the royal bank of scotland group plc - investors – rbs/media/files/r/rbs-ir/capital...the royal...

TRANSCRIPT

OFFERING MEMORANDUM CONFIDENTIAL

The Royal Bank of Scotland Group plcA9.1.1

A13.1.1

$1,600,000,000 Fixed Rate/Floating Rate Preferred Capital SecuritiesIssue Price: 100%

The Royal Bank of Scotland Group plc (the ‘‘Issuer’’) is offering $1,600,000,000 Fixed Rate/Floating Rate Preferred Capital Securities (‘‘Capital Securities’’). TheCapital Securities will accrue interest at the rate of 6.990% per annum from (and including) October 4, 2007 (the ‘‘Issue Date’’) up to (but excluding) October 5,2017 (the ‘‘First Reset Date’’), payable semi-annually in arrears on April 5 and October 5, of each year, commencing April 5, 2008. From (and including) theFirst Reset Date, the Capital Securities will accrue interest at the rate of 2.67% per annum above the London interbank offered rate for 3-month U.S. dollardeposits, reset quarterly, payable quarterly in arrears on January 5, April 5, July 5 and October 5 in each year, starting on January 5, 2018, all as more fullydescribed under ‘‘Description of the Capital Securities — Coupon Payments’’.

Coupon Payments (as defined herein) may be deferred in the Issuer’s absolute discretion, as more fully described under ‘‘Description of the CapitalSecurities — Coupon Payments — Deferral of Coupons’’. Whilst any Coupon Payment is so deferred, the Issuer shall not and shall procure that no member of theGroup (as defined herein) shall (i) declare or pay a distribution or dividend on any Junior Securities (as defined herein) (other than a final dividend declared, madeor paid by the relevant company before the Issuer gives notice that such Coupon Payment is to be deferred and other than distributions or dividends paid by amember of the Group which is wholly-owned by another member of the Group); or (ii) redeem, purchase or otherwise acquire for any consideration any JuniorSecurities or Parity Securities (as defined herein). No interest shall accrue on any such deferred Coupon Payment.

No payment of principal or interest in respect of the Capital Securities may be made on the due date for payment unless the Issuer is able to make suchpayment and remain solvent immediately thereafter, all as more fully described in ‘‘Description of the Capital Securities — Status and Subordination —Subordination — Condition of Payment’’. Subject to the provisions contained in ‘‘Description of the Capital Securities — Status and Subordination —Subordination — Winding-up’’, the Issuer shall have no liability to pay any amount in respect of the principal or interest in respect of the Capital Securities to theextent that the Issuer is insolvent or would become so as a result of making such payment.

The Capital Securities have no fixed final maturity date and will be repaid only in the event the Issuer redeems or repurchases the Capital Securities, asdescribed under ‘‘Description of the Capital Securities — Redemption’’.

The Issuer may at its option redeem in whole, but not in part, the Capital Securities at 100% of their principal amount plus accrued and unpaid interest, ifany, on any Reset Date (as defined herein) all as more fully described under ‘‘Description of the Capital Securities — Redemption — Issuer’s Call Option’’. Inaddition, at any time before the First Reset Date, the Issuer may redeem the Capital Securities in whole, but not in part, upon the occurrence of certain specifiedevents relating to taxation or the treatment of the Capital Securities by the U.K. Financial Services Authority, all as more fully described under ‘‘Description ofthe Capital Securities — Redemption’’.

A13.5.1

The Capital Securities will be unsecured obligations of the Issuer, will be subordinated to the claims of Senior Creditors (as defined herein) and will rankpari passu without preference among themselves, all as more fully described under ‘‘Description of the Capital Securities — Status and Subordination’’. If theIssuer is in Winding Up or in a Qualifying Administration (as each term is defined herein), the Issuer shall pay in respect of the principal and of interest on eachCapital Security (in lieu of any other payment by the Issuer) such amount, if any, as would have been payable to the relevant holder (the ‘‘Holder’’) if, on the dayprior to the commencement of the Winding Up or the notice by the administrator, as the case may be, and thereafter, such Holder and/or the Trustee (as definedherein) were the holder of one of a class of Notional Preference Shares (as defined herein) on the assumption that the amount that such Holder was entitled toreceive in respect of each Notional Preference Share on a return of assets in such Winding Up or in a Qualifying Administration were an amount equal to theprincipal amount of the relevant Capital Security and any other outstanding Payments together with any Deferred Coupon Payment which arises under‘‘Description of the Capital Securities — Status and Subordination — Subordination — Condition of Payment’’.

Application will be made to the Financial Services Authority in its capacity as competent authority for the purposes of the Financial Services and MarketsAct 2000 (the ‘‘FSMA’’) (the ‘‘U.K. Listing Authority’’) for the Capital Securities to be admitted to the official list of the U.K. Listing Authority (the ‘‘OfficialList’’) and to the London Stock Exchange plc (the ‘‘London Stock Exchange’’) for the Capital Securities to be admitted to trading on the London StockExchange’s Gilt-Edged and Fixed Interest Market (the ‘‘Market’’). References in this Offering Memorandum to the Capital Securities being ‘‘listed’’ (and allrelated references) shall mean that the Capital Securities will have been admitted to the Official List and will have been admitted to trading on the Market. TheMarket is a regulated market for the purposes of the Investment Services Directive 93/22/EEC.

Investing in the Capital Securities involves risks. See ‘‘Risk Factors’’ beginning on page 9.None of the Capital Securities, the Ordinary Shares (as defined herein) or any securities issuable upon substitution of the Capital Securities have been or will

be registered under the U.S. Securities Act of 1933, as amended (the ‘‘Securities Act’’). In the United States, the offering is being made only to qualifiedinstitutional buyers (‘‘QIBs’’) in reliance on the exemption from registration provided by Rule 144A under the Securities Act (‘‘Rule 144A’’). Prospectivepurchasers that are QIBs are hereby notified that the seller of the Capital Securities may be relying on the exemption from the provisions of Section 5 of theSecurities Act provided by Rule 144A. Outside the United States, the offering is being made in offshore transactions in reliance on Regulation S under theSecurities Act (‘‘Regulation S’’) and, with regard to qualified investors in the European Economic Area, in reliance on private placement exemptions implementingArticle 3(2) of the Prospectus Directive (as defined herein). For a description of certain restrictions on transfers of Capital Securities, see ‘‘Book Entry, TransferRestrictions and Summary of Provisions Relating to the Capital Securities while in Global Form’’.

The Capital Securities will be in registered book-entry form. The Capital Securities sold in the United States pursuant to Rule 144A will be represented byone or more global certificates in registered form (each, a ‘‘Restricted Global Certificate’’) and registered in the name of a nominee of, and will be deposited witha custodian for, The Depository Trust Company (‘‘DTC’’) on or about the Issue Date. The Capital Securities sold outside the United States pursuant toRegulation S will be represented by a global certificate in registered form (the ‘‘Regulation S Global Certificate’’, and together with the Restricted GlobalCertificate, the ‘‘Global Certificates’’) and registered in the name of a nominee of, and deposited with, a common depositary for Euroclear Bank S.A./N.V.(‘‘Euroclear’’) and Clearstream Banking, societe anonyme (‘‘Clearstream, Luxembourg’’, together with Euroclear, the ‘‘Clearing Systems’’) on or about the IssueDate.

On issue, the Capital Securities are expected to be rated ‘‘Aa3’’ by Moody’s Investors Service, Inc. (‘‘Moody’s’’), ‘‘A’’ by Standard & Poor’s RatingServices, a division of The McGraw-Hill Companies, Inc. (‘‘Standard & Poor’s’’) and ‘‘AA’’ by Fitch Ratings Ltd. (‘‘Fitch’’). A credit rating is not arecommendation to buy, sell or hold securities and may be subject to revision, suspension, reduction or withdrawal at any time by the assigning rating agency.

Joint Lead Managers and Joint Bookrunners

MERRILL LYNCH & CO. RBS GREENWICH CAPITALSenior Co-Managers

Banc of America Securities LLC Wachovia SecuritiesJunior Co-Managers

Goldman, Sachs & Co. Lehman BrothersSeptember 26, 2007

TABLE OF CONTENTS

Certain Definitions*********************************************************************** iv

Documents Incorporated by Reference******************************************************* v

Forward-Looking Statements ************************************************************** vii

Overview ****************************************************************************** 1

Risk Factors **************************************************************************** 9

Use of Proceeds************************************************************************* 21

Capitalization of the Group *************************************************************** 22

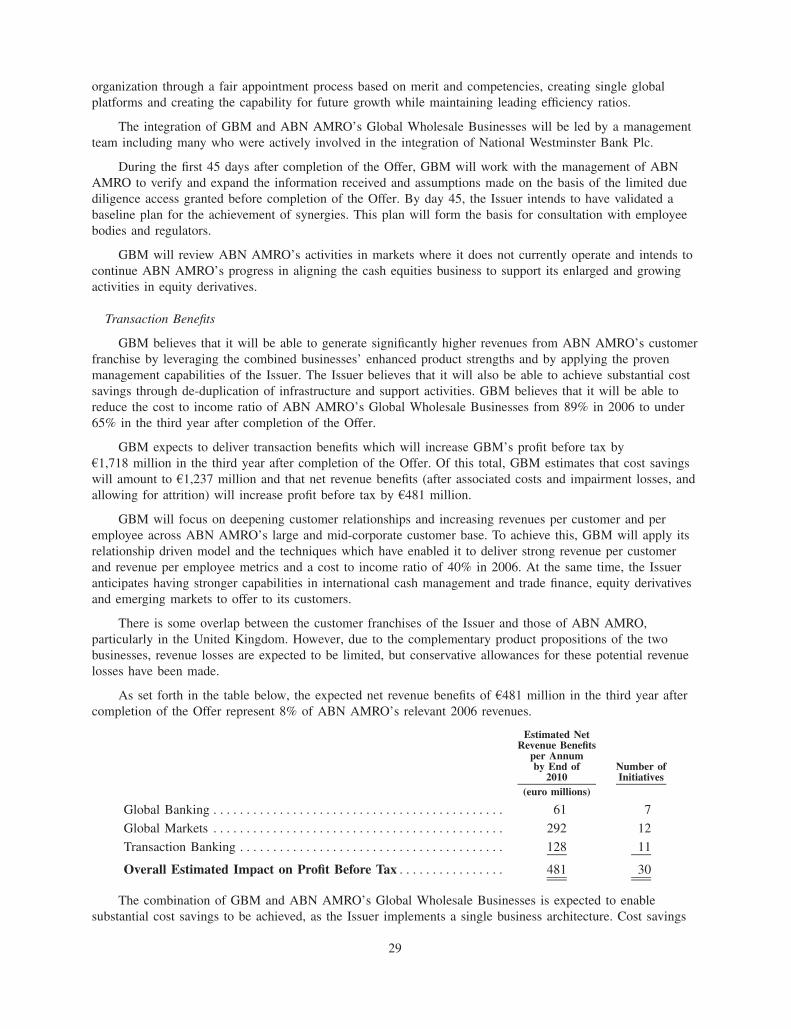

The ABN AMRO Offer ****************************************************************** 24

Description of the Group ***************************************************************** 32

Directors******************************************************************************* 34

Description of the Capital Securities ******************************************************** 36

Plan of Distribution********************************************************************** 63

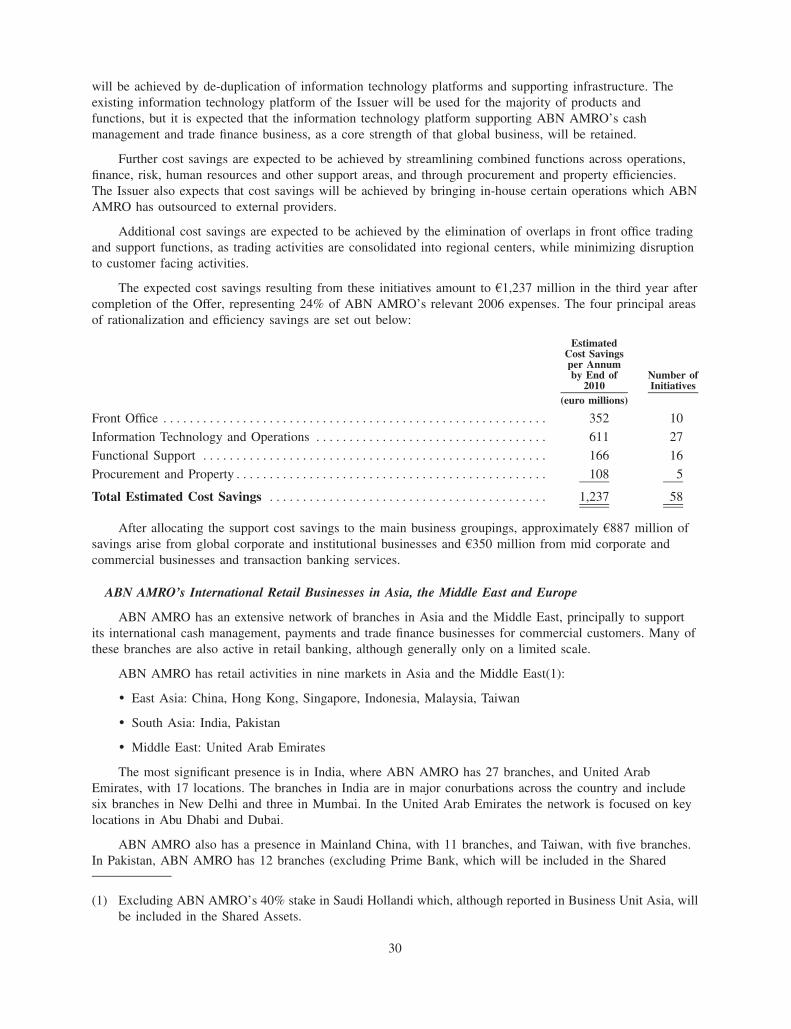

Taxation ******************************************************************************* 65

Selling Restrictions ********************************************************************** 70

Book Entry, Transfer Restrictions and Summary of Provisions Relating to the Capital Securities while inGlobal Form************************************************************************** 71

Legal Opinions************************************************************************** 78

Experts ******************************************************************************** 78

Enforcement of Civil Liabilities and Service Of Process **************************************** 78

General Information ********************************************************************* 79

A 9.1.2

A13.1.2

The Issuer accepts responsibility for the information contained in this Offering Memorandum. To thebest of the knowledge of the Issuer (which has taken all reasonable care to ensure that such is the case), theinformation contained in this Offering Memorandum is in accordance with the facts and does not omitanything likely to affect the import of such information.

A 9.13.2

A13.7.4

Where information in this Offering Memorandum has been sourced from third parties, this informationhas been accurately reproduced and as far as the Issuer is aware and is able to ascertain from the informationpublished by such third parties no facts have been omitted which would render the reproduced informationinaccurate or misleading. The source of third party information is identified where used.

You are authorized to use this Offering Memorandum solely for the purpose of considering aninvestment in the Capital Securities offered in this offering as described in this Offering Memorandum. ThisOffering Memorandum is based on information provided by the Issuer and by other sources that the Issuerbelieves are reliable. You acknowledge and agree that the initial purchasers of the Capital Securities namedunder ‘‘Plan of Distribution’’ (the ‘‘Initial Purchasers’’) have not separately verified the information containedherein and, accordingly, make no representation or warranty, express or implied, as to the accuracy orcompleteness of such information, and nothing contained in, or incorporated by reference in, this OfferingMemorandum is, or shall be relied upon as, a promise or representation by the Initial Purchasers. You maynot reproduce or distribute this Offering Memorandum, in whole or in part, and you may not disclose any ofthe contents of this Offering Memorandum or use any information in this Offering Memorandum for anypurpose other than considering an investment in the Capital Securities. You agree to the foregoing byaccepting delivery of this Offering Memorandum.

No person is authorized to give information or to make any representation in connection with thisoffering or sale of the Capital Securities other than as contained in, or incorporated by reference in, thisOffering Memorandum. If any such information is given or made, it must not be relied upon as having beenauthorized by the Issuer or the Initial Purchasers or any of their affiliates or advisers or selling agents.Neither the delivery of this Offering Memorandum nor any sale made hereunder shall under any

i

circumstances imply that there has been no change in the Issuer’s affairs or that the information set forth inthis Offering Memorandum is correct as of any date subsequent to the date hereof.

In making an investment decision, prospective investors must rely upon their own examination ofthe Issuer, the Group and the Capital Securities and the terms of this Offering Memorandum,including the risks involved. Investors should satisfy themselves that they understand all the risksassociated with making investments in the Capital Securities. If a prospective investor is in any doubtwhatsoever as to the risks involved in investing in the Capital Securities, he or she should consult his orher professional advisors. See ‘‘Risk Factors’’ for further details of such risks.

This Offering Memorandum does not constitute an offer of, or an invitation by or on behalf of theIssuer or the Initial Purchasers to subscribe or purchase any of the Capital Securities. Prospectiveinvestors should also inform themselves as to the legal requirements and tax consequences within thecountries of their residence and domicile for the acquisition, holding or disposal of Capital Securitiesand any foreign exchange restrictions that might be relevant to them. The distribution of this OfferingMemorandum and the offering and sale of the Capital Securities in certain jurisdictions may berestricted by law. The Initial Purchasers require persons into whose possession this OfferingMemorandum comes to inform themselves about, and to observe, any such restrictions. For adescription of certain restrictions on the offering and sale of the Capital Securities, see ‘‘SellingRestrictions’’ and ‘‘Book Entry, Transfer Restrictions and Summary of Provisions Relating to theCapital Securities while in Global Form’’. This Offering Memorandum does not constitute an offer of,or an invitation to purchase, any of the Capital Securities in any jurisdiction in which such offer orsale would be unlawful. No one has taken any action that would permit a public offering of the CapitalSecurities.

STABILIZATION

In connection with the issue of any Capital Securities, Merrill Lynch, Pierce, Fenner & SmithIncorporated (‘‘Merrill Lynch’’) (the ‘‘Stabilizing Manager’’) (or any person acting on behalf of theStabilizing Manager) may over-allot Capital Securities or effect transactions with a view to supporting themarket price of the Capital Securities at a level higher than that which might otherwise prevail. However,there can be no assurance that the Stabilizing Manager (or any person acting on behalf of the StabilizingManager) will undertake any stabilization action. Any stabilization action may begin on or after the date onwhich adequate public disclosure of the terms of the offer of the Capital Securities is made and, if begun,may be ended at any time, but it must end no later than the earlier of 30 days after the issue date of theCapital Securities and 60 days after the date of the allotment of the Capital Securities. Any stabilizationaction or over-allotment must be conducted in accordance with all applicable laws and rules.

NOTICE TO PROSPECTIVE INVESTORS IN THE UNITED STATES

None of the Capital Securities, the Ordinary Shares or any securities issuable upon substitution of theCapital Securities offered hereby have been or will be registered under the Securities Act, or with anysecurities regulatory authority of any state or other jurisdiction in the United States, and may not be offered,sold, pledged or otherwise transferred except pursuant to an exemption from, or in a transaction not subjectto, the registration requirements of the Securities Act and in compliance with any applicable state securitieslaws. The Capital Securities offered hereby have not been recommended by any U.S. federal or statesecurities commission or regulatory authority. Furthermore, the foregoing authorities have not confirmed theaccuracy or determined the adequacy of this Offering Memorandum. Any representation to the contrary is acriminal offense in the United States.

This Offering Memorandum is being provided to a limited number of institutional and othersophisticated investors for informational use solely in connection with the consideration of the purchase of theCapital Securities offered hereby pursuant to Rule 144A or Regulation S. Its use for any other purpose is notauthorized.

ii

Until 40 days after the commencement of this offering, an offer or sale within the United States by anydealer (whether or not participating in this offering) of the Capital Securities initially sold pursuant toRegulation S may violate the registration requirements of the Securities Act if such offer or sale is madeother than in accordance with Rule 144A. See ‘‘Plan of Distribution’’ in this Offering Memorandum.

Each subsequent purchaser of the securities offered hereby will be deemed by its acceptance of thoseCapital Securities to have made certain acknowledgments, representations and agreements intended to restrictthe resale or other transfer of those Capital Securities as set forth in the Capital Securities or described in thisOffering Memorandum and, in connection therewith, may be required to provide confirmation of itscompliance with such resale or other transfer restrictions in certain cases. See ‘‘Selling Restrictions’’ in thisOffering Memorandum.

NOTICE TO NEW HAMPSHIRE RESIDENTS ONLY

NEITHER THE FACT THAT A REGISTRATION STATEMENT OR AN APPLICATION FOR ALICENSE HAS BEEN FILED UNDER CHAPTER 421-B OF THE NEW HAMPSHIRE REVISEDSTATUTES (‘‘RSA’’) WITH THE STATE OF NEW HAMPSHIRE NOR THE FACT THAT ASECURITY IS EFFECTIVELY REGISTERED OR A PERSON IS LICENSED IN THE STATE OFNEW HAMPSHIRE IMPLIES THAT ANY DOCUMENT FILED UNDER RSA 421-B IS TRUE,COMPLETE AND NOT MISLEADING. NEITHER ANY SUCH FACT NOR THE FACT THAT ANYEXEMPTION OR EXCEPTION IS AVAILABLE FOR A SECURITY OR A TRANSACTION MEANSTHAT THE SECRETARY OF STATE HAS PASSED IN ANY WAY UPON THE MERITS ORQUALIFICATIONS OF, OR RECOMMENDED OR GIVEN APPROVAL TO, ANY PERSON,SECURITY OR TRANSACTION. IT IS UNLAWFUL TO MAKE, OR CAUSE TO BE MADE, TOANY PROSPECTIVE PURCHASER, CUSTOMER OR CLIENT ANY REPRESENTATION INCON-SISTENT WITH THE PROVISIONS OF THIS PARAGRAPH.

NOTICE TO PROSPECTIVE INVESTORS IN THE UNITED KINGDOM

This Offering Memorandum is being distributed only to, and is directed at (a) persons outside the UnitedKingdom, (b) persons who have professional experience in matters relating to investments who fall withinArticle 19(1) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the‘‘Order’’) and (c) high net worth entities, and other persons to whom it may otherwise lawfully becommunicated, falling within Article 49(1) of the Order (all such persons together being referred to as‘‘relevant persons’’). The Capital Securities are available only to, and any invitation, offer or agreement tosubscribe, purchase or otherwise acquire such Capital Securities will be available only to or will be engagedin only with, relevant persons. Any person who is not a relevant person should not act or rely on thisdocument or any of its contents.

NOTICE TO PROSPECTIVE INVESTORS IN THE EUROPEAN ECONOMIC AREA

This Offering Memorandum is an advertisement and is not a prospectus for the purposes of EU Directive2003/71/EC (the ‘‘Directive’’) and/or Part VI of the FSMA. A final form prospectus will be prepared andmade available to the public in accordance with the Directive. Investors should not subscribe for anysecurities referred to in this document except on the basis of information contained in the final formprospectus. The final form prospectus, when published, will be published in accordance with the Directive.

iii

CERTAIN DEFINITIONS

In this Offering Memorandum, the following terms are used:

) ‘‘ABN AMRO’’ means ABN AMRO Holding N.V.,

) ‘‘ABN AMRO ADSs’’ means the ABN AMRO American depositary shares, each of which representsone ABN AMRO ordinary share,

) ‘‘ABN AMRO Businesses’’ is defined under ‘‘The ABN AMRO Offer’’ in this Offering Memorandum,

) ‘‘ABN AMRO Group’’ refers to ABN AMRO and its subsidiaries,

) ‘‘ABN AMRO ordinary shares’’ means the ordinary shares, nominal value of 40.56 per share, ofABN AMRO,

) ‘‘Bank of America Agreement’’ refers to the Purchase and Sale Agreement, dated as of April 22,2007, between Bank of America and ABN AMRO Bank in respect of ABN AMRO North AmericaHolding Company, the holding company for LaSalle Bank Corporation, including the subsidiariesLaSalle N.A. and LaSalle Midwest N.A., including any amendment thereto,

) ‘‘Citizens’’ means Citizens Financial Group, Inc.,

) ‘‘Consortium and Shareholders’ Agreement’’ refers to the consortium and shareholders’ agreemententered into by the Consortium Banks and RFS Holdings,

) ‘‘Consortium Banks’’ means Fortis, RBSG and Santander, collectively, and, if the context so requires,their affiliates and RFS Holdings; and ‘‘Consortium Bank’’ means any of them individually,

) ‘‘Fortis’’ means Fortis N.V. and Fortis SA/NV and the group of companies owned and/or controlledby Fortis N.V. and Fortis SA/NV,

) ‘‘Group’’ means The Royal Bank of Scotland Group plc and its subsidiaries,

) ‘‘Offer’’ means the offer by RFS Holdings open to all holders of ABN AMRO ordinary shares whoare located outside of the United States, the offer by RFS Holdings open to all holders ofABN AMRO ordinary shares who are U.S. holders (within the meaning of Rule 14d-1(d) under theSecurities Exchange Act of 1934, as amended) and the offer by RFS Holdings open to all holders ofABN AMRO ADSs, wherever located,

) ‘‘RBS Greenwich Capital’’ means Greenwich Capital Markets, Inc.,

) ‘‘RBSG ordinary shares’’ means the ordinary shares, nominal value £0.25 per share, of RBSG,

) ‘‘RBS plc’’ means The Royal Bank of Scotland plc,

) ‘‘RBSG’’or ‘‘Issuer’’ refers to The Royal Bank of Scotland Group plc (except as the context mayotherwise require, in which case such reference includes our subsidiaries),

) ‘‘RFS Holdings’’ means RFS Holdings B.V.,

) ‘‘Santander’’ means Banco Santander Central Hispano, S.A.,

) ‘‘Transaction’’ means the proposed acquisition by RFS Holdings of ABN AMRO pursuant to the Offerand the reorganization of ABN AMRO and its subsidiaries following completion of the Offer asfurther described in the Issuer’s Form F-4, which the Issuer initially filed with the SEC on July 20,2007, as further amended, and

) ‘‘Ulster Bank’’ means Ulster Bank Group.

iv

DOCUMENTS INCORPORATED BY REFERENCE

This Offering Memorandum incorporates by reference important business and financial information aboutthe Issuer that the Issuer files with the SEC and, as a result, this information is not included in or deliveredwith this Offering Memorandum. This means the Issuer can disclose important information to you byreferring you to those documents. The information incorporated by reference is an important part of thisOffering Memorandum and information that the Issuer files with the SEC after the date of this OfferingMemorandum will automatically be deemed to update and supersede the information in this OfferingMemorandum.

A9.11.3.3

A9.11.1

A9.11.2

A9.11.3.1

A9.11.4.1

The Issuer incorporates by reference into this Offering Memorandum the following business and financialinformation, which has been previously published and has been filed with the U.K. Financial ServicesAuthority: (i) its Annual Report on Form 20-F for the fiscal year ended December 31, 2006, filed with theSEC on April 24, 2007 and the audited consolidated annual financial statements of the Group for the financialyear ended December 31, 2005 together with the audit report thereon contained on pages 134 to 229 of theIssuer’s Annual Report and Accounts 2005; (ii) its interim financial results for the six months ended June 30,2007 on Form 6-K furnished to the SEC on August 15, 2007; (iii) a Form 6-K furnished to the SEC onSeptember 25, 2007, containing certain pro forma unaudited condensed combined financial information andthe related notes thereto in relation to the proposed acquisition of ABN AMRO and (iv) any subsequentForm 6-K containing updated or revised pro forma financial information ((iii) and (iv) together referred toherein as the ‘‘Pro Forma Financial Information’’). Unless otherwise noted, all documents incorporated byreference and filed with the SEC have the SEC file number 001-10306.

Such documents shall be incorporated in, and form part of, this Offering Memorandum, provided thatany statement contained in a document which is incorporated by reference herein shall be modified orsuperseded for the purpose of this Offering Memorandum to the extent that a statement contained hereinmodifies or supersedes such earlier statement (whether expressly, by implication or otherwise). Any statementso modified or superseded shall not, except as so modified or superseded, constitute a part of this OfferingMemorandum.

The Issuer’s Annual Report on Form 20-F includes, among other things, information about its business,the identity of directors and senior management, its history and development, its organizational structure, itssignificant properties, its operating and financial review and prospects, its liquidity and capital resources, itsemployees, its major shareholders and related party transactions. It also includes the Issuer’s audited financialstatements as of and for the three years ended December 31, 2006.

You are advised that the Pro Forma Financial Information has been derived from Amendment No. 5 to theIssuer’s Registration Statement on Form F-4 filed with the SEC on September 24, 2007 (‘‘Amendment No. 5’’).This Registration Statement has not yet been declared effective by the SEC and remains subject to review andcomment by the SEC until such date as it is declared effective. As a result of such review and comment and asa consequence of changes to relevant share prices, interest rates and currency exchange rates during theintervening periods, any amendments to the Registration Statement subsequent to Amendment No. 5 areexpected to amend, supplement or revise the Pro Forma Financial Information.

Upon written or oral request, the Issuer will provide free of charge a copy of any or all of thedocuments that we incorporate by reference into this Offering Memorandum, other than exhibits which arenot specifically incorporated by reference into this Offering Memorandum. To obtain copies you shouldcontact us at Citizens Financial Group, Inc., 28 State Street, Boston, Massachusetts 02109 U.S.A. Attention:Donald J. Barry, Jr., telephone (617) 725-5810. Documents incorporated by reference are available from usupon request without charge. You may also obtain documents incorporated by reference into this OfferingMemorandum from the internet site of the SEC, at http://www.sec.gov.

v

You should rely only on the information contained in, or incorporated by reference into, this OfferingMemorandum in deciding whether to invest in the Capital Securities. The Issuer has not authorized anyone toprovide you with information that is different than what is contained in, or incorporated by reference into,this Offering Memorandum. This Offering Memorandum is accurate as of its date. You should not assumethat the information contained in this Offering Memorandum is accurate as of any date other than that date,and the mailing of this Offering Memorandum to you shall not create any implication to the contrary.

vi

FORWARD-LOOKING STATEMENTS

From time to time, the Issuer may make statements regarding its assumptions, projections, expectations,intentions or beliefs about future events, including statements relating to the Transaction and the Pro FormaFinancial Information included in this Offering Memorandum. The Issuer cautions that these statements mayand often do vary materially from actual results. Accordingly, the Issuer cannot assure you that actual resultswill not differ materially from those expressed or implied by the forward-looking statements. You should readthe sections entitled ‘‘Forward-looking statements’’ in the Issuer’s Annual Report on Form 20-F for the yearended December 31, 2006, and in the Form 6-K with the Issuer’s interim financial results for the six monthsended June 30, 2007, and in the Form 6-K with the Pro Forma Financial Information, which are incorporatedby reference in this Offering Memorandum as described under ‘‘Documents Incorporated by Reference’’above.

The Issuer undertakes no obligation to publicly update or revise any forward-looking statements, whetheras a result of new information, future events or otherwise. In light of these risks, uncertainties andassumptions, forward-looking events discussed in this Offering Memorandum or any information incorporatedby reference in this Offering Memorandum might not occur.

Statements that are not statements of historical fact, including expressions and expectations, are forward-looking in nature and are based on current plans, estimates and projections. The forward-looking statementsinclude statements regarding the Issuer’s financial position; the Issuer’s expectations concerning futureoperations, margins, profitability, liquidity and capital resources; the Issuer’s business strategy and other plansand objectives for future operations and all other statements that are not historical facts. In some cases youcan identify forward-looking statements by terminology such as ‘‘seek(s),’’ ‘‘intends,’’ ‘‘aims,’’ ‘‘expects,’’‘‘will,’’ ‘‘may,’’ ‘‘believe(s),’’ ‘‘should,’’ ‘‘anticipate(s),’’ ‘‘project(s),’’ ‘‘probability,’’ ‘‘risk,’’ ‘‘target,’’‘‘goal,’’ ‘‘objective,’’ ‘‘estimate,’’ ‘‘future,’’ ‘‘potential,’’ ‘‘predicts,’’ and similar expressions. The Issuer hasbased these forward-looking statements on the Issuer’s current expectations and projections about futureevents. Although the Issuer believes that these statements are based on reasonable assumptions, they aresubject to numerous factors, risks and uncertainties that could cause actual outcomes and results to bematerially different from those projected. It is also possible that any or all events described in forward-looking statements may not occur.

vii

(This page intentionally left blank)

OVERVIEW

This overview highlights information contained elsewhere in this Offering Memorandum. Because it is anoverview, it does not contain all the information you should consider before investing in the CapitalSecurities. Before making an investment decision in relation to Capital Securities, you should carefully readthis entire Offering Memorandum, including the section entitled ‘‘Risk Factors’’ and the Issuer’s financialstatements and Pro Forma Financial Information, including the notes thereto, which are incorporated byreference in this Offering Memorandum. Unless otherwise indicated, all financial information refers to that ofthe Group on a consolidated basis.

The Group

A9.4.1.1

A9.6.1

A9.4.1.4

A9.5.1.2

The Royal Bank of Scotland Group plc had a market capitalization of £59.9 billion as at June 30, 2007.The purpose of the Group is to carry on the business of banking in all its aspects, including (but withoutlimitation) the transaction of all financial, monetary or other business. Headquartered in Edinburgh, the Groupoperates in the United Kingdom, the United States and internationally. The Group’s operations are conductedprincipally through RBS and its subsidiaries (including National Westminster Bank Plc (‘‘NatWest’’)), otherthan the general insurance business (which is primarily conducted through Direct Line Group and ChurchillInsurance). Both RBS and NatWest are U.K. clearing banks whose origins go back over 275 years. In theUnited States, the Group’s subsidiary Citizens Financial Group, Inc. is a commercial banking organization.The Group has a diversified customer base and provides a range of products and services to personal,commercial and large corporate and institutional customers. The registered office is 36 St Andrew Square,Edinburgh EH2 2YB, Scotland and the principal place of business is RBS Gogarburn, PO Box 1000,Edinburgh EH12 1HQ, Scotland, telephone +44 131 626 0000.

The Group had total assets of £1,011.3 billion and shareholders’ equity of £41.5 billion as at June 30,2007. The Group had a total capital ratio of 12.5% and tier 1 capital ratio of 7.4% as at June 30, 2007.

Key Features of the Offering

The following key features are provided solely for your convenience. These key features are not intendedto be complete. You should read the full text and more specific details contained elsewhere in this OfferingMemorandum. For a more detailed description of the Capital Securities, see ‘‘Description of the CapitalSecurities’’. Terms used in this overview and not otherwise defined have the meanings given to them in the‘‘Description of the Capital Securities’’ section.

Issuer************************ The Royal Bank of Scotland Group plc.

A13.4.1Securities Offered************** $1,600,000,000 in aggregate principal amount of Fixed Rate/FloatingRate Preferred Capital Securities.

A13.4.5Issue Price ******************* 100%

A13.4.8Issue Date******************** October 4, 2007

Coupon Payments************** The Capital Securities bear interest at the Coupon Rate from (andincluding) the Issue Date.

The Coupon Rate in respect of the period from (and including) the IssueDate to (but excluding) October 5, 2017 (the ‘‘First Reset Date’’) is6.990% per annum. Coupon Payments during this period will be paid,subject as provided herein, semi-annually in arrears on April 5 andOctober 5 in each year, with the first such payment being made onApril 5, 2008 and the last such payment being made on the First ResetDate.

After the First Reset Date, the Coupon Rate in respect of each ResetPeriod shall be the aggregate of 2.67% per annum and the London

1

interbank offered rate for three-month deposits in U.S. dollars. CouponPayments during this period will be paid, subject as provided herein,quarterly in arrears on January 5, April 5, July 5 and October 5 in eachyear, with the first such payment being made on January 5, 2018.

A13.4.10

Yield ************************ The effective yield of the Capital Securities is 6.990% per annum andapplies in respect of the period until the First Reset Date only. The yieldis calculated as at the Issue Date on the basis of the Issue Price. It isnot an indication of future yield.

A13.4.6Subordination ***************** The rights and claims of the holders of the Capital Securities aresubordinated to the claims of Senior Creditors. Payments in respect ofthe Capital Securities will be conditional upon the Issuer being solventat the time of payment, as provided in ‘‘Description of the CapitalSecurities — Status and Subordination — Subordination — Condition ofPayment’’, and the Issuer shall have no liability to pay any such amountto the extent that the Issuer is insolvent or would become insolvent as aresult of making such payment.

The holders of Capital Securities will, in the event of the Winding Upor Qualifying Administration of the Issuer, be subordinated andpostponed in right of payment in the manner provided in the Trust Deedand as specified under ‘‘Description of the Capital Securities — Statusand Subordination — Subordination — Winding-up’’.

Deferral of Payments andRestrictions during Period ofDeferral******************** The Issuer may elect to defer any Coupon Payment in its absolute

discretion. Subject as provided under ‘‘Description of the CapitalSecurities — Alternative Coupon Satisfaction Mechanism — Market Dis-ruption’’, no interest will accrue on any Deferred Coupon Payments. If,on any Coupon Payment Date, all Coupon Payments in respect of theCapital Securities which would otherwise have been due on such dateshall not have been paid as a result of either the exercise by the Issuerof its discretion to defer such Coupon Payments or the operation of theprovisions relating to subordination as more fully described under‘‘Description of the Capital Securities — Subordination — Condition ofPayment’’, then from the date on which payment was originally, orwould have been, due until (x) the date on which the Issuer next pays infull the Coupon Payment due and payable on a Coupon Payment Dateon all outstanding Capital Securities or, if earlier, (y) any OptionalDeferred Coupon Settlement Date upon which the Issuer satisfies in fullall Outstanding Coupon Payments, the Issuer shall not and shall procurethat no member of the Group shall (i) declare or pay a distribution ordividend on any Junior Securities (other than a final dividend declared,made or paid by the relevant company before the Issuer gives notice thatsuch Coupon Payment is to be deferred and other than distributions ordividends paid by a member of the Group which is wholly-owned byanother member of the Group); or (ii) redeem, purchase or otherwiseacquire for any consideration any Junior Securities or Parity Securities.

Subject to the Issuer being solvent in accordance with ‘‘Description ofthe Capital Securities — Status and Subordination — Condition of Pay-ment’’, the Issuer may elect to pay such Deferred Coupon Payment atany time, provided that the Issuer must satisfy such Deferred Coupon

2

Payment on the first to occur of (i) the redemption of the CapitalSecurities, (ii) the substitution or variation of the terms of the CapitalSecurities under ‘‘Description of the Capital Securities — Redemption —Substitution or Variation instead of Redemption’’ or (iii) the substitutionof the Capital Securities under ‘‘Description of the Capital Securities —Redemption — Substitution for Substituted Preference Shares’’.

Optional Redemption *********** The Capital Securities are perpetual securities and have no final maturitydate. However, the Capital Securities may be redeemed in whole, butnot in part, at the option of the Issuer, on any Reset Date at theirprincipal amount together with any Outstanding Payments provided thatthe Issuer is solvent at the time of such redemption and will remainsolvent immediately thereafter, as more fully described under ‘‘Descrip-tion of the Capital Securities — Redemption — Issuer’s Call Option’’.

Redemption due to Tax Event**** The Issuer may elect to redeem all, but not some only, of the CapitalSecurities at their principal amount together with any OutstandingPayments at any time prior to the First Reset Date, if the Issuer satisfiesthe Trustee that:

(i) it has or will or would, but for redemption, become obliged to payadditional amounts as provided or referred to under ‘‘Description of theSecurities — Taxation’’;

(ii) any Coupon Payment would be a ‘‘distribution’’ for UnitedKingdom tax purposes;

(iii) in respect of the obligation of the Issuer to make any CouponPayment on the next following Coupon Payment Date, it would not toany material extent be entitled to have any attributable loss or non-trading deficit set against the profits of companies with which it isgrouped for applicable United Kingdom tax purposes (whether under thegroup relief system current as at the date of this Offering Memorandumor any similar system or systems having like effect as may from time totime exist); or

(iv) in respect of our obligation to make any Coupon Payment on thenext following Coupon Payment Date, it would otherwise suffer adversetax consequences,

in each such case, as a result of any change in, or amendment to, thelaws or regulation of the United Kingdom or any political subdivision orany authority thereof or therein having power to tax, or any change inthe application or official interpretation of such laws or regulations,which change or amendment becomes effective on or after the date ofthis Offering Memorandum and cannot be avoided by the Issuer takingreasonable steps available to it (each a ‘‘Tax Event’’), all as more fullydescribed under ‘‘Description of the Capital Securities — Redemption —Redemption due to Taxation’’.

Redemption due to Capital Disqualification Event ******** The Issuer may elect to redeem all, but not some only, of the Capital

Securities at their principal amount together with any OutstandingPayments, provided it is solvent at the time of such redemption and willremain solvent immediately thereafter, at any time prior to the FirstReset Date, if a Capital Disqualification Event has occurred and iscontinuing, all as more fully described under ‘‘Description of the Capital

3

Securities — Redemption — Redemption for Capital DisqualificationEvent’’.

Substitution or Variation instead ofRedemption***************** If the Issuer has a right to redeem the Capital Securities for tax reasons

or due to a Capital Disqualification Event, then it may, instead of givingnotice to redeem, substitute at any time all (but not some only) of theCapital Securities for, or vary the terms of the Capital Securities so thatthey remain Qualifying Tier 1 Securities or become Qualifying UpperTier 2 Securities, and the Trustee shall agree to such substitution orvariation, all as more fully described in ‘‘Description of the CapitalSecurities — Redemption — Substitution or Variation instead ofRedemption’’.

In connection therewith, all Deferred Coupon Payments (if any) will besatisfied by the operation of the Alternative Coupon SatisfactionMechanism.

If the Issuer varies the terms of the Capital Securities or substitutes newsecurities or non-cumulative preference shares for the Capital Securities,the tax (including United States federal income tax) consequences ofsuch variation or substitution are uncertain because such consequenceswill depend on the terms and conditions that are varied or the terms andconditions of the substituted securities. In certain cases a Holder mayrecognize a gain or loss for tax (including U.S. federal income tax)purposes on such a variation or substitution and have to pay tax thereon,even though no cash will actually be distributed to the holder pursuantto the variation or substitution. Prospective holders should consultwith their own tax advisor about the potential tax consequences tothem of a variation or substitution of the Capital Securities and ofreceiving, holding, and disposing of new securities. This OfferingMemorandum does not describe the tax consequences for Holders ofany such substitution or variation.

Purchase ********************* The Issuer may (subject to the prior consent of, or notification to (andno objection being raised by) the U.K. Financial Services Authority, ineach case solely to the extent then required) at any time purchasebeneficially or procure others to purchase beneficially for its accountCapital Securities in the open market, by tender or by private treaty.Capital Securities purchased or otherwise acquired by the Issuer shall besurrendered to the Registrar for cancellation.

Substitution for SubstitutedPreference Shares************ At any time a Capital Breach Event has occurred and is continuing, the

Issuer may cause the substitution of all, but not some only, of theCapital Securities for Substituted Preference Shares.

The terms of the Substituted Preference Shares shall provide that (x) theSubstituted Preference Shares will have a First Reset Date (or as suchterm may otherwise be defined in the terms thereof) which falls on thesame day as the First Reset Date; (y) the Issuer has the right to choosewhether or not to pay any dividend on the Substituted PreferenceShares; and (z) any dividend payable on the Substituted PreferenceShares shall be non-cumulative, and otherwise shall in all materialrespects provide the holders thereof with at least the same economicrights and benefits as are attached to the Capital Securities, in all cases

4

as more fully described under ‘‘Description of the Capital Securities —Redemption — Substitution for Substituted Preference Shares’’.

In connection with any Preference Share Substitution, all DeferredCoupon Payments and Accrued Payments (if any) will be satisfied onthe Substitution Date by the operation of the Alternative CouponSatisfaction Mechanism.

The Issuer will procure that transfers of the Substituted PreferenceShares, or the relevant certificates in the case of Substituted PreferenceShares deposited in an ADR Facility, shall be able to be effectedbetween holders thereof free of any stamp duty, stamp duty reserve taxor similar taxes arising on transfer of such securities.

The Issuer will pay any stamp duty reserve taxes or capital duties orstamp duties or similar taxes payable in the United Kingdom arising onthe allotment and issue of the Substituted Preference Shares, includingtheir delivery to a common depositary and/or deposit in an ADR Facility(and the issue of the relevant certificates in respect thereof).

If the Issuer substitutes the Capital Securities with Substituted Prefer-ence Shares, the tax (including United States federal income tax)consequences of such substitution are uncertain because such conse-quences will depend on the terms and conditions of the SubstitutedPreference Shares. In certain cases Holders may recognize gain or lossfor tax (including U.S. federal income tax) purposes on such asubstitution and have to pay tax thereon, even though no cash willactually be distributed to the holder pursuant to the substitution.Prospective holders should consult with their own tax advisor aboutthe potential tax consequences to them of a substitution and ofreceiving, holding, and disposing of such Substituted PreferenceShares. This Offering Memorandum does not describe the taxconsequences for Holders of any such substitution.

Alternative Coupon SatisfactionMechanism ***************** Investors will receive payments in respect of the Capital Securities in

cash. However, as more fully described in ‘‘Description of the CapitalSecurities — Alternative Coupon Satisfaction Mechanism’’, (i) in respectof any Deferred Coupon Payment and/or any Accrued Payment, theIssuer must, and (ii) in respect of any Coupon Payment, the Issuer may,satisfy its obligation to make such payments (which term does notinclude any payment of principal) to holders by issuing and/ortransferring Ordinary Shares to the Trustee or its agent.

If any ACSM Payment is to be satisfied through the issue of OrdinaryShares then: (i) by or before the close of business on the seventhbusiness day prior to the relevant ACSM Payment Date, the Issuer willissue and/or transfer to the Trustee such number of Ordinary Shares (the‘‘Payment Ordinary Shares’’) as, in the determination of the CalculationAgent, will have a market value as near as practicable to, but not lessthan, the relevant ACSM Payment to be satisfied in accordance with theAlternative Coupon Satisfaction Mechanism; and (ii) the Trustee hasagreed to use reasonable endeavors to effect the transfer or instruct itsagent to effect the transfer of such Payment Ordinary Shares to or to theorder of the Calculation Agent as soon as practicable and theCalculation Agent shall be required to agree in the Calculation Agency

5

Agreement to use reasonable endeavors to procure purchasers for suchPayment Ordinary Shares.

The Issuer has agreed to fund any shortfall through issuing additionalPayment Ordinary Shares as part of the operation of a similar shareissue, exchange and sale mechanism to that summarized above.

The Issuer shall not be entitled to exercise its option to redeem,substitute or vary the terms of the Capital Securities until such time as ithas available for issue such number of Payment Ordinary Shares as isrequired to be issued in accordance with the Alternative CouponSatisfaction Mechanism for the purposes of satisfying in full inaccordance with ‘‘Description of the Capital Securities — AlternativeCoupon Satisfaction Mechanism’’ any ACSM Payment required to besatisfied in connection with such redemption, substitution or variation ofthe terms of the Capital Securities.

Market Disruption Event ******** If there exists, in the Issuer’s opinion, a Market Disruption Event withrespect to Payment Ordinary Shares on or after the 15th business daypreceding any ACSM Payment Date, then the relevant ACSM Paymentmay be deferred until such time as the Market Disruption Event, in theIssuer’s opinion, no longer exists.

Any such deferred ACSM Payment will be satisfied as soon aspracticable following such time as the Market Disruption Event nolonger exists. Interest shall not accrue on such deferred ACSM Payment,unless, as a consequence of the existence of the relevant MarketDisruption Event, the Issuer does not satisfy the relevant ACSMPayment for a period of 14 days or more after the due date therefor, inwhich case interest shall accrue on such deferred ACSM Payment at arate determined in accordance with the provisions under ‘‘Description ofthe Capital Securities — Coupon Payments’’ and shall be satisfied onlyin accordance with the provisions under ‘‘— Alternative CouponSatisfaction Mechanism,’’ as soon as reasonably practicable after therelevant deferred ACSM Payment is made, all as more fully describedunder ‘‘Description of the Capital Securities — Alternative CouponSatisfaction Mechanism — Market Disruption’’.

Additional Amounts************ All payments by the Issuer or on the Issuer’s behalf of CouponPayments, Deferred Coupon Payments and Accrued Payments in respectof the Capital Securities shall be made without withholding of ordeduction for, or on any account of, any present or future tax, duty orcharge of whatsoever nature imposed or levied by or on behalf of theUnited Kingdom or any authority thereof or therein having power to tax,unless the withholding or deduction is required by law. In that event theIssuer shall pay such additional amounts as will result (after suchwithholding or deduction) in the payment to Holders of the sums whichwould have been receivable (in the absence of such withholding ordeduction) from it in respect of the Capital Securities, subject tocustomary exceptions.

Remedy from Non-Payment ***** The sole remedy against the Issuer available to the Trustee or anyHolder for recovery of amounts owing in respect of any payment ofprincipal or interest in respect of the Capital Securities will be theinstitution of proceedings for the winding-up of the Issuer and/orproving in such winding-up.

6

Form ************************ The Capital Securities will be issued in registered form. CapitalSecurities which are offered and sold outside the United States inreliance on Regulation S will be represented by interests in theRegulation S Global Certificate, registered in the name of the nomineefor a common depositary for Euroclear and Clearstream, Luxembourg onor about the Issue Date. Up to and including the fortieth day after thelater of the commencement of the offering of the Capital Securities andthe Issue Date, beneficial interests in the Regulation S Global Certificatemay be held only through Euroclear or Clearstream. Capital Securitieswhich are offered and sold in the United States in reliance onRule 144A will be represented by interests in the Restricted GlobalCertificate, deposited with a custodian for, and registered in the name ofa nominee of, DTC on or about the Issue Date. Interests in the GlobalCertificates will be shown on, and transfers thereof will be effected onlythrough, records in book-entry form maintained by DTC and its directand indirect participants, in the case of the Restricted Global Certificate,and Euroclear and Clearstream, Luxembourg, in the case of theRegulation S Global Certificate. Individual Certificates evidencingholdings of Capital Securities will only be available in certain limitedcircumstances. See ‘‘Book Entry, Transfer Restrictions and Summary ofProvisions Relating to the Capital Securities while in Global Form’’.

Denominations **************** The Capital Securities will be issued in minimum denominations of$100,000 and integral multiples of $1,000 in excess thereof.

Securities Law Restrictions ****** The Issuer has not registered the Capital Securities, the Ordinary Sharesor any securities issued upon the substitution of the Capital Securitiesunder the Securities Act or any state securities law. You may only offeror sell Capital Securities in a transaction exempt from or not subject tothe registration requirements of the Securities Act. The CapitalSecurities offered hereby are being offered and sold in the United Statesonly to qualified institutional buyers in accordance with Rule 144Aunder the Securities Act and to investors outside the United States inreliance on Regulation S under the Securities Act. See ‘‘SellingRestrictions’’ and ‘‘Book Entry, Transfer Restrictions and Summary ofProvisions Relating to the Capital Securities while in Global Form’’.

A13.4.3Governing Law**************** The Trust Deed and the Capital Securities are governed by the laws ofEngland, except that the status and subordination of the CapitalSecurities and the corresponding provisions of the Trust Deed relating tothe subordination of the Capital Securities are governed by the laws ofScotland. The Paying and Transfer Agency Agreement is governed bythe laws of England.

A13.5.1

Listing and Trading ************ Applications have been made to the U.K. Listing Authority for theCapital Securities to be admitted to the Official List and to the LondonStock Exchange for the Capital Securities to be admitted to trading onthe Market.

Taxation ********************* For a summary of the U.K. tax and U.S. federal income taxconsequences of, and ERISA considerations relating to, an investment inthe Capital Securities, see ‘‘Taxation.’’

A13.4.11Trustee ********************** BNY Corporate Trustee Services Limited.

7

A13.5.2Paying Agent, Registrar********* The Bank of New York of 40th Floor, One Canada Square, LondonE14 5AL.

Use of Proceeds *************** The Issuer will use the net proceeds from the sale of the CapitalSecurities, estimated to be approximately $1,583.5 million after thededuction of estimated fees and expenses, to fund in part the cashportion of the Offer attributable to RBSG, to strengthen the Group’scapital base and for general corporate purposes. The Issuer may issueother securities, including other capital securities, debt securities andpreference shares, in connection with financing the portion of the Offerwhich is attributable to the Issuer.

A13.7.5Ratings ********************** The Capital Securities are expected on issue to be rated ‘‘Aa3’’ byMoody’s, ‘‘A’’ by Standard & Poor’s and ‘‘AA’’ by Fitch. A creditrating is not a recommendation to buy, sell or hold securities and maybe subject to revision, suspension, reduction or withdrawal at any timeby the assigning rating agency.

A13.4.2Securities Codes: ************** Restricted Capital Securities

CUSIP: 780097AS0

ISIN: US780097AS09

Regulation S Capital Securities

Common Code: 32386504

ISIN: XS0323865047

8

RISK FACTORS

A13.2

A9.3.1

Investing in the securities offered using this Offering Memorandum involves risk. You should carefullyconsider the following factors and the other information in this Offering Memorandum and the informationincorporated by reference herein before deciding to invest in the Capital Securities. If any of these risksoccurs, the business, financial condition, and results of operations of the Group could suffer, and the tradingprice and liquidity of the Capital Securities could decline, in which case you could lose part or all of yourinvestment. The Issuer also believes that the factors set forth in this section under ‘‘Risks Relating to theCapital Securities’’ may affect its ability to satisfy its obligations under the Capital Securities. All of thesefactors are contingencies which may or may not occur and the Issuer is not in a position to express a viewon the likelihood of any such contingency occurring. The Issuer believes that the factors described belowrepresent the principal risks inherent in investing in the Capital Securities, but the Issuer may be unable topay interest, principal or other amounts on or in connection with the Capital Securities for other reasons andthe Issuer does not represent that the statements below regarding the risks of holding any Capital Securitiesare exhaustive. Terms used in this section and not otherwise defined have the meanings given to them in the‘‘Description of the Capital Securities’’ section. The Issuer is the Group’s ultimate parent company and isaffected by business and financial risks across the spectrum of the Group’s operations.

Risks Related to the Business of the Group

Set out below are certain risk factors which could affect the Group’s future results and cause them to bematerially different from expected results. The Group’s results could also be affected by competition andother factors. Although the following sets out all the material risk factors which may affect the Group’sresults and of which the Issuer is aware, the factors discussed below may not be a complete andcomprehensive statement of all potential risks and uncertainties its businesses face. Investors should note thatthey bear the risk of insolvency of the Issuer.

The Group’s business and earnings are affected by general business and geopolitical conditions.

The performance of the Group is influenced by economic conditions particularly in the United Kingdom,United States and Europe. Downturns in these economies could result in a general reduction in businessactivity and a consequent loss of income for the Group. It could also cause a higher incidence of credit lossesand losses in its trading portfolios. Geopolitical conditions can also affect the earnings of the Group. Terroristacts and threats and the response of governments in the United Kingdom, United States and elsewhere tothem could affect the level of economic activity. The business of the Group is also exposed to the risk ofbusiness interruption and economic slowdown following the outbreak of a pandemic.

The financial performance of the Group is affected by borrower credit quality.

Risks arising from changes in credit quality and the recoverability of loans and amounts due fromcounterparties are inherent in a wide range of the businesses of the Group. Adverse changes in the creditquality of its borrowers and counterparties or a general deterioration in the United Kingdom, United States,European or global economic conditions, or arising from systemic risks in the financial systems, could affectthe recoverability and value of the assets of the Group and require an increase in its provision for impairmentlosses and other provisions.

Changes in interest rates, foreign exchange rates, equity prices and other market factors affect thebusiness of the Group.

The most significant market risks the Group faces are interest rate, foreign exchange and bond andequity price risks. Changes in interest rate levels, yield curves and spreads may affect the interest rate marginrealized between lending and borrowing costs. Changes in currency rates, particularly in the sterling-dollarand sterling-euro exchange rates, affect the value of assets and liabilities denominated in foreign currenciesand affect earnings reported by the Issuer’s non-U.K. subsidiaries, mainly Citizens, RBS Greenwich Capitaland Ulster Bank, and may affect income from foreign exchange dealing. The performance of financial

9

markets may cause changes in the value of its investment and trading portfolios. The Group has implementedrisk management methods to mitigate and control these and other market risks to which it is exposed.However, it is difficult to predict with accuracy changes in economic or market conditions and to anticipatethe effects that such changes could have on the financial performance and business operations of the Group.

The insurance businesses of the Group are subject to inherent risks involving claims.

Future claims in the general and life assurance business of the Group may be higher than expected as aresult of changing trends in claims experience resulting from catastrophic weather conditions, demographicdevelopments, changes in mortality rates and other causes outside its control. Such changes would affect theprofitability of current and future insurance products and services. The Group re-insures some of the risks ithas assumed.

Operational risks are inherent in the businesses of the Group.

The businesses of the Group are dependent on its ability to process a very large number of transactionsefficiently and accurately. Operational losses can result from fraud, errors by employees, failure to documenttransactions properly or to obtain proper authorization, failure to comply with regulatory requirements andConduct of Business Rules, equipment failures, natural disasters or the failure of external systems, forexample, those of the suppliers or counterparties of the Group. Although the Group has implemented riskcontrols and loss mitigation actions, and substantial resources are devoted to developing efficient proceduresand to staff training, it is only possible to be reasonably, but not absolutely, certain that such procedures willbe effective in controlling each of the operational risks faced by the Group.

Each of the businesses of the Group is subject to substantial regulation and regulatory oversight. Anysignificant regulatory developments could have an effect on how the Group conducts its business and onthe results of operations.

The Group is subject to financial services laws, regulations, administrative actions and policies in eachlocation in which it operates. This supervision and regulation, in particular in the United Kingdom and theUnited States, if changed, could materially affect the business of the Group, the products and services offeredor the value of assets.

Future growth in the earnings of the Group depends on strategic decisions regarding organic growthand potential acquisitions.

The Group devotes substantial management and planning resources to the development of strategic plansfor organic growth and identification of possible acquisitions, supported by substantial expenditure to generategrowth in customer business. If these strategic plans do not reach completion in a timely manner or on a costeffective basis or do not otherwise meet with success, the earnings of the Group could grow more slowly ordecline.

The risk of litigation is inherent in the operations of the Group.

In the ordinary course of the business, legal actions, claims against and by the Group and arbitrationsarise; the outcome of such legal proceedings could affect the financial performance of the Group. See‘‘General Information — Litigation’’.

The Group is exposed to the risk of changes in tax legislation and its interpretation and to increases inthe rate of corporate and other taxes in the jurisdictions in which the Group operates.

The activities of the Group are subject to tax at various rates around the world computed in accordancewith local legislation and practice. Action by governments to increase tax rates or to impose additional taxeswould reduce its profitability. Revisions to tax legislation or to its interpretation might also affect the resultsof the Group in the future.

10

Governmental policy and regulation may have an adverse effect on the results of the Group.

The businesses and earnings of the Group can be affected by the fiscal or other policies and otheractions of various governmental and regulatory authorities in the United Kingdom, the European Union, theUnited States and elsewhere.

There is continuing political and regulatory scrutiny of the operation of the retail banking and consumercredit industries in the United Kingdom and elsewhere. The nature and impact of future changes in policiesand regulatory action are not predictable and are beyond the control of the Group, but could have an adverseimpact on its businesses and earnings.

In the European Union, these regulatory actions included an inquiry into retail banking in all of the then25 member states by the European Commission’s Directorate General for Competition. The inquiry examinedretail banking in Europe generally. On January 31, 2007, the European Commission announced that barriersto competition in certain areas of retail banking, payment cards and payment systems in the European Unionhad been identified. The European Commission indicated that it will use its powers to address these barriersand will encourage national competition authorities to enforce European and national competition laws whereappropriate. Any action taken by the European Commission and national competition authorities could havean adverse impact on the Issuer’s payment cards and payment systems businesses and on the retail bankingactivities in the European Union countries in which it operates.

In the United Kingdom in September 2005, the Office of Fair Trading (‘‘OFT’’) received a super-complaint from the Citizens Advice Bureau relating to payment protection insurance, or PPI. As a result, theOFT commenced a market study on PPI in April 2006. In October 2006, the OFT announced the outcome ofthe market study and, on February 7, 2007, following a period of consultation, the OFT referred the PPImarket to the U.K. Competition Commission for an in-depth inquiry. This inquiry could continue for up totwo years. Also, in October 2006, the U.K. Financial Services Authority published the outcome of its broadindustry thematic review of PPI sales practices in which it concluded that some institutions fail to treatcustomers fairly.

In April 2006, the OFT commenced a review of the undertakings given following the conclusion of theCompetition Commission Inquiry in 2002 into the supply of banking services to small and mediumenterprises (‘‘SMEs’’).

The OFT has carried out investigations into Visa and MasterCard credit card interchange rates. Thedecision by the OFT in the MasterCard interchange case was set aside by the Competition Appeals Tribunalin June 2006. The OFT’s investigations in the Visa interchange case and a second MasterCard interchangecase are ongoing. The outcome is not known, but these investigations may have an impact on the consumercredit industry in general and, therefore in this sector of the Group’s business. On February 9, 2007, the OFTannounced that it was expanding its investigation into interchange rates to include debit cards.

On September 7, 2006, the OFT announced that it had decided to undertake an investigation of theapplication of its statement on credit card fees to current account unauthorized overdraft fees. Theinvestigation was completed in March 2007. On March 29, 2007, the OFT announced its decision to conducta formal in-depth investigation into the fairness of bank current account charges. On April 26, 2007, the OFTannounced a formal market study into personal current accounts in the United Kingdom. The study will focuson the impact of free-if-in-credit current accounts on competition and whether they deliver value toconsumers. The OFT expects to complete the market study by the end of 2007. In common with other banksin the United Kingdom, the Group has received claims from customers in respect of current accountadministrative charges. The financial performance of the Group could be adversely affected if, by legalprocess or regulatory action, such charges are determined to be, in whole or in part, penalties or unfair.

On January 26, 2007, the U.K. Financial Services Authority issued a Statement of Good Practice relatingto Mortgage Exit Administration Fees. On March 1, 2007, the Group adopted a policy of charging allcustomers the fee applicable at the time the customers took out the mortgage. In addition, any customers whohad previously been charged a higher fee than was applicable at the time they took out the mortgage and who

11

complained were refunded the difference in fees. This approach was one of the options recommended by theU.K. Financial Services Authority.

On April 26, 2007, the Office of Rail Regulation referred the leasing of rolling stock for franchisedpassenger services and the supply of related maintenance services in Great Britain to the U.K. CompetitionCommission for an inquiry lasting up to two years. The Group includes the Angel Trains group, a rollingstock leasing business operating in this market.

On May 15, 2007, the Competition Commission published its final report into the supply of personalcurrent account banking services in Northern Ireland. It is anticipated that a statutory instrumentimplementing the remedies set out in the report will be made in October 2007. The Group includes UlsterBank, which is active in the Northern Ireland current account market.

Other areas where changes could have an adverse impact include:

) the monetary, interest rate and other policies of central banks and regulatory authorities;

) general changes in government or regulatory policy or changes in regulatory regimes that maysignificantly influence investor decisions in particular markets in which the Issuer operates or mayincrease the costs of doing business in those markets;

) other general changes in the regulatory requirements, such as prudential rules relating to the capitaladequacy framework;

) changes in competition and pricing environments;

) further developments in the financial reporting environment;

) expropriation, nationalization, confiscation of assets and changes in legislation relating to foreignownership; and

) other unfavorable political, military or diplomatic developments producing social instability or legaluncertainty which, in turn, may affect demand for the products and services of the Issuer.

Risks Related to the Transaction

The consummation of the Offer is subject to the satisfaction or waiver of certain Offer conditions, all ofwhich, except for the minimum acceptance condition and the government and regulatory approvalsconditions, must be either satisfied or waived prior to the expiration of the Offer period. There can beno assurance that the Offer conditions will be satisfied or waived and that the Issuer will complete theacquisition of the ABN AMRO Businesses.

The consummation of the Offer is subject to the satisfaction or waiver of certain Offer conditions, all ofwhich, except for the minimum acceptance condition and the government and regulatory approvals conditions,must be either satisfied or waived prior to the expiration of the Offer period (as such Offer period may beextended in accordance with applicable law and regulation). These conditions include (i) acceptance of theOffer by the holders of at least 80% of the ABN AMRO ordinary shares, calculated on a fully diluted basis,(ii) the completion of the sale of LaSalle Bank Corporation (‘‘La Salle’’) and the retention of the proceedstherefrom within the ABN AMRO Group, (iii) the absence of a material adverse change in respect of thebusiness, cash flow, financial or trading position, assets, profits, operational performance, capitalization,prospects or activities of either the ABN AMRO Group, RFS Holdings or any of the Consortium Banks,(iv) the absence of a material adverse change in national or international capital markets, financial, political oreconomic conditions or currency exchange rates or exchange controls, (v) the absence of material litigation orother proceedings, (vi) the absence of injunctions or other restrictions on the consummation of the Offer,(vii) the granting of all necessary regulatory approvals and (viii) the declaration by the European Commissionthat the concentrations resulting from the Transaction are compatible with the competition and antitrust rulesof the common market (each Offer condition, an ‘‘Offer Condition’’ and, collectively, the ‘‘OfferConditions’’). There can be no assurance that any or all of the Offer Conditions will be satisfied or waived.In addition, the Offer is subject to a competing offer by Barclays plc (‘‘Barclays’’). There can be no

12

assurance that the Offer will be consummated and the acquisition of the ABN AMRO Businesses will becompleted.

Obtaining required regulatory approvals may delay completion of the Transaction, and compliance withconditions and obligations imposed in connection with regulatory approvals could adversely affect thebusinesses of the Group and the businesses of ABN AMRO.

The Transaction will require various approvals or consents from, among others, the Dutch Minister ofFinance (Minister van Financien) and the Dutch Central Bank, as the case may be, the U.K. FinancialServices Authority, the Bank of Spain, the European Commission and various other antitrust authoritiesoutside the European Union, other bank regulatory, securities, insurance and other regulatory authoritiesworldwide. RFS Holdings and the Consortium Banks have made all necessary filings for the approval of thechange of control of ABN AMRO with their home regulators, in so far as these are required, and have madesubstantially all other applications for regulatory change of control approval. Approval has been requestedfrom, amongst others, the FSA, the Dutch Minister of Finance (Minister van Financien), the SpanishSecurities Market Commission (Comision Nacional del Mercado de Valores), and the Belgian Banking,Finance and Insurance Commission (Commission Bancaire, Financiere et des Assurances). In a number ofjurisdictions, including the Netherlands and the United Kingdom, such approvals have already been granted.Other than approvals by competition and antitrust authorities, obtaining regulatory approval for thereorganisation (as opposed to the acquisition) of ABN AMRO is not a condition to the Offer. Accordingly,formal consent from bank regulators for the subsequent proposed restructuring has not yet been applied for inmost jurisdiction where regulatory consent is required. The governmental entities from which these approvalsare required, including the Dutch Central Bank, may refuse to grant such approval, or, may impose conditionson, or require divestitures or other changes in connection with, the completion of the Transaction. Theseconditions or changes could have the effect of delaying completion of the Transaction, reducing theanticipated benefits of the Transaction or imposing additional costs on the Issuer or limiting its revenuesfollowing completion of the Transaction, any of which might have a material adverse effect on the Group’sbusiness, financial condition or prospects after completion of the Transaction. In order to obtain theseregulatory approvals, the Consortium Banks may have to divest, or commit to divesting, certain of thebusinesses of ABN AMRO and/or the Consortium Banks to third parties. In addition, the Issuer may berequired to make other commitments to regulatory authorities. These divestitures and other commitments, ifany, may have an adverse effect on its business, results of operations, financial condition or prospects afterthe completion of the Transaction.

Following completion of the Offer and insofar as not already obtained, regulatory approvals for thereorganization of the ABN AMRO Group will be sought from the relevant regulators once the ConsortiumBanks have obtained the necessary information to be able to prepare and complete the approval applications.While the Consortium Banks will be aiming to obtain these regulatory approvals as soon as practicablefollowing completion of the Offer, the period from completion of the Offer to receipt of such approvals forthe reorganisation will be largely dependent on the time required to obtain the necessary information tosubmit the applications for approval, the duration of the relevant regulatory review process and effects of anyconditions imposed on the reorganization by any regulator. There could therefore be a delay in completingthe reorganization, reducing the anticipated benefits of the Transaction or imposing additional costs on us orlimiting our revenues following completion of the Transaction, any of which might have a material adverseeffect on our business, results of operations, financial condition or prospects after completion of theTransaction.

Certain jurisdictions claim jurisdiction under their competition or antitrust laws in respect of acquisitionsor mergers that have the potential to affect their domestic marketplace. A number of these jurisdictions mayclaim to have jurisdiction to review the Transaction. Such investigations or proceedings may be initiated and,if initiated, may have an adverse effect on its business, results of operations, financial condition or prospectsafter the completion of the Transaction.

13

The information relating to ABN AMRO contained in this document is derived primarily from publiclyavailable information, which the Issuer has been unable independently to verify. As a result, the Issuer’sestimates of the impact of the Transaction on the Pro Forma Financial Information incorporated byreference in this Offering Memorandum may be incorrect.