the proposal - supreme 2.0

DESCRIPTION

The Proposal- Including: the new product, the rationale, ansoff's matrix, USP, the mission statement, company objectives and strategy, the target demographic, the new range theme and range plan, boston matrix, sourcing strategy, critical path, pricing strategy, place and distribution strategy, brand positioning and DNA, competitors, promotional objectives and strategies, Financials, proposal SWOTTRANSCRIPT

SUPREME 2.0proposal

proposal reportAuthor: Bianca Hammond (0909167)Unit Leader: Mary Carson

efmm 3002 final major project

april 2012

Executive Summary // 005

Introduction // 006

the proposol

The New Product/Service // 008

Rationale // 009

Ansoff’s Matrix// 010

Wearable Technology Chart // 011

USP // 012

Which Markets // 013

THE COMPANY

Supreme 2.0- The New Label // 014

Mission Statement // 015

Objectives & Strategies // 016

the people

The Urban Elitist // 017

The Self-Promoters // 023

Generation Hactivate // 029

Demographics // 035

Economics // 036

Psychographic Profile // 037

Buying Attitude // 039

the product

Product Categories // 043

Theme: Industrial Revolution // 44

Range Plan // 046

Technical features // 052

Consumer Benefits // 055

Boston Matrix // 056

Sourcing Strategy // 057

Critical Path // 058

the price

Pricing Strategy // 059

Price Band Matrix // 061

THE place

Place and Distribution // 062

In-Store // 063

Visual Merchandising // 064

position

Streetwear Brand Positioning // 065

Key Streetwear Competitors // 066

Wearable Technology Market // 068

Alternative Products // 069

Staking our Position // 070

The Brand DNA // 071

PROMOTION

Promotional Objective // 072

The Strategy Overview // 073

Advertising // 075

Pr Activity // 077

Online Strategy // 079

The Launch Event // 081

financials

Capital Funding // 083

Financial Drivers // 084

proposal swot

Strengths // 085

Weaknesses // 086

Opportunities // 087

Threats // 088

conclusion

appendices

bibliography

THERE IS SOMETHING MISSING, A NEW THING COMES ALONG AND ADDRESSES THAT NEED, AND A MOVEMENT ARISES. PART OF THATENERGY THAT MAKES “COOL” IS FROM THE NOVELTY OF IT’S NEWNESS, THE FUEL OF CREATIVITY AS PEOPLE DISCOVER IT AND ADD TO IT.BUT SOMEWHERE AT THE ROOT OF THE MOVEMENT IS NEED.

- MARK LEWMAN- CREATIVE DIRECTOR OF COOL BRANDS

SUMMARY“Youth don’t buy stuff; they buy what stuff does for them” - Youth Mobile Report 2012

In an increasingly competitive and fragile market this statement is becoming increasingly true and it is important for brands to start thinking about what they can do for their consumer rather than what their consumer can do for them.

Following extensive research we found that the concept of ‘wearable technology’ was developing at a fast pace and predicted to transform the fashion industry in years to come. At present there is a gap in the market for an innovative forward thinking youth brand such as Supreme to be one of the first brands to bring ‘wearable technology’ to the commercial market. The intention is to develop a ‘new wave of wearable technology that prizes style, comfort and utility’ (Fastcompany) and then link these products back to social media in a way which is relevant and valuable to the youth demographic.

The target consumer is rapidly embracing technology and social media and viewing it as their ‘window of opportunity’ so products which incorporate this will have more ‘social currency’ and therefore a higher level of significance and relevance in the life of the youth consumer. The aim of the proposal centers on providing and communicating the multi functions and opportunities that both the brand and its products can provide for the consumer.

With the introduction of this new product range Supreme hope to carve out a strong and unique position-ing within the youth fashion market, differentiate from the competition, increase relevance and more importantly start thinking about how they can interact and collaborate with their consumer in order to develop a more meaningful and productive relationship.

executive

// 005figure 1

INTRODUCTIONFollowing extensive research and analysis into the youth fashion market it was revealed that there was a gap in the market for a niche youth brand to develop a product range based around wearable technology products which connect to social media. It was found that the growing importance of technology and social media in the lives of the youth consumer combined with their need to have the most exclusive and innovative products meant that a product extension into wearable technology was potentially a breakthrough idea.

The aim of this proposal is to filter down information gathered from the previous market research report and use it to develop a strong and impactful marketing plan to support the launch of the new product range as well as put the company in the best possible position to achieve it’s objectives.

The core focus of this report is the consumer. It is imperative that every idea, strategy or tactic to be implemented is created with the needs and wants of the consumer at heart.

The proposal will take shape by firstly introducing the new product followed by an introduction to the new Supreme 2.0 label who will launch the product. The marketing mix comes next where the target market will initially be identified before moving on to develop the product, price, place and promo-tional mix based around both the needs of the consumer as well as the brand identity guidelines.

The majority of the information which has been analysed to support this proposal has come from sources such as FutureLab and WGSN which offer insightful information into emerging consumer trends and attitudes. Thorough primary research has also been undertaken in order to get an even deeper understanding behind the thought processes of the target consumer. This type of information is key because at the core of this proposal is the needs of the consumer. With this information it has been possible to develop a consistent and cohesive strategy which has been tailored to meet the needs of the identified consumer.

// 006figure 2

the proposolThe Gap//The new product//Ansoff’s Matrix//USP//

// 006

wearable technology? social media? integration/connectivity?

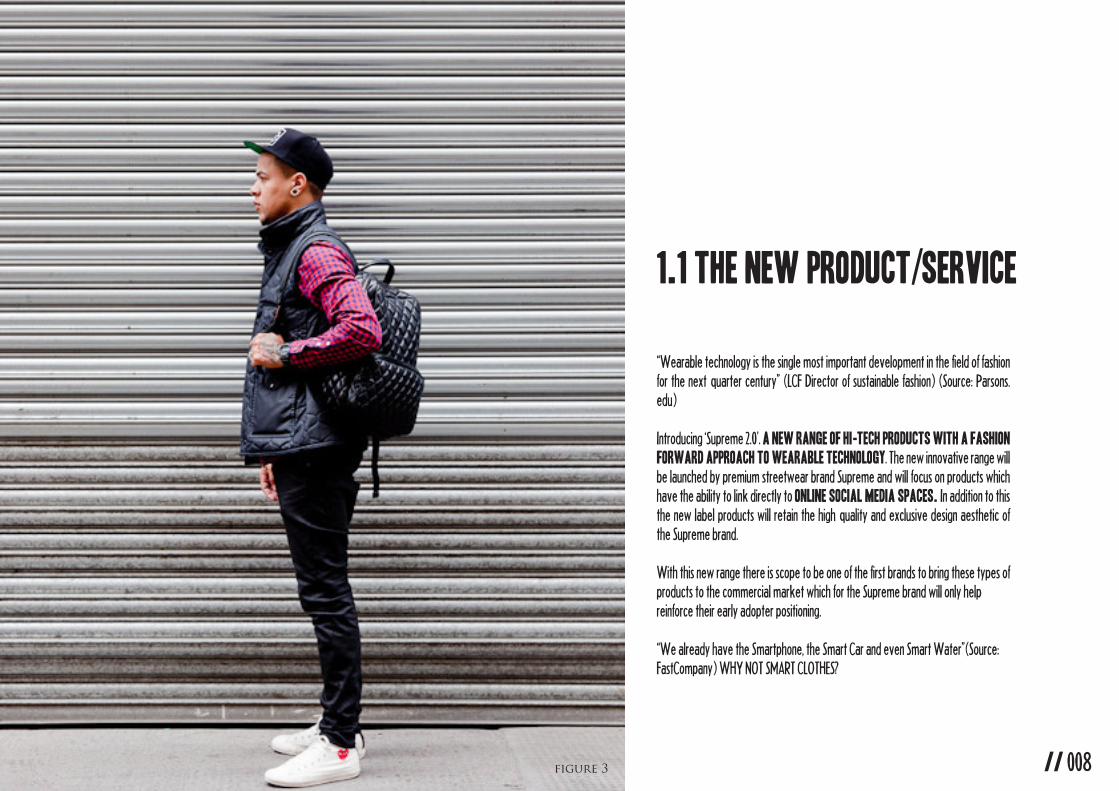

1.1 THE NEW PRODUCT/SERVICE

“Wearable technology is the single most important development in the field of fashion for the next quarter century” (LCF Director of sustainable fashion) (Source: Parsons.edu)

Introducing ‘Supreme 2.0’. A new range of hi-tech products with a fashion forward approach to wearable technology. The new innovative range will be launched by premium streetwear brand Supreme and will focus on products which have the ability to link directly to online social media spaces. In addition to this the new label products will retain the high quality and exclusive design aesthetic of the Supreme brand.

With this new range there is scope to be one of the first brands to bring these types of products to the commercial market which for the Supreme brand will only help reinforce their early adopter positioning.

“We already have the Smartphone, the Smart Car and even Smart Water”(Source: FastCompany) WHY NOT SMART CLOTHES?

// 008figure 3

Figure 38:http://supremeny.tum-blr.com

Three in ten (31%) male luxury goods buyers look for items showcasing advanced technical features or capabilities, contrasted to less than a fifth of female luxury shoppers. This reflects men’s greater interest in gadgets (Source: Mintel: Consumer attitudes towards luxury brands 2011)

growing numbers of men are choosing to buy fewer items but better quality clothing with more than one in five (22%) investing in quality garments this year compared to one in eight in 2010 (source: Mintel Mens Fashion lifestyles 2011)Market trend: Nextism: - the demand for new products with im-

proved features, updated design and novel enhanced experiences (Source: Trendwatching)

rationale

// 009

// 009

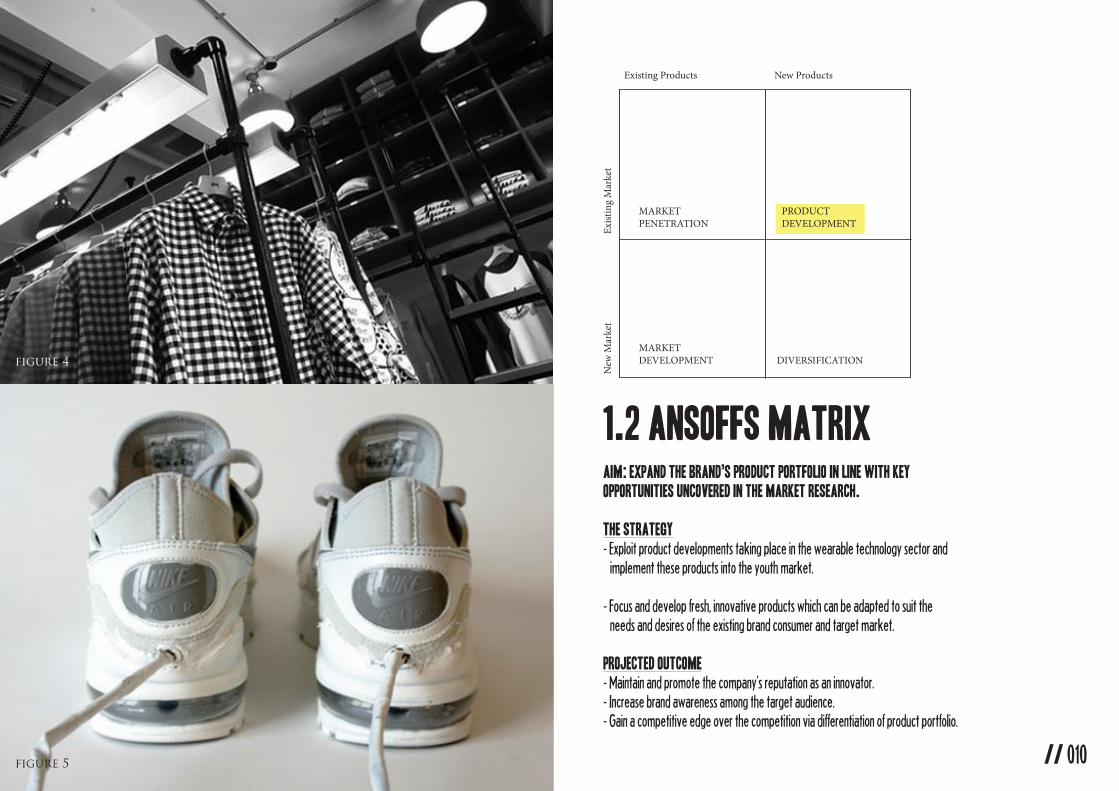

MARKETPENETRATION

PRODUCTDEVELOPMENT

MARKETDEVELOPMENT DIVERSIFICATION

Existing Products New Products

New

Mar

ket

Exist

ing

Mar

ket

1.2 ANSOFFS MATRIXAim: Expand the brand’s product portfolio in line with key opportunities uncovered in the market research.

The Strategy- Exploit product developments taking place in the wearable technology sector and implement these products into the youth market.

- Focus and develop fresh, innovative products which can be adapted to suit the needs and desires of the existing brand consumer and target market.

Projected Outcome- Maintain and promote the company’s reputation as an innovator.- Increase brand awareness among the target audience.- Gain a competitive edge over the competition via differentiation of product portfolio.

// 010

figure 4

figure 5

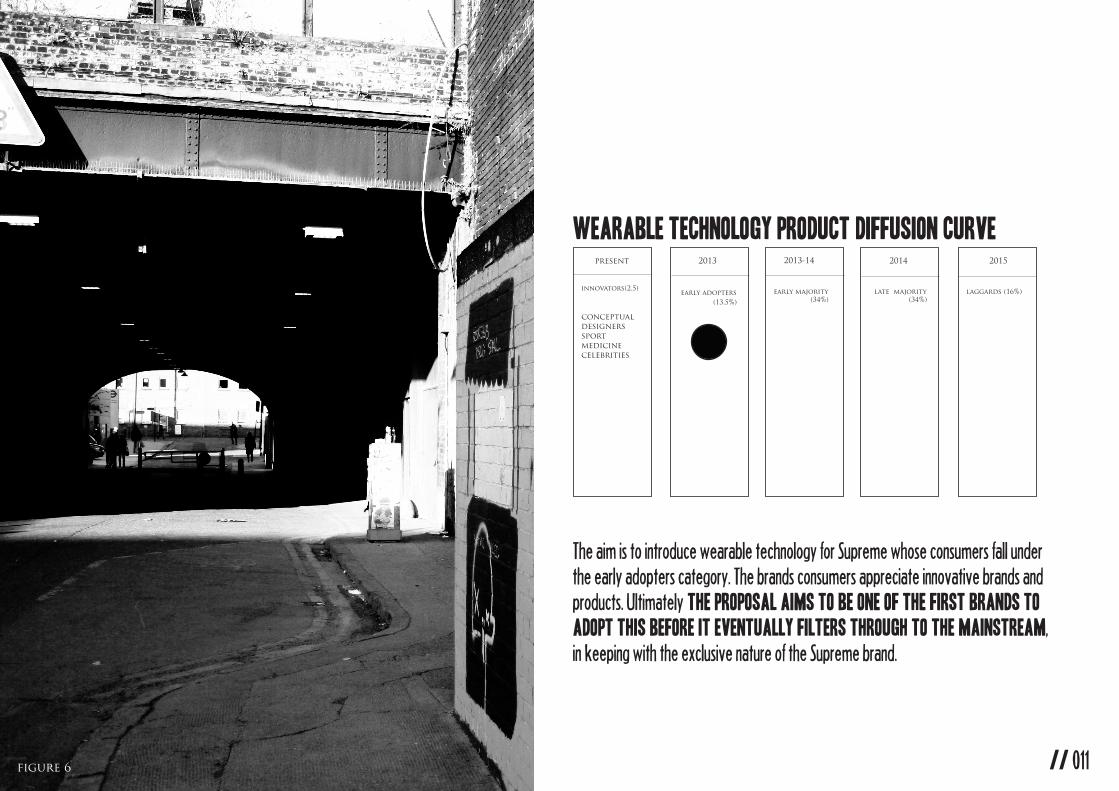

Wearable technology Product diffusion curve

present 2013 2013-14 2014

innovators(2.5)early adopters (13.5%)

early majority (34%)

late majority (34%)

laggards (16%)

conceptual designerssportmedicinecelebrities

The aim is to introduce wearable technology for Supreme whose consumers fall under the early adopters category. The brands consumers appreciate innovative brands and products. Ultimately the proposal aims to be one of the first brands to adopt this before it eventually filters through to the mainstream, in keeping with the exclusive nature of the Supreme brand.

2015

// 011figure 6

// 011

1.3 USP Supreme represents fresh ideas done right. They’re always one step ahead and always limited so people want it. With the 2.0 label the brand are not only using technology to interact with the consumers it’s become part of the brands products in a way which benefits and truly enriches the the brands consumers and community.

figure 7

// 013

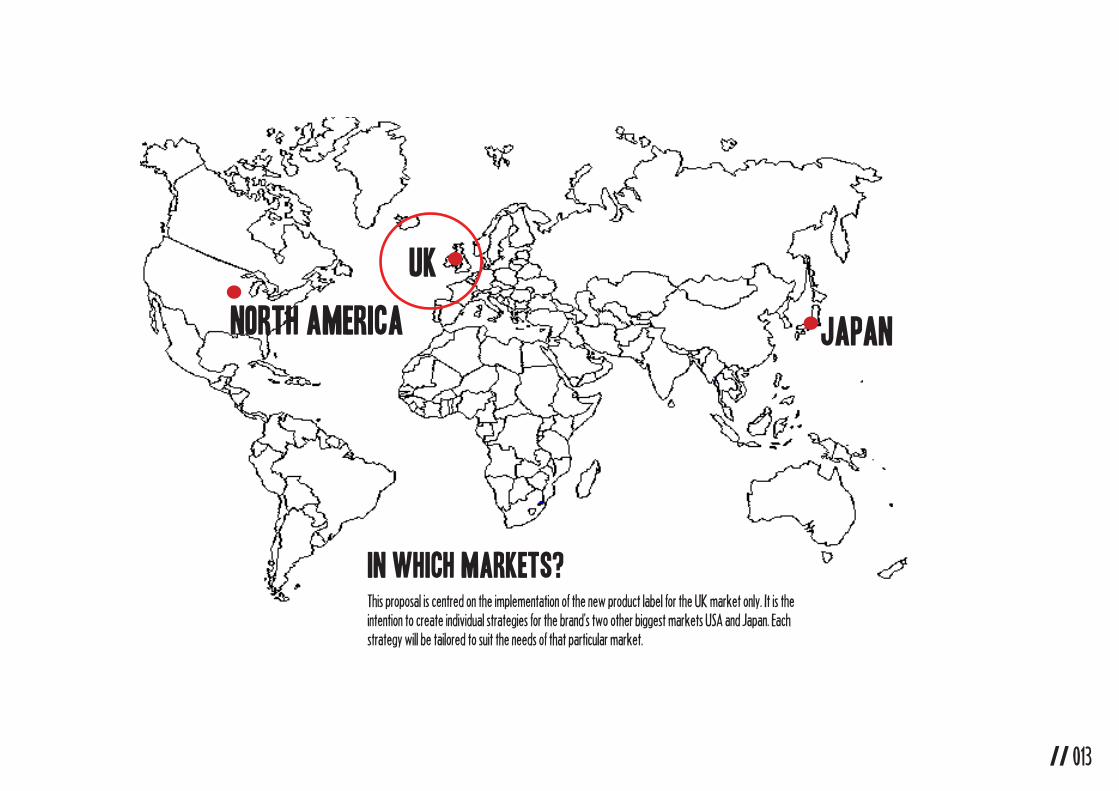

japan

uk

north america

in which markets?This proposal is centred on the implementation of the new product label for the UK market only. It is the intention to create individual strategies for the brand’s two other biggest markets USA and Japan. Each strategy will be tailored to suit the needs of that particular market.

// 013

the companysupreme 2.0//mission statement//company objectives//company strategy//

The next generation of streetwear. Supreme 2.0 is an innovative and experimental streetwear label with a focus on technology, digital media and the needs of a new generation of creative’s. We are the Supreme ruler of culture.

figure 8// 014

SUPREME 2.0the supreme ruler

of culture

// 014

2.1 MISSION STATEMENTSupreme 2.0 believe in championing product innovation and providing our consumerswith products which slot into their everyday lives with a higher purpose. Everything isappropriated, reconceptualised and refitted in Supreme’s hands to be made better.

figure 9 // 015

2.2 company strategy

objectives

Diversify the Supreme brand product portfolio in order to gain an edge over the competitors and retain a higher level of market share.

Reposition the Supreme brand as a cutting edge innovator within its nichesector. (The brand currently gets pigeon holed as ‘just a skatewear’ brand)’This perception should ideally be shifted.

Develop a higher brand awareness and demand amongst the target audience.

Focus on developing products based around the relevance to the consumer.

strategiesContinuously collaborate with product designers to ensure that the label is constantly launching fresh innovative and exclusive products.

Blink and you’ll miss it strategy- Production of small quantities and short product runs. This strategy is already adopted by the brand and will be implemented for the 2.0 label. The strategy helps to enforce the brands positioning as exclusive and encourages the need for consumers to buy immediately.

We plan to know as much as possible about our consumers so we can fulfil our objective of continually delivering the most relevant products.

Keeping an eye on the competition! We recognise the need to stay one step ahead of our competitors in order to win over the target market and capture a greater share of the market.

// 016

// 016

the peoplemarketing typologies//demographics//economics//psychographic//buying attitudes//

figure 10

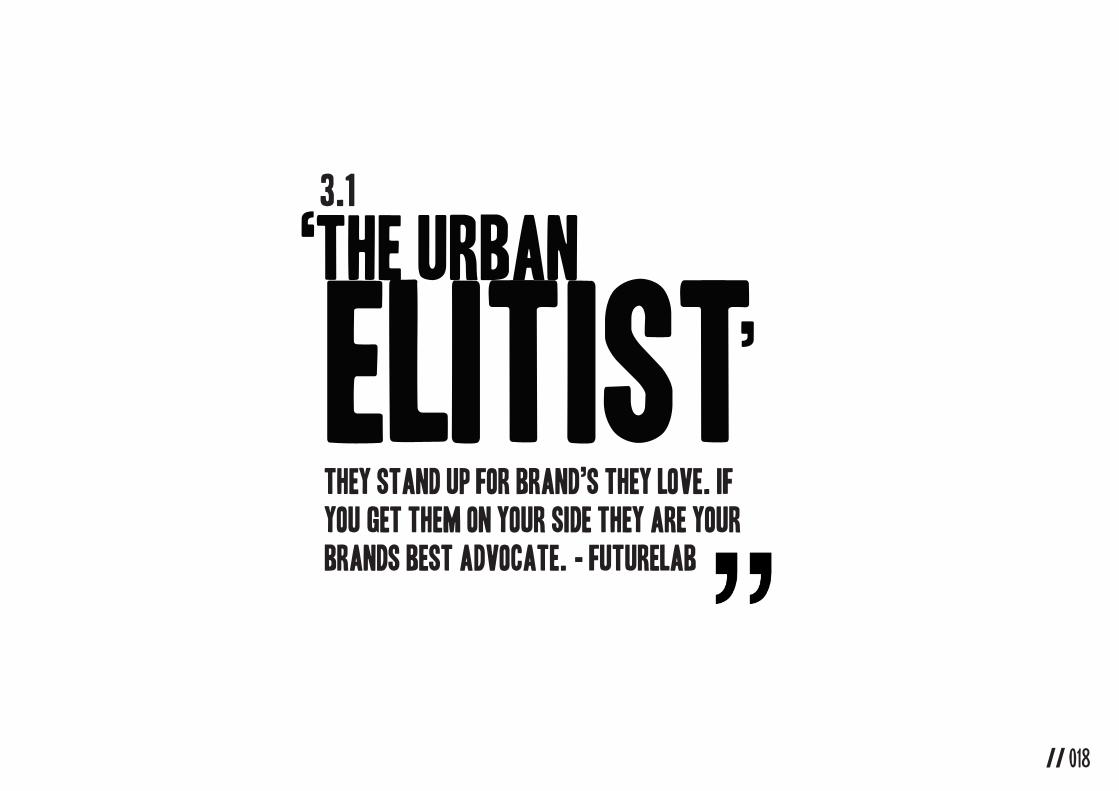

‘the urban

elitist’

THEY STAND UP FOR BRAND’S THEY LOVE. iF YOU GET THEM ON YOUR SIDE THEY ARE YOUR BRANDS BEST ADVOCATE. - FUTURELAB

// 018

3.1

they stand out to fit in.fitting in with their tribeof friends, while maintainingindividuality. (Source:ccbuzz)

figure 11

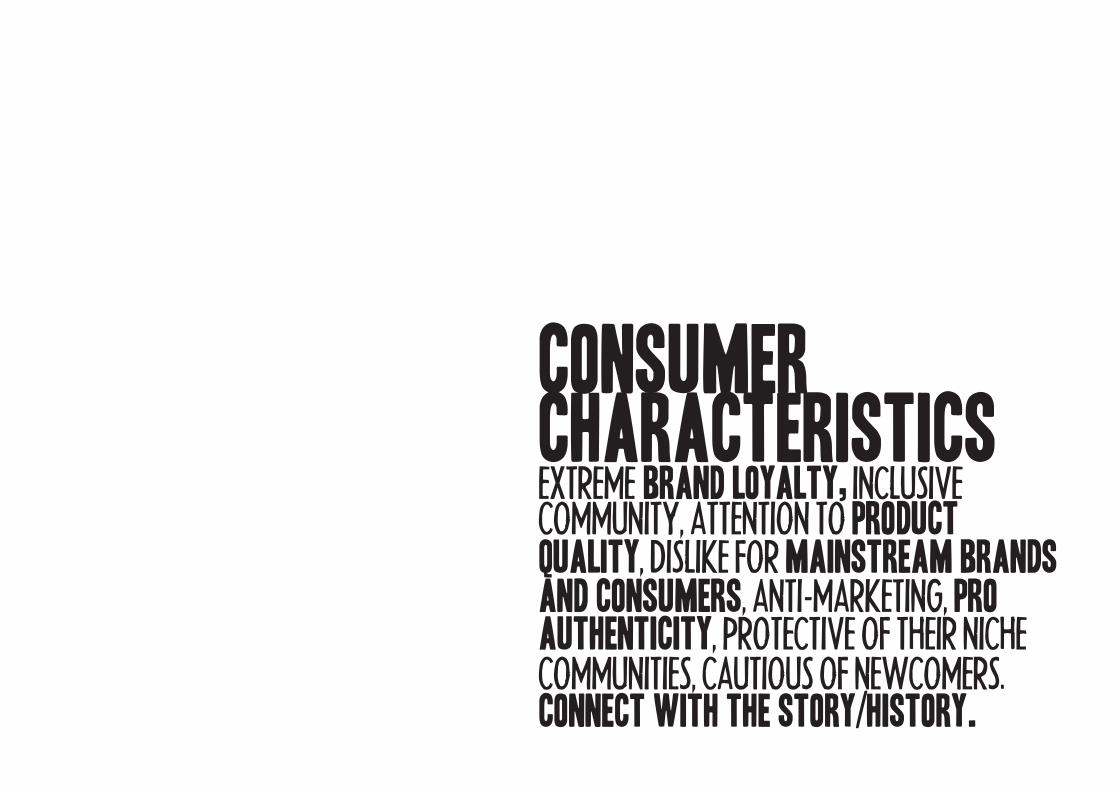

consumercharacteristicsEXTREME BRAND LOYALTY, INCLUSIVECOMMUNITY, ATTENTION TO PRODUCTQUALITY, DISLIKE FOR MAINSTREAM BRANDSAND CONSUMERS, ANTI-MARKETING, PROAUTHENTICITY, PROTECTIVE OF THEIR NICHECOMMUNITIES, CAUTIOUS OF NEWCOMERS.CONNECT WITH THE STORY/HISTORY.

// 020figure 12

The Urban Elitist uses social media to interact with likeminded individuals within their online niche communities. They regularly review, recommend and discuss their favourite brands and products.

social media & technology?

The Urban Elitist values brands that reflect their personality and lifestyle. They want strong brands with a strong and honest point of view. The Urban Elitist is not interested in trends; they are interested in the story, history and culture of a brand. The Urban Elitist wants great product design and great quality, fast fashion is not an option. In line with this they tend to be invest in premium status brands operating within a niche market.

ATTITUDE towards brands

// 022

figure 13

‘the SELF

PROMOTeR’

THE SELF-PROMoter’s are better educated, more selfesteemed, more demanding, more technologically savy, more empowered and more wired to win at thegame of life- fast company

// 024

3.1

figure 18

Creating empires founded on the cult of their personality

(Source:FutureLab)

figure 14

consumercharacteristicsOPTIMISTIC & ENTREPRENEURIAL, EARLYADOPTER, LOVE TECHNOLOGY AND GADGETS, PREFERS LIMITED EDITION PRODUCTS, SEES THEMSELVES AS TRENDSETTERS. HIGH ONLINEVISIBILITY, PLATFORMS FOR PERSONAL PROMOTION. FAVOUR ‘ENABLER’ BRANDS THAT ALLOW USERS TO CREATE THEIR OWN TERMS.

THE NEW MILLENNIALS LOVE FORTECHNOLOGY IS NOW BEDDING ITSELF DOWN AS THE WAY THINGS SHOULD BE DONE (Source:FutureLab)

figure 15

social media and technologyThe Self-Promoters are using social media mainly as a platform to promote themselves and gain exposure. They recognise the opportunities that can be gained from it and are utilising these tools in order to try and build a future for themselves. As well as this the Self-Promoter uses social media for inspiration and to connect and collaborate with other likeminded people. For example WGSN’s ‘Tumblr Tribes’ describes various online youth communities who use the social media platform Tumblr as a place to creatively share images, ideas and inspirations.

Unlike the Urban Elitist the Self-Promoter is not so rigidly brand loyal. However if a brand continues to put out innovative and exclusive merchandise they will continue to shop with that brand. The Self-promoter likes to mix and match and generally shops in high street, premium and luxury sectors. For the ‘Self promoter’ it’s all about how much ‘social currency’ a brand can offer them. They like to think of themselves as trendsetters and are keen to get their hands on the latest products on the market. Every brand they purchase from is an extension of their personal brand and how they wish to portray themselves, so selection is crucial.

attitude towards brands

// 028

87.1% OF THE TARGET GROUP SURVEYED SAID THAT THEY VIEW THE INTERNET AS A TOOL FOR PROMOTING THEMSELVES - Survey Results (2011)

figure 16

‘generation

hactivate’

digitally engaged twenty something’s and teens who are putting their own mark on the ways in which technology gets developed and in turn getsshaped into consumable products- wgsn

// 030

3.1

figure 17

consumercharacteristicsREBELLIOUS CREATIVES, EXPRESSION OFTHEIR PERSPECTIVE. TECHNOLOGICALLYADVANCED,RESPECT FOR INNOVATION, DIY ATTITUDE, LEADERS NOT FOLLOWERS, COMMUNITY BASED INITIATIVES.

figure 18

Generation Hactivate are at the forefront of all the latest and cutting edge aspects of technology and digital media. This group use social media for inspiration, research and information. Like the Self-promoters social media is also very important to Generation Hactivate in terms of promotion and exposure. They are keen to express their ideas and visions through this medium.

Generation Hactivate are drawn to products and brands that adopt fresh and innovative approaches. This group are conceptually driven, they like to think outside of the box and they expect brands to, too. In addition they are keen to interact and collaborate with brands onprojects. Generation Hactivate are active individuals, they thrive on being a part of the process.

social media & technology

attitude towards brands

// 034

HAVING GROWN UP IN A DIGITAL AGE THEY AREHARDWIRED INTO THE MAIN FRAME OF INTERNET CULTURE. INSTRUMENTAL IN SHAPING A NEW FRONTIER OF HUMAN INTERACTION VIA DIGITALTECHNOLOGY. (Source:FutureLab)

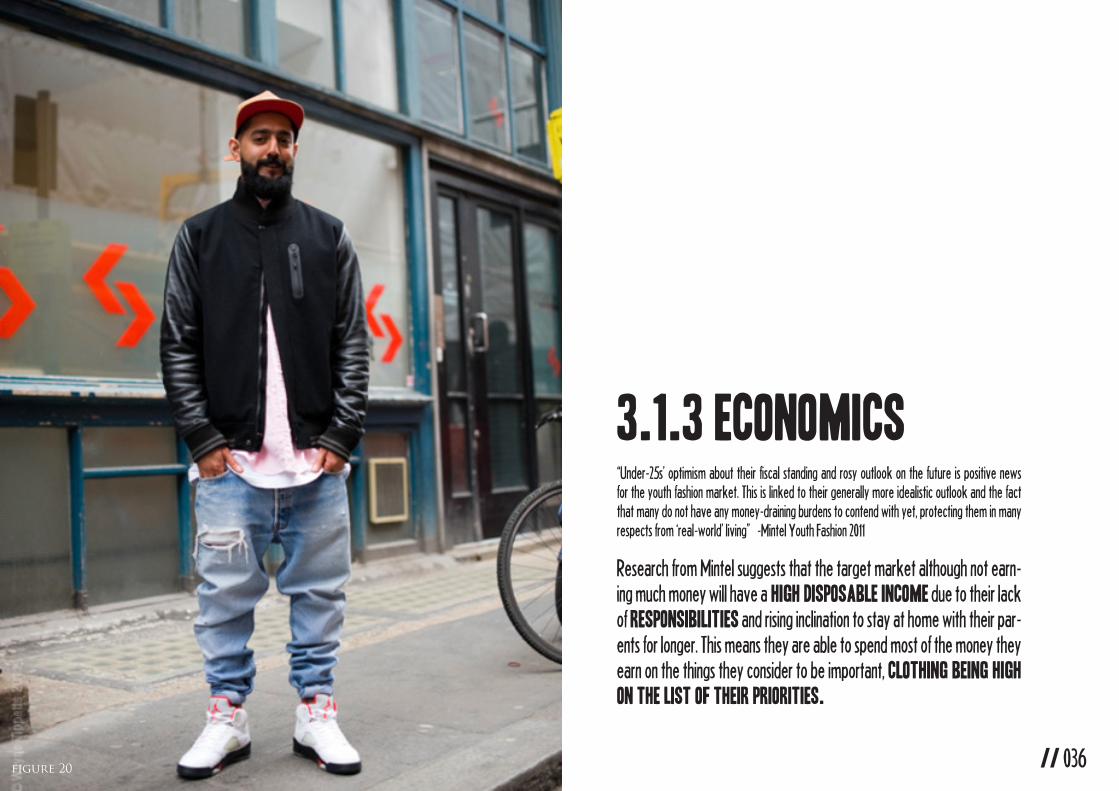

3.1.2 demographics//age: 18-30 years oldgender: malelocation: london/large uk cities

figure 19

3.1.2 demographics//age: 18-30 years oldgender: malelocation: london/large uk cities

Research from Mintel suggests that the target market although not earn-ing much money will have a high disposable income due to their lack of responsibilities and rising inclination to stay at home with their par-ents for longer. This means they are able to spend most of the money they earn on the things they consider to be important, clothing being high on the list of their priorities.

“Under-25s’ optimism about their fiscal standing and rosy outlook on the future is positive news for the youth fashion market. This is linked to their generally more idealistic outlook and the fact that many do not have any money-draining burdens to contend with yet, protecting them in many respects from ‘real-world’ living” -Mintel Youth Fashion 2011

3.1.3 economics

// 036figure 20

figure 21

// 038

The target consumer falls into the early adopter category. As identified in the marketing typologiesthis group of consumer’s value and seek out exclusive brands and products. They like things that express innovation or creativity and so tend to latch on to emerging trends much earlier than the mainstream market.

3.1.4 Psychographic profile

figure 21a

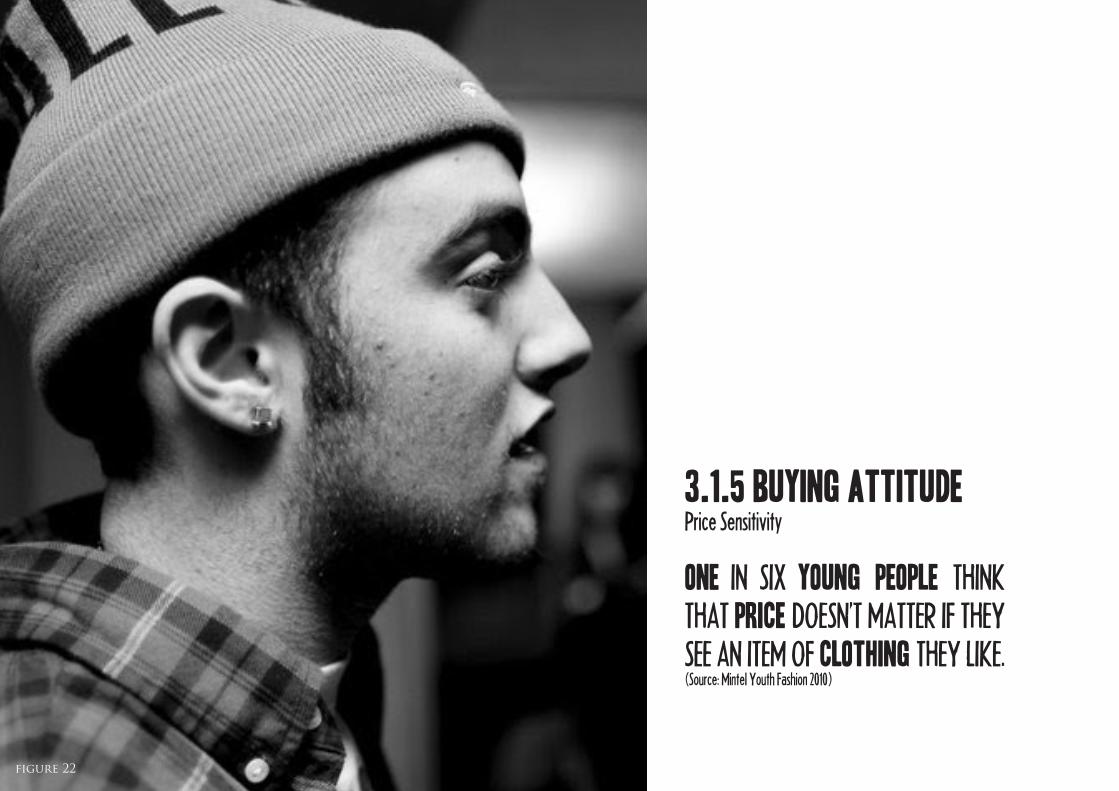

One IN SIX YOUNG PEOPLE THINK THAT PRICE DOESN’T MATTER IF THEY SEE AN ITEM OF CLOTHING THEY LIKE.(Source: Mintel Youth Fashion 2010)

3.1.5 Buying AttitudePrice Sensitivity

figure 22

3.1.5 Buying AttitudePrice Sensitivity

THE 16-24S TEND TO BE BRAND LOYAL AND ARE SIGNIFICANTLY MORE LIKELY THAN OVER 25s (32% V 20%) TO BUY FROM FAMILIAR BRANDS AND SHOPS THEY TRUST.(Source: Mintel Clothing retail 2011)

3.1.5 Buying AttitudeBrand Loyalty

figure 23

“Nobody is out there to help us ” So this generation is primarily driven by the desire of fulfillment”

Source: TheNewConsumerfigure 23

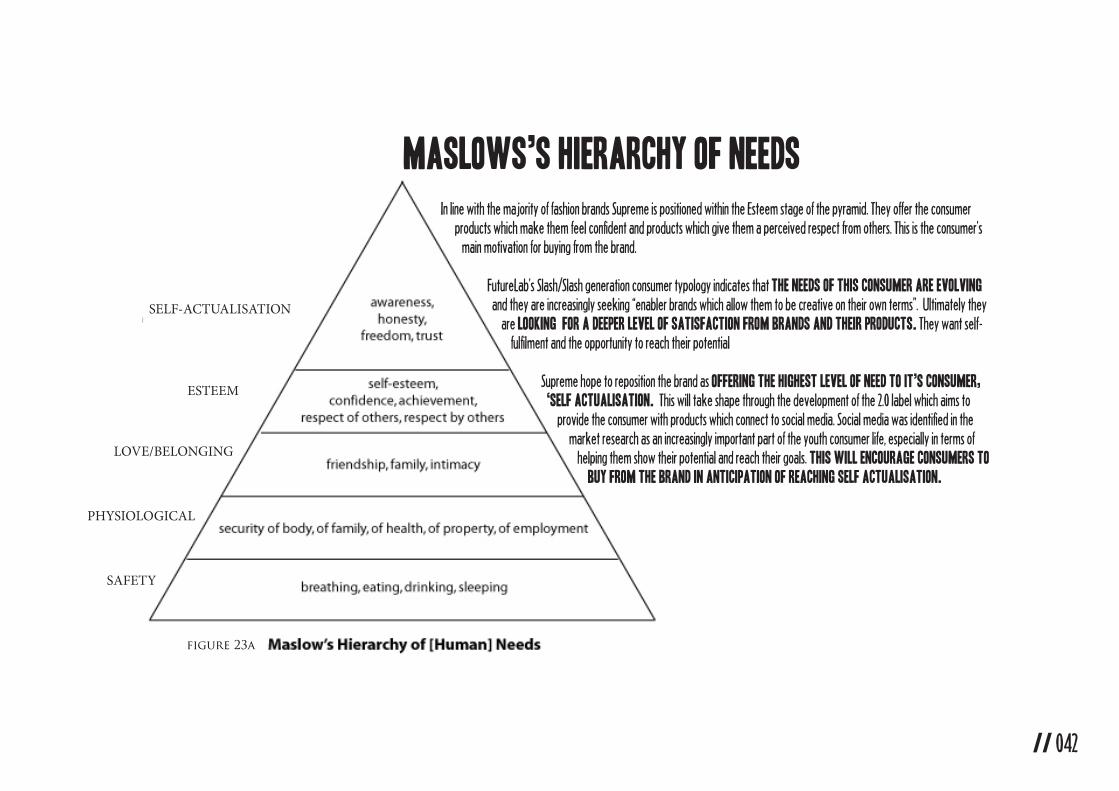

LOVE/BELONGING

SAFETY

PHYSIOLOGICAL

SELF-ACTUALISATION

ESTEEM

Maslows’s Hierarchy of NeedsIn line with the majority of fashion brands Supreme is positioned within the Esteem stage of the pyramid. They offer the consumer products which make them feel confident and products which give them a perceived respect from others. This is the consumer’s main motivation for buying from the brand.

FutureLab’s Slash/Slash generation consumer typology indicates that the needs of this consumer are evolving and they are increasingly seeking “enabler brands which allow them to be creative on their own terms”. Ultimately they are looking for a deeper level of satisfaction from brands and their products. They want self- fulfilment and the opportunity to reach their potential

Supreme hope to reposition the brand as offering the highest level of need to it’s consumer, ‘Self Actualisation. This will take shape through the development of the 2.0 label which aims to provide the consumer with products which connect to social media. Social media was identified in the market research as an increasingly important part of the youth consumer life, especially in terms of helping them show their potential and reach their goals. This will encourage consumers to buy from the brand in anticipation of reaching Self Actualisation.

// 042

figure 23a

productthe product//the range plan//technical features//consumer benefits//boston matrix//sourcing strategy//

4.2.1 The product categories.The Supreme 2.0 label is compromised of wearable technology items such as the ‘The Bloggers backpack’, The E-charge Backpack and The video stream sunglasses (Refer to technical features) as well as non-tech-nical items such as T-shirts and Snapbacks.

Quality is King!Quality and design are a core focus for the new product range in line with expectations identified at the focus group stage where it was found that the consumer wanted great design and quality first and foremost.

Design directionThe new range is influenced heavily by the aesthetics of the classic Supreme label. Supreme 2.0 takes the classic minimalism of Supreme and updates it with edgy high end features to give it an even more exclusive and premium feel.

FabricsFor the AW13 collection fabric and texture are key elements of the design. The collection makes use of hardwearing fabrics such as mesh and denim mixed with luxurious trimmings such as leather to bring out the raw but premium design direction.

“Design wise I would appreciate some-thing more sleek and high quality but at the same time casual” -

Leon - Focus Group

“Without great design I’m not sure that I would solely buy based on concept” - Simon - Focus Group

// 043

revolutionindustrialthe a/w13 range theme

figure 24

figure 25

4.2.2 RANGE PLAN FOR SUPREME 2.0 LABEL A/W13 COLLECTION

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME2.0

SUPREME2.0

SUPREME2.0

SUPREMEStudio Label 2.0

SUPREME 2.0studio label

SUPREME 2.0studio label

STYLE SKETCH FABRIC COLOUR SIZES rrp

onesize

onesize

onesize

onesize

£190

£190

£210

£250

£60.80

£60.80

£67.20

£80.00

£60.00

£60.00

£65.00

£70.00

68.42%

68.42%

72%

69.05%

90

90

70

50

5,400.00

5,400.00

3,750.00

3,500.00

17,100,00

17,100,00

12,500,00

14,700,00

68.42%

68.42%

69.05%

72%

‘NEO’ backpack

‘CYPHER’ backpack

‘NEORELOADED’backpack

‘TURBO’backpack

cotton

leather

tetra//44% polyethylene33% polyester19% cotton

polyester

tull glamour//58% polyester42% metal

denim

leather

tull glamour//58% polyester42% metal

leather

tetra//44% polyethylene33% polyester19% cotton

68% actual margin total total totalmargin cost achieved quantity cost retail margin

greyblack

greyblack

grey/bluesilver

silver

68% actual margin total total totalmargin cost achieved quantity cost retail margin

onesize

onesize

onesize

onesize

onesize

£110

£160

£160

£35 £25 77.27%

£51.20

£51.20

100 11,000.00 77.27%

£35 78.13% 78.13%

£35 78.13% 78.13%

60

40

2,500.00

2,100.00 9,600.00

1,400.00 6,400.00

‘TURBOii’backpack

‘TITUS’backpack

‘MORPHEUS’backpack

‘MORPHEUS ii’backpack

‘galatic’backpack

£250 £80 £75 70% 40 3,000.00 10,000.00 70%

£110 £35.20 £25 77.27% 150 3,750.00 16,500.00 77.27%

leather

tetra//44% polyethylene33% polyester19% cotton

polyester

leather

denim

tetra//44% polethylene33% polyester19% cotton

leather

tetra

polyester

STYLE SKETCH FABRIC COLOUR SIZES rrp 68% actual margin total total totalmargin cost achieved quantity cost retail margin

navy bluesilverblack

light grey

bluegrey

greyblack

78%

78%

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

s,m,l

s,m,l

s,m,l

s,m,l

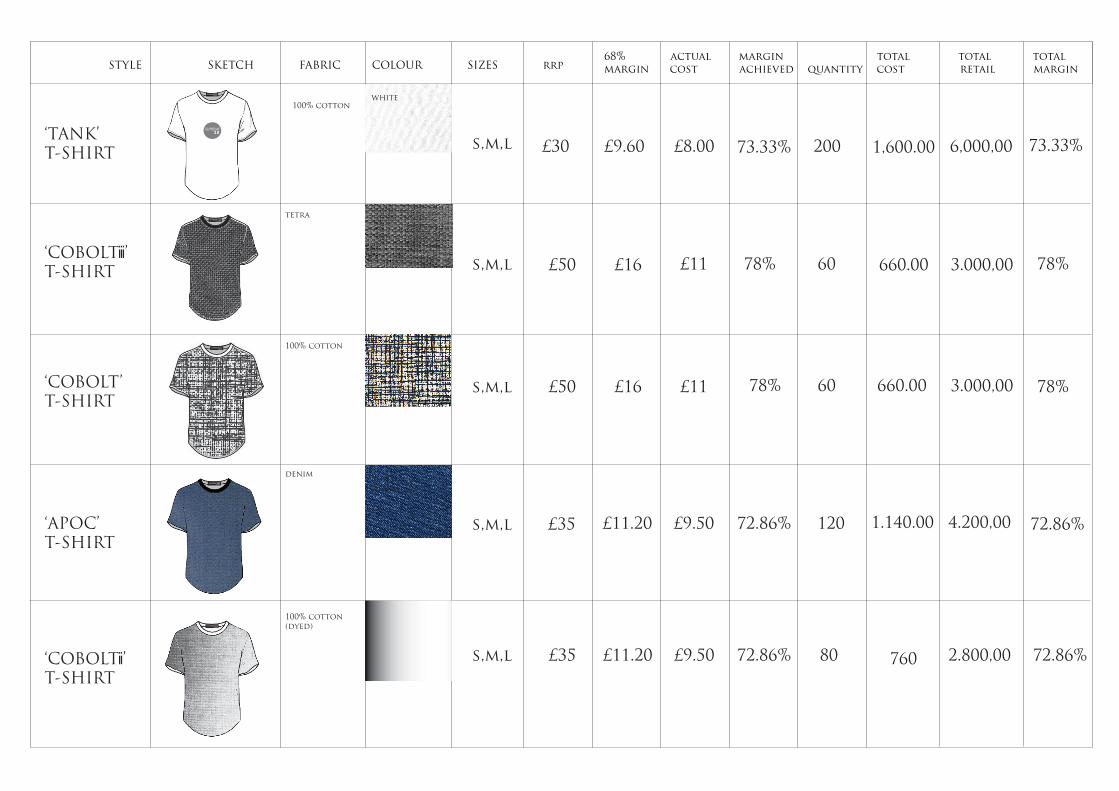

£30 £9.60 £8.00 73.33% 200 1,600.00 6,000,00

£50

£50

£16

£16

£11

£11 78%

78% 60

60

660.00

660.00

3.000,00

3.000,00

£35

£35

£11.20

£11.20

£9.50

£9.50

72.86%

72.86%

120

80

1.140.00

760

4.200,00

2.800,00

72.86%

72.86%

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0‘TANK’

T-SHIRT

‘APOC’T-SHIRT

‘COBOLT’T-SHIRT

‘COBOLTiii’T-SHIRT

‘COBOLTii’T-SHIRT

s,m,l 73.33%

100% cotton

tetra

100% cotton

denim

100% cotton(dyed)

68% actual margin total total totalmargin cost achieved quantity cost retail margin STYLE SKETCH FABRIC COLOUR SIZES rrp

white

bluedenim

s,m,l

s,m,l

s,m,l

s,m,l

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME2.0

SUPREME2.0

SUPREME2.0

SUPREMEStudio Label 2.0

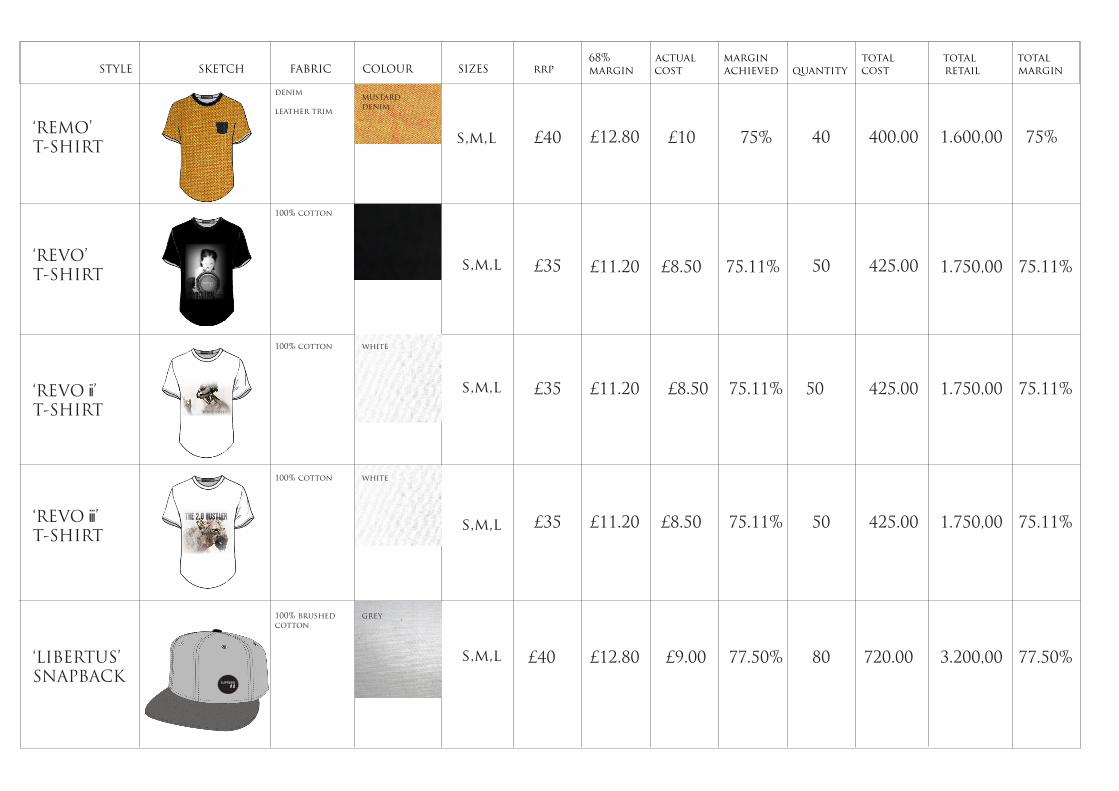

s,m,l £40 £12.80 £10 75% 40 400.00 1.600,00 75%

£35 £11.20 £8.50 75.11% 50 425.00 1.750,00 75.11%

£35 £11.20 £8.50 75.11% 50

50

425.00

425.00

1.750,00

1.750,00

75.11%

75.11%75.11% £8.50 £11.20£35

£40 £12.80 £9.00 77.50% 80 720.00 3.200,00 77.50%

‘REMO’T-SHIRT

‘REVO’T-SHIRT

‘REVO ii’T-SHIRT

‘REVO iii’T-SHIRT

‘LIBERTUS’SNAPBACK

denim

leather trim

100% cotton

100% cotton

100% cotton

100% brushed cotton

STYLE SKETCH FABRIC COLOUR SIZES rrp 68% actual margin total total totalmargin cost achieved quantity cost retail margin

mustarddenim

white

white

grey

onesize

onesize

onesize

onesize

onesize

£45

£45

£50

£14.40

£14.40 £9.50

£9.50

78.89%

78.89% 60

40

£570.00

£380.00

2.700.00 78.89%

1.800.00 78.89%

£16.00 £11.00 78% 60 £660.00 3.000.00 78%

£45 £14.40 £10.50 76.67% 60 £630.00 2.700.00 76.67%

£250 £80 £75 70% 150 11.250.00 37.500.00 70%

‘MAXXUM’SNAPBACK

‘ORACLE’SNAPBACK

‘FUTORIA’SNAPBACK

‘GRAXX’SNAPBACK

‘XYCLOP’GLASSES

brushed cotton

leather

denim

leather

tetra

brushed cotton

denim

leather

STYLE SKETCH FABRIC COLOUR SIZES rrp 68% actual margin total total totalmargin cost achieved quantity cost retail margin

Total 1,800 £51.505 £191.650

mustard

silver

navy

blue

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME2.0

SUPREME2.0

SUPREME2.0

SUPREMEStudio Label 2.0

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label SUPREME 2.0

studio label

SUPREME 2.0studio label

SUPREME 2.0

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME 2.0studio label

SUPREME2.0

SUPREME2.0

SUPREME2.0

SUPREMEStudio Label 2.0

SUPREME 2.0studio label

SUPREME 2.0studio label The Feature

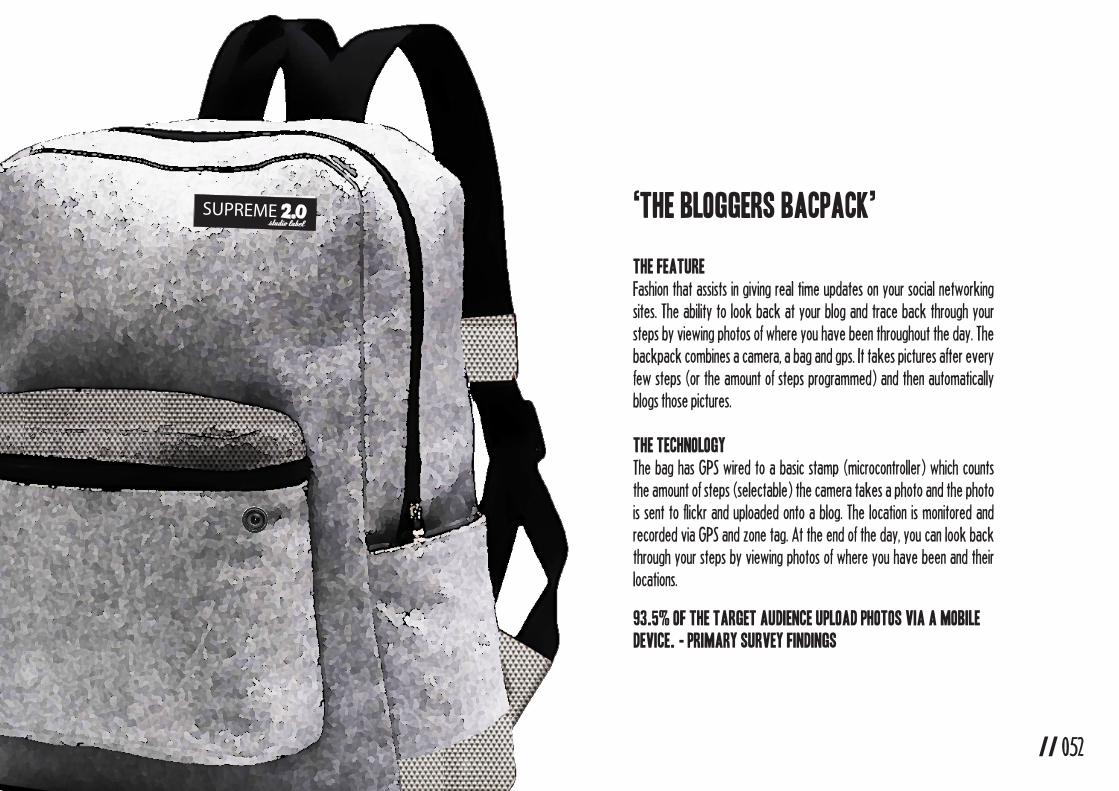

Fashion that assists in giving real time updates on your social networking sites. The ability to look back at your blog and trace back through your steps by viewing photos of where you have been throughout the day. The backpack combines a camera, a bag and gps. It takes pictures after every few steps (or the amount of steps programmed) and then automatically blogs those pictures.

The technologyThe bag has GPS wired to a basic stamp (microcontroller) which counts the amount of steps (selectable) the camera takes a photo and the photo is sent to flickr and uploaded onto a blog. The location is monitored and recorded via GPS and zone tag. At the end of the day, you can look back through your steps by viewing photos of where you have been and their locations.

‘THE BLOGGERS BACPACK’

93.5% of the target audience upload photos via a mobile device. - primary survey findings

// 052

93.5% of the target audience upload photos via a mobile device. - primary survey findings

THE TECHNOLOGYIts Bluetooth and Wi-Fi capable for instant media transfers tocomputers and most Iphone and Android devices. And with the Eyez mobile app, you can instantly broadcast the video footage in real time to your favourite social networking sites.

‘THE VIDEO STREAM SUNGLASSES’

THE FEATURERecord whats happening around you and upload in real time. A solution for capturing moments without compromising style or convenience. the latest innovation in personal video recording technology. a hd camera embedded within a pair of glasses designed to record live video data and take pictures.

45.2% of the target audience upload video via a mobile device - primary survey findings.

// 052 // 053

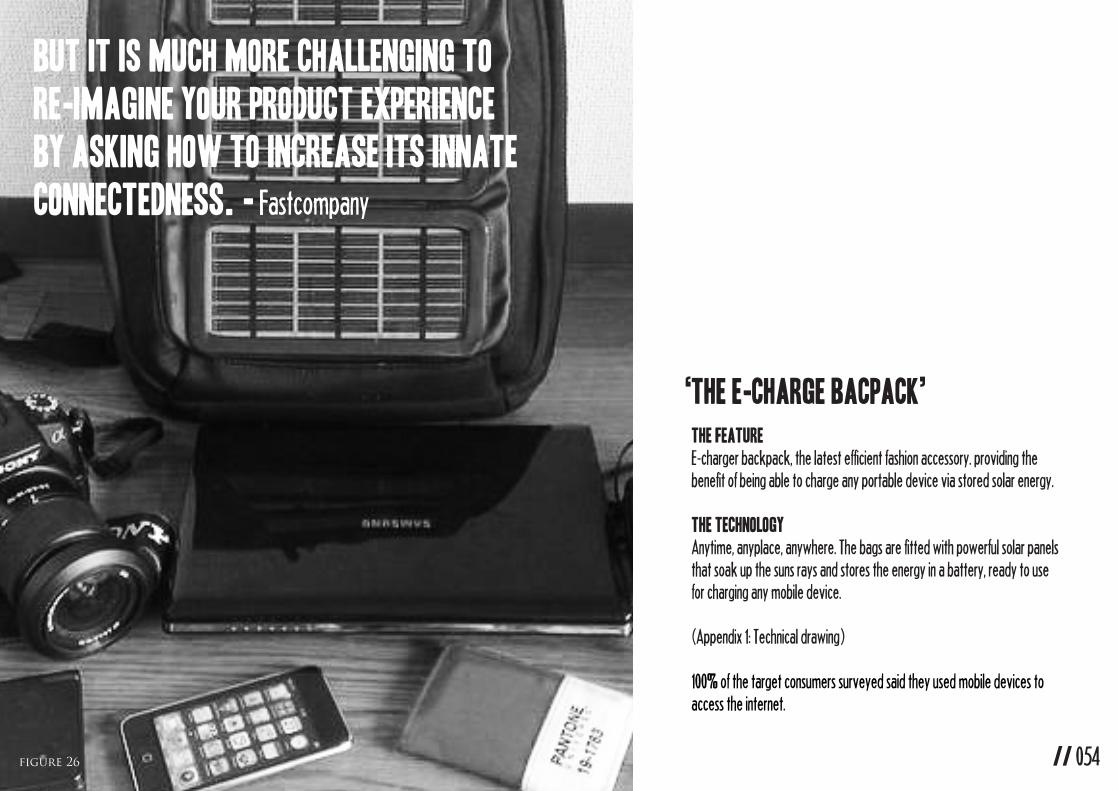

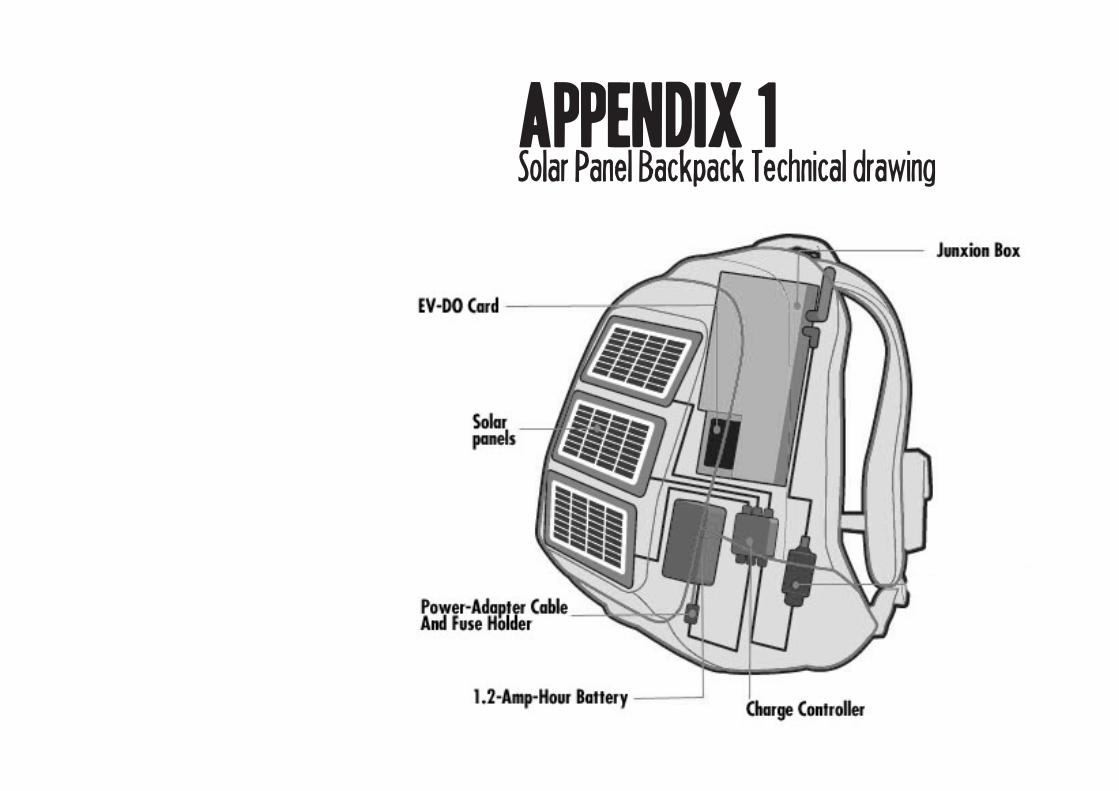

THE FEATUREE-charger backpack, the latest efficient fashion accessory. providing the benefit of being able to charge any portable device via stored solar energy.

THE TECHNOLOGYAnytime, anyplace, anywhere. The bags are fitted with powerful solar panels that soak up the suns rays and stores the energy in a battery, ready to use for charging any mobile device.

(Appendix 1: Technical drawing)

100% of the target consumers surveyed said they used mobile devices to access the internet.

‘THE E-CHARGE BACPACK’

figure 26

But it is much more challenging to re-imagine your product experience by asking how to increase its innate connectedness. - Fastcompany

// 054

‘Marketing is not about providing products or services it is essentially about providing changing benefits tothe changing needs and demands of the customer’(P.Tailor 7/00)

// 054

figure 27

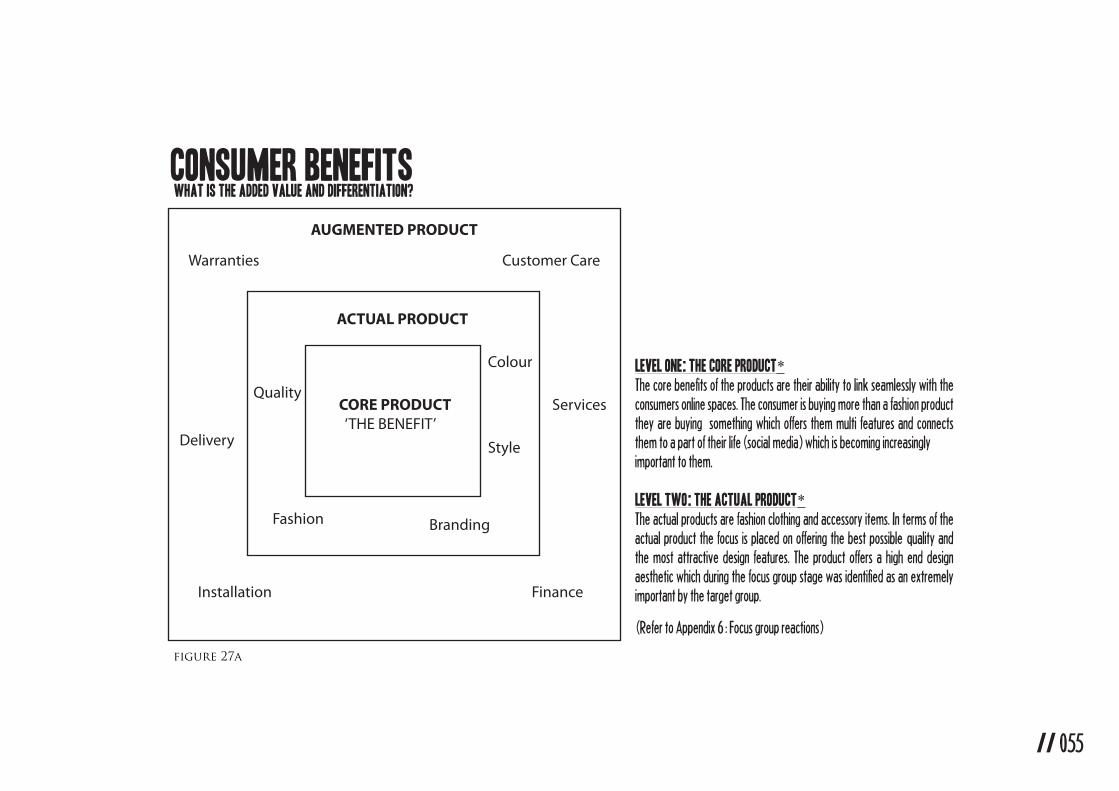

CORE PRODUCT ‘THE BENEFIT’

ACTUAL PRODUCT

Colour

Style

BrandingFashion

Quality

Customer Care

FinanceInstallation

Services

Delivery

Warranties

AUGMENTED PRODUCT

LEVEL ONE: THE CORE PRODUCT*The core benefits of the products are their ability to link seamlessly with the consumers online spaces. The consumer is buying more than a fashion product they are buying something which offers them multi features and connects them to a part of their life (social media) which is becoming increasingly important to them.

level two: the actual product*The actual products are fashion clothing and accessory items. In terms of the actual product the focus is placed on offering the best possible quality and the most attractive design features. The product offers a high end design aesthetic which during the focus group stage was identified as an extremely important by the target group.

consumer benefitsWhat is the added value and differentiation?

(Refer to Appendix 6 : Focus group reactions)

// 055

figure 27a

figure 28

reasoning for the development of this new product

The classic Supreme range is currently classed as a problem child for the brand. It has a relatively strong position in the streetwear fashion market and therefore market share is high. However the streetwear market in general is in decline (Refer to market research)

For premium streetwear brands the future outlook is tough. The industry is becoming increasingly competitive, espe-cially since it has low barriers to entry. This has caused a continuous in stream of new streetwear brands popping up on the market.

With this new product range the brand are spreading the risk and hoping to offset the sales decline in the streetwear market. Product extension into the developing market of wearable technology appears to be a good move for the brand. It is a fairly untapped market and so there is potential for the brand to win a high share of the market.

It also creates a stronger positioning for the brand in the streetwear market where the new products will offer the brand a strong USP and therefore the competitive edge over other brands.

boston matrix

SUPREME2.0

// 056

figure 28a

4.2.3 sourcing strategyThe technology based products will require a longer lead time and will beproduced in Cambodia with a lead time of 4 months from initial order to delivery. For these products which are not trend led and are based on short runs (will not be repeated) a sourcing strategy of long lead times works well. There is no urgency to produce these items quickly. The lead time has also been made long in order to factor in the unique production requirements of the products as well as product testing procedures.

For the non-technological items such as the T-shirts and Snapbacks a short lead time strategy will be implemented. (a maximum of 1 month) This is be-cause these items are fairly easy to make and unlike the technological items are not based on short-runs (have the possibility of being reproduced/ordering more quantities) and therefore shorter lead times are preferable in order to achieve a healthy supply and demand balance.

// 057figure 29

// 057

The Critical Path

CORPORATE STRATEGY

STREET STYLERESEARCH

MARGIN(LONDON)TRADESHOW

CONCEPTDEVELOPMENT

RANGE PLANFINALISED

RAISE ORDERSFROM SUPPLIERS(long lead time products)

FINAL ORDERCOMPLETE. BOTH SHORT & LONG TERMPRODUCTS.

RAISE ORDERSFOR SHORT TIME LEAD PRODUCTS.

TRANSPORTATION TOTHE UK.

QUALITY CONTROL& PRODUCT TESTING HOLD IN STORAGE

ADVERTISE/PROMOTELAUNCH PRODUCTSIN-STORE

REPLENISH BEST-SELL-ING NON-TECHNICALSEASON STARTS

ANALYSE CLEAR SEASON ENDS.

FIRST PROTOTYPE & ADJUSTMENTS.(long lead time products)

// 058

pricepricing strategy//price band matrix//

4.3 pricing strategy

// 059

Supreme 2.0 will adopt a premium pricing strategy considering that the product offering is unique and of a premium quality.

Price elasticity of demand- The new product range is price inelastic (a high price tag does not affect the quantity demanded substantially) due to the fact that there are relatively few substitute products on the market and because the product offerings are unique. Therefore a premium pricing strategy becomes justified due to the unique nature of the products.

The nature of the product- The price range is not substantially outside of the price bracket of the classic Supreme range and these products have the added benefit of the technical features. If the consumer is willing to pay for the classic Supreme range it is likely they will be willing to invest a little more in the 2.0 label considering that the new products have more features. This can be backed up by the primary research which indicated that the consumer was willing to pay a premium price for the product.

The reputation of the brand- The pricing is standard for the Supreme brand. It’s consumers expect premium pricing from the brand and in terms of maintaining the brands premium position the pricing will continue to reflect this.

What the market will bear- The pricing has also been benchmarked against the pricing of similar products on themarket. So for example research indicates that the alternative E-charge backpacks are being sold anywhere from £40 (by a no name label) upwards to £800 by RLX Ralph Lauren. These factors have been taken into consideration and priced accordingly and in a way which best represents the brands identity and positioning.

“AS LONG AS THE DESIGN IS STRONG I WOULD PAY AT THESE PRICES.SIMiLAR ITEMS I OWN ARE AROUNd THESE PRICES ANYWAY. IT’S MORE ABOUT THE QUALITY AND DESIGN FOR ME MORE THAN ANYTHINg”- Leon - Focus Group

figure 30

The non-technical products such as the t-shirts and snapbacks have been introduced and priced at the lower end of the pricing scale. This strategy has been adopted in order to add more accessibility to the consumer. The introduction and pricing of these non-technical items will also help the brand to generate more profit and volume sales from the new product range.

bloggers backpack

e-charge backpack

sunglasses

t-shirts

snapbacks

£190 £250

£110 £160

£250

£30 £50

£40 £50

lowest price highest price

// 061

placeplace strategy//the distrubution //instore//visual merchandising//

“tHE STORE IS NOT ONLY A PLACE WHERE WE SELL PRODUCTS BUT ITS A STRONG COMMUNICATION TOOL AND A CHANCE TO GENERATE, EXCITING BRAND EXPERIENCES FOR THE CUSTOMER” figure 31

// 062

The Supreme 2.0 product range will be sold via the existing Supreme brand store based in London alongside the original label products. This is the Supreme’s only UK store and all Supreme products are sold exclusively here. When the product is limited to one store only the availability of the product becomes less accessible. This is consistent with the brand strategy which aims to retain an element of exclusivity. The Supreme 2.0 label and its products are aimed at a niche audience who seek brands and products which are limited and less mainstream.

Buyer behaviour- The consumer prefers to buy from a small retailer because they value a personal, real-life interactive sales service.

Manufacturer retailer consumer

The brand will adopt a direct retail channel distribution strategy whereby the brand sells straight to the consumer. Supreme will sell the 2.0 label products through the existing Supreme London retail store which is directly owned and operated by the brand. This type of distribution strategy is beneficial in terms of, exercising complete control over brand identity and in-store brand experience. It is also beneficial for, obtaining better quality information from the market and the ability to read sell out figures every day. This type of distribution strategy allows the brand to be closer to the consumer and will give a deeper level of insight into the needs and wants of the consumer.

4.4 Place distribution

// 062 figure 51

The selection of sales force and sales technique is an extremely important element of the place strategy. The brand needs to create a friendly tight knit community like store experience. The sales team need to represent the identity of the Supreme brand in order for them to communicate effectively with the consumer.

Product Knowledge- The sales staff will be given training in order to have a good knowledge of the new products and their technical features. Sales staff with product knowledge is especially important when dealing with technical items.

In terms of the competition many of the streetwear brands do not have stores in the UK and sell via multi brand retailers. This gives Supreme 2.0 an advantage in the fact that we can create an in-store brand experience and interact with the target market in a way that they cannot.

in-store

figure 32

3.6.4 vm//In terms of the store visual merchandising, no drastic changes will be made to the Supreme London store. The upstairs part of the store will be dedicated to the new 2.0 label range.

This section of the store will consist mostly of display cases and stands that will hold the new products.. For example Snapbacks and Sunglasses will be placed in these museum style display cases. While the backpacks will be placed on stands and shelves within their individual packaging boxes.

figure 33// 064

positionstreetwear positioning//the competitors//wearable technology//staking our position//the brand dna//

// 064

figure 34

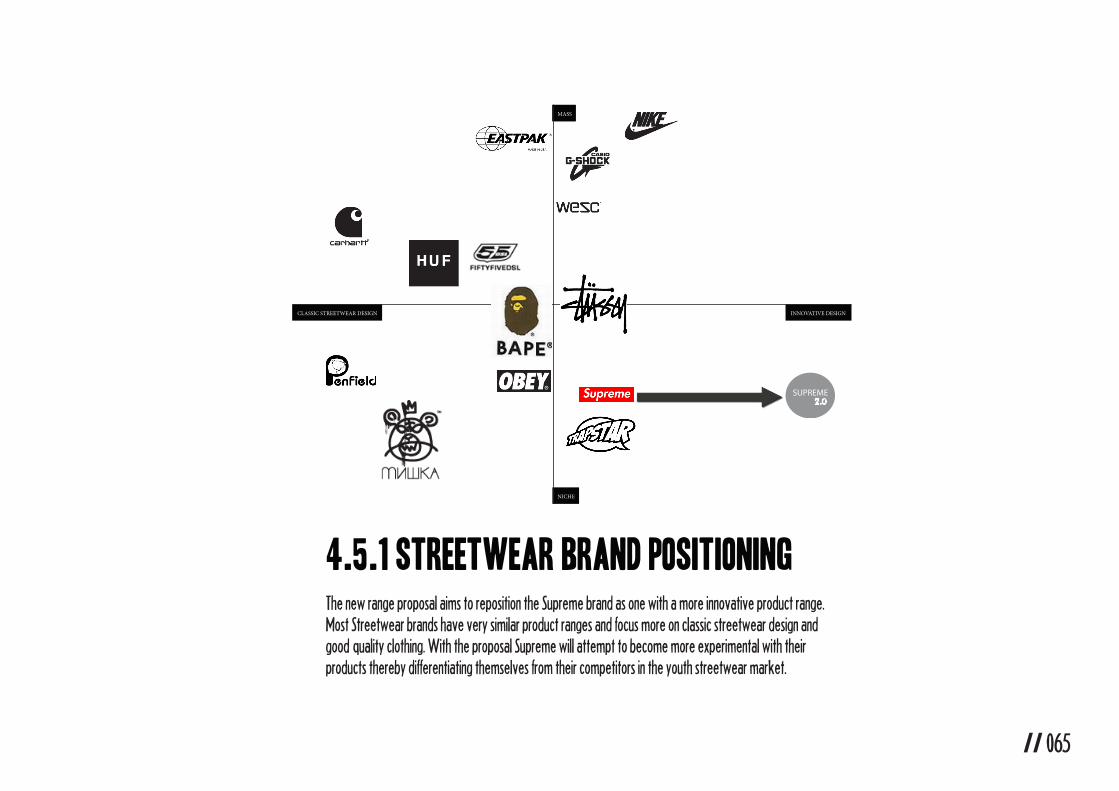

4.5.1 Streetwear brand positioningThe new range proposal aims to reposition the Supreme brand as one with a more innovative product range. Most Streetwear brands have very similar product ranges and focus more on classic streetwear design and good quality clothing. With the proposal Supreme will attempt to become more experimental with their products thereby differentiating themselves from their competitors in the youth streetwear market.

// 065figure 34

MASS MASS

NICHE

INNOVATIVE DESIGN CLASSIC STREETWEAR DESIGN

SUPREME2.0

figure 35

// 067

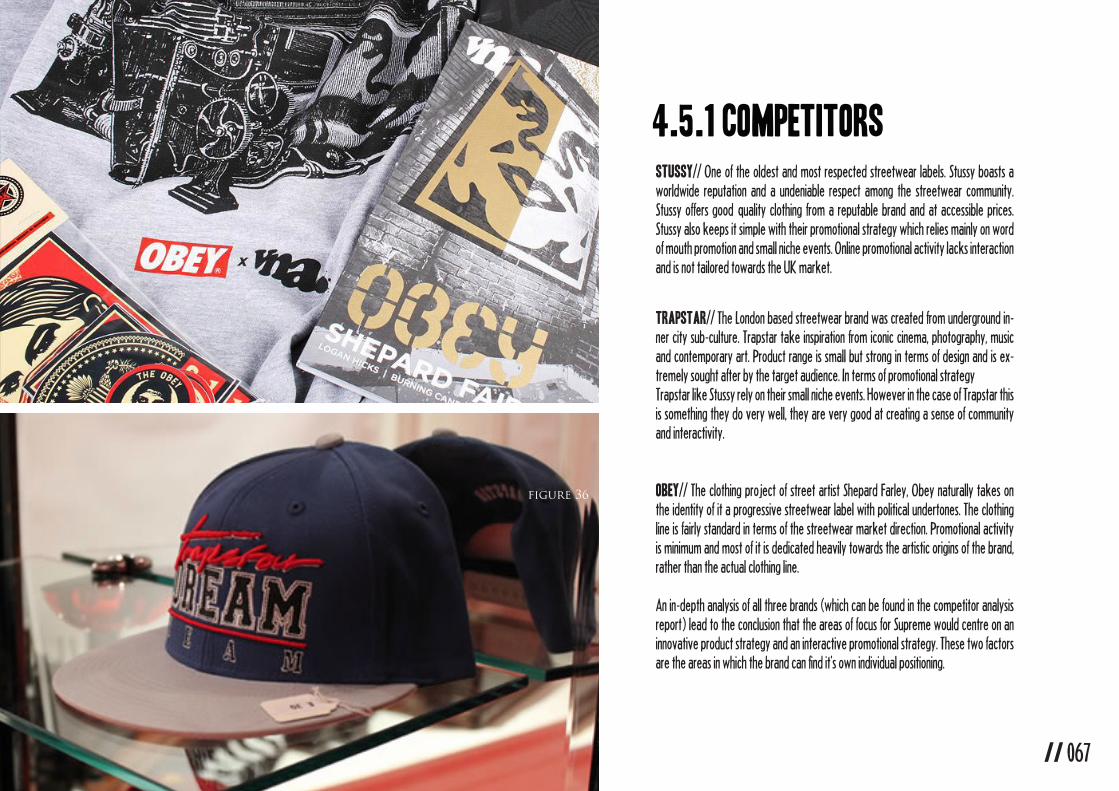

Stussy// One of the oldest and most respected streetwear labels. Stussy boasts a worldwide reputation and a undeniable respect among the streetwear community. Stussy offers good quality clothing from a reputable brand and at accessible prices. Stussy also keeps it simple with their promotional strategy which relies mainly on word of mouth promotion and small niche events. Online promotional activity lacks interaction and is not tailored towards the UK market.

Trapstar// The London based streetwear brand was created from underground in-ner city sub-culture. Trapstar take inspiration from iconic cinema, photography, music and contemporary art. Product range is small but strong in terms of design and is ex-tremely sought after by the target audience. In terms of promotional strategy Trapstar like Stussy rely on their small niche events. However in the case of Trapstar this is something they do very well, they are very good at creating a sense of community and interactivity.

Obey// The clothing project of street artist Shepard Farley, Obey naturally takes on the identity of it a progressive streetwear label with political undertones. The clothing line is fairly standard in terms of the streetwear market direction. Promotional activity is minimum and most of it is dedicated heavily towards the artistic origins of the brand, rather than the actual clothing line.

An in-depth analysis of all three brands (which can be found in the competitor analysis report) lead to the conclusion that the areas of focus for Supreme would centre on an innovative product strategy and an interactive promotional strategy. These two factors are the areas in which the brand can find it’s own individual positioning.

figure 36

4.5.1 competitors

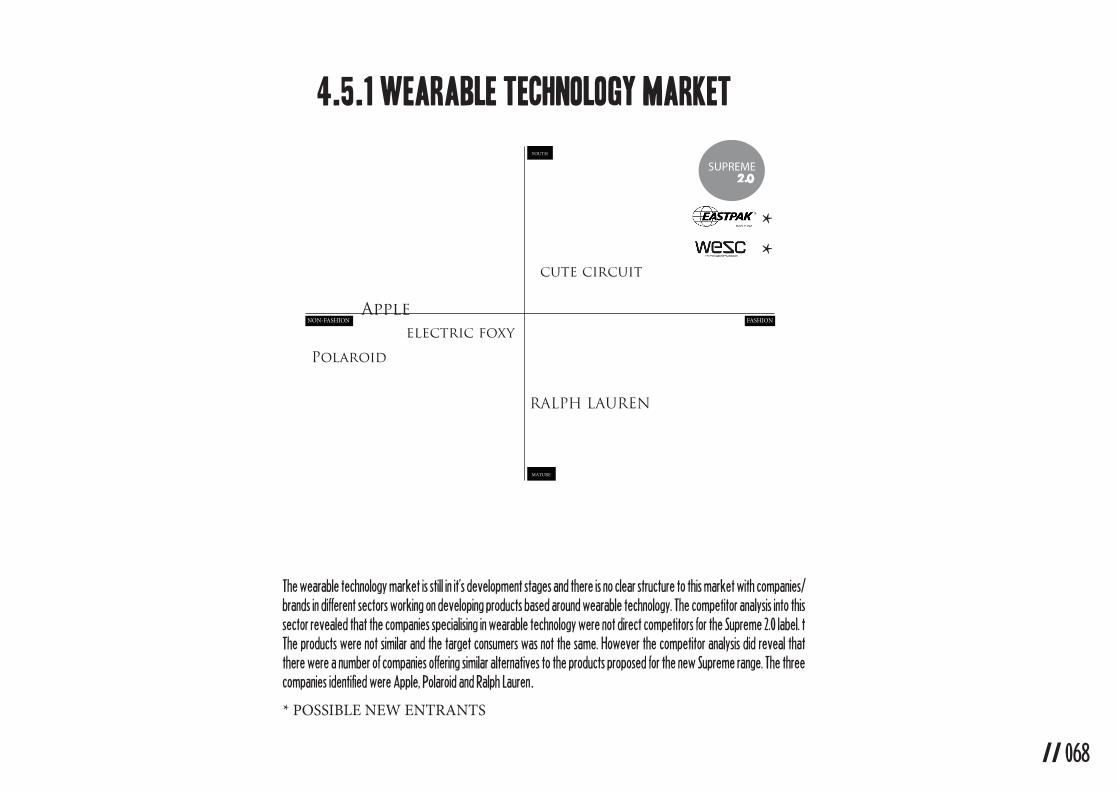

4.5.1 wearable techNOLOGY MARKET

YOUTH

MATURE

NON-FASHION FASHION

electric foxy

Apple

Polaroid

cute circuit

SUPREME2.0

RALPH LAUREN

**

The wearable technology market is still in it’s development stages and there is no clear structure to this market with companies/brands in different sectors working on developing products based around wearable technology. The competitor analysis into this sector revealed that the companies specialising in wearable technology were not direct competitors for the Supreme 2.0 label. tThe products were not similar and the target consumers was not the same. However the competitor analysis did reveal that there were a number of companies offering similar alternatives to the products proposed for the new Supreme range. The three companies identified were Apple, Polaroid and Ralph Lauren.

* POSSIBLE NEW ENTRANTS

// 068

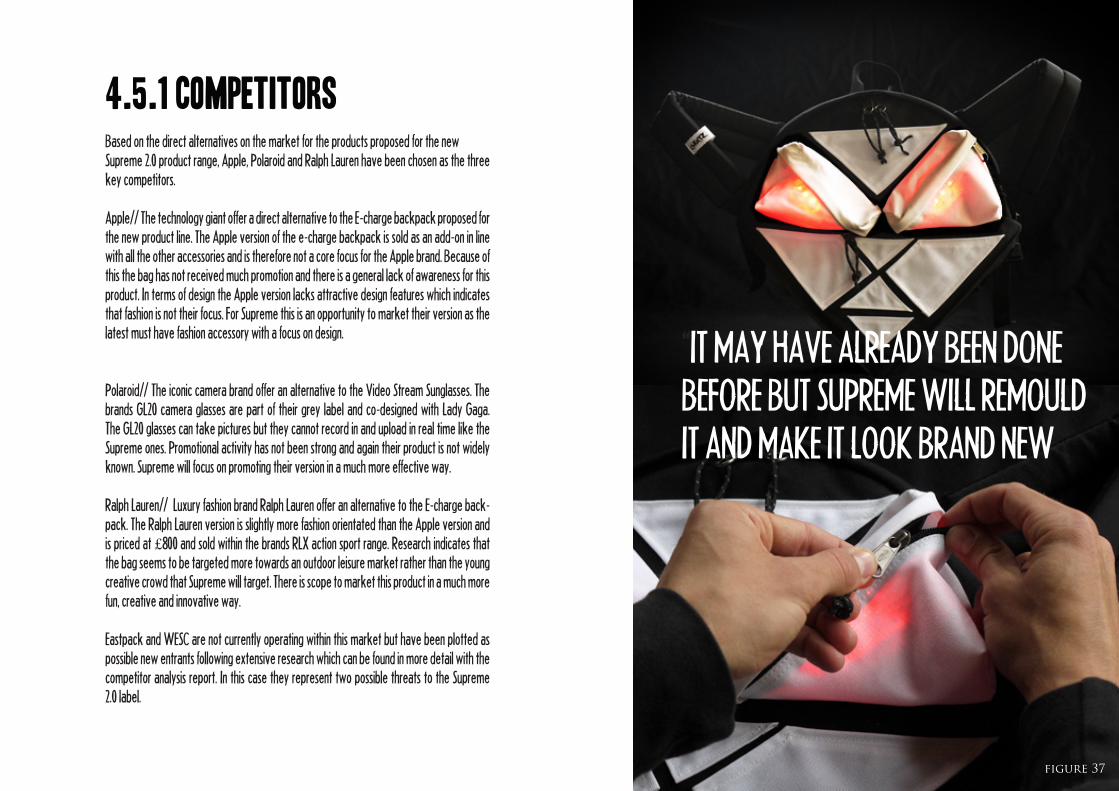

Based on the direct alternatives on the market for the products proposed for the new Supreme 2.0 product range, Apple, Polaroid and Ralph Lauren have been chosen as the three key competitors.

Apple// The technology giant offer a direct alternative to the E-charge backpack proposed for the new product line. The Apple version of the e-charge backpack is sold as an add-on in line with all the other accessories and is therefore not a core focus for the Apple brand. Because of this the bag has not received much promotion and there is a general lack of awareness for this product. In terms of design the Apple version lacks attractive design features which indicates that fashion is not their focus. For Supreme this is an opportunity to market their version as the latest must have fashion accessory with a focus on design.

Polaroid// The iconic camera brand offer an alternative to the Video Stream Sunglasses. The brands GL20 camera glasses are part of their grey label and co-designed with Lady Gaga. The GL20 glasses can take pictures but they cannot record in and upload in real time like the Supreme ones. Promotional activity has not been strong and again their product is not widely known. Supreme will focus on promoting their version in a much more effective way.

Ralph Lauren// Luxury fashion brand Ralph Lauren offer an alternative to the E-charge back-pack. The Ralph Lauren version is slightly more fashion orientated than the Apple version and is priced at £800 and sold within the brands RLX action sport range. Research indicates that the bag seems to be targeted more towards an outdoor leisure market rather than the young creative crowd that Supreme will target. There is scope to market this product in a much more fun, creative and innovative way.

Eastpack and WESC are not currently operating within this market but have been plotted as possible new entrants following extensive research which can be found in more detail with the competitor analysis report. In this case they represent two possible threats to the Supreme 2.0 label.

“IT MAY HAVE ALREADY BEEN DONE BEFORE BUT SUPREME WILL REMOULD IT AND MAKE IT LOOK BRAND NEW

// 068figure 37

4.5.1 competitors

figure 38 // 070

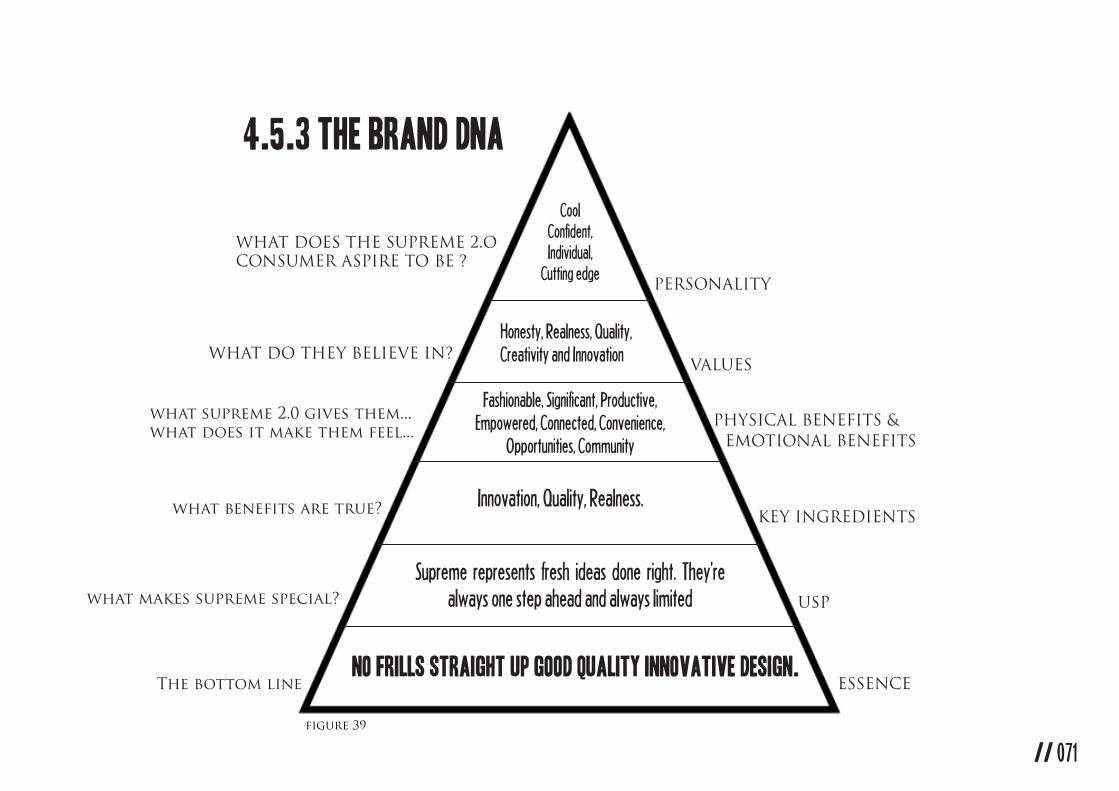

“staking our position” What makes Supreme 2.0 different?

Our products move beyond just the fashionable element. Our products have purpose function and relevance.

4.5.2 position

PERSONALITY

VALUES

EMOTIONAL BENEFITSPHYSICAL BENEFITS &

KEY INGREDIENTS

USP

ESSENCE

WHAT DOES THE SUPREME 2.O CONSUMER ASPIRE TO BE ?

WHAT DO THEY BELIEVE IN?

what supreme 2.0 gives them...what does it make them feel...

what benefits are true?

what makes supreme special?

The bottom line

CoolConfident,Individual,

Cutting edge

Honesty, Realness, Quality, Creativity and Innovation

Fashionable, Significant, Productive,Empowered, Connected, Convenience,

Opportunities, Community

Innovation, Quality, Realness.

Supreme represents fresh ideas done right. They’re always one step ahead and always limited

No frills straight up good quality innovative design.

4.5.3 the brand DNA

// 070 // 071figure 39

4.5.2 position

pROMOTIONobjectives & strategy//advertising campaign//pr activity//online communication//the events//

marketing objectives//

New product/label introduction. Build awareness for the new Supreme 2.0 label and its products.

Communicate the identity of the new label and how it repre-sents the target audience.

Communicate the benefits and unique attributes of the new product to that target audience.

Develop the Supreme brand community- engage consumers with ongoing conversation, interaction and involvement.

// 072figure 40

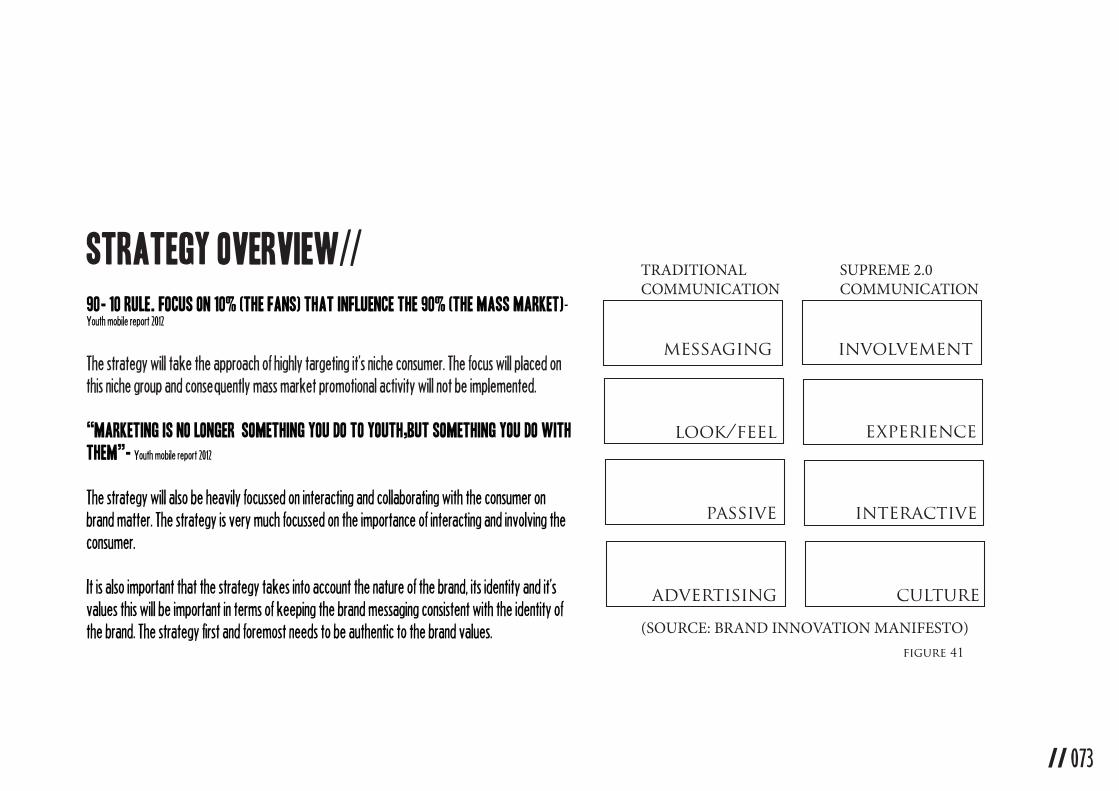

strategy overview//90- 10 rule. Focus on 10% (the fans) that influence the 90% (the mass market)- Youth mobile report 2012

The strategy will take the approach of highly targeting it’s niche consumer. The focus will placed on this niche group and consequently mass market promotional activity will not be implemented.

“mARKETING IS NO LONGER SOMETHING YOU DO TO YOUTH,BUT SOMETHING YOU DO WITH THEM”- Youth mobile report 2012

The strategy will also be heavily focussed on interacting and collaborating with the consumer on brand matter. The strategy is very much focussed on the importance of interacting and involving the consumer.

It is also important that the strategy takes into account the nature of the brand, its identity and it’s values this will be important in terms of keeping the brand messaging consistent with the identity of the brand. The strategy first and foremost needs to be authentic to the brand values.

messaging involvement

look/feel experience

passive interactive

advertising culture

TRADITIONALCOMMUNICATION

SUPREME 2.0COMMUNICATION

(SOURCE: BRAND INNOVATION MANIFESTO)

// 073

figure 41

// 073

“mARKETING IS NO LONGER SOMETHING YOU DO TO YOUTH,BUT SOMETHING YOU DO WITH THEM”

user generated content.collaborative.

Mobile Youth Report 2012

figure 42

They will demand a voice in, a stake in, even a creative point of view about, everything that your business does, from the product itself to the way it is sold and marketed - FastCompany

Any new innovation is now irrelevant to advertisers unless it is being used to forward the art and craft of storytell-ing. - WGSN

Marketing to this generation may be more like a two player game, where everyone’s looking for the win win. How will your campaigns create a sense of play on the part of the audience, a sense of depth and levels, a sense of engagement, a vali-dation loop, and ultimately a sense of material and emotional victory.- FastCompany

// 075

figure 43

4.6.1 Advertising//

The campaign story

The campaign story is inspired by a new generation of young people who are active in taking charge of their futures and carving out opportunities for themselves. The advertising aims to leave the target audience feeling empowered, significant and part of a revolutionary movement.

The campaign story will be communicated via street posters and a short online film trailer. The choice of street posters is generally a route most streetwear brands take. Whilst it is important for the new label to be perceived as fresh and innovative, it is also important that it comes across as an authentic streetwear brand. Furthermore the target consumer is heavily resistant to mass marketing and so the choice to keep it simple and authentic is the best route for the new label.

However as well as the street posters the campaign message will also be communicated via the release of a short online trailer depicting this new revolutionary world run by young creative’s.

The advertising material

The imagery used for the posters will come from user generated content. The campaign will make use of iconic Tumblr imagery and therefore incorporates content that has originally been created by the target consumer and then selected carefully to a make a cohesive and impactful visual campaign. The use of user generated content is consistent with the marketing strategy guidelines which aim to create a collaborative and interactive relationship between brand and consumer. (Refer to marketing pack for more detail)

// 075

Rather than follow a traditional top-down commerce model, where brands dictate what consumers should buy, Slash/Slashers subscribe to a new system based on peer networks, recommendations and approval. ‘The brand is alive and kicking,’ says PR and marketing specialist Raoul Shah of Exposure. ‘It’s just no longer only controlled by big corporations and traditional media outlets.’ - FutureLab

An elite group of tastemakers is emerging, away from the traditional media, entertainment and music industry communities. An endorse-ment from an underground Slash/Slash personality could have the same effect as, if not a greater one than, an advertisement in a style magazine. Slash/Slash kids are honest and real, but are also fully aware of the benefits their endorsements could bring. - FutureLab

// 077figure 44

target mediaIn terms of media, the focus will be placed on gaining coverage in influential online consumer media as well as niche specialised media based in the urban culture community. This is in line with the marketing strategy guidelines which aim to create a highly targeted and tailored PR strategy to capture the attention of the specific target group only.

Mass media publications will be avoided (just like the traditional Supreme brand strategy) as the objective is to reach the niche not the mass. The target consumer values sources that they view as authentic and this is most likely to be consumer blogs or nicheblogs that specialise in streetwear/urban culture.

brand ambassadorsUse of influential brand ambassadors to promote the new label and the products will be an important tactic the label will adopt in order to influence the target audience.

The brand ambassador role will involve the promotion of the new label and its products though their online space. They will be expected to document their experiences of the Supreme 2.0 label products on their online space. The aim is to create a buzz and anticipation for the launch of the new products among the viewers (target audience).

4.6.2 pr activity//

// 077 // 078

figure 45

virtual communityA central focus for the online marketing strategy centres on the development of a Supreme 2.0 brand virtual community. This is in line with the market research where it was found that the target consumer was a part of multiple online communities where they discussed, reviewed, recommended and bonded over many of their favourite brands.

In light of this it is logical that we provide these consumers with an official Supreme brand community online, where the consumer can get this same community feel but with a more interactive brand experience.

It is a great way for the new label to gain more insight into the needs of their consumers, as well as develop deeper more mean-ingful relationships with the customers and the brand community as a whole.

online video series As part of the online promotional strategy the label will introduce an online video series which will document the life of creative entrepre-neurial young people. The series will follow them on their journey to reaching their goals. The viewers will gain access into the daily routines of these people and an insight into what they have to do in order to get where they would like to go.

The documentary series will work in collaboration with online media channel SBTV and will be an on-going series across all future promotional campaigns. In order to continuously cast new people the brand will allow viewers the opportunity to send in their story to be considered for a feature on the show.

The video series is consistent with everything the 2.0 label stands for and so is consistent with the brand mission and values. It is also a great opportunity for the individual’s who feature on the show to gain exposure for themselves as well as inspiring for the viewer who is likely to be someone who can identify with the characters in the show.

4.6.3 online strategy//

social mediaThe focus will centre on microblog application Tumblr. Why? It’s based on targeting more specific niche groups and represents the importance of visual imagery, a theme which runs throughout the entire marketing campaign.

It generally has more of an authentic communal based feel, compared to the corporate nature of Facebook and Twitter promotional activity. This makes it perfect for the target audience who rejectcorporate brands and marketing and value authentic community based brands.

The original Supreme label already have a Tumblr site and the plan is to launch a separate Tumblr for the 2.0 label which will display all imagery related to the 2.0 label as well as various other inspirational imagery.

In summary the social media focus is NOT about providing the latest brand information or special promotions (like many other streetwear brands) but is simply about communicating visually with the target audience.

figure 46

figure 57

SUPREME2.0

sponsorshipBoth the pre-launch press event and the in-store product event will be sponsored and completely funded by premium cider brand Kopparberg. They will also provide the drinks at both events. Kop-parberg target a similar consumer to Supreme and focus on sponsoring the events of cool youth brands in order to promote themselves, this makes them the perfect sponsor for the Supreme brand.

// 082

4.6.4 the launch event//

pre-launch press event‘The evolution of the Supreme brand from past to present. A creative hi-tech themed installation based on the history and journey of the Supreme.

Aims and objectives of the event-Welcome the Supreme 2.0 label-Create a brand experience that communicates the brand identity-Anticipated press coverage by inviting target media-Showcase the product features.-Create a buzz and anticipation for the official in store product launch-Encourage pre-orders-Encourage sign-ups to the virtual supreme community.

in-store launch eventThe in store launch is a lot more laid back community based event. Supreme want to celebrate the launch of their new 2.0 label with their closest friends and most loyal supporters. At this event the products will be available to purchase for the first time

Aim and objectives of the event-Welcome the new Supreme 2.0 product range and label-Create a community feeling and interact with consumers-Encourage more signups for the virtual Supreme store-Generate a healthy proportion of sales for the from the new range

financialsstock investment//other costs//capital funding//financial drivers//

5.1 Capital Funding

The initial funding to develop this new product label will come from Supreme’s internal finances.There will also be some funding provided by Kopparberg a premium cider brand who will sponsor all events associated with the launch of the new range.

In terms of stock, figures show that an initial investment of £52, 000 will be required. As well as a budget of around £65.000 in order to finance the costs associated with launching the new label and range.

// 083

figure 47

// 084

5.2 financial drivers

From the sale of the new range the brand is predicted to achieve sales revenue of approx £192,000. After taking into consideration all the costs associated with the launch of the new label the predicted profit to be made is £72,800. This is a healthy profit for the small label of a niche independent brand.(Appendice 3: Profit and Loss Statement) (Appendice 2: Cash Flow Forecast)

swotstrengths//weaknesses//opportunities//threats//

6.1 SWOT Analysis//strengthsDifferentiation from other steetwear brands on the market in terms of product portfolio gives the brand a competitive edge. This is beneficial for a brand operating within the streetwear market which is in decline and becoming increasingly competitive.

Unisex nature of the products means that the market potential is larger than the actual target market.(Appendice 4: the Tomgirl marketing typology)

Products which are relevant and beneficial to the consumer in correlation to the growing importance of technology and social media give them more incentives to purchase.

Added fashion element to the proposed products carves out a clear brand positioning for Supreme against companies with similar products.

Utilising online and social media mediums for promotion will add to the brands mission of collaborating with the consumer and at the same time save costs.

Marketing a new product to an existing market minimises risk, especially when research indicates that the product will sell among this group. Furthermore Supreme have a strong brand following as well as a strong reputation which should encouragethe new range to sell.

Online strategy- Creation of an online brand community not only reinforces brand loyalty but it is another touch point/ interaction point with the customer which communicates the brand identity.

Existing store- Supreme currently have a store in London and this will minimise the costs of starting the new label because theyhave the space to place the new label.

// 085

6.2 swot analysis//WeaknessesDifficulty in reaching a large audience and retaining the exclusive nature and niche positioning of the brand.

Small production quantities means that the brand can not take advantage of economies of scale and thereforethe potential profit margins are minimised.

Product Licensing- The technology incorporated into the products does not belong to the brand. This means thatthe cost price for the products are higher due to licensing fees. This also means that other brands can potentiallystart producing the same products.

The cost of research and development to continually source new products for the range could potentially be a highcost for the brand and there are no guarantees

Initial costs of setting up the new label and product range are high. Especially the costs associated with promotingand creating the new label identity.

// 086

6.2 swot analysis//WeaknessesDifficulty in reaching a large audience and retaining the exclusive nature and niche positioning of the brand.

Small production quantities means that the brand can not take advantage of economies of scale and thereforethe potential profit margins are minimised.

Product Licensing- The technology incorporated into the products does not belong to the brand. This means thatthe cost price for the products are higher due to licensing fees. This also means that other brands can potentiallystart producing the same products.

The cost of research and development to continually source new products for the range could potentially be a highcost for the brand and there are no guarantees

Initial costs of setting up the new label and product range are high. Especially the costs associated with promotingand creating the new label identity.

6.3 swot analysis // OpportunitiesCollaborating with wearable technology product designers on future products for the new range.

The Launch of the new label in the brands two other biggest markets, North America and Japan.

Possibility of increasing distribution channels and selling products through selected retailers such asDover street market, a store which previously stocked the Supreme brand before the opening of thebrand’s own London store.

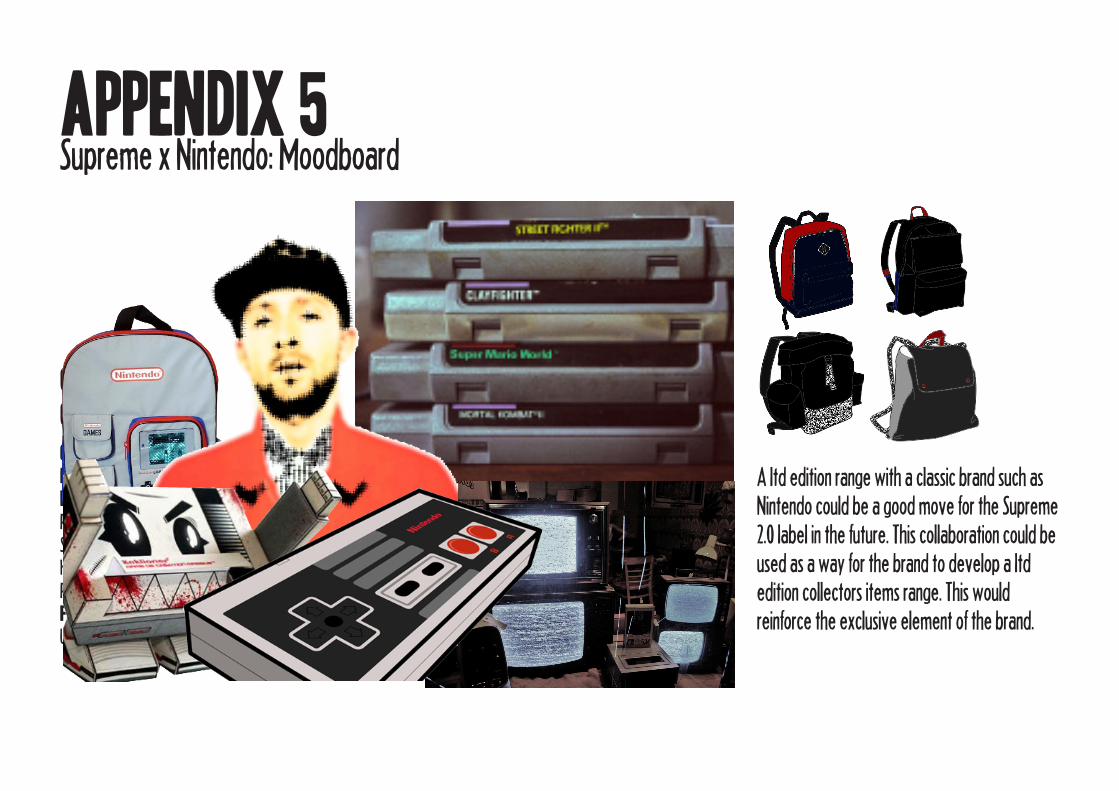

Collaborations with other brands on future limited edition product lines. (Appendix 5)

// 086 // 087

6.4 swot analysis // threatsPossible confusion between Supreme and Supreme 2.0. Could the new label potentially damage the reputation of the original product line?

Possibility of technology giants such as Apple moving aggressively into the market.

Legal barriers associated with bringing technology products to the market.

// 088

7. conclusions

// 088 // 089figure 48

The findings from the market research indicate that there is a new generation of digitally engaged consumers who are looking for brands and products which can offer them something unique, innovative and at the same time meaningful. These consumers are heavy users of social media and technology and are using it in ways to produce opportunities for themselves.

100% of the target market surveyed said that they used a mobile device to access the internet

87.1% of the target market surveyed said that they viewed the internet as a tool for promoting themselves

As a result of these findings it has been established that there is a clear gap in the market for Supreme to launch a new product line and label compromised of hi-tech products which link back to social media in a way which is relevant to the target demographic. The need for this new product line has been backed up by thorough research throughout the report including the fact that 93.5% of the target group surveyed said they would buy from the product range.

This proposal is beneficial for Supreme who are operating in an extremely com-petitive market with little differentiation. The introduction of this new product range and label therefore will give the brand the chance to carve out a clear ad unique positioning and increase their chances of appealing to their target audience by offering them products with a higher relevance and purpose in their life.

appendices

APPENDIX 1Solar Panel Backpack Technical drawing

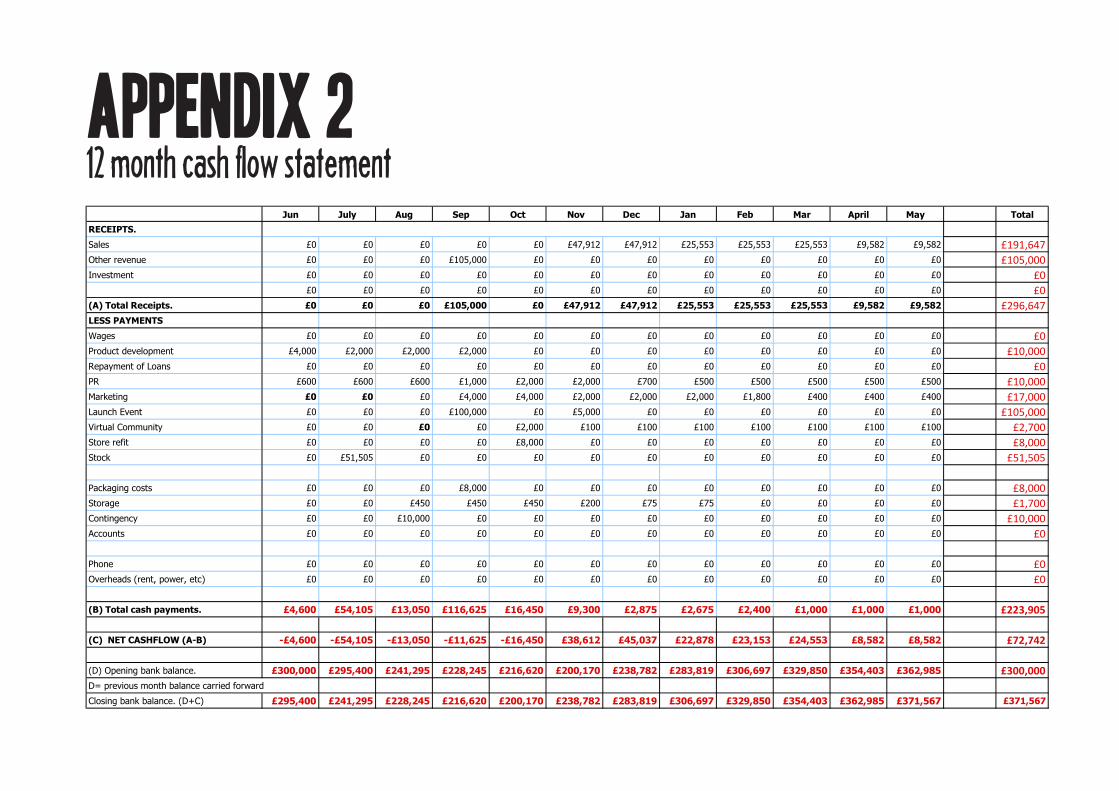

APPENDIX 2Jun July Aug Sep Oct Nov Dec Jan Feb Mar April May Total

RECEIPTS.

Sales £0 £0 £0 £0 £0 £47,912 £47,912 £25,553 £25,553 £25,553 £9,582 £9,582 £191,647Other revenue £0 £0 £0 £105,000 £0 £0 £0 £0 £0 £0 £0 £0 £105,000Investment £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0

£0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0(A) Total Receipts. £0 £0 £0 £105,000 £0 £47,912 £47,912 £25,553 £25,553 £25,553 £9,582 £9,582 £296,647LESS PAYMENTS

Wages £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0Product development £4,000 £2,000 £2,000 £2,000 £0 £0 £0 £0 £0 £0 £0 £0 £10,000Repayment of Loans £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0PR £600 £600 £600 £1,000 £2,000 £2,000 £700 £500 £500 £500 £500 £500 £10,000Marketing £0 £0 £0 £4,000 £4,000 £2,000 £2,000 £2,000 £1,800 £400 £400 £400 £17,000Launch Event £0 £0 £0 £100,000 £0 £5,000 £0 £0 £0 £0 £0 £0 £105,000Virtual Community £0 £0 £0 £0 £2,000 £100 £100 £100 £100 £100 £100 £100 £2,700Store refit £0 £0 £0 £0 £8,000 £0 £0 £0 £0 £0 £0 £0 £8,000Stock £0 £51,505 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £51,505

Packaging costs £0 £0 £0 £8,000 £0 £0 £0 £0 £0 £0 £0 £0 £8,000Storage £0 £0 £450 £450 £450 £200 £75 £75 £0 £0 £0 £0 £1,700Contingency £0 £0 £10,000 £0 £0 £0 £0 £0 £0 £0 £0 £0 £10,000Accounts £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0

Phone £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0Overheads (rent, power, etc) £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0 £0

(B) Total cash payments. £4,600 £54,105 £13,050 £116,625 £16,450 £9,300 £2,875 £2,675 £2,400 £1,000 £1,000 £1,000 £223,905

(C) NET CASHFLOW (A-B) -£4,600 -£54,105 -£13,050 -£11,625 -£16,450 £38,612 £45,037 £22,878 £23,153 £24,553 £8,582 £8,582 £72,742

(D) Opening bank balance. £300,000 £295,400 £241,295 £228,245 £216,620 £200,170 £238,782 £283,819 £306,697 £329,850 £354,403 £362,985 £300,000D= previous month balance carried forward

Closing bank balance. (D+C) £295,400 £241,295 £228,245 £216,620 £200,170 £238,782 £283,819 £306,697 £329,850 £354,403 £362,985 £371,567 £371,567

12 month cash flow statement

Annual Profit/Loss Statement Year 1

RECEIPTS. Per Annum Sales £191,647.00Other revenue £105,000.00Investment £0.00

(A) Total Receipts. £296,647.00

LESS PAYMENTSWages £0.00Repayment of Loans £0.00PR £10,000.00Marketing £17,000.00Events £105,000.00Virtual Community £2,700.00Store refit £8,000.00Product development £10,000.00Stock £51,505.00Packaging £8,000.00Storage £1,700.00Insurance £0.00Contingency £10,000.00Accounts £0.00Overheads (rent, power, etc) £0.00(B) Total cash payments. £223,905.00

(C) NET CASHFLOW (A-B) £72,740.00

(D) Opening bank balance. £300,000.00

Closing bank balance. (D+C) £371,567.00

Profit and LossBreakdownFrom the sale of the new range the brand is predicted to make £191,647 before taking intoconsideration into the costs associated with launching the new label and products.

The brand will also recieve a sum of £105,000 from the Kopparberg brand the official sponsors of the Supreme 2.0 launch events. This money is soley for the launch and press events.

In terms of costs the brand will not face the high costs of wages, overheads etc. This is because they will benefit from the resources of the original Supreme brand

The biggest cost to the brand will be the cost of the stock followed by the PR, marketng and product development.

APPENDIX 3

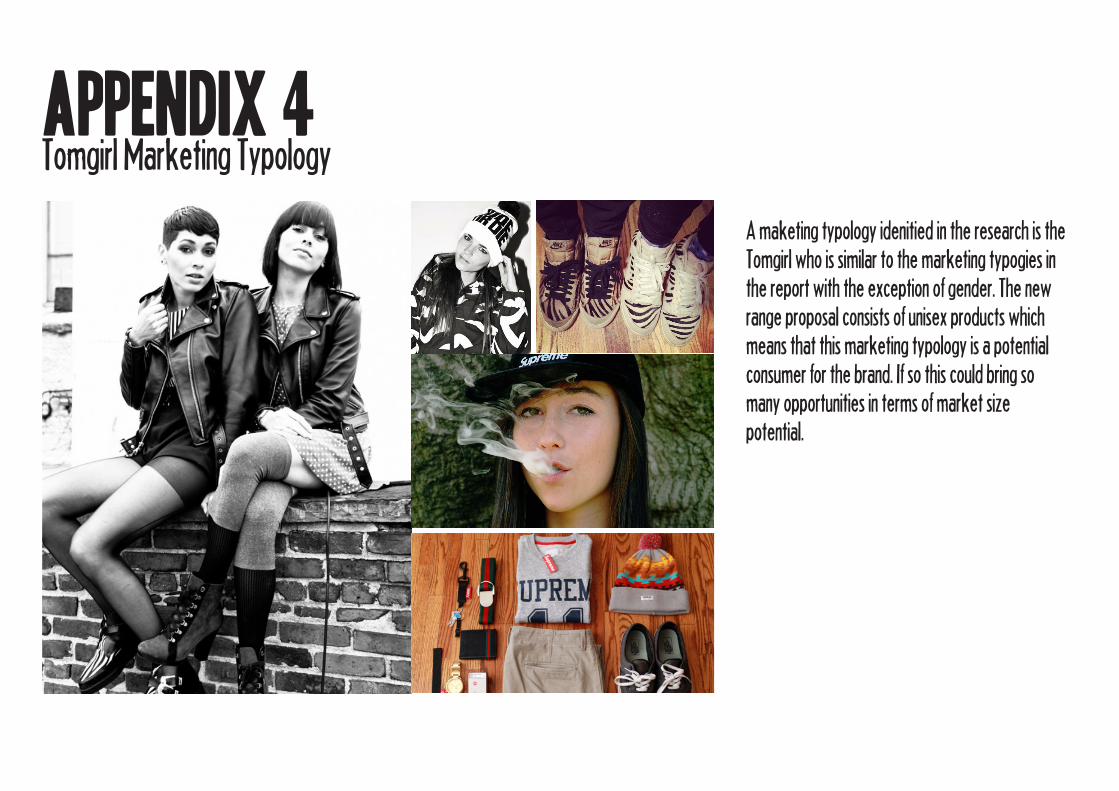

APPENDIX 4Tomgirl Marketing Typology

A maketing typology idenitied in the research is the Tomgirl who is similar to the marketing typogies in the report with the exception of gender. The new range proposal consists of unisex products which means that this marketing typology is a potential consumer for the brand. If so this could bring so many opportunities in terms of market size potential.

APPENDIX 5Supreme x Nintendo: Moodboard

CONSUMERCHARACTERISTICSOPTIMISTIC & ENTREPRENEURIALEARLY ADOPTERSLOVE TECHNOLOGY & GADGETSPREFERS LIMITED EDITION PRODUCTSSEES THEMSELVES AS TRENDSETTERSHIGH ONLINE VISIBILITYPLATFORMS FOR PERSONAL PROMOTIONfavour ‘enabler’ BRANDS THAT ALLOWUSERS TO CREATE THEIR OWN TERMS

A ltd edition range with a classic brand such asNintendo could be a good move for the Supreme2.0 label in the future. This collaboration could be used as a way for the brand to develop a ltd edition collectors items range. This wouldreinforce the exclusive element of the brand.

APPENDIX 6Focus Group and Questionnaire Extracts

“I honestly didn’t know that this was even possible, I think its a great idea. For me im constantlt updating my blog with pictures of my life for my readers and i also post alot of inspiration photos on my tumblr so something like this would be great.” - Lewis//Focus group on Bloggers Backpack

“ I don’t know anyone who wouldnt find this useful” - Joel//Focus group on E-charge Backpack

“I use my phone constantly so something like this is definately needed for me” - Leon//Focus group on E-charge Backpack

“Any product that helps me to maintain my blog gets a thumbs up from me, especially products that sound as cool as these” - Survey response.

“Would be so awesome to do instant posts and being to charge my blackberry the go, lifesaver!” - Survey response.

bibliography

bibliographyArthur, R: WGSN (2011) Story Building over Telling (Online) (Ac-cessed 20th November) http://www.wgsn.com/content/report/Market-ing/Communication_Strategy/2011/October/from_storytellingtostory-building.html

Arthur, R : WGSN (2011) Managing social momentum: Ad tech Lon-don (Online) (Accessed 20th November)http://www.wgsn.com/con-tent/report/Marketing/Communication_Strategy/2011/October/man-aging_social_momentumadtechlondon.html

Dawson, R (2010) The rise of mini-blogging in 2011: Tumblr will con-tinue to soar (Online) (Accessed 15th October 2011)http://rossdaw-sonblog.com/weblog/archives/2010/12/the_rise_of_min.html

Decool, Z (2010) Millennial’s and New Consumerism (Online) (Ac-cessed 8th October) http://www.thenewconsumer.com/2010/10/07/millennials-and-new-consumerism/#more-1379

Forbes (2011) 5 Reasons Why Your Online Presence Will Replace Your Resume in 10 years (Online) (Accessed on 15th 2011) http://www.forbes.com/sites/danschawbel/2011/02/21/5-reasons-why-your-online-presence-will-replace-your-resume-in-10-years/2/

The Future Laboratory (2011) Trend Forecasting (Public talk)

The Guardian (2011) Britain’s new entrepreneurs: young guns go for it (Online) (Accessed 15th October 2011) http://www.guardian.co.uk/business/2011/mar/06/young-british-entrepreneurs

Harbison, N (2011) Kaiser chiefs use innovative social media cam-paign to launch album(Online) (Accessed 10th December) http://www.simplyzesty.com/social-media/kaiser-chiefs-use-innovative-so-cial-media-campaign-to-launch-album/

Mintel (2010) Youth Fashion- UK (Online) (Accessed 4th Novem-ber 11) http://academic.mintel.com/sinatra/oxygen_academic/my_re-ports/display/id=480974&anchor=atom#atom0

Mintel (2011) Men’s Fashion Lifestyles – UK (Online) (Accessed 4=15th November 11) http://academic.mintel.com/sinatra/oxygen_ac-ademic/my_reports/display/id=545463&anchor=atom#atom0

Mintel (2011) Consumer attitudes towards luxury brands – UK (On-line) (Accessed 5th December) http://academic.mintel.com/sinatra/ox-ygen_academic/my_reports/display/id=545468&anchor=atom#atom0

Mintel (2011) Clothing retail –UK (Online) (Accessed 19th Novem-ber 11) http://academic.mintel.com/sinatra/oxygen_academic/my_re-ports/display/id=545205&anchor=atom#atom0

Mintel (2011) Youth Fashion 2011- UK (Online) (Accessed 23rd De-cember 11) http://academic.mintel.com/sinatra/oxygen_academic/my_reports/display/id=604853&anchor=atom#atom0

Neilson social media report (2011) (Online) (Accessed 5th November 2011) http://blog.nielsen.com/nielsenwire/social/

Preston, L (2010) WGSN: JPEG GEN MASH-UP (Online) (Accessed 8th October) http://www.wgsn.com/?_kk=WGSN&_kt=ce609ddb-b4d7-4690-ac25-d9f8c737682f&gclid=CNCF_unsqa0CFYILtAodV-VkJtA

Preston, L (2011) WGSN: Radical Revolutionaries: Youth Attitudes (On-line) (Accessed 8th October) http://www.wgsn.com/?_kk=WGSN&_kt=ce609ddb-b4d7-4690-ac25-d9f8c737682f&gclid=CNCF_unsqa-0CFYILtAodVVkJtA

Robinson, K (2011) Understanding the Millennial consumer (Online) (Accessed 8th October) http://cccbuzz.exbdblogs.com/2011/07/06/understanding-the-millennial-consumer/

Shore, N (2011) Are You M Ready? (Online) (Accessed 8th October) http://www.fastcompany.com/1742592/are-you-m-ready

BOF (2012) Inside Supreme: Anatomy of a Global Streetwear Cult (Online) (Accessed 27th Feb 2012) http://www.businessoffashion.com/2012/01/inside-supreme-anatomy-of-a-global-streetwear-cult-%E2%80%94-part-i.html

Telegraph (2010) Is wearable technology the future of fashion (Online) (Accessed 3rd Novermeber 2011) http://fashion.tele-graph.co.uk/article/TMG7710379/Is-wearable-technology-the-future-of-fashion.html

Trendwatching(2011)NEXTISMhttp://trendwatching.com/trends/recommerce

Trendwatching(2011) REPYOUTATIONhttp://trendwatching.com/trends/innovationextravaganza/

Russell, M – 11 Amazing augmented reality ads (Online) (Ac-cessed 15th April)http://www.businessinsider.com/11-amaz-ing-augmented-reality-ads-2012-1#net-a-porter-makes-store-fronts-interactive-1

Macdonald, A (2012) – WGSN: 90s Tomboy: Youth Trend (Online) (Accessed 4th March 2012) – WGSN.COM

Arthur, R (2012) WGSN, Bloggers and brands: building the right partnership (Online) (Accessed 17th Feb 2012)

Preston, L (2012) – WGSN- Tumblr Tribes: Youth Visual Lan-guage (Online) (Accessed 17th Feb 2012)

Preston, L (2012) – WGSN: Generation Hack-tivate: Youth Attitudes (Online) (Accessed 4th March 2012) WGSN.COM

Report: (2012) Youth Mobile Culture – Part 1(Online) (Ac-cessed March 1st 2012) http://www.mobileyouthreport.com

Admin (2011) Traditional PR is dead, Wanna survive? (On-line) (Accessed 1st March 2012) http://fashionablymarketing.me/2011/05/traditional-pr-and-new-tactics/

O’Hear, B (2007) Brands in secondlife (Online) (Accessed March 15th 2012) http://www.zdnet.com/photos/brands-in-second-life/62330

Grant, J (2006) The Brand Innovation Manifesto: How to build brands; redefine markets and deft conventions

Tailor.P: (Online) http://www.learnmarketing.net/marketing.htm (Ac-cessed 4th March 2012)

Wipperfurth, A (2005) Brand Hijack: Marketing Without Marketing : Portfolio Hardcover

Hutchings, E (2011) Hugo Boss Creates Online Video Interview Series (Online) (Re- Accessed 11th Feb 2012) http://www.psfk.com/2011/12/hugo-boss-creates-online-video-interview-series.html

Figure 1: Supreme shirt- exe summaryhttp://www.supremenewyork.com/shop/

Figure 2: (Edited) Trapstar lookbookhttp://djcable.blogspot.co.uk/2011/06/trapstar-x-goonies-video-look-book.html

Figure 3: Shai Spooner//twitterh t t p : / / t w i t t e r . c o m / # ! / H b y H / s t a -tus/148843623616745473/photo/1

Figure 4: Stussy storehttp://www.freshnessmag.com/2008/09/12/stussy-harajuku-chapter-store-preview/

Figure 5: Nike wiishttp://www.njgm.co.uk/#Nike78-Nike-Wiis

Figure 6: Photography of Bianca Hammond

Figure 7: USP Graffiti pageh t t p : / / w w w . s m a s h i n g m a g a z i n e .com/2008/09/14/tribute-to-graffiti-50-beauti-ful-graffiti-artworks/

LIST OF ILLUSTRATIONSFigure 8: http://madfuture.com/

Figure9:http://7thmanmagazine.blogspot.co.uk/2010/10/diesel-kicks-ass.html

Figure 10 http://yfrog.com/keciqbyj

Figure 11: http://yinnyang.co.uk/2011/09/meet-the-bakers/http://supremeny.tumblr.com/

http://hypebeast.com/2009/03/supreme-x-nike-sb-bruin-collection/

Figure 12:http://supremeny.tumblr.com/

Figure 13:http://www.sleepwalkbillion.com/page/2http://yfrog.com/keciqbyj

Figure 14:WGSN.COMhttp://dopecheftv.tumblr.com/

Figure 15: http://www.sleepwalkbillion.com/page/2

http://supremeny.tumblr.com/

Figure 16: http://ambrosiaforheads.com/2011/09/mac-miller-face-the-facts/

Figure 17: http://mac-miller.tumblr.com/post/9229563198

Figure 18: http://brokentoysoldiers.tumblr.com/

http://yinnyang.co.uk/

Figure 19: http://supremeny.tumblr.com/

Figure 20: WGSN.COM Figure 22: http://mac-miller.tumblr.com/post/922956319

Figure 23: http://supremeny.tumblr.com/

Figure 24: http://thearcadekids.wordpress.com/

Figure 25: Concept boards

Figure 26: http://www.flickr.com/photos/chris-tianoliff/

Figure 27: http://www.findkopparberg.com/

Figure 28: http://supremeny.tumblr.com/

Figure 29: http://brokentoysoldiers.tumblr.com/

Figure 30: http://supremeny.tumblr.com/

Figure 31: http://www.thedailystreet.co.uk/2011/09/supreme-london-store-launch-recap/

Figure 32: http://www.highsnobiety.com/news/2011/09/19/supreme-london-store-offi-cial-announcement-and-a-look-inside/

Figure 33: http://www.highsnobiety.com/news/2011/09/19/supreme-london-store-offi-cial-announcement-and-a-look-inside/

Figure 34: http://www.findkopparberg.com/

Figure 35: Brokentoysoldiers.tumblr.com

Figure 36: Brokentoysoldiers.tumblr.com

Figure 37:Brokentoysoldiers.tumblr.com

Figure 38:http://supremeny.tumblr.com

Figure 40: http://www.trendhunter.com/

Figure 42: http://www.trendhunter.com/http://madfuture.com/http://www.dopechef.tv/wp/

Figure 43:(Edited)http://madfuture.com/

Figure 44: http://mitchandsuavecom/2012/01/12/shai-spooner-inside-docu-mentary/

Figure 45: https://blogs.monash.edu/pres-to/2012/04/02/utilising-the-virtual-world-for-effective-pr/http://vimeo.com/34501542

Figure 46: http://www.thedailystreet.co.uk/2012/03/carhartt-wip-e1-store-launch-recap/

Figure 47:http://supremeny.tumblr.com/

Figure 48: Brokentoysoldiers.tumblr.com