the retail (r)evolution – power to the customer

TRANSCRIPT

The Retail (R)evolution – Power to the customerThe fundamentals of the smart energy system

Customers are the essence of our business. Delivering the services they need and expect is our top priority. In this paper we set forward the industry’s vision of customers’ role in the changing electricity system and we analyse the type of market design, regulatory framework and empowering actions that will open up new opportunities for them.

The paper addresses consumer associations, policymakers and regulators across Europe.

It is divided in two sections:

First, we explain the changes affecting the power system as a whole and the resulting need for more flexibility. We then take a closer look at the downstream segment of the system (retail and distribution). A real flexibility and efficiency potential exists there and it is our belief that revolutionary changes are happening on that side of the system, making it possible to grasp this potential while creating new opportunities for customers: innovative products, new types of energy services and demand response programmes.

Second, we look at the framework needed to pave the way for this smart energy system. - The consumer framework identifies the kinds of actions needed to empower customers

to take part in the system and ensure they benefit from the new opportunities it offers.- The regulatory framework contains six clear recommendations for policymakers and regulators

looking to set the course for tomorrow’s smart energy system.

PART A WHY EUROPE NEEDS A SMARTER ENERGY SYSTEM

CHAPTER 1 GAME-CHANGER FLEXIBILITY: THE POWER SYSTEM IN TRANSITION 31.1 The power sector is in the midst of transformative changes 31.2 A more flexible system is necessary – and possible 5

CHAPTER 2 THE RETAIL REVOLUTION: READY FOR SMARTNESS? 92.1 A changing customer’s environment with new opportunities 92.2 The untapped flexibility potential? 14

PART B THE FUNDAMENTALS OF THE SMART ENERGY SYSTEM 14

CHAPTER 3 GETTING THE CUSTOMER ON BOARD 173.1 Awareness and Trust 183.2 Choice 22

CHAPTER 4 GETTING THE REGULATORY FRAMEWORK RIGHT 25Recommendation 1 – Show customers the value of becoming more active 26Recommendation 2 – Set up a secure, efficient and transparent framework for data exchange 27Recommendation 3 – Clearly separate competitive and regulated activities 28Recommendation 4 – Unblock market access for Demand Response 29Recommendation 5 – Incentivise smart grid investments 30Recommendation 6 – Set up supportive innovation policies 31

table of contents

1

part A

WHY EUROPE NEEDS A SMARTER ENERGY SYSTEM

GA

ME-

CH

AN

GER

FLE

XIB

ILIT

Y:

THE

PO

WER

SYS

TEM

IN

TR

AN

SIT

ION

3

1.1 The power sector is in the midst of transformative changes

The power sector is undergoing one of the most profound changes in its history. The liberalisation of the energy industry, together with the EU targets for decarbonisation and renewable energy sources (RES) as well as ground-breaking ICT developments have huge consequences on the way the sector works: we are moving rapidly towards a more decentralised, more sustainable, and smarter power system. These drivers also have significant effects on the system’s downstream side, covering retail and distribution. A new service model is emerging, based around energy efficiency offerings, smart grids, decentralised generation and, most importantly, new types of customers: more aware and demanding, more active and engaged.

chapter 1

GAME-CHANGER FLEXIBILITY: THE POWER SYSTEM IN TRANSITION G

AM

E-C

HA

NG

ER F

LEXI

BIL

ITY:

TH

E P

OW

ER S

YSTE

M I

N T

RA

NS

ITIO

N

4

GAME-CHANGER FLEXIBILITY: THE POWER SYSTEM IN TRANSITION

Customers today are using an ever larger number of electronic appliances, for reasons linked to comfort, entertainment, e-health, environment and security. This increase of appliances in and around the home combined with the progressive introduction of new loads such as heat pumps and electric vehicles is likely to cause electricity demand from households to rise. At the same time, new technologies such as micro-CHP and solar photovoltaic have made power generation at household level a real economic possibility. Customers with such installations no longer only consume energy, but produce electricity as well.

Change is also being driven by concerns about the high dependence on imported fossil fuels and climate change. The signing of the Kyoto Protocol, the European Energy and Climate package (the “20-20-20” targets), and the EU Emissions Trading Scheme (ETS) have brought about the large-scale development of electricity generation from variable renewable sources. This change is all-encompassing: it includes utility-scale projects like wind and solar parks as well as smaller scale, decentralised energy resources such as roof-mounted solar panels and micro combined heat and power systems (micro-CHP).

Advances in technology and telecommunications mean that customers across Europe are starting to take matters into their own hands: they are becoming more and more interested in value added products and services that match their shifting expectations in today’s more interactive, real-time, and on-demand world. Home energy management systems are developing; they will ultimately allow customers – directly or indirectly – to participate in the energy market. Electricity grids are also benefiting; they are turning into more intelligent and automated two-way streets with bi-directional communication and power flows.

The European power industry is being reshaped by four main drivers

The liberalisation of the European energy industry was first conceived in the 1990s as a way to encourage competition in the sector, thus providing customers with greater choice of services at lower prices. At the turn of the millennium, this project took shape with the ‘unbundling’ of utilities: a process whereby formerly integrated monopolistic utilities separate their generation and retail activities from their transmission and distribution activities. Market trends across Europe indicate that liberalisation is bearing fruit, with wholesale markets becoming more competitive and customers increasingly benefiting from new types of products and energy-related services 1.

1 Note, however, that regulated tariffs are still present in 18 EU Member States.

Increasing use of electrical appli-ances and local power generation

Concerns about security of supply and climate change

ICT developments

Increased competition

1

3

2

4

5

GAME-CHANGER FLEXIBILITY: THE POWER SYSTEM IN TRANSITION

GA

ME-

CH

AN

GER

FLE

XIB

ILIT

Y:

THE

PO

WER

SYS

TEM

IN

TR

AN

SIT

ION

1.2 A more flexible system is necessary – and possible

The aforementioned shifts in energy policy, technology, and customer focus bring new opportunities for customers and the industry. Customers will more and more benefit from new services, be able to save on their energy bill and potentially become electricity producers themselves. Companies will tailor and offer new types of products and services. But these developments also pose new challenges to the electricity industry, which has to cope with a higher share of variable and decentralised generation, while maintaining constant supply and fair prices for customers.

Operating the electricity system is becoming more challenging

Electricity differs from other energy products in that it cannot (yet) be stored in large quantities – at best it can be stored indirectly through e.g. the storage of fuel or water in a reservoir. Instead, at every point in time, the system must produce exactly the amount of electricity that is being consumed. This ‘balancing’ of the system was relatively straightforward in the traditional one-way system, in which electricity was produced by large power plants that ran steadily on gas, coal, nuclear or hydro, and in which demand was relatively easy to predict. Balancing is more challenging in a system that is shifting towards smaller, variable, less predictable and more dispersed renewable generation that cannot guarantee a predetermined amount of electricity at a certain point in time.

6

GAME-CHANGER FLEXIBILITY: THE POWER SYSTEM IN TRANSITION

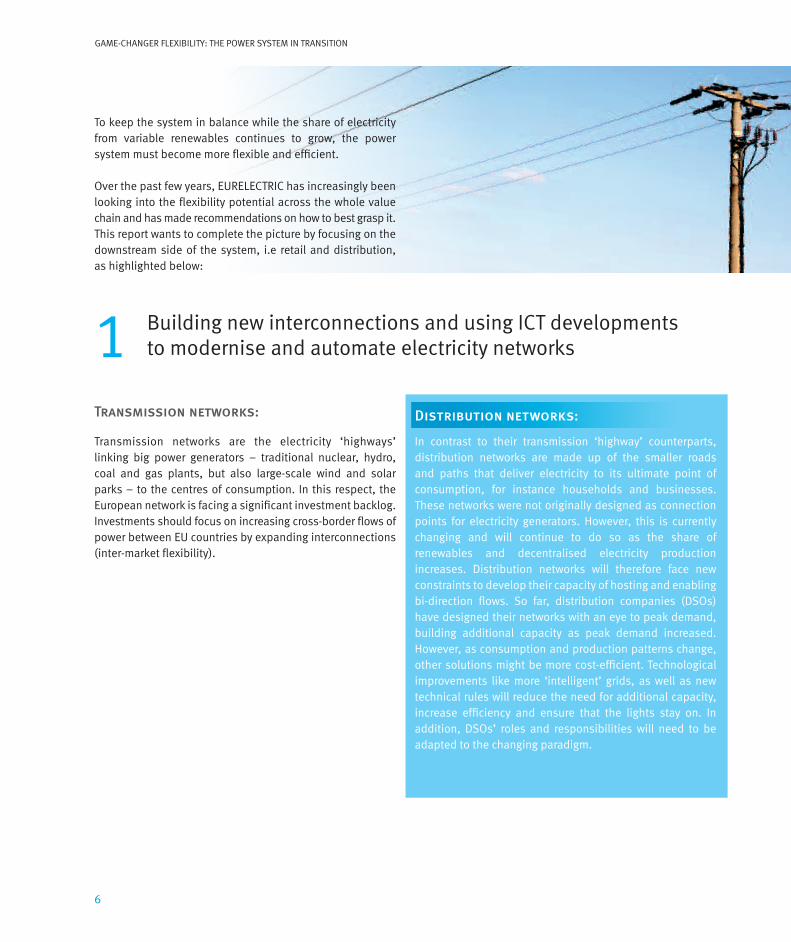

To keep the system in balance while the share of electricity from variable renewables continues to grow, the power system must become more flexible and efficient.

Over the past few years, EURELECTRIC has increasingly been looking into the flexibility potential across the whole value chain and has made recommendations on how to best grasp it. This report wants to complete the picture by focusing on the downstream side of the system, i.e retail and distribution, as highlighted below:

Distribution networks:

In contrast to their transmission ‘highway’ counterparts, distribution networks are made up of the smaller roads and paths that deliver electricity to its ultimate point of consumption, for instance households and businesses. These networks were not originally designed as connection points for electricity generators. However, this is currently changing and will continue to do so as the share of renewables and decentralised electricity production increases. Distribution networks will therefore face new constraints to develop their capacity of hosting and enabling bi-direction flows. So far, distribution companies (DSOs) have designed their networks with an eye to peak demand, building additional capacity as peak demand increased. However, as consumption and production patterns change, other solutions might be more cost-efficient. Technological improvements like more ‘intelligent’ grids, as well as new technical rules will reduce the need for additional capacity, increase efficiency and ensure that the lights stay on. In addition, DSOs’ roles and responsibilities will need to be adapted to the changing paradigm.

Transmission networks:

Transmission networks are the electricity ‘highways’ linking big power generators – traditional nuclear, hydro, coal and gas plants, but also large-scale wind and solar parks – to the centres of consumption. In this respect, the European network is facing a significant investment backlog. Investments should focus on increasing cross-border flows of power between EU countries by expanding interconnections (inter-market flexibility).

Building new interconnections and using ICT developments to modernise and automate electricity networks1

7

GAME-CHANGER FLEXIBILITY: THE POWER SYSTEM IN TRANSITION

GA

ME-

CH

AN

GER

FLE

XIB

ILIT

Y:

THE

PO

WER

SYS

TEM

IN

TR

AN

SIT

ION

heatlightingproduction

ict

labcontrol roomsupply chain

Market integration should be completed:

The EU is set to create an integrated European market by 2014. This requires additional interconnections between EU countries as well as EU-wide market rules allowing every player to benefit from the same conditions across Europe. This would improve competition and optimise cross-border flows.

Mature renewable technologies should be part of the market: Technologies like on- and off-shore wind and solar PV are ready to play a full role in the market. Such generators should be treated like any other generator, selling their production into the market and bearing the same obligations and responsibilities. In addition, convergence towards market-based support mechanisms for not yet mature renewables would expose such generators to market prices that reflect variations in demand and supply, thereby ensuring that the production becomes more cost-efficient and flexibility is more suitably priced.

Back-up generation needs a viable business case: Conventional generation has a crucial role to play as a flexible fall-back option when there is not enough wind or sun. However, the current situation is very challenging as many power plants have difficulties to cover their fixed costs while facing a future in which the increase of renewables means that they will be running even less.

Storage potential should be exploited to the full:

Storage is another flexible solution to reduce temporary mismatches between supply and demand. Today, the only economically viable large-scale storage option consists of vast water reservoirs used to produce hydropower. However, double grid fees and user charges are discouraging new investment and are even leading to the decommissioning of existing plants. We believe Europe’s hydropower potential can – and should – be further developed. Other types of (not yet mature) storage technologies should be supported via R&D funding.

Retail customers should be allowed to provide flexibility:

Another crucial source of flexibility could come from demand response (DR), by which customers react to price signals and financial incentives – either directly or indirectly by means of automation. Many large and energy-intensive industrial customers already use demand response services, for instance reducing their electricity consumption when prices are high. At household level, these services are still at a very early stage.

Improving market rules to allow generation, storage, and demand response to provide flexibility to the system2

8

GAME-CHANGER FLEXIBILITY: THE POWER SYSTEM IN TRANSITION

Customers will progressively move to the centre of the electricity system

9

THE

RET

AIL

REV

OLU

TIO

N:

REA

DY

FOR

SM

AR

TNES

S?

chapter 2

THE RETAIL REVOLUTION: READY FOR SMARTNESS?

2.1 A changing customer’s environment with new opportunities

Until very recently, the electricity retail business was simply about delivering electricity to people’s doorstep. In a world with regulated tariffs and without competition, retailers 2 had little incentive and room to innovate, while customers had no interest in becoming more active.

This situation is now changing rapidly. With the progressive liberalisation of the energy sector, retailers have started to offer more sophisticated services to household customers and businesses 3. In most EU member states, switching rates are increasing steadily.

2 For the sake of clarity and conciseness, in this paper, “retailer” means all market parties active in the retail business: supplier, service provider, aggregator etc.

3 Note, however, that regulated tariffs are still present in 18 EU Member States.

There are currently 32 energy retailers in the Netherlands that deliver electricity and/or gas to customers and small businesses. Many are so-called retail-only companies that were created after market liberalisation. They offer different contract forms: contracts for electricity and/or gas, contracts with fixed or variable prices, one-year contracts or contracts that are fixed for several years. A growing number offer contracts, which include solar PV and energy efficiency measures such as insulation, double-glazing, and condensing boilers. Some are also involved in application of high-efficiency cogeneration and/or efficient

district heating and cooling. There are also companies specialised in local collective projects for larger groups of customers (with e.g. the application of solar PV or wind). With the introduction of smart meters, many retailers have started to develop tools geared towards raising awareness and reducing consumption, for example smartphone apps, online tools and home displays. In 2012, 12.7% of all Dutch energy customers – both households and businesses – switched their electricity and/or gas retailer. This is the highest switching rate to date and roughly double the rate in 2004, the first year of liberalisation.

The retail market in the Netherlands today

THE

RET

AIL

REV

OLU

TIO

N:

REA

DY

FOR

SM

AR

TNES

S?

10

THE RETAIL REVOLUTION: READY FOR SMARTNESS?

The customer’s environment is also being shaped by other industries, in particular in the area of information and communication technologies. The number and variety of electronic appliances that customers purchase are increasing. Today it includes media devices (TV, computers, tablets, smartphones), heating systems (thermostats, air conditioning, heat pumps), white goods (washing and drying machines, dishwashers, ovens, refrigerators), and distributed energy resources (solar panels, batteries, electric vehicles). The drivers for this development usually lie outside the energy world, in areas of comfort, entertainment, as well as economic and environmental considerations.

As smart meters are installed across Europe in the coming years, an unprecedented amount of energy data will become available. For the first time, in-depth knowledge of actual consumption and understanding of the thermal behaviour of housing will all be achievable, meaning that retailers will be able to ‘tailor’ their offers to customers’ usage. Such innovative offers will deliver powerful messages to customers about the value of altering their electricity consumption – provided that market-reflective end-user prices are in place.

Customers willing to share their consumption data could, for example, benefit from tailored energy efficiency services,

Example of an existing DR progamme: Hot water management in France

Today in France, 8 out of 12 million electric boilers are controlled by a rippled signal that enables the boilers to be switched on or off according to off-peak/on-peak electricity prices, thereby optimising consumption while ensuring that customers continue to have the hot water they need. In this automated system, customers need not take any action, although they can always decide to override the system if they wish to do so.

house improvement or demand-response programmes. Crucially, they will be able to save money by using energy more efficiently and flexibly, and by producing, storing and selling electricity.

Demand response (DR) – in particular – will take many shapes and forms, depending on the preferences of the customer, the level of technology development, and the value of flexibility in the market. Examples of such offers include:

• Time-of-Use (ToU) contracts: higher ‘on-peak’ prices and lower ‘off-peak’ prices.

• Dynamic pricing: prices fluctuate to reflect changes in the wholesale prices and local network loading.

• Critical peak pricing: same rate structure as for ToU, but with much higher prices when supply is scarce or system reliability is compromised.

Retailers already propose different types of DR products, some requiring a more hands-on role for customers, for example adjusting consumption based on information received on their smartphone, others relying on some forms of automation. Many on-going pilot projects are testing new types of products to gather knowledge on customers’ actual interest and participation.

11

THE RETAIL REVOLUTION: READY FOR SMARTNESS?

THE

RET

AIL

REV

OLU

TIO

N:

REA

DY

FOR

SM

AR

TNES

S?

0:00 1:30 3:00 4:30 6:00 9:00 12:00 15:00 18:00 21:007:30 10:30 13:30 16:30 19:30 22:30

0,15

0,10

0,25

0,20

0,05

0

0,30

0,40

0,35

€/K

Wh

capacity tariffelectricity tarifftaxes

Example of a pilot project on dynamic pricing

In the summer of 2012, the Dutch DSO Enexis started three dynamic pricing pilot projects in cooperation with retailers GreenChoice and Dong Energy in order to investigate the potential ‘energy flexibility’ of household customers and the required cooperation between the market parties. One integrated kWh tariff is offered to customers, which varies every hour

based on the local network loading and the prices on the wholesale market. In addition customers receive information about the locally produced energy. In this pilot project, the tariffs are presented to customers by means of an in-home energy display. Every participating household has a smart appliance which is programmed on the basis of the supplied energy tariffs.

12

THE RETAIL REVOLUTION: READY FOR SMARTNESS?

In a more distant future and if the customer so wishes, the home itself could become the interface with the energy system (and other systems), optimising consumption and production by means of automated control of appliances according to individual preferences regarding comfort, lifestyle, scheduled actions, budget, expected savings, and prices.

All these developments produce a fundamental change to the currently known retail and distribution businesses, giving rise to a “smarter” system in which all dimensions interact much more with one another. Whilst “smart” is often used to describe all sorts of innovative technologies, products or processes, e.g. smart grids, smart meters, smart appliances, it should rather refer to the system as a whole.

Without entering into technical details, one could say that the smart energy system is intelligent, using analytics and automation to turn data into insights (and products) and to manage resources more efficiently. Crucially, it is steered by competitive markets and regulation that incentivise customers, retailers and DSOs to interact in a way that delivers optimal outcomes.

The home of the future: example of a new single house

Source: McKinsey Home of the Future Initiative.

Building fabrics• Roof and walls

insulation with aerogel

• Active windows• Double shell building

Appliances and electronics• Advanced

washing machines, refrigerators, freezer, etc.

• Television and other electronics

Smart applications• Home area network

Micro generation• Solar PV

Central systems• Electric heat pump• Nano technologies

(i.e., NanoAir and NanoFilters)

• Lighting

13

THE RETAIL REVOLUTION: READY FOR SMARTNESS?

THE

RET

AIL

REV

OLU

TIO

N:

REA

DY

FOR

SM

AR

TNES

S?

Conceptually, the smart energy system is made up of four building blocks with the following interaction stem

Electricity customers (households, SMEs and industry) – with or without their own local production (for example from solar PV) – can potentially make their flexibility available to the power system. They will manage and adjust their electricity consumption – directly or indirectly by means of automation – in response to real-time information, incentives and price signals.

The future distribution networks will have to be designed to meet a mix of variable generation and consumption. They should have the possibility to request and enable flexibility from distributed generation and load in order to optimise network availability in the most economic manner. DSOs will therefore play a fundamental role in developing and managing the infrastructure of the smart energy system: they will increasingly move beyond their traditional role of “building and connecting” towards “connecting and managing”.

Conventional generation and decentralised energy resources (including decentralised generation (DG) and storage) cover a wide range of resources which can benefit from making flexibility available to the power system.

An important feature of a smart energy system is its openness to new ideas and business propositions that will create value. Retailers and third party aggregators will be active in encouraging customers and small generators to offer flexibility by opening up interesting retail opportunities. They will aggregate individual flexibility in sufficiently large volumes for it to act on the wholesale/balancing/ancillary services markets and thus help keep the system balanced.

req

ues

tfl

exib

ilit

yh

and

lefl

exib

ilty

pro

vid

efl

exib

ilty

Network management

Generation

Markets

Consumption

14

THE RETAIL REVOLUTION: READY FOR SMARTNESS?

Such flexibility could be beneficial to the whole system, including customers themselves:

• On the one hand, customers would save money and lower their electricity bills, with no adverse impact on their comfort and electricity use.

• On the other hand, customers could help reduce grid congestion – by shifting demand to times when there is idle grid capacity – and generation costs – by shifting demand to times when there is more renewable power available 5. This flexibility would reduce or postpone investments in network and generation capacity, lowering the cost of keeping the system up and running.

They will, however, only be willing to deliver flexibility if they are convinced that the benefits (e.g. energy and financial savings, knowledge about one’s consumption, simplicity linked to automation, etc.) outweigh the costs (e.g. potential actions to be performed, potential loss of autonomy, cost of equipment, etc.).

In a system with more – and more diverse – electric appliances connected to the network, the potential sources of flexibility are increasing. This flexibility comes in many forms. Some appliances like batteries allow electricity to be stored, decoupling power consumption from the end-use. Others can help shift power consumption to different times without affecting the end-use, e.g. a dishwasher. And yet others, for example boilers, can reduce, interrupt or even increase power consumption instantly, if needed 4.

Moreover, as homes become smart, delivering standardised and interoperable connectivity, accessing this flexibility will become easier.

2.2 The untapped flexibility potential ?

4 See “Shift, not drift: Towards active demand-response and beyond”, THINK, June 2013.

5 Examples include water boilers that charge when the electricity price is lowest and renewable electricity is available, heat pumps that stop because a power line is overloaded, or electric vehicles that adapt their charging patterns to balance out fluctuating renewable power.

What is flexibility at household level?

Flexibility at household level is the ability of an appliance connected to the power system to change its consumption profile (time or level of consumption) through automation or direct action by the customer. Customers’ flexibility potential will depend on the appliances they have, but also on their lifestyle and, crucially, individual preferences.

15

THE RETAIL REVOLUTION: READY FOR SMARTNESS?

THE

RET

AIL

REV

OLU

TIO

N:

REA

DY

FOR

SM

AR

TNES

S?

Such flexibility will depend on the customer’s preferences and vary geographically and over time – according to local and regional circumstances. It will also compete with flexibility provided for instance by generation or storage. The market will determine the most cost-efficient way of providing flexibility at a given point in time.

While uncertainties about the exact potential remain, there is little doubt that demand response will eventually have a valuable role to play. Enabling changes to the regulatory framework can – and should – already be made today, allowing this flexibility potential to take off and its value to be exploited to the full.

Customers’ flexibility can be beneficial to the system, the customer and the retailer

Ulrich lives in Copenhagen and has just moved into a new house equipped with a heat pump which consumes 2,000 kWh of electricity a year at an annual cost of €600 – based on a retail price of €0.30/kWh including taxes. The heat pump allows him to maintain an indoor temperature which satisfies his comfort requirements, i.e. 20 -22°C during the day and 16- 18°C at night.

A retailer approaches Ulrich offering him both electricity supply and remote management of his heat pump, while guaranteeing a temperature within his comfort zone. Ulrich is happy as he now pays only €550 a year, thus saving €50.

Using controls and automation, the retailer switches off the heat pump for short periods of time when electricity prices are high, without the temperature in the house falling outside Ulrich’s comfort zone. In this

way, the cost of powering the heat pump is reduced by €50 a year. The retailer also switches the heat pump’s consumption, when it benefits the power system, earning a further €25 by selling these services to the market or to the system operator. Ulrich’s contract nevertheless gives him the option to control the device himself if needed.

The retailer has thus reduced the net cost of operating Ulrich’s heat pump to €525 a year. Ulrich saves €50, while the retailer receives €550 from him and earns an additional €25 a year by offering this flexibility to the market.

This fictitious example shows that the customer, the retailer and the system stand to gain from using the heat pump’s flexible electricity consumption.

part B

THE FUNDAMENTALS OF THE SMART ENERGY SYSTEM

17

GET

TIN

G T

HE

CU

STO

MER

ON

BO

AR

D

chapter 3

GETTING THE CUSTOMER ON BOARD

The transition to the smart energy system can only be achieved if it builds on trust and is supported by the broader public. This means that changes have to be explained to customers, so that they understand why changes are necessary, what they imply, how much they will cost and – above all – how to gain from them.

Customers are first and foremost looking for products that suit their needs and preferences at the lowest possible cost. Their support for the transition to the smart energy system will, in our view, depend on three main building blocks: increasing their (1) awareness and (2) trust so that they are willing – and able – to (3) make choices in a competitive environment.

Politicians, regulators, consumer groups and the energy industry each have a role to play in this process:

l The industry must work to enhance customers’ trust – in pre-sale areas like marketing and contracting and in post-sale operations like customer care, billing, and dispute resolution – and to design offers that respond to customers’ needs.

l EU and national authorities are responsible for setting the right regulatory framework and effectively transposing existing legislation 6.

l Member states, national regulatory authorities (NRAs), businesses and consumer associations have a shared responsibility to inform and educate consumers in order to improve their understanding and engagement in retail energy markets.

AwArenessof the opportunities offered by the market, of switching possibilities,

of their own consumption and preferences

TrusTin the market actors

and processes (switching, billing, etc.)

ChoiCeof different products

and services

6 This includes the Third Energy Package, the Energy Efficiency Directive (EED), the Consumer Rights Directive (CRD) and the Alternative Dispute Resolution (ADR) Directive.

GET

TIN

G T

HE

CU

STO

MER

ON

BO

AR

D

18

GETTING THE CUSTOMER ON BOARD

and will continue to guide the actions and commitments of our members when engaging with customers. Whilst the industry can certainly do more 7, a lot will also depend on a better regulatory framework, starting with the correct implementation of existing legislation.

In the table below we summarise our views on the RASP principles and the type of regulatory actions needed from EU and national authorities to help the industry translate those principles into reality.

At the 5th Citizens’ Energy Forum (November 2012), European energy regulators CEER and European consumer organisation BEUC presented their 2020 vision for Europe’s energy customers. This vision is based on the four so-called RASP principles: Reliability, Affordability, Simplicity and Protection & Empowerment.

EURELECTRIC endorses this vision: we believe that the RASP principles are essential to create awareness and increase trust. This is why these principles have guided

RELIABILITY

3.1 AwAreness TrusT

7 Examples of national and EU-level actions that EURELECTRIC and its members are taking in this regard are detailed in the EURELECTRIC paper “Translating the BEUC/CEER 2020 Vision for Europe’s energy customers into reality” (December 2013).

what we believe what we need

Customers should be able to rely on:

- their energy contract, - the information on offers and conditions they receive

from retailers,- the different market processes (switching, billing,

moving, etc.) and services they are offered.

Member States should fully implement existing EU legislation, e.g. switching within 3 weeks (3rd Energy package), billing on actual consumption (Energy Efficiency Directive).

l

19

GETTING THE CUSTOMER ON BOARD

GET

TIN

G T

HE

CU

STO

MER

ON

BO

AR

D

what we believe what we need

Customers should be able to benefit from:

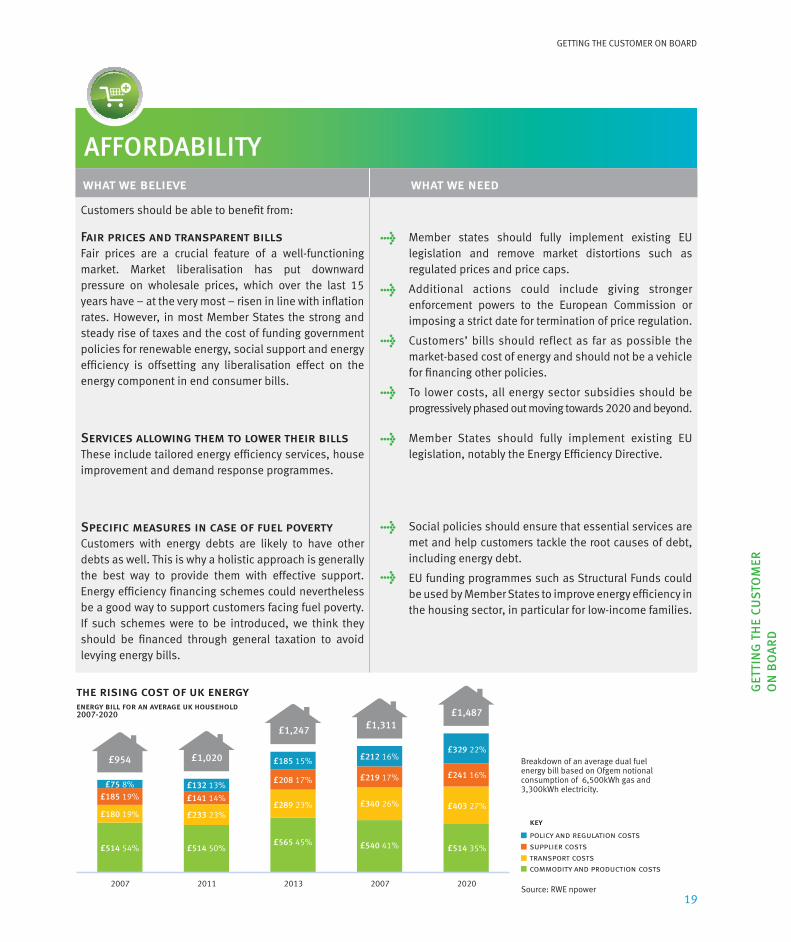

Fair prices and transparent billsFair prices are a crucial feature of a well-functioning market. Market liberalisation has put downward pressure on wholesale prices, which over the last 15 years have – at the very most – risen in line with inflation rates. However, in most Member States the strong and steady rise of taxes and the cost of funding government policies for renewable energy, social support and energy efficiency is offsetting any liberalisation effect on the energy component in end consumer bills.

Services allowing them to lower their bills These include tailored energy efficiency services, house improvement and demand response programmes.

Specific measures in case of fuel povertyCustomers with energy debts are likely to have other debts as well. This is why a holistic approach is generally the best way to provide them with effective support.Energy efficiency financing schemes could nevertheless be a good way to support customers facing fuel poverty. If such schemes were to be introduced, we think they should be financed through general taxation to avoid levying energy bills.

Member states should fully implement existing EU legislation and remove market distortions such as regulated prices and price caps.

Additional actions could include giving stronger enforcement powers to the European Commission or imposing a strict date for termination of price regulation.

Customers’ bills should reflect as far as possible the market-based cost of energy and should not be a vehicle for financing other policies.

To lower costs, all energy sector subsidies should be progressively phased out moving towards 2020 and beyond.

Member States should fully implement existing EU legislation, notably the Energy Efficiency Directive.

Social policies should ensure that essential services are met and help customers tackle the root causes of debt, including energy debt.

EU funding programmes such as Structural Funds could be used by Member States to improve energy efficiency in the housing sector, in particular for low-income families.

AFFORDABILITY

2007 2011 2013 2007 2020

supplier coststransport costs

policy and regulation costs

key

commodity and production costs

£75 8%£185 19%

£180 19%

£514 54%

£132 13%

£141 14%

£233 23%

£514 50%

£185 15%

£208 17%

£289 23%

£565 45%

£212 16%

£219 17%

£340 26%

£540 41%

£329 22%

£241 16%

£403 27%

£514 35%

£954 £1,020

£1,247 £1,311£1,487

the rising cost of uk energyenergy bill for an average uk household2007-2020

Breakdown of an average dual fuel energy bill based on Ofgem notional consumption of 6,500kWh gas and3,300kWh electricity.

Source: RWE npower

l

l

l

l

l

l

l

20

GETTING THE CUSTOMER ON BOARD

SIMPLICITYwhat we believe what we need

It is up to market parties to translate the complexity of the market into the simplicity that customers want by ‘packaging’ attractive products.

Customers should have easy access to the information necessary to compare offers and make informed choices.

There are many ways to help customers choose the products best suited to their needs without hampering marketing innovation:• Quality guaranteed price comparison tools can

assist customers in navigating the retail market and comparing the characteristics of energy products.

• Retailers can offer personalised advice to their customers, e.g. which is the cheapest and most appropriate tariff considering their consumption profile and preferences.

Simplicity is best guaranteed if the retailer remains the main point of contact for customers. This is even more relevant in demand response markets with smart meters because of the increased amount of data exchanged.

Simplicity is also linked to better regulation. Overwhelming customers with information is not always helpful. Instead, the focus should be on providing them with meaningful data.

l

l

l

l

The accuracy and objectivity of price comparison tools should be certified, e.g. with a ‘trust mark’ from the energy regulator or an independent and competent consumer organisation.

Some form of standardisation, e.g. in the terminology used, may be necessary to allow for accurate comparison of offers.

Make retailers the main point of contact for customers to simplify their retail market experience.

Policymakers and stakeholders – through consultation processes – should assess the impact of current national legislative provisions and requirements regulating the presentation of offers and bills to strike a balance between simplicity and comprehensiveness.

21

GETTING THE CUSTOMER ON BOARD

GET

TIN

G T

HE

CU

STO

MER

ON

BO

AR

D

PROTECTION AND EMPOWERMENT

Money Saving Expert is the UK’s biggest consumer website with over 13 million users a month and seven million recipients of the weekly email. The Cheap Energy Club is a service that aims to alert customers when cheaper energy deals become available, or when it is time to switch away from a tariff that is ending.

This service takes into account exit fees and other key tariff information, providing personalised calculations. The data supporting these is kept in a personal data store provided by all filed. Almost 300,000 users have signed up to the club in a short space of time.

Customer empowerment in practice: Money Saving Expert – Cheap Energy Club

what we believe what we need

Customer protection is more necessary than ever, given the ageing population, increasing technological and income gaps in society, and the economic crisis. To avoid being counterproductive, such protection must be targeted.

Customers can be considered “vulnerable” for different reasons (financial, health, etc.) and need different strategies to cope with their vulnerability. Member States should provide market neutral support.

Protection from unfair commercial practices is as important for energy as it is for all other retail markets. Customers should have the means to resolve any queries, such as easy access to their supplier’s customer service and independent third party complaint resolution bodies (ADR).

Data security and privacy should be guaranteed. Customers should always give their agreement before their data is made available to a third party other than their retailer and DSO.

l

l

Member States should fully implement existing EU legislation, such as the Third package (e.g. Member States have to define the concept of “vulnerable customers”), the Alternative Dispute Resolution Directive and the Consumer Rights Directive (CRD).

The definition of vulnerable customers used by Member States should properly identify those, and only those, in real need of assistance with respect to their energy needs.

22

GETTING THE CUSTOMER ON BOARD

I value convenience and efficiency

14% 13%

18%

22%15%

18%

Methodology note: Results based on a conjoint analysis.Base: All respondents.Source: Revealing the Values of the New Energy Consumer, Accenture, 2011, www.accenture.com

I prefer to manage myelectricityconsumptionon my own

I like testing newtechnologies

I prefer a familiar experience

I want the best service for me and my family

I look aboveall for thebest financialrewards

Ser

vice

-cen

tric

s

Te

ch-savvys Self-reliants Social-independents Traditionalists Cost-sensitives

Awareness and trust are two essential steps to empower customers. However, without choice they will not be better off.

As some recent studies demonstrate 8, customers have different energy needs and there is no single measure that will make them all more aware of their flexibility and savings potential.

While some customers will be looking for the simplest products, others will seek to reduce their environmental impact, pursue energy efficiency measures, or even install their own distributed generation units. This reflects a broader trend of customers becoming accustomed to a wider variety of choices in other traditionally “passive” services: in telecommunications, internet, banking and the like, customers are no longer content to be positioned exclusively at the receiving end. Many want to have more options and influence on how the companies that provide those services operate. It is only natural, then, to see some customers extending this behaviour into an area as fundamental as energy.

This is why it is crucial to ensure that customers can freely choose from a range of products, services and contract types designed by competing retail companies. They should be able to base their choices not only on price and brand, but

8 “Actionable Insights for the New Energy Consumer”, Accenture end-consumer observatory 2012; “Shift, Not Drift: Towards Active Demand Response and Beyond”, THINK, June 2013.

9 Accenture’s global survey is based on questionnaire-led interviews with 10,158 residential end consumers in 19 countries (among which 10 European countries), conducted online in native languages in December 2011 for Accenture by Harris Interactive. The selected countries represent a range of regulated and deregulated markets. For countries with large and/or diverse populations, participants were selected from a broad spectrum of locations.

also on features such as billing type and frequency, contract duration (price insurance), terms of payment, service level, granularity of information, and type of generation fuel mix (green or grey).

Choice enhances engagement and competition, putting downward pressure on prices and upward pressure on service standards. The challenge for retailers and policymakers is to ensure that those choices are explained as simply as possible, whilst ensuring that customers are not misled.

Customers have increasingly different values and preferences 9

Source: Accenture 2011

3.2 ChoiCe

23

GETTING THE CUSTOMER ON BOARD

GET

TIN

G T

HE

CU

STO

MER

ON

BO

AR

D

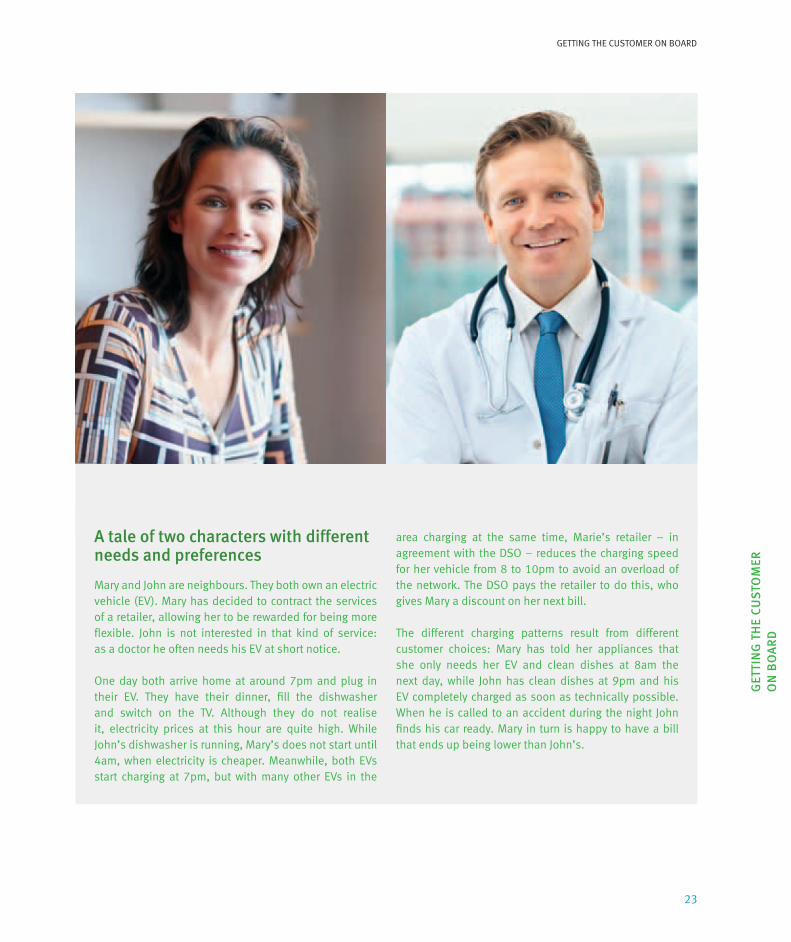

A tale of two characters with different needs and preferences

Mary and John are neighbours. They both own an electric vehicle (EV). Mary has decided to contract the services of a retailer, allowing her to be rewarded for being more flexible. John is not interested in that kind of service: as a doctor he often needs his EV at short notice.

One day both arrive home at around 7pm and plug in their EV. They have their dinner, fill the dishwasher and switch on the TV. Although they do not realise it, electricity prices at this hour are quite high. While John’s dishwasher is running, Mary’s does not start until 4am, when electricity is cheaper. Meanwhile, both EVs start charging at 7pm, but with many other EVs in the

area charging at the same time, Marie’s retailer – in agreement with the DSO – reduces the charging speed for her vehicle from 8 to 10pm to avoid an overload of the network. The DSO pays the retailer to do this, who gives Mary a discount on her next bill.

The different charging patterns result from different customer choices: Mary has told her appliances that she only needs her EV and clean dishes at 8am the next day, while John has clean dishes at 9pm and his EV completely charged as soon as technically possible. When he is called to an accident during the night John finds his car ready. Mary in turn is happy to have a bill that ends up being lower than John’s.

24

GETTING THE CUSTOMER ON BOARD

As technologies evolve so too defining, understanding and serving energy customers. In fact, for retailers, traditional household segmentation may no longer be valuable. They will have to consider overlapping customer types that require differing levels of sophistication to understand and engage. Smart meters will allow customers to share detailed consumption data with their energy retailer who will be able to build improved energy profiles to support more specific energy savings advice.

The insights from more sophisticated, data-driven analysis of customer behaviour, demographics and expressed interests will also enable retailers to customise packages and programmes. As they start to offer a wider variety of offers, it will be critically important to develop expertise in test marketing and running pilot projects. Fine-tuning such capabilities will help retailers more accurately gauge customer interest levels, develop the right packages, and spot emerging trends.

Retailers must consider overlapping customer types

Bill payerConsumers who pay for energy usage.

Premise occupantEnergy-consuming occupant of a specific premise.

ProsumerEnergy consumers who both purchase and supply energy.

Roaming consumerConsumers that roam within and outside of the energy provider’s service area.

Community consumerGroups of consumers who have joined together to manage, purchase and/or generate energy within their own communities.

Source: Accenture 2011

25

GET

TIN

G T

HE

REG

ULA

TOR

Y FR

AM

EWO

RK

RIG

HT

Society expects utilities to pave the way and finance the transition towards the smart energy system. However, the needed investments and innovative solutions will only occur if an appropriate regulatory framework is in place. Such a framework should strike a fine balance between stability and flexibility:

- On the one hand, it should be stable and transparent, both in the regulated (distribution) and in the competitive (retail) part of the electricity business. Predictable rules – and changes to those rules – will spur investment and attract innovative financing models.

- On the other hand, it should retain enough flexibility to apply to different national contexts and adapt to

changing circumstances over time. The right ‘level of smartness’ for an electricity system will depend, among other things, on the state and structure of the national grid, the share of variable renewables, electric vehicles and storage in the system, and customer preferences. A one-size-fits-all model would not be appropriate.

The framework should be aligned with the existing EU targets while reflecting the individual needs of each country. It should be developed in discussion between relevant stakeholders and the national authorities.

This chapter sets out recommendations in six areas where we believe decisive action by national and European policymakers and regulators should be taken.

chapter 4

GETTING THE REGULATORY FRAMEWORK RIGHT

GET

TIN

G T

HE

REG

ULA

TOR

Y FR

AM

EWO

RK

RIG

HT

EURELECTRIC’s customer vision builds on

supported by the right regulatory framework

AwAreness TrusT ChoiCe

1Show customers the value of becoming more active

2Set up a secure, efficient and transparent framework for data exchange

3Clearly separate competitive and regulated activities

4Unblock market access for Demand Response

5Incentivise smart grid investments by DSOs

6Set up supportive innovation policies

26

Recommendation 1

Encouraging customers to provide flexibility to the energy system is only possible if they receive clear financial signals that lead them to become more active in energy retail markets. This requires the following:

Ensure that electricity markets function properlyMember states must stop discretionary intervention in retail electricity pricing. Blanket price regulation prevents customers from seeing the value of becoming more active. It should be phased out as a matter of urgency 10. In addition, even in countries without blanket price regulation, a large part of household electricity bills is regulated (taxes, charges). This part of the bill remains unaffected by changes in wholesale prices. The larger it is, the lower the signalling effect for customers, reducing the likelihood that customers’ flexibility potential will be used.

Allow distribution tariffs to be cost-reflectiveand avoid cross-subsidisation and free-ridingNetwork tariffs should be more capacity based. Such a tariff structure would encourage more efficient use of the network capacity and avoid cross-subsidisation.

Send one unambiguous signal to customersSensible regulation should allow market parties to send unambiguous price signals to customers. Retailers will translate the complexity and sophistication of a well-functioning market into the simplicity that customers demand, by packaging attractive products. Successful retailers will offer products that are easy for the customer to understand and that effectively reduce any complexity in costs (wholesale prices and variable network tariffs). As situations might arise in which the interests of retailers to use load flexibility for supply portfolio management will be in direct conflict with the need of DSOs to maintain local grid stability, a new set of contractual agreements will be needed between the different market players.

Make the customer bill simple and transparentDepending on customers’ needs, retailers should be allowed to provide them with a bill that differentiates between the energy, network and tax components (including support schemes). Customers should also have easy access to disaggregated billing information, e.g. when demand response is bundled with other service offers. However, there is a trade-off between accuracy and simplicity. The ultimate aim is to ensure that customers understand the bill they receive. It should be up to customers and retailers to agree on the level of information contained in the bill, bearing in mind that information can also be communicated by other means (e.g. internet).

Show customers the value of becoming more active

10 Special measures could be considered for vulnerable customers, depending on the national situation.

Further information is available in the following EURELECTRIC reports:

“Network tariff structure for a smart energy system”, May 2013

“Active Distribution System Management, A key tool for the smooth integration of distributed generation”, February 2013

“Customer Centric Retail Markets: A Future-proof market design”, September 2011

“EURELECTRIC views on Demand-Side Participation”, August 2011

27

Recommendation 2

GET

TIN

G T

HE

REG

ULA

TOR

Y FR

AM

EWO

RK

RIG

HT

Data exchange is indispensable for the proper functioning of the smart energy system and will be a key means of creating new value. Without appropriate data, neither DSOs nor retailers will be able to perform their tasks. DSOs need technical data to operate the distribution system safely and efficiently, and to expand it as necessary. Retailers need consumption data in order to hold their energy portfolio in balance and “package” innovative products and services based on customer preferences.

However, most customers will only be comfortable sharing their data if they are confident that these are stored securely in a way that safeguards their privacy. Any framework for data exchange between customers, retailers and DSOs must take these concerns into account. EURELECTRIC believes that customers should always explicitly give their consent before their data are made available to third parties and should be informed for what purpose the data are used.

In general, we think DSOs - as regulated, neutral entities – are best-placed to ensure effective customer data protection. In most EU Member States, DSOs already collect metering data from customers. Decoupling the collection of such data from

processes carried out by market parties (e.g. contracting, billing) creates a level playing field on which all market players can compete, while customers can be sure that data is only passed on with their consent. At the same time, data handling should not be unnecessarily costly. Setting up additional data-handling entities would raise costs, create redundancies and increase the potential for communication errors. A decentralised or centralised DSO-run data hub 11

which handles all data related to DSO assets and connection points could be more efficient.

Finally, the creation of a smart energy system will only be possible if actors from different sectors – be it energy, ICT, telecoms, transport, or building and facility management – find new ways of cooperating. Such cross-sectorial cooperation is needed to develop the standards, processes and protocols missing today, and without which creating a truly cost-efficient and competitive environment is not really possible.

11 For countries where the DSO is not the owner of the meter, e.g. the UK, the data handling model could be different.

Standardisation makes economic sense

Standards for information exchange are an efficient means of integrating the different players and components that make up the smart energy system. They are also a good way to reduce costs, by e.g. allowing retailers to monitor and remotely control – with the agreement of the customer – appliances, solar panels, electric cars and other distributed energy resources in a standardised way. Standardised information exchange also reduces the cost of switching retailers, improving competition in the market.

This implies a certain level of standardised messages, both within the home and between the energy system

and the home. Divergent industrial or national initiatives in this field could hamper the take-off of smart appliances. A common European approach, i.e. a clearance of nationwide existing ‘smart grid’ projects, is preferable.

Standards for smart grids are being set at EU level, but gaps nevertheless remain. Work on issues such as interoperability and demand response should be stepped up. Closed technological standards that hamper innovation should be avoided in favour of data interfaces that allow interoperability of different systems.

Further information is available in the following EURELECTRIC reports:

“Communicating smart meters to customers – which role for DSOs?”, June 2013

“The role of Distribution System Operators (DSOs) as Information Hubs”, June 2010

Set up a secure, efficient and transparent framework for data exchange

28

The role of energy retailersInnovative products will become a strategic tool for market players to differentiate themselves from their competitors. The business case for new products will depend on the existence of a level playing field, with fair market conditions and accessibility for all market participants. This can be achieved through:

- The existence of a liberalised energy market. Customers must be able to choose between several retailers and different products per retailer. Barriers for retailers to enter new markets should be low, for instance through interoperable data and similar supply licences across the EU.

- The legal framework has to ensure competition. The market should not be distorted by interventions such as price regulation or poorly designed and ineffective renewable energy support schemes.

- Adequate rules and supervision mechanisms should exist in order to guarantee an effective separation (unbundling) of market players’ retail businesses on the one hand and the regulated infrastructure (grid) on the other.

Reliable electricity supply should always come first. As the roles and responsibilities of entities evolve, negative impacts on security of supply or quality of service must be avoided.

Like today’s energy system, the smart energy system will be composed of regulated entities (DSOs) and commercial players (e.g. suppliers, ESCOs, aggregators, etc.). A well-functioning division of work between both types of players, as well as well-functioning interactions between market players should be ensured.

The regulatory framework should draw a clear distinction between the roles of competitive and regulated players. In a smart energy system, retailers will ‘package’ innovative products based on customers’ preferences. DSOs, in turn, will act as ‘neutral market facilitators’ by providing retailers with the necessary data in a timely and non-discriminatory manner.

The role of DSOsProper implementation of EU legislation, in particular the Second and Third Energy Packages, is key for DSOs to take up their role of neutral market facilitators and become active system managers. For instance, DSOs could procure flexibility from distributed energy sources – either directly or via retailers. This would allow them to plan or operate their grids more efficiently, while ensuring transparent and non-discriminatory connection and access to the network.

Clearly separate competitive and regulated activities

Recommendation 3

Further information is available in the following EURELECTRIC reports:

“Customer Centric Retail Markets: A Future-proof market design”, September 2011

“EURELECTRIC views on Demand-Side Participation”, August 2011

29

GET

TIN

G T

HE

REG

ULA

TOR

Y FR

AM

EWO

RK

RIG

HT

Customers will only take up a more pro-active role in the smart energy system if the gains they stand to make are worth the effort of becoming more involved. While large industrial customers can directly offer their balancing services in the market, smaller customers will participate through their retailers or third parties that aggregate demand response from many customers.

Much of this development will depend on innovation in the commercial segment. However, some market and network rules, like rules on balancing, will need to be adjusted so that demand response can offer flexibility on the market. Such rules should be non-discriminatory, granting equal market access to demand response and traditional sources of flexibility like generation. Unblocking market access in this way will make it technically and legally possible for large industrial customers and aggregators of commercial, industrial and residential loads to participate in energy markets.

Unblocking market access for demand response requires the following regulatory changes:

1. Proper national transposition of the 3rd Electricity Directive and the Energy Efficiency Directive, to overcome the absence of clear technical modalities for demand response access and participation in the market.

2. The network codes, particularly on Demand Connection, Balancing and System Operation should pave the way for demand response. They should set rules that allow all flexibility providers to compete on a level playing field.- Rules for day-ahead, intraday, reserves and other

ancillary services markets should be adapted, where necessary, to demand response requirements. Similarly,

the rules regarding bid sizes, reaction times, ramp-rates, metering and verification should be adjusted so that demand response potential can be fully exploited. This will require TSOs and regulators to redefine which services they require to operate the system, and possibly add new services that better fit the characteristics of demand response.

- The balancing responsibility should be clearly defined and consistently metered. At minimum, the balance responsible party (BRP) should always be informed ex-ante of third party aggregators’ (i.e. aggregators who are not the retailer of the customer) actions and a consistent way of handling the impact of these actions – including compensation – on the BRP has to be found.

3. The flexibility from demand response (and other sources) is not only useful for the market and for the transmission system operators (TSOs), but could also help DSOs to manage the distribution networks. Any framework regulating demand response for TSOs should therefore take care not to hinder the development of flexibility services for DSOs, for instance by creating extra costs (e.g. duplication of communication channels).

4. Technical interfaces of electrical and thermal equipment (e.g. heating control systems, hot water production units, storage systems, e-mobility, cooling systems, dishwashers etc.) should be opened to allow them to participate in demand response programmes.

Unblock market access for Demand Response

Recommendation 4

Further information is available in the following EURELECTRIC report:

“Active Distribution System Management, A key tool for the smooth integration of distributed generation”, February 2013

30

Distribution grids represent the backbone of the future smart energy system. Services and products in the competitive segment of the system, e.g. home automation, small distributed generation, aggregation services, and smart appliances, will only develop to their full potential if the distribution grid can integrate them. Ensuring a supportive regulatory framework for the distribution business is therefore a prerequisite for the emergence of a healthy and vibrant smart energy system.

Yet in most member states, the current network regulation does not properly reward DSOs for investing in more intelligent grids. Instead regulation is often focused solely on cost reduction – an approach unsuited to an environment in which networks need to adapt to a new role. An adequate regulatory framework will need to allow both cost-effective investments in distribution networks and proper risk allocation. Regulation focusing on short-term cost reduction only may not be compatible with innovation. It must be adapted to reward DSOs for adopting the most sustainable solutions in the long run, be they conventional investment or innovative active system management solutions.

In order to promote smart grid investments, regulation should include all of the following characteristics:

• National regulators will have to find the right balance between two main concerns: containing network costs and enabling smart grid investments. To this end they should include smart grid investments in the regulatory asset base and ensure a fair rate of return for DSOs.

• Network investments have a long technical and economic lifetime. Regulatory risk is one of the strongest deterrents to such capital-intensive investments. Regulators should therefore ensure long-term regulatory stability and visibility. At the same time regulatory incentives schemes and benchmarking techniques should be clear, simple and not leave room for interpretation. This will help grid companies to develop a solid business case.

• Regulation should remain technology-neutral: regulators should not attempt to “pick winners”, i.e. to choose or promote specific smart grid technologies and configurations. This should give grid companies the freedom to develop more cost-ef f icient and innovative grid solutions.

incentivise smart grid investments

Recommendation 5

Further information is available in the following EURELECTRIC reports:

“Active Distribution System Management – A key tool for the smooth integration of distributed generation”, February 2013

“10 steps to smart grids”, May 2011

“Regulation for smart grids”, February 2011

31

GET

TIN

G T

HE

REG

ULA

TOR

Y FR

AM

EWO

RK

RIG

HT

Innovation will be key in developing the smart energy system and satisfying the diverse needs and preferences of European customers.

Regulation should not become a stumbling block to innovation by prescribing business models, removing incentives for R&D, or hampering the creation of new products and services. Instead, the political framework should enable competition and entrepreneurship among market and network players, leading to innovation in new business models, products, and processes.

Stable and coherent regulation will enable long-term planning and investment. Moreover, properly designed market-based mechanisms are essential to support mass deployment of near-commercial technologies.

The development of the smart energy system will also depend on how the power sector links its businesses to other sectors – notably transport and information and communication technologies (ICT). Continued development of individual (grid or generation) technologies must be synchronised across sectors, technologies and business models.

The European Commission’s proposed programme for research and innovation, Horizon 2020, still contains elements of a silo approach with, for example separate budgets for ICT, transport, climate and energy. This reflects the structure of the current Strategic Energy Technologies (SET) Plan, which is set up along individual technology platforms. The Commission’s work to develop an Integrated Roadmap for the SET Plan is a good starting point for a new systems approach: we support the initiative to bring new stakeholders, including network operators, into the various structures and platforms related to energy innovation.

Finally, stronger focus should be placed in supporting the final ‘innovation mile’, i.e. the part of the innovation process that is closest to the market. This will ensure that the smart energy system leaves the drawing board and becomes reality – to the benefit of power companies and customers alike.

Recommendation 6

set up supportive innovation policies

Further information is available in the following EURELECTRIC report:

“Utilities: Powerhouses of Innovation”, May 2013

TF Market Model for a Smart Energy System:

Ulrik STRIDBAEK (DK) ChairOlivier CHATILLON (FR); Paul DE WIT (NL); Oliver FRANZ (DE); Oliver GUENTHER (DE); Wolfram HERPPICH (DE); Jean-Paul KRIVINE (FR); Riccardo LAMA (IT); Pauline LAWSON (GB); Wlodzimierz LEWANDOWSKI (PL); Sandra MAEDING (DE); Joao MARTINS DE CARVALHO (PT); Rosie MCGLYNN (GB); Ulf MOLLER (NO); Elsa NOVO (ES); Petter SANDOY (NO); Ville SIHVOLA (FI); Herwig STRUBER (AT); Jorge TELLO GUIJARRO (ES); Donald VANBEVEREN (BE); Elliott WAGSCHAL (NL).

Contact:

Sébastien DOLIGÉ, Advisor Markets/Retail Unit – [email protected] NOYENS, Advisor DSO Unit – [email protected]

EURELECTRIC pursues in all its activities the application of the following sustainable development values:

Economic Development Growth, added-value, efficiency

Environmental Leadership Commitment, innovation, pro-activeness

Social Responsibility Transparency, ethics, accountability

The Union of the Electricity Industry – EURELECTRIC is the sector association representing the common interests of the electricity industry at pan-European level, plus its affiliates and associates on several other continents.

In line with its mission, EURELECTRIC seeks to contribute to the competitiveness of the electricity industry, to provide effective representation for the industry in public affairs, and to promote the role of electricity both in the advancement of society and in helping provide solutions to the challenges of sustainable development.

EURELECTRIC’s formal opinions, policy positions and reports are formulated in Working Groups, composed of experts from the electricity industry, supervised by five Committees. This “structure of expertise” ensures that EURELECTRIC’s published documents are based on high-quality input with up-to-date information.

For further information on EURELECTRIC activities, visit our website, which provides general information on the association and on policy issues relevant to the electricity industry; latest news of our activities; EURELECTRIC positions and statements; a publications catalogue listing EURELECTRIC reports; and information on our events and conferences.

Union of the Electricity Industry - EURELECTRIC

Boulevard de l’Impératrice, 66 boîte 21000 BrusselsBelgiumT.: + 32 (0)2 515 10 00F.: + 32 (0)2 515 10 10website: www.eurelectric.org twitter.com/EURELECTRIC D

esig

n by

ww

w.g

ener

is.b

e /

© p

hoto

s: iS

tock

, Dre

amst

ime,

Shu

tter

stoc

k

D2013/12 .105/48