the structure of wholesale produce markets

TRANSCRIPT

ficfi. Hi

THE STRUCTURE

OF

WHOLESALE PRODUCE MARKETS

^w•^6t«« Rt^í^^^•

,AP

M^R 2S ^^^^

600 ^:^ ¿02^3

Agricultural Economic Report No. 45

UNITED STATES DEPARTMENT OF AGRICULTURE Economic Research Service

Marketing Economics Division

THE STRUCTURE

OF

WHOLESALE PRODUCE MARKETS

Issued Apru 1964 ^ Agricultural Economic Report No. 45

UNITED STATES DEPARTMENT OF AGRICULTURE

Economic Research Seryice Marketing Economics Division

other Publications From This Study

Published by the U.S. Department Of Agriculture THE CHANGING ROLE OF THE FRUIT AUCTIONS, by Alden C. Manchester. Mktg.

Res. Rpt. No. 331, June 1959. CHAINSTORE MERCHANDISING AND PROCUREMENT PRACTICES. THE CHANGING

RETAIL MARKET FOR FRESH FRUITS AND VEGETABLES, by William E. Folz and Alden C. Manchester. Mktg. Res. Rpt. No. 417, July 1960.

THE ORGANIZATION OF THE WHOLESALE FRUIT AND VEGETABLE MARKET IN BOSTON, by Alden C. Manchester. Mktg. Res. Rpt. No. 515, January 1962.

THE ORGANIZATION OF THE WHOLESALE FRUIT AND VEGETABLE MARKET IN WASHINGTON, D.C., by Aldcu C. Manchester. Mktg. Res. Rpt. No. 524, February 1962.

THE ORGANIZATION OF THE WHOLESALE FRUIT AND VEGETABLE MARKETS IN DENVER, SALT LAKE CITY, EL PASO, ALBUQUERQUE, AND BUTTE, by Alden C. Manchester. Mktg. Res. Rpt. No. 541, June 1962.

THE ORGANIZATION OF THE NEW YORK CITY WHOLESALE FRUIT AND VEGETABLE MARKET, by Alden C. Manchester. Mktg. Res. Rpt. No. 542, June 1962.

THE ORGANIZATION OF THE WHOLESALE FRUIT AND VEGETABLE MARKET IN PITTSBURGH, by Aldcu C. Manchester. Mktg. Res. Rpt No. 557, August 1962.

THE ORGANIZATION OF WHOLESALE FRUIT AND VEGETABLE MARKETS IN DALLAS- FORT WORTH, HOUSTON AND LITTLE ROCK, by AldcH C. Manchester. Mktg. Res. Rpt. No. 558, August 1962.

THE ORGANIZATION OF THE WHOLESALE FRUIT AND VEGETABLE MARKET IN PHILADELPHIA, by Joscph C. Podauy. Mktg. Res. Rpt. No. 559, August 1962.

THE ORGANIZATION OF THE WHOLESALE FRUIT AND VEGETABLE MARKETS IN DETROIT, ALBANY-SCHENECTADY-TROY, AND WEST VIRGINIA, by Alden C. Manchester. Mktg. Res. Rpt. No. 562, October 1962.

THE ORGANIZATION OF THE WHOLESALE FRUIT AND VEGETABLE MARKETS IN SEATTLE-TACOMA, PORTLAND, AND SPOKANE, by W. Fred Chapman, Jr. Mktg. Res. Rpt. No. 563, October 1962.

THE ORGANIZATION OF THE WHOLESALE FRUIT AND VEGETABLE MARKETS IN MIAMI AND TAMPA-ST. PETERSBURG, by Robcrt W. BohuU. Mktg. Rcs. Rpt. 593, April 1963.

Published by State Experiment Stations PRODUCE WHOLESALERS IN THE CAPITOL DISTRICT, NEW YORK, 1958, by D. C.

Hodges and R. Brian How, Cornell University. A.E. Ext. 106, 1961. WHOLESALE MARKETING OF FRESH FRUITS AND VEGETABLES IN OMAHA AND

LINCOLN, NEBRASKA, by Clarence J. Miller. Nebr. Agr. Expt. Sta., Dept. Agr. Econ. Rpt. No. 21, June 1961.

WHOLESALE FRUIT AND VEGETABLE MARKETS IN EL PASO AND ALBUQUERQUE, by James L. Stallings and Jere E. Boyer. N. Mex. Agr. Expt. Sta., Res. Rpt. 43, July 1960.

THE PORTLAND WHOLESALE FRUIT AND VEGETABLE MARKET, by AldcU C. Manchester and Charles H. Merchant. Maine Farm Res., Jan. 1961.

ORGANIZATION OF THE LOUISVILLE WHOLESALE FRUIT AND VEGETABLE MARKET, 1959, WITH CHANGES SINCE 1936, by C. D. PhiUips. Ky. Agr. Expt., Sta., Bui. 674, September 1961.

Foreword This is the final report of a study of organization and operation of wholesale

fruit and vegetable markets throughout the country. This is part of a program of research designed to broaden understanding of the food marketing system and, thereby, to make it more efficient. A number of reports on the individual markets studied have been published by the Department and cooperating experiment stations. (See the list on the inside front cover.)

The cooperation of naany persons was necessary to make this study possible. John K. Hanes was assistant project leader. Joseph C. Podany, W. Fred Chapman, Jr., Robert A. Bohall, Alvin Z. Macomber, Merritt M. Thomas, George L. Capel, Dale L. Stallings, William T. Manley, James W. Diunas, Mrs. Priscilla Bonnucelli, and Mrs. Dorthy Lundquist were invaluable members of the team. The Fruit and Vegetable Division of the Agricultural Marketing Service furnished information and counsel, especially Arthur E. Browne and Fred S. Nightingale. We are most grateful for the cooperation of research personnel from many experiment stations, including Donald E. Farris and Roy E. Lambert of Arkansas; C. D. Phillips of Kentucky; Harlon D. Traylor of Louisiana; Charles H. Merchant, L. J. Jewett and Fred A. Perkins of Maine; Frank J. Smith of Minnesota; Heinz Speilman and Edward H. Ward of Mon- tana; Clarence J. Miller and George B. O'Neal of Nebraska; JereBoyer and James Stallings of New Mexico; D. C. Hodges, Donald Marion, and R. Brian How of Cornell; Mark Fowler and Kermit Bird of Oklahoma; J. F. Pittman of South Carolina; Ellis Lamborn and Reed D. Taylor of Utah; Paul A. Atkins and W. W. Armen trout of West Virginia ; and Jerry Gunnelson and W. F. Mueller of Wisconsin.

Ill

Contents Page

Highlights V Introduction 1

The study 1 Classification of firms 2

PART I

The marketing system for fresh fruits and vegetables. _ 3 Shipping-point markets 3 Wholesale markets 4

Wholesale market structure, 1958-59 8 Number, size, and type of firms 8 Commodity specialization 14 Interfirm relationships 19 Legal form of organization 22 Marketing channels 22 Functions and services of wholesalers 35 Risk-taking 46 Functions of brokers and distributors 46 Functions of different types of markets 49

Buying methods of wholesalers 53 Terms of purchase 55 Procurement practices 55

The structure of the retail market for produce 59 Functions performed by retail organizations 62 Physical handhng functions 65

Buying methods of retail organizations 67 Buying organizations 68 Sources of produce 69 Buying methods from local farmers 70 Buying methods trom shipping point 72 Direct buying and the terminal market 76

Costs, margins, and efiiciency 77 Payroll and employees 82 Unit margins 85 Marketing charges in different types of markets. 86 Returns to owners and managers 87 Target margins -- 87 Brokerage and commission rates 89

Page The price-making process 92

Price-making systems 93 The use of market information in price making. _ 95 Price variability 95

PART II

The changing marketing system 97 Changes in the structure of the retail market 99

The growth of direct buying 100 Warehouse prepackaging 101

Changes in the structure of wholesale markets 101 Number, size, and type of firms 102 Entrance and exit of wholesalers 106 Growth and decline 107 Changes in trade channels 107 Changes in services 110 The place of fruit auctions in a changing market-

ing system 111 Outlook of wholesalers 111

PART III

The nature of competition in produce markets 113 Shipping-point markets 113 Wholesale markets 114 Product differentiation 114 Retail markets 115

Prospects 117

Literature cited 120 Appendix: Definitions of terms 121

General terms 121 Size of firms 121 Types of firms 121 Terms of purchase 122 Marketing costs and margins 123

Index 125

IV

Highlights

Many changes have taken place in the produce marketing system in the past quarter century. Direct buying by chains and other retail organi- zations has increased markedly. Many whole- salers have gone out of business, but many others have entered the field. Consumer-unit packaging has become an important element in wholesale and retail markets. To understand better the present organization of wholesale produce markets, as well as the changes which have taken place since the 1930's, the Economic Research Service studied 52 wholesale markets of all sizes and types throughout the country.

These markets were selected to represent the wholesale markets of the United States. They received about 1.6 million carlots of fresh fruits and vegetables out of a total market supply of 2.2 million carlots in 1958. There were about 5,200 wholesalers in these markets, plus 315 chains, retailer cooperatives, and wholesaler- sponsored voluntary groups handling produce. About 30 percent of the wholesalers in the country doing about 20 percent of the business were outside these markets in small cities and towns.

Wholesalers: The 5,200 wholesalers in these markets were made up of the following groups, all in round numbers:

1,600 primary handlers—^receivers, commission merchants, service wholesalers, etc.—selling 800,000 carlots of produce;

2,560 secondary handlers—1,000 jobbers, 540 truck jobbers, 500 purveyors, 200 prepackagers, and 300 tomato repackers—selling 335,000 carlots;

120 shippers and truckers—these are mixed-load shippers and less than carload lot shippers and truckers headquartered in the markets—selling 30,000 carlots;

110 importers and exporters with sales of 220,000 carlots;

500 brokers and distributors selling about 500,000 carlots of produce;

135 cooperative and importers' sales agencies sellmg 185,000 carlots;

10 auctions with sales of 46,000 carlots; 140 buying brokers and buying offices buy-

ing 50,000 carlots. One third of the primary handlers sold more than

500 carlots each. Fifteen percent sold more than 1,000 carlots. On the other hand, 95 percent of the secondary handlers sold less than 500 carlots each per year. Only a handful of prepackagers and banana jobbers handled more than 2,000 carlots during the year.

A third of the brokers and distributors sold less than 500 carlots annually, a fourth between 500 and 1,000 carlots, and another fourth between 1,000 and 2,000. Nearly 80 percent of the buying brokers and two-thirds of the buying offices purchased less than 500 carlots.

Concentration of control, measured by the share of the volume sold by the 4 largest primary handlers in each market, is almost entirely a function of the size of the market. In the smallest markets, the 4 largest firms did all or nearly all of the business. In the largest markets, they had about 15 percent of the business, even though the biggest firms had average sales of 3,000 to 4,000 carlots per year in the largest markets compared to a few hundred carlots in the smallest.

The wholesalers in these markets received 1.1 million carlots of produce directly from shipping points, from local growers, and from other mar- kets, including imports. Brokers and distribu- tors bought 28 percent of this total, plus about half again as much which they sold to out-of-town customers and which bypassed the market. Cooperative and importers' sales agencies sold 9 percent of the total entering the market, and nearly as much which bypassed the market, Receivers, commission merchants, service whole- salers, and other primary handlers piu-chased half of the total themselves and another 11 percent bought through brokers and distributors. The remaining 13 percent entering the markets was bought by prepackagers, jobbers, importers, shippers, and other types of wholesalers.

The importance of brokers and distributors varied greatly among markets, from nothing to two-thirds of the total purchases of wholesalers. In about a quarter of the markets, brokers and distributors bought more of the produce directly from shipping point and other outside sources than did receivers, jobbers, and other wholesale handlers. Most of these ''broker" markets are between Chicago and the Rocky Mountains, from Texas to Minnesota.

In 40 percent of the markets, direct purchases by chains and other retail organizations accounted for 35 percent or more of the produce entering the market. None of the large markets and only a few of the medium-sized ones are in this group. The largest markets in the group are Washington, D.C., Seattle, Wash., and Miami, Fla. The smallest are Charleston, W. Va., and Butte, Mont.

Prepackaging: Over 1,000 wholesalers pre- packaged or repacked nearly 114,000 carlots of produce in 1958. Two-thirds of the volume was put up by 200 prepackagers and 270 tomato repackers. The remainder was handled by wholesalers of almost every type, with receivers, receiver-jobbers, and service wholesalers account- ing for the biggest share. Over 600 firms pre- packaged or repacked only 1 commodity; nearly 200 put up 2 different commodities; another 200 put up 3 or 4 items; and 27 firms packaged 5 or more commodities.

Chains and other retail organizations pre- packaged or repacked 32,500 carlots of produce. The national chains accounted for over three- fourths of this quantity. Potatoes are packaged by more retail organizations than any other commodity.

Retail Organizations: The retail side of these markets was composed of 249 chains or divisions of chains and 66 retailer cooperatives and wholesaler-sponsored volimtary groups which han- dled produce. At least 160 other small chains buy no produce directly from shipping point and several hundred retailer cooperatives and vol- untary groups do not handle produce. Five restaurant chains also bought some produce di- rectly. The retail organizations as a group han- dled about 600,000 carlots of produce. Most of the chains are large—66 percent of them handled more than 1,000 carlots and 16 percent more than 4,000 carlots. The retailer cooperatives and vol- untary groups are somewhat smaller—about three-fourths handled between 500 and 2,000 carlots and only a few more than 2,000.

On the selling side, the retail market is divided about like this:

Percent of total produce

sales by Chains with 11 or more stores each: retailers National chains 17 Regional chains 12 Local chains with produce warehouse 7 Local chains without produce warehouse 2

All chains 38 Chains with 2 to 10 stores each 9

All chains 47

Retailer cooperatives with produce ware- house 3

Voluntary groups with produce warehouse. _ 2 Other grocery stores 39 Specialty fruit and vegetables stores 9

All retail stores 100

The importance of chains and other types of retailers varies decidedly from one market to another. The percentage of total retail produce business done by chains, cooperatives, and voluntaries ranged from 19 to 84 percent. In most of the markets this share fell between 40 to 60 percent. The share of the largest single retailer in the market ranged from 5 to 42 percent ; in over half the markets this share was between 15 and 25 percent.

vi

Direct Buying: Direct purchases from shipping point, from local farmers, and from other markets by chains, cooperatives, and voluntaries were 26 percent of the total receipts in these markets in 1958—for the country as a whole, approximately 20 percent. These firms bought another 5 percent of the total through local brokers and sales agencies. In terms of their total volume the chains and other retail organizations bought 50 percent direct from shipping point; 6 percent from local farmers; 7 percent from firms in other markets, including brokers, and other warehouses of the same chain; 13 percent through local brokers and sales agencies, with deliveries directly to the chain warehouse; 24 percent from receivers, jobbers, prepackagers, and other wholesalers in the local market.

The procurement methods and buying organizations of the different groups vary from one to another, but there are broad similarities within the major types. Each of the three national chains has an extensive field buying staff, with offices (year-round or seasonal) in all the major producing areas, who are in direct touch with growers and shippers and can buy largely on the basis of actual inspection. The national chains buy 70 percent of their total supplies directly from shipping point, mostly through field buyers.

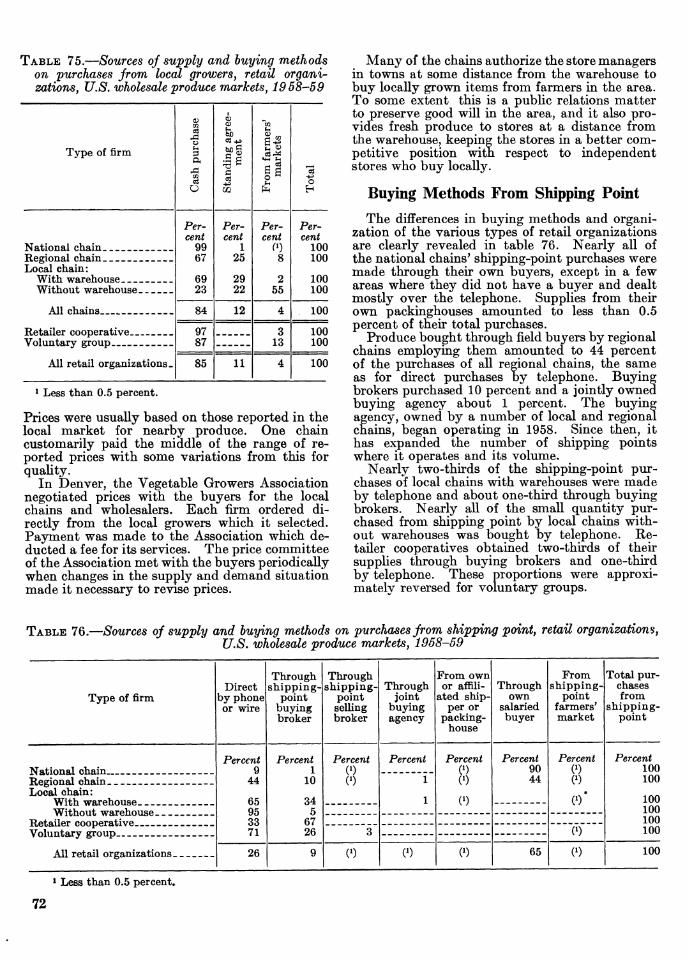

The regional chains—those with several warehouse divisions in different markets—are not large enough to maintain field buying offices as extensive as those of the national chains, but many have a few field offices in the most important production areas. They buy about half of their supplies directly from shipping point. About 45 percent of their direct purchases are made through their own buyers at shipping point and another 45 percent directly by telephone. About 10 percent is bought through buying brokers at shipping point.

Local chains—those with only one warehouse division—have no field buyers. Their direct purchases from shipping point amount to a little less than 30 percent of their volume. Nearly two-thirds of their direct purchases are made by telephone directly to the shipper and about a third through shipping-point buying brokers.

Most chains, like most wholesalers, made use of U.S. grades in buying directly from shipping point, at least to some extent. Over half of the retail organizations buying directly from shipping point generally purchased produce of higher quality than U.S. No. 1, compared with about 11 percent of wholesalers who bought direct. Frequently, such buyers did not have detailed specifications, but asked for *'good quality'' or ^Hhe best available.'' The meaning of such terms was clarified over time as a buyer and seller did business with one another.

Growth of Direct Buying: Direct buying of fresh fruits and vegetables by chains dates back to the early 1920's. The national chains adopted

he practice first, but by the late twenties a number of large local and regional chains were also buying directly. By 1936, 12 percent of the volume entering the major wholesale markets was purchased directly from shipping point by chains.

After World War II, there was a rapid increase in the number of chains large enough to engage in direct buying. Most of the direct buying is done by national and regional chains—in 1958, 90 percent. There has been little change in the percentage of retail food store business done by the national chains since the mid-1930's. However, over this same period, the share of the regional chains has increased sharply, as the number increased. In 1935, three regional chains were doing about 3 percent of the total retail food store business. By 1948, eight regional chains had 5 percent of the business and, by 1958, 20 of them did 12 percent of the business. Thus, most of the increase in direct buying resulted from the increased number and sales of regional chains. The remaining portion of the increase was caused by some large local chains starting to buy directly, and by a number of retailer cooperative and volun- tary chains adding produce to the commodities which they carried.

Changes in Wholesale Markets: Between the late 1930's and the late 1950's, the volume of fruits and vegetables sold by farmers and imported for fresh market, excluding that eaten on farms where grown, increased 12 percent. With direct purchasing by chains and other retail organizations increasing during this period, the total volume handled by the wholesale marketing system probably declined about 10 to 12 percent. The number of wholesalers in these markets listed in the Red Book declined 19 percent between 1939 and 1958. Receivers, commission merchants, and receivers-jobbers declined 27 percent; jobbers declined 29 percent; brokers 41 percent; and buying brokers 8 percent. During the same period, the number of repackers and pre-packagers listed increased from 15 to 205; truck jobbers increased from 383 to 572; and the number of importers and exporters was unchanged.

Since 1939, 5,100 wholesalers have left the produce business. But, in that same period, 3,700 others entered the field in these markets. Of the firms in business in 1958, 8 percent had been in business 50 years or more; 33 percent 30 years or more; and 19 percent had been orga- nized within the past 10 years.

The fruit auctions developed as the major distributors of citrus fruits and west coast deciduous fruit. In 1930, they handled 84 percent of the citrus fruit received in auction cities and nearly as high a percentage of western deciduous fruits. They were the mass distributors of these fruits at the wholesale level. They maintained this position fairly well during the 1930's.

Auction sales declined from 33 percent of all citrus and 10 percent of all deciduous fruit

sold fresh in 1937 to 15 percent of the citrus and 6 percent of the deciduous fruit in 1957. They sold about half of the citrus fruit and western deciduous fruit received in the auction cities in 1956-57.

The auctions are becoming more and more specialty distributors rather than mass distrib- utors. Sales of higher valued fruits are holding up much better than those of lower priced, larger quantity items. The attractions of direct buying by chains, wholesalers, and others are much greater for the large-quantity commodities. The auctions seem well suited to the sale of imported fruit—most of it from Chile and Argentina—and the New York City auction probably will retain these commodities.

Nature of Competition Produce markets both at shipping point and

wholesale are essentially competitive in nature. In most of these markets, the number of firms is quite large, but, even where it is not, the variability in quality of fruits and vegetables compels buyers to maintain actual or potential alternative sources and sellers alternative outlets. The existence of these alternate sources or outlets precludes the exercise of any significant power, even by the largest buyers or sellers. The largest buyer in one fairly typical major shipping- point market purchased a little over 10 percent of the produce.

At the retail level, the competitive situation is somewhat different. The largest groups— chain or affiliated—typically have a substantial share of the business. Each attempts to augment his share by differentiating the products and services which he offers from those of his compet- itors. The largest group in a market usually has some measure of market power, but it is severely circumscribed by actual and potential competition from others in the market. No one has a monopoly of the appeals to consumers. The group which makes its appeal in terms of higher quality fruits and vegetables than its competitors must be prepared to charge some- what higher prices for them or forego some of the profits from the produce department. The group which relies on the appeal of low prices must be prepared to offer a quality level some- what lower than that of its high-quality competitors or forego profits. Thus, there are leaders and followers in the retail field, but no leader can count on being followed where his competitors do not wish to go—the market power of the leader is employed only within a narrow sphere.

Prospects Looking ahead 5 or 10 years, where might some

of these changes lead? The Limits of Direct Buying: Obviously, the

controlling factor in the expansion of direct purchasing is the share of the total fruit and vegetable market controlled by chains—corporate,

Vll

voluntary, and cooperative—which are large enough to buy economically direct from shipping point. To some extent, the decisions of expanding organizations to go into direct buying and how far to go into it will be conditioned by the per- formance of the terminal markets. If adequate supplies of produce are available at competitive prices on the terminal markets, the incentive for smaller groups to buy direct will be much less.

While there is no basis on which to predict the precise nature of the structure of food retailing in the years ahead, a projection of the changes of the past 30 years seems to indicate further growth of buying groups of all types which are big enough to buy directly from the shipping point if they wish to do so. The outside limits of such growth seem to be set by the needs of at least three groups: (1) restaurants, hotels, and institutions; (2) imaffiliated independent grocery stores; and (3) chains making some local purchases. A conservative estimate might be for direct buying to increase from a fifth to something like a third of total sales in the next 10 to 15 years.

Fruit Auctions: The share of the total volume of fruit sold by the auctions probably will continue a slow decline for a number of years. There may be a further decline in the number of such auc- tions, continuing the trend of the last 40 years.

Wholesalers: The share of the total volume handled by receivers, jobbers, service wholesalers, and other terminal-market operators as a group probably will continue to decline somewhat as direct buying by various types of chains increases. The possible limits to this decline have been indicated, and it is quite possible that the decline will not go this far, particularly if smaller chains

find that they can obtain supplies on the local markets which are competitive in quality and price with those which other firms are purchasing from shipping points.

The traditional function of wholesale distribution—purchasing large lots and breaking them down into smaller lots for sale to retailers and secondary wholesalers—probably will become less and less important. Many terminal market operators will need to become specialists.

The Nature of Marketing: Two general, interrelated trends are at work in the marketing system for fresh fruits and vegetables. One is the shift toward more specialized markets. The changes in the types of fruit handled by the auctions are evidence pointing in this direction. The increase in the consumer-unit packaging is another. The shift toward direct buying is also related. Many chains see direct buying as a means of providing their stores with produce which more nearly meets their own requirements than the varied supplies from many sources which are available on the wholesale market.

The second change is the shift in emphasis from what may be called trading to merchandising. The emphasis in old-line wholesale markets often was on the opportunity to make a profit from changes in prices. This type of emphasis is disappearing gradually. More and more the opportunities for profit are to be found in performing a service which contributes to orderly marketing and to moving the commodity through the marketing channels in a steady flow. The supermarkets—chains and independents—are geared to this type of marketing. The rest of the marketing system is gradually adjusting to such an outlook.

VIU

THE STRUCTUEE OF WHOLESALE PRODUCE MARKETS By Alden C. Manchester, Agricultural Economist, Marketing Economics Division, Economic Research Service

Introduction This is a study of the nature of competition

in the fresh fruit and vegetable business, of the structure or organization of produce markets, the behavior of firms in these markets, and of the efficiency with which markets of various types perform their finictions. Its primary focus is on markets at the wholesale level, but it also considers the competitive process at shipping point and at the retail level.

Wholesale produce markets and the marketing system in which they operate developed into the modern form between about 1880 and the mid- 1920-s. In the four decades since then, there have been many changes in the organization and functions of wholesale markets. While the total volmne handled by the produce-marketing system increased about one-eighth from the late 1930's to the late 1950's, the increase in direct buying by chains and afllliated groups brought a decline in the vohmie handled by wholesalers of something like 10 percent. There was a substantial turnover in wholesalers, with a net decline of nearly one- fifth. The retail level became dominated by the supermarket, with its emphasis on mass merchandising of relatively standardized goods at lower margins than had prevailed in earlier periods. These and many other changes brought about further changes in the nature of produce marketing which are stiU affecting producers, packers, and wholesalers. This study analj^zes the present structure and functions of wholesale produce markets, changes during the last 30 years, and the outlook for the next decade or two.

Most of the fresh fruits and vegetables marketed in the United States pass through one or more wholesale markets. These markets play a key role in the produce marketing system, and the efficiency with which they perform their many functions is of major importance to the firms in the markets, to farmers, packers, shippers, retailers, and consumers.

The Study

The primary information for this study was supplied by 2,620 firms in 52 markets selected to represent all of the wholesale markets in the Nation on the basis of three factors: (1) size of market; (2) importance of direct buying by retail

711-059—64 2

organizations; and (3) importance of service wholesalers.

In each sample market, all firms in the metro- politan area were contacted in a combination mail-and-telephone sm'vey to determine: (1) type of firm; (2) commodity specialization; and (3) size of firm. In the small markets, all firms were interviewed. In the larger markets, a sample of firms classified on the basis of these three factors was interviewed. The sample in the largest market ranged from all of the large firms to as low as 20 percent of the smallest firms. The data supplied by the firms interviewed were expanded to represent all of the firms identified in the maü-and-telephone survey. All data were obtained for the calendar year 1958, except in Louisville and Pittsburgh, where the needs of cooperating agencies made it necessary to obtain information for 1959. For convenience, throughout this report ^^1958" is used to include data for 1959 from these two markets.

Additional information, primarily historical, was obtained from a wide variety of sources (5, 6, 11, 15, 17, 21, 22, 27, 32)}

Generous cooperation was forthcoming from many State experiment stations. Survey data were obtained by experiment station personnel in the following markets : Experiment station Market Arkansas Little Rock Kentucky Louisville Maine Portland Minnesota Duluth-Superior Montana Butte Nebraska Lincoln and Omaha New Mexico Albuquerque New York (Cornell) Albany-Schenectady-Troy Oklahoma Oklahoma City and Tulsa Utah Salt Lake City West Virginia All markets in State Wisconsin Milwaukee

Fieldwork was conducted jointly by experiment station and U.S. Department of Agriculture personnel in these markets : Experiment station Market Louisiana New Orleans Maine Boston, Mass. New Mexico El Paso, Tex. South Carolina Columbia and Greenville

Ï Italic numbers in parentheses refer to Literature Cited, p. 120. See also: BRANCH, G. V. DETROIT'S NEW UNION TERMINAL MARKET. Paper presented at meeting of Nati. Assoc. Mktg. Off., Detroit, 1928.

1

The information for the San Francisco-Oakland market was obtained by the University of CaU- fornia under contract with the Department and for Pittsburgh by the Midwest Research Insti- tute under contract. In all other markets, the information was obtained by Departmental personnel.

Classification of Firms For purposes of this study, the firm is defined

as the individual business operation. This does not necessarily coincide with the legal definition of the firm or with other definitions. For a number of companies, a single corporation conducting more than one operation is defined as two firms. For example, a legal entity operating both as a receiver and a prepackager generally is treated as two firms. This permits treatment of different types of operations as single-function firms, rather than trying to handle mmtiple operations under one ownership as a single firm which does not fit any of the definitions. The ownership of such multiple-firms is described on pages 19 to 22.

Each type of firm was defined in terms of the way in which three major functions—buying, selling, and physical handling—were performed. Firms which received more than half of their produce directly from shipping point (including direct purchases from shipping point and purchases through local brokers and agencies) were distinguished from those which received more than half from local wholesale handlers. In terms of the selling function, firms were classified as selling more than half or less than half of their produce to wholesalers or retail organizations with warehouses. Firms which handled the merchandise themselves were generally classified as wholesale handlers, while those that did not were brokers and agencies. Firms which prepack- aged, repacked tomatoes, or processed bananas were classified as separate types of firms if they carried out these functions for more than haK of their produce.

Application of these criteria resulted in the following types of firms, by major groupings (for definitions of each type, see appendix, p. 121) :

Retail organizations Chains, retailer cooperatives, voluntary

groups.

Wholesalers Wholesale handlers—firms physically han-

dling the merchandise. Primary handlers—firms receiving more

than half of their produce directly from shipping point.

Receivers Commission merchants Receiver-jobbers Commission wholesalers Service wholesalers Wholesale grocers

Secondary handlers—firms receiving less than half of their produce directly from shipping point in most cases. A few firms are classified here on other criteria.

Jobbers Jobbers (delivery) Banana jobbers Service jobbers Secondary wholesalers Truck jobbers Piu-veyors Receiver-piKveyors Prepackagers Tomato repackers

Shippers and truckers Mixed-load shippers L.c.l. (less-than-carload lot) shippers Packers-shippers Merchant truckers Itinerant truckers

Importers and exporters Importers Commission importers Exporters

Brokers and agencies—mostly firms which do not physically handle the merchandise.

Brokers and distributors Selling brokers Auction representatives Terminal brokers Carlot distributors Distributors

Sales agencies Cooperative Importer's

Others Buying brokers Buying oflâces Sales agents Auctions

PART I

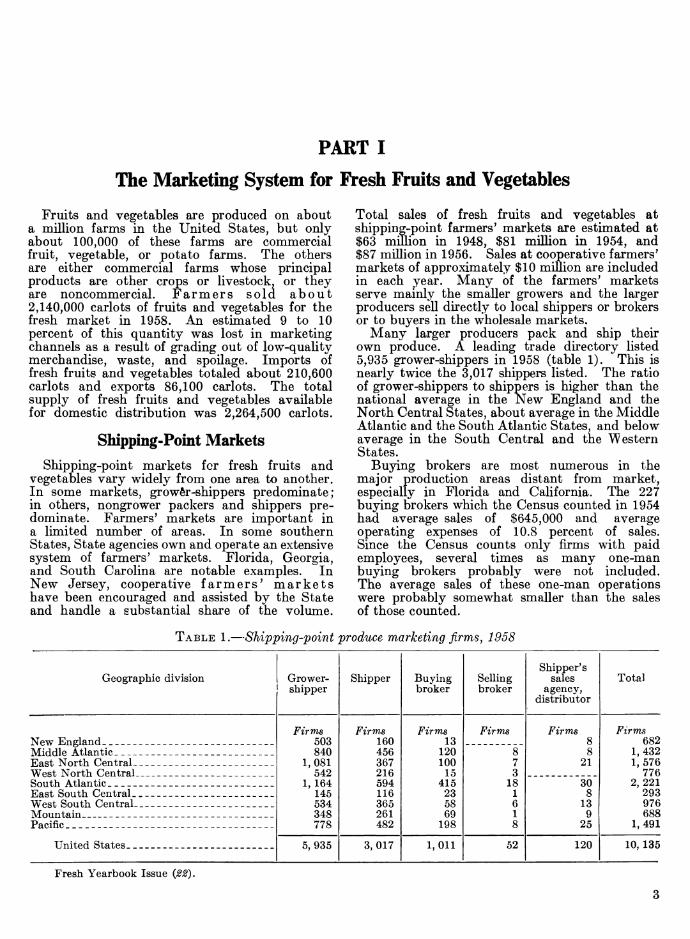

The Marketing System for Fresh Fruits and Vegetables

Fruits and vegetables are produced on about a million farms in the United States, but only about 100,000 of these farms are commercial fruit, vegetable, or potato farms. The others are either commercial farms whose principal products are other crops or livestock, or they are noncommercial. Farmers sold about 2,140,000 carlots of fruits and vegetables for the fresh market in 1958. An estimated 9 to 10 percent of this quantity was lost in marketing channels as a result of grading out of low-quality merchandise, waste, and spoilage. Imports of fresh fruits and vegetables totaled about 210,600 carlots and exports 86,100 carlots. The total supply of fresh fruits and vegetables available for domestic distribution was 2,264,500 carlots.

Shipping-Point Markets Shipping-point markets for fresh fruits and

vegetables vary widely from one area to another. In some markets, grower-shippers predominate; in others, nongrower packers and shippers pre- dominate. Farmers' markets are important in a limited number of areas. In some southern States, State agencies own and operate an extensive system of farmers' markets. Florida, Georgia, and South Carolina are notable examples. In New Jersey, cooperative farmers' markets have been encouraged and assisted by the State and handle a substantial share of the volume.

Total sales of fresh fruits and vegetables at shipping-point farmers' markets are estimated at $63 million in 1948, $81 million in 1954, and $87 million in 1956. Sales at cooperative farmers' markets of approximately $10 million are included in each year. Many of the farmers' markets serve mainly the smaller growers and the larger producers seU directly to local shippers or brokers or to buyers in the wholesale markets.

Many larger producers pack and ship their own produce. A leading trade directory listed 5,935 grower-shippers in 1958 (table 1). This is nearly twice the 3,017 shippers listed. The ratio of grower-shippers to shippers is higher than the national average in the New England and the North Central States, about average in the Middle Atlantic and the South Atlantic States, and below average in the South Central and the \\^estern States.

Buying brokers are most numerous in the major production areas distant from market, especially in Florida and California. The 227 buying brokers which the Census counted in 1954 had average sales of $645,000 and average operating expenses of 10.8 percent of sales. Since the Census counts only firms with paid employees, several times as many one-man buying brokers probably were not included. The average sales of these one-man operations were probably somewhat smaller than the sales of those counted.

TABLE 1.—Shipping-point produce marketing firms, 1958

Geographic division Grower- shipper

Shipper Buying broker

Selling broker

Shipper's sales

agency, distributor

Total

New England _ ___ Firms

503 840

1,081 542

1, 164 145 534 348 778

Firms 160 456 367 216 594 116 365 261 482

Firms 13

120 100

15 415

23 58 69

198

Firms Firms 8 8

21

Firms 682

Middle Atlantic _ _ 8 7 3

18 1 6 1 8

1,432 East North Central 1,576 West North Central _ _ _ 776 South Atlantic 30

8 13

9 25

2,221 East South Central._ _ __ __ _ 293 West South Central 976 Mountain _ _ _ _ 688 Pacific - - 1,491

United States 5,935 3,017 1,011 52 120 10, 135

Fresh Yearbook Issue

Buying brokers represent a number of whole- salers or retail organizations in buying at shipping point. Many of them move from one shipping point to another, following the crops. They bought 8 percent of the produce for the firms in the major wholesale markets covered in this study.

Farmer cooperatives sold $859 million of fruits and vegetables in 1958-59 {12). This includes not only fruits and vegetables for the fresh market but also those which were canned, frozen, or processed in other forms. The business of bargaining associations which do not physically handle the merchandise is also included. These sales were made by 714 fruit and vegetable cooperatives and 48 other associations whose primary business was in farm supplies or in marketing other farm products. Local co- operatives sold $516 milhon of fruits and vegetables. Regional associations had fruit and vegetable sales of $741 million, including $398 million sold for member local associations, also included in the sales of local cooperatives.

Perhaps a thousand or more truckers buy produce at shipping point, haul it to market, and sell it for whatever profit they can make. Many are for-hire truckers who regularly or occasionally purchase a load to provide themselves with a backhaul. For instance, some truckers who regularly haul fruits and vegetables from Florida, Georgia, and other southern States on a for-hire basis make a fairly regular practice of buying a load of apples in the Appalachian area, often the lower quahty merchandise, and hauling it to Atlanta or other southern cities for sale. Thus they obtain a return load and the possibility of making a profit if market conditions are good.

Nearly 4,400 truckers of fresh fruits and vegetables were hcensed by the Department of Agricidture imder the Perishable Agricultural Commodities Act in 1959. Those licensed in- cluded most of the truck jobbers as well as a fairly large number of for-hire truckers who wished to have a PACA license if the opportunity for a profitable backhaul became available, or for other reasons. Some probably did not have the opportunity, and many others probably took advantage of it only once or twice during the year.

Wholesale Markets Probably 90 percent of the fresh fruits and

vegetables consumed in this country passes through one or more wholesale markets. Not all of this is handled by wholesalers. Farmers sell an unknown proportion directly to consmners at roadside stands, at the farm, and on the tree. They also sell some produce directly to retail stores.

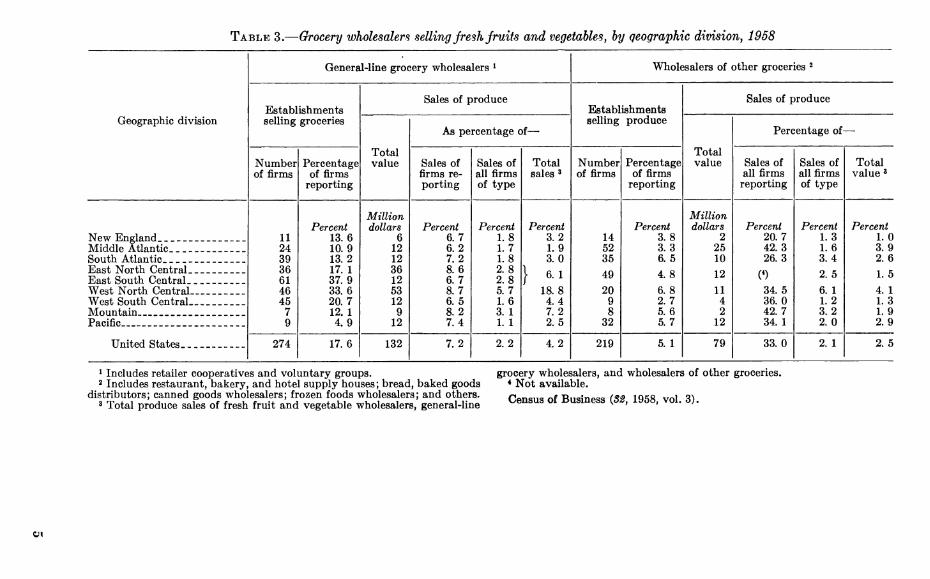

Most wholesalers handling fresh fruits and vegetables are produce specialists. Some firms whose main line of business is in dry groceries or other types of food also handle some produce (table 2). Fruit and vegetable wholesalers sold 93 percent of the fruits and vegetables sold by all the wholesalers with identifiable sales of produce in 1958. General-line grocery wholesalers, includ- ing retailer cooperatives and voluntary groups, sold 4 percent of the total. Wholesalers selling other groceries—probably mostly frozen foods wholesalers—sold 2.6 percent of the total, and meat, poultry, and fish wholesalers accounted for 0.4 percent.

TABLE 2.—Merchant wholesalers selling fresh fruits and vegetablesj United States, 1958

Type of wholesaler

Establishments selling fresh fruits and

vegetables

Total

Fresh fruit, vegetable General-line grocery ^ Poultry, poultry products Fish, seafood Meat, meat products Other groceries and related products ^_-

Total produce wholesalers

Number 6,291

274 25

219

6,886

Percentage of each type of

wholesaler

Sales of fresh fruits and vegetables "

Total value

Percent 100.0 17.6 1.9 1.0 2.3 5. 1

Million dollars

2,925 132

2 1 7

79

As percentage of-

Total produce

sales

Percent 92.9 4.2

. 1

.02

. 2 2. 6

3, 146 100. 0

All sales of firms selling

produce

Percent 94.5 7.2 8.5

21. 1 10. 1 33.0

All sales of firms of this type

Percent 94. 5

2. 2 .2 . 2 .3

2. 1

1 Sales of fresh fruit, vegetable wholesalers represent sales of all firms in the group. Sales of other types of wholesalers are only those of firms reporting commodity- line sales.

2 Includes retailer cooperatives and voluntary groups.

3 Includes restaurant, bakery, hotel-supply houses; bread, baked goods distributors; canned foods whole- salers; frozen foods wholesalers; and others.

Census of Business {31, 1958, vol. 3).

TABLE 3.— Grocery wholesalers selling fresh fruits and vegetablesj by geographic division, 1958

General-line grocery wholesalers ^ Wholesalers of other groceries ^

Establishments selling groceries

Sales of produce Establishments selling produce

Sales of produce

Geographic division

Total value

As percentage of—

Total value

Percentage of —

Number of firms

Percentage of firms

reporting

Sales of firms re- porting

Sales of all firms of type

Total sales 3

Number of firms

Percentage of firms

reporting

Sales of all firms reporting

Sales of all firms of type

Total value 3

New England 11 24 39 36 61 46 45

7 9

Percent 13.6 10.9 13.2 17. 1 37.9 33.6 20.7 12. 1 4.9

Million dollars

6 12 12 36 12 53 12

9 12

Percent 6.7 6.2 7.2 8.6 6.7 8.7 6.5 8.2 7.4

Percent 1.8 1.7 1.8 2.8 2.8 5.7 1.6 3. 1 1. 1

Percent 3.2 1.9 3.0

} »■■ 18.8

4. 4 7.2 2.5

14 52 35

49

20 9 8

32

Percent 3.8 3.3 6.5

4.8

6.8 2.7 5.6 5.7

Million dollars

2 25 10 12

11 4 2

12

Percent 20.7 42.3 26.3

34.5 36.0 42.7 34. 1

Percent 1.3 1.6 3.4

2.5

6. 1 1.2 3.2 2.0

Percent 1. 0

Middle Atlantic 3.9 South Atlantic 2.6 East North Central 1.5 East South Central West North Central 4. 1 West South Central-__ 1.3 Mountain 1.9 Pacific 2.9

United States 274 17.6 132 7.2 2. 2 4.2 219 5. 1 79 33.0 2. 1 2.5

1 Includes retailer cooperatives and voluntary groups. 2 Includes restaurant, bakery, and hotel supply houses; bread, baked goods

distributors; canned goods wholesalers; frozen foods wholesalers; and others. 3 Total produce sales of fresh fruit and vegetable wholesalers, general-line

grocery wholesalers, and wholesalers of other groceries. * Not available. Census of Business (5^, 1958, vol. 3).

Only about 5 percent of the sales of fruit and vegetable wholesalers was of other products, principally dry groceries and frozen foods. Produce was a minor part of the sales of most of the other types of wholesalers, except those selling other groceries, who had about a third of their sales in produce, and the eight fish merchants with 21 percent of their sales in produce.

The general-line grocery wholesalers selling produce were concentrated to a considerable ex- tent in Minnesota, the Dakotas, Iowa, Nebraska, Missouri, and Kansas (table 3). Most wholesale grocers handling produce in this region and in the West South Central Region were units of "chain" organizations of wholesale grocers. There were only a few of these organizations in other parts of the country.

The wholesalers of other groceries selling prod- uce were scattered over the country, although they were more important in the Middle Atlantic and West North Central States than elsewhere (tables).

Pruit and vegetable wholesalers were less con- centrated in the larger cities than meat and specialty-line grocery wholesalers, but more con- centrated than poultry and egg wholesalers and general-line wholesalers. Conversely, fewer fruit and vegetable wholesalers were located in areas of less than 300,000 population than any of the other thi*ee types of food wholesalers.

The Markets Studied

The 52 markets covered in this study were chosen to represent 145 wholesale produce markets throughout the country, as follows:

Size of market (1,000 carlots) All markets

Sample markets

43 or more Number

7 6

13 7

48 16 12 36

Number 7

25 to 42 3 15 to 24 7 10 to 14 4 3to9 14 2to2.9 4 ltol.9-_ -. 4 Less than 1 _ 9

Total 145 52

The universe represented by this sample con- tains nearly all of the metropolitan areas with enough wholesalers so that they might be called 'Wholesale markets." In general, wholesalers outside the markets studied here are in cities or towns with one to four firms. Such places seldom have enough volume to generate more than token sales between wholesalers, so there is considerable justification in not calling such groups of firms *'wholesale markets."

In 1958, there were nearly 5,200 produce whole- salers in wholesale markets and 2,274 in all other places (table 4). Wholesale handlers in the whole-

sale markets averaged about 80 percent larger than those in other places. This is partly because truck jobbers were relatively more numerous in small towns, and they seldom handle more than 100 carlots apiece per year. Most of the primary handlers in the smaller cities and towns were receiver-jobbers. About 125 brokers were listed in these other towns and cities. Probably many of them were shipping-point brokers.

TABLE 4.—Number of wholesalers and retail orga- nizations fiandling produce, wholesale markets and all other places, 1958

Type of firm Wholesale markets

All other places

Total

Receiver, commission mer- chant

Firms

943

656 1,536

481

Firms

128

918 285

38

Firms

1 071 Receiver-jobber, service

wholesaler 1, 574 Jobber, purveyor. _ 1, 821 Prepackager, repacker 519

Total 3,616 1,369 4,985

Truck jobber. _ 540 89 30

112

452 101

is'

1, 192 Trucker. _ __ 190 Shioper 30 Importer, exporter 130

Total 771 771 1, 542

All wholesale handlers. 4,387 2, 140 6,527

Broker 420 78

136 10

166

126 5 3

546 Distributor 83 Sales aeencv ... 139 Auction __ 10 Bu3âng broker, buying office,

sales agent 166

All brokers and agen- cies - 810 134 944

All wholesalers 5,197 2,274 7,471

Chain 257 36 30 16

137 13 46

550

394 Retailer cooperative Voluntary group

49 76

Wholesale grocer 566

All firms 5,536 3,020 8,556

Over 100 chains, most of which were small, were located outside the wholesale markets. The aver- age produce volume per chain probably was considerably less than half that of chains in the wholesale markets. There were 550 wholesale grocers in these places listed as handlers of fruits and vegetables. A high proportion of them handled only a few "hardware" items, such as potatoes and onions, sometimes with the addition of apples and citrus. About half of these whole- sale grocers were located in the South Central States.

Truck jobbers were most often found in the less-urbanized areas—the South, the Midwest, and the Mountain States. Jobbers were con-

centrated in the Northeast, where they were close enough to terminal markets to obtain their sup- plies personally.

The wholesale markets in this study handled about 1.6 million carlots of produce in 1958. Wholesalers in other places probably sold about one-half million carlots, much of which was bought either from wholesale handlers or through brokers and distributors in these wholesale markets.

Types of Markets

The markets studied are divided into seven types on the basis of four major characteristics—• the size of the market and three functional attri- butes (table 5). The functions considered include the importance of each market as a local wholesale market, each market's importance as a supplier of out-of-town wholesale buyers, and the importance of retail organizations as suppliers of the market.

The seven largest markets, each handling 48,000 carlots or more, are designated primary markets. Secondary markets, handhng from 9,000 to 34,000 carlots apiece, were divided into three functional groups: (1) Local wholesale markets, with sales to local wholesalers averaging 19 percent of the net supply for resale; (2) out-of-town wholesale mar- kets, with sales to out-of-town wholesale buyers averaging 32 percent of the net supply for resale ; and (3) other secondary markets, where neither type of wholesale sales was of major importance.

Tertiary markets, each with a net supply of from 4,000 to 7,000 carrots, were divided into: (1) chain markets, where direct purchases by retail organizations averaged 54 percent of the net supply, and (2) other tertiary markets, where direct purchases by retail organizations averaged 25 percent of net supply. Small markets, with net supply of 1,000 to 3,000 carlots each, consti- tute the final category.

TABLE 5.—Characteristics oj wholesale produce markets, by type oj market, 1958

Type of market and location Net supply

Sales to local whole- salers by primary

and secondary handlers ^

Sales to out-of-town wholesalers, retail organizations, and

exports 2

Direct pur- chases by

retail organi- zations 3

Primary markets : New York _-

lyOOO carlots 236 141 121 70 58 51 48

Percent 31 27 23 14 16 13 29

Percent 17 35 47 13 41 22 12

Percent 21

Los Angeles 9 Chicaffo -- 17 Philadelphia _ 23 Boston 20 San Francisco - _- 17 Detroit 31

Average - 103 24 23 18

Secondary markets: Local wholesale :

Pittsburgh - - 34 30 24 20 19 19 17 14

26 23 11 16 15 17 19 29

24 17 4 2

28 19 26 24

24 Dallas-Fort Worth __ 23 Washington 36 Houston 20 Denver 32 Miami - 47 Milwaukee 38 Louisville -_ 31

Average - 23 19 18 29

Out-of-town wholesale : Atlanta 29

17 16 17 15 13 13

9

9 8 6 1

13 12

5 11

48 36 41 25 34 28 31 40

22 New Orieans 23 Albanv-Schenectadv-Trov _ 47 Columbia 9 Tamna-St. Petersburg 31 Salt Lake City -- __ 21 Oklahoma City ___ 35 Raleigh 51

Averaere 16 8 32 29 Other:

Seattle-Tacoma 22 21 17

9

5 4 6 9

17 13

3 4

35 Minneapolis-St. Paul 20 Portland. Oree_ - 25 Omaha -- -- 49

Average _ 15 7 8 33

See footnotes at end of table.

TABLE 5.—Characteristics oj wholesale produce markets, by type of market, 1958—Continued

Type of market and location Net supply

Sales to local whole- salers by primary

and secondary handlers ^

Sales to out-of-town wholesalers, retail organizations, and

exports 2

Direct pur- chases by

retail organi- zations *

Tertiary markets: Chain:

Wichita ___ _

1,000 carlots

6 5 5 5

Percent

8 25

0 6

Percent

8 3

14 10

Percent

37 45 85 66

Little Rock Portland, Maine _ Greenville

Average - 5 5 3 54

Other: El Paso 7

5 5 4

13 12 13 18

15 10 12 51

20 35 27 99

Tulsa - Spokane Huntington

Average 5 14 22 25

Small markets: Winston-Salem 3

3 3 3 3 2 2 1

9 1 7 3

48 28 13 11 28 15

1 10

Albuquerque Duluth-Superior 20

40 28 51 27

Charleston --- -_- Wheeling Butte 1 Lincoln Other West Virginia 17

Average 2 3 22 18

1 Percentage of net supply for resale. 2 Excluding sales to out-of-town truck jobbers.

• Percentage of net supply.

Wholesale Market Structure 1958-59 The elements composing the market for fresh

fruits and vegetables or any other commodity are the firms which buy, sell, and handle the product. The relationships among those firms in buying, seUing, and handüng the product and in ownership or control constitute the structure or organization of the market.

Number, Size, and Type of Firms The wholesale produce markets of the United

States, comprised of 5,541 firms, had total sales of 2.7 million carlots in 1958 (tables 6 and 7). The sales figures included sales from one whole- saler to another^ as well as sales to retail organi- zations. About 1,600 primary handlers sold nearly 800,000 carlots. These included nearly 700 receivers, nearly 500 receiver-jobbers, and about 250 commission merchants.

Over 2,500 secondary handlers had total sales of 335,000 carlots. About 1,050 jobbers of five diflFerent types handled 148,000 carlots; 540 truck jobbers, 25,000; 484 purveyors and receiver- purveyors, 73,000; and 481 prepackagers and tomato repackers, 89,000 carlots. About 120 shippers and truckers sold 31,000 carlots and 112 importers and exporters sold 68,000 carlots of produce.

8

The 810 brokers and agencies had total sales of 849,000 carlots. These included 498 brokers and distributors seUing 495,000 carlots; 136 cooperative and importer's sales agencies with 257,000 carlots; 10 auctions with 46,000 carlots; 139 buying brokers and buying offices with 50,000 carlots; and 27 sales agents for New York City purveyors with 3,000 carlots.

There were 323 chains and affiliated groups which bought some produce directly from shipping point, not including many small chains which bought all of their produce from local wholesalers. These retail organizations had a total volume of 602,000 carlots of produce in 1958. In addition, 5 chain restaurants bought directly from shipping point.

Most wholesale handlers were small firms— nearly two-thirds sold less than 200 carlots in 1958 and another fifth sold between 200 and 499 carlots (table 6). Thirty-seven percent of the primary handlers, 81 percent of the secondary handlers, 71 percent of the shippers and truckers, and 46 percent of the importers and exporters sold less than 200 carlots a year. Wholesale handlers with sales of 1,000 carlots or more— 6 percent of the total—^made 38 percent of the sales of the entire group. The 10 percent with

TABLE'6.—Number oj firms oj each type and percentage distribution by size, U.S. wholesale produce markets, 1958-59

All firms

Size of firm, by annual volume of sales

Type of firm Less than

200 carlots

200 to 499 carlots

500 to 999 carlots

1,000 to 1,999

carlots

2,000 to 3,999

carlots

4,000 or more

carlots

Primary handlers: Receiver

Number 691 252 486

40 130

16

Percent 34 27 52 36 20 38

Percent 32 23 29 41 24 28

Percent 18 25 13 18 37

9

Percent 12 21

5 5

15 25

Percent 3 4 1

Percent 1

Commission merchant ^ _ _ 0) Receiver-jobber Commission wholesaler Service wholesaler 5 Wholesale grocer

Total 1,615 37 29 19 12 2 Ci)

Secondary handlers: Jobber 290

422 260

44 36

540 359 125 207 274

83 83 70 50 74 99 81 58 57 88

14 15 25 46 18

1 16 29 20 11

2 1 3 2 8

(0

2

Jobber (delivery) Banana jobber (}) Service jobber Secondary wholesaler Truck jobber Purveyor 3

12 17

0)

1 1 4

(0

Receiver-purveyor Prepackager 2 Tomato repacker

Total 2,557 81 14 3 1 (0 Shippers and truckers:

Mixed-load shipper 16 8 6

66 23

19 25 25

6 9

55 25 58

3

19 7 L.c.l. shipper 38 12 Packer-shipper 17 Merchant trucker 91

91 Itinerant trucker

Total .- 119 71

42 43 51

11

23 13 34

14

6 13 10

3

11 13 4

1

11 18

1

Importers and exporters: Importer 41

23 48

7 Commission importer Exporter

Total - 112 46 26 9 8 8 3

All wholfiSfllp. hiindlfirs 4,403 64 20 10 5 1 (0 Brokers and distributors :

Sellin g broker 362 28 30 48 30

11 8

10 8

13

22 21 36 15 44

27 39 17 27 33

28 28 26 19

7

12 4

11 23

3

1 Auction representative Terminal broker Carlot distributor 8 Distributor

Total 498 11 23 27 26 12 1

Sales agencies : Cooperative 79

57 23

7 31 12

23 13

17 23

5 23

1 21 Importer's.^

Total 136 15 26 19 19 12

50 2

9

Others: Auction 10

121 18 27

ñfi Buying broker 47

23 78

32 43 22

14 29

5 5 Buying office

Sales agent

All brokers and agencies _ 810 19 25 23 21 9 3

See footnotes at end of table.

TABLE 6.—Number ojfirms oj each type avd percentage distribution by size, U,S. wholesale produce market, 1958-59—Continned

AU firms

Size of firm, by annual volume of sales

Type of firm Less than

200 carlots

200 to 499 carlots

500 to 999 carlots

1,000 to 1,999

carlots

2,000 to 3,999

carlots

4,000 or more

carlots

Chains: Nflt.ional chain

Number 294 2 64

71 20

Percent Percent 6 6

22 28

Percent 6

21

25 5

Percent 46 21

17 15

Percent 16 31

23

Percent 26

"Rpffional chain 3

7 57

17 Local chain:

With warehouse 7 W^it.hniit "warehouse

Total 249 7 12 15 30 20 16

Tîpt.nilpr noonerative - 36 30

6 11 20

48 43

27 37

6 2 Vrklnn+ßrv ffroiiri - -

All rpt.ail oro"anizations 315 6 13 24 30 17 13

5 78 22

1 Less than 0.5 percent. 2 Number of warehouse divisions.

TABLE 7.—Sales by each type of firm, and percentage distribution by size, U.S. wholesale produce markets, 1958-59

Type of firm

Primary handlers: Receiver Commission merchant. Receiver-jobber Commission wholesaler Service wholesaler Wholesale grocer

Total or average..

Secondary handlers: Jobber Jobber (delivery) Banana jobber Service jobber Secondary wholesaler.. Truck jobber Purveyor Receiver-purveyor Prepackager Tomato repacker

Total or average. _

Shippers and truckers: Mixed-load shipper L.c.l. shipper Packer-shipper Merchant trucker Itinerant trucker

Total or average..

See footnote at end of table.

10

AU firms

1,000 carlots

365 169 144

14 92

7

792

33 52 47 10 6

25 46 27 60 29

335

12 7 5 5 2

31

Size of firm, by annual volume of sales

Less than 200

carlots

Percent 6 4

12 11 3 7

6

45 52 31 22 42 93 40 23 12 62

40

61 72

16

200 to 499 carlots

Percent 20 12 30 39 12 20

19

0)

39 35 42 54 28 7

37 38 20

32

C)

6 8

20 28

10

500 to 999 carlots

Percent 23 26 30 32 39 10

27

0)

12 6

12

30

0) 0)

0) 40

17

0) 44

58 19

34

1,000 to 1,999

carlots

Percent 31 40 23 18 28 63

31

C) 0) 0)

0) 0)

18

C)

"(0"

18

2,000 to 3,999

carlots

Percent 13

0) 5

18

13

0) 0)

10

0)

0)

4,000 or more

carlots

Percent

0)

i})

0)

TABLE 7.— Sales by each type oj firm, and percentage distribution by size, U.S. wholesale produce markets 1958-ô9—CoTLtm\iea

All firms

Size of firm, by annual volume of sales

Type of firm Less than

200 carlots

200 to 499 carlots

500 to 999 carlots

1,000 to 1,999

carlots

2,000 to 3,999 carlots

4,000 or more

carlots

Importers and exporters: Importer

Number 39 17 12

Percent 1 5 9

Percent 6 5

46

Percent 3

12 25

Percent 14 20 20

Percent 33 58

Percent 4

Commission importer Exporter

Total or average 68 3 13 9 16 34 24

All wholesale handlers 1,228 16 22 23 23 11 4

Brokers and distributors: Selling broker. 355

23 26 76 15

1 1 1 1 4

8 10 14

3 22

19 34 15 12 41

37 0)

34 15

C)

0) C)

36 35

0)

0) Auction representative Terminal broker Carlot distributor 34 Distributor

Total or a vera ce 495 1 8 19 33 31 7

Sales agencies : Cooperative 55

202 2 1

16 1

24 3

30 8

0) 17

0) Importer's 71

Total or average 257 1 4 7 13 16 58

Others: Auction 461

3

23 0)

77 Buying broker 12

7 48

28 27 42

32 0)

0) 0) Buying office

Sales agent

All brokers and agencies 849 2 8

1 1

5 19

15 24 25 26

Chains: National chain 261

167

107 7

2 6

13 0)

23 13

16 0)

17 36

44

57 Regional chain 1

1 13

45 Local chain:

With warehouse Without warehouse

Total or average 542 1 2 5 19 27 46

Retailer cooperative 35 25

1 3 9

34 38

35 53

0) en Voluntary group

\ j

All retail organizations 602 1 2 8 21 25 43

1 Withheld to avoid disclosure of individual firm's operations.

sales of 500 to 999 carlots accounted for another 23 percent. Most of the large firms were primary handlers—15 percent of them accounted for nearly half of the total sales of the group.

In contrast, there were few small brokers and agencies. Only 19 percent had sales of less than 200 carlots, while about 33 percent had sales oí 1,000 carlots or more, accounting for three-fourths of all sales of the group. Most of the small firms were buying brokers and sales agents, while the large firms were mostly selHng brokers, terminal brokers, carlot distributors, or sales agencies.

Most retau organizations are large. In 1958, 60 percent handled more than 1,000 carlots apiece. The local chains are considerably smaller than the national and regional groups. Retailer coopera- tives and voluntary groups are predominantly in the middle-size groups, between 500 and 2,000 carlots.

Type of Firm by Type of Market The distribution of different types of firms is an

important element in the organization of the vari- ous classes of markets. The organization of a

11

large and complex market such as New York or Chicago is different from the organization of a small, straightforward market such as Albu- querque or Lincoln. The large market performs a greater variety of functions and requires a greater variety of firms.

Receivers were foimd in all the primary markets and all the secondary markets but one, Oklahoma City. They were found in only half of the tertiary chain markets, all of the other tertiary markets, and only a quarter of the small markets. Sales of receivers accounted for a third of the net supply for resale in all wholesale markets, ranging from 9 percent in small markets to 40 percent in sec- ondary local wholesale markets (table 8).

Commission merchants and commission whole- salers are confined mostly to the larger markets. They sold 28 percent of the net supply for resale in primary markets and no more than 8 percent in any other type of market. They were most important in Philadelphia and Boston.

The importance of service wholesalers varied inversely with that of receivers in many of the markets. They were most important in small markets and tertiary chain markets. On the con- trary, there were no service wholesalers in four of the seven primary markets and in only one, Detroit, were they of much importance. Although five of the eight secondary local wholesale markets had service wholesalers, they were important only in the Dallas-Fort Worth and the Milwaukee markets. They played a major role in one out-of- town wholesale market—Salt Lake City—and a moderate one in New Orleans and Albany- Schenectady-Troy.

Wholesale grocers found in only seven of the wholesale markets studied were confined largely to the Plains and Mountain States.

Jobbers were most important in the more com- plex primary markets, where they accounted for 18 percent of the net supply for resale, ranging from 8 percent in San Francisco-Oakland to 32 percent in New York City, the largest market of all. They accounted for 16 to 17 percent of the net supply for resale in all other primary markets except Los Angeles. There were no jobbers in over half of the small markets and in Seattle- Tacoma and Portland, Maine.

Truck jobbers were not a major factor in any type of market, although they were fairly im- portant in a few markets—notably Louisville and Houston. About 20 percent of the markets had none at all.

Purveyors became important chiefly in cities with a substantial hotel and restaurant business such as Miami, Washington, San Francisco, and New York. Their importance in Greenville and Raleigh may be due more to institutional business.

Prepackagers and tomato repackers accounted for 6 to 9 percent of the net supply for resale in all types of markets except the tertiary. Two small markets had none.

Brokers and distributors were most important in markets located between Chicago and Denver east-west, and Minneapolis-St. Paul, and Houston and Dallas-Fort Worth north-south. Outside of this area, they accounted for more than 50 percent of the net supply for resale only in San Francisco- Oakland, Albany-Schenectady-Troy, and Wheel- ing.

Buying brokers were found only in the larger markets. They were most important in Boston and Philadelphia, where they represented cus- tomers both at the fruit auctions and the terminal sales, accounting for 11 to 12 percent of the volume. They handled 6 to 8 percent of the

TABLE 8.—Sales of specified types of wholesalers as percentage^ of net supply for resale, U.S. wholesale produce markets, 1958-59

Commis- sion mer- Serv- Job- Purveyors Repack- Brokers

Receiv- chants ice Whole- bers Truck and re- ers and and dis- Buying Type of market ers and com- whole- sale of all job- ceiver- pre- trib- brokers

mission salers grocers types bers purveyors pack- utors whole- agers salers

Per- Per- Per- Per- Per- Per^ Per- Per- Per- Per- cent cent cent cent cent cent cent cent cent cent

Primary 34 28 1 C) 18 2 7 7 40 7 Secondary:

Local wholesale 40 8 14 C) 9 4 9 9 48 2 Out-of-town whole-

sale 39 18

17 38

9

1 3

6 14

25 7

37

4

--

(0

10 4

10 5 9

3 2

3 6 2

4 3

13 8 2

9 6

11

1

45 65

27 36 31

1 Other _ -

Tertiary : Chain _ _ __ Other.. _ __ 6

Small

All markets 33 15 8 1 13 3 6 8 44 4

1 Less than 0.5 percent.

12

business in New York, Los Angeles, Detroit, and Pittsburgh and 4 percent in Chicago and New Orleans. In these cities the bulk of their pur- chases were made at the fruit auctions, except in Los Angeles, an important shipping market, and New Orleans where they bought substantial quan- tities of bananas.

Firm Size and Market Type

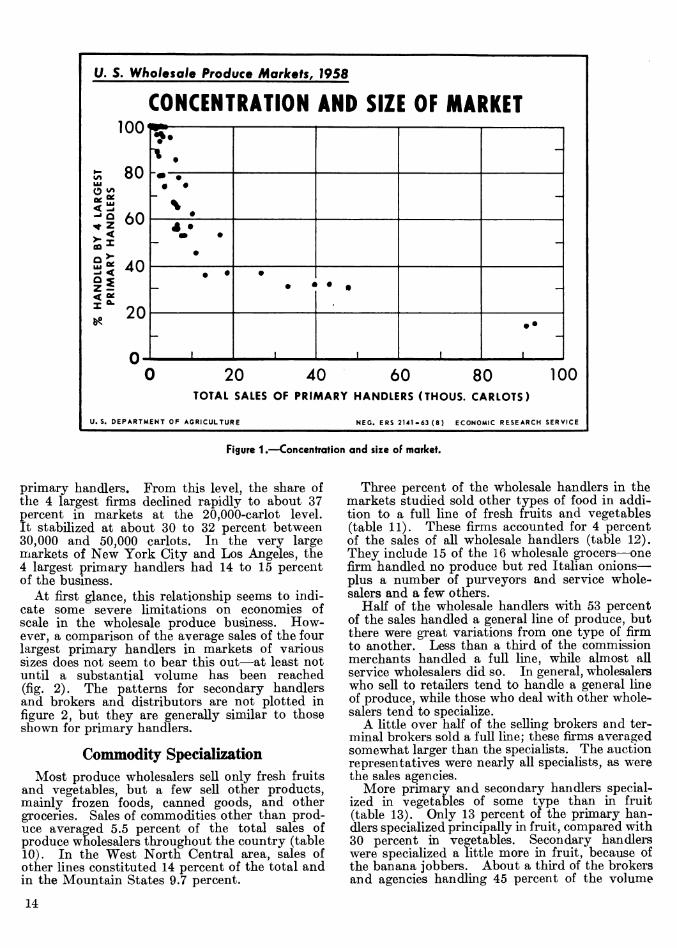

The largest wholesalers are foimd in the largest markets. Firms seUing as much as 4,000 carlots a year were located only in the primary markets (table 9). The largest firms accoimted for 8 per- cent of the sales of primary handlers in primary markets and 12 percent of the sales of brokers and distributors. In secondary markets, the larg-

est firms of primary handlers and of brokers and distributors sold between 2,000 and 3,999 carlots. In tertiary and small markets, the largest firms were generally in the next smaller size class.

Secondary handlers averaged smaller than either primary handlers or brokers and distributors (table 9). However, the pattern of larger firms in larger markets is similar to that of the other groups of firms, except that the largest firm in the primary markets were in the 2,000 to 3,999 carlot group.

Concentration, as measured by the share of the 4 largest primary handlers, is almost entirely a function of the size of the market (fig. 1). In the smallest markets, the four largest primary han- dlers did from 95 to 100 percent of the business. In some markets, there were only two or three

TABLE 9.—Percentage distribution of volume sold by major groups of handlers in specified types of markets^ by size of firm, U.S. wholesale produce markets, 1958-59

Firms with sales of—

Type of handler and market Less than

200 carlots

200 to 499

carlots

500 to 999

carlots

1,000 to 1,999

carlots

2,000 to 3,999

carlots

4,000 or more

carlots

All firms

Primary Handlers

Primary

Percent

4

8 8 4

8 10 20

Percent

16

22 19 22

34 16 33

Percent

22

19 21 45

58 39 38

Percent

33

40 41 23

Percent

17

11 11 6

Percent

8

Percent

100 Secondary:

Ijonal wholesale 100 Out-of-town wholesale - 100 Other 100

Tertiary : Chain 100 Other 35

9 100

Small - - 100

All markets 6 19 26 33 12 4 100

Secondary Handlers

Primary 37

38 50 58

34 33 47

30

40 25 24

66 32 36

15

17 25 18

12

5

6 100 Secondary :

Local wholesale _ 100 Out-of-town wholesale 100 Other 100

Tertiary: Chain 100 Other 35

17 100

Small 100

All markets 40 32 16 9 3 100

Brokers and Distributors

Primary 2

1 0)

1

5

9

6 3 5

16 23 16

25

23 11 23

26 54

26

41 27 29

53 23 62

26

29 59 42

12 100 Secondary:

Local wholesale 100 Out-of-town wholesale 100 Other 100

Tertiary: Chain 100 Other ___ - 100

Small -- - - -- 22 100

All markets __ _ _ 1 8 23 31 32 5 100

Less than 0.5 percent.

13

1 U. s. Wholesale Produce Markets, 1958

%

HA

ND

LE

D

BY

4 LA

RG

ES

T P

RIM

AR

Y

HA

ND

LE

RS

^

K3

i^

O

0

0

O

CONCENTRATION AND SIZE OF MARKET

-

• • • • -

4 • m •

• -

• • • • * • • -

1 1 1 1

• •

1

0 20 40 60 80 100 TOTAL SALES OF PRIMARY HANDLERS (THOUS. CARLOTS)

U.S. DEPARTMENT OF AGRICULTURE NEC. ERS 2141-63(8) ECONOMIC RESEARCH SERVICE

Figure 1.—Concentration and size of market.

primary handlers. From this level, the share of the 4 largest firms declined rapidly to about 37 percent in markets at the 20,000-carlot level. It stabilized at about 30 to 32 percent between 30,000 and 50,000 carlots. In the very large markets of New York City and Los Angeles, the 4 largest primary handlers had 14 to 15 percent of the business.

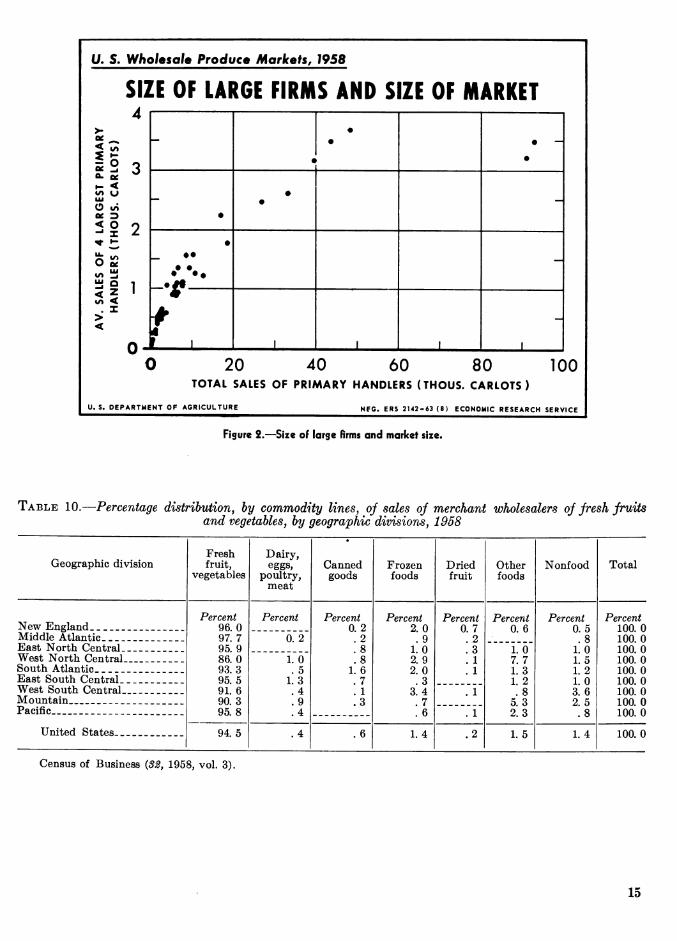

At first glance, this relationship seems to indi- cate some severe limitations on economies of scale in the wholesale produce business. How- ever, a comparison of the average sales of the four largest primary handlers in markets of various sizes does not seem to bear this out—at least not until a substantial volume has been reached (fig. 2). The patterns for secondary handlers and brokers and distributors are not plotted in figure 2, but they are generally similar to those shown for primary handlers.

Commodity Specialization Most produce wholesalers sell only fresh fruits

and vegetables, but a few sell other products, mainly frozen foods, canned goods, and other groceries. Sales of commodities other than prod- uce averaged 5.5 percent of the total sales of produce wholesalers throughout the country (table 10). In the West North Central area, sales of other lines constituted 14 percent of the total and in the Mountain States 9.7 percent.

Three percent of the wholesale handlers in the markets studied sold other types of food in addi- tion to a full line of fresh fruits and vegetables (table 11). These firms accounted for 4 percent of the sales of all wholesale handlers (table 12). They include 15 of the 16 wholesale grocers—one firm handled no produce but red Italian onions— plus a number of pm*veyors and service whole- salers and a few others.

Half of the wholesale handlers with 53 percent of the sales handled a general line of produce, but there were great variations from one type of firm to another. Less than a third of the commission merchants handled a full line, while almost all service wholesalers did so. In general, wholesalers who sell to retailers tend to handle a general line of produce, while those who deal with other whole- salers tend to specialize.

A little over half of the selling brokers and ter- minal brokers sold a full line; these firms averaged somewhat larger than the specialists. The auction representatives were nearly all specialists, as were the sales agencies.

More primary and secondary handlers special- ized in vegetables of some type than in fruit (table 13). Only 13 percent of the primary han- dlers specialized principally in fruit, compared with 30 percent in vegetables. Secondary handlei*s were specialized a little more in fruit, because of the banana jobbers. About a third of the brokers and agencies handling 45 percent of the volume

14

U. s. Whofeso/e Produce Markets, 1958

SIZE OF LARGE FIRMS AND SIZE OF MARKET

<

O

<

O in

> <

4 •

o

< u

O

3

2

« • • —

•

• • -

X •

tu

Û 1

—

< X

•

n- 1... 1 1 J 20 40 60 80 100

TOTAL SALES OF PRIMARY HANDLERS (THOUS. CARLOTS )

DEPARTMENT OF AGRICULTURE MFC. ERS 2I«-63 {«) ECONOMIC RESEARCH SERVICE

Figure S.—^Size of large firms and market size.

TABLE 10.—Percentage distnbution, by commodity lines, of sales of merchant wholesalers of fresh fruits and vegetables, by geographic divisions, 1958

Geographic division Fresh fruit,

vegetables

Dairy, eggs,

poultry, meat

Canned goods

Frozen foods

Dried fruit

Other foods

Nonfood Total

New England Percent

96.0 97.7 95.9 86.0 93.3 95.5 91. 6 90.3 95.8

Percent Percent 0.2 .2 .8 .8

1. 6 .7 . 1 .3

Percent 2.0 .9

1.0 2.9 2.0 .3

3.4 .7 .6

Percent 0.7 .2 .3 . 1 . 1 ...

__.

Percent 0. 6

Ï."Ô' 7.7 1.3 1.2 .8

5.3 2.3

Percent 0.5 .8

1.0 1. 5 1.2 1.0 3.6 2.5 .8

Percent 100 0

Middle Atlantic _ 0.2 100 0 East North Central__ _ _ _. 100 0 West North Central _ _ 1.0

. 5 1.3 .4 .9 .4

100 0 South Atlantic _ 100 0 East South Central _ 100 0 West South Central.__ 100 0 Mountain _ 100 0 Pacific 100 0

United States 94.5 .4 .6 1.4 .2 1.5 1.4 100 0

Census of Business {SZ, 1958, vol. 3).

15

TABLE 11.—Degree oj specialization oj wholesalers, by type of firm, U.S. wholesale produce markets, (Percentage of each type of firm)

1958-59

Firms handling complete line of produce Firms specializing in —

Type of firm No speciali- zation

Some speciali- zation

Plus other

types of food

Several com-

modity classes

One class of

com- modities

A single com-

modity

Several commodi-

ties of different classes

Total

Primary handlers: Receiver

Percent 36 23 67 20 83

Percent 2 7 2 3 3

Percent

__

___

94

Percent 22 27

8 51

2

Percent 21 20

9 12

1 6

Percent 11

5 7 3

Percent 8

18 4

11

Percent 100

Commission merchant 100 Receiver-jobber 100 Commission wholesaler. __ 100 Service wholesaler 100 Wholesale grocer 100

Average 47 3 2 18 15 7 8 100

Secondary handlers: Jobber 47

71 3 3

1 2

22 13

9 4

8 1

100 5 3 3 _-

21 93

10 6

100 Jobber (delivery) 100 Banana jobber 100 Service jobber 88

38 73 63 70

5

5 6 1 2 2 9

2 3

15 3 4

16 7

100 Secondary wholesaler

--- 4

37 5 9

11 16

13 4 2 8

33

100 Truck jobber _ 100 Purveyor 100 Receiver-purveyor _ 100 Prepackager 100 Tomato repacker 100

Average 47 2 4 9 6 24 8 100

Shippers and truckers: Mixed-load shipper 28

76 17

7

53 12

13 6 12

100 L.c.l. shipper 100 Packer-shipper 50

21 35

33 20 30

100 Merchant trucker. 31

15 21 20

100 Itinerant trucker 100

Average 14 28 23 18 17 100

Importers and exporters: Importer 20

45 12

38 18 19

42 33 11

100 Commission importer __ 4

19 100

Exporter 5 19 15 100

Average 9 2 8 7 22 25 27 100

All wholesale handlers 45 2 3 13 10 18 9 100

Brokers and distributors: Selling broker 43 6

4 2 18

47 23 17 10

15 38

3 17 10

10 11 18 48 40

6 100 Auction representative« _* 100 Terminal broker 51

12 37

5 100 Carlot distributor 2 4 100 Distributor 3 100

Average 38 5 2 19 16 16 4 100

Sales agencies: Cooperative 3 1 88 1

100 7 100

Importer's _ _ 100

Average-_ 1 1 51 43 4 100

Others: Auction 100

22 100

Buying broker 57 89

100

37

4 13 4 11

100 Buying office 100 Sales agent 100

4 1 16 All brokers and agencies 20 18 4 100

1 Less than 0.5 percent.

16

TABLE 12.—Degree of specialization oj wholesalers ^ by type of firm, U.S. wholesale produce markets, 1958-59 (Percentage of volume of each type of firm)

Firms handling complete line of produce Firms specializing in—

Type of firm No speciali- zation

Some speciali- zation

Plus other

types of food

Several com-

modity classes

One class of

com- modities