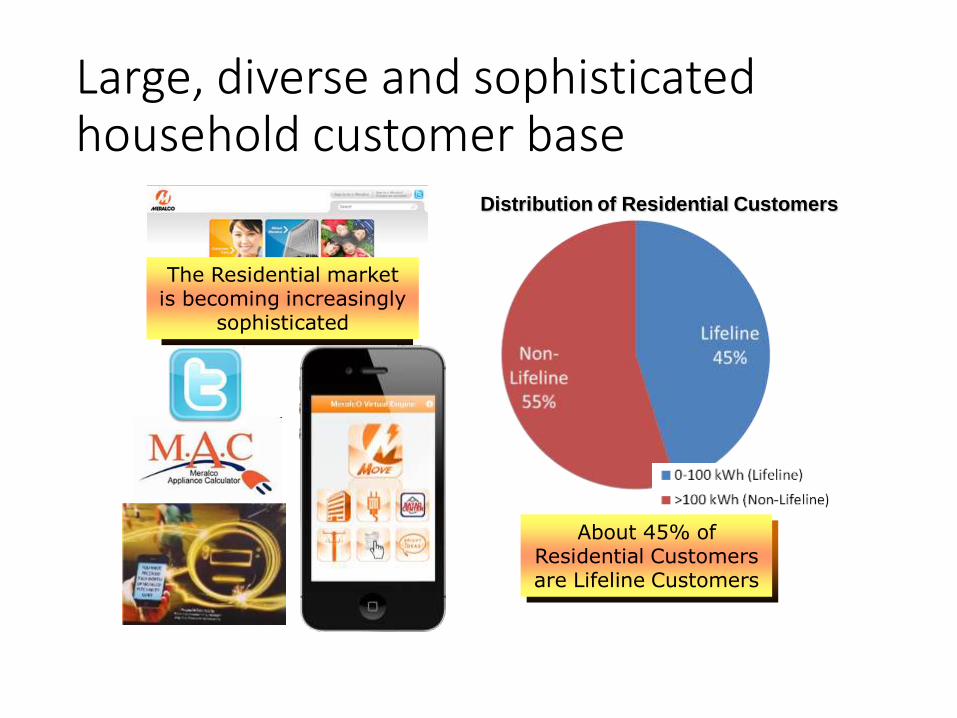

Large, diverse and sophisticated household customer base

The Residential market is becoming increasingly

sophisticated

About 45% of Residential Customers are Lifeline Customers

Distribution of Residential Customers

Meralco serves the country’s center of commerce & industry and its hub of government services & infrastructure

• Providers of outsourced business processes

• HQ of shared services of global companies

• Deustche Bank, Chevron, etc.

• Hotels & hospitals

• Telecoms & transportation

• Internet backbone, LRT & MRT, airport, etc.

• All major media companies

• Malacañang, Senate & House of Representatives, Supreme Court,

• Armed Forces, National Police & Office of Civil Defense

• PAG-ASA

11

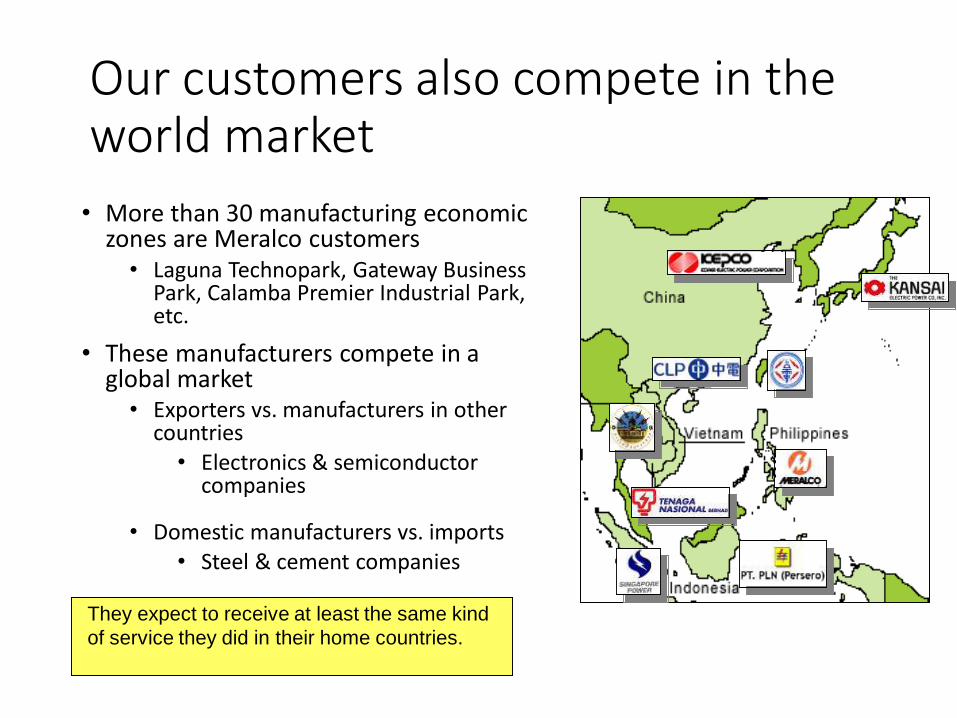

Our customers also compete in the world market

• More than 30 manufacturing economic zones are Meralco customers• Laguna Technopark, Gateway Business

Park, Calamba Premier Industrial Park, etc.

• These manufacturers compete in a global market• Exporters vs. manufacturers in other

countries • Electronics & semiconductor

companies

• Domestic manufacturers vs. imports • Steel & cement companies

They expect to receive at least the same kind

of service they did in their home countries.

Power Prices

12

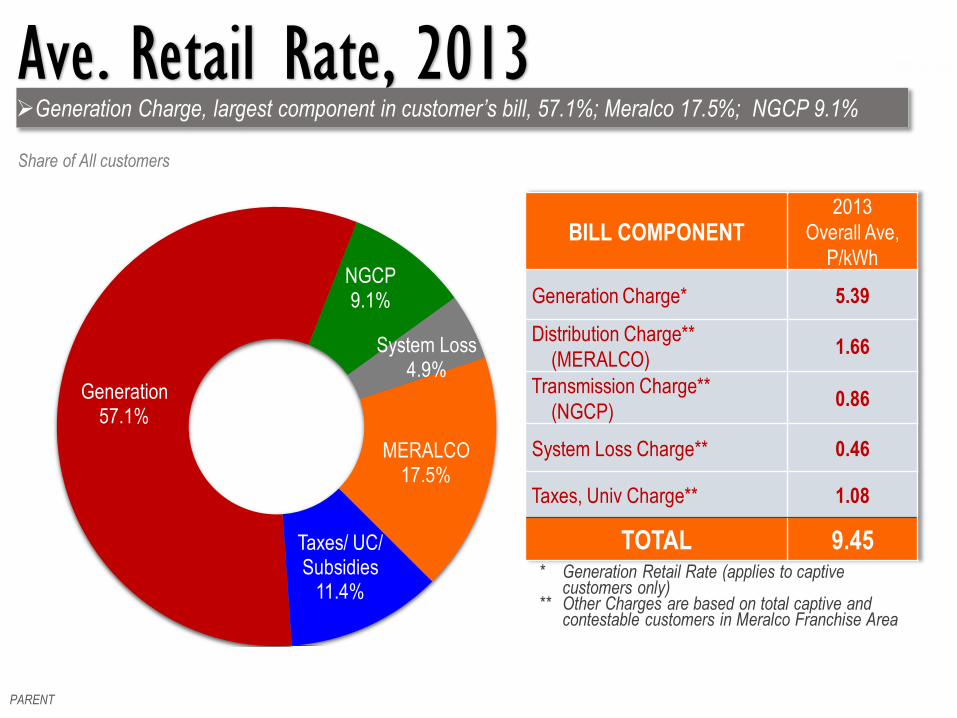

Ave. Retail Rate, 2013Generation Charge, largest component in customer’s bill, 57.1%; Meralco 17.5%; NGCP 9.1%

PARENT

* Generation Retail Rate (applies to captive customers only)

** Other Charges are based on total captive and contestable customers in Meralco Franchise Area

Generation57.1%

NGCP9.1%

System Loss4.9%

MERALCO17.5%

Taxes/ UC/ Subsidies

11.4%

Share of All customers

BILL COMPONENT2013

Overall Ave,

P/kWh

Generation Charge* 5.39

Distribution Charge**

(MERALCO)1.66

Transmission Charge**

(NGCP)0.86

System Loss Charge** 0.46

Taxes, Univ Charge** 1.08

TOTAL 9.45

Regional Comparison of Electricity PricesFindings of the International Energy Consultants

• Philippine tariffs are “fully cost-reflective, which is sound economic policy”• Policy is similar to Singapore, Japan, and Australia

• Rates in Thailand, Malaysia, South Korea, Taiwan, & Indonesia are low due to “government subsidies”• “Tariffs remain well below the cost”

• “Poor economic policy … unsustainable”

John Christopher Morris, Ph.D.

Managing Director

Comparison of Average Retail Electricity Tariffs

0.00

15.00

30.00

USc

/kW

h

Bundled excl taxes

Unbundled Generation

Unbundled Transmission

Unbundled Distribution

Other Taxes & Charges

Notes:

1. Weighted average tariff (all customer categories), excluding VAT

2. Tariffs are for January 2012

Source: International Energy Consultants

“Cost-reflective” “Government subsidized”

Government subsidies in other Countries• Subsidy is up to 54% of the power cost

• Subsidies are through: subsidized fuel, cash grants, additional

debt, deferred expenditures

Source: International Energy Consultants

•VAT•Royalty/Tax on

indigenous fuels or Duty/Tax on imported fuels

•Real Property Tax•Other taxes & fees

•3% franchise tax, in lieu of all other taxes

Transmission

•VAT•Local Franchise Tax on pass

through gen/ trans/ system loss charges *

•Local Franchise Tax on distribution charges

•Real Property Tax•Energy Tax on residentials•Universal Charges incl FIT•Other taxes & fees

* not applicable to electric coops

Distribution

DELIVERYGENERATION

Phl Power Market is a fully-priced market. No Subsidies and heavily “taxed”

The power sector is heavily taxed

Supporting Economic Development

18

Strategic Imperatives

• Given the strategic nature of Meralco’s market, power security and competitiveness are very critical concerns

• Adequate, reliable and reasonably priced power supply

• Customer-centric processes and systems

• Highly robust and customer responsive network and service infrastructure

Investing to support development

CPIP 115 kV Line, Calamba Premiere

Industrial Park (CPIP), Calamba, Laguna

Laguna Bel-Air Substation, Sta. Rosa, Laguna

Carmelray 83-MVA Bank No. 2, Carmelray

Industrial Park, Calamba, Laguna

5,430 5,339

6,099

6,869

9,175 8,890 9,053

8,748

10,321 10,187

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

CAPITAL EXPENDITURES(in millions of Pesos)

Constant improvement of electric service performance to meet more stringent customer needs

21

3

3.5

4

4.5

5

5.5

6

6.5

7

7.5

2009 2010 2011 2012 2013

Tim

es

SAIDI, Forced and PAI

90

100

110

120

130

140

150

2009 2010 2011 2012 2013

Tim

es

CAIDI, Forced and PAI

60

70

80

90

100

110

120

130

140

150

2009 2010 2011 2012 2013

Min

ute

s

SAIDI, Pre-arranged

SAIDI: System Average

Interruption Duration Index

CAIDI: Customer Average

Interruption Duration Index

Consistent reduction of system loss

11.10

10.21 10.109.65

9.28

8.617.94

7.35 7.04 6.92

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

System Loss Cap8.5%

9.5%

1.5

8%

Record low system loss of 6.92% in 2013

Enabling emerging technologiesRenewable Energy Act of 2008

RE Act

Fiscal IncentivesNon-Fiscal Incentives

Renewable Portfolio

Standards (RPS)

Feed-in-Tariff Scheme (FIT)

Net Metering

Green Energy Option

• Promotes the development and commercialization of

renewable energy resources

• Provides incentives to investors in renewable energy

Customer Exports Energy to the Distribution Network• Daytime with Energy generated by the Solar PV

• Household uses up a portion of the Energy generated by Solar PV for basic load

• Energy generated in excess of the Household load is exported to the Distribution Network

Customer Imports Energy from the Distribution Network• E.g., Night time with no Energy generated by the Solar PV

• Household Energy demand is supplied by the Distribution Network

Energy

Imported

Energy

Exported

₱kWh Imported

₱kWh Exported

₱Net Billed Amount

l e s s

Import Meter

Export Meter

Import Meter

Export Meter

Net Metering: Customer as SupplierFirst program of the RE Act to be implemented

Meralco Smart Grid Vision 2021

27