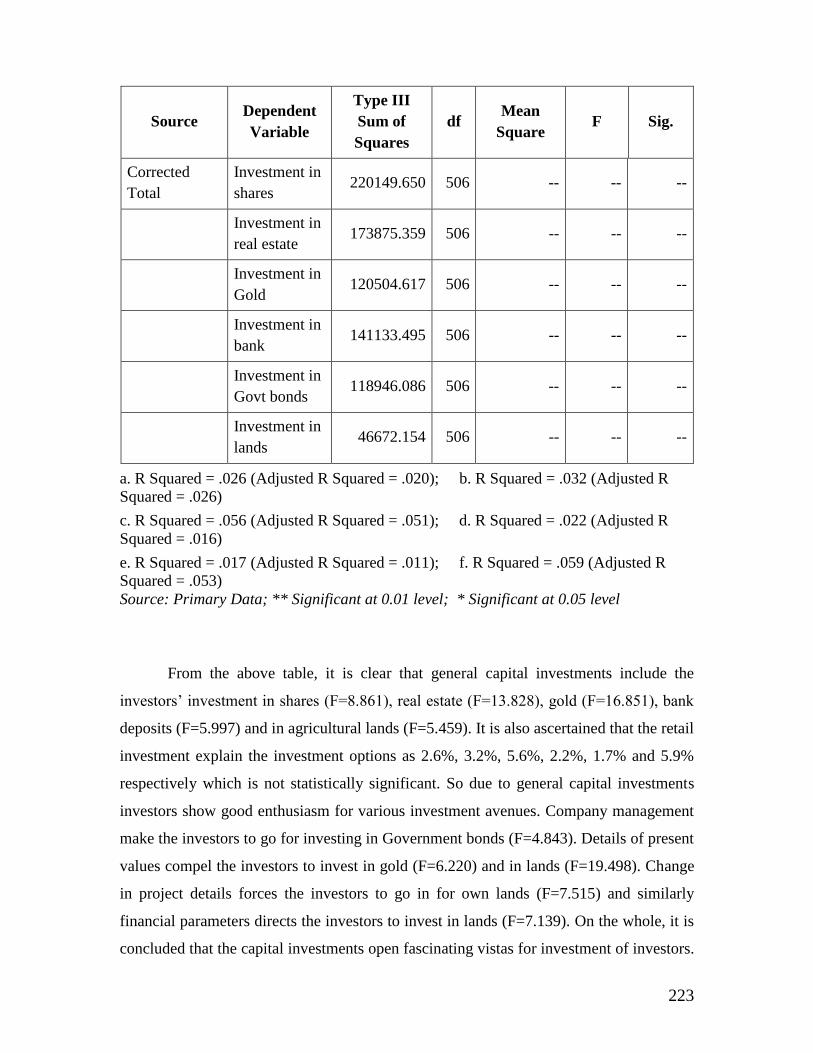

the retail investors behaviour on equity shares …

TRANSCRIPT

1

THE RETAIL INVESTORS BEHAVIOUR ON

EQUITY SHARES IN CHENNAI CITY – A STUDY

Thesis submitted to the

Bharathidasan University, Tiruchirappalli

for the award of the Degree of

DOCTOR OF PHILOSOPHY IN COMMERCE

By

N.SRIVIDHYA,M.Com., M.Phil., MBA.,

Associate Professor, Dept. of Management Studies,

Sri Manakula Vinayagar College of Engineering,

Madagadipet, Puducherry.

Under the Guidance of

Dr.S.RAJKUMAR, M.Com., M.Phil., B.Ed., Ph.D.,

Principal and Research Advisor,

Naina Mohamed College of Arts and Science,

Rajendrapuram, Arantangi Taluk,

Pudukkottai District.

May - 2012

2

Dr. S. RAJKUMAR, M.Com., M.Phil., B.Ed.,

Ph.D,

Principal & Research Advisor,

Naina Mohamed College of Arts and Science,

Rajendrapuram, Aranthangi Taluk,

Pudukkottai District.

e-mail:

Mobile/ Phone:9443588201

Date:

This is to certify that the Ph.D. thesis entitled “The Retail Investors

behaviour on Equity Shares” – A Study is a bonafide record of research work done

by Mrs.N.Srividhya, under my guidance and supervision and the thesis has not

previously formed the basis for the award of any degree, diploma, fellowship or

similar title. The thesis represents entirely an independent work of the candidate.

CERTIFICATE

3

N.Srividhya, M.Com., M.Phil., M.B.A.,

Associate Professor, Dept. of Management Studies,

Sri Manakula Vinayagar Engineering college,

Madagadipet, Puducherry 605107.

Date:

I, N.Srividhya, Ph.D. Scholar, Department of Management Studies, Sri

Manakula Vinayagar Engineering college, Madagadipet, Puducherry, do hereby

declare that the thesis entitled “The Retail Investors behaviour on Equity Shares” –

A Study submitted to Bharathidasan University, Tiruchirappalli for the award of

the degree of “DOCTOR OF PHILOSOPHY IN COMMERCE” is my original

work and that the thesis has not formed the basis for the award of any degree,

diploma, associate ship, fellowship or any other similar titles.

Counter Signed Research Scholar

DECLARATION

4

ACKNOWLEDGEMENT

Dr. S. Rajkumar, my Research Advisor, Principal, Naina Mohamed

College of Arts and Science, Rajendrapuram, Aranthangi Taluk, Pudukkottai

District is the inspiring force behind this research work. He has been my Guide in

the true sense of word. He offered me valuable guidance and suggestions to

complete this work successfully. This study would not have been possible but for

his immense help.

I feel immense pleasure to express my heart-felt gratitude to my Doctoral

committee members Dr.S.Sekar, Principal, Urumu Dhanalakshmi College,

Kattur, Tiruchirappalli – 620 019 and Dr.E.Mubarak Ali, Associate Professor,

P.G. and Research Department of Commerce, Jamal Mohamed College,

(Autonomous), Tiruchirappalli, for providing me the valuable suggestions to make

this study.

The help of librarian of Bharathidasan University is gratefully

acknowledged for their assistance in literature collection.

My acknowledgements are due to all the publishers of both the research

articles and popular articles of mine in their leading national and International

Journals by giving me an opportunity to write my views and findings. I wish to

extend my heartfelt thanks to all the Colleges and Universities for giving me an

opportunity to present my papers on the emerging issues.

I render my thanks to the entire respondents for the co-operation and co-

ordination extended by them in the collection of data needed for the research.

I wish to make a special mention about my better half Mr._G.

Ravichandran, who helped in all the way from the beginning to the end of my

research journey. He gave his moral support in all spheres of my research work. I

am at a loss for words when I think about the sacrifices made by my dear daughter

Selvi._R. Vishnu Priya, and my son Selvan. R. Maadhav, who had to suffer my

absence during the period of my research work.

(N.Srividhya)

5

CONTENTS

CHAPTER TITLE PAGE

NO

I INTRODUCTION AND RESEARCH DESIGN 1

II REVIEW OF LITERATURE 17

III CONCEPTUAL FRAMEWORK OF INDIAN

CAPITAL MARKETS

66

IV ANALYSIS – I 102

V ANALYSIS - II 139

VI FINDINGS, CONCLUSIONS, SUGGESTIONS 236

BIBLIOGRAPHY

ANNEXURE - QUESTIONNAIRE

6

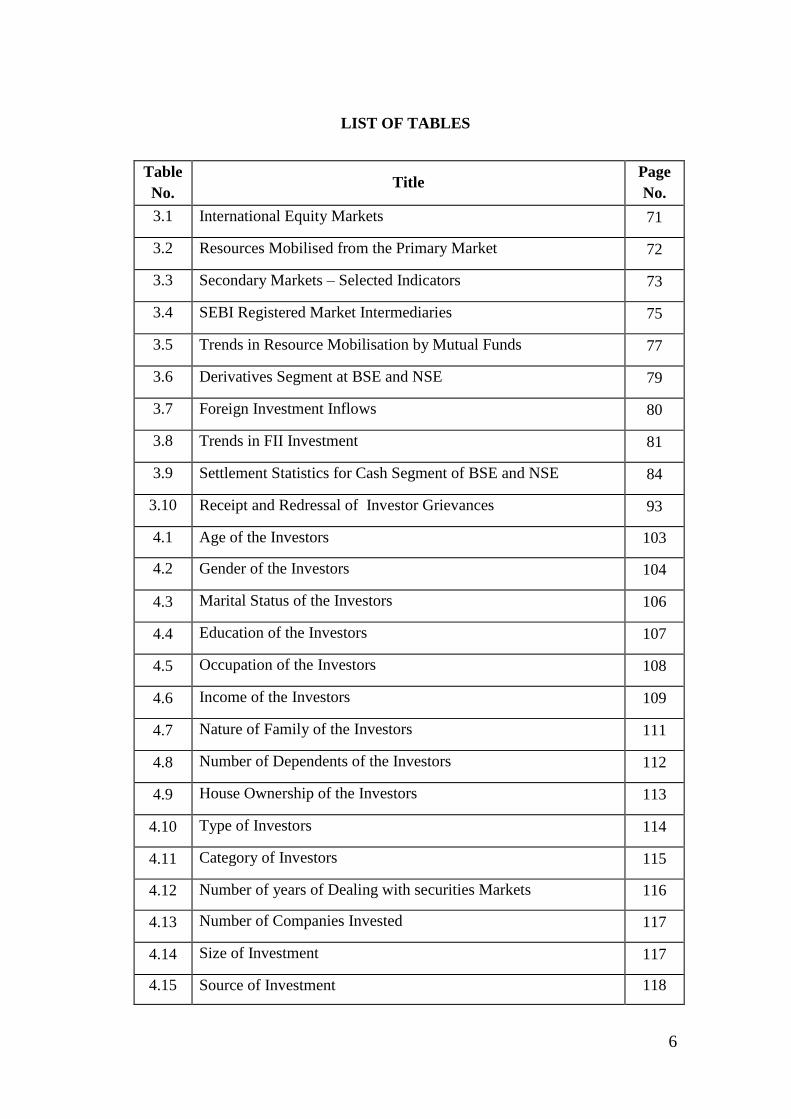

LIST OF TABLES

Table

No. Title

Page

No.

3.1 International Equity Markets 71

3.2 Resources Mobilised from the Primary Market 72

3.3 Secondary Markets – Selected Indicators 73

3.4 SEBI Registered Market Intermediaries 75

3.5 Trends in Resource Mobilisation by Mutual Funds 77

3.6 Derivatives Segment at BSE and NSE 79

3.7 Foreign Investment Inflows 80

3.8 Trends in FII Investment 81

3.9 Settlement Statistics for Cash Segment of BSE and NSE 84

3.10 Receipt and Redressal of Investor Grievances 93

4.1 Age of the Investors 103

4.2 Gender of the Investors 104

4.3 Marital Status of the Investors 106

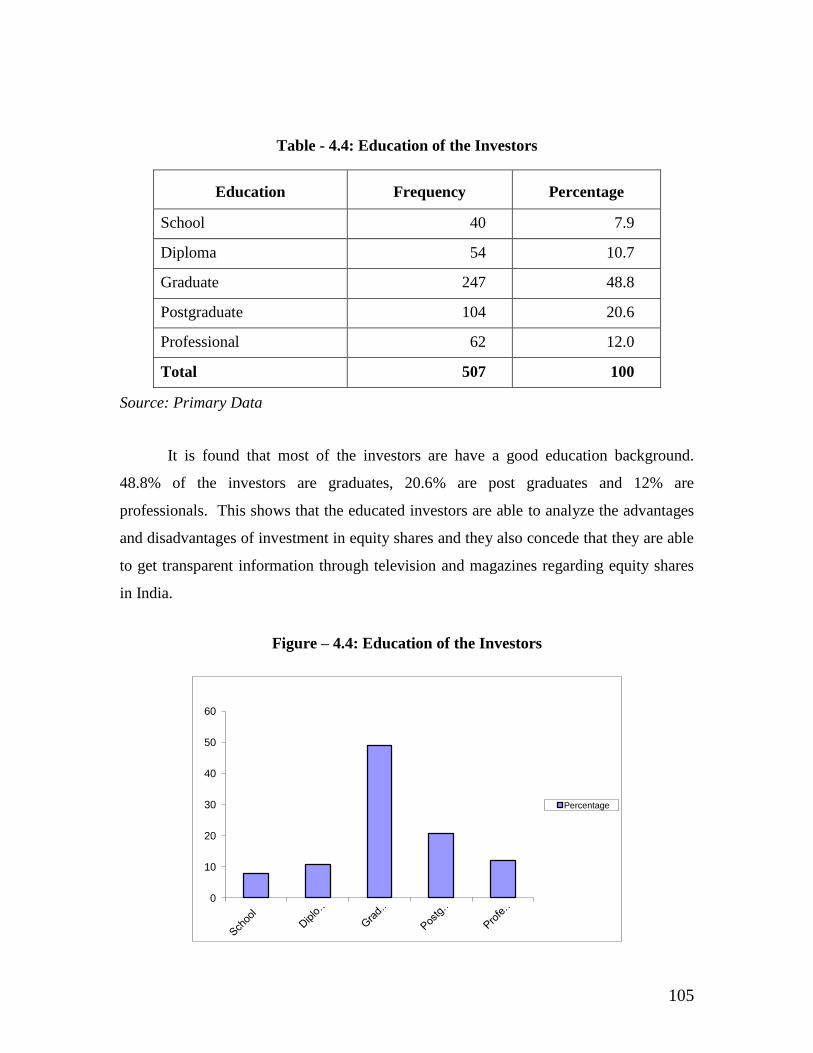

4.4 Education of the Investors 107

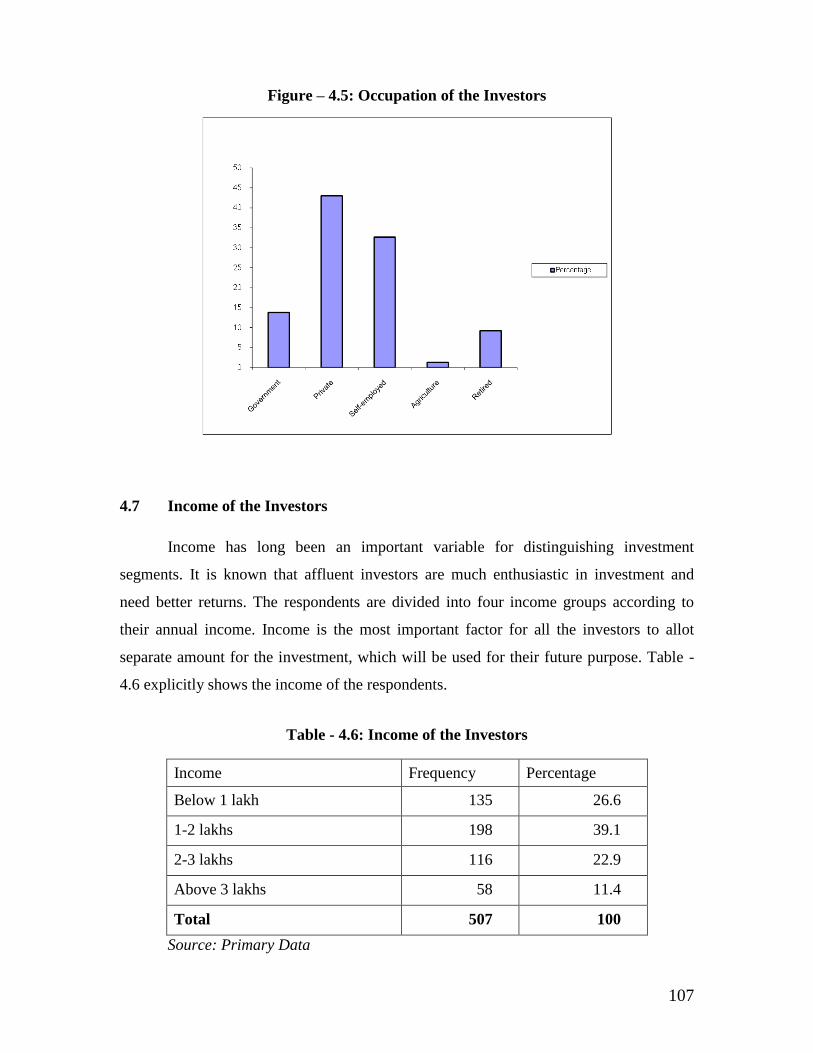

4.5 Occupation of the Investors 108

4.6 Income of the Investors 109

4.7 Nature of Family of the Investors 111

4.8 Number of Dependents of the Investors 112

4.9 House Ownership of the Investors 113

4.10 Type of Investors 114

4.11 Category of Investors 115

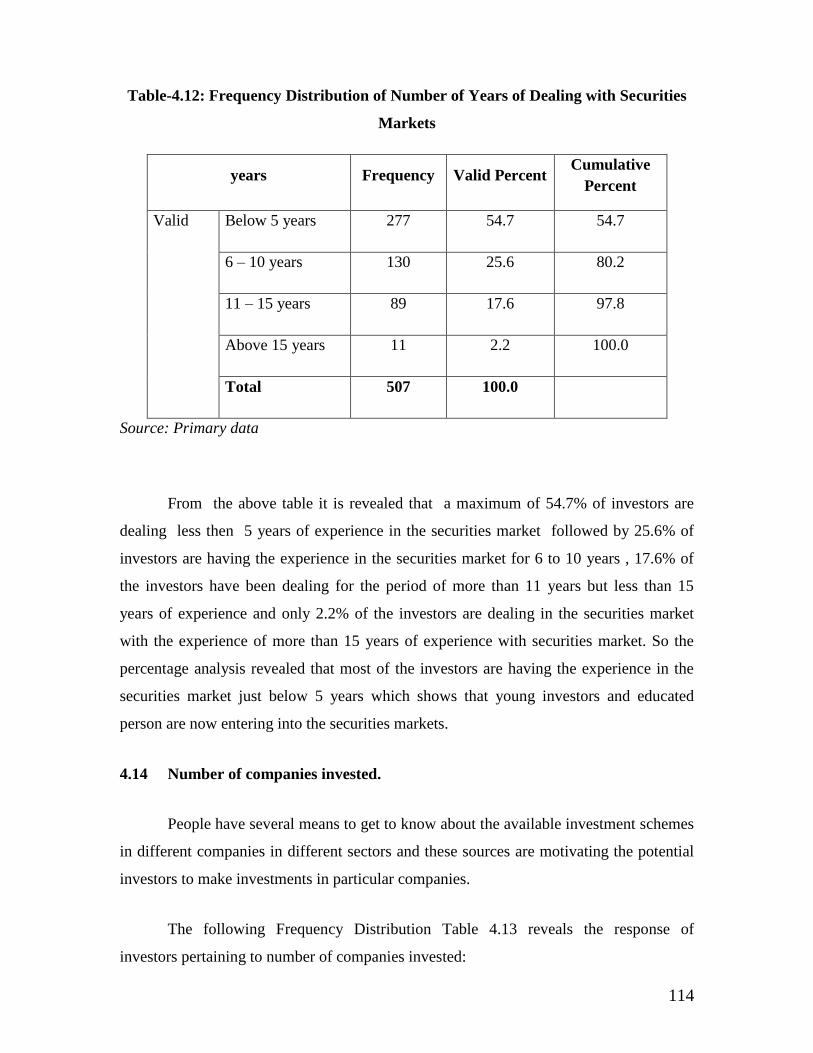

4.12 Number of years of Dealing with securities Markets 116

4.13 Number of Companies Invested 117

4.14 Size of Investment 117

4.15 Source of Investment 118

7

Table

No. Title

Page

No.

4.16 Percentage of Savings invested in Securities Markets 119

4.17 Sources of Information 120

4.18 Criteria for Investments 121

4.19 Member of Investors’ Forum 121

4.20 Awareness of Malpractice of Intermediaries 122

4.21 Mode of Trading 122

4.22 Awareness of Financial Sector Reforms in India 123

4.23 Frequency Distribution of Index 124

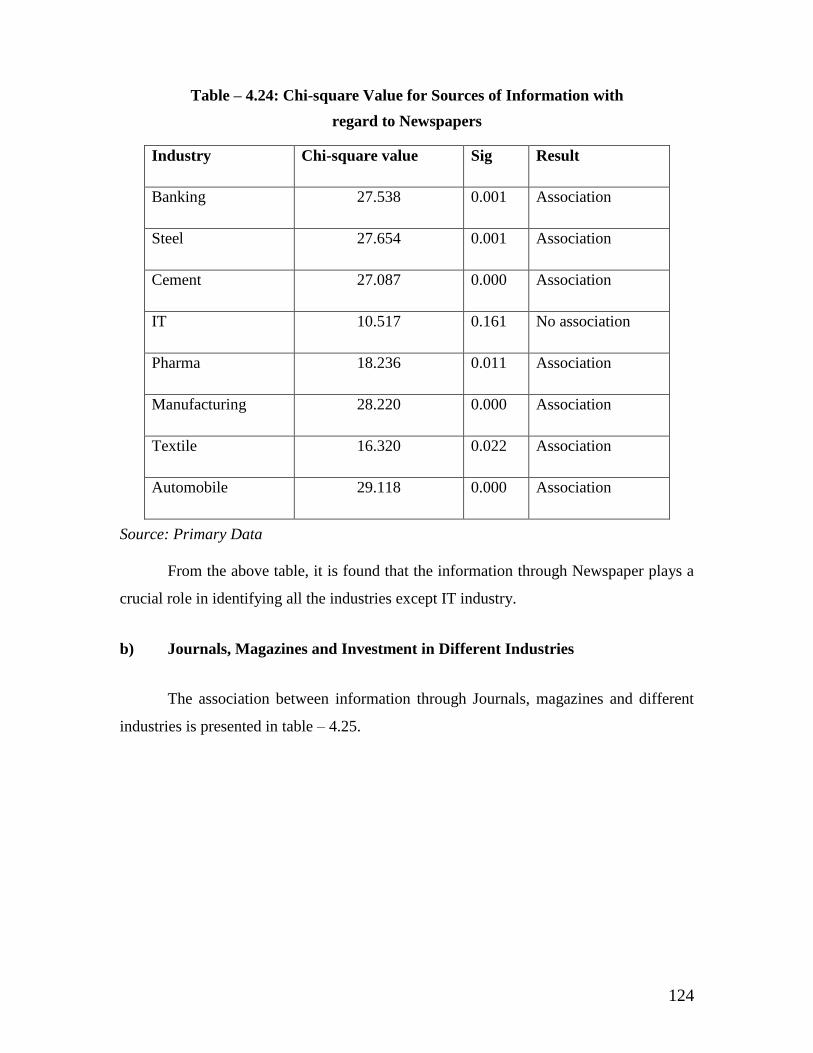

4.24 Chi-square value for sources of Information with regard to News

papers 125

4.25 Chi-square value for sources of Information with regard to

Journals and Magazines 126

4.26 Chi-square value for sources of Information with regard to T V 126

4.27 Chi-square value for sources of Information with regard to stock

Brokers 127

4.28 Chi-square value for sources of Information with regard to

Investment Consultant 128

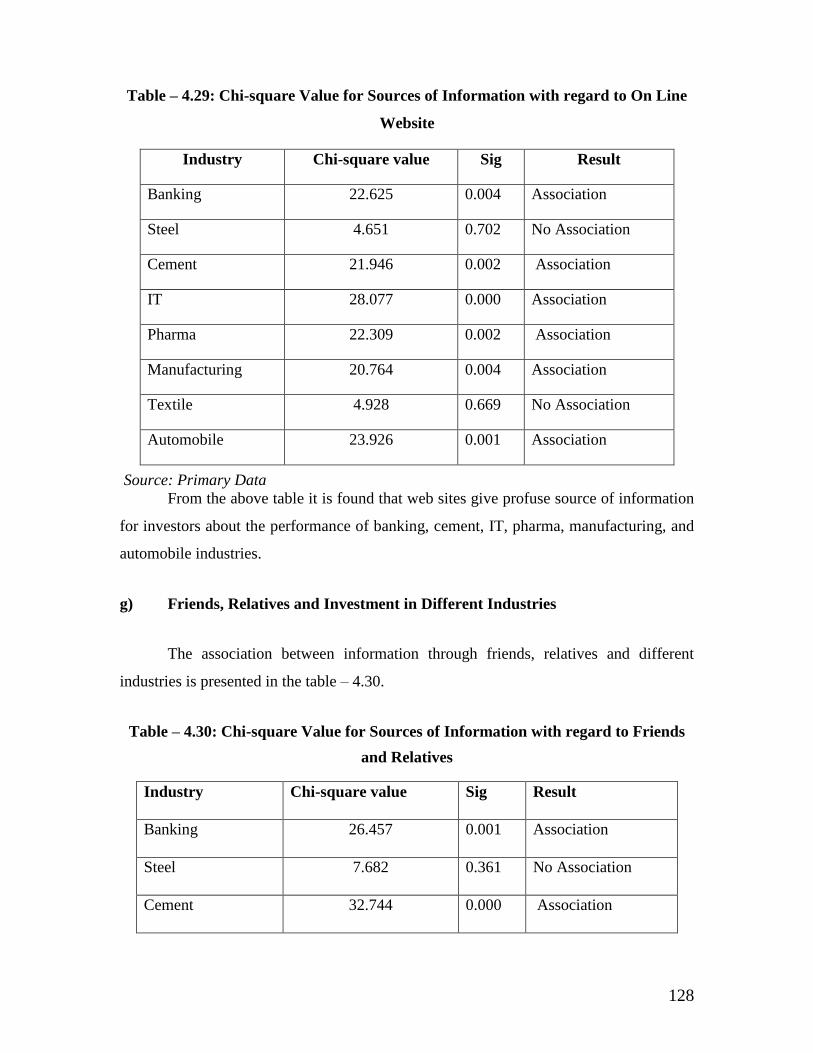

4.29 Chi-square value for sources of Information with regard to On

line website 128

4.30 Chi-square value for sources of Information with regard to

Friends and Relatives 129

4.31 Mean and Standard Deviation for preference of Investments and

their Ranks 130

4.32 Mean and Standard Deviation for Ranking of Industries 131

4.33 Mean and Standard Deviation of Reasons for Investments and

their Ranks 132

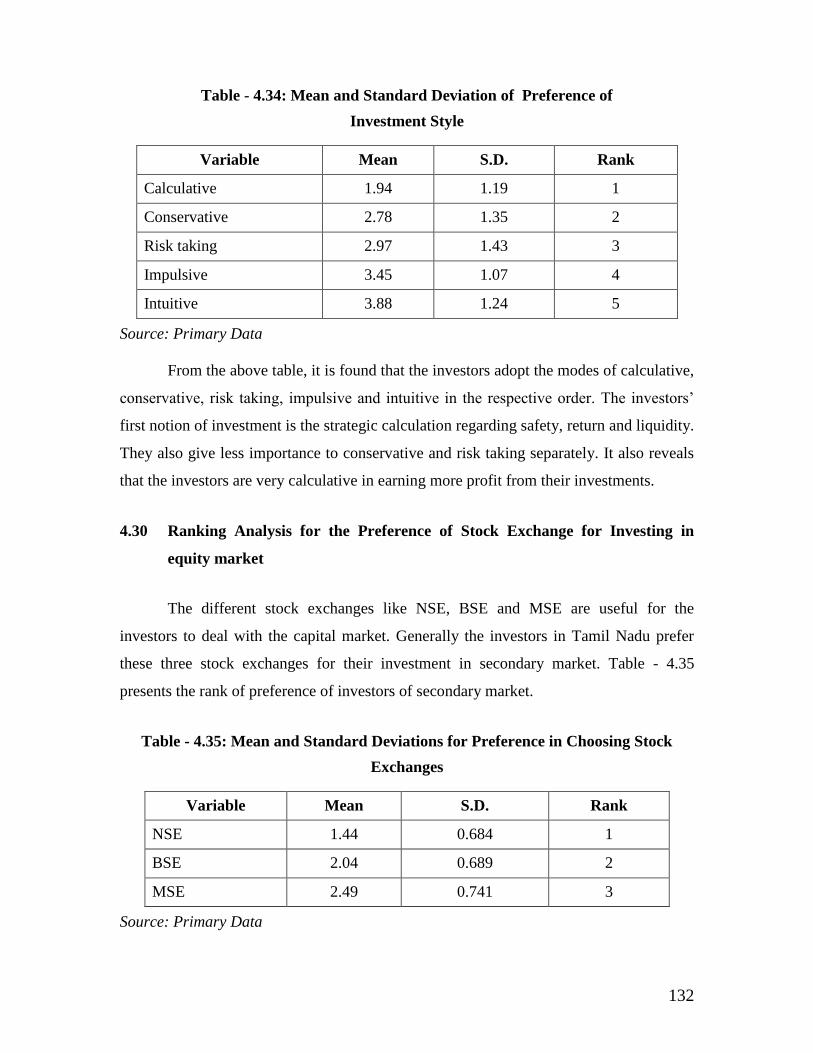

4.34 Mean and Standard Deviation of Preference of Investment Style 132

4.35 Mean and Standard Deviations for Preference in Choosing Stock

Exchanges 133

4.36 Paired Samples Statistics for the Factors of the risk and return 134

4.37 Paired Samples Correlations for the Factors of the Investment in

equity market 135

4.38 Paired samples Test Values for the Factors of the Latest Reforms

in Capital market 136

8

Table

No. Title

Page

No.

4.39 Frequency Distribution of Percentage of expected return 137

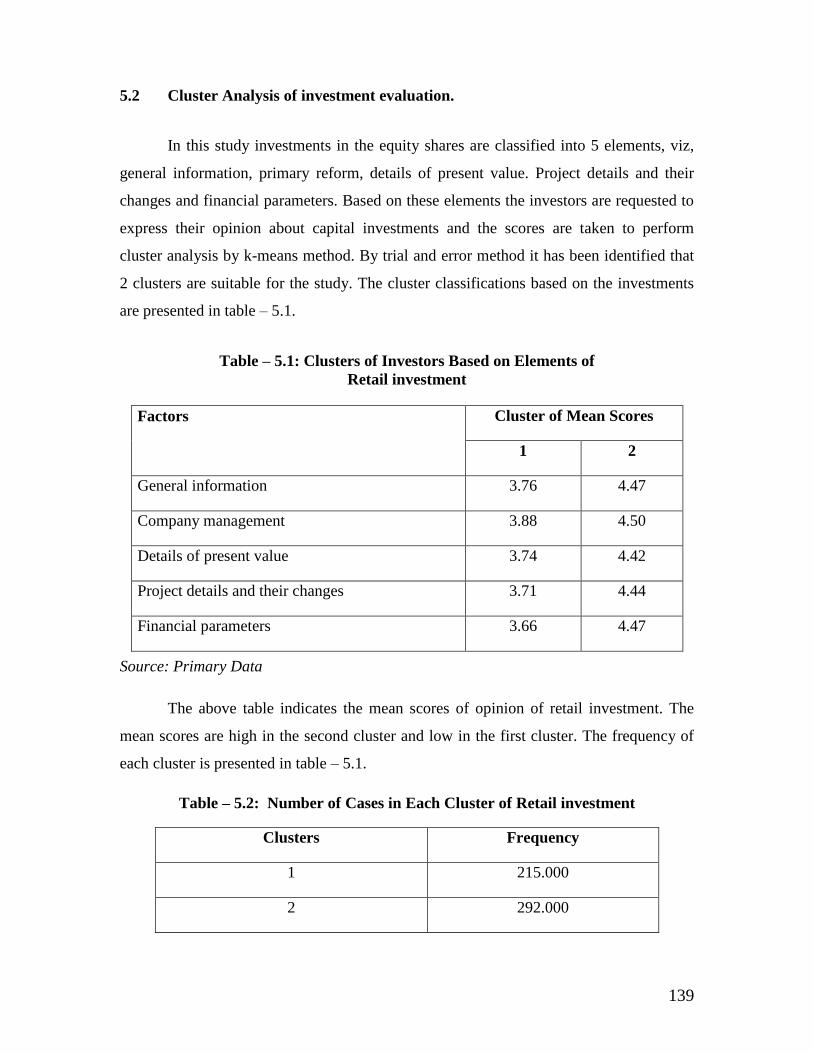

5.1 Clusters of Investors Based on Elements of Retail Investment 140

5.2 Number of cases in Each cluster of Retail Investment 140

5.3 Paired Samples statistics for the Elements of Retail Investment 141

5.4 Paired Samples correlations for the Elements of Retail

Investment 142

5.5 Paired Samples Test values for the Elements of Retail

Investment 143

5.6 Correlation Matrix for Number of year Dealing 145

5.7 Correlation co-efficient Table for percentage of savings in Share

Market 146

5.8 ANOVA for the Elements of capital investments with respect to

investment in shares 147

5.9 ANOVA for the Elements of Retail Investment with respect to

Investment in Government Bonds 148

5.10 ANOVA for the Elements of Retail Investment with respect to

Investment in Fixed Deposits 149

5.11 ANOVA for the Elements of Retail Investment with respect to

Investment in Gold 150

5.12 ANOVA for the Elements of Retail Investment with respect to

Investment in Debentures 151

5.13 ANOVA for the Elements of Retail Investment with respect to

Investment in Mutual Funds 152

5.14 ANOVA for the Elements of Retail Investment with respect to

Investment in Real Estate 153

5.15 ANOVA for the Elements of Retail Investment with respect to

the Reason for Investment - Return 155

5.16 ANOVA for the Elements of Retail Investment with respect to

the Reason for Investment - Liquidity 156

5.17 ANOVA for the Elements of Retail Investment with respect to

the Reason for Investment – Tax Benefits 157

5.18 ANOVA for the Elements of Retail Investment with regard to the

Investment Decisions influenced by Abridged Prospectus 159

5.19 ANOVA for the Elements of Retail Investment with regard to the

Investment Decisions influenced by T V Channels 160

5.20 ANOVA for the Elements of Retail Investment with regard to the 161

9

Table

No. Title

Page

No.

Investment Decisions influenced by Consultant

5.21 ANOVA for the Elements of Retail Investment with regard to the

Investment Decisions influenced by websites 162

5.22 Association between preference of Investment in Equity Shares

and Clusters of Investors 163

5.23 Chi-square for preference of Investments in Equity shares 164

5.24 Multivariate General Linear Model for percentage of

Investments 165

5.25 Association Criteria for Investment and Clusters of Awareness 168

5.26 Chi-square Test and criteria for Investments 169

5.27 Final Cluster Centres for Awareness of the equity Investment 170

5.28 Frequency of Clusters for Awareness of the latest Reforms in

Capital Market 170

5.29 ANOVA for the Elements of Retail investment with regard to

preference of Investment in Banking Sector 172

5.30 ANOVA for the Elements of Retail investment with regard to

preference of Investment in FMCG 173

5.31 ANOVA for the Elements of Retail investment with regard to

preference of Investment in Pharma Sector 174

5.32 ANOVA for the Elements of Retail investment with regard to

preference of Investment in PSE Sector 175

5.33 ANOVA for the Elements of Retail investment with regard to

preference of Investment in MNC Sector 176

5.34 ANOVA for the Elements of Retail investment with regard to

preference of Investment in IT Sector 177

5.35 ANOVA for the Elements of Retail investment with regard to

preference of Investment in Manufacturing Sector 178

5.36 ANOVA for the Elements of Retail investment with regard to

preference of Investment in Service Sector 179

5.37 Investment in Equity Shares is Higher Risk and Clusters of

Awareness on Retail Investment 180

5.38 Chi-square Test Statistics for Investment in Equity Shares is

Higher Risk 181

5.39 ANOVA for the Elements of Retail Investment with regard to

preference of Stock exchanges - Sensex 182

5.40 ANOVA for the Elements of Retail Investment with regard to 183

10

Table

No. Title

Page

No.

preference of Stock exchanges - Nifty

5.41 ANOVA for the Elements of Retail Investment with regard to

preference of Stock exchanges – CNX 100 184

5.42 Reason for Preference Given to Stock Exchange Dealing and

Cluster of Awareness on Retail Investment 185

5.43 Chi-square Tests for Reason of preference Given to Stock

Exchanges 186

5.44 Experience in Dealing shares through Electronic mode (demat)

and Cluster of Awareness on Elements of Retail investment 187

5.45

Chi-square Tests statistics showing Experience in Dealing shares

with Electronic mode (demat) and Cluster of Awareness on

Elements of Retail investment

187

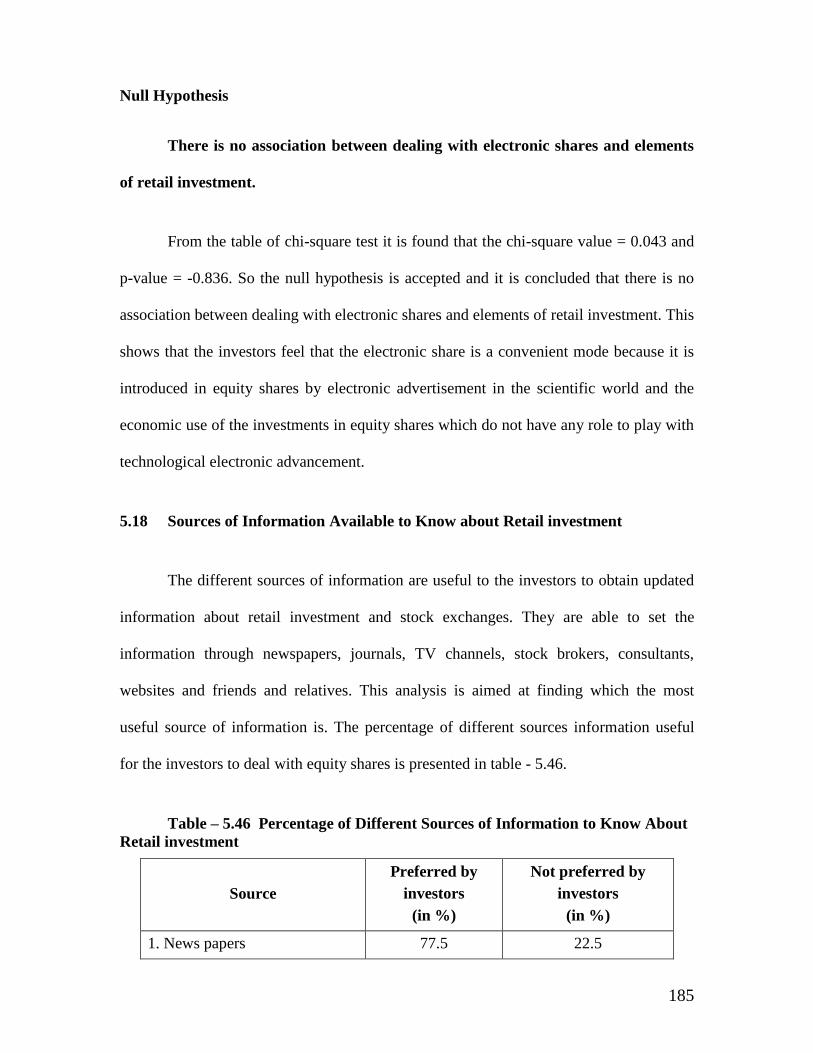

5.46 Percentage of Different sources of Information to know About

Retail investment 189

5.47 Paired Samples statistics for the Factors of the equity investment 190

5.48 Paired Samples correlations for the Factors of the equity

investment 191

5.49 Paired Samples Test values for the Factors of the equity

investment 192

5.50 Multivariate Tests (b) for the Impact of the Latest Reforms in

Capital Market 194

5.51 Impact of the equity investment objectives on the Element of

Investment decision Tests of Between – Subjects Effects 195

5.52 ANOVA for Group means of investment options 199

5.53 Co-efficient of correlations for Number of years Dealing in

Capital market 200

5.54 ANOVA for the Latest Reforms Based on Percentage of savings 201

5.55 Variance of Independent variable on General information’s and

Cluster 1(b) 203

5.56 ANOVA (b.c) for General information’s and Cluster 1 203

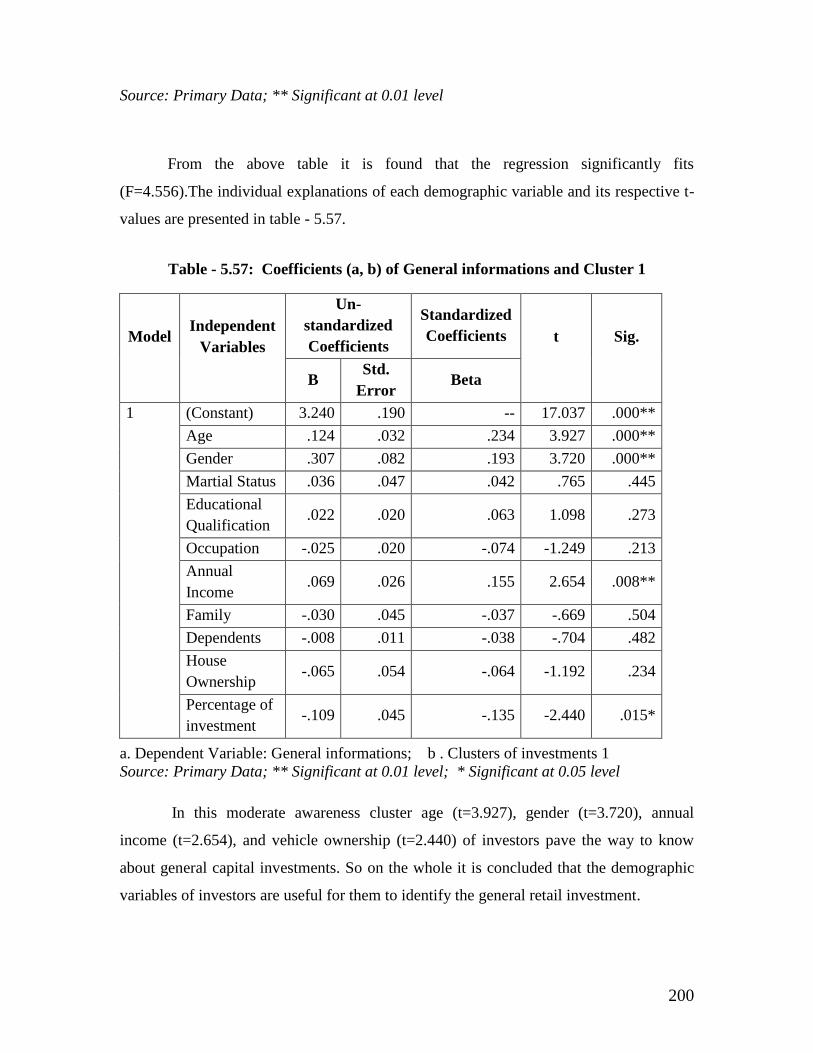

5.57 Coefficients (a.b) of General information’s and Cluster 1 204

5.58 Variance of Independent variable on General information’s

and Cluster2 (b) Cluster 2(b) 205

5.59 ANOVA (b, c) for General information’s and Cluster 2 205

5.60 Coefficients (a, b) of General information’s and Cluster 2 206

11

Table

No. Title

Page

No.

5.61 Variance of Independent Variable for Company

management and Cluster 1(b) 207

5.62 ANOVA (b, c) for Company management and Cluster 1 207

5.63 Coefficients (a, b) of Company management and Cluster 1 208

5.64 Variance of Independent Variable for Company management and

Cluster 2(b) 209

5.65 ANOVA (b,c) for Company management and Cluster 2 209

5.66 Coefficients (a,b) for Company management and Cluster 2 210

5.67 Variance of Independent variable on Details of present values

Cluster 1 (b) 211

5.68 ANOVA (b,c) for Details of Present values and Cluster 1 211

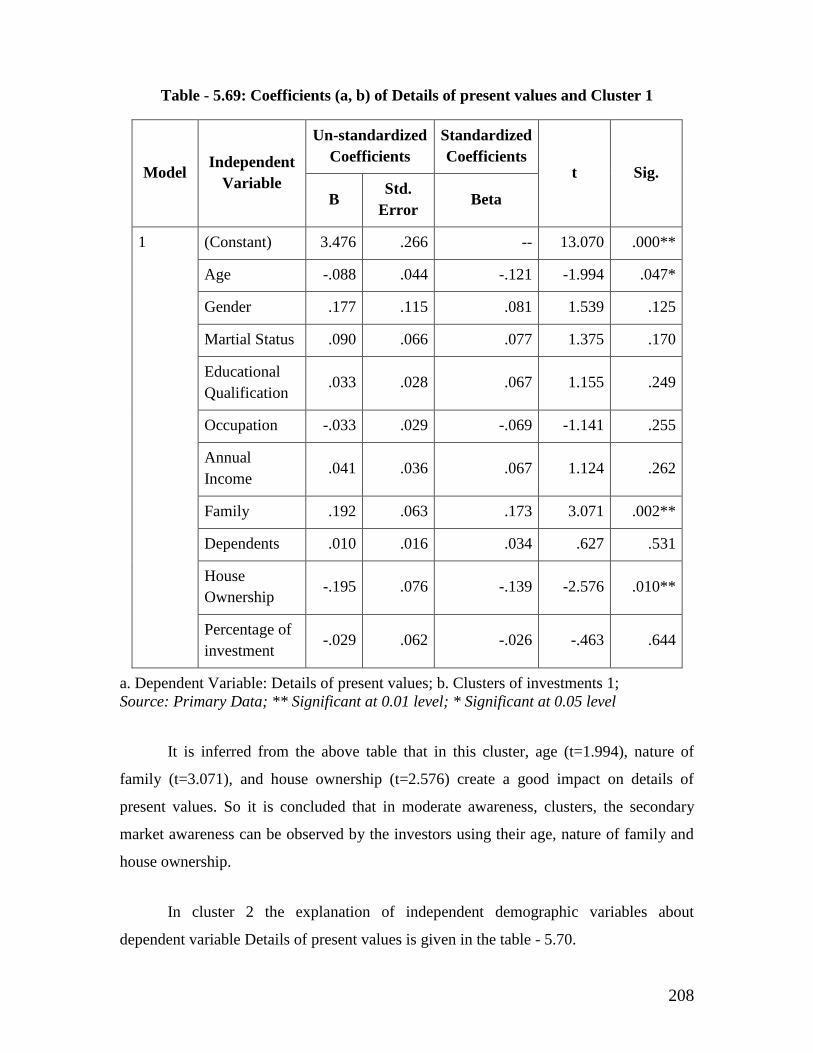

5.69 Coefficients (a,b) of Details of present Values and Cluster 1 212

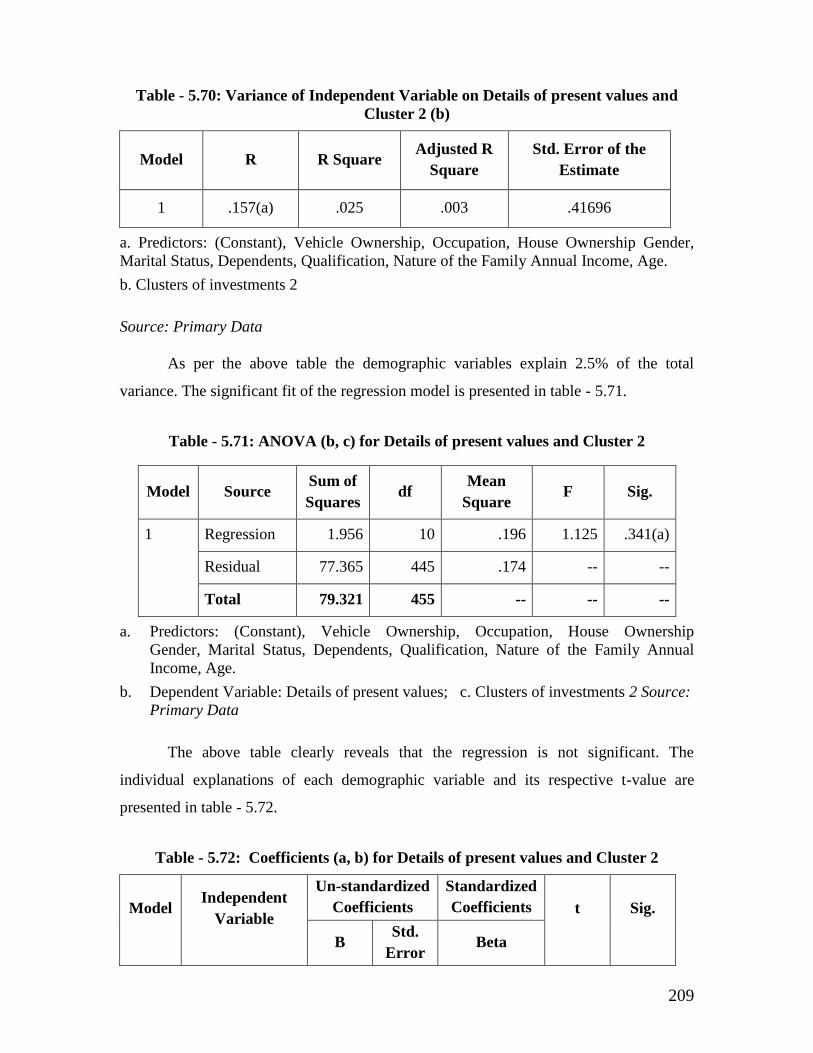

5.70 Variance of Independent Variable on Details of present values

and Cluster 2(b) 213

5.71 ANOVA (b,c) for Details of present values and Cluster 2 213

5.72 Coefficients (a, b) for Details of present values and Cluster2 214

5.73 Variance of Independent Variable on project details and their

changes and Cluster 1(b) 215

5.74 ANOVA (b,c) for project details and their changes and Cluster 1 215

5.75 Coefficients (a,b) for project details and their changes and

Cluster 1 216

5.76 Variance of Independent Variable on Project details and their

Changes and Cluster 2(b) 217

5.77 ANOVA (b, c) for project details and their changes and Cluster 2 217

5.78 Coefficients (a,b) for project details and their changes Cluster 2 218

5.79 Variance of Independent Variable on Financial parameters and

Cluster 1 (b) 219

5.80 ANOVA (b,c) for Financial parameters for Cluster 1 219

5.81 Coefficients (a, b) for Financial Parameters and Cluster 1 220

5.82 Variance of Independent Variable on Financial parameters and

Cluster 2 (b) 221

5.83 ANOVA (b, c) for Financial parameters for Cluster 2 221

5.84 Coefficients (a.b) for Financial parameters and Cluster 2 222

12

Table

No. Title

Page

No.

5.85 Impact of Retail investment preference of returns Amount

Received and Tests of Between – Subjects Effects 223

5.86 Impact of Demographic Variables on the investment objectives,

decision and satisfaction – Tests of Between –Subjects Effects 228

LIST OF FIGURES

Figure

No. Title

Page

No.

4.1 Age of the Investors 104

4.2 Gender of the Investors 105

4.3 Marital status of the Investors 106

4.4 Education of the Investors 107

4.5 Occupation of the Investors 109

4.6 Income of the Investors 110

4.7 Nature of the Family of Investors 111

4.8 Number of Dependents of the Investors 112

4.9 House ownership of the Investors 113

5.1 Investment pattern in stock market 235 - 236

13

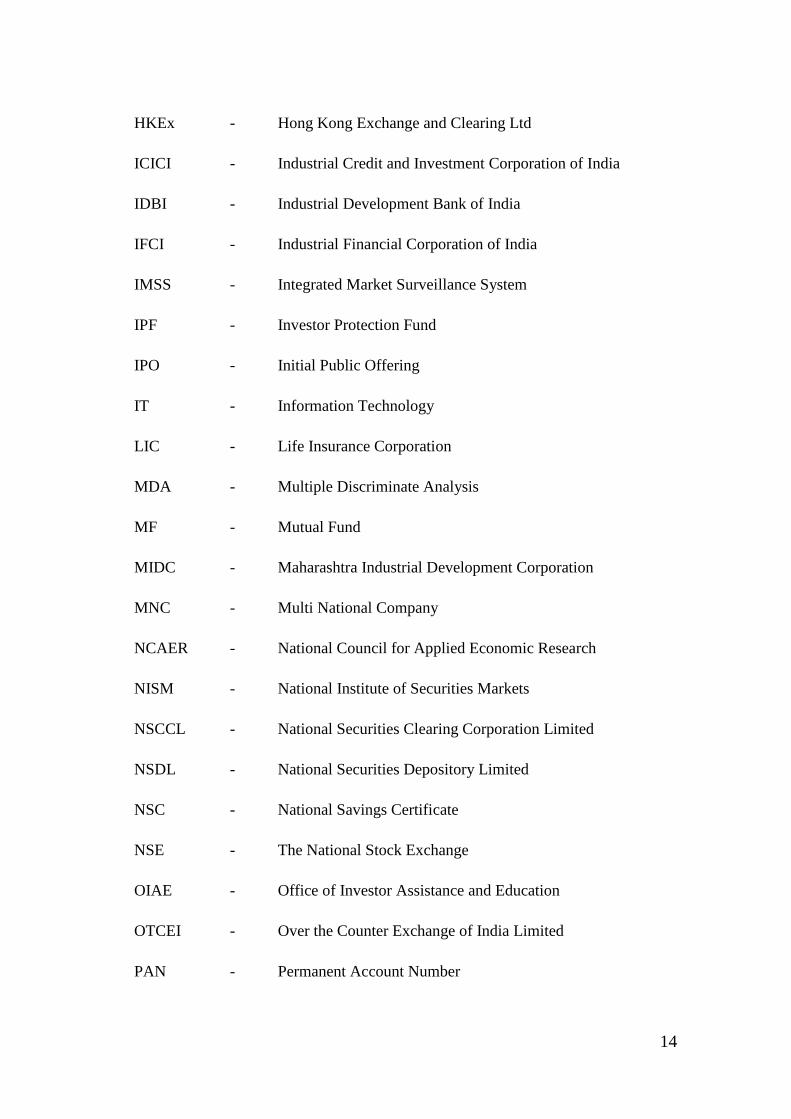

LIST OF ABBREVIATIONS

ADRs - American Depository Receipts

AMFI - Association of Mutual Funds in India

AUM - Assets Under Management

BSE - Bombay Stock Exchange

C&D - Corporatisation and Demutualisation

CAGR - Compounded Annual Growth Rate

CC - Clearing Corporation

CDSL - Central Depositary Services (India) Limited

CH - Clearing House

MSX - Madras Stock Exchange

ECS - Electronic Clearing Scheme

EDIFAR - Electronic Data Information Filing and Retrieval

EPS - Earnings Per Share

FAQs - Frequently Asked Questions

FIIs - Foreign Institutional Investors

FMCG - Fast Moving Consumer Goods

GDP - Gross Domestic Product

GDRs - Global Depository Receipts

GDS - Gross Domestic savings

GETFs - Gold Exchange Traded Funds

GIC - General Insurance Corporation

14

HKEx - Hong Kong Exchange and Clearing Ltd

ICICI - Industrial Credit and Investment Corporation of India

IDBI - Industrial Development Bank of India

IFCI - Industrial Financial Corporation of India

IMSS - Integrated Market Surveillance System

IPF - Investor Protection Fund

IPO - Initial Public Offering

IT - Information Technology

LIC - Life Insurance Corporation

MDA - Multiple Discriminate Analysis

MF - Mutual Fund

MIDC - Maharashtra Industrial Development Corporation

MNC - Multi National Company

NCAER - National Council for Applied Economic Research

NISM - National Institute of Securities Markets

NSCCL - National Securities Clearing Corporation Limited

NSDL - National Securities Depository Limited

NSC - National Savings Certificate

NSE - The National Stock Exchange

OIAE - Office of Investor Assistance and Education

OTCEI - Over the Counter Exchange of India Limited

PAN - Permanent Account Number

15

PE ratio - Price Earnings ratio

PPF - Public Provident Fund

PSE - Public Sector Enterprises

QIBs - Qualified Institutional Buyers

RBI - Reserve Bank of India

RSEs - Regional Stock Exchanges

SEBI - Security Exchange Board of India

SGF - Settlement Guarantee Fund

SMAC - Securities Market Awareness Campaign

STP - Straight Trough Processing

UTI - Unit Trust of India

VSAT - Very Small Aperture Terminal

16

CHAPTER - I

INTRODUCTION

Introduction Chapter deals with a brief note about importance of capital

market, Statement of the problem, Objectives of the study, Hypothesis, scope of the

study, Geographical coverage, Field work and collection of data, Limitations of the

study, Research methodology, Main study, Sample size, Tools used in the study,

Operational definitions and Chapter arrangement.

The capital market is used as a main vehicle to mobilize funds for the

economic growth of the country. It performs crucial functions like the conversion of

savings of the households and institutions into investment, creation of financial

assets and development of asset-related products. A well functioning securities

market is conducive to the sustained economic growth of any country in the world1.

There exists a direct relationship between the development in the securities market

and economic growth of a country. The securities market provides a bridge between

ultimate savers and ultimate investors and creates the opportunity to put the savings

of the cautious at the disposal of the enterprising, thus promising to raise the total

level of investment and growth. It allocates scarce savings to the enterprises and

forces them to focus on their performance, which is continuously evaluated through

share prices in the market. It thus converts a given stock of investible resources to a

large flow of goods and services.

The development of the securities market changes the quantum and

composition of savings and investment of the households. The availability of yield-

bearing securities induces people to consume less and invest more in high yielding,

divisible, liquid securities. A strong domestic stock market performance forms the

basis for the well performing domestic corporate to raise capital in the international

markets. The securities market facilitates the internationalization of the economy by

linking it with the rest of the world. This linkage happens through the inflow of

capital in the form of portfolio investment.

17

Financial markets across the globe are undergoing profound, unprecedented

and fast–paced changes2. Technology has revolutionized the processes and the

information explosion has sparked off remarkable changes in the way the world

market has been operating. Change has become an inevitable phenomenon.

Indian Capital market is one of the fastest growing markets in the world. It

has grown impressively during the recent years in tune with the global financial

markets. The Indian Capital Market comprises of two segments, namely, the

Primary and the Secondary market. The fresh issue of securities takes place in

primary market and trading among investors takes place in secondary market. The

primary market is the major channel through which the savings of the households

are mobilized by the companies directly for investment purposes. It is the centre

stage of the capital market that really boosts industrial and financial activities by

providing long term funds to the corporate and the government. It infuses new

securities, adding volume and wider base of securities in the secondary market. The

secondary market affords liquidity to the investment in securities and reflects the

general health of the economy.

Indian corporates mainly raise funds through capital market. Two types of

capital are essentially raised viz., Equity and Debt. Equity forms part of the net

worth and the Debt forms part of the outside liability of the firm. The capital raised

through equity is superior to that of debt capital for both the firm and the investor.

Equity enhances the borrowing power of the firm from banks and financial

institutions. If a firm is able to mobilize sizable amount of equity capital through

primary market, it can approach banks to fund long-term investment. From the

investor’s point of view, it could be noticed that over the long term, the equity

investments have out-performed debt and other asset classes across the globe. In

India, looking at the 8 years Compounded Annual Growth Rate (CAGR), equity

returns have out-performed debt to the tune of 15.8 percent3.

The Indian Capital Market has witnessed unprecedented euphoria from the

early nineties and it has won critical appreciation from various quarters4. At present

there are 19 Stock Exchanges in India. The National Stock Exchange (NSE) and

18

Bombay Stock Exchange (BSE) together account for more than 99 percent of the

total turnover having a combined market capitalization of $ 125.5 billion. Around

9600 companies are listed in NSE and BSE.

Success of equity issues totally depends on the confidence of the investors. If

the investors perceive high profitability prospects, they will invest in equity. There

are two types of investors, namely, institutional investors and retail investors

(households). Institutional investors are huge investors who operate through

Portfolio Managers. Portfolio Managers only shuffle around the holdings in the

existing scrips in their basket, based on their subjective evaluation of various scrips

but they do not inject the much needed risk capital to upcoming enterprises to

undertake new industrial activities. Even Foreign Institutional Investors (FII’s)

generally bring capital into the country only to acquire shares in the existing highly

profitable companies but do not provide risk capital to the corporate world. It is the

Retail Investor i.e. the household sector, who is the only source of providing risk

capital5. The Retail Investor provides this risk capital, either directly by investing in

equity market or through collective schemes popularly called as Mutual Funds.

There are 39 Mutual Funds offering about 600 schemes to the households, managing

assets to the tune of Rs. 3,10,171 crores (US $ 68 billion) at the end of October

20066. Indian retail investors have been directly participating in equity markets and

taking price fluctuations for decades. The household sector generates more than $ 30

billion of savings every year, which is available to the Indian financial system. It is

the only source of providing risk capital within the country.

It is globally recognized that the growth of the economy depends to a large

extent on the growth of the securities market, as it provides the vehicle for raising

resources and managing risks. The growth of the securities market is the result of

high confidence of the investors, that too the retail equity investors, the only risk

capital providers of yesterday, today and tomorrow.

1.2 STATEMENT OF THE PROBLEM

The stock market is one of the most vital and dynamic sectors in the financial

system making an important contribution to the economic development of a country.

19

Investors are the backbone of the capital market and they are not alike. Institutional

investors are capable of understanding the intricacies involved in the stock market

activities but the retail investors lack adequate awareness about it. As the bulk of the

savings of the country generally emanate from the households, and the retail investor

is still the major source of risk capital to upcoming enterprises, to undertake new

industrial activities, the capital market cannot grow without their participation,

directly or indirectly.

With the liberalization of the Indian capital markets, securities market has

grown into one of the most dynamic, modern and efficient markets. The

infrastructure and operating efficiency of the Indian stock markets are well

appreciated by its global counterparts. In India, to encourage, enhance and safeguard

retail investor participation and to make the markets more efficient, a number of

reforms have been initiated by the Security Exchange Board of India (SEBI). In the

case of fixed price public issues and book built issues, 50 percent and 35 percent

shares respectively are being allotted to the retail investors7. As small investors find

it difficult to participate directly in the capital market to a significant extent, SEBI

encourages mutual fund industry to offer innovative products to suit the risk appetite

of the retail investors.

In spite of all the efforts taken by SEBI to attract and enhance retail

participation, the household (retail) savings and investment scenario is highly

disappointing. According to the SEBI – NCAER survey, only 7.4 per cent of the

Indian households directly participated in the securities market in 2000 as against

about 50 percent in the USA. As the economy grew at 8.5% in 2003-04, GDS (Gross

Domestic Savings) rate reached 28.1 percent of GDP, (Gross Domestic Product) and

the household financial savings increased to 11.4 percent of GDP, but the capital

market instruments contributed barely 1.4 percent of the financial savings and

investment. In 2004 – 2005, though India’s GDS in proportion to GDP was 29.1

percent, the investment by households in shares and debentures stood at a meager

0.8 percent of GDP8.

20

Despite the developments happening in the capital market in India and even

after a decade of existence of a vibrant capital market, the equity instruments are not

considered as an attractive household investment.

The ill effect of such a phenomenon is that, if such a situation persists, the

performance of the capital markets will be determined and dominated by a few large

and wealthy players. High dependence on FII funds will lead to a volatile and high

risk market which will make the retail investor the only risk capital provider-extinct.

This will hamper the whole growth of the securities market and in turn the economic

growth of the nation. So bringing the retail investors back into the equity market

would be a very healthy structural development for the nation itself.

The recent economic recession had a great impact on stock market. The

developing countries also taste the economic downtrend. The Indian economy is also

not left out. Before the recession, Indian economy was moving at a faster rate

because of the growth in information technology and other sectors. But after the

recession the economic level comes down and there will be some velocity in the

Indian stock market conditions. As the regulatory system is so strong in India, the

stock market is able to withstand many odds. Since the stock market is all the time

unpredictable and unstable, the investors are all the time at very high risk. They have

to consider many factors like Economic environment, Political stability, Industrial

growth etc., before they invest. Though there are many studies on the stock market

related areas, the information provided to the investor and industry is not sufficient.

As a result the investor and the stock market players will be searching for required

information. There are some research gaps in the existing literature relating to the

stock market.

Hence the current study is undertaken to fill the gaps in the existing research

in the field of stock market and also to provide required information to the investors

as well as industry.

21

1.3 OBJECTIVES OF THE STUDY

1. To study the investment pattern of retail equity investors in Chennai.

2. To analyse the information search and investment option of retail investors.

3. To identify the various investment preferences and investors perception on

risk and return.

4. To examine factors influencing investment evaluation and decision of

investors.

5. To evaluate investors level of satisfaction and their futuristic perceptions

towards retail equity investment.

6. To find the relationship between demographic variables of investors and

their investment objectives, decision and satisfaction.

1.4 RESEARCH HYPOTHESES

1. There is no significant difference between level of risk and returns of

investors.

2. There is no association between investment objectives and satisfaction.

3. There is no association between investment decision and satisfaction.

4. There is no significant influence of demographic variables of investors and

investment objectives, decision and satisfaction.

5. The factors of level of investor’s satisfaction do not differ significantly with

respect to share investments.

1.5 SCOPE OF THE STUDY

The present study covers the investment pattern with regard to retail

investment in equity shares. This study opens fascinating vistas over investor’s

22

preference, perceptional differences and their predominant objectives. This also

paves the way to study the pre and post investment satisfaction in an intensified

manner. It also focuses exact problems associated with equity investment of retail

equity investors in Chennai city.

1.6 GEOGRAPHICAL COVERAGE

The area of coverage of the study is Chennai the capital of Tamilnadu in

India. Chennai is opted for study because of its role in industrial and economic

development of the country.

1.7 FIELD WORK AND COLLECTION OF DATA

Personal interview by the researcher is the major tool used for data

collection. Structured interview schedule is used during personal interviews.

Interviews are conducted at various stock broking houses and at the residence of the

equity investors at their convenience. Before the interview, proper rapport is

established. The data collected are recorded by the researcher in the interview

schedule. The schedules thus filled up are thoroughly checked to ensure accuracy,

consistency and completeness. On an average, each interview took about an hour.

The data thus collected were categorized and posted in the master table for further

processing.

1.8 LIMITATIONS OF THE STUDY

The major limitations of the study are:-

The study is confined to Chennai District alone. Hence the findings

may not be generalised for the other parts of the country.

The study is confined to the retail equity investors alone. Institutional

investors remain uncovered.

The limitations associated with the statistical tools are applicable for the

tools employed in this study also.

23

RESEARCH METHODOLOGY

1.9 PILOT STUDY AND PRE-TESTING

A preliminary investigation is undertaken by contacting 75 investors of

equity shares to identify the important variables regarding characteristic features of

equity shares, instrument and the changes, return of investments, investment

decisions and satisfaction. The purpose of the pilot study is to test the quality of the

items in the questionnaire and to confirm the feasibility of the study. This

preliminary investigation is conducted in different parts of Chennai. The random

sampling method, Cronbach alpha method and Hotellings t-square test are applied. It

is found that the Cronbach alpha value is 0.912 and hotelling t-square value is

422.31 which are statistically significant at 5 per cent level.

It is ascertained that the items in Likert’s five point scale of the questionnaire

are highly reliable and the samples satisfy the normal distribution rationally. So, the

items in the questionnaire can be used further in the study.

1.10 MAIN STUDY

The data is collected for the study by means of a two section questionnaire

(refer Appendix). Section 1 for the questionnaire is framed to obtain the general

information about investment preferences, percentage of investment in equity shares

and different portfolio and sources of information of the equity investment. Section

II deals with the characteristic features of equity shares, their changes, and return on

investments. The section –I of the questionnaire is designed in optional type, where

as the section II is designed in Likerts 5-point scale, ranging from 5-strongly agree,

4-agree, 3-neutral, 2-disagree, 1-strongly disagree. The questionnaire with covering

letter is handed over personally to each and every respondent and they are requested

to return the filled in questionnaire after 15 days, when the researchers visit them.

The respondents took the period of 15 days to 2 months to return the completed

questionnaire.

24

1.11 SAMPLE SIZE

Initially 623 questionnaires are circulated to investors in all the areas of

Chennai city, by following simple random sampling method. Out of the 623

questionnaires only 514 respondents returned the filled in questionnaires. But only

507 of them are found usable. Hence, the exact sample of the study is 507.

1.12 DATA ANALYSIS

The sources of data are primary as well as secondary. The data collected

from the investors’ survey constitutes primary and information gathered through

books, journals, magazines, reports, dairies are considered as the secondary source.

The data collected from both the sources is scrutinized, edited and tabulated. The

data is analyzed using statistical package for social sciences (SPSS) and other

computer packages. The following statistical tools are used in the study.

1. Measures of central tendency and measures of dispersion.

2. Parametric t-test.

3. One-way analysis of variance.

4. Factor analysis.

5. K-means cluster analysis.

6. Multiple discriminant analysis

7. Multiple regression analysis.

8. Non-parametric chi-square analysis

1.13 OPERATIONAL DEFINITIONS

a. Investment

The use of capital is to create money, either through income producing

vehicles or through more risky ventures designed to create capital gains.

25

b. Investment Practices

Usual and repeated way of doing investment (i.e.) usual investment pattern,

preferences, perceptions, investment objectives, factors generally influencing

investments, investment satisfaction, investor’s confidence and problems faced by

investors regularly.

c. Retail Equity Investor

Individual share investor or households investing in shares or small investor.

d. Institutional Investor

Corporates investing huge money in securities.

e. Primary Market

A market where corporates directly issue securities i.e., where initial public

offering is made.

f. Secondary Market

A market where the already issued securities are traded.

g. Mutual Funds

Small investor, collective investment scheme.

h. Derivatives

Financial contracts, whose values are derived from the value of an

underlying primary financial instrument (i.e.) stock futures and options.

i. Dividend

The part of company’s profit distributed to shareholders.

j. Capital Gain

26

Gain arising due to sale of stock.

k. Liquidity

Availability of stock coupled with buyers and sellers for it in the market.

l. Volatility

Sharp rise or fall of share prices over a short period of time.

m. Rights, Bonus and Stock Splits

Rights : A Method of raising additional capital from the existing share

holders.

Bonus : Shares are issued to the existing shareholders at free of

cost in some decided ratio.

Stock splits : Splitting the face value of existing shares and distributing

additional shares on pro-rata to shareholders.

n. Floor Based, Forward Trading

Trading on the stock exchange floor, where contracts traded today are settled

at some future date at the price decided today.

o. Anonymous Screen Based Electronic Trading

Buying and selling of securities using computers and electronic matching of

orders on price / time priority without knowing who the trader is.

p. Clearing and T+2 Rolling Settlement

Clearing is the process by which all the transactions between members are

settled. T+2 Rolling Settlement is the system where trades executed during the day

are settled based on the net obligations for the day. The maximum time that may be

taken for settlement is T+2 (i.e.) Trading day + 2 working days.

27

q. Straight Through Processing (STP)

STP is a system, which allows electronic capturing and processing of

transactions in one pass from the point of order origination to the final settlement.

r. Dematerialisation

The process by which shares in the paper form are converted into electronic

form popularly called as demat.

s. Market Capitalisation

The market value of a company found by multiplying the number of ordinary

shares outstanding with its current market price.

t. Fundamental Analysis

Method of predicting the behaviour of company stock by looking at

fundamental information about the company such as financial health, sales, earnings

and dividends.

u. Technical Analysis

Techniques of predicting share price behaviour by studying the price

movements and trading volumes using charts.

v. Corporatisation and Demutualisation

The system where ownership, management and trading membership would

be segregated from one another.

w. Settlement Guarantee Fund

Fund maintained by the stock exchange to take care of investor claims,

which may arise out of non-settlement of obligations by the trading member as he

has been declared a defaulter or expelled.

28

x. Circuit Breakers

It is an investor protection measure by SEBI to curb excessive price

volatility. It brings about a nation – wide coordinated halt in trading on all equities.

y. Mark-to-Market Margin

It is a risk containment measure computed based on mark-to-market loss of a

trading / clearing member.

z. VaR Based Margins

It is a risk containment measure intended to cover the largest loss that can be

encountered on 99% (value at risk) of the days.

1.14 CHAPTER ARRANGEMENT

Chapter - I Introduction - deals with a brief account on history of equity shares,

elements of equity shares, need and importance of the study and research

methodology.

Chapter - II Review of literature - relevant to the present study, studies on

information search, awareness of factors of characteristics of equity shares and

capital market and investment preferences are included in this chapter.

Chapter - III A conceptual frame work of Indian Equity shares - An Overview -

explains the growth of the market, trends in various years and certain important

overviews.

Chapter - IV Analysis of investment preference and decision deals with an

analysis of primary data with the help of statistical tool.

Chapter - V Analysis of investment satisfaction and portfolio choice –encounters

with multivariate statistical analysis of the primary data

29

Chapter - VI Summary of Findings, Suggestions and Conclusions - summarizes

the findings along with the suggestions to the investors for framing the investment

strategies.

1.15 SUMMARY

In this chapter, the research design is adopted as per the norms and followed

by review of literature in the next chapter.

REFERENCES

1 Levine and Ross, “Stock market Development and Economic Growth”, The

world Bank Economic Review, Vol. 1012), 2008, pp: 323 – 339.

2 Bajpai G.N, “Indian Securities Markets – New Bench Marks”, SEBI

Bulletin, Vol.1, No.8, August 2009, pp: 5-14.

3 “Retail Investments into Equity”, IIM Working paper series, E27119, p:4.

4 Tarapore wala, Russi Jai, “The Union Budget 2005 -06 and the Capital

Market”, BMA Review, Vol. III, No.26, March 14-278, 2006.

5 Ramesh Gupta, “Retail Investor – A lost Species”, IIM Working paper

series, E 15378, p:1.

6 Chopra V.K, “Capital Market Reforms in India: Recent Initiatives”, SEBI

Bulletin, Vol.4, No. 11, Nov 2008, pp: 7-11.

7 Chopra V. K, “Investor Protection: An Indian Perspective”, SEBI Bulletin,

Vol.4, No.11, Nov 2010, pp: 11-15.

8 Ibid., Pp.24-26

30

CHAPTER - II

REVIEW OF PREVIOUS STUDIES

INTRODUCTION

Chapter two portrays review of literature, which briefly discusses about six

objectives which is stated in the objectives of the study.

Behavioural Finance is the study of how humans interpret and act on

information to make informed investment decisions. It is one of the most interesting

and fascinating fields of research throwing light on the motives, preferences,

perceptions and expectations of the investors. The emergence of behavioural finance

has presented a new realm for analyzing the ways in which investors make decisions

that includes psychological factors, as well as providing new grounds of modeling

investor behaviour. The study of investor behaviour has attracted researchers with a

variety of backgrounds. In this chapter the various literatures over a period of 10

years has been reviewed and presented.

2.2 The investment profile and pattern of retail equity investors.

1. Mart Grinblatt and Matti Keloharju, (2011), in their study entitled, “The

Investment Behaviour and Performance of Various Investor Types: Study of

Finland’s Unique Data set”, analysed the extent to which past returns

determine the propensity to buy and sell. The study revealed that foreign

investors tend to be momentum investors, buying past winning stocks and

selling past losers. Domestic investors, particularly households contradicted

the same. This difference in Investor behaviour was consistent in regular

intervals. The portfolios of foreign investors outperformed the portfolios of

households, even after controlling the behaviour difference.

2. Maruthu Pandian. P, Benjamin Christopher , (2010), conducted a study

entitled, “A Study on Equity Investor Awareness” in order to study the stock

31

market literacy of the investors about the company, stock exchanges as well

as capital market regulatory bodies. The primary data using multiple

regression, path analysis and chi-square test along with ANOVA clearly

revives difference in the awareness among the investors. The research work

found that the awareness index is high among young male investor, post-

graduates and meticulous business men.

3. Society for Capital Market Research and Development, (2009), conducted a

survey entitled, “Indian Household Investors Survey-2004”, the study was

based on direct interviewing of a very large sample of 5908 household heads

over 90 cities and across 24 states. The study states that price volatility, price

manipulation and corporate mismanagement / fraud have persistently been

the household investors’ top three worries in India. A large percentage of

investors had a negative opinion on company managements. A majority of

retail investors in India do not regard mutual fund equity schemes as a

superior investment alternative to direct holding of equity shares. Retail

investors overwhelmingly prefer bank deposits rather than liquid / money

market funds. Shareholding in 3-10 companies is the dominant practice

among retail shareholders in all income and age classes. Middleclass

investors are long term and conservative. Equity shares have achieved a

much higher degree of penetration among middleclass households compared

to other capital market instruments.

4. HorstRaff and Michael J.Ryan, (2008), in their paper, “Firm-Specific

Characteristics and the Timing of Foreign Direct Investment Projects”, this

paper uses a proportional hazard model to study foreign direct investment by

Japanese manufacturers in Europe between 1970 and 1994. We divide each

firm’s investment total into a sequence of individual investment decisions

and analyze how firm-specific characteristics affect each decision. We find

that total factor productivity is a significant determinant of a firm’s initial

and subsequent investments. Parent-firm size does not have a significant

influence on the initial decision to invest. Large firms simply have more

investments than smaller firms. Other firm-specific characteristics, such as

32

the R&D intensity, export share and keiretsu membership, also play a role in

the investment process.

5. Sudershan kuntluru and D. Mohd Akbar Alikhan , (2009) , in their article,

“Financing pattern of foreign and domestic owned pharmaceutical

companies in India”, foreign Direct investment has often seen as major

source of long term capital which provides bundle of other benefits to the

host county company. In this paper, we made an attempt to examine the

financing pattern of foreign and domestic owned pharmaceutical companies

in India. It has been hypothesized that there is no significant difference

between the financing pattern of domestic and foreign owned companies.

The financing pattern has been analyzed based on traditional methodology

such as common size statement, trend analysis and ratio analysis. The results

and analysis indicate mat domestic companies are highly levered than

foreign owned companies in pharmaceutical industry.

6. William A. Birdthistle and M. Todd Henderson, (2009), in their article, “one

Hat Too many? Investment Desegregation in private Equity”, the nature of

private-equity investing has changed significantly as two dynamics have

evolved in recent years: portfolio companies have begun to experience

serious financial distress, and general partners have started to diversify and

desegregate their investment strategies. Both developments have led private-

equity shops—once exclusively interested in acquiring equity positions

through leveraged buyouts—to invest in other trenches of the investment

spectrum, most particularly public debt. By investing now in both private

equity and public debt of the same issuer, general partners are generating a

host of new conflicts of interest between themselves and their limited

partners, between multiple general partners in the same consortia, and

between private investors and public shareholders.

7. Diptendu simlai, (2009), in his paper, “An inquiry into the origin and growth

of the capital market in India”, India’s modern capital market did not emerge

in a day. This market, since its inception in the 18th century with the

33

establishment of the Bank of Hindustan (1770) in Calcutta, laid the

foundation of the modern capital market in India according to A. K. Sur, a

noted stock market economist of his time (Sur, Evolution of Capital Market

in India, Economic Affairs, Nov-Dec/1960). The objective of this paper is to

trace the evolution of this market right from the late 18th century up to our

times. For purposes of our study the entire time span has been divided into

four periods. The first covers the 18th and 19th centuries. The second

extends from the early 20th century up to 1947, the year of Independence.

For the enormous impact of the economic reforms upon the capital market,

the post-Independence era has been divided into two periods: one ending

with 1990 and the other starting with 1991.

8. Yadagiri. M and P.Rajender, (2009), in their article, “Analysis of investment

portfolio of scheduled commercial banks”, the reforms have unleased

tremendous changes in the banking sector. The government of India issued

guidelines to the banks by permitting and encouraging them to diversify their

activities and contributing to the equity of companies by offering financial

services.

2.3 The information search and investment option of retail investors.

9. Bloomfield, Libby and Nelson, (2011), in their study entitled, “Confidence

and the Welfare of Less Informed Investors”, have indicated that less

informed investors are over confident in investments. Providing more

information to professional investors only could harm the welfare of less

informed investors if less informed investors are not aware of the extent of

their informational disadvantage.

10. Statman, (2010), in his research entitled, “A Century of Investors”,

compared the investors a century ago with investors today. He concluded

that today’s investors are more rapidly informed than their predecessors, but

they are neither better informed nor better behaved.

34

11. Stout, (2010), in his study entitled, “The Investor Game”, has indicated that

investors have adaptive and not rational expectations. Adaptive expectations

result in both trust and mistrust in securities market based on past actions.

12. Shivkumar Deene, Madari D.M and Gangashetty, (2009), in their paper,

“Capital market Reforms: some issues”, capital market is vital for the

development and strength of economy. A strong and vibrant capital market

assists corporate world initiatives, finance and exploration of new processes

and instruments facilitates management of financial risk. Retail investor is

the backbone of the capital market. But with the expansion of the capital

market, scams and anomalies, also multiplies. It ultimately leads to the

dilution of the faith of the small investor, mutual funds, pension funds,

Foreign Institutional Investor and insurance companies in the capital.

Realising that the government made different as capital market reforms. This

includes educating capital market participants regarding their rights and

duties for proper functioning of capital market.

13. Alok Kumar, (2009), in his paper, “Who Gambles In the Stock Market? “this

paper examines whether socio-economic and psychological factors, which

are known to influence lottery purchases, lead to excess investment in

lottery-type stocks. The results indicate that, unlike institutional investors,

individual investors prefer stocks with lottery-type features. The demand for

lottery-type stocks increases during bad economic times and demand shifts

influence the returns and idiosyncratic volatility of those stocks. The

evidence of the study indicates that people’s attitudes towards gambling are

reflected in their stock investment choices and stock returns.

14. Nagarajan. R, (2006), in his article, “Green shoe option in IPO”, for

stabilizing post-listing share price, a company making an Initial Public Offer

(IPO) through the Book Building mechanism can hold the Green Shoe

Option. This is an option that allows underwriter of an Initial Public Offering

to sell additional shares to the public. The challenge for the regulator would

be to keep fraudulent issues away from the market. In order to avoid

35

fraudulent issues investors too should do their homework before investing in

IPO, because it is investor's hard earned money and he should invest it

carefully.

15. Subha. M.V, (2008), in her article entitled, “Indian Capital Markets–A Road

Ahead”, addressed the current issues in the Indian capital market, lack of

individual participation and the ways of restoring investor confidence. The

article concluded that the responsibility of creating an environment of trust

and confidence lies with the regulators, stock exchanges and companies.

Each of them should act in a responsible way and provide a healthy

atmosphere for the functioning of an efficient capital market.

16. Kavitha Ranganathan (2008), in their paper, “A study of fund selection

behavior of individual investors towards mutual funds: With reference to

Mumbai city”, consumer behavior from the marketing world and financial

economics has brought together to the surface an exciting area for study and

research: Behavioral finance. As this is a serious subject analysts seem to

treat financial markets as an aggregate of statistical observations, technical

and fundamental analysis. A rich view of research waits this sophisticated

understanding of how financial markets are also affected by the “financial

behavior” of investors. Hence, this study is an attempt to examine the related

aspects of the fund selection behavior of individual investors towards mutual

funds, in the city of Mumbai and it showed the way for further research in

this field.

17. Jones Nilsson , (2007), in his article, “Investment with a Conscience:

Examining the Impact of Pro-Social Attitudes and Perceived Financial

Performance on Socially Responsible Investment Behavior”, this article

addresses the growing industry of retail socially responsible investment

(SRI) profiled mutual funds. The study examined the impact of a number of

pro-social, financial performance, and socio-demographic variables on SRI

behavior in order to explain why investors choose to invest different

proportions of their investment portfolio in SRI profiled funds. Some 528

36

private investors including women were investigated the results showed that

women and better-educated investors were more likely to invest a greater

proportion of their investment portfolio in SRI. Overall, the findings indicate

that both financial perceptions and pro-social attitudes are connected to

consumer investment in SRI.

18. Mahabaleswara Bhatta. H.S., (2009), in his paper, “Behavioral Finance- A

discussion his individual investor biases”, in this article, an attempt has

been made to throw light on the investors’ biases that influence decision

making process. Empirical studies have time and again proved that the

irrational behaviors have caused stock market bubbles and crashes. The

knowledge so developed through the studies would provide a framework of

behavioral principles within which the investors react. The article suggests

for a time bound program to educate and counsel the individual investors

about the wisdom required in stock trading and be aware of unethical and

tactical practices of brokers ,shady dealings of the companies and the insider

trading.

19. Chattopadhyay. P, (2010), in his article, “Retail investors in IPO

subscription”, in the liberalization regime of India, there has been a renewed

emphasis on the equity cult and a growing stress of what is termed market

capitalization. The number of retail investors has already become substantial

and is still growing. This underlines the need for safety and security of the

money invested along with the promise of augmented yield. These have

required the government and the regulatory bodies to provide necessary

systems and methods for safeguarding the interests of the small, retail

investors The Securities and Exchange Board of India has recently mooted a

proposal to the effect that in the cases of retail investors seeking to subscribe

to the share offers by the public limited companies, cash transactions should

take place only after the allotment has been made. The proposed intention of

SEBI is to be lauded; there are other parts which are not as commendable.

The proposal does not appear fool-proof on one side, and may be easily

subject to abuse, on the other. Least of all, the proposal may not restore

37

parity between the institutional and retail investors, which is the major

objective of the new approach. The steps taken by the regulatory authorities

are not enough and the centrifugal forces triggered internally, that would lead

to undesirable repercussion.

2.4 Investment preferences and investors perception on risk and return.

20. Rajarajan. V, (2011), conducted a study entitled, “Investors Life Styles and

Investment Characteristics”, with the objective of analyzing the investors life

styles and to analyse the investment size, pattern, preference of individual

investors on the basis of their life styles. Data was collected from 405

investors in Madras using questionnaire method. The investors were

classified into 3 groups’ viz., active investors, individualists and passive

investors. Cluster Analysis, Correspondence Analysis and Kruskal Wallis

Test were used to study the association between lifestyle groups and the

various investment related characteristics. The study revealed that the level

of expenses, earnings and investment were associated with the size of the

household. Active investor group was dominated by officers, individual

group by clerical cadre and passive investors group by professionals. The

expected rate of return from investments varied between investment styles.

The study clearly indicated that market performance of the share, company’s

operating level, capital performance and the expectation of the investors

were found to influence the risk perception of the investors.

21. Bandgar. P.K, (2011), in his study entitled, “A Study of Middleclass

Investor’s Preferences for Financial Instruments in Greater Bombay”, studied

the existing pattern of financial instruments in India and the performance of

middle class investors, their behaviour and problems. Questionnaire was

administered to collect data. Average, Skewness, Chi-square test and Fisher

Irving Test were used to analyse the data. The study revealed that only 16%

of the investors were facing difficulties in buying and selling securities.

Middle-class investors were highly educated but they were lacking skill and

knowledge to invest. Female investors preferred to invest in risky securities

38

as compared to male investors. The study also revealed that there was a

moderate and continuing shift from bank deposits to shares and debentures,

and a massive shift towards traditional financial instruments namely, life

insurance policies and government securities.

22. Charles Lee, M.C and Balakrishna Radhakrishna, (2010), in an article

entitled, “Inferring Investor Behaviours: Evidence from TORQ Data”, made

an attempt to examine the several techniques commonly used to infer

investor behaviour from transaction data. They adopted Lee-Ready (1991)

algorithm for distinguishing trade decision. The results show that frequency,

size and direction of observed trades provide a reasonable basis for

evaluating the incoming flow of market orders.

23. Dechow, Hutton and Sloan, (2011), in their study entitled, “Mastering

Finance”, found that analysts’ growth forecasts are routinely over optimistic

around new equity offerings, but the most over optimistic are those analysts

employed by the lead underwriters of the offerings.

24. Malcolm Baker and Jeffrey Wurgler, (2011), in their paper, “A catering

theory of dividends”, we develop a theory in which the decision to pay

dividends is driven by investor demand. Managers cater to investors by

paying dividends when investors put a stock price premium on payers and

not paying when investors prefer nonpayer. To test this prediction, we

construct four time series measures of the investor demand for dividend

payers. By each measure, nonpayer’s initiate dividends when demand for

payers is high. By some measures, payers omit dividends when demand is

low. Further analysis confirms that the results are better explained by the

catering theory than other theories of dividends.

25. Selvam. M, et.al, (2010), in their study entitled, “Equity Culture in Indian

Capital Market’, examined the need for promoting equity culture, which

deserves special attention for the development of economic growth. The

study discussed in detail the current trend of equity culture, its implications

39

and its revival and remedial measures. The study suggested intervention by

government, SEBI and RBI and evaluation of suitable credit policy for

projects in order to assure safety and assured returns to the investors, in order

to restore investor confidence.

26. Alexander LJungquist and Matthew Richardson , (2010), in his study, “The

Investment Behaviour of Private Equity Fund managers”, using a unique

dataset of private equity funds over the last two decades, this paper analyzes

the investment behavior of private equity fund managers. Based on recent

theoretical advances, we link the timing of funds’ investment and exit

decisions, and the subsequent returns they earn on their portfolio companies,

to changes in the demand for private equity in a setting where the supply of

capital is ‘sticky’ in the short run. We show that existing funds accelerate

their investment flows and earn higher returns when investment opportunities

improve and the demand for capital increases. Increases in supply lead to

tougher competition for deal flow, and private equity fund managers respond

by cutting their investment spending. These findings provide complementary

evidence to recent papers documenting the determinants of fund-level

performance in private equity.

27. Santi Swarup. K, (2010), in his survey entitled, “Measures for Improving

Common Investor Confidence in Indian Primary Market: A Survey”,

analysed the decisions taken by the investors while investing in primary

markets in the first part: secondly the factors affecting primary market

situation in India was analysed and finally the survey evaluates various

revival measures available for improving investor confidence. The survey

was conducted in 10 cities in India by mailing questionnaire. The survey

results of 367 investors revealed that the investors give importance to own

analysis and market price as compared to broker’s advice.

28. Stephanie Desrosiers, Jean - Francois L”Her and Jean – Francois Plante ,

(2010), in their article, “Style management in Equity Country Allocation”,

strategies that entailed country selection based on relative strength

40

(momentum) posted significant market risk– adjusted returns over the past

30 years, but relative-value strategies based on book value of equity to

market value of equity did not. Because these two fixed-style strategies are

negatively correlated, using them for style diversification and for style timing

(rotation) is potentially rewarding. In the study described here, style

diversification enhanced return and lowered risk but style timing provided

consistent risk-adjusted performance that was superior to the performance of

fixed-style strategies or style diversification.

29. Jaspal Singh and subhash chandler , (2011) , in their article, “Investors’

preference for investment in mutual funds: An empirical evidence”, since

interest rates on investments like PPF, NSC, bank deposits, etc., are falling,

the question to be answered is: What investment alternative should a small

investor adopt? One of the alternatives is to invest in capital markets through

mutual funds. This helps the investor avoid the risks involved in direct

investment. Considering the state of mind of the general investor, this article

figures out: (i) the preference attached to different investment avenues by the

investors; (ii) the preference of mutual funds schemes over others for

investment; (iii) the source from which the investor gets information about

mutual funds; and (iv) the experience with regard to returns from mutual

funds. The results show that the investors consider gold to be the most

preferred form of investment, followed by NSC and post Office schemes.

Hence, the basic psyche of an Indian investor, who still prefers to keep his

savings in the form of yellow metal, is indicated. Investors belonging to the

salaried category, and in the age group of 20-35, years showed inclination

towards close-ended growth (equity-oriented) schemes over the other scheme

types. A majority of the investors based their investment decision on the

advice of brokers, professionals and financial advisors. The findings also

reveal the varied experiences of respondents regarding the returns received

from investments made in mutual funds.

30. Gnana Desigan. C. et.al, (2011), in their study entitled, “Women Investors

Perception Towards Investment–An Empirical Study”, identified the

41

investment pattern, preference, influencing factors and problems of women

investors in Erode town. The findings of the study reveal that, women

investors prefer to invest in bank deposits and jeweler, they are influenced by

safety and liquidity and the problems faced by them are cumbersome

procedures and formalities, commission and brokerage.

31. Shobana. V.K. and Jayalakshmi. J, (2010), in their study entitled, “Investor

Awareness and Preferences”, studied the investors’ preferences, the level of

investor awareness and the factors influencing investor awareness of 100

respondents in Salem District. The study reveals that real estate, bank

deposits and jeweler were the preferred investments. Investors above 50

years of age, post graduates and professionals had high level of awareness.

Age and education do not have any significant influence over investor

awareness but occupational status leads to difference in the awareness level

of people.

32. Meir Statman, Steven Thorley and Keith Vorkink, (2010), in their paper,

“Investor overconfidence and Trading volume”, the proposition that

investors are overconfident about their valuation and trading skills can

explain high observed trading volume. With biased self-attribution, the level

of investor overconfidence and thus trading volume varies with past returns.

We test the trading volume predictions of formal overconfidence models and

find that share turnover is positively related to lag returns for many months.

The relationship holds for both market-wide and individual security turnover,

which we interpret as evidence of investor overconfidence and the

disposition effect, respectively. Security volume is more responsive to

market return shocks than to security return shocks, and both relationships

are more pronounced in small-cap stocks and in earlier periods where

individual investors hold a greater proportion of shares.

33. Viswambharan A.M, (2008), in his article entitled, “Indian Primary Market –

Opportunities and Challenges”, has examined the recent trends in primary

market, the current IPO system – book building process, opportunities for

42

investors, problems faced by the investors and has suggested that investors

should rely on long term investment than speculation. Investor education

shall be strengthened. Commercial banks may take-up investment

consultancy for their clients to improve investor participation.

34. Narendra Jadhav, (2010), in his article, “Development of Securities Market –

The Indian Experience”, the Indian securities markets have witnessed far-

reaching reforms in the post-liberalization era in terms of market design,

technological developments, settlement practices and introduction of new

instruments. The markets have achieved tremendous stability and as a result,

have attracted huge investments by foreign investors. There still is

tremendous scope for improvement in both the equity market and the

government Securities market. However, it is the corporate debt market,

which needs to be given particular emphasis given its importance for

providing long-term finance for development.

35. Dan palmon and Fred Sudit, (2011), in their article, “shareholders’ defensive

security shares”, the purpose of this paper is to explore the possibilities and

merits of offering shareholders an equity instrument (new class of common

shares) designed to protect their investments from managerial opportunism.

To this end, we propose a special class of shares, the Shareholders ’

Defensive Security Shares (SDSS), which would oblige Boards of Directors

to declare a pre-specified extra dividend whenever executive pay exceeds a

contractually pre-determined threshold. SDSS could be extended into a

larger class of Defensive Security Instruments (DSI) that includes regular

bonds, convertible bonds, and preferred stocks. We argue that this defensive

equity, the Shareholders ’ Defensive Security, or SDSS, could be beneficial

to managers as well as shareholders. What’s more, the use of SDSS is

completely voluntary and requires no additional regulation.

36. Kameswari. P, (2008), in his article, “Foreign Direct investment and its role

in developing Indian economy”, investment is an important factor in

influencing the economic development of a country. Developing countries

43

like India have investment requirements far greater than their domestic

savings can meet. Their investment deficits can be bridged by foreign capital

flows in the form of Foreign Direct Investment and Portfolio Investment.

But the huge flows of foreign capital may introduce some problems like

inflation. In the interest of future economic growth and development a

developing economy has to institute some safeguards in its national interest

while welcoming the foreign investment. This article studies how India is

faring in its efforts to attract foreign direct investment and in channelising

the flows for the growth of economic development.

37. Som Sankar Sen and Santanu Kumar Ghosh , (2008) , in their paper, “Stock

Market Liquidity of BSE and NSE: A Comparative Study (1995- 2005)”, this

study compares between BSE and NSE in terms of Stock Market Liquidity

during the study period of January 1995 to December 2005. The study

reports that mean liquidity of NSE is higher than that of the BSE during this

period. It also reveals that in most of the months BSE remains more

vulnerable than NSE during this span of time in terms of liquidity. A

monthly pattern of liquidity could be observed in case of NSE but no such

monthly pattern is there in case of BSE. Finally, a positive correlation

between these two exchanges has been reported indicating no significant

movement of volume from one exchange to another.

38. Nissim Ben David, (2008), in his paper, “An indicator for internalization of

analyst’s recommendations by investors”, this paper proposes an index for

evaluating the internalization of an analyst’s recommendations by investors

at various points of time that follow the recommendation day. The model is

applied to the Israeli stock market for the years 2004 and 2005. The results

indicate that investors in the Israeli stock market internalize a

recommendation 14 days after its publication. Internalization continues 30

days after the publication day. The importance of this paper is that it is the

first time an index for evaluating investor’s reaction to analyst’s

recommendations in various stock markets has been proposed. Such

information is valuable, since it can improve investment strategies that

44

follow the publication of an analyst’s recommendation. An investor would

prefer buying a recommended stock when he expects a large return and

would sell it when the recommendation’s effect is exhausted.

39. Mohanty. B.K , (2008), in his article, “Market capitalization: A suitable

growth approach for share holders’ value creation”, before economic reforms

were initiated in 1991, companies in the Indian corporate sector had to

function amidst the license regime, quotas and restrictions, high taxes and

host of other rules and regulations. Companies are now allowed to borrow

from and invest abroad quite liberally. All this has done wonders for

corporate India. Over the past 15 years of reforms, corporate profits have

gone from Rs. 6440 crore in financial year 1991 to Rs.1,67,801 crore in

financial year 2006.

40. Henry L. Petersen and Harrie Vreden burg, (2009), in their article, “Morals

or Economics? Institutional Investor Preferences for Corporate Social

Responsibility”, this article presents the results of a study that analysed

whether social responsibility had any bearing on the decision making of

institutional investors. Being that institutional investors prefer socially

aligned organizations, this study explored to what extent the corporate

actions and/or social/environmental investments influenced their decisions.

Our results suggest that there are specific variables that affect the perceived

value of the organization, leading to decisions to not only invest, but whether

to hold or sell the shares, and therefore having a consequential impact on the

capital market’s valuation.

41. Sakthivel. N, (2010), in his paper, “EVA – MVA: Shareholders’ value

measure”, maximizing shareholders value is becoming the new corporate

standard in India. The corporate, who gave the lowest preference to the

shareholders’ inquisitiveness, are now bestowing the utmost inclination to it.

Shareholders’ value is measured in terms of the returns they receive on their

investment. The returns can either be in the form of dividends or in the form

of capital appreciation or both. For measuring the corporate financial

45

performance, there are accounting profitability measures and shareholders’

value based measures. Accounting profitability measures include ROI, ROE,

EPS, ROCE and DPS etc., Shareholders valued based measures include EVA

and MVA. EVA in Indian environment and relationship between EVA

(Economic Value Added) and MVA (Market Value Added).

2.5 Factors influencing investment evaluation and decision of investors.

42. Iran Peacock and Stuart Cooper, (2011), in their article, “Private equity:

implications for financial efficiency and Stability”, this article (1) describes

the current state of the UK private equity market. It also considers the extent