the technology and cost to implement next generation...

TRANSCRIPT

The Technology And Cost To Implement Next Generation Device

Technologies.

Mark Thirsk Linx Consulting

2

q Major technological challenges q Maturing industry with slower growth q Cost challenges q EUV and 450mm q Rapid introduction of new materials

n Linx Consulting and IC Knowledge have developed a unique modeling capability that can evaluate these scenarios in a detailed and self consistent manner.

Overview

3

The Markets We Serve

Chemical Exports Electronics Exports Electronics Imports

© Copyright SASI Group (University of Sheffield) and Mark Newman (University of Michigan).

4

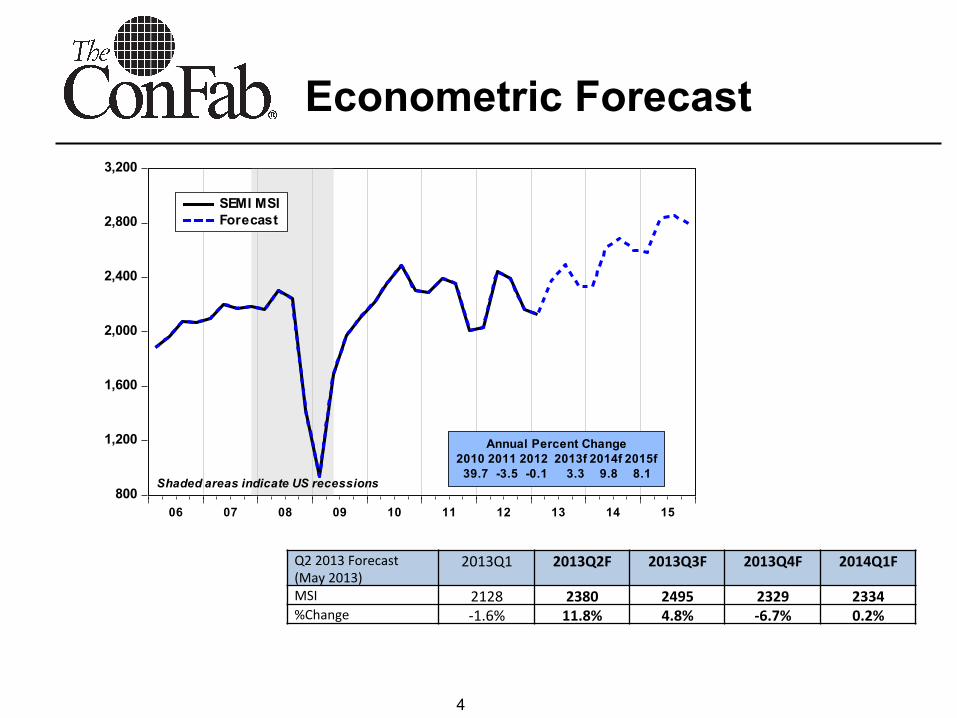

Econometric Forecast

800

1,200

1,600

2,000

2,400

2,800

3,200

06 07 08 09 10 11 12 13 14 15

SEMI MSIForecast

Shaded areas indicate US recessions

Annual Percent Change2010 2011 2012 2013f 2014f 2015f

39.7 -3.5 -0.1 3.3 9.8 8.1

Q2 2013 Forecast (May 2013)

2013Q1 2013Q2F 2013Q3F 2013Q4F 2014Q1F

MSI 2128 2380 2495 2329 2334 %Change -‐1.6% 11.8% 4.8% -‐6.7% 0.2%

5

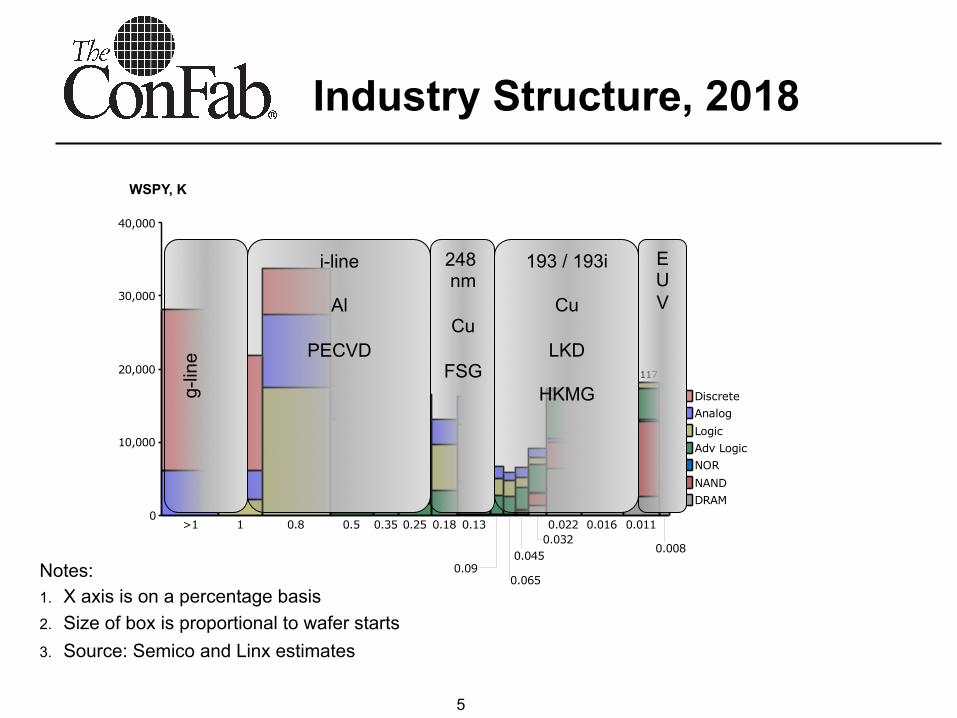

Industry Structure, 2018

0

10,000

20,000

30,000

40,000

>1 1 0.8 0.5 0.35 0.25 0.18 0.13 0.022 0.016

20,826

0.011

18,117

0.090.065

0.0450.032

0.008

DRAMNANDNORAdv LogicLogicAnalogDiscrete

Notes: 1. X axis is on a percentage basis 2. Size of box is proportional to wafer starts 3. Source: Semico and Linx estimates

WSPY, K g-

line

i-line Al

PECVD

248 nm

Cu

FSG

193 / 193i

Cu

LKD

HKMG

EUV

6

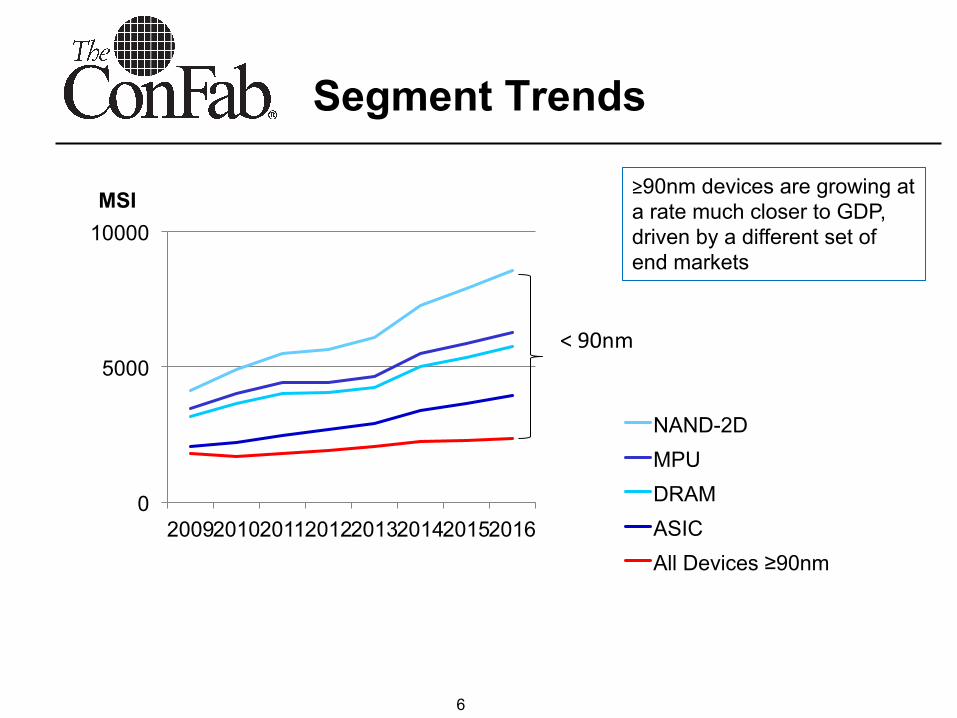

Segment Trends

0

5000

10000

2009 2010 2011 2012 2013 2014 2015 2016

MSI

NAND-2D MPU DRAM ASIC All Devices ≥90nm

< 90nm

≥90nm devices are growing at a rate much closer to GDP, driven by a different set of end markets

7

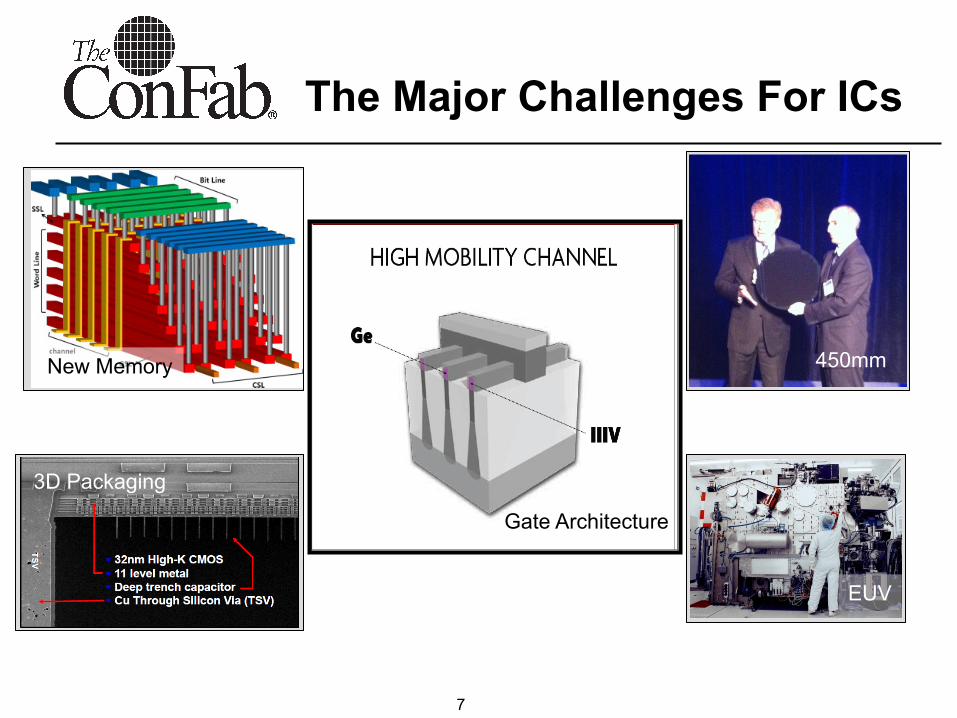

The Major Challenges For ICs

3D Packaging

450mm

Gate Architecture

EUV

New Memory

8

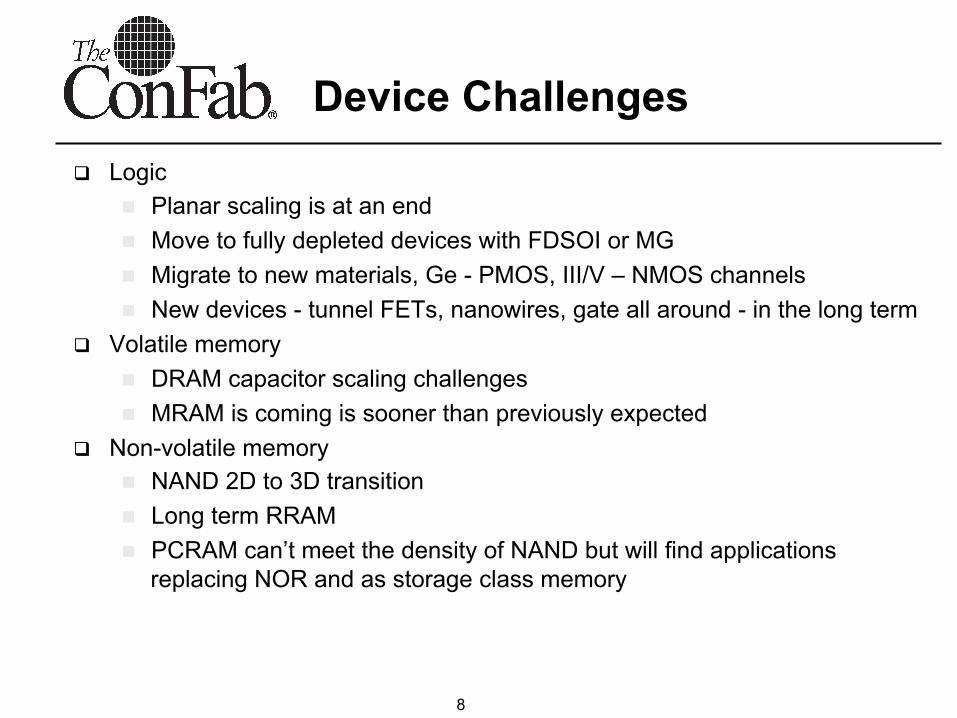

q Logic n Planar scaling is at an end n Move to fully depleted devices with FDSOI or MG n Migrate to new materials, Ge - PMOS, III/V – NMOS channels n New devices - tunnel FETs, nanowires, gate all around - in the long term

q Volatile memory n DRAM capacitor scaling challenges n MRAM is coming is sooner than previously expected

q Non-volatile memory n NAND 2D to 3D transition n Long term RRAM n PCRAM can’t meet the density of NAND but will find applications

replacing NOR and as storage class memory

Device Challenges

9

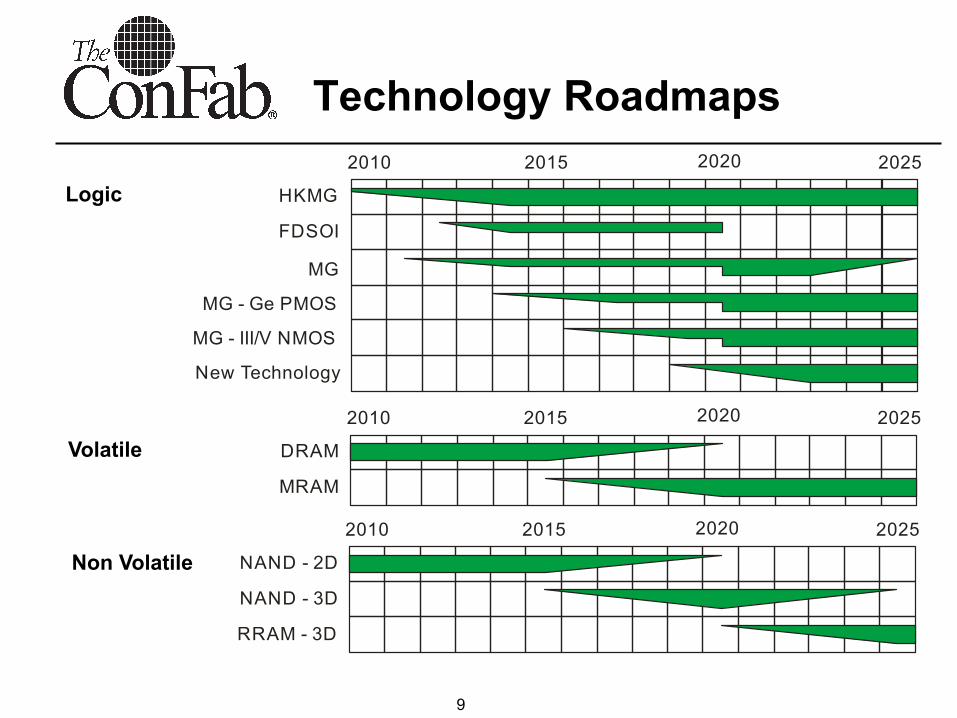

Technology Roadmaps 2010

HKMG

FDSOI

MG

MG - Ge PMOS

MG - III/V NMOS

New Technology

2015 2020 2025

2010

DRAM

MRAM

2015 2020 2025

2010

NAND - 2D

RRAM - 3D

NAND - 3D

2015 2020 2025

Logic

Volatile

Non Volatile

10

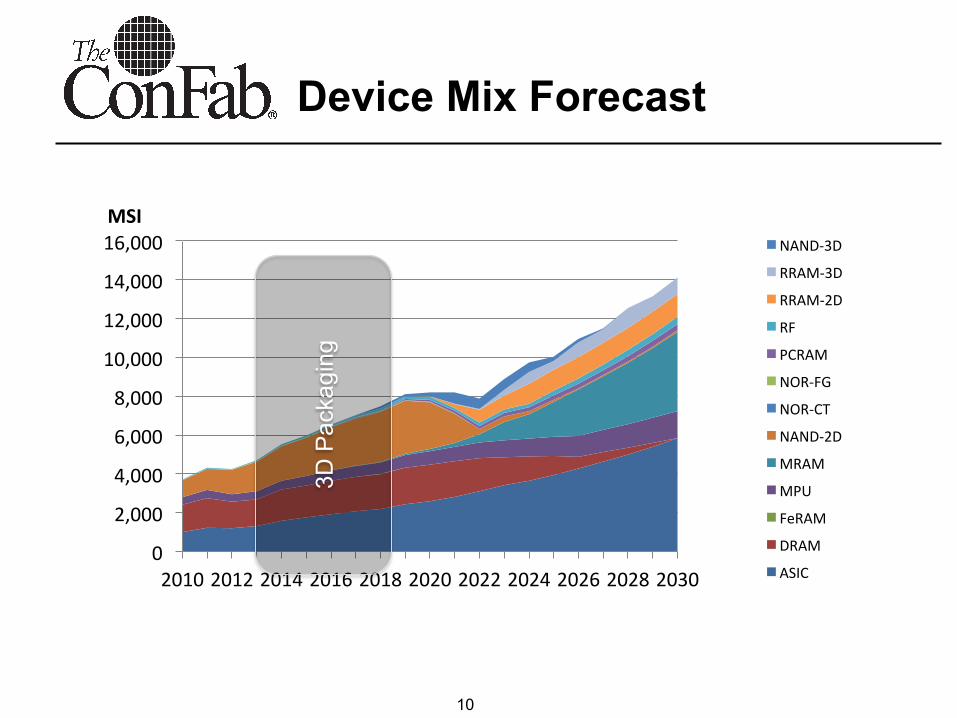

Device Mix Forecast

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

MSI NAND-‐3D

RRAM-‐3D

RRAM-‐2D

RF

PCRAM

NOR-‐FG

NOR-‐CT

NAND-‐2D

MRAM

MPU

FeRAM

DRAM

ASIC

3D P

acka

ging

11

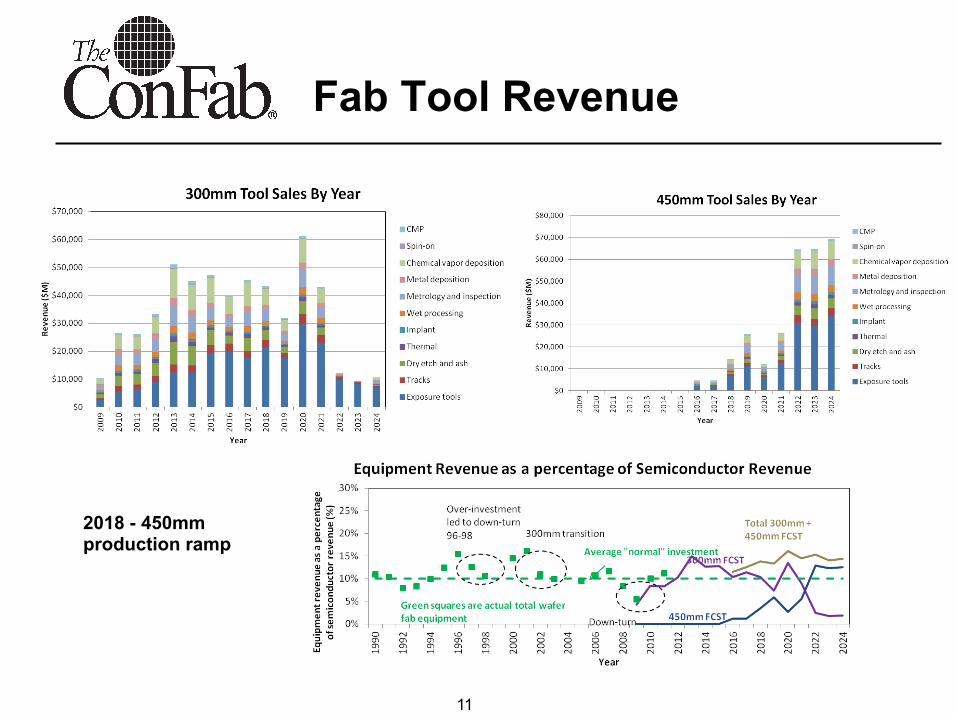

2018 - 450mm production ramp

Fab Tool Revenue

12

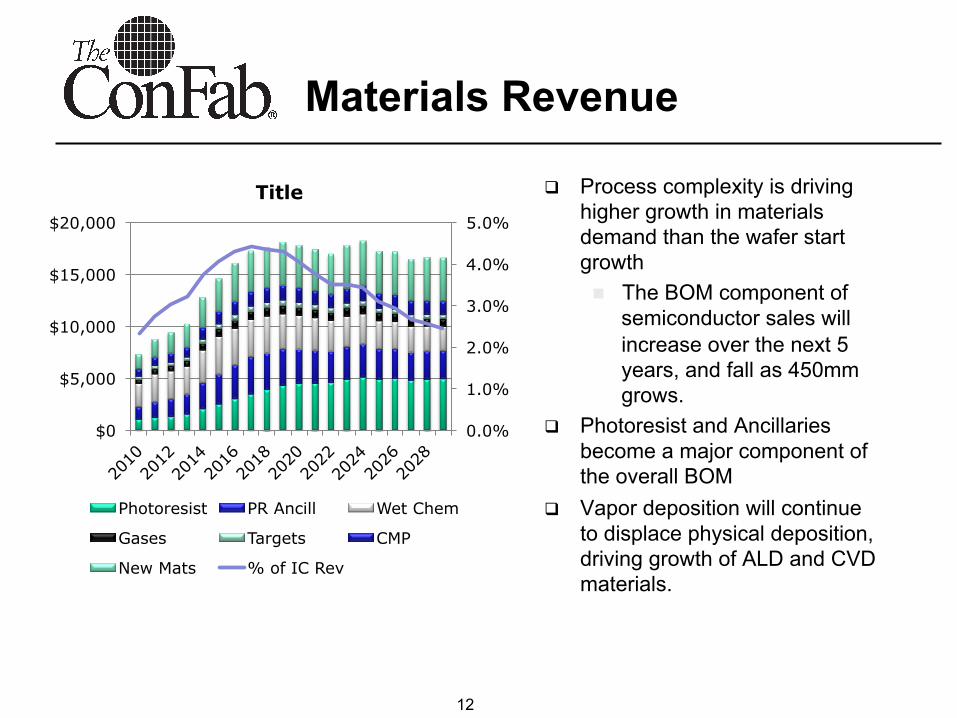

Materials Revenue

q Process complexity is driving higher growth in materials demand than the wafer start growth n The BOM component of

semiconductor sales will increase over the next 5 years, and fall as 450mm grows.

q Photoresist and Ancillaries become a major component of the overall BOM

q Vapor deposition will continue to displace physical deposition, driving growth of ALD and CVD materials.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

$0

$5,000

$10,000

$15,000

$20,000

Title

Photoresist PR Ancill Wet Chem

Gases Targets CMP

New Mats % of IC Rev

13

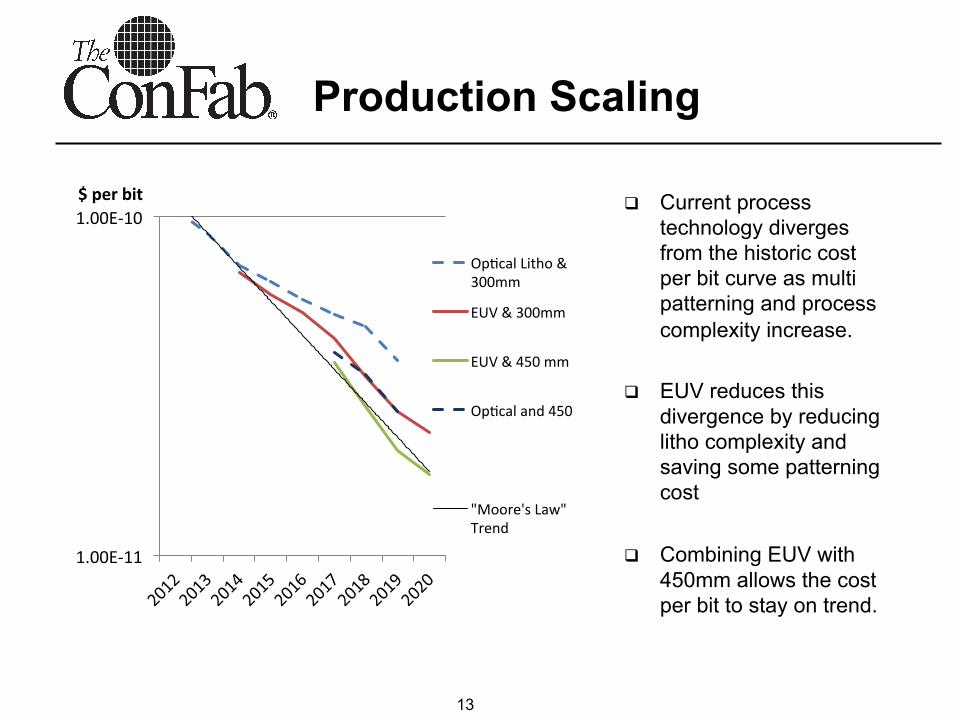

Production Scaling

q Current process technology diverges from the historic cost per bit curve as multi patterning and process complexity increase.

q EUV reduces this divergence by reducing litho complexity and saving some patterning cost

q Combining EUV with 450mm allows the cost per bit to stay on trend.

1.00E-‐11

1.00E-‐10

1.00E-‐09

$ per bit

OpOcal Litho & 300mm

EUV & 300mm

EUV & 450 mm

OpOcal and 450

Minimum

"Moore's Law" Trend

14

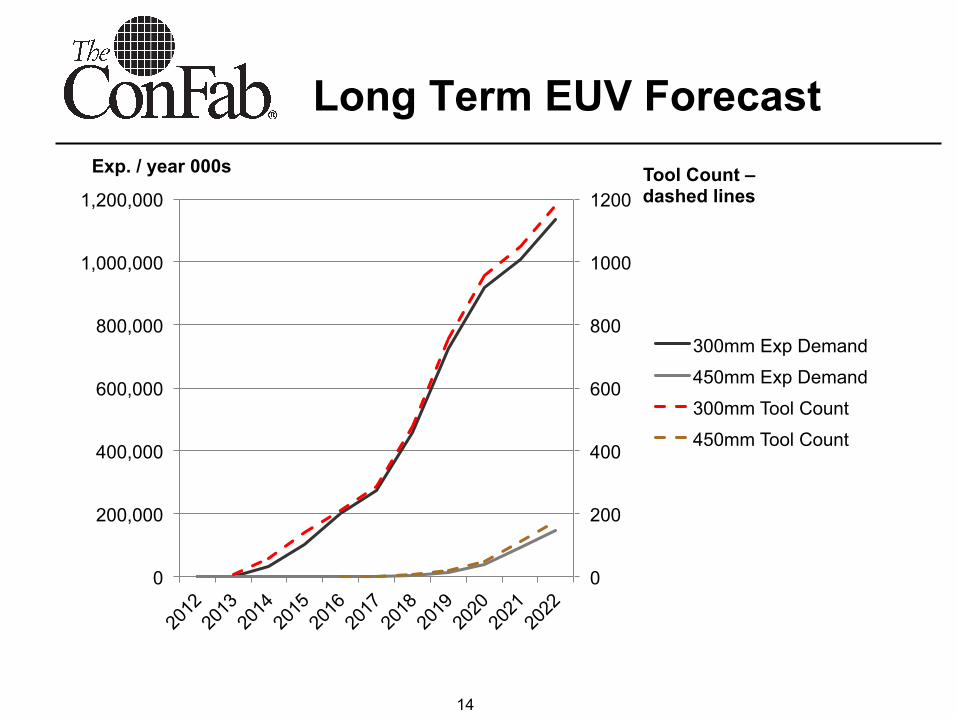

Long Term EUV Forecast

0

200

400

600

800

1000

1200

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000 Tool Count – dashed lines

Exp. / year 000s

300mm Exp Demand

450mm Exp Demand

300mm Tool Count

450mm Tool Count

15

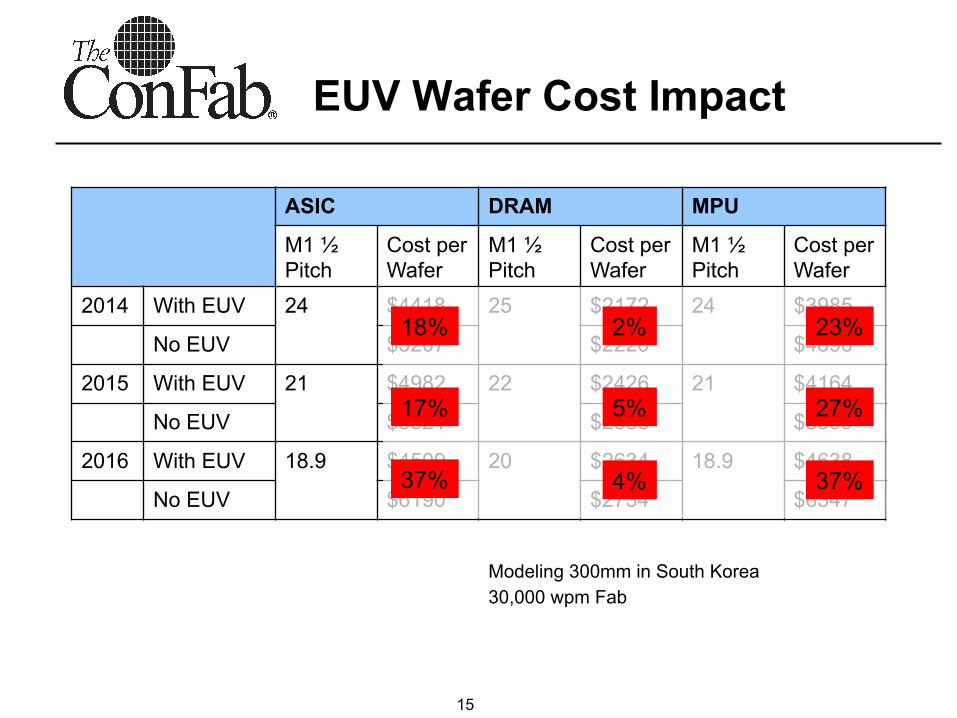

EUV Wafer Cost Impact

ASIC DRAM MPU

M1 ½ Pitch

Cost per Wafer

M1 ½ Pitch

Cost per Wafer

M1 ½ Pitch

Cost per Wafer

2014 With EUV 24 $4418 25 $2172 24 $3985

No EUV $5207 $2220 $4890

2015 With EUV 21 $4982 22 $2426 21 $4164

No EUV $5821 $2538 $5359

2016 With EUV 18.9 $4509 20 $2634 18.9 $4638

No EUV $6190 $2734 $6347

Modeling 300mm in South Korea 30,000 wpm Fab

18%

17%

37%

2%

5%

4%

23%

27%

37%

16

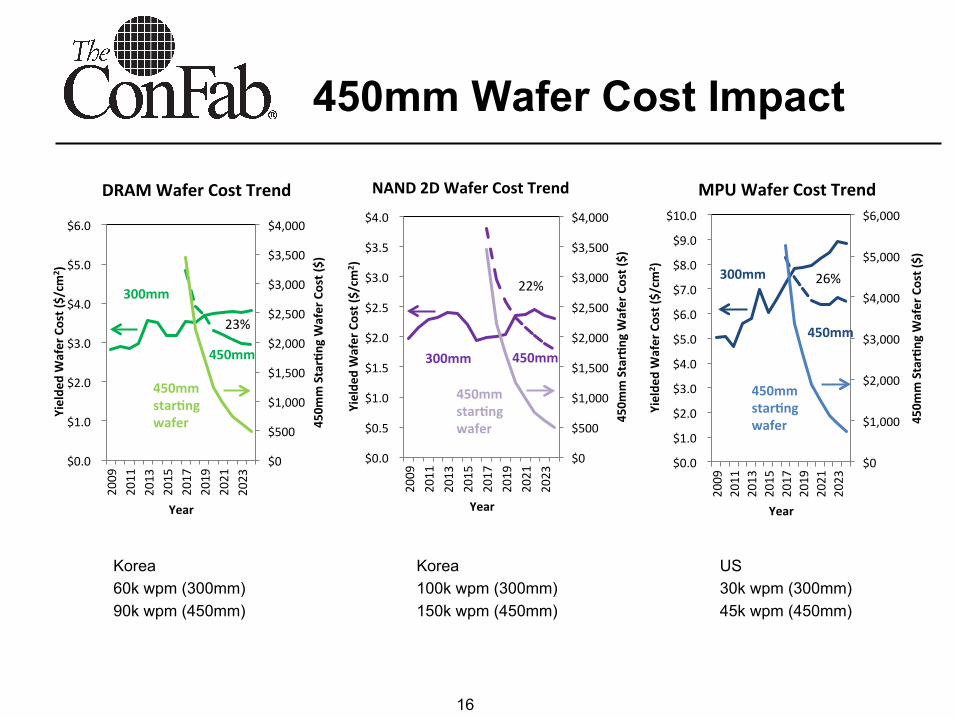

450mm Wafer Cost Impact

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

2009

2011

2013

2015

2017

2019

2021

2023

450m

m Star=ng W

afer Cost ($)

Yielde

d Wafer Cost ($/cm

2 )

Year

DRAM Wafer Cost Trend

300mm

450mm

23%

450mm star=ng wafer

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

2009

2011

2013

2015

2017

2019

2021

2023

450m

m Star=ng W

afer Cost ($)

Yielde

d Wafer Cost ($/cm

2 )

Year

NAND 2D Wafer Cost Trend

300mm 450mm

22%

450mm star=ng wafer

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

$9.0

$10.0

2009

2011

2013

2015

2017

2019

2021

2023

450m

m Star=ng W

afer Cost ($)

Yielde

d Wafer Cost ($/cm

2 )

Year

MPU Wafer Cost Trend

300mm

450mm

26%

450mm star=ng wafer

Korea 60k wpm (300mm) 90k wpm (450mm)

Korea 100k wpm (300mm) 150k wpm (450mm)

US 30k wpm (300mm) 45k wpm (450mm)

17

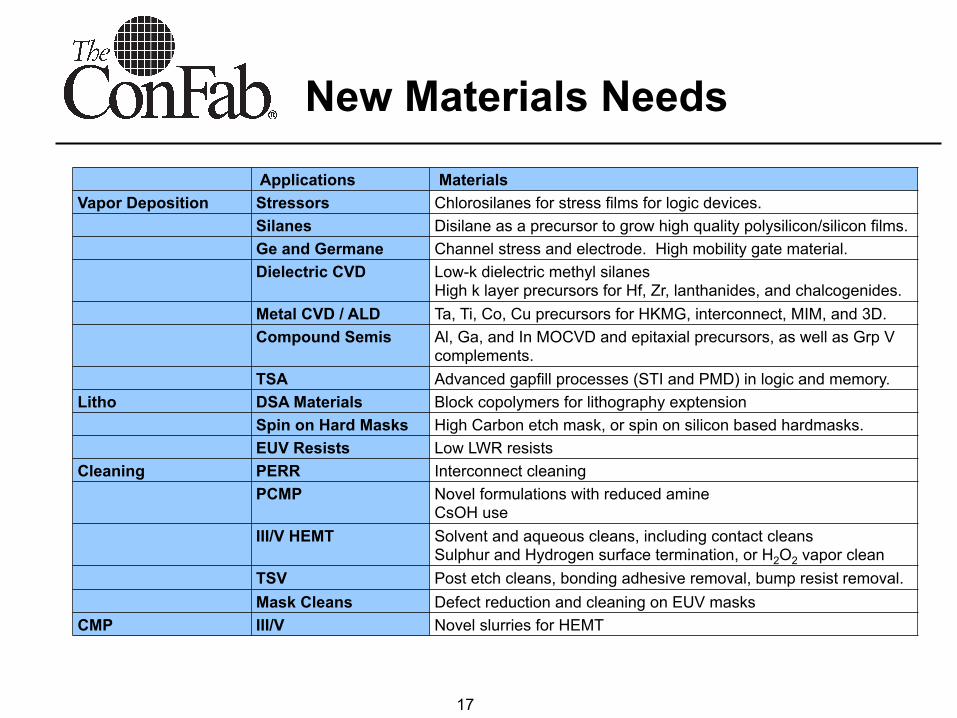

New Materials Needs

Applications Materials Vapor Deposition Stressors Chlorosilanes for stress films for logic devices.

Silanes Disilane as a precursor to grow high quality polysilicon/silicon films. Ge and Germane Channel stress and electrode. High mobility gate material. Dielectric CVD

Low-k dielectric methyl silanes High k layer precursors for Hf, Zr, lanthanides, and chalcogenides.

Metal CVD / ALD Ta, Ti, Co, Cu precursors for HKMG, interconnect, MIM, and 3D. Compound Semis Al, Ga, and In MOCVD and epitaxial precursors, as well as Grp V

complements. TSA Advanced gapfill processes (STI and PMD) in logic and memory.

Litho DSA Materials Block copolymers for lithography exptension Spin on Hard Masks High Carbon etch mask, or spin on silicon based hardmasks. EUV Resists Low LWR resists

Cleaning PERR Interconnect cleaning PCMP Novel formulations with reduced amine

CsOH use III/V HEMT Solvent and aqueous cleans, including contact cleans

Sulphur and Hydrogen surface termination, or H2O2 vapor clean TSV Post etch cleans, bonding adhesive removal, bump resist removal. Mask Cleans Defect reduction and cleaning on EUV masks

CMP III/V Novel slurries for HEMT

18

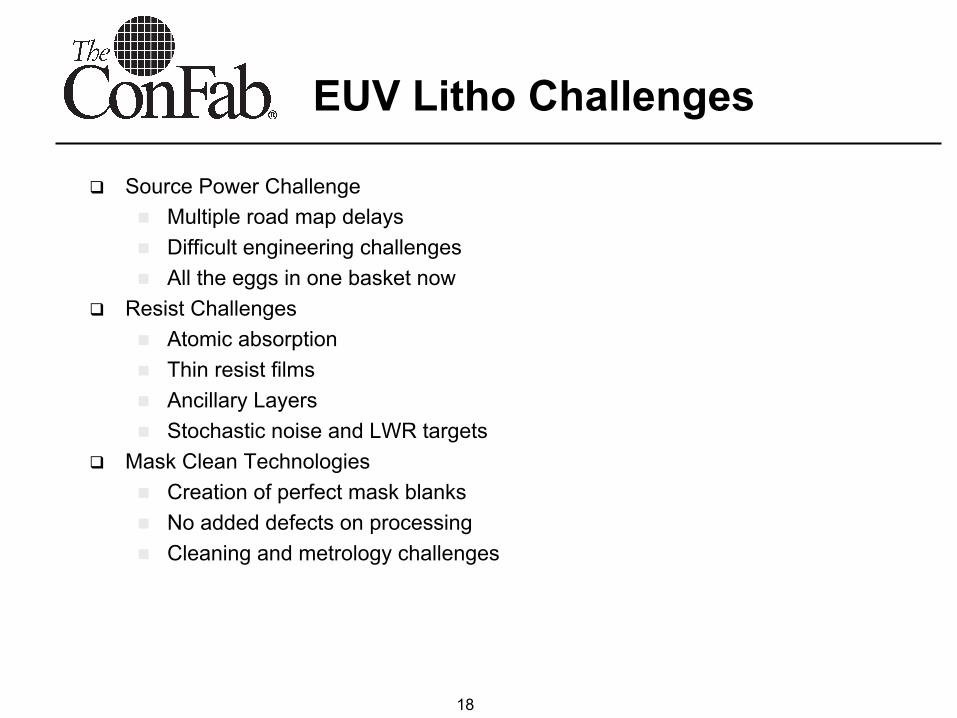

EUV Litho Challenges

q Source Power Challenge n Multiple road map delays n Difficult engineering challenges n All the eggs in one basket now

q Resist Challenges n Atomic absorption n Thin resist films n Ancillary Layers n Stochastic noise and LWR targets

q Mask Clean Technologies n Creation of perfect mask blanks n No added defects on processing n Cleaning and metrology challenges

19

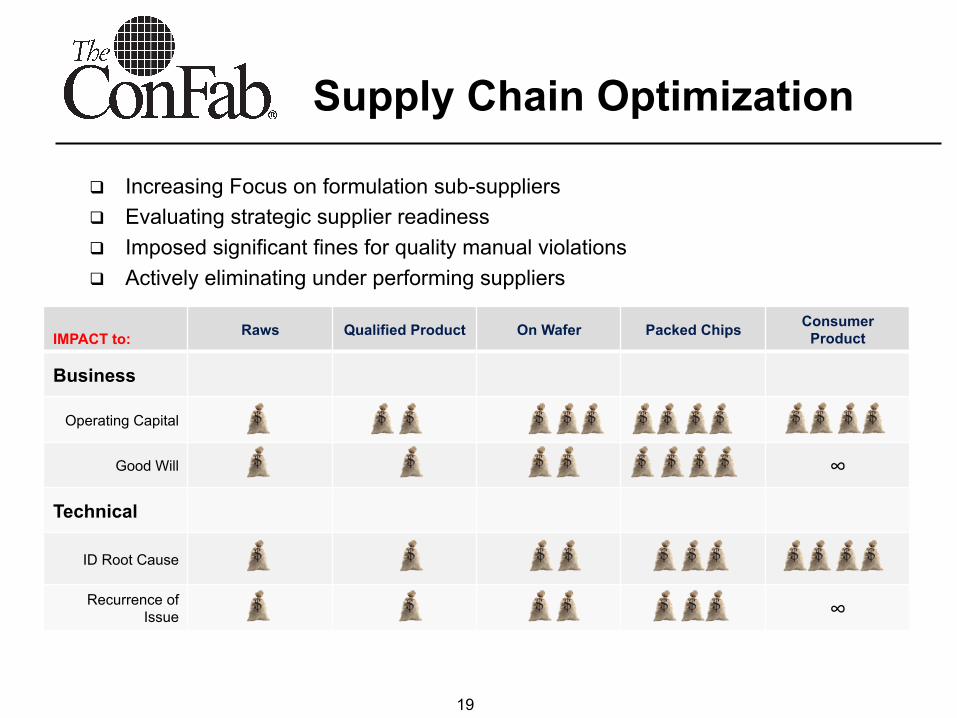

Supply Chain Optimization

q Increasing Focus on formulation sub-suppliers q Evaluating strategic supplier readiness q Imposed significant fines for quality manual violations q Actively eliminating under performing suppliers

IMPACT to: Raws Qualified Product On Wafer Packed Chips Consumer Product

Business

Operating Capital

Good Will ∞

Technical

ID Root Cause

Recurrence of Issue ∞

20

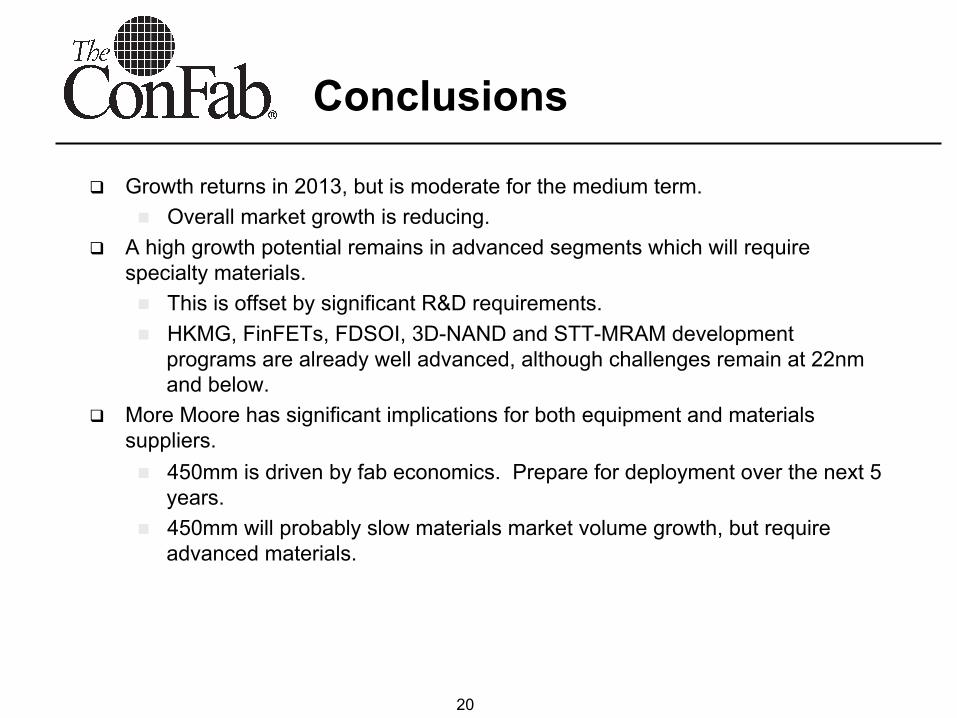

Conclusions

q Growth returns in 2013, but is moderate for the medium term. n Overall market growth is reducing.

q A high growth potential remains in advanced segments which will require specialty materials. n This is offset by significant R&D requirements. n HKMG, FinFETs, FDSOI, 3D-NAND and STT-MRAM development

programs are already well advanced, although challenges remain at 22nm and below.

q More Moore has significant implications for both equipment and materials suppliers. n 450mm is driven by fab economics. Prepare for deployment over the next 5

years. n 450mm will probably slow materials market volume growth, but require

advanced materials.

21

Conclusions

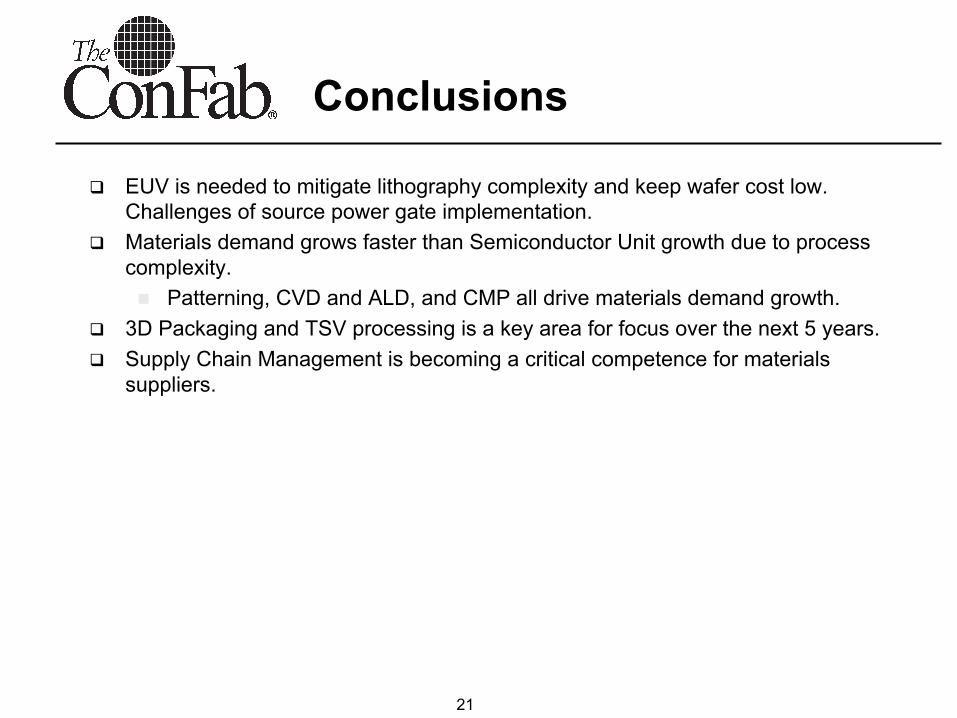

q EUV is needed to mitigate lithography complexity and keep wafer cost low. Challenges of source power gate implementation.

q Materials demand grows faster than Semiconductor Unit growth due to process complexity. n Patterning, CVD and ALD, and CMP all drive materials demand growth.

q 3D Packaging and TSV processing is a key area for focus over the next 5 years. q Supply Chain Management is becoming a critical competence for materials

suppliers.

22

Sources and Models

q IC-Knowledge q Strategic Cost Model - equipment edition - easily project wafer cost and

equipment requirements for the next 15 years based on the ITRS. Allows extensive process and equipment customization.

q IC-Knowledge & Linx Consulting q Strategic Cost Model - materials edition - easily project wafer cost, equipment

and materials requirements for the next 15 years based on the ITRS. Allows extensive process, material and equipment customization.

q Linx Consulting q Econometric Semiconductor Forecast – monthly forecasts of silicon area

demand developed in collaboration with Hilltop Economics LLC.

23

Contacts

PO Box 384 Mendon MA, 01756 [email protected] (617) 273 8837 PO Box 20 Georgetown, MA 01833 [email protected] Px: (978) 352 - 7610 Fx: (978) 352 - 3870