the sixth carbon budget aviation

TRANSCRIPT

1

The Sixth Carbon Budget

Aviation

2

This document contains a summary of content for the aviation sector from the

CCC’s Sixth Carbon Budget Advice, Methodology and Policy reports.

3

The Committee is advising that the UK set its Sixth Carbon Budget (i.e. the legal limit

for UK net emissions of greenhouse gases over the years 2033-37) to require a

reduction in UK emissions of 78% by 2035 relative to 1990, a 63% reduction from

2019. This will be a world-leading commitment, placing the UK decisively on the

path to Net Zero by 2050 at the latest, with a trajectory that is consistent with the

Paris Agreement.

Our advice on the Sixth Carbon Budget, including emissions pathways, details on

our analytical approach, and policy recommendations for the aviation sector is

presented across three CCC reports, an accompanying dataset, and supporting

evidence.

• An Advice report: The Sixth Carbon Budget – The UK’s path to Net Zero,

setting out our recommendations on the Sixth Carbon Budget (2033-37)

and the UK’s Nationally Determined Contribution (NDC) under the Paris

Agreement. This report also presents the overall emissions pathways for the

UK and the Devolved Administrations and for each sector of emissions, as

well as analysis of the costs, benefits and wider impacts of our

recommended pathway, and considerations relating to climate science

and international progress towards the Paris Agreement. Section 7 of

Chapter 3 of that report contains an overview of the emissions pathways for

the aviation sector.

• A Methodology Report: The Sixth Carbon Budget – Methodology Report,

setting out the approach and assumptions used to inform our advice.

Chapter 8 of that report contains a detailed overview of how we

conducted our analysis for the aviation sector.

• A Policy Report: Policies for the Sixth Carbon Budget and Net zero, setting

out the changes to policy that could drive the changes necessary

particularly over the 2020s. Chapter 8 of that report contains our policy

recommendations for the aviation sector.

• A dataset for the Sixth Carbon Budget scenarios, which sets out more

details and data on the pathways than can be included in this report.

• Supporting evidence including our public Call for Evidence, 10 new

research projects, three expert advisory groups, and deep dives into the

roles of local authorities and businesses.

All outputs are published on our website (www.theccc.org.uk).

For ease, the relevant sections from the three reports for each sector (covering

pathways, method and policy advice) are collated into self-standing documents

for each sector. A full dataset including key charts is also available alongside this

document. This is the self-standing document for the aviation sector. It is set out in

three sections:

1) The approach to the Sixth Carbon Budget analysis for the aviation sector

2) Emissions pathways for the aviation sector

3) Policy recommendations for the aviation sector

The approach to the Sixth Carbon

Budget analysis for the aviation

sector

5 Sixth Carbon Budget - Aviation

The following sections are taken directly from Chapter 8 of the CCC’s

Methodology Report for the Sixth Carbon Budget.1

Introduction and key messages

This chapter sets out the method for the aviation sector’s Sixth Carbon Budget

pathways.

The scenario results of our costed pathways are set out in the accompanying

Advice report. Policy implications are set out in the accompanying Policy report.

For ease, these sections covering pathways, method and policy advice for the

aviation sector are collated in The Sixth Carbon Budget – Aviation. A full dataset

including key charts is also available alongside this document.

The key messages from this chapter are:

• Background. Aviation emissions accounted for 7% of UK GHG emissions in

2018 and were 88% above 1990 levels. Emissions have been relatively flat

from 2008-2018, with increasing international travel being offset by some

improvements in efficiencies and by falling military and domestic aviation

emissions. 2020 has likely seen a drop in GHG emissions of over 60% from

2019, due to the impact of COVID-19, with a return to pre-pandemic

passenger levels not expected until 2024.2

• Options for reducing emissions. Mitigation options considered include

demand management, improvements in aircraft efficiency (including use

of hybrid electric aircraft), and use of sustainable aviation fuels (biofuels,

biowaste to jet and synthetic jet fuels) to displace fossil jet fuel.

• Analytical approach. Our starting point for this analysis has been the 2019

Net Zero report, and the underlying DfT demand, efficiency and emissions

modelling.

– We have adapted and updated this analysis to fit to a new set of

demand scenarios (consistent with those considered by the Climate

Assembly), before introducing significantly higher shares of sustainable

aviation fuels than previously considered.

– This includes new evidence on the costs and emissions savings of

sustainable aviation fuels, fitting with our Fuel Supply analysis, and the

added capital costs of efficiency improvements.

• Uncertainty. We have used the scenario framework to test the impacts of

uncertainties, to inform our balanced Net Zero Pathway. The key areas of

uncertainty we test relate to sustainable aviation fuel supplies and costs of

synthetic jet fuel, the mix of SAF options, the profile for expansion in

passenger demand over time (with mid-term or no net expansion of

airports), and whether there will be long-term structural change in the

sector due to COVID-19. Out of all the CCC’s sectors, Aviation has been

most impacted by COVID-19, and continues to face the highest

uncertainties about the future size of the sector.

We set out our analysis in the following sections:

1. Sector emissions

2. Options for reducing emissions

3. Approach to analysis for the Sixth Carbon Budget

Sixth Carbon Budget - Aviation 6

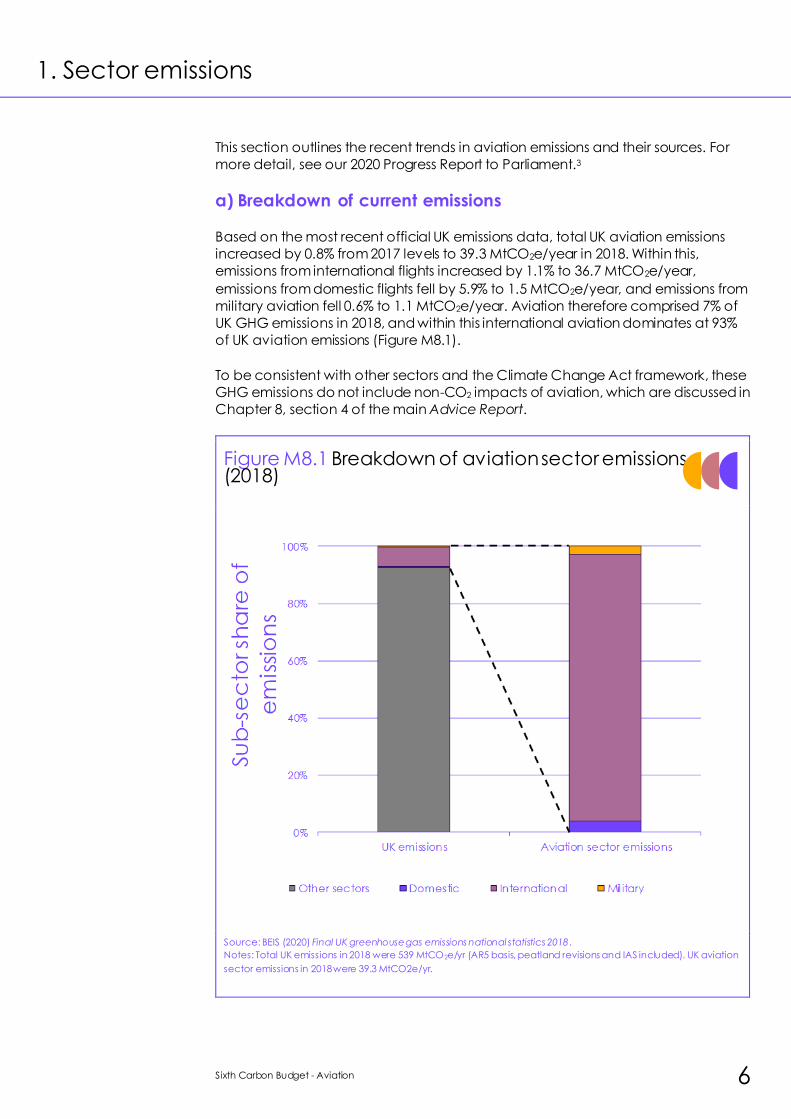

1. Sector emissions

This section outlines the recent trends in aviation emissions and their sources. For

more detail, see our 2020 Progress Report to Parliament.3

a) Breakdown of current emissions

Based on the most recent official UK emissions data, total UK aviation emissions

increased by 0.8% from 2017 levels to 39.3 MtCO2e/year in 2018. Within this,

emissions from international flights increased by 1.1% to 36.7 MtCO2e/year,

emissions from domestic flights fell by 5.9% to 1.5 MtCO2e/year, and emissions from

military aviation fell 0.6% to 1.1 MtCO2e/year. Aviation therefore comprised 7% of

UK GHG emissions in 2018, and within this international aviation dominates at 93%

of UK aviation emissions (Figure M8.1).

To be consistent with other sectors and the Climate Change Act framework, these

GHG emissions do not include non-CO2 impacts of aviation, which are discussed in

Chapter 8, section 4 of the main Advice Report.

Figure M8.1 Breakdown of aviation sector emissions (2018)

Source: BEIS (2020) Final UK greenhouse gas emissions national statistics 2018.

Notes: Total UK emissions in 2018 were 539 MtCO2e/yr (AR5 basis, peatland revisions and IAS included). UK aviation

sector emissions in 2018 were 39.3 MtCO2e/yr.

7 Sixth Carbon Budget - Aviation

We have also estimated UK aviation emissions for 2019 at 39.6 MtCO2e/year, a 0.9%

increase on 2018 levels. This combines 11% falls in domestic and military emissions

with a 1.7% increase in international aviation emissions.

However, given the COVID-19 pandemic and its impact on the aviation sector,

and the need to reflect this in our analysis in the near-term, we have also

estimated a fall in 2020 GHG emissions of over 60% from 2019 levels (and then a

recovery to 2024), as detailed below in section 3(e). The emissions estimates from

2019 onwards will revised once official BEIS final GHG emissions data is published.

b) Emissions trends and drivers The breakdown of aviation emissions since 1990 is shown in Figure M8.2. Overall,

emissions from domestic and international aviation in 2018 were 124% above 1990

levels, and military aviation emissions have fallen 71% from 1990 levels.

Figure M8.2 Breakdown of aviation sector emissions (1990-2019)

Source: BEIS (2020) Final UK greenhouse gas emissions national statistics 2018; BEIS (2020) Provisional UK greenhouse

gas emissions national statistics 2019; BEIS (2020) Energy Trends; CCC estimates for 2019.

Aviation emissions rose strongly throughout the 1990s and early-to-mid 2000s, due

to increasing passenger demand, with only minor falls seen around 1990 and 2000

due to economic down-turns.

Emissions fell significantly during 2007-2010 due to the financial crisis, then stayed

relatively flat in the early 2010s, but have been rising again in recent years.

Sixth Carbon Budget - Aviation 8

UK aviation emissions in 2018 were therefore the same as in 2008, as falls in

domestic and military aviation emissions have been balanced by a rise in UK

international aviation emissions. Over the same 2008-2018 period, the total number

of UK terminal passengers rose by 24% to reach 292 million in 2018, with a further 2%

increase seen in 2019.

The increase in emissions has been more modest than growth in passengers due to

increased plane loadings, decreases in average flight distance (due to faster

growth in flights to the EU than other international destinations) and some

improvements in fleet efficiency.

9 Sixth Carbon Budget - Aviation

2. Options for reducing emissions

Several different emissions reduction options have been explored within the

Aviation sector. These include:

• Demand management. A reduction in the annual number of passengers

versus a counterfactual with unlimited passenger demand growth.

Demand management policies could take several forms, either reducing

passenger demand for flying through carbon pricing, a frequent flyer levy,

fuel duty, VAT or reforms to Air Passenger Duty, and/or restricting the

availability of flights through management of airport capacity. Our analysis

only assumes a demand profile is achieved, and does not model the

policies required to achieve these profiles.

• Aircraft fleet-efficiency improvements, achieved via a combination of

airspace modernisation, operational optimisation, aircraft passenger

loadings, aircraft design and new engine efficiency improvements, as well

as introduction of hybrid electric aircraft (significant falls in jet use, but

adding some use of electricity via on-board batteries and motors). Our

analysis uses fleet fuel tCO2/passenger values from DfT modelling, and does

not model individual improvements from the list above.

• Sustainable aviation fuels (SAF). These are “drop-in” replacements for fossil

jet fuel, meeting international fuel specifications (and currently allowed to

be blended at up to 50% by volume), and have nil accounting CO2

emissions on combustion. SAF production routes considered include:

– Biomass to Fischer-Tropsch (FT) biojet, with or without CCS;

– Biogenic waste fats/oils to Hydroprocessed Esters and Fatty Acids

(HEFA) biojet;

– Biogenic fraction of waste* to Fischer-Tropsch (FT) biojet, with or

without CCS; and

– Synthetic jet fuel produced via Direct Air Capture (DAC) of CO2

and low-carbon H2.

Our analysis uses these four SAF options to displace fossil jet fuel, and each

SAF option has its own deployment and cost profile, based on the

availability of the feedstocks, efficiencies, input energy, capital and

operating costs. Each route is discussed in more detail in the Fuel Supply

chapter.

* Note that the non-biogenic fraction of waste converted to FT jet will still have fossil accounting CO2 emissions on

combustion in aviation, and so is included within fossil jet fuel figures, not as SAF.

Sixth Carbon Budget - Aviation 10

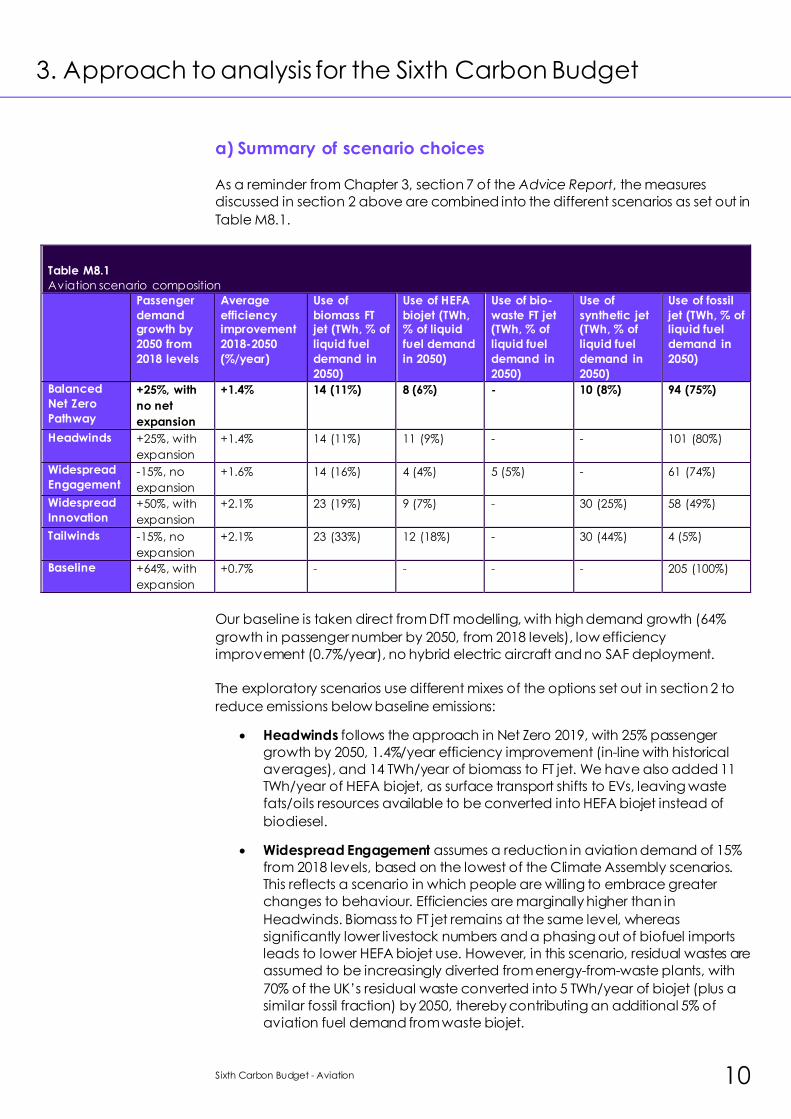

3. Approach to analysis for the Sixth Carbon Budget

a) Summary of scenario choices

As a reminder from Chapter 3, section 7 of the Advice Report, the measures

discussed in section 2 above are combined into the different scenarios as set out in

Table M8.1.

Table 1.11:Table 1.11

Table M8.1

Aviation scenario composition

Passenger

demand growth by

2050 from

2018 levels

Average

efficiency improvement

2018-2050

(%/year)

Use of

biomass FT jet (TWh, % of

liquid fuel

demand in

2050)

Use of HEFA

biojet (TWh, % of liquid

fuel demand

in 2050)

Use of bio-

waste FT jet (TWh, % of

liquid fuel

demand in

2050)

Use of

synthetic jet (TWh, % of

liquid fuel

demand in

2050)

Use of fossil

jet (TWh, % of liquid fuel

demand in

2050)

Balanced

Net Zero

Pathway

+25%, with

no net

expansion

+1.4% 14 (11%) 8 (6%) - 10 (8%) 94 (75%)

Headwinds +25%, with

expansion

+1.4% 14 (11%) 11 (9%) - - 101 (80%)

Widespread

Engagement -15%, no

expansion

+1.6% 14 (16%) 4 (4%) 5 (5%) - 61 (74%)

Widespread

Innovation +50%, with

expansion

+2.1% 23 (19%) 9 (7%) - 30 (25%) 58 (49%)

Tailwinds -15%, no

expansion

+2.1% 23 (33%) 12 (18%) - 30 (44%) 4 (5%)

Baseline +64%, with

expansion

+0.7% - - - - 205 (100%)

Our baseline is taken direct from DfT modelling, with high demand growth (64%

growth in passenger number by 2050, from 2018 levels), low efficiency

improvement (0.7%/year), no hybrid electric aircraft and no SAF deployment.

The exploratory scenarios use different mixes of the options set out in section 2 to

reduce emissions below baseline emissions:

• Headwinds follows the approach in Net Zero 2019, with 25% passenger

growth by 2050, 1.4%/year efficiency improvement (in-line with historical

averages), and 14 TWh/year of biomass to FT jet. We have also added 11

TWh/year of HEFA biojet, as surface transport shifts to EVs, leaving waste

fats/oils resources available to be converted into HEFA biojet instead of

biodiesel.

• Widespread Engagement assumes a reduction in aviation demand of 15%

from 2018 levels, based on the lowest of the Climate Assembly scenarios.

This reflects a scenario in which people are willing to embrace greater

changes to behaviour. Efficiencies are marginally higher than in

Headwinds. Biomass to FT jet remains at the same level, whereas

significantly lower livestock numbers and a phasing out of biofuel imports

leads to lower HEFA biojet use. However, in this scenario, residual wastes are

assumed to be increasingly diverted from energy-from-waste plants, with

70% of the UK’s residual waste converted into 5 TWh/year of biojet (plus a

similar fossil fraction) by 2050, thereby contributing an additional 5% of

aviation fuel demand from waste biojet.

11 Sixth Carbon Budget - Aviation

• Widespread Innovation assumes demand growth of 50% from 2018 levels,

based on the highest demand amongst the preferred Climate Assembly

scenarios. Efficiencies are much higher, based on the DfT scenario

selected. More biomass is assumed to be diverted to FT biojet, along with

HEFA biojet making up ~25% of supply, and the other 25% of the fuel mix is

assumed to be made up of synthetic jet fuel. We did not increase the

blending of synthetic jet fuel above 25% due to the high costs of synthetic

jet fuel, and the high penetration of biomass to hydrogen in the

Widespread Innovation scenario (where it would be more efficient to make

biojet direct from the biomass, rather than via a hydrogen intermediary).

However, the overall choices fit with the overall scenario design philosophy

of maximal technical change.

• Tailwinds combines the most stretching of the scenarios above – a

reduction in demand, high efficiency, and the maximal resource

allocations for the biojet and synthetic jet fuel from the other scenarios.

Waste to jet has not been included, as the remaining energy-from-waste

(EfW) plants in our analysis all retrofit CCS before 2050, ensuring 95%

capture of the fossil & biogenic carbon. However, putting the residual

waste instead into new jet production plants with CCS would likely lead to

a very similar outcome in terms of GHG emissions.*

Our scenario for the Balanced Net Zero Pathway takes elements from each of the

above pathways:

• Demand growth: Our demand growth by 2050 matches Headwinds at 25%,

although the passenger growth profile is more gradual due to an

assumption of no net capacity expansion at UK airports in this scenario. This

arises as a function of 2050 passenger numbers (365 million passengers)

being within current UK airport capacities (at least 370 million passengers),

and the need to ensure the UK achieves Net Zero by 2050 with aviation still

one of the largest emitting sectors. We therefore do not assume a surge in

emissions occurs in the early 2030s, as happens with the airport expansion

modelled in the Headwinds and Widespread Innovation scenarios. Airport

expansion could still occur under the Balanced Pathway, but would require

capacity restrictions elsewhere in the UK (i.e. effectively a reallocation of

airport capacity).

Box M8.1

Climate Assembly scenarios

The Climate Assembly debated five aviation scenarios, with changes in demand from

2018 to 2050 of -15%, +20%, +25%, +50% and +65%. Growth of 65% growth was highly

unpopular - a majority wanted to see a 25-50% growth in flights, with the higher end of the

range acceptable if technology was developed to mitigate the additional emissions.

However, the weighted average of scenario Borda votes was +24% growth, and the

report also noted that a majority voted for +25% growth or less. This gives added

confidence that the required demand management to keep the Balanced Net Zero

Pathway to only 25% growth by 2050 would be acceptable to the UK general pub lic.

Source: Climate Assembly UK (2020); CCC analysis.

* This assumes that jet production is maximised and that other co-products (e.g. diesel, LPG) also still displace fossil fuels

(increasingly difficult to 2050 as other sector counterfactuals decarbonise); and that EfW plants with CCS are

displacing grid electricity with zero emissions by 2050 (rather than displacing fossil gas with CCS plants).

Sixth Carbon Budget - Aviation 12

• Efficiency: The Balanced Net Zero Pathway takes the same efficiency

assumptions as in the Headwinds scenario, in line with historical average

improvement.

• SAF: Use of SAF matches Headwinds and Widespread Engagement for

biomass to FT jet, and similar assumptions are taken on HEFA biojet (with

slight differences due to waste fats/oils availability). Our Balanced Net Zero

Pathway also assumes some synthetic jet fuels might be available in 2040s,

at one third of the level deployed in the Widespread Innovation scenario,

due to the higher costs of hydrogen and Direct Air Capture in the Balanced

Net Zero Pathway compared to the Widespread Innovation scenario.

Similar to the Tailwinds scenario, we have not allocated residual waste to

jet fuel in this scenario.

The resulting GHG emissions in the Balanced Pathway grow during 2021-2023 with

the return in passenger numbers post-COVID, before flat demand, efficiency

measures and the start of SAF deployment lead to falls in emissions to the early

2030s. The more back-ended passenger growth in the Balanced Pathway

(compared to Headwinds) has passenger numbers starting to grow from the mid-

2030s, meaning that emissions continue to decline to 2040, as this later passenger

growth is able to be accommodated by further improvements in efficiency and

the continued uptake of SAF (compared to emissions increasing in Headwinds in

the early 2030s with earlier passenger growth). The Balanced Pathway therefore

only sees growth in passenger numbers towards 2050 once SAF is commercially

proven and contributing at scale (in this scenario, there is 8% SAF used in 2035,

increasing at slightly above 1 percentage point a year). From 2040, DfT modelling

then introduces a new generation of aircraft (including the start of hybrid electric

aircraft) that lead to further falls in emissions, with continued SAF uptake and

passenger numbers continuing to increase to 2050.

Aviation measures reduce sector emissions to 23 MtCO2e/year by 2050 in the

Balanced Pathway, and all scenarios have positive emissions. The aviation sector

will therefore require significant amounts of GHG removals to be developed to

offset an increasing proportion of the sector’s (declining) gross emissions to 2050,

and aviation is therefore likely to be a key driving force behind the long-term

deployment of engineered removals.

b) Sector classifications

Note that with our current sector classifications, some emissions reduction options

have been counted outside of the CCC’s Aviation sector, even if these emissions

reductions are achieved via aviation policy and could count towards a separate

Net Zero goal for the sector. For example:

• Sequestering biogenic CO2 by installing CCS on UK biojet production

facilities is counted within the CCC’s engineered GHG removals sector, as

a form of bioenergy with CCS (BECCS).

• Airlines paying for Direct Air Capture with CCS (DACCS) in the UK, in order

to offset their remaining aviation gross emissions, is also counted within

CCC’s engineered GHG removals sector.

• Airlines paying for tree planting in the UK, in order to offset their remaining

aviation gross emissions, is counted within CCC’s Land Use, Land Use

Change & Forestry (LULUCF) sinks sector.

13 Sixth Carbon Budget - Aviation

These do not constitute recommendations on emissions accounting, merely what

we have assumed for this analysis. These ‘negative emissions’ options are discussed

in greater detail in the LULUCF and engineered GHG removals chapters.

This CCC sector classification also means that whilst some SAF fuels can be strongly

carbon-negative on a lifecycle basis at the point of use (e.g. if there is upstream

biogenic CCS involved in their production), our Aviation sector analysis only

considers the direct accounting CO2 emissions from the use of SAF in the sector, i.e.

nil and not negative. If an alternative accounting methodology were followed, the

negative emissions from upstream biogenic CCS could be counted within the

Aviation sector emissions, but then these upstream negative emissions would have

to be excluded from the GHG removals or LULUCF sinks sector to avoid double-

counting. Overall, these discussions reflect emissions accounting classifications and

do not affect aggregate UK emissions.

The residual aviation emissions in the Widespread Innovation scenario are used to

calculate the Direct Air Capture with CCS requirement (14.5 MtCO2/year) in both

the Widespread Innovation scenario and the Tailwinds scenario. DACCS costs,

energy inputs and deployment profiles are discussed in the GHG removals sector.

c) Analytical steps

The aviation analysis for the Sixth Carbon Budget advice consists of the following

steps:

• Coverage.

– Aviation is split into three sub-sectors: domestic, international and

military.

– Emissions cover CO2, N2O and CH4.

– Coverage is for UK, Scotland, Wales and Northern Ireland.

• Abatement measures are split into three types: demand, efficiency

(including hybrids) and SAF.

– Domestic and international passenger demand and fuel use

trajectories to 2050 are sourced from DfT aviation modelling,

thereby incorporating DfT efficiency assumptions.

– Trajectory start points were adjusted for 2015-2019 actual NAEI4

and CCA data5, and estimated COVID-19 impacts in 2020-23

(discussed below), and trajectories then re-scaled to meet

passenger growth targets for 2050 (discussed above).

– The domestic share of DfT fuel use increases from 3.4% today to

3.9% by 2050. Military fuel use is derived separately from NAEI4

and held fixed to 2050. Freight flights are included within DfT

trajectories, so are implicitly assumed to scale with CCC

passenger profiles.

– SAF deployments from the CCC’s Fuel Supply sector modelling

are used to calculate residual fossil jet demands, with the same

SAF % blend assumed to be used in each sub-sector (including in

military aviation).

– Direct accounting CO2, CH4 and N2O emissions are calculated

based on fuel use, then split into sub-sectors and DAs (discussed

below).

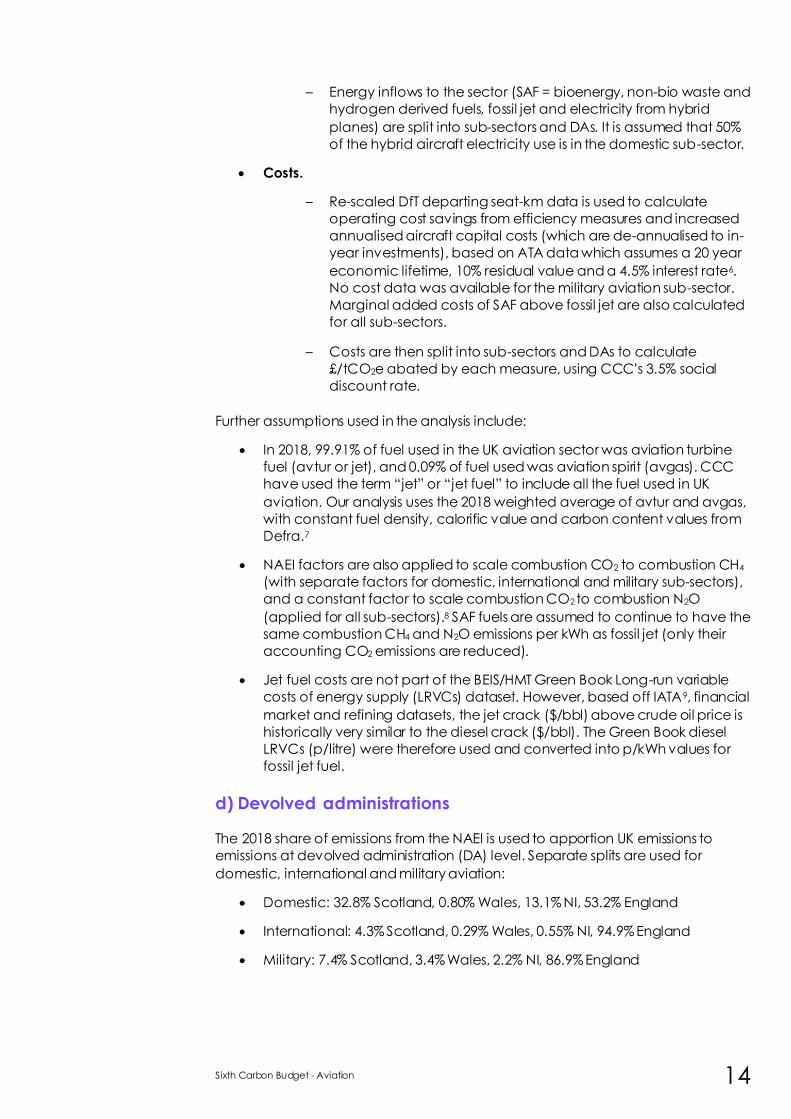

Sixth Carbon Budget - Aviation 14

– Energy inflows to the sector (SAF = bioenergy, non-bio waste and

hydrogen derived fuels, fossil jet and electricity from hybrid

planes) are split into sub-sectors and DAs. It is assumed that 50%

of the hybrid aircraft electricity use is in the domestic sub-sector.

• Costs.

– Re-scaled DfT departing seat-km data is used to calculate

operating cost savings from efficiency measures and increased

annualised aircraft capital costs (which are de-annualised to in-

year investments), based on ATA data which assumes a 20 year

economic lifetime, 10% residual value and a 4.5% interest rate6.

No cost data was available for the military aviation sub-sector.

Marginal added costs of SAF above fossil jet are also calculated

for all sub-sectors.

– Costs are then split into sub-sectors and DAs to calculate

£/tCO2e abated by each measure, using CCC’s 3.5% social

discount rate.

Further assumptions used in the analysis include:

• In 2018, 99.91% of fuel used in the UK aviation sector was aviation turbine

fuel (avtur or jet), and 0.09% of fuel used was aviation spirit (avgas). CCC

have used the term “jet” or “jet fuel” to include all the fuel used in UK

aviation. Our analysis uses the 2018 weighted average of avtur and avgas,

with constant fuel density, calorific value and carbon content values from

Defra.7

• NAEI factors are also applied to scale combustion CO2 to combustion CH4

(with separate factors for domestic, international and military sub-sectors),

and a constant factor to scale combustion CO2 to combustion N2O

(applied for all sub-sectors).8 SAF fuels are assumed to continue to have the

same combustion CH4 and N2O emissions per kWh as fossil jet (only their

accounting CO2 emissions are reduced).

• Jet fuel costs are not part of the BEIS/HMT Green Book Long-run variable

costs of energy supply (LRVCs) dataset. However, based off IATA9, financial

market and refining datasets, the jet crack ($/bbl) above crude oil price is

historically very similar to the diesel crack ($/bbl). The Green Book diesel

LRVCs (p/litre) were therefore used and converted into p/kWh values for

fossil jet fuel.

d) Devolved administrations

The 2018 share of emissions from the NAEI is used to apportion UK emissions to

emissions at devolved administration (DA) level. Separate splits are used for

domestic, international and military aviation:

• Domestic: 32.8% Scotland, 0.80% Wales, 13.1% NI, 53.2% England

• International: 4.3% Scotland, 0.29% Wales, 0.55% NI, 94.9% England

• Military: 7.4% Scotland, 3.4% Wales, 2.2% NI, 86.9% England

15 Sixth Carbon Budget - Aviation

These DA splits are held fixed over time in all scenarios, except for in the Baseline,

Headwinds and Widespread Innovation scenarios, where expansion in London

airports from 2030 to 2033 is assumed (delayed from DfT modelling which assumes

this happens from 2026):

• This expansion leads to domestic DA splits reaching 28.7% Scotland, 0.73%

Wales, 10.9% NI, 59.7% England by 2033, before a linear return to 2018 DA

splits is assumed by 2050.

• International DA splits reach 3.8% Scotland, 0.27% Wales, 0.48% NI, 95.4%

England by 2033, before a linear return to 2018 DA splits is assumed by 2050.

• No change assumed in military aviation DA splits.

As show in Figure M8.3, Welsh aviation emissions to not rebound post-COVID as

much as other DAs relative to the 2020 base year, due to the outsized influence of

military aviation emissions in Wales, where fuel use has been assumed to be held

flat from 2019. Scotland and NI have much smaller military sub-sectors relative to

their combined domestic and international emissions, and so their emissions profile

matches the UK profile with the COVID-19 recovery.

Figure M8.3 Comparison of emission pathways for the UK, Scotland, Wales, Northern Ireland

Source: CCC analysis.

Notes: Aviation sector GHG emissions for the Balanced Net Zero Pathway, split into DAs, and re-based from 2020

levels (which is at the bottom of the COVID-19 dip, hence strong growth in the following years).

Sixth Carbon Budget - Aviation 16

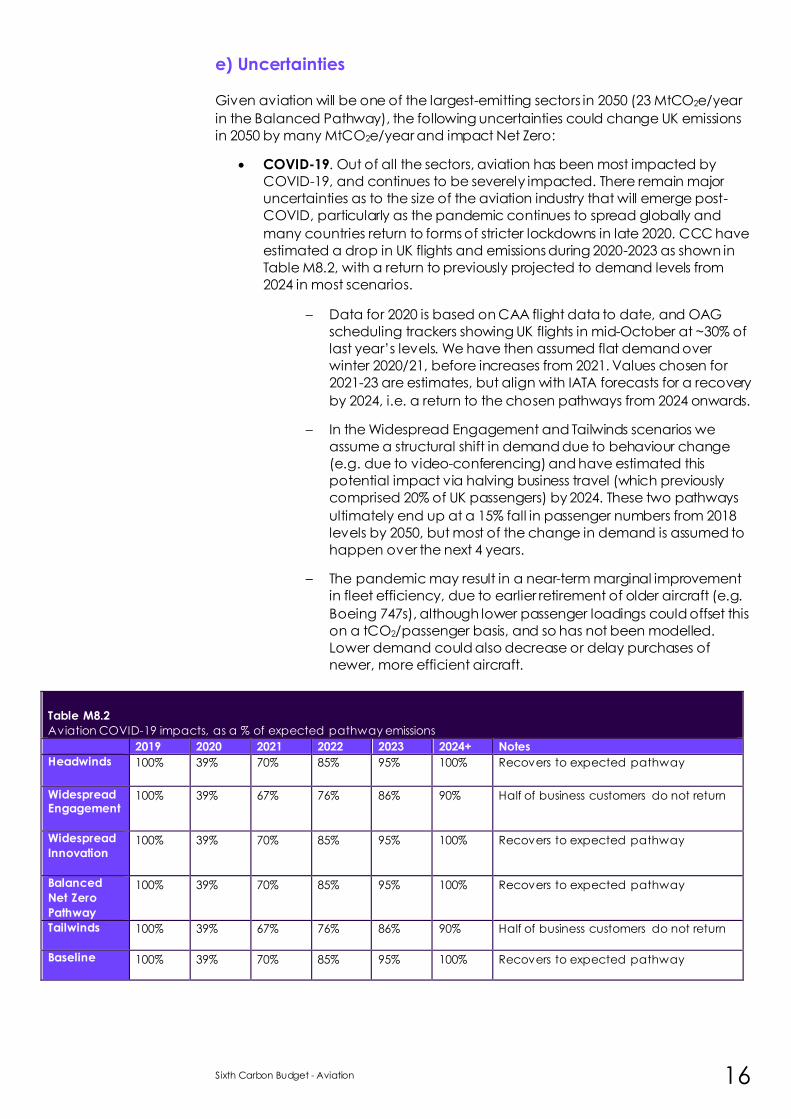

e) Uncertainties

Given aviation will be one of the largest-emitting sectors in 2050 (23 MtCO2e/year

in the Balanced Pathway), the following uncertainties could change UK emissions

in 2050 by many MtCO2e/year and impact Net Zero:

• COVID-19. Out of all the sectors, aviation has been most impacted by

COVID-19, and continues to be severely impacted. There remain major

uncertainties as to the size of the aviation industry that will emerge post-

COVID, particularly as the pandemic continues to spread globally and

many countries return to forms of stricter lockdowns in late 2020. CCC have

estimated a drop in UK flights and emissions during 2020-2023 as shown in

Table M8.2, with a return to previously projected to demand levels from

2024 in most scenarios.

– Data for 2020 is based on CAA flight data to date, and OAG

scheduling trackers showing UK flights in mid-October at ~30% of

last year’s levels. We have then assumed flat demand over

winter 2020/21, before increases from 2021. Values chosen for

2021-23 are estimates, but align with IATA forecasts for a recovery

by 2024, i.e. a return to the chosen pathways from 2024 onwards.

– In the Widespread Engagement and Tailwinds scenarios we

assume a structural shift in demand due to behaviour change

(e.g. due to video-conferencing) and have estimated this

potential impact via halving business travel (which previously

comprised 20% of UK passengers) by 2024. These two pathways

ultimately end up at a 15% fall in passenger numbers from 2018

levels by 2050, but most of the change in demand is assumed to

happen over the next 4 years.

– The pandemic may result in a near-term marginal improvement

in fleet efficiency, due to earlier retirement of older aircraft (e.g.

Boeing 747s), although lower passenger loadings could offset this

on a tCO2/passenger basis, and so has not been modelled.

Lower demand could also decrease or delay purchases of

newer, more efficient aircraft.

Table 1.11:Table 1.11

Table M8.2

Aviation COVID-19 impacts, as a % of expected pathway emissions

2019 2020 2021 2022 2023 2024+ Notes

Headwinds 100% 39% 70% 85% 95% 100% Recovers to expected pathway

Widespread Engagement

100% 39% 67% 76% 86% 90% Half of business customers do not return

Widespread

Innovation

100% 39% 70% 85% 95% 100% Recovers to expected pathway

Balanced

Net Zero

Pathway

100% 39% 70% 85% 95% 100% Recovers to expected pathway

Tailwinds

100% 39% 67% 76% 86% 90% Half of business customers do not return

Baseline

100% 39% 70% 85% 95% 100% Recovers to expected pathway

17 Sixth Carbon Budget - Aviation

• GDP/economic outlook. We have not attempted to calculate a long-term

reduction in aviation demand due to structural changes to the economy or

long-term level of GDP due to COVID-19 (flights have historically correlated

to GDP). We have also not considered any reductions in supply via e.g.

failures of airports, airlines or engine manufacturers. Lower long-term fossil

jet fuel prices and slowed aircraft sales and development cycles could

lead to smaller efficiency gains than previously projected, although this has

also not been modelled.

• Efficiency measures are expected to be cost saving in all scenarios, and

under a range of fossil fuel costs and passenger demands. However, costs

have not been modelled by DfT, and the DfT model is not an aircraft

stock/sale model.

We have therefore had to infer added investment costs in each year from

representative ATA aircraft Class data, applied to DfT seat-km/year outputs,

and de-annualising using annual changes. There are therefore some years

with particularly large or small (or even very occasionally negative*) capital

costs, due to the limitations of the datasets.

• Future aircraft.

– The uptake of electric hybrid aircraft in the DfT modelling is

relatively modest (around 9% of aircraft kilometres by 2050,

consuming 6-7% of jet fuel). The DfT model assumes that full

electric planes will not be commercialised by 2050, and it does

not have a role for hydrogen turbine or hydrogen fuel cell planes

by 2050 either. There could be break-throughs in these aircraft

options, although the time taken to design, build, test, scale-up,

certify and manufacture new aircraft propulsion systems (and the

new aircraft bodies to accommodate them and their energy

stores on-board) is significant – at least several decades.

– Even if one of these options were commercialised in the 2040s, it

would be challenging to immediately achieve a large % share of

aircraft sales, and given the 20-30 year lifetimes of aircraft, this will

not lead to a significant fleet penetration by 2050. These full

electric or hydrogen options have energy storage limitations, and

would be most suited for domestic or short-haul flights and/or

smaller airplane classes, which make up a relatively small share

of UK aviation emissions.

– Combined, these range, aircraft class and development timings

mean that 2050 penetrations of these options are likely to be

limited, or they could occupy small niches by 2050 – although

neither is likely to significantly improve the overall UK emissions

profile. Long-haul flights dominate UK aviation emissions and are

likely to stay using a hydrocarbon fuel until 2050 or beyond,

hence the need for SAF.

* A negative capital cost is possible, and would indicate a net sale of assets in the year. This only occurs where there is

a particularly large divergence in demand from the Baseline scenario, at which point the sector may down-size.

Sixth Carbon Budget - Aviation 18

• SAF is expected to be an added marginal cost, and this marginal cost will

depend heavily on the counterfactual fossil jet cost, the cost of feedstocks

(especially for synthetic fuels using hydrogen and DAC CO2), and the future

improvement in processing plant costs (including the addition of CCS to FT

routes which will significantly increase fuel GHG savings). Our scenarios

explore different hydrogen and DAC costs, but hold costs of biomass,

waste and waste fats/oils fixed over time (prices may well rise over time, but

CCC analysis is only focused on resource costs). Processing costs are

assumed to fall over time (as they are largely determined by global

progress in SAF scale-up), and do not vary between scenarios. However,

the earliest, high-risk projects, or smaller UK projects, or projects further from

feedstocks or CO2 sequestration sites, might be significantly more expensive

than modelled. SAF costs are therefore have some level of uncertainty.

• Impact of demand policies. Although we have assessed how much

efficiency and SAF costs would subtract/add to an indicative trans-Atlantic

ticket price, our analysis is only taking the outputs of DfT modelling, and we

do not have the ability to feed the specific decarbonisation costs back in

to the demand framework to calculate the impact on passenger demand.

This limitation also applies to demand management policies – DfT modelling

internally assumes a rising carbon price, which reduces demand from an

original counterfactual scenario, but CCC again only take the outputs after

this internal carbon pricing is applied to demand. The particular policies

that might be utilised to manage demand could have different impacts on

ticket prices (e.g. carbon pricing, frequent flier levy, VAT, fuel duty, APD

reform, airport capacity management). CCC analysis has focused on the

outcomes (demand, fuel and emissions), rather than prescribing or

modelling the policy method for achieving the demand levels required.

• Measure interdependencies. Theoretically, any combination of the

mitigation measures discussed in section 2 would be possible, as they

separately impact demand, fuel use and fuel accounting emissions.

However, scenarios that rely on high amounts of technical change or new

expensive fuels will likely either require a profitable sector to fund this RD&D,

customers being willing to pay more, and/or more government intervention

(regulation or support). Scenarios with negative growth, if repeated

globally, are likely to result in a slower uptake of new, more efficient aircraft,

and less investment in SAF due to depressed fossil fuel prices. Delivery of the

Tailwinds scenario would therefore be particularly challenging – a reduction

in demand from 2018 levels, with maximal efficiency and 95% SAF by 2050.

• Non-CO2 impacts. These impacts are discussed in Chapter 8, section 4 of

the Advice Report. There remain significant uncertainties in the science and

mitigation options, and therefore uncertainties regarding the policy

response and any interactions with sector GHG emissions (e.g. re-routing

aircraft around super-saturated atmospheric zones to avoid cirrus cloud

formation could increase GHG emissions).

19 Sixth Carbon Budget - Aviation

1 CCC(2020) The Sixth Carbon Budget – Methodology Report. Available at: www.theccc.org.uk

2 IATA (2020) Recovery Delayed as International Travel Remains Locked Down 3 CCC (2020) 2020 Progress Report to Parliament

4 National Atmospheric Emissions Inventory (2020) UK Greenhouse Gas Inventory, 1990 to 2018:

Annual Report for submission under the Framework Convention on Climate Change

5 Civil Aviation Authority (2020) Airport data 2019

6 ATA & Ellondee (2018) Understanding the potential and costs for reducing UK aviation emissions

7 Defra (2020) Greenhouse gas reporting: conversion factors 2020 8 All the analysis is conducted on an IPCC AR5 basis with carbon feedbacks, using 34 tCO2e/tCH4

and 298 tCO2e/tN2O. 9 IATA (2020) Jet Fuel Price Monitor

Emissions pathways for the

aviation sector

21 Sixth Carbon Budget - Aviation

The following sections are taken directly from Section 7 of Chapter 3 of the CCC’s

Advice Report for the Sixth Carbon Budget].1

Introduction and key messages

Aviation is one of the sectors in which we expect there to be significant remaining

positive emissions by 2050, given the limited set of options for decarbonisation.

Remaining residual emissions will need to be offset by greenhouse gas removals

(see section 11) for the sector to reach Net Zero.

The evidence base on how to achieve GHG savings in aviation in the UK relies on

internal modelling from DfT, Climate Assembly UK demand scenarios and internal

CCC analysis of sustainable aviation fuel costs. Further details are provided in the

Methodology Report.

We present the scenarios for aviation emissions in three parts:

a) The Balanced Net Zero Pathway for aviation

b) Alternative pathways for aviation emissions

c) Investment requirements and costs

a) The Balanced Net Zero Pathway for aviation

In the Balanced Net Zero Pathway, the aviation sector returns to close to pre-

pandemic demand levels by 2024. Thereafter, emissions gradually decline over

time (Figure A3.7.a) to reach 23 MtCO2e/year by 2050, despite modest growth in

demand.

This gradual reduction in emissions is due to demand management, improvements

in efficiency and a modest but increasing share of sustainable aviation fuels:

• Demand management. The Balanced Net Zero Pathway does allow for

some limited growth in aviation demand over the period to 2050, but

considerably less than a ‘business as usual’ baseline. We allow for a 25% in

growth by 2050 compared to 2018 levels, whereas the baseline reflects

unconstrained growth of around 65% over the same period. We assume

that, unlike in the baseline, this occurs without any net increase in UK airport

capacity, so that any expansion is balanced by reductions in capacity

elsewhere in the UK.

• Efficiency improvements. The fuel efficiency per passenger of aviation is

assumed to improve at 1.4% per annum, compared to 0.7% per annum in

the baseline. This includes 9% of total aircraft distance in 2050 being flown

by hybrid electric aircraft.

• Sustainable aviation fuels (SAF) contribute 25% of liquid fuel consumed in

2050, with just over two-thirds of this coming from biofuels1 and the

remainder from carbon-neutral synthetic jet fuel (produced via direct air

capture of CO2 combined with low-carbon hydrogen, with 75% of this

synthetic jet fuel assumed to be made in the UK and the rest imported).

1 Biofuels are assumed to be produced with CCS on the production plant – overall carbon-negative but assumed to

have zero direct CO2 emissions in aviation. Removals are accounted for in section 11.

The Balanced Pathway has 25% growth in demand by 2050 compared to 2018 levels, but with no net expansion of UK airport capacity.

A quarter of jet fuel by 2050 is made from sustainable low-carbon sources.

22

Figure A3.7.a Sources of abatement in the Balanced Net Zero Pathway for the aviation sector

Source: BEIS (2020) Provisional UK greenhouse gas emissions national statistics 2019; CCC analysis.

Demand management plays a critical role in ensuring GHG emissions continue to decrease, particularly while efficiency benefits and SAF take time to scale up.

23 Sixth Carbon Budget - Aviation

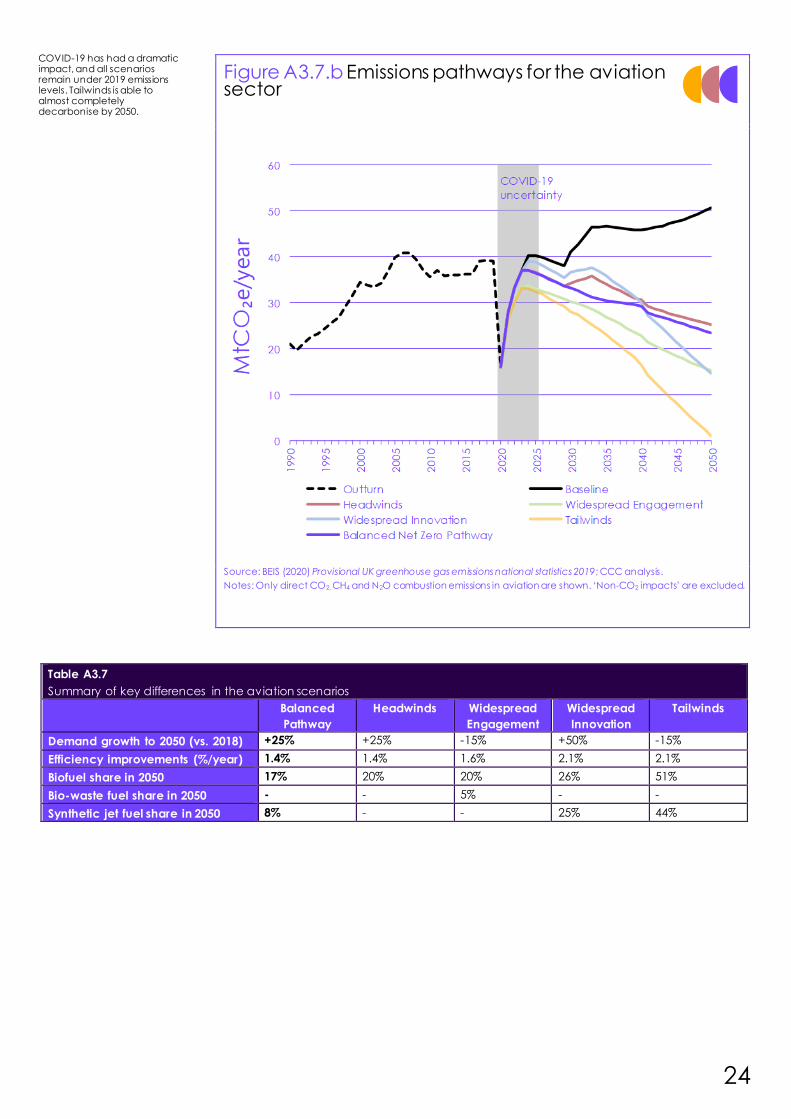

b) Alternative pathways for aviation emissions Each of our exploratory scenarios for aviation sees emissions fall from 2018 to 2050

by more than 35% (Figure A3.7.b), though with different contributions from

efficiency improvements, sustainable fuels and constraints on demand (Table

A3.7):

• Headwinds assumes the same 25% growth in demand from 2018 to 2050 as

in the Balanced Pathway, although with higher demand in the 2030s due to

a net increase in airport capacity. Improvements in efficiency are as in the

Balanced Pathway, while biofuels comprise 20% of the fuel mix by 2050.

Emissions are 25 MtCO2e in 2050, 36% below 2018 levels.

• Widespread Engagement has lower demand, with an overall reduction of

15% on 2018 levels and therefore around half the 2050 demand as in the

baseline. This is in line with the Climate Assembly UK’s ‘flying less’ scenario. It

includes a substantial reduction in business aviation due to widespread

near-term adoption of videoconferencing. Efficiency improvements are

slightly faster than those in the Balanced Pathway at 1.6% per annum, while

the share of biofuels in 2050 is slightly lower at 20%, with a further 5%

contribution from the biogenic fraction of waste-based fuels.2 Emissions in

2050 are 15 MtCO2e, 62% below 2018 levels.

• Widespread Innovation has a greater contribution from technological

performance, both in terms of improved efficiency (2.1% per annum) and

the contribution of sustainable aviation fuels. By 2050, around a quarter of

fuel use is biofuel, with a further quarter carbon-neutral synthetic jet fuel.

These technical improvements lead to a lower carbon-intensity and lower

cost of aviation, although demand in this scenario is considerably higher,

reaching 50% above 2018 levels by 2050 (in line with the Climate Assembly

UK’s ‘technological change’ scenario). Emissions in 2050 are 15 MtCO2e,

63% below 2018 levels.

• In Tailwinds, the reductions in demand under Widespread Engagement are

combined with the technology improvements in Widespread Innovation.

Demand in 2050 is 15% below 2018 levels and efficiency improves at 2.1%

per annum. Very similar volumes of sustainable fuels are used as in

Widespread Innovation, but when applied to the lower fuel consumption in

Tailwinds these comprise a higher combined share of 95% of fuel use.

Emissions in 2050 are 1 MtCO2e, 97% below 2018 levels.

In each case, for the aviation sector to reach Net Zero by 2050, the remaining

emissions will need to be offset with greenhouse gas removals (see section 11).

In addition to the GHG emissions presented here, aviation also has non-CO2

warming impacts due to contrails, NOx emissions and other factors. While outside

of the emissions accounting framework used by UK carbon budgets (see Chapter

10), we estimate the additional warming from these non-CO2 effects in section 4 of

Chapter 8.

2 Waste-based fuels save less CO2 than biofuels, due to approximately half of the waste carbon content being of

fossil origin. Only the biogenic fraction of wastes save CO2 compared to fossil jet fuel.

Widespread Innovation assumes much higher demand growth is possible, due to rapid technology development.

Widespread Engagement assumes lower demand in 2050 than in 2018, due mainly to reduced business travel.

24

Figure A3.7.b Emissions pathways for the aviation sector

Source: BEIS (2020) Provisional UK greenhouse gas emissions national statistics 2019; CCC analysis.

Notes: Only direct CO2, CH4 and N2O combustion emissions in aviation are shown. ‘Non-CO2 impacts’ are excluded.

Table A3.7

Summary of key differences in the aviation scenarios

Balanced

Pathway

Headwinds Widespread

Engagement

Widespread

Innovation

Tailwinds

Demand growth to 2050 (vs. 2018) +25% +25% -15% +50% -15%

Efficiency improvements (%/year) 1.4% 1.4% 1.6% 2.1% 2.1%

Biofuel share in 2050 17% 20% 20% 26% 51%

Bio-waste fuel share in 2050 - - 5% - -

Synthetic jet fuel share in 2050 8% - - 25% 44%

COVID-19 has had a dramatic impact, and all scenarios remain under 2019 emissions levels. Tailwinds is able to almost completely decarbonise by 2050.

25 Sixth Carbon Budget - Aviation

c) Investment requirements and costs In our 2019 Net Zero report, we identified aviation as one of the sectors with cost-

effective GHG savings, given that efficiency gains could offset the added costs of

sustainable aviation fuels. Our updated Sixth Carbon Budget pathways estimate

the full costs and savings involved:

• In the Balanced Net Zero Pathway we estimate total added investment

costs above our baseline of around £390 million/year in 2035 and £570

million/year in 2050, for efficiency improvements and hybridisation (Figure

A3.7.c).

• However, these added investment costs are offset by operational cost

savings of around £1,230 million/year in 2035 and £2,750 million/year in

2050. There are also added operational costs of using sustainable aviation

fuels, given their additional cost above fossil jet fuel, of £470 million/year in

2035, and £1,520 million/year in 2050 (Figure A3.7.d). We have not assigned

any costs or savings to reductions in demand in our scenarios.

Figure A3.7.c Breakdown of aviation sector additional investment

Source: CCC analysis.

Notes: Additional investment in Balanced Net Zero Pathway compared to the baseline, due to higher costs of more

efficient aircraft. No costs or savings have been assumed for reductions in demand vs. the baseline trajectory. No

military aviation cost data available.

The capital costs of improved aircraft efficiency are more than offset by fuel savings. Sustainable aviation fuels add significant costs.

International aviation dominates UK aviation emissions and investment.

26

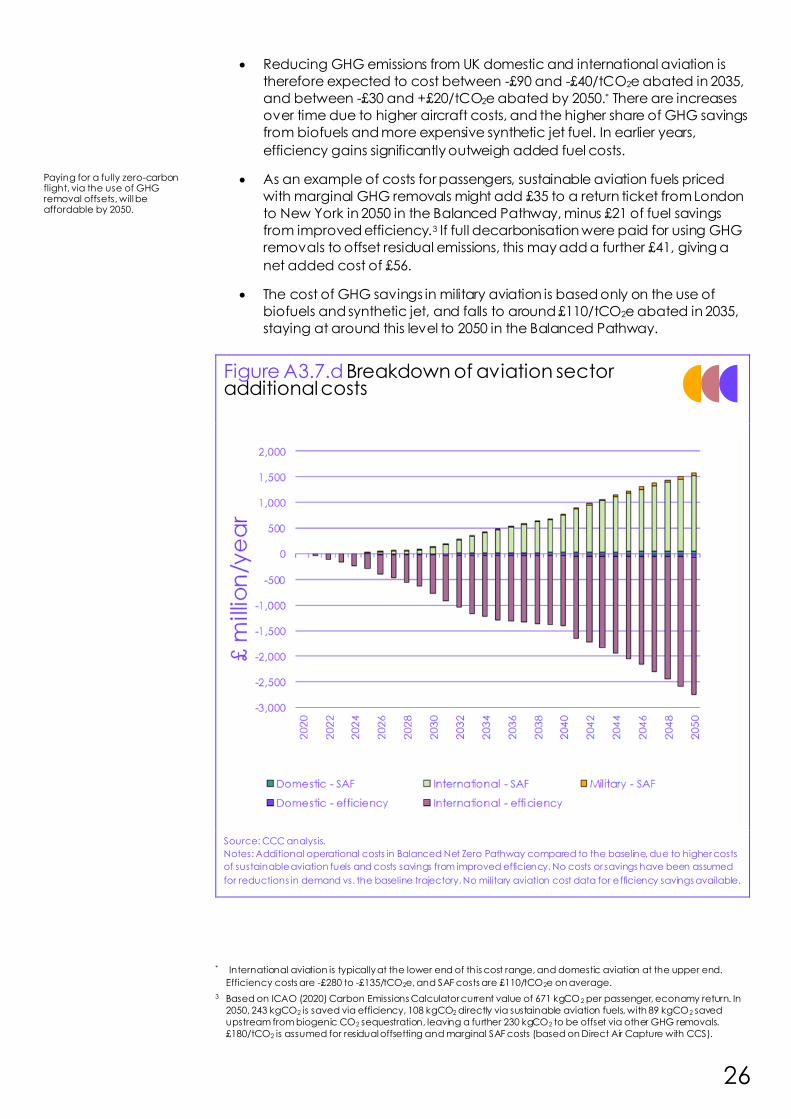

• Reducing GHG emissions from UK domestic and international aviation is

therefore expected to cost between -£90 and -£40/tCO2e abated in 2035,

and between -£30 and +£20/tCO2e abated by 2050.* There are increases

over time due to higher aircraft costs, and the higher share of GHG savings

from biofuels and more expensive synthetic jet fuel. In earlier years,

efficiency gains significantly outweigh added fuel costs.

• As an example of costs for passengers, sustainable aviation fuels priced

with marginal GHG removals might add £35 to a return ticket from London

to New York in 2050 in the Balanced Pathway, minus £21 of fuel savings

from improved efficiency.3 If full decarbonisation were paid for using GHG

removals to offset residual emissions, this may add a further £41, giving a

net added cost of £56.

• The cost of GHG savings in military aviation is based only on the use of

biofuels and synthetic jet, and falls to around £110/tCO2e abated in 2035,

staying at around this level to 2050 in the Balanced Pathway.

Figure A3.7.d Breakdown of aviation sector additional costs

Source: CCC analysis.

Notes: Additional operational costs in Balanced Net Zero Pathway compared to the baseline, due to higher costs

of sustainable aviation fuels and costs savings from improved efficiency. No costs or savings have been assumed

for reductions in demand vs. the baseline trajectory. No military aviation cost data for efficiency savings available.

* International aviation is typically at the lower end of this cost range, and domestic aviation at the upper end.

Efficiency costs are -£280 to -£135/tCO2e, and SAF costs are £110/tCO2e on average.

3 Based on ICAO (2020) Carbon Emissions Calculator current value of 671 kgCO2 per passenger, economy return. In

2050, 243 kgCO2 is saved via efficiency, 108 kgCO2 directly via sustainable aviation fuels, with 89 kgCO2 saved

upstream from biogenic CO2 sequestration, leaving a further 230 kgCO2 to be offset via other GHG removals.

£180/tCO2 is assumed for residual offsetting and marginal SAF costs (based on Direct Air Capture with CCS).

Paying for a fully zero-carbon flight, via the use of GHG removal offsets, will be affordable by 2050.

27 Sixth Carbon Budget - Aviation

1 CCC(2020) The Sixth Carbon Budget – Methodology Report. Available at: www.theccc.org.uk

Policy recommendations for the

aviation sector

29 Sixth Carbon Budget - Aviation

The following sections are taken directly from Chapter 8 of the CCC’s Policy

Report for the Sixth Carbon Budget.1 Chapter 8 covers aviation & shipping policy

recommendations together – we have excluded shipping-only content here.

Table P8.1

Summary of policy recommendations in aviation and shipping

Aviation • Formally include International Aviation emissions within UK climate targets when setting the Sixth

Carbon Budget.

• Work with ICAO to set a long-term goal for aviation consistent with the Paris Agreement, strengthen

the CORSIA scheme and align CORSIA to this long-term goal.

• Commit to a Net Zero goal for UK aviation as part of the forthcoming Aviation Decarbonisation

Strategy, with UK international aviation reaching Net Zero emissions by 2050 at the latest, and domestic aviation potentially earlier. Plan for residual emissions, after efficiency, low -carbon fuels

and demand-side measures, to be offset by verifiable greenhouse gas removals, on a sector net

emissions trajectory to Net Zero.

• There should be no net expansion of UK airport capacity unless the sector is on track to sufficiently

outperform its net emissions trajectory and can accommodate the additional demand.

• Monitor non-CO2 effects of aviation, set a minimum goal of no further warming after 2050, research

mitigation options, and consider how best to tackle non-CO2 effects alongside UK climate targets

without increasing CO2 emissions.

• Longer-term, support for sustainable aviation fuel (SAF) should transition to a more bespoke policy,

such as a blending mandate. However, near-term construction of commercial SAF facilities in the

UK still needs to be supported.

• Continue innovation and demonstration support for SAF technologies, aircraft efficiency measures,

hybrid, full electric and hydrogen aircraft development and airspace modernisation.

Progress in decarbonising aviation and shipping has been slow over the past

decade, and changes in emissions have primarily been driven by changes in

demands along with some improvements in efficiency. Policy to date has been

mainly driven by international fora (negotiations at ICAO and the IMO), although

neither organisation has both established ambitious 2050 global goals and a set of

policies to meet these goals.

The main policy challenges in aviation and shipping are the international nature of

these sectors requiring fuel infrastructure coordination, long asset lifetimes and

economic competitiveness concerns.

Aviation policy in the UK has previously focused on aerospace developments,

although several announcements have been made in 2020, with an Aviation

Decarbonisation Strategy now due in 2021. Funding is still mainly directed at

innovation and demonstration activities, rather than long-term market deployment

support for sustainable aviation fuels and GHG removals.

Our recommendations are based on an assessment of existing policies and

announcements, a review of evidence (including the views of the Climate

Assembly) and updating our existing findings set out in our 2020 Progress Report

and 2019 International aviation & shipping letter.2

This chapter covers:

1. The respective roles for international and domestic policy

2. Existing UK policy, gaps, and planned publications

3. Key policy changes needed

Sixth Carbon Budget - Aviation 30

1. The respective roles for international and domestic policy

Even with their emissions formally included in UK carbon budgets and the Net Zero

target, the primary policy approach to reducing emissions from international

aviation and shipping (IAS) should be at the international level. These sectors are

global in nature and there are some risks that a unilateral UK approach to reducing

these emissions could lead to carbon leakage (under certain policy choices) or

competitiveness concerns.

The UK has played a key role in progress by both the International Civil Aviation

Organisation (ICAO) and International Maritime Organisation (IMO). In the context

of international negotiations at the ICAO and the IMO, inclusion of IAS emissions in

the Net Zero target should not be interpreted as a rejection of multi -lateral

approaches or as prejudicing discussions on burden sharing.

However, international approaches are unlikely to overcome all barriers to

decarbonising the IAS sectors. Supplementary domestic policies should also be

pursued where these can help overcome UK-specific market barriers, and where

these do not lead to adverse impacts on competitiveness and/or carbon leakage.

a) International approaches At the international level, global policies consistent with the ambition in the Paris

Agreement are required to provide a level playing field for airlines and shipping

operators, and to guard against the risk of competitive distortions. The international

trade bodies for both aviation and shipping have begun to develop their

approaches but further progress is required:

• Aviation. The ICAO’s current carbon policy to 2035, the Carbon Offsetting

and Reduction Scheme for International Aviation (CORSIA), aims to ensure

that most emissions increases above a baseline year are balanced by

offsets.

– In light of COVID-19, ICAO agreed a baseline year change to 2019

(instead of averaging over 2019-2020). This will reduce offset

requirements in the initial years of the scheme as the sector recovers.

CORSIA’s list of eligible emissions reduction measures has also been

finalised.

– A new long-term goal for global international aviation emissions is now

required that is consistent with the Paris Agreement. CORSIA then

needs to be extended and aligned with this goal, and rules need to

be put in place to ensure that CORSIA offsets deliver genuine emission

reductions, transitioning to sustainable, well-governed greenhouse gas

removals (see Chapter 11).

Inclusion of IAS emissions in UK climate targets does not imply taking a unilateral policy approach for them.

International approaches are unlikely to overcome all barriers to decarbonising the IAS sectors.

ICAO needs to set a long-term goal aligned with the Paris Agreement, and strengthen CORSIA.

31 Sixth Carbon Budget - Aviation

b) Supplementary domestic policies Supplementary domestic policies that have limited competitiveness or carbon

leakage risks should be pursued in parallel to international approaches to

decarbonisation. These include support for developing alternative fuels and

associated infrastructure, managing demand, decarbonising domestic fleets, and

kick-starting a UK market for greenhouse gas removals (see Chapter 11). These

domestic policy recommendations are discussed in section 3 below.

By taking these domestic and international policy approaches in parallel to

including IAS formally within carbon budgets and the Net Zero target, the UK will

be contributing fully to the global effort to tackle aviation and shipping emissions.

Domestic policy can focus on supporting low-carbon fuels, managing demand, domestic fleet decarbonisation and developing GHG removals.

Sixth Carbon Budget - Aviation 32

2. Existing UK policy, gaps, and planned publications

a) Aviation

Existing UK policy in Aviation has been focused on match-funding for aircraft

technology development (e.g. the £300million Future of Flight Challenge), and

traded certificate price support for aviation biofuels and synthetic jet fuels under

the Renewable Transport Fuel Obligation (RTFO)’s ‘development fuels’ sub-

mandate. Recent announcements include:

• The Jet Zero Council has also been established as a forum with the

ambition for developing zero-emissions commercial flight.

• £15 million has been invested into FlyZero, with the Aerospace Technology

Institute looking at design challenges and the market opportunity for zero-

emissions aircraft concepts from 2030.

• £15 million will be invested in a new grant-funding competition for SAF

production.

• A SAF clearing house will be set up to enable UK to certify new fuels.

• A planned consultation on a SAF blending mandate has been announced,

for a potential start in 2025.

• An aviation Net Zero Consultation and following Strategy were planned for

2020. Plans are to now consult on a combined Aviation Decarbonisation

Strategy in 2021.

However, there remain significant gaps within the policy framework for aviation.

Government support at present is focused on innovation funding and

demonstration activities, but without clear long-term policy mechanisms driving

SAF uptake or valuing negative emissions in the UK:

• The RTFO development fuels sub-mandate is unlikely to drive significant

development of jet fuels, as it can be met with cheaper fuels.

• There is currently no price signal for GHG removals in the UK.

• There is a lack of larger-scale deployment support and policy frameworks

specifically for sustainable aviation fuel and GHG removals.

Although the UK aviation industry has committed to a Net Zero goal for 2050 (via

the Sustainable Aviation coalition),3 this is not yet a policy goal for Government.

Higher-level strategic gaps include the lack of formal inclusion of international

emissions in UK carbon budgets and the Net Zero target, and the need for a sector

emissions trajectory to inform demand management and airport capacity policies.

Further research is also needed on non-CO2 effects and potential mitigation

options.

Aerospace development has been a focus in UK policy, although the RTFO is yet to bring forward renewable jet fuel.

Government announcements and support to date focuses on innovation and demonstration, but long-term deployment policy needs developed.

UK aviation industry has committed to reaching Net Zero by 2050.

33 Sixth Carbon Budget - Aviation

3. Key policy changes needed

a) Aviation

The Government should include international aviation emissions within the Sixth

Carbon Budget, subsequent carbon budgets and the 2050 Net Zero target.

The forthcoming Aviation Decarbonisation Strategy should commit to a 2050 Net

Zero goal for UK aviation, with use of verifiable GHG removals (but with limits), and

set out demand management policies to ensure a trajectory to 2050 is achieved

and that non-CO2 effects are addressed.

i) Aviation emissions on the way to Net Zero

The Government should commit to UK international aviation reaching net zero

GHG emissions by 2050 at the latest, and UK domestic and military aviation

potentially earlier.

This will necessarily entail having a plan for how verifiable greenhouse gas removals

will offset residual emissions over time (i.e. after contributions from efficiency

improvements, low-carbon fuels and demand-side measures). DfT should set a net

emissions trajectory for aviation (net of a constrained level of GHG removals), or as

a minimum, interim targets on the way to 2050.

• Following the Balanced Net Zero Pathway, the remaining 23 MtCO2e/year

of gross aviation emissions in 2050 would require 40% of total UK engineered

greenhouse gas removals to be assigned to the aviation sector to achieve

Net Zero within aviation.

• With the ramp-up in GHG removals in the UK over time, Figure P8.1 gives an

indicative net aviation emissions trajectory that could be followed if 40% of

UK GHG removals were assigned to aviation in all years.

• Interim targets for aviation emissions net of greenhouse gas removals could

therefore be 31 MtCO2e/year in 2030, 21 MtCO2e/year in 2035 and 14

MtCO2e/year in 2040.

• Setting an aviation sector net emissions target and trajectory is not

obviated by IAS inclusion with carbon budgets. This is more important in

aviation than other emitting sectors, given that without policy action

aviation emissions could rise significantly (as would non-CO2 effects) and

that, even with appropriate action, residual positive GHG emissions are very

likely to remain by 2050 (and need compensating for with greenhouse gas

removals). The UK aviation industry has also already committed to a 2050

Net Zero target.

This plan should dovetail with the wider overall strategy for Net Zero, which should

set out how this can be achieved with manageable volumes of sustainable

greenhouse gas removals.

International aviation emissions to be included in Carbon Budgets.

Government should commit to a 2050 Net Zero goal for UK aviation, with use of verifiable GHG removals.

An emissions trajectory to 2050 will set expectations for use of GHG removals over time.

Inclusion of IAS in Carbon Budgets does not diminish the value of a sector target and trajectory.

Sixth Carbon Budget - Aviation 34

Figure P8.1 Indicative UK aviation emissions trajectory to achieve Net Zero with GHG removals

Source: CCC analysis.

Note: Net of GHG removals trajectory assumes that 40% of UK engineered GHG removals are assigned to/bought by the aviation sector. COVID-19 recovery assumed from 2020 to 2024.

ii) Demand management

Demand management policy should be implemented, as given expected

developments in efficiency and SAF deployment, demand growth will need to be

lower than baseline assumptions, and likely constrained to 25% growth by 2050

from 2018 levels for the sector to contribute to UK Net Zero.

If efficiency or SAF do not develop as expected, further demand management will

be required. Conversely, if efficiency and SAF develop quicker, it may be possible

for demand growth to rise above 25%, provided that additional non-CO2 effects

are acceptable or can be mitigated.

A demand management framework will therefore need to be developed and in

place by the mid-2020s to annually assess and, if required, act as a backstop to

control sector GHG emissions and non-CO2 effects.

• There are a number of demand management policies that could be

considered, as we outlined in our 2019 IAS letter.2 However, the Climate

Assembly has provided valuable evidence that demand management

policies will have to be fair and be seen as fair, with a clear preference for

any taxes to increase as people fly more and fly further (Box P8.1).

0

5

10

15

20

25

30

35

40

2020

2025

2030

2035

2040

2045

2050

MtC

O₂e/year

GHG removals assigned to aviation Net of GHG removals

Balanced Net Zero Pathway

From the Balanced Net Zero Pathway, aviation emissions net of GHG removals fall relatively smoothly from the mid-2020s to 2050 Net Zero.

Demand management policy is required, as demand growth will need significantly constrained from baseline assumptions, and there are non-CO2 risks.

Demand management needs to act as a back-stop to keep emissions on track to the sector trajectory to Net Zero.

35 Sixth Carbon Budget - Aviation

• As part of providing wider information regarding transport choices,

Government should also consider the feasibility and benefits of providing

flight CO2 labelling to prospective aviation passengers, building on the work

of the Civil Aviation Authority (CAA).

The Government should assess its airport capacity strategy in the context of Net

Zero and any lasting impacts on demand from COVID-19. Investments will need to

be demonstrated to make economic sense in a Net Zero world and the transition

towards it.

• Unless faster than expected progress is made on aircraft technology and

SAF deployment, such that the sector is outperforming its trajectory to Net

Zero, current planned additional airport capacity would require capacity

restrictions placed on other airports.

• Going forwards, there should be no net expansion of UK airport capacity

unless the sector is assessed as being on track to sufficiently outperform a

net emissions trajectory that is compatible with achieving Net Zero

alongside the rest of the economy, and is able to accommodate the

additional demand and still stay on track.

Box P8.1

Climate Assembly aviation demand findings

Box 8.1 from the Methodology Report, Chapter 8, highlights the Climate Assembly’s

preferences regarding demand growth. The Assembly recommended 25-50% demand

growth by 2050 from 2018, depending on how quickly technology progressed. A

weighted average of the scenario votes was a 24% growth.

80% of assembly members ‘strongly agreed’ or ‘agreed’ that taxes that increase as

people fly more often and as they fly further should be part of how the UK gets to Net

Zero. Assembly members saw this as fairer than alternative policy options, such as a

carbon tax that would impact all flights.

There were also strong calls for making alternatives to flying cheaper and better, and for

the UK to influence the rest of the world in implementing global decarbonisation policies.

Source: Climate Assembly UK (2020).

No net expansion of UK airport capacity unless the sector is on track to sufficiently outperform its trajectory.

The Climate Assembly stated a clear preference for demand taxes to increase as people fly more and fly further.

Sixth Carbon Budget - Aviation 36

iii) Wider supporting policies

Alongside the Aviation Decarbonisation Strategy, UK policy should also:

• Set out a policy package for supporting the near-term deployment of

commercial sustainable aviation fuel (SAF) facilities in the UK (with carbon

capture and storage (CCS) where applicable). This may involve capital or

loan guarantee support. In the mid-term, SAF support should transition to a

more bespoke policy than the RTFO.

– The existing RTFO will not be suitable for delivering mass commercial

roll-out of SAF, due to decreasing liquid road fuel use. It may also make

more sense for long-term SAF deployment to be paid for by the

aviation sector rather than road fuel users.

– Government has indicated willingness to consider introducing a SAF

blending mandate from 2025,4 which could ultimately provide more

certainty to SAF plant investors than the RTFO. A SAF mandate is likely

to be more effective than Contracts for Difference (as the technology

maturity of many routes are not high enough and there are variable

feedstock costs), inclusion in an Emissions Trading Scheme (likely

insufficient and volatile pricing signal) or carbon taxation (would have

to be high to incentivise initial SAF deployment, and not perceived as

fair by the Climate Assembly).

– Whether the mandate’s added SAF costs then fall to the aviation

sector or general taxation will depend on the policy design and any

concerns regarding UK operator competitiveness or carbon leakage.

Several other European countries already have SAF blending

mandates and are introducing ambitious blending trajectories, which

suggests the risk of leakage is decreasing (e.g. France is targeting 5%

by 2030 & 50% by 2050; Finland & Sweden 30% by 2030; Germany 2%

by 2030; with an EU-wide proposal for 1-2% by 2030).4

– Ongoing uncertainty until 2025 about a new UK SAF mandate, and

withdrawal of SAF from the RTFO, may risk delaying first commercial

SAF projects in the UK reaching financial close for several years.

Consideration could be given to either RTFO grandfathering, starting

the SAF mandate earlier or running it in parallel to the RTFO.

• Continue innovation and demonstration support for newer SAF

technologies, ensuring fuels can meet international standards. The newly

announced £15m competition focused only on SAF is welcome, although is

smaller than previous competitions.

• Continue RD&D support for aircraft efficiency measures, hybrid, full electric

& hydrogen aircraft development and airspace modernisation. Continue

to use existing delivery bodies, such as ATI, the Future of Flight Challenge,

NATS, and guided by the Jet Zero Council.

• Continue to enforce strict sustainability standards, and work to consistently

account for fuels produced with biogenic CO2 capture without allowing

double-counting of any GHG removals.

4 From our analysis, potential UK SAF blending levels could be 1.5-3.5% by 2030, 4-9% by 2035 and 11-17% by 2040,

although the top end of these figures could almost be doubled in a Tailwinds scenario, due to faster technology

deployment and higher biofuel imports.

Support is needed for the UK’s first commercial SAF plants.

A SAF blending mandate could provide more certainty to SAF plant investors.

Many other European countries already have SAF blending mandates, so carbon leakage risks are decreasing.

Strict sustainability standards will need to be enforced, any double-counting of removals avoided, and SAF plants should be built with CCS.

37 Sixth Carbon Budget - Aviation

– SAF facilities should have to install CCS, or be built CCS ready, in order

to maximise GHG savings from any concentrated CO2 streams or

dilute flue gases.* The 2022 Bioenergy Strategy should set a date after

which all new build plants must use CCS, and a date after which

existing plants should retrofit CCS.

– An accounting choice needs to be made as to whether the consumer

of a fuel made with CCS gets to account for the GHG removals (i.e.

fuels can be carbon negative, further reducing end-use sector direct

emissions),5 or whether the producer of the fuel gets to account for the

GHG removals (and the fuel is carbon neutral).

– Any GHG removals accounted for within a fuel carbon intensity factor

or by a producer cannot also be claimed by another actor or sector.

– A clear GHG savings methodology needs to be established for wastes.

• Monitor non-CO2 effects of aviation, continue to work to reduce scientific

uncertainties, and fund research into mitigation options such as SAF

benefits and engine design improvements.

– Once mitigation options are better characterised, consider policy

responses as to how best to tackle them alongside UK climate targets

without increasing CO2 emissions.

– As a minimum goal, there should be no additional non-CO2 warming

from aviation after 2050. If mitigation options develop quickly, or new

risks are identified, DfT could consider an earlier date, or setting a

maximum level of allowable non-CO2 warming from a base year.

Alongside efforts at ICAO, the Aviation Decarbonisation Strategy and the package

of domestic policies, plus parallel progress on a mechanism for deploying GHG

removals in the UK (see Chapter 11), should put UK aviation emissions on track to

contribute fully to meeting the Sixth Carbon Budget and the Net Zero target. A

summary of the required steps in aviation is given in Figure P8.2.

* Some SAF conversion plants do not produce CO2, and hence these CCS provisions may not apply to them. For

example, synthetic jet fuel routes use CO2 as a feedstock, and waste fats/oils to biojet will produce little CO2.

However, these plants may still have dilute flue gas streams from which CO2 should still be captured.

5 UK biofuels policy currently uses GHG emissions thresholds (gCO2e/MJ of fuel) as one set of eligibility criteria for

support. Setting a negative GHG emissions threshold may lead to perverse outcomes, where only less efficient plants

meet the threshold. Any negative threshold would have to be accompanied by a minimum efficiency and would

preclude carbon-neutral fuels. It is likely more appropriate to maintain low positive GHG emissions thresholds for

eligibility purposes but allow additional benefits to flow to conversion plants capturing biogenic CO 2 (this may be

achieved already by the design of wider GHG removals policies).

There should be no additional non-CO2 warming after 2050.

Sixth Carbon Budget - Aviation 38

Figure P8.2 Timeline of key outcomes and policy requirements under the Balanced Pathway (2020-50)

Source: CCC analysis. Note: SAF = Sustainable Aviation Fuel. BECCS = Bioenergy with carbon capture and storage

39 Sixth Carbon Budget - Aviation

1 CCC(2020) Policies for the Sixth Carbon Budget and Net Zero . Available at: www.theccc.org.uk

2 CCC (2019) Net-zero and the approach to international aviation and shipping emissions 3 Sustainable Aviation (2020) UK aviation commits to net zero carbon emissions by 2050

4 Argus (2020) Europe makes legislative push for aviation transition