the rise of china presented to financial executives international orange county chapter may 9, 2007

TRANSCRIPT

THE RISE OF CHINA

Presented to Financial Executives International

Orange County Chapter

May 9, 2007

TOPICS

INTRODUCTION POLITICAL SITUATION ECONOMIC CONDITION FINANCIAL ENVIRONMENT CONCLUSION

INTRODUCTION

“It now appears that global stock market corrections are made in China.”

Stephen Roach of Morgan Stanley

GLOBAL ECONOMY

Revolutionize the relative prices of labor, capital, goods and assets

Oil price high, yet no inflation Manufactured low-priced goods Lid on wages Excess liquidity – low interest rates – high

asset prices Bond yields low

POLITICAL LEADERS

1949: Chinese Communist Party 1st generation: Mao Zedong 2nd generation: Deng Xiaoping (1978-97) 3rd generation: Jiang Zemin 4th generation: Hu Jintao (March 2003)

DENG XIAOPING

1978-1997 Policy of “Socialism with Chinese

Characteristics” Economic openness and foreign trade Iron grip on politics 1989: Tiananmen Incident

JIANG ZEMIN

Prime Minister: Zhu Rongzhi Role of capitalism 1992: FDI exploded July 1997: Hong Kong turnover 2001: WTO membership

Open to more foreign investment and tradeIncrease the pace of privatization – only a third is under

state controlled Global economic force - Double its share of global

manufacturing output

HU JINTAO

Nov 2002: Hu Jintao was named Prime Minister: Wen Jiabao Steps toward financial transparency 2008: Olympic games 2010: Shanghai World Trade

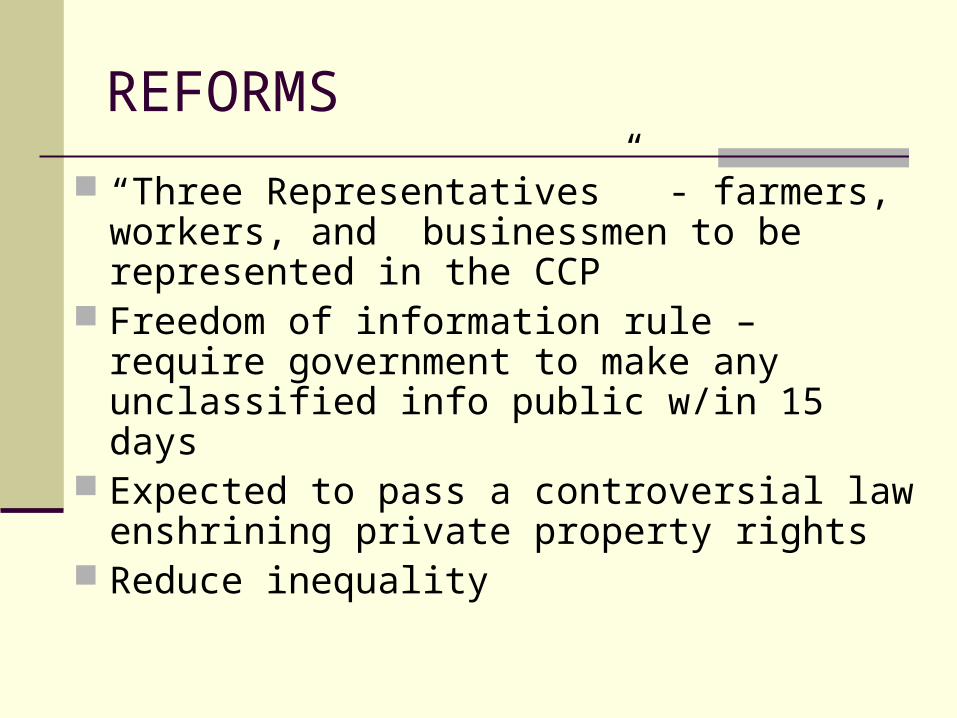

REFORMS

“Three Representatives” - farmers, workers, and businessmen to be represented in the CCP

Freedom of information rule – require government to make any unclassified info public w/in 15 days

Expected to pass a controversial law enshrining private property rights

Reduce inequality

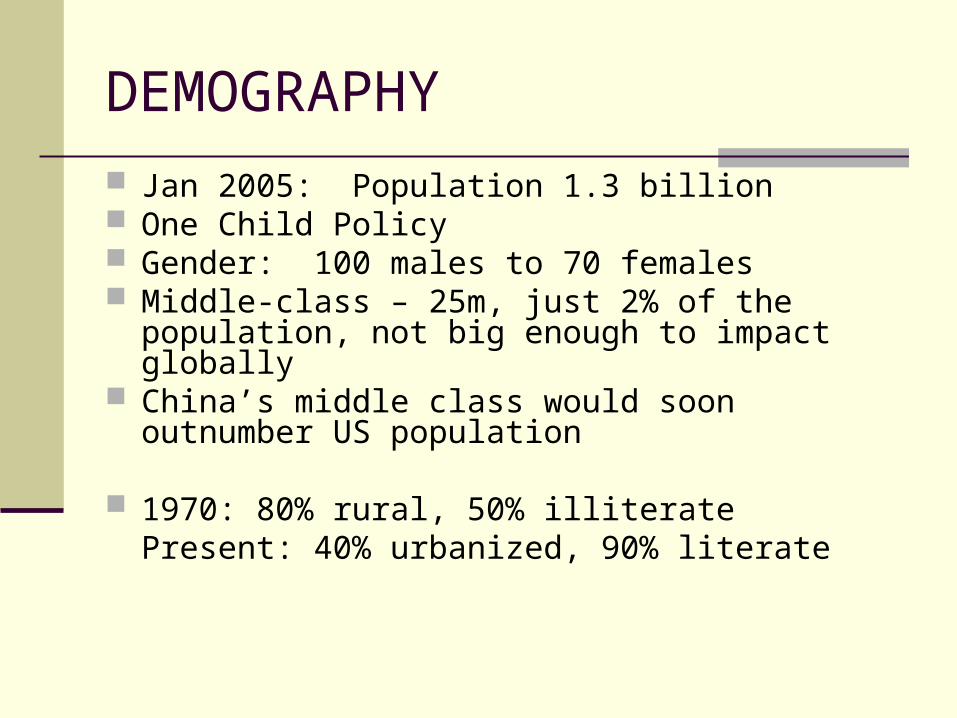

DEMOGRAPHY

Jan 2005: Population 1.3 billion One Child Policy Gender: 100 males to 70 females Middle-class – 25m, just 2% of the population, not big

enough to impact globally China’s middle class would soon outnumber US

population

1970: 80% rural, 50% illiteratePresent: 40% urbanized, 90% literate

MACROECONOMIC DATA(2006 estimate)

Inflation rate – 1.5% Unemployment rate – 4.2% Labor force – 798.1 million

Agriculture – 45% Industry – 24% Services – 31%

GDP growth – 10.5% Agriculture – 12.46% Industry – 47.28% Services – 40.26%

NATIONAL OUTPUT

World’s 4th largest economy (nominal GDP = $2.68 trillion)Expects GDP to top America by 2027

2nd in Purchasing Power Parity terms = $10 trillionIn just 4 years, China is likely to become #1

GDP per capita (nominal) = $2034 (Rank 105th) GDP per capita (PPP) = $7593 (Rank 80th) Wealthiest cities: around $7000 in 2006

US: 1839-86 (double per capita GDP)China: 1978-87, 1987-96

ECONOMIC CLOUT

Currency and trade imbalances – source of political irritations

Dec 2006 : First semi-annual “Strategic Economic Dialogue”

High-level delegation US-China mutual interdependence

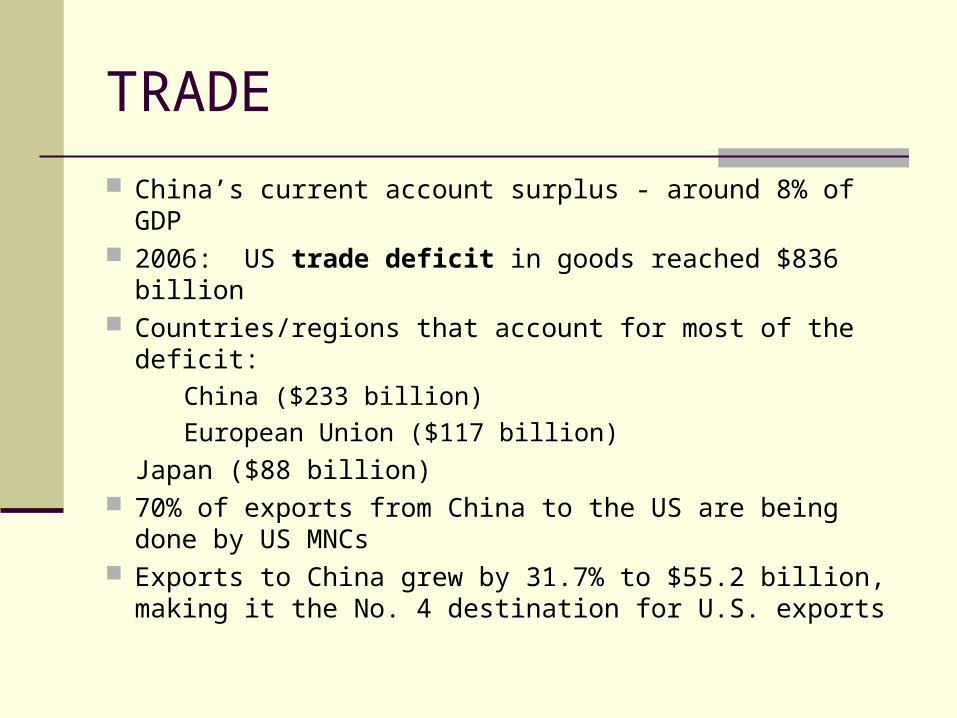

TRADE

China’s current account surplus - around 8% of GDP 2006: US trade deficit in goods reached $836 billion Countries/regions that account for most of the deficit:

China ($233 billion)

European Union ($117 billion)

Japan ($88 billion) 70% of exports from China to the US are being done

by US MNCs Exports to China grew by 31.7% to $55.2 billion,

making it the No. 4 destination for U.S. exports

TRADING PARTNERS(2005)

Exports = $974 billion f.o.b. (2006) US – 21.4% Hong Kong – 16.3% Japan – 11% South Korea – 4.6% Germany – 4.3%

Imports = $777.9 billion f.o.b. (2006) Japan – 15.2% South Korea – 11.6% Taiwan – 11.2% U.S. – 7.4% Germany – 4.6%

FX RESERVES

China's massive hoard is the result of large current-account surplus significant inward foreign direct investment huge inflows of speculative capital over the past

couple of years

Explosion in reserves creates excess liquidity risks fuelling higher inflation asset-price bubbles imprudent bank lending

LOWER YUAN

By keeping the Yuan down China is feeding a trade surplus that is

creating a growing political backlash in America and Europe

G7 urged Beijing to let the Yuan rise to help ease serious "imbalances" in global finance

DOLLAR OR EURO

About 70% of its FX is invested in dollars, mainly Treasury securities

Propped up the dollar and reduced American bond yields

Need to diversify reserves out of dollars Increase in reserves into euros and emerging

Asian currencies Shifting money into euros would push down

the dollar

MANAGED FLOAT

A big shift out of dollars could push up bond yields and hence mortgage rates

Help U.S. manufacturers by raising their competitors‘ costs

Pegged to the dollar into ‘managed float’ Yuan rising at an annual rate of almost 7%

against dollar since September 2006 On November 13th the yuan hit a new high of

7.864 to the dollar

MARKET

Population – 1.3 billion Rapid urbanization Rising standard of living Increasing demand for consumer goods Think Yao, not Mao MNC – imperative to have China strategy

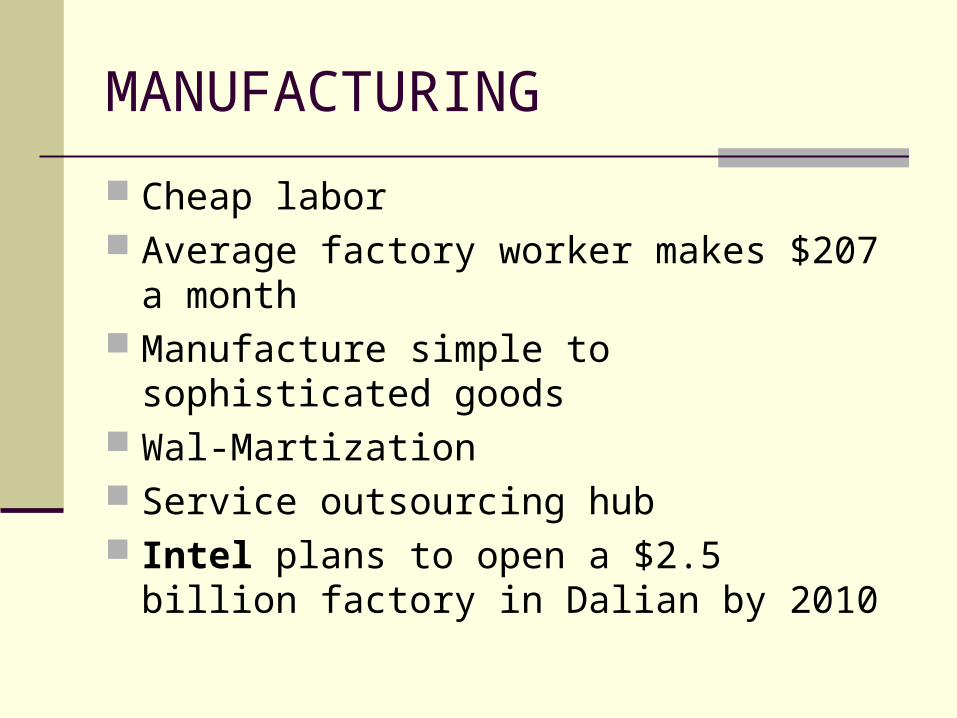

MANUFACTURING

Cheap labor Average factory worker makes $207 a month Manufacture simple to sophisticated goods Wal-Martization Service outsourcing hub Intel plans to open a $2.5 billion factory in

Dalian by 2010

FINANCIAL MARKET

Weakest link State-owned banks Loans are made on the basis of non-market

considerations Banking sector – still murky Limits foreign ownership to 25% High saving rate explains why deposits have

grown faster than loans

STOCK MARKET

2007: Open its financial sector to foreign competition and investment

Require companies listed in Shanghai and Shenzhen stock markets to adopt norms similar to the International Financial Reporting Standards

Need foreign expertise and technology to meet international financing reporting standards

BANKING SERVICES

Foreign financial houses spent about $23b to offer a wide range of banking services – credit cards, mortgages, personal finance

More than $1.8 trillion in personal savings -- and a savings rate of close to 50% -- could become the financial market of the 21st century

OTHER ISSUES

Corruption Lack of transparency Intellectual Property Rights Underdeveloped legal infrastructure China premium (20-30% lower) valuation of

risk

THANK YOU