the shape of recovery: what’s next?

TRANSCRIPT

The Shape of Recovery:

What’s Next?

22

Panelists

Leon LaBrecque

JD, CPA, CFP®, CFA

Chief Growth Officer

248.918.5905

Matt Pullar

Vice President, Private Client

Services

216.774.1192

3

As an independent financial services firm, our salaried, non-commission professionals have access to a variety of solutions and resources and our recommendations are based solely on what works best for you, not us.

About Sequoia Financial Group

1. What are we monitoring?

2. What are we hearing from our

investment partners?

3. What are we recommending?

Financial Market Update

4

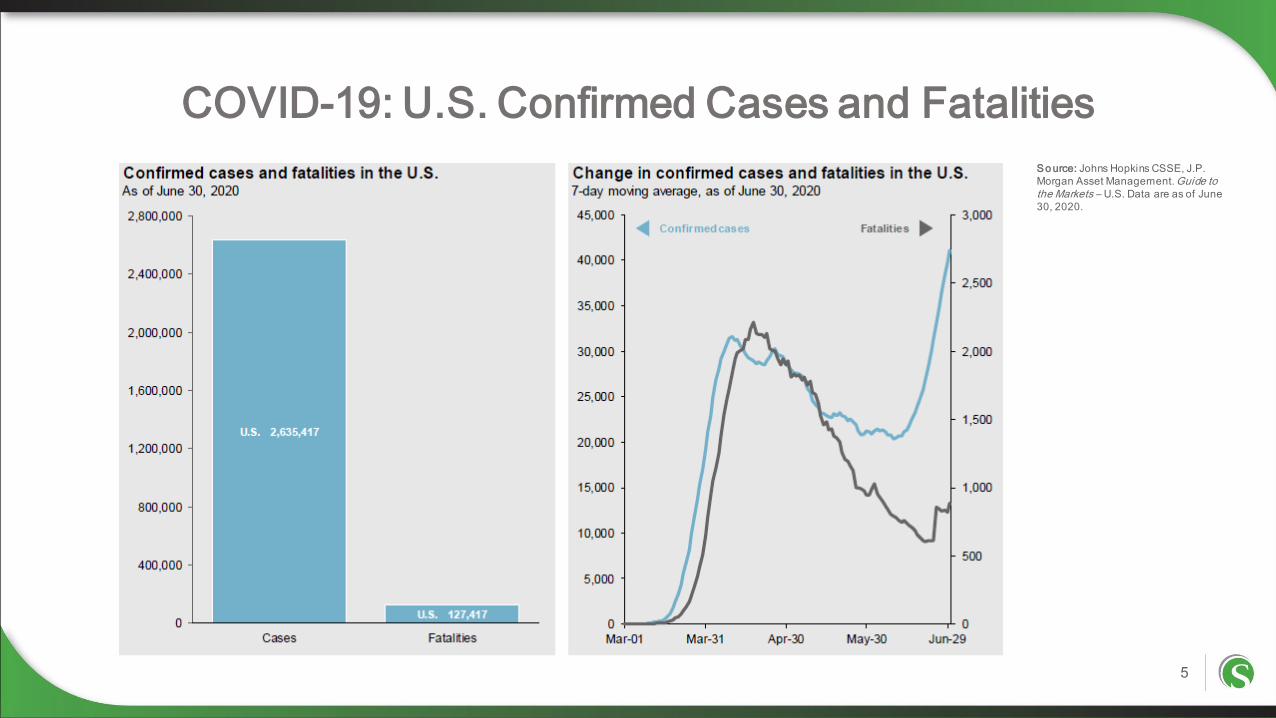

COVID-19: U.S. Confirmed Cases and Fatalities

5

So urce: Johns Hopkins CSSE, J.P.

Morgan Asset Management. Guide to the Markets – U.S. Data are as of June

30, 2020.

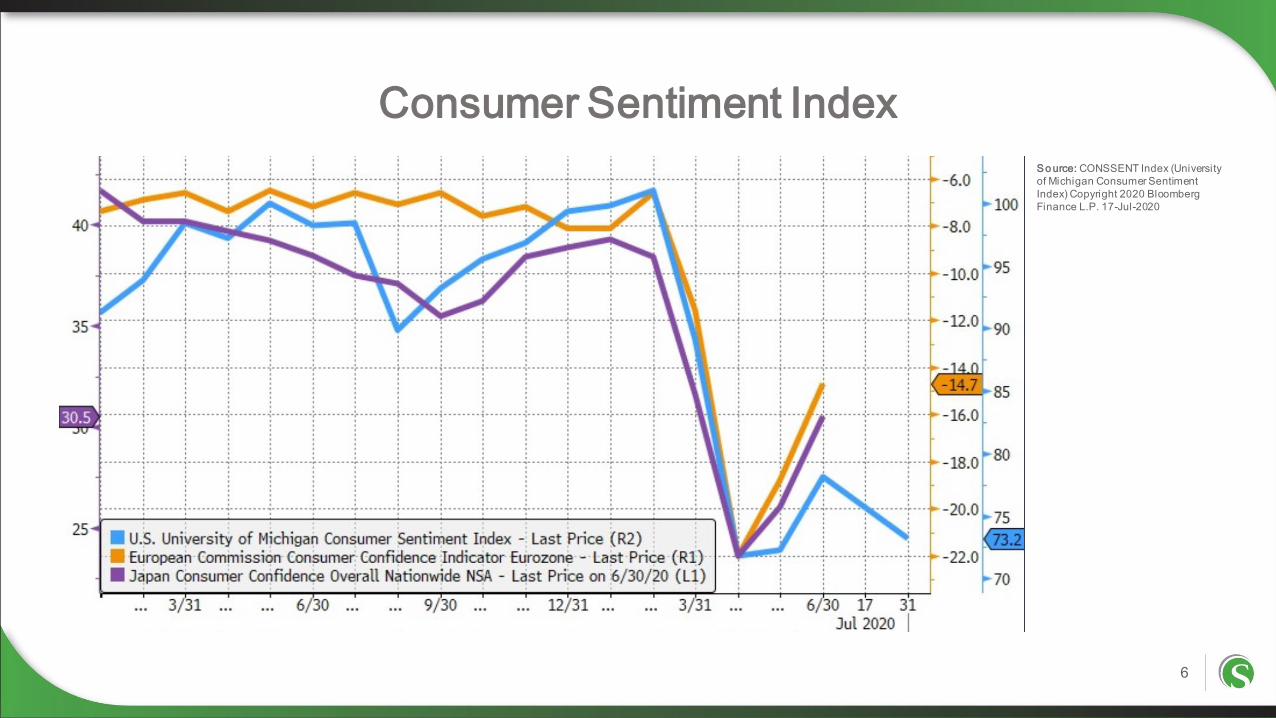

Consumer Sentiment Index

6

So urce: CONSSENT Index (University

of Michigan Consumer Sentiment

Index) Copyright 2020 Bloomberg

Finance L.P. 17-Jul-2020

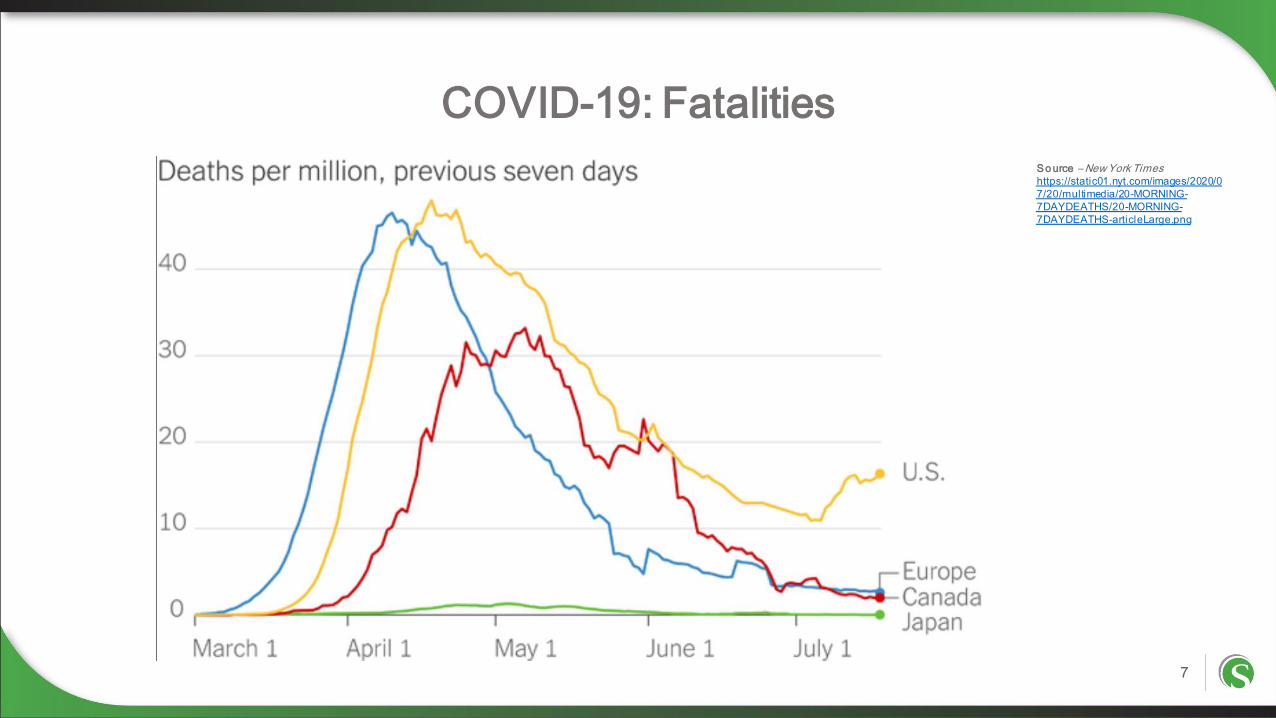

COVID-19: Fatalities

7

So urce – New York Times https://static01.nyt.com/images/2020/0

7/20/multimedia/20-MORNING-

7DAYDEATHS/20-MORNING-

7DAYDEATHS-articleLarge.png

High-Frequency Economic Activity

8

So urce: Apple Inc., FlightRadar24,

Mortgage Bankers Association (MBA),

OpenTable, STR, Transportation

Security Administration (TSA), J.P.

Morgan Asset Management. *Driving

directions and total global fl ights are 7-

day moving averages and are

compared to a pre-pandemic baseline.

Guide to the Markets – U.S. Data are

as of June 30, 2020.

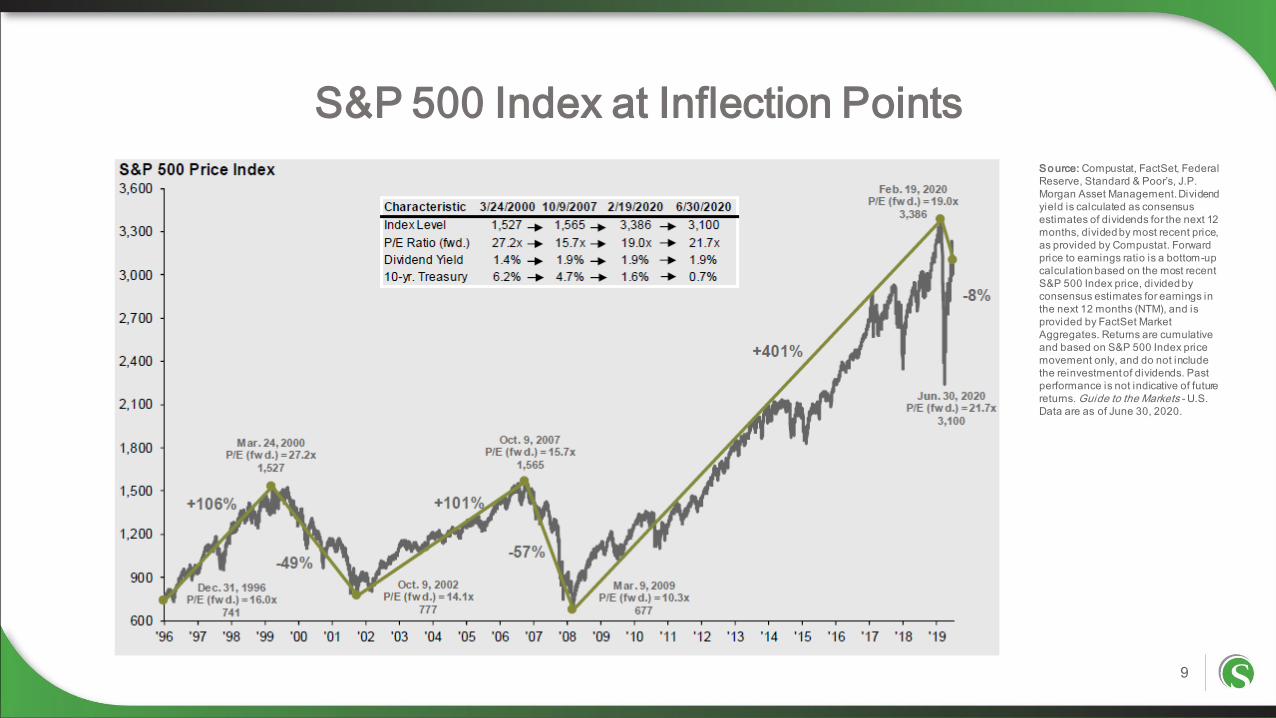

S&P 500 Index at Inflection Points

9

So urce: Compustat, FactSet, Federal

Reserve, Standard & Poor’s, J.P.

Morgan Asset Management. Dividend

yield is calculated as consensus

estimates of dividends for the next 12

months, divided by most recent price,

as provided by Compustat. Forward

price to earnings ratio is a bottom-up

calculation based on the most recent

S&P 500 Index price, divided by

consensus estimates for earnings in

the next 12 months (NTM), and is

provided by FactSet Market

Aggregates. Returns are cumulative

and based on S&P 500 Index price

movement only, and do not include

the reinvestment of dividends. Past

performance is not indicative of future

returns. Guide to the Markets - U.S.

Data are as of June 30, 2020.

S&P 500 Valuation Measures

10

So urce: FactSet, FRB, Robert Shiller,

Standard & Poor’s, Thomson Reuters,

J.P. Morgan Asset Management. Price

to earnings is price divided by

consensus analyst estimates of

earnings per share for the next 12

months as provided by IBES since July

1995, and FactSet for June 30, 2020.

Current next 12-months consensus

earnings estimates are $143. Average

P/E and standard deviations are

calculated using 25 years of IBES

history. Shiller’s P/E uses trailing 10-

years of inflation-adjusted earnings as

reported by companies. Dividend yield

is calculated as the next 12-months

consensus dividend divided by most

recent price. Price to book ratio is the

price divided by book value per share.

Price to cash flow is price divided by

NTM cash flow. EY minus Baa yield is

the forward earnings yield (consensus

analyst estimates of EPS over the next

12 months divided by price) minus the

Moody’s Baa seasoned corporate bond

yield. Std. dev. over-/under-valued is

calculated using the average and

standard deviation over 25 years for

each measure. Guide to the Markets –U.S. Data are as of June 30, 2020.

Bear Markets and Subsequent Bull Runs

11

So urce: FactSet, NBER, Robert Shiller,

Standard & Poor’s, J.P. Morgan Asset

Management.*A bear market is defined

as a 20% or more decline from the

previous market high. The related

market return is the peak to trough

return over the cycle. Periods of

“Recession” are defined using NBER

business cycle dates. “Commodity

spikes” are defined as movement in oil

prices of over 100%over an 18-month

period. Periods of “Extreme Valuations”

are those where S&P 500 last 12-

months P/E levels were approximately

two standard deviations above long-run

averages, or time periods where equity

market valuations appeared expensive

given the broader macroeconomic

environment. “Aggressive Fed

Tightening” is defined as Federal

Reserve monetary tightening that was

unexpected and/or significant in

magnitude. Bear and Bull returns are

price returns. Guide to the Markets –U.S. Data are as of June 30, 2020.

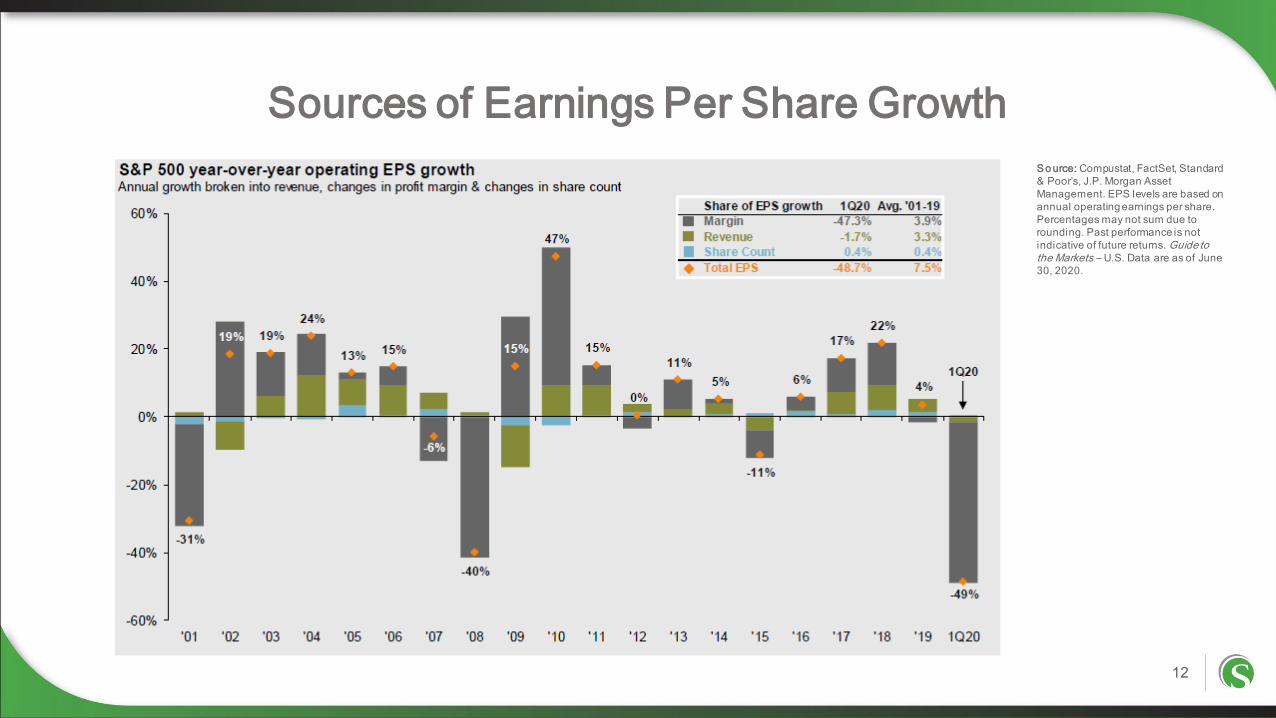

Sources of Earnings Per Share Growth

12

So urce: Compustat, FactSet, Standard

& Poor’s, J.P. Morgan Asset

Management. EPS levels are based on

annual operating earnings per share.

Percentages may not sum due to

rounding. Past performance is not

indicative of future returns. Guide to the Markets – U.S. Data are as of June

30, 2020.

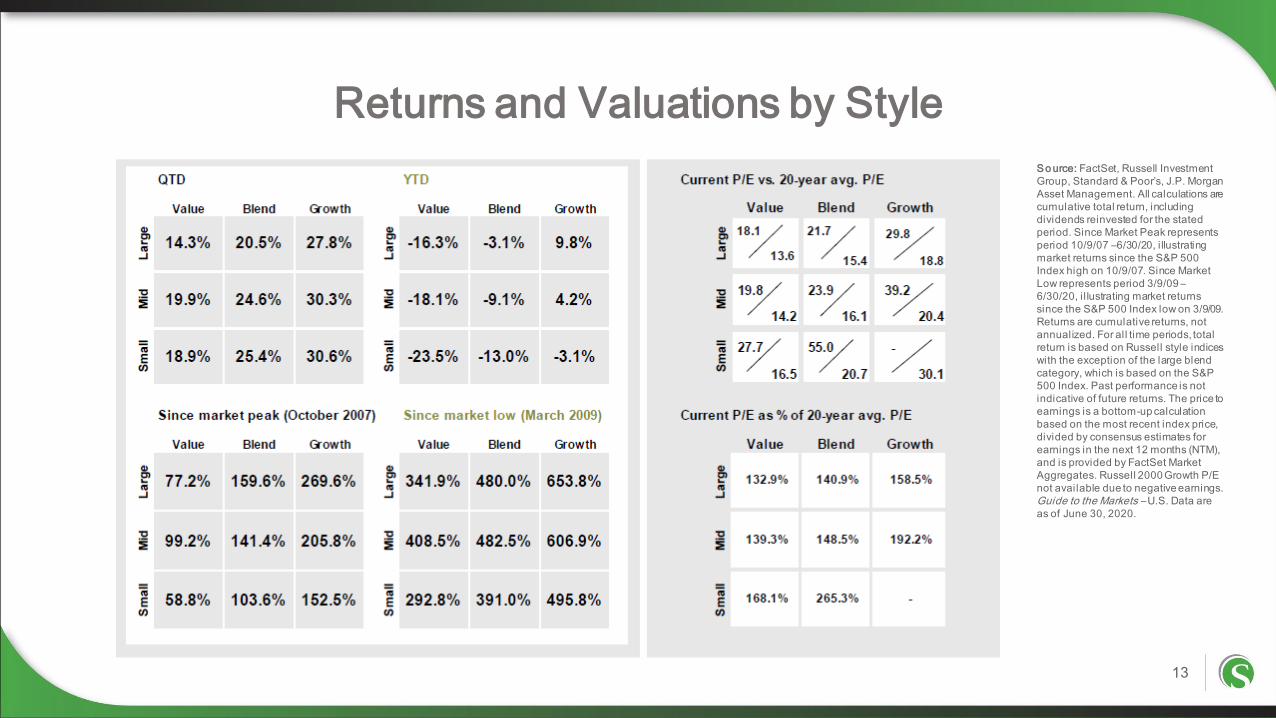

Returns and Valuations by Style

13

So urce: FactSet, Russell Investment

Group, Standard & Poor’s, J.P. Morgan

Asset Management. All calculations are

cumulative total return, including

dividends reinvested for the stated

period. Since Market Peak represents

period 10/9/07 –6/30/20, i llustrating

market returns since the S&P 500

Index high on 10/9/07. Since Market

Low represents period 3/9/09 –

6/30/20, i l lustrating market returns

since the S&P 500 Index low on 3/9/09.

Returns are cumulative returns, not

annualized. For all time periods, total

return is based on Russell style indices

with the exception of the large blend

category, which is based on the S&P

500 Index. Past performance is not

indicative of future returns. The price to

earnings is a bottom-up calculation

based on the most recent index price,

divided by consensus estimates for

earnings in the next 12 months (NTM),

and is provided by FactSet Market

Aggregates. Russell 2000 Growth P/E

not available due to negative earnings.

Guide to the Markets – U.S. Data are

as of June 30, 2020.

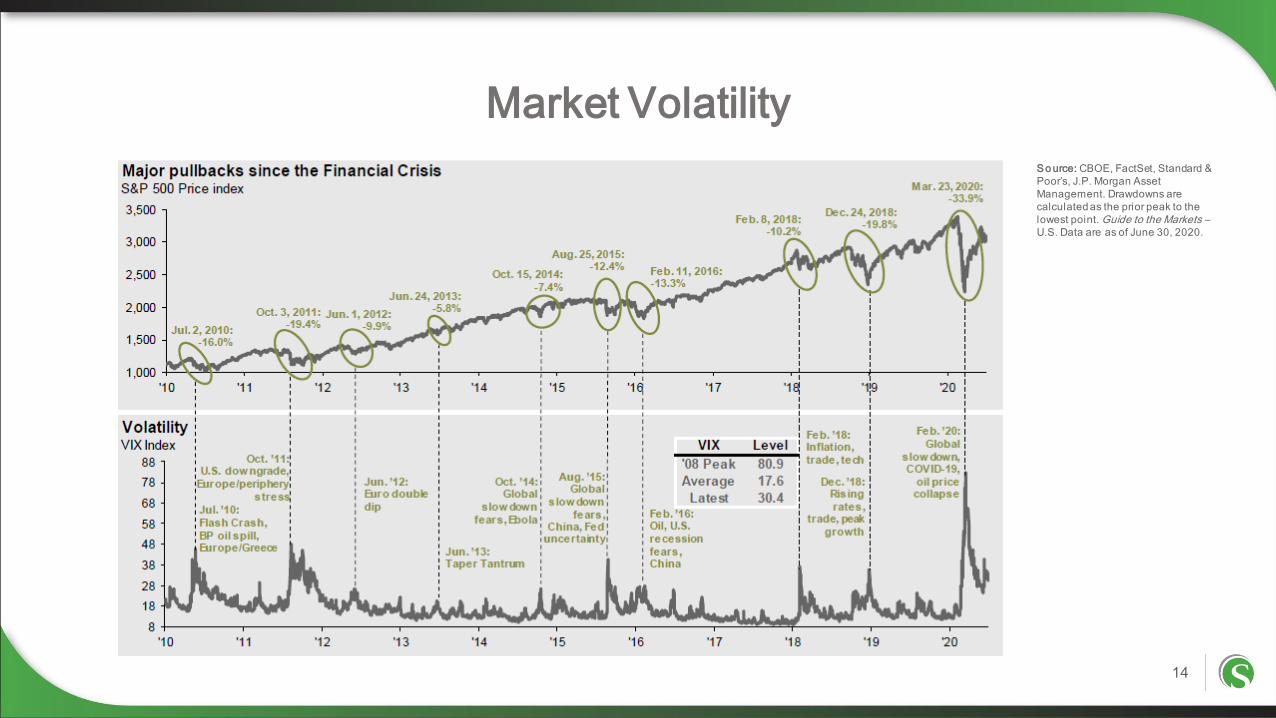

Market Volatility

14

So urce: CBOE, FactSet, Standard &

Poor’s, J.P. Morgan Asset

Management. Drawdowns are

calculated as the prior peak to the

lowest point. Guide to the Markets –U.S. Data are as of June 30, 2020.

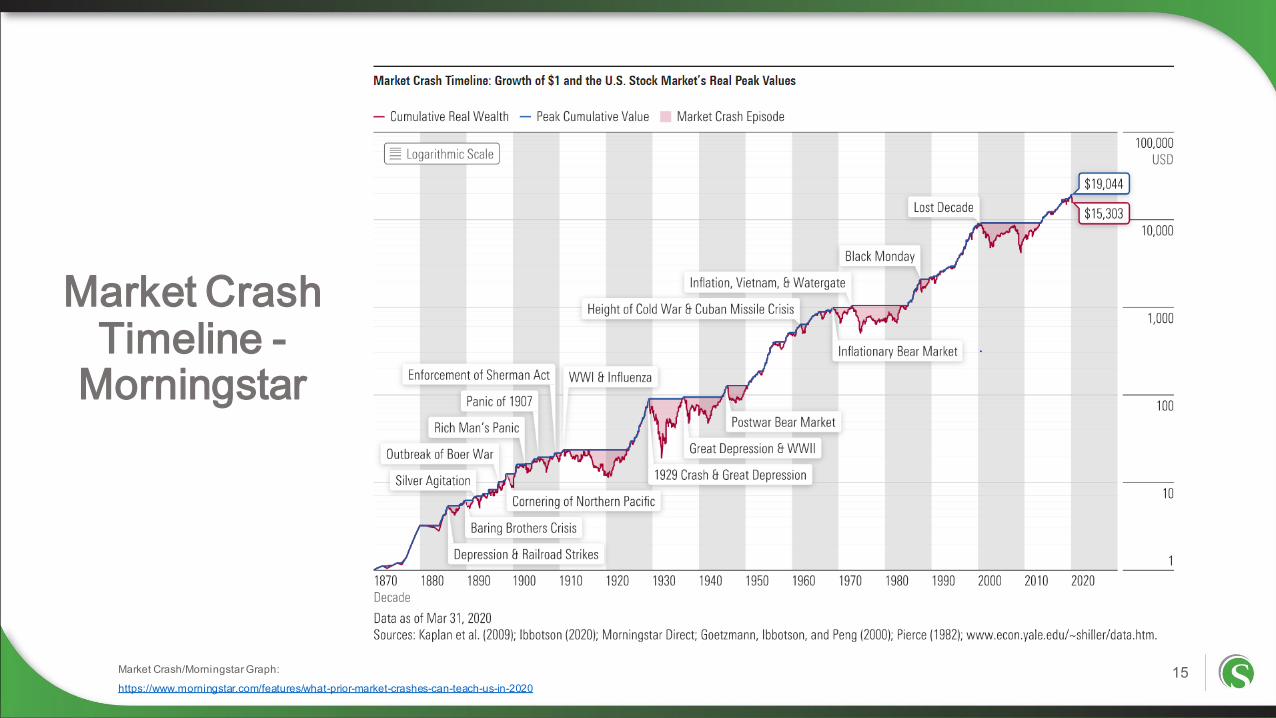

Market Crash Timeline -

Morningstar

15Market Crash/Morningstar Graph:

https://www.morningstar.com/features/what-prior-market-crashes-can-teach-us-in-2020

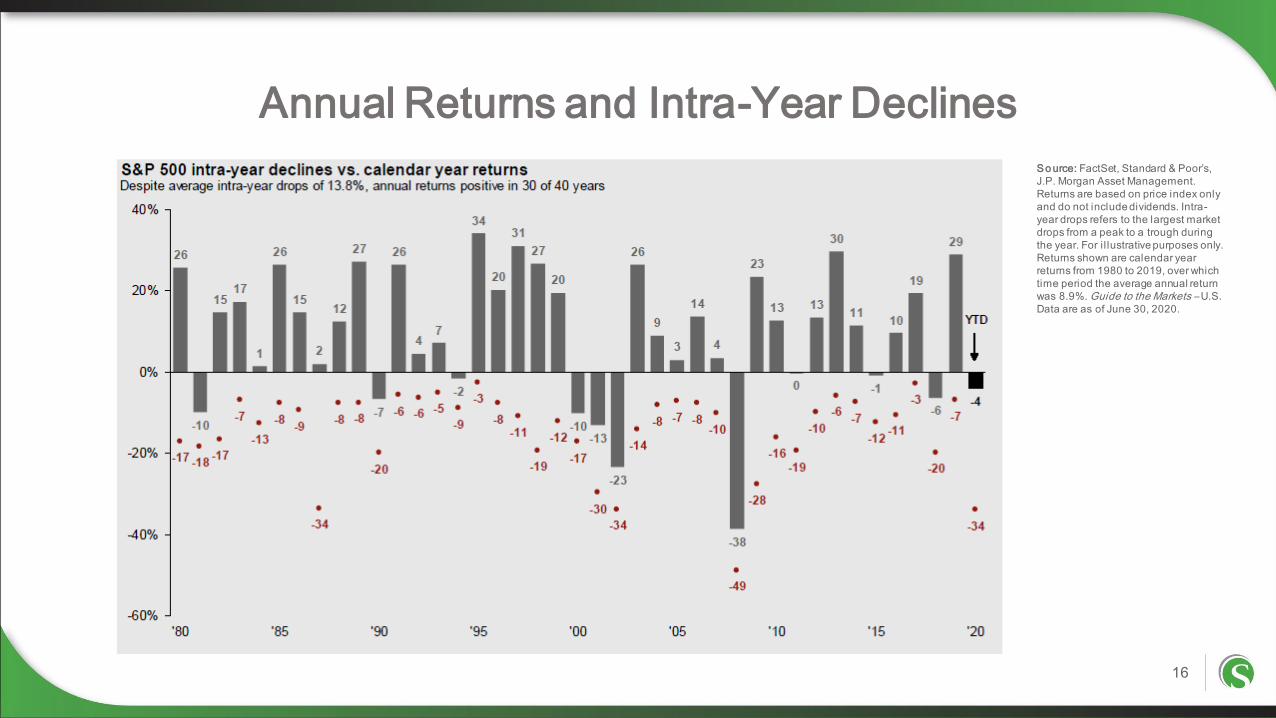

Annual Returns and Intra-Year Declines

16

So urce: FactSet, Standard & Poor’s,

J.P. Morgan Asset Management.

Returns are based on price index only

and do not include dividends. Intra-

year drops refers to the largest market

drops from a peak to a trough during

the year. For i l lustrative purposes only.

Returns shown are calendar year

returns from 1980 to 2019, over which

time period the average annual return

was 8.9%. Guide to the Markets – U.S.

Data are as of June 30, 2020.

17

What are we recommending?

Slightly defensive positioning given stock market rally since March low

Underweight International stocks relative to global benchmark

Re-balance periodically

Revisit investment strategy within the context of your overall financial plan

Financial Market Update

1. Prospective shape of the recovery? V, U, W, or L?

2. How is this different from other disasters?

3. What is the new paradigm?

4. How much will this really cost?

5. How will we pay for it?

6. What changes?

7. What are the second and third level effects of the crisis?

Questions

18

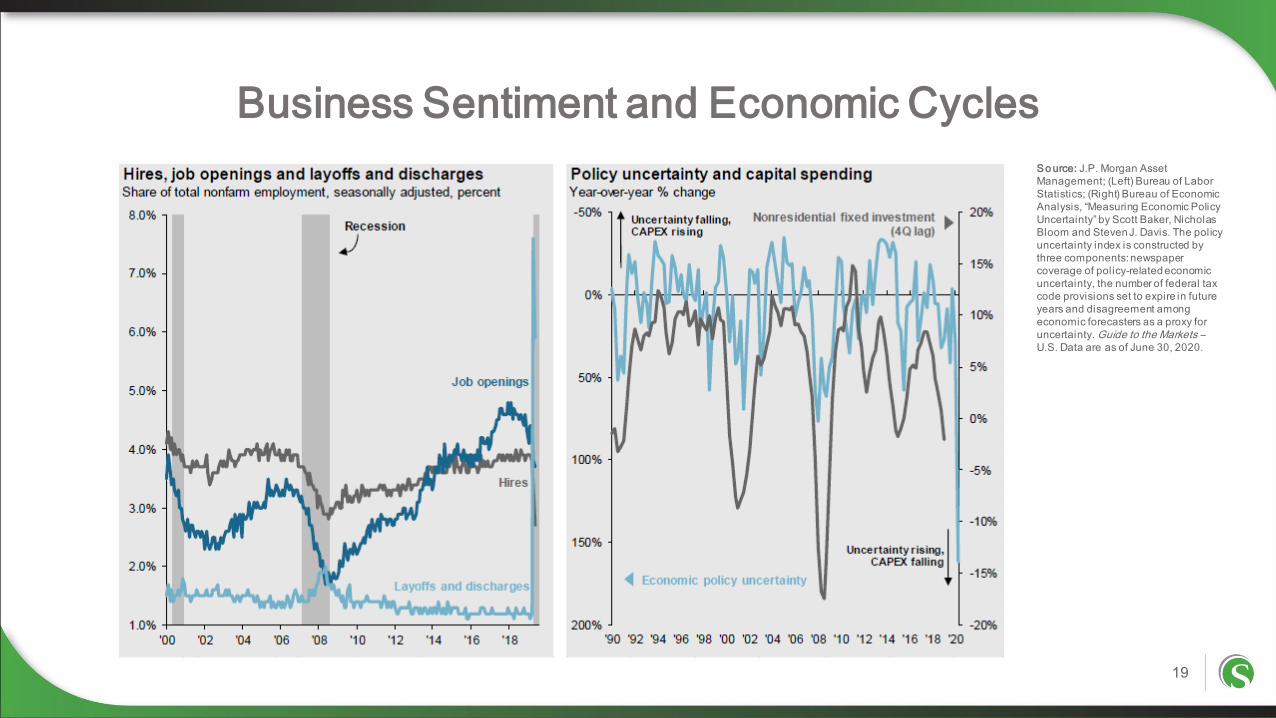

Business Sentiment and Economic Cycles

19

So urce: J.P. Morgan Asset

Management; (Left) Bureau of Labor

Statistics; (Right) Bureau of Economic

Analysis, “Measuring Economic Policy

Uncertainty” by Scott Baker, Nicholas

Bloom and Steven J. Davis. The policy

uncertainty index is constructed by

three components: newspaper

coverage of policy-related economic

uncertainty, the number of federal tax

code provisions set to expire in future

years and disagreement among

economic forecasters as a proxy for

uncertainty. Guide to the Markets –U.S. Data are as of June 30, 2020.

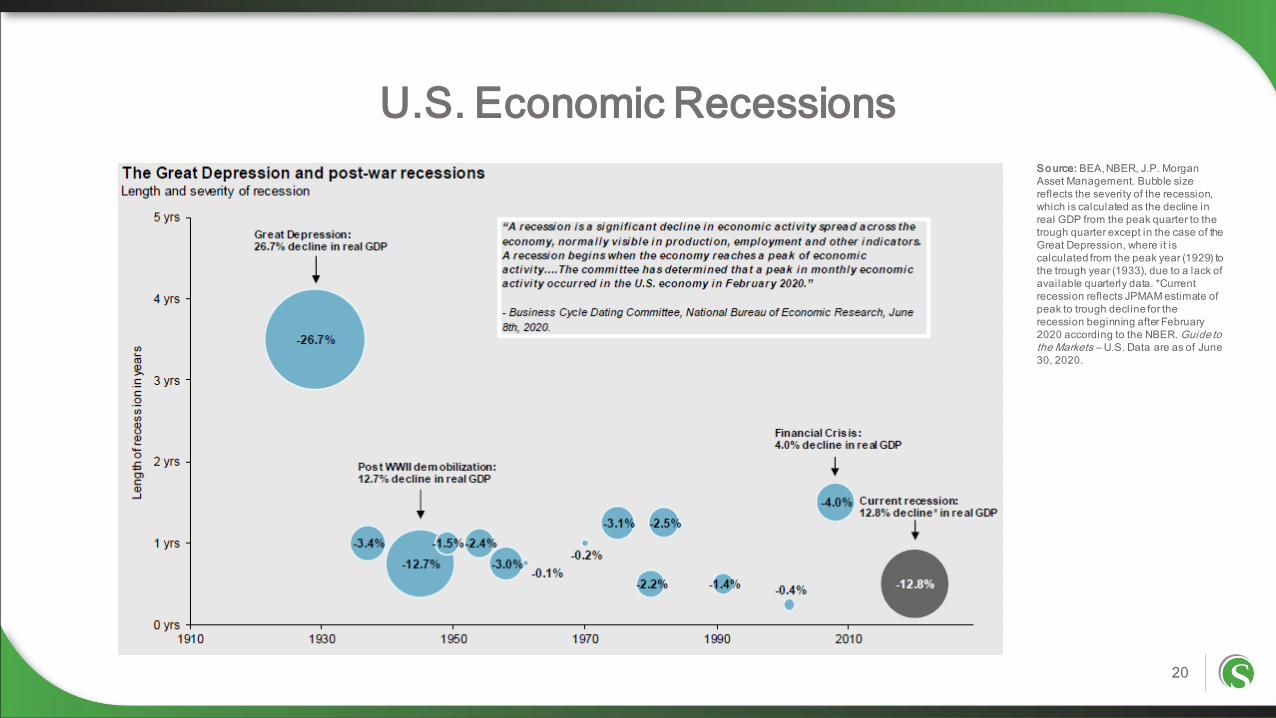

U.S. Economic Recessions

20

So urce: BEA, NBER, J.P. Morgan

Asset Management. Bubble size

reflects the severity of the recession,

which is calculated as the decline in

real GDP from the peak quarter to the

trough quarter except in the case of the

Great Depression, where it is

calculated from the peak year (1929) to

the trough year (1933), due to a lack of

available quarterly data. *Current

recession reflects JPMAM estimate of

peak to trough decline for the

recession beginning after February

2020 according to the NBER. Guide to the Markets – U.S. Data are as of June

30, 2020.

GDP/Per Capita PPP

21

Depression of 1920-21

Recession of 1937-38

Recession of 1949,

Fed Tightening

Recessio…

Beginning of WW1

Post WW1 Recession

The Great Depression

Beginning of WW2

Reduced Government

Spend from WW2

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

1910 1915 1920 1925 1930 1935 1940 1945 1950 1955

US GDP Data:

https://www.rug.nl/ggdc/historicaldevelopment/maddison/releases/maddison-project-database-2018

GDP/Per Capita PPP & Top Tax Bracket

22

Depression of 1920-21

Recession of 1937-38

Recession of 1949,

Fed Tightening

Recession of 1953

Beginning of WW1

Post WW1 Recession

The Great Depression

Beginning of WW2

Reduced Government

Spend from WW2

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

1910 1915 1920 1925 1930 1935 1940 1945 1950 1955

US Top Marginal Tax Rate Data:

https://fred.stlouisfed.org/series/IITTRHB

GDP/Per Capita PPP & Debt/GDP

23

Depression of 1920-21

Recession of 1937-38

Recession of 1949,

Fed Tightening

Recessio…

Beginning of WW1

Post WW1 Recession

The Great Depression

Beginning of WW2

Reduced Government

Spend from WW2

0%

20%

40%

60%

80%

100%

120%

140%

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

1910 1915 1920 1925 1930 1935 1940 1945 1950 1955

US Debt/GDP Data:

https://data.imf.org/?sk=806ED027-520D-497F-9052-63EC199F5E63&sId=1390030341854

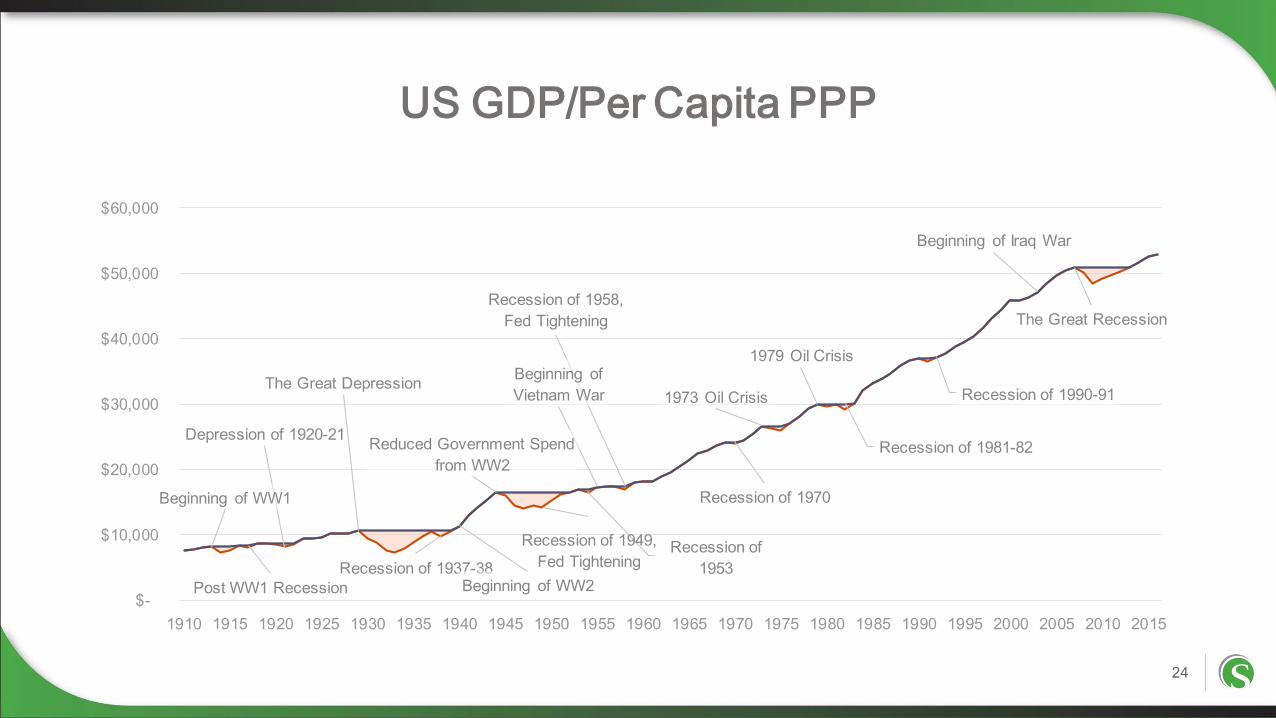

US GDP/Per Capita PPP

24

Depression of 1920-21

Recession of 1937-38

Recession of 1949,

Fed TighteningRecession of

1953

Beginning of WW1

Post WW1 Recession

The Great Depression

Beginning of WW2

Reduced Government Spend

from WW2

Beginning of

Vietnam War

Recession of 1958,

Fed Tightening

Recession of 1970

1973 Oil Crisis

1979 Oil Crisis

Recession of 1981-82

Recession of 1990-91

Beginning of Iraq War

The Great Recession

$-

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

1910 1915 1920 1925 1930 1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

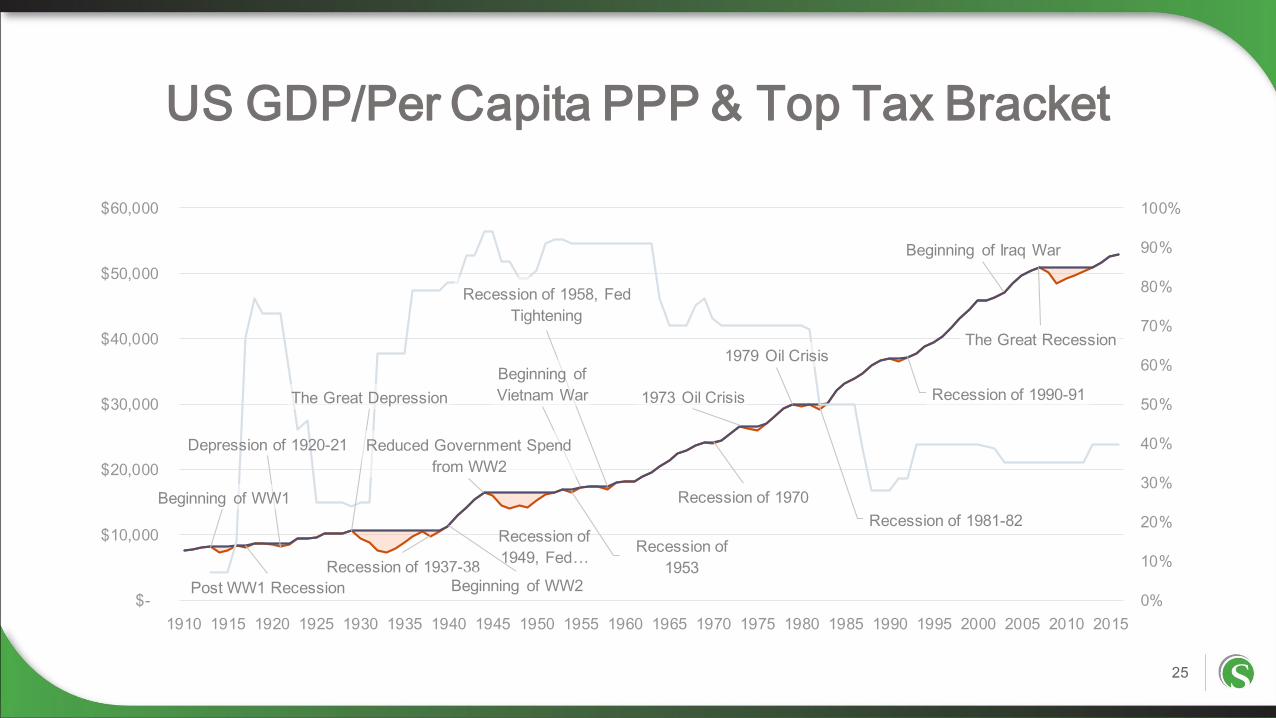

US GDP/Per Capita PPP & Top Tax Bracket

25

Depression of 1920-21

Recession of 1937-38

Recession of

1949, Fed …Recession of

1953

Beginning of WW1

Post WW1 Recession

The Great Depression

Beginning of WW2

Reduced Government Spend

from WW2

Beginning of

Vietnam War

Recession of 1958, Fed

Tightening

Recession of 1970

1973 Oil Crisis

1979 Oil Crisis

Recession of 1981-82

Recession of 1990-91

Beginning of Iraq War

The Great Recession

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$-

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

1910 1915 1920 1925 1930 1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

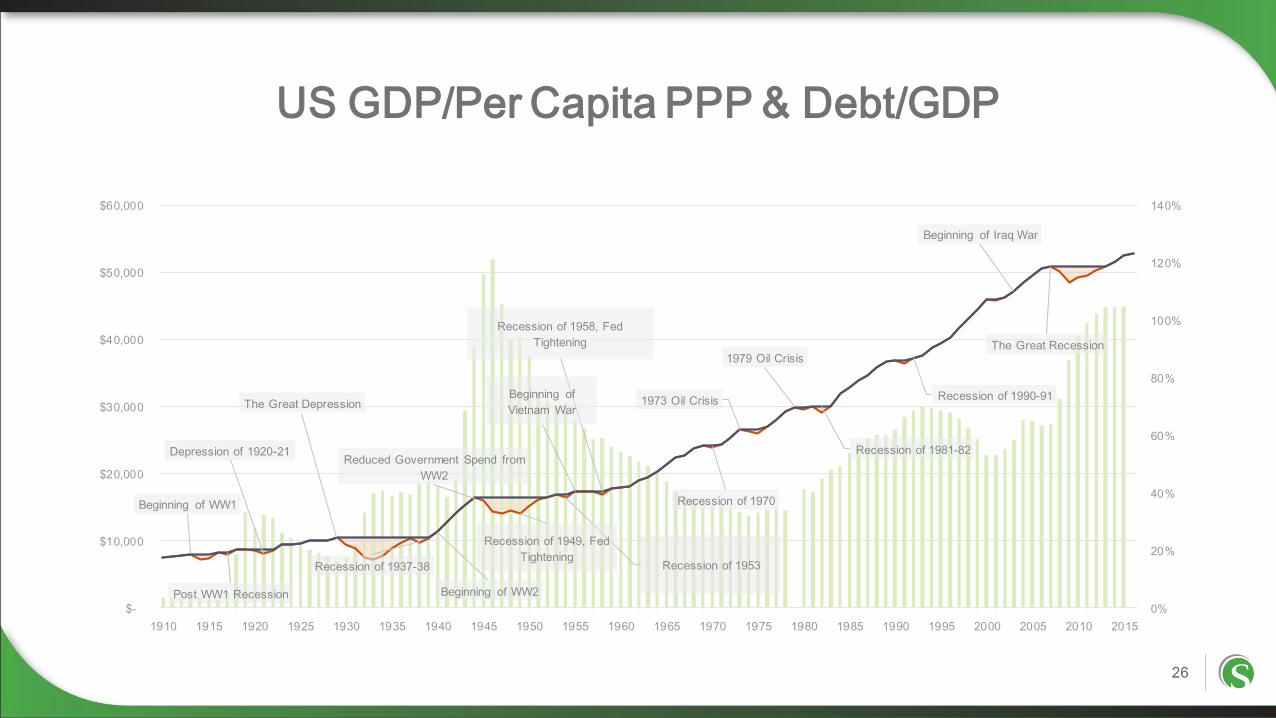

US GDP/Per Capita PPP & Debt/GDP

26

Depression of 1920-21

Recession of 1937-38

Recession of 1949, Fed

TighteningRecession of 1953

Beginning of WW1

Post WW1 Recession

The Great Depression

Beginning of WW2

Reduced Government Spend from

WW2

Beginning of

Vietnam War

Recession of 1958, Fed

Tightening

Recession of 1970

1973 Oil Crisis

1979 Oil Crisis

Recession of 1981-82

Recession of 1990-91

Beginning of Iraq War

The Great Recession

0%

20%

40%

60%

80%

100%

120%

140%

$-

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

1910 1915 1920 1925 1930 1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

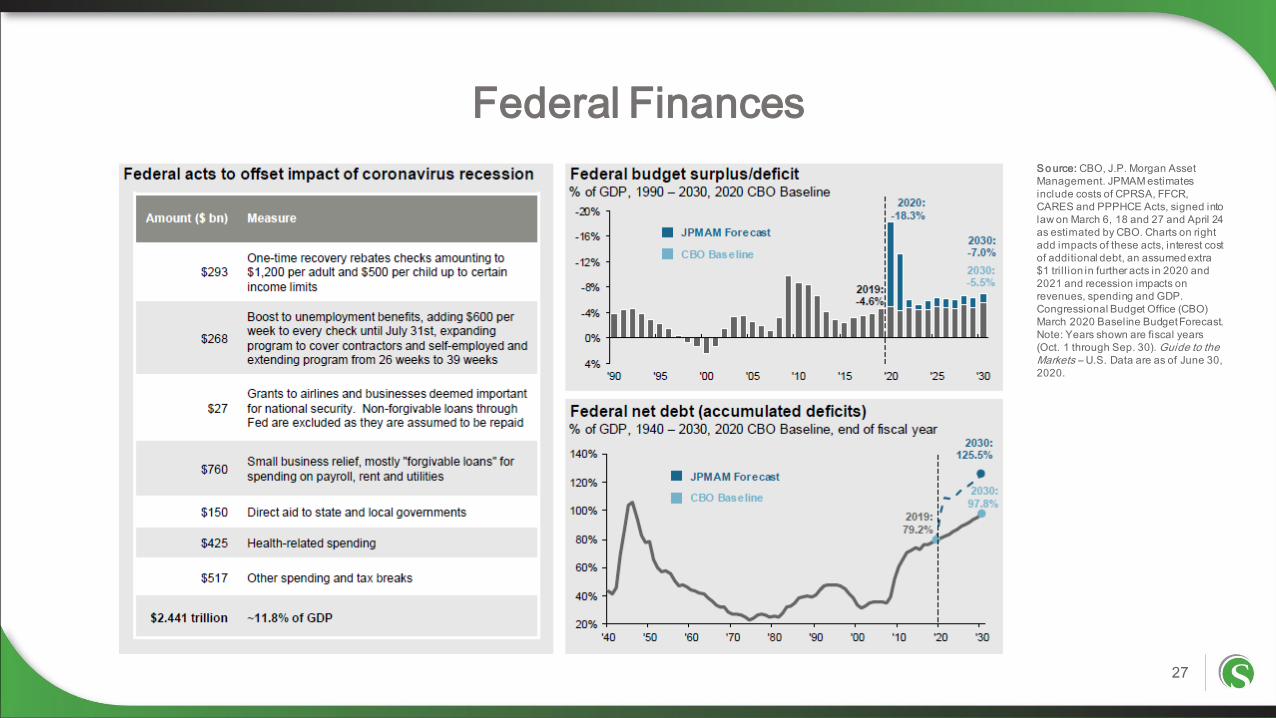

Federal Finances

27

So urce: CBO, J.P. Morgan Asset

Management. JPMAM estimates

include costs of CPRSA, FFCR,

CARES and PPPHCE Acts, signed into

law on March 6, 18 and 27 and April 24

as estimated by CBO. Charts on right

add impacts of these acts, interest cost

of additional debt, an assumed extra

$1 tri l l ion in further acts in 2020 and

2021 and recession impacts on

revenues, spending and GDP.

Congressional Budget Office (CBO)

March 2020 Baseline Budget Forecast.

Note: Years shown are fiscal years

(Oct. 1 through Sep. 30). Guide to the Markets – U.S. Data are as of June 30,

2020.

The Federal Reserve Balance Sheet

28

So urce: FactSet, Federal Reserve, J.P.

Morgan Investment Bank, J.P. Morgan

Asset Management. Currently, the

balance sheet contains $4.2 tri llion in

Treasuries and $1.9 tri l lion in MBS.

The end balance forecast is $4.7 tri llion

in Treasuries and $2.2 tri ll ion in MBS

by December 2020. *Balance sheet

forecast assumes the Federal Reserve

maintains its current pace of purchases

of Treasuries and MBS through

December 2020 as outlined in the June

2020 FOMC meeting. **Loans include

primary, secondary and seasonal

loans, maiden lane securities and

loans extended through newly

established corporate credit facilities.

Loan figures shown are max usage

over the QE period referenced and are

not growth of loan portfolio over the

period. ***QE4 is ongoing and the

expansion figures are as of the most

recent Wednesday close as reported

by the Federal Reserve. Guide to the Markets – U.S. Data are as of June 30,

2020.

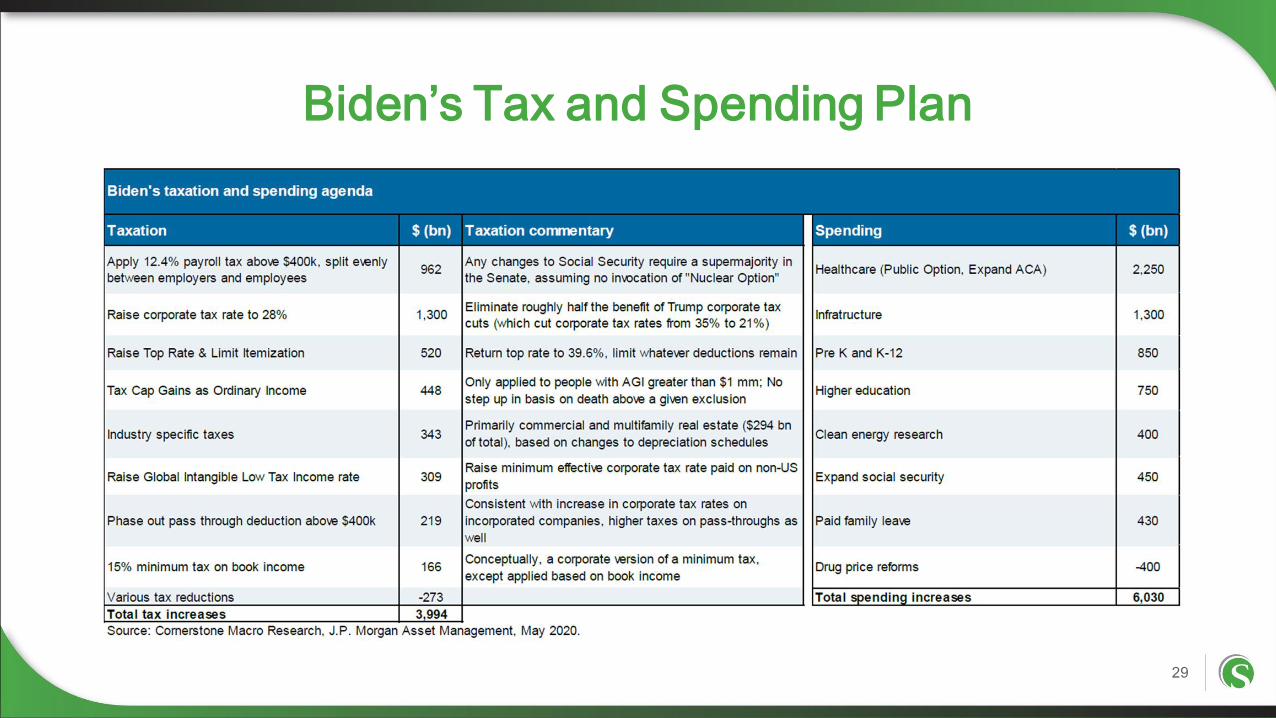

Biden’s Tax and Spending Plan

29

Comparison of Tax Plans

30

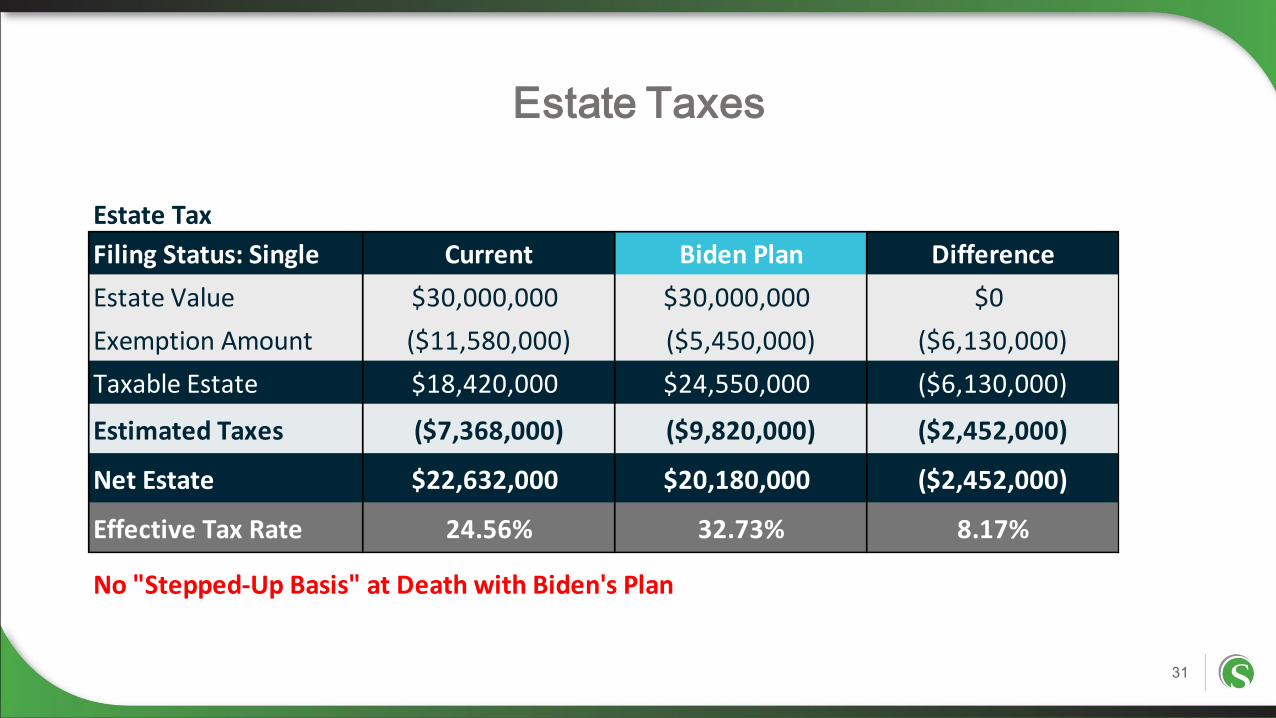

Estate Tax

Filing Status: Single Current Biden Plan Difference

Estate Value $30,000,000 $30,000,000 $0

Exemption Amount ($11,580,000) ($5,450,000) ($6,130,000)

Taxable Estate $18,420,000 $24,550,000 ($6,130,000)

Estimated Taxes ($7,368,000) ($9,820,000) ($2,452,000)

Net Estate $22,632,000 $20,180,000 ($2,452,000)

Effective Tax Rate 24.56% 32.73% 8.17%

No "Stepped-Up Basis" at Death with Biden's Plan

Estate Taxes

31

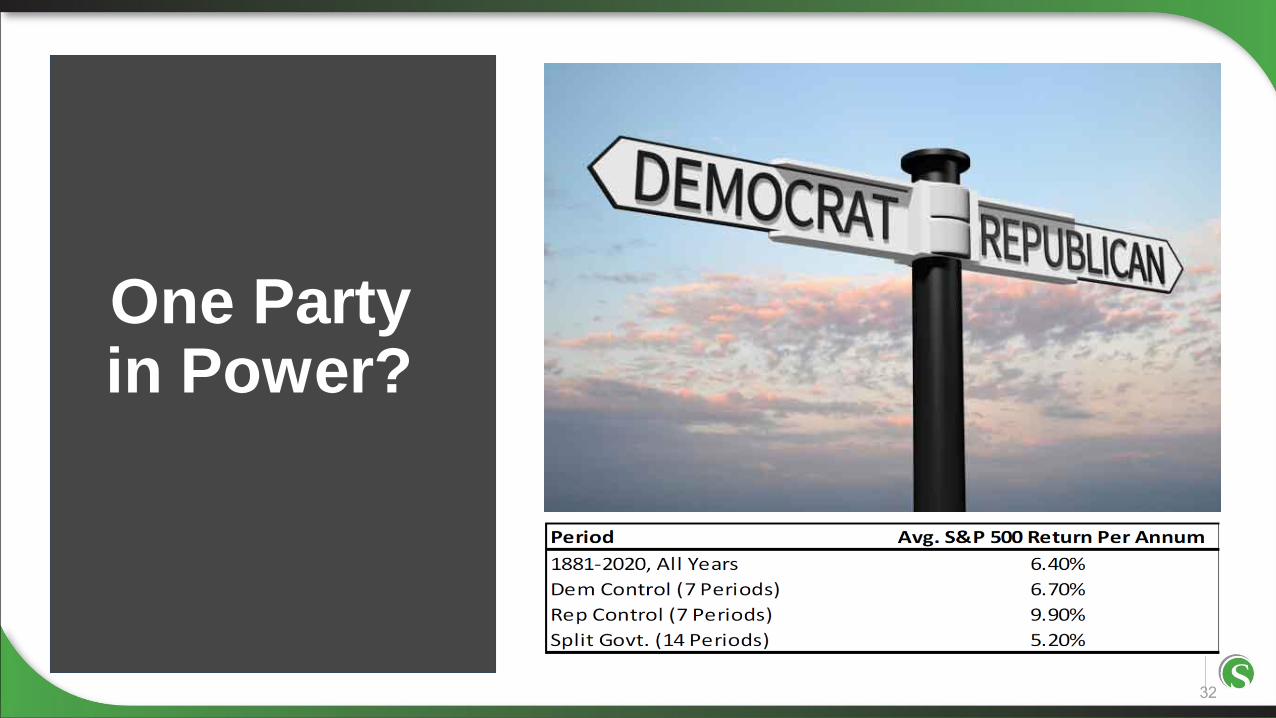

One Party in Power?

32

Extend your investment timeframe

Understand your liquidity needs

Evaluate capacity to shift your investment objective

Determine if current planning opportunities are a fit for you (ex., Roth conversions, intrafamily loans, wealth transfers)

The Intersection of Financial Planning

& Investment Strategy

33

34

Next Steps

Talk with your advisor

Review or establish your financial plan

Review your current investment strategy in the context of your plan

• Evaluate liquidity/cash buffer

• Analyze how you are invested based on what you are investing for

3535

Questions & Answers

FOR MORE INFORMATION VISIT:

COVID-19:

PODCAST:

TALK TO AN ADVISOR:

sequoia-financial.com/COVID-19-RESOURCES

sequoia-financial.com/PODCASTS

sequoia-financial.com/TALK

Leon LaBrecque

JD, CPA, CFP®, CFA

Chief Growth Officer

248.918.5905

Matt Pullar

Vice President, Private Client

Services

216.774.1192

This material does not constitute tax, legal, investment or any other type of professional advice. You should consult with a qualified tax, legal or financial advisor prior to making a decision. The financial instruments discussed in this brochure may not be suitable for all investors and investors must make their own investment decisions based upon their specific financial situations and investment objectives. Information has been obtained from sources believed to be reliable, but we do not guarantee their accuracy or completeness. While we have taken great care in the preparation of these materials, we cannot be responsible for clerical, computational, or other errors. Except where otherwise indicated herein, the information provided herein is based on matters as they exist as of the date of preparation, and may not be updated or otherwise revised to reflect information that subsequently becomes available, or changes occurring after the date hereof.

Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

©2020, Sequoia Financial Group, all rights reserved.

Disclosures

36

3500 Embassy Pkwy | Suite 100 | Akron, OH 44333

888.225.3777

sequoia-financial.com